Abstract

Mobile payment services (MPS) are gaining popularity and growth as innovative methods of payment. However, still due to pro-innovation bias, less attention has been given of barriers to innovation as compared to the adoption of the technology. The current research focuses on the various users’ barriers to MPS adoption intentions (AIs). The study established a research model supported by the extended innovation resistance theory, including information barriers (InfBs), lack of facilitating conditions and lack of perceived novelty (LPN). A total of 357 valid questionnaires were collected from MPS non-users and hypotheses were tested via structural equation modelling and artificial neural network. The research findings indicate that usage barriers, value barriers, InfBs, unavailability of facilitating circumstances and LPN adversely affect MPS AIs. This research has several practical and theoretical implications to build strategies to overcome barriers in the adoption of MPS.

Introduction

Owing to the technological advancement in the digital payment sector, there have been dramatic shifts in consumer behaviour (Patil et al., 2018). One of the biggest changes in digital payment technology in the last decade has been the rise of mobile payments (Humbani & Wiese, 2018; Upadhyay et al., 2022). Mobile payment services (MPS) have become a popular way of payment for both retail and private sectors. Over the previous decade, many mobile payment channels (like Paytm, Phone pay, Google Pay, Apple Pay, and PayPal) have emerged in the retail consumer sector (Khanra et al., 2021). This study majorly focuses on three aspects of MPS that are UPI (unified payment system), mobile wallets, and mobile banking. These are the major ways to perform mobile based transactions in India (Data Security Council of India (DSCI), 2020). MPS are a popular and fashionable digital invention that offers a variety of benefits, such as, adaptability, effectiveness, efficiency and facilitating rapid monetary transactions (Raman & Aashish, 2021; Upadhyay et al., 2022). However, despite providing convenience and benefits to customers, mobile-based systems are slow to catch in established and developing nations (Khanra et al., 2020). This suggests that more research needs to be done to find out what hinders consumer behaviour from the acceptance and use of these methods.

The mobile payment system ecosystem has changed drastically in the recent years. Over the previous decade, many mobile payment channels (namely Paytm, Phone pay, Google Pay, Apple Pay and PayPal) have emerged in the retail consumer sector (Khanra et al., 2021). The number of MPS has grown a lot, and by 2023, the market is expected to be worth about $2,100 billion, with a compounded annual growth rate of 15% (ACI Worldwide, 2021). MPS is especially relevant in the context of a cash-dominated (Pal et al., 2019; Sobti, 2019) and emerging economy such as India as MPS can play a crucial role in financial inclusion for the underprivileged population (Pal et al., 2021). India has 26% of the smartphone base in the world, while merely 7.7% of the Indian population is using MPS for their daily financial activities (GSM Association, 2020). India is the second biggest smartphone market in the world, where 68% of the Indian population still have a preference for cash payments, while 48% consider e-payments did not offer enough value and about 55% find it difficult to understand the whole process of the digital payments (Sinha et al., 2019). Hence, India is lagging in MPS in comparison to the other economies of the world which is a daunting task in front of policymakers and researchers.

Resistance is a natural reaction to innovations since they have the potential to disrupt existing lifestyles (Ram & Sheth, 1989). Users’ resistance to financial technology has always been a big problem (Cham et al., 2022; Eriksson et al., 2021). The previous research initiatives aimed to explore the antecedent to adoption and use (Gupta et al., 2019; Shankar & Datta, 2018; Upadhyay et al., 2022) while little effort (Kaur et al., 2020) has been made to comprehend consumer resistance to MPS in the Indian context. Moreover, findings from the current studies are not sufficient to explain the causality of the relationships that lead to MPS resistance. The resistance to innovation and acceptance is a topic that has not been fully explored yet, and it should get more attention (Cham et al., 2022; Chaouali & Souiden, 2019). In the light of above argument, the current study is focused on pre-adoption behaviour of non-users of mobile payment system and fills the research gap in this context.

