Abstract

Abstract

This study examines the impact of automated teller machine (ATM) service quality on customer satisfaction and its effect on customer loyalty. The data were collected from 360 ATM users in Karachi, Pakistan, using a structured questionnaire. After the data screening process and the removal of outliers, 322 responses were found useable. To identify the dimensions of ATM service quality and their relationship with customer satisfaction and customer loyalty, exploratory factor analysis, confirmatory factor analysis and structural equation modelling (SEM) were used. The findings indicate that (a) fulfilment, reliability, ease of use, and security and privacy are the major dimensions of ATM service quality, (b) dimensions such as convenience and responsiveness are positively insignificantly correlated with customer satisfaction and (c) customer satisfaction significantly influences customer loyalty. This study suggests concrete strategies for bank managers to improve customer experience with ATM and identifies the issues to be resolved in order to improve ATM service quality.

Introduction

In the course of last 20 years, an increase in employment costs and advancement in technology has convinced service providers towards exploring technology-based service opportunities that empower clients in the direction of yielding self-governing services (Dabholkar, 1996; Lin & Chang, 2011). Technology is one of the most significant drivers in many service sectors in terms of attracting more customers, providing better services and improving transaction execution (Boon-itt, 2015). Service providers want the consumers to use technology because it increases services processes, enhances proficiency of services, offers efficient assistance to customers and multiplies services delivery alternatives (Curran & Meuter, 2005).

Self-service technologies (SSTs) are ‘high-tech edges which aid customers in creating self-regulating services of uninterrupted employee participation in service’. It is considered as a substitute for banks that are responsible for cash deposit and withdrawal as well as over the counter transactions (Iberahim, Taufik, Adzmir, & Saharuddin, 2016). SSTs are intentionally intended towards advancing excellence to fulfil the needs of the customers (Zhao, Mattila, & Eva Tao, 2008).

Automated service quality has turned into a viable tool because of its ability to easily duplicate a bank product, but not its level of service. Therefore, by accepting the consequences of automated service quality, reimbursements are offered to banks in terms of enhancing the level of service quality, gaining competitive advantages, expanding their market share, increasing their innovation ability and finally improving the bank performance (Al-Hawari, 2011).

Meuter, Ostrom, Roundtree, and Bitner (2000), and Lin and Chang (2011) suggested automated teller machines (ATMs), check-in machines and automated ticketing, telephone banking and online services as examples of SSTs and stated that customers who take advantage of SSTs appreciate service surrounded by extra flexible time frames plus additional channels. Bitner (2001) stated that service providers correspondingly enhance efficiency as well as effectiveness over SSTs.

ATM service quality is stated as ‘customer’s total assessment and verdict for quality of services delivered by means of ATM channel’ (Narteh, 2013). Lower labour cost, efficiency, more consumer involvement, standardization of service delivery, customer satisfaction and loyalty are the reasons for the introduction of ATMs in retail banking (Al-Hawari & Ward, 2006; Hsieh et al., 2012; Narteh, 2015).

Service quality is an essential requirement for creating and sustaining a satisfactory relationship with customers in a traditional banking context (Sureshchandar, Rajendran, & Anantharaman, 2002). Rod, Ashill, Shao, and Carruthers (2009) observed a direct association between automated service quality and customer satisfaction. According to Day (2003), Wong and Zhou (2006), Olorunniwo, Hsu, and Udo (2006), and Aslam and Frooghi (2018), service quality has been found as an important determinant to attain customer loyalty and satisfaction. According to Parasuraman, Zeithaml, and Berry (1988), advocated service quality is measured by variance concerning customer anticipations of a service provider’s performance and assessment of services they received. Lee and Lin (2005) and Gefen (2002) used the SERVQUAL model by modifying its dimensions to measure the service quality (Shachaf, Oltmann, & Horowitz, 2008).

Several studies have been conducted to investigate the effect of the ATM service quality on customer satisfaction globally (Narteh, 2013, 2015; Proença & Rodrigues, 2011), but none of such studies have been conducted in Pakistan. Khan (2010) stated that ease of use, efficiency, reliability, privacy, responsiveness; convenience and efficiency are the factors of ATM service quality. However, his research ignored a vital ATM service quality dimension, that is, fulfilment, which has been assumed as a foremost automated quality dimension (Parasuraman, Zeithaml, & Malholtra, 2005; Wolfinbarger & Gilly, 2003) as well as customer loyalty (Ariff, Yun, Zakuan, & Ismail, 2013). Narteh (2015) determined security and privacy as one of the quality dimensions.

Bearing in mind the significance of SSTs in the retail banking industry, there is a need to expand the study and explore some concerns (inconsistency in operations) of service quality that influence customer loyalty and customer satisfaction in retail banking sector of Karachi, Pakistan.

With the continuous acceptance of ATMs as a service delivery choice in retail banking, the research into the dimensions of service quality of ATM and their association with customer satisfaction and customer loyalty is an important requirement and this study aims to fulfil this research need.

In Pakistan, banks are offering automated services to attain superior success in these vibrant environs. Banks must be able to deliver a high level of service quality to their customers to increase their cost-effectiveness and attractiveness. This study attempts to observe the impact of the ATM service quality on customer satisfaction and its influence on customer loyalty. Furthermore, the study discovers issues that are to be focussed in order to improve service delivery through the ATMs. Findings from the assessment could also offer bank managers insights to increase and develop customer satisfaction and loyalty in retail banking for using ATMs.

The next section reviews the related literature and presents the framework of the study and service quality dimensions with respect to customer satisfaction, and then objective and rationale of the study are discussed. Data source, sample frame and empirical model are incorporated in the section of methodology, followed by the section of data analysis. At the end, the paper presents the discussion, managerial implications and directions for future research.

Review of Literature

Conceptual Framework

For predicting the acceptance of new technologies, Davis (1986) proposed the technology acceptance model (TAM) that is an adaptation of the theory of reasoned action (TRA) (Ajzen & Fishbein, 1980). TAM comprises subsequent conceptions: perceived ease of use (PEOU), perceived usefulness (PU), attitudes towards use and intention to use/actual use (King & He, 2006; Lin & Chang, 2011). TAM postulates that PEOU is a main element that affects acceptance of information system, whether directly or indirectly over PU. The aim of the TAM is to deliver a broad-spectrum description of the elements of acceptance of technology that is proficient in clarifying users’ behaviour towards technology (Davis et al., 1989). According to Kumar, Lall, and Mane, (2017), the TAM model states that if an application is perceived to be easy to use, it would have a greater level of acceptance. Sahi and Gupta (2013) argued that an application that is apparent to be stress free to use than another is more likely to be accepted by the users. For the adoption of innovation, both PEU and PU have been used and the influence of PU on system utilization is found more significant (Lucas, Swanson, & Zmud, 2008; Robey, 1979).

Wang, Butler, Hsieh, and Hsu (2008) also discovered the casual impact of ease of use (EOU) on PU, and noticed that consumers are focussed to adopt an innovation primarily because technology is easy to use and secondarily for usefulness of the technology for them. Both the factors significantly affect customers’ attitude and intention to use SSTs, as consumers are expected to be more satisfied with SSTs, if they consider that using the system will increase their productivity and performance.

Davis et al. (1989), Wang, Wang, Lin, and Tang (2003), and Pikkarainen, Pikkarainen, Karjaluoto, and Pahnila (2004) have revealed that PEOU is the main element of acceptance by user and it has a significant impact on the proposed system use. While acknowledging the robustness and supremacy of the TAM, they continue towards extending the model with external determinants critical to technology adoption and use (Dimitriadis & Kyrezis, 2010; Wu & Lederer, 2009).

