Abstract

Only 31 firms out of Bombay Stock Exchange 100 index firms have adopted integrated reporting (IR); thus, these companies form the test case as the study examines the firm characteristics which motivate these 31 from the top 100 companies. The data are considered for five financial years ending 2020. Logistic regression is performed, and our result indicated that the company’s size, its structural complexity, and part of the Environmental social governance index affect the adoption of IR. We contribute to the growing body of literature by explaining the factors that influence the adoption of IR, which is now more important in light of the impending International Sustainability Standards Board of IFRS. Also, it will assist current and prospective stakeholders in determining how the firms’ characteristics can predetermine their chances of adopting newer reporting norms and practices.

Introduction

Corporate reporting in India and globally has evolved over the years to become more transparent, comprehensive and relevant in providing information to key stakeholders. The regulatory developments have increased the accountability of businesses towards societal issues. Therefore, corporates are expected to disclose non-financial information relating to their social commitments along with financial performance reporting. The separate disclosures of non-financial information and performance figures in the sustainability reports and traditional financial accounting reports respectively, have progressively increased (KPMG, 2015). Though, the disconnection between these disclosures has not satisfied the expectations of stakeholders who require a combined picture of the value created by the company (Cheng et al., 2014). In contrast, it has been observed that the risk of information overload increases with consolidated disclosure (de Villiers et al., 2014).

When compared to a sustainability report and an annual financial report, which are issued as two separate reports, a single integrated report (IR) encompasses financial as well as non-financial information and presents it as a complete document (Eccles et al., 2010). It was developed to satisfy the need of investors and stakeholder groups for better reporting that connected financial with non-financial performance. Eccles et al. (2010) observed that an IR communicates holistic view effectively to all stakeholders keeping their interests in mind. A summary by Jhunjhunwala (2014) of the International Integrated Reporting framework published by the International Integrated Reporting Council (IIRC) states that the framework allows a business to inform its stakeholders about its value creation process in a coordinated and comprehensive way, which promotes effective and efficient capital allocation. In a cross-country comparative study done on the importance of Environmental social governance (ESG) during COVID-19 period, it was observed by Singhania and Saini (2021) that for increasing the ESG practices in a country, governance measures such as sustainability reporting and IR practices need to be taken up strongly. Attention is therefore being given to IR by scholars (Vitolla et al., 2018) and professionals.

A detailed review of prior literature (Soriya & Rastogi, 2021) of the period 2011 to 2020 shows that 30% of the studies in the area of IR have been on the implementation of IR, 23% on the concept of IR, 19% on determinants of IR, 15% on Sustainability and IR and 14% on value relevance and IR. Studies that have examined the determinants of IR have attempted to find factors that improve the voluntary adoption or quality of IR. Such studies have focussed on certain features such as effect of a company’s cultural system (García-Sánchez et al., 2013) or country-specific attributes (Frias-Aceituno et al., 2013a; Jensen & Berg, 2012); characteristics of a firm such as the size of the company and its profitability (Frias-Aceituno et al., 2014; García-Sánchez et al., 2013), corporate governance (Fiori et al., 2016; Frias-Aceituno et al., 2014; Izzo & Fiori, 2016); as also a combination of such characteristics (Busco et al., 2019). The findings of these studies have thrown up contradictory views. Most of these studies have been conducted in countries in Africa and European Union. The United States, Italy and United Kingdom have also undertaken research in this field as these are in the early stages of implementing IR. According to Nag and Bhattacharya (2016), few Indian companies have adopted sustainability reporting. As India too is in the process of implementing IR, a need is felt to study how these firm-specific characteristics impact the adoption of IR by Indian companies. The results of the study would benefit the regulators (Securities and Exchange Board of India [SEBI], 2017) in planning the adoption of mandatory disclosure of IR in the country. At present IR in India is a voluntary disclosure. This study thus fills the gap by examining the firms’ characteristics that motivate the adoption of IR in an emerging market.

This study explains the literature review discussion, current knowledge and gaps followed by the theoretical framework and hypothesis testing in the second section. The subsequent section describes the research design and methodology, followed by the section that describes the empirical results. The findings and the conclusion of the article are described in the final section.

Literature Review

Benefits of IR over Traditional Reporting

The IIRC was established in 2010 as the primary global initiative advocating the use of IR. It brought together the regulators, companies, investors, accounting standard setters, accounting professionals and other related entities on one platform. In 2013, the IIRC released an international framework that considered a method of reporting which captures value creation. The need for such a framework was felt as the conventional sustainability reports were inadequate in integrating all relevant information (Velte & Stawinoga, 2017). According to Rowbottom and Locke (2013), the traditional reports allegedly failed to fulfil the requirements of the investors with the result that IR emerged. IR connected ESG information with financial aspects in a separate business document rather than reporting the two separately (GRI, 2015; IIRC & SASB, 2013). It thus offered a solution to corporates dissatisfied with conventional sustainability reporting.

Value Reporting Foundation in 2015 stated that an IR explains how business is impacted by society, which is in converse with a sustainability report that discusses how an organization’s actions impacted society and the environment. It considered IR to expand the company’s balance sheet to demonstrate its dependence upon financial and nonfinancial resources.

IR is considered to be a medium through which top management communicates with the stakeholders, mainly investors, about the sustainability issues faced by the company and the initiatives taken by it to contribute to the short as well as medium and long-term growth of the business (Churet & Eccles, 2014; IIRC, 2013). Prior literature documents that a company’s commitment towards IR generates several benefits for it, which include a better quality of management in terms of its effectiveness to create value over the long run (Churet & Eccles, 2014); reduction in information asymmetry, resulting in improved engagement with external stakeholders, leading to cost reduction, better allocation of resources and synchronized reporting (Burke & Clark, 2016); improvement in corporate reputation leading to attracting more institutional investors (Serafeim, 2015; Steyn, 2014). Brown and Dillard (2014) highlighted that IR describes how the value of the company is created over some time. A study conducted in South Africa (Bernardi & Stark, 2016) showed the IR efficacy in more accurate forecasts by analysts. Maniora (2015) observed that IR’s benefits depend on several factors, including the sample group being studied. Thus, the study contradicted the notion that IR is a superior reporting mechanism. Kumari and Vincent (2022) highlighted the ambiguity related to non-financial information included in the IR.