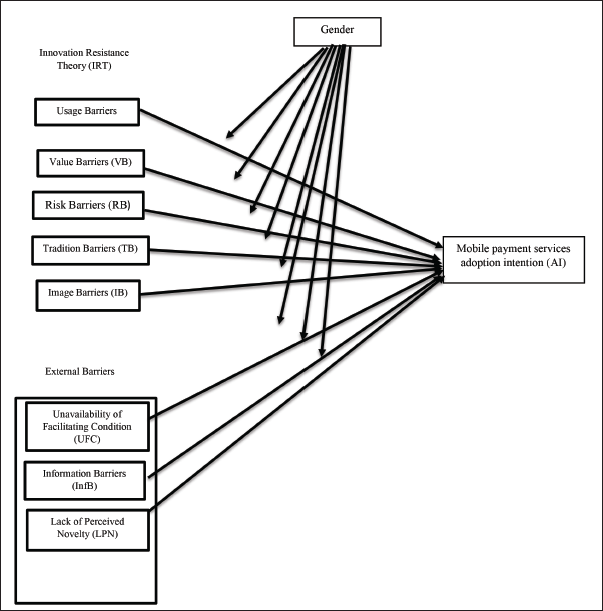

Keeping in view the variations in the factors such as digital divide (Pal et al., 2020), digital penetration (Farah et al., 2018) and digital resources (Hossain et al., 2018), the current study integrates the innovation resistance theory (IRT) framework with three external barriers viz; the lack of perceived novelty (LPN), information barriers (InfBs) and the unavailability of facilitating conditions (UFCs) Indians are not new to mobile phones, but using digital payments is a new idea for them (Sinha et al., 2019; Talwar et al., 2020). Because of this, they may need information and assistance from their service provider to get familiar with MPS. Apart from that, the lack of infrastructure support in emerging nations is a threat to adopting digital payment services (Upadhyay et al., 2022; Venkatesh et al., 2012). Integrated model provides a ‘complete account of the casual mechanism underlying the relationships and unique insight that cannot be obtained from a single theory driven model’ (Samar & Mazuri, 2019). Further, it has been observed that gender is a significant factor in technology adoption (Chawla & Joshi, 2020; Laukkanen, 2016; Mukerjee et al., 2020), and it plays an important part in both the segmentation of the market as well as the female empowerment (Martins et al., 2014; Venkatesh & Morris, 2000). Finally, the authors analyzed the effect of gender as the moderating factor on the relationship between the factors underlying extended IRT theory and the adoption intention of the users. Hence, the goal of this study is to address the research gap regarding the barriers contributing the non-adoption of MPS in India, and examining how gender influences the barriers in adoption of MPS. The study intends to solve the following research questions:

RQ1: What are the various barriers that impede the adoption of mobile payments among the non-users? RQ2: How does gender moderate the influence of each barrier on MPS acceptance intention?

In order to address the two concerns indicated above, the conceptual model for the research was developed using the research approach recommended by Ram & Sheth, (1989). The present study brings several implications for MPS providers, businesses, government officials and other key stakeholders. First, integrated model will provide better comprehensive insights which can help service providers, engineers and marketers to reframe their strategies based on the findings of the study. Second, the study based on structural equation modelling and artificial neural network (SEM-ANN) framework will help to better understand the complexity in decision making due to non-usage of MPS. Third, the study contributes theoretically and through empirically validated results to the existing literature on technology resistance and adoption which may be further used by the other researchers.

The article has been organized into six sections. The first section begins with overview and problem statement related to barriers in adoption of MPS. This is followed by the section that deals with the relevant literature. The subsequent section gives the theoretical background of the study and hypothesis formulation; next, the methodology and data analysis techniques are discussed. The penultimate section describes the results of the study. Lastly, the implications, steps for future research and the limitations are discussed.

Review of Literature

Existing Studies Related to Resistance Toward MPS Adoption

Most previous MPS research initiatives aimed to understand the constructs influencing adoption intention and usage (Chawla & Joshi, 2019a; Kapoor et al., 2020; Moorthy et al., 2020; Saha et al., 2022; Shankar & Datta, 2018). Comparatively, minimal efforts have been made to comprehend consumer resistance to MPS in the Indian context. In the Indian context, Sivathanu (2019a) results showed that the use of electronic payment systems was affected by behavioral intention to use and innovation resistance. Similarly, Kaur et al. (2020) studied consumer barriers to using and recommending MPS and found that usage, risk, and value obstacles were adversely connected with MPS adoption intentions. Similarly, Chaouali and Souiden (2018) investigated mobile banking resistance among elder users in France using age as a moderator and compared the connections between psychological and functional barriers. The findings investigated that all barriers had an impact on resistance behavior and cognitive age moderated these relationships. Laukkanen (2016) his study in Finland explored how consumer demographics as well as adoption barriers influence consumer adoption vs. rejection choices and found that the value barrier was the biggest hurdle to adopting online and mobile banking. It was also found that decisions about adoption and rejection were highly predicted by gender and age. Leong et al. (2019) examined the barriers to m-wallet adoption via the perspective of IRT in Malaysia. The results of the study observed that there were substantial impacts of usage barrier, tradition barrier, risk barrier, and value barrier along with perceived novelty, education level, and income level on the innovation resistance of m-wallets.

Innovation Resistance Theory

Resistance is a natural reaction to innovations since they have the potential to disrupt established lifestyles (Ram & Sheth, 1989). In reality, most of the retail innovations go through the aversion stage, some of them fail at the initial phase, while others flourish after overcoming obstacles (Kuisma et al., 2007; Ram & Sheth, 1989). Customers face several barriers that make it hard to adopt new ideas (Laukkanen et al., 2009). Since retail customer resistance to innovations may affect the outcome of financial innovations, companies and service providers delivering new consumer solutions must get a deeper understanding of the phenomena of innovation resistance (Antioco et al., 2010; Heidenreich et al., 2016). When the users witness the changes brought about by the innovation, functional barriers will arise, while psychological barriers will emerge if the innovation goes against people’s values or beliefs (Moorthy et al., 2017). In business research literature, IRT has frequently been used to study consumer resistance to many areas such as mobile social commerce (Mani & Chouk, 2017), mobile commerce (Moorthy et al., 2017), mobile banking (Arif et al., 2020) and mobile wallet (Leong et al., 2019). The IRT’s extensiveness provides a upright foundation as a theoretical framework for looking at user resistance to innovations (Chouk, 2019).

Extension of IRT Model (Information Barriers, Lack of Perceived Novelty and Unavailability of Facilitating Condition)

The lack of information about a new product or service is an InfB (Dotzauer & Haiss, 2017; Kuisma et al., 2007) which hinders its adoption. When consumers do not feel like they know enough about a new product or service and do not get support from the service providers offering it, they are less likely to buy it because it is too risky (Kuisma et al., 2007). In India, people do not use new payment methods because they are not aware about the MPS or it’s hard for them to get the information they need (Pal et al., 2019). Apart from that, the lack of infrastructure support in emerging nations is a threat to adopting digital payment services (Upadhyay et al., 2022; Venkatesh et al., 2012). Most MPS require users to have smartphones with internet access to download and use an app. They also need to know how to use the app and make sure it works with their bank accounts or debit cards (Moorthy et al., 2020). However, these things are not always the same in developing countries (Pal et al., 2020). Besides, perceived novelty is a prominent subjective notion that drives IT innovation adoption (Leong et al., 2019). Perceived Novelty in the MPS context relates to the degree to which users’ attitude to MPS is determined by its perceived newness (Leong et al., 2019). Chung and Liang (2020) revealed that LPN has a substantial impact on MPS resistance. Previous literature has explored the InfBs (Kuisma et al., 2007; Laukkanen, 2016), UFCs (Moorthy et al., 2020; Pal et al., 2020; Venkatesh et al., 2012) and LPN (Choi et al., 2017; Leong et al., 2019) in the different context of digital innovation. The present study has explored the impact of these three barriers along with IRT framework to comprehend the holistic view leading to mobile payment resistance in India.

