Abstract

This article presents an analysis of the trends and patterns of foreign direct investment (FDI) in Mongolia, a former centrally planned economy which embarked on economic reforms in 1990. Since then, there has been a dramatic increase in FDI inflow into the country. The volume of FDI rose from less than one per cent of GDP in 1991 to 80 per cent by 2010. These foreign-owned enterprises have made a significant contribution to the country’s export earnings, but their effects on employment-creation and hence poverty-reduction remains very small. This appears to be largely due to a heavy concentration of foreign firms in relatively capital-intensive mining sectors rather than labour-intensive light manufacturing. Further, there is evidence to support growing business confidence that Mongolia has a potential of FDI to become a major player in global commodity markets with its rich gold, copper, zinc, uranium, coal, molybdenum and oil reserves.

Introduction

This article contributes to the literature on foreign direct investment (FDI) in transition economies using Mongolia as a case study. Mongolia embarked on a wide range of reforms following the disintegration of the former Soviet Union (FSU) in the late 1980s, enabling her to become a full member of the World Trade Organization (WTO) within seven years (in 1997). This was a remarkable achievement for a developing country with no experience in market institutions during its five decades of association with the then Soviet Union.

The aim of this article is to investigate the effects of policy shift on foreign investment in Mongolia which lacks technology, capital and know-how. The investigation of the Mongolian experience is particularly important given the studies examining the experience of small transition economies where market-oriented reforms are sparse. The available studies mainly focus on large economies of Central and Eastern Europe, which have limited relevance to small-transition economies such as Mongolia (for example, Bandelj, 2002; Bellak et al., 2009; Bevan and Estrin, 2000; Deichmann, 2001; Egger, 2000; Galego et al., 2004; Janicki and Wunnava, 2004; Kinoshita and Campos, 2002; Majocchi and Strange, 2007; Walkenhorst, 2004). 1 In this study, we aim to fill this gap by examining trends and patterns of foreign direct investment in Mongolia, which might provide useful insights to other developing and transition economies.

The article is organized as follows: the second section presents an analytical framework to place the Mongolian experience in context. The third section provides a brief profile of the economy and a summary of foreign investment policy regime. The fourth examines the trends and patterns of FDI in Mongolia, while the fifth section investigates the role of FDI in the Mongolian economy. The sixth section concludes the article.

Analytical Framework

As defined by UNCTAD (2008), FDI is an investment involving a long-term relationship and reflecting a lasting interest and control by a resident entity in one economy (foreign direct investor or parent enterprise) in an enterprise resident in an economy other than that of the foreign direct investor (FDI enterprise or affiliate enterprise or foreign affiliate). It is commonly argued that foreign firms bring capital and technology to least developed countries (LDCs) which these countries desperately need to foster growth. Therefore, FDI is expected to contribute to economic growth which is believed to improve living standards of the local population (Sharma and Bandara, 2010).

The location theory suggests that the multinational enterprise (MNE) would choose foreign markets in which it can maximize economic gains by integrating its firm-specific advantage with local endowments (Liu, 1997). Salvatore (2007) identified several reasons for the activities of MNEs abroad. These are: (a) to exploit some unique production knowledge or managerial skill (horizontal integration); (b) to gain control over a foreign source of a needed raw material or a foreign marketing outlet (vertical integration); (c) to avoid import tariffs and other trade restrictions and/or to take advantage of production subsidies; (d) to enter a foreign oligopolistic market; (e) to acquire a foreign firm to avoid future competition; or (f) the unique ability to obtain financing.

In an attempt to explain the determinants of FDI, Dunning (1993) developed a theoretical framework, which is widely known as ownership, location and internalization (OLI). According to this framework, the capability and willingness of one country’s enterprises to supply either to a foreign or domestic market from a foreign location depends on their possessing or being able to acquire certain assets (as outlined below), or such assets not been available at such favourable terms to another country’s enterprises. Such assets are referred to as ownership-specific (O) advantages because they are assumed to be unique to firms of a particular nationality of ownership. Such assets might be specific to a particular location (location-specific assets) in their origin and use, but available to all firms. These include not only Ricardian-type endowments, but also the cultural, legal, political and institutional environment in which they are deployed, market structure and government legislation and policies.

Dunning (1993) argues that the following location-specific factors are important for foreign investors when choosing the location of their business. These include: (a) spatial distribution of natural and created resource endowments and markets; (b) input prices, quality and productivity (for example, labour, energy, materials, components, semi-finished goods); (c) international transport and communication costs; (d) investment incentives and disincentives (including performance requirements, etc.); (e) artificial barriers (for example, import controls) to trade in goods and services; (f) societal and infrastructure provisions (commercial, legal, educational, transport and communication); (g) cross-country ideological, language, cultural, business and political differences; (h) economies of centralization of R&D production and marketing; and (i) the economic system and strategies of government—the institutional framework for resource allocation.