Firm-Specific Determinants of IR

According to an earlier research, firm traits can account for a company’s actions concerning adopting IR. Velte and Stawinoga (2017) explained that in line with legitimacy theory, economic and enterprise-specific factors (e.g., size, profitability and the industry), internal (board diversity) corporate governance factors and external (civil law in the country, the legal framework and investor protection rules stipulated by the regulators) corporate governance factors affect the decision of the organization to adopt IR. A comparative study of IR in 10 countries (Eccles et al., 2019) grouped the countries into three groups based on the quality of disclosure: High, medium and low quality. According to Girella et al. (2019), firm size, profitability, the market-to-book ratio and the board size were all significant factors in the voluntary adoption of IR. Board diversity and non-executive directors on the board impacted IR but were not found to be significant. The study also observed that country characteristics related to firms like the Corruption Perception Index, rating of the country, firms existing in collectivist and feminist countries and having long-term orientation are found to have a significant and positive impact on the adoption of IR.

The studies by Girella et al. (2019), Velte and Stawinoga (2017) and many more failed to capture the year-wise effect of these variables on IR. The present study attempts to examine the impact of these factors on IR reporting in India and also considers the time-year effect to study the trend of IR adoption in India.

Indian Perspective

Regulatory Environment

The regulatory developments in India brought by the Companies Act 2013, SEBI Listing requirements, Corporate Social Responsibility Legislation and Business Responsibility Reporting, focused on improving the quality of disclosures. A circular from SEBI in 2017 advised the top 500 listed businesses to consider using an IR framework for annual reporting. According to Grant Thornton Bharat’s report (2020) on IR, India has seen significant progress over the past few years in adopting IR as the top companies were already preparing a Business Responsibility Report as per SEBI’s instructions. To encourage and recognize companies for producing outstanding IRs, the Institute of Chartered Accountants of India (ICAI) included IR as an award category in its ICAI Awards for Excellence in Financial Reporting in 2019. It is noteworthy that IR which started with two to three companies almost 5 years back, has gradually gained importance and has become the preferred reporting framework for many of India’s big corporate firms. IR has been adopted by almost 50% of Nifty50 companies (AICL, 2020). A strong regulatory thrust on disclosures by the SEBI has made IR increasingly popular among mid and small-cap companies as well (AICL, 2020).

Research on IR

Scholars across the globe have given IR great importance. From the Indian perspective, very few studies have examined aspects related to the adoption of IR by Indian companies. An early study conducted by Athma and Rajyalaxmi (2013) opined that IR should be promoted amongst Indian companies by creating awareness about it to increase adoption. According to Ghosh (2019) and Ghosh and Bhattacharya (2020), around 60 of the 102 Indian companies studied had highly or moderately integrated their financial and non-financial data into their reporting. They further observed that companies must disclose more about their business model, strategy and manufacturing capital to show highly IR. The present study attempts to explain the financial and non-financial factors that influence the adoption of IR rather than the integration of these factors into IR. Another study in the Indian context was done by Mishra et al. (2022), who studied the perception of the preparers towards IR. It was observed that the preparers have a positive perception of IR, and the expected benefits from IR adoption, impact this perception. Our research examines a different perspective of IR. It investigates the voluntary adoption of IR in India by analysing firm-specific characteristics that may impact IR disclosures.

According to Soriya and Rastogi (2021), more research needs to be conducted on the disclosure practices, and perception of different stakeholders towards IR before the disclosure of the IR framework is made mandatory for Indian-listed companies by the SEBI. This study will therefore contribute to the extant literature focusing on India.

Theoretical Framework

Voluntary Disclosure Theory

Companies provide comprehensive information regarding the creation of financial and non-financial value for stakeholders in accordance with the voluntary disclosure theory (Dhaliwal et al., 2012). Information asymmetries between stakeholders and enterprises can be reduced by the voluntary disclosure of information by businesses (Verrecchia, 2001). According to Verrecchia (1983), minimizing information asymmetry guards against potential unfavourable selection issues. According to this study, information asymmetry is diminished by the voluntary sharing of financial and non-financial information through IR.

Signalling Theory

According to the signalling theory, a company’s disclosure of information directly signals stakeholders about its quality and thus reduces the risk associated with investor uncertainty arising due to information asymmetry (Hsiao & Kelly, 2018). Quality is a distinguishing characteristic in most signalling models, and it can be interpreted in many ways (Connelly et al., 2011). One of the ways in which quality is interpreted is that it reflects the signaller’s knack to fulfil and satisfy the requirements of the observers of the signal, that is, the outsiders. Voluntary disclosure to creditors and investors improves their understanding of the company’s financial and non-financial conditions. This lessens knowledge asymmetry and improves information transparency (Fiori et al., 2016). It is observed that companies disclose more information to send out a signal that they stand apart from other companies by focussing on the needs of investors and stakeholders (Campbell et al., 2001). Disclosure of information by a company acts as a signal to the market about the company’s efforts to reduce information asymmetry to increase its value (Frias-Aceituno et al., 2014). In this study, voluntary disclosure through IR is considered a signal to the stakeholders about the high quality of the company and the high involvement of stakeholders when compared to their competitors.

