Abstract

Despite banks not having any significant direct negative impacts on the environment and society, they adopt environmental, social and governance (ESG) accounting. Meanwhile, ESG reporting consumes additional resources and exposes firms’ strategies to competitors. The study employed a legitimacy theory to investigate the impact of ESG reporting on the financial sustainability of banks in Ghana. The study relied on 10 years of annual reports of all the banks in Ghana. The banks’ ESG reporting practices were assessed based on a content analysis method. The financial sustainability was measured based on return on assets (ROA) and net interest margin (NIM). Evidence showed that environmental reporting (ERI) impacted the banks’ NIM and ROA inversely and significantly, whilst governance reporting had a positive but insignificant relationship with NIM and ROA. The result further demonstrated that social reporting (SRI) impacted NIM and ROA positively and significantly. The overall ESG reporting had a negative and significant relationship with the banks’ financial sustainability. Hence, the ESG reporting did not improve the financial sustainability of banks, and banks in Ghana have less of an incentive to report on ESG as opposed to banks in other countries, where such reporting generally makes financial sense.

Keywords

Introduction

Between 2012 and 2018, some banking and nonbanking institutions in Ghana collapsed, which resulted in the loss of billions of dollars of depositors’ monies and those of investors. To ensure a sustainable banking sector, the Bank of Ghana injected more than 1.2 billion dollars into the sector (Knott, 2018). Prior to the collapse of these banks, the Bank of Ghana attempted to revive these banks by extending liquidity support to them. In addition to the monies the Government of Ghana lost in that process, several individuals lost their jobs, which experts estimated could affect more than 40,000 individuals (Galindo, 2019). Besides, the level of public confidence in the Ghanaian bank sector in Ghana ebbed, which threatened their existence. This unfortunate case could have a negative impact on the Ghanaian economy since the banking sector contributes substantially to Ghana’s gross domestic product (GDP).

The causes of the collapse of the banks are well documented. A report by an auditing firm, KPMG revealed, among other things, a lack of timely and relevant reporting practices by the banks as the major cause of their failures. This attracted stakeholders’ interest since research shows that public confidence in capital markets declined substantially because they no longer trusted the stand-alone financial reporting practice of firms (Casonato et al., 2019). A stand-alone financial reporting is believed to lack transparency and accountability because it fails to report the impacts of firms’ activities on the environment and society. This view is crucial because transparency and improvement in the reporting practice of firms have been identified as a major instrument that will help attract investors and improve the financial performance of firms in Ghana (Ackah & Lmaptey, 2017). Accordingly, Ghanaian firms were advised to look beyond the conventional financial accounting system and include environmental, social and governance (ESG) information in their reporting system. ESG reporting was considered a management tool that could restore credibility and confidence in the Ghanaian banking sector (Ackah & Lamptey, 2017). ESG reporting is an accounting practice that provides relevant information relating to ESG issues of firms to their stakeholders.

Meanwhile, ESG reporting consumes additional resources and exposes firms’ strategies to competitors (Sharma et al., 2019). Despite this, banks in Ghana have started to provide ESG information (Ackah & Lamptey, 2017). This is intriguing, given that the activities of banks do not have any significant direct negative impact on the environment and society. This raises a question about whether banks financially benefit from ESG reporting, given that it cost resources to provide them. This question is legitimate because, in other countries, firms are committing large sums of resources in responsible businesses, especially in ESG issues; for instance, at the beginning of 2018, US$12.6 trillion, representing 26% of assets under management in the USA, was under ESG management strategy (Buallay et al., 2020). Besides, the size of socially responsible investment in the USA increased by US$8.7 trillion from 2016 to 2018, representing 38% increment.

