Abstract

Adoption of an electronic marketplace (EM) business model for business-to-business (B2B) transactions has increased over the years. In part, this evolution and adoption of B2B EMs can be explained by the Internet-enabled disintermediation of the existing value chains of businesses, followed by cybermediation. This study aims to understand the platform architecture design and governance-related factors and strategic choices that influence the success of B2B EM start-ups. We draw from the literature on the ‘Temple Framework’ and the classification of B2B EMs by transaction content, structure, and governance to identify these critical factors. Given that the literature is primarily based in the context of developed economies, the factors and choices identified from the review are empirically validated using three case studies in the Indian B2B context. Thus, this exploratory study aims to help founder managers of emerging-economy B2B EMs by providing a checklist to avoid common pitfalls.

Keywords

Introduction

The term ‘platform business’ encompasses different types of marketplaces with distinct architectures and externalities (Dai & Kauffman, 2002; Tauscher & Laudien, 2018). In the context of electronic marketplaces (EMs), a ‘platform’ refers to the total of a ‘firm’, ‘product’, ‘service’ or ‘technology’ (including ‘components’, ‘architecture’ and ‘rules’) that mediates transactions between two or more user groups (often called demand-side and supply-side user groups). A decade ago, minimal e-commerce businesses existed outside the business-to-customer (B2C) space. However, due to the widespread adoption of the Internet, databases and networking technologies, the second wave of e-commerce players, referred to as EMs, is being witnessed in the business-to-business (B2B) space. A B2B EM is a platform of interactive business communities providing meditation to those engaged in business activities (Dai & Kauffman, 2002; Engström & Salehi-Sangari, 2007; Minier, 2003).

The widespread adoption of the Internet significantly reduced the search, transaction and new-product development costs emanating from the traditional business model’s information asymmetry. Riding on these triple advantages, EMs began to rise in the late 1990s in North America during the dot-com era. Today, EMs support all significant types of B2B transactions, such as sales via catalogue, contracts, auctions, reverse auctions and request for quote (RFQs) and trading via exchanges (Chong et al., 2011; Dai & Kauffman, 2002; Minier, 2003). These B2B EMs significantly reduce transaction costs by automating purchase and sales processes. They also minimize information inefficiencies by bringing in price transparency and aggregating real-time information (Bruun et al., 2002; Engström & Salehi-Sangari, 2007). During the last three decades that this model has been around globally and the two decades it has been there in the Asian region, there have been more failures than successes (Chong et al., 2011). As per a Goldman Sachs report, as quoted in the Economic Times, India’s e-commerce market is expected to be worth around $99 billion by 2024, of which the B2B e-commerce is estimated to be a $60-billion revenue opportunity (Agrawal, 2021). In the developed-economies context, the various reasons making it difficult to establish a B2B marketplace include high initial capital investment, the chicken-and-egg problem, high operational costs, choices about positioning and value proposition, functionality and the existence of several user groups (Bruun et al., 2002; Chong et al., 2011). The institutional void of the emerging economies makes it even more difficult for a B2B EM start-up to deal with the aforementioned issues. It thus becomes essential to have a ready reckoner of critical success factors to aid these B2B EM start-ups. This article addresses the research question: What factors and strategic choices are crucial for B2B EM start-ups in an emerging-economy context?

A selective–intensive literature review was undertaken to develop a thorough understanding of the factors responsible for the success and failure of B2B marketplaces. Subsequently, three Indian B2B cases were explored to validate these factors identified from the literature empirically. These three Indian firms with different growth rates—hypergrowth, high growth and below-average growths—were chosen to cover the entire spectrum from highly successful to unsuccessful platforms. This study analyses these Indian start-ups on various parameters, including platform transactions, architecture and B2B EM mobilization strategies. This exploratory study aims to contribute to the understanding of founder managers of emerging-economy B2B marketplaces by providing a checklist to avoid common pitfalls. The remaining portion of the article is organized as follows: The literature review is followed by empirical case studies, followed by the discussion, implications and conclusion sections.

Literature Review

Business-to-Business Marketplace Model

Crafting a strategy for an EM’s success begins with understanding its business model and the transactions involved. This business model’s core aspect is to provide a venue for business organizations to interact, primarily to purchase and sell products or services. However, facilitating transactions is not the only function of the marketplace. B2B EMs are known to extend functionalities, such as cataloguing, financing, logistics and value-added analytics (Engström & Salehi-Sangari, 2007; Minier, 2003). Extending these functionalities allows EMs to build a business model on the following three core value propositions: increasing market efficiencies, increasing supply chain efficiencies and new value creation (Bruun et al., 2002; Dai & Kauffman, 2002; Grieger, 2003), resulting in cost savings and revenue enhancements for all their stakeholders.

E-marketplaces can increase market efficiency by reducing transaction costs, increasing transparency and bringing together buyers and sellers to meet their needs more economically and more profitably. Reduced information asymmetry and availability of enough buyers and sellers facilitate price discovery improvements. By providing platform user groups (both buyer and supplier sides) with collaboration tools and support, such as inventory management, demand forecasting and production planning, EMs can increase monitoring and prevention of pilferage across the supply chain, thereby enhancing supply chain efficiency and cost savings (Engström & Salehi-Sangari, 2007; Grieger, 2003; Minier, 2003). Building on the insights generated from real-time big data available from connected touchpoints spread across the entire value chain, the supply chain within and across various industries may be redesigned. This way, EMs allow fundamental changes in doing business and exploiting opportunities within and across industries to profitably create and deliver value-added services (Bruun et al., 2002; Grieger, 2003).

