Abstract

Prior studies captured the influence of managerial behaviour in terms of their efficiencies and abilities on firm performance. However, the impact of managerial performance permanency on firm performance is still a grey area. This study aims to compare the influence of managerial behaviour and its permanency on firm performance by controlling the effect of corporate governance. The data envelopment analysis has been used to capture the managerial behaviour, which considers the data for 11 years from 2009 to 2019. The data were gathered from 492 firms listed on the stock exchanges of Pakistan, Bangladesh and India. The influence of managerial behaviour and comparison between permanent and temporary organizational behaviour on firm performance has been tested using the generalized method of moments. The results showed that permanency in managerial behaviour has a more positive impact on firm performance than short-term managerial behaviour. The study’s outcome is helpful for the board of directors and policymakers to maintain stability in managerial behaviour in terms of their efficiencies to improve firm performance.

Keywords

Highlights

Managerial behaviour permanency in terms of utilization of resources influences firm performance.

Corporate governance is positively associated with firm performance.

Data envelopment analysis is better measurement of managerial efficiency behaviour.

Introduction

In management and business research, managerial performance inside organizations has long been a subject of crucial relevance. Managers’ ability to effectively lead and make decisions can significantly impact a company’s success as a whole and its capacity to adjust to a constantly shifting business environment (Do Adro et al., 2022). Despite substantial research, understanding the effect of management permanence on business performance is a somewhat unexplored subject. This study aims to fill this knowledge gap by shedding light on the connection between managerial performance longevity and its effects on firm performance (FP).

Businesses are continually looking for ways to optimize their operations and strengthen in today’s dynamic competitive business environment (Hossain et al., 2022). The ability of a company’s management team is an important aspect of its success (Yung & Chen, 2018). Making strategic decisions, encouraging innovation and promoting organizational growth all depend on having effective managers. However, the conventional view of management performance frequently focuses on near-term evaluations, routine assessments and instant results. This study intends to dive into the long-term implications of management performance in addition to the standard method (Noor et al., 2020). Managers struggle to improve FP, which is required to achieve the ultimate objective of the firms, that is, ‘maximization of shareholders’ wealth. The investors, creditors and other stakeholders make their decisions by reviewing the firm’s financial and operational condition, for which an impressive element is the income statement, from which the firm’s performance is measured (Akbari et al., 2018). The managers are key factors with skills, knowledge, positive behaviour and cognition that are essential in making the accounting statement attractive.

The significance of consistency and continuity in leadership has recently come to light thanks to changes in the business world (Yung & Chen, 2018). The advantages of keeping high-performing managers on for a long time are becoming increasingly apparent to organizations. The necessity for constant strategic direction, staff morale and sustained success motivates the emphasis on leadership longevity (Khan et al., 2023). This pattern shows that, compared to prior research, the duration of management performance may significantly impact business outcomes.

Despite the literature’s wide coverage of the value of competent management, there is a glaring knowledge vacuum about how the consistency of managerial performance affects company success. Our understanding of the long-term implications of managerial success is lacking since current research frequently focuses on immediate results. This study tries to close this gap by examining whether and to what extent management performance permanence is linked to enhanced business performance. So, does the stability of managerial performance have a substantial effect on the performance of the firm? This is the primary research topic addressed in this study. We have the following research goals to answer this question. (a) To investigate the connection between the length of management performance permanency and business performance. (b) To determine what influences the relationship between management performance longevity and business performance. (c) To offer helpful suggestions for businesses looking to improve their performance through strategic management techniques.

First, the study delivers empirical evidence of the relationship between managerial behaviour (MB) and FP. Afterward, the effect of consistency (permanency) of MB on FP has been tested. The permanency of managerial positive behaviour is required to utilize resources properly and to take competitive advantage. Therefore, it is a theoretical and empirical contribution of the study for adding MB permanency (MBP) and its influence on FP. The concept of MBP has been taken from the study by Jeong et al. (2018) and Noor et al. (2020), which has been carried out on CSR permanency. The study measured MB at the first stage based on data envelopment analysis (DEA), an input–output-based method. Afterward, by following Jeong et al. (2018), MBP was measured using a dummy variable, 1 if managerial efficiency is equal to or more than 3 times over the most recent 4 years and otherwise 0. Moreover, the slope dummy, that is (MB*MBP), the interaction of dummy variable and MB, has been used to compare the effect of MBP with MB temporary in nature.

