Abstract

The ideal board remuneration issue has always been a challenge in many countries. The reason for looking at ideal board remuneration is that the ideal remuneration should have an impact on the board performance and, in turn, lead to board effectiveness. However, the development of ideal board remuneration in Indonesian state-owned enterprises (SOE) has been based on relatively little research. Considering the relative importance attached by boards to a variety of governance tasks in SOEs, the primary aim of this article is to shed light on the extent of board remuneration impact performance of the board in implementing good corporate governance in Indonesian SOEs. The exploratory nature of this study led to the adoption of a qualitative research methodology that uses semi-structured interviews and publically available documents to collect a range of data pertaining board remuneration and the work of boards. Interviews were conducted with six informants from four Indonesian SOEs and Ministry of SOEs. The findings of this research demonstrate that the current Indonesian SOEs’ board remuneration system is not adequate as well as has a negative impact on the performance of the board. This was due to demotivation of active members and conflict of interest among members of the board, peculiarities to the performance of individual members of the board of commissioners. This study makes a significant contribution to both the board and the corporate governance field by addressing the basic research gaps of board remuneration issues in SOEs. The gap is addressed by providing a more coherent framework for effective board remuneration system that reflects more clearly the real experiences of those involved at the board level.

Keywords

Introduction

In the light of the alarming number of governance scandals hitting the corporate world, such as Enron, World.com and Waste Management (Cadbury, 1999; Clarke, 2004), it is important to understand what can drive the boards leading the firms to adhere to high ethical standards and strive for stretch targets. The board as governing body is responsible for setting the enterprise’s direction, formulating strategy, policymaking, supervising management and being accountable (Tricker, 2015). Generally, the governing body is the body that is responsible for the enterprise’s decisions and its performance (OECD, 2004). When the shareholders entrust their funds to the company, legally, the governing body is required to make decisions not only to conserve their fund but also to increase them (Leblanc & Gillies, 2005). A review of a number of articles yields some of the titles used by the governing bodies, such as the board of directors (BoD), the supervisory boards, the boards of commissioners (BoCs), the board of governors and just governing body (Tricker, 2015). This study will refer to the governing body as ‘the boards’ and ‘the BoCs’ (to explain the boards in Indonesia).

However, the problems of passive boards in the work of boards have prompted public concern over the governance (Baxi, 2005). These facts ushered in a new era of pressure for change (Leblanc & Gillies, 2005). Some studies, such as Kakabadse (2010), Tricker (2015) and Garratt (2015), found that board remuneration has an important role to play among other factors. It is because remuneration is essential factors to get world class members to accept the position on state-owned enterprises (SOEs) boards (Tricker, 2015). Thus, the SOEs’ board remuneration issues have been in the spotlight across the globe in recent time.

The ideal board’s remuneration is contentious in many countries. There are two issues that are usually discussed in relation to ideal remuneration (Tricker, 2015). First, the board members consider whether the remuneration levels are adequate. Second, the board members consider whether the level of remuneration has an impact on board members’ commitment and dedication to their role. According to some scholar, a reward system without considering the individual performance may trigger contentious discussion among members of the boards and the stakeholders. The remuneration needs to be sufficient to attract the necessary members to the board and the management, to provide the incentive for improved average performance, to reward success and to retain the members’ commitment to the SOEs (National Committee of Corporate Governance [NCCG], 2006).

However, the question of how remuneration should be determined in order to balance the interests of the board members with the shareholders has always been a challenge (Kakabadse, 2010). In the past, the board and management body’s remuneration was always determined by the majority of shareholders, and it has been often contentious. Many criticisms arose on the grounds that such remuneration was often out of line with the market and unrelated to performance (Tricker, 2015). An OECD (2005) survey showed that at that time, the majority of OECD countries did not offer an attractive remuneration package commensurate with the responsibilities of the members of SOE boards.

Furthermore, although many scholars have discussed the link between board remuneration and performance but given their empirical studies, there are divergent opinions regarding ideal board’s remuneration and whether or not board’s remuneration has a big influence on the effectiveness of boards. Tricker (2015) also argues that although there was a surge in academic interest in linking the board remuneration and corporate governance from the 1990s, the research has so far failed to offer a convincing explanation of ideal’s board remuneration. Those researches have contributed little to the practice of the subject. Thus, it may be necessary to have a further investigation on the impact of remuneration on the works of the board in SOEs.

The article is organized as follows: the next section discusses the board in Indonesian SOE. This is followed by a literature review overboard remuneration. The objectives of the study and rationale of the study are discussed in the third and fourth sections. The fifth section explains the methodology used in the study. The impact of board remuneration to the work of BoC is analyzed in sixth section and summarized in an integrated framework. Finally, the conclusion is drawn in the last section.

The Board Structure in Indonesian SOEs

The SOEs are important for Indonesia’s economy as the SOEs own important resources. The SOEs not just make direct contributions from their products and services to the state budget, but also make indirect contributions from the realization of the social functions for the country’s prosperity (Djajanto, 2007). From 132 SOEs (November 2012), the SOEs total assets amount to around US$150 billion (McLeod, 2008) and SOEs hold 40.23 per cent of the total market capitalization on the Indonesian Stock Exchange (equal to 493.26 trillion Rupiahs).

