Abstract

This article aims to analyse the effects of positive tone in management reports on stock return volatility. It is expected that this article contributes to the literature about disclosure by proposing an objective textual content analysis of management reports, focussing on optimistic words or expressions employed by firms and their effect on stock return volatility. The sample consisted of management reports and financial data from 576 different Brazilian firms’ stocks. Regarding volatility, our measure is based on daily stock returns from 1 April 2011 to 23 October 2020. The data related to positive tone and control variables were based on the fiscal years 2010–2019. Therefore, the database contains 3,945 stock-year observations. The study hypothesis was tested through a regression model with panel data. The main results suggest that companies with higher positive disclosure tone scores do not necessarily present lower stock return volatility in the subsequent period. The objective content of financial reports (for example, in relation to profitability) seems to be related to stock volatility; however, the tone of subjective expressions does not represent the main determinant of stock volatility.

Introduction

Disclosure and returns volatility seem to be closely related elements, since poor information environments may lead to higher risk. Prior literature has already indicated some evidence about the effects of disclosure on stock return volatility. Coluccia et al. (2017), for example, reported that firm industries with high disclosure levels presented lower stock volatility. According to Zhang et al. (2015), information disclosure implies market stability, since it brings efficiency to the markets. Furthermore, Du (2018) stated that environmental informational disclosure is valuable to mitigate information asymmetry. In view of this, we conducted a textual analysis of management reports and, based on the frequency of optimistic words and expressions disclosed, we examined their effects on stock return volatility.

It is worth mentioning that some previous studies already examined the relationship between disclosure and volatility, which include Cormier et al. (2011), Xu and Liu (2018), Tasnia et al. (2020), among others. Nevertheless, Lang and Stice-Lawrence (2015) affirmed that very little is known about certain aspects of accounting information associated with textual elements, precisely due to difficulties in handling, quantifying and analysing textual data. Early researches, like Loughran and McDonald (2011), Bodnaruk et al. (2015) and Yekini et al. (2016), have already addressed disclosure tone from a textual analysis perspective. We expect to expand previous research by analysing the disclosure tone of management reports using a textual analysis perspective and, then, testing the effect of disclosure on stock return volatility.

This article contributes to literature on disclosure, specifically regarding the effect of positive tone in management reports on stock return volatility, by proposing an objective analysis of textual content in the reports, focussing on optimistic words or expressions employed by firms. Researches that analyse corporate reports disclosure, usually, employ an index created from scores of various sentences or items related to disclosure, or a dummy variable receiving 1 if the firm publishes a determined corporate report or 0 otherwise.

The main concern with those procedures is that disclosure indexes or dummy variables usually do not capture important elements, which are not identified in the set of items that compose the index or the dummy variable. For example, an index or dummy variable may capture the effect of a topic or subject disclosed, but cannot identify the meaning and sentiments associated with the disclosure, which can only be determined through the analysis of textual content. Loughran and McDonald (2016) argued that, with the increase of computer power, textual analysis methods are emerging in accounting and finance studies. Loughran and McDonald (2016) also stated that, to measure the tone of a financial document, researchers usually count the number of words, which are related to a sentiment word list, scaled by the number of words in the document.

In addition, there is high subjectivity in the process of selecting the overall index elements, as well as in weighting, which compromises the reproduction of previous studies by other independent researchers, as a way of corroborating prior findings. Loughran and McDonald (2016) indicated three main advantages of textual analysis through word list when compared to traditional methods. First, it avoids researcher subjectivity, since disclosure is measured automatically, through word count. Second, it allows the analysis of large samples and extended documents, because frequency is tabulated by computers. And finally, with a publicly available word list, it is possible to replicate previous studies. Therefore, here we expect to overcome the limitations of traditional disclosure measures, since we did not employ a disclosure index or dummy variable, but an automated textual analysis based on positive expressions counting.

With regard to practical contributions, this research may help shareholders and potential investors in understanding the implications of information disclosed in management reports on stock returns volatility and, as a consequence, collaborate for decision-making. From the firm’s perspective, this study indicates that, on one hand, the content of financial reports, related to profitability, for example, can affect stocks volatility; on the other hand, the tone adopted in the text of managerial reports is not necessarily related to stocks volatility in the subsequent period (based on the main results of this article and based on the criteria used to conduct the quantitative analysis).

