Abstract

For the past few decades, spin-offs have become a popular restructuring strategy among Indian businesses; however, there is little research on how the Indian market responds to this development. This article examines the effect of spin-offs on stock prices in the wake of the announcement of this event by employing the event study methodology. The results are based on 163 spin-off announcements of companies listed on the Bombay Stock Exchange over a 24-year period from 2000 to 2023. Using the market model, the study has identified positive cumulative abnormal returns of 3.32% during the days surrounding the spin-off announcement. Moreover, sector-wise returns are also examined, and it is found that all sectors react positively to the announcement of spin-offs, with the trading sector generating the highest cumulative returns of 7.03%. This study contributes to the limited literature on the effects of spin-offs on shareholders’ wealth in India by adopting a relatively longer period to include the influence of all corporate spin-offs since they became tax-free in 2000, testing the robustness of results through various parametric and non-parametric tests, which has not been done earlier in any of the limited studies conducted in the Indian context, and also enhancing the analytical depth of the results by performing a sector-wise analysis of these returns. These findings can assist corporate policymakers in considering spin-offs as a feasible strategy for increasing shareholders’ value. They may also affect the spin-off announcement timing since companies may want to take advantage of favourable market conditions. Besides, they could aid potential investors in their decision to invest in companies with spin-off prospects.

Introduction

Within the ever-changing realm of corporate strategies, companies constantly seek methods to improve productivity, simplify complex business models and increase shareholders’ value. The spin-off (also referred to as demerger) of unrelated business segments is one strategic approach that has gained popularity over time. This process helps diversified companies make the shift from highly diversified to pure-play businesses (Comment & Jarrell, 1995; Khorana et al., 2011). Besides, this strategic move is primarily intended to help a company get back on track with its core competencies, increase operational effectiveness and—above all—unlock shareholders’ value.

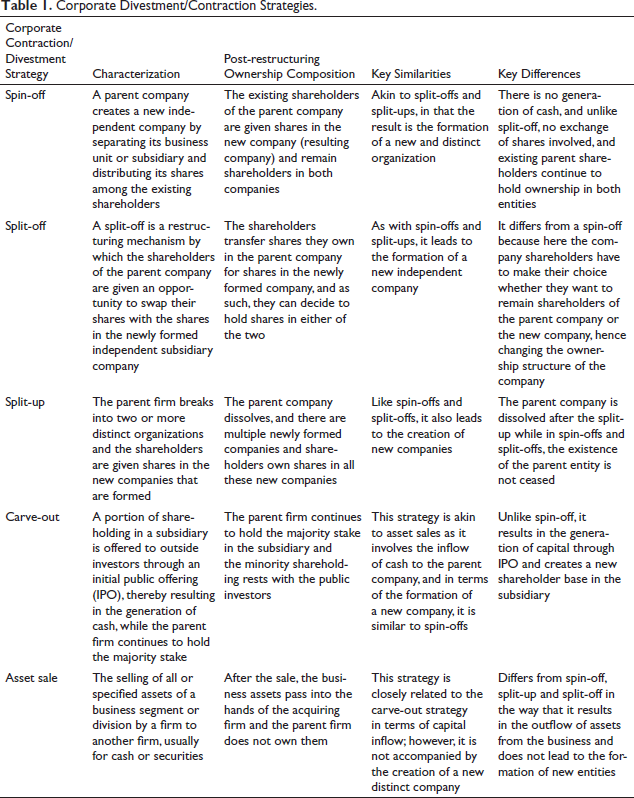

To reduce risk and take advantage of growth opportunities, conglomerates have historically frequently increased the size of their portfolios across a range of sectors and industries. This wide diversification, though, occasionally resulted in inefficiencies and lower returns for shareholders (Lord & Saito, 2019). As a result, the failure to achieve intended success through over-diversification urges the conglomerates to resort to corporate restructuring through contraction (Schweizer & Lagerströmb, 2020). This contraction can be accomplished through various restructuring strategies, namely spin-off, split-up, split-off, equity carve-out and asset sale (Brauer, 2006; Silva & Moreira, 2019), as summarized in Table 1. Typically, companies predominantly respond to their over-diversified model by implementing the strategy of spin-offs to eliminate non-core, unrelated business divisions (Owers & Sergi, 2021; Unifi Capital, 2022). This helps them focus management time, capital and resources on their core business operations, frequently resulting in increased competitiveness, superior financial performance and improved strategic alignment (Khaugani & Priscillah, 2020).

Corporate Divestment/Contraction Strategies.

Corporate Divestment/Contraction Strategies.

Apart from this, spin-offs offer a distinctive approach for diversified companies to separate their business units (Nazir & Chisti, 2023). Through this restructuring strategy, one or more business undertakings are transferred to a newly established or already existing corporate entity. The parent company’s shareholders retain ownership in the new company (also referred to as the resulting company) since the shares are allocated to them proportionately (Krishnaswami & Subramaniam, 1999). This method of corporate restructuring is tax-free, subject to the fulfilment of certain conditions, and does not result in any cash flows (Gertner et al., 2002).

Corporate spin-offs are the reverse and mirror images of corporate mergers (Hite & Owers, 1983). While mergers are corporate marriages, spin-offs are corporate divorces where some business divisions are separated for the benefit of the whole company. As far as mergers are concerned, the value is generated through positive synergy, whereas in the case of spin-offs, the value is generated through the elimination of negative synergy, also termed anergy (Fluck & Lynch, 1999).

Over several decades, spin-offs have evolved as a welcoming restructuring strategy by conglomerates to sharpen their focus and unlock their hidden value (Khorana et al., 2011). One of the earliest known spin-offs was the break-up of Standard Oil Co. in 1919, where 34 separate companies were formed (Library of Congress, n.d.; Pratt, 2012). Since then, the number of spin-offs all over the world has been growing, with North America majorly contributing to its growth (Figure 1) (Khorana et al., 2011; Morgan Stanley, 2023). The recent famous global spin-offs have been conducted by Novartis, which spun off its generic and biosimilar drug-making business as Sandoz (Reuters, 2023), and General Electric, which spun off its clean energy business as GE Vernova (Reuters, 2024). In India, corporate restructuring through spin-offs gained momentum from 2000 when it was declared tax-free (Ghosh, 2014). The first decade of the twenty-first century marked the dawn of spin-off activity in India, with famous spin-offs of Reliance Industries Limited (2005) distributing the business empire between the two Ambani brothers, and Larsen and Toubro (2004) separating its cement business to focus on its engineering and construction business. Over the past few years, many famous conglomerates in India, such as Pfizer Inc., Piramal Enterprises, Reliance Industries Limited and Forbes & Co., have also undertaken this contraction strategy to unlock their shareholders’ value and increase their operational efficiency.