Critical Success Factors

Critical success factors (CSFs) are defined as ‘the few key areas of an activity in which the favourable results are absolutely necessary for a particular project to achieve its goals’ (Srivastava & Misra, 2014, p. 364; Somiah et al., 2020; Focacci et al., 2005). Extant research notes that factors critical for organizational success can broadly be classified into two groups: context and choices (Bruun et al., 2002). The sources of exogenous contextual factors include industry environment and macro and spatially pertinent environmental factors (Bullen & Rockart, 1981; Srivastava & Misra, 2014). The understanding of context thus involves developing an appreciation of firms’ external environment. Apart from the context, firms’ internal factors—resources and capabilities, value chain activities—and the competitive strategy choices made by firms impact the firm performance (Bruun et al., 2002; Bullen & Rockart, 1981; Srivastava & Misra, 2014). For B2B EMs too, the choices with respect to the competence portfolio, strategy, organization structure, financing, platform design and governance need to be made. As there is ample literature on how to study a firm’s external and internal environments and strategy, organization structure and financing choices (Bruun et al., 2002; Srivastava & Misra, 2014), this article focuses more on elaborating factors especially related to platform architecture and its strategic mobilization. There are three sets of choices or questions around a successful platform to be answered to arrive at a winning strategy, namely preliminary checks, platform structure choices and platform launch and growth choices (Chong et al., 2011).

Preliminary Checks

Setting up a platform that adds value to the user groups and is more than just a basic e-commerce (online) sales channel involves addressing the following four preliminary questions (Bruun et al., 2002; Chong et al., 2011). The first question is whether the platform provides functions other than e-commerce. If the organization offers only an e-commerce facility, defined here as a ‘channel’ to procure order, it is not an EM. The second question is whether the platform’s technology offers a function essential to create new or increased value. If the only functionality offered by a firm is a digital storefront, only the arbitrage value is being exploited. This behaviour is much less than the ideal scope of an EM. The third question is whether the platform has sufficiently attractive value propositions for both buyers and sellers. If the platform only facilitates the discovery of members of the user groups and offers only space or time arbitrage, the value proposition elements are not sufficiently attractive for the firm to grow big as an EM. The fourth question is whether the platform solves business problems for many players in the industry. If the only problem that the firm solves is getting input for its operations, it is also less than ideal for a firm to aspire to be an EM. In a nutshell, if the answers to the above questions are no or yes in a somewhat limited sense, then what probably exists is an online sales channel or website of a firm that has other (direct and indirect, physical) sales channels. After having answered ‘yes’ to the questions mentioned above, the next step is to make the platform structure choices.

Platform Structure

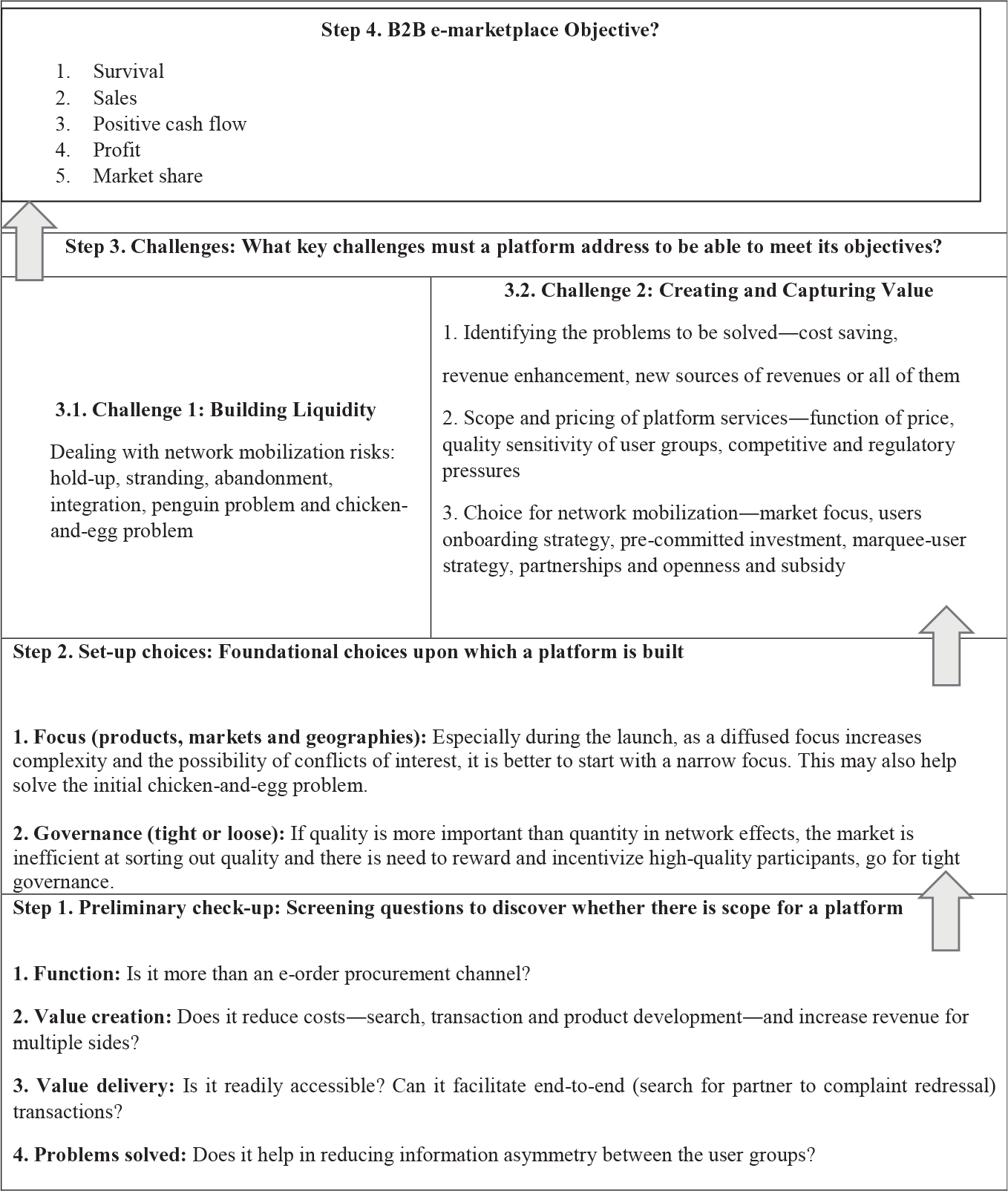

The ‘Temple Framework’ is the most commonly referred framework for creating a winning strategy–structure combination for B2B EMs (Bruun et al., 2002). Proposed by Bruun et al. (2002), the Temple Framework has three main components—the objective, the challenge, and the setup—as elaborated in Figure 1. The set-up comprises five elements—focus, governance, functionality, technology and partnerships (Bruun et al., 2002)—that form the crux of the platform’s strategic positioning and paves the way for the platform to address the challenges. As per the Temple Framework, the two key challenges to building a successful EM are creating liquidity and creating and capturing value (Bruun et al., 2002; Engström & Salehi-Sangari, 2007). The basic idea is that to achieve the ultimate platform objective, namely profitability, an EM must c uilding liquidity and creating and capturing value.

