Abstract

The purpose of this study is to examine firms’ motives for reporting fixed assets at revalued amount. The study analysed 30 manufacturing firms listed in Colombo Stock Exchange (CSE) for a period of two years from 2012 to 2013, employing Mann–Whitney U test and bivariate and multivariate logistic regression. It is found that manufacturing firms tend to report their property, plant and equipment (PP&E) at revalued amount, when land and building dominates their fixed assets, and firms whose PP&E is dominated by plant and machinery are inclined towards reporting fixed assets at historical cost. However, all such other factors investigated as firm size, carrying amount of PP&E (ppe), intensity of PP&E (ippe), returns on total assets (roa) and return on equity (roe) fail to explain the accounting choice between cost and revaluation models. The probability for a revaluation to occur, on the other hand, is found to be significantly and positively associated to financial leverage, indicating that highly levered manufacturing firms tend to revalue their assets, may be with the expectation of creating possibilities for additional borrowing. Further, no other variables investigated associate with the probability for a revaluation to occur, though prior researches support such association. Findings reveal that fixed assets revaluation motives may be characterized by the nature of fixed assets and their market dynamics characterized by the nature of economy in which firms operate. Findings also suggest that fair value accounting is relevant to manufacturers with high levels of land and building within their asset structure. Fixed assets revaluation motives may differ across countries which should accordingly be valued by financial analyst and investors. Future research should focus on value relevance of revaluation decision of firms in developing countries. Revaluation decisions should be analysed as first-time revaluation and frequency of subsequent revaluations. This is the first study in Sri Lanka reporting the evidence for fixed asset revaluation motives.

Introduction

International Accounting Standards (IAS) 16—Property, Plant and Equipment (PP&E), which has been fully adopted in Sri Lanka through Sri Lanka Accounting Standards (LKAS) 16 provides that an item that qualifies for recognition, as an asset shall initially be measured at its cost. However, subsequent measurement of an item of PP&E can be either at cost or revalued amount, and firms are entitled to elect from among these two measurement alternatives. According to IAS 16, if a firm chooses to continue reporting an item of PP&E at cost, that PP&E shall be carried at its cost less any accumulated depreciation and any accumulated impairment losses. Alternatively, if a firm elects to revalue its PP&E, the carrying amount of that asset whose fair value can be measured reliably will be its fair value at the date of such revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses. 1

Firms, hence, need to choose the appropriate measurement basis for PP&E, because, as stated by Jana and Marta (2014), the choice of measurement base impacts all accounting information being used for making decisions by investors, creditors, suppliers, employees and other stakeholders. On the other hand, different measurement options carry their own merits and demerits, and vary in terms of cost of their implementation. Historical cost is criticized as to provide irrelevant and outdated information, while reporting at fair value is largely believed to more precisely reflect company’s financial position.

Proponents of fair value accounting maintain that fair values for assets or liabilities echo current market conditions, and hence provide timely information, thereby increasing transparency (Palea, 2014). It has been used to realize a more realistic value for past investments (Rajan, 2002). Reporting the fixed assets at fair value is however costly than reporting at historical cost. Various costs are attached to the assets revaluation decision. 2 Yao et al. (2015) describe to the extent that agency costs relating to fair value estimation may offset the benefits arising from the use of fair value accounting. At the other extreme, fair value accounting is contested as to be irrelevant, misrepresentative and, thereby, unreliable, especially on the grounds of potential market inefficiencies, irrational behaviours of investors and liquidity problems (Palea, 2014).

Therefore, companies may be expected to revalue their PP&E, when the anticipated benefits of revaluation exceed associated costs (Whittred & Chan, 1992). That is, firms elect to revalue their PP&E, when revaluation is a net gain and relevant to information users. Therefore, it is justifiable to assume that costs relating to revaluation are rewarded (Watts, 1977) as firms act rationally. Though there is no conclusive evidence grossly disproving the cost model over the revaluation model, Gaeremynck and Veugelers (1999) hold that revaluation often provides a reliable indication for potential investors. Thus, prior studies have found that revaluation of fixed asset has significant impact on firms’ valuation (Aboody, Barth, & Kasznik, 1999; Barth & Clinch, 1998; Courtney & Cahan, 2004; Easton, Eddey, & Trevor, 1993; Emanuel, 1989; Ghicas, Hevas, & Papadaki, 1996; Jaggi & Tsui, 2001; Standish & Ung, 1982). Iatridis and Kilirgiotis (2012) show that asset revaluation causes favourable effect on firms’ financial plans and position. Further, Cotter (1999) in his study about the relationship between asset revaluations and debt contracting claims that revaluation leads to a reduction of leverage, and it provides credible signals of exit values of assets. However, Gaeremynck and Veugelers (1999) hold that investors weigh revaluation depending upon company assets’ intensity, approach of fair value measurement, geographical area, etc., and is usually associated with investors’ expectations.

Barlev, Fried, Haddad and Livnat (2007) showed that revaluation motives can be related to financial needs, capital intensity and matters in relation to political costs. Thus, academic researchers have shown that motivation for revaluation of PP&E stems from various factors and reasons; some of which include debt contracts or high leverage (Brown et al., 1992; Choi, Pae, Park, & Song, 2013; Cotter, 1999; Iatridis & Kilirgiotis, 2012; Lin & Peasnell, 2000; Whittred & Chan, 1992), poor liquidity (Easton et al., 1993; Lin & Peasnell, 2000), size and fixed asset intensity (Easton et al., 1993; Iatridis & Kilirgiotis, 2012; Jung, Pourjalali, Wen, & Daniel, 2013; Lin & Peasnell, 2000), reserve depletion (Choi et al., 2013; Lin & Peasnell, 2000), issues of bonus shares (Brown et al., 1992; Lin & Peasnell, 2000; Whittred & Chan, 1992), takeover threats (Brown et al., 1992; Lin & Peasnell, 2000; Whittred & Chan, 1992) and foreign operations (Iatridis & Kilirgiotis, 2012), etc. In addition, Lin and Peasnell (2000) have also identified that revaluation decision may be influenced by such economic factors as strike frequency, tightness of lending agreements, indebtedness, raising new debt, declining operating cash flow, growth prospects, existence of assets which can be revalued and prior revaluation pattern.

Pinto and Pais (2015) report that accounting choice may be employed by managers in a strategic way in periods of greater pressure. It is, therefore, possible that the decision of assets revaluation may be used for a management opportunism and as an alternative means to manipulate earnings. Missonier-Piera (2007), therefore, argues that there is worthy reason to inquire the motivations behind this accounting practice, as asset revaluation carries no direct impact on cash flow of the firm while there are implementation costs. In the context that firms have discretion over the adoption of either option for measuring their PP&E and to decide upon the frequency of revaluation, if revaluation is opted as measurement of PP&E, the motives behind such discretions become as a matter of investigation. Besides, Barlev et al. (2007) show that the incentives for and effects of revaluation are not uniform across various country classifications. This argument necessitates the testing of management’s motives for fixed assets revaluation in different countries. Barać and Šodan (2011) state that prior studies in this subject were mainly conducted in developed and market-oriented economies. It may, therefore, be worthwhile to understand the revaluation motives of firms in Sri Lanka as a developing economy.

The remaining sections of this study have been organized as follows: the first to come is a review of literature that mainly outlines theoretical framework form which hypotheses are developed. The next section provides a description of methodology and specification of empirical models to test the hypothetical relationship between the variables. The fourth section describes the results and findings followed by the final section concluding the study with its managerial implications, limitations and future scope of research.

Review of Literature and Hypothesis Development

Accounting for Property, Plant and Equipment

LKAS 16—PP&E, reflecting its international counterpart IAS 16, defines property, plant and equipment as ‘tangible items that are held for use in the production or supply of goods or services, for rental to others, or administrative purposes and are expected to be used during more than one period’. It normally includes such fixed assets as land and buildings, plant and machinery, furniture, office equipment, computers, fixtures and fittings, and motor vehicles.

