Abstract

We present a multifarious view on the presence of long memory across 33 countries, subsampled as developed, emerging and frontier economies for the period 2000–2018. We employ the classical rescaled range test, and two semi-parametric tests proposed by Geweke Porter-Hudak (1983) and the frequency domain test proposed by Robinson (1995) to decipher the presence of long memory. The results confirm that while there exists no long-range dependence for developed countries, the return series in the emerging and the frontier countries display long memory characteristics. The rationale for such result emerges from market quality parameters such as size, liquidity, trading and settlement mechanism or sound regulatory framework. These results are of importance for the global investor community for asset allocation, risk management and portfolio diversification purposes.

Introduction

In the past few decades, the extant literature claimed to understand several theories regarding the behaviour of financial asset returns, among which, the theory of efficient market hypothesis (EMH hereafter) postulated by Fama (1970), holds the utmost prominence. EMH asserts that current market prices instantaneously absorb all relevant information and do not provide scope for any abnormal returns. On the other hand, efficient resources allocation is not achieved when the market is inefficient, as a result, the price signal understates and overstates the impact of new information (see for e.g., Ali et al., 2018; Mensi et al., 2017; Pagan, 1996). Thus, in order to understand such mispricing, two extreme views exist. The first view states that returns are generated by a random walk process, and hence, it is difficult to predict future returns based on past information, as suggested by EMH. This is called as random walk hypothesis (RWH). There exists a mixed composition of literature in favour of RWH (Larson, 1960) and against it (Dusak, 1973; Stevenson & Bear, 1970). The other view is the mean reversion theory, which proclaims that returns tend to move to their mean value; hence, it is quite predictable to decipher the future path based on their past path. Literature relating to mean reversion is also mixed in nature. While some researchers supported it (e.g., see Fama & French, 1988; Poterba & Summers, 1988), others were against it (e.g., see Kim et al., 1991; Richardson, 1993; Richardson & Stock, 1989).

Amidst this discussion, an important asset return characteristic that is of long memory has been significantly studied in various asset classes (e.g., see Assaf, 2008; Barkoulas et al., 1999; Coakley et al., 2016; Crato & Ray, 2000; Elder & Jin, 2009; Fernandez, 2010). Long memory is a unique characteristic which describes the correlation structure of a stationary process at distant lags. If a time series exhibits long memory, then its autocorrelation function decays gradually at a slower rate and is characterized by distinct but non-periodic cycles (Barkoulas & Baum, 1996). The associated dependence in the first and second moments of the series leads to identifiable patterns which provide opportunities to exploit market conditions and to earn abnormal returns. The literature on long memory is also mixed. While several researchers report evidence in support of the long memory (e.g., see Abbritti et al., 2016; Alexander et al., 2019; Bariviera, 2017; Bouri et al., 2019; Caporale et al., 2018; Kristjanpoller & Bouri, 2019; Kristjanpoller et al., 2020; Mynhardt et al., 2014; Niu & Wang, 2014; Nystrup et al., 2017; Phillip et al., 2019; Shahzad et al., 2020; Singh & Chakraborty, 2017), others (Batten et al., 2005; Berg & Lyhagen, 1998; Crato & Ray, 2000; Jacobsen, 1995; Lo, 1991; Lu & Perron, 2010; Serletis & Rosenberg, 2007) do not find long memory properties in financial series. A possible reason for such different findings is that the degree of persistence might change over time, as argued by Corazza and Malliaris (2002), Bennett and Gartenberg (2016).

Thus, presence of long memory repeals EMH, which suggests that return series follows martingale process, and hence, probabilities of generating abnormal returns are nullified (Ding & Granger, 1996; Gil-Alana, 2006; LeRoy, 1989). Also, assets pricing models like capital asset pricing model (CAPM) and arbitrage pricing theory (APT) are unrealistic if the continuous process exhibits long-term dependence. Some researchers also report the inappropriateness of derivative pricing models in the presence of long memory (Maheswaran, 1990).