The remainder of this article is structured as follows. The second section comprises a literature review, in which relevant concepts and results from previous studies are discussed. The objectives of this article are indicated in the third section, followed by section four with the theoretical framework that supports them. The fifth section comprises the methodology, in which the procedures for sample definition, data collection and analysis techniques are described. The sixth session comprises data analysis, including tables with the main findings, which are discussed in the seventh section. Finally, the conclusions are presented, followed by managerial implications, limitations and suggestions for future research.

Review of Literature

Disclosure and Volatility

Disclosure and stock volatility are closely related elements, because lack of information implies higher risk. According to Dai et al. (2019), the stock price crash risk results from insufficient reporting of negative information. Specifically, regarding corporate social responsibility (CSR) reporting, since it is a relevant non-financial type of disclosure, Dai et al. (2019) affirmed that it constitutes an aspect that impacts a firm’s informational environment and, as a consequence, its stock price crash risk. In order to improve the quality of the information environment, Schreder (2018) indicated three specific elements that must be met by firms, namely: proper quantity of relevant information disclosed to investors; high precision of that information; and wide dissemination of information among the various groups of investors. From this, it is possible to assert that firms can reduce their stock price crash risk by disclosing information.

Another way to observe the effects of disclosure on stock return volatility is based on legal (mandatory by law) and discretionary (voluntarily developed) activities. Harjoto and Jo (2015) argued that analysts are more informed about mandatory activities than voluntary ones, and, because of that, the former would reduce stock return volatility while the latter would increase it. From a multivariate regression analysis, Harjoto and Jo (2015) found lower stock return volatility for firms with a higher CSR index. Moreover, when segregating CSR activities into mandatory and discretionary, Harjoto and Jo (2015) confirmed that mandatory CSR is better to explain decreases in stock return volatility than discretionary CSR. In face of this, it is possible to see that additional factors, such as mandatory or voluntary CSR activities, should be considered when analysing disclosure and its impacts. That is the reason a positive disclosure tone was added in the context of this study.

Previous Studies

Egginton and McBryer (2018) associated CSR disclosure strategies with equity market liquidity, including volatility of returns, from a sample of 3,511 firms. The authors documented a positive relationship between CSR disclosure and market liquidity, that is, the market positively reacts to CSR transparency, improving equity liquidity. This effect was more prominent for firms that, in the beginning, had a poor informational environment (lack of analyst following).

Li et al. (2020) advanced the discussion by conjecturing that annual report disclosure timing impacts future stock price crash risk. Li et al. (2020) argued that managers may delay annual report disclosure for periods of low market attention in order to conceal bad news. From a sample of Chinese companies in the period between 2001 and 2017, Li et al. (2020) found that when a firm changes its annual report publication date, it is likely that the firm faces greater stock price crash risk in subsequent times.

Some previous studies also showed that the nature of information presented in the reports, that is, whether it is composed of positive or negative words or expressions, generates market reactions, including impacts on performance and stock volatility. Li (2008) analysed the association between annual report readability and firm performance and earnings persistence. The findings suggested that when firm performance is poor, managers have incentives to produce annual reports with bad readability. In contrast, if the prospects of good performance are high, managers tend to adopt transparent information disclosure, presenting the good news.

In this regard, Kothari et al. (2009) conducted a content analysis of more than 100,000 reports, including firms, analysts and business press, with the objective of identifying the effects of disclosure on a firm’s capital market (their measures for the firm’s capital market were cost of capital, return variability, and analyst forecast error dispersion). The main results indicated that a positive disclosure tone is negatively associated with the cost of equity capital, stock return volatility and analyst forecast dispersion. On the other hand, a negative disclosure tone presented an opposite effect.

Yekini et al. (2016) studied the tone of the narratives published in annual reports of UK companies through the frequency analysis of positive words in the texts, and found that, in fact, the market seems to react to a positive tone in annual reports, so that the stock prices tend to increase around the disclosure date. Plumlee et al. (2015) documented a positive (negative) association between the firm stock price and the positive (negative) items of their disclosure index, which was employed to study the quality of voluntary environmental disclosure, thus suggesting that positive (negative) expressions in firms’ reports may trigger a market reaction.