Focus

The choice of focus for a platform involves identifying the right set of target buyer and seller segments and choosing the product categories to offer to them. An unclear direction would result in selling many products to many users while not providing enough value to anyone. The approach, especially in the beginning phase, should be to choose one focal product-buyer–product-seller category combination, provide enough value to both the buy- and supply-side user groups, to attract them to the platform, and quickly dominate the selected market space to create a critical mass of transactions (Bruun et al., 2002; Engström & Salehi-Sangari, 2007). The three choices concerning identifying the focal market concern geographic coverage, horizontal vs. vertical focus (product category and segment) and the range of services offered (Engström & Salehi-Sangari, 2007). First, it is beneficial for a platform to serve a limited geographic territory at the beginning of its life cycle. After understanding buyers’ and sellers’ spatially determined needs and the regulatory requirements of a restricted geographic area well, the platform can scale to buyer–seller spaces and geographic locations resembling the initial targets. There is an argument favouring starting at a large scale to achieve economies of scale as early as possible in the organizational life cycle; however, it may depend upon the variability of the need for target customer segments spread across geographies and local regulations. The second choice concerns horizontal or vertical scope. Horizontal EMs are industry-agnostic and are based on functions or products. Vertical EMs, on the other hand, are industry-specific and are more general in terms of functional and product variety. The choice of focus depends on the core value proposition that the platform intends to offer. The value proposition of horizontal EMs is usually lower transaction costs for sellers and lower price for buyers. The value proposition of vertical EMs is collaboration, as they are well positioned to cater to each industry’s unique needs (Engström & Salehi-Sangari, 2007). Third, in addition to facilitating the trade of products, a platform can distinguish itself by offering several value-added services, such as access to payment gateways, banking, insurance services and data analytics. These services also provide other benefits to a platform, such as a hedge against adoption and envelopment risks, a feedback mechanism and enhancement of platform rent appropriation potential through complements. Especially during an EM’s launch, a diffused focus increases the risk of creating too much complexity and conflicts of interest among the multiple sides or a challenge of prioritization among target markets and geographies. It may also be easier to solve the initial chicken-and-egg problem—no user moves to join the group because of lack of other users—by starting with a narrow focus, namely fewer products, sides and geographies, and at least partially vertically integrating into some of the ‘missing’ sides by oneself (Hagiu, 2014).

Governance

Ensuring appropriate governance—who can join and regulate the transactions and redress complaints—is vital for increasing the adoption rate of the e-marketplace by both the seller and buyer user groups. In terms of governance, the broadest choice a platform has is to be either neutral or biased and either open or closed (Engström & Salehi-Sangari, 2007; Kaplan & Sawhney, 2000). A third-party platform intended to facilitate information flow and transactions between user groups should ideally be neutral and provide comparable benefits to both sides. However, a biased platform may be needed to build traction to attract it onto the platform, especially during the launch phase. Platforms strongly biased forever towards a side run the risk of deterring the other side, moving away from the platform. A neutral form of governance helps create a perception of trust and fairness and facilitates setting standards and regulations, garnering collaboration, lowering channel conflicts and increasing market and supply chain efficiency (Bruun et al., 2002; Grieger, 2003). However, the biggest challenge of a neutral platform, especially during the early phase, is that it faces the chicken-and-egg problem: Neither side is willing to commit to the platform.

A platform sponsor may choose to keep the platform closed, maintaining close control over the entire platform architecture and uses. As a thumb rule, tighter governance norms are preferred when quality members in user groups matter more than the mere number of participants in user groups for members’ transaction and experience. Often, the market is not efficient, perhaps because of information asymmetry, the asymmetric bargaining power of participants or lack of a contract enforcement mechanism in weeding out poor-quality members, and high-quality participants need to be rewarded and incentivized to join the platform and participate in transactions (Hagiu, 2014). However, some platforms may require a certain degree of openness to make the platform value proposition feasible and appealing. While deciding to open the platform, a platform sponsor needs to make three choice combinations, namely roles, extent and external partners. While ‘roles’ refers to who can be buyers, sellers, platform sponsors and platform providers, ‘extent’ refers to the degree of their flexibility in development, commercialization, use and non-discriminatory rules, and ‘external partners’ refers to involving complementors and third-party providers to be part of the value net.

Functionality

Offering optimal functionality requires creating a powerful value proposition, the core elements of which need to be designed, integrated, built and profitably provided to the demand- and supply-side user groups. A modified version of the ‘3C Framework’—commerce, content and collaboration—developed by A. T. Kearney (2000) helps us understand B2B EMs’ value proposition (Bruun et al., 2002; Engström & Salehi-Sangari, 2007; Kearney, 2000). Commerce refers to the transaction structure and pricing. Before deciding on the type of transaction structure, one needs to understand the product complexity, available liquidity (transactions) and participants’ maturity about e-commerce (Bruun et al., 2002). Depending on the number of participants on the demand and supply sides, a platform could take different structures: buyer-centric, third-party exchange or seller-centric. A buyer-centric platform (e.g., the Indian Government e-Marketplace [GeM]) has many suppliers and few buyers. A third-party exchange (e.g., Udaan, Moglix) has many suppliers and buyers, whereas a seller-centric platform (e.g., McKesson) has few suppliers but many buyers. A platform’s transaction structure also concerns whether the platform may or may not facilitate online transactions. A platform that does not enable any online trade would only be an online catalogue or lead generator. A platform that allows online transactions acts as an intermediary, that is, as the ‘dealer’ (holds inventory) or the ‘broker’ (does not keep inventory).

