Abstract

This article aims to examine the performance implications of dynamic capabilities in the banking firms and explain the degree of influence that learning, integration, reconfiguration and alliance management dynamic capabilities are likely to have on a bank’s financial and non-financial performance. Using 439 samples of managers in Indian banking firms, structural equation modelling (SEM) was directed and found that dynamic capability is a vital driver of banks’ performance. Learning, integration and alliance management dynamic capabilities have significant relationship with banks’ financial and non-financial performance. The insignificance of reconfiguration capability for financial performance is also revealed. Practically, findings will serve banking sector, useful course-of-action to overcome the present competitive-pressures as well counter the future challenges through depth knowledge on specific dynamic capability investment and respective performance-improvement. Stranded on these findings, practical implications, limitations and future research directions are also conversed.

Introduction

In today’s globalized and competitive business landscape, banking sector has been acknowledged as the barometer of the economy (Kaur, 2010) which echoes the macroeconomic variables. Nowadays, due to the global megatrends (global marketplace, demographic shifts, changing workforce and digital business) accompanied with stakeholder pressures and lacklustre growth in banking industry throughout the world, banking firms are compelling the quest for profitable growth and survival. They are challenged to define a bank’s new core and structure, adopt advanced technology and shape the new strategies and operating models for the realization of competitiveness over the coming decade (Ernst & Young, 2015). The major issue is how to survive, grow and attain outstanding performance? Concerning to the same, Ernst & Young (2015) report pointed out that ‘the most successful institutions will be those that can reinvent themselves to overcome the pressures of today while becoming flexible enough to respond to the world of tomorrow’. All these facts create a baseline for managers to rethink and ascertain the vital drivers of banks’ performance.

On the back of strong banking sectors, currently Indian economy has been considered as one of the most vibrant global economies (KPMG-CII Report, 2014). In the past two decades, Indian banking industry has steadily progressed towards a deregulated market economy from a regulated environment. It has shown rapid expansion, kindled by liberalization, globalization and the inauguration of various policies and reforms, such as Indian Financial & Banking Sector Reforms (1991). This growth and expansion have abetted the economy to bounce back to a positive growth level. Being a knowledge-intensive service sector, Indian banking industry alone subsidizes approximately 11.8 per cent to Indian service sector, which contributes 57 per cent to the gross domestic product (GDP) and ranked India 12th in terms of services GDP (Economic Survey, 2012–2013). The current size of Indian banking asset has crossed US$1.8 trillion in 2013 and is estimated, in 2025, to pass US$28.5 trillion. Experts predict that this industry has the prospect to become the largest banking industry in the world (KPMG-CII Report, 2014).

Keeping into mind the full realization of this expected potential and paybacks of the banking industry to the economy (infrastructure development, employment opportunities, financing of SMEs and MSMEs, foreign exchange and investment benefits, reach to global market and revival in economy) and globalized market (potential market for investment), government has introduced various policy measures which not only stimulate development and revolution in the banking sector but also open new domestic and international level opportunities. Competitive pressure also emerged and compels banking firms to sustain their performance and maintain competitiveness (Arrawatia & Misra, 2014; KPMG-ICC Report, 2013; Singh & Kaur, 2015; Sufian & Noor, 2012). Having found the significance of banking sector to the economy along with the opportunities, challenges and quest for survival and enhanced performance, it is noticeably vital to examine the performance factors of the banking firms in the present dynamic, competitive and constantly changing business milieu.

Recently, the dynamic capability notion has become a predominant theoretical framework in the management literature, for analyzing how firms change with respect to high-velocity markets and win the competition. Dynamic capabilities are well defined as the capability to integrate and reconfigure firm resources and competences to respond to changing market environments (Teece, Pisano & Schuen, 1997, p. 516). Researchers have discussed their role in value creation, performance advantage and competitiveness enormously (Eisenhardt & Martin, 2000; Helfat et al., 2007; Teece, 2007; Teece et al., 1997). They found that dynamic capabilities are prerequisite for the firms to address the changing market milieus and sustain the long-term survival of the firm; it delivers right knowledge to the right person at the right time, boosts knowledge sharing (Tseng & Lee, 2014) and equipped firms to reconfigure and transform resources to be faster in grasping opportunities. Therefore, it is vital for the firms to value the principles of dynamic capabilities and possess knowledge on how to effectually manage them to sustain augmented performance, more specifically, in manufacturing, service and knowledge-oriented industry segments (Chien & Tsai, 2012; Eisenhardt & Martin, 2000; Teece et al., 1997; Wang & Ahmed, 2007; Wu, 2006).

These industries retain more intangible resources and capabilities than tangible resources (Bontis & Fitz-enz, 2002). If the same holds true in banking industry that is considered as a core knowledge-intensive service industry (Mondal & Ghosh, 2012) and are facing environmental changes and intense competition like other industries, dynamic capabilities may become one of the essential component of the bank’s strategy to respond to dynamic business milieus and further move to the ensuing phase of performance enhancement. In this vein, Mondal and Ghosh (2012) and Shih et al. (2010) also stress that a prerequisite for the success of banks is developing firm’s capabilities to cope with dynamically changing environment. This suggest that without constantly renewing and reinventing firm’s capabilities through dynamic capabilities, firm will find it challenging. However, review of literature reveals little understanding into how banks deploy dynamic capabilities and how dynamic capabilities influence their performance.

In addition, although studies on performance-related aspect of the firm in different industries have given insights into the significant value of dynamic capability factor for performance improvement, literature review reveals that not enough thoughtfulness has been given to the role frolicked by different dimensions of dynamic capability for subsidizing different performance advantage. Most researchers use an overall score of dynamic capability and performance (Chien & Tsai, 2012; Hsu & Wang, 2012; Hung et al., 2007; Hung, Yang, Lien, McLean & Kuo, 2010; Lin & Wu, 2014; Pavlou & El Sawy, 2011; Sher & Lee, 2004; Tseng & Lee, 2012; Wang & Ahmed, 2007; Wu, 2006; Zhou & Wu, 2010). Thus, how the different elements of dynamic capability contribute towards the realization of different performance advantage is not completely clear. In fact, prior findings are inadequate and limited and their association has yet to be entirely determined. Moreover, in spite of the advanced theoretical arguments about dynamic capabilities notion and their association with firm performance, relevant empirical work complementing these theoretical arguments is still limited (Helfat et al., 2007). Most of the empirical investigations, concluding such research findings, have been extensively based on case studies. Studies utilizing inferential statistics and providing empirical evidence on the linkages among the constructs are scant (Easterby–Smith, Lyles & Peteraf, 2009; Eriksson, 2014; McKelvie & Davidsson, 2009; Prieto & Easterby-Smith, 2006), specifically through multivariate statistical techniques. Concerning this, as Protogerou et al. (2011) mentioned whether dynamic capabilities influence performance is open for further investigation still. In light of these gaps, the present inquiry attempts to study the influence of different dynamic capabilities on the performance of banks.

The article has been structured in the subsequent way. The next section deals with theoretical foundation of the constructs and linkages, followed by objectives of the study and methodology. Later on, discussion, implications and limitations along with future research avenues have been discussed.

Theoretical Foundation

Dynamic Capability

Since the dawn of 1990s, the most influential strategic management paradigm which attributes sustainable competitive advantage and performance of the firm on VRIN (Valuable, Rare, Inimitable and Non-substitutable) resources and their implications, namely, resource-based view (RBV), was critiqued. The reason was its inability to elucidate the effect of market dynamism on performance (Lengnick-Hall & Wolff, 1999) and its failure to explain the creation and deployment of resources in dynamic markets for sustainable competitiveness. In an attempt to address these shortcomings, Teece et al. (1997) walked a few steps ahead with RBV in dynamic market environments and proposed a new line of theory, dynamic capability view (DCV), that explicates competitive advantage in dynamic markets. This theory submits that availability of firm’s resource stock does not engender rents per se, rather than firm’s resource stock needs to be evolve, employ and renew over the period of time as their external environment changes to sustain competitive advantage (Augier & Teece, 2009; Teece et al., 1997). And, further underscores the significance of dynamic-capability that enables firm’s to renew its stock of capabilities by purposefully creating, extending and modifying internal and external resources in order to realise evolutionary fitness (Chien & Tsai, 2012; Eisenhardt & Martin, 2000; Helfat et al., 2007; Teece, 2007; Teece & Pisano, 1994; Teece et al., 1997). Underlining this significance of dynamic capabilities, scholars, academicians and practitioners have shown their interest in this strategically significant firm-level variable. Consequently, many frameworks on dynamic capability definitions, conceptualizations and outcomes emerged in the literature employing diverse perspectives.