Literature Review

Managerial Behaviour and Firm Performance

Managers are the main characters in making decisions for investment efficiency, which leads to FP (Quah et al., 2020). To increase the FP by making the best possible investment, it is vital to study and research the elements that contribute to this. Making choices reveals the individuality of the decision-maker, and difficult choices are frequently influenced by cognitive and behavioural aspects (Gan, 2019; Hambrick & Mason, 1984). These behavioural and reasoning decisions impact forecasting upcoming events, options and outcomes (Hambrick & Mason, 1984). The ability of managers (decision-makers) to make strategic decisions, such as those involving financing, production innovation, seizing investment opportunities and forward integration, is reportedly influenced by their physiological characteristics and cognitive base values. The resource-based perspective hypothesis emphasizes the value of managers and shows how the firm’s potential to gain a competitive advantage strongly depends on managers’ capacity for efficient resource use (García-Meca & García-Sánchez, 2018; Holcomb et al., 2009). Instead, according to the echelons hypothesis, managers have unique traits and differ from one another in terms of their cognitive approaches, which causes them to choose differently, particularly in complex situations (Bamber et al., 2010). According to this hypothesis, managers’ traits affect corporate choices and financial planning through how they perceive the business environment (Hambrick, 2007).

According to Andréou et al. (2016) and Chang et al. (2010), managerial conduct significantly influences FP’s operational and financial production. Theoretically, professional managerial knowledge supports FP, according to Dutta’s (2008) discussion. One advantage of management behaviour regarding effectiveness, credibility and capacity is that it may help generate more money to take advantage of investment opportunities. In contrast, they make better use of resources to produce cash flows from the business’s operations. Consequently, managerial practices influence FP.

Consistency in MB is very important for the growth and performance of the organization. Good MB and hard work in the completion of some crucial tasks are not a short-term process, as most managers do during the management of the organization’s operation (O’Reilly, 1989; Laverty, 1996; Pfeffer, 1995; Pfeffer & Veiga, 1999). They work hard and use their managerial skills and abilities when an organization is growing up and stop working hard when the organization becomes successful. As a result, the performance of the organization diminishes (Bandura, 2012). So, consistency in the management ability and development of a good and efficient team is a long-term process and necessary for the success of every organization. A good managerial ability is the style of the managers, and this style should be as consistent as growth is necessary for the organization (Alam, 2022). Another aspect is consistency in decision-making. A good managerial ability is presented through the decisions of managers. These decisions are of many types, such as decisions about production, about purchase of raw materials in the off-season, hiring of staff, the shift of work and even these decisions relating to employees’ termination or the manager’s supporting team. In all types of decision, management role should be consistent (Jamalnia & Feili, 2013). A good manager with the ability to continuity in behaviour ensures that his action follows his words. It means if commitment is made on the part of management, it is important to follow that commitment at any cost.

Studies have recently examined the idiosyncratic impact of managers on organizational decisions (Bamber et al., 2010). According to the initial study by Bertrand and Schoar (2003), managers’ particular management philosophies impact operational and financial choices. The resource-based view hypothesis elaborates on the significance of managers and states that a company’s capacity to maintain its competitive advantage depends on its managers’ ability to use its resources efficiently (García-Meca & García-Sánchez, 2018; Holcomb et al., 2009). Another key to the firm’s success is the continuity and enhancement of MB in exploiting abilities. Therefore, permanent MB enhances the FP more than temporary MB regarding resource utilization.

Corporate risk-taking is necessary for a firm to survive, and more capable managers are more willing to take risks than less capable managers (Yung & Chen, 2018). As a result, managers’ willingness to take chances to explore investment possibilities enhances the company’s performance (John et al., 2008). To improve the FP, managers are mobilizing forces that make the most use of available resources and investment possibilities. The management pursues and takes advantage of investment opportunities that maximize value and help the company grow rationally. However, managers cannot take advantage of these opportunities due to a lack of resources (Naeem & Li, 2019). At this point, management’s task begins, since they can decide how to invest the available assets. Effective management is crucial to the success of the company and its expansion. The future of the company and the maximization of shareholder wealth depend on the effective, efficient and long-term use of resources. By identifying industry trends, accurately predicting product demand and investing in value-adding projects, managers with positive behaviour and abilities play a crucial part in achieving this goal (Lee et al., 2018). Managers with exceptional ability take chances, while managers with less exceptional ability do not (Yung & Chen, 2018). On the one hand, savvy managers take risks when they take advantage of investment possibilities with limited resources to contribute to profitability and value addition. On the other hand, they continue to play a significant role in strategic corporate choices and operational planning, which enhances long-term financial performance.

