Abstract

This study investigates the impact of cash holding of target firms on acquisition propensity. We investigate the moderating role of family ownership and takeover regulations on the association between takeovers and cash holding of the target firms by employing the logit regression model. Using data of Indian listed firms for 2003–2019, we observe that the cash holdings of the target firms have a positive and significant effect on their likelihood of acquisition. However, cash-rich-family firms have a negative but insignificant effect on the likelihood of acquisition, implying that the entrenchment effect due to family ownership dominates the liquidity effect of cash holding. When the family has more than 51% ownership in the firms, the ownership effect fully outweighs the cash effect. Further, using a regulatory intervention that impacts the ownership structure of the firms as an exogenous shock, the study shows that regulatory framework changes further exacerbate the entrenchment effect on the likelihood of takeovers, which does not allow for an active takeover market. Our results are robust to the alternative definitions of family firms and the takeover objectives. This study provides insight to the policymakers regarding the response of family firms to changes in regulation and also contributes to the literature on acquisition in countries with concentrated ownership structures.

Introduction

Mergers and acquisitions (M&A) activity has surged globally, with deals totalling $3.8 trillion in 2022. Emerging countries such as China and India have experienced high M&A deal volumes, with $733 billion and $81.7 billion, respectively, even amidst the pandemic (PwC, 2020). In India, M&A activity increased post-liberalization (Aggarwal & Garg, 2022). Ownership structures, particularly family ownership, influence M&A (Caprio et al., 2011; Tarsalewska, 2021) and are crucial as many firms globally are family-controlled (Olubukola et al., 2017; Yoshikawa & Rasheed, 2010). In East Asia, around 50% of firms are family-controlled, compared to over 90% in India.

Studies indicate that ownership structures impact acquisition likelihood (Caprio et al., 2011). Some find that family ownership fosters M&A (Fuad et al., 2023), while others argue that concentrated ownership by institutional shareholders, families and the state reduces it due to dilution concerns (Nogueira & Kabbach de Castro, 2020). The literature on family firms presents mixed results. Like, bidding family firms may pursue M&A for succession (Feito-Ruiz & Menéndez-Requejo, 2010), diversification (Defrancq et al., 2016) or socioemotional wealth (SEW) preferences (López-Delgado et al., 2024; Schierstedt et al., 2020). Conversely, target family firms prefer internal growth (Shim & Okamuro, 2011), resist takeovers to preserve SEW (Diéguez-Soto et al., 2021; Gómez-Mejía et al., 2018) and fear control loss (Miller et al., 2010). Family ownership also reduces cross-border acquisitions (Arena et al., 2022).

Further, cash-holding decisions vary for family and non-family firms due to differences in ownership and governance (Alghadi et al., 2021; Azinfar & Shiraseb, 2016). Family firms hold more cash due to risk aversion and control retention (Caprio et al., 2020; Suk et al., 2019), with concentrated ownership boosting reserves (Tayem et al., 2019). Cash holdings influence M&A activity in different ways—while liquidity can make target firms more attractive to acquirers seeking financial flexibility (Massa & Xu, 2013), excess cash may deter takeovers, as firms often use buybacks or other defensive strategies to resist acquisition attempts (Pinkowitz, 2000). Inefficient capital allocation may signal weak management, reducing attractiveness. Family ownership levels also influence cash holdings (Durán et al., 2016), affecting acquisition probability (Caprio et al., 2011).

We extend Caprio et al. (2011) by examining target firms’ cash reserves, liquidity and entrenchment effects of family firms on takeover probability in an emerging market. India, characterized by weak governance (Rajagopalan & Zang, 2008), low investor protection (Leuz et al., 2003), high family ownership (Chakrabarti et al., 2008) and large cash holdings (Maheshwari & Rao, 2017), provides a unique setting.

Securities and Exchange Board of India (SEBI) introduced the Substantial Acquisition of Shares and Takeovers (SAST) regulations in 1997 to regulate takeovers and protect minority shareholders, with major amendments in 2002 and 2011. The 2011 revisions, including a higher creeping acquisition limit, larger offer size, initial threshold for mandatory bids and liberal exemptions, impacted family stakeholding post-2011, enabling promoters to increase control (Varottil, 2015). This regulatory shift provides a natural experiment to assess family ownership’s effect on acquisition probability before and after 2011.

Using pooled cross-sectional data (4,029 listed non-financial, non-government Indian firms from BSE/NSE, 2003–2019), we find that target cash reserves increase acquisition probability (liquidity effect), but high family ownership (>20%) deters takeovers (entrenchment effect). High family ownership reduces cash-rich firms’ appeal, though insignificantly, suggesting that the entrenchment effect dominates the liquidity effect. This negative relationship intensifies post-SAST 2011, supporting the entrenchment view.

The results remain robust for alternative family ownership definitions of family firms, viz. 40% and 51%, except when cash interacts with ownership, turning significantly negative beyond these levels. The negative relationship between family ownership and takeover probability weakens above 51%, suggesting that families with lower ownership prioritize control and resist dilution, while higher ownership aligns interests with minority shareholders, reducing control concerns (Basu et al., 2009). Thus, family ownership levels influence takeovers differently in India. Findings also hold when considering the objective of change in control without consolidation of holdings objectives.

This article contributes to the present literature in the following three ways. First, we provide new evidence on the impact of family ownership on takeover decisions across family ownership levels. Second, this study provides new insights into corporate liquidity and ownership structures, highlighting entrenchment over liquidity effects. Third, we demonstrate SEBI SAST 2011’s role in strengthening family ownership’s negative impact on acquisitions.