Originally, dynamic capability was defined from capability perspective as the capability to integrate and reconfigure firm resources and competences to respond to changing market environments (Teece et al., 1997). In the same line, dynamic capability was further sketched by Eisenhardt and Martin (2000) as ‘a set of specific and identifiable processes’ that integrate and redeploy resources into the best configuration, such as strategic decision-making, product development and alliance management and cultivate new capabilities and market opportunities and inaugurate process perspective. Using a routine perspective, dynamic capability was also explained as ‘a learned and stable pattern of collective activities’ (Zollo & Winter, 2002). Following Teece et al.’s (1997) thinking, dynamic capability was further outlined as firm’s capability ‘to purposefully create, extend, or modify its resource base’ (Helfat et al., 2007). Using processes and routines perspectives, later on, dynamic capabilities was also drafted as firm’s routines and processes that enable reconfiguration of its source base to acclimatize the changing business conditions and empower firms’ adaptations to realize and achieve competitive edge in a dynamic environment (Pavlou & El Sawy, 2011). Ensuing routine perspective, dynamic capabilities was recently defined as ‘bundles of interrelated routines which, shaped by path dependency, enable an organization to renew its operational capabilities in pursuit of improved performance’ (Piening et al., 2012).

In line with these diverse perspectives towards dynamic capability conceptualization, a wide variety of capability dimensions have been proposed, namely, learning, integration and reconfiguration (Eisenhardt & Martin, 2000; Teece et al., 1997), adaptive, absorptive and innovative capabilities (Wang & Ahmed, 2007), learning (Zahra, Sapienza & Davidsson, 2006), sensing, learning, integrating and coordinating (Pavlou & El Sawy, 2011), timely decision-making capacity, strategic sense-making capacity and change implementation (Lin & Wu, 2014), alliance management capabilities (Helfat et al., 2007), R & D capabilities and marketing capabilities (Hung et al., 2007).

Grounded on previous literature, the present inquiry outlines dynamic capabilities as firm’s capability to manage alliances, learn, integrate and reconfigure resource base to address the changing business conditions and sustain their competitiveness. Consistent with this theorization, dynamic capabilities are conceptualized as comprising four dimensions, namely, learning, integration, reconfiguration (Eisenhardt & Martin, 2000; Teece et al., 1997) and alliance management capability (Kale & Singh, 2009; Schilke & Goerzen, 2010). Learning capability is the firm’s capability to support effective and efficient operations through internal and external learning in accordance with environmental ups and downs (Cohen & Levinthal, 1990; Lavie, 2006). Integration capability is the firm’s capability to cultivate new resource base and capabilities by identifying the firm’s current resource stock, evaluating their value and integrating them to meet the environmental challenges (Teece et al., 1997). Reconfiguration capability is the firm’s capability to recombine and restructure resources and operating capabilities in accordance with market and technology change (Teece, 2007). Alliance management capability is the firm’s capability to create or modify the resource base in order to include the alliance partners’ resources (Helfat et al., 2007).

Towards Firm Performance: The Role of Dynamic Capability

Since the theorization of dynamic capability rational, substantial studies emerged not only in its native domain but also in other domains to explore the dynamic capability performance and competitive advantage implications. These studies reveal some positive and significant covenant. Review of literature highlights that dynamic capability enables firms to sense the market opportunities, create, integrate and reconfigure resource base, routines and structures to match firm’s resource base with fluctuating business milieus, grasp available opportunities (Chien & Tsai, 2012; Li & Liu, 2014; Pavlou & El Sawy, 2011; Teece et al., 1997; Tseng & Lee, 2012), improve the efficiency and effectiveness of firms comebacks to environmental turbulence (Hitt, Bierman, Shimizu & Kochhar, 2001) and in due course fortify increased performance (Helfat et al., 2007; Hsu & Wang, 2012; Hung et al., 2007, 2010; Lin & Wu, 2014; Teece, 2007; Wang & Ahmed 2007; Wu, 2006; Zhang, 2007; Zhou & Wu, 2010; Zollo & Winter, 2000; Zott, 2003). Following the above-mentioned dynamic capabilities theorization, this section attempts to study the role of different dynamic capabilities as an underlying factor of firm performance.

The Role of Learning Capability

Literature highlights that learning capability facilitates organizational learning process and supports internal and external learning (Goh & Richards, 1997) which increases firms’ strategic capability to adapt and respond to changing market scenario (Grant, 1996; Lavie, 2006) and makes them able to improve their results and realize long-term performance (Noruzy, 2013; Senge, 1990). Firms possessing learning capability have the potential to regulate their managerial and operational systems, anticipate environmental and market fluctuations and in due course attain higher financial performance (Calantone, Cavusgil & Yushan, 2002; Ellinger et al., 2002; Senge, 1990). Hence, availability of learning capability conveys the firms’ potential to transform their resources and capabilities in new and idiosyncratic ways to cultivate other knowledge-driven capabilities which are mandatory to sustain firm performance (Teece et al., 1997). Grant (1996) cited that the availability of learning is indispensable for fostering knowledge process and improving firm performance. Zollo and Winter (2002) maintain learning as an enabler of improvement in firm performance through reconfiguration of resources. Prieto et al. (2006) also confirmed the corroboration of learning capabilities and financial and non-financial performance of the firm. Noruzy (2013) maintained that firms with higher level of learning capability significantly demonstrate the higher level of acquisition, creation and sharing the application of knowledge and in turn derive enhanced performances in manufacturing industry. Ensuing RBV and DCV, Lin and Wu (2014) also cited the role of learning capability for increased performance. Collecting this evidence, learning capability enhances firms’ likelihood to transform their resources and capabilities, cope up with environmental changes and further enhance their performance. Based on these rationales, this study hypothesizes the following.

The Role of Integration Capability

Since 1990s, researchers cited integration capability as an essential condition for sustaining performance improvement. They found that firms’ capability to integrate firms’ resources that are present in their internal and external aspects determine their competence for sustainable competitive advantage in dynamic environment (Aoki, 1990; King & Tucci, 2002). Grant (1996) mentioned that success and failure of the firms have significant bearing on firms’ capability to integrate their resources. In the same line, Porrini (2004) also elucidated how integration know-how and competence attained through alliances intensify performance of the firm. Wu (2006) also brought the key concern of the management aiming increased financial performance in a rapidly changing business environment towards integration dynamic capabilities in Taiwanese IT firms, based on RBV theorization. Thus, integration capability influences firm performance. Pavlou and El Sawy (2011) mentioned that dynamic capabilities allow an enterprise to acclimatize to the fluctuating market environments by integrating its source base and eventually attaining an edge over rivals in new product development context. Tseng and Lee (2014) also advocated that firms should possess integration capability and deploy their resources and activities to realize enhanced financial (sales, revenue, profit and return on investment) and non-financial performances in context of Chinese SMEs, following the knowledge-based view (KBV) and DCV. Taking these rationales, effective and efficient integration of firm’s resource base, know-hows and competence enhances firm’s capability to acclimatize the fluctuating market environments and realize financial and non-financial performance improvements. Based on these rationales, this study hypothesizes the following.

The Role of Reconfiguration Capability

Extant literature on capability and performance association offers sizable evidence on firm’s possession of reconfiguration capability and subsequent performance improvement. Researchers submitted that firm’s continual pursuit of recreation and reconfiguration of resources is vital to deal with the impact of environmental changes and sustain long-term performance (Lavie, 2006; Teece, 2007; Wang & Ahmed, 2007). Teece et al. (1997) found the significance of resource transformation for giving timely address to market and technology drifts and cited reconfiguration capability as one of the key dynamic capabilities for augmenting performance (Eisenhardt & Martin, 2000). Wu (2006) also corroborated the utilization of dynamic reconfiguration capabilities indispensable to realize superior financial performance in the context of IT firms, drawing on RBV. Hence, firm’s reconfiguration capability shares substantial associations with firm’s performance improvement. Zhou and Wu (2010) declared that deployment and reconfiguration of resources and capabilities strengthen the influence of technological know-how and further intensify firm performance. Chien and Tsai (2012) mentioned that firms’ ability to reconfigure their knowledge resource base empowers them to augment their performance in restaurant chain context. Lin and Wu (2014) also draw attention to the role of reconfiguration capability for enhancing firm’s financial performance in Taiwanese context, based on RBV and DCV theorization. Drawing on this discussion, reconfiguration capability empowers firms to sense and reconfigure resources, routines and structures and make them more capable to recognize changes in the business environment and clutch available opportunities for improvements in performance. Based on these rationales, this study hypothesizes the following:

The Role of Alliance Management Capability

Researchers mentioned that alliance management capability empowers firms to acquire, share, store and apply alliance management know-how in ongoing and future alliances (Kale & Singh 2009; Kale et al., 2007) and pave a way for superior alliance management (Anand & Khanna, 2000) and diverse alliance aftermaths for both the firm and the alliance (Dyer & Singh 1998), such as stock market gains (Kale, Dyer & Singh, 2002), profitability and sales (Rocha Gonçalves & Goncalves, 2011), innovative outcome (Rothaermel & Hess, 2007) and alliance success (Feller, Parhankangas, Smeds & Jaatinen, 2013; Kale & Singh, 2007; Naqshbandi & Kaur, 2011). Based on RBV, KBV, DCV and competence-based theory, Kale and Singh (2009) and Sluyts, Matthyssens, Martens and Streukens (2011) argued that alliance management capability facilitates alliance experience and increases firms’ overall alliance success by crafting an alliance function and founding alliance learning processes. Spralls, Hunt and Wilcox (2011) quoted that firms’ ability to manage the networks significantly foster trust, lift exchange of information which in turn affect the financial performance of the firms. It suggests that alliance management capability and firm performance are significantly associated. Naqshbandi and Kaur (2011) submitted that alliance success, firm’s flexibility, innovative output and competitive advantage have bearing on AMC, drawing on the literature review. Kauppila (2013) endorses that alliance management capability affects firm performance in Finnish manufacturing firm context, based on RBV. Recently, Niesten and Jolink (2015), in their review paper, also cited the significant association between alliance management capabilities and firm performance based on the prior alliance literature review. Collating these theoretical and empirical evidences, it is maintained that firms’ ability to manage their alliances and deploy their resources and capabilities via alliance experience, portfolios and learning processes augments firms’ performance. Based on these rationales, this study hypothesizes the following.

Objective of the Study

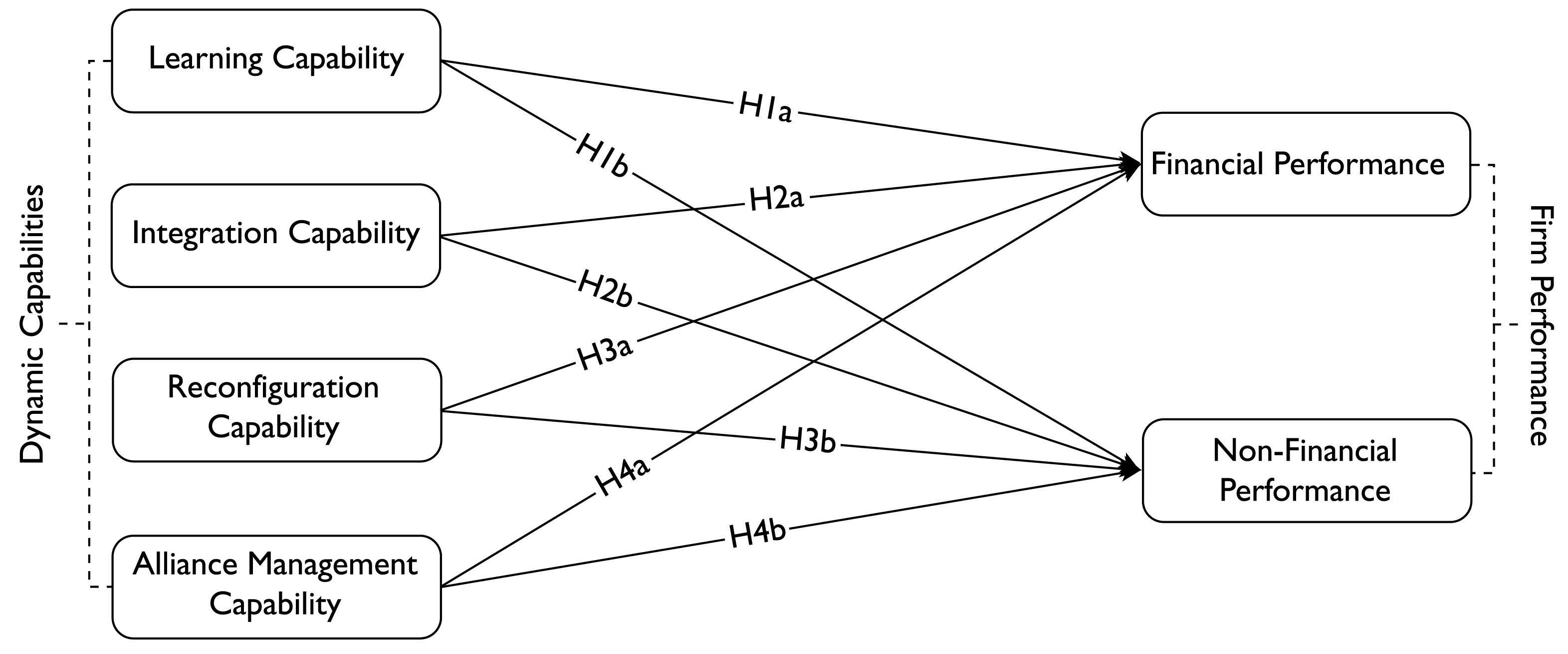

Drawing on the literature, this study raises a prominent research question: Whether dynamic capabilities influence the development of performance in the banking firms? Accordingly, the major area of interest of this article is to determine the association between the dynamic capabilities and performance of the banking firms and examine the degree of influence each dimension of dynamic capabilities is likely to have on a bank’s financial and non-financial performance. The major aim is to offer strategic direction for dynamic capability portfolio investment and subsequent performance improvement in the banking firms. In this concern, an integrated framework is also developed and hypotheses are proposed as shown in Figure 1. The proposed framework assumes that dynamic capabilities comprise learning, integration, reconfiguration and alliance management capabilities which directly influence financial and non-financial performance of the firm. A sample of 49 Indian banking firms was selected to collect the data. The structural equation modelling (SEM), a multivariate analysis technique, was employed as the statistical tool to examine the following research hypothesis that will answer the research question as discussed earlier.

H1. Learning capability has a significant influence on (i) financial and (ii) non-financial performance of the banking firms.

H2. Integration capability has a significant influence on (i) financial and (ii) non-financial performance of the banking firms.

H3. Reconfiguration capability has a significant influence on (i) financial and (ii) non-financial performance of the banking firms.

H4. Alliance management capability has a significant influence on (i) financial and (ii) non-financial performance of the banking firms.