Legitimacy Theory

The legitimacy theory forms the basis of voluntary social and environmental disclosures by firms. According to Mousa and Hassan (2015), companies use social and environmental reporting to increase and maintain their legitimacy in the eyes of various stakeholders. The voluntary disclosures made by a company indicate its legitimacy to act and thereby create value. Hence, in IR disclosure, the financial and non-financial aspects gain significance for the financial capital providers (Lee & Yeo, 2016). As a lack of proper disclosures to the external parties indicates an unfavourable outcome, the signalling theory states that the benefit is in using voluntary disclosures to display suitable results (Hughes, 1986). According to Verrecchia (1983), negative consequences do not incentivize voluntary disclosures by the company. Nevertheless, legitimacy theory suggests that negative information disclosed under certain circumstances ensures legitimacy in action by making available detailed explanations (Lai et al., 2016; de Villiers & van Staden, 2011). Voluntary disclosures will increase when the anticipated benefits exceed anticipated costs (Adams, 2002). According to Husted (1998), the anticipated benefits arising on account of voluntary disclosures may be dependent upon the company’s anticipated need to ensure the legitimacy to act driven by the stakeholders’ expectations. Further, considerations of voluntary disclosure theory are connected to concerns of socio-economic aspects (García-Sánchez et al., 2013) as well.

Stakeholder Theory

Stakeholder theory provides a strong theoretical base for this study as it is most often used to examine the determinants of voluntary disclosure. The theory suggests that firms should be able to create value through their strategies for their capital providers and all external parties impacted by the firms’ decisions and corporate actions (Freeman, 2010). According to Connelly et al. (2011) and Hahn and Kühnen (2013), firms make voluntary disclosures to reduce information asymmetry in line with signalling theory. This reduction helps firms to manage their stakeholder relations better. To sustain and improve their stakeholder relations, companies adopt an IR to show a comprehensive picture of their financial and non-financial aspects of value creation (Steyn, 2014). Therefore, all three theories—legitimacy, signalling and stakeholder—are interconnected (Albers & Günther, 2010; Hahn & Kühnen, 2013).

Hypotheses Development

A systematic literature review on IR from 2011 to 2020 conducted by Soriya and Rastogi (2021), showed that studies have indicated Corporate Governance mechanisms, high economic development, board characteristics, assurance of sustainability report, size and establishment, low leverage and extent and quality of credibility enhancement mechanism as some of the determinants that are positively associated with IR reporting and its quality.

The review further states that studies have shown some factors that are negatively associated with IR practices including the cost of capital, earnings forecast error, profitability, growth opportunities, auditor type and length of reports.

The present study attempts to test some of the factors listed above and others that are listed in past literature, in the Indian context.

Size

The stakeholder theory and voluntary disclosure theory suggest that as the number of stakeholders that are interested in a company’s activities increase, there is a rise in both need and benefits arising from voluntary disclosures (Gray et al., 2001). Accordingly, there is a need for larger companies to ensure stable stakeholder relationships as public awareness is high for such companies (Dienes et al., 2016; Hahn & Kühnen, 2013). Thus, bigger-sized companies may benefit from the adopting IR (Ho & Taylor, 2007). Past studies (Frias-Aceituno et al., 2013b, 2014; García-Sánchez et al., 2013) reported a positive relation between company’s size and its preparation of IR. However, Fuhrmann (2019) contradicted the study and stated that there was no significant association between size of the company with the probability of disclosing an IR. Thus, large companies may not find any reason to integrate financial and non-financial information in a single report. Based on legitimacy theory, we envisage that larger companies faced with a high level of public awareness are therefore more inclined to make a voluntary disclosure of IR.

H1: The adoption of IR is positively and significantly impacted by a company’s size.

Performance

According to past research, an association exists between a company’s performance and voluntary disclosures’ expected costs and benefits (Fuhrmann, 2019). Following the signalling theory, a company can signal a superior ability to generate returns through the practice of voluntary disclosures. The increase in voluntary disclosures may enable a company to limit the risk of problems arising due to adverse selection (Verrecchia, 2001; Wagenhofer, 1990). In contrast, increased disclosures of high financial returns may lead to attracting new competitors in the industry which may impair the company’s wealth creation. Thus, high profitability may reduce voluntary disclosures (Wagenhofer, 1990). Fuhrmann (2019) also observed a negative impact of profitability on the disclosure of an IR. However, there are many studies that observe that it is more likely that profitable companies will disclose IRs (Frias-Aceituno et al., 2013a, 2014; Garcia-Sanchez et al., 2013). This is further supported by Reverte (2009); it was observed that profitable companies use their resources and disclose more while companies constrained by resources do not help with voluntary disclosures. In line with the major studies and based on legitimacy and signalling theory, we expect the presence of a significant association between performance and adoption of IR. H2: The adoption of IR is positively and significantly impacted by a Company’s performance.

Leverage

Prior literature has discussed that voluntary disclosures by companies satisfy financial capital providers’ information needs (Healy & Palepu, 2001). When there are many strategic shareholders, voluntary disclosures are required for creating value on a sustained basis according to Leuz and Verrecchia (2000). This was supported by a few studies which reported that companies with a high number of strategic shareholders see the importance of an information environment that allows for valuation processes (Cheng et al., 2014; Serafeim, 2015). A review of past literature shows that studies indicate a contrary relationship with debt providers. As per a study by Eng and Mak (2003), debt providers have the ability to ensure strict compliance due to the covenants in the agreements and hence do not give importance to the overall value creation ability. As per Lai et al. (2016), there is an insignificant relationship between leverage and adoption of IR. According to Barnea and Rubin (2010), in order to reduce information asymmetry between lenders and other stakeholders, firms would disclose more information in terms of number, quality and variety (financial and non-financial). Literature also demonstrates that businesses will voluntarily disclose an IR if the debt providers lack the private information or the capacity to rely on covenants (Ahmed & Courtis, 1999; Cormier et al., 2004; Eng & Mak, 2003).

On the basis of the main results of past studies, we expect highly leveraged firms to be more inclined to make a voluntary disclosure of IR.

H3: The adoption of IR is positively and significantly impacted by a company’s leverage.