In this context, the present study aims to examine this possible explanation by estimating the persistence of 33 benchmark stock market indices sub-sampled from developing, emerging and frontier countries (based on their degree of economic development) in the financial time series for the period 2000–2018. The analysis was carried out using three long memory approaches, that is, R/S analysis with the Hurst co-efficient, and two semi-parametric tests, that is, Geweke and Porter-Hudak’s (1983) test (GPH hereafter) and Robinson’s (1995) Gaussian semi-parametric test (RGSE hereafter), for estimating the fractionally differenced d statistics. These semi-parametric tests are considered vis-à-vis parametric test as the latter requires correct specification of p and q or else it leads to inconsistent results of the fractional differencing parameter d.

The present article contributes to the literature in the following ways: first, the recent literature on long memory behaviour of returns is primarily focused on the developed markets and few focus on emerging markets (see Alexander et al., 2019; Mynhardt et al., 2014; Shahzad et al., 2020). However, the current article, along with developed and emerging markets, studies the case of the frontier markets also. The rationale behind studying these markets is as follows: As the developed and emerging markets are characterized by low correlation with other markets, hence investors may allocate assets for effective diversification. Also, investors venture to these markets with expectation of higher returns. Hence, it becomes quintessential to provide a cross-country evidence for the investment community. Second, we employ conventional re-scaled analysis method along with two confirmatory semi-parametric methods in the current article to test the robustness and temporal stability of the long memory. Third, we use a rich dataset for 33 countries over a year of 19 years. The period is also significant in the global perspective as the financial markets during this period have witnessed several macro-economic events such as global financial crisis; sovereign debt crisis in France, Greece and Spain; swings of oil prices; trade wars between China and America; and regional armed conflict.

The rest of this article is organized as follows. The second section presents the theoretical insights into long memory modelling. The third section describes data and methodologies. The empirical results and discussions are detailed in the fourth section, followed by conclusion with our observations and further scope of work in the last section.

Theoretical Perspectives

Long-range dependence has been studied in varied areas by different researchers since long; early instances are from the works of Hurst (1951, 1957), Mandelbrot and Wallis (1968) who used it for studying operational hydrologic variability. Mandelbrot (1972) tested financial data for long memory with the Hurst methodology, and Mcleod and Hipel (1978) applied it to water resources and environmental systems. These wide-ranging applications have given rise to various definitions of long memory.

Consider

The usual definition of long memory in the covariance stationary series

Alternatively, long memory is defined in time and frequency domains.

Long memory as per time domain can be defined by specifying a hyperbolic decay of the auto-covariance:

where d is the long memory parameter and

The frequency domain-based definition of long memory using spectral analysis methods is expressed as

for

Finally, the classical theory of stationary time series requires the existence of Wold decomposition theorem postulated by Wold (1938). Following this fundamental tool, the long memory property can be expressed as

For

Further, Granger and Joyeux (1980) and Hosking (1981) introduced the fractional differencing parameter in the ARIMA framework in order to test for the long memory properties in a time series. Baillie (1996) asserts that the fractional differencing parameter lies between I(0) and I(1). Following Palma (2007), a time series

Where

B is the backshift operator, which is given as

where

where is the gamma function for d < 1/2, d ≠ 0, −1, −2..., and

The fractional differencing parameter d determines the memory process. The time series is said to exhibit long memory if d is between 0 and 0.5. In case d is less than 0, then it is said to be anti-persistent and displays negative memory.

Data and Methodology

To achieve the objective of the article, we use the benchmark indices of 33 stock markets sub-sampled as 17 developed, 10 emerging and 6 frontier countries. The basis of classification is in reference to the MSCI Annual Country Classification Review 2019. The daily value of indices has been culled out from Bloomberg database for the period 2000–2018. The daily returns have been calculated by using

The current study employs three long memory approaches, that is, R/S analysis with the Hurst coefficient, and two semi-parametric tests, that is, Geweke and Porter-Hudak’s (1983) semi-parametric test and Robinson’s (1995) Gaussian semi-parametric test, for estimating the fractionally differenced d statistics.

Rescaled Range (R/S) Analysis

The R/S analysis is an ideal statistical tool for analysing the occurrence of rare events and is robust to possible nonlinear process where, normality assumption may not be needed. The result of the R/S analysis is the Hurst exponent, which is a measure of the bias or trend in a time series.