Research Approach

Sample and Data Collection Procedure

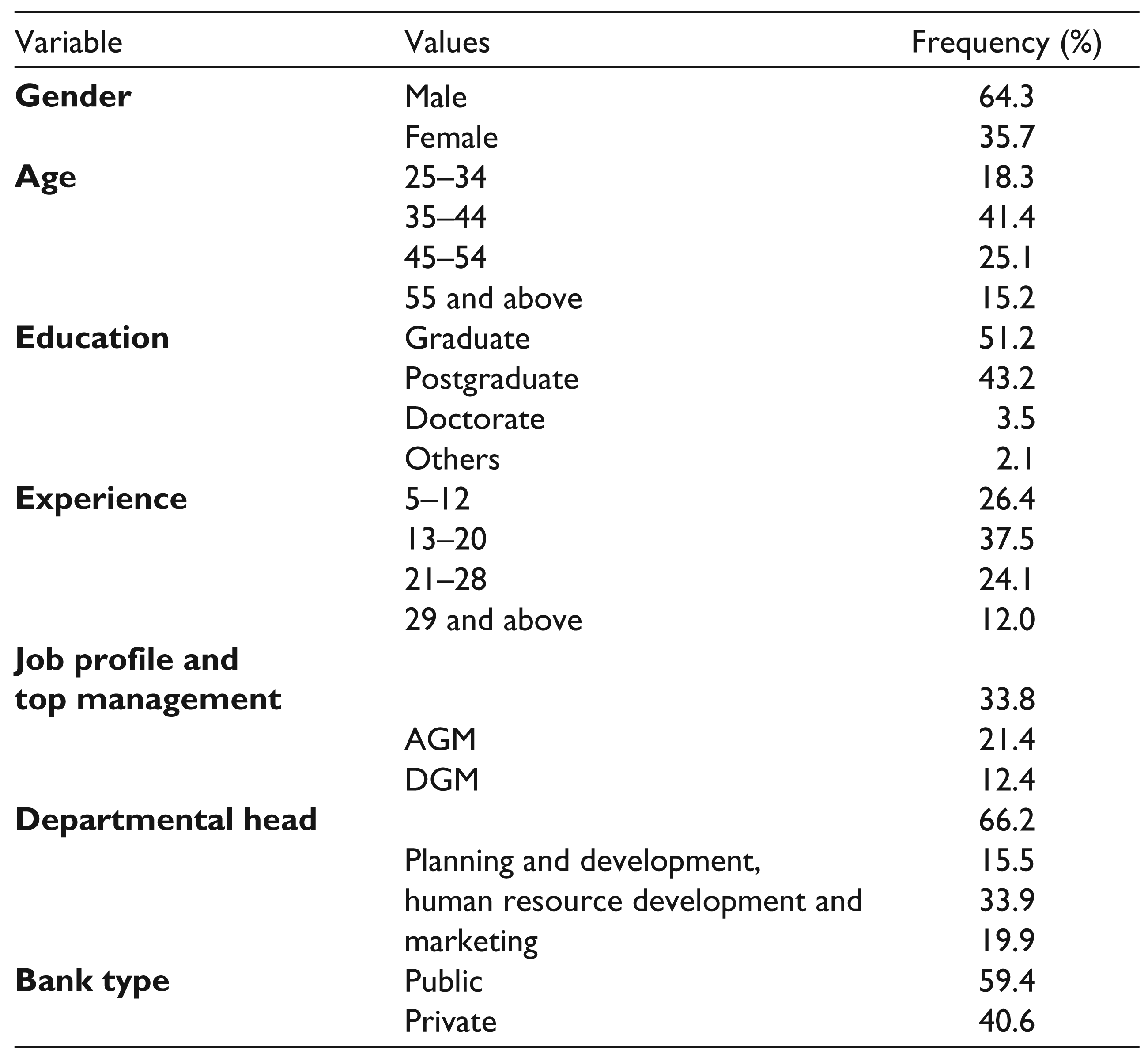

The present inquiry employs survey methodology with the sampling frame of 49 Indian banking firms comprising 22 private and 27 public sector banks for primary data collection. Following key informants technique, different cadres under top-level management (AGM and DGM) and middle-level management (departmental heads of planning and development, human resource development and marketing under) were ascertained as the respondents. Employing diverse cadres under the different managerial level curb the common response bias that may arise due to provision of data for all employed constructs from the same source. The websites of respective banks and Reserve Bank of India were visited for required information. Simple random sampling plan was utilized for respondent’s identification. An extra caution was made to identify potential informants and few questions were added in the questionnaire for verifying their appropriateness, taking into account the use of single information source and resultant potential measurement error. Prior researchers also utilized the same (Hsu & Sabherwal, 2012). A total of 498 respondents received questionnaires with covering letter, via 273 field survey and 225 mail survey. Follow-up mails and calls were employed to increase the response rate. In total, 439 questionnaires were reverted valid and usable with 89.77 per cent response rate. The data collection was scheduled between January and August 2014. Characteristics of the sample are illustrated in Table 1.

Profile of Respondents’ N = 439

Instrument Operationalization and Pre-testing of the Scale

To develop the measurement scales of the present study, dynamic capability and firm performance literature have been reviewed and standardized questionnaire was developed that served as the main data collection instrument.

Dynamic Capability

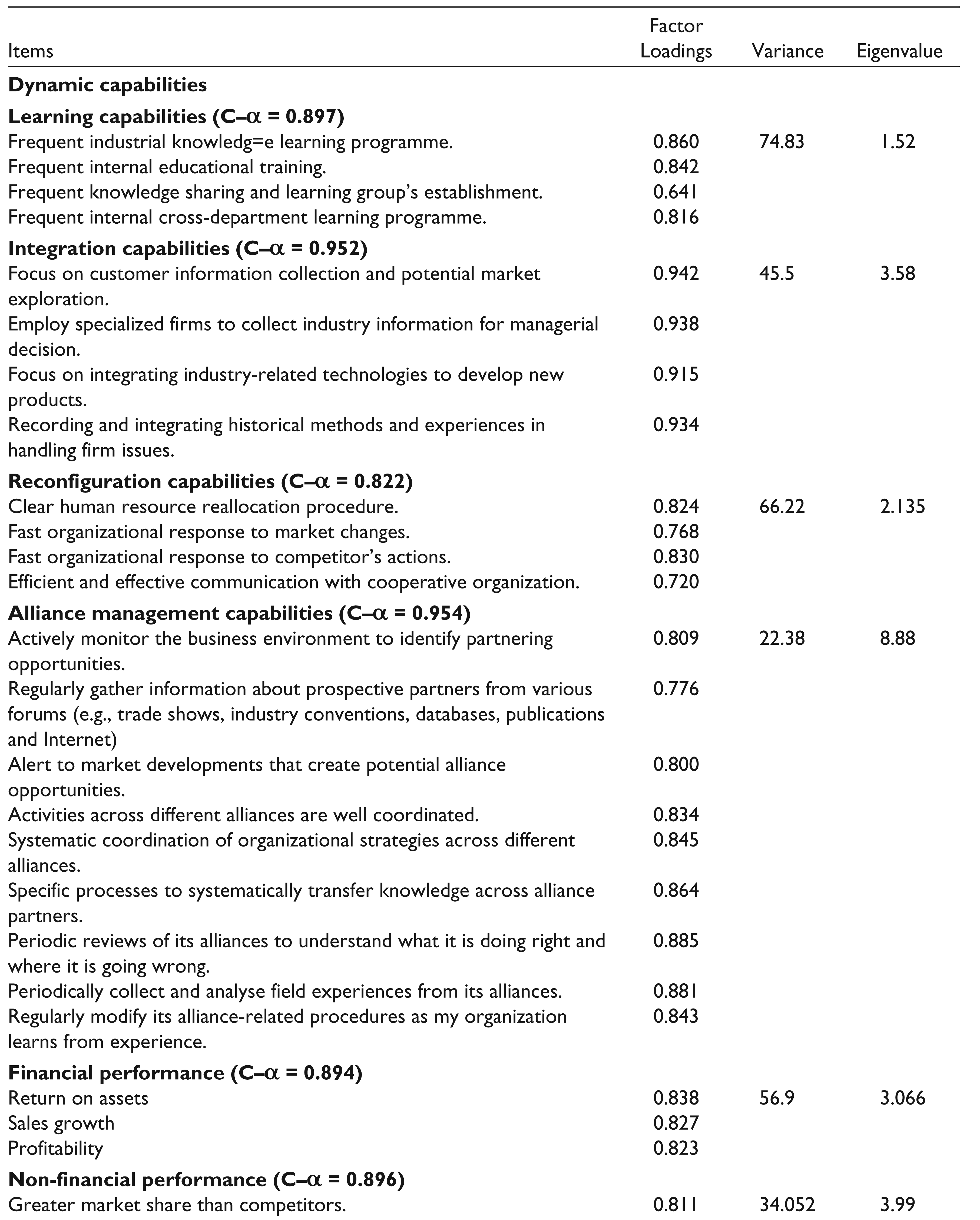

It was operationalized as a four-dimensional second-order construct, drawing on the previous literature. The first-order dimension of dynamic capability consists of learning, integration, reconfiguration and alliance management capability that explain the unique aspect of conceptual realm of dynamic capability and are measured independently to investigate their inference with financial and non-financial performance measures of the firm. To measure learning (assessed with four items), integration (four) and reconfiguration (four) dynamic capability, a 12-item scale was adopted which was utilized and empirically validated by Lin and Yu (2014) (it was developed by Eisenhardt and Martin [2000] and Teece et al. [1997]). As to alliance management dynamic capability, Kandemir, Yaprak and Cavusgil’s (2006) nine-item scale was employed.