Structural Complexity

An organization can be considered complex if there are horizontal, vertical and spatial differences across the company (Kusdi, 2009) or multiple independent parts (Cara et al., 2017). Past studies have stated that an organization’s complexity can be looked at from various parameters. Such as the number of industries that a firm operates in (Bushman et al., 2004; Cohen & Lou, 2012); the number of geographies in which a firm is located, and its number of units or departments (Kusdi, 2009); the size of the firm and proportion of its intangible assets (Lee & Yeo, 2016). According to Liu et al. (2015), the structural complexity of an organization may be assessed through the number of subsidiaries, among other characteristics. Some studies in the past have reported that IR is starting to be in demand by complex companies (Frias-Aceituno et al., 2013b, 2014; Garcia-Sanchez et al., 2013). According to Bushman and Smith (2001), firms having high growth opportunities benefit from a strong disclosure policy. Such firms reduce information asymmetry and agency costs by disclosing more. This helps in reducing their cost of external financing. It is expected that firms having more subsidiaries have high growth opportunities. Accordingly, this study expects that companies with more subsidiaries will have a positive inclination towards IR.

H4. The adoption of IR is positively and significantly impacted by its structural complexity.

ESG Index

The investigation of the connection between a company’s ESG performance and its voluntary disclosures has recently become a popular research issue. According to Lai et al. (2016), the higher a firm’s ESG disclosure rating score, the more the disclosure of IR supports voluntary disclosure theory (e.g., Dye, 1985; Verrecchia, 1983). Lai et al. (2016) further observed that when a firm gives importance to non-financial performance disclosure in its IR, its stakeholders signal that it creates value through its ESG actions. Considering the stakeholder and signalling theories, it may be studied whether a company having an ESG score and being a part of the ESG Index adopts IR or not.

H5: The adoption of IR is positively and significantly impacted by it being an ESG Index constituent.

Age

Sawitri’s (2016) research on Indonesian listed companies observed that companies listed for extended periods have more knowledge about investors’ needs for information. The study also reported that older companies have more experience disclosing information needed by stakeholders. Such companies were found to be better at corporate reporting. This argument was supported by a study conducted by Yulyan et al. (2021), wherein it was concluded that companies with longer operating life make a broader disclosure of information to satisfy stakeholders’ needs through IR. The observation that a company’s age positively affects IR is in sync with agency theory as the longer the company operates, the more information asymmetry there is (Jensen & Meckling, 1976). Based on these arguments, we anticipate that companies in operation for an extended period are positively inclined to make a voluntary disclosure of IR.

H6. The adoption of IR is positively and significantly impacted by a company’s age.