The dataset is portioned into sequential non-overlapping blocks, as

The final step is to apply an OLS regression with

The value of H can be interpreted in the following ways:

H = 0:50 denotes a random and statistically independent (uncorrelated) series—a random walk. The present does not influence the future. The correlation coefficient is 0. Its probability density function is normal. Such process increases with the square root of time. 0:50 < H ≤ 1:00 denotes a ‘persistent’ or trend-reinforcing series, that is, the data contain long-term memory and have a tendency to follow the current trend in the next period. This process is said to be mean-averting. H < 0:50 denotes an ‘anti-persistent’ or ergodic series, that is, the data have a tendency to reverse the current trend. This process is said to be mean-reverting.

Geweke and Porter-Hudak Semi-parametric Test

Geweke and Porter-Hudak (1983) proposed the GPH test, a semi-parametric estimate of the fractional integration d, which is robust to non-normality in the time series. Under the assumption that spectral density of stationary process may be written as

By defining

Robinson’s Gaussian Semi-parametric Test

Robinson (1995) suggests a Gaussian semi-parametric estimate of the self-similarity parameter H. It is assumed that the spectral density of the time series, denoted by f(.), behaves as

with respect to H, where

Empirical Results

Summary Statistics

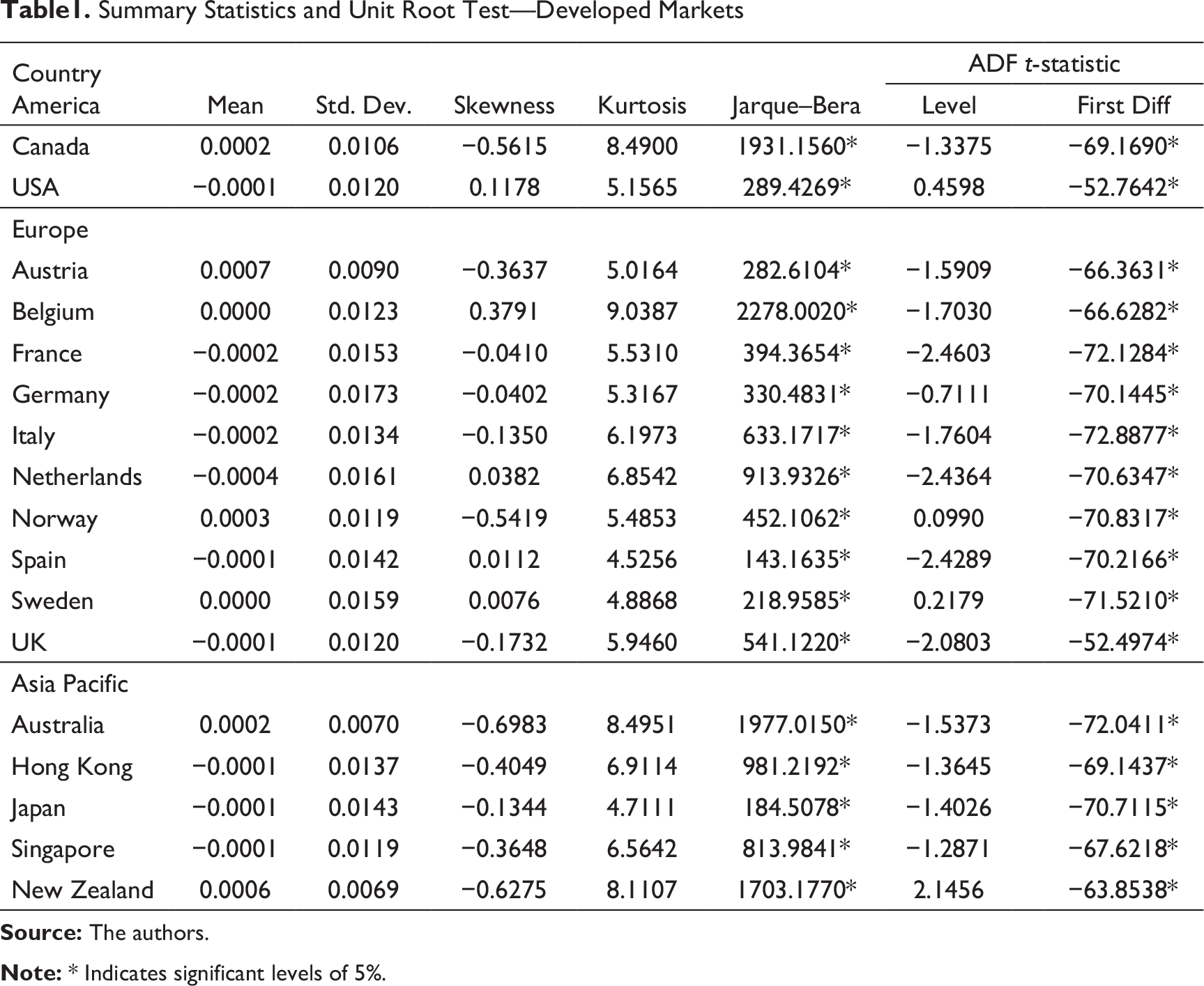

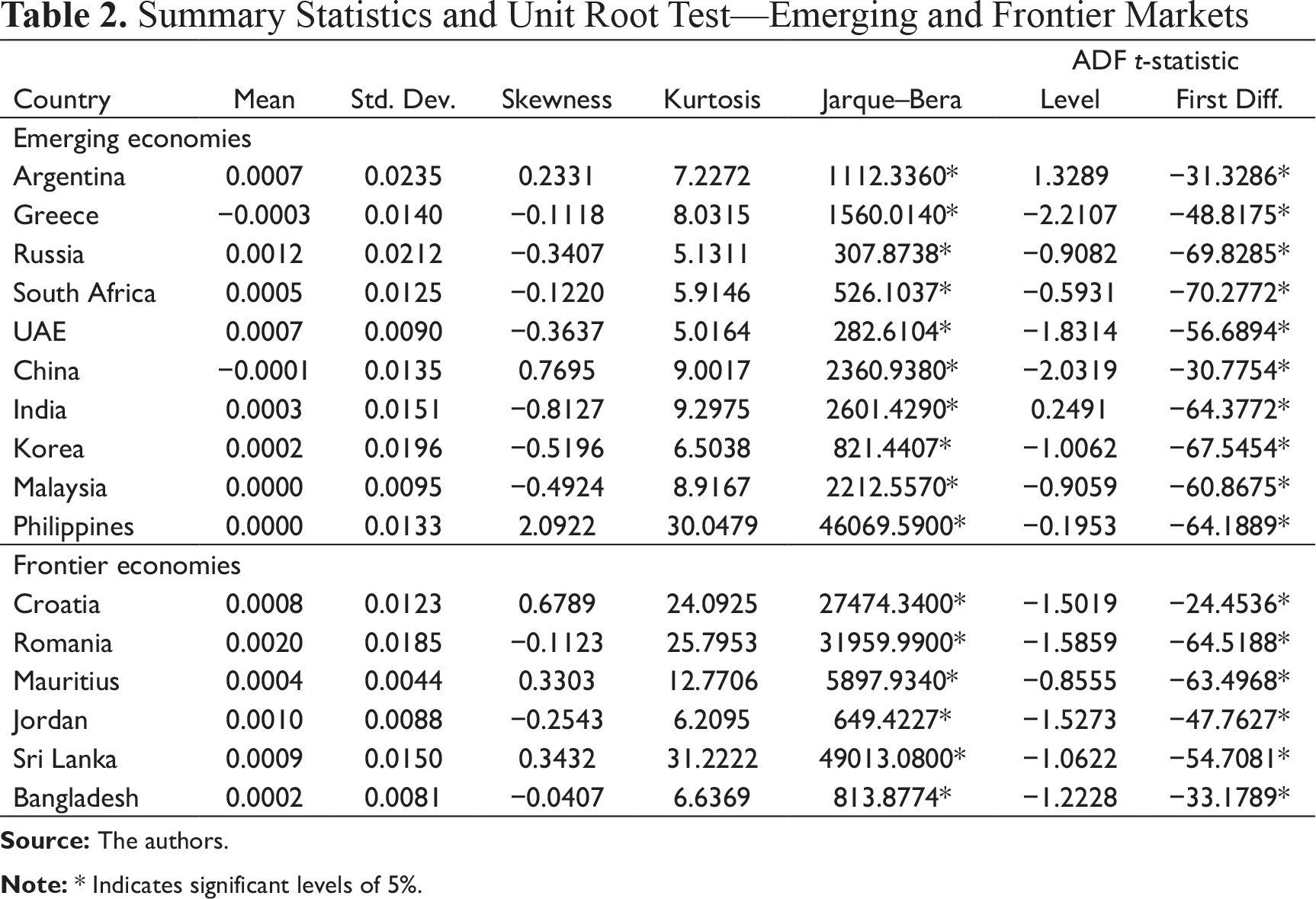

Tables 1 and 2 present the summary statistics of the return series of major stock indices from the developed, emerging and frontier markets. The data appear to be non-normal. Most of the developed, emerging and frontier market return series except USA, Belgium, Netherlands, Spain, Sweden, Argentina, China, Philippines, Croatia, Mauritius and Sri Lanka exhibit negative skewness, possibly owing to the significant negative returns associated with the global financial crisis of 2007. The return series show high kurtosis and are leptokurtic in nature. All the series satisfy the null hypothesis of normality of Jarque–Bera tests at 1 per cent level of significance. The Augmented Dickey Fuller (ADF) test results confirm that the return series are stationary at their first difference. It can be noted here that, stationarity is not a necessary condition for long memory property of financial time series.