Firm Performance

Firm performance was operationalized as a two-dimensional second-order construct, based on the previous literature consisting of financial performance and non-financial performance as the first-order dimension. The present study drawing on the study of Protogerou et al. (2011) uses subjective measures to operationalize performance dimensions, for three reasons. First, the use of perceived measures of performance not only is consistent with objective measures but also subjugates respondents’ unwilling-

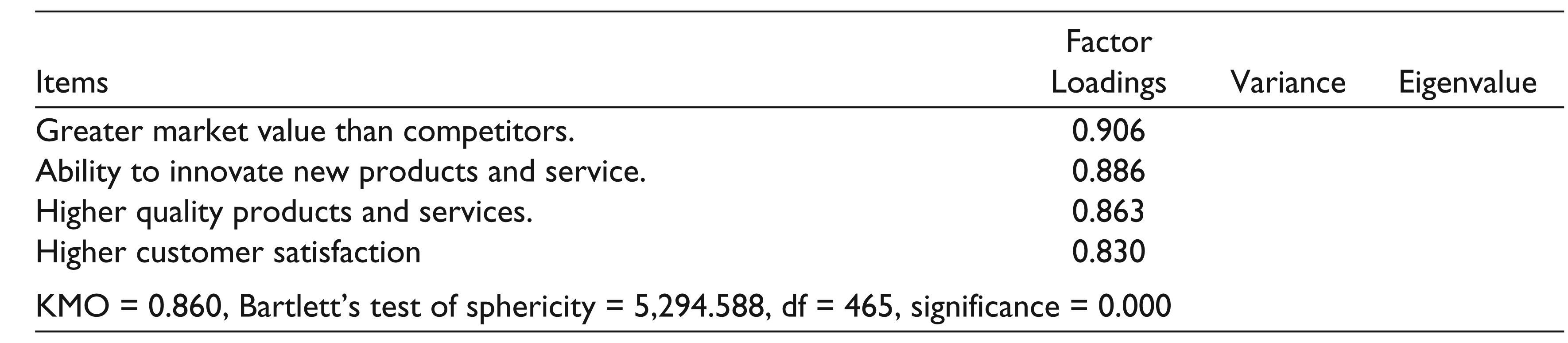

ness to provide objective outcomes of performance (Dess & Robinson, 1984). Second, subjective performance measures are commonly utilized and accepted in strategy-related research. Third, perceived measures permit comparisons across different industries firms and contexts (Song et al., 2005). To measure financial performance, five perceptual measures were adopted from the scales of Calantone et al. (2002) and Ellinger et al. (2002). As to non-financial performance, five diverse perceptual measures were adopted from Choi and Lee (2003), Chenhall and Langfield-Smith (2007) and Hoque and James (2000) scales.

Four management academicians were consulted to find the second thought on developed measurement scales and rectify any potential deficit. Content validity of the scales was also ensured at this juncture. Simple random samples of 39 managers were employed to clarify the ambiguity of questions and to certify the usefulness of the scale in the investigated context. Throughout the questionnaire, items were measured on ‘Seven-point-Likert-type scales’ ranging from ‘strongly-disagree’ (1) to ‘strongly-agree’ (7). The final questionnaire consists of demographic questions, the independent variables (dynamic capability) and the dependent variables (firm performance). All items are listed in Table 2.

Analytical Strategy

Based on the statistical standards suggested by prior researchers, empirical analysis of the employed data set was initiated with preliminary analysis and exploratory factor analysis (EFA) followed by descriptive statistics, correlation and scale reliability and validity analysis to check the potential biases and data appropriateness (SPSS 21). Subsequently, SEM was directed (AMOS 21) to test the hypothesis.

Preliminary Analysis of the Data (Tests for Potential Biases and Appropriateness of Data)

Preliminary analysis of the employed data set was initiated with the data normality and inconsequentiality of multivariate outliers’ issue. Mahalanobis distance (D2) values, calculated via SPSS 21, reveal the absence of the multivariate outliers in the data set. Data normality was confirmed, following Kline (1998). No statistical variances between survey results via mail and field (Wilks’ lambda = 0.77, p = 0.70) were also verified through MANOVA test. Non-response bias in data was also assessed by comparing early response (first four-month response) and late responses (last three-month response). The t-tests of the group means across the two early and late response groups reveal no significant differences (Wilks’ lambda = 0.72, p = 0.42) and reject a non-response bias (Armstrong & Overton, 1977). The significant difference between the population and employed sample was also rejected at 95 per cent confidence level via Kolmogorov–Smirnov test. Further, given that the measurement scales on employed constructs and sub-constructs were adapted from prior literature, the EFA was piloted for measurement quality estimation, following the standards suggested by Hair, Black, Babin, Anderson and Tatham (2006). The results reveal that all items meet the cut-off value essential for retaining them in measurement scale (Table 2). Additionally, common method bias was calculated via procedural and statistical steps (Podsakoff, MacKenzie, Lee & Podsakoff, 2003). Procedural steps incorporated seriousness in identifying informants, protecting respondent anonymity, balancing the measurement order and fetching information from different managers under different cadre as mentioned earlier. Statistical steps comprised Harman’s single-factor test (Podsakoff & Organ, 1986) and correlation scores (Pavlou et al., 2007).

Exploratory Factor Analysis Results

According to Podsakoff and Organ (1986), all items should be subjected to EFA. From un-rotated factor solutions, if a single factor emerges or else if a first factor describes the majority of the variance in the variables, then a common method bias exists. The analytical results revealed that neither of these situations detained (Table 2). The EFA analysis yielded six factors with no factor describing the majority of the variance (22.38 per cent was the largest variance described by reconfiguration capability). According to Pavlou et al. (2007), among all constructs, the correlation scores should not be above 0.80. The results revealed that all the values meet the criteria (Table 3). So, common method bias is of little issue and no major threat for the present inquiry. Finally, as respondent deals with two levels of management and sample of the study deals with two banking sectors, position and sector bias test were directed across these groups. Results reveal no statistically different measures across these two groups. So, results reveal no biased response patterns across position and sector groups. Thus, the employed data set is free from potential biases and is appropriate for further analysis.

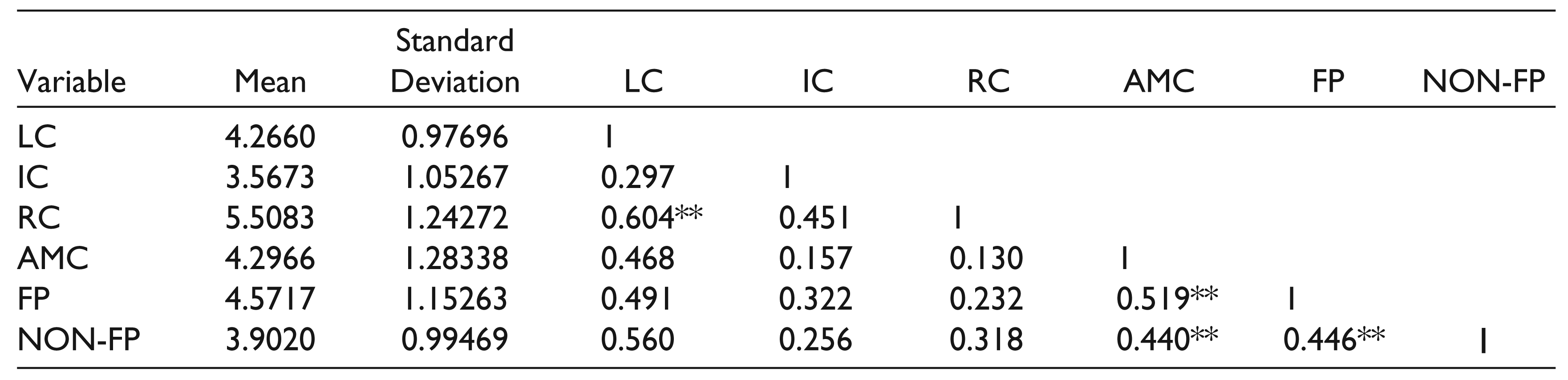

Descriptive Statistics and Correlation

Further, descriptive statistics and correlation among the employed constructs were estimated. Correlation coefficient among the constructs measures the constructs conceptual and empirical distinctiveness and reveals that all employed constructs are distinct. The highest correlation coefficient exists (0.604) between integration and reconfiguration capability (Table 3).

