Abstract

This article examines the role of reputation building in family business contexts through relationships between the appointment of female on board (FOB) and the establishment of risk management (RMCOM) and corporate social responsibility committees (CSRCOM). Family firms perceive FOB as decreasing their firm control. The study also analyses the moderating effect of FOB on the aforementioned nexus. This article shows that family firms with FOB and through the signalling effect can be perceived by stakeholders as more authentic and managing their reputation and image; moreover, FOB negates the benefit of a CSRCOM, but better controls asymmetric information through creating an RMCOM.

Introduction

Family ownership significantly influences corporate governance (CG) in family firms by shaping decision-making processes, management structures and long-term strategies. Such ownership concentration reduces typical agency (agency costs I) problems between owners and managers, as family members often play dual roles as owners and managers. Furthermore, family ownership in family controlled firms has different incentives than diffuse shareholders in widely held companies (James, 1999). Large investors often exercise CG in order to protect their interests. Such firms with respectable corporate reputations use their names as a canopy brand for their products and services to expand into new markets (Dowling, 2006). Nevertheless, the question of whether family ownership delivers motivations to lessen agency costs (through an improved alignment of shareholder and executive goals) remains an open empirical issue.

Agency theory focuses on synchronising conflicts between managers and owners; it attempts to separate ownership and control, using voting rights on management decisions (Chen et al., 2011). In common law countries, ownership is mainly diffused (Holderness, 2009). Schulze et al. (2001) mention that decreasing agency costs for family firms naturally aligns the ownership’s and management’s welfare, including altruism, with growth prospects and risk. However, the problem of self-control that arises from influential owner-managers continues to haunt family firms. This remains a challenge to the CG in the family firm.

As such, family connections may be an important determinant of CG, though this relationship has received inadequate consideration. Moreover, in the presence of family ownership, small investors must feel protected by law to be attracted to these firms; this study analyses whether this condition holds true. Additionally, Crisóstomo et al. (2023) show that shareholder control arrangement, precisely dominant and shared control, is pertinent for firm reputation in Brazil, characterised by civil law, high ownership concentration and poor protection of minority shareholders.

In this regard, appointing women on corporate boards has been widely considered as a good governance practice (Sarkar & Selarka, 2021) and a suitable business decision as it is expected to heighten the firm’s value through its performance (Simpson et al., 2010). Moreover, gender diversity wields influences on aspects other than financial performance, such as emphasising corporate social responsibility (CSR) activities and alleviating fraud (e.g. Shaukat et al., 2016). Bear et al. (2010) show that female directors enhance firm reputation by boosting CSR strength ratings. In this vein, Bargoni et al. (2023) report that family firms consider reputational issues and external prestige in society to be crucial, based on the socioemotional wealth of family firms. They rely on building and promoting reputation and image for family legacy, community respect and long-term survival. In this respect, creating risk management (RMCOM) and CSR committees (CSRCOM) could contribute to boost external trust, signal modern governance and better professionalisation of both family and business.

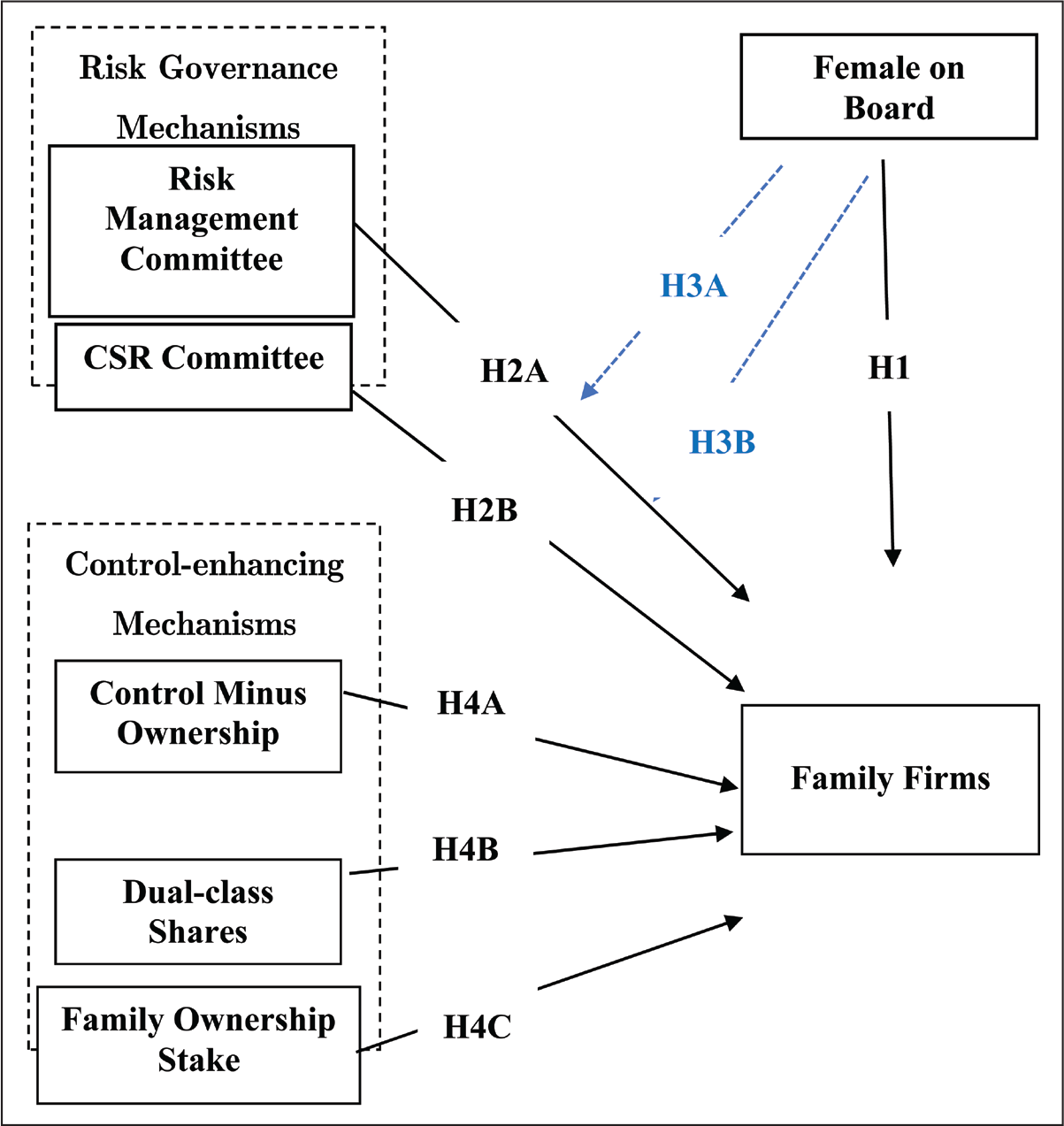

At this level, the study examines the potential mechanisms for a thorough reputation analysis of family businesses. The aforementioned discussion on the possible relationship between reputation and family-managed firms suggests that board gender diversity and the risk governance mechanisms in family firms are open questions that still need to be addressed empirically. More precisely, the purpose of this article is two-fold. First, the article attempts to analyse the relationship between the gender diversity on boards, the establishment of CSRCOM and RMCOM, and the presence of family-managed firms. Second, the study explores the moderating effect of female on boards on the relationship between the existence of risk governance mechanisms and the presence of family-managed firms.

This study contributes to the ongoing literature in several ways. First, the study explores the effect of an obscure aspect of CG, namely the CSRCOM and RMCOM. This study highlights to what extent the presence of such committees influences the reputation and image of family firms. This offers new insights into how formal governance structures add value to stakeholders’ trust and corporate reputation. Second, the study expands research on gender diversity on the boards by analysing the moderating role of women on boards from a reputational perspective. In this respect, this study shows that women boost the relationship between RMCOM and CSRCOM and the presence of family firms. This allows us to bridge studies on gender diversity with the literature on family business and reputation. Afterwards, these findings connect family-specific purposes in terms of reputation and image with modern governance mechanisms, indicating to what extent family controlled businesses balance their socioemotional wealth motives with external legitimacy and reputation. The study finally contributes to the ongoing literature on family firms by offering a global panel analysis combined with multi-theoretical foundations, taking into consideration the agency, signalling and resource-dependency theories and emphasising the essential role of women on boards through the lenses of reputation management.

In the rest of article, the second section reviews the literature and highlights the hypotheses, the third section introduces the research methodology, the fourth section discusses data and descriptive statistics, the fifth section presents the empirical results, the sixth section reports robustness checks. The seventh section discusses the results, and the eighth section concludes.

Literature Review and Hypotheses Development

Family firms are generally considered as crucial organisational forms (e.g. La Porta et al., 1998) and are defined by their socioemotional wealth, which focuses on trust, compassion, relationships and reputation (Wang et al., 2023). Such a non-economic goal tends to foster long-run orientations of family firms and their concerns for stakeholders (Wang et al., 2023), contingently implying a more considerate environment (Hernandez-Perlines et al., 2021) and enabling female leadership opportunities (Wang et al., 2019).

According to the agency theory, managers, who are often family members, may extract private benefits such as excessive compensation and large perquisites (Sarkar & Selarka, 2021). This could be especially documented; the family members have control rights that seem to be in excess of their cash-flow rights (Masulis et al., 2009). Under the stewardship theory, individuals in leadership positions could not be self-serving people, but they manage to further collaborative decision-making. In this respect, individuals endeavour to set up firm reputation and abilities, sometimes at the expense of personal sacrifices (Sarkar & Selarka, 2021).