The disclosure tone may even indicate firms’ future environmental performance. Arena et al. (2014), among other aspects, examined the relationship between environmental disclosure tone and future environmental performance of 288 firms from the oil and gas industry. They found that a positive disclosure tone is associated with positive environmental performance, that is, the use of optimistic language in firms’ reports signals good forthcoming environmental outcomes. Although Arena et al. (2014) did not approach stock return volatility in their findings, it is reasonable enough to say that firms with good environmental performance face benefits in this sense, according to previous researches, that include Muhammad et al. (2015), Cai et al. (2016) and Wamba et al. (2020).

Methodological Review

To identify methodological procedures employed by similar research on the subject, aiming to strengthen the research design of this study, we conducted a methodological review of recent previous studies that address disclosure and its resulting impacts on firms.

Li et al. (2020) examined the relationship between the disclosure timing of annual reports and its impacts on stock price crash risk, based on a sample composed of Chinese-listed firms in the period 2001–2017. The study adopted as its main analysis procedures descriptive statistics and regression models with panel data. The models were estimated using ordinary least squares, with the inclusion of fixed effects for industry and year. The standard errors were clustered at the firm level.

In a previous study, Egginton and McBrayer (2018) evaluated the effect of CSR disclosure strategies on equity market liquidity. The methodological procedures included descriptive statistics, bivariate analysis and multivariate analysis. The bivariate analysis was performed using Pearson's and Spearman's correlation coefficients between variables. With regard to the multivariate analysis, linear regression models estimated by the ordinary least squares method were employed. Similar to Li et al. (2020), Egginton and McBrayer (2018) also included in their models the fixed effects arising from the fiscal-year and industry. The robust standard errors were clustered by industry.

Maji (2019) analysed the disclosure of labour practices and decent work and its impact on financial performance of firms from Japan, South Korea, India and Indonesia during the period 2009–2017. The labour practices and decent work disclosure were measured through content analysis. As for data analysis, it employed descriptive statistics and quantile regression models.

To evaluate environmental disclosure practices, Chaklader and Gulati (2015) studied 50 Indian companies. Chaklader and Gulati (2015) started from a literature review, and classified profitability, industry, leverage, multinational status and environmental certification as independent variables. An environmental disclosure index was established as a dependent variable. The variables were analysed using descriptive statistics and regression models with pooled data.

Regression models with pooled data were also employed by Nag and Bhattacharyya (2016). In order to examine the corporate social responsibility strategies and activities disclosed in annual reports, as well as their relationship with firm's performance, Nag and Bhattacharyya (2016) studied annual reports of 30 Indian companies from 2007 to 2011. The analysis procedures included Pearson's correlation and regression models with pooled data.

Given this brief methodological review, it is observed that regression analysis with panel data is the most employed methodological procedure in related studies. Therefore, to achieve the objective of investigating the effects of positive tone in management reports on stock return volatility, we considered regression analysis with panel data as the main methodological procedure of this research.

Objectives

The objective of this article is to examine the effects of positive tone in annual management reports on stock return volatility. Here, it is conjectured that when firms adopt an optimistic tone in their management reports, their stock return volatility tends to decrease, because external users of financial information will consider less-risky-to-hold equity shares of firms with overall good information disclosures and low informational asymmetry. Our assumption of a relationship between a positive tone and stock return volatility is based on the discretionary disclosure theory, where managers tend to voluntarily disclose only the information that may generate positive outcomes and withhold, as long as possible, the negative news (Dye, 1985; Verrecchia, 1983).

Theoretical Framework and Rationale of the Study

The theoretical framework underlying this study is based on voluntary disclosure theory. According to Verrecchia (1983), when a manager of a risky asset has discretion in disclosing information to investors, the manager's decision to make the information public or not will depend on its effect on the asset’s market value. This occurs because disclosing information has a cost, which may reduce the value of the underlying asset. In view of this, Verrecchia (1983) stated that managers tend to voluntarily disclose only positive information about the firm, retaining unfavourable ones in order to prevent its disclosure from compromising firms’ assets value.