Corporate Governance (CG) and FP

CG mechanisms that drive higher FP have been extensively researched (Tanjung, 2020), but inclusive empirical results in the context of some emerging economies are still a challenge for researchers. CG is the main element contributing to FP, and poor CG practices harm shareholders’ interests and result in business failure (Li et al., 2021). A series of studies were carried out to investigate the influence of CG practices on FP and found that CG is an essential element for FP (Black et al., 2012; Cheung et al., 2011; Klapper & Love, 2004; Ullah & Kamal, 2022).

Mostly, researchers are on the same page that effective CG enhances FP, due to which agency issues between management and shareholders are minimized (Black et al., 2012; Cheung et al., 2011; Enache & Hussainey, 2020; Klapper & Love, 2004). Therefore, CG is a mechanism that protects the investors’ rights and minimizes the agency issue, which leads to FP. However, the determination of the measurement of CG is another problem for researchers, as no prominent measure is available in the literature (Aldamen et al., 2020). However, a CG index (CGI) is being used as a single measure and an emerging theme (Brown et al., 2011; Filatotchev et al., 2006). Therefore, the study uses a single measure of the CGI, measured by the board structure index, to pinpoint its influence on FP.

Ferriswara et al. (2022) discovered a strong link between sustained management success and firm profitability. However, little investigation has been conducted into the underlying mechanisms and environmental variables that affect this association. Juyumaya and Torres (2023) suggested that stable leadership teams display higher strategic consistency and employee engagement levels. There is not enough thorough research on how long-term effects affect corporate performance beyond financial measurements. Yang et al. (2023) highlighted the value of consistent leadership in resolving organizational crises. There is not enough study on how crisis management and managerial permanence interact. Klein et al. (2023) highlighted the importance of organizational memory and knowledge retention in companies with reliable management. Few studies evaluate how managerial permanence affects information transfer and learning methods.

Reviewing critical literature, the following hypotheses for this research have been developed to show the impact of management performance permanency on the performance of firms.

Hypothesis

H1: MB is positively associated with FP.

H2: MBP enhances the firm’s performance more than temporary MB in terms of utilization of skills.

H3: CGI positively affects the firm’s performance.

Research Methodology

Information asymmetry in emerging markets is common (Choe et al., 2005), for which managerial skills and abilities are essential in these economies. Therefore, the study aims to capture the influence of MB on FP listed on the stock exchanges of South Asian emerging economies (Pakistan, Bangladesh and India). A stratified random sampling is used to gather the data from listed non-financial firms on emerging economies’ stock exchanges. Emerging economies are classified into two strata (Next-11 and BRICS), and two South Asian economies (Pakistan and Bangladesh) are selected from stratum one (Next-11) and one South Asian economy (India) from the other stratum (BRICS). The data were gathered from 492 companies in the non-financial sector listed on the stock exchanges of Pakistan (PSX), India (NSE) and Bangladesh (DSE). The data have been collected from 200 companies listed on the Indian Stock Exchange, 195 on the Pakistan Stock Exchange and 97 companies have been listed on the Dhaka Stock Exchange. The data time frame is 11 years (2009–2019). So, the panel data have been taken into account.

Research Models and Statistical Techniques

To test the hypotheses statistically, the following research equations have been used.

The FP is measured by return on assets (ROA) and Tobin’s Q (TQ), MNB is for MB, CGI is represented by CGI. Control variables (Con) are firm size, firm age, leverage and sale growth for firm i and year t. The slope dummy (MNB*MBP) is a part of research equations, which has been used to differentiate the effect of MB and its permanency on FP. By following Aksar and Ahmed (2022), the CGI has been measured based on principal component analysis (PCA), and board size (BS), board independence (BI), and board meetings (BM) are part of this index.

In the study, panel data are applicable, due to which generalized methods of moments (GMM) are used to test the hypothesis, and lagged explanatory variables are taken as instrumental variables. Applying GMM is beneficial to address the issue of endogeneity and unobserved heterogeneity (Busch & Lewandowski, 2018; Tzouvanas et al., 2020).