Conceptual Model and Hypothesis Development

Usage Barriers

Usage barriers (UBs) deal with the usability of the service and changes required from the perspective of the user like acquiring new skills and changing old behaviours (Kleijnen et al., 2009; Laukkanen et al., 2009). This was discovered to have a high inverse correlation with the intention to adopt online and internet banking (Laukkanen, 2016; Laukkanen et al., 2007). Similarly, the intentions of users to adopt and use MPS (Cham et al., 2022; Joachim et al., 2017) are negatively correlated with UBs. Along the same line, other researchers have also discovered that use obstacles are positively associated with consumers’ resistance to the digitization and mobile banking (Arif et al., 2020; Yu et al., 2015). Therefore, the hypothesis is suggested as follows:

H1: There is a negative association between UBs and AI towards MPS.

Value Barriers

The monetary and performance value of innovation compared to its substitute is known as the value barrier (VB) (Ram & Sheth, 1989). The biggest hurdle to using online and mobile banking services is the cost (Laukkanen, 2016) and innovation must have a compelling ‘performance-to-price value’ in comparison to other options, for its acceptance. Users’ opposition to mobile banking was shown to positively correlate with VBs (Mullan et al., 2019; Yu et al., 2015). Results indicate that a lower benefit of mobile payments over other methods of traditional payments leads to a lesser possibility of users adopting the innovation (Cham et al., 2022; Rombe et al., 2021). Thus, the hypothesis is postulated as follows:

H2: There is a negative association between VBs and AI towards MPS.

Risk Barriers

Innovations in technology are always seen as risky, particularly when it comes to financial transactions since consumers are extremely worried about issues with security, fraud and personal information (Anouze & Alamro, 2019; Zhang & Luximon, 2021). Risk barriers (RBs) include the uncertainty that comes with every new technology (Laukkanen & Kiviniemi, 2010). Customers who use MPS can be at risk for fraud, financial loss, slow Internet or short smartphone battery life. As a result of the uncertainties related with the innovation, RBs have the potential to become obstacles in the way to the adoption of the same (Cham et al., 2022; Moorthy et al., 2017; Zhang & Luximon, 2021). The following assumption is generated from the above discussion:

H3: There is a negative association between RBs and AI towards MPS.

Tradition Barriers

Laukkanen (2005) defined tradition barriers (TBs) as hurdles provided by any innovation that causes modifications in a user’s current habit, behaviour or culture. Traditional cash-based payment systems are incompatible with MPS, which demands users to make payments digitally (Dotzauer & Haiss, 2017). TBs appear to have an inverse relationship with AIs for mobile services (Joachim et al., 2017) and mobile commerce (Moorthy et al., 2017) as well. Hence based on literature, the following is derived from the preceding discussion:

H4: There is a negative association between TBs and AI towards MPS.

Image Barriers

It refers to an unfavourable perception that has evolved as a response towards an invention (Laukkanen, 2005). The image of the innovation is a vital direction for the consumer to adopt the service and product (Chung & Liang, 2020). Consumers do not frequently regard MPS to be secure, which leads to a poor image (Leong et al., 2019). There are presently hundreds of mobile payment companies all over the world attempting to serve humanity and meet every financial need (Alkhowaiter, 2020); however, the image barrier (IB) exists as a significant inhibitor of mobile banking adoption (Laukkanen, 2016; Mullan et al., 2019; Rombe et al., 2021). IBs appear to have an inverse relationship with AIs in the case of m-wallets as well (Alam et al., 2021; Leong et al., 2019; Pal et al., 2020). Accordingly, the hypothesis is:

H5: There is a negative association between IBs and AI towards MPS.

Information Barriers

InfB is present because people do not know enough regarding the new product or service (Laukkanen & Kiviniemi, 2010). When customers are not aware of an invention and do not get assistance from the company that made it, they are less willing to buy it because there is too much uncertainty (Kuisma et al., 2007). Resistance gets worse when service providers do not give enough information or provide any help (Laukkanen et al., 2009). Another critical feature of InfBs is related to the overburden of information, which indicates that the concretion of technical advancements creates increasing resistance (Kleijnen et al., 2009). In earlier studies also users have expressed their hesitation about using mobile banking services because of lack of unfamiliarity and information (Lin et al., 2019). The above discussion yields the following hypothesis:

H6: There is a negative association between InfBs and AI towards MPS.

Unavailability of Facilitating Conditions

It has been frequently observed in previous digital payment articles, especially in poor countries where the digital divide has hindered people’s usage of ICTs (Pal et al., 2020). Facilitating environments has been a key driver of attitude towards adoption in research that focuses on users from low-income groups (Raleting & Nel, 2011). Compared to developed countries, digital penetration in underdeveloped countries is shockingly low in terms of telecom revenues, broadband subscribers and Internet use (Farah et al., 2018; Upadhyay et al., 2022). As a result, the lack of facilitating conditions plays a significant barrier in developing nations. The above discussion leads to the hypothesis:

H7: There is a negative association between unavailability of facilitating conditions and AI towards MPS.

