Abstract

This study attempts to establish the relationship between market dynamics and service components for the quality of the service of e-banking over a period of 5 years. The study used the Kano et al. (1984) questionnaire to identify the 15 variables, determining the customer’s satisfaction for quality improvement in e-banking services, based on a survey conducted among bank customers. Kano model’s attributes of CS were quantified by calculating the CS and dissatisfaction index with the average satisfaction coefficient over the time frame. The study concludes that over time, the customer requirement has gone through a major shift from one category to the other. To maximize customer satisfaction, this study will help the banking sector to identify the essential and competitive customer requirements, and design products and services accordingly.

Keywords

Introduction

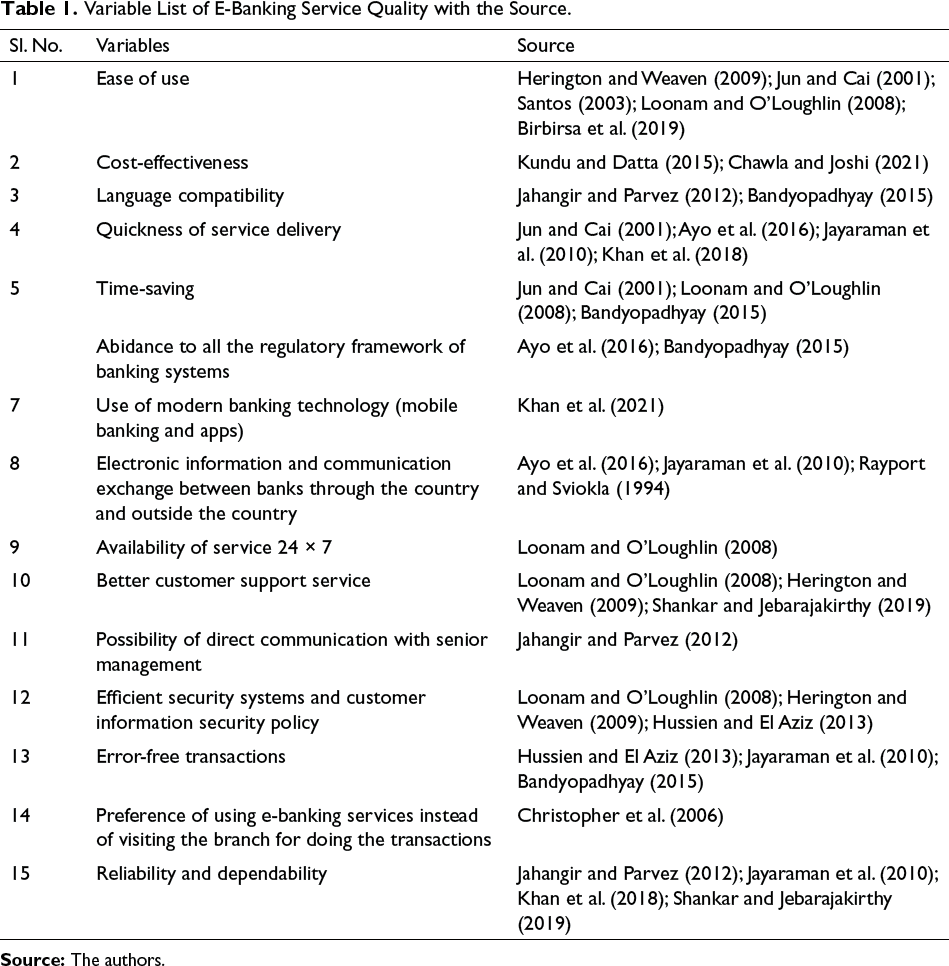

Modern economists, Alfred Marshal, J. R. Hicks and R. G. Allen, attributed the theory of consumer behaviour built on both the cardinal and ordinal approaches. Using the ordinal approach of understanding, customer requirements—CRs (Gupta & Shri, 2018) have become a top priority for businesses competing on a worldwide scale. To continue growth and survival in the market, businesses can no longer rely solely on high-volume and low-cost production. Instead, to stay competitive in the market, businesses focus on meeting customer wants or requirements to ensure customer satisfaction (CS). Fulfilment of the CRs does not always imply a higher degree of CS (Matzler & Hinterhuber, 1998). Hence, it is necessary to understand CRs in all the sectors of the economy, and these can be better recognized in the industry’s competitive landscape, which has significantly changed (Choudhury, 2013) over time. Private banks have entered the Indian banking sector, which was traditionally dominated by public sector banks. The new era of digital banking has shifted the bargaining power in the banking sector from sellers to buyers. This has prompted bankers to differentiate themselves from the competition by improving the service quality of their offers to meet the changing CRs of the customers (Chauhan & Choudhary, 2016). In this era of the ‘digital economy’, the demand for the service offering of e-banking has changed over the years. The service offering differentiation and cost optimization are highly required for the sustainability of the banking industry. These can be achieved through digital platforms like mobile banking (M-banking) (Chawla & Joshi, 2021). Global non-cash transactions volume has reached 334 billion transactions (Cap Gemini, 2014), which has been a clear indication that a major number of customers were inclined towards the digital channel of banking. Customers preferred e-banking as a major channel of service.

To outlive in the growing and dynamic world, banks must create as well as retain customers by providing high-quality services. Banks must constantly identify the needs of the customers and make proper strategies to meet those needs by offering appropriate services to the customers. The Indian banking has been previewing the growth of the Internet banking service delivery channels. Indian banks, both public and private, have adopted the electronic delivery channel (Chauhan & Choudhary, 2016). Therefore, service delivery has become an important challenge for banks. To manage this challenge, the manager needs to determine the service quality areas that require more attention. At the same time, it is possible that some of the service quality factors are not necessary for customers, but if they are not of a specific standard, customers will be disappointed (Bandyopadhyay, 2015). This distinction results in the prioritization of the improvement of service quality determinants to achieve CS. The linear relationship between the service quality determinants and CS has been measured in literature (Cristobal et al., 2007; Parasuraman et al., 1988) and focused on the non-linear function (Danaher, 1997). This study opts Kano et al. (1984) methodology to explore the relationship to discover a definite relationship between service quality determinants and CS proposed in the previous literature (Nilsson-Witell & Fundin, 2005; Yang, 2003). To address the need, the authors of this study started by identifying the attributes of e-banking service quality improvement required for determining CS. The reason is, with time, the CR has seen a shift, so concerning the time, the service quality dimensions of e-banking have also seen a lot of changes (Choudhury, 2013), and finally presented the exact relationship among these variables. By doing this, this study captured the shift of service quality requirements of e-banking recently.

The study is organized in the following sections: the conceptual framework covers the literature review to identify the service quality variables and the Kano model application to measure CS. The methodology section of the study covers the empirical model, design and method. The results and discussion part presents the analysis and discussion of results. The final section of the study includes the concluding observations, implications and recommendations with the future scope of research.

Literature Review

Role of Customer Satisfaction

According to Koutsoyiannis (1979), ‘to analyse the demand for a good, one has to examine the customer behaviour, since the market demand is the aggregate of individual demand’. Individual demand depends on consumer satisfaction after consuming the commodity. Satisfaction or utility can be measured for a few commodities in terms of money spent on it. This approach is known as the cardinal approach. However, most of the time, satisfaction is unmeasurable. At that point, consumers rank the commodity, as they do not have full knowledge about the utility of various commodities to make their choice.

CS has attracted many researchers in the recent past. Ngo (2015) in his paper presented the literature review on how to measure the level of CS with respect to different approaches and methodologies. The main objective was to provide a conceptual basis to understand existing methodologies used for measuring CS. The paper reviewed 103 articles and papers presented in international conferences. This emphasizes the importance of CS to understand the CRs.

Importance of E-banking

The implementation of technology in the banking sector, that is, the concept of e-banking, resulted in a major revolution in marketing strategies and practices, which has resulted in exorbitant operations of the banking industry. Multiple authors like Finn and Lamb (1991), Bouman and van der Wiele (1992), Ekinci and Riley (1999), Gagliano and Hathcote (1994), and Brodie (2007) studied the importance of e-banking in their studies. The efficient delivery of services can be provided to customers only if the bank maintains a better framework of functioning. The Internet-based banking system provides maximum comfort and convenience to customers while performing bank transactions.

Christopher et al. (2006) also reflected in their study that e-banking is an important channel that provides products and services to customers to stay profitable and successful. The new digital platforms for banking like M-banking resulted in better service variation and helped the banks to optimize the cost (Chawla & Joshi, 2021).

