Abstract

This study empirically investigates the quadratic effects of bank diversification, size and global financial crisis on risk-taking behaviour and performance. To unfold those effects, it uses the generalized method of moments (GMM) estimator and also uses an unbalanced panel data set on a large sample consisting of 542 bank-year observations between 2004 and 2015. The key results for emerging economies are as follows: (a) increasingly higher non-performing loan ratio makes the bank underperforming and unstable; (b) benefits derived from bank diversification are heterogeneous and confirms portfolio diversification theory; (c) small-sized banks of Bangladesh ensure higher advantage from portfolio mix over large banks; (d) large banks of South Africa achieve higher benefit from income diversification over small-sized banks; and finally, this study evidences that during the financial crisis, emerging economies can use portfolio diversification as a mechanism for controlling risk and improve bank performance. Mainly, emerging countries can rely on income diversification and should involve this mechanism with systematic risk a great care of.

Keywords

Introduction

After the recent global financial crisis (GFC), the banking sector has experienced significant changes in both developed and emerging countries. 1 Market competition and liberalization have forced banks to shift their primary sources of income from interest-based business (Meslier et al., 2014; Zhou, 2014). These changes have been broadly addressed in developed countries based on the implications of income diversification to performance and risk, but to date, no real consensus has been reached (Zhou, 2014). Most studies find that although income diversification makes it easier for a bank to gain profit, it simultaneously brings extra risk (e.g., Demsetz & Strahan, 1997; DeYoung & Roland, 2001; Lepetit et al., 2008; Stiroh, 2004a, 2004b; Williams, 2016). Diversified income may lead to other channels of risk, that is, credit risk, market risk, liquidity risk or operational risk. But the theory of portfolio suggests that specialization of income, that is, non-interest business income, may diversify their risks if there is no association of traditional business. In the light of agency theory, some researchers have proposed that diversification and the firm’s growth are the ‘consequence of managerial self-interest in endeavoring to lessen risk and lifting stability and market power simultaneously’ (Amihud & Lev, 1981; Jensen & Meckling, 1976). Contrary to evidence, Laeven and Levine (2007) reported a similar finding showing the impact of income and assets diversity on the firm’s value. A diversified bank may be confronted by conflicts between insiders and outsiders like the bank and its customers. Besides, based on free cash flow hypothesis (Jensen, 1986), agency costs would be aggravated when retention ratio becomes higher and drives managers to divert funds for diversification. Compared to those conceivable theories above, the theory of diversification is characterized by resource-based (Chatterjee & Wernerfelt, 1991; Peteraf, 1993). Resources from the financial market are categorized into two aspects: (a) interest-bearing assets, (b) non-interest-bearing assets. The latter ones are often signified as diversified assets, and they have long been absent in the literature, but today’s diversification trend seems to support this view. However, the smart corporate managers will benefit from diversification regarding market power (Berry, 1971; Palepu, 1985) and growth (Guth, 1980).

There is an ongoing debate in the literature whether the inclusion of bank diversification is beneficial or not. In this regard, some studies (such as Amidu & Wolfe, 2013; Baele et al., 2007; Campa & Kedia, 2002; Landskroner et al., 2005; Reichert & Wall, 2000) suggest that diversification of banks improves bank’s stability, as non-interest income increases and reduces the probability of bank failure (DeYoung & Torna, 2013). Besides, the risk exposure issue with assets diversification remains unsettled. Based on the data of more than 4000 commercial banks from 1979 to 1986, Liang and Rhoades (1991) report that (financial assets and geographical) diversification has implied a negative relation with risk. Based on South Asian banks, Nguyen et al. (2012) find that banks are more stable when they diversify across interest and non-interest activities along with significant market power. Similar to South Asian banking, Edirisuriya et al. (2015) find that income diversification increases profit only by one point, improves solvency and declines with a higher level of income diversification beyond this performance. Their study also concludes that a continued diversification of assets does not imply itself to proceed to improve market performance.

Based on the data from 29 Asia-Pacific countries, Lee et al. (2014) find that banking industry can enhance its performance with diversification. According to the data of 62 Chinese commercial banks, Zhou (2014) empirically shows that there is no evidence to prove the relationship between income diversification and bank risk, but the overall risk responds parallel to the proportion of non-interest income increases as well as its volatility. However, very few papers (e.g., Amidu & Wolfe, 2013; Nguyen et al., 2012; Sanya & Wolfe, 2011) have been focused on emerging countries and found some opposite result from the evidence above. So, the continuously increasing number of findings motivates researchers to study the relevant field of different financial systems and explore the following questions: How does bank diversification affect risk and performance in emerging economies? Is the bank diversification in different bank sizes of emerging economies the same? Does bank diversification have any effect on bank risk and performance during the financial crisis? The prior literature fails to provide consensus on these inevitable questions. Many empirical studies have elaborated on bank diversification, but most of them focused on a particular single country’s banks or regional banks, but this study is intended to underpin two different countries under same emerging economies frontier. This study is the extension of Zhou (2014) who considered 62 Chinese commercial banks during 1997–2012 and assessed the influence of income diversification on operating risk and overall risk. Our study is also the extension of Meslier et al. (2014) who considered 39 commercial banks of Philippines from 1999 to 2005 and assessed the diversification effect only on bank performance. In our case, additionally, we find two different emerging economies and their performance measures including credit risk and the interaction of financial crisis.

To solve the existing problems, this article aims to conduct a study on risk and performance in emerging economies based on the data of Bangladesh and South African banking industry over the recent period (2004–2015), during which noteworthy financial crisis happened in the emerging economies banking sector. During this timeframe, both countries adopted multiple structural changes in financial intermediation system and banks have taken a series of remedies to improve the profitability, stability and overall competitiveness. On this ground, this study is imperative for policy issues in developing and emerging economies. However, the choice of countries is not arbitrary. Though this study confines to two countries, it will have the contribution beyond the boundaries and differential outcomes of two emerging economies.

This article is organized as follows: the second section introduces the background of banking industries of two emerging economies, followed by the third section that reviews the previous literature. The fourth section outlines research framework. The fifth and sixth sections report the empirical findings and robust results, respectively. Finally, the seventh section concludes and provides some policy implications.

Institutional Background of Sample Emerging Economy

Banking Sector of Bangladesh

After the independence, the banking system in Bangladesh started its journey with only 11 banks, including two state-owned specialized banks, six nationalized commercialized banks and three Foreign Banks. During the 1980s, the banking industry significantly expanded due to the active entrance of private commercial banks. Currently, banks in Bangladesh are mainly of two types, that is, (a) scheduled bank: the bank which gets license to operate under Bank Company Act, 1991 (Amended up to 2013) and (b) non-scheduled bank: the bank which is established for special and definite objective and operates under the acts that are enacted for meeting up those objectives. This bank cannot perform all functions of scheduled bank.

At present, 56 scheduled banks (till December 2015) are operating under full supervision and control of Bangladesh Bank

2

as per Bangladesh Bank Order, 1972 and Bank Company Act, 1991. Besides, four categories of scheduled banks are available in Bangladesh like:

State-owned commercial banks (SOCBs): There are four SOCBs which are fully owned by the Government of Bangladesh. Specialized banks (SDBs): four specialized banks are now operating, which were established for specific objectives like agricultural or industrial development. The Government of Bangladesh majorly owns these banks. Private commercial banks (PCBs): There are 39 private commercial banks, which are majorly owned by shareholders or institutional owners. PCBs can also be categorized into two groups, that is, (a) Conventional PCBs: 31 Conventional PCBs are now operating in the industry. They perform the banking functions in conventional fashion, that is, interest-based operations. (b) Islamic Shari’ah-based PCBs: There are eight Islamic PCBs based on Islamic Shari’ah principles, that is, profit-loss sharing (PLS) mode in Bangladesh, and they execute banking activities according to Islamic Shari’ah. Foreign commercial banks (FCBs): nine FCBs are operating in Bangladesh as the branches of the banks which are originated in abroad.