The article proceeds as follows: Section 2 reviews literature. Section 3 outlines data and models. Section 4 discusses results, Section 5 presents robustness checks and Section 6 concludes.

Literature Review and Hypothesis Development

A takeover occurs when an acquirer gains control of a target company by purchasing its shares (SAST Regulations, 2011). This study examines how target firms’ ownership structure and cash reserves influence takeovers. Firms accumulate cash when managers retain free cash flow instead of investing (Jensen, 1986), potentially leading to agency issues if managers prioritize self-interest over shareholder value. Kalcheva and Lins (2007) argue that firm value improves when excess cash is distributed as dividends.

Family ownership shapes control and decision-making. While high cash reserves attract acquirers, concentrated family ownership can act as a defence, reducing attractiveness. Additionally, cash-rich firms may demand a higher takeover premium, making them less appealing. This study explores how Indian family firms use cash holdings as both a liquidity buffer and a takeover defence.

The brief literature is based on two strands: First, we consider the relationship between cash reserves and takeover activities. Second, we consider the relationship between cash and family ownership, and its likely impact on acquisition probability.

Cash Reserves of Target Firms: Impact on the Probability of Acquisition

Cash plays a key role in strategic decisions like takeovers (Kumar & Oberoi, 2019). Research shows a positive link between cash holdings and takeover likelihood (Hu & Yang, 2016). Jensen (1986) argues that cash-rich firms attract acquirers, offering financial flexibility (Shastri, 1990) and enabling debt settlement (De Jong & Fliers, 2020). However, Agyei‐Boapeah (2019) finds a negative link between cash and acquisitions in the UK, while Huyghebaert and Luypaert (2010) suggest that low-cash acquirers pursue takeovers to offset weak organic growth. Most studies focus on acquirers’ cash; this study examines target family firms’ cash and its impact on takeover likelihood.

Research indicates that cash-rich targets are less likely to be acquired due to agency issues and weak controls (Harford, 1999; Jo & Pan, 2009). Prior studies, mostly in developed markets with lower cash holdings, show a negative correlation between cash reserves and acquisitions for target firms but a positive one for bidders. Given India’s high cash holdings and limited research on target firm cash, further study is needed. Based on this, we hypothesize that:

H1: The cash reserves of target firms reduce the probability of acquisition.

Cash Reserves of Family-owned Firms and Probability of Acquisition

Despite the global dominance of family firms, the impact of their cash reserves on takeovers remains unclear. Research on family firms’ cash-holding policies is mixed (Correggi et al., 2025), with little focus on its effect on takeover probability. This study aims to fill that gap.

Family firms’ cash holdings are often valued lower due to dominant shareholders extracting private benefits, which increase agency costs (Gupta & Bedi, 2020; Moolchandani & Kar, 2022). This, in turn, may reduce their attractiveness as acquisition targets. While literature suggests family firms hold more cash but with lower marginal value (Kalcheva & Lins, 2007), Liu (2011) argues they have less cash and spend quickly on projects favouring family interests. Brockman et al. (2009) find that S&P 500 family firms hold more cash, aligning with Guizani et al. (2018) and Sun et al. (2019). However, Cambrea et al. (2022) and Parrado‐Martínez et al. (2024) argue that family firms derive more value and incur lower costs than non-family firms when increasing their cash holdings. These higher cash reserves enable family firms to resist takeovers by funding strategic projects, repaying debt or increasing shareholder payouts, which make them less appealing to potential acquirers. Conversely, low cash reserves may make them more vulnerable to takeovers, as they may lack the financial flexibility to fend off acquisitions. Given this, we hypothesize:

H2: Cash reserves of family-owned target firms reduce the probability of acquisition.

Family Ownership and SEBI SAST 2011 Regulation: Impact on the Probability of Acquisition

SEBI introduced the SAST code in 2011, based on the Achuthan Committee’s recommendations (2010), shaping India’s takeover regulations. These rules aim to provide minority shareholders with the best exit opportunity during substantial acquisitions or control changes, thereby influencing corporate governance.

Over time, SEBI SAST amendments have impacted key takeover provisions, including trigger limits for open offers, creeping acquisitions, offer size, offer price, change in control and public shareholding (Dixit et al., 2023). Certain modifications, such as a higher creeping acquisition limit, increased offer size, initial threshold for mandatory bids and liberal exemptions, have enabled family owners to consolidate holdings (Varottil, 2015). Promoters use takeover rules for creeping acquisitions to increase stakes, leading to concentrated ownership (Selarka, 2018). A larger offer size and threshold for mandatory bids further support this trend (Dixit et al., 2023). Therefore, post-2011, we expect a rise in promoter shareholding, strengthening the negative link between family ownership and takeovers, as well as the interaction effect of family ownership, cash reserves and acquisitions. This leads to the following hypotheses:

The discussion is summarized as the following hypotheses.

H3: SEBI SAST 2011 regulations strengthen the negative relationship between target family ownership and the probability of takeover.