Bolton and Drew (1991) suggested that customer satisfaction causes service quality. Bitner, Ostrom, and Meuter (2002) and Proença and Rodrigues (2011) acknowledged ease of access and convenience to services as reimbursements of SSTs that encourage customer satisfaction; however, out-of-order hardware and software cause dissatisfaction. Perceived service quality is assumed to have an indirect positive effect on loyalty via satisfaction (Eakuru & Matt, 2008). In previous studies, dimensions of ATM service quality are found to be significantly related to customer satisfaction (Narteh, 2015).

In the current study, we have applied the TAM theory to support the relationship of ATM service quality with customer satisfaction and customer loyalty. Hence, based on the previous research (Khan, 2010; Narteh, 2015), we have extended the model of ATM perceived service quality with the added construct of Customer Loyalty (Ariff et al., 2013; Eakuru & Matt, 2008; Ribbink et al., 2004). The service quality hypothesis development is discussed in the next section.

Self Service Technology

SSTs are ‘high-tech edges which aid customers in creating self-regulating services of uninterrupted employee participation in service’. It is considered as a substitute for banks, which is responsible for cash deposit and withdrawal as well as over the counter-transactions (Iberahim et al., 2016).

Makarem, Mudambi, and Podoshen (2009) said that, by attractive SSTs, the firm’s crucial purpose is to deliver superior value to customers at convenient times and at cheaper costs in order to satisfy and retain customers. In the past two decades, the introduction of SSTs in business world has resulted in an overabundance of academic research (Agnihothri, Sivasubramaniam, & Simmons, 2002; Hsieh et al., 2012; Joseph & Stone, 2003; Lee & Allaway, 2002; Snellman & Vihtkari, 2003). The results of these studies suggest that customers assess technology-based service innovations more confidently, if the assumed innovation has the features of high expectedness, controllability, and outcome attractiveness. Though, like all other man-made inventions, SSTs sometimes do fail, and while interacting with technology-based service delivery systems, customer frustration is also evident (Parasuraman, 2000). The frustration has been largely accredited to the lack of readiness and confidence on the part of customers in operating tech-based service delivery interfaces (Ganguli & Roy, 2010). In spite of these problems, SSTs have become enduring features of retail banking service delivery and an examination into their quality dimensions and how they affect customer satisfaction especially in emerging countries is critical for managing customer satisfaction and loyalty of retail banks.

Customer Satisfaction

According to Saleem and Rashid (2011), customer satisfaction is usually regarded as the degree to which a product or service delivered by a firm meets customer expectations. Molina, Martín-Consuegra, and Esteban (2007) claimed that satisfaction results from the feelings consumers attain throughout and later the consumption process.

According to Oliver (1980) and Meng, Tepanon, and Uysal (2008), the expectancy-disconfirmation paradigm is constructed on the intention that customers form expectancies about a product or service prior to consumption. However, Cronin and Taylor (1992) have debated that neither expectation nor disconfirmation has any influence on customer satisfaction due to the diverse definitions of customer expectations as well as the problems in its measurement.

Service Quality and Customer Satisfaction in Automated Channels

Services function as the most prominent phenomena that customers can experience and perceive, and service quality can be assessed based on the interactions of customers with service providers, technology interface and physical evidence (Hanaysha, 2016). Day (2003), Wong and Zhou (2006), Olorunniwo et al. (2006), and Gursoy and Swanger (2007) postulated that service quality is related to customer satisfaction and loyalty. Parasuraman et al. (1988) propose that service quality is measured by the difference between customer expectations of service provider’s performance and their evaluation of the service they received. Various models have been established in the previous studies to measure service quality. The SERVQUAL model, proposed by Parasuraman et al. (1988), and the alternative SERVPERF model by Cronin and Taylor (1992) have acknowledged extensive research consideration and solicitation in the service quality texts. According to Cronin and Taylor (1992), the SERVQUAL model, in spite of its shortcomings, seems to have attained a recognized status with service quality research. The model is built on the statement that service quality is dependent on five major factors of reliability, tangibles, empathy, assurance and responsiveness (Parasuraman et al., 1988). Lee and Lin (2005) and Gefen (2002) used the SERVQUAL model and altered its dimensions to measure service quality. In situations where machines are used to substitute employees in the service delivery process, new dimensions of service quality might be perceived as central by customers. The inference from these studies is that service quality dimensions in traditional services cannot be entirely valid to automated service environments.

ATM Service Quality and Customer Satisfaction

ATMs are electronic devices which let customers deposit, withdraw and transfer money, pay bills and perform other financial transactions without the assistance of a branch representative or a teller. From the prior research, it is evident that ATM is the electronic version of the brick-and-mortar banking hall and customers visit the ATM to make financial transactions, be it withdrawals, deposits or balance enquiry, as they would have done in the normal banking halls. Santos (2003) stated that ATM service quality is the customers’ overall evaluation and judgement of the excellence of services provided through ATM channels. Research shows that ATM quality dimensions are multi-dimensional (Katono, 2011; Khan, 2010; Narteh, 2013). Narteh (2013) identified several dimensions of ATM service quality, such as reliability, convenience, security and privacy, ease of use, fulfilment and responsiveness.

Reliability

Reliability is the capability to carry out the required service precisely and reliably (within the traditional service quality research) (Parasuraman et al., 1988). Wolfinbarger and Gilly (2003) claimed that reliability is the robust interpreter of customer satisfaction in electronic channels. The reliability dimension is critical because it embeds the active competency to perform the undertaken service dependably and accurately. In the ATM environment, reliability predicts the ability of the machine to function all the time, and provide error-free and consistent services. In online transactions, Stiakakis and Georgiadis (2009) found reliability as the essential benchmark of higher electronic service quality. Within ATMs, both Khan (2010) and Katono (2011) found reliability to be an essential ATM quality dimension which impacts customer satisfaction.

Convenience

Convenience refers to the situation where work is simplified with no hassle (Aslam, Arif, & Farhat, 2017). Convenience is regarded as the site or location of the ATM and includes 24/7 accessibility of the services to the customers (Narteh, 2013, 2015). ATMs are conveniently located at bank branches, or off sites, such as shopping malls and college campuses. The bank’s ATM card is compatible with other banks ATM platforms and this makes it possible for customers to withdraw money from other ATMs at a small fee (Narteh, 2015). It lessens the troublesomeness involved in using ATMs and is found to be positively correlated with customer satisfaction (Al-Hawari et al., 2005). If the ATMs are conveniently located, it reduces the inconvenience involved with covering long distances in order to carry out bank transactions. Joseph and Stone (2003), Al-Hawari et al. (2005), Khan (2010), and Katono (2011) stated that convenience has been the most used dimension of ATM service quality and has been found to be positively correlated with customer satisfaction.

Ease of Use

Technology can be threatening to some customers, and therefore, one expects that ATMs should be intended to abridge the transactional process for customers. Davis et al. (1989) described the ease of use as the extent to which the potential user anticipates target system to be stress-free. If users feel that electronic banking is easy to use and free of stress, then the likelihoods of them using the system will be higher (Chong, Ooi, Lin, & Tan, 2010). This study uses the concept to mean the degree to which ATMs offer trouble-free transaction for the customer. Ease of use is a key element in defining the acceptance and use of various corporate information technologies such as online banking (Gounaris & Koritos, 2008). Researchers such as Al-Hawari et al. (2005) and Khan (2010) found that ease of use leads to customer satisfaction in case of ATM usage.

