Abstract

This article assesses the causal relationship between outward foreign direct investment (FDI) and various sides of firm performance, using micro data from Portuguese manufacturing firms during 2006–2014. To control for the possible endogeneity of outward FDI strategies, propensity score matching is combined with difference-in-difference approach. Our analysis shows that the learning effects for parent firms in Portuguese manufacturing depend on the underlying outward FDI strategy. The findings suggest that outward FDI could contribute to enhance firms’ productivity and their scale of operations. However, those learning effects seem to be mostly visible when firms engage in vertical outward FDI. Further, outward FDI, vertical or horizontal, appears to enhance the integration of Portuguese firms into the global economy through increased export intensity. From a managerial and policy perspective, the findings support the argument that outward FDI can indeed be at root of upgrading performance and firm’s restructuring in a small, open and peripheral economy such as Portugal.

Introduction

Outward foreign direct investments (FDI) from Portuguese firms is a quite recent phenomenon. It took off mainly in the 1990s with the Portuguese authorities electing the internationalization of firms as a political goal. Portugal is not a unique case, as, by that time, outward internationalization had become an increasingly important target of public intervention in most Organization for Economic Co-operation and Development (OECD) countries (UNCTAD, 2001). Therefore, Portugal joins the group of latecomers of outward FDI, replicating the pattern of evolution of the most developed countries. More recently, several public incentives and legal instruments relevant to outward internationalization had been enacted and implemented. The impact of such home country support measures towards internationalization is visible in the slightly upward time trend in Portuguese outward FDI. At the end of 2014, Portuguese outward FDI stock was equivalent to 24 per cent of GDP.

The existing studies on Portuguese outward FDI have mostly focussed on the analysis of the drivers of outward FDI. They mostly investigate whether the growth of outward FDI results from a new strength of Portuguese firms and the need to exploit firm’s competitive advantage, or it mainly represents a loss of comparative attractiveness of the domestic location and hence the need to develop firm’s competitive advantage by accessing advanced knowledge and capabilities. Understanding firms’ internationalization strategies and home country-specific context is a topical issue that fosters stimulating research around the world. See, for instance, Bruhn et al. (2016) for the case of developing countries.

Apart from the determinants of outward FDI, to examine whether outward FDI is a catalyst for upgrading firm’s performance is an important issue, as frequently trade policies heavily rely on the extent of learning/upgrading of outward FDI. Micro-level evidence for supporting such policies is therefore topical and deserves further attention. If there are no rewards at micro-level, and hence no macroeconomic consequences, then policies designed to foster internationalization, in particular outward FDI, may be wasting resources.

The remainder of the article is structures as follows: the second section presents and discusses the relevant literature review and theoretical framework, followed by the study’s objectives. The fourth section describes the main data set used in the empirical analysis, presents the empirical strategy and results related to key factors that drive selection into outward FDI. The fifth section outlines the empirical strategy for examining learning effects from outward FDI and discusses the corresponding empirical results. The final section concludes the article by highlighting the main findings, managerial and policy implications and avenues for future research.

Literature Review and Theoretical Framework

Similar to knowledge spillovers, as a form of technology transfer from inward FDI (see, for instance, Djulius, 2017), the effects on productivity, as a result of gaining experience and obtaining new knowledge from outward FDI, may be positive. Firm’s investments abroad provide increased competitive pressure and new business opportunities. They might obtain superior technology or knowledge, or they may achieve total cost reduction by using low-priced production factors. These learning/upgrading effects may raise firm’s productivity. Previous studies examining outward FDI effects on local firms are not fully unanimous, as they do not necessarily succeed in detecting a positive causal effect on firms’ productivity (Hayakawa et al., 2012). Nonetheless, some empirical findings suggest that there are positive learning effects that provide performance upgrading at home. Navaretti and Castellani (2004) and Imbriani et al. (2011) for Italian manufacturing firms, Wei et al. (2010) for Chinese firms, Ito (2015) and Hayakawa et al. (2016) for Japanese firms Hijzen et al. (2011) for French firms, among others, claim positive impact of outward FDI on parent firms productivity. However, other works analysing the learning effect in investing abroad fail in detecting a positive and significant causal effect (see, for instance, Damijan et al., 2014; Hijzen et al., 2007) for manufacturing firms.

In addition to productivity, there are empirical works analysing the impacts of FDI on production, exports, investment, employment and skilled labour composition (see, for instance, Castellani et al. (2008), Navaretti and Castellani (2004) and Navaretti et al. (2010) for Italian firms; Navaretti and Castellani (2004) and Hijzen et al. (2011) for French firms and Hijzen et al. (2007) for Japanese firms). Most of the works report considerable heterogeneity of the effects of outward FDI on production, exports, investment, employment and skilled labour composition with regard to host countries, industries and types of investments. If outward FDI improves firm’s productivity and simultaneously there is heterogeneity on other measures of firm operations, this would suggest that firms undergo a deep restructuring process. Therefore, in order to derive meaningful conclusions regarding the effects of outward FDI, more detailed analyses are required. This study explores a causal link between outward FDI and different aspects of firm operation in order to assess whether outward FDI causes the parent firm to undergo restructuring processes and to upgrade performance.

Objectives

Our analysis differs from the existing literature in three respects. First, rather than focusing on a narrow outcome of upgrading performance, a wider range of outcomes, which can potentially be driven by outward FDI decisions, are addressed and interrelated to understand what kind of restructuring process outward FDI could be fostering. Second, we examine firms in a small, open and developed economy, but within the context of the European Union (EU), it is a peripheral economy that traditionally was being a net receipt of FDI. The more recent propensity of Portuguese firms for outward FDI offers a rich and yet unexplored context to add understanding on the consequences of the globalization of firm activities. In particular, it allows us to seek further knowledge on key factors that yield heterogeneity in selection and learning effects. Third, the implications of outward FDI are examined for different qualitative FDI types: horizontal outward FDI (H_OFDI) and vertical outward FDI (V_OFDI). Unlike previous studies examining qualitative differences between H_OFDI and V_OFDI, which rely mainly on host country differences (see, for instance, Debaere et al., 2010; Hijzen et al., 2011; Navaretti et al., 2010), in this study, the distinction between H_OFDI and V_OFDI is based on each pair of parent firm and overseas affiliates at two-digit industry level. H_OFDI is recorded if parent firm has overseas affiliates that operate in the same two-digit industry; otherwise, it is recorded as V_OFDI.