Summary Statistics and Unit Root Test—Developed Markets

Summary Statistics and Unit Root Test—Emerging and Frontier Markets

Hurst, GPH and RGSE Test Results

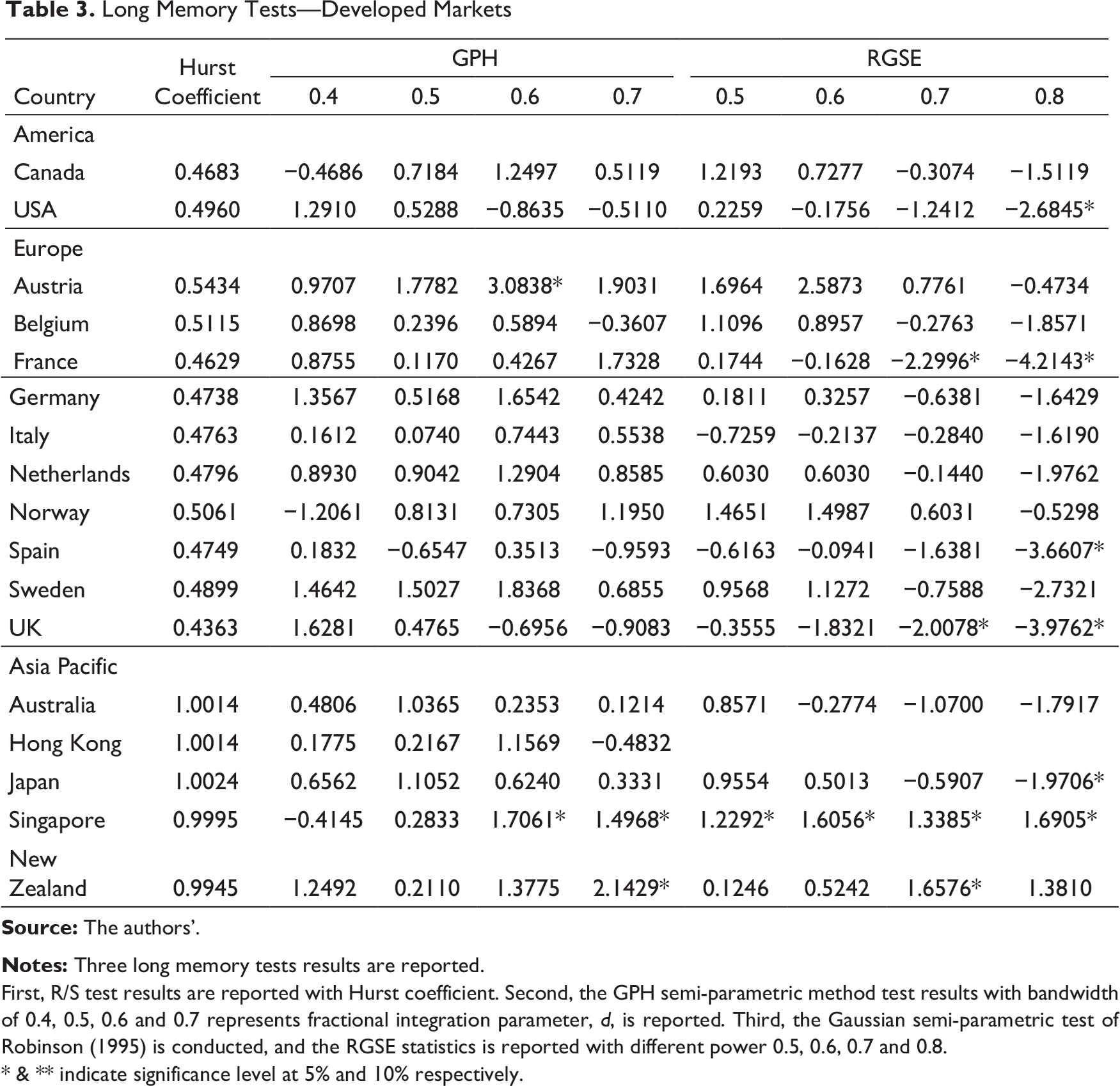

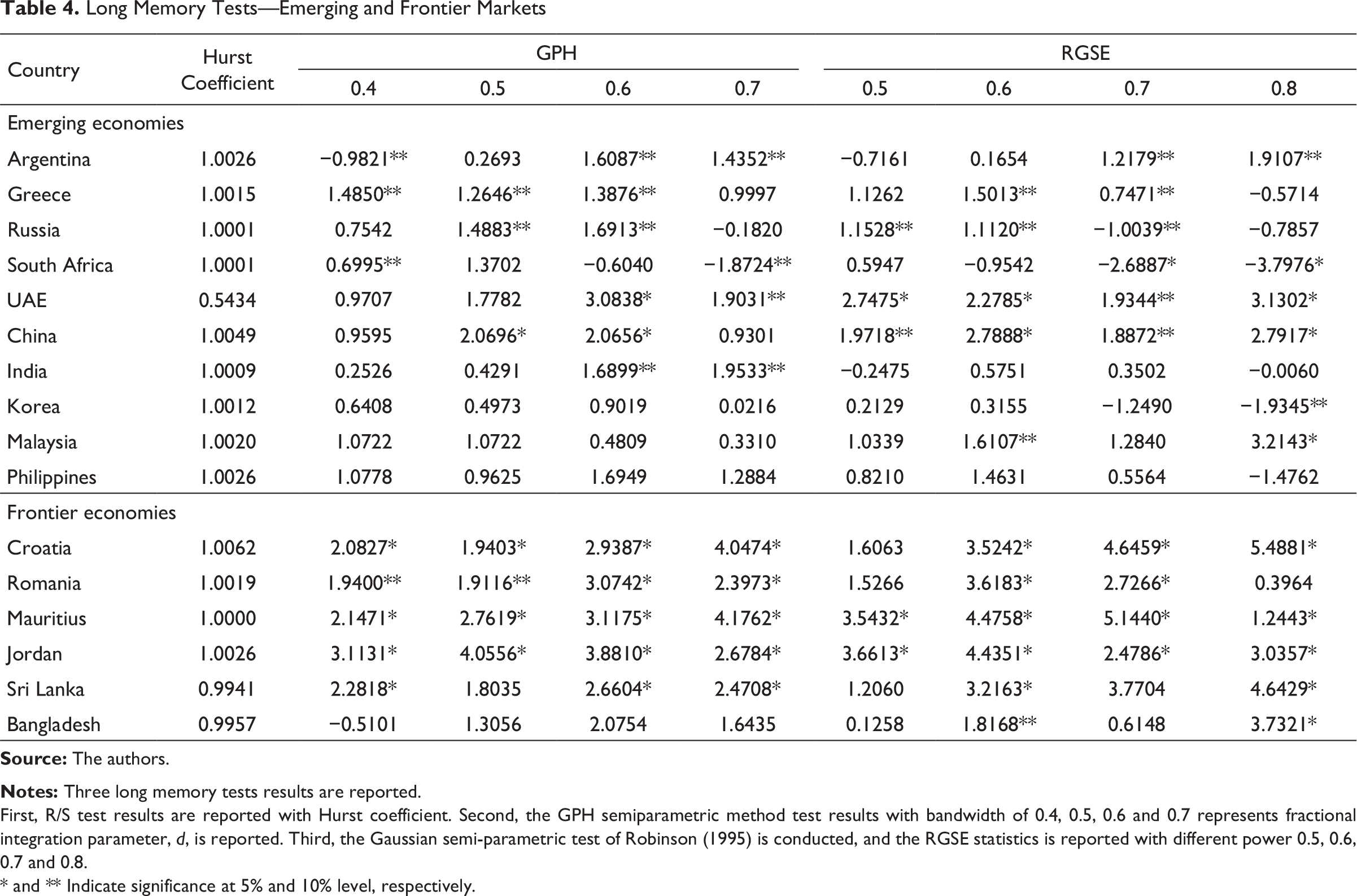

Tables 3 and 4 report the results of the three sets of long memory tests for the returns series from the developed, emerging and frontier markets. In each table, first, the R/S test is conducted, and the Hurst coefficient is reported. Second, the GPH semi-parametric test is conducted, and the GPH fractional differencing parameter d is reported for bandwidths 0.4, 0.5, 0.6 and 0.7. Third, the RGSE test is conducted and the RGSE fractional differencing parameter d is reported with power of 0.5, 0.6, 0.7 and 0.8.

Long Memory Tests—Developed Markets

First, R/S test results are reported with Hurst coefficient. Second, the GPH semi-parametric method test results with bandwidth of 0.4, 0.5, 0.6 and 0.7 represents fractional integration parameter, d, is reported. Third, the Gaussian semi-parametric test of Robinson (1995) is conducted, and the RGSE statistics is reported with different power 0.5, 0.6, 0.7 and 0.8.