Lack of Perceived Novelty

Users’ perception of innovation as a novel, unique or updated one is referred to as perceived novelty (Mani & Chouk, 2017). Perceived novelty promotes positive attitudes towards IT innovation (Wells et al., 2010). Customers detect novelty only when there is a rapid change in the product’s idea or feature (Ram & Sheth, 1989). In earlier studies as well, consumers’ attitudes towards innovation and resistance to smart products have been assessed in terms of perceived novelty (Choi et al., 2017; Leong et al., 2019; Mani & Chouk, 2017). Keeping in view that LPN may have a crucial impact on customers’ apprehension to adopt MPS; the following hypothesis has been developed:

H8: There is a negative association between LPN and AI towards MPS.

Moderation Role of Gender in Adoption Intention

Demographics are important predictors of consumer rejection, adoption or intention to use (Laukkanen, 2016). So far, demographic studies have mostly focused on innovation adoption rather than innovation opposition. As a consequence, a study into the effect of demographics profiles on mobile payment resistance is crucial. Previous studies have revealed that gender is essential in explaining behavioural intention in innovation system research (Arif et al., 2020; Gupta et al., 2019; Tavera-Mesías et al., 2022). According to Dutta and Omolayole (2016), there is a substantial difference between the factors that influence men and women in terms of their propensity to accept new technologies. This is because the features of technology adoption have distinct effects on men and women. Gender had a big role in clients’ acceptance or rejection in e-banking in Finland (Laukkanen, 2016). Thus, the hypotheses have been drawn as follows (Figure 1):

H9: Gender moderates the relation between MPS AI and barriers to adoption (UB, VB, RB, TB, IB, InfB, UFC and LPN).

Research Methodology

Instrument

The research explored how non-users perceive about the barriers in adopting MPS in India. This was accomplished with the use of a 32-item questionnaire based on eight constructs derived from previous literature. Similar to Leong et al. (2019), items were derived from the previous literature and adapted in the context of MPS to ensure the construct validity of the measures. The items related to UBs and IBs were extracted from (Kaur et al., 2020; Kuisma et al., 2007; Laukkanen, 2016) while for value, tradition and RBs were derived from (Arif et al., 2020; Cham et al., 2022; Leong et al., 2019), items for InfBs were adapted from (Kleijnen et al., 2009; Kuisma et al., 2007; Laukkanen & Kiviniemi, 2010), items for unavailability facilitating conditions were adapted from (Pal et al., 2020; Venkatesh et al., 2012) and those for LPN were derived from (Choi et al., 2017; Mani & Chouk, 2017). The items for the mobile payment AI were adapted from (Daştan & Gürler, 2016; Pal et al., 2020). In this study, a 7-point Likert scale was adopted, which ranges from (1) Strongly agree to (7) Strongly disagree (Laukkanen, 2005, 2016).

Data Collection

This study used non-probability purposive sampling because there was no reliable database of Indian digital payment non-users (Baabdullah et al., 2019). Initial data for the pilot testing were obtained from a random sample of 60 respondents. During the pretest, experts who know much about MPS adoption were interviewed to assess the face validity and content validity of the survey instrument. From January 2022 to May 2022, data were collected by WhatsApp, Facebook, email and other social media platforms. Apart from that, the data were also collected manually from the non-users. This research’s aim and procedures were clearly explained to the participants. In case of manual collection of data participants were clearly asked whether they are using MPS or not. While in case of online data collection the second part of the questionnaire measuring barriers to MPS could be filled only if in the first part respondents give the response that they are currently non users of MPS. Hence, only non-users were targeted as per the goal of the study. Then the non-users were navigated to the questionnaire which measures the barriers for MPS. Furthermore, participation was fully anonymous and voluntary, and no reward was provided. The survey was sent to about 1200 non-users, but only 430 were filled out. So, the rate of responses was 35%. Finally, 73 responses were eliminated in the data screening process, reducing the data to 357 responses for further analysis. To analyze non response bias, author conducted paired sample t – test, in which the first early and last 50 respondents are taken. Early and last response did not witness significant changes (p>0.05). Therefore, the results draw confidence and witnessed no response bias (Ismail & Isa, 2011).

Data Analysis Technique

The dataset was evaluated with IBM SPSS 21 and IBM Amos 21. First, the study examined the measurement model. Then, it looked into the validity and reliability of the statements. The scholars next examined the offered hypotheses’ statistical significance to analyse the structural model. This was followed by ANNs Analysis. SEM is useful for modeling complex relationships between latent and observed variables, while ANN is powerful in identifying non-linear patterns in data (Lee et al., 2020). By integrating these two methods, SEM-ANN can provide a more accurate and comprehensive analysis of complex data sets (Al-sharafi et al., 2022; Wong et al., 2022). Hence, this research made sure that the advantages of SEM and ANN were used by limiting the input parameters for the ANN analysis to the relevant predictors discovered by the SEM (Lee et al., 2016).