Descriptive Statistics and Correlation Table

Measurement Model, Scale Reliability and Validity Analysis

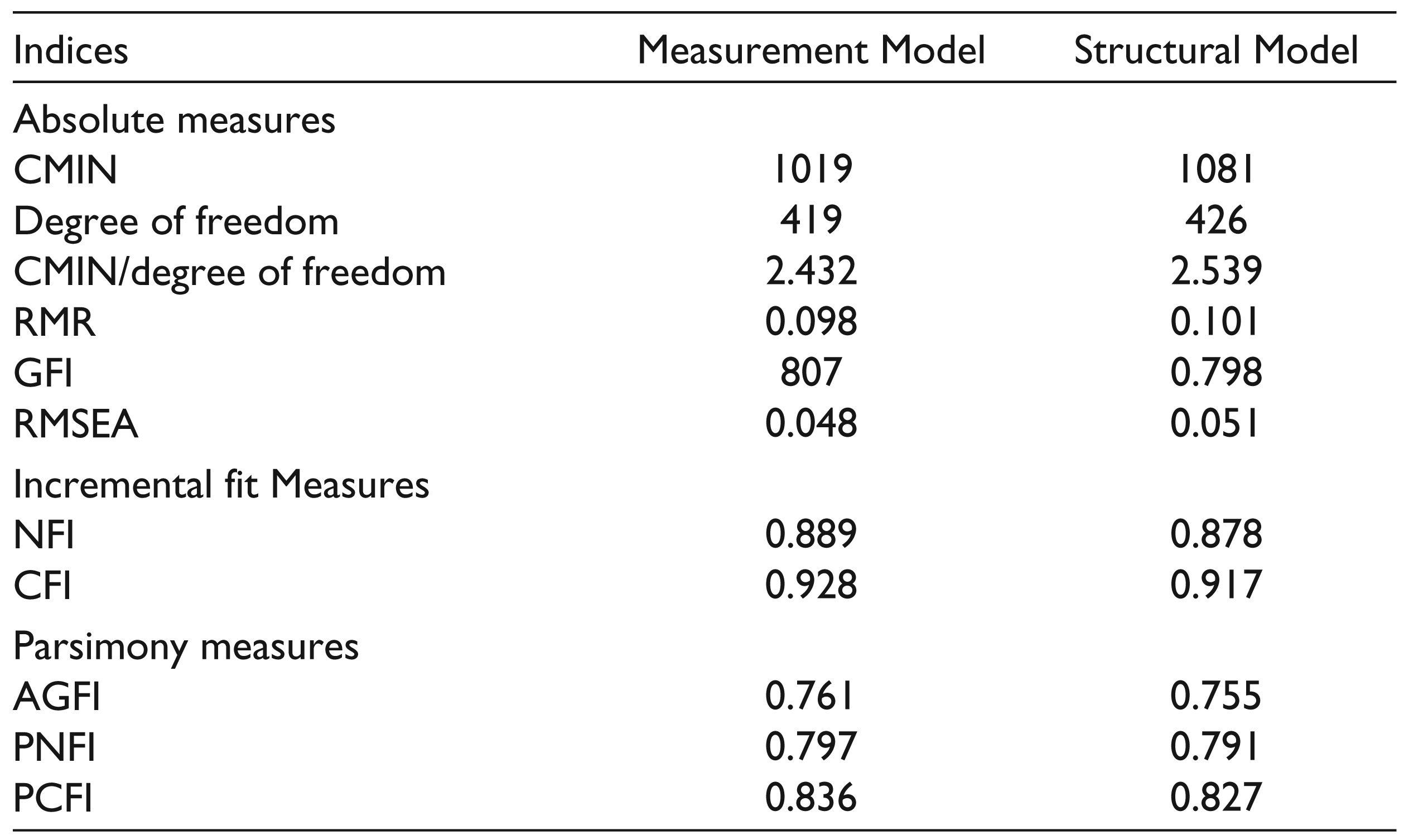

Following Anderson and Gerbing’s (1988) standards, the study proceeds with the estimation of the measurement model and embraces multiple fit indices of diverse categories (absolute, incremental and parsimonious fit indices) based on the recommendation of Bagozzi and Yi (1988), Hair, Black, Babin and Anderson (2009) and Hu and Bentler (1995). The calculated fit indices satisfy the recommended threshold level (Table 4) and confirm the good model fit achieved by the measurement model.

Fit Indices Value

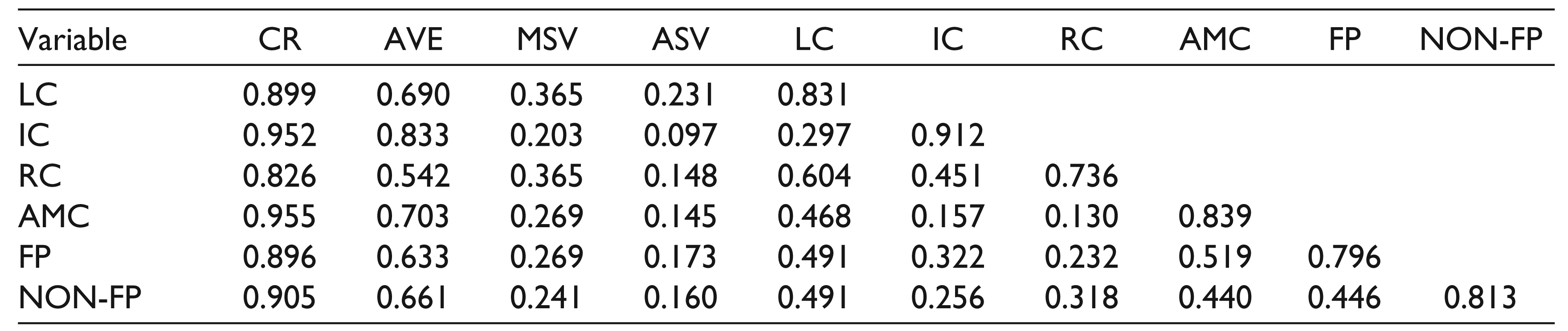

With respect to measurement validity, CFA was directed. Results achieve the suggested threshold level (Tables 2, 3 and 5) and confirm the recommended reliability and validity. Factor loadings for all the values were higher than 0.641, composite reliabilities values were above than 0.826, Cronbach’s alpha (C-α) values were higher than 0.822 and average variance extracted (AVE) values were higher than 0.542. Hence, internal reliability and convergent validity was achieved (Anderson & Gerbing, 1988; Bagozzi & Yi, 1988; Fornell & Larcker, 1981; Hair, Anderson, Tatham & Black, 1998; Pavlou et al., 2007). Further, regarding discriminant validity, four statistical methods suggested by Bagozzi and Baumgartner (1994), Fornell and Larcker (1981), Hair et al. (1998) and Kline (1998) were applied. According to Bagozzi and Baumgartner (1994), the correlations among the constructs should be below 0.7. Compliant with Fornell and Larcker (1981), AVE value of the construct should be greater than the squared correlation of any respective inter-construct correlations. In accordance with Hair et al. (1998), maximum shared variance and average shared variance values of the constructs should not exceed the AVE value. Additionally, in line with Kline (1998), constructs correlations should not be extremely low (<0.1) or extremely high (>0.85). All these criteria were satisfied in results (Tables 3 and 4) and thus discriminant validity was established. Pertaining to the validity, nomological validity was also established to verify the degree to which constructs are related to each other in a manner established by theory.

Structural Model and Testing of Hypothesized Relationships

Given the above-mentioned good measurement model fit, the structural model and relationships were estimated with maximum likelihood estimation (Anderson & Gerbing, 1988). Following the fit indices threshold recommended by Bagozzi and Yi (1988), Hair et al. (2009) and Hu and Bentler (1999), it was confirmed that the estimated fit indices of the structural model recommend a suitable fit to the research data (Table 4), hence paving way for the examination of the four clusters of hypothesized relationship.