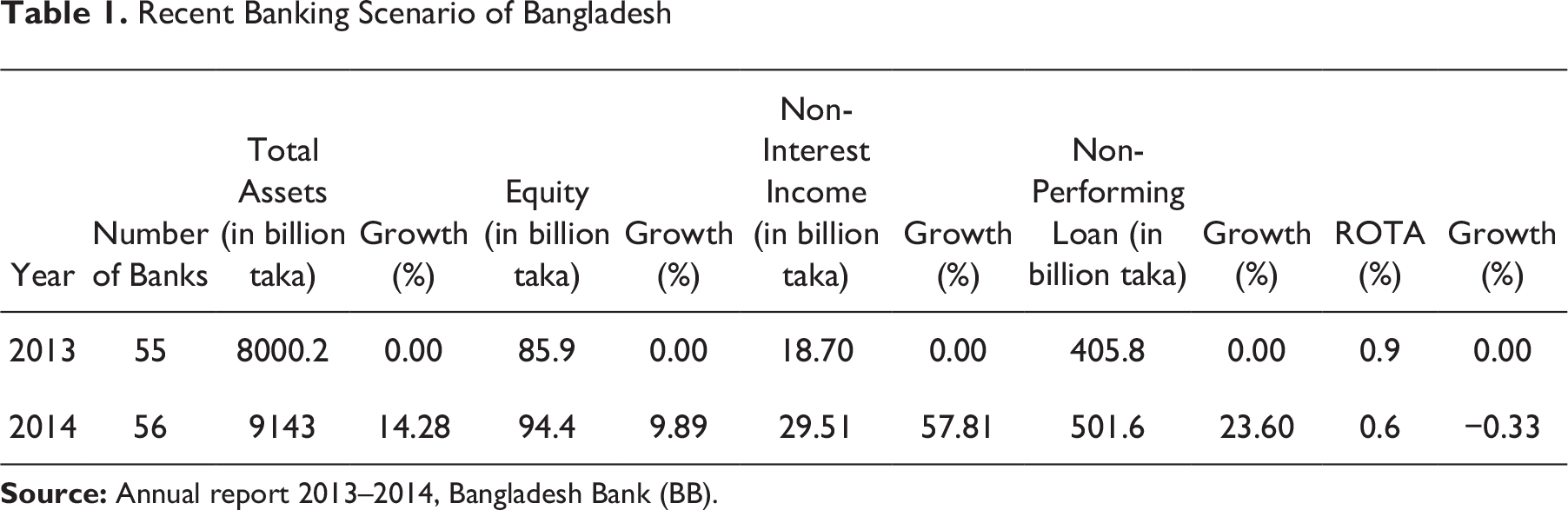

In October 2015, Bangladesh Banks maintained US$27,058.40 million as an international reserve, 3 which replicates the instantaneous growth of Bangladesh banking systems. According to Bangladesh Bank statistics, currently 9,040 branches of all scheduled banks are working in Bangladesh, and this focuses on a view to forecasting a sound, efficient and stable financial system. The banking industry is emerging rapidly with incremental change of number of banks, branches, assets, equities, diversified income and strategies, etc. However, the overall assets of this industry amount to BDT (the local currency of Bangladesh is Taka) 9143 billion in 2014, which shows an overall increase of 14.28 per cent compared to 2013 (Table 1). Other indicators also document the incremental progression except for return on total assets (ROTA), which declines a bit in 2014.

Recent Banking Scenario of Bangladesh

Recent Banking Scenario of South Africa

Banking Sector of South Africa

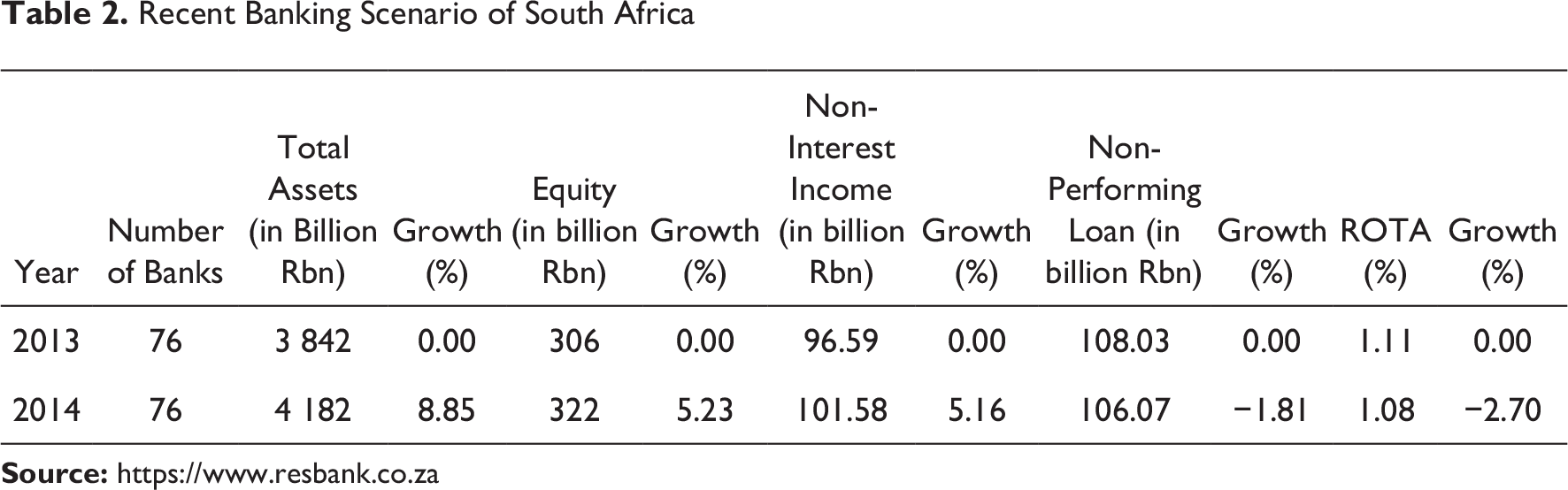

The Reserve Bank is the guardian of all banks of the South Africa. The central bank was established in 1921 under special Act of Parliament, the Currency and Banking Act, 1920 (Act No. 31 of 1920). By the central bank’s recent statistics, currently, it has 74 banks. All these banks are comprised as 10 locally controlled banks, 6 foreign controlled banks, 3 mutual banks, 38 foreign bank representatives, 15 branches of foreign banks, and 2 banks in liquidation. The country’s banking industry is gradually increasing with an incremental change of its assets, equities and diversified income.

However, the overall assets of this industry amount to Rbn (the local currency of South Africa is Rand) 4182 billion in 2014, which shows an overall increase of 8.85 per cent compared to 2013 (Table 2). Equity and diversified income have increased gradually, while South African banks show a negative growth of ROTA in 2014 and an improvement in credit management.

In the financial crisis on 1 January 2008, South Africa took a major exercise over several years to implement Basel II—a revised capital framework that was supervised by the Basel Committee. After the financial crisis, it needed South Africa to move along with the global financial reforms. That is why they, on 1 January 2013, have implemented amended regulations that are in line with Basel III regulatory frameworks, carrying on to the multiple phases until 1 January 2019.

Previous Studies and Development of Hypotheses

A modern global financial system shifts the traditional business into financial conglomerates. Instead of focusing on lending activities, financial institutions are now looking for diversifying their functions through foreign exchange, investment in securities, investment management, insurance policy, financial derivatives and planning and off-balance sheet items. This diversity influences risk as well as performance. Consequently, we divide this section into the literature on the effect of diversification on risk and performance.