Pricing, a crucial aspect of the platform value proposition, determines the adoption rate of EMs among various participants and the possible rent appropriation. Hagiu (2014) notes the following six determinants of pricing on a platform. First, the side that can capture cross-side network effects (which is poorer if the subsidy side transacts with rival platforms) should be charged more. Second, the more price-sensitive user group should be charged less. Third, the more quality-sensitive user group should be charged less (e.g., gamers), and the other side should be charged more (e.g., game developers). Fourth, the level of subsidy (of freebies) to one side is capped by the cost of output (or freebies). Fifth, the level of subsidy (or freebies) to a user is also capped by the user’s (marquee) brand value. Sixth, the same-side network effects (if negative) set the upper limit on freebies for the subsidy side. Depending upon the product/service, pricing can be made in one or more combinations of the following options: transaction fee, subscription fee, license fee, value-added service fee and advertising fee (Bruun et al., 2002).

Content refers to the scope of products and services offered via the platform. Combining the two sourcing choices—‘spot sourcing’ and ‘systematic sourcing’—for the two types of goods and products (i.e., ‘manufacturing’ and ‘operating’) inputs can lead to four platform categories based on the ‘scope’ (Engström & Salehi-Sangari, 2007; Kaplan & Sawhney, 2000). Platforms that engage in spot sourcing of operating inputs are called ‘yield managers’ (e.g., Employees, iMark.com, CapacityWeb.com). In contrast, platforms that engage in spot sourcing of manufacturing inputs are called ‘exchanges’ (e.g., PaperExchanges.com, IMX Exchange, e-Steel). Platforms that engage in systematic sourcing of operating inputs are called ‘MRO’ (manufacture, repair and operations) supplies or ‘hubs’ (e.g., IndustryBuying, Udaan, Amazon Business). Platforms that engage in systematic sourcing of manufacturing inputs are called ‘catalogue hubs’ (e.g., ChemDex, Moglix, PlasticsNet.com). The platform must identify one of these categories based on the target buyer–seller segments and the industry buying patterns to build a successful platform (Bruun et al., 2002; Kaplan & Sawhney, 2000). MRO hubs function as demand aggregators (enable buyers to aggregate demand and benefit from price discounts) or transaction facilitators (improve transaction efficiency by automating ordering process and management). They are commonly industry-agnostic (horizontal) platforms. The Indian B2B e-marketplace pioneer ‘Udaan’ is one platform as an MRO hub. Catalogue hubs function as supply consolidators, offering buyers low prices and access to a fragmented and diverse supplier base and assisting with valuable information. Catalogue hubs are industry-specific (vertical) platforms. The yield manager’s function is to create liquidity in illiquid markets, match uncertain demand and supply to ensure resource utilization and smooth price volatility. The value of yield managers is in bringing price transparency, better yields to suppliers for excess capacity and flexible expansion/contraction of operations for buyers. Exchanges function as single- or double-sided auctions allowing buyers and sellers to post bids and ask for prices according to ongoing demand–supply conditions (Bruun et al., 2002; Kaplan & Sawhney, 2000). The Indian GeM is an example of exchanges with reverse-auction features. The third element of the value proposition, collaboration, has commonalities with the broad set-up-related choice, partnership, as discussed in the following section.

Technology and Partnership

The design and delivery of the product/service component of B2B EM value proposition to the user groups’ platforms must be collaborated upon with supply chain partners, including trading participants and third parties. Third-party partnerships may include partnerships for logistics, payment service provision, integration with legacy IT systems, warehousing and broking. Strong and well-defined collaborations with third parties lead to a tightly integrated and agile supply chain (Grieger, 2003). The technology base of the platform has a crucial role to play in the success of the platform via advanced functionalities, such as market making, procurement integration, collaboration tools, ability to work with legacy systems and extranet and frictionless integration with the Enterprise Resource Planning (ERP) of trading and third-party partners (Bruun et al., 2002; Engström & Salehi-Sangari, 2007; Kearney, 2000).

A critical decision concerns the platform’s technical standards and the degree of openness to ensure future compatibility and agility. A platform sponsor should consider diffusing its technology when the technology needs to be combined with other firm value chain activities to be profitable, when it requires third-party development of complementary goods and when competitors can launch strategically equivalent technology (Schilling, 1999) quickly. The premise of any technical choice should be a vision of a scalable, flexible and secure platform (Grieger, 2003). As traditional businesses’ wisdom goes, platforms also need to focus on their core competencies and establish partnerships to ensure a complete system and share responsibilities and rents to ensure partnership sustainability (Bruun et al., 2002; Kearney, 2000). Some of the critical partnerships to establish are those with investors, existing buyers and sellers, new buyers and sellers, broker intermediaries, new infomediaries, industry associations, content providers, IT (information technology) vendors and software developers.

Challenges

In building liquidity and creating and delivering value, challenges are faced by B2B EMs (Bruun et al., 2002). Liquidity refers to the ‘transactions done’ on an EM (Bruun et al., 2002, p. 292). Reaching high levels of liquidity early in its life allows an EM to exploit economies of scale, build a knowledge base about the customer, product, technology and trends and exploit economies of scope in operations and offerings. This setting eventually guides EM to market leadership. This early liquidity leads to an increased transaction growth rate as time progresses, driven by positive network externalities.

Some of the risks the user groups may perceive which delay the early onset and growth of liquidity are business stealing or competitive risk, hold-ups, stranding, abandonment, integration, the penguin problem and the chicken-and-egg problem (Eisenmann, 2007; Farrell & Saloner, 1986; Katz & Shapiro, 1994). A user perceives the business stealing or competitive risk when it is likely to have too many rivals on its side and fears losing its customer base to rivals. A user perceives the hold-up risk when it fears that the dominant platform may extract too much value from the transaction. While the stranding risk makes the user unsure about which platform will dominate and fear backing the wrong side, the abandonment risk makes the user unsure whether the platform sponsor would continue to make the required investments to keep the platform afloat and growing. Users perceive integration risk when they fear that the platform provider may also perform network-user roles (especially that of the supply-side user) (Eisenmann, 2007; Katz & Shapiro, 1994). In new markets, uncertainty is usually high, and users have different expectations. Fragmented users in such a market cannot communicate expectations or coordinate behaviour, which may cause network growth to halt. This condition is referred to as the ‘penguin problem’ (Eisenmann, 2007; Farrell & Saloner, 1986). The ‘chicken-and-egg problem’ refers to the scenario where neither the demand-side user group nor the supply-side user groups is willing to join the EM because of lack of enough participants on the other side (Eisenmann, 2007; Katz & Shapiro, 1994). EMs need to make strategic choices, described in the next section, to mitigate these risks for early user groups and to protect their competitive edge over time.