H4: SEBI SAST 2011 regulations strengthen the negative relationship between cash-rich, family-owned target firms and the probability of takeover

Data and Methods

Data

The study utilizes pooled cross-sectional data from 4,029 publicly listed, non-financial, non-governmental firms in India from 2003 to 2019, sourced from CMIE Prowess, a reliable financial database based on annual reports (Jindal & Seth, 2019). Prior research, including Das (2021) and Gopalan et al. (2014), has widely used Prowess for studying takeovers and cash holdings. Data on M&A deals from 2002–2003 to 2018–2019 are sourced from SEBI, India’s securities market regulator, which serves as the regulatory and supervisory authority overseeing the mandatory bid rule and open offer process during takeovers (Dash et al., 2024). This study focuses on the pre-COVID-19 period, specifically up to the year 2019, to eliminate potential fluctuations and skewness in the data caused by the pandemic. We acknowledge that the COVID-19 pandemic brought significant disruptions that may have influenced firm behaviour, financial performance and market dynamics. However, our decision to restrict the data set to the pre-COVID period (up to 2019) is driven by the need for methodological clarity and consistency. Analyzing firm-level outcomes during a relatively stable macroeconomic and regulatory environment allows us to isolate the effects of ownership structures and institutional mechanisms without the confounding influence of crisis-related shocks.

The inclusion of post-2019 data could introduce external distortions that are difficult to separate from the core variables under study, such as ownership concentration and takeover regulation enforcement. By focusing on the pre-pandemic period, we enhance the internal validity of our analysis and ensure that the results are attributable to underlying structural features rather than temporary crisis responses.

At the same time, we believe the institutional insights from this period remain relevant in the post-pandemic context, as key features of Indian corporate governance—such as promoter dominance, concentrated ownership and regulatory enforcement gaps—continue to persist. This continuity strengthens the contextual grounding of our study and ensures that the findings remain useful for ongoing policy dialogue and future empirical exploration.

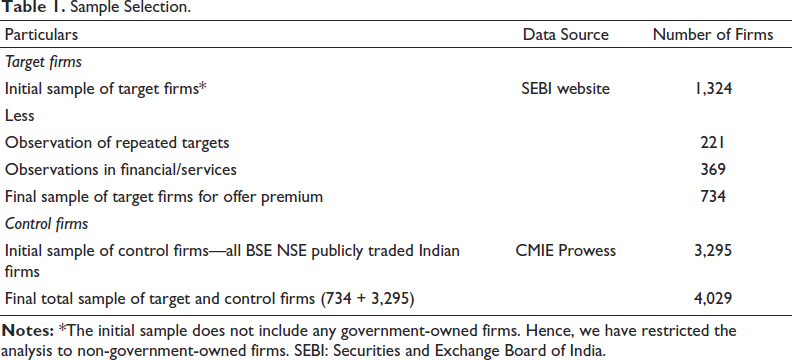

Data before 2002–2003 were unavailable due to missing SEBI offer letters. Financial and government firms are excluded due to distinct regulations. Table 1 outlines the sample selection process.

Sample Selection.

Sample Selection.

We obtain information on deal-specific characteristics like deal value, objectives of the deal, date of public announcement and method of payment from SEBI open offer data. SEBI does not give a breakup of completed and incomplete deals; hence, we cannot separate the deals based on completion. The payment for all deals in our sample is based on cash.

For the takeover likelihood, the dependent variable, acquisition probability, is defined as a dummy variable taking the value 1 for target firms and 0 otherwise. Our sample consists of 27,282 firm-year observations with 734 target and 3,295 control firms.

Logistic regression is the most widely used method for analyzing binary outcome data. A logistic regression model with a single predictor variable is called simple logistic regression. When the model includes multiple predictors, which can be both categorical and continuous, it is referred to as multiple or multivariable logistic regression (Nick & Campbell, 2007). Since our study focuses on the probability of takeover, a binary variable, taking the form of 1/0, with 1 if the firm is taken over and 0 if the firm is not taken over, and includes multiple predictor variables, we use a multiple logistic regression model.

Variables

This section outlines the dependent, independent and control variables used in the study. The primary dependent variable is the probability of takeover, represented by a dummy that takes the value of 1 if an acquirer takes over the firm and 0 otherwise.

Other variables are as follows: Total Promoter and Total Promoter Square are the total ownership percentages of promoters in the firm and its squared term, respectively. The Total Promoter Square is included in the model to capture the potential non-linear effects of promoter ownership on the likelihood of a takeover (Srivastava & Bhatia, 2022). Since the research focuses on family firms, promoter ownership held by family members plays a significant role in strategic decisions of takeovers. By adding both the Total Promoter variable and its square term, the model can account for both linear and curvilinear relationships, allowing the analysis to detect whether the impact of promoter ownership on takeover increases or decreases with a change in promoter ownership levels. Our primary variables of interest are Cash and Family Ownership. Cash and cash equivalents at the end of the year and total assets have been collected from CMIE Prowess. Cash and cash equivalents at the end of the year are then divided by total assets to arrive at our variable of interest, Cash. Therefore, Cash is a ratio of cash and cash equivalents and total assets (Zeng & Chan, 2023). Family Ownership is measured as a dummy that takes the value 1 if the fraction of shares owned by the family shareholders is more than 20% and 0 otherwise. In the literature on US and European countries, an ownership threshold above 20% is used to define family firms as this level is sufficient to ensure control (Sraer & Thesmar, 2007; Villalonga & Amit, 2006). Therefore, in alignment with prior research, we use 20% or more as a threshold in our study to define the family business. Further, at 20%, family shareholders typically have substantial influence over key decisions, including takeovers, without necessarily holding majority control. PB represents the ratio of the market value of shares outstanding to the book value of equity (Caprio et al., 2011). Controlling for PB ensures that the study considers whether takeovers are influenced by the firm’s market valuation relative to its actual assets. ROTA is the return on total assets (Caprio et al., 2011) used to account for profitability. A firm’s profitability can impact its attractiveness as a takeover target, affecting the likelihood of acquisition. Debt Equity is the ratio of the company’s total debt and shareholder’s equity, used to control financial risk. Firms with high debt may be less appealing to acquirers due to financial distress, while lower debt might make them less risky and more attractive to certain acquirers. Total Assets are the log value of total assets (Nogueira & Kabbach de Castro, 2020) used in the study to control for the firm’s size affecting the attractiveness of target firms. Age is the number of years since establishment (Schierstedt et al., 2020) to account for the firm’s maturity. Older firms may be either adept or inept at adapting to their age, making them more or less attractive as acquisition targets. These variables ensure that the analysis focuses on the specific effect of family ownership on takeover likelihood while accounting for these additional influences.