According to IAS 16 and LKAS 16, the cost of an item shall be recognized as PP&E, if it is likely that future economic benefit from that item would flow to the entity for more than one accounting period, and the cost of the item can be measured reliably. An item of PP&E that meets the requirements for recognition as an asset shall be measured at its cost at the initial recognition. However, for measuring the PP&E after its recognition (i.e., to subsequently carry the amount in financial position statement), an entity shall choose between either the cost model or the revaluation model as its accounting policy. The standard requires the firm to apply such preferred policy to an entire class of PP&E. The cost of an item of PP&E represents the cash price equivalent at the recognition date. Upon the payment deferred beyond usual credit terms, the difference between the cash price equivalent and the total payment shall be recognized as interest over the period of credit unless such interest is capitalized in accordance with LKAS 23—Borrowing Cost. However, if a firm acquires a PP&E through an exchange for any non-monetary asset or assets, or a combination of both, the cost of such an item of PP&E shall be measured at fair value except (a) the exchange transaction results in lacking commercial substance or (b) the fair value of neither the asset received nor the forgone is reliably measurable. The item acquired shall be subject to this rule, even if an entity cannot immediately derecognize the asset given up. If the acquired item is not measured at fair value, its cost is measured at the carrying amount of the asset given up. If an entity had chosen to adopt revaluation model for measuring its PP&E after the initial recognition at cost, it can do so for any class of item of PP&E whose fair value can be measured reliably. Revalued amount of PP&E will be its fair value at the date of the revaluation less any subsequent accumulated depreciation and subsequent accumulated impairment losses. Revaluations need to be made with sufficient regularity to ensure that the carrying amount does not differ materially from that would be determined using fair value at the end of the reporting period.

Motivations to Revalue

Firm Size and Revaluation

Many researches investigating the motives for revaluation find a significant relation between PP&E revaluation and company size. According to Watts and Zimmerman (1986) large companies are politically more sensitive than small companies and large companies are more likely to revalue in order to show a conservative picture of profitability, thereby lowering the attention of the press and government. Reflecting this position, there are studies that report a positive relationship between the choice to revalue PP&E and size of the firms (e.g., Barać & Šodan, 2011; Barlev et al., 2007; Brown et al., 1992; Jung et al., 2013; Lin & Peasnell, 2000). Large firms get more attention in the capital market and would, therefore, be more likely to reveal more information. Similar argument would apply for firms that have foreign operations and foreign financial exposure (Mubarak & Hassan, 2006). In a similar vein, firms that operate internationally tend to provide higher levels of disclosure, especially when they display higher debt ratios and need to report to their creditors (Zarzeski, 1996). Firms resort to upward revaluations in an effort to present a favourable financial situation, and attract investors and reinforce their investment opportunities (Missonier-Piera, 2007). Firms tend to be eager to report upward revaluations but reluctant to report downward revaluations, in which case they might argue that any downward revaluations are temporary and not likely to occur in the future. Since an upward asset revaluation can provide firms with the ability to equalize their book value with their market value, it can be assumed that it may also reduce the possibility of undervalued bids. Firms with low fixed assets would be more inclined to perform fixed asset revaluations. Iatridis and Kilirgiotis (2012) claim that smaller firms have low fixed assets, thereby higher returns on total assets (roa) and more need for capital. Their tendency to borrow more and retain their earnings would urge them to perform fixed asset revaluations. Iatridis and Kilirgiotis (2012) also provide that large and financially visible firms exhibit higher growth and capital needs, and would, therefore, tend to perform fixed asset revaluations in order to reinforce their financial position and market picture. In the context of these arguments, this study hypothesizes that total asset (toa) significantly determines the firms’ decision to account their fixed assets at revalued amount (H1).

Intensity of Assets and Revaluation

The property prices have been increasing in recent years; the disparity between the book value and the fair value will be greater for property than for other PP&E items (Brown et al., 1992). Therefore, companies will tend to revalue PP&E only, when they gain net advantage. Net gain out of revaluation may not be possible, if the size of the PP&E is small. According to Brown et al. (1992), the potential benefits arising from a revaluation would be greater for companies with larger PP&E. Jung et al. (2013) implies that amount of non-financial assets positively relates towards CFO’s fair value option for non-financial assets. Carrying amount of PP&E is, therefore, hypothesized to significantly determine the firms’ decision to report their fixed assets at revalued amount (H2). Choi et al. (2013) report that land is preferred for revaluation than other depreciable assets. They also add that companies are likely to select depreciable assets for revaluation only after they select land. Land and buildings generally represent a larger proportion of PP&E, and may, therefore, be likely to determine the management motives for revaluation of fixed assets. The present research, thus, seeks to investigate whether intensity of land and building (ilb) significantly determines fixed assets revaluation decision (H3), and whether the intensity of plant and machinery (ipm) significantly determines the fixed assets be revalued (H4). Further, Cheng and Lin (2009) also show that revaluers have significantly higher fixed asset intensity. This informs that companies with higher ratios of PP&E to total assets (PP&E intensity) are more likely to revalue PP&E than those with lower PP&E intensity. This study also, therefore, predicts that intensity of PP&E (ippe) significantly influences the reporting of fixed assets at revaluation (H5).

Leverage and Revaluation

Many studies have found a positive relationship between revaluation and financial leverage and debt covenants (e.g., Brown et al., 1992: Lin & Peasnell, 2000; Whittred & Chan, 1992). Lin and Peasnell (2000) found that upward revaluations of fixed assets positively relate to gearing and debt covenants. It is, thus, expected that firms with high incidence of financial leverage may be more inclined towards revaluing their fixed assets, thereby archiving a reduction in debt ratio leading to an enhanced borrowing capacity. The firm’s debt-to-asset or debt-to-equity ratios are improved, when the revaluation of fixed assets positively impacts the book value of total assets and the asset revaluation reserve, thereby resulting a strong financial position leading to reduction in debt restrictions or interest charges. It was, thus, argued that firms are more likely to undertake assets revaluation, when the financial leverage level is high in their statement of financial position (Lin & Peasnell, 2000). Whittred and Chan (1992) investigated revaluations of Australian companies during the period of 1980–1984 and found that opportunities for a company to grow constraints posed on borrowing and amount of cash reserves were behind the revaluation decision. Further, Brown et al. (1992), who also examined the motives for revaluation choice in Australia during the high and low inflationary periods, found that companies revalue normally when they are subject to higher debt-to-asset ratios, higher fixed-asset intensity and lower tax-free reserves than non-revalues. Whittred and Chan (1992) and Brown et al. (1992) found that Australian companies are more likely to revalue their PP&E, when they are highly levered.

Companies revalue PP&E to enhance their borrowing capacity (Cotter & Zimmer, 1995; Jaggi & Tsui, 2001), when they anticipate the need to raise capital in the future. Companies that encounter this constraint and in need of future financing are motivated to increase their bond issuing capacity through assets revaluations. Similarly, a survey finding of Easton et al. (1993) also revealed that companies revalue PP&E mainly to lower financial leverage. Jung et al. (2013) analyses the responses of 209 CFOs of US firms, and report that CFOs in the US are resistant to fair value option for non-financial assets and that the factors such as firm size, leverage, the amount of non-financial assets, and expertise in fair value measurements positively affect the CFOs’ responses to fair value option for non-financial assets. Choi et al. (2013) suggest that Korean companies are more likely to revalue PP&E to improve their financial position or reduce debt contracting costs rather than to reduce political costs or to signal better future prospects. Choi et al. (2013) also report that revaluation companies are more likely to elect depreciable classes of PP&E, when they are highly levered, experience equity depletion and report losses. Therefore, revaluation is also sought to lower the contracting costs of companies facing constraints in mobilizing debt capital. Revaluation remedies this situation and leads to an improvement in financial leverage. This study, hence, predicts that financial leverage (lev) significantly determines the firms’ decision to measure their fixed assets at revalued amount (H6).