Security and Privacy

An ATM should also deliver customers with security and privacy. Security includes defence of customers from deception and monetary loss, whereas privacy is fortification of personal information (Zeithaml, Parasuraman, & Malhotra, 2002). Casaló, Flavián, and Guinaliu (2007) defined security as ‘the technical assurance that the legal obligation and practices concerning privacy will be met successfully’.

In Bangladesh and Brazil, privacy and security were found to be of serious value and an important enabler for customers in online transactions (Hernandez & Mazzon, 2007; Jahangir & Begum, 2008; Kim, Kim, & Lennon, 2006). Similarly, Chong et al. (2010) found security and privacy as important factors in the adoption of Internet banking in Vietnam. Every customer expects protection for their money and personal information from their banks. In the studies of USA, Australia and Pakistan, security and privacy were considered as important ATM service quality dimensions (Al-Hawari et al., 2005; Joseph & Stone, 2003; Khan, 2010). Consequently, the current study assumes that security and privacy will be positively correlated with customer satisfaction.

Fulfilment

It is the degree to which the site’s assurances about order delivery and item readiness are encountered (Parasuraman et al., 2005). The fulfilment of websites has a noteworthy influence on total quality, satisfaction and loyalty intents (Wolfinbarger & Gilly, 2003). Previous studies related to ATM considered fulfilment as a quality dimension to measure consequence desirability or the degree to which the ATM performs outcomes to meet the customers’ expectations. This includes the genuineness of notes provided by the ATM (eradicate counterfeits), the amount provided to customers per transaction, and the ATM’s transactional charges imposed on customers. Narteh (2015) found availability of cash and the quality of bank notes to be important ATM service quality variables.

Responsiveness

Like all technologies, ATMs are also sometimes disposed to service failures. Responsiveness measures the accomplishment of strategies which the banks introduce to get better services, when ATM services are undesirably established (Narteh, 2015). Responsiveness or recovery is a major determinant in many electronic service quality scales (Narteh, 2013, 2015; Parasuraman et al., 2005). With ATMs, response or recovery quality deals with the banks’ ability to handle customer complaints arising as an outcome of transactional failures as well as reimbursing customers in contradiction of losses experienced, such as money illegally withdrawn out of their accounts. Khan (2010) and Narteh (2015) stated that effective ATM response strategies anticipate customer satisfaction in Pakistan.

Customer Satisfaction and Customer Loyalty

The function of both customer satisfaction and perceived value is known as customer loyalty (Alhemoud, 2010). It is profoundly believed that commitment means to rebuy desired product/service dependably in prospect, thus causing repetitive same-brand/same-set purchasing, regardless of situational effects and marketing determinations ensuring possibility to cause switching behaviour (Al-Hawari, 2011). The degree to which a customer exhibits repeat purchasing behaviour from a service provider possesses a positive attitudinal disposition towards the provider, and considers using only this provider when a need for this service arises (Fianko et al., 2015).

According to Fianko et al. (2015), a loyal customer may not necessarily be a satisfied customer. Oliver (1999) points out that satisfaction and loyalty are related. Satisfaction is, therefore, a function of relative level of expectation and perceived performance. Expectations are built on the basis of previous experience with the same or similar situations, statements made by friends, or other associates. A customer is said to be loyal to a brand that provides a satisfactory experience. Beerli, Martin, and Quintana (2004) stated that satisfaction has been shown to have its effect on customer loyalty and conclude that satisfaction together with personal switching costs is an antecedent of loyalty.

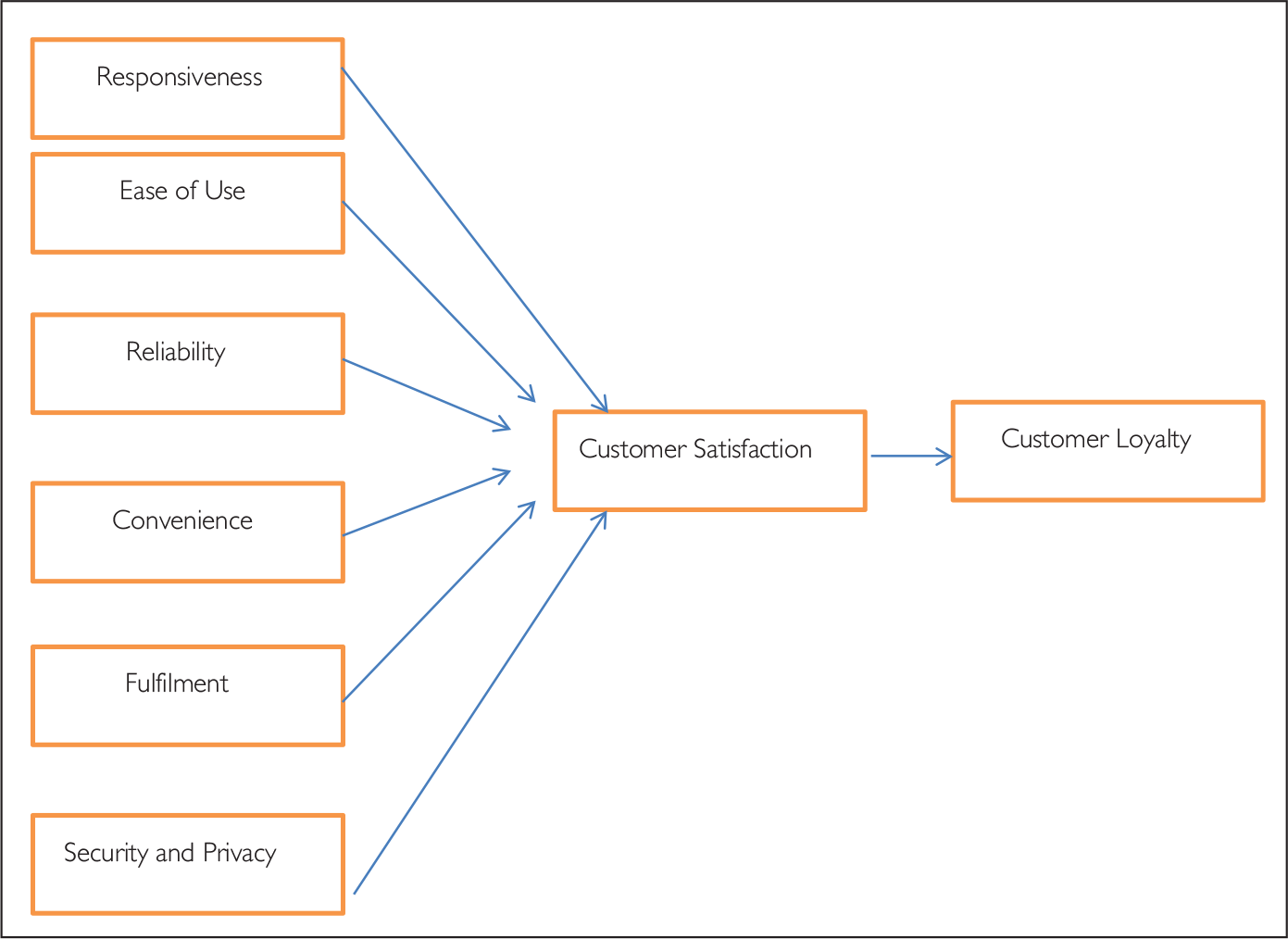

Building on the existing literature revised above, the current study suggests that reliability, convenience, ease of use, security and privacy, responsiveness, and fulfilment are projected to be the chief dimensions of ATM service quality, which will impact customer satisfaction and influence customer loyalty.