In developing countries such as South Africa, Brazil and India, firms are mandated to report their ESG activities (Buallay et al., 2020). However, in other countries such as Ghana, firms are not obligated to provide information on their ESG activities. This lack of compulsion may undercut or increase the benefits of ESG reporting. There is some evidence to suggest that firms’ financial sustainability is linear to ESG reporting (Carè & Forgione, 2019; Lee & Yeo, 2016; Zhou et al., 2017). Conversely, Carnevale et al. (2009) and Sharma et al. (2019) document an inverse relationship between ESG reporting and firms’ financial sustainability. Besides these conflicting findings, banks are often excluded from studies relating to ESG reporting and financial sustainability because of their unique characteristics. This leaves a gap in the literature, which needs to be filled.

The aim of this study is to examine the impact of ESG reporting on the financial sustainability of banks in Ghana. The study found that there is no immediate financial gain to banks in Ghana for reporting on ESG. This study has managerial and policy implications because it complements the banks’ management and the Bank of Ghana’s resolve to have a financially sustainable banking sector in Ghana.

Literature Review

Theoretical Framework

In this study, legitimacy theory is used to explain the relationship between ESG reporting and firms’ financial sustainability. Legitimacy theory holds that firms operate in a society with various stakeholders. To be successful, the firms must obtain and maintain the support of multiple stakeholders. Since firms operate in communities with various stakeholders, they attempt to win their trust and confidence by engaging in responsible activities (Silvestri et al., 2017). Such activities project them as responsible firms that care about the interests of multiple stakeholders. This implies that legitimacy theory relates to the concept of a social contract, which highlights a firm’s reliance on its environment, the varied anticipation of the society and its effort to justify its existence by legitimizing its operations (Al-Abrrow et al., 2019; Casonato et al., 2019).

Plumlee et al. (2015) explained that firms achieve legitimacy by voluntarily providing ESG information that explains their activities affect the society and the environment as well as the measures instituted to assuage the negative impacts of their activities. By reporting their ESG activities, firms attempt to influence the perception of the stakeholders. If the firms succeed in positively projecting themselves, the stakeholders would, in turn, receive them favourably and will like to do business with them (Beretta et al., 2019; Deegan, 2002; Tewari & Dave, 2012). This will increase the confidence of stakeholders, particularly suppliers, customers and investors, and attract more capital and favourable business transactions. Eventually, the financial performance of the firms would be impacted positively. The growing number of studies on legitimacy theory suggests that ESG reporting is mostly an avenue to achieve an organization’s objectives. Some studies, including Campbell et al. (2003), Plumlee et al. (2015) and Casonato et al. (2019), showed that legitimacy explains the relationship between ESG reporting and firms’ performance.

Empirical Literature Review and Hypothesis Development

There is an upsurge of interest in ESG reporting among firms because of its potential impact on their sustainability. Studies such as Lee and Yeo (2016), Zhou et al. (2017) and Carè and Forgione (2019) showed that ESG reporting had a positive impact on the financial performance of firms. Some streams of literature, such as those of Carnevale et al. (2009), Sharma et al. (2019) and Al-Hiyari and Kolsi (2021), also demonstrated that ESG reporting hurts the performance of firms. The argument advanced by these studies is that ESG reporting consumes resources that exceed the benefits obtained from such practices. These conflicting results may be caused by the institutional arrangements and the distinct features of the countries studied. This suggests that context is a significant variable in exploring the relationship between ESG reporting and firms’ performance. Nonetheless, these findings demonstrate that ESG reporting impacts the performance of firms, which can be either positive or negative. However, these studies mainly relate to manufacturing, extractive and other firms whose activities have been proven to have a negative impact on the environment and society. These studies excluded banks because banks have unique operational features that do not substantially negatively impact the environment and society.

Some studies also concentrated on the impact of ESG reporting on the performance of banks and financial institutions. The empirical evidence of most of these studies showed a positive relationship between ESG reporting and banks’ performance; for instance, Buallay et al. (2020) investigated the impact of ESG reporting on the performance of banks in the Middle East and North Africa (MENA) regions. The authors showed that the combined ESG reporting had a significant positive impact on the value and financial performance of the banks. The authors further demonstrated that social reporting (SRI) had a negative and significant impact on the banks’ profitability. In Bangladesh, Dhar and Chowdhury (2021) also examined the relationship between environmental accounting and the banking sector’s financial performance. They demonstrated that banks that adopted ESG reporting enjoyed better financial performance and higher market value. In a related study, Carè and Forgione (2019) investigated the impact of environmental disclosure on the performance of EU15 listed firms. They demonstrated a positive and significant relationship between environmental reporting (ERI) and the performance of the banks.