Diversification and Risk

This section explores the relationship between bank (income and assets) diversification and risk. Therefore, we will focus on the literature that relates both diversifications to non-interest income and non-interest-bearing assets. Hypothetically, it is expected that an increase in income and assets diversification leads to increasing net earnings, thus declining credit and interest rate risk. Non-interest income has been greatly emphasized in today’s banks’ revenue composition because it can diversify risk (Allen & Santomero, 2001; Laeven & Levine, 2007). Stiroh (2004a), Stiroh and Rumble (2006) also report that higher level of non-interest income in US banks promotes the increase of revenue over time through reducing risk. Furthermore, Brunnermeier et al. (2012) demonstrated that banks with higher non-interest income reveal higher levels of systemic risk. In similar stands, DeYoung and Roland (2001) refer that the expansion of fee-based income could lead to more variability of profits and worsen the risk-return trade-off. By analysing European banks, Chiorazzo et al. (2008) provide somewhat different results that risk-adjusted returns increase with income diversification and the responsiveness of gain fluctuate conversely with bank size. Whereas, the opposite effect is also available for Lepetit et al. (2008), who find that small banks also generate higher risk when non-interest income drives banks. Other studies (such as De Jonghe, 2010; Demirg-Kunt & Huizinga, 2010; Fiordelisi et al., 2011) have also found that revenue diversification is positively associated with banks’ risk. In another similar stand, Baele et al. (2007) find that non-interest income undoubtedly increases bank’s franchise value with higher systematic risk. From the evidence of Australian banks, Williams (2016) shows a positive relation between non-interest income and risk, lower level of non-interest income and higher revenue concentration decline risk. Asian counterpart Pennathur et al. (2012) explore the ownership impact on income diversification for the Indian banks over the period of 2001–2009 and find different ownership has a diverse impact on income diversification and risk. They also document that private and public banks earn less regarding fee-based income than foreign banks. Recently, Edirisuriya et al. (2015) examine the effect of bank diversification on stock market responses in South Asian region from 1999 to 2012. They find that banks achieve higher market value and solvency when diversifying through interest income, but only beyond that level, performance indicators are negatively associated with higher levels of diversification. Moreover, Zhou (2014) documents that no significant relation was observed between bank diversification and risk when considering 62 Chinese commercial banks during 1997–2012. But the concern of risk exposure to assets diversification is still ignored in the literature. Relying on the US bank-holding company, Stiroh and Rumble (2006) find a positive impact of assets diversification on market performance and risk. While conversely, Liang and Rhoades (1991) report that greater assets and larger geographic diversifications are involved with lower risk. Recently, based on South Asian banks, Edirisuriya et al., (2015) reported no significant relation between assets diversification and risk.

However, above literature analysed the distinct influence of bank diversification on risk profile for most developed economies such as Japan, South Korea and USA. Diversification of banks and size effect on risk and performance to the emerging markets remain ambiguous. To assess the possible impact of bank diversification on risk, we will test the following hypothesis:

Diversification and Performance

Recently, the performance of financial institutions has been received heightened attention. There is now a wide range of literature of this arena, but this section represents the relationship between the bank (income and assets) diversification and performance. Concerning the impact of bank diversity on performance, it is also found debatable around the literature. Some studies (such as Baele et al., 2007; DeYoung & Roland, 2001; Stiroh & Rumble, 2006) based on the most developed economies show that the relationship between revenue diversification and bank performance confirms the portfolio hypothesis. Additionally, other studies (e.g., De Jonghe, 2010; Lepetit et al., 2008; Stiroh, 2004b) hold opposite views against their results and highlight an adverse effect of diversification. With few exceptions, Mercieca et al. (2007) find that the diversification had no direct benefits within or across business lines for small European banks from 1997 to 2003. More interestingly, they find an inverse relation between non-interest income and bank performance and Trujillo-Ponce (2013) also observed that exception.

On the other hand, a very few papers have briefed on asset measures of diversification and provide mixed evidence concerning its impact on performance; for example, Rossi et al. (2009) illustrate the positive effect of asset diversification on profit efficiency by reducing risk and cost. Curi et al. (2015) also support the previous conclusions based on technical efficiency as a measure of foreign bank performance. But from the South Asian counterpart, continuous diversification of assets does not improve performance (Edirisuriya et al., 2015). While Elyasiani and Wang (2012) show a contrary result by focusing on the US bank-holding companies from 1997 to 2007 and no relation has been explored by Acharya et al. (2012).

However, in contemporary, Asian emerging economic view, the involvement of non-interest activities improves bank performance and risk-adjusted profits (Meslier et al., 2014; Pennathur et al., 2012; Sanya & Wolfe, 2011). These findings also align with the extensive study of Lee et al. (2014) who consider 29 Asia-Pacific countries, covering the period between 1995 and 2009, for a total of 2372 banks. Unlike the previous section, no consensus has been reached regarding the relationship between bank diversification and performance; although many studies have been conducted in developed countries, emerging economy of different countries is still unexplored. Thus, we test the following hypothesis:

Data and Variables

Data Collection and Time Frame

We compose our bank-level variables from the financial statements of 32 commercial banks in Bangladesh and 16 commercial banks’ data in South Africa were received from the Bankscope database of Bureau van Dijk’s company over the period 2004–2015. This gives us a total of 542 unbalanced panel observations. We ignore data from foreign bank representatives, specialized banks and liquidation, as these data were irrelevant and inconsistent in nature. We consider the period 2008–2009 as a GFC year by modifying GFC variable of Williams (2016). The GFC sharply slowed down the South African economy from the fourth quarter of 2008 and officially entered into a crisis in the first quarter of 2009 (SARB, 2009). 4 As our article based on economy of South Africa and Bangladesh, we consider a regular period to control such crisis and these years are also supported by Kumbirai and Webb (2010).

