Abstract

The main aim of this article is to examine the relation between institutional ownership and stock liquidity. Using a large sample of Indian firm data for the period 2001–2012, we estimate two liquidity measures, Amihud illiquidity and HL-spread. We find that institutional ownership is negatively related to the stock liquidity. We also find that the negative institutional ownership–stock liquidity relation is mostly driven by foreign institutional investors (FIIs) and Bank ownership. Conversely, retail ownership is positively related to the stock liquidity. Importantly, we find that institutional investors are more likely to hold liquid stocks. These findings are consistent with the hypothesis that the level of institutional ownership proxies for informed investors, while they trade liquid stock to reduce price impact cost.

Introduction

Liquidity of a financial asset has been identified as an important factor in the smooth functioning of financial markets. It helps market participants to fulfil unexpected financial needs without undergoing into major losses. Liquidity is also a key factor in the price discovery of an asset and hence, it has received substantial attention from the researchers all over the world. Previous studies show that liquidity and returns are related directly (Amihud et al., 2005; Chu, 2013; O’Hara, 2003). In this article, we examine the relation between liquidity and institutional ownership by using two prominent measures of liquidity, Amihud (2002) and daily low-high spread (Corwin and Schultz, 2012) and various types of investor categories such as: foreign institutional investors, domestic institutional investors such as as mutual funds, banking institutions which comprise of banks, financial institutions and insurance companies, and non-institutional investors such as corporate investors, and retail investors. We also examine bidirectional relation of liquidity with each type of investor as well as aggregate ownership to find out the impact of each of the investor’s holding on the stock liquidity and vice versa.

The main emphasis of this article is on an emerging market where the legal system is weak and regulatory inefficiencies exist which makes it different from the developed markets. Hence, the existing evidence on the US and other developed markets may not be true for emerging markets. Moreover, previous studies do not incorporate heterogeneity among institutional investors. In this article, we argue that heterogeneity among different investor types may have diverse impact or preference for the stock liquidity. For example, in order to minimize the trading cost due to high churning, mutual fund managers prefer more liquid stocks as compared to venture capitalists. None of the previous studies examine the relation of heterogeneity of institutional investors and stock liquidity except study of Rhee and Wang (2009), which studies the relation of only foreign investors with the stock liquidity in Indonesian stock market.

In order to examine the relation between liquidity and institutional ownership, the researchers test two hypotheses: adverse selection hypothesis and trading hypothesis. Adverse selection hypothesis postulates that in the presence of informed traders who take the advantage of information, uninformed traders deter to trade. Therefore, large number of informed traders in the market leads to higher spreads, which in turn reduces liquidity (Easley and O’Hara, 1987; Glosten and Milgrom, 1985; Grossman and Stiglitz, 1980; Kyle, 1985).On the other hand, the trading hypothesis posits that in the presence of large number of informed traders, competition among them leads to free flow of information and which in turn makes the market more efficient. The improvement in the market efficiency reduces the uncertainty and informed traders are more likely to trade which increases the liquidity. However, the trading hypothesis posits that the stock liquidity reduces price impact in order to execute large trades (Demsetz, 1968; Merton, 1987).

To test the above hypotheses, we use the cross-sectional data of the firms listed on National Stock Exchange of India (NSE) for the period from 2001 to 2012. Our findings show that there is negative relation between institutional ownership and stock liquidity. The results are robust to two proxies used in this study: Amihud measure and Spread measure. Our results are consistent with the adverse selection hypothesis which says that the information asymmetry between informed and uninformed investors leads to lower liquidity. We find a significant negative impact when the institutional ownership variable is interacted with size, and business group dummy. The above results are true when we take the investor category to be homogeneous. Our results differ when we examine the relation of liquidity with various investor types. Each category of investors shows a different impact on liquidity. When we examine whether institutional investors demand for the stock liquidity to reduce price impact, we find that institutional ownership is negatively related to a lag of using Amihud (2002) and spread measures, showing that stock liquidity attracts institutional investors to form block ownership.

In summary, we provide extensive evidence to improve our understanding on the relation between stock liquidity and institutional ownership and our findings complement a rich literature on institutions’ roles in equity market. This study has several features that differentiate it from existing literature. First, prior studies use institutional ownership as a variable to measure its impact on the stock liquidity. However, we show that heterogeneity among institutional and individual investors also play significant role in the stock liquidity and our evidence is important in understanding the impact of diversity of institutional and individual investors. Second, we empirically test new measure of liquidity proposed by Corwin and Schultz (2012). Third, most of the evidences are reported on advanced countries. In particular, very minimal evidence exists with respect to emerging markets where insiders are expected to dominate the ownership. In this scenario, institutional investors play a passive role in corporate control. Therefore, this article will have information value for developed countries.

The article is organized as follows. Section 2 introduces to literature in this area. Section 3 explains the data and methodology. Section 4 demonstrates the empirical results and section 5 concludes the article.

Literature Review

Sarin et al. (1999) analyze the relation of ownership structure with the stock liquidity by taking bid-ask spread and quoted depth as proxies of stock liquidity whereas insider and institutional holdings are taken as proxies for ownership. The study uses 786 firms listed on NYSE/AMEX in the year 1985. The cross-sectional analysis shows that insider and institutional ownership has a positive relation with spread and negative relation with quoted spread. However, no relation is found between institutional holdings and adverse selection costs and at the same time, higher insider ownership leads to more information asymmetry faced by traders. The authors also report that the firms which have high fraction of institutional holdings have large average transaction size. Similarly, Naes (2004) also examine the relation between liquidity of stock and ownership structure of the firm using monthly data for a period of two years. The results show that the ownership concentration has a negative relation with spread and information costs. However, there is no significant relation between institutional ownership and liquidity.