As the nature of FDI varies, the motives for international production and its determinants differ. The relative importance of different location-specific determinants depends on several aspects of investment, such as the motive for investment, the type of investment and the sector of investment. Dunning (1993) proposed location-specific determining factors for six types of international production: (a) natural resource-seeking; (b) market-seeking; (c) efficiency-seeking; (d) strategic asset-seeking; (e) trade and distribution (import and export merchanting); and (f) support services.

According to the proposition, possession of natural resources and related transport and infrastructure, tax and other incentives are locational advantages for natural resource-seeking investors, while material and labour costs, market size and characteristics, government policy (for example, with respect to regulations and import controls, investment incentives, etc.) are important for market-seeking investment. Countries with an advantage of low labour costs and efficient infrastructure can attract efficiency-seeking investment. For strategic asset-seeking investors, any of the advantages that are important for the first three types of investment mentioned above, that offer technology, markets and other assets in which the firm is deficient are attractive factors. For trade and distribution investors, factors such as source of inputs and local markets, proximity to customers and after-sales service are important, while availability of markets, particularly those of ‘lead’ client’s location advantages are determining factors of location for investors who engage in support services activities.

Dunning (2006) argues that among policy related factors that affect FDI decisions, policies relating to functioning and structure of markets (especially competition and merger and acquisition (M&A) policies), bilateral international agreements on FDI, privatization and price reform policies and industrial/regional policies have become more important during the last decade in addition to traditional policy factors. He also argues that among the factors related to business facilitation, investment incentives and promotion schemes, form and quality of the legal property system, protection of intellectual property rights, good institutional infrastructure and support (for example, banking, legal, accountancy, services), social capital, region-based cluster and network enhancement and legislation/policies designed to reduce corruption and corporate malfeasance have become important determinants of location besides traditional factors under globalization.

Profile of the Mongolian Economy and Foreign Investment Policy Regime

A Brief Profile of the Economy

Mongolia is a landlocked country located between the Russian Federation (in the north) and the Republic of China (in the east, south and west). It has a population of 2.7 million and an area of 1.5 million square kilometres. Its economy is traditionally based on livestock breeding and the country is rich in natural resources, including many mineral resources. The livestock sector employs about 34 per cent of the total workforce as of 2010, while mining, due to its capital intensity, absorbs only 3 per cent of the workforce. The services sector employs 40 per cent of the workforce, while the contribution of trade and commerce to employment creation is 14 per cent (Davaakhuu, 2013). Mongolia’s exports are dominated by minerals and metals representing 81 per cent of total exports, while its imports are mainly machinery and fuel contributing more than 60 per cent to total imports in 2010.

Mongolia was under a state planning economic system from late 1940 to 1989. During this period production and investment decisions were regulated by the government and there was no role for the private sector. Further, the economy was highly integrated with the former Soviet Union (FSU) and the other planned economies of the Council for Mutual Economic Assistance (CMEA), and the economy was closed for foreign investment.

Foreign Investment Policy Regime

With the collapse of the socialist system in the late 1980s, Mongolia faced a severe macroeconomic crisis. For instance, unemployment rose, the budget deficit surged and inflation reached over 100 per cent, forcing the government to open up its economy in 1990, leading to liberalization of state-controlled prices and tariffs, privatization of state-owned properties, liberalization of the trade and investment regime, establishment of a two-tier banking system, adoption of a floating exchange rate and creation of a favourable legal environment for private sector development. To further encourage foreign investment, Mongolia introduced the Foreign Investment Law (FIL) in 1993. In line with the commitment to WTO membership, gained in 1997, Mongolia consistently updated the foreign investment policy. 2

Under the Mongolian investment legislation, foreign companies are subject to the same legal framework as domestic firms for matters of incorporation and other corporate activities. Neither foreign nor domestic firms face restrictions on obtaining foreign exchange and making transfers of investment funds, profits and payments. No restriction is imposed on the size and content of investment and all foreign investors are required to register with the Foreign Investment and Foreign Trade Agency (FIFTA). The FIL requires all foreign investors to show assets registered in Mongolia as a precondition for registration. The minimum requirement for the assets was raised from US$10,000 in 2007 to US$100,000 by 2008 primarily to protect small domestic investment. Foreign investors in the country enjoy rights with regards to their property, operation and profits. These include: (a) to possess, use, and dispose of their property including the repatriation of investments which contributed to the equity of a business entity with foreign investment; (b) to manage or to participate in managing a business entity with foreign investment; (c) to transfer their rights and obligations to other persons in accordance with the law; and (d) to remit income, profit gained under the legislation of Mongolia and payments abroad without any barriers. Furthermore, as a legal guarantee for a stable environment to conduct business activities, the government signs a stability agreement with large foreign investors intending to undertake an investment project of not less than US$20 million in the event of a request by the investor. The agreement consists of freezing the existing tax rules and regulations, and maintaining certain favourable tax exemptions for them for a specified period of time.