Objectives

Due to the importance and increase in usage of SSTs, the objective of this study is to investigate the effect of ATM service quality on customer satisfaction and customer loyalty. Responsiveness, ease of use, reliability, convenience, fulfilment, and security and privacy have been taken as the dimensions of service quality. By considering these dimensions, customer satisfaction as well as the impact of customer satisfaction on customer loyalty has been assessed in the present study.

Rationale of Studies

The purpose of the study is to identify the service quality dimensions that help in increasing customer satisfaction, which leads to loyalty. Due to the increase in the usage of SSTs and the acceptance of ATMs as service delivery choice in retail banking, there is a need to identify the factors that help in satisfying the customer.

Methodology

To foresee the ATM service quality impact on customer satisfaction and loyalty, primary data were collected through a self-administered questionnaire. The questionnaire was designed for use as a survey instrument to record the respondents’ experiences and perceptions about ATM service on a 5-point Likert-type scale that varied from ‘strongly disagree’ (1) to ‘strongly agree’ (5). The technique used for data collection and the sources from where the questionnaire was adapted are mentioned in data source. Under the sample frame, the target audience of this study was mentioned. Statistical tests which were applied on the data are mentioned under the heading of Data analysis tool.

Data Source

Exploratory Factor Analysis

Sample Frame

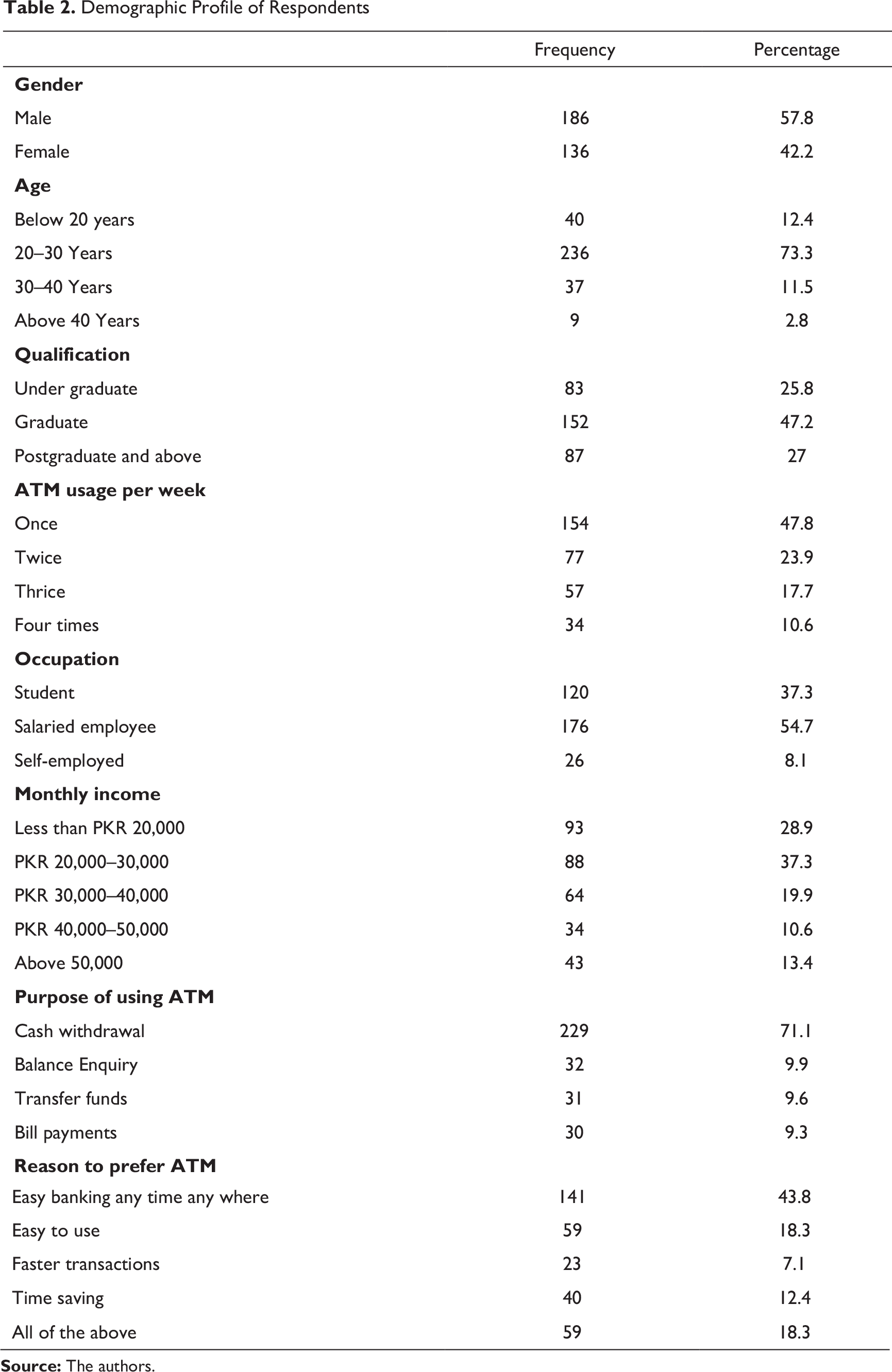

Data were collected from ATM users of different banks in Karachi, since this market segment is viewed as important for the continued advancement of the retail banking industry.

Data Analysis Tools

Reliability analysis was performed to evaluate the internal consistency of the items. Exploratory factor analysis was performed using the option of varimax rotation in order to compile the construct using SPSS 22.0. After performing exploratory factor analysis, confirmatory factor analysis was performed to check all the model fitness criteria. To further test the hypothesized relationships among the latent variables, the structural equation modelling (SEM) was employed using IBM SPSS Amos 22.0.

Empirical Model

Founded on the aforementioned literature review, the study proposes a framework which guides the current research.