Profitability and Revaluation

According to Barlev et al. (2007), companies with potential for more favourable future prospects tend to revalue their PP&E. They argue that asset revaluation is detrimental to the current and future roa due to an increase in the asset base and subsequent increased depreciation charges when depreciable assets are revalued upwards. The current earnings also decrease, when the revaluation gives rise to a decrease in value for some items in the chosen class of PP&E. Hence, Barlev et al. (2007) assumed that companies that forecast better future performance can afford to revalue. Barać and Šodan (2011) analyses Croatian-listed companies and show that profitable companies with low liquidity ratio, low cash flow ratio and increasing debt are more likely to perform upwards revaluation. Gaeremynck and Veugelers (1999), in contrast, argue that revaluation signals poor performance or closeness to debt constraints of firms. Choi et al. (2013) also suggest that revaluing companies are likely to choose their depreciable classes of PP&E, when they report losses. Unsuccessful companies make use of the opportunity to revalue the PP&E in the expectation of enhancing their borrowing capacity or in the endeavour of restructuring the firm followed by violation of debt covenants. Accordingly, they claim that successful companies can distinguish themselves from less successful companies by electing not to revalue PP&E. This study, therefore, holds the hypothesis that revaluation is also dependent on the firms’ financial performance measured by roa (H7) and return on equity (roe; H8).

The objective of the present study is, therefore, to investigate the impact of firm size, fixed assets and its intensity, financial leverage and profitability in determining Sri Lankan firms’ decision to measure their fixed assets at revalued amount.

Methodology

Data

This study was conducted among the companies listed in the Colombo Stock Exchange (CSE) in manufacturing sector. When this research was conducted, there were 294 companies belonging to 20 sectors listed in the CSE, and out of which there were 36 companies operating in manufacturing sector. Except for 6 companies having incomplete data, all other 30 firms in manufacturing sector were taken for this analysis. The study covers two years of 2013 and 2012, and the data of selected firms were obtained from the publicly published annual reports of the firms.

Variables

The independent variables in this investigation are total assets (toa), carrying amount of PP&E (ppe), intensity of land and building (ilb) measured by carrying amount of land and building divided by carrying amount of PP&E, intensity of plant and machinery (ipm) measured by carrying amount of plant and machinery divided by carrying amount of PP&E, ippe measured by carrying amount of PP&E divided by total assets, financial leverage (lev) measured by debt-to-equity ratio, return on assets (roa) calculated as profit after taxation divided total asset and returns on equity (roe) calculated as profit after taxation divided by book value of equity.

Firms’ decision to measure their fixed assets at revalued amount is the dependent variable and analysed in two dimensions: the first dimension is that firms’ accounting choice between cost and revaluation models for accounting their PP&E; and the second dimension is that the probability for a revaluation to occur in a given accounting year. These two dimensions are, thus, constituted as two dependent variables, which are ‘the management’s choice between either cost or revaluation model for accounting PP&E’ which is notated by δ sign and ‘the management’s decision to revalue PP&E in years under review’ which is denoted by σ sign. Accordingly, δ has two possible values—either 1 or 0—where 1 is assigned for the firms that use revaluation model. Revaluation of at least a single class of fixed assets at least once during or before the periods under study is considered enough for a firm to be designated as to follow revaluation model. Conversely, 0 is assigned for the firms adopting cost model. Similarly, dependent variable σ also has two possible values—either 1 or 0—where the firms that revalue its PP&E in the year under review (occurrence of revaluation) take the value of 1 and 0, if the firm did not revalue its PP&E in a given year (non-occurrence of revaluation).

The information about firms’ accounting policy choice between revaluation and cost model, and the information about whether there has been a revaluation of fixed assets during the year under observation have been obtained by reviewing financial statements and note disclosures thereof. Firms recognize revaluation surplus/loss in the statement of comprehensive income and accumulate it in revaluation reserve in statement of movement in equity. Firms have also disclosed the details of their revaluation activities in the notes to financial statements.

Empirical Models

This study employs both univariate and multivariate methods to test the research hypotheses. Univariate analysis is sought to evaluate the relationships between an individual explanatory variable and a dependent variable. As most of the variables are not normally distributed, Mann–Whitney U test has been employed, as it tests for differences in the explanatory variables between two different groups. The study also employs logistic regression for performing bivariate and multivariate tests. Logistic regression does not rely on the assumption of normal distribution of data and uses maximum likelihood method rather than the ordinary least squares estimation. It is predominantly useful for situations in which the dependent variable is dichotomous. Dependent variables of the present study are dichotomous whereby dependent variable denoted by δ takes two possible values—either 1 or 0—where 1 designates that firms use revaluation model and 0 is assigned for the firms adopting cost model. Similarly, dependent variable σ may take either 1 or 0, and it is 1, if a revaluation occurs in the year under review and 0 otherwise. Logit (p) is the log (to the base e) of the odds ratio or likelihood ratio that the dependent variable is 1. Logit (p), in relation to the dependent variables δ and σ, can be illustrated as:

where p(δ) is the probability that a firm in manufacturing sector chooses revaluation model to account their fixed assets and p(σ) is the probability for a revaluation to occur in the year under review.

Bivariate regression models seek to test hypothetical relationship between a dependent variable and each independent variable separately. Bivariate logistic regression models in relation to each hypothesis under investigation can be represented as:

Multivariate regression models in relation to δ and σ can be represented as:

where, p(δ) is probability that a firm in manufacturing sector chooses revaluation model to account their fixed assets, p(σ) is the probability for a revaluation to occur in the year under review, toa is total assets, ppe indicates carrying amount of PP&E, ilb intensity of land and building in PP&E, ipm is intensity of plant and machinery in PP&E, ippe denotes intensity of PP&E, lev is financial leverage, roa is return on assets and roe is return on equity.