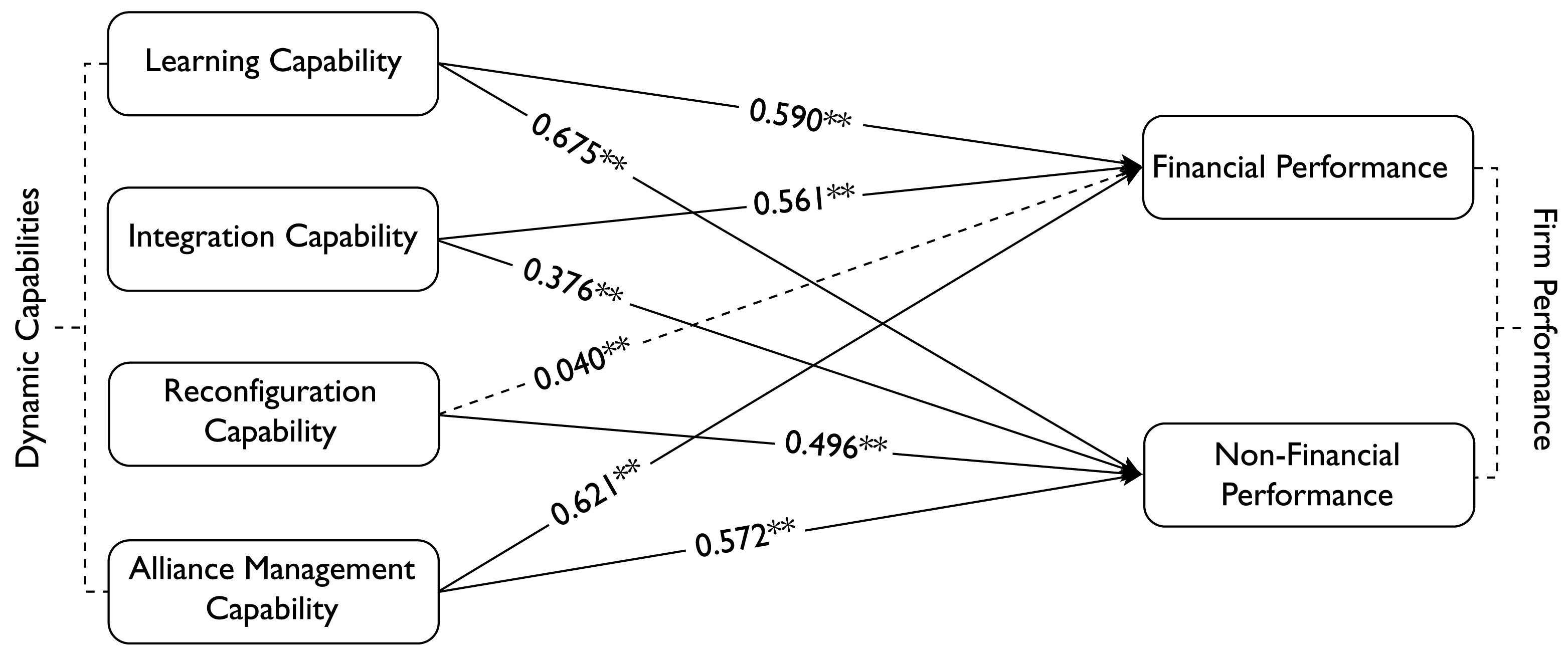

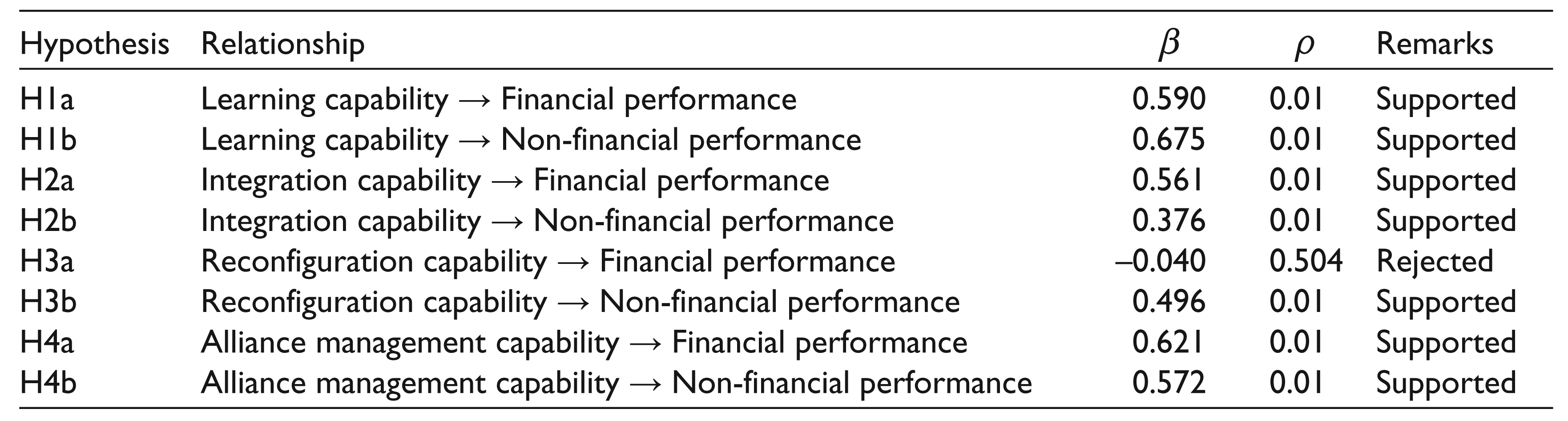

From the testing phase, the statistical significance of every structural parameter value was studied to verify the validity of hypothesized relationship between dynamic capability dimensions and firm’s financial and non-financial performance (Figure 2 and Table 6). From these analytical results, in the first hypotheses cluster, it was confirmed that learning capability has a positive and significant association with financial ( β = 0.590, ρ = 0.00) and non-financial performance of the banking firms ( β = 0.675, ρ = 0.00). In the second cluster, results established that integration capability has a positive and significant association with financial ( β = 0.561, ρ = 0.00) and non-financial performance of the banking firms ( β = 0.376, ρ = 0.00).

Discriminant Validity

In the third cluster, results confirmed that reconfiguration capability has an insignificant association with financial performance ( β = –0.040, ρ = 0.504) and significant association with non-financial performance of the banking firms ( β = 0.496, ρ = 0.00). In the fourth cluster, findings corroborated that alliance management capability has a significant association with financial performance ( β = 0.621, ρ = 0.00) and non-financial performance of the banking firms ( β = 0.572, ρ = 0.00). Thus, the hypotheses H1a, H1b, H2a, H2b, H3b, H4a and H4b were empirically sustained. Conversely, the results do not upkeep the hypotheses H3a because the reconfiguration capability has no association with financial performance (β = –0.040, ρ = 0.504). In other words, in the predicted directions, respective path coefficients are not significant (Figure 2 and Table 6).

Results of Hypothesis Testing

Discussion

The major interest of this article is to determine the association between the dynamic capabilities and performance of the banking firms. Although substantial scholarly submissions have explained the performance implications of dynamic capabilities, this explanation is not fully understood and still surrounds with inadequate findings. Besides, this aspect has never been studied in banking firms, even when it is cited. This inquiry makes contributory steps towards filling this potential gap. From the SEM results, the linkages of dynamic capability and firm performance in Indian banking firms have been spelt out and several key findings are realized.

From the empirical results, learning capability has proven to be significantly influencing the financial and non-financial performance of the investigated banking firms. This outcome is on par with the verdicts from the inquiry of Teece et al. (1997) which confirmed that learning capability enhances firms’ potential to cultivate new and idiosyncratic resources and capabilities mandatory to improve the performance of the firm. This finding is further concomitant with the study of Noruzy (2013), which mentioned that learning capability facilitates learning process and knowledge sharing and in turn enables firms to attain performance. In line with this finding are the studies of Lin and Wu (2014), Lavie (2006), Prieto and Easterby-Smith (2006), Ellinger et al. (2002), Senge (1990) and Zollo and Winter (2002). The findings also reveal that investigated banking firms intensely accentuated on learning capability in which a suitable environment and required training and medium needs to be provided at different managerial levels to support learning process and develop learning capabilities. Thus, reckoned as the most effective mode to cultivate performance, firms will continue to grow and improve the performance, when firms hold learning capability.

Integration capability has also revealed to considerably associate with financial and non-financial performance of the investigated banking firms. The finding from this study corresponds with Teece et al.’s (1997) study in which integration capabilities enhance firm’s performance. Explicitly, this finding is also in line with Tseng and Lee’s (2014) study where integration capability has been established as a strategic factor for deploying firm’s resources, improving sales, revenue, profit and return on investment and others non-financial performance outcomes. Similar suggestion was also made by Iansiti and Clark (1994), King and Tucci (2002), Wu (2006) and Pavlou and El Sawy (2011). From the outcomes, when firms hold capability of integrating resources along with know-hows and competence, they will be able to adapt and respond to fluctuating market environments and correspondingly to survive and enhance their performance.

An additional finding of this study is that reconfiguration capability has a significant influence on firms’ non-financial performance, while no significant relationship was testified between reconfiguration capabilities and financial performance among the investigated banking firms. It depicts that the time and work being financed into reconfiguration capability are deemed ineffective. This can be due to the dynamism in the environments which led frequent changes and create challenges for the firms to update their resources. And for which firms were incapable to clutch or else to apply appropriately. This study contrast the findings of former study of Lin and Wu (2014) and Wu (2006) which confirms that repetitive search of resources reconfiguration is indispensable for enhancing financial performance. However, the study of Protogerou et al. (2011) supported the results in which indirect relationship of dynamic capability and performance was concluded. Whereas in concern with affirmed significant influence of reconfiguration capability on firms’ non-financial performance, the findings of the study are substantiating with the prior studies (Eisenhardt & Martin, 2000; Teece et al., 1997) in which resource transformation capability was mentioned as a key capability to sustain performance in dynamic market context. This verdict is also parallel with Wang and Ahmed (2007), Wu (2006) and Zhou and Wu (2010). These findings suggest that banking firms’ performance outcomes have bearing on their reconfiguration capability investment and possession.