Above and beyond, the existence of women directors on corporate boards has largely been considered a good governance practice (Sarkar & Selarka, 2021). Compared to their male counterparts, women show distinguishable strengths, experiences and attributes that increasingly contribute to monitoring and controlling of management and board deliberations (e.g. Houcine & Derouiche, 2024). Many previous studies reported that men tend to resolve several issues differently from women (Haberman & Danes, 2007). Women try to adopt a more participatory and interactive style; however, as more female family directors exist, conflicts with non-family subgroups become more widespread, damaging firm performance (Garcia-Meca & Santana- Martín, 2023). Therefore, women can improve a firm’s capability to address ambiguity and be flexible (Bettinelli et al., 2018). Women tend to be more transformational, democratic and show a trust-building leadership style (Sarkar & Selarka, 2021). They are also more likely to make more ethical and socially responsible decisions (Lopez-González et al., 2019). So, raising board gender diversity could improve the capability of the board in playing its strategic and control roles (Adams & Ferreira, 2009).

By leafing through the literature on women’s participation in family firm boards, most studies have increasingly focused on female involvement and firm performance. Minguez-Vera and Martín (2011) report that women’s presence on boards contributes to a negative effect on firm performance. This could be explained by the less risky strategies adopted by female directors. Using social feminist theory, D’Amato (2017) professes that women and men may lead a firm in different ways and achieve different performance as they differ in risk appetites, leadership styles and business purposes. Based on resource-dependency theory, women board members could serve as a precious source of gaining key resources for sustainable performance (Khatri & Kjærland, 2023). In this regard, women on boards offer innovative ideas and perspectives given their accommodative attitudes and exceptional behaviours (Abbas & Frihatni, 2023). Therefore, the study concludes that the literature agrees on the positive role that women serve in businesses, particularly their monitoring, participatory, flexible and interactive style in managing family firms.

With the aim of apprehending and disentangling the relationship between female involvement and family firm, the research formulates the following hypothesis:

H1: FOB is positively related to the presence of family-managed firms.

On the other hand, the relationship between family firms and sustainability practices has been analysed from different theories, such as the social capital theory, organisational identity theory, resource-based view theory, inference theory and socioemotional wealth theory (Bargoni et al., 2023). For instance, from a socioemotional wealth theory perspective, Citterio et al. (2024) profess that family firms develop CSR policies to sustain their intrinsic values and the societal standing created by the family. Rehman and Hamdan (2023) show that the relationship between CSR performance and family firms is stronger when the member is a female participant. In this respect, many studies have analysed the impact of CSRCOM features on CSR engagement (e.g. Godos-Diez et al., 2018). Chu et al. (2024) indicate that the choice of a company’s decision to adopt a CSRCOM is forged by external demands from different and internal stakeholders’ needs associated with setting up a separate CSRCOM. Hence, since family firms care about developing CSR policies in response to their stakeholders, they are more likely to establish a CSRCOM.

Further, Amin et al. (2023) analyse the effect of CEOs’ personal features on firms’ risk taking and the moderating effect of family ownership on this relationship. Based on the upper echelons theory, they report that CEOs with finance-related educational background and female CEOs decrease the firm’s risk-taking behaviour. Zahra (2005) establishes that family involvement improves the firms’ risk management. Particularly, setting up an RMCOM can help offer assistance to the BoD in improving risk management, carrying out risk oversight functions and enhancing the quality of risk reporting and monitoring (e.g. Malik et al., 2021). Bates and Leclerc (2009) indicate that the existence of an RMCOM could hinder the board from effectively overseeing operational and strategic. Malik et al. (2023) and Nasution (2019) argue that the agency and signalling theories can explain the establishment of an RMCOM. Based on agency theory, the RMCOM could act as a monitoring mechanism that enhances the firm’s value and reduces agency costs through extensive internal control. From the signalling theory, the existence of an RMCOM signals indirectly to investors that the firm handles asymmetric information through such a committee. Hence, since family firms care about improving risk management and reducing asymmetric information, they are more likely to establish an RMCOM.

From the aforementioned, the following hypotheses are proposed:

H2A: The formation of a CSR committee is positively related to the existence of family-managed firms. H2B: The establishment of a risk management committee is negatively related to the existence of family-managed firms.

Few investigators have focused on the relationship between the BoD structure and firms’ sustainability practices. Burke et al. (2019) show that the board-level commitment improves corporate social performance. Brammer et al. (2006) examine CG practices and environmental disclosure. Arayssi et al. (2020) add social disclosure to the list. In particular, many researchers have investigated the impacts of board gender diversity on CSR and social and ethical concerns, proving the existence of a difference in this relationship among family and non-family firms (e.g. Cruz et al., 2019). In this regard, Bettinelli (2011) finds that the main function of females on the board is to monitor managers’ actions and protect the family’s interests. Rodriguez‐Ariza et al. (2017) show that CSR commitment is not significantly affected by the presence of female directors, since they tend to act in agreement with the family attitude towards CSR. Samara et al. (2019) display that females on corporate boards can serve as a vehicle for controlling family firms’ owners to attain economic purposes and enhance the reputation of the business and family. There is ample evidence about female directors leading to reduced risk or improve risk management in the firm (Firdaus & Adhariani, 2017; Chen et al., 2016). Few studies have examined the effect of gender diversity on the RMCOM. Jia (2019) finds that the gender diversity on RMCOM is related to a lower probability of financial distress, demonstrating that women excel in monitoring and reducing firms’ excessive risky behaviour. Since females on boards monitor managers and tend to establish CSR practices and reduce different types of risks, the study posits that females moderate the relationship between CSCOM and RMCOM in relation to family firms.

Based on the aforementioned discourse, the study proposes the following hypotheses:

H3A: FOBs plays a moderating role in the relationship between the CSRCOM and family firms. H3B: Female on boards plays a moderating role in the relationship between the RMCOM and family firms.

Family ownership introduces complexities in decision-making due to overlapping roles. This can lead to conflicts when decisions are influenced by personal preferences rather than business needs. Although family firms suffer fewer agency conflicts between owners and managers (agency costs I) owing to their concentrated ownership structures (Pindado & Requejo, 2015), the conflict between family owners and minority owners (agency costs II) may not be diminished. As a matter of fact, Purkayastha (2022) professes that dominant family control diminishes type I agency costs, while raising type II agency costs given the family’s voting power.

Some agency costs associated with family firms remain. Dual-class shares allow managers better negotiation power on the side of shareholders in a takeover pursuit, increasing shareholders’ wealth. Family firms being managed more closely and efficiently may engage less in dual-class shares control. Such practices may yield private benefit of control (shifting from agency costs I to agency costs II) and render wealth maximisation inconsistent with CG in family firms.

Family ownership influences corporate reputation in family firms through several unique mechanisms tied to their identity, governance and socioemotional priorities. Family members often identify intensely with their business, as the firm’s reputation is strictly linked to their personal and family legacy. This identification motivates family directors to aim for a good reputation, adding to the socioemotional wealth of the firm (Deephouse & Jaskiewicz, 2013). While prioritising this corporate image, decisions and efforts try to avoid reputational risks. Salehi et al. (2020) report that the reputation of a family firm and discretionary accrual management are significantly and negatively related. To enhance their reputation, they often engage in CSR activities, according to stakeholder theory, in order to preserve a positive public image that reinforces their stakeholder relations (Adewole, 2024). Moreover, when the family’s name is connected with the firm’s, it entices family firms to invest in reputation-building initiatives, because any harm to the firm’s image directly disturbs the family’s position in society (Rovelli et al., 2022).

Anderson and Reeb (2003) recognise two motives explaining why family firms decrease agency costs: concentrated ownership that may entice the agency cost reduction, and superior practical knowledge about the firm’s operation that allows better monitoring, reducing agency costs I. Small shareholders hope that somebody else monitors, therefore they free ride. Reddy and Wellalage (2023) report that diminishing family ownership involves a greater firm financial performance. Hence, the presence of agency costs II in family firms may lead to higher control minus ownership rights, fewer dual-class shares if management is closer, and higher ownership stake if owners identify strongly with the family firms.

From the above discussion, the study proposes the following hypothesis:

H4A: Control minus ownership is positively related to the existence of family-managed firms. H4B: Dual-class shares are negatively related to the existence of family-managed firms. H4C: Family ownership stake is positively related to the existence of family-managed firms.

To sum up, the conceptual model summarises the aforementioned hypotheses and highlights the different relationships under study (see Figure 1).

>Methodology

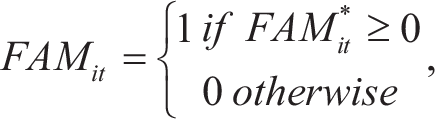

This study considers the panel probit model in order to analyse the aforementioned relationships. In Equation (1), the dependent variable measures the utility to the firm from having a founder or a family member descendant in the role of a director or a large shareholder, as a proxy for the existence of a family firm, albeit exerting considerable control over the firm’s decisions. The dependent variable (FAM*) is latent since it cannot be observed directly, as it represents firm i’s utility from having a founder or descendant or family member as a director or a large shareholder at a certain time t.

On the other hand, the independent variables are common to the two main regressions in this article; these variables are female on boards and risk governance mechanisms. The control-enhancing mechanisms, board mechanisms and institutional mechanisms are considered as control variables. The study enumerates the independent variables used in this model one by one and explains how they are measured and where they have been used in the related literature.