Given the growing adoption of spin-offs by conglomerates as a corporate contraction method, this study examines the complex dynamics of this restructuring strategy, paying close attention to how this reorganization affects shareholders’ value. It attempts to disentangle the intricate relationship between the pursuit of pure-play strategies in the form of corporate spin-offs and shareholders’ value by examining 163 spin-offs that companies undertook between 2000 and 2023. The literature in this context is scant in India, as few studies have attempted to investigate the relationship between spin-off announcements and the market reaction. Moreover, there is no study to date to the best of the authors’ knowledge that has done a sector-wise analysis of market reaction to corporate spin-offs. Therefore, to contribute to the literature and address these gaps, the key research questions of this study are as follows:

Do corporate spin-offs in India create value for shareholders? How do different industrial sectors react to corporate spin-offs?

The primary contribution of this study is that it addresses a major methodological gap in the limited available research on corporate spin-offs in the Indian context. Compared to previous research studies that have mostly used simple t-tests to assess the effects of spin-offs on shareholders’ wealth, the present work utilizes various sophisticated and robust parametric and non-parametric significance tests generally used in the context of event analysis. Event study analysis is inherently challenging, especially in the event-date clusters where abnormal returns (AR) exhibit sectional correlation and event-induced volatilities cause distortions. To address these problems, a variety of significance tests, both parametric and non-parametric, are provided throughout the research works on event study hypothesis testing (Dutta, 2014). Moreover, the distribution of daily stock returns is more skewed than normal distributions due to their fat-tailed nature, emphasizing the application of non-parametric tests (Fama et al., 1969). Therefore, these tests provide a more comprehensive and robust examination of the market’s reaction to corporate spin-offs. Furthermore, the study’s sample period is drawn from 2000 to 2023, reflecting 24 years’ worth of data that effectively capture the changing face of corporate and financial structures in India; also, a sector-wise analysis is done to study if there is any difference in the market response to spin-offs across different industrial sectors.

This study fills a critical gap in both empirical scope and analytical depth in the Indian context by combining advanced statistical techniques with an extensive data set. Along with improving the methodological rigour of spin-off studies in India, it also provides deeper insights into the impact of spin-offs on shareholder returns across different sectors. This study will offer valuable insights for corporate executives, investors and academicians to comprehend the benefits and ramifications of spin-offs in the current fiercely competitive and quickly changing business world.

The rest of the study is structured as follows: The literature is reviewed in Section 2, the materials and methods used in this study are described in Section 3, the results are discussed in Section 4 and the study’s conclusion and implications are presented in Section 5.

The most common kind of corporate restructuring and inorganic growth models used by conglomerates worldwide to satisfy their growth cravings is the merger and acquisition of various companies (Buckley & Ghauri, 2002; Kumar & Kumar, 2019). However, since the 1980s, spin-offs have become an increasingly popular method of corporate restructuring (Dillow, 1996). The desire to divest unrelated businesses, the need to transform in a competitive environment, and pressure from shareholders are some of the main factors driving the growing number of spin-offs (Deloitte, 2018; Oliveira et al., 2023). According to Berger and Ofek (1995), diversification reduces value, and this reduction is more pronounced in industry diversifications that are unrelated. The shares of conglomerates are frequently found to trade at a price known as the ‘conglomerate discount’—a tendency of the market to undervalue the shares of diversified companies. A typical rationale for this behaviour is that investors pay more for companies that are separate entities than when they are parts of diversified firms because they are more likely to comprehend and analyze single-industry or ‘pure-play’ securities (Stern & Chew, 1998). Consequently, to recover this loss in value, companies must sharpen their focus by divesting non-core or unrelated business divisions (Comment & Jarrell, 1995), as it has been evidenced that spinning off unrelated units enables the management to concentrate on the business in which it has expertise (Daley et al., 1997; Ito, 1995; Jain et al., 2011). The markets’ optimism regarding the restructuring firm’s capacity to enhance its financial results manifests itself in the positive ARs surrounding spin-offs (Bhana, 2004).

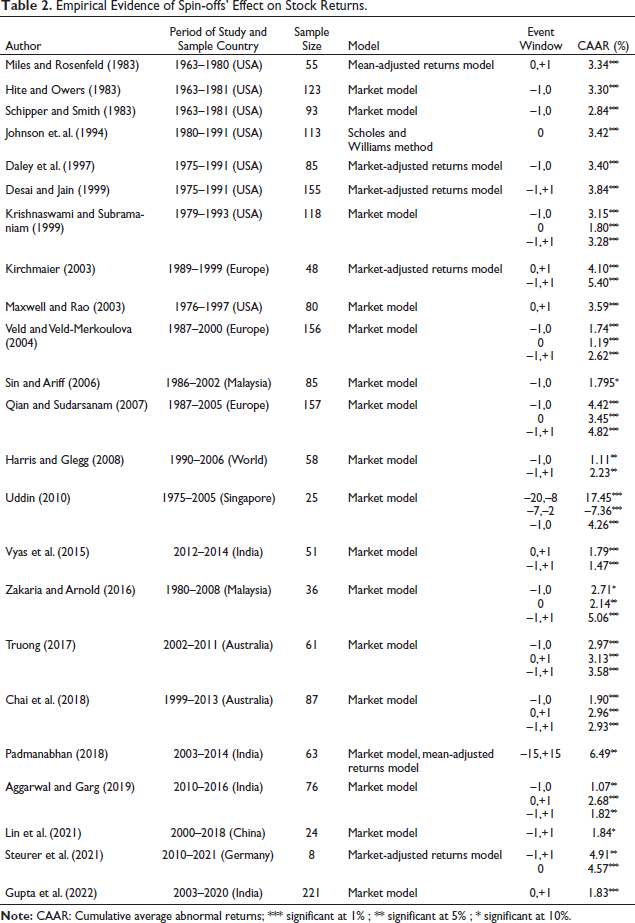

The academic literature provides an abundance of evidence demonstrating value generation for shareholders by spin-offs. A concise synopsis of earlier research on the effect of spin-off announcements on shareholder value can be found in Table 2. To mention a few, studies by Burch and Nanda (2003), Chai et al. (2018), Miles and Rosenfeld (1983), Parrino (1997) and Veld and Veld-Markoulova (2008) have documented positive stock returns around the spin-off announcement dates. The majority of research studies on the effects of spin-offs on shareholders’ wealth originate in the United States and Europe; however, lately, studies from Asia-Pacific have started to surface (Nazir & Chisti, 2023).

Empirical Evidence of Spin-offs’ Effect on Stock Returns.

Empirical Evidence of Spin-offs’ Effect on Stock Returns.

Miles and Rosenfeld (1983) carried out the first empirical study to examine the effect of spin-off announcements on stock prices. The study, which focused on 55 US companies that had spun off their divisions, found that spin-off announcements had a favourable impact on stock prices to the tune of 3.34%. The study ascribed the favourable returns to the spun-off division’s relative size and the removal of negative synergies. Similar findings were made by Schipper and Smith (1983), Johnson et al. (1994), Desai and Jain (1999), and Maxwell and Rao (2003) while examining the effects of US company spin-offs on stock prices over various time periods and found notable favourable returns ranging from 2.84% to 3.84%.