The empirical analysis proceeds in several steps. Firstly, domestically owned manufacturing firms were identified and examined whether they hold subsidiaries abroad, the indicator of outward foreign investments being made. Secondly, the assessment of the effects of outward FDI on the evolution of firm performance across Portuguese multinational enterprises (MNEs) and pure domestic firms is carried out.

Disentangling correlation and causality in the context of FDI poses numerous challenges. The chief challenge in identifying outward FDI effects is selection. If Portuguese MNEs are not representative of the universe of Portuguese firms, subsequent heterogeneity in the evolution of firm performance might not be attributable to outward FDI as it was well documented by, for instance, Arnold and Javorcik (2009) and Hijzen et al. (2013) in the case of ownership changes. To mitigate this threat to identification, we examine the effects of outward FDI using the propensity score matching technique combined with difference-in-difference estimators. The matching technique creates the missing counterfactual of a MNEs had it remained purely domestic. For that, Portuguese MNEs were paired up with a pure domestic firm with very similar observable characteristics, which have power to explain outward FDI decisions at firm level. Therefore, our empirical strategy has an explicit focus on the direction of causality and allows us to control for time-invariant observables and unobservable differences between Portuguese MNEs (treated firms) and pure domestic firms (the control group). Our difference-in-difference inferences on the matched sample comprise 319 outward FDI cases. For each case, the type of outward FDI (H_OFDI versus V_OFDI) is assessed.

Our analysis, based on manufacturing firm-level data from Amadeus, covering the period 2006–2014, shows that the learning effects for parent firms in Portuguese manufacturing depend on the underlying outward FDI strategy. Having overseas subsidiaries seems to have no effect either on productivity (either total factor productivity or labour productivity) or on export intensity. The positive changes taking place in the parent firms are in terms of investment, capital–labour ratio and total assets per employee. These findings suggest that outward FDI leads to some restructuring in parent firms, mainly in terms of the transfer of know-how and technology, which do not always engender upgrading productivity. Looking at outward FDI-types, parent firms with V_OFDI seem to engage in a more profound restructuring process (either in terms of employment, skill composition and investment) that leads to upgrading performance, which becomes visible in increasing productivity and export intensity.

Methodology

Data

The empirical analysis in this article draws mainly on data from Amadeus, covering the 2006–2012 period. This data set is collected yearly from official business registers, annual reports and other complementary sources. The firm-level records include information on number of employees, industry code, geographical location, detailed balance sheets and profit and loss account. This extent of information allows us to compute total factor productivity (TFP), labour productivity and other aspects of firm operations. More importantly, the data show full list of shareholders and subsidiaries, which allows us to identify pure domestic firms and Portuguese MNEs.

One of the key variables of interest is firm productivity. TFP has been obtained as the residual from industry-specific estimation of a logarithmic Cobb-Douglas production function, in which firm’s add value is regressed on labour inputs measured as the number of employees, on the book value of tangible fixed assets that account for capital, and intermediate inputs comprising materials, energy and other goods and services used in production. Using information available in Eurostat, all variables have been deflated using industry-specific price indices for added value, a price index for investment goods for capital stocks and a general producer price index for intermediate inputs. The production function has been estimated using the semi-parametric estimator suggested by Levinsohn and Petrin (2003). We are able to obtain TFP for about 148,000 firm observations, providing a large choice of control units for the matching procedure.

