Abstract

This study aims to explore how CSR-related messages posted by CEOs on social media are beneficial in fostering social capital, which in turn impacts the FP and online reputation of the firm. The study also examines whether there is any difference in FP due to sharing of CSR-related messages by CEOs before and during the pandemic. Hierarchical regression is used to examine the influence of CEOs CSR related tweets on FP and online reputation. The study reveals that by posting CSR-related messages on Twitter, CEOs can build social capital available on social media, which leads to better FP and online reputation. Findings also indicate that there is no statistically significant difference in FP and online reputation of the firm due to sharing of CSR-related messages by CEOs before and during the pandemic. Our research makes a significant addition to the empirical studies of CSR, social media and social capital theory.

Introduction

Cash flows for corporations have been significantly impacted due to COVID-19. While the effect may only last a short while for some companies, it will persist for a long time and cause financial misery for companies (Ellul et al., 2020). Social media improves communication within and across companies with a diverse group of internal and external stakeholders (Schniederjans et al., 2013). A firm’s social media communication should include CSR content to provide opportunities for the consumer to co-create values with the relevant brands (Okazaki et al., 2020). The growth of both investments and socially responsible activities offers an opportunity for firms to improve their efficiency in the most significant way (Kapelko et al., 2021).CSR communication impacts consumer reactions and purchase intentions of the customers (Bartikowski & Berens, 2021). Sustainable business practices and the return on equity (ROE) of the firm are highly correlated (Medcalfe et al., 2022). The financial performance of the firm will positively improve as a result of using social media (Schniederjans et al., 2013).

Past literature indicates that many CEOs are not on social media platforms due to many reasons, such as (a) A brand’s reputation may suffer through improper use of social media. If an executive of a company posts inappropriate content on social media, the company can control the damage to its reputation. However, if the CEO of a company posts inappropriate content on social media, it becomes challenging to control the damage to reputation. (b) Many CEOs purposefully refrain from posting on social media for a number of reasons. They might not desire unconstrained attention or the need to concentrate on managing and frequently updating a social media platform (Forbes, 2016).

Good corporate governance and corporate ethics are ensured by the integration of CSR into all aspects of a company’s operations (Atale & Helge, 2014). It can be easier for a corporation to be perceived as socially responsible if it shows support for societal goals and sustainable development. This corporate social responsibility, often known as CSR, needs to be efficiently communicated because excessive communication could have a negative effect on how consumers view the company (Viererbl & Koch, 2022). The dissemination of information about a company’s activities related to its CSR can help chief executive officers improve the attitudes and behaviours of stakeholders toward the organization (Thakur, 2023). Many firms are not following the practice of presenting their CSR activities in a transparent manner because negative corporate social responsibility disclosures create idiosyncratic risks for the firms (Mishra & Modi, 2013). Negative Corporate social responsibility disclosure may worsen these risks and provide further weapons to competitors and critics with hidden agendas (Dubbink et al., 2008). Firms avoid disclosing their corporate social responsibility activities transparently because they fear losing legitimacy, their image or facing other undesirable outcomes (Mishra & Modi, 2013).

Social media provides organizations with a way to communicate with their customers in real-time. Organizations can gain a competitive advantage by having a presence on social media platforms (Ravaonorohanta & Sayumwe, 2020). A vital component in creating strategic initiatives is organizational identity, which is viewed as an intangible asset of an organization (Ybañez et al., 2023). We assumed that discussion about the CSR activities of the firm on social media is the social responsibility of the Chief executive officers. Such types of information sharing about CSR not only increase awareness about CSR activities among the stakeholders but also draw attention to the potential for the firm of the CEO to adopt appropriate CSR practices. Corporate executives play a crucial role in maintaining openness, good conduct and governance for CSR (Muniapan & Satpathy, 2013). Implementing CSR strategies and environmentally friendly innovations for goods, processes, and services can help businesses make decisions that will ultimately result in steady revenue, enhanced profits, a steady customer base and enhanced market share (Le, 2022).

Our study extends prior research that mainly focused on the aggregate concept of CSR. The present research aims to identify the impact of segregate CSR orientation of CEOs on Twitter and its impact on FP and online reputation of the organization because the aggregate concept of CSR carries the risk of neutralizing individual dimensions of CSR. Prior literature (Galbreath & Shum, 2012; Gillan et al., 2021; Lee, 2020; Lins et al., 2017; Pham & Tran, 2020) identified the impact of CSR reporting or CSR disclosure on FP. Business performance is negatively impacted by the COVID-19 outbreak. The detrimental impacts of COVID-19 on business performance are mitigated in nations that have superior institutions, more developed financial systems, and superior healthcare systems (Ellul et al., 2020). The pandemic has worsened people’s sense of fear and uncertainty because they could lose their jobs and their source of income. The temporary closure of the industries of entertainment, transportation, farming, construction, retail, restaurants, textile, jewels, production, and start-ups results in a significant loss of revenue (Debata et al., 2020). Therefore, The study also examines whether there is any difference in firm performance due to sharing of CSR-related messages by CEOs before and during the pandemic. Prior literature (Galbreath & Shum, 2012; Gillan et al., 2021; Lee, 2020; Lins et al., 2017; Pham & Tran, 2020) not explored how CSR-related messages posted by CEOs on social media, helpful in building social capital, which in turn impacts the FP and online reputation of the firm.