Additionally, a significant association of alliance management capability and financial and non-financial performance of the investigated banking firms has been established. This finding is in parallel with Niesten and Jolink’s (2015) deductions. These findings are also in same line with the studies piloted by numerous scholars in the likes of Kale and Singh (2009), Kauppila (2013), Naqshbandi and Kaur (2011), Rothaermel and Deeds (2006), Schreiner, Kale and Corsten (2009) and Sluyts et al. (2011) which recommend that ability to manage alliances clenches a vital position to promote alliances, realize success and enhance various performance advantages. Verified from the former studies, firms need to actively participate in alliance function and learnings to foster alliance management capability and further augment their financial and non-financial performance. What requires is the proper implementation of alliance management capability.

Thus, analytical results of the present study submit a strong illustrative influence of the sub-model unfolding directional connections from dynamic capabilities to performance. The influence of the linkages between dynamic capabilities and performance also upholds the inferences of former studies of Chein and Tsai (2012), Hsu and Wang (2012), Hung et al. (2010), Lin and Wu (2014), Tseng and Lee (2012), Wu (2006) and Zhou and Wu (2010). In other words, empirical findings support the initial conceptual discussion that submitted the direct influence of dynamic capabilities on firm performance. Additionally, this study is also a contrast of prior studies of Hsu and Sabherwal (2012) and Protogerou et al. (2011) in which direct association between dynamic capability and performance did not exist.

Finally, the relative significance of learning, integration, reconfiguration and alliance management dimensions of dynamic capability to firm’s financial and non-financial performance has also been found. Learning capability plays a dominant role above and beyond that of integration and alliance management dynamic capability in case of financial performance outcome. Integration capability shows a crucial role relatively higher than alliance management dynamic capability exerts. With reference to the non-financial performance, again learning capability plays a vital role more than alliance management, reconfiguration and integration capability. Alliance management and reconfiguration also emerged as contributory factors more significant than integration capability. These quantitative results allowed the inference that with respect to variations in different dynamic capabilities, the respective fluctuation in terms of performance will exist. Learning capability emerged as one of the key priority for banks to augment their performance.

Theoretical Contribution of the Study

The major contribution that this study made is towards the ongoing debate on the dynamic capabilities and performance linkages. Although researchers agree on the performance implications of dynamic capabilities, they debated on direct significance. This study examined this debated association in different geographical and empirical contexts and confirmed the direct effect of dynamic capabilities on performance. Thus, it turns against the doubts articulated by some researchers and makes a significant step (Drnevich and Kriauciunas, 2011; Easterby-Smith et al., 2009; Eriksson, 2014; Helfat et al., 2007).

Explanation of dynamic capability notion in banking industry as a driving factor for performance improvement also makes a valuable contribution in management domain. Although service, biotechnology, semiconductors, knowledge-intensive industries and joint ventures have always been the context for the most dynamic capability research works, it would be equally substantial to explore this notion in more traditional industries unveiling different limitations and features (Easterby-Smith et al., 2009) such as banking industry.

Another contribution this study made is the exploration of dynamic capability constructs in India-like emerging economies more specifically, definition, dimension and performance aspects. Although geographical boundaries of dynamic capability construct have been broadened from Western economy to emerging economies context like China (Lin & Wu, 2014), India-like emerging economies are far behind in the queue. This inquiry authenticates dynamic capability notion in Indian economy context, where the competition, political and legal support, market opportunity and challenges to business entities are very high. Findings of the study will update the academicians and professionals understanding on this concept and further deployment of its value in Indian and similar emerging economies. In this way, this study satisfies Easterby-Smith et al. (2009) and McKelvie and Davidsson’s (2009) call. In addition, the study illuminates the relative significance of different dynamic capabilities for performance enhancement. In case of performance value of alliance management capability and integration capability, this study responds to the calls for further research made by Lin and Wu (2014).

Thus, the study offers a series of deductions to provide practical implications and extend the current state of knowledge.

Managerial Implications of the Study

Banking industry is not an exception to change.

The key practical insight engendered by this inquiry, is that if banking professionals desire to deal with the fast changing business milieu and enhance the performance of the banks, they must be competent to learn new knowledge, reconfigure and integrate their resources and manage their alliance rapidly and efficiently. They should have complete understanding of the value of dynamic capabilities, to take a leading role in the competition. Important thing they need to know the significance of particular type of dynamic capabilities which have high value to achieve the specific benchmark in performance and develop appropriate practices, training and programmes for building them. In this way, they will be able to reinvents themselves to adapt the changing environments and augment performance. Based on empirical analysis, the present study delivers four patterns of insights.

First, as per the role of learning capability for enhancing learning and creating new knowledge, implementation of various practices for instance internally through appropriate Human Resource Management (HRM) practices and training programmes and externally through managing alliances (Fang & Zou, 2010) is recommended. In this manner, banking managers can employ learning capability to acquire, share and apply knowledge, create learning, build new knowledge and competencies, and coordinate their resources and capabilities to derive enhanced firms performance

Second, consistent with the role played by integration capability banking managers are advised to adopt knowledge management processes and practices to nurture learning and build integration capability (Pavlov & Savy, 2011; Tseng & Lee, 2014). It empowers firms to reinvent their capabilities by integrating firm’s resources base and competency stock according to the market dynamism and competitiveness and cashback the market opportunities, address the market dynamism and further to augment firm performance..

Third, banking professionals are suggested to employ various policies and practices, appropriate to build their reconfiguration capability and to make a proper match between firms resources (internal and external both) and changing business milieu. This capability will assists them to renew and redeploy their competence pool to realize the required organizational change in accordance with market demands.

Fourth, the study maintains that the firms with high level of alliance-management capability attain success in improving their performances. Hence professionals should adopt HRM practices and suitable culture to foster alliance-management capability. Overall, this study serves decision makers a base for strategic decision-making regarding specific dynamic capability investment and respective performance improvement. Finally, this study recommends that the bank-managers should leave no stone unturned to cultivate developing dynamic capability for developing and improving the performance of the banks.

Limitations and Future Avenues

Given that this study employed self-reported data with single method study, the possibility of common response bias is raised (Podsakoff et al., 2003). As mentioned by Podsakoff et al. (2003), collecting longitudinal data can be one possible way to avoid this issue. Given the cross-sectional research design, the causality can neither conclusively demonstrate nor dismiss inverse causality. Hence, experimental and longitudinal studies and qualitative research design would be valued to unearth an exhaustive understanding of the association. Furthermore, causality attained at this stage may not be generalizable to other sectors and other economies. It would also be interesting to explore the association in other businesses and economic context. It is also likely that banking firms in different economies will have diverse causality. It could be the potential subject for further investigation to explore how the influence of dynamic capability diverges from those recognized in this study. Later research can also compare between the banking industries of different countries. One potential area could be to emphasize on specific industries and evaluate the model between industries to conclude the impacts of industry on dynamic capabilities and performance.

Paving the way into the new empirical context for dynamic capability, the examination of the model into other knowledge-intensive service industries and mature industries is also open for investigation (Easterby-Smith et al. 2009; Eriksson, 2014). Incorporation of more dynamic capabilities, which may be of abundant significance to high performance, can also update capability performance understanding. The insignificant association of reconfiguration capability and financial performance also needs further exploration. In concern with financial technique, this study employed perceptual measures (reason for this is given). Future study should incorporate objective measures. Concerning non-financial performance measures, future research should employ the balanced scorecard (Sveiby, 1997) or the Skandia navigator (Skandia, 1994) to identify specific type of dynamic capabilities corresponding to performance measures. Furthermore, objective and long-term measures of firms’ performance, such as technical fitness and evolutionary fitness, would be valued as suggested by Helfat et al. (2007) and Teece (2007). Predictors of each type of dynamic capabilities could be questioned in the research model. In addition, political, relational and environmental factors may have significant impact on dynamic capabilities and performance association, as the banking industry is surrounded and influenced by these factors.

Footnotes

Acknowledgements

Authors are grateful to the Indian Institute of Technology, Roorkee for their immense support and are also indebted to bank managers for their insightful comments, encouraging support, during the data collection.

The authors are also grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.