Analysis

Demographic Profile

Demographic Profile of Respondents

Descriptive Statistics

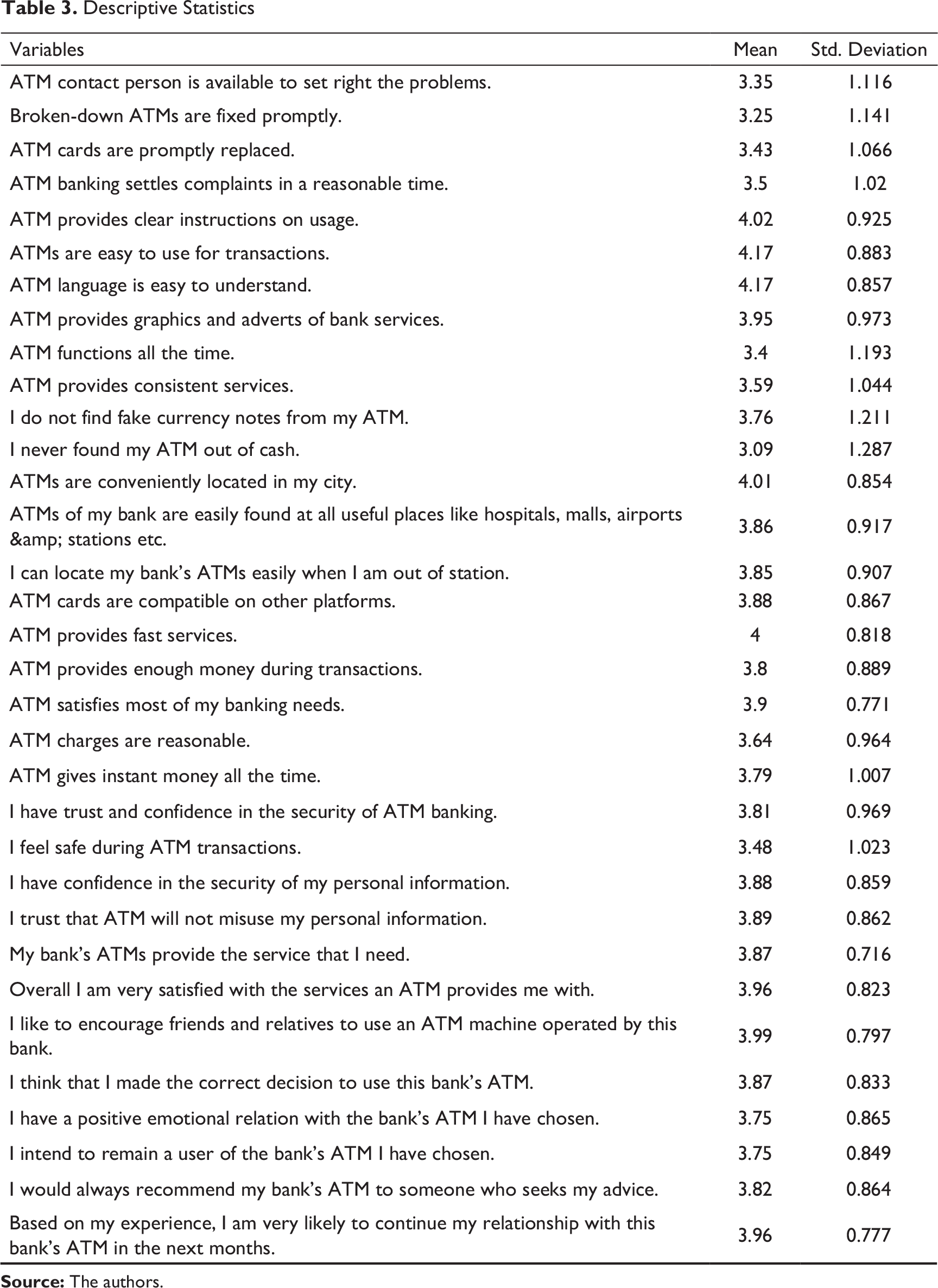

Descriptive Statistics

Factor Adequacy, Reliability and Validity of Construct Scales

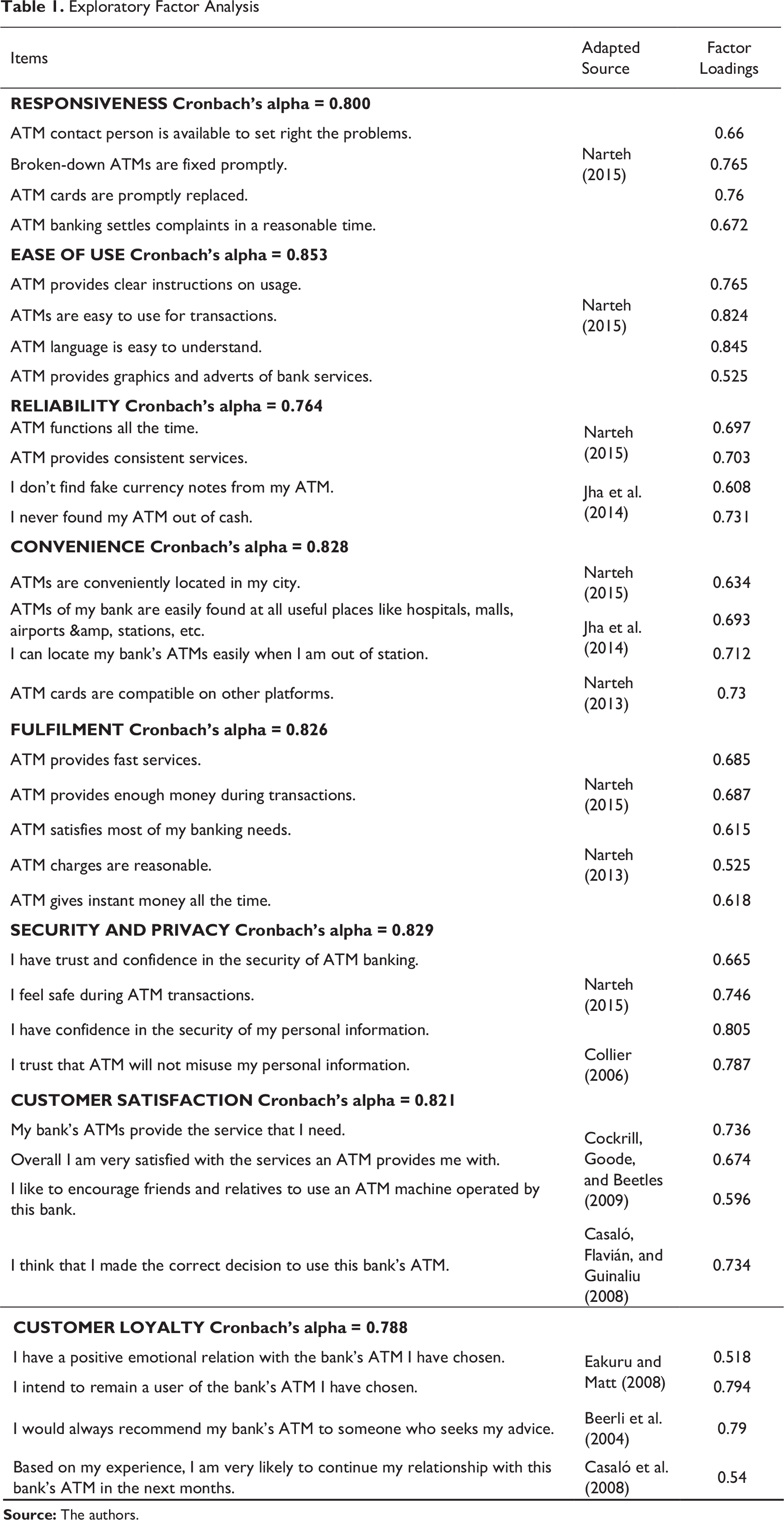

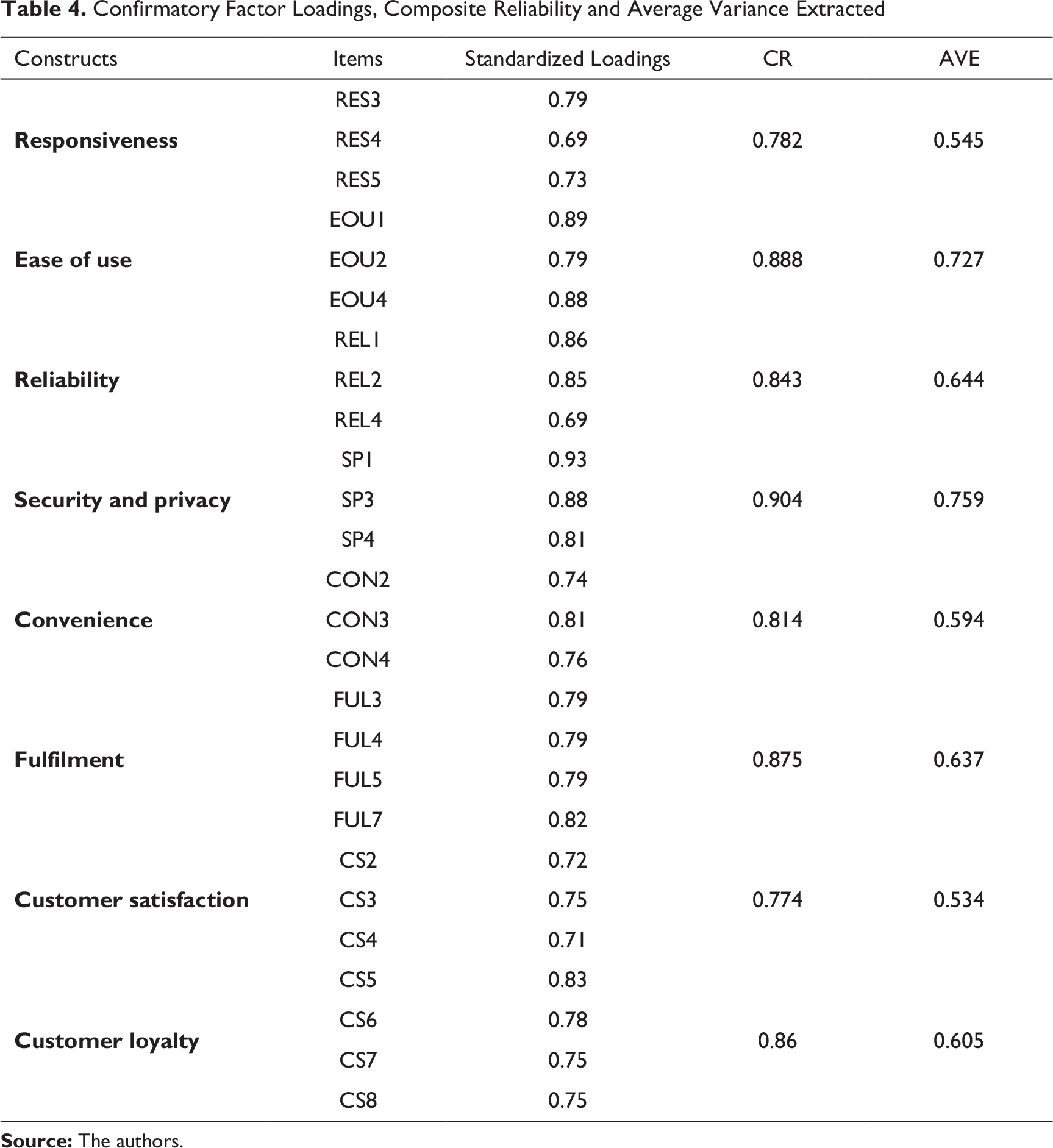

To check the dimensionality of the instrument, all the items of the questionnaire were factor analyzed by using varimax rotation. The validation process was initiated using an initial exploratory analysis of reliability and dimensionality. The values of the Bartlett test of sphericity and the Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy, which were 0.000 and 0.899 (>0.60), respectively, confirmed that there is a significant correlation among the variables (Hair, Anderson, Babin, & Black, 2010). The variables with loadings of at least 0.5 and factors with a reliability threshold of 0.7 (Hair, Black, Babin, Anderson, & Tatham, 2006) were incorporated into the analysis. Cronbach’s α statistics for the constructs range from 0.764 for reliability to 0.853 for ease of use, which advocates that scales are adequately reliable (Hair et al., 2010). Table 1 illustrates the overall factor loadings and reliability of the individual items.

Confirmatory Factor Loadings, Composite Reliability and Average Variance Extracted