Creating and delivering value is another critical challenge EM start-ups face. Participants have no reason to join an EM start-up if it cannot position itself as an enabler of additional means of creating and capturing value. While the probability of a user engaging in a transaction increases with an increase in the user base on the other side, it decreases with an increase in the user base on the same side. Thus, the trade-off that EM start-ups face is that of achieving a critical mass on either side. Too many players on one side (e.g., sellers) are good for the other (buyers) but not necessarily for the same side (suppliers). A related choice concerns the pricing of services. While charging of higher prices would ensure an EM’s profitability initially, it would hinder the EM from achieving critical mass on the users’ side.

On the other hand, charging nominal prices or charging selectively may ensure a quick rise in liquidity on the platform, reducing the platform’s rent appropriation potential. There is thus a trade-off between quick amassment of liquidity (volume of the transaction) vs. profitability. Apart from the nature of the services and the user groups, competition and regulation also play a role in determining prices for the user groups at EMs. Following a set of launch and growth strategies may be helpful for an EM to overcome the challenges.

Launch and Growth Strategies

Having established the platform’s architecture, the next set of choices involve choosing its launch and growth strategies. The choices a platform needs to make before its launch to ensure faster and deeper adoption involve market focus, services, onboarding strategy, pre-committed investment, marquee-user strategy, partnerships and openness and subsidy (Evans, 2009; Evans & Schmalensee, 2010; Gawer, 2011; Parker et al., 2016). At the launch, a platform can focus on a niche market (geographically or by industry or customer) or start with a broad base. To test the value proposition and user responses, a platform may begin with a niche or targeted user group and build and gradually expand its focus based on feedback. For instance, the commonly used social media platform ‘Facebook’ was initially launched for a niche group of college students. As the platform evolved with more users entering it, it was taken to new markets (customer segments) and user groups. This strategy has proved to be successful for several platform businesses, such as Amazon, Moglix, Udaan and Uber. Second, when a platform is launched, it may or may not provide complementary services. The challenge here is that the platform sponsor would ideally want to offer a full suite of benefits. However, the platform is limited by its resources, technical capabilities, partnerships, the uncertainty of adoption and the competitors’ time to market. The second set of choices a platform makes are about offering some services, namely should some services be provided independently or as a bundle and the core proposition (Parker et al., 2016).

Third, a B2B platform has a minimum of two user sides—buyers and sellers. Depending upon the centricity (buyer-centricity, seller-centricity or neutrality), industry, market focus and other architecture choices, a platform could be launched with one or both sides. The simultaneous strategy involves establishing both sides together to ensure market making and demand–supply match. For instance, Udaan found both buyer and seller sides at once. A sequential strategy is demonstrated when the platform is launched with access to one side, followed by the other side over time. For instance, YouTube was first launched for viewers with its content, followed by the opening up of the platform for advertisers and content creators. In cases where it is initially difficult to attract buyers or sellers, platform sponsors may be required to take up one side’s role. For instance, when McKesson launched its B2B platform for medical supplies, it acted as a supplier to buyers on the platform (Evans, 2009; Parker et al., 2016). Fourth, by nature, some platforms may require upfront commitments—economic or order-quantity or time-to-deliver or technical—from the users at the time of joining the platform. For instance, Diners Club required pre-commitment from restaurants, as well as banks and payment networks.

Fifth, having a marquee user may be an ideal strategy for faster adoption when launching a platform. For instance, it may be a good idea for a buyer-centric platform to engage a marquee buyer to interest other EM buyers. Sixth, during the launch, partnerships can help increase adoption. Increasing platform openness would also improve adoption. To this end, the platform has choices for interoperability, licensing of new providers to expand the network, broadening of platform sponsorships, absorption of complementary services from other platforms and backward compatibility. However, some of these choices could be irreversible—once the platform has been opened, it may be necessary to keep it open to partners throughout its life. Seventh, attracting interest to the platform may require providing price subsidies to buyers and sellers. The choice is about the users to whom subsidy shall be provided and whether it would be on the product and/or on complementary services (Bruun et al., 2002; Evans, 2009; Gawer, 2011; Parker et al., 2016).

Empirical Exploration

To complement the above-noted understanding derived from the literature review, an exploratory investigation, through secondary data, was conducted for three B2B EMs from India. The geographic focus was limited to India to control for macro-spatial exogenous environmental factors. All the three case studies pertain to a certain segment of B2B EMs, namely third-party exchanges, which predominantly focus on systematic sourcing and are also online distributors (and not just lead generators), brokers or dealers. This setting allows us to control for industry- and sector-specific exogenous environmental factors. These three firms are: Udaan (

Case 1: Udaan

According to its website, Udaan is India’s largest national B2B distribution platform designed to solve Indian businesses’ small- and large-trade and sourcing problems across sectors. Launched in 2016, Udaan is an industry-agnostic platform based out of Bangalore, India. It was started by three founders who were ex-employees of Flipkart, India’s home-grown B2C e-commerce firm. Udaan has become a worldwide case study for witnessing hypergrowth and turning into a unicorn start-up within 18 months of its launch, possibly the fastest ever to do so. Udaan started as a logistics platform for staples, electronics and apparel and focused on the region of Bangalore and some other areas within the state of Karnataka, India. The platform’s adoption rate was fast, and soon, it diversified in terms of products, geography and services.