Along with Indonesia political and economic reforms, the governance reformation in Indonesian SOEs began in 1998, and from 2002, the SOEs have implemented the code of good corporate governance (GCG) as their best practice. However, the performance of Indonesian SOEs is still very disappointing, and fraud cases are still occurring. According a report from Indonesian Corruption Watch (Kompas, 2011) from the 132 SOEs, there were 17 SOEs had recorded lossess and had problems. It is because these SOEs do not have commercial value or high potential for political intervention on their activities or the decision-making of the board (Irene, 2010). Moreover, the Indonesian Corruption Watch (ICW) still found indications of corruption in substantive amounts at some of Indonesian SOEs in 2010–2011 (Irawan, 2012). Other cases were found at P. T. Jamsostek (Daryanto, 2005), WaskitaKarya (Wika; Sugiyarto, 2008) and P. T. AdhiKarya (Rastika, 2013) and all their former directors are now being arrested for allegations of corruption.

Most of these fraud cases happened as a result of weak controls by the BoCs over the management board or BoDs (Habir, 2005). Business executives, scholars and the government think that the existence of the BoCs is primarily driven by legislation rather than by a real understanding of the work of the BoCs (Kamal, 2008). Interestingly, this kind of understanding is similar to the understanding of other countries that hold conventional views about boards (Tan & Wang, 2007). Moreover, the governance structure may also impact the behaviour of the board and relationships between board and management as an agent (Sinha, 2006). While governance structure of Indonesian SOEs is relatively specific, when compared to other Western countries. The governance structure in Indonesian SOEs uses a two-tier model, but with a different path (Kamal, 2008). This kind of model is applied to all types of companies including SOEs.