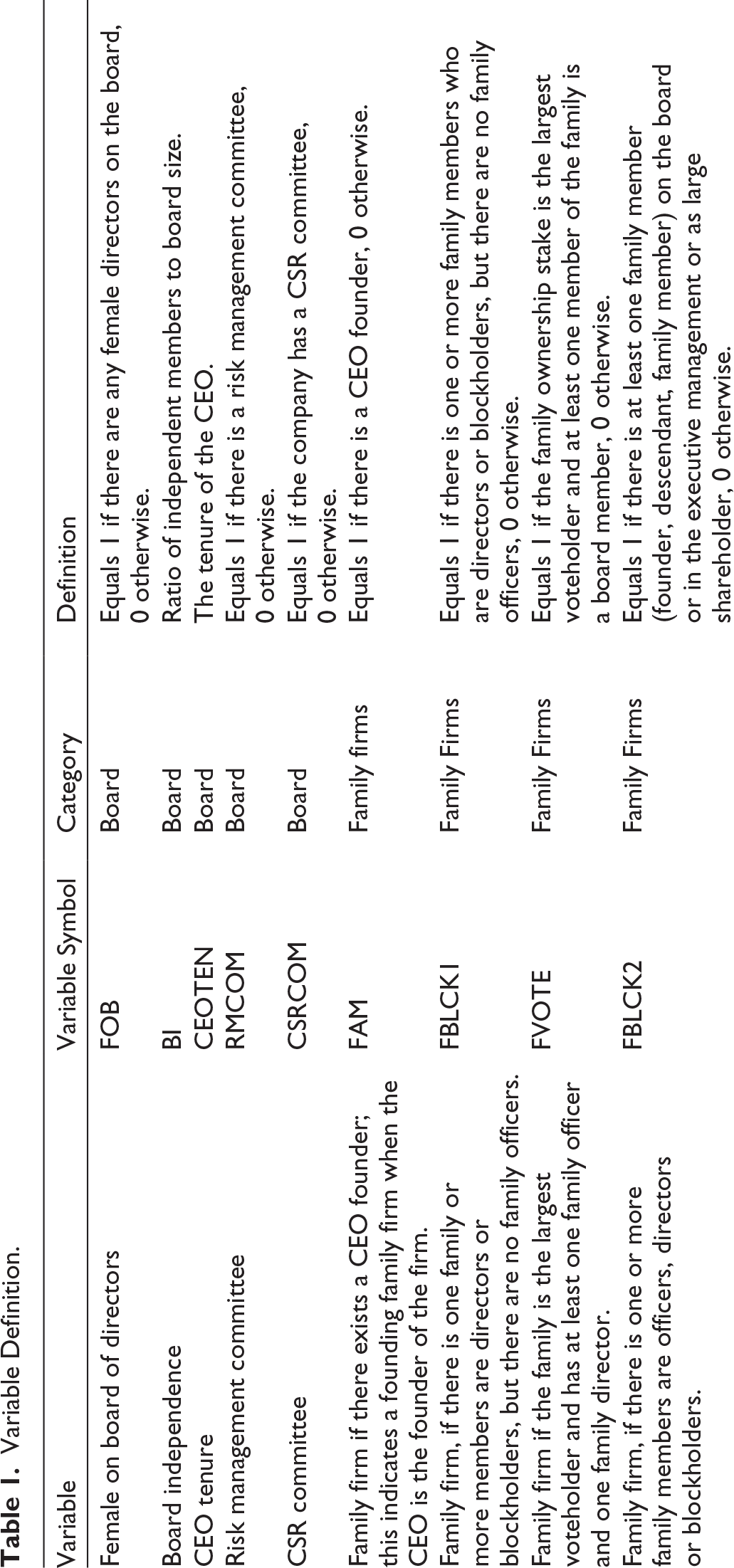

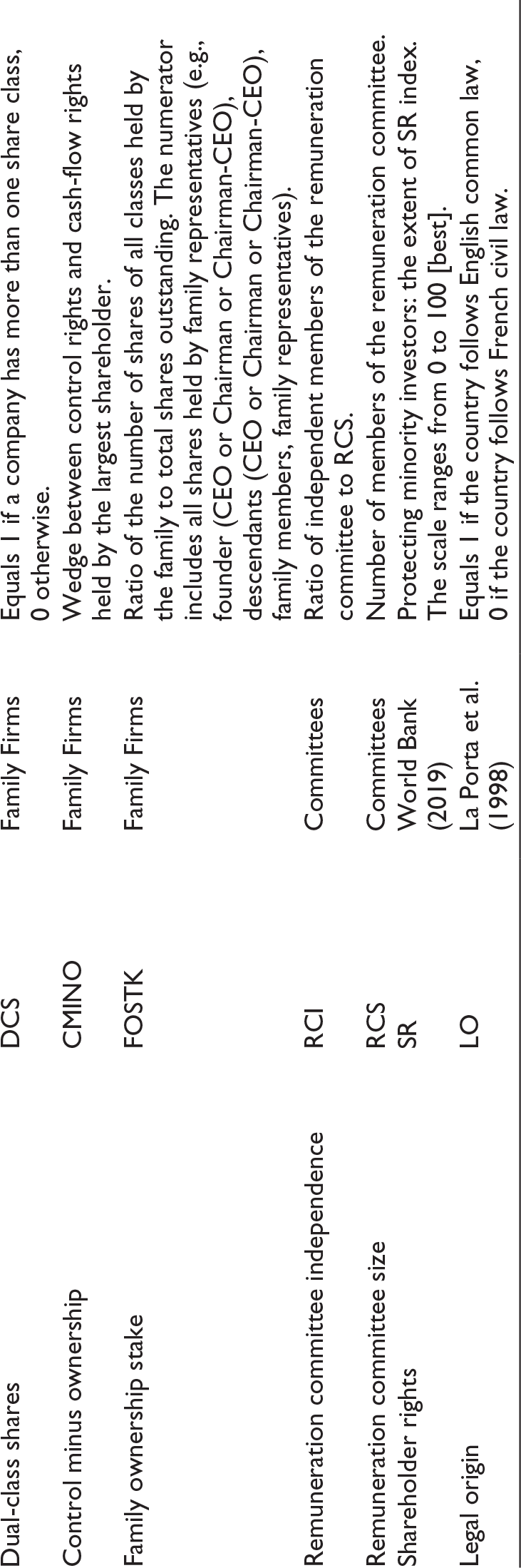

The study starts with a female on board, a key independent variable. Some previous studies have employed the percentage of female directors on board in order to quantify board gender diversity (e.g. Ahern & Dittmar, 2012; Liu et al., 2014), whereas some others have used the number of female directors on board (e.g. Carter et al., 2010; Simpson et al., 2010). In this case, following Sarkar and Selarka (2021), the study uses the dummy variable (FOB) that equals 1 if the board includes at least one woman director and 0 otherwise as a proxy for board gender diversity. The study then uses variables to proxy risk governance mechanisms. First, the CSRCOM (CSRCOM) is a variable which indicates the existence of CSRCOM in a family firm. It is represented as a dummy variable which is coded as 1 if a firm has a CSRCOM and 0 otherwise (Kubo & Sasaki, 2024; Meqbel et al., 2025; Samarawickrama et al., 2024). Recall that the establishment of a CSRCOM reflects the commitment of a company towards enhancing its sustainability engagement (Meqbel et al., 2025) and progress on the firm’s environmental, social and ethical issues (Bifulco et al., 2023). Second, the RMCOM is measured using a dummy variable. It is coded 1 if the family firm has established such a committee and 0 if there is no RMCOM. Such a proxy has largely been used by many researchers, such as Malik et al. (2023), Alduneibat (2023) and Hines and Peter (2015). By establishing such a committee, the board of directors can get assistance in improving the risk management, carrying out risk oversight functions and fostering the quality of risk reporting and monitoring (e.g. Agustin & Utama, 2024; Malik et al., 2021).

To control the impact of other firm features, the study uses variables for control-enhancing mechanisms, institutional mechanisms and board mechanisms. The study starts with control-enhancing mechanisms. Firms maintain control of voting rights through ownership of high-voting stocks, while issuing low-voting stock if needed. This scheme can amplify the wedge between control rights and cash-flow rights, thereby magnifying the conflict of interests between the family and outsider investors. Thus, families can use their influence to reduce firm-specific risk, which potentially benefits the family but may be detrimental to outside shareholders. However, Claessens et al. (2002) and Cronqvist and Nilsson (2003) have documented that the separation of voting rights from cash-flow rights increases agency costs and suboptimal investment decisions, since it leads to increased entrenchment and controlling owners to derive large private benefits (Hagelin et al., 2006). Ownership and control rights can differ among other things due to dual-class shares which provide different voting rights for given cash-flow rights, deviating from the one-share one-vote scheme. In this case, control minus ownership (CMINO) is measured as the difference between control and cash-flow rights held by the largest shareholder. This variable quantifies an entrenchment effect of excess control rights (Maury, 2006; Zhou et al., 2013). Dual-class shares (DCS) is measured as a dummy variable which is set to 1 if a firm has more than one share class, 0 otherwise (e.g. Sekerci & Pagach, 2020). The study uses ‘Family Ownership Stake’ abbreviated as FOSTK, as defined in Table 1, in conformity with Schulze et al. (2001), to control for the effect of ownership concentration on governance practices, measuring this variable as the reported percentage of the firm’s shares held by the eight largest family shareholders. A higher family ownership stake can yield the family a higher power to expropriate minority shareholders, but it may, on the other hand, provide a better alignment of the family incentives with those of minority shareholders; hence, a large stake can lead to more alignment of family owners with the shareholders. Share prices often rise after the sudden death of the founder of family firms, hinting that the flow of benefits of control diminishes in this instance (Shleifer & Vishny, 1997).

Afterwards, the study uses civil law origin (LO) and shareholders’ rights (SR) as institutional mechanisms. In order to induce shareholders to initiate investing, they need forcible protection provided by the court system. Moreover, French civil law does not encourage external finance, whereas English common law does (La Porta et al., 1998). This prompts us to use legal origin to showcase this effect; civil law countries are coded with zero, while common law countries are coded with 1.