Similarly, Dye (1985) also assumed that managers would predominantly disclose positive voluntary information. Dye (1985) proposed that investors do not have enough knowledge to know the scope of private information that managers hold. Because of this, under normal conditions, investors will not understand the non-disclosure of voluntary information as a sign that managers are withholding bad news about the firm. Therefore, negative voluntary information would be disclosed by managers only when its resulting costs are low, or, in cases, in which the informational asymmetry between a manager and an investor is too high that could cause losses to the firm (Dye, 1985).

In this sense, based on voluntary disclosure theory, the rationale of the study is that a positive tone in voluntary disclosure information may work as a signal of good future prospects for the firm. This positive signal could lead market agents to evaluate the firm as less risky and, as a consequence, could decrease stock return volatility. Founded on these arguments, we present the following hypothesis:

Methodology

Sample Frame

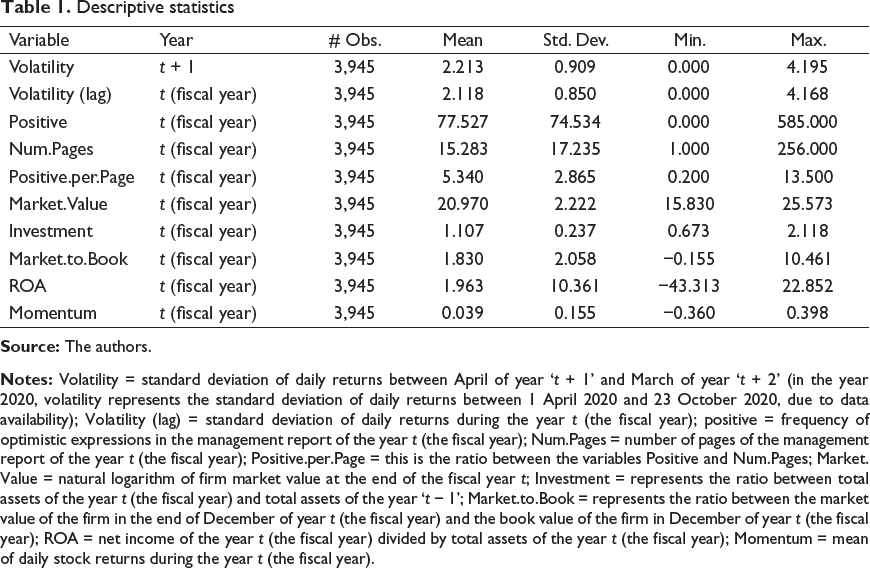

The sample of this study consisted of management reports and financial data of 576 stocks of Brazilian-listed firms. The period of study covers the years from 2010 to 2020 using the following reasoning: (a) for volatility calculation, the study considers daily stock returns of the period from 1 April 2011 to 23 October 2020. In each period, from ‘April of year t + 1’ to ‘March of year t + 2’, we calculated the standard deviation of daily stock returns, which represents an annual measure for stock return volatility; and (b) data related to the positive tone in management reports, financial data and control variables are based on the fiscal years 2010–2019. Therefore, our measure for volatility is annual (the standard deviation of daily stock returns between the period from ‘April of year t + 1’ to March of year t + 2’) and the measures for financial data, control variables and positive tone, which are also annual, since they are based on annual reports (in year t). Using this reasoning, the database consists of 3,945 stock-year observations.

Data Source

The reports were collected from the Brazilian Securities and Exchange Commission’s (CVM) electronic site. It was observed that 11 companies disclosed their management reports using scanned documents (22 firm-years observations). In those cases, it was not possible to access their positive report tone, so these observations were considered as missing values and were excluded from the final sample (these observations represent less than 1% of the final sample). The financial data was obtained from the Economatica database (Economatica, 2020).

Empirical Model

The dependent variable was stock return volatility, which was proxied by the standard deviation of daily returns between April of fiscal year ‘t + 1’ and March of fiscal year ‘t + 2’. Therefore, the quantitative model considers the information of management reports of year t and the stock return volatility (based on standard deviation of daily stock returns) from April of the year ‘t + 1’ to March of the year ‘t + 2’, in order to capture the variation of volatility after the management report disclosure.