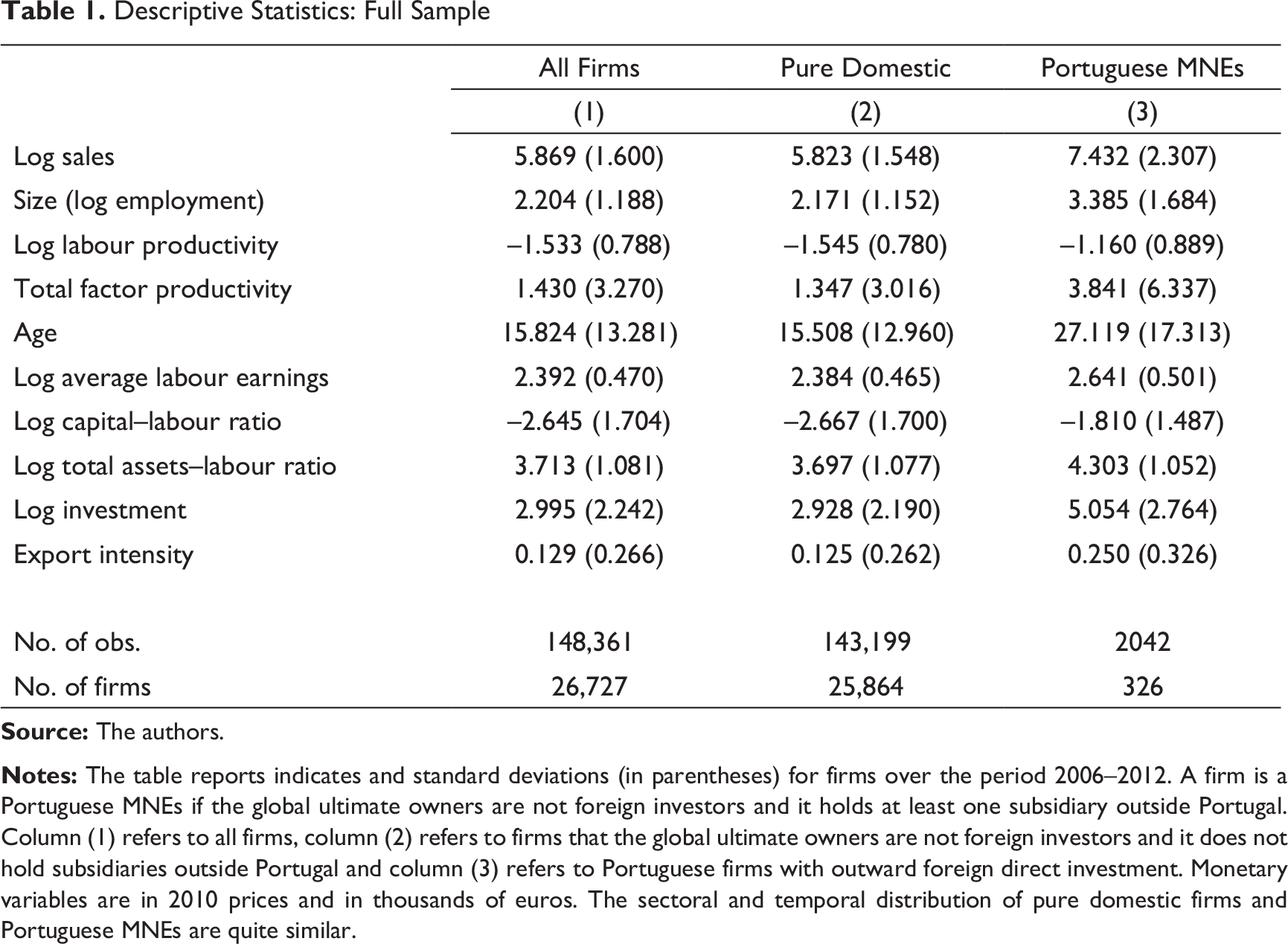

A firm engaging in outward FDI is designed as a Portuguese MNE. It occurs if the global ultimate owners are not foreign investors and it holds at least one subsidiary overseas over 2006–2012. Using that criterion, we have data on 326 Portuguese MNEs. Table 1 reports descriptive statistics on the full sample used in the estimation. Column (1) reports statistics on the universe of firms that was possible to get TFP estimates. The other two columns distinguish between firms owned by Portuguese investors and with no overseas subsidiary and firms owned by Portuguese investors and with at least one overseas subsidiary.

Descriptive Statistics: Full Sample

Overall, the descriptive statistics reveal that Portuguese MNEs tend to be larger, older, more productive, pay higher average wages and are more integrated into the global economy through higher export intensity than pure domestic firms. Further, Portuguese MNEs seem to invest significantly more in fixed assets than domestic ones. Or, alternatively, one can interpret this finding as indicating that Portuguese firms with better capital intensity are more prone to invest abroad. Given the similar sectoral distribution of firms among pure domestic firms and Portuguese MNEs, with the five most represented sectors being NACE25—manufacture of fabricated metal products, NACE10—manufacture of food products, NACE23—manufacture of other non-metallic mineral products, NACE16—manufacture of wood and of products of wood and cork and NACE14—manufacturing of wearing apparel, the explanation on these differences can hardly be routed on the sectoral composition. In fact, these differences seem to reflect initial heterogeneity in firm-specific characteristics among pure domestic and Portuguese MNES as well as change induced by outward FDI. Therefore, the estimation strategy has to control for selection bias and to be able to disentangle self-selection effects from learning effects.

Estimation Strategy

In order to create the missing counterfactual of a Portuguese MNE had it remained pure domestic (i. e., concentrating all operations in Portugal), we firstly explore the patterns of selection into overseas operations. Evidence from several previous studies (e. g., Antras & Yeaple, 2014; Grossman et al., 2006) suggest that parent’s scale, whether measure through either employment or sales, and productivity are key drivers of the self-selection of firms into outward FDI. Further, our data reveal substantial performance premiums in terms of productivity and scale of operations associated with firms with overseas subsidiary.