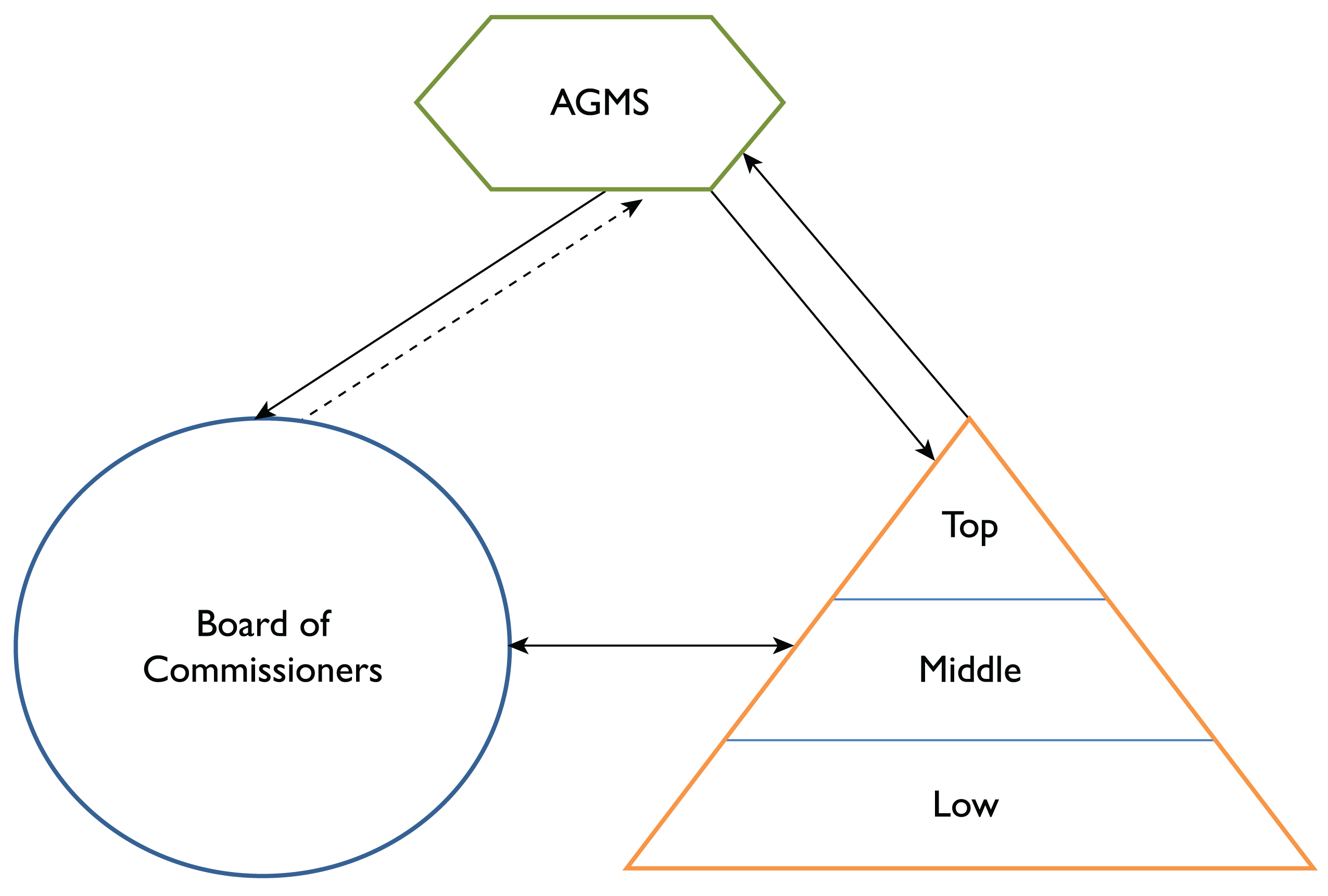

In Indonesia, the governance structure of each SOE makes a tripod that consists of (a) the annual general meetings of shareholders (AGMS), (b) the BoC as the supervisory board and (c) The BoD as the management (Syakhroza, 2005). The shareholders are a group of people who invest their money as capital and have a share of the company’s profits. The BoD is responsible for the company’s operational management while the BoC is the group of people who supervise and give advice to the BoD (NCCG, 2006). The separation between the BoD and the BoC in the Indonesian governance structure is consistent with the idea of a two-tier model, as all members of the BoC are non-executive directors. However, unlike the two-tier model, where the board is structured between the shareholders and the management. The structure of the BoC in Indonesia is ‘side by side’ (parallel) to the BoD (Figure 1).

The study by Sari (2013) finds that the structure of the BoC in Indonesia which ‘side by side’ (parallel) to the BoD provides further confirmation that the BoC is not meant to have a dominant role in governing the SOE. As a result, until now, stakeholders have not recognized the importance of the work of the BoC in the operation of the SOEs (Tjager, Alijoyo, Djemat, & Soembodo, 2003). Within this structure, the selection mechanism, power, functions and working relationships of the BoC are different from the two-tier model including their remuneration process.

Review of Literature

Remuneration is one of the key factors in getting world class members to accept the position on SOE boards (Tricker, 2015). Remuneration is traditionally seen as the total income of an individual and may comprise a range of separate payments determined according to different rules. A remuneration strategy, therefore, is the particular configuration or bundling of payments that go to make up an individual (World Health Organization [WHO], 2000). Thus, a company’s remuneration strategy may consider (Kaplan Financial, 2002)

offering more benefits in kind to compensate for lower basic salary. non-cash motivators for all or some of the company employees, for example, childcare vouchers, company car scheme or additional holiday. availability of company resources, for example, there may be insufficient cash available to pay an annual bonus, but share options might be an alternative. encouraging a long-term loyalty through share purchase schemes.

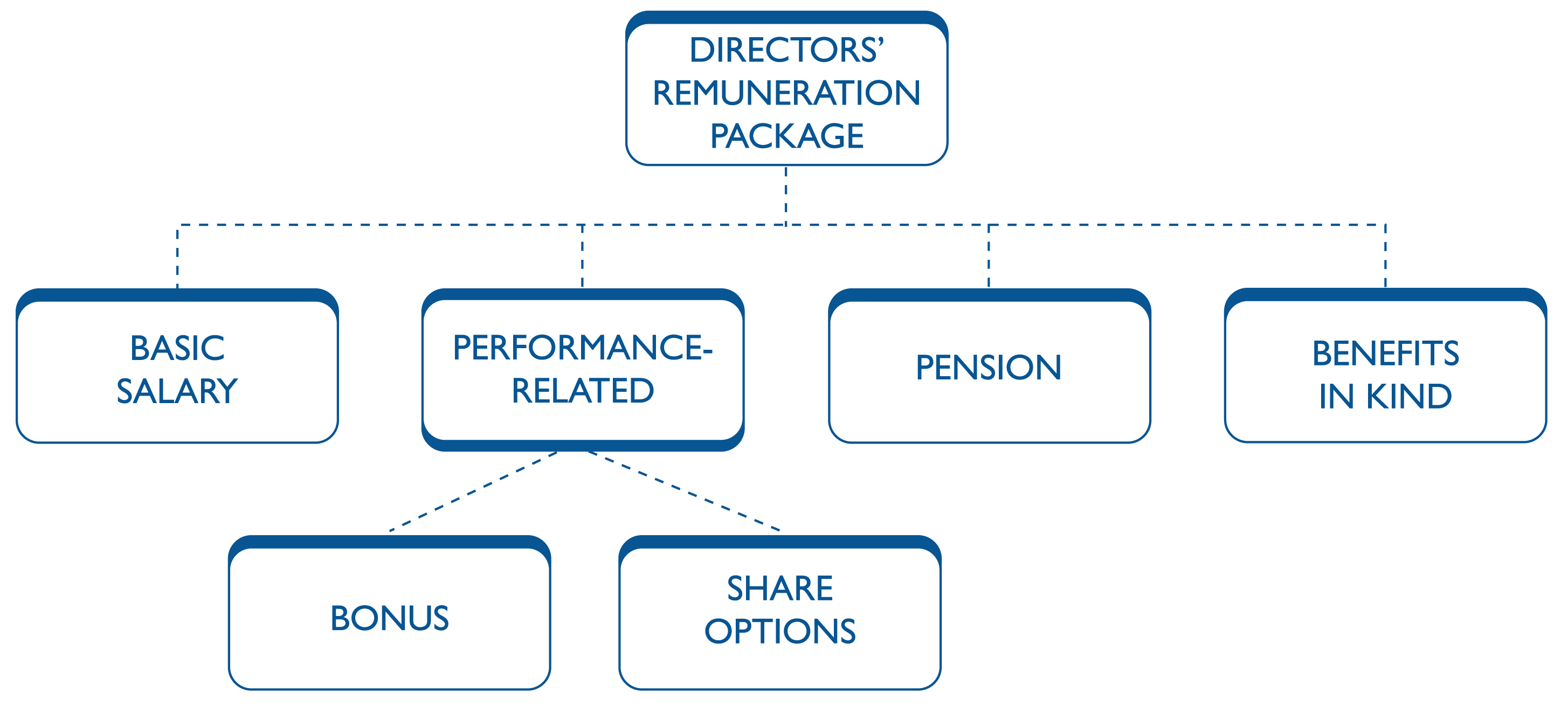

Usually, components of boards’ remuneration package are composed of the financial compensation and other non-financial awards received by an executive from their firm for their service to the organization. It is typically a mixture of salary, bonuses, shares or call options on the company’s stock, benefits and perquisites, ideally configured to take into account government regulations, tax law, the desires of the organization and the executive, and rewards for performance (see Figure 2 for details):