Rubin (2007) investigates the relation between firm’s ownership structure and liquidity. The ownership is divided into three categories which are insider investors, non-insider investors and others. By analyzing NYSE TAQ intraday data for 20 quarters ranging from 1999 through 2003 for 1,369 firms, they find that the relation between institutional ownership and liquidity is two-sided. It is found that the liquidity has a positive relation with institutional ownership levels and negative relation with institutional concentration. As far as the relation of liquidity with insider ownership is concerned, a negative relation of insider ownership with the trade-driven measures of liquidity and positive relation with the order-driven measures of liquidity are found. Deviating from the previous work, Agarwal (2007) documents a non-monotonic (U-shaped relation) between liquidity and institutional ownership. The author examines the data of 8,558 US firms listed on NYSE and AMEX from 1980 to 2005. The results show that the net effect of institutional ownership on liquidity is the combined effect of both adverse selection and information efficiency.

Rhee and Wang (2009) add another dimension to the previous studies on the relation between institutional ownership and the stock’s liquidity by specifically examining the impact of foreign institutional ownership on the liquidity of the stocks listed on Jakarta Stock Exchange. Three measures of liquidity are studied which are: bid-ask spread, quoted depth and price sensitivity. The month-end free float percentage of shares held by foreign institutional investors is taken as a measure of foreign institutional ownership. The study examines the bidirectional relation between foreign institutional ownership and liquidity and finds results similar to previous studies. The results show that foreign institutional holdings have a negative impact on the liquidity which challenges the traditional notion that the foreign institutions increase the liquidity in an emerging market.

Data and Methodology

In this study, we use two measures of liquidity; Amihud (2002) illiquidity measure. Many studies such as Acharya and Pedersen (2005), Hameed et al. (2010) and Karolyi et al. (2012) have used Amihud measure to measure liquidity. Studies such as Goyenko et al. (2009) show that Amihud liquidity measure is more reliable measure of liquidity using daily data. Also, most of the studies on emerging markets are based on this measure as high frequency data is not available. It has been proved that Amihud measure is highly correlated with the high frequency benchmarks such as bid-ask spreads and depth measures. For a stock i in a year y, Amihud measure is calculated as follows:

Where, Ni,y is the number of days on which the stock is traded in a year and

Our second measure of liquidity is the daily high-low spread estimator called HL-spread measure given by Corwin and Schultz (2012). This measure gives a simple way to estimate bid-ask spread using daily high-low prices without the need of transaction level data. This measure has several advantages; it outperforms several well-known measures such as Roll (1984) covariance estimator, the LOT measure given by Lesmond et al. (1999) and it is very simple to apply. Unlike Holden (2009) or Hasbrouck (2009) measures, this does not need much time and energy to compute and hence can be used for larger samples. Specifically, it has been tested in the Indian context and proved to be highly reliable. It is computed in the following way:

Where,

and

Here, Ht and Lt are the daily high and low prices.

We calculate each of the measures on a daily basis and average them annually. We collect the data on stock prices, volume, etc. for all the NSE listed stocks from PROWESS database for a period of 12 years from 2001 to 2012. We collect the ownership data of each of the ownership category; foreign institutional ownership, corporate ownership, mutual fund ownership, ownership by banks and individual ownership from PROWESS database. We consider the percentage of shares held by each of the individual investor category for our study. We obtain this measure on an annual basis for each of the stock in our sample for the time period 2001–2012, which covers around 800 firms on NSE. We also calculate the stock returns on annual basis and standard deviation of the stocks over the year as a measure of volatility.