Results

Demographics

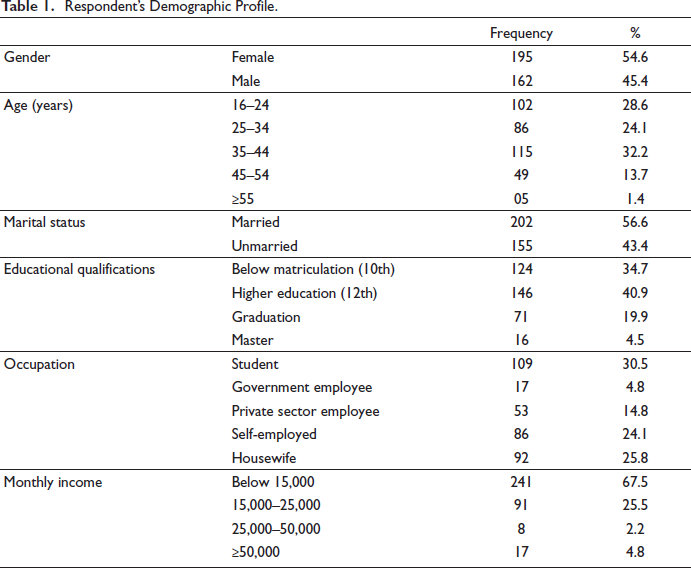

The respondent’s demographic profile of collected data is shown in Table 1. There were 162 female and 195 male respondents in the sample. Around 54.6 percent of male and 45.4 percent of female fall into this category. Participants in the study’s non-user group ranged in age from 16 to 55 and above. The age range of 35 to 44 years was represented by the majority of respondents (32.2 %). About half of the respondents (49.9 %) identified as self-employed and housewives, followed by students (30.5%), private employees (14.8%), and government employees (4.8%) in order of occupation. 34.7% of respondents had less than a high school diploma, 40.9% had post-secondary degrees, and the remaining respondents had bachelor’s or master’s degrees.

Respondent’s Demographic Profile.

Common Method Bias (CMB) Test

Self-acknowledged measurements are vulnerable to CMB, therefore, data are evaluated. When Harman’s single component was first examined, statistical analysis showed that it only accounted for 23.394% of the total variation which is less than the threshold limit of 50% of the variance (Podsakoff, 2003) indicating the absence of CMB-related problems. Second, by converting each measure into a single-item second-order construct, common latent factor analysis was carried out to further demonstrate that CMB is not a problem (Hew et al., 2017). For this, the difference between the models for 1DF is 2.137 chi-square value which was below the threshold value indicating that there is no issue with CMB.

Measurement Model

The measurement model aided in determining the survey instrument’s reliability and validity. GFI (0.889) and AGFI (0.862) absolute indices were found to be close to, if not greater than, 0.9 (Baumgartner & Homburg, 1996; Doll et al., 1994). The values of RMR = 0.0482 (<0.08), root mean square error of approximation (RMSEA) = 0.045 (<0.08), CFI = 0.940 (>0.90) and TLI = 0.930 (>0.90) (Fan et al., 2009; Kumar, 2012). Further, standardized Chi-square values are following standards and are quite good (1<1.708<3). These metrics are satisfactory and predictive of a high degree of quality model adjustment.

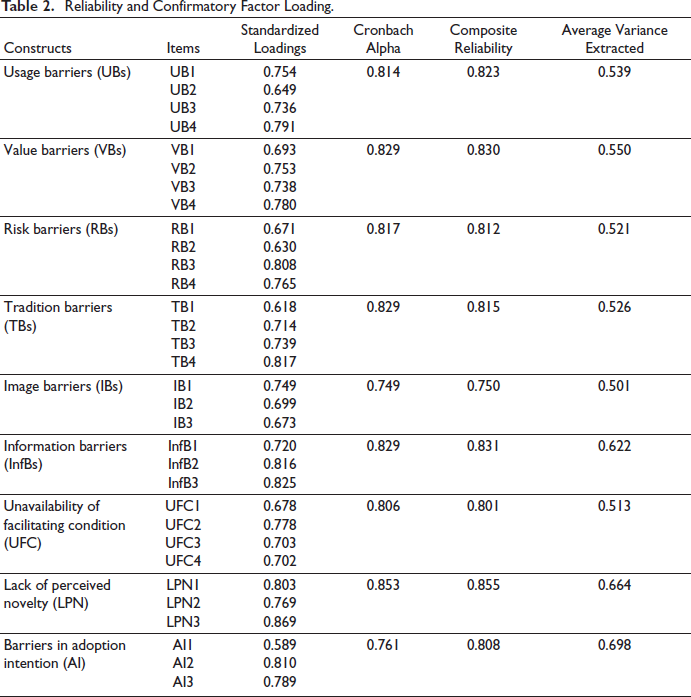

Composite Reliability

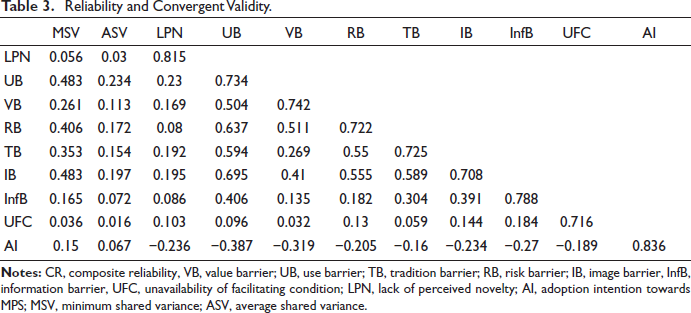

Composite reliability (CR) and Cronbach’s alpha values are shown in Table 2, and both are more than 0.70. The results support the model and confirm that the model has good construct reliability (Hew et al., 2018). Further, the value of the average variance extracted (AVE) is more than 0.50 which indicates that convergent validity is also good. Thus, it confirms the constructs validity (Leong et al., 2018; Nordman & Tolstoy, 2016). For the discriminant validity, Table 3 shows that AVEs are more than the minimum shared variance (MSV) and average shared variance (ASV).

Reliability and Confirmatory Factor Loading.

Reliability and Convergent Validity.