The current study uses the social capital theory as a theoretical framework. The term ‘social capital’ refers to the intangible assets that individuals have access to and are related to their network of social bonding (Bourdieu, 1986). The social structure of networks, regulations, and trust that fosters public collaboration and coordination for mutual benefit is known as social capital (Putnam, 1993). A person’s social capital is their goodwill. Individuals are able to make use of goodwill to facilitate the sharing of information, the exertion of influence, and the accomplishment of shared goals (Adler & Kwon, 2002). Social influencer CEOs disclosed more about CSR initiatives than CEOs of Fortune companies, which may have helped them get more shares and likes from Twitter’s social capital (Grover et al., 2019). Social capital is a new idea that has a lot of potential for evaluating the significance and worthiness of public relations efforts (Taylor, 2011). An intangible asset that people can access and is associated with their social bonding is social capital.

Corporate managers know that CSR activities are helpful in building social capital and trust (Lins et al., 2017). Social capital measures the value of social relationships and connections that improve economic capital and boost the financial position of the company or organization (Smerek & Denison, 2007). Social capital affects corporate performance, especially for companies that value formal and informal networking (Saha & Banerjee, 2015). For instance, in two current surveys of CEOs conducted by PwC (2013, 2014), CEOs acknowledged having intentions to increase their companies’ involvement in CSR projects to regain stakeholder trust post the crisis. However, there is a dearth of scholarly literature on social capital and CSR. A book written by Sacconi and Degli Antoni (2011) presents a collection of empirical studies indicating that corporations can generate social capital and trust through CSR practices. Past research (Grover et al., 2018, 2019) indicates that CEOs can build social capital by posting CSR messages on Twitter.

Business organizations can assess social capital in public relations at the organizational level by offering public access to information, services, and networking tools through CSR activities (Taylor, 2011). Strong social capital, as measured by CSR intensity, was associated with higher stock returns (Lins et al., 2017). Two elements determine an individual’s social capital: (a) the place of a person within the network and (b) the individual’s access to weaker ties within the network (Burt, 2000). A company’s social capital may contribute to its (a) long-term viability; (b) edge over its rivals; and (c) success in providing services; and it can create more opportunities for the company if it is strategically utilized (Thakur & Hale, 2013).

We attempt to address the following research questions through a big data-based research methodology using mixed research methods (Grover et al., 2019).

How does CSR orientation of CEOs on social media impact financial performance of the firm?

How does CSR orientation of CEOs on social media impact the online reputation of the firm?

How does CEOs’ CSR orientation on social media impact firm performance pre and during COVID-19?

This study had been divided into six sections. The first section of the study presents an introduction. In the second part, we provided an overview of the theoretical background, model development and hypotheses development for the study. The third part presents the research methodology used for performing the analysis. The fourth part presents the findings of the study. In the fifth part, we present a discussion of the study. The sixth part contains the conclusion of the study.