Methodology

Sample

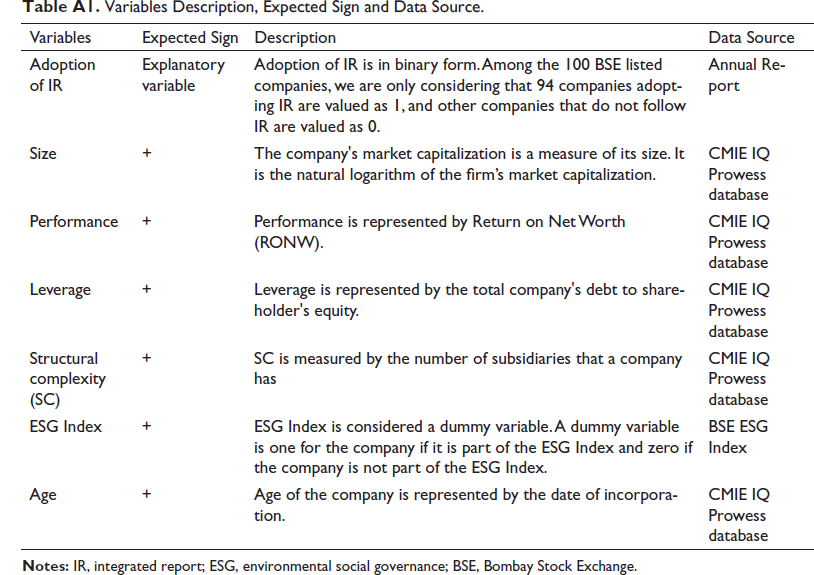

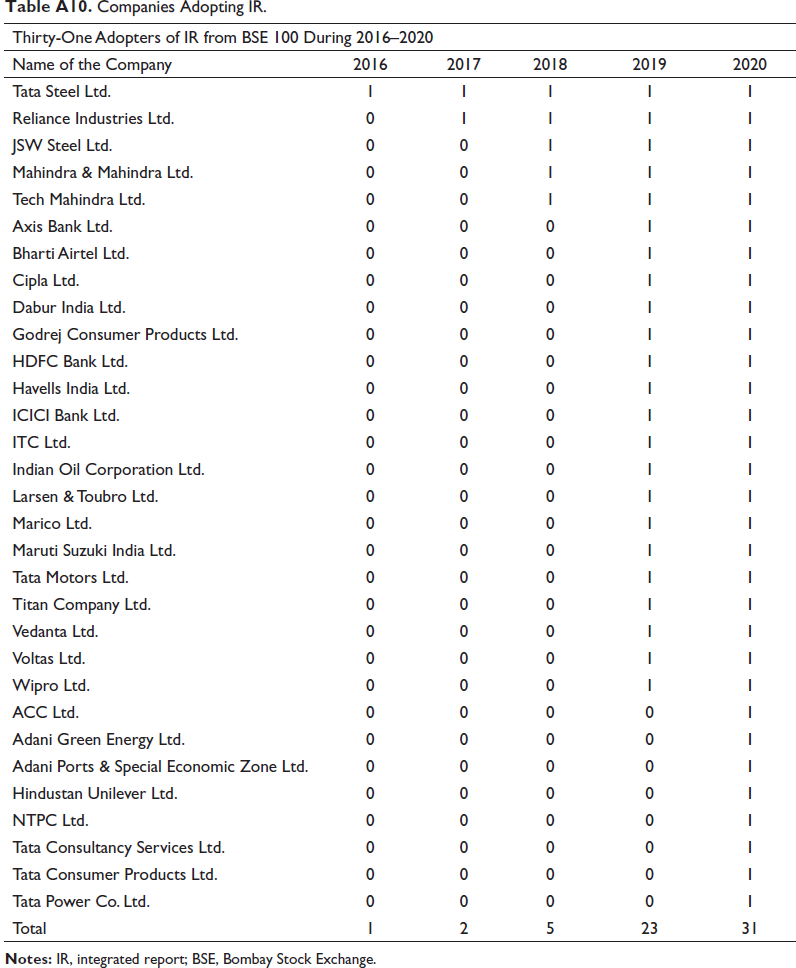

The sample is extracted from the Standard Poor Bombay Stock Exchange Sensitivity Index representing 100 largest and most liquid Indian companies, and these companies are within the Bombay Stock Exchange (BSE) Large Mid Cap. These companies approximately cover two-thirds of the market capitalization of the listed universe at BSE. We have considered BSE 100 companies because the largest companies adopt IR. The total number of companies reporting IR is 31, and approximately 33% of the companies report IR from the sample of companies. The sample consists of 94 companies based on the availability of the relevant data. The period considered for the study is the financial year (FY) 2016 to 2020 because IR started in 2013 only. During the starting years, IR adopted by the companies was significantly less, and IR was voluntary in 2017–2018 for the top BSE companies as per the market regulator SEBI. The information was collected from the Prowess IQ database for firm-level variables and manually collected the data of IR through the company’s websites. Few studies, such as those (Banik & Chatterjee, 2021; Saripalle et al., 2018), have used the CMIE IQ Prowess database, one of the accepted databases. A list of the adopters (see Table A10) and non-adopters of IR (See Table A11) is provided in the Appendix.

Variables

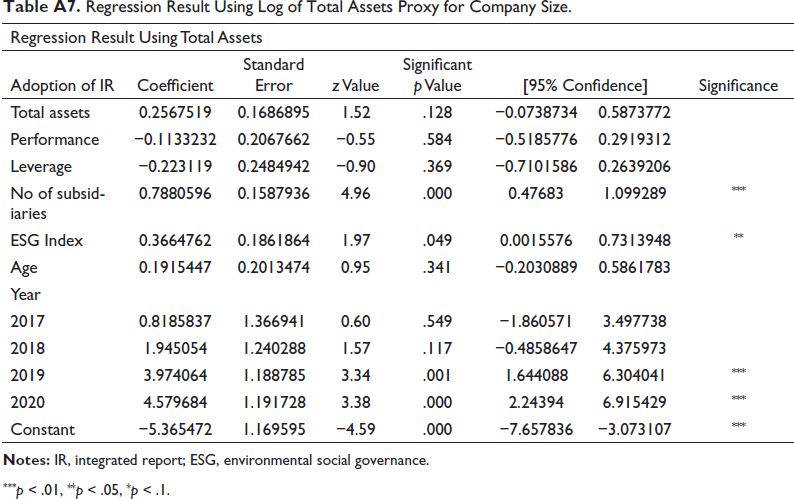

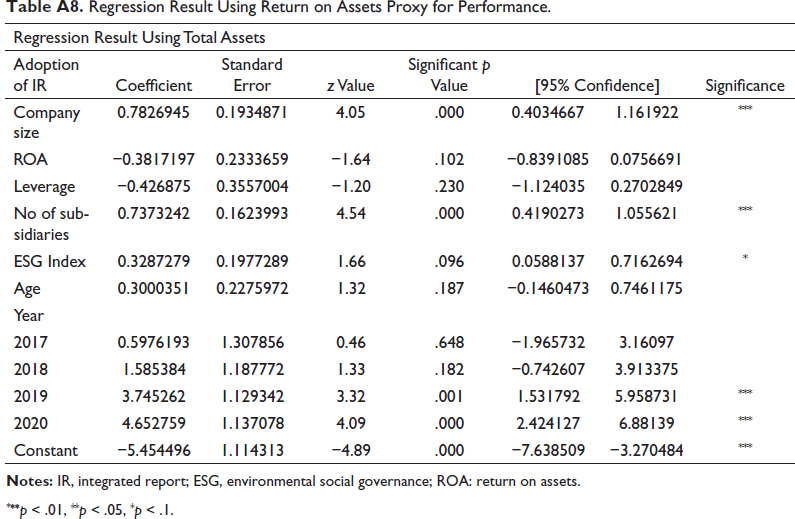

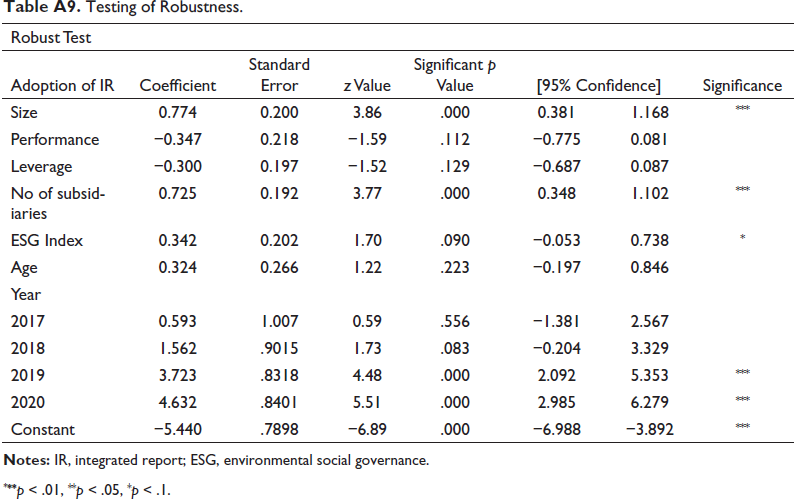

Many studies in the previous literature (Frias-Aceituno et al., 2014; Fuhrmann, 2019; Vitolla et al., 2020) have majorly considered the proxies (like a log of market capitalization and log total assets for the size of the company). Similarly, proxies for performance (such as return on assets, return on net worth and return on equity) are considered. Lastly, for the leverage variable studies have considered debt to equity as the best proxy for their results. Hence, the results are more significant with the proxies we have considered in our study, as shown in Table A1. We have also run the test of robustness (see Table A9). Regression results are also provided for the company’s size using the proxy log of total assets (refer to Table A7), where the output is not significantly and positively related to the main regression output in Table A4, whereas for performance variable using the return on asset proxy (refer to Table A8) is consistent with the main result in Table A4.