Lastly, the study controls for board mechanisms by taking into consideration remuneration committee independence (RCI), remuneration committee size (RCS), board independence (BI) and CEO tenure (CEOTEN). Some family owners can expropriate minority shareholders’ wealth through extravagant remuneration. Hence, remuneration committee’s—that mainly exist in higher turnover firms—objectivity and independence can be compromised in such instances. Buchanan (1975) expresses that parents tend to be disproportionately generous, permitting children to enjoy a free ride, in comparison with non-family firm managers. Board performance indicator is given by a compensation arrangement with managers according to Bartholomeusz and Tanewski (2006). This brings about the importance of the independence of the compensation committee and its size as measures of the BoD being in charge of the firms’ processes, such as the effective negotiations with managers that would lead to strong performance measures. Main and Johnston (1993) note that a number of non-executive (independent) directors is needed to create a meaningful remuneration committee. Cybinski and Windsor (2013) show that the independence of the remuneration committee may align CEO remuneration with firm performance for larger firms, and help monitor the remuneration of directors. Anderson and Reeb (2003) found a positive correlation between BI and firm performance for family firms in the United States. Family firms tend to allow a greater duality between the chairman of the board and the CEO roles (Bartholomeusz & Tanewski, 2006). Family firms introduce survivorship bias, that is, the more successful companies are less likely to have CEO turnover, and such CEOs are expected to be more entrenched and follow more persistent strategies (Ghosh et al., 2011; Schulze et al., 2001). This observation is captured by the variable CEO tenure. It shows a strong positive relationship with family firms, consistent with the fact that these firms tend to be more profitable on average than non-family firms (Anderson et al., 2003). Additionally, agency costs rise if family managers enjoy nepotism as opposed to meritocracy and are inferior to hired professionals, as modelled theoretically by Gomez-Mejia et al. (2001). However, Morck et al. (2000) suggest that founder CEOs draw on original and value-strengthening skills to the firm. Therefore, the study considers the following panel probit model:

The corresponding observation rule is as follows:

where FAM it in Equation (3) represents a binary variable. The independent variables included in Equation (1) are: female on board (FOB it ), CSR committee (CSRCOM it ), RM committee (RMCOM it ), family ownership stake (FOSTK it ), CEO tenure (CEOTEN it ), remuneration committee independence (RCI it ), remuneration committee size (RCIS it ), board independence (BI it ), control minus ownership (CMINO it ), dual-class shares (DCS it ), legal origin (LO it ), shareholder rights (SR it ), and the error term (uit). Equation (2) adds the interaction terms between CSRCOM and FOB, and RMCOM and FOB to all the previous variables in Equation (1). All the variables in these equations are fully defined in Table 1.

Variable Definition.

Data and Descriptive Statistics

NRG Metrics database provides information on roughly 8,000 publicly listed firms throughout the world that cover 46 countries and major stock markets, with wide geographical market coverage ranging from Europe to North America, East Asia and the rest of the world. The sample includes thousands of firms traded on these stock exchanges from 2014 to 2024, hence forming a time-series panel data set. It includes data on CG; such variables are sensibly stationary over time. The panel set consists of a total of 53,317 firm-year observations. A family-controlled firm is an entity closely managed and/or largely owned by the founding family members (Westhead & Howorth, 2007). Non-executive directors usually provide independent oversight, serve on sub-committees of the BoD, and are usually paid a fee for their services.

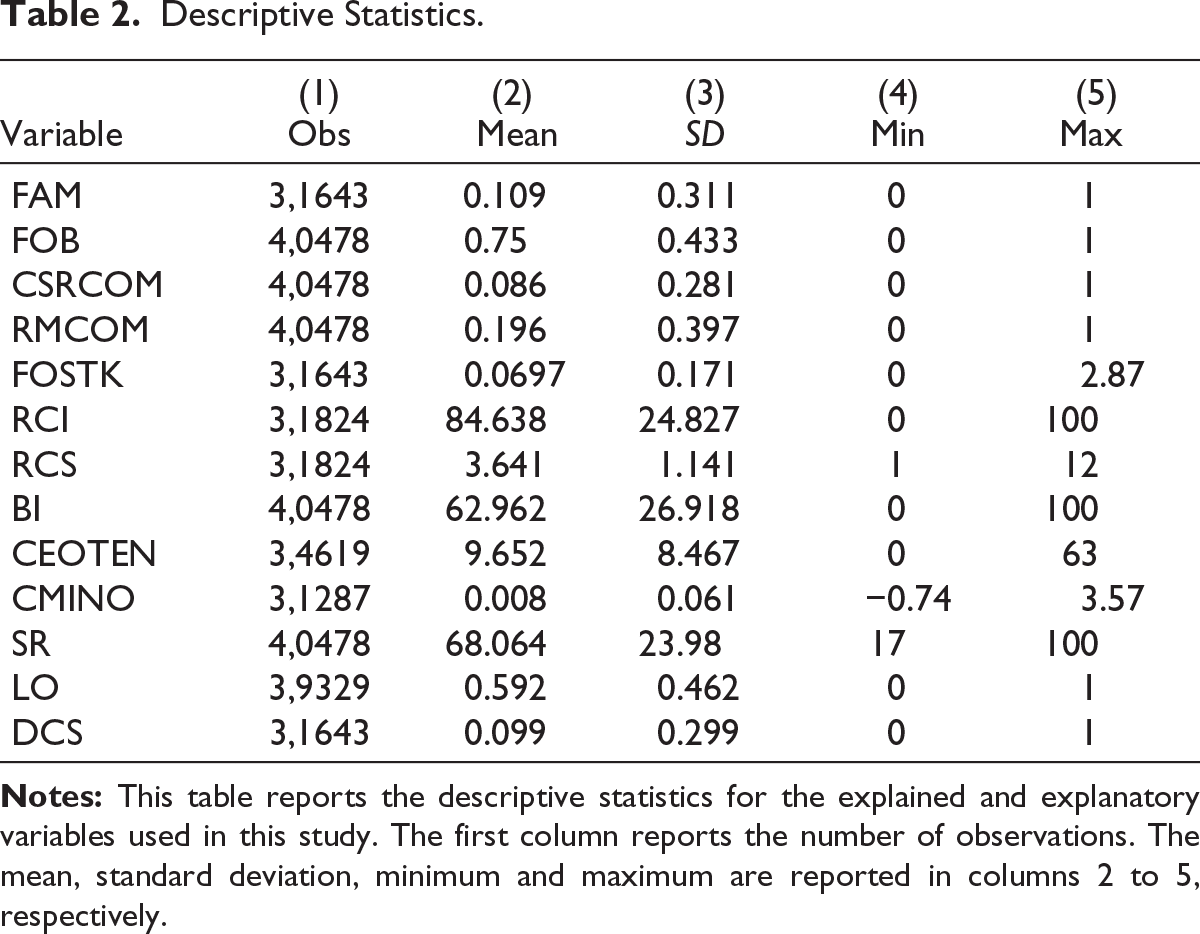

Table 2 presents the descriptive statistics for the variables used in this model. Since the number of observations that were used was 31,287, it can be inferred that about 3,129 firms were used here. Family firms (described as firms that have a CEO founder), indicating that a founding family firm represents about 11% of the total firm observations. Most of the remuneration committees are independent, and an average size of 3.64; boards are on average independent. The overall sample average CEO tenure is 9.65 years, with family firms having an average of 12.9 years compared to non-family firms’ average of 7.8 years. About 10% of firms have DCS (13% in family firms and 8% in non-family firms), and the average ownership of families is 7%. Family ownership, as expected, averages to 22% in family firms and less than 1% in non-family firms. About 95 of firms have a CSRCOM, compared to 20% with a risk management committee.

Descriptive Statistics.

The difference (wedge) between cash-flow and voting rights through multiple share classes, measured by CMINO, is 1.5% for founding family firms but only 0.5% for non-family blockholder (either private investor, state, another company or miscellaneous) firms. This is a clear sign that family firms try to preserve control in their companies.

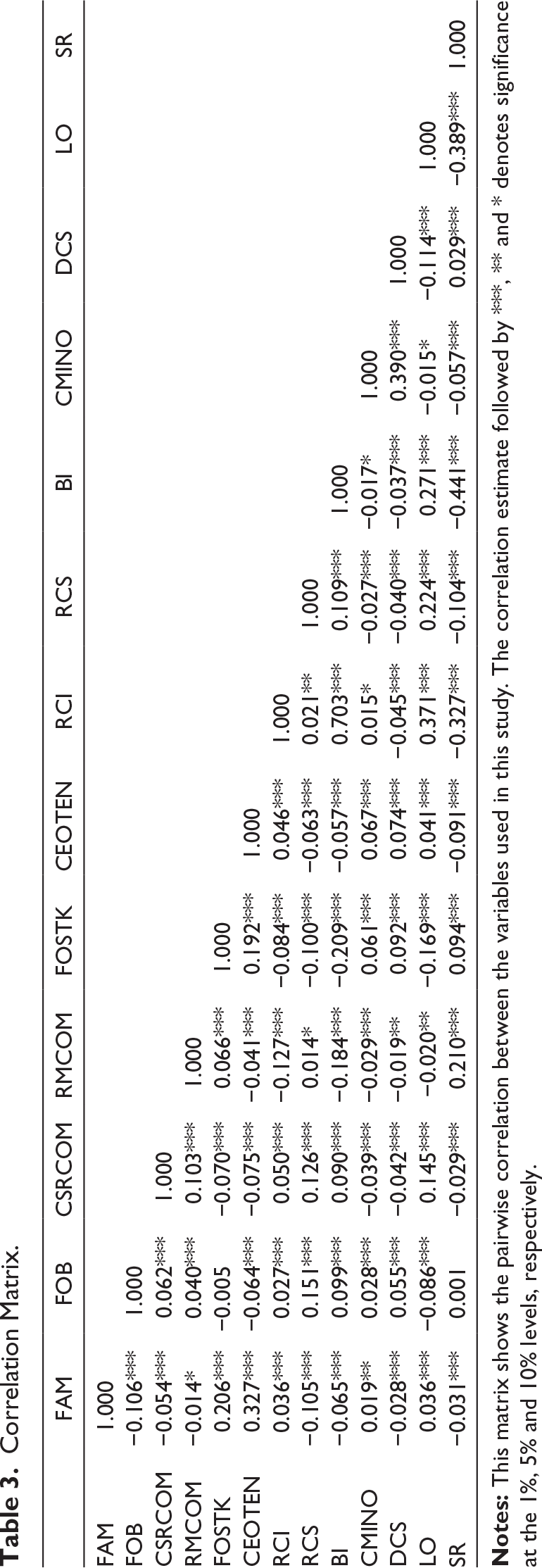

Table 3 reports the correlation matrix which highlights the statistical relationships between different variables. At first glance, the study can report some asymmetry patterns between variables. The magnitude and sign of the correlation coefficients seem to change among variables. For instance, the correlation value between women on boards and family firms is equal to −0.106 whereas the correlation value between civil legal origin and CSRCOM is equal to 0.145.