However, the need to develop a remuneration strategy that links reward to performance is the greatest challenge facing the remuneration committee. There is a critical need to ensure the board is

motivated to strive to increase performance; adequately rewarded when performance improvements are achieved; seen to be paid appropriately for their efforts and success; not criticized for excessive pay; and retained through market-based pay levels.

It is very hard for a country to find qualified people experienced in business without a good remuneration package. The remuneration of the board consists of the total pay and benefits with two broad components: fixed, which includes base salary and benefits including pensions, and variable, which includes annual bonuses, fees, share options, restricted shares, reimbursement of personal expenses and any other benefits (CIMA, PWC, & Radley Yeldar, 2007).

Clearly, the remuneration should be sufficient to attract board members, to provide an incentive for better than average performance, to reward success and to retain the important board members’ involvement in the company. Moreover, the board members consider whether the level of remuneration has an impact on board members’ commitment and dedication to their role.

In some countries, there are maximum limits to the remuneration of SOE boards (OECD, 2005). For instance, in Poland, the wage of an SOE board member is no more than six times the average wage in the industrial sector concerned, while, in the Slovak Republic, remuneration cannot be higher than five times the average national wage (OECD, 2005). There are few countries that apply board remuneration through a standardized methodology, such as New Zealand. State-owned enterprises boards’ remuneration methodology in New Zealand does not relate the board’s fees with their performance. Each SOE is placed into one of six fee bands, with a unit rate for each member. Each member receives approval for an annual lump sum of fees based on the unit rate multiplied by the number of the member, with a loading of 2 for the chair and 1.5 for the deputy chair. The unit rate incorporates an allowance for sub-committee work. These unit rates are aligned to the private sector averages, but with a reduction to reflect the public service element of appointment to the SOE boards (OECD, 2004).

There are few cases where part of the board members’ remuneration is performance-related, such as in UK, where board member remuneration is a combination of base pay and bonuses based on performance. Other developed countries generally establish a specialized authority to determine the remuneration of SOEs’ boards to avoid conflict of interest and to de-politicize the issue (Okhmatovskiy, 2010). Overall, there is a strong tendency in OECD’s countries to make the remuneration packages more attractive for members of SOEs’ boards in order to get professionals participating on the boards.

According to Kakabadse, Yang and Sanders (2010) and Lu (2009), most members of board exercise other duties because their remuneration incentive system has failed to meet market demand. As a result, they spend a little time on the job as a member of the board and depend on what they are given by the executive management in term of information (Adams & Ferreira, 2004). This is the reason why many members of boards are not able to participate in every decision and only have a rudimentary understanding of the company’s operations (Lipton & Lorsch, 1992).

Countering these problems, the OECD recommended the establishment of a remuneration committee. The remuneration committee mostly consists of independent commissioners who will make fair recommendations to the shareholders for the remuneration of the board and management (OECD, 2004). According to Price Waterhouse Coopers and the UK Institute of Management Accountants, to achieve good governance, the reward schemes must be linked to the company’s performance, be aligned with shareholders’ interests and the company’s strategy and be based on current market practice (Cochrane, 2007). Those objectives require four principles for a remuneration policy: competitiveness, be performance linked, be shareholder aligned and be simple and transparent (CIMA et al., 2007). However, until today, none of the countries had applied those four principles, although there is a strong underlying tendency in many OECD countries that have re-evaluated the board reward schemes in order to bring them more into line with the four principles like in the private sector. For example in Norway, the newly adopted corporate governance principles for SOEs state that the board compensation and incentive system shall promote the creation of value in companies and shall be generally regarded as reasonable (Norwegian Government Policy, 2002).

A good structure of boards’ remuneration usually consists of fixed annual and short-and long-term incentive elements. The fixed incentives recognize the status of the recipients and enable them to undertake current and future lifestyle planning. Meanwhile, the short-term and long-term incentives motivate and reward employees for making the company successful (Leblanc & Gillies, 2005). Ideally, the structure is in line with the company’s objectives, market position and the conditions of the company (CIMA et al., 2007).

Objectives

Based on the gap in knowledge of the boards and using Indonesian SOEs as the context of the study, this research focuses on the extent of board’s remuneration impact performance of the board in implementing GCG in Indonesian SOEs. It assesses the link between the boards’ remuneration system and the effectiveness of the BoCs. The following research question guided this study:

How effective is the boards’ remuneration system impact on the work of the Boards of Commissioners in Indonesian State-owned Enterprises?

In addressing this question, some sub-questions are examined as follows:

To what extent does the remuneration package impact on the work of the BoCs in Indonesian State-owned Enterprises? To what extent does the remuneration levels are adequate for members of the BoCs in Indonesian State-owned Enterprises?