Some studies also document a negative relationship between ESG reporting and firms’ performance; for instance, Matuszak and Rozanska (2017) investigated the relationship between social responsibility disclosures and the financial performance of Polish firms. The authors found a negative relationship between the banks’ social responsibility disclosures and their net interest margin (NIM), suggesting that the banks that disclosed more social information performed poorer. In a similar study, Buallay (2019) examined the link between ESG reporting and the performance of banks in Europe and concluded that social responsibility reporting has a significant negative association with the banks’ return on assets (ROA), return on equity (ROE) and Tobin’s Q. This finding also implies that ESG reporting reduces the financial performance of banks. A related study conducted by Al-Dhaimesh and Al Zobi (2019) in Jordan found that environmental disclosure had no impact on the performance of banks whilst the aggregate ESG reporting had a significant positive impact on the financial performance of banks.

In Africa, some studies have also been conducted on this subject matter. One of such studies is that of Matemane and Wentzel (2019) who investigated the impact of integrated reporting on the financial performance of banks listed on the Johannesburg Stock Exchange. The study found no relationship between integrated reporting and the banks’ performance measured by ROE, ROA and Tobin’s Q. The study further found no significant difference between the banks’ performance before and after integrated reporting adoption. This evidence shows that banks do not benefit from the adoption of ESG reporting. Similarly, Adegboyegun et al. (2020) investigated the relationship between integrated reporting and the financial performance of banks in Nigeria. The study documented that integrated reporting had no significant relationship with the financial performance of the banks in the short run. However, evidence showed a significant positive relationship between integrated reporting and the banks’ performance in the long run. This result implies that the banks did not enjoy the immediate benefits from adopting ESG reporting.

From the preceding discussion, it can be stated that ESG reporting can influence the performance of firms. However, the direction of the relationship is conflicting among various studies. What is clear is that the direction of the relationship between ESG reporting and firms’ performance can be influenced by context, as espoused by Tilt (2016). This provides opportunities for further research to investigate the phenomenon in the context of banking institutions in Ghana. The weight of previous empirical evidence leads to the development of the following hypothesis.

Objective and Rationale of the Study

The activities of banks do not have any significant direct negative impacts on the environment and society, but they adopt ESG accounting, which consumes resources. Given this, the aim of the study is to investigate the impact of ESG reporting on the financial sustainability of banks in Ghana.

Methods

The study relied on the annual reports of all the commercial banks in Ghana. The study covered 10 years, from 2010 to 2019. During this period, 37 distinct banks existed at different periods. Due to mergers, takeovers and liquidations, 23 banks were operational as of December 2019. Consequently, those 23 banks were considered for the study. However, the study employed the following extra criteria to determine the banks to include in the study: the banks must have been in operation for at least 4 years and had a minimum of 4 consecutive years of annual reports to permit a longitudinal analysis. Based on these criteria, the study excluded Consolidated Bank Ghana Limited, which was established in 2018. As a result, the study included 22 banks in Ghana.

The ESG reporting practices were obtained from the annual reports of the banks. The study targeted 220 annual reports. However, one firm had 6 years of missing data. Two additional firms each also had 3 years of missing annual reports. Therefore, 12 annual reports were missing. Consequently, 208 annual reports were used for the study. The ESG reporting elements considered in this study were ESG information. The scores of each of the information categories were aggregated to provide the banks’ ESG reporting scores.