Correlation Matrix.

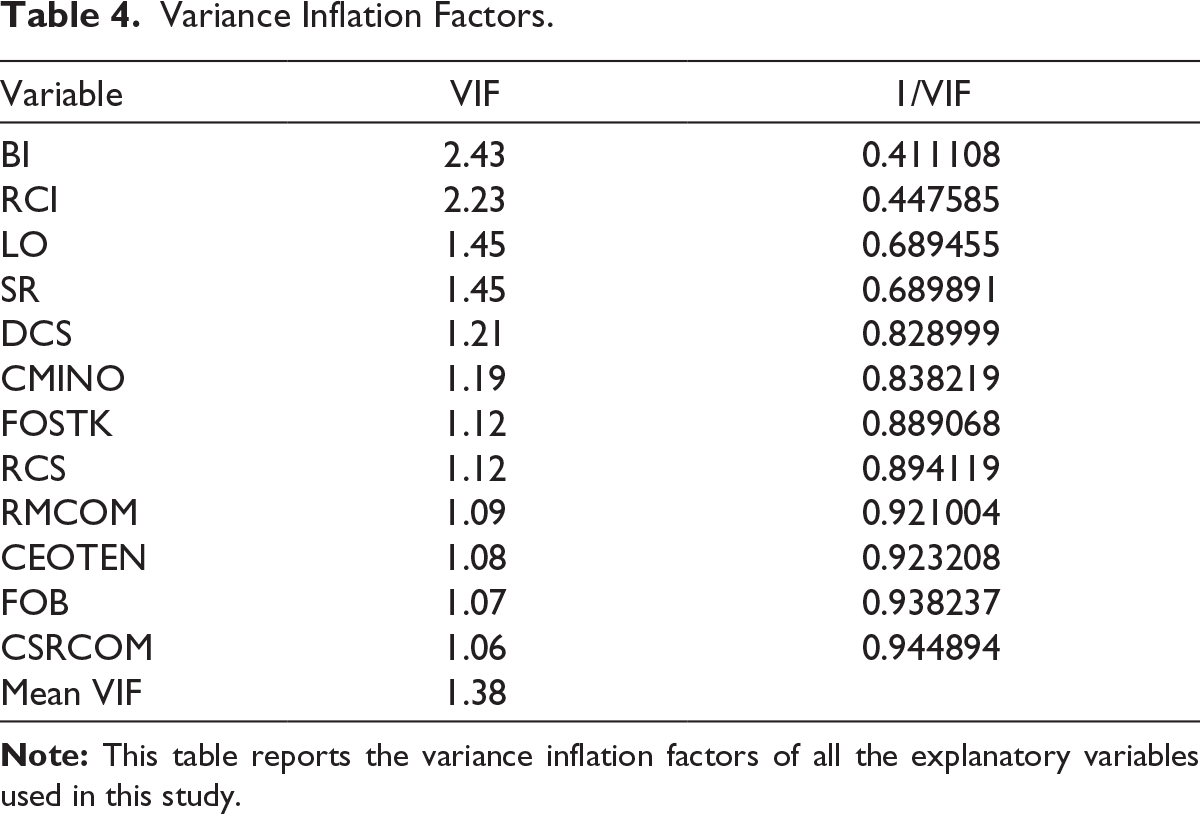

Afterwards, the study examines the multicollinearity between independent variables, given that it can be a challenge to obtain a reliable interpretation of the impact of each explanatory variable on the dependent variable. In this regard, Table 4 reports the results of computing the variance inflation factor (VIF), which can identify the existence of multicollinearity. According to Daoud (2017), a VIF value equal to (resp. above) 1 (resp. 5) reflects no multicollinearity (resp. the existence of multicolinearity), values up to 5 are also acceptable. From Table 4, all the independent variables in this model show a VIF value equal to 1. Therefore, one might retain all the explanatory variables to estimate this model. The mean VIF for the variables in this model is 1.38.

Variance Inflation Factors.