Definition of Variables

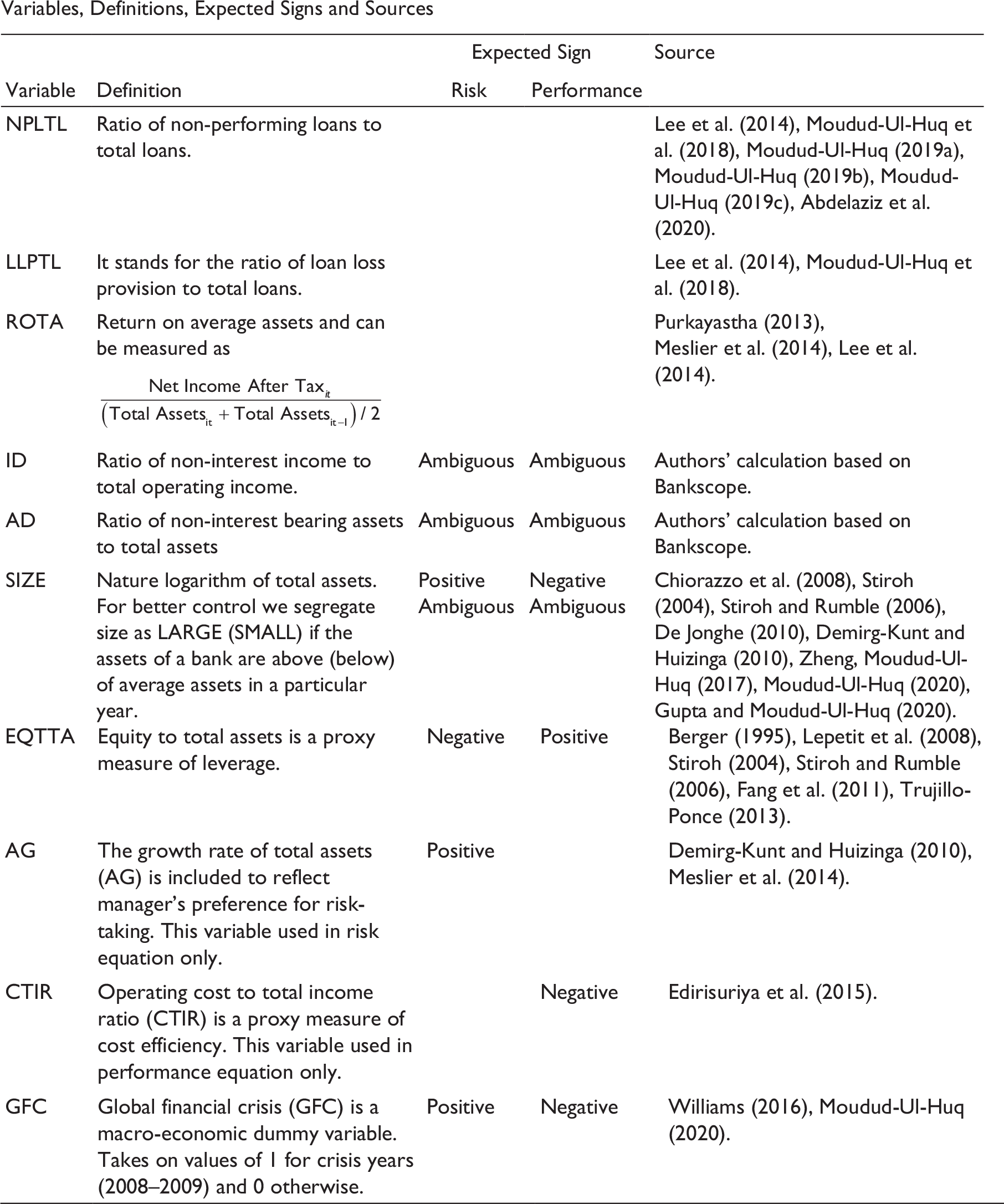

We introduce four classes of variables: (a) the measurement of bank risk, (b) the measurement of income diversification, (c) the measurement of bank performance and (d) control variables, which are explained in Appendix A.

Bank Risk Measures

In response to bank diversification, we have used credit risk as the main measure of risk that proxied by non-performing loans to total loans (NPLTL). Non-performing loans comprise of three components, that is, sub-standard, doubtful and bad or loss. The higher ratio of NPLTL indicates a riskier investment portfolio (Barth et al., 2004; Berger et al., 2005; ElBannan, 2015; Gonzalez, 2005). A loan loss provision of total loans (LLPTL) is used as an alternative measure of bank risk. A higher ratio of LLPTL indicates the ability of banks to absorb losses from total loans and advances and lower bank risk.

Bank Performance Measure

To measure the performance of a bank, we use the income statement return on average assets (ROTA). If portfolio diversification works, then higher ROTA may reduce the risk. In this study, we did not consider another alternative measure for bank performance because many regulators believe ROTA is the best measure to assess the bank performance (Hassan & Bashir, 2003; Rivard & Thomas, 1997). The main reason behind their argument is that ROTA is not distorted by high equity multipliers and reflects a better measure of the bank’s ability to produce a return from its assets portfolio.

Bank Diversification Measures

To verify the impact of bank diversification upon risk and performance, two measures of bank diversification are employed. By following Stiroh (2004a), Stiroh and Rumble (2006), Meslier et al. (2014), Edirisuriya et al. (2015) and Williams (2016); we use income diversification (ID) as the first measure of bank diversification as it reflects revenue portfolio diversification. The variable (ID) is equal to the proportion of non-interest income to total operating income, where non-interest income is the composition of fee-based revenue, related investment income and other non-interest income. On the one hand, operating income is the summation of net interest income 5 and non-interest income. A higher coefficient refers greater bank diversification on its revenues. For another measure of bank diversification, we employ assets diversification (AD), which is defined as the ratio of non-interest-bearing assets 6 to total assets. A higher ratio indicates a greater diversification of the bank’s assets portfolio. This measure is in line with Edirisuriya et al. (2015). However, if portfolio diversification holds, then it signifies better performance of banks with well-adjusted risk.

Empirical Research Framework

Prior literature implies that the relationship between bank risk and performance is an important area in the context of risk evaluation of banks. Bank risk-taking may be dependent on its performance. On the one hand, a better-performed bank often seeks additional risk than a poor one, ‘ceteris paribus’, while reverse consequence may occur if moral hazard hypothesis is in the driving seat and poorly performed banks have the inclination to take more risk based on risk-return trade-off. At the same time, the overall performance of bank may also be dependent on bank risk. Extra risks may produce additional pressure on management to execute decision regarding costs and diversification that impede the growth of performance. For example, sometimes it becomes more costly to control a high-risk project. In that case, bank risk is expected to have an adverse impact on performance. From the active risk-taking point of view, the bank can be rewarded through making a trade-off between risk and return. However, through diversification, bank can run for better performance with minimizing risk. Therefore, the bi-directional causality of the interplay between risk and performance along with bank diversification implies that it may be well matched in a simultaneous equation framework. But there is a dearth of literature that focused the impact of bank diversification on risk and performance, respectively. With very few studies such as Pennathur et al. (2012) and Williams (2016) consider diversification impact on bank risk and Lee et al. (2014), Curi et al. (2015), Edirisuriya et al. (2015) show the relationship between bank diversification and performance or efficiency. So, to show the significant effect of bank diversification on risk and performance together, we empirically specify the following equation along with the impact of GFC:

We run this regression equation separately for risk and performance. Where, the endogenous variable Yi,t represents: (a) non-performing loans to total loans (NPLTL) is the main measure of risk and loan loss provision to total loans (LLPTL) is used as an alternative measure of risk for robustness checks, and (b) return on average assets is a proxy measure of performance. Where, in equation subscripts, i refers the number of commercial banks (i.e., i =1, 2, …, 32 for Bangladeshi commercial banks and i = 1, 2, …, 16 for South African commercial banks); j covers the number of bank-level control variables, and t indicates period (i.e., t = 2004, 2005, …, 2015), β is the series of parameters to be estimated and

From the above control variables, we also put emphasis on size to allow the influences on risk and performance that stem from the different sizes of banks. This variable is considered as a significant determinant of return and risk taking of banks after the 2007–2008 global financial crises (Kaufman, 2014). Large banks are characterized as ‘too big to fail’ proposition, well diversified, highly levered, securitized, more volatile in return (Demsetz & Strahan, 1997; Hussain & Hassan, 2005). Besides, Saunders et al. (1990) empirically show that large banks have lower risk and lower variability of return when banks are regulatory optimized. Usually, large banks are mostly supported by regulators during a crisis,

8

where small banks tend to accumulate more capital ratios over the regulatory requirement to sustain during the crisis. Small-sized banks may lie on ‘conservative principle’ to survive during the crisis and generate profit through diversification. But particularly, there is no consensus of study which analysed joint effect of different size and diversification portfolio on risk and performance. Therefore, we extend our baseline equation (Equation [1]) by segregating size as LARGE and SMALL and examine an explicit effect of different size and bank diversification on risk and performance, respectively, in the following equations:

Here, the variable

However, the absence of prior literature on the joint effect of bank diversification and financial crisis motivate us to extend our baseline regression (Equation [1]) further. The financial crisis may badly weaken the financial health alone of the banking industry as evidenced by Williams (2016), but the joint interaction between the financial crisis and bank diversification may lead to appreciation in that case. So, the next equation is empirically constructed as follows:

where the variable

In the presence of lagged endogenous variables, the ordinary least squares (OLS) approach may produce biased and inconsistent estimates in the simultaneous equations. Note that in a panel data framework, the equations specify dynamic structures and there may have the existence of endogeneity, autocorrelation, and heteroscedasticity problem. That is why, to account for such potential issues, we use the generalized method of moments (GMM) estimator, which is also known as the system-GMM estimator, developed for dynamic panel models by Arellano and Bover (1995), Blundell and Bond (1998). Recently, this system estimator has been used by Lee et al. (2014) and Meslier et al. (2014). But both these studies have been limited to assess the relationship between diversification and performance. Moreover, to perform this estimator, we select white cross-section for GMM weights and coefficient covariance method, respectively.