In the United Kingdom, a study was conducted by Murray (2008) to examine the market reaction to 60 spin-off announcements and found that while companies pursuing spin-offs receive some positive returns when they announce their plans to spin-off, there is no noteworthy response at the time of the spin-off. The study noted a comparatively small percentage of parent firms that received a positive response, emphasizing that debt lenders are more capable of affecting both the initial decision to spin off and the dissemination of any anticipated excess returns when bank debt predominates in parent companies. Similarly, McNeil and Moore (2005) investigated 153 spin-off events carried out in the United States and observed significantly positive returns. The findings demonstrated the inverse relationship between spin-off returns and the effectiveness of capital allocation to the units slated for divestiture, indicating the market’s faith in the spin-off’s ability to enhance capital allocation efficiency through restructuring. Building on these findings, Zakaria and Arnold (2016) probed 36 spin-offs accomplished in Malaysia over a period of 28 years from 1980 to 2008 and contended the outperformance of the stocks of the engaged firms around the spin-off announcement. The outperformance of the stocks was found to be associated with the political linkage of the firms (i.e., informal ties of the firms with the leading politicians of the country). Similarly, a market intelligence report by S&P Global in 2017, based on 516 and 666 spin-offs carried out during the periods 1989–2015 and 1993–2015 in the United States and international markets, respectively, established that spin-offs in the United States as well as international markets outperform their industry peers. Turning to a different demographic and economic structure, Lin et al. (2021) investigated the wealth effects of spin-offs in China by examining 24 spin-off announcements made from 2000 to 2018. The study noted that, despite being a socialist market economy, the reaction of Chinese markets to the spin-off announcements is similar to that of the private capital economies; that is, spin-offs receive a positive reaction from the markets, leading to positive returns around the announcement date.

Indian Studies

In India, Padmanabhan (2018) investigated a sample of 63 spin-offs from 2003 to 2014 to gain insights into whether the spin-off announcements affect the wealth of shareholders and established that the Indian markets positively reacted to this corporate move. The findings of this study were upheld by Aggarwal and Garg (2019), who examined 76 firms that underwent spin-offs during 2010–2016 and noticed impressive returns to the shareholders around the release of news about the spin-offs. Expanding on these findings, Gupta et al. (2022) analyzed a bigger sample of 221 spin-offs and noted significant positive returns to the tune of 1.35% on the day following the announcement of the event.

In summary, the extant literature indicates that spin-off announcements typically elicit a favourable response from the stock market, leading to a rise in shareholder wealth. The aforementioned review makes it clear that although spin-off announcements have been the subject of a great deal of literature overseas, particularly in the United States, minimal research has been done on them in the Indian context until recently. This deficiency in literature is also highlighted in the systematic literature review of the effects of corporate spin-offs on stock prices by Nazir and Chisti (2023), who underscore the abundance of spin-off research in the developed economies, particularly in the United States and Europe, and call for further investigation in emerging economies to gain deeper insights into how markets around the globe react to this type of corporate restructuring.

Considering the unique dynamics of the Indian stock market, the inadequacy of research in this context cannot be addressed by merely extending the findings from developed economies to the Indian market. The stock market in India exhibits distinct characteristics in terms of investor sentiments (Chakraborty & Subramaniam, 2020; Jana, 2016), policy uncertainty (Aggarwal & Saradhi, 2023; Das et al., 2019), investor composition (Syamala et al., 2014; Tayde & Rao, 2011; Vijaya, 2014) and volatility (Ahmed et al., 2018; PH & Rishad, 2020). Consequently, this distinct nature of the market underscores the importance of monitoring the investors’ response to the conglomerates’ spin-off strategy in India. Therefore, this study attempts to add to the scant body of knowledge regarding the impact of corporate spin-offs on stock returns in Indian markets. Moreover, the currently available literature lacks a sector-wise analysis of the market’s reaction to corporate spin-offs. The significance of sector-wise analysis of corporate events has been highlighted by empirical studies that have shown differing sector-wise market reactions across a range of markets and corporate events (Al-Khasawneh & Essaddam, 2012; Gupta, 2017; Mian & Sankaraguruswamy, 2012; Pandow & Butt, 2018; Rao & Reddy, 2015; Tawatnuntachai & D’Mello, 2002). Consequently, this study attempts to fill this gap by examining the ARs generated in response to this event by various sectors. Furthermore, the few studies conducted in India that were previously covered in this review (Aggarwal & Garg, 2019; Gupta et al., 2022; Padmanabhan, 2018) have not employed the robust and advanced econometric test that is imperative to improve the reliability of the results of an event study analysis (Brown & Warner, 1980; Fama et al., 1969). Therefore, to enhance the methodological rigour of the Indian spin-off studies, this study employs an advanced methodology to investigate the ARs consequent to this corporate restructuring strategy.

Materials and Methods

Data

The list of spin-offs of companies has been taken from the Bombay Stock Exchange (BSE), as in comparison to the National Stock Exchange (NSE), it has a large number of companies listed on it; by the end of 2023, BSE has over 5,300 listed companies, while NSE has around 2,300 listed companies. This larger number of listed companies in BSE allows for a more comprehensive and representative sample for our research.

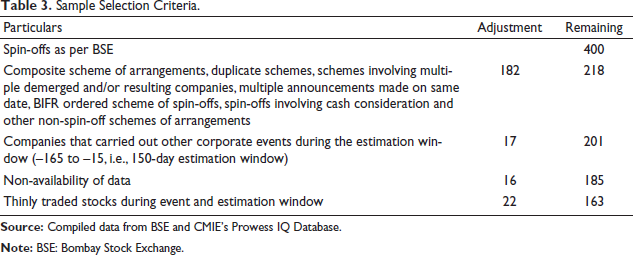

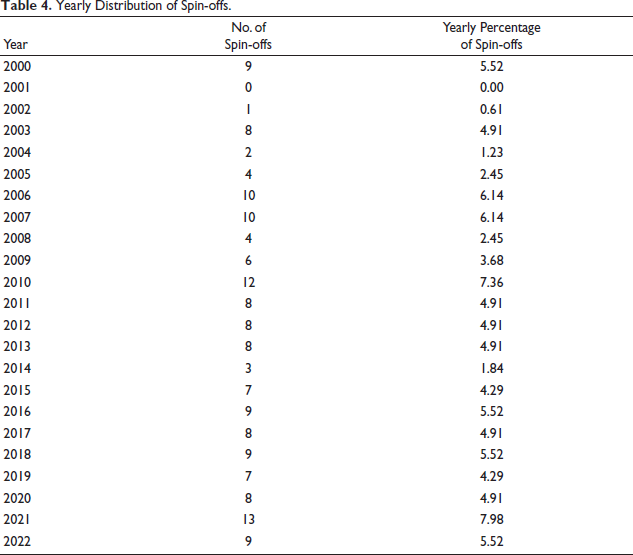

Listed companies that have announced spin-offs from 2000 to 2023 have been considered. The beginning of the sample period has been taken as 2000, as spin-offs got daylight only after 2000, when they were declared tax-free under the Finance Act, 2000, subject to the fulfilment of certain conditions. As per the records, 400 spin-offs have been announced during the sample period. The sample filtration used to obtain the final sample of 163 spin-offs examined in this study is displayed in Table 3. The yearly distribution of spin-offs is presented in Table 4. In our analysis, the event date is the announcement date, which is the day on which the stock exchange is informed of the approval of the spin-off by the board. The announcement dates are extracted from the CMIE Prowess IQ database and manually cross-checked against the BSE’s corporate announcements archive section. The daily stock price data of the individual securities of the sample have been obtained from CMIE Prowess and to capture the market movement, the S&P BSE Sensex index has been considered.