Main Results

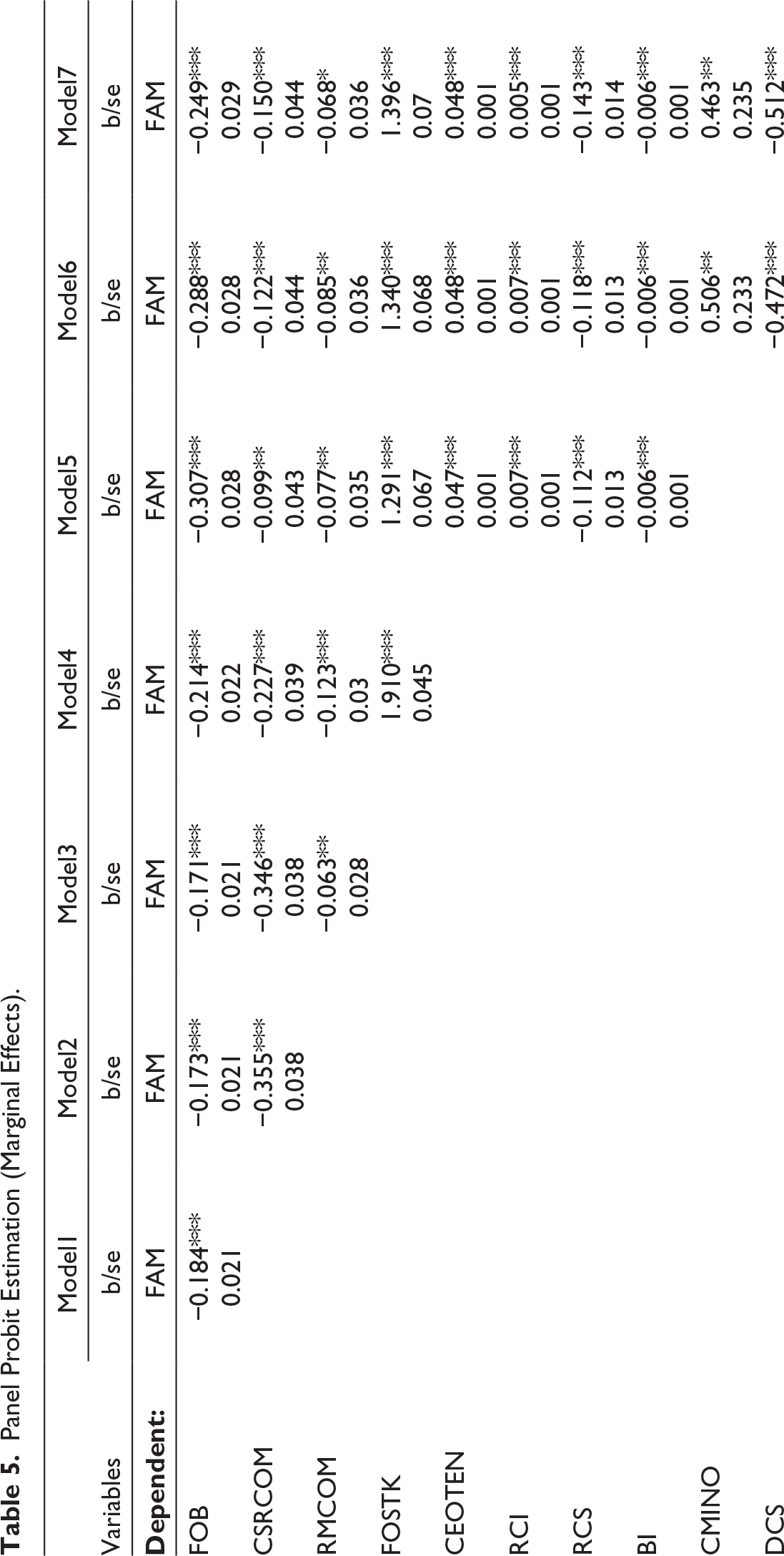

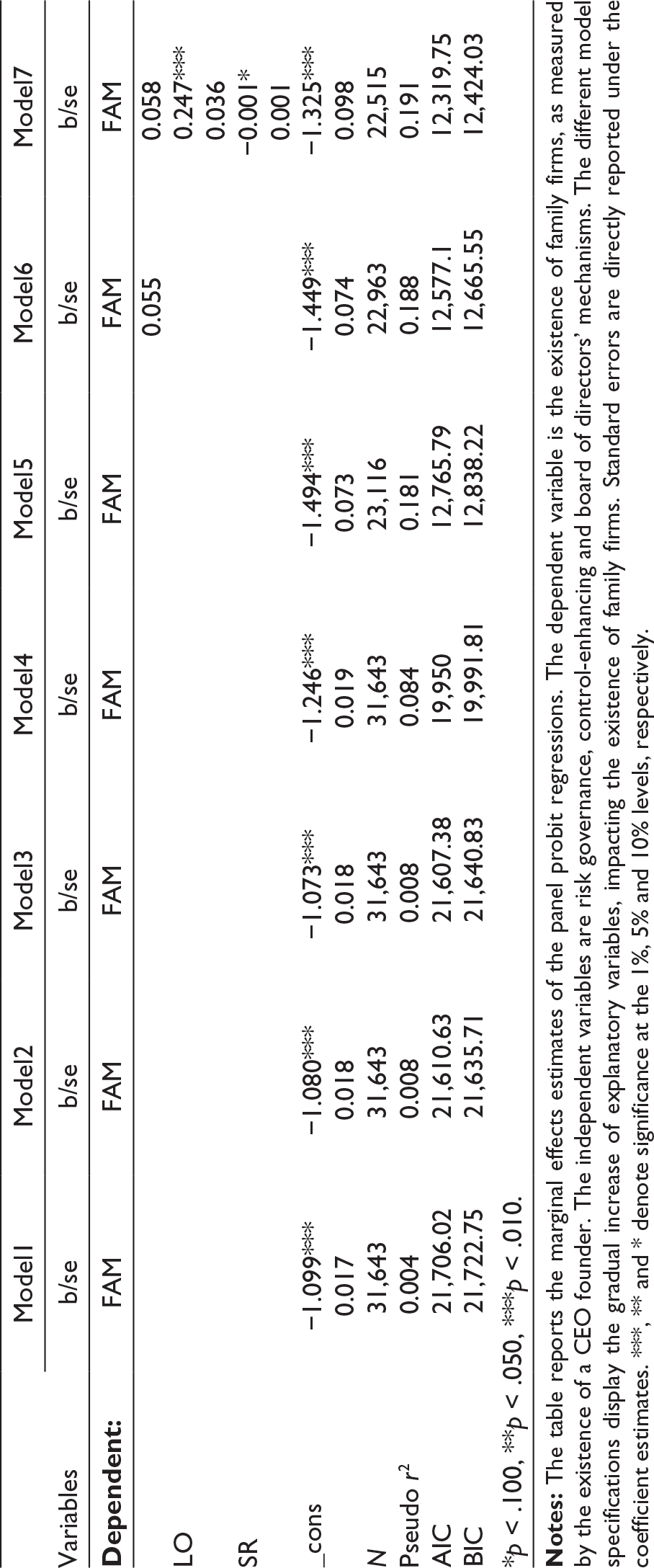

Table 5 shows the probit regression results for the family firms characterised by the presence of a CEO founder (measured by ‘FAM’) and independent variables, as specified in Equation (1). Other variables measuring the existence of family firms (i.e., ‘FBLCK1’, as defined in Table 1) were regressed using Equation (1) (results not reported here), but the study has chosen ‘FAM’ because it fits the data the best. From Table 5, model 1 looks at results with only FOB of directors. In model 2, the study includes the CSRCOM. In model 3, the study adds the risk management committee. The study adds the family ownership stake in model 4, and the study adds the remaining board mechanisms variables in model 5, namely CEO tenure, RCI and size and BI. In model 6, the study adds the control-enhancing mechanisms, control minus ownership and DCS. In column 7, the study adds the institutional mechanisms, legal origin and SR dummies.

Panel Probit Estimation (Marginal Effects).

The study finds that the FOB of directors significantly reduces the probability of family firms’ occurrence. This result is robust across all specifications. The study also finds that the family ownership stake, CEO tenure, RCI, and control minus ownership all have a positive and statistically significant effect on the probability of family firms. On the other hand, CSRCOM, RCS, BI, dual class shares all significantly decrease the probability of family firm occurrences. Moreover, having a common law tradition significantly increases the probability of family firms.

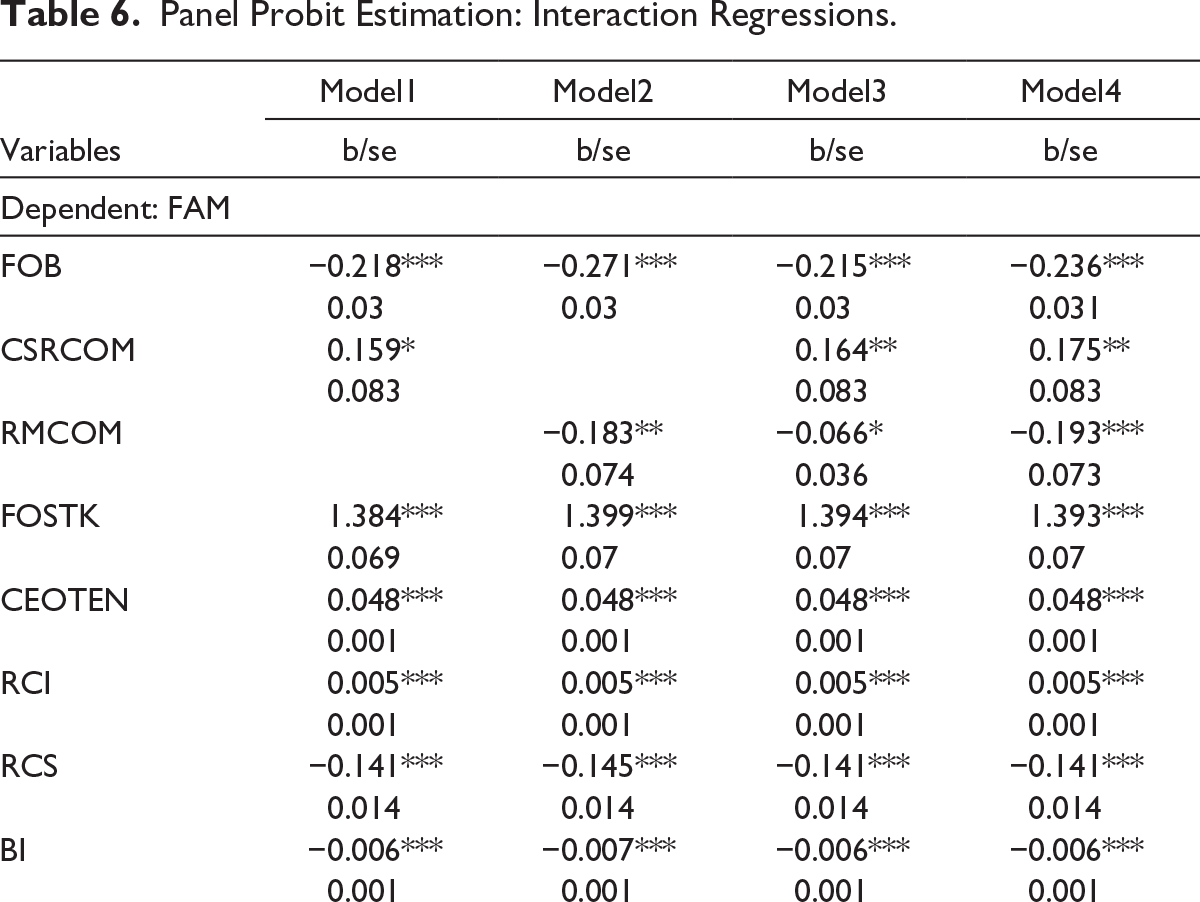

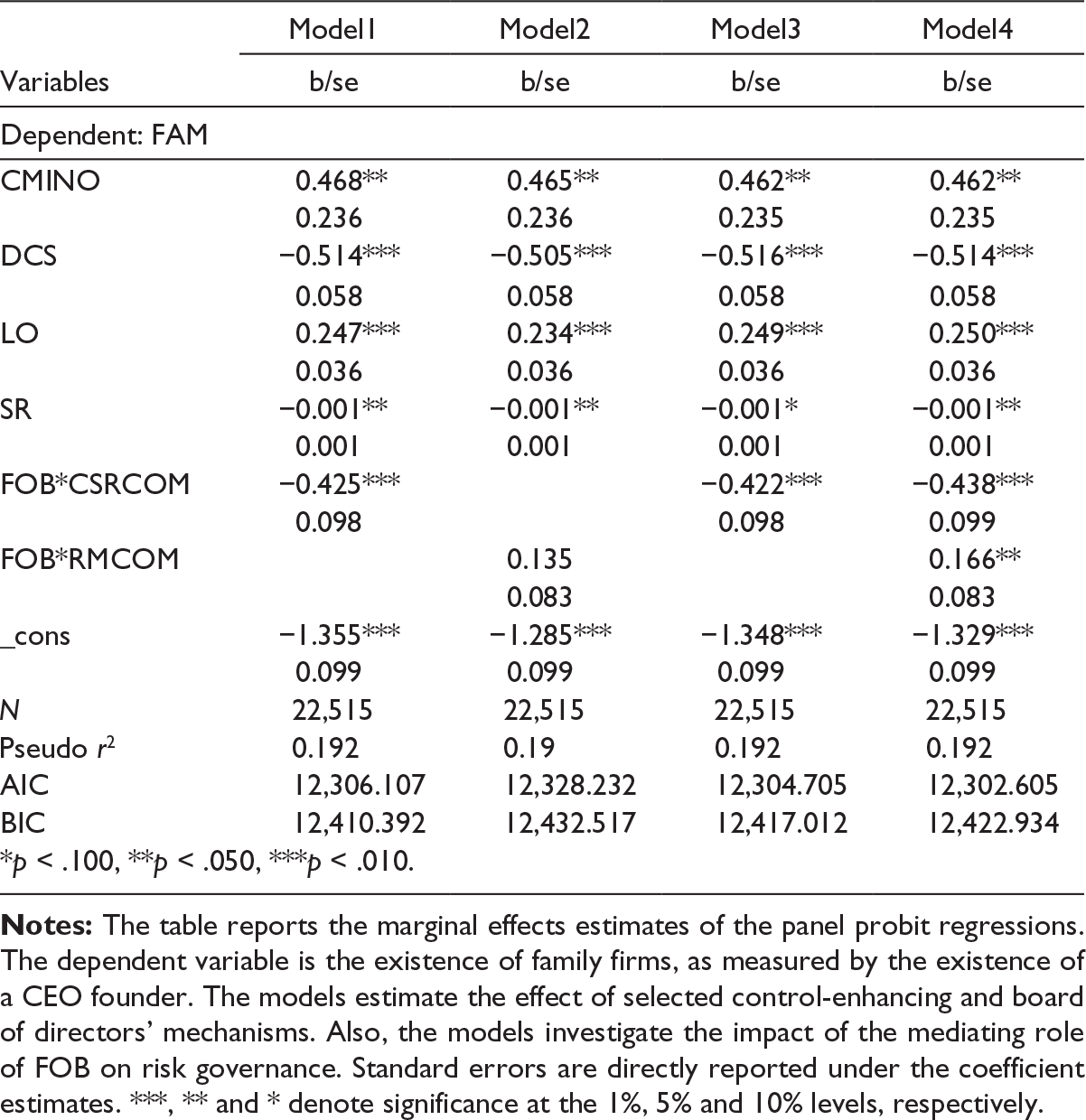

Next, the study looks at the interaction effect of FOB with both CSRCOM and RMCOM reported in Table 6. The study does so by examining the effect of the cross variable between FOB and both committee dummies. This relationship is examined by committee type. In model 1, the existence of FOB when used as a moderator for the existence of the CSRCOM significantly reduces the existence of such a committee in family firms. This moderation effect is robust in model 3, when the risk management committee is added. Model 4 shows that FOB as a moderator reduces the existence of CSRCOM but significantly increases the existence of a risk management committee in family firms.