Results and Discussion

Descriptive Statistics

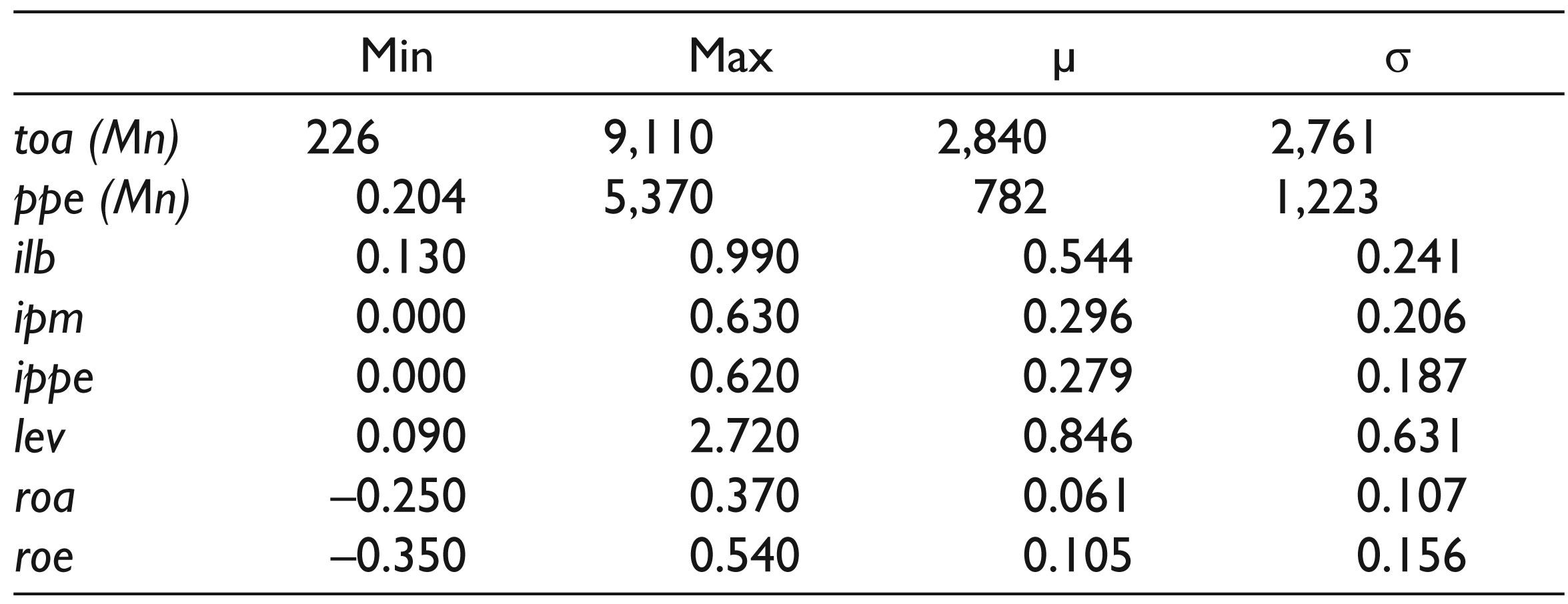

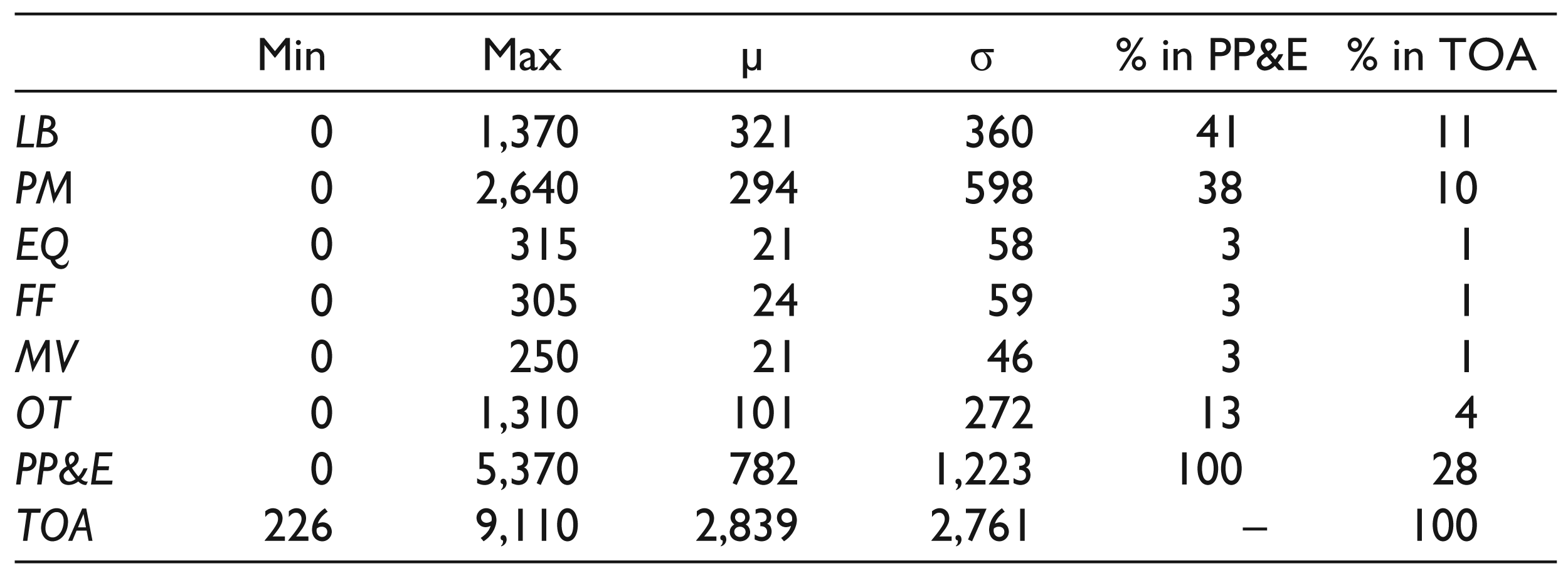

Descriptive statistics related to the independent variables of this study are provided in Table 1. Accordingly, the average total assets of a firm in manufacturing sector during the periods under review is approximately Sri Lankan Rupees (LKRS) 2,840 million, out of which an average of LKRS 782 million is the carrying amount of PP&E (proportion of PP&E in the total asset is termed as ippe, which is nearly 28 per cent). Companies in manufacturing sector in Sri Lanka have predominantly grouped their PP&E into main categories of land and building, plant and machinery, equipment, furniture and fittings, motor vehicle and others. From Table 2, about 41 per cent of the total PP&E belongs to land and building (which is 11 per cent in total assets), while 38 per cent constitutes to plant and machineries (which is 10 per cent in total assets), and both together make up about 79 per cent of the total PP&E. Other descriptive statistics related to the PP&E and its components are given in Table 2.

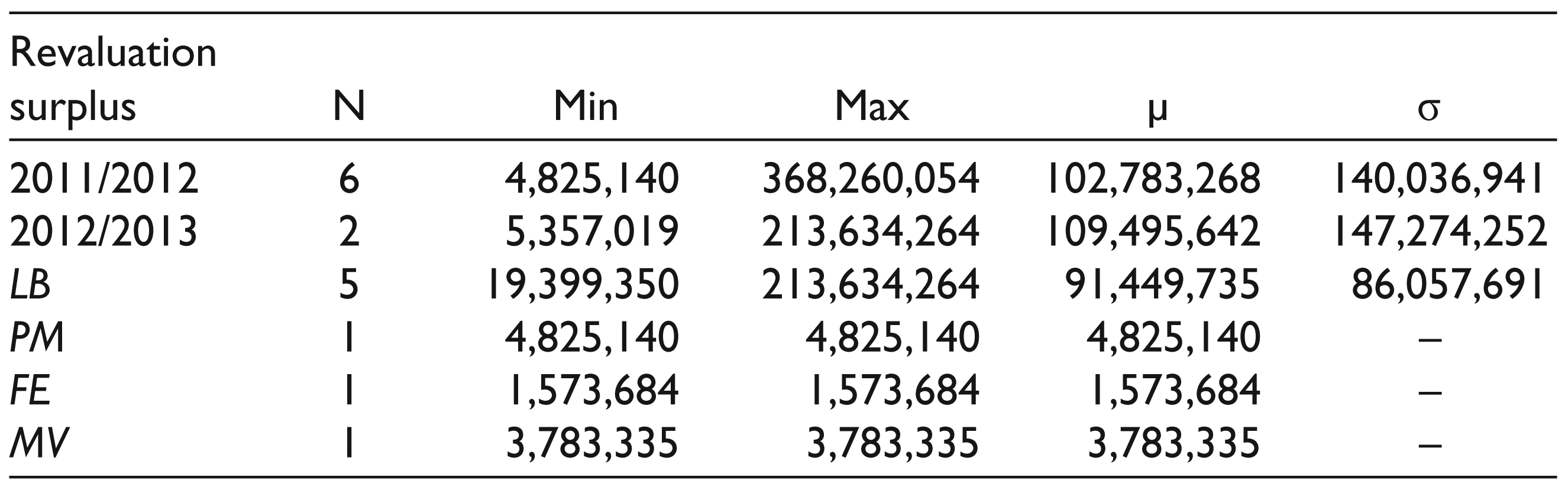

Out of 60 firm-year observations, only 8 revaluations had occurred during the years of the study, which represent nearly 13 per cent out of the total observations. As summarized in Table 3, 6 revaluations have occurred in the year 2011/2012, and it is 2 in the financial year 2012/2013. Out of 8 revaluation activities during the period under review 5 revaluations are related to land and building, while each such other category of assets as plant and machinery, furniture and equipment, and motor vehicles has been revalued only once out of 60 observations. All revaluations in the years under review have resulted in revaluation surplus.