First, the dimensions of BS, BM and BI are taken into consideration while creating the CGI, which is based on PCA. The corporations’ annual reports were used to compile information about BM, BS and BI. The metrics for FP are TQ (market-based proxy) and ROA (book-based proxy). The ratio of net profit to total assets is used to calculate ROA. TQ is calculated by dividing the total assets by the sum of the debt’s book value and the equity’s market value.

DEA, which estimates how well managers utilize the firm’s resources, is used to calculate management by objectives (Demerjian et al., 2013). DEA was initially developed for a study by Demerjian and McVay in 2012, and this method’s benefit is that it considers numerous inputs and outputs at once (Lee et al., 2018). Alternative metrics, like media citation on managers (Francis et al., 2008), industry-adjusted ROA, stock returns (Fee & Hadlock, 2003; Rajgopal et al., 2006) and pay for performance sensitivity, can be used to measure MB (Milbourn, 2003). These measurements, however, only consider characteristics related to managers and ignore important aspects of a corporation. Additionally, they influence perceived rather than actual MBs. However, Demerjian et al. (2012) measurement of MB based on DEA shows managerial performance in production with constrained resources as a function of managers’ experiences and psychological characteristics. By solving the following optimization [Eq. (3)], first, the firm efficiency has been determined (Park & Song, 2019), and then firm efficiency has been used in Eq. (4) to determine managerial efficiency (behaviour) from its residual values.

CGS stands for ‘cost of goods sold’, SGAE for ‘sales and general administrative expenses’, PPE for ‘property, plant and equipment’ and INT for ‘intangible assets and output’, all of which are considered inputs. v1, v2, v3 and v4 represent the optimal weights of corresponding inputs.

FE represents the firm efficiency obtained from Eq. (3), and then the residual values have been obtained by using Eq. (4) for the determination of managerial efficiency (behaviour). In Eq. (4), TA is for total assets, MS is for market share and FA is for firm age. BS represents the business segment, and FGNC represents the foreign currency translation. The source of data for these variables is S&P Global and Wharton Research Data Services (WRDS).

The second stage is the determination of the residuals from Eq. (4), which describes MB in terms of performance for each period t and each firm i. Following that, the necessity of managerial conduct, Jeong et al. (2018) and Noor et al. (2020) used this method to determine CSR permanence but was used to determine continuity (MBP). A dummy variable has been used to quantify management behaviour permanence (MBP), which is 1 if MB has occurred at least 3 times in the past 4 years. If not, the variable is 0. The study further used a slope dummy, that is (MB*MBP), the interaction of dummy variable and MB, to compare the effect of MBP with MB temporary in nature.

The introduction of control variables minimizes the bias of the results (García-Sánchez, 2020). Control variables in this study included firm size (as measured by the natural log of total assets), firm age (as measured by the natural log of years the company has been in business), sale growth, sale volatility (as measured by the standard deviation of the four most recent years of sales), slack (as measured by the ratio of cash to PPE) and leverage (debt to total asset). WRDS is where the data for the control and FP variables are collected.