After estimating stock return volatility and collecting the other variables, we observed some cases higher than three times the interquartile range plus the median (and lower than three times the interquartile range minus the median). To address this concern, we applied the winsorize procedure (we use a level of 2%, in other words, 1% in each tail) in all scalar variables.

The main independent variable was the positive tone of management reports. We measured this variable considering the frequency of optimistic expressions in each management report included in the sample divided by the document’s number of pages. The disparity in the frequency of positive words and reports’ length justified the weighting based on the number of pages. The list of positive words is available in Appendix A. The study of Yekini et al. (2016) was used as a reference for the positive words and expressions list. Also, unlike previous studies (Burgwal & Vieira, 2014; Clarkson et al., 2013; Plumlee et al., 2015), here a disclosure index was not employed, but instead a metric for positive expressions based on automated textual analysis was employed.

The quantitative model used to test the relationship between positive tone and stock return volatility considers the variables’ positive tone, volatility and other six controls: (a) lagged volatility: measured by standard deviation of daily returns in the previous period (Bui & Nguyen, 2019); (b) market value: measured by natural logarithm of firm market value (Zaremba et al., 2020); (c) investment: rate of change in total assets over the last two fiscal years (Fama & French, 2015); (d) market-to-book ratio: measured by firm market value divided by firm book value (Ahmed et al., 2020). It is important to note that companies with a negative book value were also excluded from the sample in the respective year; (e) return on assets (ROA): measured by net income divided by total assets (Azrak et al., 2020); and (f) momentum: mean stock returns of the previous year (Ahmed & Alhadab, 2020). Equation (1) indicates the model used for hypothesis testing.

where Volatilityit+1 = standard deviation of daily stock returns of stock i considering the period between April of fiscal year ‘t + 1’ and March of fiscal year ‘t + 2’; Positive.per. Page it = indicates the frequency of optimistic expressions in the management report of stock i in the period t, divided by the document number of pages; Volatility it = indicates the standard deviation of daily returns of stock i in the period t; Market.Value it = indicates the natural logarithm of the firm related to the stock i in the period t; Investment it = indicates the rate of change in total assets from the two last fiscal years related to the stock i in the period t; Market.to.Book it = indicates the ratio between firm market value and firm book value in relation to the stock i in the period t; ROA it = indicates the net income of the year divided by the total assets of the firm related to the stock i in the period t; Momentum it = the average of daily stock returns of stock i in the period t.

In line with previous research (for example, the studies of Li et al., 2020; Nag & Bhattacharyya, 2016), we used regression analysis with panel data to test the study hypothesis (H1). In order to select the most appropriate model (fixed effects, random effects or pooled data), we evaluated the results of three tests: Hausman, Chow and Breusch and Pagan. The results of these three tests indicated the fixed effects panel data as the most appropriate model to estimate the coefficients of Equation 1. The variance inflation factor (VIF) was also considered in order to analyse if multicollinearity would be a concern.

Analysis and Discussion

Descriptive statistics

In this study, the unit of period used in the analysis is annual. Following this reasoning, our measure for volatility is annual (the standard deviation of daily stock returns between the period from ‘April of year “t + 1”’ to ‘March of year “t + 2”’) and the measures for financial data, control variables and positive tone are also annual, since they are based on annual reports (in year t).