We also include a year dummy, SAST 2011, to obtain the effect of amendments in SEBI (SAST) regulation in November 2011. We have controlled for industry and year-specific fixed effects in the regression models to test for unobserved macroeconomic factors, which may potentially affect the likelihood of the firm’s acquisition.

Model Specifications

We examine the association between acquisition probability, cash holding, family ownership and other firm characteristics using the following equations:

where,

The subscript i indexes firm and t stands for the year (t = 2003–2019). Xk,i,t is a vector of explanatory variables, including firms’ financial characteristics and ownership structure variables, potentially impacting the acquisition likelihood (Harford, 1999). εit represents an idiosyncratic component. We winsorize all financial variables at 1% and 99% levels to moderate the probable bias in our outcomes brought about by outliers. Robust standard errors are considered in all models to account for potential heteroscedasticity in the data.

Descriptive Statistics

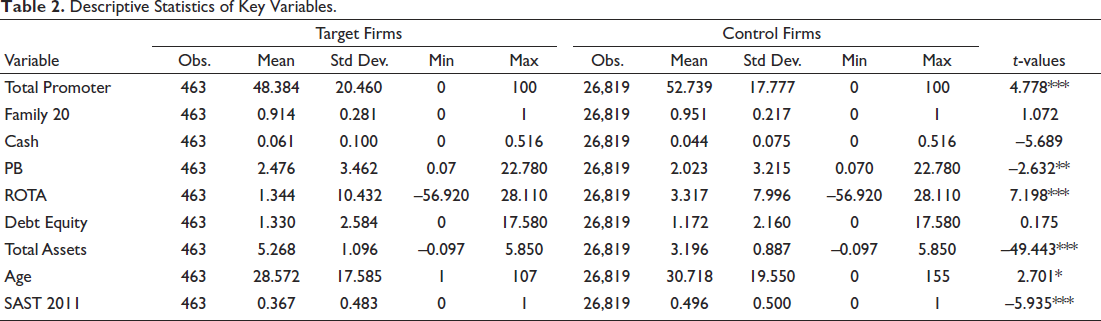

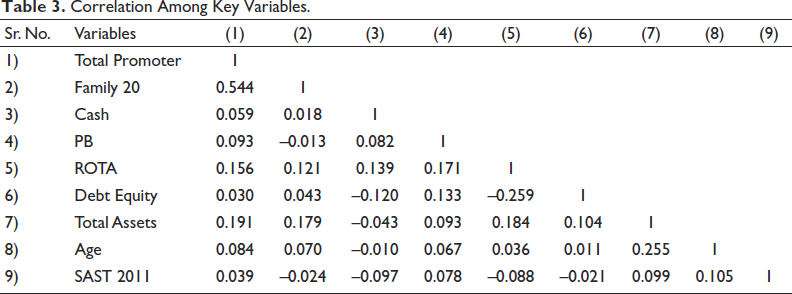

This study analyzes how cash reserves and ownership of target firm influence a firm’s likelihood of acquisition, using firm attributes. Table 2 presents descriptive statistics, showing higher promoter holding and return on assets (ROA) in control firms, while target firms have a higher PB ratio, indicating overvaluation. Target firms underperform in cash holdings and ROA but not in total assets. Lower ROTA in target firms suggests bidders seek underperforming firms for value creation. Target firms generally have more assets, which can be used as collateral for takeover financing (Ambrose & Megginson, 1992). Older firms are less likely to be acquired, possibly due to rigidity and inefficiency. Table 3 discusses variable correlations.

Descriptive Statistics of Key Variables.

Descriptive Statistics of Key Variables.

Correlation Among Key Variables.

Table 4 presents regression results on acquisition probability, family ownership and target firms’ cash holdings. High promoter ownership negatively impacts acquisition likelihood (Columns 1 and 2), supporting the entrenchment hypothesis. Using a family ownership dummy over 20% of family ownership levels, we find a significant negative association with takeover probability (Column 3). This suggests family-owned firms are less likely to be acquired due to control-enhancing mechanisms like differentiated voting rights, reinforcing entrenchment (Hamberg et al., 2013). The entrenchment effect aligns with agency theory, as concentrated ownership reduces information asymmetries, limiting opportunistic takeovers (Jensen, 1986). Similar findings exist for European (Caprio et al., 2011), US (Bauguess & Stegemoller, 2008; Miller et al., 2010) and emerging market firms (Nogueira & Kabbach de Castro, 2020), indicating family owners resist relinquishing control.

Salience of Family Ownership, Cash-rich, Family-owned Firms as a Determinant of the Probability of Takeover.