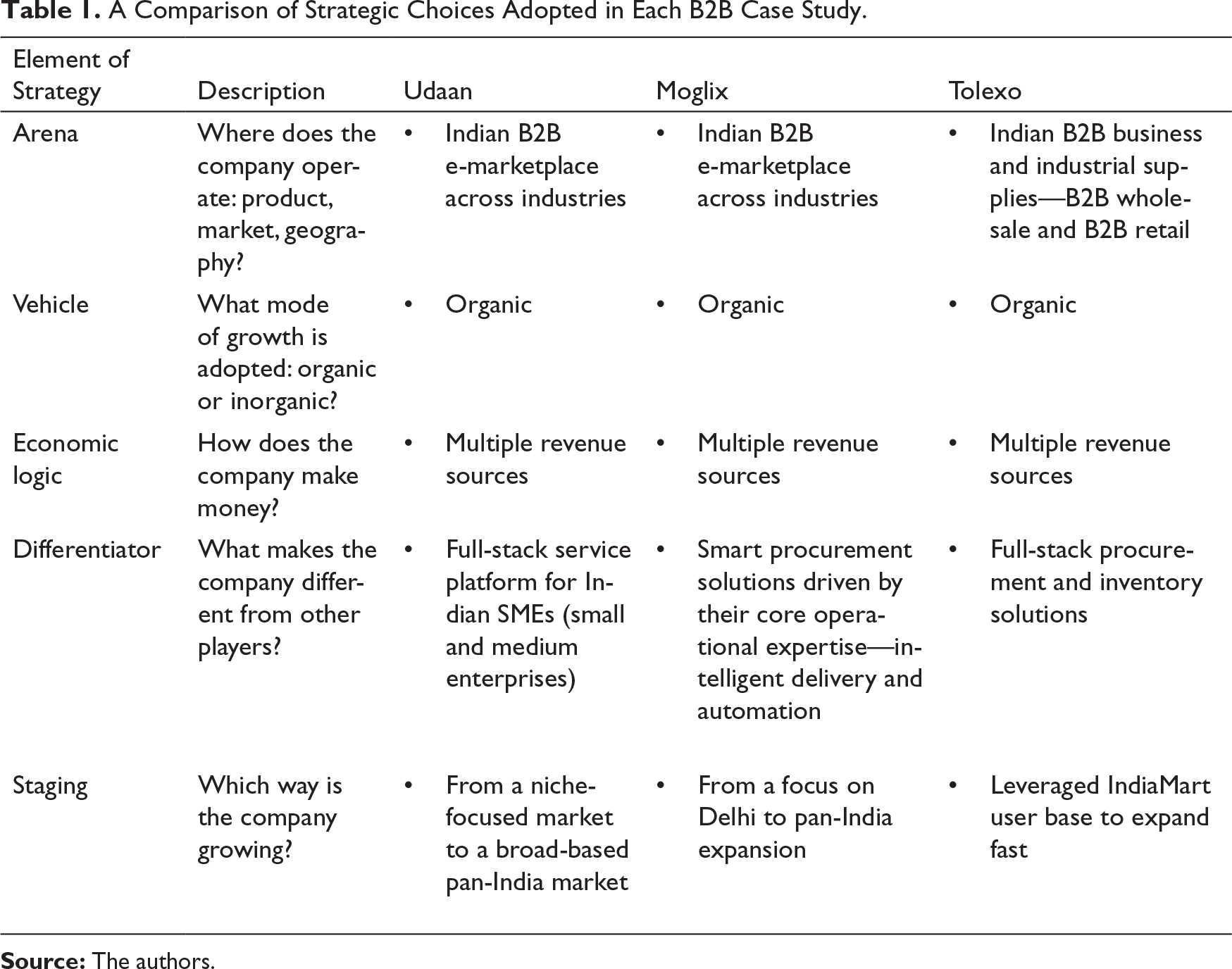

The three founders had a robust technology and operations background that helped lay down the foundation of the organization. The team had the right knowledge, skill set, network and experience in operations, supply chain, logistics and technology to kick-start the hypergrowth of the organization. This also helped Udaan raise adequate capital ($870 million in total funding over 3 years) to fund the growth. The hypergrowth witnessed came from the strategic choices of Udaan, which can be summarized using the five elements of the strategy framework (Hambrick & Fredrickson, 2005) as outlined in Table 1.

A Comparison of Strategic Choices Adopted in Each B2B Case Study.