Theory and Model Development

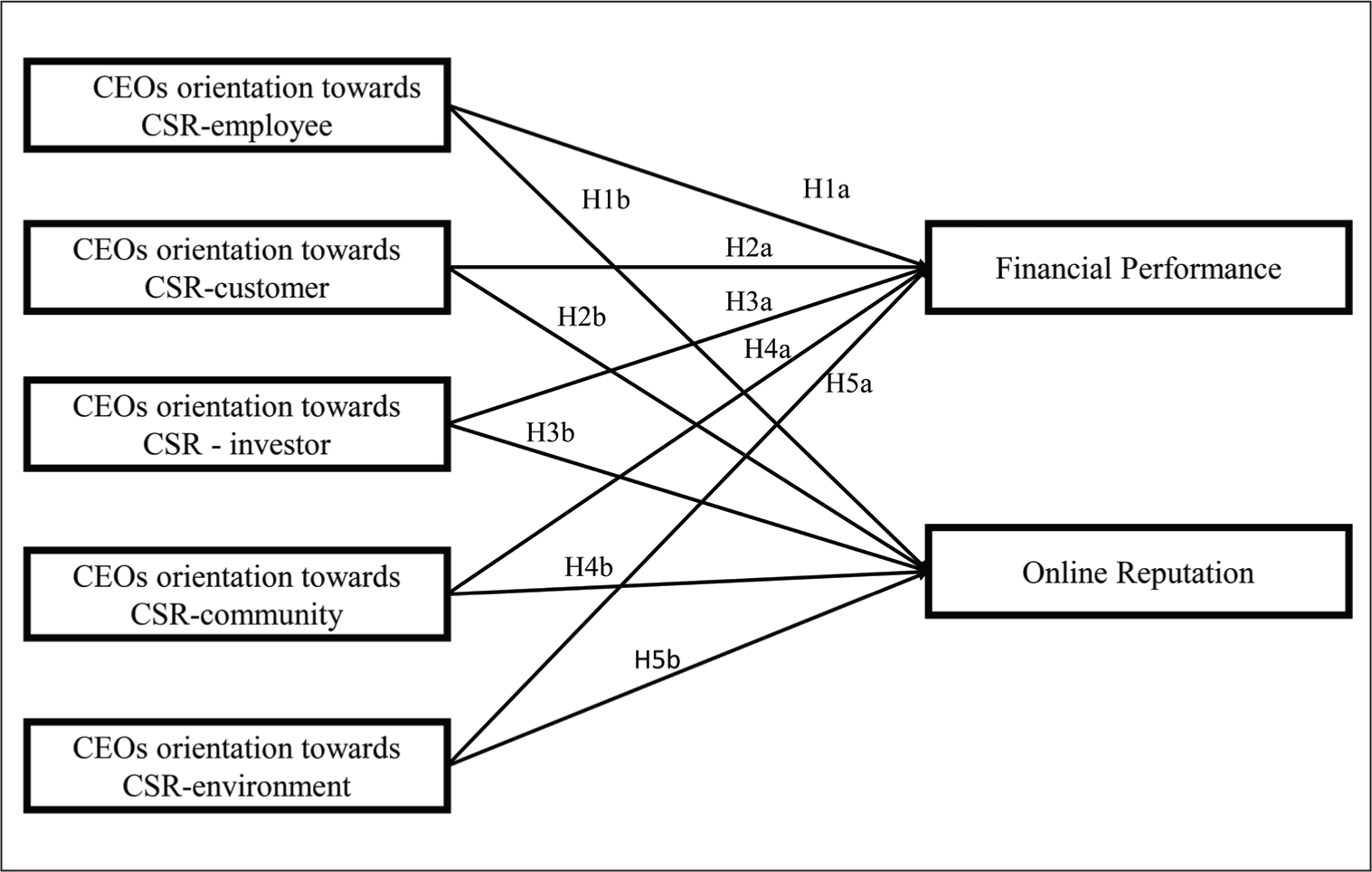

The success of a firm depends on positive employee attitudes, and CSR is one approach to achieving this (Santhosh & Baral, 2015). Sharing messages related to employees, work engagement, workplace and diversity on social media platforms encourages stakeholders to provide feedback on CSR-related policies of firms; based on the received feedback, the firm can improve their employee-related CSR practices, which in turn improves job satisfaction of employees (Abitbol & Lee, 2017). CSR serves as another weapon to strengthen adherence to organizational principles and raise staff morale (Jha & Dash, 2023). Figure 1 presents research model.

Presents Research Model.

The intention of a company to consider the welfare of employees and meet their needs is reflected in strategic policies and practices towards employees. CSR is recognized as an essential foundation that fosters employee loyalty, establishes legitimacy, shapes the public’s view, and facilitates good working relationships with other various stakeholder groups (Maqbool & Hurrah, 2020). Message quality and reliability of the source of messages or tweets positively impact the online reputation (Castellano & Dutot, 2017). Hence, we framed the following hypotheses:

H1a: CSR orientation of CEOs towards employees is positively associated with financial performance of the firm. H1b: CSR orientation of CEOs towards employees is positively associated with online reputation of the firm. H1c: When CEOs discuss about employees related CSR activities pre and during COVID-19, there is a statistically significant difference on financial performance and online reputation of the firm.

Concerning CSR, corporations are increasingly pressured to communicate their position and policies to customers and to show that they act in good faith and appear trustworthy (Kollat & Farache, 2017). Customer-orientated CSR practices increase the profitability of the company (Mishra & Suar, 2010). CSR improves financial performance by enhancing reputation and customer satisfaction (Pham & Tran, 2020). A lower customer satisfaction rate can harm the firm’s market value (Luo & Bhattacharya, 2006). The actions of customers who participate in brand co-creation are positively influenced by how they view CSR engagement on social media (Sung & Lee, 2023).

The customer feels satisfied when the firm responds to their messages on social media platforms, and customer satisfaction is positively associated with Tobin’s q and firm’s market performance (Chung et al., 2020). Corporate reputation can be improved by using engaging channels to communicate about CSR, which in turn leads to an enhanced return on investment, return on assets (ROA), sales growth and profit growth (Eberle et al., 2013; Galbreath & Shum, 2012). By focusing on corporate ability, CSR strategy impacts online reputation (Dutot et al., 2016). Hence:

H2a: CSR orientation of CEOs towards customers is positively associated with financial performance of the firm. H2b: CSR orientation of CEOs towards customers is positively associated with online reputation of the firm. H2c: When CEOs discuss about customers related CSR activities pre and during COVID-19, there is a statistically significant difference on financial performance and online reputation of the firm.