Empirical Model

The dependent variable in our study takes the value in the binary form of 1 or 0. We have used the binary logistic regression model to understand the association between the adoption of IR and the firm characteristics to know the statistical significance. Logistic regression model is appropriate when the dependent variable is dichotomous (binary) in any regression analysis. It explains the data and the relationship between one dependent binary variable and one or more ordinal, interval, nominal or ratio-level independent variables. Logistic regression is a predictive analysis. Ten events per variable is a minimal criterion for sample size considerations in logistic regression analysis (Vittinghoff & McCulloch, 2007). We have considered the time year effect in our study to understand the trend of the IR adoption which other studies (Frias-Aceituno et al., 2013a, 2013b, 2014; Girella et al., 2019) in the past have failed to capture the year wise effect.

Pooled Logistic regression with year fixed effect model is used for testing the research hypotheses for determinants.

YIR = β0 + β1 Size t + β2 Performance t + β3 Leverage t + β4 Structural Complexity t + β5 ESG Index t + β7 Age t + ε

Results and Discussions

Descriptive Statistics

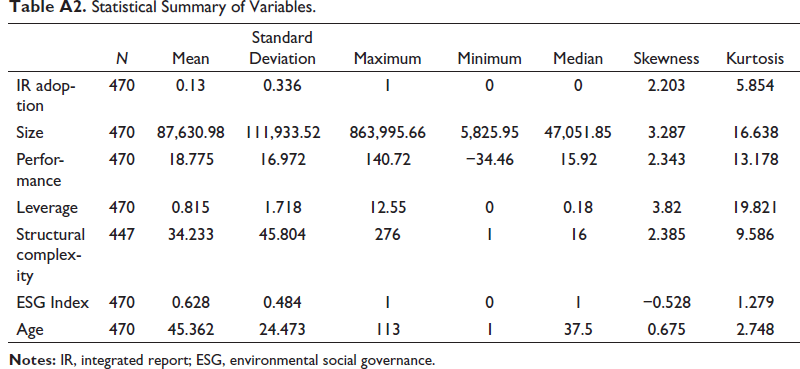

Table A2 presents the descriptive statistics for the firm-level characteristics. It can be observed that 13% of the companies listed on top of BSE 94 have adopted IR because IR is currently voluntary in India. The results are consistent with companies with higher rating AA as per the study (Girella et al., 2019). The company’s average size is 87,630.982 crores (87,6310 million). The average leverage is 0.81, with a standard deviation of 1.71, indicating that this study’s sample is highly leveraged. The average performance shows that the companies have 18.77%, indicating the prudent use of shareholders’ money. The average number of subsidiaries is 34.23 demonstrates that the company has a more complex structure and diversified operations and reduces liability protection and taxation. Sixty-three percentage of BSE 100 companies are part of the ESG Index. The average age of the company is 45.36 indicates that there are more chances of adopting IR as more companies are old. As there is the unavailability of data regarding the number of subsidiaries for a few companies, the number of observations is less than 470.

Multivariate Analysis

Multicollinearity

While using pooled logistic regression with year fixed effects model, it is necessary to test whether those independent variables are not highly correlated. Many estimation methods have been developed in the literature to deal with the presence of outliers (Birkes & Dodge, 1993; Huber, 1973). For this purpose, the variables were checked using the Variance Inflation Factor (VIF) test. Standardization is one of the robust techniques that aim to reduce the effect of outliers in the data. According to Jim Frost (2017), standardizing the variables refers to subtracting the mean and dividing by the standard deviation, known as standardization. We have applied the standardization technique using the VIF (Ando, 2018; Kullab et al., 2022; Saleh et al., 2005). If the value exceeds 10 in VIF and the tolerance value is lower than 0.10, there is a multi-collinearity problem (Hair et al., 2010). It is evident from Table A4 that the tolerance and VIF meet the acceptable criteria of lower than 0.10 for tolerance and less than 10 in VIF. As a result, multi-collinearity is not a concern for the regression model. The Standardization technique is used for all the variables such as size, performance, leverage, structural complexity, ESG Index and age, which removes extreme outliers from the data.