Sample Selection Criteria.

Sample Selection Criteria.

Yearly Distribution of Spin-offs.

Market efficiency theory suggests that stock prices take into account all pertinent information to which traders in the market have access. Should this be accurate, then stock prices will promptly reflect any newly disclosed financial information that affects investors’ decisions. Thus, anything that produces newly pertinent information is considered an event. Being a corporate event, a market reaction is anticipated in the case of a spin-off.

The finance literature has broadly recognized and employed the event study methodology to ascertain the fluctuation of stock prices around the event. The body of existing research makes clear that the event study methodology is the accepted approach for examining how spin-off announcements affect stock price behaviour (Binder, 1998; Nazir & Chisti, 2023).

The semi-strong form of the efficient-market hypothesis serves as the theoretical foundation for event study analysis. According to this theory, stock prices reflect all information that is accessible to the public. It offers a useful mechanism for assessing business events such as mergers, spin-offs and other corporate events (Cox & Portes, 1998). Event study analysis makes it possible to value new information by attributing otherwise inexplicable changes in stock prices to it, and consequently, these prices offer the most accurate assessment of how these unforeseen announcements fluctuate the valuation of a company (Cortés et al., 2015). Accordingly, the standard event study methodology, as described by MacKinlay (1997), has been employed in this investigation, and the analyses are carried out using Stata 17.0.

Event Study Analysis

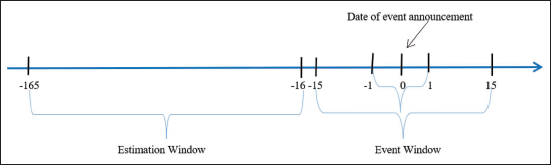

The date the stock exchange is notified that the board has approved the spin-off will be referred to as ‘day 0’ and will serve as the event date. In case the day of notification is not a trading day, ‘day 0’ will be the first trading day immediately after the stock exchange is notified.

To determine whether there are any notable ARs in the event window, the present study intends to analyze the returns under an event window of 31 days, starting from 15 days before the spin-off announcement and ending 15 days after the announcement, including day 0, the day of the announcement (refer to Figure 2).

Graphical Presentation of Event and Estimation Windows.

Graphical Presentation of Event and Estimation Windows.

Stock returns can either be simple returns or log returns (continuously compounded returns). When compared to simple returns, many event studies favour log returns (Fama et al., 1969; Kliger & Gurevich, 2014; Padmanabhan, 2018). The advantage of using log-transformed returns is that negative values are removed, and the distribution’s normality is enhanced. In this study, log returns have been used. So, the model is:

The above equation is a time-series regression executed for each firm’s stock in the sample, where LogeRit = ln [(Pt)/(Pt–1)] representing the natural log of continuously compounded rate of return on the firm I’s stock on day t through the estimation window, where Pt is the adjusted closing price on the day ‘t’ and Pt–1 is the adjusted closing price on day ‘t–1’.

LogeRmt = ln [(It)/(It–1)] representing the natural log of the continuously compounded rate of return on the market index (S&P BSE Sensex) on day t through the estimation window, where It is the S&P BSE Sensex closing price on day ‘t’ and It–1 is the S&P BSE Sensex closing price on day ‘t–1’.

βi represents the firm’s beta, that is, the sensitivity to market movements.

αi represents the security i’s return when the market return is zero.

εit is the security i’s error term at time t.

The daily abnormal returns are determined as:

where

ARit is the abnormal return of security I at time t.

Rit is the natural log of continuously compounded rate of actual return of security I at time t.

rit is the natural log of continuously compounded rate of normal or expected return of security.

I at time t determined using the model-estimated parameters.

The average abnormal return (AAR

t

) of all the sample firms on day t during the event window is determined using the below formula:

where

AR it stands for the security i’s AR at period t.

N represents the total number of sample firms.

The final step in the event study analysis application is the estimation of cumulative average abnormal returns (CAAR), which are expected to demonstrate the collected reaction of the market to the corporate event.

where

CAAR s,T represents the cumulative sum of average abnormal returns during the period s to T.

AAR t represents the estimated average abnormal returns at period t.

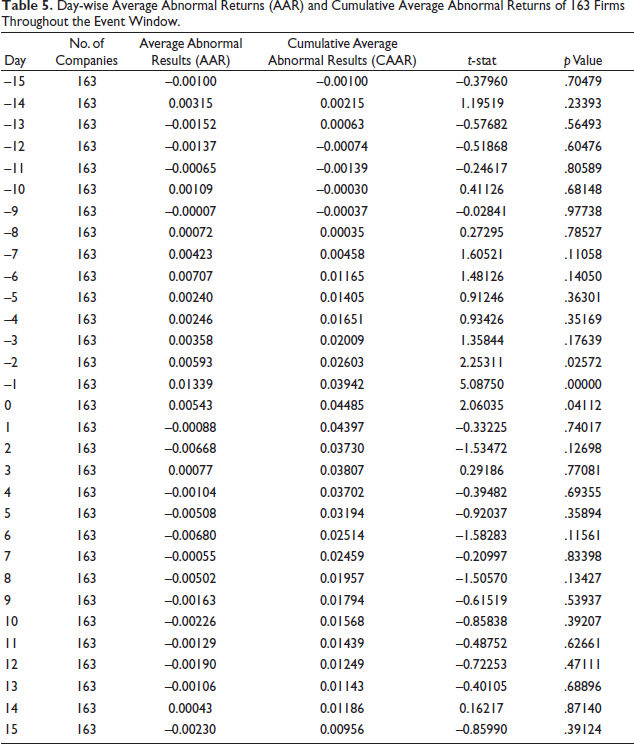

Table 5 displays the AAR earned by the shareholders of the 163 companies that announced spin-offs during the event window of 31 days, comprising 15 days prior to the spin-off announcement, the day of announcement and 15 days post the announcement of the corporate event. Along with AAR, CAARs have also been determined to see the aggregate unusual returns yielded by the stocks. It is evident from the table that returns are highest on day –1, that is, 1.34% positive ARs with a t-stat of 5.09, showing significance at the 1% level. After day –1, another day that yields higher returns is day –2, with a favourable return of 0.59% at the 5% significance level with a t-stat of 2.25. The spin-off announcement day (day 0) generates a return of 0.54% at a 5% level of significance, having a t-stat of 2.06.