Salience of Family Ownership, Cash-rich, Family-owned Firms as a Determinant of the Probability of Takeover.

As shown in Columns 1–4 in Table 4, a significantly positive coefficient of cash shows that target firms’ higher cash reserves are positively associated with an increased likelihood for target firms to participate in acquisitions. This provides evidence for the liquidity effect and supports H1. A rise in the cash reserves of target firms induces bidding firms to make bids with the expectation of using these reserves to fund acquisitions (Browne & Rosengren, 1987) or finance value-enhancing projects. Target firms’ cash reserves will strengthen bidding firms’ liquidity position post-acquisition. Our results align with Kumar and Oberoi (2019), who document a positive association between the likelihood of a firm engaging in M&A and cash reserves. Cash-rich firms can provide financial flexibility and coinsurance to potential bidders (Billett et al., 2004).

Cash-rich, Family Firms and Acquisition Probability

The results of the interaction of family ownership and cash holding appear in Column 4 of Table 4. The objective of interaction is to capture the probability of the acquisition of cash-rich, family-owned target firms. We observe that the coefficient of the interaction term between cash reserves and family ownership is negative over 20% degree of family ownership, though not significant. This also shows that cash-rich, family-owned firms are less likely to be acquisition targets than their poor cash counterparts. These findings of Column 4 of Table 4 do not support H2 as the interaction effect is insignificant. However, our outcomes demonstrate that family ownership makes cash-rich firms less attractive, suggesting that the entrenchment effect increases the dominance over the liquidity effect. Our results also imply that family ownership reduces liquidity efficiency in the target firms as family members might misuse cash to maximize their personal benefits or invest in projects that do not generate positive returns for the firm. The severity of the entrenchment effect of family ownership is so high that it eliminates the liquidity effect in target firms, even though family firms hold larger cash than non-family firms. These findings allow us to provide evidence on the entrenchment effect vis-à-vis the liquidity effect.

PB exhibits a positive effect. Ideally, the coefficient of the PB ratio should be negative as bidders find undervalued firms attractive. This implies that our results are counterintuitive for the PB ratio. Some of the coefficients of control variables in Table 4 are consistent with the coefficients in prior studies. ROTA’s negative but significant coefficient suggests that acquirers might be inclined to target poorly performing firms. This negative association is consistent with Palepu’s (1986) argument that the bidders can unlock greater value in poorly performing firms through efficient management. Consistent with Caprio et al. (2011), we find that the sign of debt equity ratio is negative and significant across all columns, which indicates that highly levered firms are less appealing takeover targets because they provide less post-takeover free cash flow to service debt taken to fund the takeover and exhaust new debt issuing capacity. Total assets measure the firm size and significantly increase acquisition probability (Wu & Chung, 2019). Older organizations are less likely to be acquisition targets. The reason might be that the firms have become increasingly rigid and inept in adapting to age (Coad et al., 2018).

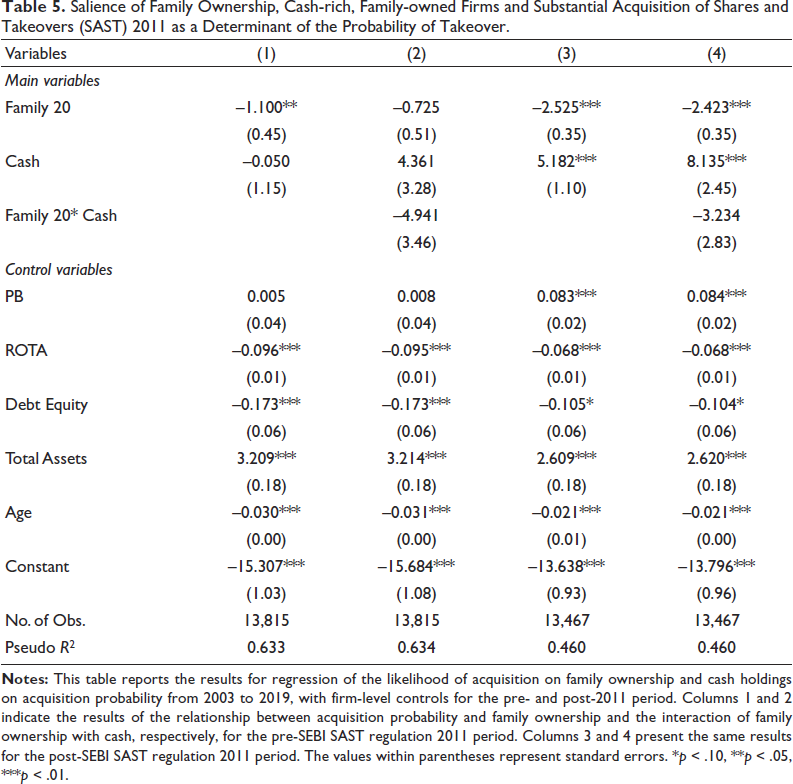

Regulatory Change and Acquisition Probability

Next, we investigate the role of amendments in SEBI (SAST) regulation in 2011 on the acquisition likelihood of family-owned firms. The results in Columns 1 and 2 of Table 5 present the impact of family ownership on acquisition likelihood in the pre-2011 period. Columns 3 and 4 present the results for the post-2011 period. As seen in Columns 1 and 3, the negative effect of family ownership on acquisition probability intensifies post-2011. This results from higher stakeholding of promoters after 2011 due to regulatory changes resulting in greater entrenchment. It indicates that modifications in takeover codes in 2011 have favoured promoters to increase their holdings in the firm, making it difficult for bidders to acquire such firms. Thus, Columns 1 and 3 of Table 5 support H3. One more finding concerns the cash holding of family members before 2011 and after 2011. As we can observe from Columns 2 and 4, the cash holdings of family firms negatively influence acquisition likelihood both before and after 2011, but without any significance. Again, these results support the prominence of the entrenchment effect over the liquidity effect, which results from escalated equity ownership of family members after 2011, reducing the attractiveness of such firms’ cash holdings. The above discussion demonstrates that Columns 2 and 4 of Table 5 do not provide evidence in support of H4.