Rationale of the Studies

Board Remuneration System in Indonesian SOEs

The remuneration of the BoC and the BoD members in Indonesian SOEs is regulated by Minister Regulation No.2 /2009. It states that the remuneration of the BoC and the BoD members consists of salary, allowances, insurance and bonuses. However, the concept of the BoC’s remuneration formula in Indonesian SOEs differs from private enterprise, as it is not based on performance. According to regulations, the salary of the BoC and BoD members follow this formula (Ministry of State-owned Enterprises, 2009, p. 4):

Salary = Basic Salary × Industry Adjustment Factor × Inflation Factor × Position Factor The calculation amount of Position Factor in the salary’s formula is as follows:

Factor for President Directors is 100 per cent. Factor for Directors members is 90 per cent of President Directors. Factor for President Commissioners is 4 per cent of President Directors. Factor for BoC members is 36 per cent of President Directors.

Besides a salary, the BoC and the BoD members receive several allowances, such as a communication benefit, pension fund, clothing, housing and transportation (Ministry of State-owned Enterprises, 2009). They also receive other benefits, such as membership of clubs, vehicles, health benefits and legal services. Beside those, members of the BoC and the BoD get incentives if there is an enhancement in the performance of the enterprise without considering the enterprise losses. However, this incentive can only be given to the BoC and the BoD members if they achieve 70 per cent of their target (Ministry of State-owned Enterprises, 2009).

The government recommended that SOEs should have remuneration committees with independent commissioners as the chairman of the committee to determine the BoC and the BoD’s remuneration (Ministry of State-owned Enterprises, 2009). The remuneration committee needs to establish a formal and transparent procedure for developing a policy about the remuneration of members of the BoC and the BoD (NCCG, 2006). Their job is to provide sufficient incentives to attract and retain top members in a competitive market for talent by rewarding success while avoiding excess and appearing to reward failure (Hardjapamekas, 2000). In addition, although the remuneration committee is led by an independent commissioner, in practice the commissioner may not be completely independent (NCCG, 2006). The loyalty towards their own members of the BoC (government commissioner), because they were nominated by them, may make the commissioners feel obliged to them. Of course, the question remains as who should fix the remuneration of the members of remuneration committees (Daniri, 2006).

For transparency, in the case of listed SOEs, the statement of remuneration policy and amount of the remuneration of each member of the BoC and the BoD is published in the SOE’s annual report. Transparency is important in corporate governance (Ministry of Finance, 2006). However, compared to developed countries’ regulations on remuneration report transparency (Tricker, 2015), Indonesian regulation does not require details of the performance criteria in incentive schemes or pensions and retirement benefits. The government only requires details of members of the remuneration committee, a statement of the company’s policy on the BoC’s remuneration for the future, and the amount of remuneration (Ministry of Finance, 2006).

With this unique remuneration system, it may be interesting to know the impact of using such formula to achieve an ideal remuneration as well as balancing the interests of the BoC and the BoD against those of the shareholders. Thus, this study addresses this research gap through exploration of the relationship between board remuneration and effectiveness of the board in Indonesian SOEs. Accordingly, this study is enriched by qualitative data in the form of in-depth interviews with four main actors, the members of the boards, management, government officers and CG experts, to gain an in-depth understanding of the extent of board remuneration that has impacted the boards’ performance from various perspectives and experiences. Most previous studies of boards’ remuneration in SOEs have relied solely on the quantitative approach (Dogan & Smyth, 2002; Kakabadse, 2010). This approach is largely drawn from the business and economic perspectives which associate the boards with firm performance. Meanwhile, to understand the complex practices of the boards, it needs a different perspective, a perspective that is able to view the work of the boards through the potential interaction of other variables, such as relationships, board behaviour and personalities. It will be more effective if future studies take account of qualitative data. A more comprehensive understanding of the effective boards can be achieved by examining how the remuneration system actually impact boards’ work in implementing GCG in SOEs.