* & ** indicate significance level at 5% and 10% respectively.

Long Memory Tests—Emerging and Frontier Markets

First, R/S test results are reported with Hurst coefficient. Second, the GPH semiparametric method test results with bandwidth of 0.4, 0.5, 0.6 and 0.7 represents fractional integration parameter, d, is reported. Third, the Gaussian semi-parametric test of Robinson (1995) is conducted, and the RGSE statistics is reported with different power 0.5, 0.6, 0.7 and 0.8.

* and ** Indicate significance at 5% and 10% level, respectively.

Developed Markets

Table 3 reports the results of the developed markets indices classified as America, Europe and Asia-pacific markets. The R/S test results confirm that the stock indices return of developed markets such as America and Europe demonstrate no autocorrelation, and the returns are statistically independent series, evident from the Hurst coefficient of 0.5 or marginally lower than 0.5. It implies that these markets are random walk and do not possess long memory. This result is in line with works of Weron (2002), Grech and Mazur (2005), Krištoufek (2010). Conversely, we find that, within the developed markets, the Asia-pacific countries’ stock indices portray presence of long memory in their returns, evident from the Hurst coefficient that ranges from 0.5 to 1. In fact, as developed markets, these indices are expected to display market quality indicators such as size, liquidity and regulatory framework. This led us to re-test the long memory properties with two semi-parametric tests like GPH and RGSE. It can be inferred from the fractional differencing parameter d, reported in Table 3, that all the major stock indices from the developed nations of America and Europe do not exhibit long memory property in their return series. However, contrasting results are reported for GPH and RGSE tests for the stock indices from the developed Asia-pacific region. The results indicate weak evidence of long memory pattern in the return series of these markets. Overall, we can say that the stock markets from the region are maturing like their European or American counterparts in terms of characteristics of developed market quality.