Correlation Results

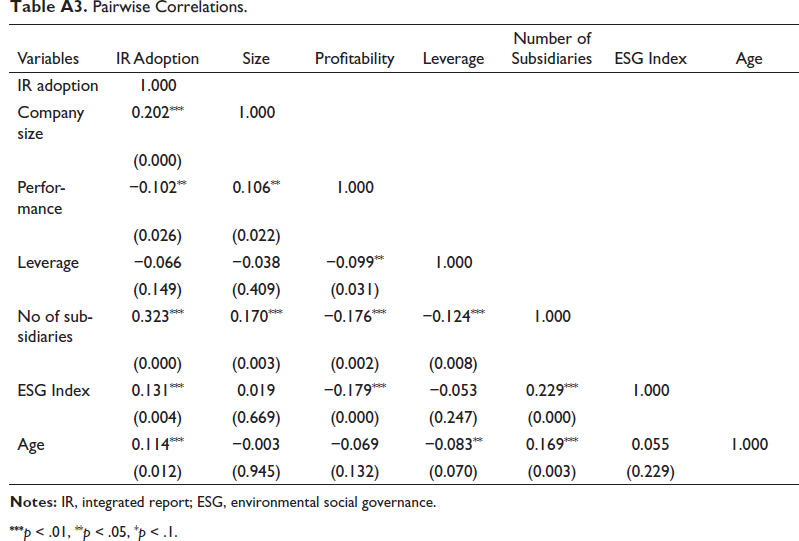

Table A3 presents the pairwise correlation analysis between IR and company determinants. It is clearly evident that adoption of IR and company size is positive but significantly correlated (r = 0.202; p < .01). Such result shows that there is increase in the company size when company adopts IR. Similarly, adoption of IR also has positive but significantly correlated with number of subsidiaries (r = 0.323; p < .01), ESG Index (r = 0.131; p < .01), age (r = 0.114; p < .01). There is increase in number of subsidiaries, ESG Index and age when company adopts IR. In contrast, adoption of IR and profitability is negative and significantly correlated (r = −0.102; p < .01). Company size is positively and significantly correlated with profitability (r = 0.106; p < .05) and number of subsidiaries (r = 0.170; p < .01). Profitability is negative and significantly correlated with Leverage (r = −0.099; p < .05), number of subsidiaries (r = −0.176; p < .01) and ESG Index (r = −0.179; p < .01). Leverage is negative and significantly correlated with number of subsidiaries (r = −0.124; p < .01) and age (r = −0.0835; p < .1). Number of subsidiaries is positive and significantly correlated with ESG Index (r = 0.229; p < .01) and age (r = 0.169; p < .01).

Regression Results

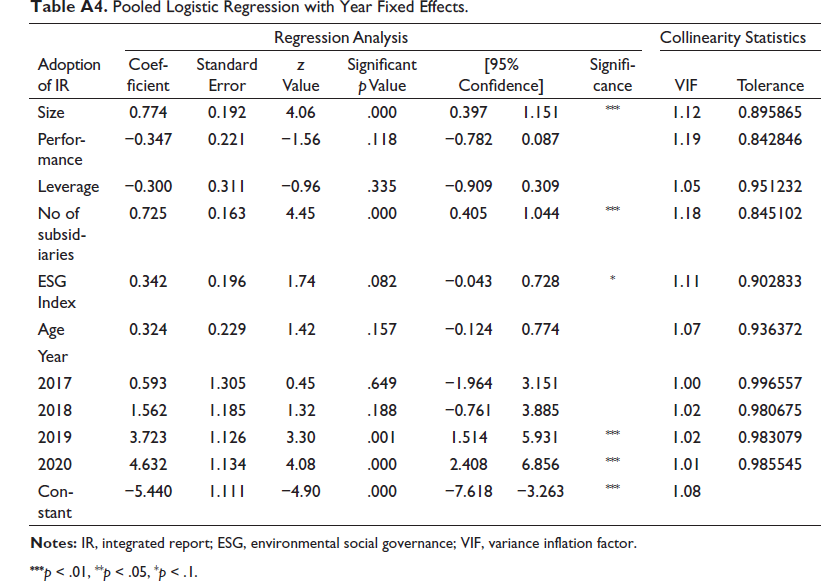

Table A4 presents the Pooled Logistic Regression with the year fixed effects model. Independent variable Size has a positive and significant relationship (at 99% confidence level, the coefficient of company size = 0.774, p value for company size = .00) on adoption of IR. Therefore, we accept the hypothesis (H1). From earlier studies (Bonsón & Escobar, 2004; Oyelere et al., 2003; Prencipe, 2004), it is clear that company size positively influences the quantity of information disclosed. The results are in line with the stakeholder and voluntary disclosure theory and reveal that big companies are more in light of the public representing greater sensitivity to their image. As the potential users of the financial information increase, demand and pressure on the company for disclosure increases.

The variable performance has a negative and insignificant effect (coefficient of profitability = −0.347 and p value of profitability = .11). Therefore, the hypothesis (H2) is rejected. It is not significant for management to prepare an IR because the economic considerations of the companies do not result in perceived benefits arising from voluntary disclosure theory and the information attained from an IR. Leverage has a negative and insignificant impact (coefficient of leverage = −0.300 and p value of leverage = .33). Therefore, it is not possible to accept the hypothesis (H3).

The number of subsidiaries representing structural complexity has a positive and significant impact (at 99% confidence level, coefficient of the number of subsidiaries = 0.725 and p value of subsidiaries = .00) on the adoption of IR. A large number of subsidiaries indicates a more extensive organizational framework. A company’s number of subsidiaries significantly affects information disclosure (Haniffa & Cooke, 2002; Hossain, 2008; Speigal & Yamori, 2004). According to Cooke (1989), better management information systems (MIS) are needed to keep track of structurally complex companies. The preparation of such MIS assists in reducing information costs and leads to more disclosure. Therefore, hypothesis (H4) is accepted.

The ESG Index shows a positive and significant relationship with IR adoption (at 90% confidence level, coefficient of ESG Index = 0.342, the p value of ESG Index = 0.082). The results are consistent with other studies (Lai et al., 2016) and thus highlight the indications for a positive impact of the adoption of IR. This result leads us to accept (H5) and supports the voluntary disclosure theory.

Age has a positive and insignificant effect (coefficient of age = 0.324 and p value of age = .157). Therefore, the hypothesis (H6) is rejected because the old companies are not inclined to IR disclosures, so not in sync with agency theory. However, results are inconsistent with several studies (Akhtaruddin, 2005; Bhatia & Dhamija, 2015; Owusu-Ansah, 1998) that an organization’s age influences the disclosure’s extent, possibly because older firms are likely to make a good impression (Suchman, 1995). According to Vitolla et al. (2020), old companies prepare better-quality IRs than new ones.

Moreover, in the years FY 2019 and 2020, highly significant results are there at a significance of 1% (p value of the 2018–2019 year = .001, the p value of the 2019–2020 year = .00). However, the number of companies adopting IR in the year 2019–2020 (approximately 33%) is more than that of the year 2018–2019 (about 25%).

Table A5 represents the summary of the pooled logistic regression with year-fixed effects. The amount of explanatory power of the pooled logistic regression with year fixed effects the value of pseudo R2 = 0.384 explains that 38.4% of the variations in the adoption of IR which is described by variations in the firm characteristics. The p value below the threshold of .05 means that the model in the current study depicts a significant improvement in the fit.

A negative constant in the results shows that the adoption of IR, in our case, has a p value less than .5 means that the probability of the desired event is less than .5, where β0 will be negative, and above .5, it will be positive.