Empirical Results

Descriptive Statistics

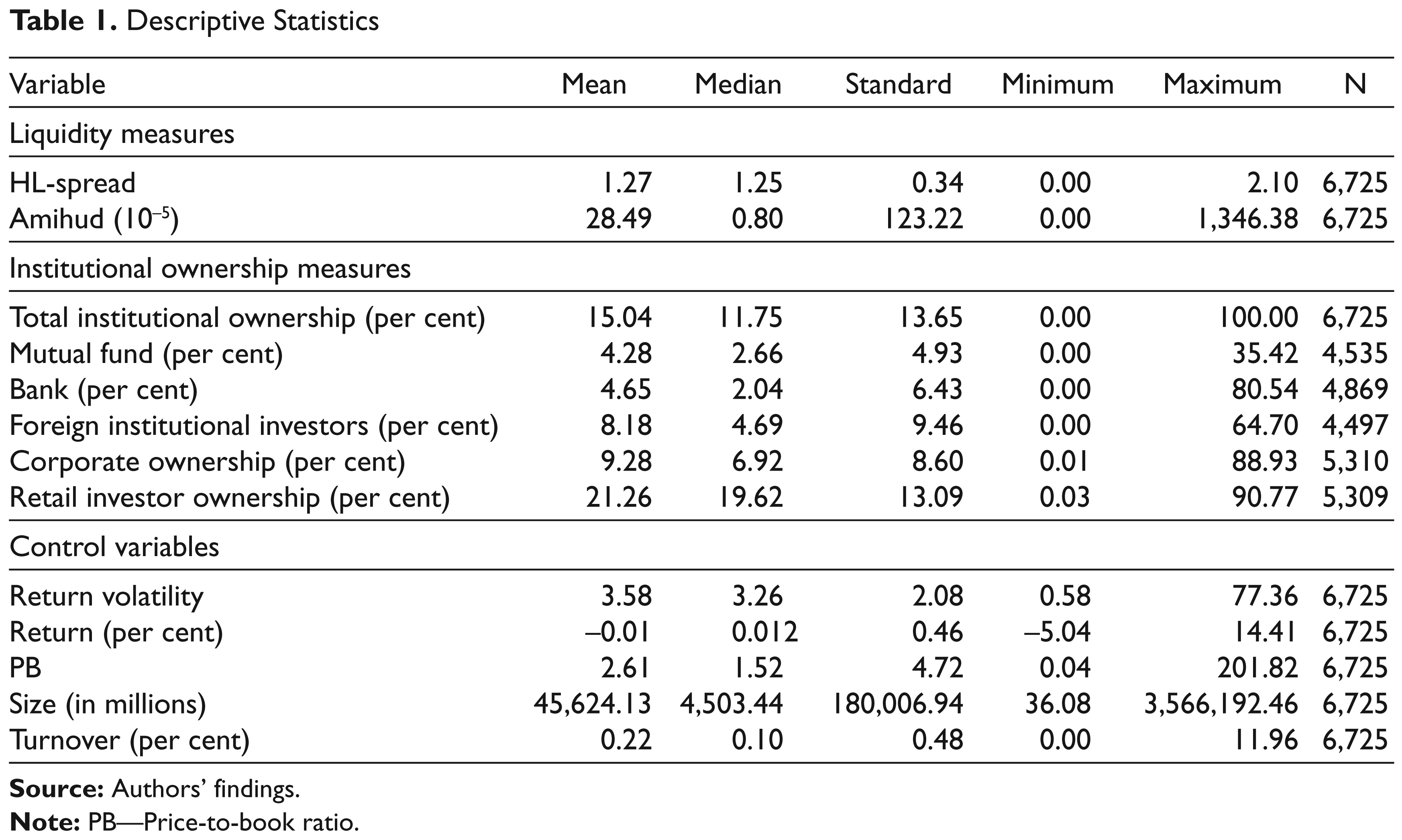

Table 1 reports the descriptive statistics of institutional ownership and proxies of stock liquidity; HL-spread and Amihud illiquidity. 1 We also report the descriptive statistics of all control variable used in the regression model. Our descriptive statistics show that institutions hold, on an average 15.04 per cent ownership in Indian firms, which are lesser than as reported on the US (27.5 per cent). One of the reasons of this variation could be a domination of insider ownership (49.11 per cent as reported by Sarkar, 2013). Moreover, we also find that Mutual Fund, Bank, Foreign Institutional Investors, Corporate and retail investors hold, on average, 4.28, 4.65, 8.18, 9.28 and 21.26 per cent respectively. The mean value of our stock liquidity proxies is 1.27 per cent for HL-spread and 28.49 for Amihud illiquidity. In our study the institutional ownership ‘Bank’ refers to banks, financial institutions and insurance companies. We grouped all three categories under one heading because all these investors exhibit the similar behaviour and also, many of the firms do not have sufficient observations on individual investor categories.

Cross-sectional Regressions for Relation between Liquidity and Ownership

In this section, we examine the relation between stock liquidity and institutional ownership. If institutional investors have access to price sensitive information we expect that HL-spread and Amihud illiquidity to be higher for firms with large institutional ownership than firms with low institutional ownership. To examine the relation between liquidity and institutional ownership, we estimate the following pooled regression.

The sample has NSE listed firms and the above summary statistics are calculated annually during the period from 1 January 2000 to 31 December 2012. HL-spread is high-low bid-ask spread and is calculated on the basis of daily high-low prices and is averaged annually. Amihud is the illiquidity measure given by Amihud and is also calculated on daily basis and averaged annually. Ownership measures are calculated on the basis of percentage of shares held by each investor type. Total institutional ownership is the percentage of shares held by institutions in the sample firm at the end of each year. Mutual fund is the percentage of shares held by mutual funds in the sample firm at the end of each year. Bank is the percentage of shares held by banks in the sample firm at the end year. Foreign institutional ownership is the percentage of shares held by foreign institutions in the sample firm at the end of each year. Corporate ownership is the percentage of shares held by other corporate firms in the sample firm at the end of each year. Lastly, Retail investor ownership is the percentage of shares held by retail/individual investors in the sample firm at the end of each year. Control variables are also calculated on annual basis. Return Volatility is calculated as standard deviation of a stock over the year. Return is the percentage log-return calculated annually. Price-to-book ratio (PB) is the ratio of market price to the book value of stock measured at the end of each year. Size is the total annual market capitalization measured in millions. Turnover is the volume divided by number of shares outstanding at the end of each year.

Descriptive Statistics

Where, Liqit represents either Amihud illiquidity or HL-spread for firm i in year t. Our list of control variables is motivated by previous studies (Rhee and Wang, 2009) that are deemed to be predictors of the stock liquidity. These include firm size, returns, return volatility, turnover and PB. Firm size (Size) is measured as the log of market value of equity.

Institutional investors may prefer large cap stocks; therefore, we include a lag of firm size. Returns are calculated as average of daily returns over a year. Standard deviation of a stock returns over the year is considered as a potential proxy of return volatility. Turnover is annual trading volume over a year scaled by total outstanding shares. We include this variable to control for heterogeneity among investors’ opinions as heterogeneity among investors may impact stock liquidity (Hong and Stein, 2003). One lag of dependent variable is also included to control for persistence in the stock liquidity.

Impact of Ownership on Liquidity

(ii) ***, ** and * show the value significant at 1, 5 and 10 per cent respectively.

(iii) IO—institutional ownership.

(iv) FE—fixed effects.

(v) N—number of observations.