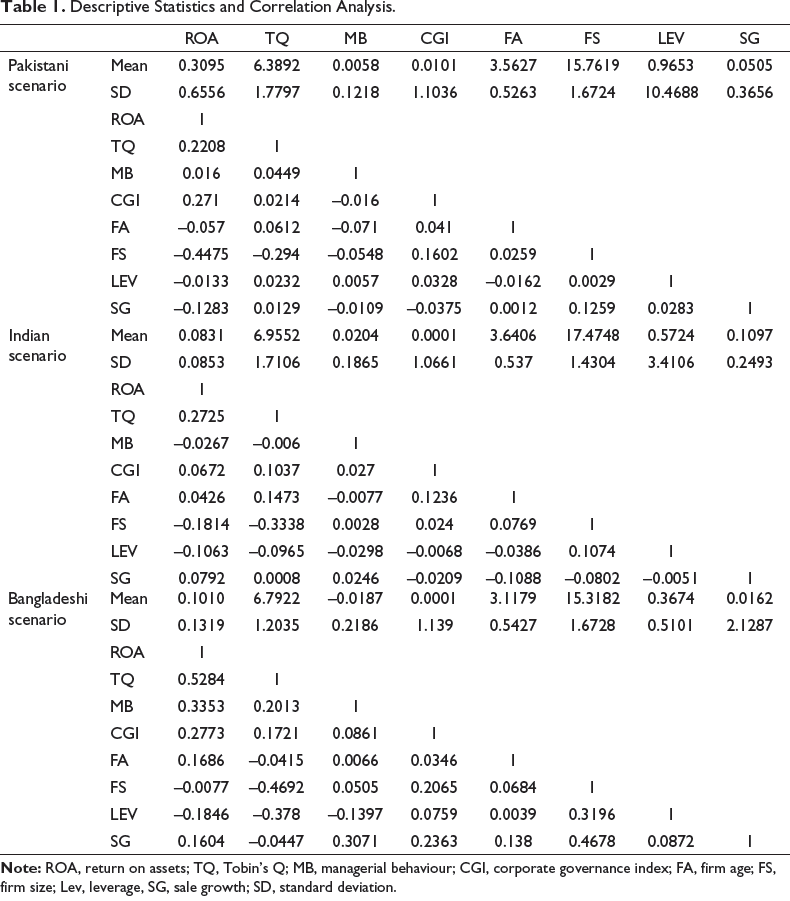

Descriptive Statistics and Correlation Analysis

Table 1 reports the descriptive statistics about the study variables in Pakistan, India and Bangladesh scenarios, respectively. The average FP measured by ROA is 30.95% in the Pakistani context, 8.9% in the Indian context and 10.10% in the Bangladeshi scenario. As depicted by the standard deviation values, these average values deviate more in Pakistan than in other economies. In all three countries, the average FP measured by TQ is from 6.3 to 6.9. The average MB in Pakistan is found as 0.0058, in India as 0.0204, and in the Bangladeshi scenario, it is seen as –0.0187. The CG measured by the board structure index (CGI) averages 0.0001 and 0.0101 in the scenario of all three countries. The findings also provide the scenario’s average value for control variables across all three emerging economies. To illustrate the average variance in the data of all variables across the time, the standard deviation values are also provided. The outcomes also display the connections between the various factors. In the Pakistan, India and Bangladesh scenario, there are only modest co-efficient correlations between the explanatory and control variables.

Descriptive Statistics and Correlation Analysis.

Descriptive Statistics and Correlation Analysis.

A high correlation between explanatory variables indicates the issue of multi-co-linearity (Hair et al., 2010). In our study, weak relationships between explanatory and control variables indicate no serious issue of multi-co-linearity in using all variables for further analysis.

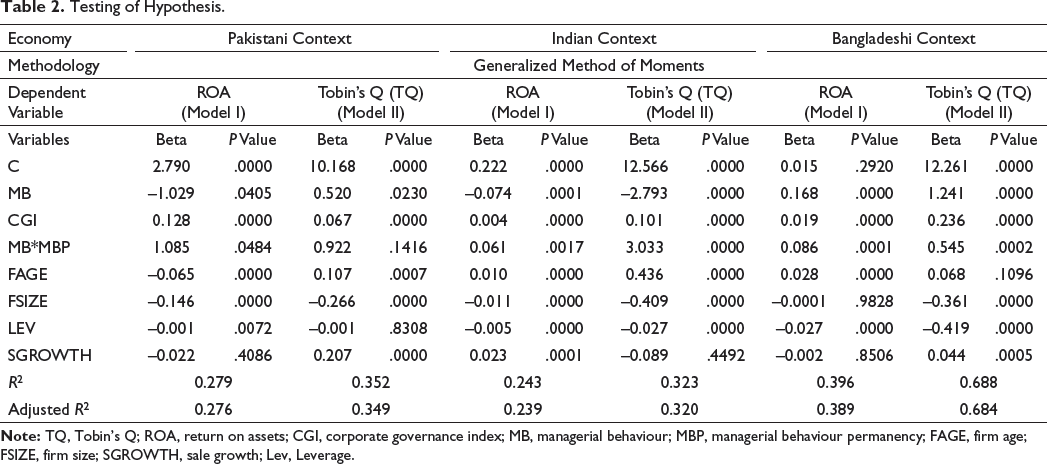

In Table 2, the results show the empirical status of the study’s hypothesis. In the context of all three emerging economies, the GMM was applied to address the problem of endogeneity and unobserved heterogeneity. Firm age, firm size, leverage and sale growth were used in Models (I and II) and all three emerging economies as control variables to minimize the biases in the results.