The banks’ ESG reporting was assessed based on a content analysis method. Consistent with studies such as Ackah and Lamptey (2017) and Matemane and Wentzel (2019), the ESG reporting was scored based on an evaluation matrix. The evaluation matrix was based on a 5-point Likert scale. The Likert scale was interpreted as follows: 5—full disclosure; 4—satisfactory disclosure; 3—some disclosure; 2—little discourse; and 1—no disclosure. The difference between the banks’ ESG disclosure practices was based on the quality of ESG information provided in their annual reports. The study measured the ESG reporting quality according to the degree to which the information met the qualitative characteristics of information dictated by the guiding principles of the Integrated Reporting Framework.

Econometric Approach

A multiple regression model was used to examine the impact of ESG reporting on the banks’ financial sustainability. The equations were estimated by employing a panel data analysis. The statistical analysis involved the use of fixed effects multiple regression model. The study adapted Ohlson’s (1995) model for the estimation. Following Al-Dhaimesh and Al Zobi (2019) and Buallay et al. (2020), the study developed models (1) and (2) to estimate the impact of ESG reporting on the banks’ financial sustainability. In model (1), the independent variable is a composite ESG reporting index (ESGRI), whereas model (2) uses three different reporting indices for E, S and G separately.

The variables in the models are explained below.

FinS it denotes the financial sustainability of a bank i at time t. The financial sustainability was measured based on two performance metrics: ROA and NIM. ESGRI it represents the ESGRI of a bank i at time t. This was determined based on the average score of the three elements of the banks’ ESG reporting. ERI it , SRI it and GRI it refer to the ESGRIs, respectively. CRAR it denotes the capital-to-risk weighted assets ratio (CRAR) of a bank i at time t. CRAR was measured as the banks’ ratio of total assets to their risk-weighted credit exposure. MgtEff it represents the management efficiency of a bank i at time t, which was measured as the ratio of cost to income. Moreover, Size it represents the size of a bank i at time t, which was measured as the natural logarithm of total assets of the banks. Leverage it is the ratio of total liabilities to owners’ equity of a bank i at time t. Age it is the number of years a bank had existed at time t. Finally, β and α are the coefficients of the variables, ε it is the stochastic error term at time t, i is the number of firms and t is the time period.

Results and Discussion

Descriptive Statistics

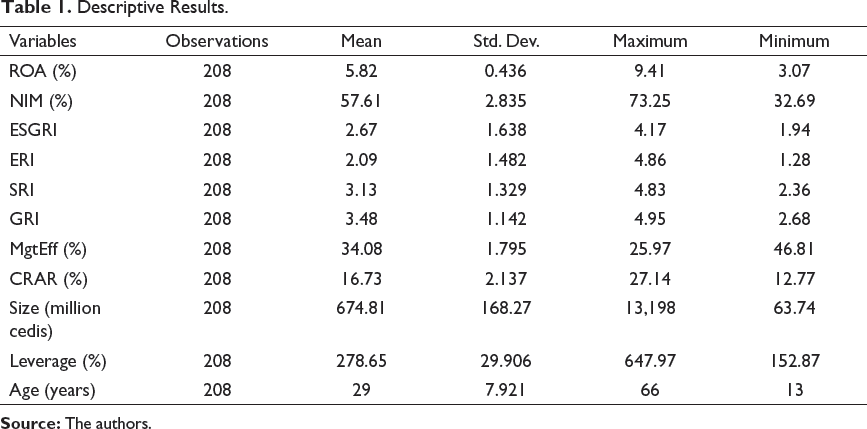

Table 1 presents the summary statistics of the variables used for the estimation. The results indicate that the average ROA of the banks is 5.82%. However, the maximum and minimum ROA of the banks were 9.41% and 3.07%, respectively, indicating that some of the banks were more profitable than others. The average NIM of the banks was also 57.61%. These results show that all the banks were profitable during the study period. It is also evident that there was a disparity in the financial performance of the banks. This study will later explore if this could result from the differences in the ESG reporting of the banks. Concerning the ESGRI, the average score was 2.67, suggesting that the banks disclosed ESG information in their annual reports. However, the standard deviation of 1.638 indicates a variation in the ESG reporting among the banks. The average ESGRIs were 2.09, 3.13 and 3.13, respectively. The standard deviations of these variables further show a wide dispersion in the banks’ reporting practices.