Foreign investment in Mongolia is guaranteed legal protection under its laws and international treaties signed by the country. According to its legislation it is prohibited to nationalize and illegally confiscate assets and capital of foreign investors (FIFTA, 2009). The country joined the ‘Washington Convention on the Settlement of Investment Disputes between the State and Nationals of Another State’ (1965) in 1996 and the ‘Seoul Convention on Investment Insurance’ (1985) in 1999. Moreover, the nation became a full member of the Multilateral Investment Guarantee Agency of the World Bank Group in 1999. It has also negotiated an ‘Agreement on Mutual Promotion and Protection of Investment’ with 19 countries and an ‘Agreement on Exemption from Double Taxation’ with 26 nations. Mongolia is among the leading countries in terms of protecting investors, ranking at 25 (World Bank, 2013).

Under the FIL and Tax Law, foreign investors in infrastructure and mining sectors, and those exporting more than 50 per cent of their total production enjoy income tax exemptions. Until 2006, Mongolia also granted exemption from customs duties and value-added tax (VAT) for all businesses and entities engaged in the selected activities in priority sectors including agriculture, exploration of mineral resources (coal, oil, gas, uranium and thorium ore and iron ore), some branches of processing industry (food production, knitting industry, fur processing, leather processing, timber production, liquid and radioactive fuel, production of chemical products, goods made of non-metal minerals, metallurgic industry and processing of a secondary raw material), infrastructure (production of electricity and steam, and water supply and water treatment) and the construction industry. While amendments to the Tax Law in 2006 phased out these tax incentives and exemptions, it brought other favourable conditions including provision for loss-carry-forwards, five-year accelerated depreciation and more deductions for legitimate business expenses. To attract foreign investment in its priority sector, Mongolia granted a 10 per cent investment tax credit (since 1 January 2007) for depreciable non-current assets. 3

Foreign investors are not required to use local goods and services, local equity, purchase from local sources or export a certain percentage of output. Furthermore, there is no requirement for foreign investors to transfer technology or sell their shares to Mongolian nationals. Its Labour Law requires foreign investors to employ Mongolian workers if such skills are available locally. This law only applies to unskilled labour categories and not to the areas where a high degree of technical expertise is required, but not available in Mongolia. Since 2002, the government has been working towards establishing free trade and economic zones to encourage foreign investment in export-oriented activities.

Mongolia’s commitment to a market-oriented economy is also reflected by a significant improvement in its international ranking in attracting FDI over time. According to UNCTAD (2011), its ranking of FDI Performance Index improved from 76 out of 140 economies in 1991 to 3 by 2010. Its position improved further after gaining the accession to the WTO (World Bank, 2009).

The policy reforms package outlined above resulted in an impressive economic growth performance in Mongolia. 4 However, the country still faces many issues and challenges. Most of these issues and challenges can be elucidated by reviewing the Trends and patterns of the FDI inflow into the country.