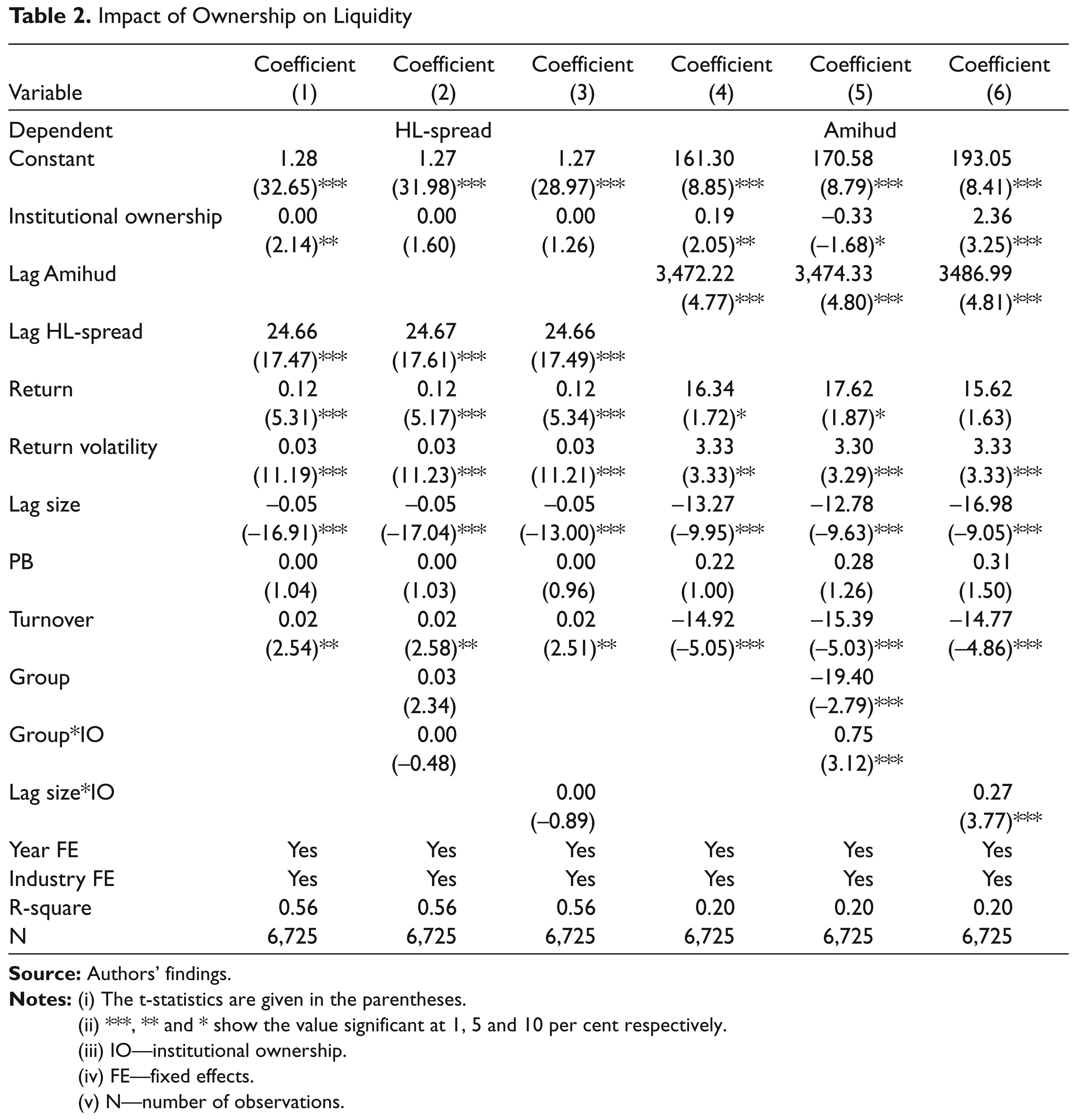

Table 2 reports the results of pooled regression where the dependent variables are HL-spread and Amihud illiquidity. The t-statistics given below the estimated coefficients are based on standard error clustered by firm and year (Thompson, 2011). We have included time and industry fixed effects in our pooled regressions to control for the unobserved heterogeneity that is constant over year and industry and correlated with the independent variable. We find strong evidence that institutional ownership increases stock illiquidity. For instance, the coefficients of HL-spread and Amihud illiquidity are 0.00 and 0.19 respectively and are statistically significant at 5 per cent level, suggesting that HL-spread and Amihud illiquidity increase with institutional ownership. This is consistent with our prediction that institutional ownership increases the risk of informed trading and imposes higher cost on market players resulting in less stock liquidity. Since, our results are obtained after controlling for stock characteristics including the lag of firm size, mean return, PB, turnover and volatility; hence our results cannot be explained by institutional investors following specific investment style. Specific investment style can be an explanatory variable for cross-sectional stock liquidity. Consistent with previous studies, we find that firm size is negatively related to HL-spread and Amihud illiquidity, indicating that large firms are more liquid than small firms. HL-spread and Amihud illiquidity increase with stock volatility; suggesting that the riskiness of a stock reduces the stock liquidity.

We also interact firm size and a dummy of business group affiliated firms with HL-spread and Amihud illiquidity; business group variable is a dummy variable which takes value one for firms affiliated with business group and zero otherwise. The rationale behind this analysis is to find whether business group affiliation and firm size matter along with institutional ownership. We expect that when two similar sized firms where one firm is dominated by institutional investors and other firm does not, then the firm with higher institutional ownership should have lower liquidity as compared to firm with less institutional ownership. Moreover, we do not predict any direction of the coefficient for firms affiliated with business groups and its interaction with institutional ownership.

Table 2 reports the regression results showing the impact of ownership variables on different measures of liquidity. In column (1), (2) and (3), the dependent variable is HL-spread and in column (4), (5) and (6), the dependent variable is Amihud illiquidity measure. Lag if both these liquidity measures are also taken as independent variables in their respective regressions. Lag size is the lag of size variable. Group is a dummy variable which takes the value when the firm is affiliated to business group and 0 otherwise. Interaction of group variable with IO (institutional ownership) and lag of size is also considered in the regression. Time and Industry fixed effects are also included in the regressions. N shows the number of observations. The definitions of other variables are given in Table 1.

However, previous studies (Khanna and Palepu, 2000) show that firm affiliated with business group is larger than that of standalone firm. Hence, we believe that the coefficient of business groups may be negative and the coefficient of interacted variable may be positive. We report these findings in columns 2, 3 for HL-spread and 4, 5 for Amihud illiquidity. These results are consistent with our predicted direction; the value of coefficient Size*Holding is positive (0.27) and significant at 1 per cent level, suggesting that similar sized firms with higher institutional ownership will have less liquidity than firms with lower institutional ownership. However, we do not find statistically significant coefficient where HL-spread is a dependent variable.