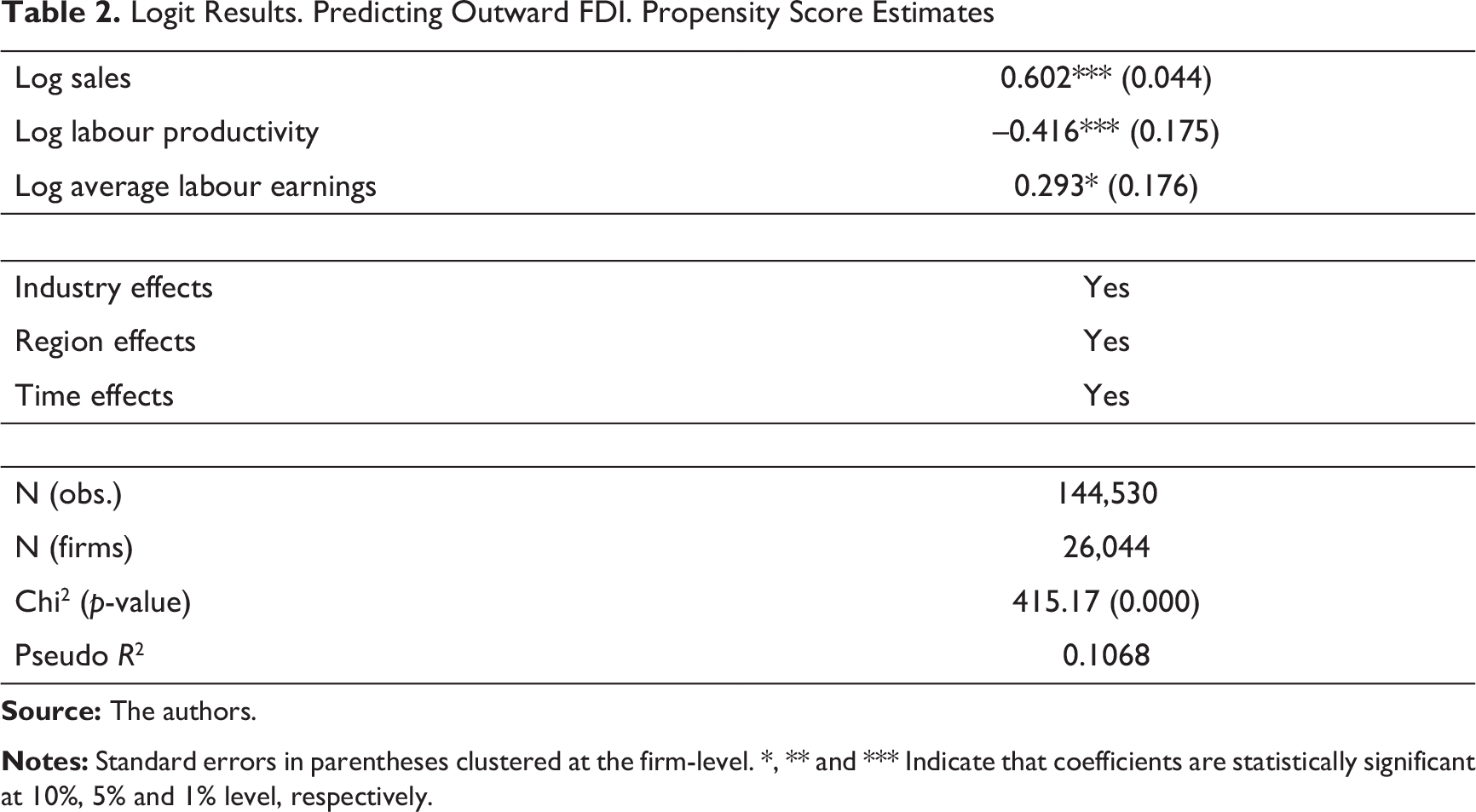

As a first step to disentangle correlation and causality in the context of outward FDI, we model empirically the probability a firm becoming a multinational enterprise, which is the basis to predict the propensity scores of being a Portuguese MNE. We do so by estimating a logit model of the binary outcome of a firm becoming multinational with observable firm-specific characteristics (sales and productivity) that would be expected to drive an outward FDI decision. To account for potential differences on firm-specific characteristics across industries, those explanatory variables are demeaned to the industry. We also include industry, region and time-specific effects to account for the role of idiosyncratic shocks at those three dimensions. Table 2 reports the results from estimation of the probability of becoming a Portuguese MNE, or the propensity score, which forms the basis of our matching procedure.

Logit Results. Predicting Outward FDI. Propensity Score Estimates

Overall, the results indicate that Portuguese MNEs differ systematically from pure domestic firms. The estimated model suggests that Portuguese MNEs tend to be larger firms. They also indicate that, conditional on size and labour productivity, firms with higher average labour earnings, which can be seen as a proxy to skill composition, are more likely to hold overseas subsidiary. Conversely, the estimates suggest that better performers, in terms of labour productivity, are more prone to be pure domestic firms. However, this result should be read with caution, as it is conditional on size and labour earnings. In fact, the negative sign of the point estimate on labour productivity may be explained by the fact that the logit model includes simultaneously three different, but positively correlated, observable firm-specific characteristics. The inclusion is justified on the grounds that they all reflect relevant heterogeneity between pure domestic and Portuguese MNEs. As the goal was to estimate the propensity score, and not looking at explanatory power of each variable, we have included them simultaneously.

Based on the propensity score, we match treated firms by year and industry, using one-to-one nearest neighbour matching without replacement. We impose an additional requirement that excludes observations outside the common support. The lowest propensity score of a treatment observation and the highest propensity score of a control observation binds the common support. The final matched sample comprises 319 Portuguese MNEs and 1714 pure domestic firms.