Trends and Patterns of FDI in Mongolia

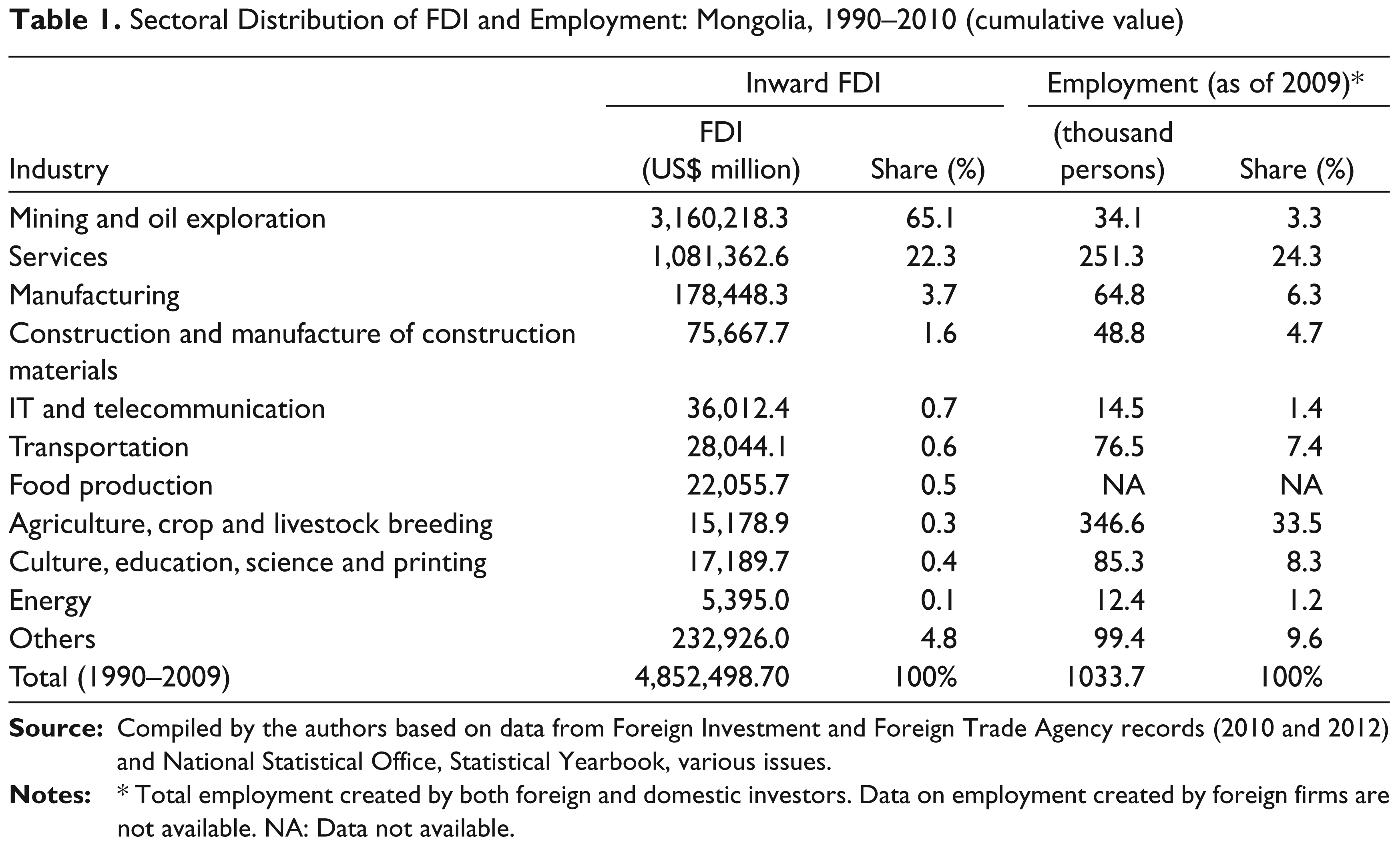

Mongolia experienced a phenomenal growth in FDI which increased from US$ 1 million (less than 1 per cent of GDP) in 1990 to US$ 1 billion (81 per cent of GDP) by 2010, due to the favourable investment climate created by the initial policy reforms in 1990, and the enactment of the FIL in 1993, and subsequent entry to the WTO in 1997. The sectroral distribution of FDI reveals a large proportion of foreign direct investment (65 per cent) has gone to mining and oil exploration, of which mining has an intrinsic comparative advantage (Table 1). This is followed by services (22.3 per cent), and light manufacturing (3.7 per cent) which mainly includes textile, beverage and food processing. With the privatization of state enterprises following market-oriented reforms, previously state-owned enterprises have also attracted significant amount of FDI.

Sectoral Distribution of FDI and Employment: Mongolia, 1990–2010 (cumulative value)