As companies become more aware of the IR practices and their benefits and advantages, they are shifting towards disclosing more IR. In this study, we used 94 IRs of top companies, out of which there are only 31 adopters of IR from 2016 to 2020, as highlighted in the Appendix. There is an increasing trend for companies adopting IR year-wise.

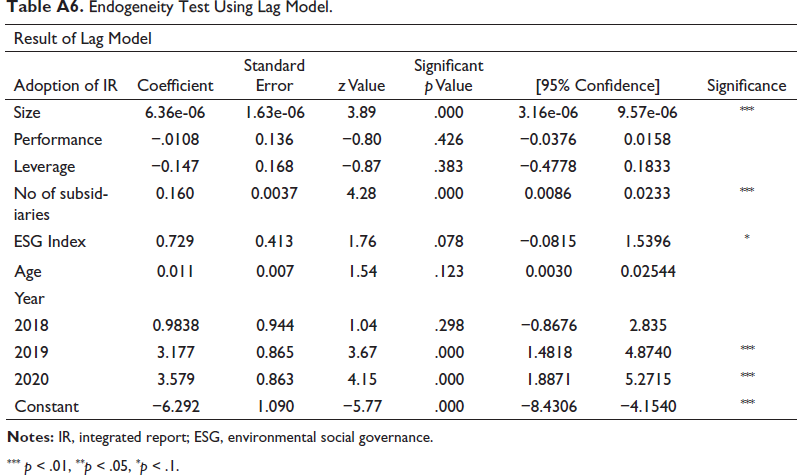

Endogeneity Test Using Lag Model

We have introduced the time lag of 1 year (Dhaliwal et al., 2011; Fuhrmann, 2020) to address the endogeneity issue. The test results in Table A6 are consistent with the main test results in Table A4; that is, the size of the company, its structural complexity and part of the ESG Index significantly positively affect the adoption of IR. As the results are consistent with the main test results, the endogeneity problem does not arise.

Conclusion

With continuous changes in the business environment, each firm’s competitiveness has become the key to its survival (Bhatia & Mehrotra, 2016). There is pressure from the stakeholders, government and international funding agencies, to provide information that is non-financial in the form of environmental reports. Disclosures related to Environmental reporting communicate the impact of the actions of the organization on the environment (Chaklader & Gulati, 2015). So, the broad business environment advances towards adopting non-financial information as part of the business’s strategy (Tewari & Dave, 2012). Nowadays, business reporting stresses value creation. IR fulfils the growing demands of companies regarding information related to financial performance and sustainability records due to the complex structure of firms. A few companies in India have started voluntarily publishing IRs to provide coherent summary information in the document format, thus helping shareholders make decisions.

This article examines the impact of firm characteristics on the adoption of IR, taking into account the postulates of three main theories of information disclosure: voluntary disclosure theory, signalling theory and legitimacy theory. Based on a multi-dimensional theoretical framework, this study analyses that societal and economic rationale frames the decision to disclose IR. The societal rationale considers the stakeholder’s considerations in that the company should act in the manner acceptable in the institutional setting to ensure legitimacy. In contrast, economic rationale includes the signalling perspective accompanied by firm characteristics.

The inferences drawn from the pooled logistic regression with year-fixed effects show that IR disclosures have a positive and significant relationship with the size of the company, number of subsidiaries and ESG Index. Therefore, the research hypotheses related to size, number of subsidiaries and ESG Index support research findings. In contrast, the remaining research hypotheses related to performance, leverage and age do not reflect the research findings.

This research clarifies the contribution to the policy front on listed companies relevant for IR adoption by studying the firm-level characteristics for IIRC. These days IIRC has moved from Breakthrough Phase to Momentum Phase and applying a repositioning strategy to make it a global norm. For proper IR disclosure practices, the government and the regulatory body guide the firm by issuing adequate guidelines through the board of capital market and professional training programs to understand IR reporting regimes better. To achieve sustainable development goals, the audit firms influence the corporate culture in respect of disclosures as they influence the preparation of IR to showcase accountability to its stakeholders by providing comprehensive reporting. After understanding the behaviour of the stakeholders, such as investors, the company’s executive turns to IR practices and more extensive disclosure to enhance its worth and place its organization as a sustainable corporate. On the company’s front, by knowing the benefits of IR, the companies may provide more information in the form of disclosure of IR to improve transparency. In contrast, controllers advise the firms to disclose the information related to IR disclosures to predict the forthcoming risk.

There are several limitations to this study. First, on the theoretical front, the current article focuses on the voluntary disclosure arena following the two most appropriate theories, that is, signalling and legitimacy theory. In the future, other theories may be considered for formulating and testing the hypothesis. Second, the focus was on the BSE 100 companies on the methodological front. Future studies may consider a larger sample and examine industry-specific characteristics that influence the motivate adoption of IR.

This article is trying to bridge the gap by first studying the impact of Structural complexity of business in respect of the number of subsidiaries on the adoption of IR in the Indian context.

Future studies can investigate how the non-IR companies maintain and manage their relationships with the stakeholders. Second, interviews with the senior managers of the companies who are preparing the IR reports voluntarily using the qualitative research method such as case studies and group discussions.

Appendix

Variables Description, Expected Sign and Data Source.

Statistical Summary of Variables.

Pairwise Correlations.

***p < .01, **p < .05, *p < .1.

Pooled Logistic Regression with Year Fixed Effects.

***p < .01, **p < .05, *p < .1.

Pooled Logistic Regression with Year Fixed Effects Model Summary.

Endogeneity Test Using Lag Model.

*** p < .01, **p < .05, *p < .1.

Regression Result Using Log of Total Assets Proxy for Company Size.

***p < .01, **p < .05, *p < .1.

Regression Result Using Return on Assets Proxy for Performance.

* **p < .01, **p < .05, *p < .1.

Testing of Robustness.

* **p < .01, **p < .05, *p < .1.

Companies Adopting IR.

Companies Not Adopting IR.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.