Service Quality Factors of E-banking

Jun and Cai (2001) categorized three important parameters of service quality for Internet banking—service product quality, customer service quality and online systems quality. The product variety was considered as a prime dimension of service product quality in the e-banking domain. The service quality attributes considered in traditional banking were no more useful, and e-service quality dimensions such as flexibility, information quality service recovery, trust and ease in access were found to be more important e-banking service qualities (Loonam & O’Loughlin, 2008). Further, factors such as site organization, personal needs, efficiency and user-friendliness were also important for understanding the service quality of the banks (Herington & Weaven, 2009). It was also stated by the researcher that factor efficiency did not contribute to customer satisfaction for bank performance. The results indicated that the overall satisfaction was found below the overall e-service quality. In the emerging economies such as the Bangladesh banking industry, factors such as communication, compatibility and convenience attracted the bank customers to use Internet banking (Jahangir & Parvez, 2012). The ease of use and trust of the users on Internet banking were needed to attract the customers, and perceived risk had a negative impact. (Birbirsa et al., 2019; Jahangir & Parvez, 2012).

The e-banking quality dimension such as empathy, incentives, privacy, assurance, usability, responsiveness, fulfilment and efficiency had a positive impact on customer satisfaction (Amangala & Wali, 2020; Hussien & Aziz, 2013; Jayaraman et al., 2010). Trust plays an important role and helps in understanding customer satisfaction with the perceived value (Kundu & Datta, 2015). Customer loyalty and satisfaction for e-banking were affected by the factors like privacy and security with reliability, whereas trust had a variation in effect between the customers (Nambiar et al., 2018; Shankar & Jebarajakirthy, 2019). Khan et al. (2021) found that the impact of trustworthiness on the usage of M- banking reduced the cost and led to cost optimization but also resulted in service variation for the bank apps in the capital city of Bangladesh. It was also observed that M-banking also had offerings (Chawla & Joshi, 2021). Ayo et al. (2016) highlighted the dimensions that had a significant impact on e-service of the important factors determining consumer satisfaction of the digital banking domain like M-banking (Khan et al., 2018). Therefore, from the aforementioned literature, researchers identified reliability, responsiveness, access and accuracy as the main sources of satisfaction of banking service product quality. The 10 variables that were identified for customer service quality include responsiveness, reliability, access, credibility, competence, communication and courtesy, understanding the customer, continuous improvement and collaboration. The variables such as accuracy, content, ease of use, aesthetics, timelines and security were part of the online system’s quality dimension. They also stated that there was no difference between e-services offered by conventional banks and modern banks dealing with Internet banking services concerning the frequency of the 17 indicators used to access service quality. Responsiveness, tangibles and assurance were the service quality dimensions that had a positive effect on CS, whereas reliability had a negative effect on CS.

Use of Kano Model for Measuring Customer Satisfaction

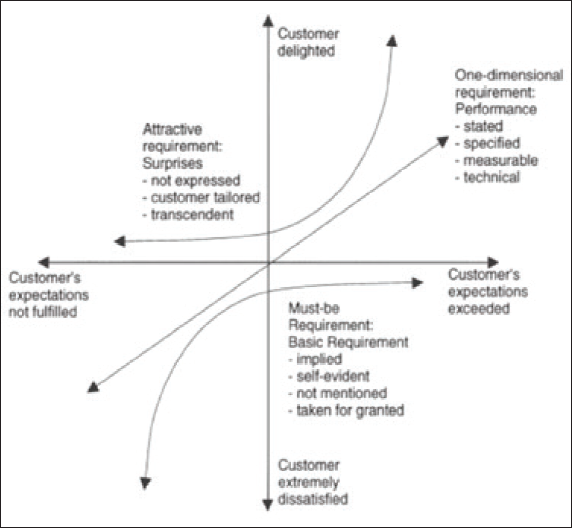

A famous tool that connects e-service quality dimensions with CS is the Kano model. Professor Nooriaki Kano of Rika University, Tokyo, one of the most outstanding scholars of quality management, proposed a model of CS, which is known as the Kano model. In this model, he classified three types of customer needs that result in CS or dissatisfaction. In the two-dimensional diagrams, the horizontal axis represents the degree of quality expected by the customer, the right-hand side indicates that the product has the expected quality, and the left-hand side shows that the product does not have the expected quality. The vertical axis indicates the degree of satisfaction and dissatisfaction. The lowest part of the axis represents customer dissatisfaction, and the highest part represents satisfaction (Figure 1).