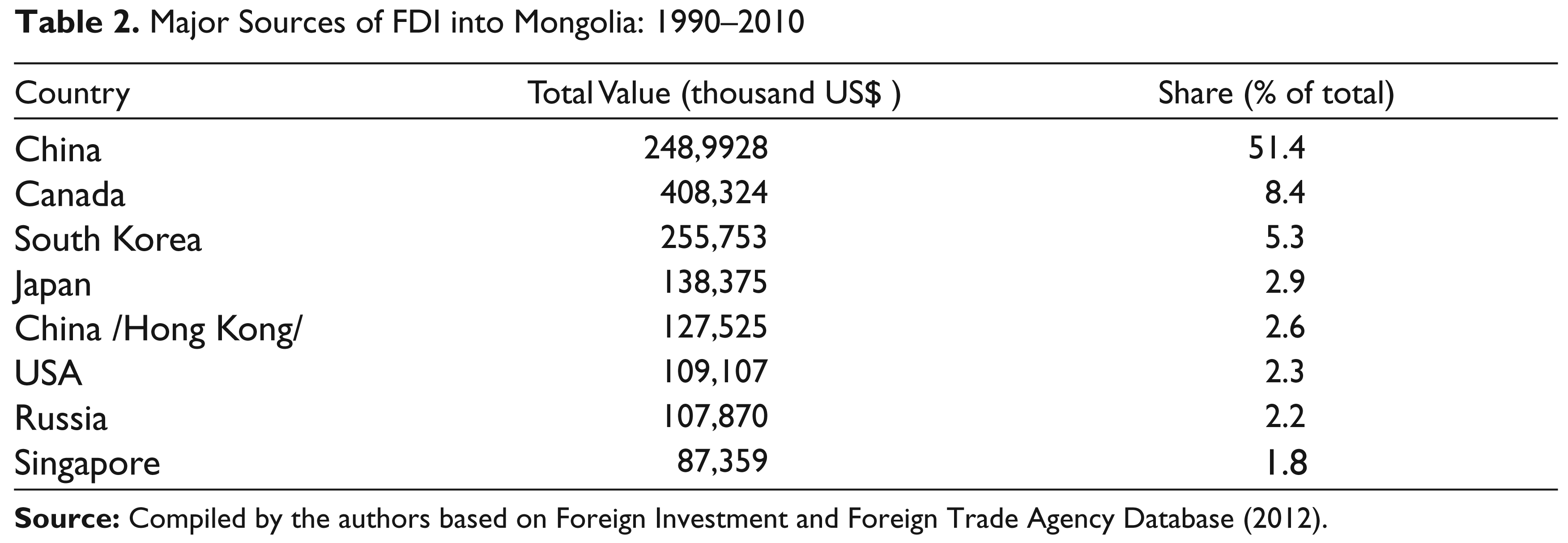

Mongolia’s geographic location being closer to resource hungry China has led to significant amount of Chinese investment flowing in to Mongolia, particularly in to the mining sector. Over 50 per cent of total foreign investment directed to Mongolia during the period from 1990 to 2010 was from China (see Table 2). The second largest source of foreign investment to Mongolia is Canada, which accounts for around an 8 per cent share, investing more than US$ 400 million in total mainly in mining. South Korea is the third largest source of FDI (5 per cent share) mainly engaged in telecommunication, services and manufacturing. Japan and Hong Kong each accounts for about 3 per cent of total investment inflow to Mongolia. Japanese investment is largely directed at telecommunication and banking sectors, although in recent years they have also shown interests in relatively larger projects in cashmere apparel manufacturing.

Despite significant influence in the past, foreign investment from Russia remains relatively small (2.2 per cent) in Mongolia. Russian firms are mainly engaged in geology and mining, construction, banking and financial services and the processed food industry. Foreign investment from the US (2.3 per cent) is largely concentrated in geology—mining and oil, while investment from other countries (Singapore and Hong Kong) remains very small. In general, Mongolia has failed to attract FDI from major industrialized economies.