Descriptive Statistics for Independent Variables

Descriptive Statistics: Intensity of PP&E and Its Components (All amounts are in millions)

Revaluation Surpluses

In manufacturing sector in Sri Lanka, maximum and minimum revaluation surplus are LKRS 368.2 million and LKRS 4.8 million, respectively in the year 2011 and 2012, and LKRS 213.6 million and LKRS 5.3 million, respectively during the year 2012 and 2013. The mean revaluation surplus amount is nearly LKRS 102.7 million in the year 2011/2012 (which is 14.26 per cent in the average carrying amount of PP&E in manufacturing sector in that year) and LKRS 109.4 million in the year 2012/2013 (which is 12.98 per cent in the average carrying amount of PP&E in manufacturing sector in that year).

Correlation Results

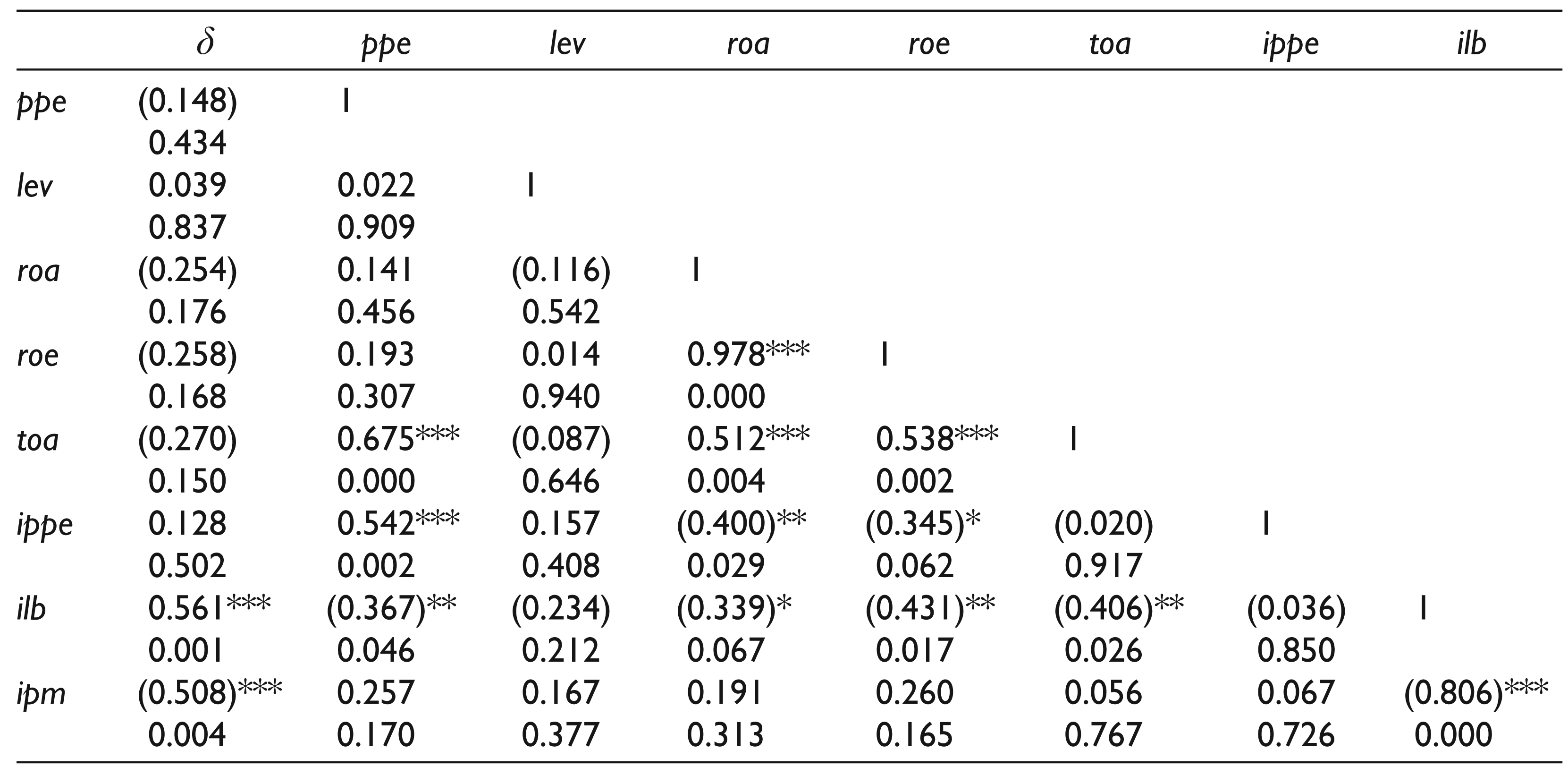

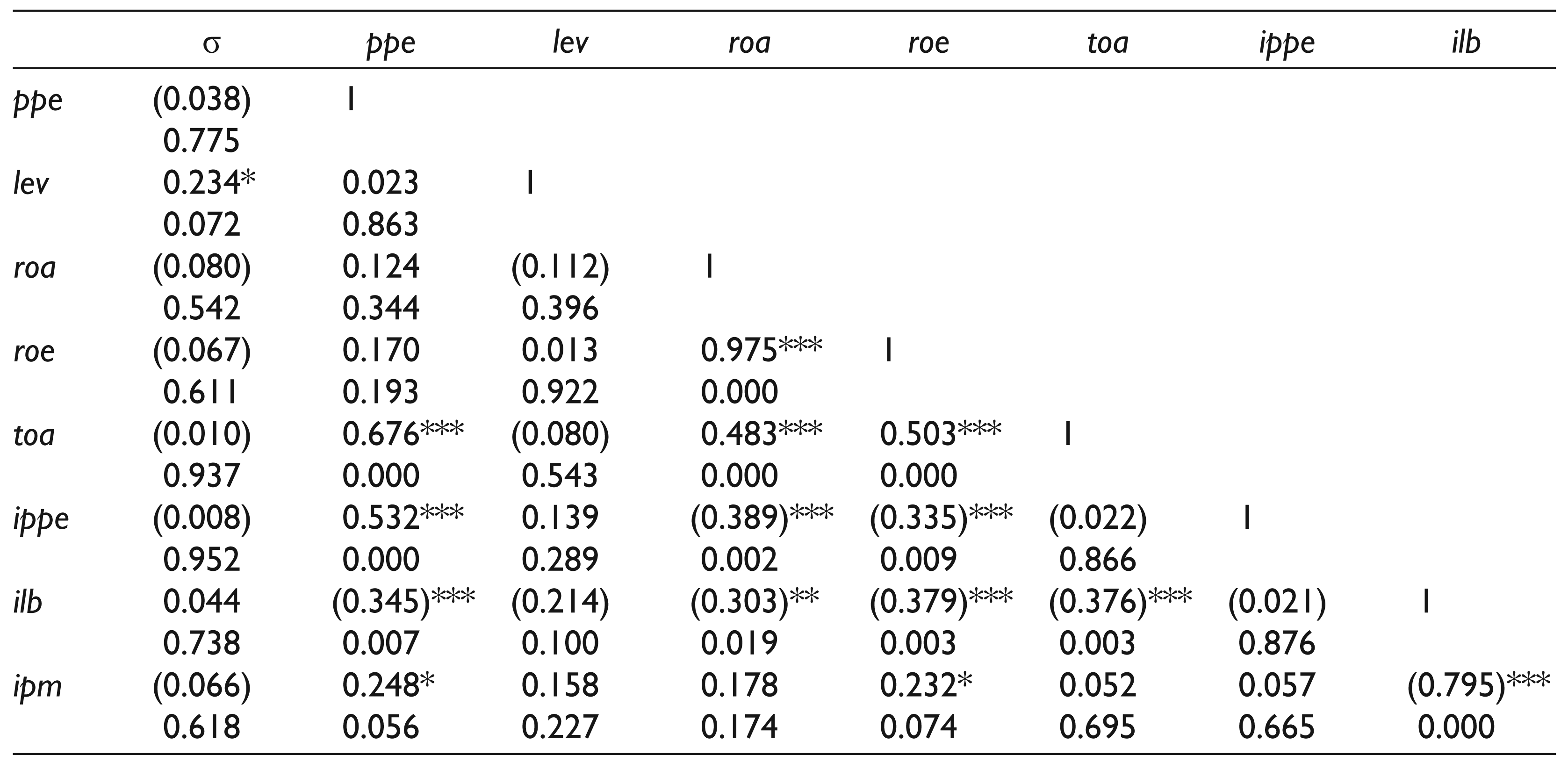

Pearson Correlation results presented in Table 4 have been obtained by correlating the independent variables and the dependent variable denoted by δ (i.e., management’s choice of accounting policies of revaluation model or cost model to measure PP&E after its recognition), and correlation results presented in Table 5 are pertinent to the association between independent variables and the dependent variable denoted by σ (i.e., occurrence of revaluation). Accordingly, δ, the choice of firms’ accounting policy to account PP&E at cost or revalued amount, that is, the occurrence of a revaluation, is significantly and positively correlated with intensity of land and building in PP&E measured by carrying amount of land and building divided by the total carrying amount of PP&E (r = 0.561, p = 0.001). Further, the intensity of plant and machinery in PP&E measured by carrying amount of plant and machinery divided by the total carrying amount of PP&E is significantly and negatively correlated with δ (r = –0.508, p = 0.004). This demonstrates that ilb and ipm are the two significant factors that associate with firms’ accounting choice between cost and revaluation models to account PP&E. The adoption of revolution model is significantly associated with firms with higher intensity of land and building, while the adoption of cost model significantly associates with firms with higher intensity of plant and machinery. Further, the variable δ has shown no significant relationship with other such factors as ippe, lev, roa and roe.

Pearson Correlation Matrix: Model Choice and Independent Variables

2. δ is a dependent variable in this study which stands for the management’s choice between either cost or revaluation model for accounting PP&E.

3. δ = 0, if the firm under observation uses cost model, and δ = 1, if the firm under observation uses revaluation model.

4. Negative r values have been provided in parenthesis.

5. *** Statistically significant at 1% level (2-tailed).

6. ** Statistically significant at 5% level (2-tailed).

7. * Statistically significant at 10% level (2-tailed).

8. ppe is carrying amount of PP&E, lev is financial leverage calculated by total debt-to-equity ratio, roa is return on assets obtained by profit after interest and tax divided by total assets, and roe is return on equity calculated by profit after interest and tax divided by total equity capital, toa is the total assets, ippe represents intensity of PP&E measured by its carrying amount divided by total assets, ilb represents intensity of land and building measured by carrying amount of land and building divided by carrying amount of PP&E, ipm refers to intensity of plant and machinery measured by carrying amount of plant and machinery divided by carrying amount of PP&E.

Pearson Correlation Matrix—Occurrence of Revaluation and Independent Variables

2. σ is another dependent variable in this study which stands for management’s decision to revalue PP&E in years under review.

3. σ = 0, if the firm under observation did not revalue any item of its PP&E in the year under review, and σ = 1, if the firm under observation revalued any item of its PP&E in the year under review.

4. Negative r values have been provided in parenthesis.

5. *** Statistically significant at 1% level (2-tailed).

6. ** Statistically significant at 5% level (2-tailed).

7. * Statistically significant at 10% level (2-tailed).

8. ppe is carrying amount of PP&E, lev is financial leverage calculated by total debt-to-equity ratio, roa is return on assets obtained by profit after interest and tax divided by total assets, and roe is return on equity calculated by profit after interest and tax divided by total equity capital, toa is the total assets, ippe represents intensity of PP&E measured by its carrying amount divided by total assets, ilb represents intensity of land and building measured by carrying amount of land and building divided by carrying amount of PP&E, ipm refers to intensity of plant and machinery measured by carrying amount of plant and machinery divided by carrying amount of PP&E.

Besides, as shown in Table 5, the probability for a revaluation to occur in the years under review is positively correlated with financial leverage at the significance level of 10 per cent (r = 0.234, p = 0.072), and it is not significantly associated with such other independent variables as ppe, roa, roe, toa, ippe, ilb and ipm (see Table 5). This positive and significant association with financial leverage indicates that occurrence of revaluation significantly associates with firms experiencing relatively higher financial leverage.