For a product or service to excel in the market, it should have comparable attributes that are essential for the product to exist and grow. There may be certain attributes that may not be economical even when they exist or are intensified. To deal with such a type of situation, the Kano model can be used. The Kano model has three basic types of attributes—Must-be (M), performance and attractiveness. However, these needs were extended into five types, which were M, one-dimensional (O), attractive (A), indifferent (I) and reverse (R) defined as follows:

Wang and Ji (2010) successfully implemented the Kano model to examine the effect of CRs determining the level of CS. The study developed a satisfaction–CR function by applying the Kano model and then explained the different types of CRs determining the level of CS.

Parasuraman et al. (1988) indicated that by using the Kano model, most of the service industries have identified the service quality parameters. The five parameters used for this purpose was empathy, responsiveness, tangibility, assurance and reliability. Many researchers have used these five parameters and found that it was more contextual. It is advisable to examine the service quality parameters across various service industries.

Strandberg et al. (2012) examined the service quality perceived by the mass affluent customers of Swedish banks with the Kano model application. They identified functional, technical and services quality dimensions and concluded that it was difficult to satisfy the mass affluent customers, and there exists a difference in the perception of the customers. With the increase in the performance and customer expectation, the change in attributes results in enhanced CS, which can be measured by using the Kano model (Zhao & Dholakia, 2009). Bandyopadhyay (2015) used the Kano model to understand the service quality elements of the banking industry in India for CS. He used 15 service quality parameters out of which the operating hours and convenience attribute got the highest rank for satisfaction index (SI) score.

Objectives of the Study

In light of the aforementioned literature review, the objectives of this study were described in two parts: first, to identify the market force dynamics and e-banking service requirements of the future and, second, to establish the association between service features and service quality relevance over a period.

Methodology

The objectives of this study were to establish the association between market dynamics and service components for e-banking services quality. It explores the variables determining the customer’s satisfaction for quality improvement in e-banking services.

Variable List of E-Banking Service Quality with the Source.

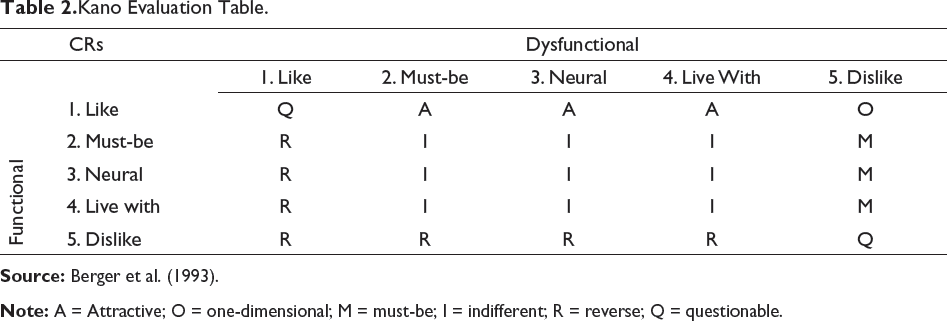

Kano Evaluation Table.

Coefficient of Customer Satisfaction

By using the evaluation table, the categories of each attribute were identified. Then, the CS coefficient was calculated by determining the value of each attribute (positive or negative). Berger et al. (1993) stated the SI as a ratio of the sum of the attributes A and O to the sum of the attributes A, O, M and I.

The dissatisfaction index (DI) was calculated by taking the ratio of the sum of the attributes O and M to the sum of the attributes A, O, M and I, and then the value calculated is represented as a negative figure.

The value of 1 for SI reflects more opportunities for fulfilling the CR. The DI value of −1 will reflect more threat of non-fulfilment of the CR.

The average satisfaction coefficient (ASC) was introduced by Park et al. (2012). It tried to calculate the average sum of the absolute value of the CS coefficient, that is, the SI value and the DI value.