Descriptive Results.

Multicollinearity Test

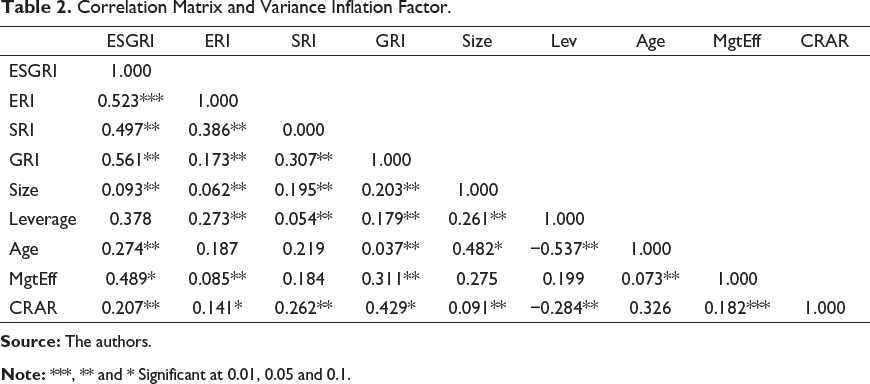

Correlation Matrix and Variance Inflation Factor.

Regression Results

Regression Results.

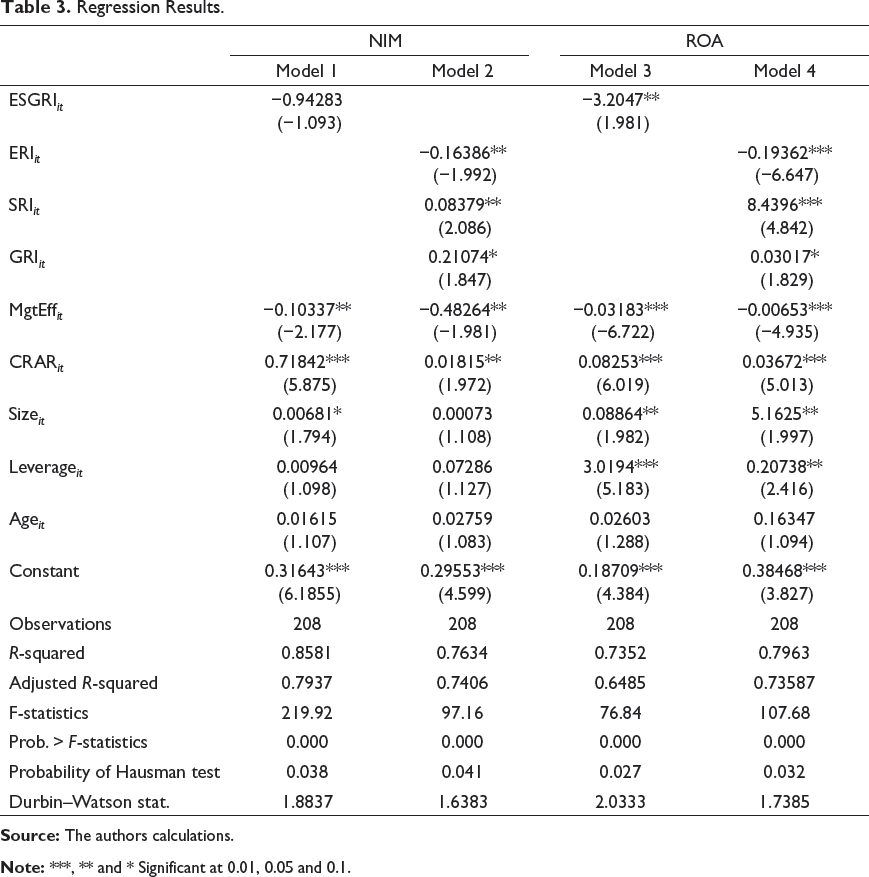

Table 3 presents the results of the relationship between ESG reporting and the financial sustainability of banks in Ghana. Model 1 estimated the relationship between the composite ESGRI and the banks’ NIM and ROA. The hypothesis predicted a positive relationship between ESG reporting and the banks’ NIM and ROA. The result contradicts the hypothesis, showing a negative and statistically significant (p < 0.05) relationship between ESG reporting and ROA. On the other hand, evidence demonstrates a negative and statistically insignificant relationship between ESG reporting and NIM. These results imply that banks suffer financially from practising ESG reporting, suggesting that they may incur more cost on ESG reporting than its associated financial benefits. This indicates that customers may not consider the ESG activities of the banks in their purchasing decision. The result is surprising, considering the several complaints made by a section of Ghanaians and media on certain firms’ activities. Moreover, this result can be the case that firms spend so much on ESG reporting production, of which no commensurate financial benefits accrue from it.

Models 2 and 4 present the results of the impact of the disaggregated components of ESG reporting on NIM and ROA. Contrary to the expectation, the result shows that ERI has an inverse and significant (p < 0.05) impact on both NIM and ROA. Besides, evidence shows that governance reporting (GRI) has positive but insignificant (p > 0.05) relationships with the banks’ NIM and ROA. These results suggest that environmental and governance disclosures do not provide any significant financial benefits to the banks. These results imply that banks do not obtain any financial benefit from each environmental and governance information disclosed in a single document. On the contrary, and confirming the hypothesis, evidence demonstrates that SRI has a positive and significant (p < 0.05) impact on the banks’ financial sustainability (NIM and ROA).

The results on the control variables showed a negative and significant relationship between management efficiency (MgtEff) and NIM and ROA. These results imply that management efficiency (MgtEff) is significant in explaining NIM and ROA of the banks. Besides, the negative and significant relationship between MgtEff and financial sustainability is possible because efficient managers can formulate effective loan policies to reduce loan delinquencies and