When we include business group dummy and interact with institutional ownership then we find that the coefficient of business group dummy is negative and statistically significant at 1 per cent level. Since, we also control for size effects in our regressions, therefore, the above result cannot be as a consequence of size effect. The coefficient of Business Group*Holding is positive and statistically significant at 1 per cent level, suggesting that institutional ownership has more impact on firms affiliated with business group compared to standalone firms.

Overall, the results of this section indicate that institutional ownership has strong negative relationship with stock liquidity, which implies that the presence of institutional ownership imposes high adverse selection cost on market participants and as a result, stock liquidity reduces in the existence of institutional investors.

Relationship between Liquidity and Heterogeneity among Investors

This section examines the heterogeneity among institutional investors. Different institutional investors may have different informational advantage and incentives to trade. Therefore, we expect that the different institutional investors will have different impact on the stock liquidity. To examine this, we estimate the following regression equation:

Also, we include corporate ownership as well as retail investors to examine the impact of uninformed traders on the stock liquidity.

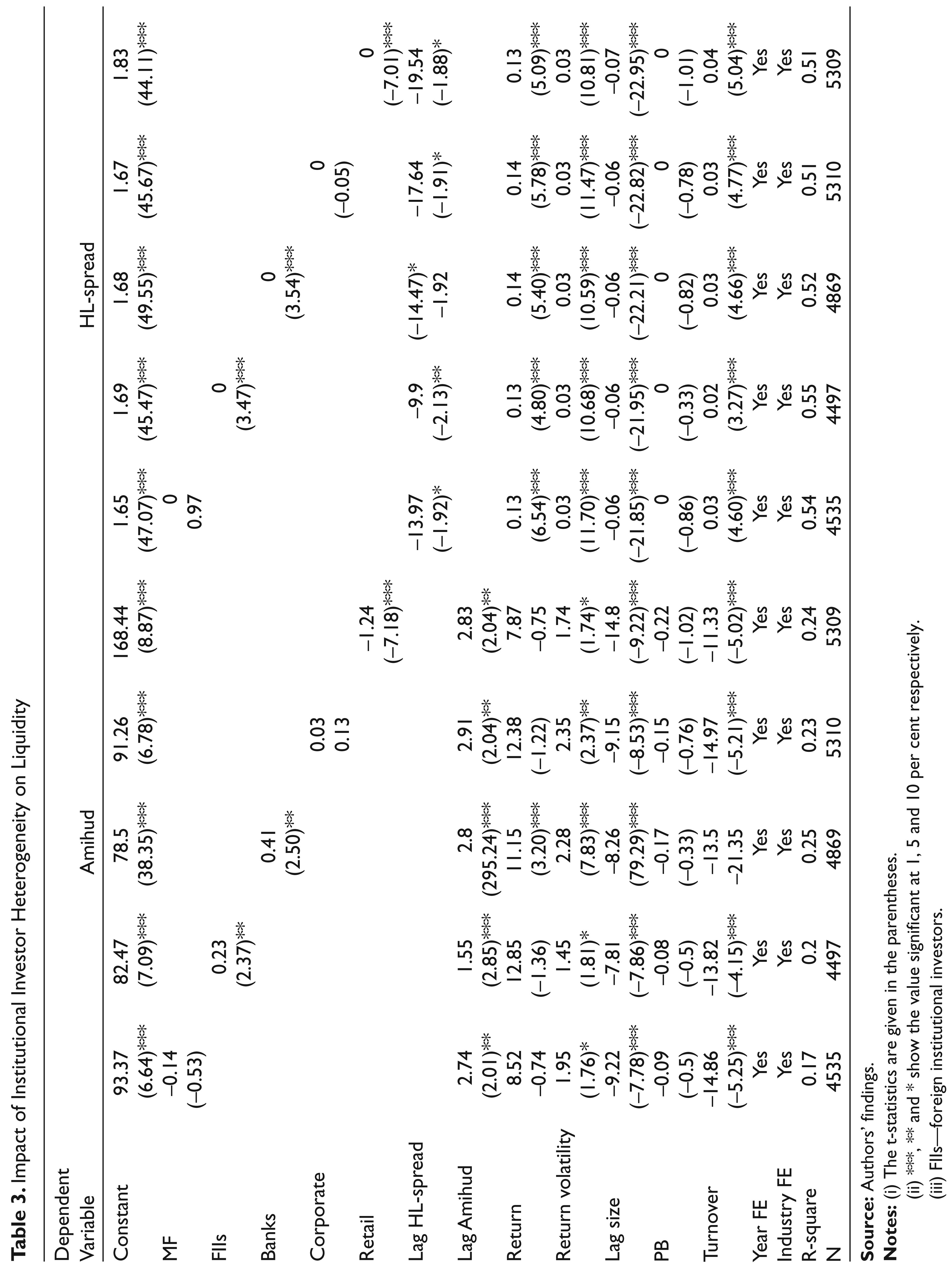

Table 3 reports the results of regressions which show the impact of all investor types independently along with other variables on both the measures of liquidity. In these regressions also, we consider year and industry fixed effects. The definitions of all other variables are same as given in Table 1.