Methodology

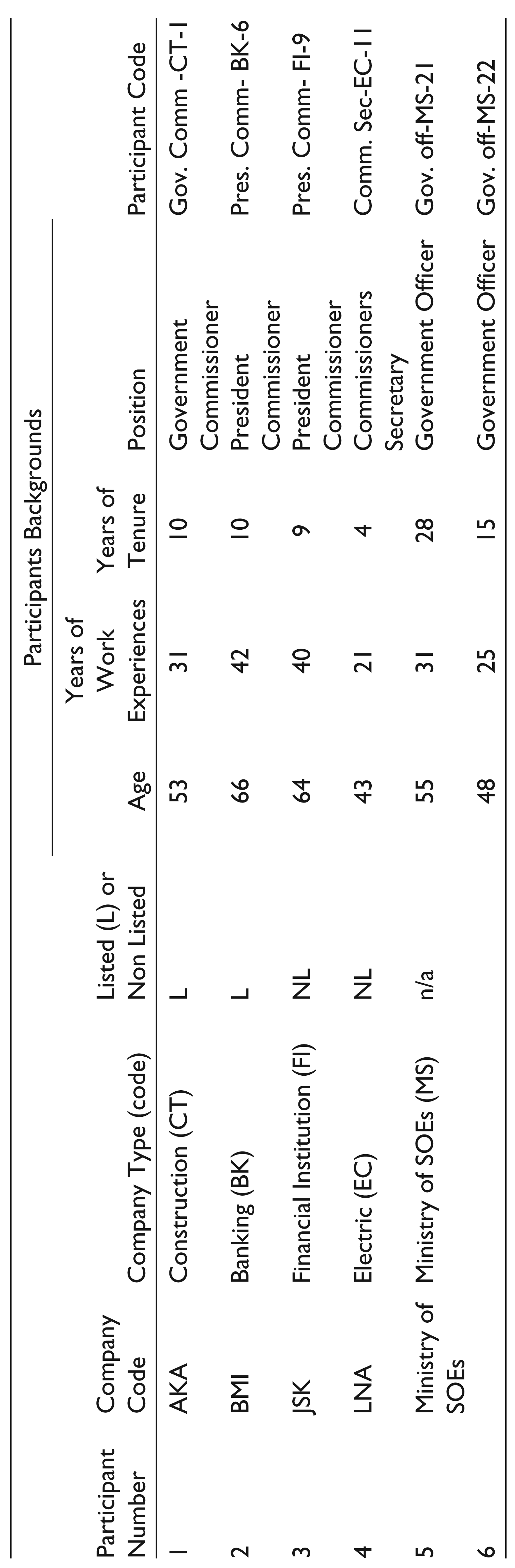

This study presents a comprehensive analysis of corporate governance issues in SOEs from the actors of governance viewpoints. The qualitative method was used in this research for data collections. Written documents, such as annual reports, board manual and government policies, were used as secondary data while the primary data were collected from a selection of four SOEs and two of them were listed on the stock exchange. The four SOEs were from construction, banking, financial institution and electric (see Table 1).

List of Participants.

A total of six in-depth, semi-structured interviews were taken for average of one hour from participants who, at that time, held a role as president commissioners, government commissioners and government officers (list of participant provided in Table 1), allowing participants to reveal their ‘real’ views and perceptions. A purposive sampling approach was used to draw sample from relevant organizations. Furthermore, there were also attempts to affect snowball sampling when some participants were suggested or introduced to other relevant people with the same characteristics to participate in this research. Access to participants was ultimately through personal contacts. Although this data did not statistically represent the views of Indonesian SOE boards, it provided preliminary perspectives on their operation.

Analysis

As discussed previously, the government determines the remuneration of the BoCs in Indonesian SOEs through a formula under Board Remuneration System in Indonesian SOEs section. Thus, questions regarding the interviewees’ thoughts about the remuneration formula arose. The answers given by participants indicated whether the current remuneration is adequate or not for the BoC.

A president commissioner gave the following answer:

It is difficult to determine the remuneration of the BoC through their index performance (KPI) because we have any. Not like the BoD, who has their own KPI, the performance of the BoC is collective. Therefore, one member of the BoC gets the same percentage with other members in the remuneration distribution. Please refer to Ministry policies for details. In another private company, the remuneration of the members is based on their attendance at committee’s meeting, but we don’t. Probably, we need to consider this too. The ministry should differentiate between the BoC members who always attend the committee’s meeting rather than those who do not. Besides it will motivate the members to attend the meeting, it also encourages new person to join with the BoC (President Commissioners from Banking Industries-6).

In other words, he wants to say that the formula established by the government for determining remuneration packages is not fair to ‘active’ members who are dedicated and committed to their duties and responsibilities. The ‘active’ members frequently feel that they are ‘underpaid’ given their legal responsibilities, the length of time required and attendance at meetings. Furthermore, his statement also may indicate that the current remuneration package is not adequate and does not attract qualified persons because it is not based on performance. Another participant, also a president commissioner, may confirm this argument. His comments are as follows:

If the BoC wants to become professional, the reward should be equal according to their professionalism. Unfortunately, current remuneration in SOE frequently is not attractive because it is usually below the market. Therefore, we do not get a qualified person who is the best in their field. For example: In financial industries, we need an expert on risk management, but the person who is an expert in this field has a standard minimum for his/her reward. Unfortunately, his/her expectation of the remuneration frequently is above the amount given by the government (President Commissioner from Financial Institutions-9).

Based on these two respondents, it may be concluded that the current remuneration is not adequate for the active BoC. Probably, this is one of the reasons why it is difficult to obtain qualified persons and want to dedicate their time completely to the BoCs as independent commissioners in Indonesian SOEs. Certainly, these feelings impact the BoC’s performance. More discussion regarding the extent of Indonesian remuneration system impacts the work of the BoC followed. It analyzed the relationship between the attractiveness of membership and the BoC’s commitment and dedication.

When we asked questions to respondent about the effect of the current system to board’s performance, their answers are not surprisingly as many scholars have suggested. The following argument is given by the government officer. He agreed that one of the factors that make the BoC effective was the ability to provide an attractive remuneration for the members.

There are two factors consider for effective BoC: First, the ability to determine the decent wealth for members of the BoC. Second is managing the law enforcement to implement the punishment-reward system according to their performance in order to achieve good governance in SOEs. Otherwise, members of the BoC will not focus conducting their duties as it occurred today (Government Officer from Indonesian Ministry of State-Owned Enterprises-21).