improve performance. These policies could minimize operational costs, which could improve both NIM and ROA. Similarly, CRAR was positive and significant in all the models, suggesting that CRAR may have had a significant impact on NIM and ROA. These results confirm the findings of previous studies, such as those conducted by Matuszak and Rozanska (2017), Sharma et al. (2019), Carè and Forgione’s (2019) and Sharma et al. (2019) who documented that banks’ performance is conditional to MgtEff and CRAR.

The results further show a positive relationship between the banks’ size and their ROA and NIM in all the models. However, the association is statistically significant (p < 0.05) in only models 3 and 4. These results imply that the size of a bank’s assets influences its ROA. Concerning the banks’ leverage, evidence indicates that it has a positive and insignificant relationship with NIM in models 1 and 2. In contrast, the relationship between leverage and ROA is positive and significant in models 3 and 4. The implication of this result is that leverage is a major variable that influences banks’ ROA. Evidence further shows that the firms’ age has a positive and statistically insignificant impact on NIM and ROA. The post-estimation results show that the model and its variables are robust. First, the R-square for all the models is more than 70%, suggesting that the models’ variables explain the variations in the dependent variables by more than 70%. These results show that the models used for the estimation are robust and their associated results are reliable. The Durbin–Watson results of all the models range from 1.6 to 2.1, suggesting that they do not suffer from autocorrelation problems.

Discussion

Evidence shows that ESG reporting has a negative and significant impact on NIM and ROA. The findings further demonstrate that environmental disclosures impact NIM and ROA negatively. Although these results are contrary to our expectations, some theoretical arguments can explain this. First, the negative impact of ESG reporting on banks’ financial sustainability can be explained by the fact that the additional costs involved in undertaking ESG activities and reporting on them might not improve the performance of firms. This is plausible because, as firms become more socially and environmentally responsible, it becomes difficult to increase their profits because they may be unable to engage in projects without assessing their environmental and social implications. In this context, these environmental and socially responsible firms may reject profitable but environmentally and socially unfriendly projects, which could affect their profits.