Structural Model Results

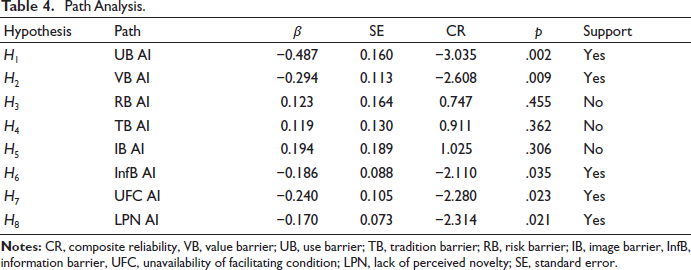

Table 4 reveals that five out of eight paths are significant. Thet statistic with 95% confidence intervals was used to evaluate the relationship’s significance. UBs (β = −0.487, CR = −3.035), VBs (β = −0.294, CR = −2.608), InfBs (β = −0.186, CR = −2.110), UFC (β = −0.240, CR = −2.280) and LPN (β = −0.170, CR = 2.314) have significant effects on adoption of MPS. Hypotheses H1, H2, H6, H7 and H8 are, therefore supported. The findings of the research corroborate with the findings of previous literature. The significant impact of UBs corresponds to (Laukkanen, 2016), but the substantial effect of VBs conforms to (Leong et al., 2019). The inverse association between InfBs and adoption is supported by studies of online banking that found a negative association between InfBs and adoption (Kuisma et al., 2007; Laukkanen et al., 2009). The UFCs has a substantial impact on the AI. This association has been supported by Pal et al. (2020). Lastly, LPN has a substantial impact on MPS adoption, therefore supporting hypothesis H8. This conforms with the findings of (Mani & Chouk, 2017; Wells et al., 2010). RBs (β = 0.123, CR = 0.747), TBs (β = 0.119, CR = 0.911) and IBs (β = 0.194, CR = 1.025) show no significant impact on MPS AI based on these criteria. Therefore, hypotheses H3, H4 and H5 are not supported.

Path Analysis.

Structural Model Results Based on Gender

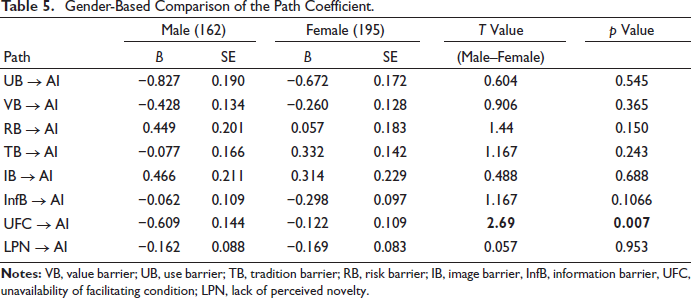

Data were grouped on male and female participants and then used a customized version of the grouping variable approach of the Amos process to analyse it to explore the moderating effects of gender. In data, the sample size of male and female participants is not the same (Hwang, 2010). However, Dunnett, (1980) and Arif et al., (2020) argue that different sample sizes can also be used to compare two groups if they came from the same population as it can be assumed that the variation is the same. Also, Sarstedt et al. (2011) suggested that comparing groups with different sample sizes might be possible.

To evaluate the moderating impact, this study applied multigroup moderation analysis. In the first phase, the basic dataset was divided into male and female sub-datasets depending on gender. In the second phase, the dataset was analysed using the same structural model. In the third phase, data were compared pair-by-pair for the path coefficient and intensity of significant differences across groups. To evaluate and identify the moderating influence, the t-statistics of the two groups were compared with their path difference. Using the method proposed by (Lowry & Gaskin, 2014), the t-statistic difference was performed to assess if there was a significant difference between the moderator variable and its related relationship (Table 5). Lastly, the results were used to make conclusions.

Gender-Based Comparison of the Path Coefficient.

The outcomes of the path coefficients are shown in Table 5. The results demonstrate that gender moderates the UFCs in the adoption of MPS. There is no interaction between gender and the seven other variables examined in this research. Males have an R-square value of 0.331 and females have an R-square value of 0.332.

Artificial Neural Networks Analysis

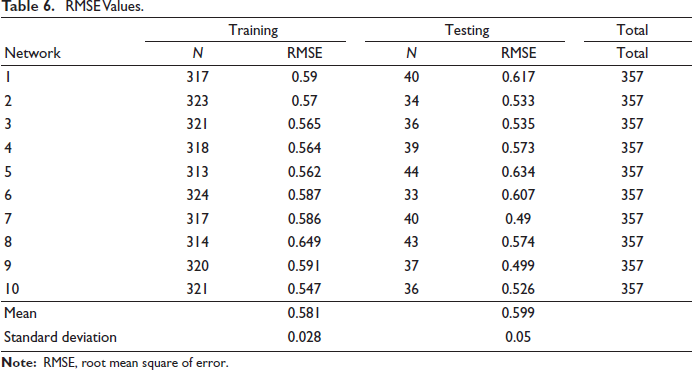

A two-stage structured technique is used for ANN analysis. First, the whole model is tested using SEM to ascertain the relative importance of each independent construct variable, which is then used as input in a second phase to assess the relative significance of each predictor construct (Leong et al., 2013; Liébana-Cabanillas et al., 2017). The ANN algorithm is capable of discovering both linear and nonlinear associations and need not to be normal distribution (Karkonasasi et al., 2018). Multilayer perceptron (MLP) and sigmoid activation algorithms were employed for the input and hidden layers (Leong et al., 2013). SPSS 21 was used for the neural network analysis. The input layer consisted of five independent SEM components (UB, VB, InfB, UFC and LPN), while the output layer included a single output variable (AI, i.e. AI of MPS). Additionally, the researcher utilized 10-fold cross-validation, in which 90% of the data were used for network training and 10% was used for testing, to avoid over-fitting (Liébana-Cabanillas et al., 2017). ANN’s input nodes are also used to figure out the importance of normalization in the sensitivity analysis. In the sensitivity analysis, the normalized importance was used to test how strong the causal relationships were. All 10 neural networks’ respective averages and standard deviations, as well as the RMSE of training and testing data, were removed to verify the model’s accuracy (Arif et al., 2020). Table 6 displays the RMSE of the validations; the RMSE for the training model is on average 0.581, while the RMSE for the testing model is 0.599 (Arif et al., 2020).