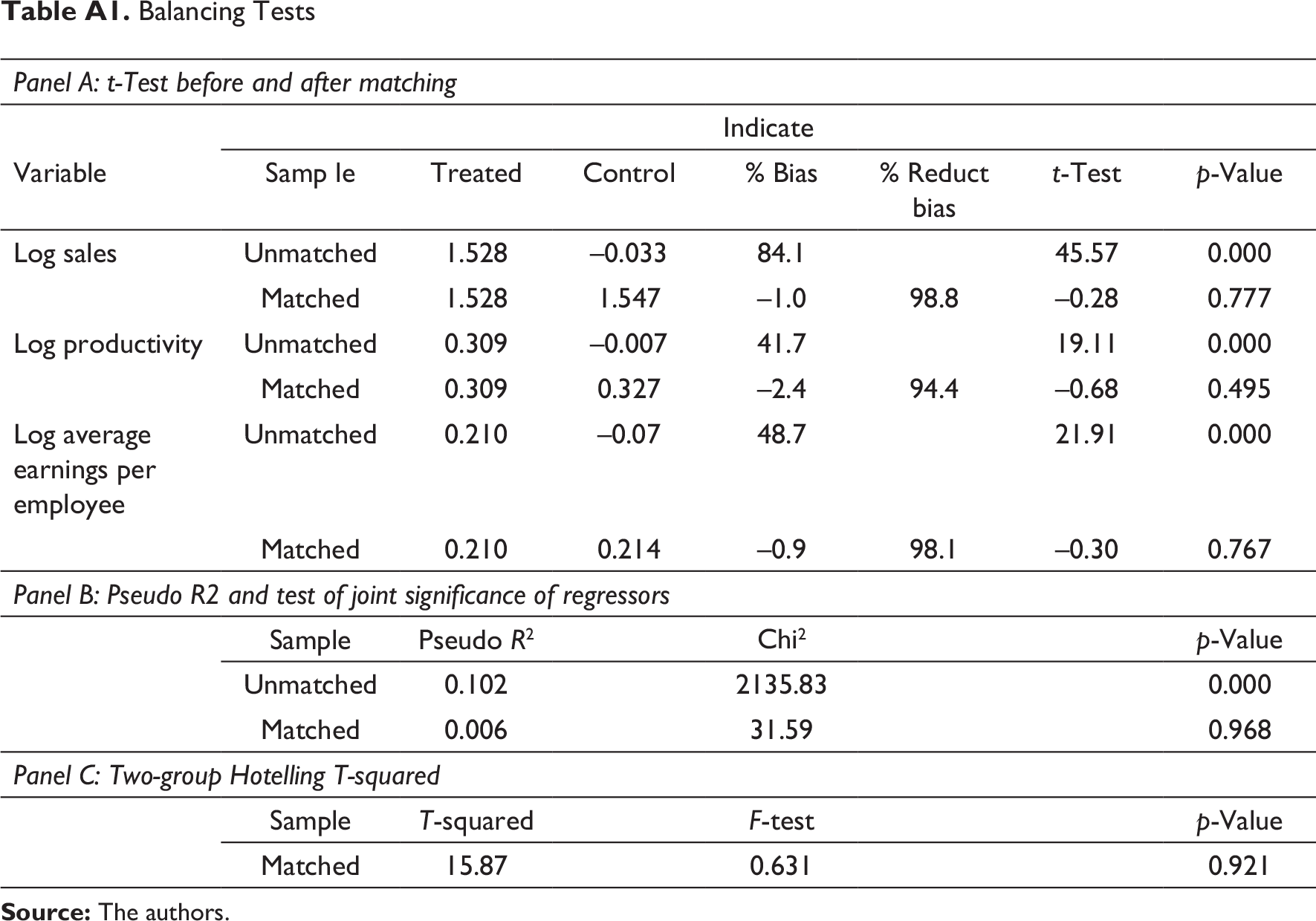

To assess how well the matching procedure performs in our case, several tests of the balancing hypothesis were carried out. Table A1 reports results from tests of matching quality. All individual t-tests and the two-group Hotelling t-square test never reject the mean equality of observable firm-specific characteristics between pure domestic and Portuguese MNEs in the matched sample. Moreover, the very small magnitude of the Pseudo R2 of the logit on the matched sample and the Chi-square test for joint significance of regressors give us confidence that our approach is capable of grouping together relatively homogenous firms.

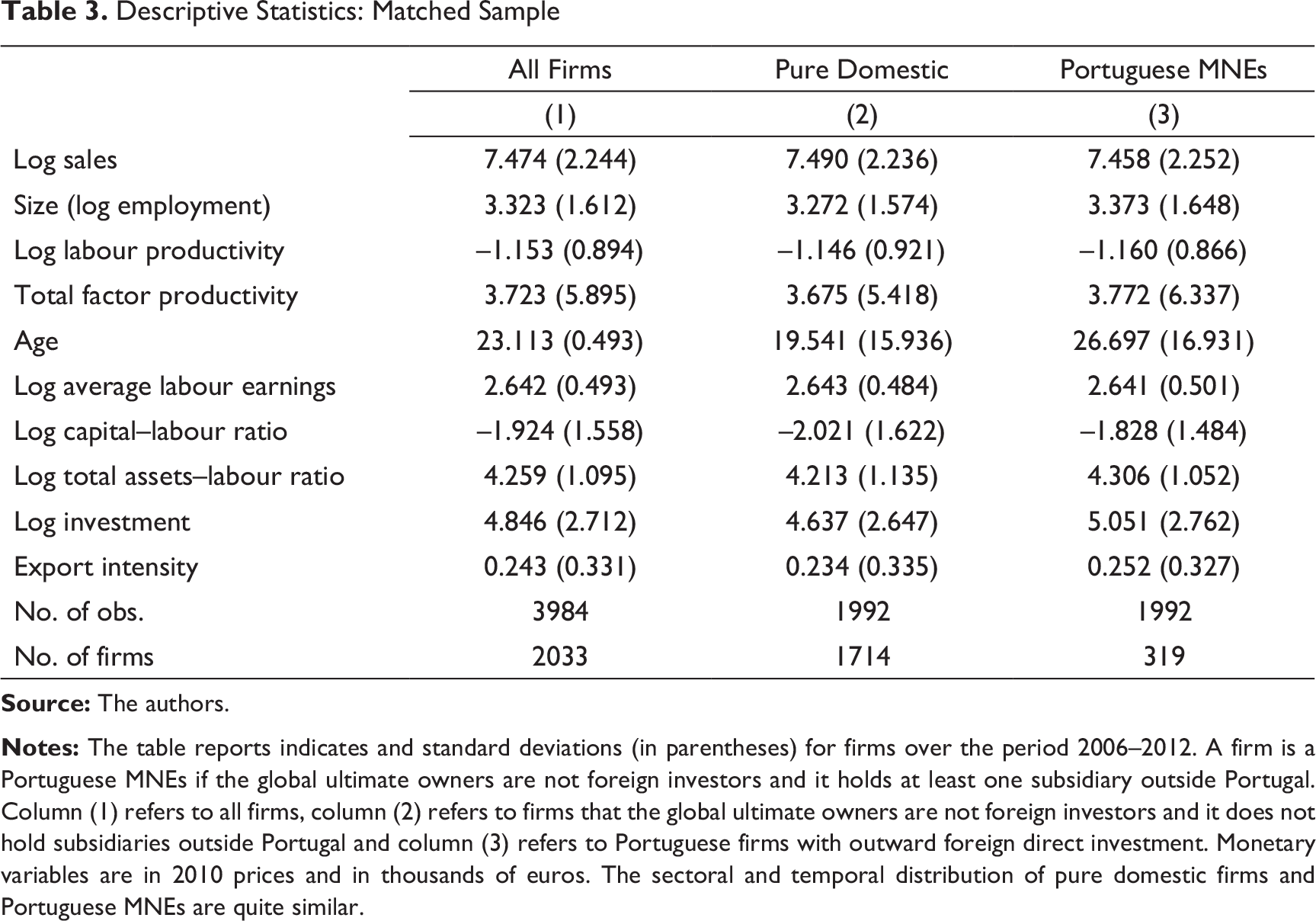

Another way to assess the overall quality of the matching procedure is looking at descriptive statistics for the sample of matched firms and comparing it with those for the full sample. Table 3 reports summary statistics for the sample of firms (treated and control) that were similar among a number of key observable firm-specific characteristics.

Descriptive Statistics: Matched Sample

In the matched sample, pure domestic and Portuguese MNEs are clearly more similar along the set of observable and measured firm-specific characteristics. The matching procedure removes almost initial heterogeneity across firms along a number of firm-specific characteristics. Notice, however, that some differences remain, given that outward FDI would affect how these firm-specific characteristics evolve over time. Moreover, the sectoral distribution of the matched sample is similar to the full sample, indicating that there is no a sectoral bias affecting firm-specific characteristics and performance.