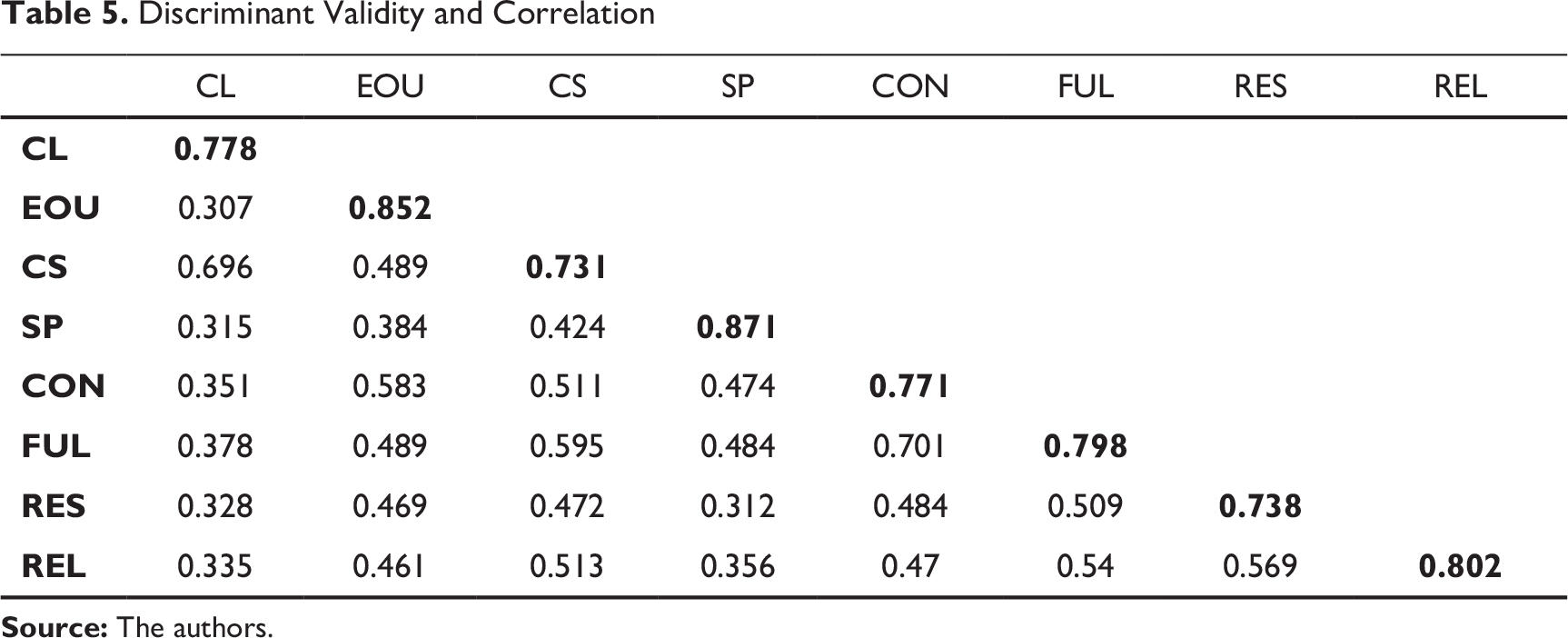

Discriminant Validity and Correlation

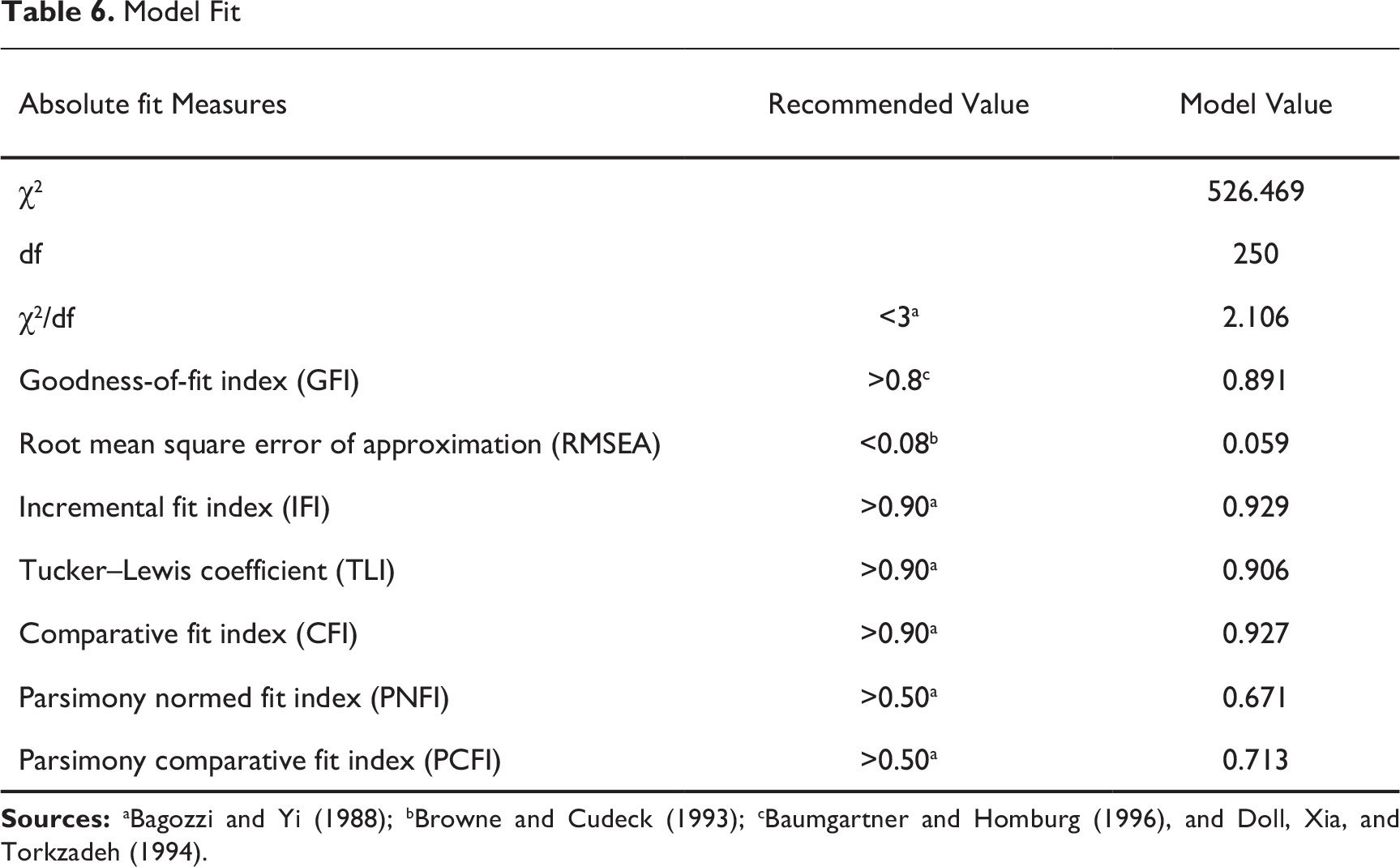

Model Fitness

To analyze the simultaneous effects of the variables included in the final construct, the model was further studied by SEM. A few items were excluded from the model in order to achieve model fitness. The items are as follows: ‘ATM banking settles complaints in a reasonable time’, ‘ATM language is easy to understand’, ‘I never found my ATM out of cash’, ‘I feel safe during ATM transactions’, ‘ATM cards are compatible on other platforms’, ‘ATM charges are reasonable’ and ‘I think that I made the correct decision to use this bank’s ATM’.

From the results of various indices, the model showed good fitness. The value of χ2(CMIN/df) was (2.106) which is between the acceptable range of 3:1(Arif, Aslam, & Ali, 2016; Kline, 2011) and CMIN is (526.469), df is 250, and the probability level is (0.000). While goodness-of-fit index (GFI) is (0.892) and possible good range of GFI is 0–1, high values show better fit, and previously values greater than 0.90 were considered good (Hair et al., 2010). Trucker Lewis Index (TLI) was found to be (0.906), which also lies in the acceptable range of 0 to 1 (Arif, Afshan, & Sharif, 2016; Aslam, Batool, & Haq, 2016; Byrne, 2013) for better model fitness. The root mean square error of approximation is (0.059), which is less than 0.07 and shows good fit (Aslam et al., 2015; Byrne, 2013). The results indicated that the overall model was a good fit at 95 per cent level of confidence. The value of standardized root mean square residual (SRMR) for the default model is found to be 0.0496, and according to Hu and Bentler (1999), it must be less than 0.08. These various indices showed that the model fits the data perfectly. All the stated values are between acceptable regions for the default model. Table 6 demonstrates the model fitness for the SEM.