Major Sources of FDI into Mongolia: 1990–2010

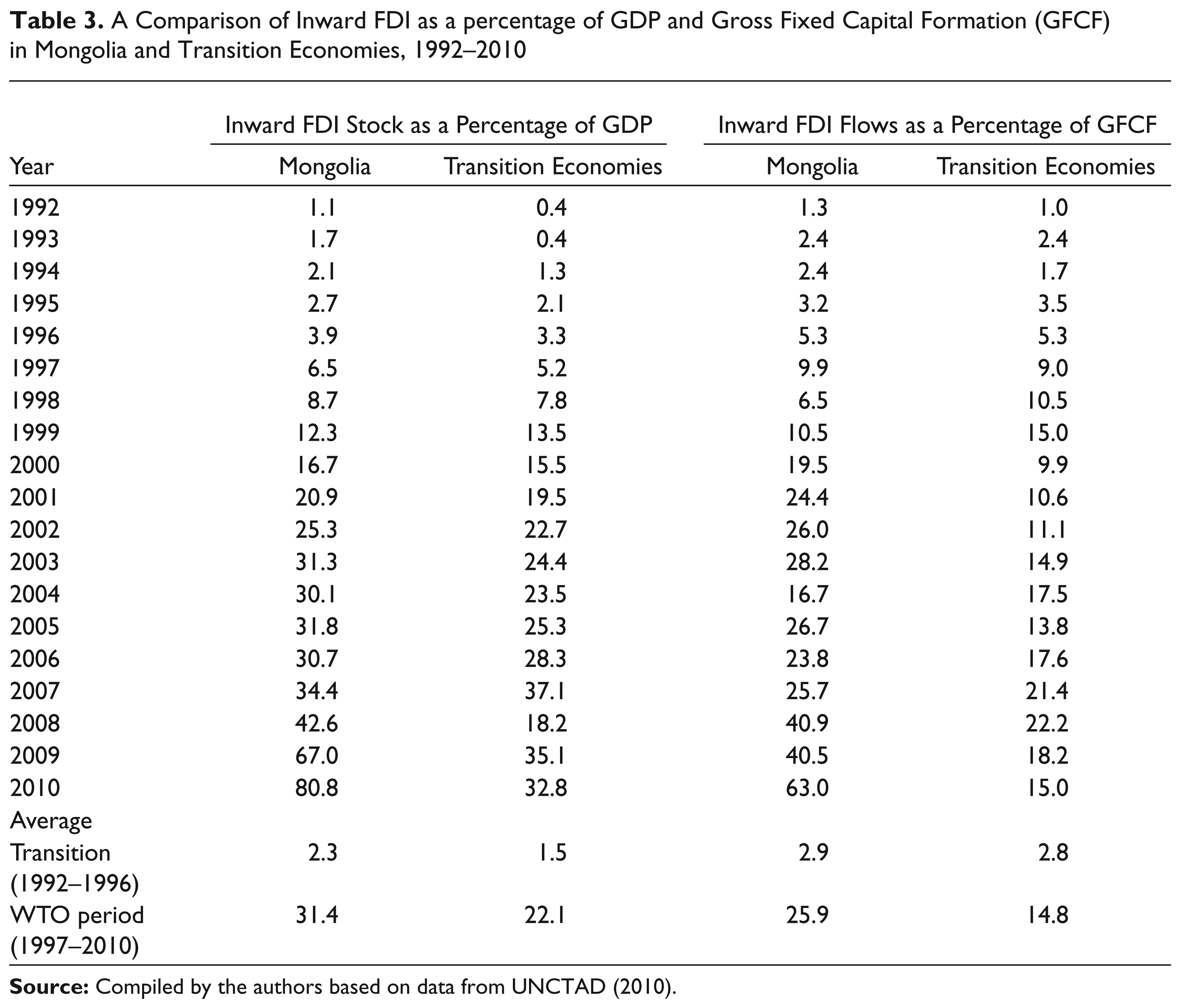

A Comparison of Inward FDI as a percentage of GDP and Gross Fixed Capital Formation (GFCF) in Mongolia and Transition Economies, 1992–2010

Another noteworthy trend observed in the case of Mongolia’s FDI inflow is that its remarkable performance compared to the other transition economies (TEs).As can be seen in Table 3, Mongolia and other TEs had a similar ‘inward FDI stock to GDP ratio’ (of around 12–13 per cent) by the turn of the century. 5 However, this ratio increased remarkably to about 81 per cent in Mongolia while, it reached only up to about mid 30 per cent in the case of other TEs by the year 2010. This trend, if identified under post and pre reform era, contribution of FDI in the Mongolian economy has averaged about 30 per cent during the WTO period (1997–2010) rising significantly from about 2 per cent during the transition period (1992–1996). This is much higher than the share of FDI in GDP in many TEs that averaged 1.5 per cent in the early 1990s and 22 per cent since the late 1990s.

It is interesting to note that the contribution of FDI in Mongolia’s GFCF is also higher compared to that of TEs. One-quarter of the country’s GFCF has been financed by FDI during the WTO period, while its share in transition economies is about 15 per cent (Table 3). The contribution of foreign capital in Mongolia’s GFCF has risen to more than 60 per cent by 2010, while it accounted for 15 per cent in TEs. This significant rise has been mainly due to large inflow of foreign investment into mining.

Another interesting observation is that foreign investment is becoming one of the significant sources of tax revenue in Mongolia. According to an estimate, based on data from the records by the General Taxation Administration and the Foreign Investment and Foreign Trade Agency (FIFTA), it contributed more than 50 per cent to the state revenue in 2010, which is a significant increase from less than 1 per cent in 2001.