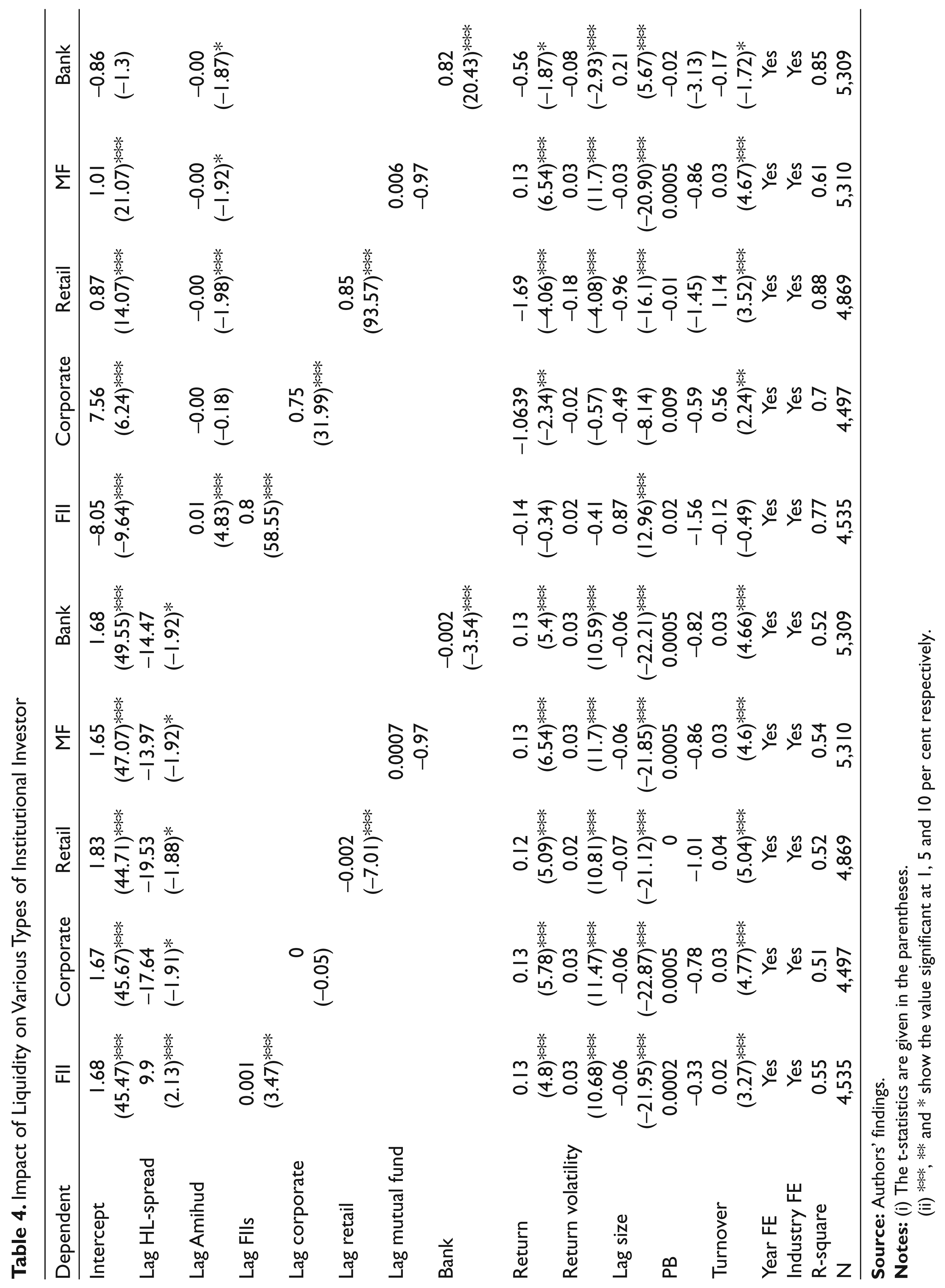

Table 4 shows the impact of liquidity on each type of investor. Lag liquidity and lag ownership for all the investor categories are also included as independent variables in the regression. Again, year and industry fixed effects are considered. The definitions of all other variables are same as given in Table 1 and Table 2.

Table 3 presents the regression results. Column (1) shows that mutual fund ownership is negatively related to HL-spread and Amiud illiquidity; however these coefficients are not statistically significant. This result is consistent with studies (Carhart, 1997) on the performance of mutual funds that show that mutual fund managers do not possess informational advantage. Columns (2) and (3) report that Bank ownership and foreign institutional investors (FIIs) ownership are negatively related to the stock liquidity, implying that Banks and FIIs enjoy informational advantage, and have adverse impact on the stock liquidity. We also report findings on corporate and retail ownership in columns (4) and (5). Consistent with previous studies, we find that retail investors improve the stock liquidity as most of the times they trade for liquidity needs. In summary, results in Table 3 indicate that institutional investors are not homogenous. They hold stocks for different reasons. Banks and FIIs ownership have negative impact on the stock liquidity.

Institutional Investors’ Preference for Liquid Stocks

Previous studies show that institutional investors more likely to hold liquid stocks since they more often trade in large quantities, and liquid stocks allow them to trade large quantities at less transaction costs. To address this concern, we examine whether the stock liquidity attracts institutional investors by using the following regression model.

Where, the dependent variable is institutional ownership for firm i and year t. Lag_Liqit is a lag variable of stock liquidity for firm i and year t.

Columns 1 and 4 of Table 4 show that the coefficient of HL-spread and Amihud illiquidity is negative, however, statistically significant for Amihud illiquidity at 1 per cent. These results suggest that to minimize transaction costs, institutional investors hold liquid stocks. These results are also consistent with previous studies such as Maug (1998) who found that stock liquidity encourages more ownership because it allows them to buy additional shares at lower impact cost. We also find that institutional investors prefer large cap stocks since they are efficiently priced.

Impact of Institutional Investor Heterogeneity on Liquidity

(ii) ***, ** and * show the value significant at 1, 5 and 10 per cent respectively.

(iii) FIIs—foreign institutional investors.

Impact of Liquidity on Various Types of Institutional Investor

(ii) ***, ** and * show the value significant at 1, 5 and 10 per cent respectively.