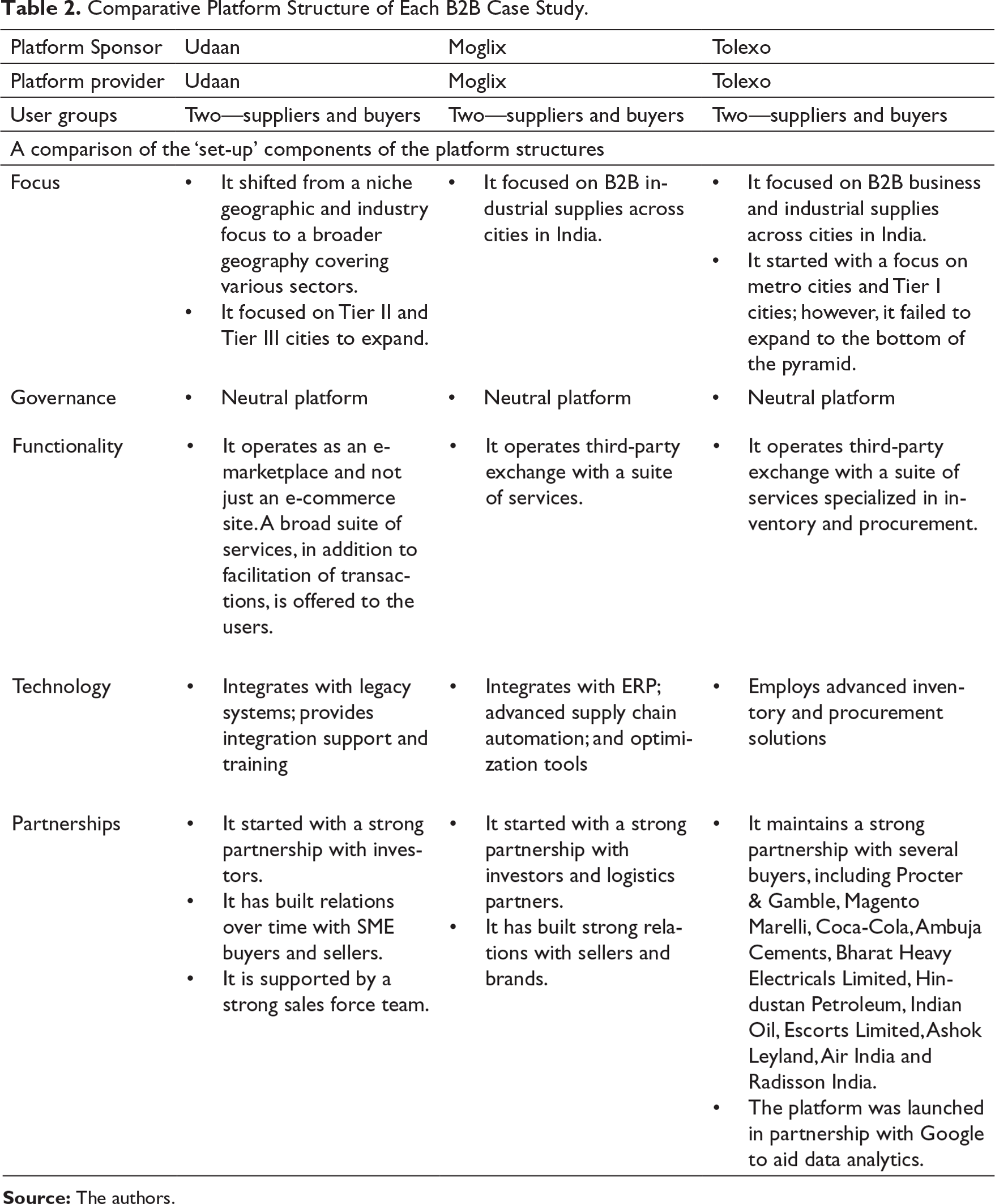

In terms of human resources policy, Udaan has always hired candidates and professionals from elite institutions, such as IITs and IIMs. The founders’ philosophy that runs deep down throughout the organization is to work for the organization and not for the CEO. Udaan has no official CEO appointed, which helps avoid political issues and disputes between the founders about power and control over the organization. The comparative platform architectures and structures of the three cases—Udaan, Moglix, and Tolexo—are outlined in Table 2.

Comparative Platform Structure of Each B2B Case Study.

The platform launch strategy adopted by Udaan included the simultaneous launch of both user sides—buyers and sellers. To the industry’s surprise, Udaan did not engage in any other strategy to entice users and fasten the adoption rate and yet was successful in building the scale based on a strong core value proposition. Udaan did not rely on any subsidy on pricing to either sellers or buyers. It was successful in attaining the critical mass necessary to gain traction and fuel the growth. Also, its other choices, such as neutrality of platform, the right set of technological support, partnerships and alliances and other strategic decisions, favoured the hypergrowth it witnessed. Udaan’s value proposition covered all three aspects: improvement in market efficiency—through matching demand and supply across the large Indian landscape and harnessing supply chain efficiency—optimization of supply chain via aggregation, logistics optimization and other supply chain practices and creation of new value—Udaan’s complete suite of services, including packaging, warehousing and working capital finance, provided all necessary complementary services to buyers and sellers to execute business transactions successfully. Udaan’s primary revenue source is the transaction fee on each transaction. The more significant chunk of revenue is from the interest income on working capital finance and other services. Udaan’s vision is to eventually shift to a revenue model from financing rather than e-commerce. E-commerce has helped it organize B2B purchasing and allowed Udaan to capture the necessary data to provide financing solutions.

Case 2: Moglix

Launched in 2015, Moglix started as a B2B platform for industrial suppliers operating in utility-based products, such as fasteners, MRO supplies and electrical, hardware and safety items. It has its headquarters in Singapore but operates out of Karnataka, India. It was founded by Mr Rahul Garg, an ex-Googler, MBA graduate from Indian School of Business (ISB) and IIT Kanpur engineer. Rahul had 9 years’ experience in strategy, product management and operations technology before starting Moglix. The founding team consisted of professionals from Google, IITians and IIM and ISB management graduates. Backed by Mr Ratan Tata, Moglix began to scale fast, growing across cities. Other eminent investors in Moglix included Accel Partners, International Finance Corporation (IFC), Sequoia Capital, Tiger Global Management and some 10 other investors.

Moglix started as a platform for transacting industrial equipment, with a revenue model of transaction fees and fees for value-added services. At its launch in 2015, the platform hosted 50 brands across 10 categories and was incubated by SAP Accelerator. The rapid expansion supported the increase of the product portfolio to 21 types from 1,000 sellers. The company also operated two warehouses in the country. However, Moglix maintained the policy of no credit as against its competitor Udaan, which, utilizing its working capital finance solutions, provided extended credit to buyers and sellers. The platform’s revenue model includes a percentage commission on every transaction; volume aggregation allowing for bulk discounts for larger customers; fees for ERP-related integration services; and pre-ordering service level agreements (SLAs). Since its launch, Moglix has been highly focused on delivery and automation, relying on its delivery services or third-party partnerships.

The organization follows a functional structure following a culture of self-leadership, intrapreneurship and a shared value to ‘get work done’. The one ordinary skill the organization maintains in its human resources policy is to build a team of innovative, fearless and hardworking candidates from top institutes of India. The platform architecture of Moglix is summarized in Table 2. The platform launch strategy adopted by Moglix included the simultaneous launch of both user sides—buyers and sellers. Given its strong partnership with sellers, Moglix initially provided subsidies to the buyer side to balance the supply–demand to increase adoption. The company engaged some marquee buyers, such as Lomax, Havells and Kirloskar, to build a base for attracting other buyers.

Case 3: Tolexo

In 2014, Tolexo was launched as a subsidiary company of IndiaMart, India’s largest online catalogue and directory. The company was founded by Brijesh Agarwal (founder of IndiaMart), Navneet Rai (co-founder of Inkfruit) and Harsh Kundra (ex-CTO [chief technical officer] of Jabong). The founders’ diverse and complementary backgrounds brought in the right experience to kick-start the B2B e-marketplace. Tolexo was soon able to raise sufficient funding from renowned investors, including Bennet Coleman and Co., Intel Capital, Amadeus Capital, Quona Capital and Westbridge Capital.