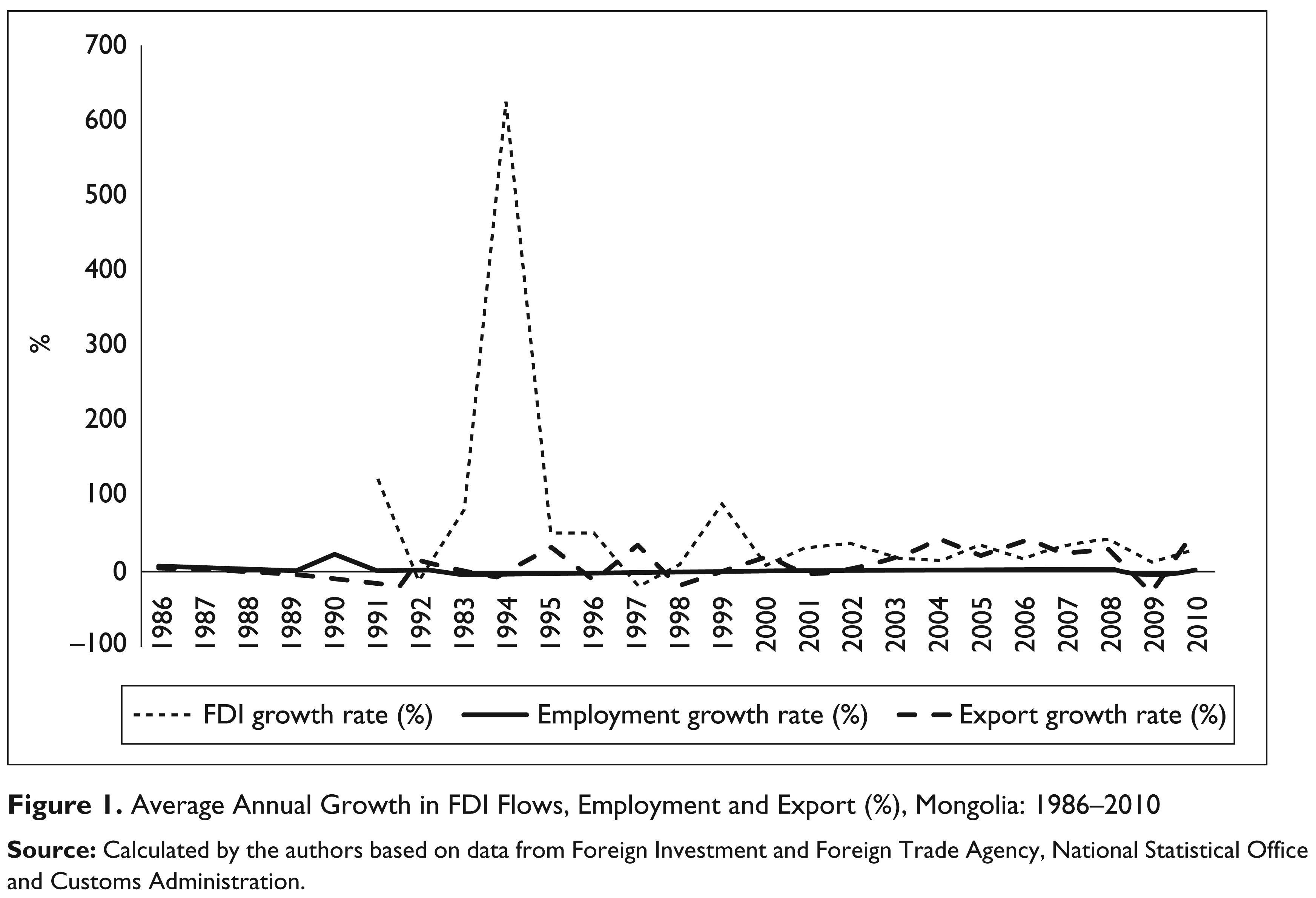

It should also be highlighted that foreign firms have made a significant contribution to the country’s export expansion, primarily in the mining sector. As can be seen in Figure 1, exports grew at an average of 20 per cent between 2001 and 2007, corresponding to the growth of foreign investment, which averaged 25 per cent, although there have been significant annual fluctuations.

While there has been a significant rise in foreign investment and exports, growth in employment, which was a key objective of policy reforms, has been virtually nil as can be seen in Figure 1. This is a significant policy concern which warrants further analysis.

Role of FDI in the Mongolian Economy

The initial policy reforms brought the Mongolian economy back on track by 1994. GDP grew from a negative 9 per cent in 1992 to a positive 2 per cent by 1994, largely due to a recovery in the agriculture, mining, trade and transport sectors. FDI surged, while inflation dropped to about 70 per cent and the government budget deficit declined to about 4 per cent of GDP. The mining sector recovered after 1992 mainly as a result of the Gold Programme (which aimed to expand mining activities) adopted by the government in 1991. The share of mining and quarrying in GDP has risen from 13 per cent during 1985–1989 to 24 per cent by 2006–2010. The manufacturing sector has been in infancy and its share in GDP has been about 6 per cent during the 2006–2008 period, while trade and services sectors have rapidly expanded.

However, the country still faces many issues and challenges. These include: the need to increase employment opportunities, primarily in the rural areas, and to improve the living standards of its population and to achieve equitable development. According to the National Statistical Office (2011), poverty has risen from about 36 per cent in 1998 to about 39 per cent by 2010. Poverty in the rural population increased from 33 per cent in 1998 to about 47 per cent by 2010, largely due to the collapse of state-owned livestock farms, the loss of livestock under severe winters and the failure to attract investment in labour-intensive manufacturing activities, while poverty in urban areas fell from 39 per cent to 32 per cent over the same period and this polarization is increasing. The poverty rate in Ulaanbaatar, the country’s capital city and economic centre, is below the national average. The number of poor in the capital city declined from 34 per cent in 1998 to about 30 per cent in 2010. This appears to be due to concentration of services and manufacturing activities in urban centres.

Further, there are two main reasons that can explain why the expected employment growth was not achieved. They are: (a) significant disparity in the distribution of FDI within the industry sector with a heavy concentration in mining; and (b) huge geographic disparity (urban vs rural) in the FDI distribution.

With regard to the disparity in the FDI within the industry sector, the mining industry has attracted 60 per cent of total FDI, but this sector has contributed only 3.3 per cent towards total employment. The nature of mining has been capital-intensive, which obviously has been the reason for low contribution to employment.

The labour-intensive manufacturing sector attracted a relatively small amount of FDI (around 5 per cent of total FDI) mainly in the textiles and apparel sub-sectors. Growth in employment in manufacturing has been a meagre 0.1 per cent during the 1992–2000 period while it has been 4 per cent per annum during the 2001–2006 period, mainly due to the participation of foreign firms in the labour-intensive apparel industry. However, this growth slowed down again to 1 per cent since 2007 due to the departure of foreign investors in the textile sector after the cessation of Multi-Fibre Agreement. According to UNIDO databases, among manufacturing sub sectors, the apparel industry is the largest contributor to employment (about 7000 people) in 2008, followed by non-metallic-mineral products (3900), the textiles industry (3300), beverages (3300), processed meat (2300), printing (1300) and leather processing (600). 6 As these manufacturing sub-sectors have foreign participation, one can argue that foreign investment is contributing to employment creation in the manufacturing industry. However, the reality is that the magnitude of employment creation in the labour-intensive manufacturing sector is low and it has not helped to uplift the rural populace above poverty as these manufacturing firms located their operations in urban areas.