Day-wise Average Abnormal Returns (AAR) and Cumulative Average Abnormal Returns of 163 Firms Throughout the Event Window.

Day-wise Average Abnormal Returns (AAR) and Cumulative Average Abnormal Returns of 163 Firms Throughout the Event Window.

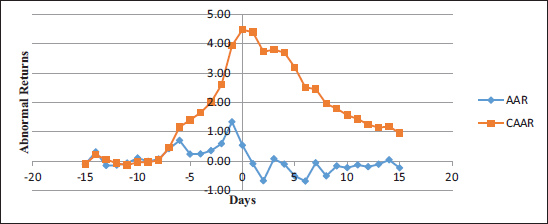

Post the announcement day, the stocks of the event firms yield comparatively decreasing returns, and these returns are statistically insignificant. This suggests that even prior to the formal announcement of the spin-off, information about it may have a bearing on the parent company’s share prices. This impact on stock price movements can be attributed to leakage of information prior to the official market disclosure, as publicly traded companies usually notify the stock exchanges whenever a board meeting to discuss a proposed spin-off is planned. Thus, it seems that the market anticipates the approval of the board in favour of the spin-off, responds to this information and factors the expectations into the stock prices. The results in Table 5 are represented graphically in Figure 3.

Daily Average Abnormal Returns (AAR) and Cumulative Average Abnormal Returns (CAAR) of 163 Firms Throughout the Event Window.

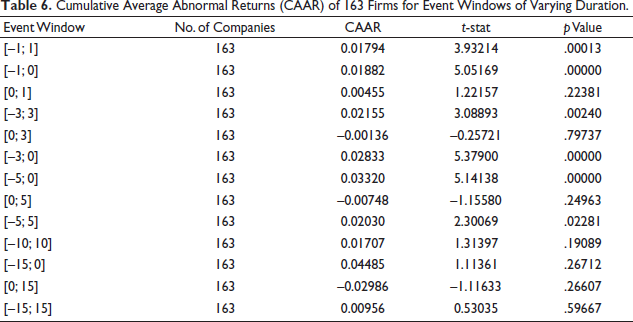

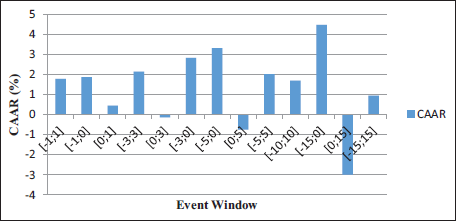

Further, Table 6 represents the CAARs investigated for various event windows of varying durations. The highest cumulative returns of 3.32% are yielded during the event window [–5;0], which are significant at 1% significance level. Event windows of [–3;0], [–3;3], [–5;5], [–1;0] and [–1;1] also generate favourable returns of 2.83%, 2.15%, 2.03%, 1.88% and 1.79% respectively, significant at 1% and 5% significance levels. These results are in conformity with Chai et al. (2018), Gupta et al. (2022), Krishnaswami and Subramaniam (1999), and Lin et al. (2021) and reflect the favourable market response and signify that the market perceives the spin-offs as a value-creating strategic move by the companies. The substantially favourable results may also indicate the confidence of investors in spin-offs as a means of better allocation of resources (McNeil & Moore, 2005) and improving corporate governance in the form of new transparent and autonomous management (Ahn & Walker, 2007). Figure 4 shows a graphic representation of the outcomes in Table 6. Moreover, the positive returns of 4.48% and 1.71% are also exhibited by other windows like [–15;0] and [–10;10] respectively, but these are statistically insignificant. Apart from positive yields, the post-event windows such as [0;3], [0;5] and [0;15] demonstrate statistically insignificant negative returns. These insignificant unfavourable returns following the announcement could indicate that the market had already factored in the information, leading to no further significant adjustment after the event announcement. The findings of this study are comparable with the results of Aggarwal and Garg (2019), Harris and Glegg (2008), Steurer et al. (2023) and Truong (2017).

Cumulative Average Abnormal Returns (CAAR) of 163 Firms for Event Windows of Varying Duration.

Cumulative Average Abnormal Returns (CAAR) of 163 Firms for Event Windows of Varying Duration.

Aggarwal and Garg (2019) evaluated 76 firms that announced spin-offs and discovered notable gains on the day of the announcement as well as one day prior to and one day following the announcement. In their study of 58 cross-border spin-offs, Harris and Glegg (2008) sought to determine whether the market response to spin-offs involving foreign subsidiaries differs from that for spin-offs involving same-country subsidiaries. They discovered that similar to same-country spin-offs, spin-offs involving foreign subsidiaries also produce sizable returns around the announcement period. Steurer et al. (2023) examined 24 firms that underwent spin-offs in Europe and recorded aggregate ARs varying between 2.63% and 4.84% across various event windows. Similarly, in the Australian context, Truong (2017) looked into how spin-offs affected stock prices by evaluating 61 spin-offs and discovered that the market reacted favourably to this divestiture strategy.