Testing of Hypothesis.

Testing of Hypothesis.

In the context of Pakistan, the results demonstrate that the explanatory power for Model I is 27.6% (adjusted R2 = 0.276), and for Model II is 34.9% (adjusted R2 = 0.349). MB influences the FP measured by the ROA negatively, but market measure TQ is influenced positively. However, the co-efficient of MB*MBP is found to be positive and significant (1.085, P value < .05) in Model I but positive and insignificant (0.922, P value > .05) in Model II. These results depict that MBP improves FP (ROA) more than temporary MB. Still, both types of MB do not change the FP (TQ) significantly.

In the context of India and Bangladesh, the MB influenced the FP significantly but negatively (–0.074, P value < .05 for Model I and –2.793, P value < .05 for Model II) in the Indian scenario and positively (0.168, P value < .05 for Model I and 1.241, P value < 0.05 for Model II) in the Bangladeshi scenario. CG measured by the board structure index (CGI) affects the FP (ROA and TQ) positively and significantly in India and Bangladesh. The co-efficient of MB*MBP in the context of both countries (India and Bangladesh) and for both models is positive and significant. These results show that MBP enhances FP (ROA and TQ) more than temporary MB in the scenario of these countries, proving that permanency matters. In all scenarios, it is clear from the slope dummy (MB*MBP) that MBP has a more positive influence on FP rather than MB temporarily.

The study’s findings align with the upper-echelon theory, which proposes that a firm’s corporate decisions and performance depend upon the managers’ characteristics and how they understand and interpret the condition of a firm (Hambrick, 2007). So, the managers’ characteristics affect the firm’s performance. According to the echelons theory, managers possess various not interchangeable cognitive characteristics, due to which, they take their own decision, especially in complex scenarios (Bamber et al., 2010). On the other side resource-based theory elaborates that the long-term competitive advantage is based upon the consistency in managerial efficiency (García-Meca & García-Sánchez, 2018), so the continuity in efficiency of managers plays an important role in improving the FP (Holcomb et al., 2009). The results of the study are supported by the upper echelons and resource view theories that MB, in terms of resource utilization, affects the FP. If they permanently utilize resources properly, they will contribute more positively to FP.

Conclusion and Research Implication

The purpose of the study is to compare the influence of MB performance and temporary MB on FP. DEA is used to measure the MB, and MBP was captured using a dummy variable with the value of 1 if MB is equal to or more than 3 times over the most recent 4 years and 0 otherwise. Furthermore, the comparison of the impact of MBP and temporary in nature on FP has been captured by using slope dummy, that is, interaction term of dummy variable for MBP and MB. The data were gathered from 492 companies listed on the stock exchanges of three South Asian emerging economies (Pakistan, Bangladesh and India). The results were obtained by applying the GMM to address the issue of endogeneity and unobserved heterogeneity. The results show that MB influences the FP positively in Pakistan and Bangladesh and negatively in India. Therefore, H1 is accepted partially. The empirical results support H2 and demonstrate that MBP enhances the FP more than temporary MB in terms of utilization of skills. CG measured by the board structure index (CGI) also affects the FP positively in the context of all three emerging economies, and these results support H3.

This research contributes to the existing knowledge about the relationship between MB and FP. Moreover, the study highlights the new term, that is, MBP, and captures its influence on FP. The results of the study are fruitful for policymakers to make effective policies and effective CG for the enhancement of MB permanently in terms of efficiency, which affects more positively than temporary managerial efficiency. The study also opens the door for researchers to conduct research about MBP.

The study was conducted only in the scenario of three economies (Pakistan, India and Bangladesh), and companies from the financial sectors of these economies are part of the study. The study introduces the new term, that is, MBP, and its influence on FP has also been captured. Therefore, this study allows researchers to work more on MBP. In future studies, the researchers may investigate the influence of MB and behaviour permanency on FP through financial reporting quality.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article.

Authors’ Contribution

Muhammad Aksar: Established conceptual framework, data analysis and interpretation.

Shoaib Hassan: Worked on literature review and hypotheses.

Javed Arshad: Worked on introduction, and helped in literature review and table setting.

Iftikhar Ali Janjua: Proof reading and helped in results discussion.

Ethical Declaration

We, the authors of this research paper, hereby declare that the study has been conducted in accordance with the highest ethical standards.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.