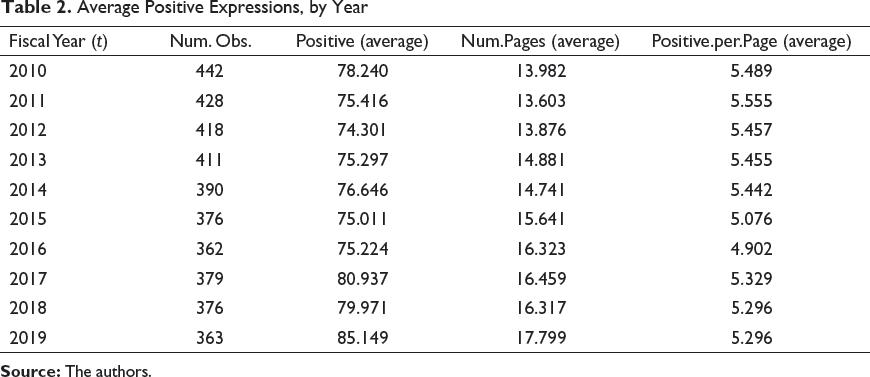

Average Positive Expressions, by Year

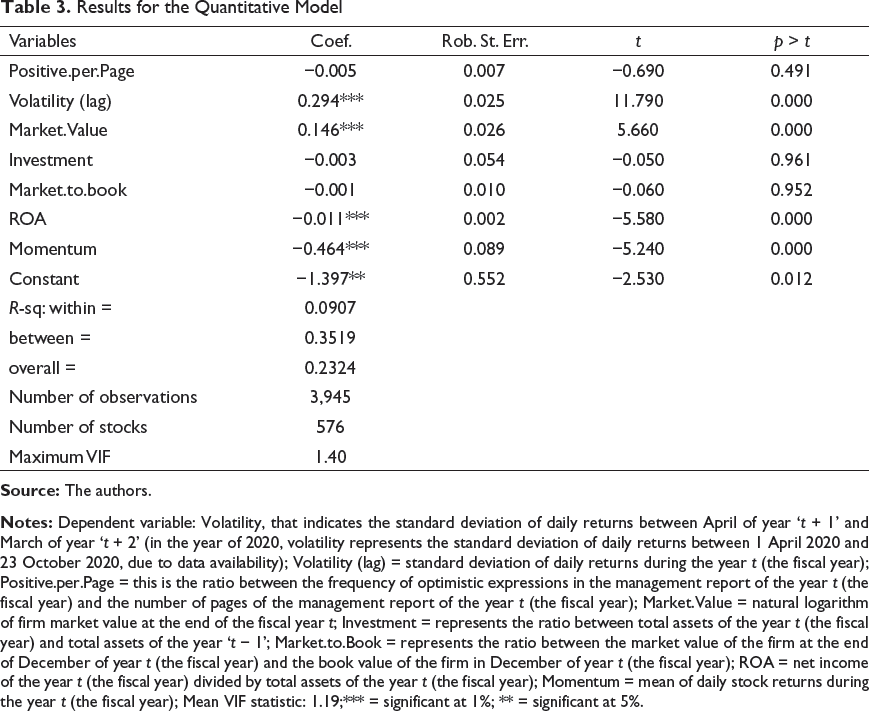

Table 3 presents results concerning the main objective of this article, which is to analyse the effects of positive tone in management reports on stock return volatility. The model has as a dependent variable, the standard deviation of stock daily returns (Volatility in t + 1) and, as the main independent variable, the frequency of positive expressions in management reports divided by the number of pages (Positive.per.Page). The model is controlled by lagged returns volatility, market value, investment change ratio, Market.to.Book ratio, return on assets and momentum. As explained in the methods section, the fixed effects model was used to estimate the coefficients, after evaluating the Hausman, Chow and Breusch and Pagan tests.

Results for the Quantitative Model

The findings show that, contrary to expectations, the effect of positive tone (variable Positive.per.Page) on stock return volatility of the subsequent year was not statistically significant. This suggests that, inconsistent with hypothesis H1, the positive tone adopted in management reports does not imply a reduction of stock return volatility. Therefore, the results are not in line with previous studies that have demonstrated the benefits of information disclosure in terms of return volatility mitigation. These previous studies include Egginton and McBryer (2018), Plumlee et al. (2015), Xu and Liu (2018) and Zhang et al. (2018).

In relation to this result, it should be mentioned that the analysis of this article focussed on the positive disclosure tone employed in management reports, and not just the disclosure of the document by itself. Therefore, although the possible improvement of the firm's informational environment from disclosure of management reports, the stock returns volatility can be reacting in relation to more objective variables that are also available in management reports (such as profitability). In other words, an optimistic disclosure tone may affect the price of stocks; however, it does not represent the main determinant of stock return volatility according to the analysis conducted in this article (its effect was not significant). Moreover, it seems that more objective variables at a firm level (such as information related to profitability and past performance of stocks) are related to stock volatility, while more subjective information (maybe reflected in the positive tone) is not enough to decrease stock return volatility.