GMM with cross-section random effect estimation has been used. 9 The random effect specification for our unbalanced panel observations is supported by the Breusch-Godfrey (Breusch, 1978; Godfrey, 1978) Lagrange Multiplier test (LM test), which rejects the null hypothesis that errors are independent within banks. A White test (White, 1980) is also applied to examine cross-sectional heteroscedasticity, and the null hypothesis of homoscedasticity is rejected at 5 per cent level of significance. We also carry out Hausman test of endogeneity for dependent variables and Hansen test for validating instruments and we cannot reject the null hypothesis that over identification restrictions are valid (results reported in bottom part of Tables 4–8). As we run regression independently for Bangladeshi and South African banks, we also depend on separate correlation matrix to trace multicollinearity problem. The highest correlation coefficient exists between AG and SIZE, which is 0.49 (CTIR and AG = −0.51) for Bangladeshi (South African) commercial bank’s Pearson’s correlation matrix. 10 The explanatory variables are free from multicollinearity problem as Kennedy (2008) confirms that multicollinearity is a challenge when the correlation is above 0.70, which is not in our case.

Empirical Results

Descriptive Statistics

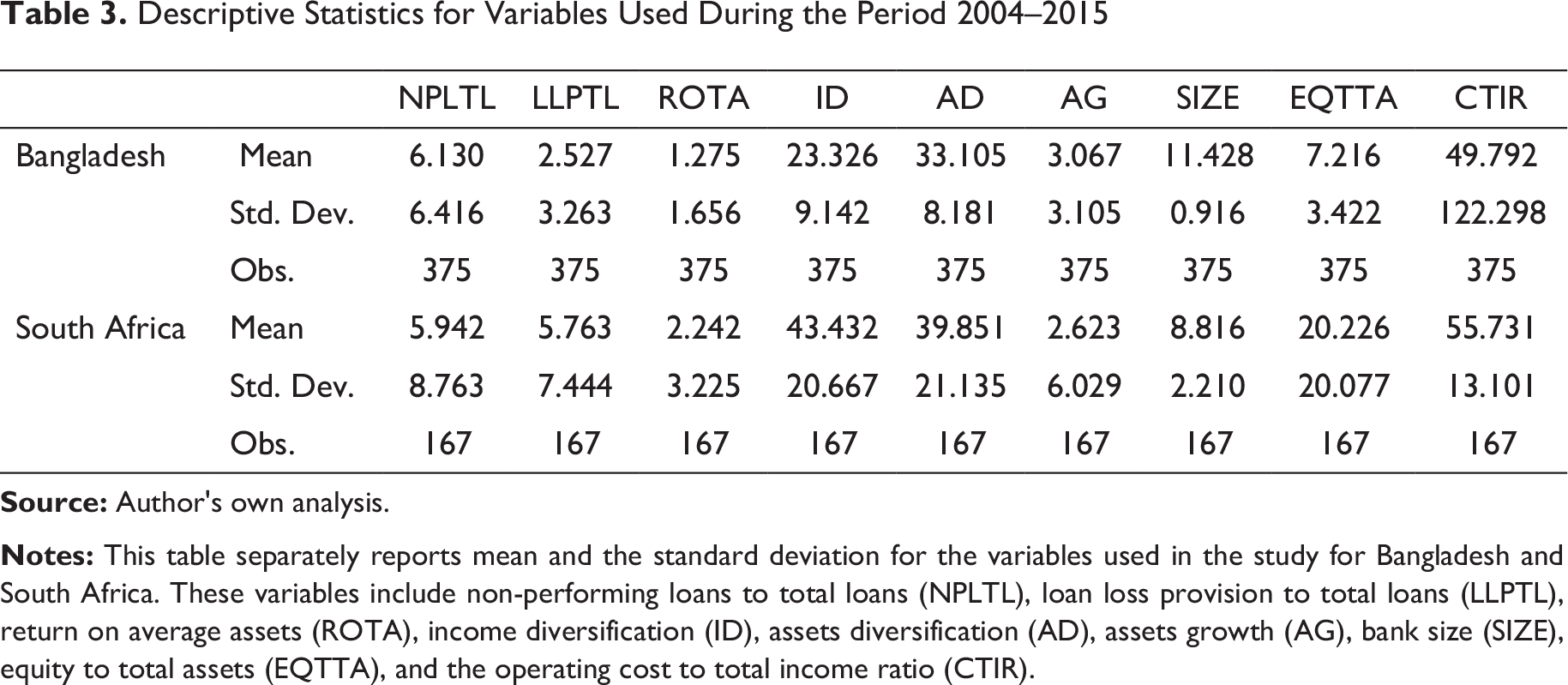

Descriptive Statistics for Variables Used During the Period 2004–2015

Influence of Bank Diversification on Risk and Performance

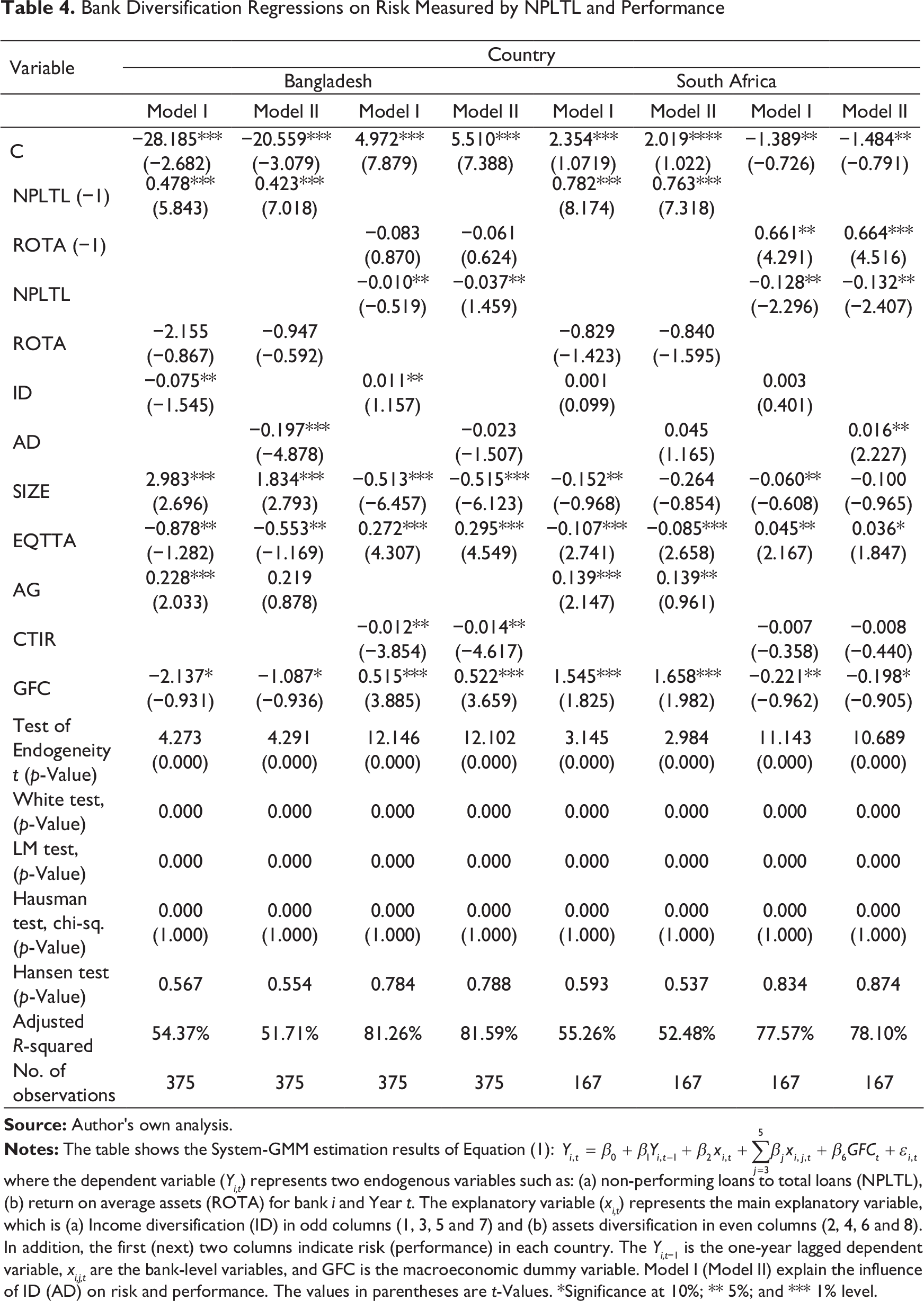

The baseline regression (Equation [1]) is used to analyse the impact of bank diversification on risk and performance, respectively, through two models, confirming that the persistent coefficients of risk in both countries are positively significant, meaning that risk will be maintained from one year to the next. This result is consistent with Lee et al. (2014). In contrast, the performance of commercial banks is not persistently determined in Bangladesh (Table 4, columns 3–4). In both countries, regression reveals that credit risk significantly deteriorates the growth of bank performance (columns 3, 4, 7 and 8). It also appears that the level of risk cannot be determined through better performance, as the coefficients of ROTA are insignificant in the models. When we consider Model I, the ratio of income diversification (ID) is negative with risk (Lee et al., 2014) and positive with performance (Chiorazzo et al., 2008; Meslier et al., 2014), which is consistent with our Hypothesis 1 and 2. But South African banks are evidencing that there is no such relationship between risk and performance. It indicates that Bangladeshi commercial banks are well diversified in risk through shifting traditional interest business to non-interest and determination of risk and performance of South African banks are not a function of income diversification. So, income diversification of South African commercial banks fails to significantly reduce (raise) the bank risk (performance) and experienced as less developed non-traditional activities (Nguyen et al., 2016). In the case of assets diversification (AD), Model II refers that Bangladeshi (South African) commercial banks significantly invest in non-interest-bearing assets to minimize (maximize) risk (performance). But these assets, viewing no significant relation with performance (risk) of Bangladeshi (South African) banks. This result partially is in line with Edirisuriya et al. (2015) who consider South Asian banks and showing no significant impact of assets diversification on market-equity to book value equity, market Z-score other than the negative impact on stock return volatility. They also predict that in emerging economies, there might be a scarcity of high-yield non-interest-bearing assets; that is why banks run for income diversification to improve performance.

Bank size of Bangladeshi commercial banks is positively (negatively) significant in risk (performance), which is indicated in columns 1 and 2 (3 and 4). This result is in line with recent studies (e.g., Demirg-Kunt & Huizinga, 2010; Edirisuriya et al., 2015; Sufian & Habibullah, 2009) and reverse from Meslier et al. (2014) and Williams (2016). On the one hand, the larger the South African banks, the lower the risk and performance as well, which signifies the risk aversion attitudes by deteriorating profit. These different attitudes of emerging economies banks motivate us to test further regressions (Equations [2] and [3]) based on size and diversification effect. This may enable us finding the effects of size with diversification on bank risk and performance.

Bank Diversification Regressions on Risk Measured by NPLTL and Performance

The coefficient of assets growth (AG) is evidenced that banks of emerging economies with lower risk aversion grow rapidly and have different operating strategies. However, the dependency of performance on the operating cost to total income ratio (CTIR) is negative and significant (insignificant) in Bangladesh (South Africa) (at the 5% level), indicating that more cost effective banks are more favorably performed in the market. More interestingly, during the GFC, the banking sector of Bangladesh proactively reduced risk and produced a return. Hence, the coefficient of GFC is negatively (positively) associated with risk in both models. The relation could be the causes of (a) voluntary adoption of Basel II and (b) introduction of financial reforms regarding reserve ratio, introducing corporate governance, etc. Apart from this, South African commercial banks much hit hard by financial crisis during 2008–09 that supports the positive (negative) coefficient of GFC (columns 5–8).