The background of IndiaMart gave Tolexo the leverage of information about the buyer and supplier base. Nearly 1.7 million SMEs and suppliers were already registered with IndiaMart. The parent company provided all types of resources for the platform—human capital, financial resources, technology base and physical infrastructure. Tolexo’s team comprises individuals from IITs, NITs (National Institute of Technology), BITS (Birla Institute of Technology and Science) and management institutes, including IIMs and FMS (Faculty of Management Studies). Tolexo’s revenue sources included marketing/advertising fees for product displays on the platform website; order handling and logistics fees and shipping fees for delivery.

Unlike Udaan or Moglix, Tolexo did not charge a transaction fee but instead provided support for order management and delivery and charged fees. The platform architecture of Tolexo has been summarized in Table 2. The platform was launched simultaneously for both buyers and sellers. Tolexo also introduced some marquee buyers to increase adoption and scale fast. Initially, in its B2B wholesale segment, Tolexo offered subsidies to buyers on bulk orders. By leveraging Google’s advertising products, like product listing ads, remarketing and shopping ad formats, Tolexo planned to drive demands. Google’s support aided Tolexo in testing and incubating B2B-category firms for fast business growth. However, to the disappointment of the entire industry, Tolexo failed as a platform during demonetization when per-unit economics failed. Tolexo decided to shut down its e-marketplace operations in 2017 to focus on an offline platform.

Discussion

Udaan and Moglix have been successful. However, Tolexo, with all its history drawn from IndiaMart, proved unsuccessful and closed down its B2B online operations in 2017. Tolexo, started by India’s largest and successful online catalogue business, IndiaMart, failed to achieve the growth necessary to generate liquidity and value in the market. It cites demonetization and business slowdown as the primary reasons for the failure of the platform. Although Tolexo made the same set of strategic choices as Udaan and Moglix, two factors that stood different for Tolexo can be attributed to its downfall. First, Tolexo more strongly felt the impact of the external environment than its peers, and second, Tolexo, being run by traditional businessmen, was not being run as a start-up to afford the initial cash burn. The owners did not wish to run a non-profitable business to attain the necessary critical mass and decided to shut operations. On the other hand, Udaan and Moglix were more risk-taking and were supported by their investors to fund capital and sail through initial losses. These two factors played out differently for Tolexo, leading to a future different from that of its other successful peers.

Based on the literature review (e.g., Bruun et al., 2002; Chong et al., 2011; Engström & Salehi-Sangari, 2007; Grieger, 2003) and empirical investigation of the three case studies, the following assortment of critical factors (and their dimensions) are identified, which may lead to the success or failure of a B2B platform in the Indian context. Some of key success factors identified in this study are: liquidity (critical mass, network effect); creation and communication of value (market efficiency—value through more transactions and better price discovery—supply chain efficiency—value through costs savings—new value creation); capture of value through an appropriate revenue model (type of revenue model, sources of revenue, suitability of revenue model as per industry and product); first-mover advantage (market share, market dominance, partnerships and alliances); neutrality and transparency (platform neutrality in the long term; transparency of policy and platform working); suite of services (complementary services); management team (experience, skills, shared values); appropriate technology (platform rules and ease of use, interoperability, compatibility, integration); strategic partnerships (marquee users, technology partners, service partners); operational efficiency (logistics, inventory, warehousing, delivery, content); and organization internal communication and interdependence (organization structure, communication flows and shared values). This list is consistent with the prior work on key success factors related to customer value (Bruun et al., 2002; Engström & Salehi-Sangari, 2007), platform governance (Kaplan & Sawhney, 2000; Parker et al., 2016), supply chain (Grieger, 2003), technology (Srivastava & Misra, 2014) and partnering (Bruun et al., 2002; Kearney, 2000).

Some key failure factors are: lack of liquidity (insufficient critical mass, poor or no network effect); insufficient value for both sides (supplier does not see value, supplier scared of price war, buyer unaware of quality, poor or insufficient enablement of suppliers); wrong entry strategy (adoption of the simultaneous or sequential approach when the other was more suitable, inability to attract marquee users); revenue model (targeting wrong set of services for earning revenue, critical mass crucial for the success of unit economics, earning income from both sides until critical mass is attained can be detrimental); governance (biased governance of platform); IT integration (underestimating the time required to integrate disparate IT systems); management team (management’s lack of right entrepreneurial mindset); financial performance (confusing industry turnover with firm’s total potential); value creation (overestimating the value created by the platform); services (incomplete or incompatible service offerings); and technology (poor quality, resistance to adoption of technology, anti-trust and privacy concerns).

Conclusion

Over the last few years, several B2B platforms have sprung up to revolutionize the way companies do business. However, as evident from research, building a platform business is challenging. Not every platform ends up gaining the critical mass necessary to provide liquidity and value to the market. Some of the key pillars upon which a platform business’ success rests are focus, functionality, governance, technology and partnerships. This study has important implications for start-up founders, especially in the Indian context.

Managerial Implications

The four key pillars noted above ensure the hygiene factor of the basic architecture of the B2B e-marketplace. Further, a careful and contextually suitable selection of the strategic launch and growth strategies—number of users, attraction of marquee clients, price subsidies—can help an entrepreneur avoid obvious mistakes while building the business. Additionally, careful monitoring and control of liquidity (critical mass), unique value creation (service design and ecosystem), delivery (supply chain optimization) and appropriation (business model innovation), timing, platform technology (design and control), management team and organizational design and strategic partnerships shall aid founders in guiding their ventures towards higher growth.

Future Scope

Future research can build on factors and choices identified in this study to develop questionnaires and conduct a large-scale empirical study in an emerging-economy context to test for generalization. Some useful lessons for an entrepreneur are as follows. First, strategic choices provide a guideline for preventing errors and a hygiene factor. However, by themselves, these choices cannot ensure success. Second, an organization’s management, values and external environment play a crucial role in determining its success or failure. Third, for a sustainable platform business, it is essential to revisit the choices repeatedly. For instance, a platform may launch with a bias towards one user group, but it must pivot itself towards neutrality for a sustainable business model over time. This study may serve as a ready reckoner for entrepreneurs and companies to run a platform business.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. The authors also thank the editor of this journal, Professor Arindam Banik, for his inputs and support during the revision of this article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.