These arguments are similar with what many scholars have suggested, that is, a good remuneration system should be adequate and sufficient to attract board members, to reward success, to provide better than average performance and to retain the influence of important board members in the company (Garratt, 2006). Otherwise, it makes the active members less motivated (their efforts are valued as same as the efforts of inactive members (Kakabadse, 2010), but also means members of the BoC do not focus on their duties (Adams & Ferreira, 2004; Lu, 2009). As a result, many members of the BoC are not able to participate in every decision, and they only have a rudimentary understanding of the company’s operations.

Interestingly, one participant from the members of the BoC provides a different perspective on the determination of the BoC’s remuneration through the use of a formula. He assumes that the formula for the remuneration package establishes a sense of fairness among members of the BoC due to collective responsibility.

As I mentioned before that, the BoC are accountable for collective performance. All the decision made by the BoC is a result of the joint decision that also means the consequences must share collectively. Therefore, for me, the Ministry is already fair in giving the remuneration package to all BoC members through this formula. Because according to this formula, all members of the BoC have been rewarded with the same amount regardless of the members being independent or government commissioners (Gov. Comm -CT-1).

Based on his opinion, we also can understand that there is a relationship between unclear job expectation and reward process. It may be assumed that without clear job expectations at the beginning of their duties, the government will find difficulty in implementing a reward system that is linked to individual’s performance.

The different arguments between these two participants may also prove that the determination of the BoC’s remuneration is not simple. According to studies, good remuneration system has to link to the company’s performance, be aligned with shareholders’ interests and the company’s strategy and involve individual performance as well as current market practice (CIMA and PWC cited in Cochrane, 2007) because, without these, the determination of remuneration will always be contentious as it will not encourage fairness, teamwork throughout the boards or motivation for members to do their job well (CIMA et al., 2007).

Furthermore, this present study also reveals that the formula established by the government to determine remuneration packages for the BoC may cause a conflict of interest among the members of the remuneration committee. The remuneration committees, who are expected to bring fair recommendations for the BoD’s remuneration package every year, will no longer be able to give valuable and justifiable consideration as the formula relates the BoC’s remuneration with the BoD’s remuneration. In other words, an increasing in the BoD’s remuneration will leverage the BoC’s remuneration. Under such a condition, it may be hard to expect that the members of the remuneration committee will be able to act in the best interest of the shareholders when they assess and decide the remuneration for the BoD.

Thus, it is logical that the remuneration committees in Indonesian SOEs have less interest in linking the BoD’ remuneration with the company’s performance, shareholders’ interest and company’s strategy. This argument was raised by a participant from the government officers who are usually involved in the meeting between the remuneration committee and government:

In Indonesian SOE, the benchmark of remuneration is President Director. For example, if the president director gets 100%, then another director is 90% from the president director. While, for BoC’s remuneration, the president commissioner get 45%, and other members get 40% from the president director. Therefore, I saw that the remuneration committee which one or two members are government commissioners come up with the decision not to increase the salary or not given a bonus to the BoD, except the SOEs has suffered a lot of losses. Most of the recommendations given by remuneration committee BoC to the shareholders are increasing the remuneration of the BoD as well as giving a bonus every year although they know that the performance of the BoD does not show a satisfaction result. Why? It is probably just because a simple reason; The BoC who also members of the remuneration committee have a particular interest. An increasing on remuneration package of the BoD will also increase the remuneration of the BoC too (Government Officer from Indonesian Ministry of State-Owned Enterprises-22).

His point is supported by another participant although her statement is more likely to justify the action instead of criticizing it.

The condition and situation of each SOE are different from each other. Sometimes, the BoC has to see certain condition make a decision on the BoD’s remuneration. We just cannot relate the decision on the BoD’s remuneration with increasing/decreasing over the company’s performance without considering other factors. There are many things required evaluation. So, I think it is normal if there are SOEs that are still giving a bonus to the BoD although they do not achieve the target giving. For example: if the profit target giving is 100 while the BoD only reached 80, I think the BoD still deserve to get the bonus and remuneration increase. We call it as a bonus for operational improvements in order to motivate the BoD in the future (Commissioner Secretary from Electric Company-11).

This statement implies that no matter what the performance of the BoD is, as long the SOEs do not suffer losses, the BoD will still receive a bonus and payment increase. So, this also means that the decision about the BoD’s remuneration may not be linked to the BoD’s performance or shareholders’ interests.

Data taken from the annual report of several SOEs, such as Indonesia Power Plant Enterprise (PLN) and Taspen Enterprise, confirm her arguments. In their GCG, report shows that the BoDs still received bonuses and remuneration increases every year even though their companies did not reach their targets (PLN, 2009; Taspen, 2010). As long the BoDs show progress in the companies’ performances, the remuneration committees will recommend the bonuses and a salary increases. Remarkably, this increase is frequently approved by the Ministry of SOEs.

Probably, the most logical reason for this is that most of the government officers in the Ministry may also be members of the BoC in SOEs and receive an advantage from increases in the BoD’s remuneration. This is supported by Abeng (2001) who argues that there is a little incentive to retain an established ideal remuneration system. The ideal remuneration system is the one linked to the company’s performance and strategy, shareholders’ interests and individual performance in Indonesian SOEs, as this ideal will be disadvantageous for government officers.