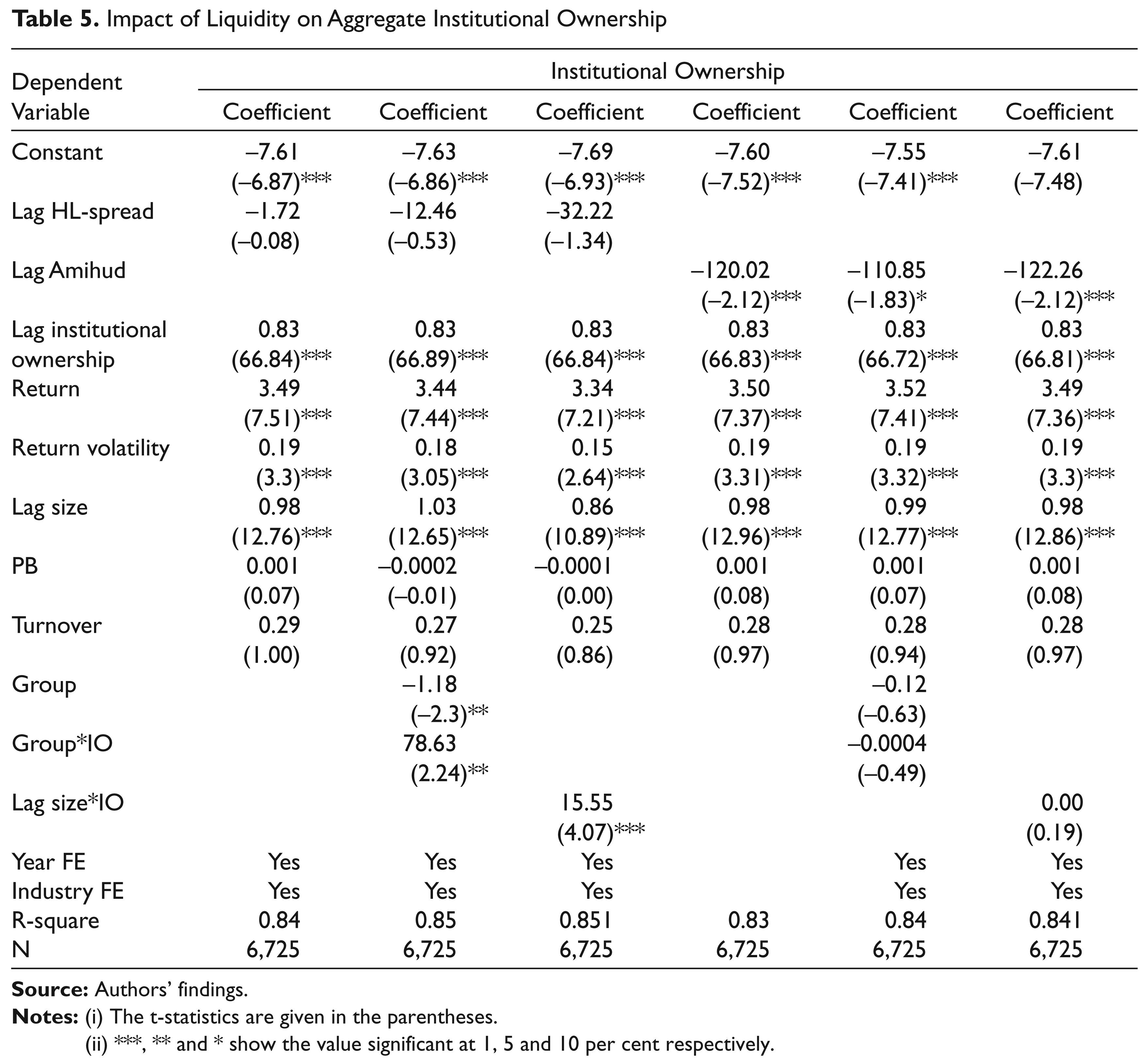

Impact of Liquidity on Aggregate Institutional Ownership

(ii) ***, ** and * show the value significant at 1, 5 and 10 per cent respectively.

In Table 5, the effect of liquidity measures along with other variables is analyzed on institutional ownership at aggregate level. Year and industry fixed effects are also considered. The definitions of all other variables are same as given in Tables 1 and 2.

Heterogeneity of Institutional Investors and Preference for Liquidity Stocks

In this section, we examine whether all type of investors demand for liquidity. Table 5 shows that irrespective of heterogeneity among investors, all investors demand for the stock liquidity. For instance, the coefficients for all investors and for each of illiquidity proxies are negative and statistically significant at appropriate level.