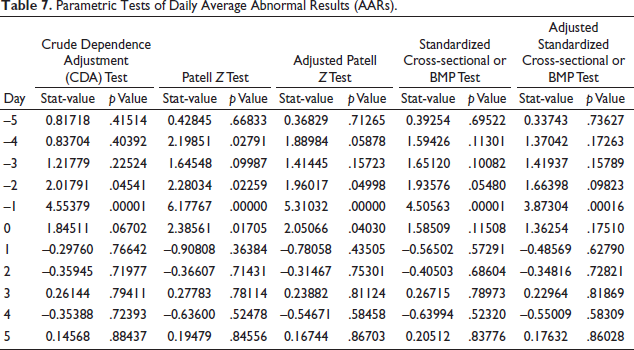

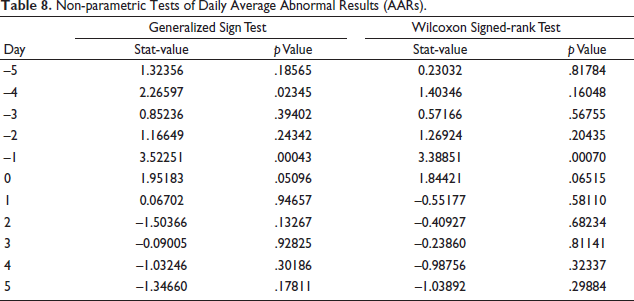

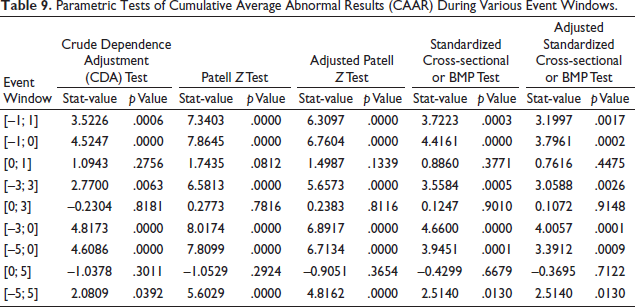

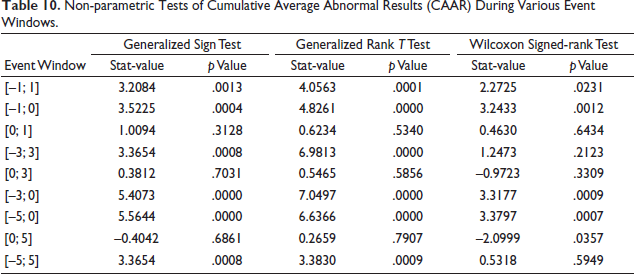

In general, event studies are challenging, especially in the event-date clusters where ARs have sectional correlation and event-induced volatilities cause distortions. To address these problems, a variety of significance tests are provided throughout the research works on event study hypothesis testing and are generally grouped into parametric and non-parametric significance tests (Dutta, 2014). Moreover, the distribution of daily stock returns is more skewed than normal distributions due to their fat-tailed nature, making the application of non-parametric tests essential (Fama et al., 1969). Therefore, to ensure the robustness of results, researchers have frequently employed both parametric and non-parametric tests, taking into account the various statistical properties and assumptions of these tests (Ahmed et al., 2023; Riley et al., 2017). Consequently, the present study has employed various parametric tests such as the crude dependence adjustment (CDA) test (Brown & Warner, 1980), Patell Z test (Patell, 1976) and similar other tests (see Table 7 for daily AAR and Table 9 for window-wise CAAR) as well as non-parametric tests such as generalized sign test (Cowan, 1992) and other accepted tests (see Table 8 for daily AAR and Table 10 for window-wise CAAR) to determine whether the returns abnormal are statistically significant. These tests also confirm the robustness of the results presented in Tables 5 and 6.

Parametric Tests of Daily Average Abnormal Results (AARs).

Non-parametric Tests of Daily Average Abnormal Results (AARs).

Parametric Tests of Cumulative Average Abnormal Results (CAAR) During Various Event Windows.

Non-parametric Tests of Cumulative Average Abnormal Results (CAAR) During Various Event Windows.

The pace at which the market embodies the event’s information content into the stock price is measured to determine the efficiency of the stock markets in India. There are notable ARs during the 2 days immediately preceding the event announcement, that is, on day –1 and day –2, and also on the announcement day itself. The period of 2 weeks subsequent to the announcement day exhibits no notable significant returns. These findings exhibit the promptness of the market in capturing the newly released information and lead to the conclusion that the Indian stock market responds swiftly to spin-off announcements and demonstrates a semi-strong form of efficiency. These results corroborate the findings of Padmanabhan (2018) and Vyas et al. (2015), who also confirmed the semi-strong efficiency of the Indian stock market.

A sector-wise analysis of corporate events is necessary to comprehend how the market reacts to these events, as different sectors have distinct growth prospects, risk profiles, regulatory environments, investor expectations and competitive dynamics. Empirical studies across a variety of markets and corporate events have exhibited varying sector-wise market reactions (Al-Khasawneh & Essaddam, 2012; Gupta, 2017; Rao & Reddy, 2015; Mian & Sankaraguruswamy, 2012; Pandow & Butt, 2018; Tawatnuntachai & D’Mello, 2002), thereby underscoring the importance of sector-wise analysis of corporate events. Following this, the present research attempts to examine the response of the market to spin-off announcements across different sectors.