Emerging and Frontier Countries

Table 4 reports the results of the emerging and the frontier stock market indices. The R/S test results show that the Hurst statistics for all the stock indices of emerging and frontier economies are greater than 0.5 indicating the presence of the long-range dependence in return series. The Hurst statistics also characterizes the market efficiency, which indicates how swiftly new market participants react to the new information that pours into the market. The results indicate that the return pattern is inter-temporally predictable and can be exploited by investors.

Further, to strengthen the findings, we conducted the semi-parametric long memory test on the return series, and the results are given in Table 4. We find that the fractional differencing factor d from the GPH test is significant for the stock indices of several emerging and all the frontier economies at select ordinates. This result implies that the emerging and frontier economies returns are dependent on the past returns displaying structural inefficiency of these markets. For this reason, the investor community keeps a watch to prevent exploitation of profitable trading opportunities in these markets. The results of the RGSE test present similar and more significant results, indicating the strong presence of long-range dependence in the return structure of the stock indices of these markets.

Discussion of Results

We infer from the results that the dynamics of long-range dependence is divergent for developed, emerging and frontier economies. While the present study does not find long-range dependence in developed markets, there is a significant presence of serial autocorrelation, that is, long memory properties, even in the distant observation in the emerging or the frontier economies. The current results are in line with Barkoulas et al. (1999), Assaf (2008) for developed market. For emerging and frontier markets, this result corroborates with the works of Ali et al. (2018) and Odonkor et al. (2019). The most important implications from these results are: One, the presence of long memory can give information about the future returns, and prediction models can be employed by the investors for exploiting profitable trades. It also indicates that the asset pricing model like capital asset pricing model and arbitrage pricing model fail to operate in markets displaying long-memory characteristics. Second, it also forms the basis for use of specific trading strategies based on the benchmark indices of the market; for instance, high persistence will indicate use of trend-oriented trading strategies, while market with low persistence will use oscillatory strategies. It also may give rise to several market anomalies. Third, as the long memory properties are time varying, they may call for timely revision of your trading strategies, indicating evidence in favour of adaptive market hypothesis.

To sum up, this result has substantial linkages to the behaviour of stock markets in developed and emerging markets. We construe this inference based on the fact that developed markets display high market quality parameters such as size, liquidity, trading and settlements systems, highly transparent and stable regulatory frameworks in comparison to their emerging and frontier counterparts. Furthermore, the results are important for the global investor community as they strive to identify markets that offer higher returns and aid portfolio diversification. Although emerging markets provide them with a solution, still these markets are marked with impediments such as high trading cost, lack of liquidity, high risk, thin and non-synchronous trading.

Conclusion

This article employs R/S test and semi-parametric fractional integration test of GPH and RGSE to analyse the long memory properties in the return series of developed, emerging and frontier economies for the period 2000–2018. The primary motivation of the article results from the mixed literature available on the long-range dependence issue. Our contribution in the article rests on the fact that we have a rich dataset of 33 countries across developed, emerging and frontier economies for a period marked by global financial crisis, currency crisis, geo-political issues, Brexit, trade wars and financial innovation like bitcoins and jolting crude-oil prices. The results suggest that while developed markets tend to be efficient, the emerging and frontier markets display long-range dependence. Our results have huge bearing on the financial models like CAPM and derivative pricing models and also on the asset allocation in these markets. It is also useful for financial engineers to develop financial models with better predictability in order to exploit these markets. The findings are useful for investors, corporate managers, researchers and policy planners for several reasons. The presence of long memory leads to arbitrage, thereby resulting in exploitation of profit for those who have access to sensitive information. Also, enhanced market-microstructures such as information flows, regulatory reforms, transparency, well developed trading technology and active investment strategies are essential for efficient markets. These changes will see the fair valuation of securities and help investors reap a return, which is risk adjusted. Hence, holistic economic development is possible after allocation of appropriate portfolio, risk diversification and hedging strategies.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.