In summary, from the data given in this section, it may be shown that there are relationships between the performance of the BoC and the remuneration system. No expectation of individual members of the BoC means that there are no individual performance evaluations and without an individual evaluation there is no reward system based on individual performance. Thus, to motivate the active members of the BoC and to attract qualified persons, the Ministry of the SOEs may rethink the use of the current formula to reward the members of the BoC.

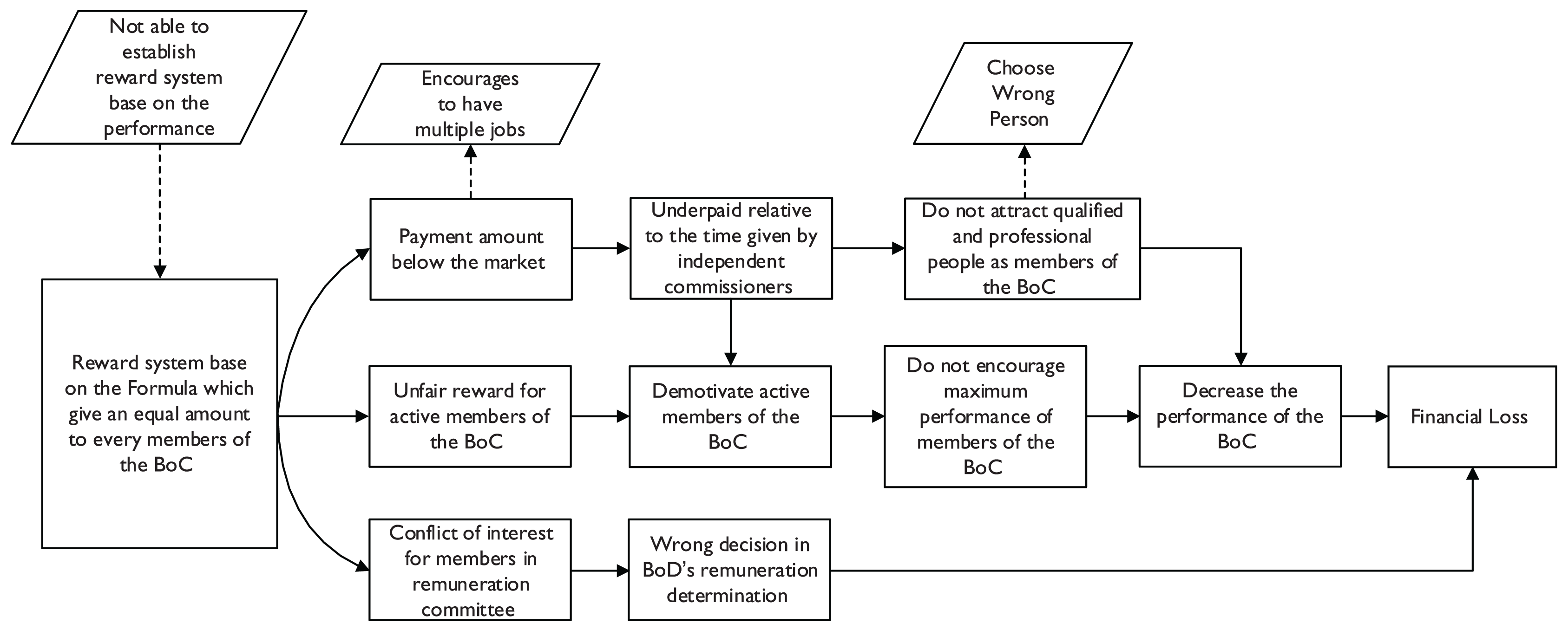

A summary of findings in this subsection is shown in Figure 3 which presents the interrelationship of variables in the remuneration process (shown by the full line) and with other factors (shown by the dashed line).

Conclusions

Based on the above discussion, this study concludes that the reward system for the BoCs exerts a strong influence on the attitudes and behaviours of BoC members. It is because the reward system sends a message regarding the members’ value to the SOEs and shows how the SOEs expect the members of the BoC to focus their time and energy. Otherwise, members of the BoCs will not have the motivation to improve their performance, and qualified members will lose motivation. Their expectation is simple; for better performance, the members of the BoCs expect higher rewards.

In the case of Indonesian SOEs, this study shows that the current remuneration is not adequate. Certainly, this is the small reward compared to that which is available in the market and the remuneration system which based on a formula that does not motivate members of the BoCs to give their best performance and does not attract qualified people to join the BoCs in Indonesian SOEs. It is because, with such a reward system, members of the BoCs will receive the same reward regardless of their performance. So it is quite normal that many members of the BoCs who are underperforming are retained. Furthermore, such system also establishes conflict of interest in making a decision over bonus and salary increasing of management. In the end, this impacts on the recruitment quality and BoC’s performance because the remuneration system in Indonesian SOEs is not linked to performance evaluations.

Meanwhile, according to several previous studies (CIMA et al., 2007), the best system to reward members of the BoCs is to emphasize performance-based pay because it values efficiency, creativity, knowledge sharing and teamwork. A good reward system will attract qualified people for the job, motivate members of the BoC to give their best performance and retain members of the BoC needed for the SOEs to have and maintain a sustained competitive advantage (Tricker, 2015).

Footnotes

Acknowledgements

We would like to acknowledge to several institution for their help: first, the authors would like to gratitude Bina Nusantara and Indonesia Directorate General Higher Education for their funding of this research and Second, the authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of this article.