Univariate Analysis

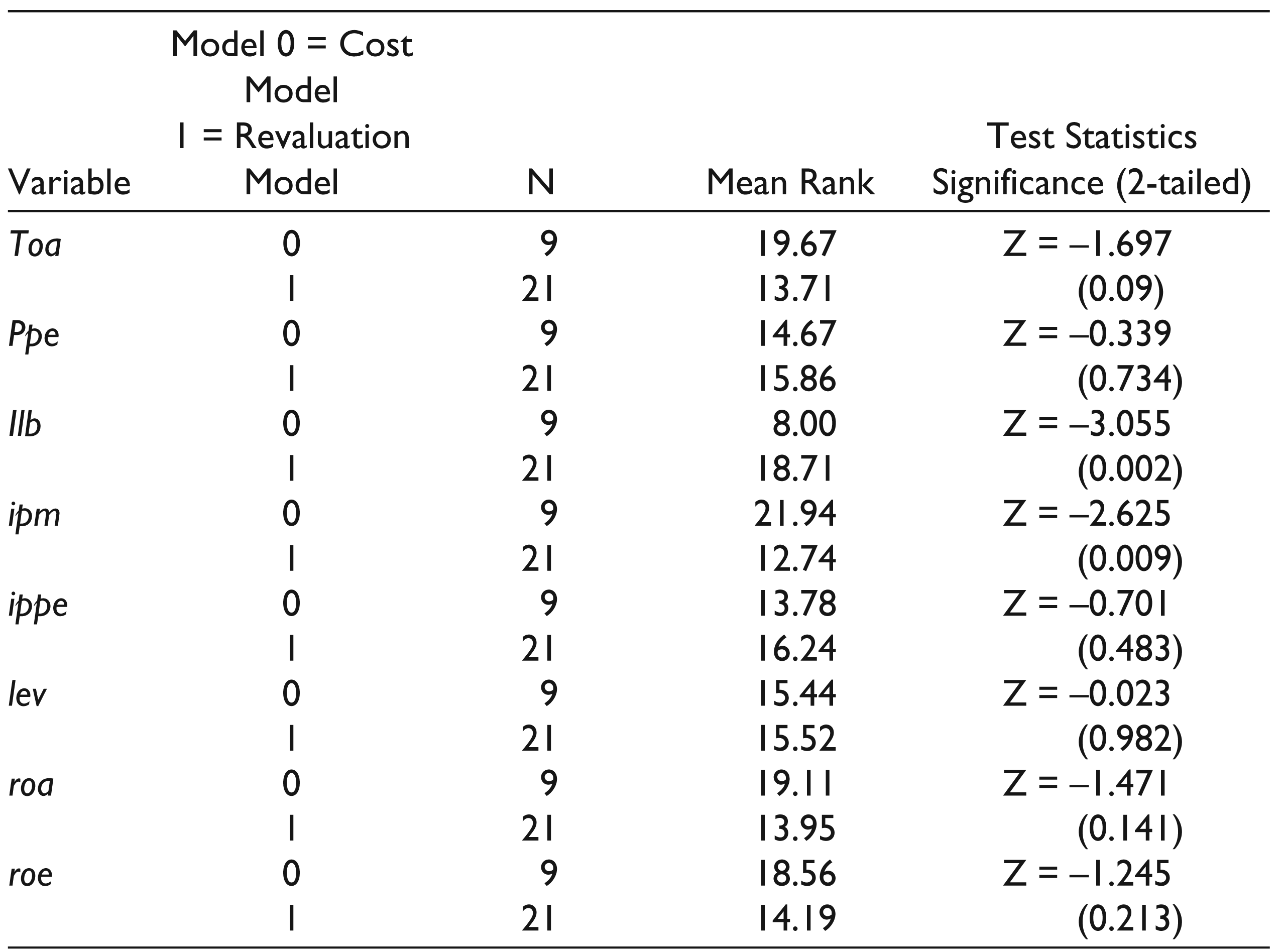

The Mann–Whitney U test is carried out on 30 manufacturing firms that have been grouped into two; those maintaining cost model and those that have adopted revaluation model for accounting their PP&E. The results are summarized in Table 6. The results showed that the two such measures as intensity of land and building (ilb) and intensity of plant and machinery (ipm) are statistically significant at the 0.01 level. Total asset is significant at 10 per cent level. All the other variables are not found to have significant relationships with the choice on model to account PP&E. Univariate analysis, thus, confirms that ilb and ipm are the two significant factors that underlie firms’ accounting choice between cost and revaluation models to account PP&E, thereby maintaining the finding that firms with higher intensity of land and building tend to adopt revaluation model, while firms with higher intensity of plant and machinery adopt cost model.

For the purpose of revealing the factors that underlie the occurrence of revaluation in a given year, all observations corresponding to the research periods were pooled. The estimation precision is said to enhance due to the increase in sample size, when observations are pooled across a relatively short period (two years for this study) and the non-stationary problem should not be serious for the pooling method (Brown et al., 1992). Anderson and Zimmer (1992), as supported by Seng and Su (2010), asserted that accounting choices are temporally independent in each year and, therefore, the pooling method is reliable for research on accounting choice. The Mann–Whitney U test is, hence, performed on the pooled sample of 60 firm-year observations to uncover the factors that underlie management’s decision to revalue PP&E in years under review. Table 7 presents the Mann–Whitney U test results on the pooled sample. Accordingly, all independent variables are not significantly related to management’s decision to revalue PP&E in years under review.

Univariate test–Mann–Whitney U Test for Model Choice (Revaluation Model or Cost Model)

Univariate Test–Mann–Whitney U Test for the Occurrence of a Revaluation. Pooled Data Analysis (2011/2012–2012/2013)