CEOs’ usage of social media for disclosure of firm activities impacts the investor’s judgments. Investors show less interest in investment when the CEO shows modesty while posting information about positive firm performance on social media. CEOs’ communication style on social media impacts the investor’s judgments and decisions about investment in the firm. Investors show less interest in investment when CEOs use humblebrags while posting information about positive firm performance. CEOs’ disclosure medium (conference calls and Twitter) also impacts investor judgments towards firms (Grant et al., 2018). Corporate social responsibility towards investors evaluates the policies and practises of the company regarding such problems as shareholder participation in decision-making, the independence of auditors, and the firm’s approach against insider trading. The widespread use of social media creates new problems and risks in maintaining a good relationship with audiences in online communities, both personally and professionally. Social networks influence the e-reputation of the firm (Castellano & Dutot, 2017). Hence:

H3a: CSR orientation of CEOs towards investors is positively associated with financial performance of the firm. H3b: CSR orientation of CEOs towards investors is positively associated with the online of the firm. H3c: When CEOs discuss about investors related CSR activities pre and during COVID-19, there is a statistically significant difference on financial performance and online reputation of the firm.

Community-oriented CSR activities consist of charitable contributions, community development programmes, public-private partnerships, community relationships, and the promotion of environmental protection programmes. Community-oriented CSR activities include Microsoft’s collaboration with an NGO, Hewlett Packard’s initiative for women self-help groups (Mishra & Suar, 2010). CSR initiatives affect the results that have a big impact on an organization’s reputation. CSR initiatives facilitate firms to enhance their reputation with a wide range of stakeholders, including employees, when firms engage in various community-oriented CSR practices (Esen, 2013). Hence:

H4a: CSR orientation of CEOs towards the community is positively associated with financial performance of the firm. H4b: CSR orientation of CEOs towards the community is positively associated with online reputation of the firm. H4c: When CEOs discuss about community related CSR activities pre and during COVID-19, there is a statistically significant difference on financial performance and online reputation of the firm.

With the growing importance of sustainable products, mechanisms, and utilities, enterprises focus on environmental laws to ensure their long-term viability and sustainability. Communication of environmental-related CSR activities on social media positively impacts customer relationships (Chu et al., 2020). Customer-to-customer correspondence activities in social media impact the FP of the firm (Parveen et al., 2015). The positive impact of assertive environmental policies on market share, return on assets (ROA), and profitability are significant in environmentally responsible firms (Ahmed et al., 1998). Environmental CSR has a beneficial effect on the reputation of a firm or brand and on the profitability of a company (Khojastehpour & Johns, 2014). Therefore, we framed the following hypotheses:

H5a: CSR orientation of CEOs towards the environment is positively associated with financial performance of the firm. H5b: CSR orientation of CEOs towards the environment is positively associated with online reputation of the firm. H5c: When CEOs discuss about environment related CSR activities pre and during COVID-19, there is a statistically significant difference on financial performance and online reputation of the firm.

Methodology

Following prior studies which explored mining user-generated content of CEOs for theory building (Grover et al., 2019; Kar & Dwivedi, 2020; Miranda et al., 2022), a mixed research methodology is used in the present study. To get critical insights, the article merged traditional data analysis techniques from social science research methodologies together with computationally intensive theory building that emerged from the computer science discipline. Availability and data access used to be a significant issues for information systems research (Kar et al., 2023). Data collection has been done from secondary sources; annual reports of companies, the internet and the company’s official website and social media, that is, Twitter.

Due to social desirability biases inherent in the aims, empirical research methods, including surveys, focus groups, interviews, and qualitative approach studies, cannot be used to investigate the questions of the study. This research used CEOs’ Twitter profiles because such tweets would reveal the leadership’s perspective on stakeholder-oriented CSR activities at a more personal and value-based level, revealing how enterprises would function under the CEO’s direction. Many organizations have more than one Twitter account, and experts usually maintain these accounts with a keen eye on pleasing social media users. Selecting the company’s own social media profile could lead to biases in the outcome since more carefully designed messaging targeting customers and shareholders would be analyzed. Therefore, tweets posted by the organization’s Twitter accounts were not used (Grover et al., 2019; Kar, 2020; Wang & Chen, 2020).

This section on research methodology has been further divided into two subsections. The first subsection explains how data has been collected from CEOs’ Twitter accounts. The second subsection discussed the methodology used for data analysis.

Data Collection

In order to collect our data set of CEOs, we first obtained a list of Fortune (2021) 1000 and Forbes Global (2021) 2000 companies from Fortune (2021) and Forbes (2021) websites, respectively. After that, we search the Twitter profiles of CEOs. In the end, 191 CEOs were found on the Twitter platform. Three criteria were established for the selection of CEOs to be included in the sample (a). We only considered only those CEOs who served in the company till the end of the financial year 2020. (b) We only included CEOs who had been in their positions for at least three years, from 2017–2018 to 2019–2020 or more. (c) We kept only those Twitter profiles whose tweets were in English. Such criteria excluded CEOs who served in companies for less than three years and those who left their companies before the end of the financial year 2019–2020. These three filters resulted in the final sample of 146 CEOs working in different companies (Capriotti & Ruesja, 2018; Grover et al., 2019; Kumar, 2022). The next task is to get the tweet posted on Twitter by CEOs. For data extraction, we use Python’s selenium module and Twitter APIs. In order to examine whether there is any difference on firm performance due to sharing of CSR related messages by CEOs before and during a pandemic, the tweets of the year January 2019 to December 2020 were segregated from the rest of their tweets.