Panel Probit Estimation: Interaction Regressions.

Robustness Checks

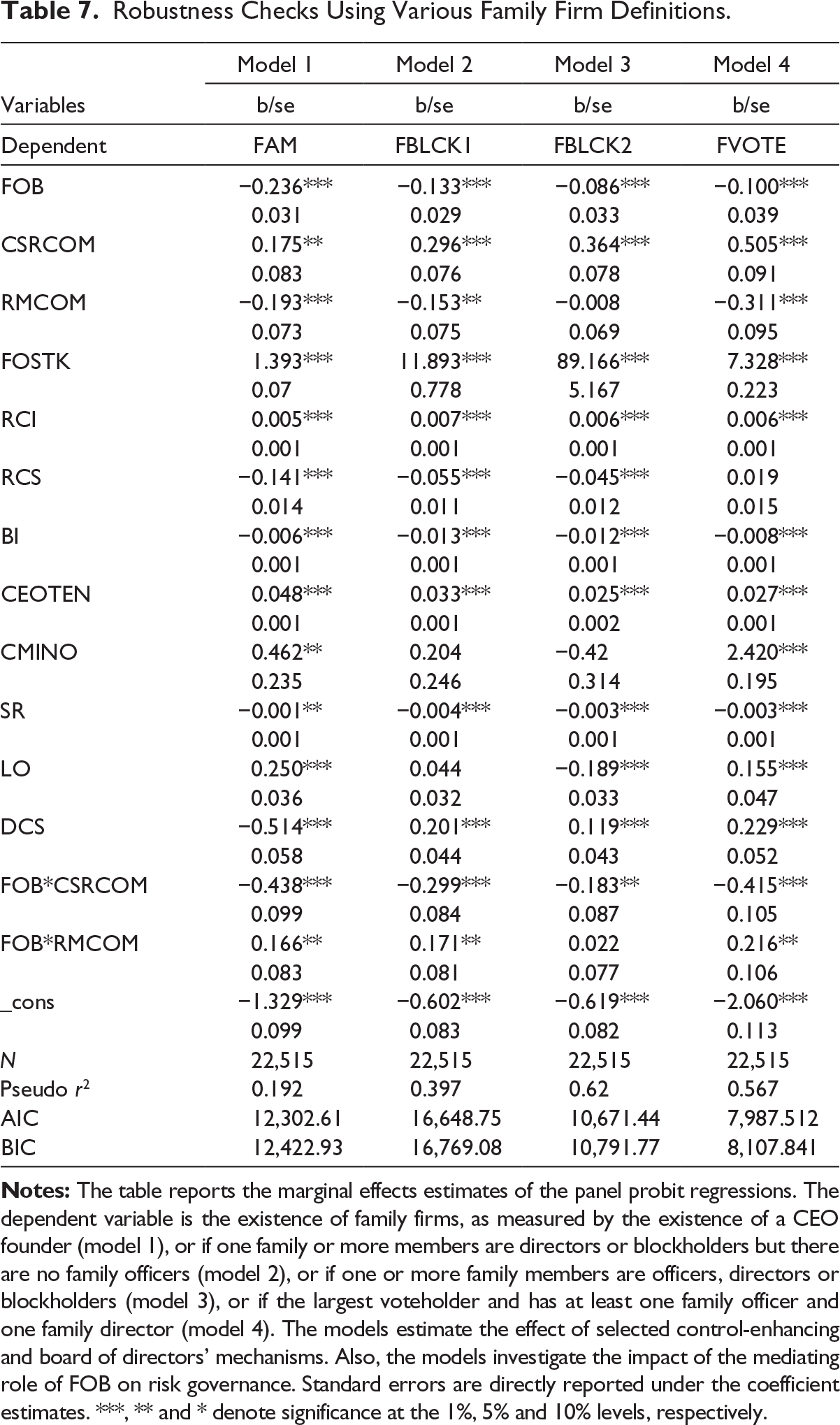

Table 7 reports the results of the robustness of the regressions with the moderating effect of FOB on both committees of the board. Model 1 repeats the same last regression from Table 6 for comparison. The study considers alternative definitions of the existence of family firms in models 2, 3 and 4. The study starts by examining the existence of one or more family members as directors or blockholders without having any family members holding office in the firm. This regression’s results are presented in model 2. The moderating effect of FOB on the CSR and risk management committees is robust to this new definition of family firms. Additionally, the study examines the definition of family firms as having at least one family member (whether a founder, descendant or family member) on the board or in the executive management or as a large shareholder of the firm. The result of the estimation of the regression using this definition is shown in model 3. The moderating effect of FOB continues to significantly reduce the chance of a CSRCOM on the board. When the definition of family firm is characterised by the family ownership stake being the largest voteholder and at least one family member is a board member, the results are shown in model 4. The moderating effect of FOB on both committees is robust to this specification of family firms as well. It is noteworthy that the pseudo r-squared for this model approaches 57%, indicating that this model explains a large proportion of the probability of a family firm existing. Results in Table 7 show that, for various definitions of family firms, the FOB significantly reduces the probability of family firms being formed. The role of CSRCOM seems to be invariably positive and significant for the family firms in this table. However, the role of the RMCOM tends to be negative and significant on such firms. The interaction terms of FOB and both committees are robust to different measures of family firms.

Robustness Checks Using Various Family Firm Definitions.

Discussion

One of the main findings concerns the negative effect of FOB on the likelihood of family firms to exist, which is in line with the agency theory that stresses family firms’ emphasis on socioemotional wealth preservation control (Garcia-Meca & Santana-Martín, 2023; Marpaung et al., 2022). This sometimes limits female board representation, especially if women directors are perceived as outsiders or challenge concentrated family control. This leads us to reject Hypothesis 1. Such a finding could be explained from different perspectives. In this regard, appointing women to boards can foster different leadership styles and larger talent selection beyond the family. This can reflect a larger migration towards institutional legitimacy and professional governance, which potentially lessens classical family control structures and thus decreases the probability of a firm operating as a family business. Compared to their male counterparts, FOB could adopt a stakeholder-oriented perspective that does not align with the socioemotional wealth orientation of such firms. Such empirical results confirm those in Fleitas-Castillo et al. (2025), who report that female members possess a different way of apprehending and resolving conflicts as they focus on integrating, cooperation and consensus. That is why they notice that cash levels are decreased when female family members attain a critical mass on the board, thus reflecting a concern for a good reputation. According to Adams and Ferreira (2009), female directors are more independent from the impact of managers compared to their male counterparts. They also argue that female directors are prone to participate in monitoring and attend the board meetings. From this perspective, the presence of women on boards is linked to greater governance quality, which in turn comes at the expense of decreased family control; this may be unacceptable to family firms. Therefore, this finding does not support those of some researchers (e.g. Biswas et al., 2022; Vieira, 2018) who suggest that family firms are more likely to appoint female directors than non-family firms.

The empirical results also show the significant and negative relationship between the CSRCOM and the presence of family-managed firms. Ulrich and Fibitz (2018) show that fewer CG instruments are employed with a greater extent of family influence in the firm. The presence of CSRCOMs is shown to increase the chances of family firms, because they care to implement a rigorous set of checks and balances on their managers (Baraibar-Diez & Odriozola, 2019; Gennari & Salvioni, 2019; Meqbel et al., 2025). Such findings could be explained by the fact that family firms prefer to manage ethical and social concerns in an informal way, rather than formalising them through the establishment of a CSRCOM. Wishing to safeguard their socioemotional wealth, family firms can prioritise their family reputation, internal values and legacy and thus ward off formal governance committees. So, they tend to reduce external oversight and protect discretion. As a matter of fact, Upadhyay et al. (2014) report that a committee is considered as a dedicated monitoring mechanism, that can offer more adequate and effective control on managerial decisions related to environmental activities, as opposed to the full board level. From the resource-based view, the establishment of CSRCOM may not be considered key to adding strategic value for family firms. In this vein, Peters and Romi (2015) argue that a CSRCOM can be established for symbolic purposes. Bifulco et al. (2023) indicate that the CSRCOM fails to play a moderating role in the relationship between firm market value and ESG score. This allows us to reject Hypothesis 2A.

As well, the study reports the significant and negative effect of RMCOM on the presence of family firms. The existence of risk management committees in family firms has been explored by some researchers, such as Malik et al. (2023) and Bates and Leclerc (2009). Family firms naturally show risk aversion tendencies according to the organisational and social identity theoretical perspectives (Zahra, 2005). The underlying thesis argues that such firms exert strong monitoring control over their firms, thereby reducing the benefits from an RMCOM. The establishment of such a committee involves forming formal board structures, using documented procedures and delegating risk oversight, which does not obviously align with the personalised governance style operated in family firms. Such a result could also be attributed to the fact that family firms could prefer centralised control, flexible, informal decision-making, particularly when facing strategic/financial risks. In this respect, the presence of an RMCOM could require a formal oversight mechanism that weakens the control and monitoring of family firms regarding some important decisions (e.g. debt and investment). Worried about the loss of autonomy, such firms may avoid establishing such a committee. From the socioemotional theory perspective, a desire to protect their identity, legacy and control could lead family-managed firms to avert governance mechanisms which could dilute such values. In this regard, D’Este and Carabeli (2022) report that family managers contribute to influence firms’ risk choices. This leads us to fail to reject Hypothesis 2B.