Analysis and Discussion

Here, we proceed by assessing and discussing the effects of outward FDI on parent-firm performance and restructuring. For each outcome of interest, we report the difference-in-differences estimates using the matched sample and distinguishing outward FDI types. In particular, we identify horizontal outward FDI and vertical outward FDI based on each pair of parent-firm and overseas affiliates at two-digit industry level. Horizontal outward FDI is recorded if parent firm has overseas affiliates that operate in the same two-digit industry, while vertical outward FDI is recorded if parent firm has overseas affiliates that operate in a different two-digit industry. There are also complex outward FDI types. That is, a parent firm may be engaged in both horizontal and vertical outward FDI at the same time in same or different locations. This type of parent firm is residual in the Portuguese context and, hence, they are excluded from the analysis based on outward FDI types of strategy.

The distinction between horizontal and vertical outward FDI aims at disclosing firm’s motivation to start operations abroad, which would drive its impact at home. Horizontal outward FDI is usually associated with market-seeking motivation, leading to significant scale effects, while vertical outward FDI tend to be driven by factor-seeking motivation, leading to some technology effects revealed in greater efficiency as well as larger exports (Hijzen et al., 2011).

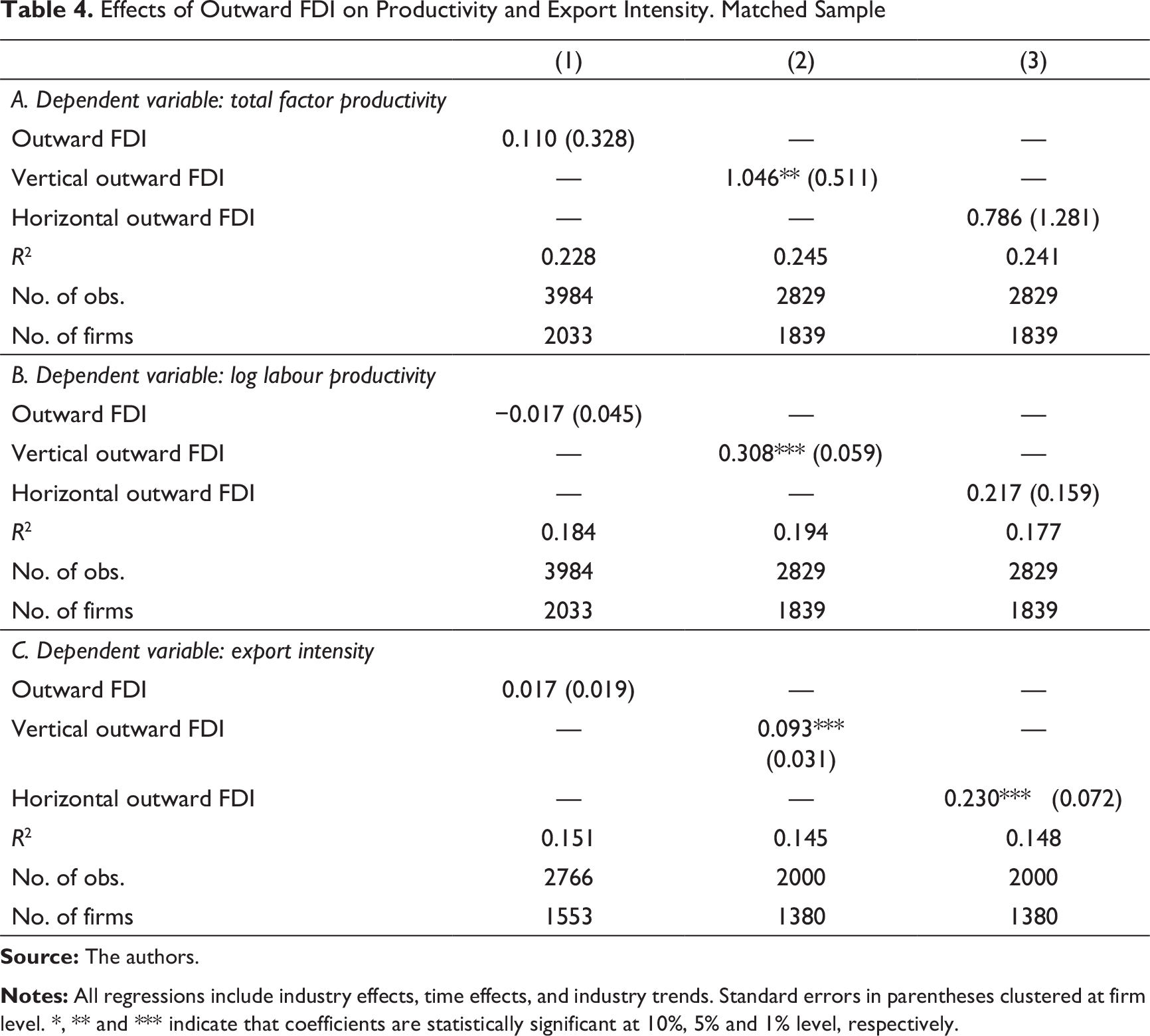

Effects of Outward FDI on Productivity and Export Intensity. Matched Sample

Vertical outward FDI seem to lead to a significant boost to firm productivity, suggesting that technology effects, in the form of greater efficiency, are at work. In the case of horizontal, market seeking, outward FDI the potential scale effects have no impact on upgrading productivity.

Interestingly, horizontal outward FDI seem to raise export intensity of parent firm more intensively than in the case of vertical outward FDI. This finding suggests some contradiction with prior assumption that horizontal, market-seeking FDI would have no significant effect on parent-firm exports. However, the Portuguese case of outward FDI may comprise some country specificities such as the higher presence in previous Portuguese colonies. Possible differences on host countries of horizontal or vertical outward FDI, in particular if there were significant differences among EU partners or outside EU territories, would have a different impact on productivity and export intensity. Our distinction between horizontal and vertical outward FDI only accounts for differences in two-digit industry, regardless of the host country. The different findings related to alternative outward FDI types suggest that the identification of host country and its impact on firm’s upgrading performance should deserve further research.