Path Analysis

Model Fit

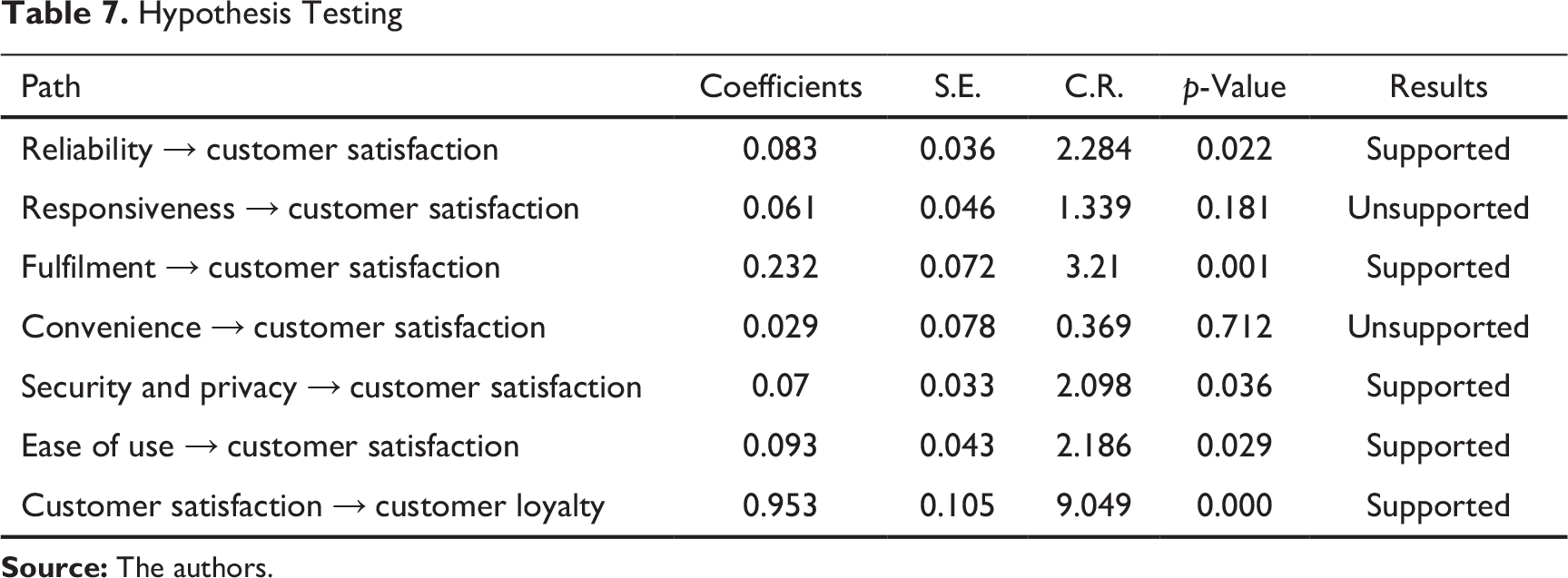

Hypothesis Testing

Discussion

The motive of the study was to examine the customer satisfaction as well as check the relationship of dimensions of ATM service quality and customer loyalty. The ATM service quality is found to be multi-dimensional, which is concordant with previous studies (Nateh, 2013, 2015). The study has delivered a comprehensive set of ATM quality dimensions and demonstrates that apart from convenience and responsiveness, dimensions such as fulfilment, security and privacy, ease of use, and reliability have a significant effect on customer satisfaction and this influences customer loyalty.

The study has discovered that fulfilment is the most essential determining factor of customer satisfaction for ATM service quality. The findings are in accordance with previous studies (Narteh, 2015), which also found that ATM must provide fast services, precisely record transactions with receipts in order to meet the needs of the customers, ensure availability of adequate quality bank notes and enough cash in a sufficiently early manner, and create receipts to approve transactions.

Second, the results showed that reliability is an important contributor of customer satisfaction of ATM services. To enhance customer satisfaction, ATMs must have technical and functional reliability and provide error-free services. The outcomes are similar to the results obtained by scholars (Narteh, 2013, 2015; Parasuraman et al., 2005) who also found that customers anticipate ATMs to function persistently, provide reliable services and create exact account records. The purpose of creating automated channels is to facilitate the clients, so that they can carry out their financial transactions during any period of the day.

Third, security and privacy is another significant dimension of ATM service quality in predicting customer satisfaction. The results suggest that all customers anticipate security, confidence, and trust for their money as well as their personal information. Installation of CCTV cameras and the presence of security guards on on-site ATMs have increased the trust factor in customers during transactions.

Moreover, the study has found that the ease of use has a significant impact on customer satisfaction. Even technology-savvy customers occasionally find technology use a bit intimidating, so customers anticipate the ATM to be effort free and less complex. The results are consistent with past studies (Narteh, 2013, 2015), which also found that the facility of an easy-to-understand language as well as user-friendly instructions are an important determinant for improving customers’ ATM experience.

Furthermore, the study revealed that customer satisfaction has a strong influence on customer loyalty. Customer satisfaction leads to customer loyalty with an estimated value of 93 per cent. The results are consistent with previous studies (Beerli et al., 2004; Casaló et al., 2008; Eakuru & Mat, 2008; Kaura, Durga Prasad, & Sharma, 2015), which found that customer satisfaction will be created, if the customers’ anticipations about the services are met, as expectations are built on the basis of previous encounters with the same or similar situations and testimonials made by friends or other associates. Satisfaction is an essential criterion for loyalty, because satisfied customers are loyal, and therefore, they incline to select the same service providers.

The results further show that responsiveness has an insignificant effect on customer satisfaction. This might be due to the reason that customers do not consider quick complaints compensations, prompt recovery of malfunctions of ATMs and replacement of ATM cards as much important as other dimensions. The results are concordant with earlier studies (Kumbhar, 2011; Wong, Rexha, & Phau, 2008) that responsiveness is not significantly associated with satisfaction in ATM services. Another reason for this insignificant result might be that if the ATM card gets trapped or damaged in the machine and customer makes complaints against it, the customer has confidence that the card would be returned to them only after displaying his identity.

Convenience has a positive insignificant impact on customer satisfaction. The results are similar to the study of Mohammed (2012), which also concluded that convenience has no attentive effect on the use of advanced IT banking services. Location of ATMs and compatibility of cards at other platforms are not the only reasons for creating customer satisfaction. Another reason might be e-banking channels that have resolved this issue, and customers feel comfortable in performing their transactions online. As this study has been conducted in Karachi city, where debit card use is very common at several shopping malls and restaurants, people can easily use their ATM cards anytime and anywhere.

Conclusion

Nowadays, SSTs have gained much popularity. SSTs are changing the way customers interact with the firm for service outcomes. This study reflects the consumer behaviour towards SSTs; mainly ATM service was focussed. For determining consumer behaviour, customer satisfaction and loyalty were considered. Different service quality dimensions (reliability, fulfilment, ease of use, convenience, security and privacy and responsiveness) were taken to assess customer satisfaction, which leads to loyalty. An adapted 5-point Likert-type scale questionnaire was used for the data collection. In total, 322 usable responses were gathered. Different statistical techniques such as EFA, CFA and SEM were implied. Reliability, content validity and discriminant validity were also examined. According to the results of path analysis, consumers get satisfied by the ATM service if it is reliable in terms of consistent service and availability of cash. Fulfilment and ease of use are also found to be the key factor, which helps in gaining satisfied customers. Consumers want to feel secure and want privacy while doing transactions; therefore, if the firm provides secure transaction facility, it can easily be able to get the satisfied customer.

Managerial Implications

This study delivers and exhibits the sustained importance of ATMs in the retail banking in Karachi. These identified dimensions will offer bank managers insights into what factors clients find to be most important in their ATM usage experience. The quality dimensions used in this study recognize the need for enhancement in ATM banking systems in order to offer value-added services to customers. In current study, continence has failed to establish a significant relation with customer satisfaction. This might be because mostly ATMs are used for cash withdrawal only and are under-utilized. A full range of bank services should be enabled through ATMs, which may add to the customer convenience and may contribute to the customer satisfaction. Banks should upgrade their ATM platforms to aid customers to receive all services, which are enabled through Internet banking, for instance, inter-bank transfer, payment of utility bills, cash deposit, making of pay-order, etc. These new services will probably attract more customers into the ATMs use and reduce the long queues in banking halls, which will help in building a robust and persistent relationship with customers. The banks should ensure that ATMs are there to fulfil the needs of customer belonging to all income classes. The ATM must provide notes of smaller denominations too, at times notes of small denomination finish quickly and customers may get ‘service denied’ message for lesser amounts. The resulting increase in customers’ inclination to use ATM for multidimensional features will also add to the demands on banks to promptly respond to meet the needs of customers. The focus of bank management should also be on delivering better interactivity, expanded assistance and increased ease of use through their ATM service, which will also ensure customer retention.

The service standards of ATMs can be improved through a two-way communication, that is, rapid response to customer queries about the ATM-associated services and regular maintenance at the ATMs to reduce failures, ensuring that all malfunctioning ATMs are fixed quickly. Banks should introduce new user-friendly, multilingual, biometric access-based, competitive systems and applications that will assist customers take the full advantage of the ATM service.

Limitations of the Study and Future Recommendations

This study is carried out in Karachi which limits the generalizability of the outcomes beyond the context of the study. Future studies must be conducted in other cities of Pakistan using random sampling in order to augment understanding of ATM quality dimensions and customer satisfaction. Future studies must investigate the relationship of additional dimensions of service quality with customer satisfaction, loyalty and retention in other SSTs (Internet banking and mobile banking), comparing the cross-cultural service quality of conventional commercial banks and Islamic banks.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.