Data Analysis

Outcome Variable

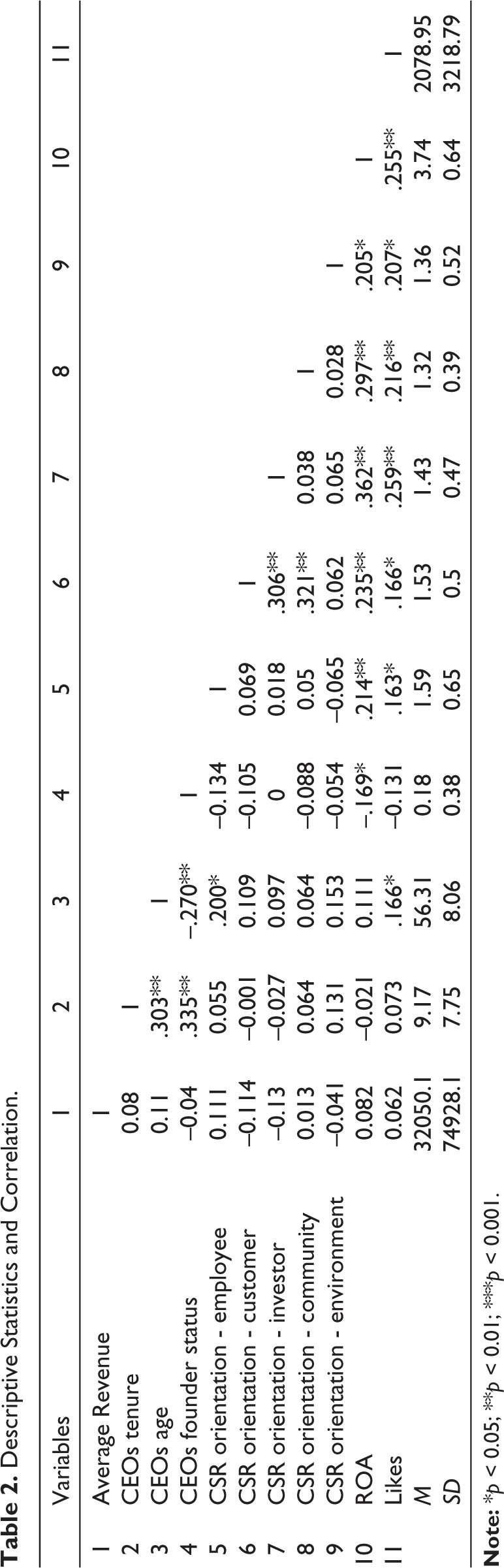

We assessed firm performance using an accounting-based measure: ROA (Adams et al., 2005; Bhat et al., 2018; Chatterjee & Hambrick, 2007; Malik & Makhdoom, 2016; Mishra & Suar, 2010; Wang & Chen, 2020). Data on accounting measure, that is, ROA were collected from annual reports of the companies for three years from 2017–2018 to 2019–2020 (Hansen & Block, 2020; Watson, 2007). A three-year average of ROA was collected from annual reports to eliminate any potential biases caused by a single-year figure (Adams et al., 2005; Mishra & Suar, 2010). We assessed the non-financial performance of the firm with online reputation, measured by likes received on CEOs’ Twitter profiles.