Joint Effect of Bank Size and Bank Diversification

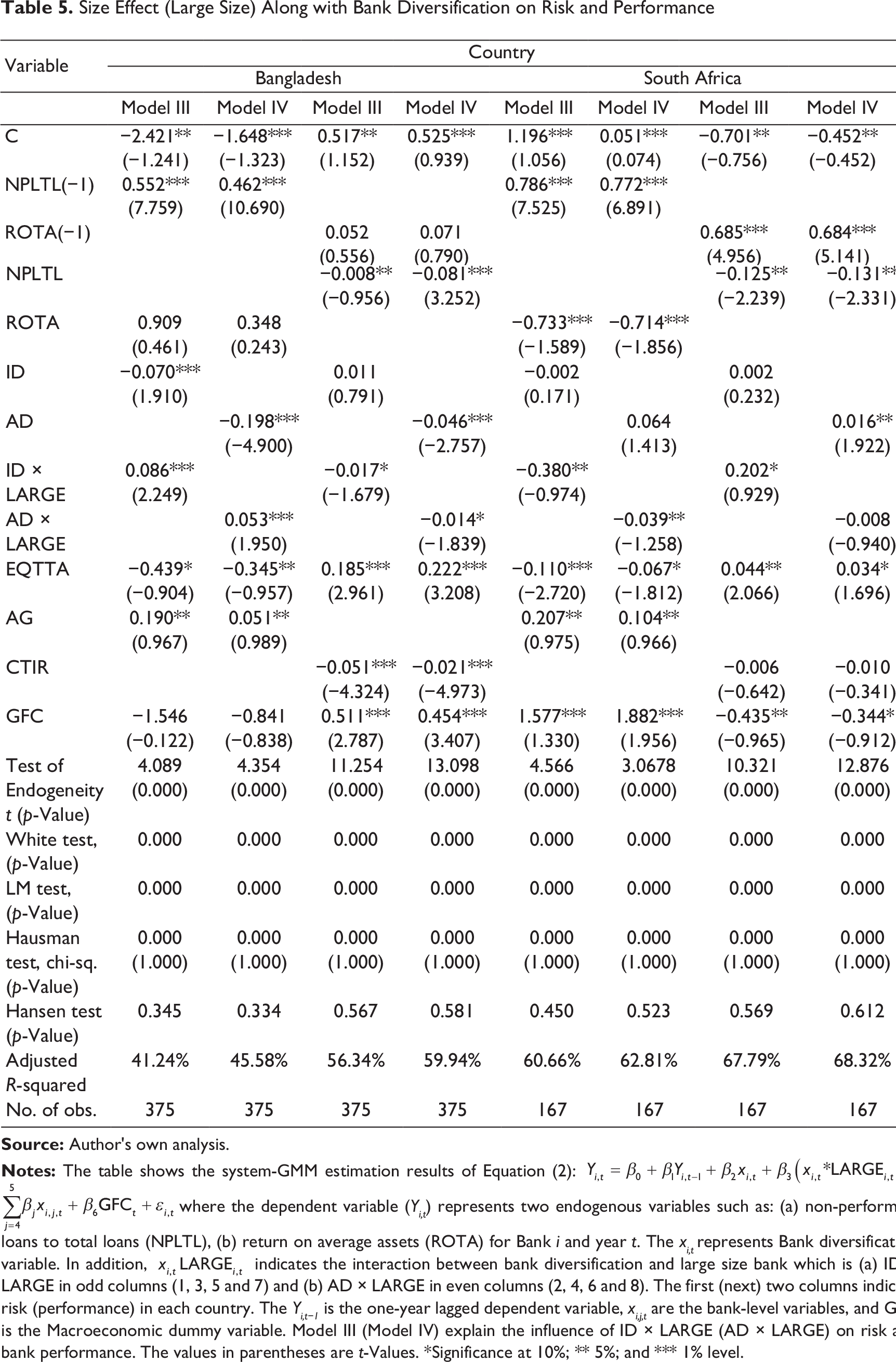

Size Effect (Large Size) Along with Bank Diversification on Risk and Performance

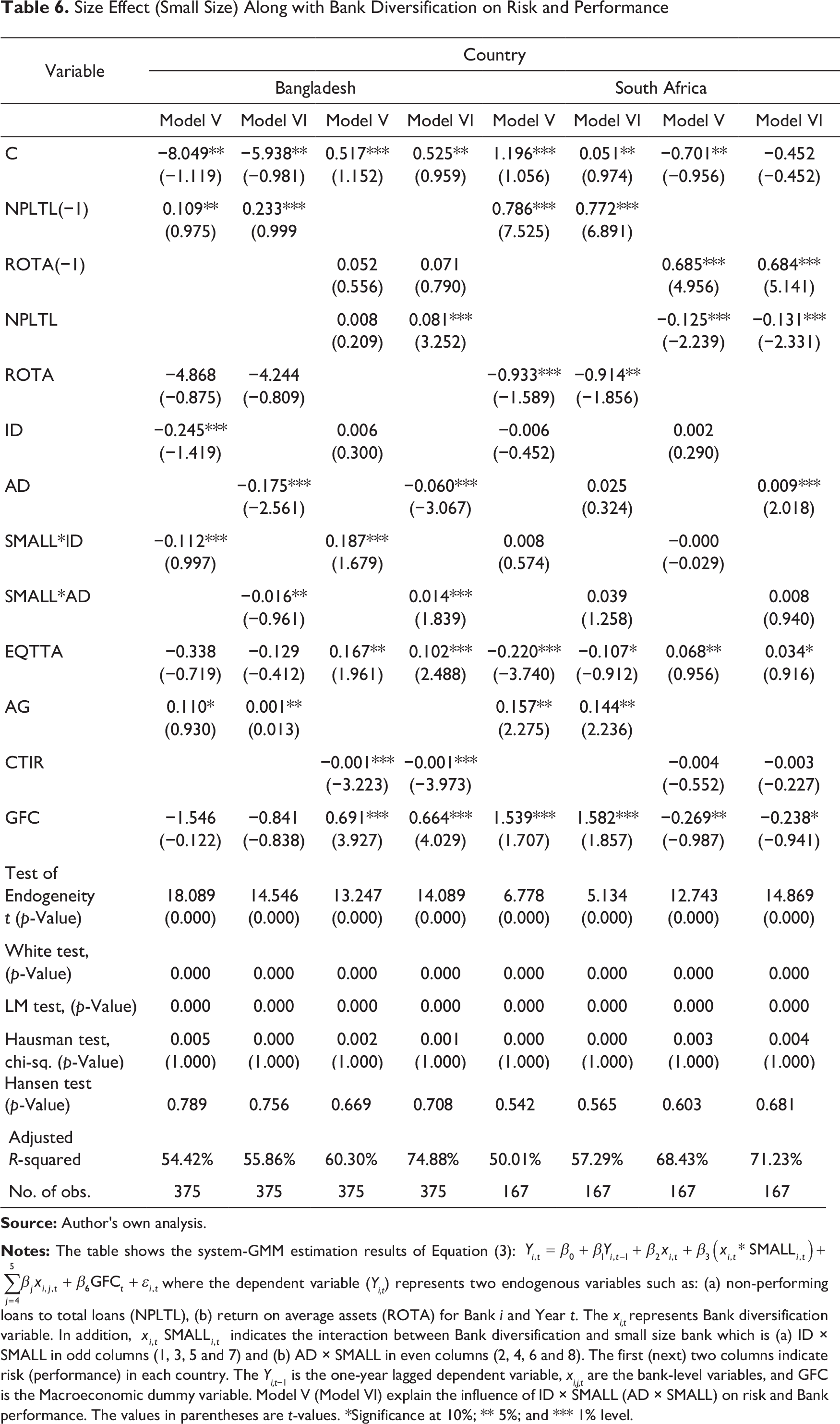

Size Effect (Small Size) Along with Bank Diversification on Risk and Performance

In a nutshell, the above results partially agree with the assumption of Edirisuriya et al. (2015) that there is a scarcity of high-yield non-interest-bearing assets in emerging markets that force banks to rely heavily on income diversification and other means of non-traditional income to diversify risk and improve market performance. But