Salience of Family Ownership, Cash-rich, Family-owned Firms and Substantial Acquisition of Shares and Takeovers (SAST) 2011 as a Determinant of the Probability of Takeover.

Salience of Family Ownership, Cash-rich, Family-owned Firms and Substantial Acquisition of Shares and Takeovers (SAST) 2011 as a Determinant of the Probability of Takeover.

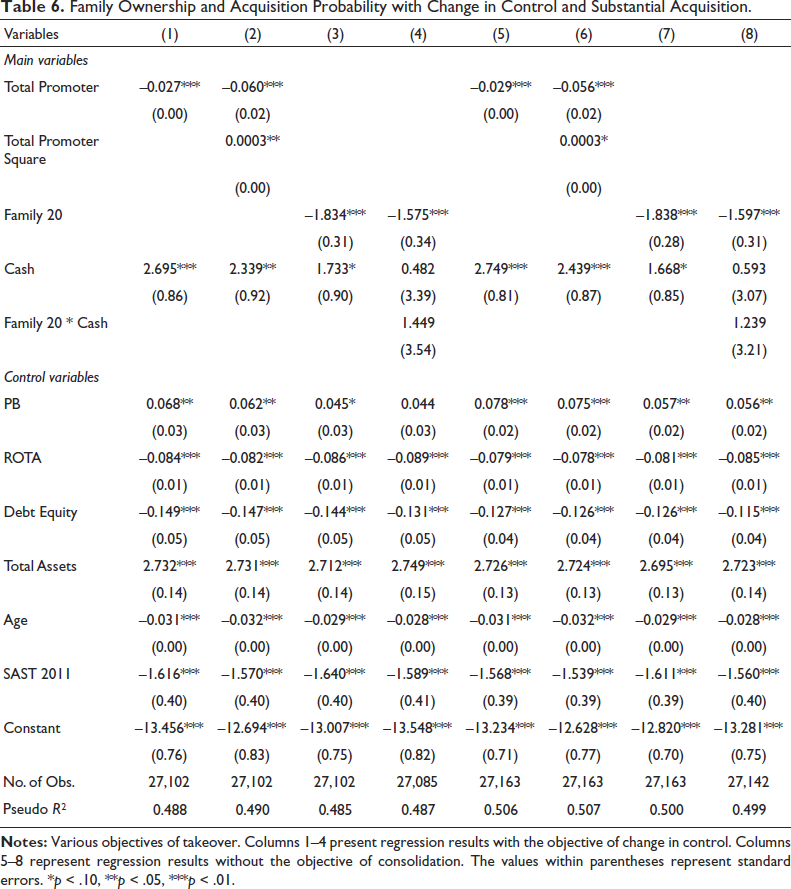

Additionally, we examine the impact of various acquisition objectives, which are classified into three categories under SEBI SAST: substantial acquisition, change in control and consolidation of holdings. Change in control implies a change in voting rights that replaces incumbents of the target firm with new shareholders. Change in control involves the right to appoint a majority of directors or to control strategic or policy decisions. Substantial acquisition indicates the acquisition of 25% or more shareholding or voting rights in the target firm through an open offer per the 2011 code. This limit was 15% in SAST 1997. Consolidation of holdings is when an acquirer already owns between 25% and 75% of target shares and bids to purchase more from the general public to consolidate his shareholding further. Such a bidder is required to make a mandatory open offer to acquire more than 5% of shares from the public. This open offer should be made for at least 26% of shares. Further, in cases involving persons acting in concert as acquirers, the shares they acquired are equivalent to a change in control. Along these lines, we assume that regarding the determination of ownership level, change in control and substantial acquisition should have similar effects on the acquisition probability. Therefore, following Ranganathan and Singh (2018), we exclude deals with the objective of consolidation under the assumption that consolidation is partial acquisition and test for the combined effect of change in control and substantial acquisition on the probability of acquisition.

Table 6 presents regression results that analyze the relationship between family ownership and acquisition probability, focusing on two objectives: change in control (Columns 1–4) and substantial acquisition without consolidation (Columns 5–8). In Column 1, the results align with previous findings, indicating that high promoter ownership lowers acquisition likelihood. This is likely due to promoters’ reluctance to face the scrutiny associated with highly visible takeover transactions and their desire to retain control of the firm. The negative coefficient of promoter ownership squared in Column 2 suggests a non-linear effect of promoter ownership on the probability of takeover as their ownership rises. Column 3 confirms that family ownership above 20% significantly reduces the likelihood of acquisition aimed at change in control, as family members are often entrenched and unwilling to relinquish control, supporting the entrenchment effect. This resistance makes family-owned firms less appealing to bidders targeting control. The positive but insignificant coefficient of cash-rich, family firms in Column 4 shows that while cash reserves are attractive to potential acquirers seeking control, the strong family ownership with high cash acts as a protective barrier, weakening the impact of cash on the likelihood of a control-focused takeover. This makes the effect statistically insignificant and highlights the dominance of the entrenchment effect in family-owned firms. The same trends are observed in Columns 5–8 for takeovers without consolidation objectives.