As a result of the above, it is curious to investigate the role of women in risk, governance and innovation to discover opportunities in other areas of managing the firm that can show that women are naturally better equipped at advancing the company. More precisely, the study investigates the moderating role of FOB on the relationship between the establishment of CSRCOM and RMCOM and the presence of family-managed firms. The empirical findings indicate that the presence of women on the board contributes to reducing the establishment of a CSRCOM, but increases the presence of an RMCOM in family firms. Bettinelli et al. (2018) explain such a finding by the females’ limited competencies and business skills. Compared to their male counterparts, women can have less ability to influence the firm’s decisions (Bettinelli et al., 2018) or are more focused on protecting family interests and preserving policies established by other family members (Rodriguez-Ariza et al., 2017). On the other hand, risks could be managed informally in family firms. Nevertheless, the appointment of women on the board could push for more formalised structures (e.g. RMCOM) in order to decrease the exposure to financial, strategic and reputational risks and guarantee better monitoring and oversight. By pushing to create an RMCOM that offers a better structured oversight of family-level risks. This allows us to confirm Hypotheses 3A and 3B.

The main contribution of this article is to provide a novel and thorough examination of the agency and resource-dependency theories in family firms, by specifically focusing on the often-overlooked role of reputation building. The study achieves this objective through the moderating effect of women on reducing CSROM and increasing RMCOM on the BoD in these types of firms. Arguably, the presence of FOB, because of their communal and communicative traits, can improve socioemotional wealth and signals improved CG reputation in the firm (Abbas & Frihatni, 2023; Wang et al., 2023). Cruz et al. (2019) argue that female family directors may impact board decisions in favour of CSR activities. If this signalling effect of governance reputation is true (Korenkiewicz & Maennig, 2023; Navarro-Garcia et al., 2022), the presence of female directors can be seen as negating the benefit of having a CSRCOM in the firm. Therefore, it is more valuable to set up a trusted identity that aligns with the family and focuses on social performance than with the pursuit of financial performance (e.g. Chua et al., 2003). In this regard, Jurado-Caraballo and Quintana-Garcia (2024) argue that corporate reputation seems to adequately solve asymmetric information in firms. By positioning themselves as engaged in gender diversity, firms manage their own reputation and attract stakeholders’ attention (O’Connor, 2001; Waymer & VanSlette, 2013). In this regard, a positive relationship was shown between the inclusion of diversity and the firm reputation (McMillan-Capehart et al., 2010). Subsequently, female board members could contribute to improving the legitimacy and credibility of such committees. Therefore, family firms that have good female board representation and establish RMCOM and CSRCOM can be perceived by stakeholders as more authentic, which in turn improves the reputation of both family and business. Hence, the existence of female board members can contribute to moderate the relationship among such governance structures and the company’s reputational outcomes in family firm contexts. In this regard, Navarro-Garcia et al. (2022) show that female directors enhance corporate reputation.

Control minus ownership is strongly associated with family firms. This practice may entrench directors; however, it may also reinforce their monitoring function to the point that it can make the degree of disclosure to the market analysts/discipline for corporate control less vital (Anderson et al., 2003; Maury, 2006; Morck & Yeung, 2003; Zhou et al., 2013). DCS may not always be associated with family firms since they reduce firm value (Villalonga & Amit, 2009) show that family firms use DCS more than non-family firms, to simultaneously maintain control of their firms and reduce their portfolio risk (Barontini & Caprio, 2006; Hagelin et al., 2006). Based on both findings, Hypothesis 4A, which states that control minus ownership is higher in family firms, seems to be supported by this sample. Hypothesis 4B is not rejected, confirming that DCS are less prevalent in this type of firms based on the fact that they tend to be better managed and more concerned about firm value. Family ownership is highly significant in family firms, supporting Hypothesis 4C and the idea that such firms try to reduce threats to corporate reputation as explained in Deephouse and Jaskiewicz (2013), Adewole (2024), Al-Dubai et al. (2014) and Demsetz and Lehn (1985).

The CEO tenure, the number of years each CEO has served, is positive; this result is consistent with the evidence of Ghosh et al. (2015), Schulze et al. (2001), Anderson et al. (2003) that family firms display survivorship bias leading them to hold longer to their CEO, who become more entrenched. This also implies that family firms care about their reputation since they favour a focus on such a long-term non-financial return (Anderson & Reeb, 2003). Family firms are characterised by independent remuneration committees, in their effort to monitor the remuneration of managers. They may invite many independent directors (Jong & Ho, 2020) to the remuneration committee. The RCI and size are vital governance aspects since they measure the BoD’s taking charge of the firm’s practices.

Main and Johnston (1993) and Cybinski and Windsor (2013) back family firms enjoying more independent remuneration committees. This shows that family firms are interested in using board mechanisms to improve CG and preserve the firm’s loss of reputation, in line with Deephouse and Jaskiewicz (2013). Moreover, the results show that its size is smaller in family firms enjoying more control, in line with Main and Johnston (1993). Boards were found to be less independent, especially when family directors are likely to hire directors who are close friends, lawyers and accountants to the board, which additionally compromises director objectivity in line with Schulze et al. (2001). This result disagrees with Bartholomeusz and Tanewski (2006). The study further found that independent directors of the board owners, when interacting with family ownership stake in family firms, tend to invest more in the firm (results not reported here). This result perhaps indicates that independent directors, being close family affiliates in this case, are positively encouraged to invest when large family ownership exists. A reasonable explanation for this result could be that the aptitude of such outsiders to monitor family management may be compromised by their lack of effectiveness in minimising family controls, hence failing to reduce agency costs II (Schulze et al., 2001; Ward & Handy, 1988).

Lastly, legal origin is positive and significant, pointing to the likelihood that family firms are mainly located in common law countries (code = 1 in Table 1). According to Ortiz (2025), high inheritance laws can reduce family involvement in managing family firms, in trying to minimise expected succession costs. Not all civil law countries are homogeneous in this regard. Ortiz (2025) mentions that Scandinavian civil law countries exhibit a lower incidence of family firms in favour of external management, backing up the obtained results. According to Shleifer and Vishny (1997), strong legal protection is needed for shareholders to invest in family firms. Therefore, shareholders whose rights are not properly guarded may use alternatives to protect their investments (Tanyeri Günsür & Alp, 2023) or may opt out of family firms, hence explaining the negative association of SR and family firms.

Conclusion

In summary, family ownership moulds CG by nurturing close oversight, emphasising long-term goals and creating unique governance mechanisms. However, it also introduces challenges that require careful management to safeguard business growth and continuity. The study contributes to the growing literature on family firms by providing a multi-year, multi-country analysis of a novel and thorough examination of the agency, signalling and resource-dependency theories; the study finds that family firms reduce the participation of FOB because they are more concerned about control, and believe they implement sufficient governance through direct monitoring of management. The study specifically focuses on the often-overlooked role of reputation and image building through the moderating effect of women on reducing CSRCOM and increasing RMCOM. The study controls in this model for control-enhancing, board structure (including family firms’ ownership stake) and institutional mechanisms. This article uniquely presents, in a global setting, evidence on the signalling effect of reputation and image building through the presence of FOB, negating the benefit of being present on the CSRCOM. Moreover, family firms intricately relate FOB to the likelihood of being represented on RMCOM as a tool of managing risk governance. Family firms with high female board representation and that establish RMCOM can be perceived by stakeholders as more authentic, which in turn improves the reputation of both family and business.

Moreover, family ownership promotes a strong commitment to maintaining and enhancing corporate reputation through long-term focus, CSR efforts and alignment with family values. These firms balance their desire to maintain the governance and control tools by projecting a modern image on their reputation. The study also notes that family firms’ total agency costs may not fall, having higher agency costs II but lower agency costs I.

These firms use independent but smaller remuneration committees, have less independent BoD, enjoy concentrated family ownership, use a higher wedge between voting and cash-flow rights, tend to have survivor CEOs and to be situated in countries that have fewer SR. In other words, these firms impose their own risk governance, possibly to signal informatively better control over asymmetric information through having females and establishing an RMCOM.

In order to address the lurking agency costs II in family firms, the study proposes legal changes for family firms (i.e., more disclosure of ESG activities) in order to consolidate reputation building (see Sageder et al., 2018) and reduce the wedge between ownership rights and control rights. Boards should be more independent to avoid corporate scandals and ethical breaches, as independent directors are more likely to blow the whistle on doubtful practices. Furthermore, the study suggests a shareholder agreement to temper family control on voting on management decisions, which would be very well perceived by stakeholders and would be desirable for improving its reputation and image (Crisóstomo et al., 2023).

The empirical results can provide insightful practical implications for different stakeholders. For management teams, appointing women on boards and officialising governance frameworks through CSRCOM and RMCOM seem to be crucial to foster the reputation, image and authenticity of both family and business. Clear communication of risks and governance processes, and transparent monitoring and reporting, not only hold family members accountable but also reduce over-concentration of power and promote objective decision-making in the firm. Another implementation of risk governance in family firms would be to support objective succession plans, reduce personal bias and secure long-term sustainability. For investors and portfolio managers, an FOB representation and the existence of risk governance committees can help them through enhancing investor protection and ethical values, ameliorating management professionalism and reducing governance-related risks, making such firms more appealing as a component of diversified investment portfolios.

Further research could study the relationship between founding family business and market maturity, the factors for the founder as CEO to be successful, and why descendants generally perform less than founders. Future studies could also investigate the impact of environmental practices and greenwashing practices on the family firms’ reputation.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.