Explanatory Variables

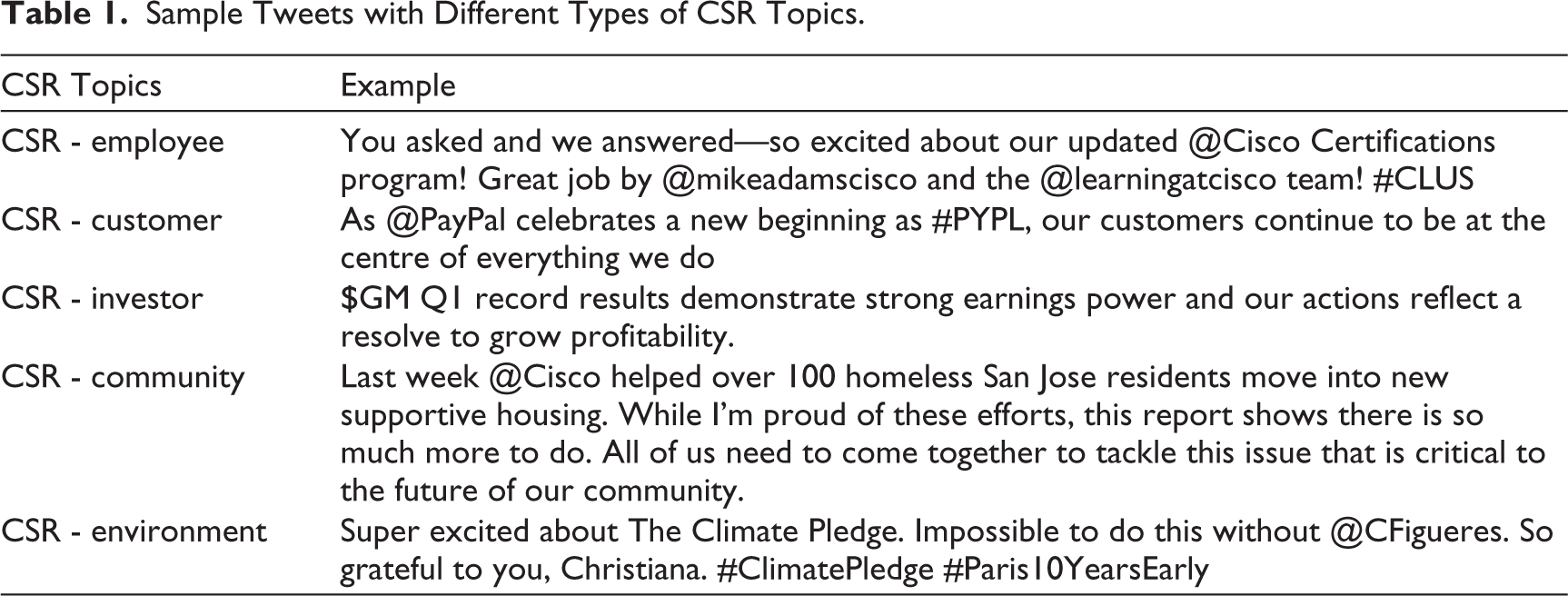

CSR-employee, CSR-customer, CSR-investor, CSR-community and CSR-environment related content posted by CEOs. After Twitter data extraction, the tweets were analyzed using the topic modelling approach. The Latent Dirichlet Allocation technique was used to perform topic modelling. The same approach has been used by (Grover et al., 2019; Kar, 2020). After that, Content analysis was performed on extracted topics (Kar, 2020; Kassarjian, 1977). In order to know about the CSR orientation of CEOs towards different stakeholders. Each topic was categorized into CSR activities: CSR- employees, CSR-customers, CSR-investors, CSR-community and CSR-environment. A research team of three individuals was created, one of whom had a background in corporate social responsibility research and two of whom had a background in information systems research.

A research team was formed to ensure category and inter-judge reliability. Following prior studies, all the 1,460 topics were evaluated, and three members of a research team allotted rates on a five-point Likert scale to the five dimensions of CSR. After that, inter-coder reliability was measured for all five dimensions of CSR (Kar, 2020). The reliability was between (Krippendorff’s a = 0.082) to (Krippendorff’s a = 0.087) for all five dimensions of CSR. Table 1 contains sample tweets for each dimension of CSR.

Sample Tweets with Different Types of CSR Topics.

Control Variables

Following prior studies, we control for four levels: CEO level, firm-level, CEO status as founder (0 = Not a founder and 1 = Founder) and industry level (Adams et al., 2005; Mishra & Suar, 2010; Wang & Chen, 2020). We control for CEO age and length of employment because active engagement in firm business dealings varies with age and length of service (Wang & Chen, 2020). We control firm size because firms may face varying degrees of bureaucratic momentum, and CEOs may possess varying power in firms of varying sizes. Firm size is measured by three years of average revenue from 2017–2018 to 2019–2020 (Mishra & Suar, 2010). We controlled for the industry effects by using a two-digit SIC code (Adams et al., 2005; Arena et al., 2018; Balasubramanian et al., 2020; Lins et al., 2017; Tang et al., 2018). We create a dummy variable with a value = ‘1’ if CEO is a founder and value = ‘0’ if CEO is not a founder (Adams et al., 2005). Data related to all firm control variables were obtained from annual reports of the companies, and information regarding CEOs control variables (CEO tenure and CEO age) were obtained from the internet and company’s official website after performing topic modelling and content analysis as mentioned in section ‘Explanatory Variables’.