Family Ownership and Acquisition Probability with Change in Control and Substantial Acquisition.

Family Ownership and Acquisition Probability with Change in Control and Substantial Acquisition.

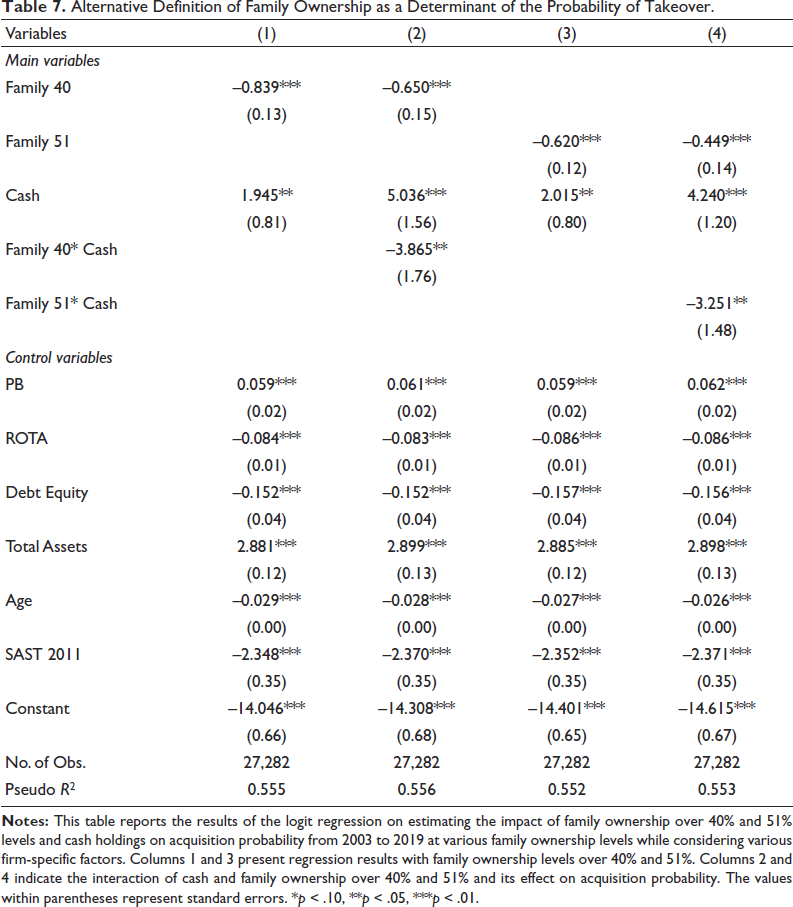

This section examines the robustness of our results with five different issues. First, we investigate the impact of heterogeneity in the levels of family ownership, viz. over 40% and 51%, on acquisition likelihood. Following Villalonga and Amit (2006), we investigated the effect of above 20% level of family ownership in our main results. As Villalonga and Amit (2006) studied US firms where the concentration of ownership is not high, a 20% family ownership level is justified. However, as the study context is Indian firms with high ownership concentration, we increased the threshold to 40%, which denotes an intermediate level of ownership in India (Kumar & Singh, 2013). Literature has also used the 51% level to define family firms (Bouzgarrou & Navatte, 2013). Over 51% of family ownership suggests family members’ control over the business, higher commitment and the transfer of business to the next generation. Therefore, it becomes crucial to assess the impact of family ownership at this level on takeovers (Chang, 2003; Saravanan, 2009). Therefore, we join the family firm heterogeneity debate by including various degrees of family ownership in the study (Pazzaglia et al., 2013).

Table 7 reports a negative relationship between family ownership and acquisition likelihood. However, if we consider heterogeneity in family ownership levels on takeover probability, the results show that over lower family ownership levels of 40%, the takeover probability is more negative, and over higher levels of ownership levels of 51%, takeover likelihood becomes less negative with little difference. Second, we use the same ownership levels to examine the effect of cash-rich, family-owned firms on acquisition probability. Columns 2 and 4 indicate that cash-rich, family-owned firms are not attractive targets. So, whether cash-rich or not, family-owned firms do not attract bidders at any level of family ownership. Bidders consider family firms too entrenched to acquire control over them or their cash reserves. However, cash-rich target firms attract bidders, as shown in all columns in the table. The results prove that the entrenchment effect dominates the liquidity effect as cash-rich target firms are attractive targets, while cash-rich, family firms are not.

Alternative Definition of Family Ownership as a Determinant of the Probability of Takeover.

Alternative Definition of Family Ownership as a Determinant of the Probability of Takeover.