RMSE Values.

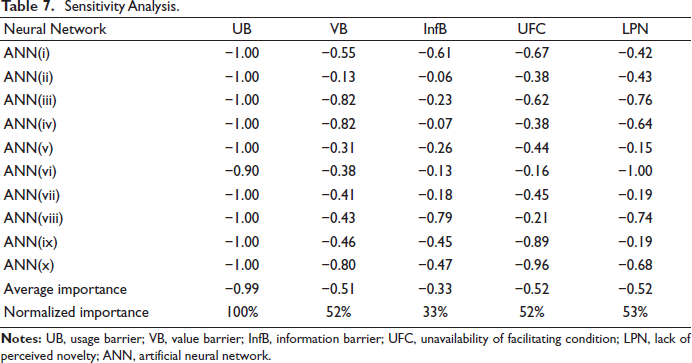

Sensitivity analysis (Table 7) is used to get the normalized importance of each independent neuron by dividing its relative importance by the maximum importance and showing it as a percentage. UB is the most significant predictor, followed by LPN (53%). This is followed by the VB (52%), the UFCs (52%) and the last InfB (33%) (Karkonasasi et al., 2018).

Sensitivity Analysis.

Discussion

The study investigated to figure out the significant barriers which discourage customers from the usage of MPS in India. H1 explored UB has the strongest, statistically significant, and inverse impact on MPS AI among the innovation barriers which is consistent with existing literature (Arif et al., 2020; Kaur et al., 2020; Leong et al., 2019). In the case of MPS, UBs serve as a barrier to the effective transformation of any newer invention into a mainstream innovation. MPS and other service providers should prioritize the usability of their products and services. Additionally, mobile payment systems should be accessible at all times and under all circumstances.

H2 investigated whether the VB is adversely related to MPS AIs and the findings provide support for the hypotheses. The possible explanation for this is that customer does not perceive the innovation’s value exceeds that of existing products or services (Chen & Kuo, 2017; Kaur et al., 2020). This is consistent with earlier studies suggesting that VBs have an inverse relationship with AI (Arif et al., 2020; Kaur et al., 2020; Leong et al., 2019). As a result, MPS and other service providers have to assist clients in managing and exercising control over their financial matters in various ways.

In contrast, H3, which proposed an inverse relationship between RBs and the desire to adopt MPS, was not supported. The findings of the study contradict the previous studies (Cham et al., 2022; Kaur et al., 2020; Leong et al., 2019) where the risks or uncertainties connected to identity theft, data security, privacy and other issues negatively affected the MPS AIs. The possible explanation for the insignificant relation in the present study can be that people assume that if they adopt an innovation, they would not make mistakes in their banking processes or they can overcome with the associated risk. Future research might analyse this link in further detail.

H4 anticipated that there is no significant relationship between TBs and intention to adopt MPS. The findings of the study contradict the majority of past research, which has revealed a significant inverse connection between intentions (Arif et al., 2020; Laukkanen, 2016; Moorthy et al., 2017) while corroborate with the research by (Kaur et al., 2020). Our results imply that the TB might be a significant barrier during the early stages of any user innovation, but it fades as the innovation matures. The other possible explanation can be that MPS is getting mature in India over some time; hence, TBs do not play a substantial influence. A potential reason for discovery is that the Indian economy has changed a lot from cash to cashless. As a result, the Indian population is either being pushed to use MPS or is being forced to do, with the rise of several MPS platforms.

The results of the study do not support hypothesis 5, which explored the negative relationship between IBs and MPS AIs. These results are contradictory to prior studies on IBs (Arif et al., 2020; Laukkanen, 2016; Moorthy, Ling et al., 2017). The technology orientation of customers might be a contributing factor to the insignificance of IBs. This is consistent with previous research suggesting that young adult MPS users do not associate MPSs with tags such as ‘hard to use’ and ‘complex to use’ (Sivathanu, 2018). The majority of the participants in the current study were young people who tended to be digitally savvy and had a positive outlook on a range of technology-based social and commercial platforms (Kaur et al., 2020; Khanra et al., 2020).

According to the findings, the InfB (H6) has an inverse and significant effect on the AI. Therefore, the extra barrier is a useful expansion of the conceptual model, at least in the context of MPS adoption. The findings support the conclusion of online banking research that a lack of information is negatively related to adoption (Kuisma et al., 2007; Laukkanen et al., 2009). As a result, the current research has boosted empirical evidence to increase the existing literature on MPS AIs as well.

H7 demonstrates a statistically significant and inverse association between the unavailability of a facilitating condition and MPS AI. Prior studies have shown mixed findings on the influence of facilitating conditions on technological adoption (Moorthy et al., 2020; Oliveira et al., 2016; Pal et al., 2020). Therefore, the present research has contributed new insights and understanding of facilitating conditions in the adoption of MPS in the Indian economy.

H8 found an inverse and statistically significant relationship between the LPN and intention to adopt MPS. This research shows that when customers consider MPS to be new, distinctive and updated, they will be ready to test the information technology and hence less hesitant to use it (Leong et al., 2019; Mani & Chouk, 2017). Prior studies have also identified novelty as a construct that favourably affects a user’s attitude towards employing a digital innovation (Leong et al., 2019).