Results and Discussion

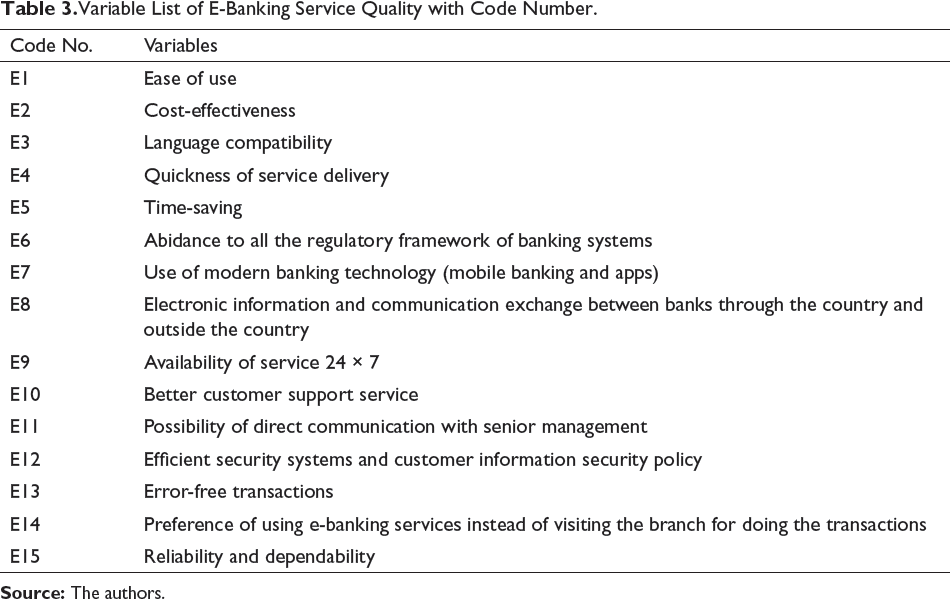

Variable List of E-Banking Service Quality with Code Number.

Demographic Profile

A total of 258 respondents were surveyed, out of which 58% were males and 42% were females. Looking at the age distribution, 56% were in the age group of 31–40 years, and 38% were in the 41–50 years age group. Regarding occupation, most of the respondents were salaried (45%) followed by business persons (32%). The educational level of the respondents has also been considered wherein most of the respondents were graduates (43%), followed by professional qualification (35%).

To administer the change in the service features and service quality requirement of the customer over the time frame, the analysis has been carried out in two parts: before 5 years represented as T1and the present period represented as T2.

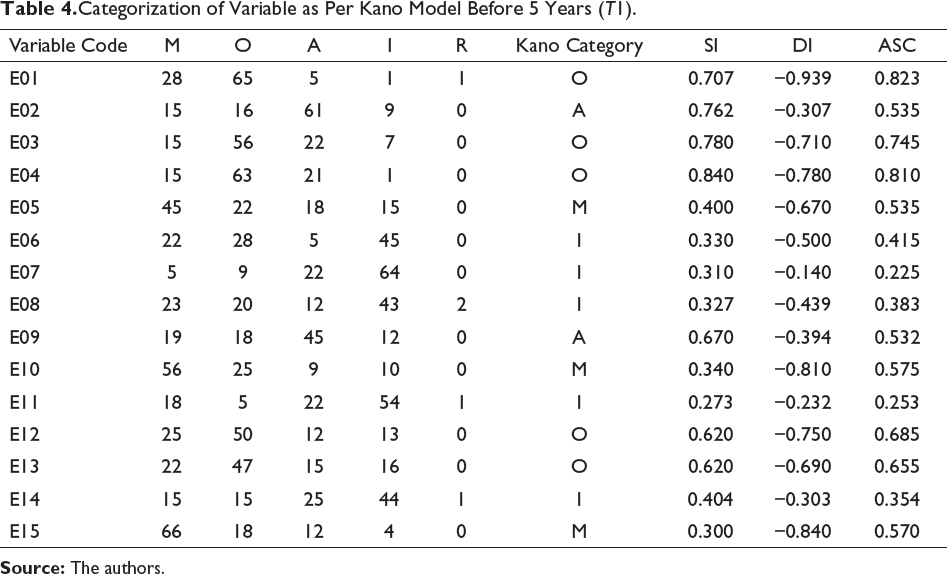

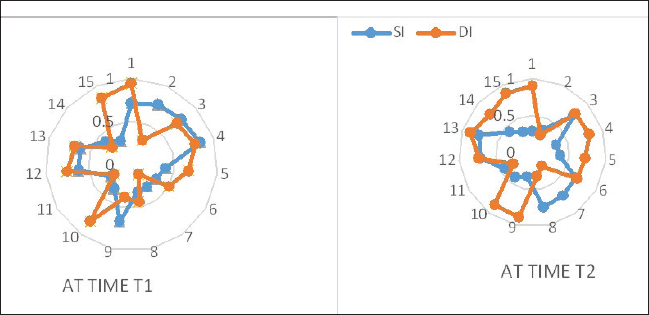

It was also found that all the O needs had the highest ASC score followed by M needs and A needs. The I needs had the least ASC score.