The services sector, on the other hand made a significant 24.3 per cent contribution to total employment, even with comparatively lower portion (22.3 per cent) of total FDI being diverted into the sector. The other noteworthy sector is agriculture, crop and livestock breeding, which contributed 33.5 per cent to total employment has received a meagre 0.3 per cent of total FDI inflow.

The second main factor that seem to have lead to very low employment generation is the vast geographic (urban vs rural) disparity in the distribution of FDI. Like in many less developed countries, FDI in Mongolia is largely concentrated in the urban areas, especially in and around the capital city. Out of total FDI inflow, over 90 per cent was attracted by the capital city Ulaanbaatar (Ulaanbaatar Region). This appears to be mainly due to a large domestic market in urban centres and the heavy concentration of the population in urban areas. 7 The other four regions have received very small amount of FDI. For example, the Central Region (which consists of five provinces including Darkhan City, one of the country’s industrial centres, and the Gobi area, which is rich in mineral resources), inhabited by about 20 per cent of the population, received about 3 per cent of the total FDI, mainly in to the mining and services sectors. The Khangai Region has received more than 1 per cent of foreign investment, most of which was in to mining, mineral enrichment and services. This region is home to the country’s largest copper mining and enrichment plant. Further, Lake Khuvsgul which attracts a significant number of tourists has attracted some tourism investment into this region. The other two regions, namely, the Western and Eastern Regions (which are far from the major cities) each have attracted less than 1 per cent of total FDI in geological exploration, oil extraction, agriculture, services (in the Eastern Region), processed food production, trade and light industry (in the Western Region).

It must be noted that despite more than a decade of market-oriented reforms, physical infrastructure in rural areas remains far from satisfactory, discouraging foreign firms from moving their business to rural areas. 8 In the absence of well-developed physical infrastructure, regional centres have failed to attract manufacturing investment. The implication of this is that foreign investment has failed to provide benefits to the rural population, leading to a rise in migration to urban centres, leaving behind rural poverty.

In summary, Mongolia was very successful in attracting much needed FID in the post-reform era. She attracted a significant amount of foreign investment, transferring its economy from an agrarian-based to an export-oriented one. The outstanding feature in FDI distribution in the country is that capital-intensive mining has absorbed about 60 per cent of the total FDI, while labour-intensive manufacturing failed to receive its due share. Further, foreign invested enterprises concentrated in urban areas, while remote and rural areas became unattractive for FDI. This phenomenon led to the failure of creating employment opportunities for the rural populace and lifting them from poverty. Therefore, it is widely believed that foreign firms have made little contribution to employment-creation and poverty-reduction strategies implemented under the Millennium Development Goals (MDGs).

In terms of export earnings, foreign-owned enterprises have made a significant contribution of 80 per cent towards total export earnings in Mongolia, but their contribution to employment remains very small (less than 5 per cent). Most of these exports are generated from resource-based activities, primarily capital-intensive mining.

Despite the lower-than-expected achievements in generating employment opportunities and lifting rural population up from existing poverty levels, Mongolia still has the opportunity to introduce further reforms and make use of untapped resources to provide benefits to the average population. The developing business confidence suggests that Mongolia has a potential in FDI to become a major player in global commodity markets with its rich gold, copper, zinc, uranium, coal, molybdenum and oil reserves (Leo Liu, 2013).

Conclusion

This article contributes to the literature on FDI in TEs using Mongolia as a case study. In particular it analyzed the trends and patterns of FDI inflow in to the country since the introduction of policy reforms in 1990, following the disintegration of the former Soviet Union. The policy reforms paved the way for an influx of FDI into the country, which has been a remarkable achievement in comparison to many other smaller transition economies. Export earnings recorded an impressive growth, while foreign-owned enterprises contributed 80 per cent towards total export earnings.

However, the phenomenal growth in FDI, and the policy reforms that facilitated the FDI inflow have failed to achieve employment creation and poverty reduction targets set out under the MDGs as the foreign firms have made little contribution to employment-creation and poverty-reduction in the rural sector. The main factors that contributed to this lower-than-expected performance are: the high concentration of FDI in the capital intensive mining sector at the expense of the labour-intensive manufacturing sector, which received a low share of total FDI inflow, and the heavy concentration of foreign-invested entreprises in urban areas, with no adequate foreign investment flowing to remote and rural areas. Given the business confidence that Mongolia has the potential to become a major player in the global commodity markets with her rich minerals such as gold, copper, zinc, uranium, coal and oil reserves, it is to her best advantage that economic policies are further reformed while uplifting the physical infrastructure in regional areas to attract investment.