Another possible reason for the negative relationship between ESG reporting and the financial sustainability of the banks is that the disclosure of extensive ESG information requires substantial resources because it involves putting in place systems for identifying, measuring and reporting such information. Moreover, providing information about the ESG processes, practices and performance of banks can attract substantial proprietary costs such as contractual, reputational and regulatory costs. Besides, banks that make ESG information disclosures are more exposed to public scrutiny and are consequently more likely to face adverse or bad publicity if they commit mistakes. By reporting on their ESG activities, these companies expose themselves to public scrutiny, which is likely to be used as a propaganda tool by their competitors, the community and distractors.

A further explanation of the negative relationships between ESG reporting and NIM, as well as ROA, is that the banks may invest resources in ESG activities and report on them without corresponding returns. In other words, contrary to legitimacy theory, the findings suggest that stakeholders might not value the disclosure of ESG information by the banks; thus, banks that committed extra resources to provide these sets of information obtained no real financial benefits. Despite the possible reasons for these results, they run variance with the findings of Carè and Forgione’s (2019) and Buallay et al. (2020). These authors demonstrated that the competitive advantages obtained through a positive image might manifest in the form of the increased ability of firms to attract and maintain quality human capital, customers and supplier loyalty, as well as increased sales. In addition, these results are inconsistent with prior studies, such as those conducted by Lee and Yeo (2016) and Dhar and Chowdhury (2021) whose evidence showed that ESG reporting has a positive impact on banks’ performance.

In contrast, these results affirm the findings of Matuszak and Rozanska (2017), Al-Dhaimesh and Al Zobi (2019), Buallay (2019) and Matemane and Wentzel (2019), who reported a negative relationship between ESG reporting and firms’ financial performance. This suggests that stakeholders/customers in Ghana did not consider the ESG activities of a bank in their decision-making. Even if they did, it might be the case that the benefits of cost savings of nondisclosure of voluntary ESG information might be more than the cost of providing such information.

On the contrary, evidence demonstrated that SRI has a positive and significant impact on the banks’ NIM and ROA, which supports the findings of earlier studies such as Lee and Yeo (2016), Zhou et al. (2017) and Carè and Forgione (2019). This result implies that banks that engage in SRI have a better financial performance. This result supports the legitimacy theory because banks can use social responsibility activities and their reporting to influence the perception and behaviour of stakeholders. More significantly, among the various components of ESG activities, the social element is more tangible, and the community can readily experience, feel and relate to. Hence, it is not surprising that banks that report their social responsibility activities enjoyed better financial performance than those that did not.

Conclusion and Managerial Implications

The study employed a legitimacy theory to investigate the impact of ESG reporting on the financial sustainability of banks in Ghana. Evidence showed that ERI had an inverse and significant impact on both NIM and ROA, whilst governance reporting had a positive but insignificant relationship with the banks’ NIM and ROA. On the contrary, SRI had a positive and significant impact on the financial sustainability of the banks, suggesting that banks that reported their social responsibility activities enjoyed better financial performance than those that did not. The study further found that the overall ESG reporting had a negative and significant relationship with the banks’ financial sustainability. The implication of these results is that the cost of providing ESG information may be more than its associated benefits. In conclusion, ESG reporting is not regarded as valuable to banks in Ghana since it did not translate into improved profitability. Overall, evidence is inconsistent with the legitimacy theory. This study has managerial and policy implications because it complements the banks’ management and the Bank of Ghana’s resolve to have a financially sustainable banking sector. By providing information on how ESG reporting affects banks’ performance, the findings would assist the Ghanaian government in future policies on environmental issues.

Limitation and Suggestions for Further Studies

The study’s major limitation is its inability to examine the short- and long-term benefit of the banks’ ESG reporting. The study suggests that further research should investigate both the short- and long-term benefits of ESG reporting. Other studies should investigate how investors react to ESG information.

Footnotes

Acknowledgement

The author is grateful to the journal’s anonymous referees for their extremely useful suggestions to improve the quality of the paper. Usual disclaimers apply.

Declaration of Conflicting Interests

Funding

The author received no financial support for the research, authorship and/or publication of this article.