Categorization of Variable as Per Kano Model Before 5 Years (T1).

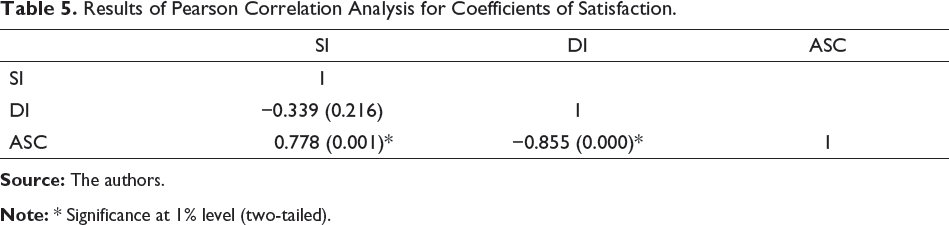

Table 5 presents the result of the Pearson correlation test to check the association of SI, DI and ASC. The SI score indicates the strong association between the fulfilment of the service quality variables of CR for CS. The DI score indicates the strong relationship between the non-fulfilment of the service quality variables of CR for customer dissatisfaction.

Results of Pearson Correlation Analysis for Coefficients of Satisfaction.

The results of the Pearson correlation analysis indicate a strong relationship between the ASC with SI and DI scores at time T1.

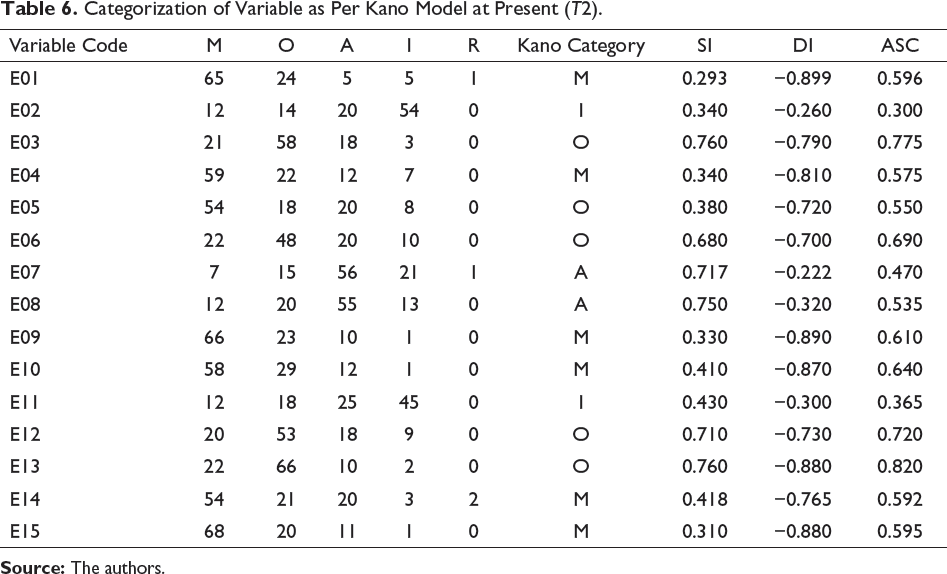

The SI and DI with the ASC were also calculated for each CR of the e-service quality dimension. It was found that most of the O needs had the highest ASC score followed by M needs and A needs. The I needs had the least ASC score.

Categorization of Variable as Per Kano Model at Present (T2).

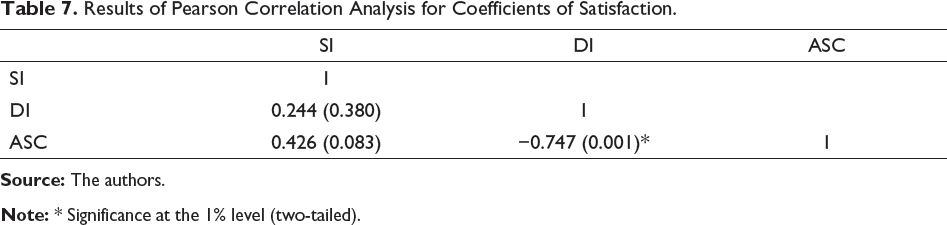

The association of SI, DI and ASC at time T2 are presented in Table 7. Again, the SI score indicates the strong association between the fulfilment of the service quality variables of CR for CS, and the DI score indicates the strong relationship between the non-fulfilment of the service quality variables of CR for customer dissatisfaction. The results of the Pearson correlation analysis indicate that there is no relationship between the ASC with SI at time T2, whereas, for the DI, there exists a strong relationship with ASC.