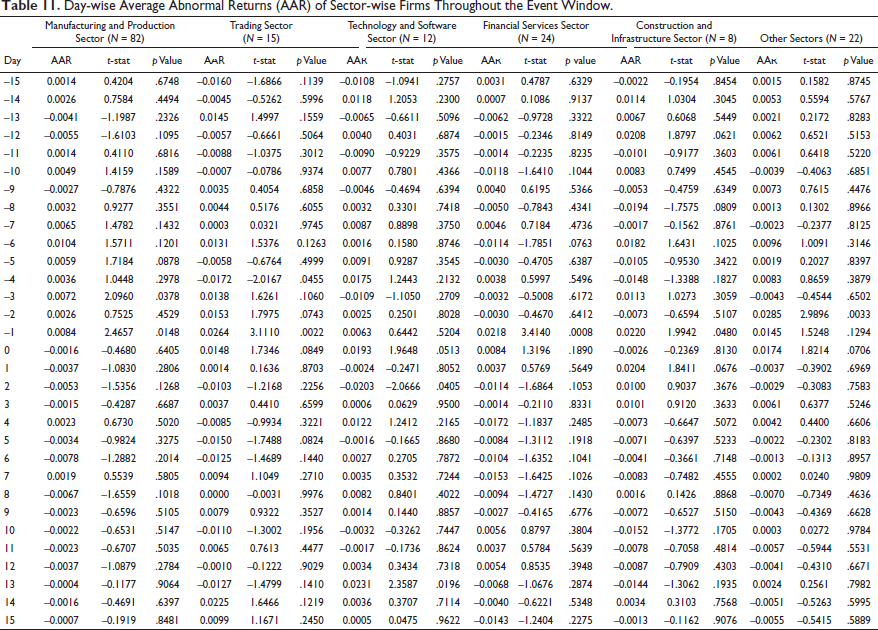

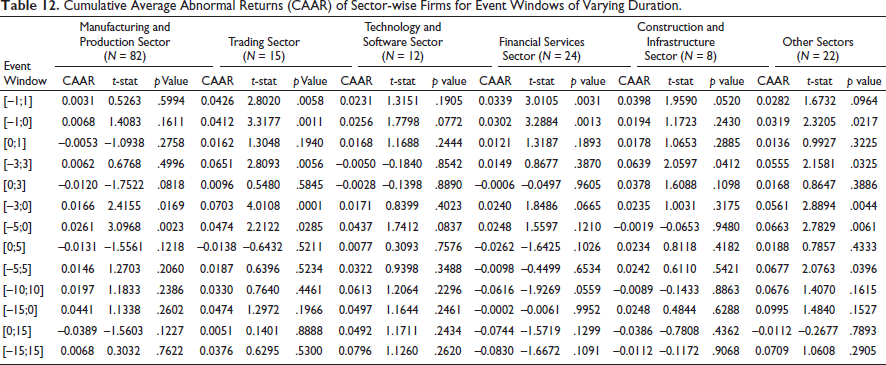

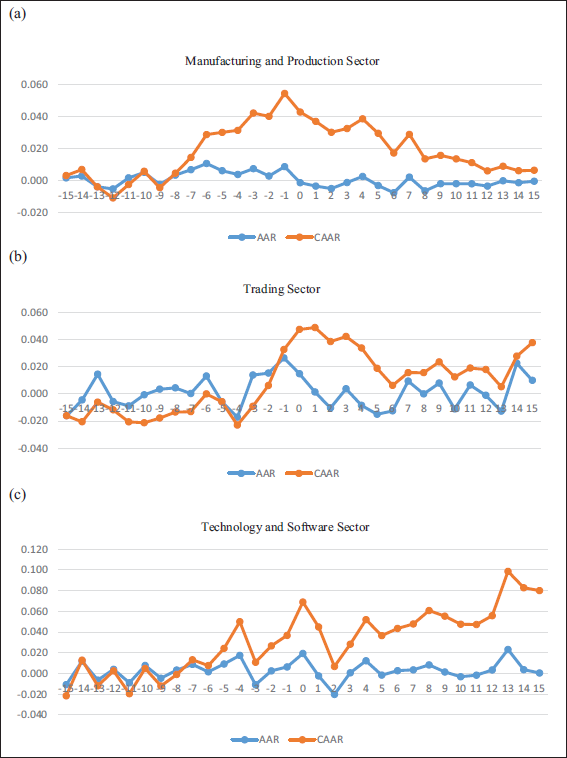

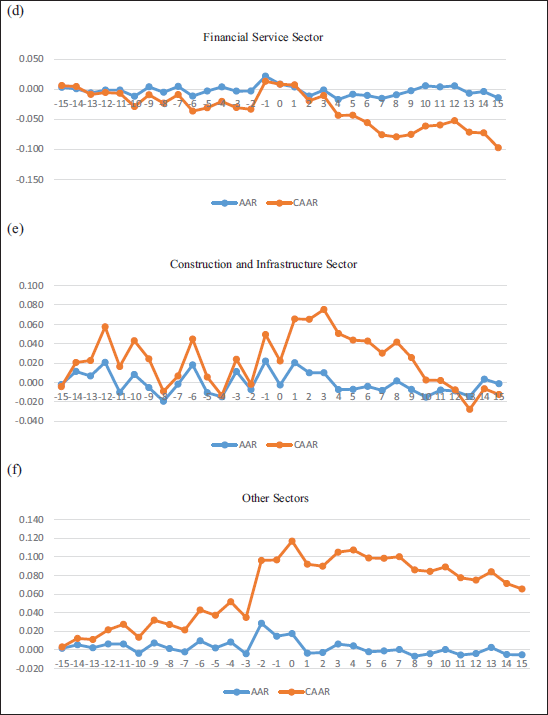

Tables 11 and 12 present the AARs and CAARs, respectively, earned by shareholders during the selected event window across six different sectors, namely manufacturing and production, trading, technology and software, financial services, construction and infrastructure, and other sectors.

Day-wise Average Abnormal Returns (AAR) of Sector-wise Firms Throughout the Event Window.

Day-wise Average Abnormal Returns (AAR) of Sector-wise Firms Throughout the Event Window.

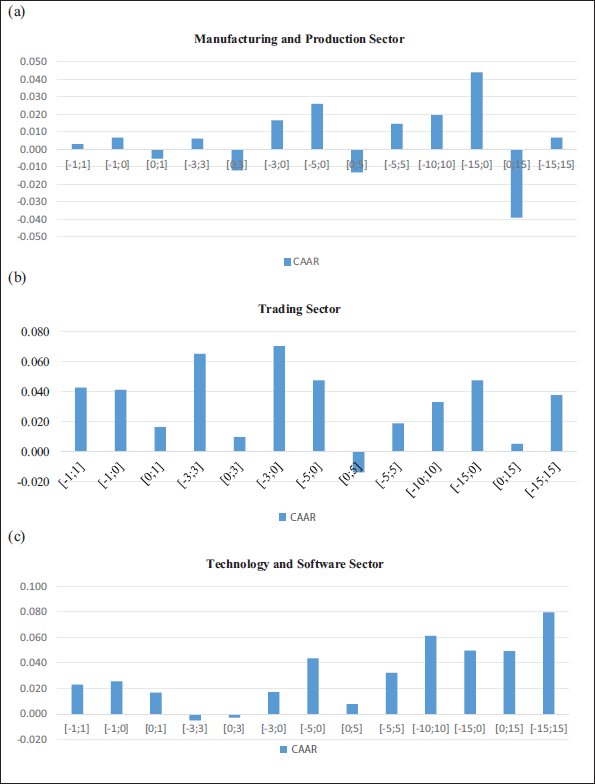

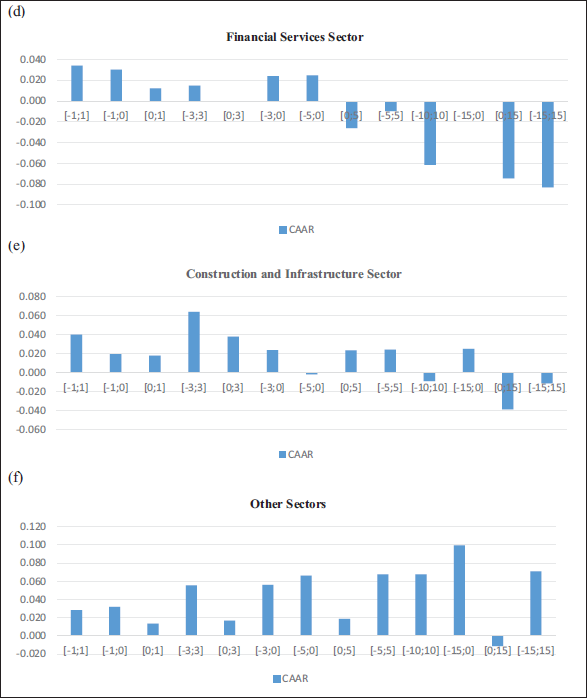

Cumulative Average Abnormal Returns (CAAR) of Sector-wise Firms for Event Windows of Varying Duration.

It is noted that, on average, all the sectors react positively to the corporate spin-offs in India, with varying levels of returns. The highest significant AARs of 2.85% are generated by the residual sector, that is, the other sector, on the event announcement day, followed by the trading sector, which generated 2.64% returns on day –1. In the financial service and construction and infrastructure sectors, the substantial positive returns to the tune of 2.18% and 2.20%, respectively, are earned on the day immediately preceding the announcement day. The technology and software sector also reports positive returns of 1.93% on the event announcement day, significant at 10% level, followed by subsequent negative returns of 2.03% on day –2. Among all the sectors, the lowest daily returns are generated by spin-offs in the manufacturing and production industry, where 0.72% and 0.84% AARs are reported on day –3 and day –1, respectively. Figure 5(a)–(f) shows the graphical representation of sector-wise AARs.