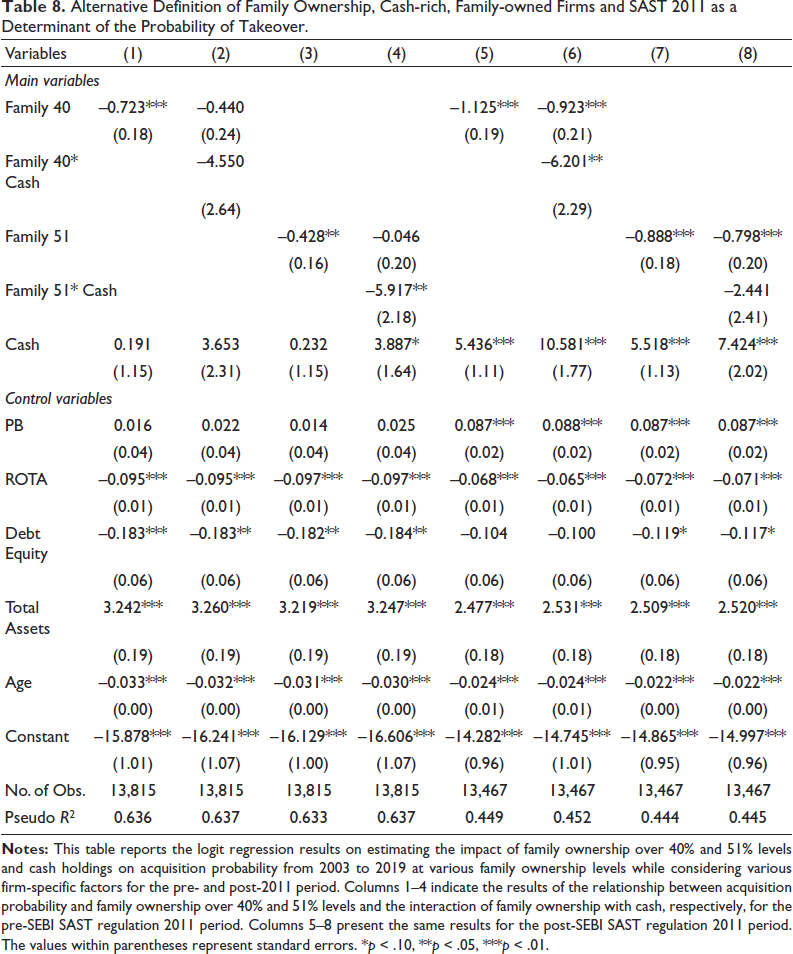

Third, we study the effect of family ownership levels over 40% and 51% on takeover probability for the pre- and post-SEBI SAST 2011 regulation period as demonstrated in Table 8. We notice that the coefficients of family ownership over 40% and 51% levels have become more negative post-2011 than pre-2011, as shown in Columns 1 and 5 for 40% family ownership levels and Columns 3 and 7 for 51% family ownership levels for pre- and post-2011, respectively. This indicates that a powerful entrenchment effect also prevails post-2011, making family firms an unattractive target. It provides evidence that the amendments in SEBI SAST regulations in 2011 have facilitated ownership concentration in promoters’ hands, making them less appealing to bidders due to the entrenchment effect. Alternatively, one can argue that it becomes difficult for bidders to buy such firms as family members do not want to reduce their stakes. Fourth, we also examine the impact of cash-rich, family-owned target firms over 40% and 51% family ownership levels on takeover probability for the pre- and post-SEBI SAST 2011 regulation period, as presented in Table 8. The results show that the coefficients of cash reserves are positive and significant post-2011 as highlighted in Columns 5–8. Additionally, both family and cash-rich, family firms are unattractive during both periods. However, post-2011 cash-rich, family firms lose their significance over family ownership levels of 51% as indicated in Column 8 of Table 8. These results highlight the prevalence of the entrenchment effect over the liquidity effect. Whether cash-rich or not, family firms do not attract bidders at any level of family ownership. Their high cash reserves do not appeal to bidders to acquire them despite the multiple benefits of corporate liquidity. The results also show that heterogeneity in the family ownership levels and cash holding of family firms affect takeover events post-SEBI SAST 2011 period.

Alternative Definition of Family Ownership, Cash-rich, Family-owned Firms and SAST 2011 as a Determinant of the Probability of Takeover.

This study examines how cash holdings in family-owned firms affect acquisition probability in India, an emerging economy dominated by family firms. Our findings provide evidence for both the liquidity and entrenchment effects. Regression results indicate that family firms are generally unattractive to bidders, supporting the entrenchment hypothesis. While cash holdings increase acquisition likelihood overall, cash-rich, family firms remain less appealing targets, suggesting entrenchment outweighs liquidity. The SAST 2011 regulation appears to strengthen this entrenchment effect, potentially detrimental for minority shareholders. These results are robust across different ownership thresholds (40% and 51%) and takeover objectives.

The findings have practical implications for managers. Firms with high cash reserves are more likely to attract bids, so managers should align cash management with strategic goals and takeover risks. Options like reinvestment, buybacks, or long-term value initiatives may reduce vulnerability to takeovers. Additionally, staying informed about regulatory changes is essential to manage takeover threats effectively.

Our study has certain limitations, which can be resolved through future research. Though our sample covers a rapidly developing economy—India, future studies may extend the sample to cover countries from various geographical regions to test whether our results and conclusions can be extended. This is because a single country’s setting and cultural aspects limit the transferability of results to other countries and institutional settings. Additionally, future research may examine whether the entrenchment and liquidity dynamics identified in this study persist in the post-COVID-19 period, given the structural and behavioural changes triggered by the pandemic. Future research can further explore the means through which cash holdings of family firms influence value creation for shareholders during takeovers.

Authors’ Contributions

Both authors contributed equally to the conceptualisation and design of the study. They jointly undertook the collection, analysis, and interpretation of secondary data. Both authors were equally involved in drafting, revising, and finalising the manuscript, and have approved its final version for submission.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.