Results of Pearson Correlation Analysis for Coefficients of Satisfaction.

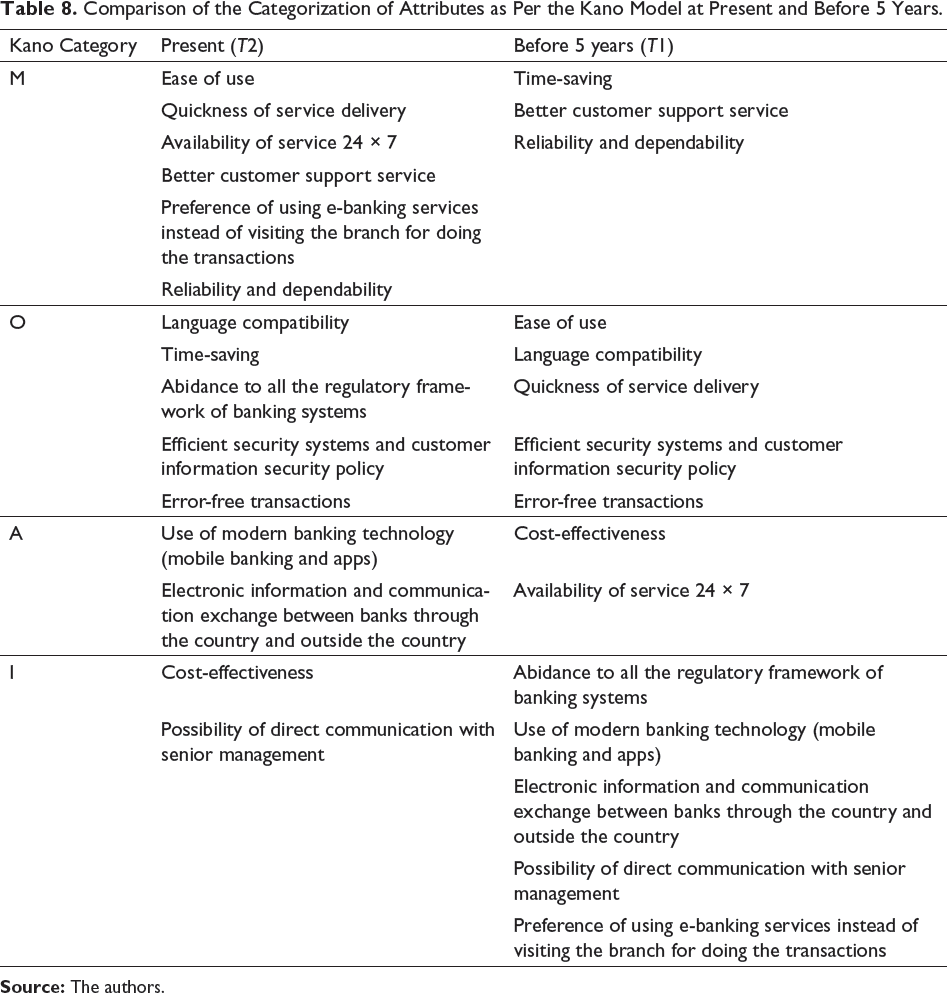

Comparison of the Categorization of Attributes as Per the Kano Model at Present and Before 5 Years.

Figure 2 represents the comparison between Kano attributes category with relevance to a certain period and how it has changed over the period. Time-saving which was an M need for 5 years has now become an O need that has a direct relationship with the degree of satisfaction of the customer. The Ease of use and the quickness of service delivery, which were O needs before 5 years have become an M need for the current period, which reflects that if these e-banking services are not present, then it will lead to dissatisfaction of the customer. The Availability of service 24 × 7 has also become an M need now, which was an A need for 5 years for customers. The e-banking service requirement, which was an I need for the customers before 5 years has now shifted to M, O and A need. The preference of using e-banking services instead of visiting the branch for doing the transactions has now become an M need, whereas the abidance to all the regulatory framework of banking systems has become an O need. Use of modern banking technology (M-banking and apps) and electronic information and communication exchange between banks through the country and outside the country have now shifted to be A needs for the customers whose presence nowadays results in greater than proportional satisfaction.

t-Test Result.