(a) Daily Average Abnormal Returns (AAR) and Cumulative Average Abnormal Returns (CAAR) of 82 Manufacturing and Production Sector Firms Throughout the Event Window. (b) Daily AAR and CAAR of 15 Trading Sector Firms Throughout the Event Window. (c) Daily AAR and CAAR of 12 Technology and Software Sector Firms Throughout the Event Window. (d) Daily AAR and CAAR of 24 Financial Service Sector Firms Throughout the Event Window. (e) Daily AAR and CAAR of 8 Construction and Infrastructure Sector Firms Throughout the Event Window. (f) Daily AAR and CAAR of 22 Other Sector Firms Throughout the Event Window.

As far as CAARs are concerned, it is evident from Table 12 that spin-offs of companies in trading sector yield the highest CAARs of 7.03%, followed by the other sectors, which give rise to cumulative returns of 6.6%. The trading sector’s superior returns indicate the investors’ confidence in its spinning-off, as trading companies are characterized by better flexibility and less capital requirements; therefore, separating the business divisions allows for better utilization of resources and increased business focus, which improves growth prospects and yields higher returns. The remaining sectors, like construction and infrastructure, financial services, technology and software, and manufacturing and production, also generate substantial favourable aggregate returns of 6.39%, 3.39%, 4.37% and 2.61%, respectively. The construction and infrastructure sector usually involves heavy capital investments, and spin-offs in this industry might imply the detachment of a poorly performing or highly capital-intensive project, which could consequently boost the growth of the business and therefore draw in investors’ interest. As far as the financial services and technology and software sectors are concerned, they often operate in rapidly evolving and competitive markets, and the moderate returns in these sectors reflect the cautious optimism of investors regarding their growth potential. The lower returns in the manufacturing and production sector could be attributed to the capital-intensive nature and prolonged gestation period of this industry, which can make investors sceptical about the ability of the firms to substantially improve their performance in the near future. CAARs of all the six sectors are graphically presented in Figure 6(a)–(f).

(a) Cumulative Average Abnormal Returns (CAAR) of 82 Manufacturing and Production Sector Firms for Event Windows of Varying Duration. (b) CAAR of 15 Trading Sector Firms for Event Windows of Varying Duration. (c) CAAR of 12 Technology and Software Sector Firms for Event Windows of Varying Duration. (d) CAAR of 24 Financial Services Sector Firms for Event Windows of Varying Duration. (e) CAAR of 8 Construction and Infrastructure Sector Firms for Event Windows of Varying Duration. (f) CAAR of 22 Other Sectors Firms for Event Windows of Varying Duration.

The varying returns highlight disparities in market dynamics across different sectors. Overall, the results demonstrate favourable responses of all sectors towards this contraction strategy of companies and indicate the acceptance of spin-offs as a method to unlock the value of shareholders.

There is a wealth of literature on the impact of spin-offs on stock prices in developed nations like the United States and Europe, but it is scarce in the context of developing economies like India. The Indian market differs from developed markets in terms of investor behaviour, including trading patterns, risk appetite and investment preferences, due to differences in cultural and demographic factors. As a result, conclusions drawn from research on developed markets cannot be applied to the Indian market. Therefore, this study attempts to better understand how Indian investors respond to corporate spin-offs and add to the scant literature in this domain by examining the spin-offs conducted over a far longer period of 24 years. The results based on 163 spin-offs announced between 2000 and 2023 exhibit notable favourable returns around the event announcement date, depicting the investors’ faith in spin-offs as a value-creating strategic move capable of reducing negative synergy and unlocking hidden value. The highest returns are 1.34%, which have been observed on day –1, and the highest cumulative returns of 3.32% have been recorded during the event window [–5;0]. These findings are consistent with studies in developed and emerging nations (Chai et al., 2018; Harris & Glegg, 2008; Lin et al., 2021; Steurer et al., 2021; Truong, 2017; Zakaria & Arnold, 2016). Moreover, unlike other studies in the Indian context that have only used the t-test to assess the significance of detected ARs, this study has added to the body of literature by employing widely accepted advanced parametric and non-parametric significance tests recommended in the literature on event study methodology to ensure the robustness of the results. Furthermore, the returns are further investigated sector-wise to comprehend the response of different sectors to this strategy, and it is concluded that spin-off leads to the generation of favourable returns of varying degrees across all sectors and is regarded as a value-unlocking contraction strategy.

Some implications flow from this study. It contributes to the limited literature on the effects of spin-offs on shareholders’ wealth in the Indian context by adopting a relatively longer study period to include the influence of all corporate spin-offs since they became tax-free in 2000 and also by enhancing the analytical depth of the results by performing a sector-wise analysis of the returns. Furthermore, the few research studies conducted in India on this topic have not used sophisticated tests of hypotheses in event studies to verify the robustness of their findings. In an effort to get around this restriction, the study examines the significance of ARs by employing various well-established parametric and non-parametric hypotheses tests and concludes that the markets respond favourably to this corporate divestiture strategy. Moreover, the findings of this research can assist corporate policymakers in considering this type of corporate contraction as a feasible strategy for increasing shareholders’ value and increasing their focus on core operations. These findings may also affect the spin-off announcement timing, since companies may want to take advantage of favourable market conditions. Additionally, a sector-wise analysis demonstrated disparities in returns across different sectors, highlighting the differing market dynamics of each sector. Accordingly, firms must tailor their spin-off strategies based on industry-specific dynamics. For instance, trading and construction firms should emphasize how spin-offs will drive growth, while technology and manufacturing firms should address concerns about synergies and operational stability. Furthermore, knowing the wealth creation potential of spin-offs, regulators can streamline the compliance framework to facilitate this restructuring process while safeguarding the shareholders. Besides, the findings could also assist potential investors in their decision to invest in diversified conglomerates with spin-off prospects that could unlock their value.

Similar to other research articles, the study also has a few limitations. This study has employed the market model, which is adopted by a majority of the event studies to identify ARs (Nazir & Chisti, 2023); however, there are some other models, such as market-adjusted, industry-adjusted and mean returns models, which can also be complemented with the market model to ensure the robustness of any detected unusual returns. Another drawback is that this study examines the overall effect of spin-offs without examining the possible explanatory factors for these positive returns. Therefore, future studies can investigate the sources of these gains to determine what drives the favourable response of the market to this contraction move. Moreover, this study has investigated the spin-off returns in the short-term horizon only. Future studies can be conducted in the long-term horizon to investigate whether the spin-offs continue to perform well or their performance deteriorates over time.

Footnotes

Authors’ Contribution

Saima Nazir: Conceived the research idea, designed the study, reviewed literature, collected and analyzed data, and drafted the manuscript.

Khalid Ashraf Chisti: Contributed to manuscript writing, and provided critical revisions and supervision throughout the project.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.