In relation to the control variables, on one hand, the volatility of the previous year presented a positive effect on the volatility of the subsequent year; moreover, large firms, on average, tended to present large levels of volatility in the subsequent year when compared to small firms. On the other hand, profitability (based on ROA) and the performance of stock returns over the previous year presented a negative effect on stock return volatility in the subsequent year.

Conclusion

The main results of this research showed that the positive disclosure tone in management reports does not necessarily decrease stock return volatility, a result that was not in line with H1. It was also observed that there has been an increase in the mean positive tone employed in management reports over recent years, as well as the average length of those documents.

The results of this study advance the understanding of the potential effects arising from corporate reports disclosures and management reports, since it was used as a relatively simple measure of textual content analysis, which was based on optimistic expressions employed in management reports, and because it was documented that the frequency of positive tone is not necessarily related to volatility. Moreover, the relationship between positive disclosure tone and volatility was explored with data from an emerging economy (Brazil), in which the speed of adjustments in stock returns based on information disclosed in corporate reports is significantly slower when compared to more developed markets. It is expected that this research contributes to the literature, since it promotes progress from previous studies by addressing not only the effects of management report disclosure on volatility, but also by evaluating the published textual content tone, focussing on optimistic words and expressions.

Regardless of this, perhaps the main contribution of this article refers to the measurement of positive disclosure tone (based on the study of Yekini et al., 2016) considering the Brazilian management reports’ textual content. It is something unusual in previous studies, which may be due to the extension of this kind of report, which usually involves large amounts of textual data and a number of pages. Consequently, this study does not suffer from limitations from the use of a general disclosure index through scores attributed to different items or sentences, such as the subjectivity in elaboration of the general index and score imputation, as well as index failures to capture disclosure elements of the reports. Although, it should be mentioned that more complete reports could present few positive expressions or incomplete reports could present a more optimistic tone, which the metric employed in this study cannot capture.

Managerial Implications

The findings discussed in this study, that stock return volatility does not necessarily decrease when voluntary information with a positive tone is disclosed, have practical and managerial implications. The first implication is that shareholders and potential investors may consider the positive tone adopted by the firm in its corporate reports as a complementary factor (nor the main determinant) when deciding whether or not to apply their resources to firm shares, in order to reduce the risks involved in the investment. Another possible managerial implication is that firm managers can consider that the disclosure tone can present a different effect on stock return volatility in relation to other objective measures (such as profitability); therefore, the tone of subjective expressions is not the main determinant of the volatility of a firm’s stocks.

Limitations and Suggestions for Future Research

Some limitations of this research should be mentioned. Since positive disclosure tone was measured through the frequency of optimistic words and expressions in management reports, this metric may not adequately capture the effects of disclosure tone in some situations. For example, extensive reports tend to have a neutral disclosure tone predominantly, due to the large number of words, both positive and negative, while brief or incomplete reports can present a more optimistic tone.

Another limitation arises from investigating only positive disclosure tone, based on the optimistic words and expressions proposed by Yekini et al. (2016). Thus, it was not possible to examine possible impacts of neutral or negative information on stock return volatility. To do so, a broader instrument with additional terms and expressions, other than the optimistic tone, would be needed.

Given these limitations, it is suggested that future research expand the analysis of disclosure tone, including additional terms and expressions to measure neutral and negative tone, in addition to the positive disclosure here. Another recommendation would be to verify whether the results found in this study would also be equivalent for other types of corporate reports, besides management reports.

Positive Words/Expressions, Based on Yekini et al. (2016) and Henry (2008).

Number of Observations by Industry

Footnotes

Acknowledgements

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply. Prof. Rodrigo Fernandes Malaquias would like to thank the National Council for Scientific and Technological Development (CNPq) for the support to develop part of this research (CNPq 303660/2019-8, PQ).

Declaration of Conflicting Interests

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Prof. Rodrigo Fernandes Malaquias would like to thank the National Council for Scientific and Technological Development (CNPq) for the support to develop part of this research (CNPq 303660/2019-8, PQ).