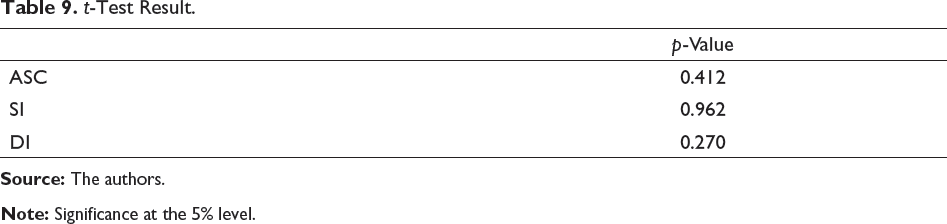

From Table 9, the p-value for ASC, SI and DI was greater than 0.05; therefore, the null hypothesis was accepted, and it can be inferred that the Kano category variable for the CR of e-banking service quality to determine CS is likely to shift over the period. Zhao and Dholakia (2009) also supported the findings with the increase in the performance and customer expectation; the change in attributes results in enhanced CS.

Conclusion

With time, the CRs shift, and the needs that are not found important or are less important become the essential requirement of the customer for availing the service. According to Roy (2010), CRs shift because of inflation and economic flux. Recession quite often results in unemployment, affecting the demand for discretionary items. Tightening of the monetary policy may lead to cost escalation for expansion activities of plants, which makes the final product costlier, sometimes fund for diversification may be altogether unavailable. Reduction of after-tax income may lower down the purchasing power of the consumer; attractiveness of investment may also be waned. The steady growth rate of per capita income may increase affluence, which in turn places a high premium on time; time-saving equipment’s improved customer service may face higher demand in their respective market. Similarly, devaluation and appreciation of money may affect the firm- and industry-level operations.

Implication and Recommendations

In this study, the Kano model has been used in the e-banking domain to identify the essential and competitive customer needs, which have mainly shifted from over five years’ time frame as well as have a huge impact on the CS levels. These were also dependent on the changing market dynamics. The study was conducted in two parts: first, the Kano model was applied to understand the CRs before 5 years, and second, it evaluated the CR for the current period and calculated SI and DI score. Before 5 years, the SI score indicates the strong association between the fulfilment of the service quality variables of CR for CS. The DI score indicates the strong relationship between the non-fulfilment of the service quality variables of CR for customer dissatisfaction. At present, the CRs have changed, and the SI score for current period evaluation also indicated a strong association between the fulfilment of the service quality variables of CR for CS, and the DI score indicates the strong relationship between the non-fulfilment of the service quality variables of CR for customer dissatisfaction. It was also found that the Kano category variables for CRs are likely to shift over the period.

The customers are looking forward to minimum requirements, for example, the M need for the present period in the e-banking service was ease of use. The customers also wanted quickness of service delivery that too available 24 × 7. Jahangir and Parvez (2012) also highlighted that the ease of use and belief of the users on Internet banking were required to attract the Bangladeshi bank customers. Bandyopadhyay (2015) also found the same result; O needs were language compatibility, time-saving, abidance to all the regulatory framework of banking systems, efficient security systems, customer information security policy and error-free transactions followed by the A needs being the use of modern banking technology (M-banking and apps) and electronic information and communication exchange between banks through the country and outside the country. The I needs were cost-effectiveness and the possibility of direct communication with senior management. Out of the 15 service quality parameters, the operating hours and convenience attribute got the highest rank concerning SI score. To increase the CS index, the banks should focus on M and O CRs for e-banking service quality. This will certainly help the banks to improve their service quality with a competitive edge over others. The study concluded the revised model of service quality dimensions for the banking industry to understand the CR in a better way. The banking industry and the regulatory bodies should focus on these minimum requirements of e-banking, which has become the need of the hour. The study contributes to redefining the CR with change in time and to be incorporated in the service offering to sustain and achieve excellence.

Scope for Future Research

The study has a few limitations, which provide the avenue for future research. The study was conducted in the eastern part of the country, so future research can be conducted with pan-Indian customer segments using the e-banking services for a better understanding of CRs. Moreover, revisiting the CRs over the period and reclassifying them for diverse types of industries can help to understand and analyse the CR of that industry, and further integration of the Kano model with the service quality dimensions will help improve the service offerings and sustain in the competitive world.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their helpful comments and suggestions in improving the article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.