in our case, small banks of Bangladesh have the opportunity to rely on assets diversification along with income diversification in their portfolio mix of income generation.

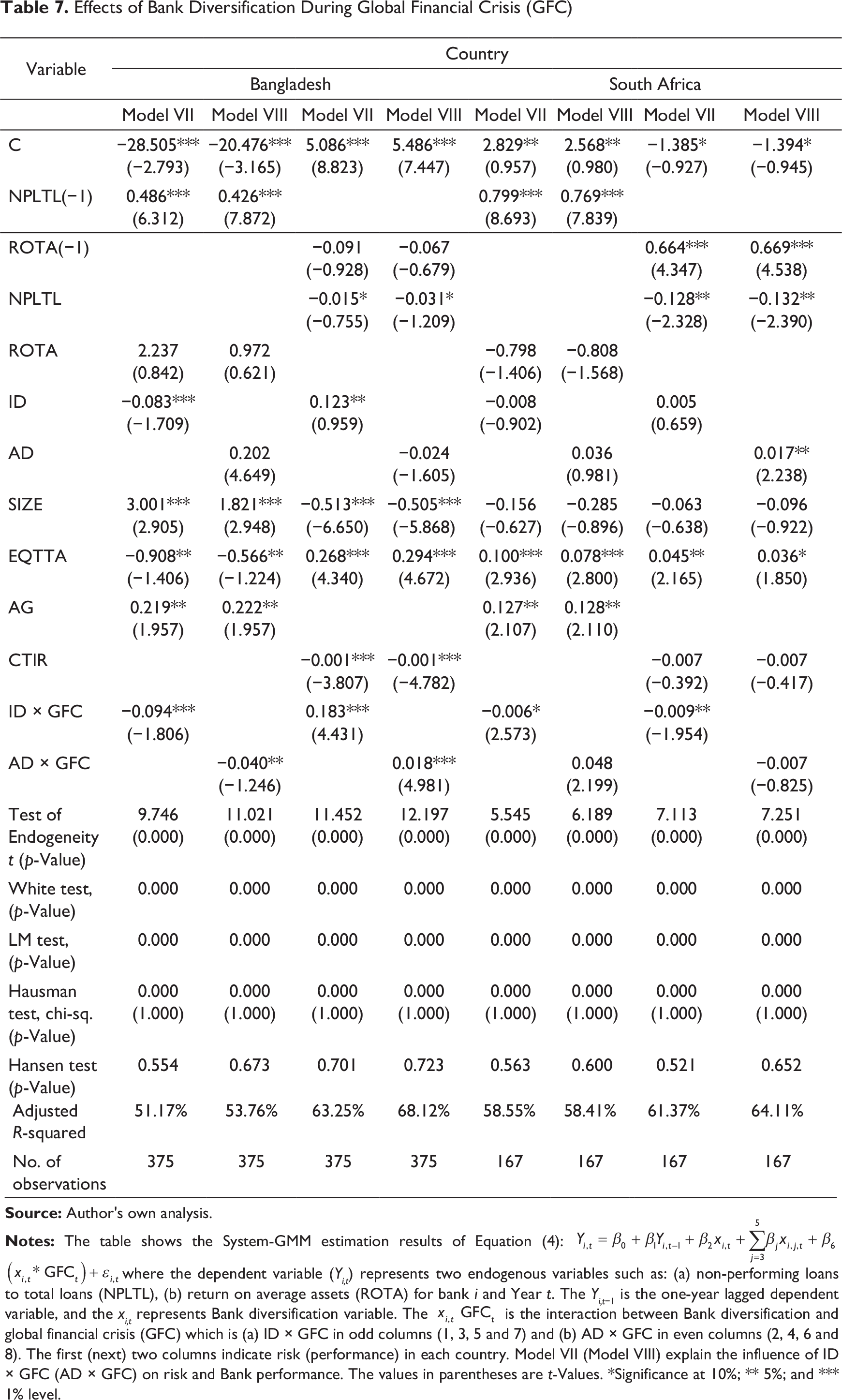

Joint Effect of Bank Diversification and Global Financial Crisis

Under this caption, we extend our article from Williams (2016) and DeYoung and Torna (2013) that given new heights of attention on bank diversification effect during the financial crisis in emerging economies other than developed countries. Hence, Table 7 exhibits such effect for measuring the bank risk and performance of two emerging economies.