Logistic Regression

Bivariate Analysis

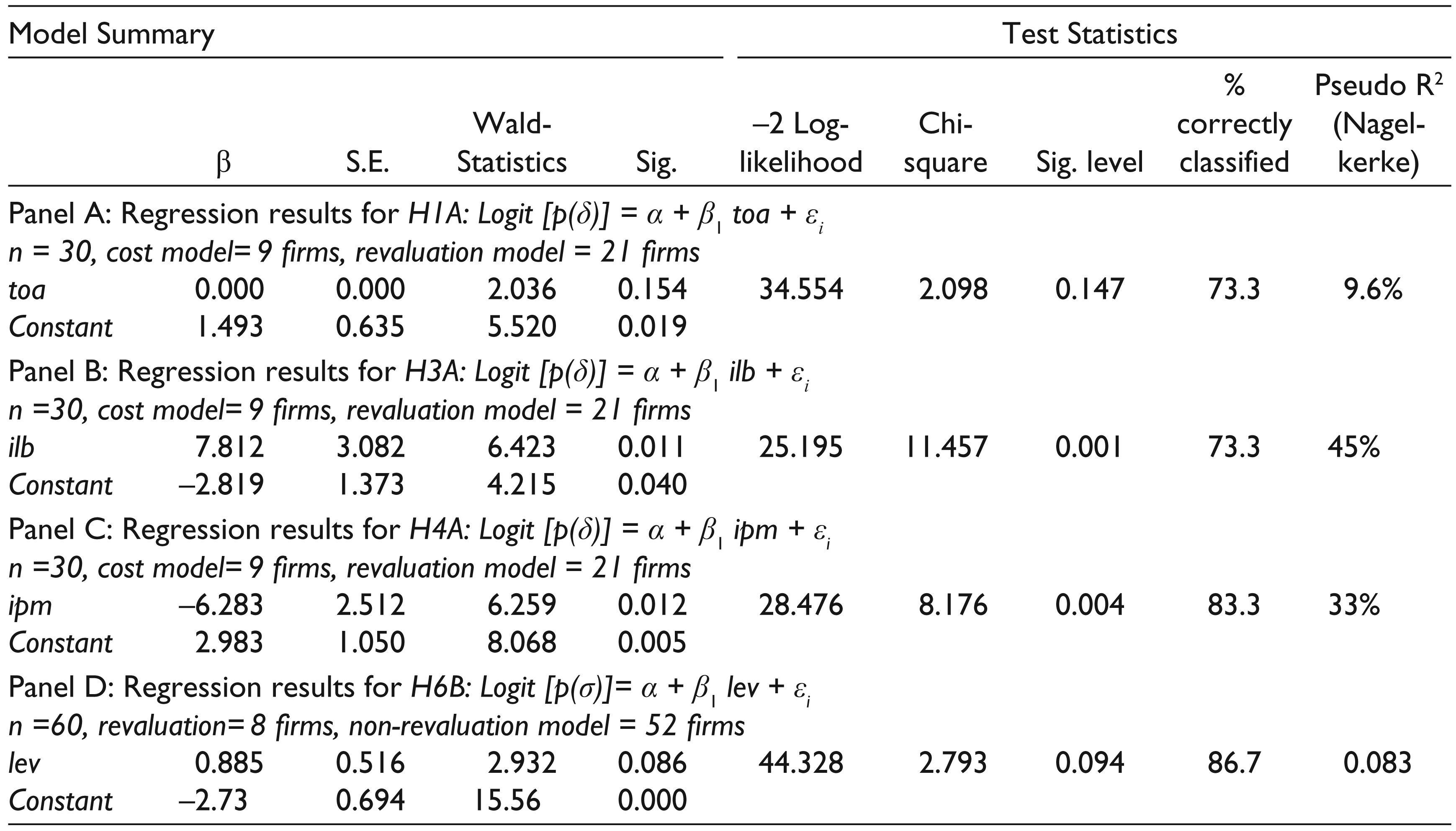

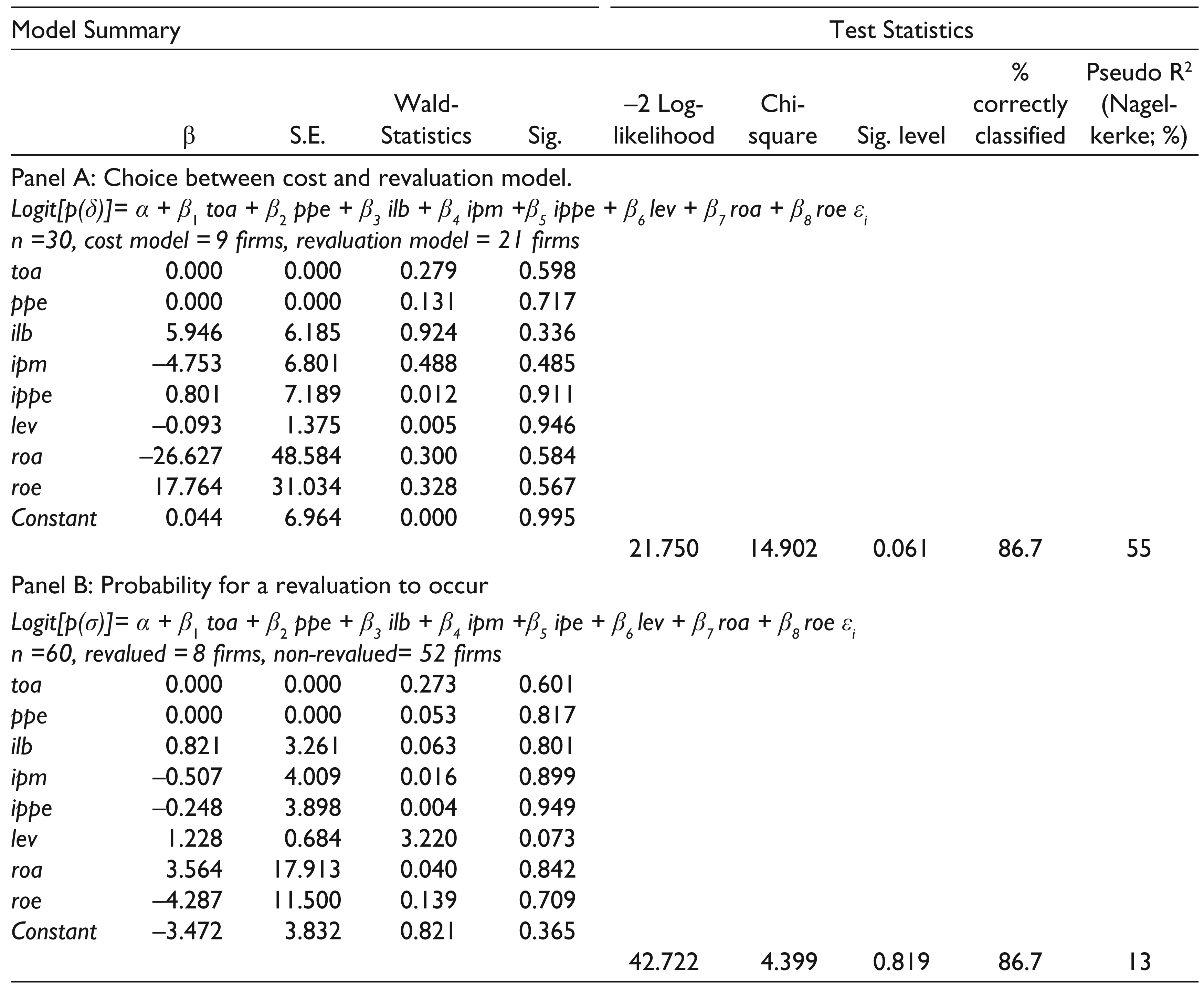

Logistic regression for bivariate model has been performed only for the independent variables having significant relationship with dependent variables concerned, when performed correlation analysis or univariate analysis. Thus, the variables toa, ilb and ipm that associate with δ at least at 10 per cent level of significance exhibited in univariate test and or correlation analysis are admitted for bivariate logistic regression. Accordingly, only the models specified earlier as 1A, 3A and 4A are regressed, and results thereof are presented, respectively, in Panel A, B and C in Table 8. Besides, only financial leverage (lev) has shown an acceptable level of association with dependent variable σ, when performed correlation analysis. Therefore, in relation to the dependent variable σ, only the model 6B is regressed and the results are presented in Panel D in Table 8. No other bivariate models with dependent variable σ was regressed due to their failure to show significant relationship, neither in univariate test nor correlation analysis.

The results of bivariate analysis are consistent with those obtained in univariate tests except that the total asset (toa) is not found to be significant at 0.05 or 0.10 level, even through the relationship between toa and δ was significant at 0.10 level under univariate analysis. On the whole, the results from both the univariate and bivariate analysis affirm that firms choose revaluation model, when they have relatively higher proportion of land and building in total PP&E [R2 (Nagelkerke) is 45 per cent], and firms have chosen cost model, when they have relatively higher proportion of plant and machinery in total PP&E [R2 (Nagelkerke) is 33 per cent].

On the other hand, the probability for a revaluation to occur is found to be related to increased financial leverage. In the contexts that all revaluations observed in the present study culminated in revaluation surplus (See Table 3), shareholder equity of revaluing firms inflates which, as stated by Colin, Nick, Tord and Pauline (2015), mechanically leads to a reduction of gearing ratio, that is, debt-to-equity of those firms. Colin et al. (2015) also claim that reduction in the debt-to-equity ratio sets up, at least, the possibility for additional borrowing, which would restore the debt-to-equity level back to its ‘acceptable’ agreed norm. It, therefore, reveals that highly levered manufacturing firms tend to revalue their assets, may be with the expectation of creating possibilities for additional borrowing.

Bivariate Logistic Regression Model Summary

Multivariate Analysis

The results of multivariate analysis presented in Table 9 reveal that multi-factor models are not able to predict the firms’ choice between cost and revaluation models for reporting their PP&E (see Panel A). They also can not show the probability for a revaluation to occur (see Panel B). Therefore, we need to recourse to bivariate model for concluding on the relationship between the variables examined in this study. Multi-factor model summaries are provided in Table 9.

Multivariate Logistic Regression Model Summary

Conclusion