Findings

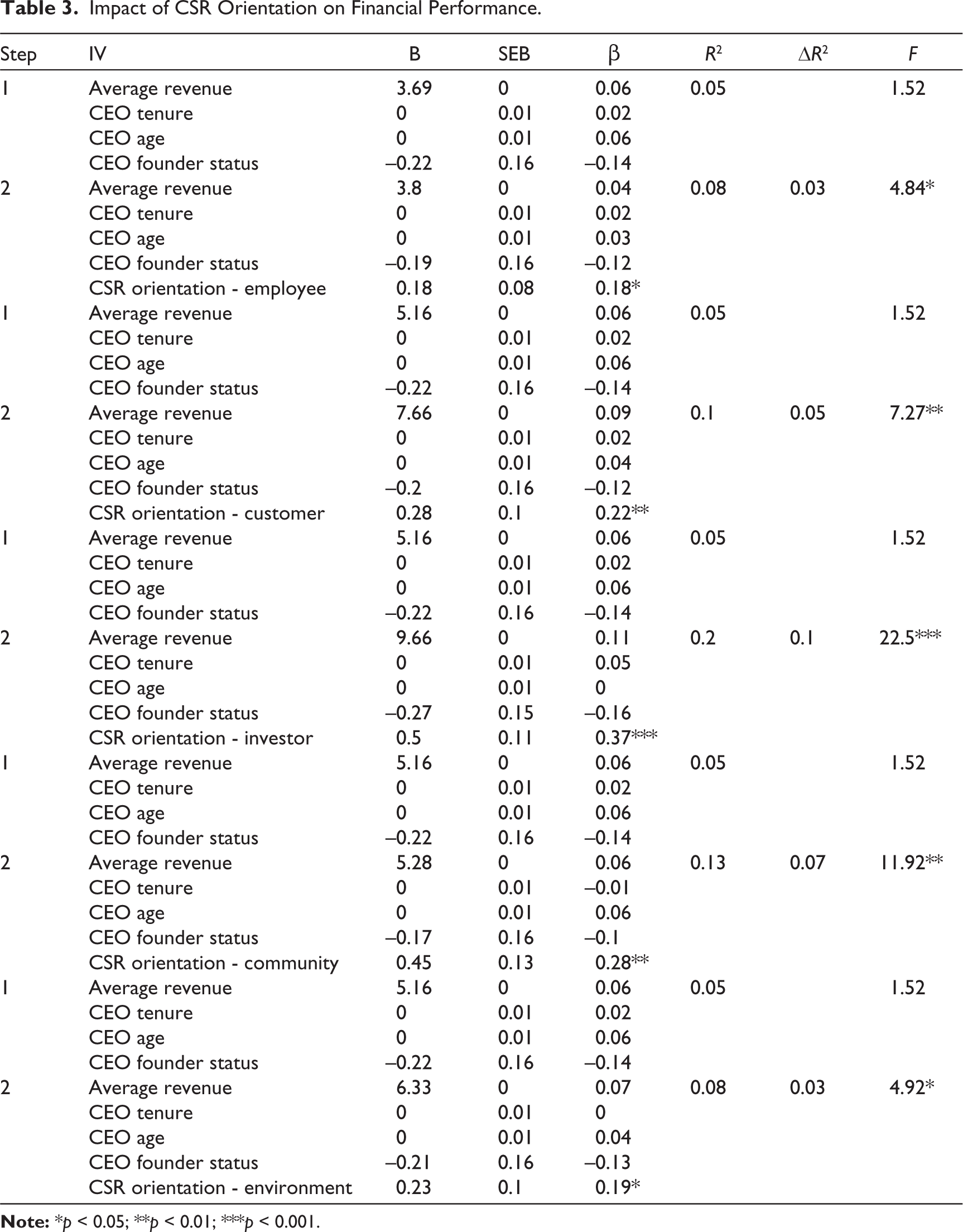

We used hierarchical regression for analyses. The results of the study supported H1a, H2a, H3a, H4a, H5a, H3b, H4b and H5b (see Tables 3 and 4).

Descriptive Statistics and Correlation.

Impact of CSR Orientation on Financial Performance.