Effects of Bank Diversification During Global Financial Crisis (GFC)

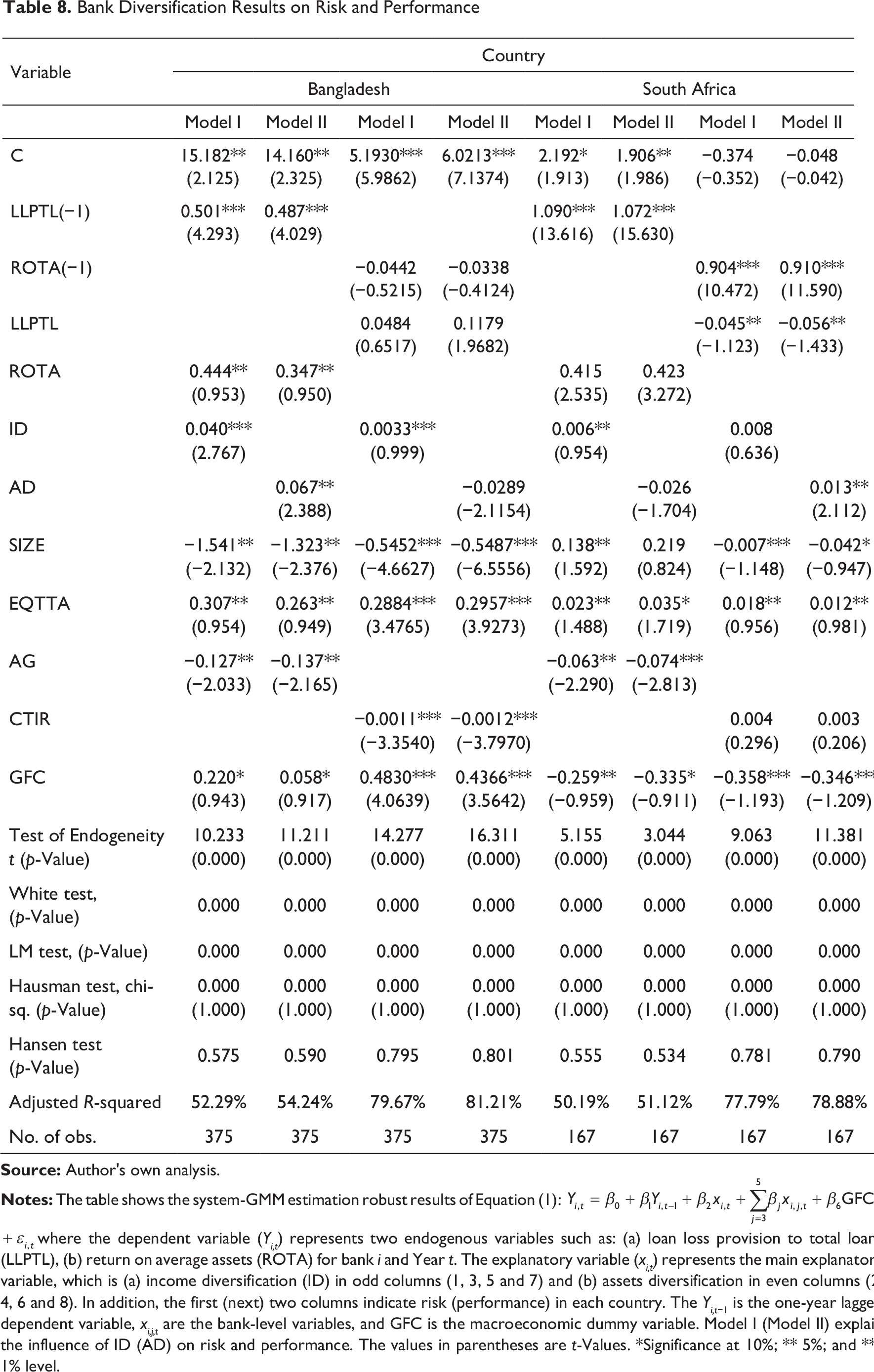

Robustness Checks

Bank Diversification Results on Risk and Performance

The key results are robust after considering an alternative measure of bank risk. The evaluation results for coefficients of bank diversification are plausible with a few exceptions to the previous results, for example, income diversification has a significant positive impact on loan loss provision to total loans (Table 8, column 5), indicating South African bank achieves greater stability through income diversification and higher assets growth (AG) raise the probability of bank failure (columns 1, 2, 5 and 6). Besides, the larger the bank size, the greater bank failure evidenced in Bangladesh, which support ‘too big to fail’ hypothesis. But South African banks are more fragile in profitability although their banks are so stable with their size (Table 8, columns 7 and 8) and consistent with Table 4 regression results. This could be placed due to bureaucratic involvement in the management (Eichengreen and Gibson, 2001).

We further analyse Equations (2)–(4) consecutively to check robustness for the joint effect of bank diversification and size and bank diversification and GFC on risk and bank performance. 14 However, in all models, the coefficients of the lagged dependent variables, that is, LLPTL (t-1) and ROTA (t-1), are consistent with prior results. Other control variables also retain their signs like Tables 4–7. Finally, higher R-squared values signify the explanatory power of the models.

Conclusions and Policy Implications

In this article, we study the effect the bank diversification has on the risk and performance of commercial banks in two emerging countries. Overall, this article highlights key points into three phases. First, because of the scarcity of high-yield non-interest-bearing assets, income diversification of Bangladesh commercial banks has significantly reduced (improved) bank risk (performance) over assets diversification that cannot improve bank performance. And the South African context combining income and assets diversification fails to generate any portfolio diversification benefit. On this ground, it may be true that the higher dependency on non-interest income 15 is riskier than interest income, as increased agency cost outweighs diversification benefits. 16 Though South African banks are stable as Bangladeshi banks they do not enjoy many benefits from portfolio diversification as failing to utilize non-interest-bearing assets through other means to improve market performance. Second, apart from the different size of banks, large banks are greatly diversified, less stable and less performed, while small banks have enjoyed more benefit entails from portfolio diversification with higher bank’s stability in Bangladesh. Whereas, large South African banks get more benefit of bank diversification with greater stability over small-sized banks. Finally, the levels of profitability raised gradually with controlled risk from continuous bank diversification were the main characteristics of Bangladeshi financial environment between 2008 and 2009. But the South African point of view, the higher dependency of non-interest income was a key instrument to combat with a massive financial catastrophe during that collapsed period.

However, based on the empirical findings, we propose some policy suggestions. First, it seems that diversification effects are heterogeneous in emerging economies. Bangladeshi commercial banks get higher diversification benefit from its non-interest income, and they should shift their traditional income to non-interest as much as possible. Notably, the South African banks need to be more watchful in the execution of diversification policy and avoid taking extensive practice in scale. As higher dependency on non-interest income generates additional risk itself, high-yield non-interest-bearing assets are yet to be explored in emerging markets. Second, much restructuring is required for large banks to introduce diversification strategy in Bangladesh as these banks are risky and less performed and small banks should be emphasized and encouraged. Whereas, large-size banks of South Africa can improve their diversification benefits especially from non-interest income and policymakers should pay much more attention to the development of small banks. They can provide an alternative package of guidelines for improving small bank’s performance. Third, income diversification is vital for both countries to deal with financial crisis. Finally, each country should give priority to non-performing loans and keep ratio as minimum as possible. As the continuous growth of this ratio is blamed for higher risk, poor performance and bank’s instability, before implementing diversification strategy in banks, emerging economies should comprehensively consider their resources, size and ability to deal with risk.

Appendix A

Variables, Definitions, Expected Signs and Sources

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.