Robustness Tests

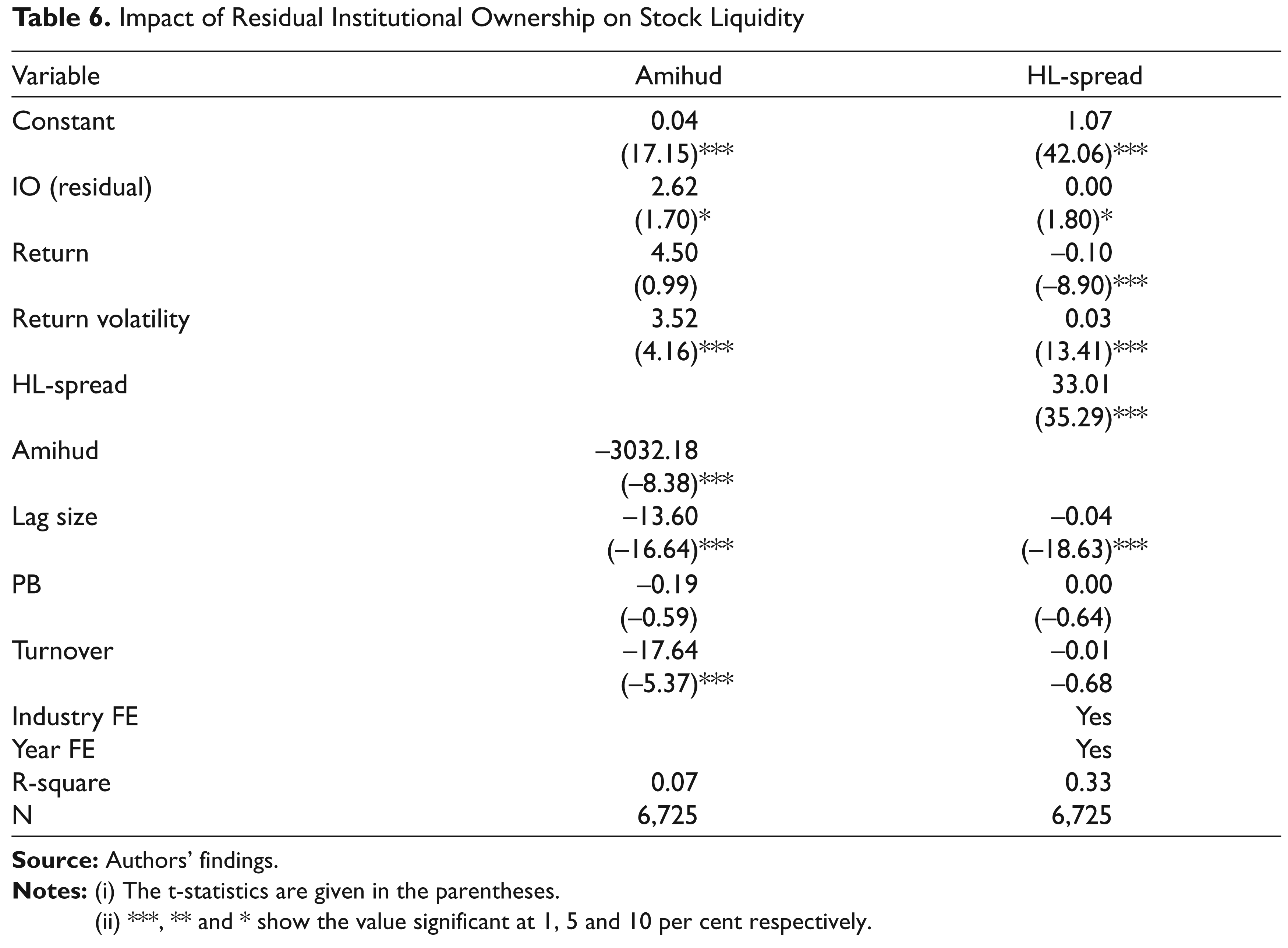

Previous section shows that institutional ownership imposes adverse selection cost and reduces stock liquidity. So far, we also assume that institutional ownership is an exogenous set. However, Yan and Zhang (2009) find that institutional investors show their preference for large stocks and stocks with higher book-to-market ratio. Therefore, our possible concern is that institutional investors may prefer stocks’ characteristics that are related to the stock liquidity. For example, mutual funds prefer mispriced stocks along with liquid stocks. To address this issue, we explore the possibility of simultaneous equations bias. Hence, we run the following two regressions:

In the first stage regressions (Eq. 4), we regress all exogenous variables on institutional ownership. Then, the residuals of first stage regressions are used in second stage regression (Eq. 5). This methodology allows us to remove the impact of stocks’ characteristics that may establish the relation between stock liquidity and institutional ownership, however, in the reality; there is no as such relation. The results of this analysis are reported in Table 6. Again our results confirm that institutional ownership increases HL-spread and Amihud illiquidity since we see that the coefficients of the residuals in this regression being less significant with a t-value of 1.70 for the Amihud measure and 1.80 for the HL-spread measure compared to the regressions in Tables 3 and 4.

Table 6 shows the impact of residuals of variable institutional ownership along with other variables on both the measures of liquidity. IO (Residual) are the residuals of first stage regression (results of which are shown in Table 2) are used in second stage regression. Industry and year fixed effects are also included. The definitions of other variables are given in Table 1.

Impact of Residual Institutional Ownership on Stock Liquidity

(ii) ***, ** and * show the value significant at 1, 5 and 10 per cent respectively.

Conclusion

In recent decades, the existence of institutions in public firms has grown rapidly and an increasing their trading activities in the stock market. In this article, we examine the role of institutional ownership in the cross-sectional stock liquidity on the emerging market, India. Particularly, we address the two hypotheses. First, the adverse selection hypothesis, the informative advantage of institutional investors imposes higher trading cost on uninformed traders, which leads to negative impact on stock liquidity. Second, the trading hypothesis, institutional investor frequently trade in large quantity, therefore, they prefer to hold liquid stocks to reduce trading cost. Moreover, we also argue that different types of institutions may have different impact on the stock liquidity.

Our empirical results demonstrate that firms with higher institutional ownership have lower stock liquidity as measured by wider HL-spread and Amihud illiquidity. Our results are consistent with the opinion (Kyle, 1985) that the intensity of informed traders discourages uninformed traders to enter the stock market, accordingly, reduces stock liquidity. We show that these results are sensitive to firm size and firms affiliated with business group; stock liquidity of two similar sized firms depends on the level of institutional ownership, and the impact of institutional ownership is more inferior on firms affiliated with business group compared to standalone firms. We also split institutional ownership into Bank, FIIs and mutual fund, and we also include corporate and retail ownership. Our empirical findings show that FIIs and Bank ownership have negative impact on stock liquidity. Conversely, retail investors facilitate to enhance stock liquidity. In second part, we find that stock liquidity facilitates institutions to increase their holding in the firm. An important implication of our findings is that if institutional ownership affects stock liquidity, then firms should not attract institutional ownership. However, institutional ownership not only entails adverse selection costs, but may also provide benefits by reducing agency problems (Morck et al., 1988). Therefore, firms should consider the advantage and disadvantage of institutional ownership before choosing most favourable ownership. Apart from this, other implication of this study is that for a liberalized developing economy like India, the participation of international institutional investors would reduce the information asymmetry and improve the stock market liquidity. However, our results could not establish this hypothesis due to various problems that exist in emerging economies. This study will help the regulators in devising measures to improve the market liquidity, and the investors to choose which companies to invest in to earn profits.

Footnotes

Acknowledgements

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.