The results of the study revealed that gender as a moderator showed that men are more open to technology if they think it will be useful, while women tend to focus more on what needs to be done. Similarly, males consider MPS to hold more value for money as compared to females. It was also found that when it comes to using technology, women tend to care more about what other people think and say than men do (Venkatesh et al., 2003). Khanra et al. (2020) also found that gender was a moderating factor in their models. Gender significantly moderates the relation between the UFCs and the intention to adopt MPS. Given that gender has a moderating effect; companies should create a good environment and make it easy for women to use MPS (Humbani & Wiese, 2018; Undale et al., 2021).

Lastly, based on the ANN approach the study identified that the UB is the most significant, followed by perceived novelty (53%), the VB (52%), the UFCs (52%) and the InfB (33%).

Conclusion

Using a two-staged SEM-ANN approach, this research has effectively confirmed the impact of IRT on customers’ resistance towards mobile payment services (Al-sharafi et al., 2022; Wong et al., 2022). The research model also included age, gender, income as demographic variables and introduced information barriers, unavailability of facilitating conditions, and lack of perceived novelty as additional variables to IRT. The results of the path estimate analysis revealed that usage barriers, value barriers, information barriers, unavailability of facilitating conditions, and lack of perceived novelty positively and significantly influence the intention to adopt MPS. On the other hand, tradition, risk, and image barriers have insignificant impact on the adoption of MPS, which contradict the previous studies (Cham et al., 2022; Kaur et al., 2020; Leong et al., 2019). The uncertain nature of transactions in developing countries, may contribute to the unclear consequences of adopting MPS. In the gender moderation analysis, it was found that female users encounter greater challenges in terms of facilitating conditions when they try to adopt mobile payment services compared to male users. The results revealed that usage barriers had the highest normalized importance, followed by value barriers, lack of perceived novelty, unavailability of facilitating conditions, and information barriers.

Theoretical Contribution

Firstly, it adds to the existing body of knowledge on consumer resistance to Internet-based mobile applications that are driven by services like Paytm, Phone pay, Google Pay, Apple Pay, UPI and other mobile banking applications. Researchers have become interested in better understanding customer resistance related to an innovation in recent years. However, in contrast to this, only a few studies in the context of India made an effort to comprehend the barriers to the adoption of MPS (Kaur et al., 2020; Sivathanu, 2019a). Hence, this study contributes to the innovation resistance theory (IRT) by applying it to the context of MPS and identifying the significant barriers to the adoption of MPS. It further provides empirical evidence to support the IRT and its application to the context of MPS. Extending the IRT theory with constructs such as information barriers, unavailability of facilitating conditions, and lack of perceived novelty along has offered holistic and comprehensive insights into the inhibitors which is the highlight of the study as there had been few prior studies that evaluated their influence on MPS acceptance (Arif et al., 2020). Secondly, by studying the moderation impact of gender on the MPS adoption intention and inhibitors has offered new insights into MPS resistance research (Arif et al., 2020; Gupta & Arora, 2019; Mukerjee et al., 2020). Therefore, these novel relationships can build fresh foundations for future academics based on the available literature.

Practical Implications

From an organizational perspective, the study’s findings have various implications for the advancement of m-payment systems in order to accelerate acceptance in India. MPS providers need to understand the factors that contribute to consumers’ resistance towards MPS adoption. Our study argues that service providers should address usage barriers, value barriers, information barriers, unavailability of facilitating conditions, and lack of perceived novelty as key priorities to gradually increase MPS adoption (Arif et al., 2020; Kaur et al., 2020). MPS providers have to focus more on usability, introduce necessary changes from the user’s perspective and provide more convenience compared to other methods available. The prospective customer should feel a high performance-to-cost ratio while using MPS. Service providers should craft better campaigns for providing guidance and increasing knowledge related to MPS which will result in consumers becoming more oriented towards MPS. Providing appropriate facilitating conditions such as smartphone with Internet access for app download and usage, as well as guidance to increase users’ understanding of the app and its connections to other components such as bank accounts or debit cards are the other measures required specially in remote areas of the country for deeper penetration of MPS (Pal et al., 2019; Raleting & Nel, 2011a). Players in the mobile payments industry must work hard to communicate to the people about the features, value, and novelty of mobile transactions to make them more aware of these services (Leong et al., 2019; Mani & Chouk, 2017). The measures will be more impactful if the moderation effect of gender is considered. The service providers should develop strategies to increase MPS adoption considering the differences between males and females particularly concerning their consumption habits (Laukkanen, 2016; Mukerjee et al., 2020; Vasudeva & Chawla, 2019). As the availability of facilitating conditions such as linking of MPS with bank accounts through MPS apps, MPS interface in native language, and being technically proficient to use MPS has a moderating impact on the adoption intention, so due diligence is required to take care of these things to widen the adoption of MPS (Chawla & Joshi, 2019a; Pal et al., 2019).

Limitations and Future Scope

The present research has definite drawbacks even though it makes a significant contribution. The research’s lack of generalizability is one of its most glaring flaws. This is primarily due to the research population as the current data describe the perception of the non-user Indian population with MPS. A future study might assess the model utilizing data collected from first-time users of all ages across geographical and cultural boundaries to get around this restriction. The research used a cross-sectional method, which means that the responses were collected at a given specific point in time. Hence, researchers may use longitudinal research in the future to study the effects of time as customers’ perceptions of various barriers may change over a period of time.

Footnotes

Acknowledgements

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the paper.

Declaration of Conflicting Interests

The authors have no conflict of interest to declare.

Funding

The authors highly acknowledge the financial support provided by the Ministry of Education, New Delhi, India in the form of a fellowship to the first author.