Another possible explanation is that a sizable increase on average earnings per employee observed in the case of vertical outward FDI (see Table 5) suggests an improvement on skilled employees, which, in turn, may lead to upgrading the quality of products and thus make them more suitable for export markets. Additionally, we have to recall that most of vertical outward FDI performed by Portuguese firms are on distribution networks, which could improve firm’s proximity to customers and their needs in foreign markets. Apart from distribution channel, vertical outward FDI could ease the access to quality raw material, which would promote product quality and exports. Jointly, those factors contribute to the surprising, unexpected impact of vertical outward FDI on parent-firm export intensity.

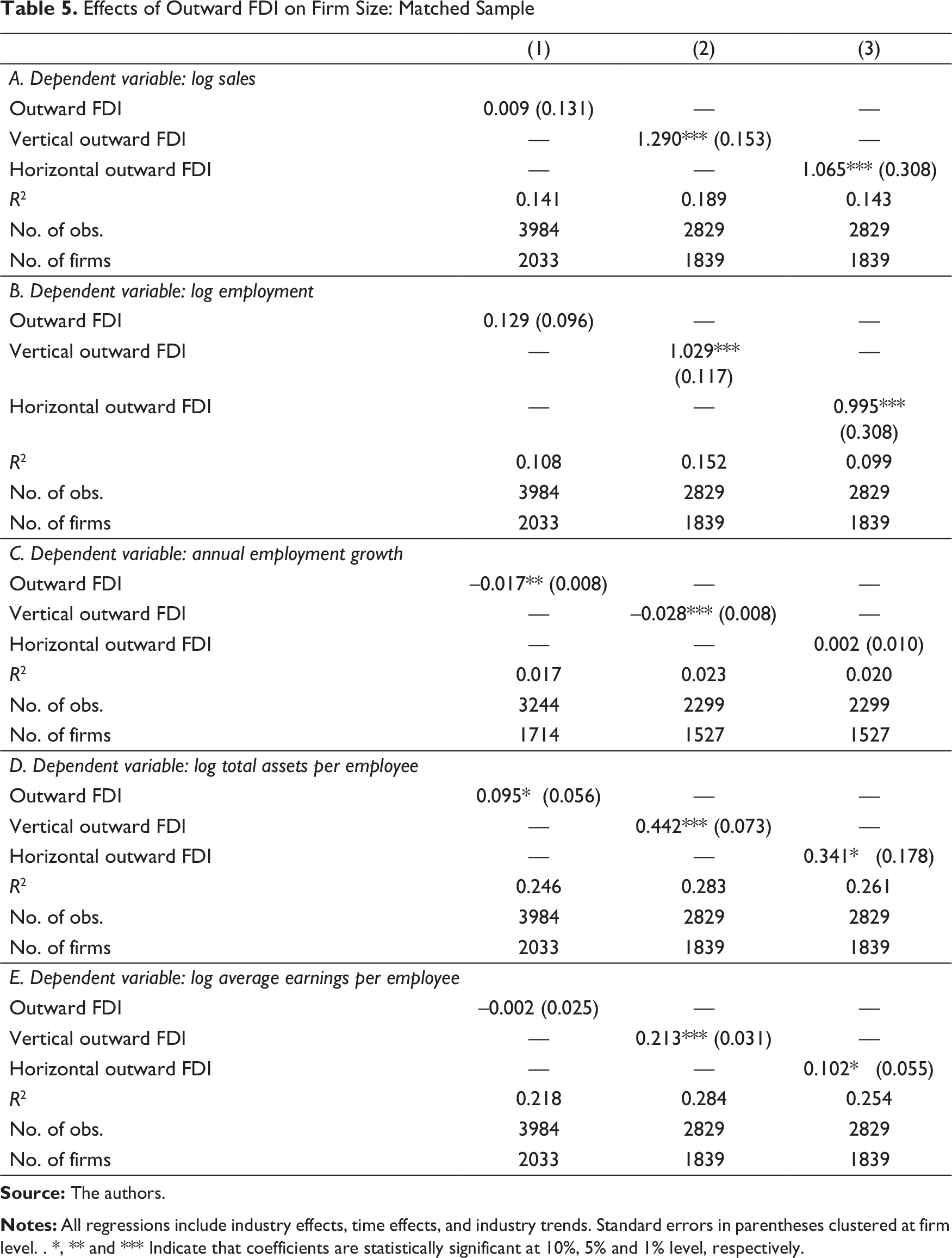

Effects of Outward FDI on Firm Size: Matched Sample

On the parent-firm size side, the empirical results suggest a difference on the growth effect. Both types of outward FDI boost firm size (measured by sales and employment) when examining the level effect. However, the growth effect of different types of outward FDI is statistically significant only in the case of vertical outward FDI. This indicates that firms performing vertical outward FDI record growth in terms of size but with a lower speed than other firms.