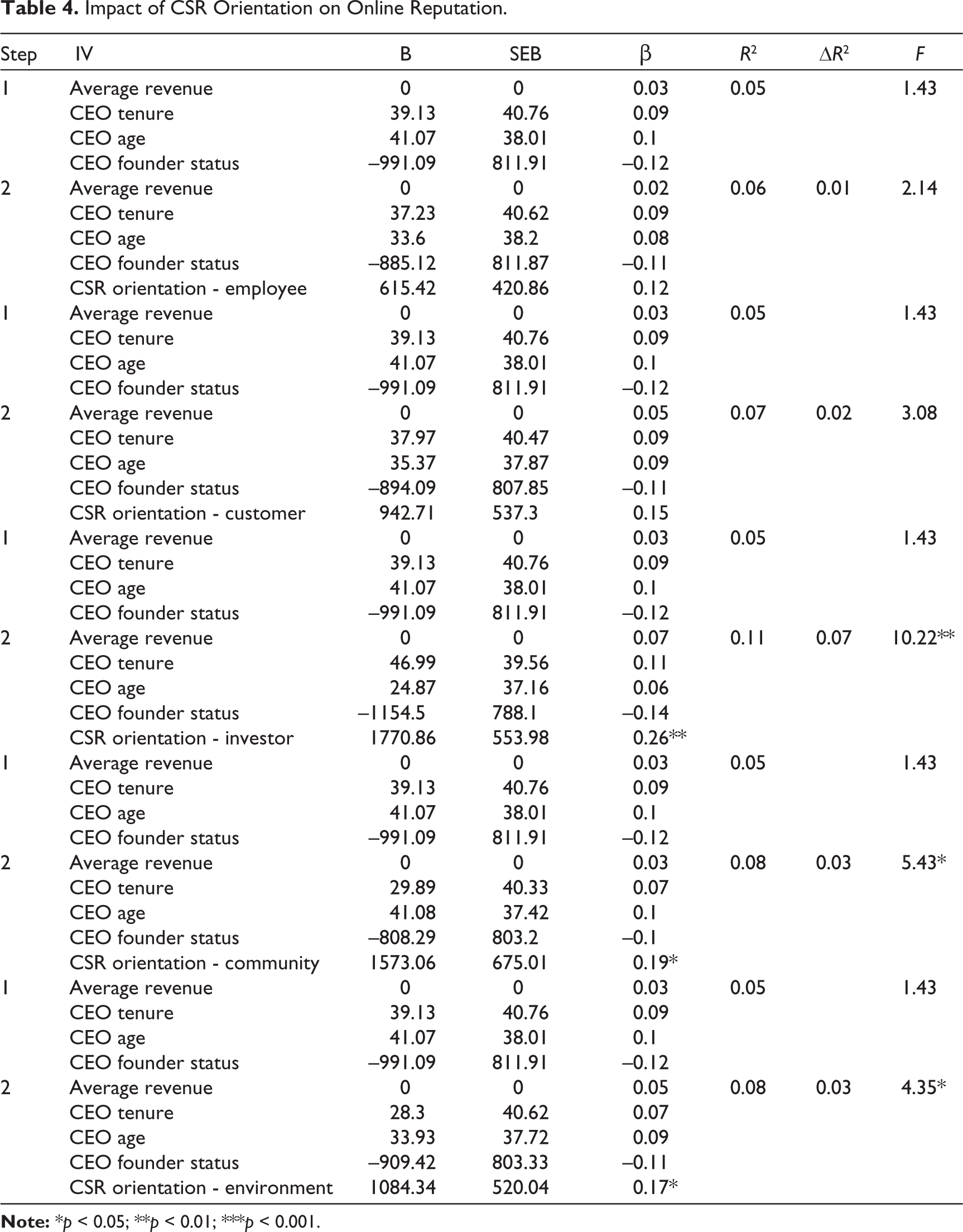

Impact of CSR Orientation on Online Reputation.

Mann-Whitney test was used to examine whether there is any difference on FP and online reputation of the firm due to sharing of CSR-related messages by CEOs before and during the pandemic. Our findings indicate that there is no statistically significant difference on FP and online reputation of the firm due to sharing of CSR-related messages by CEOs before and during the pandemic.

Table 2 presents the variables and their descriptive statistics. The correlation results revealed that CEOs who show favourable CSR orientation towards all five stakeholders—employees, customers, investors, community and environment in social media—had a higher ROA and e-reputation.

In the next step of the regression analysis, the CSR orientation of CEOs towards different stakeholders in social media impacted the firm’s financial performance. CEOs’ orientation on social media towards five dimensions of CSR, that is, CSR- employees, CSR - customers, CSR investors, CSR-community and CSR- environment, positively impact ROA of the firm.

CEOs’ orientation on social media towards CSR-investment, CSR-community, and CSR-environment positively impacts the average number of likes received on CEOs’ Twitter profiles.

Discussion

Our findings indicates that CSR orientation of CEOs towards different stakeholders in social media impacted the firm’s financial performance and online reputation. Stakeholders and investors of those companies who invest in CSR build trust in their companies, due to which the social capital of the companies increases and increased social capital improves financial performance of the firm (Lins et al., 2017). Our findings are consistent with past studies; interpersonal and intellectual dimensions of social capital have a notable impact on the financial performance of corporations (Smerek & Denison, 2007). Developing formal and informal networks allows small businesses to build social capital by building network relationships, establishing faith and collaborating on a shared goal with other stakeholders (Saha & Banerjee, 2015).

By voluntarily posting information on Twitter, organizations are rewarded for the incremental information that they provide. External stakeholder groups appear to interpret the number of a company’s Tweets as an indication of its openness and transparency, which in turn dramatically increases the company’s social legitimacy, trustworthiness, and customer loyalty, all of which contribute to enhanced corporate performance and e-reputation (Ravaonorohanta & Sayumwe, 2020). Therefore, it can be inferred that satisfied customers do not leave the company, due to which the company does not waste time finding new customers, which leads to better financial performance. When firms invest in employee-oriented CSR practices, employees will feel more satisfied with their jobs, and their job performance will improve as a result of such employee-oriented CSR practices (Golob & Podnar, 2021; Mishra & Suar, 2010). Our findings are consistent with previous studies; participating in CSR-related activities results in a better company’s reputation and increase customer satisfaction (Galbreath & Shum, 2012). As a result, reputation and customer satisfaction reduce trading costs, increase customer retention, and decrease customer defection, all of which directly impact financial performance. Communication of CSR activities by the organization on social media platforms leads to better consumer engagement (Chu et al., 2020).

Conclusion

The findings from this study provide valuable information about how CSR reporting in social media generates social capital, which influences the firm’s FP and online reputation. The present study also provides useful insights to start-ups entrepreneur, and they can also act like already established Fortune and Forbes Global CEOs and use social media platforms like Twitter to boost social capital, which leads to a better financial position and online reputation. Policymakers, academics and educators can use our findings to know about the significance of CEOs’ commitment to CSR. Our research makes a significant addition to the empirical studies of CSR and social capital theory. This study provides insights for firms whose executives do not use social media platforms for CSR reporting in social media and for those firms whose executives do not use appropriate use of social media to raise trust and reputation with financiers and stakeholders in order to build social capital, which in turn leads to enhanced firm’s profitability and online reputation. Dissemination of stakeholder-oriented CSR activities in the midst of a pandemic presents both immense challenges and massive opportunities for organizations. Disclosure of corporate social responsibility in a transparent manner in a clear and honest way gives organizatons a chance to be open and honest, which is helpful in building relationships, trust and recognition with the public. Firms can use different legitimation strategies while reporting about negative corporate social performance. Firms can report about ideas and measures implemented by the firm to tackle or avoid the negative performance or incidents in the future.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.