The motive behind the discretion of management of firms over the adoption of either cost or revaluation model to measure PP&E or the frequency of revaluation is a matter of interest of investors and economic decision-makers. This study sought to explain the motivations of firms in manufacturing sector for reporting fixed assets at revalued amount and to identify the factors that determine the probability that a firm revalues its PP&E in a given year. It was conducted in manufacturing sector in Sri Lanka. The study concludes that whether a manufacturing firm in Sri Lanka chooses to report its PP&E at historical cost or revalued amount depends on the size of land and building or the size of plant and machinery in the total carrying amount of its PP&E. Manufacturing firms in Sri Lanka tend to report their PP&E at revalued amount, when the land and building dominates their fixed assets, and firms whose PP&E is dominated by plant and machinery are inclined towards reporting the fixed assets at historical cost. However, all such other factors investigated as firm size measured by total assets, the carrying amount of PP&E, intensity of PP&E and profitability measured by roa and roe fail to explain the accounting choice between cost and revaluation models. Further, except financial leverage, all the other variables including the intensity of land and building, and the intensity of plant and machinery fail to explain the probability for a revaluation to take place in manufacturing sector. The probability for a revaluation to occur is found to be significantly and positively related to financial leverage, indicating that highly levered manufacturing firms tend to revalue their assets. As this study finds that all revaluations observed in the present study resulted in revaluation surplus, the revelations have inflated shareholder equity of manufacturing firms that revalued their fixed assets. This scenario has led to a reduction of gearing ratio of those firms creating the possibility for additional borrowing which might be a motive behind such asset revaluations. The fact that all revaluations in the years under study resulted in revaluation surplus (upwards revaluation) implicates that firms are inclined to revalue the fixed assets when it is an upwards revaluation, and the upwards revaluation is most likely to occur when assets under revaluation are land and building. This finding suggests that fair value accounting is appropriate to manufacturers with high levels of land and building within their asset structure. This also indicates that the nature of fixed assets determines the choice of firms to revalue their fixed assets. This conclusion may also be related to a general observation that fair value of land and buildings may be reliably and easily obtainable due to potentially growing and domestic market for real estates. It is, however, noteworthy that even through significant association between revaluation decision and the factors such as total assets, the carrying amount of PP&E, intensity of PP&E and profitability have been supported by prior empirical studies in other jurisdictions (mostly in developed economies), it is not established in this investigation. This inconsistency may be attributed to the developing nature of Sri Lankan economy. The finding, thus, concludes that fixed assets revaluation motives may be characterized by the nature of fixed assets and their market dynamics characterized by the nature of economy in which the firm operates. Fixed assets revaluation motives may, thus, differ across countries which should accordingly be valued by financial analyst and investors.

Managerial and Research Implications

The findings are useful for financial analysts and investors to understand the background that drives revaluation decisions in a developing economy. Findings also suggest that fair value accounting is relevant to manufacturers with high levels of land and building within their asset structure. Future research should focus on value relevance of revaluation decision of firms in developing countries. Revaluation decisions should be analysed as first-time revaluation and frequency of subsequent revaluations.

Footnotes

Acknowledgements

The author is grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.