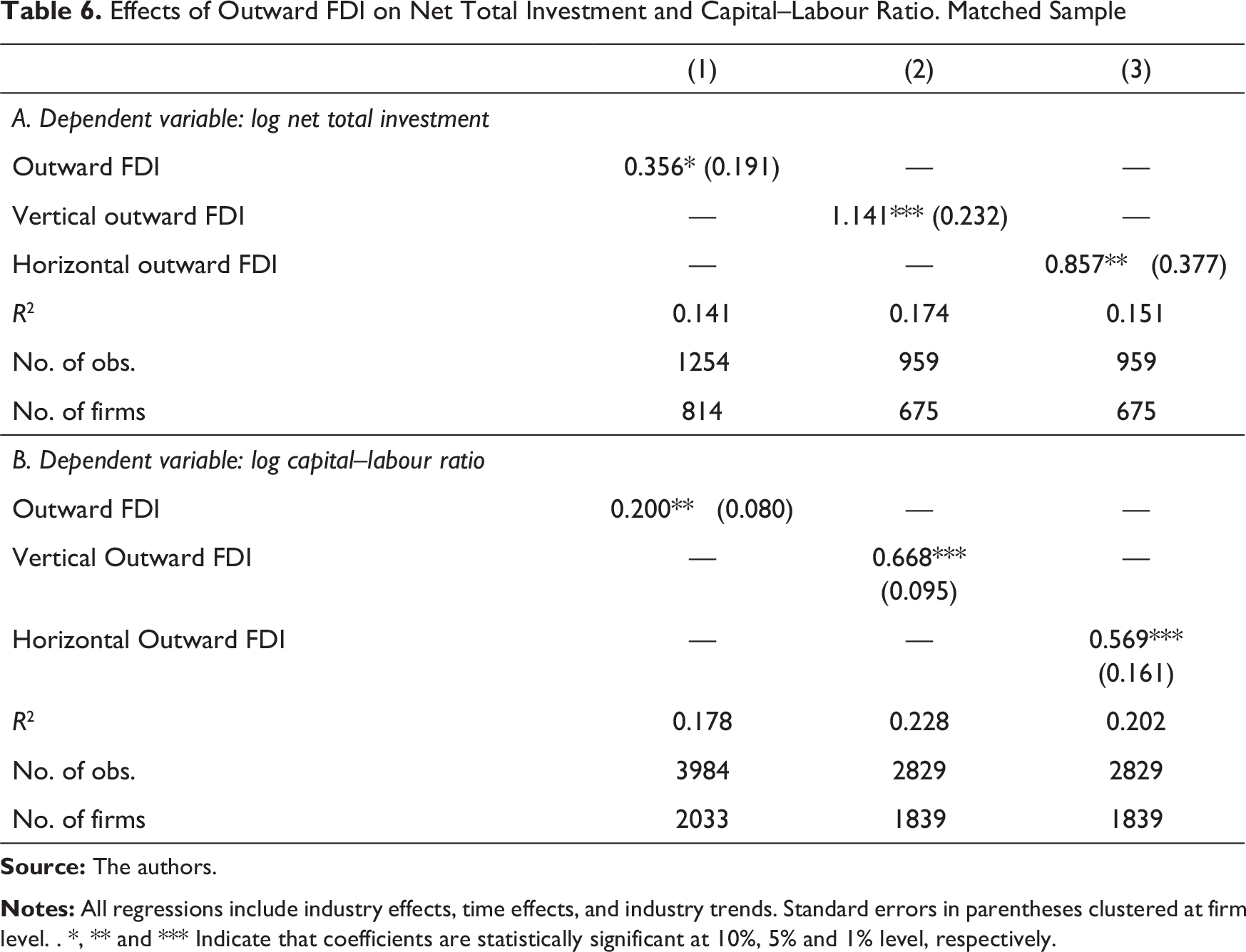

The changes taking place in firms performing outward FDI, documented so far, do extend to other aspects of parent-firm operations. Table 6 reports matching results with respect to the effects of outward FDI on net total investment and capital–labour ratio. Overall, the results show that outward FDI (both horizontal and vertical) do appear to induce increases in total investment and on the capital–labour ratio. A similar picture emerges with respect to total assets per employee (see Table 5), which shows that firm with outward FDI make available more assets per employee than on pure domestic firms.

Effects of Outward FDI on Net Total Investment and Capital–Labour Ratio. Matched Sample

How can we reconcile those technology effects, in the form of greater capital-intensity and investment, regardless of the type of outward FDI, with no evidence of upgrading productivity in the case of horizontal outward FDI? One possible explanation is that parent firm with horizontal outward FDI fail to introduce organizational and managerial changes that make the production process more efficient and using labour more effectively. That is, some financial effort, in order to upgrading technology, seems to be done, but it was not accompanied by significant changes in the production process, which, in turn, made no visible such effort in terms of productivity. Another possible explanation is that parent firm replicating the same activities in overseas locations—horizontal outward FDI—will not alter the skill composition of labour and will not be able to attract more experienced and motivated employees. This explanation is in line with the matching results in terms of average earnings per employees (see Table 5).

Conclusion

This study aims at shed additional light on the causal link between outward FDI and parent-firm performance upgrading and restructuring. While existing evidence lends some support to a positive causal relationship, little is known about whether and how a different relationship occurs in a small, open and peripheral economy such as Portugal. If Portuguese firms do not get rewards from their integration into the global economy through outward FDI, then policies designed to foster internationalization seem to fail and the assumption that outward FDI benefit parent firm may not hold true.

We exploited comprehensive data on Portuguese firms spanning the period 2006–2012 to study the effect of outward FDI on parent-firm performance at micro-level. During this period, several official home country incentives had been provided through law to promote the internationalization of domestic firms, resulting in an upward time trend in Portuguese outward FDI. We identify causality by controlling for the possible endogeneity of parent firm outward FDI decision, using a difference-in-difference approach in combination with propensity score matching. Our analysis differs from the most existing literature by considering a range of outcomes that can potentially be shaped by outward FDI decisions and by separating the analysis into different types of outward FDI.

Managerial and Policy Implications

From a managerial and policy perspective, our results provide evidence that outward FDI leads to: (a) an expansion in the scale of operations; (b) and increase on total investment, capital intensity and assets per employee; (c) an increase on integration into the global economy; and (d) different impacts on parent firm according the FDI strategy. In particular, the article provides evidence that vertical outward FDI cause technology effects, in form of greater efficiency along with scale effects. The effects associated with horizontal outward FDI are more visible in terms of scale effects. Nonetheless, we interpret the evidence provided by this study as supporting the argument that outward FDI can indeed be at root of upgrading performance and firm’s restructuring in a small, open and peripheral economy such as Portugal.

Future Research

The newness of the empirical findings in a context of a small, open and peripheral economy inspires fruitful avenues of future research. One possibility would be to examine, from a theoretical and empirical point of view, the channels that could lead to positive or negative effects of outward FDI on parent firm’s performance and whether such channels diverge according to FDI strategies and host countries. Another interesting avenue of research would be to adopt a dynamic approach in order to look at the evolution of outward FDI strategies over time and its impact on parent firm’s performance and restructuring. These topical issues are beyond the scope of this article but undoubtedly deserve further research.

Appendix A

Balancing Tests

Balancing Tests

Footnotes

Acknowledgement

The author are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received financial support from National Funds of the FCT – Portuguese Foundation for Science and Technology - within the project «UID/ECO/03182/2019.