Abstract

Building on social capital theory and shareholder value theory, this study re-examines the paradoxical impact of corporate social responsibility investments on firm performance in light of the organizational structure. In this research, the unit of analysis is limited to Indian manufacturing firms that are publicly listed on the Bombay Stock Exchange. Using panel data from 2015 to 2022 gathered from the Prowess database, this study has established empirical proxies for corporate social responsibility, organizational structure (business group vs. standalone firm), firm performance and other pertinent variables. Subsequently, panel data regression analyses have been utilized to address the research questions. More importantly, all models incorporate industry and year effects and robust standard errors to account for heteroscedasticity. While corporate social responsibility investments create social capital and enhance performance, the results offer a striking contrast—business group firms exhibit significantly higher corporate social responsibility investments yet experience lower financial returns compared to their standalone counterparts. This paradoxical phenomenon arises from business group affiliation negatively moderating the relationship between corporate social responsibility and performance. Building on social capital theory, this research suggests that firms need to consider their organizational structure when developing corporate social responsibility strategies to maximize both financial and social performance.

Keywords

Introduction

Does investing in corporate social responsibility (CSR) initiatives enhance financial performance, or does it signify a misallocation of resources? This question has sparked much discussion and differing perspectives in the academic literature (Griffin & Mahon, 1997; Ikram et al., 2019; Khan et al., 2022; Koh et al., 2023; Kong et al., 2020; Lin et al., 2019; Saeidi et al., 2015; Sarwar et al., 2024; Silva et al., 2023; Sung Kim & Oh, 2019; Waddock & Graves, 1997). Building on social capital theory (SCT), some studies indicate that CSR can enhance a company’s reputation, social capital, access to valuable resources and operational efficiency, leading to better financial performance (Asiaei et al., 2023; Cordeiro & Tewari, 2015; Soundararajan & Brown, 2016). However, another body of research argues that investing in CSR requires additional use of a company’s resources, such as labour, time and capital, which could potentially misallocate resources and hinder financial performance (Blomgren, 2011; Brammer et al., 2006; Selcuk & Kiymaz, 2017; Servaes & Tamayo, 2013). This is consistent with shareholder value theory (SVT), which posits that CSR investments divert resources from core business activities, potentially hampering profitability and shareholder returns.

In this context, the organizational structure (e.g., business group (BG) affiliated firms vs. standalone (non-BG) firms) plays a crucial role in influencing the dynamics of this CSR–performance relationship (Bothello et al., 2023; Choi et al., 2018; Sung Kim & Oh, 2019). What is the impact of a firm’s CSR investment intensity on its performance outcomes? Does the organizational structure, particularly the BG affiliation, have a significant impact on shaping the characteristics of this relationship? These interrelated questions are the missing link in the literature, even though BG dynamics are of paramount importance in the context of CSR, especially in emerging markets (e.g., India). A BG refers to a collection of interconnected firms that operate under a single parent company (Lee et al., 2023). These firms engage in collaboration and resource sharing and often operate in various industries. Therefore, they are likely to gain advantages from relational capital, economies of scale and strategic management (Bhaumik et al., 2012; Khanna & Rivkin, 2001; Mishra, 2023; Yiu et al., 2007), which can further amplify the positive effect of CSR on financial outcomes. In addition, BG-affiliated firms may be subject to increased pressure and higher expectations from stakeholders. This makes CSR more important to maintain legitimacy and prevent damage to their brand reputation. However, affiliation to a BG may serve as a safeguard against potential adverse effects of CSR investments, given that diversified groups can cross-subsidize these initiatives. Thus, it is possible that the negative effect of CSR would be mitigated through cross-subsidization of CSR initiatives. These competing arguments are the central focus of the current study and highlight the complex dynamics between CSR, financial performance and organizational structure.

Building on the tenets of SCT and SVT and the above-mentioned research questions, we have examined (a) the relationship between CSR investment and firm performance and (b) the moderating role of organizational structure on the relationship between CSR investment and firm performance. This study has considered Indian manufacturing companies as the unit of analysis. Subsequently, using the Prowess database, we have collected relevant information on manufacturing firms that are publicly traded on the Bombay Stock Exchange (BSE) between 2015 and 2022. This study is relevant and timely, especially in light of developing nations like India. India’s unique socio-economic environment, constantly evolving corporate governance frameworks and market laws make it an ideal sample to study the CSR–performance dynamics. India’s Companies Act of 2013 requires mandatory CSR expenditures. It states that businesses should invest around 2% of their average net income in CSR activities. This regulation has resulted in a significant increase in CSR investment, that is, from ₹68,390 million in FY15 to ₹1,44,310 million in FY20 (CRISIL, 2022). However, it is still unclear how successful this mandated CSR expenditure is in terms of both financial performance and social impact. More importantly, it is found that more than 50% of the firms in our sample are BG firms, and therefore, it can be construed that BG holds significant value in the Indian set-up. Note that emerging economies are characterized by weak external (e.g., capital, labour) markets and institutional voids. In emerging economies, BGs emerge as a response to underdeveloped institutions, policy distortion and market inefficiencies (Masulis et al., 2023). Also, BG firms tend to focus more on strong social and political connections (Saiyed et al., 2023), and thus, they are more inclined towards CSR activities to strengthen these relationships. Further, Indian BGs historically have a family-based ownership structure that focuses on long-term reputation and social capital (Richter & Chakraborty, 2023). Considering the above discussion, it is critical to understand CSR–performance dynamics in light of BG affiliation, especially in the Indian context.

The findings of our study indicate a positive correlation between the level of investment in CSR and performance outcomes. The findings support the notion that CSR creates social capital among a company’s stakeholders, thereby leading to a boost in the firm’s overall performance (Asiaei et al., 2023; Husaini et al., 2023; Sen & Cowley, 2013). Moreover, it is found that BG-affiliated firms invest significantly higher in CSR compared to non-BG firms (independent/standalone firms). This is mainly because affiliated firms focus on building long-term social capital and political connections (Saiyed et al., 2023). More importantly, it may be a strategic decision for BG firms to mitigate the spillover effects of negative events or misconduct by a firm with the BG. Therefore, we examine the moderating role of BG affiliation on the CSR–performance to have an in-depth understanding of the implications of affiliated firms’ higher CSR involvement. The results indicate that BG firms experience lower financial performance compared to standalone firms due to their excessive involvement in CSR activities. It highlights the idiosyncratic challenges in emerging markets, which are characterized by institutional voids and socio-economic inequalities.

This article also contributes to Sustainable Development Goals (SDGs) (e.g., SDG 4—quality education, SDG 5—gender equality, SDG 13—climate action). CSR is one of the critical strategic tools to address issues related to socio-economic and environment, mainly in developing nations with underdeveloped institutional set-ups (Banker et al., 2023). For instance, the mandatory 2% CSR investment (under India’s Companies Act, 2013) represents a policy-driven decision that aligns with the SDGs. It encourages firms to serve social welfare and environmental sustainability. However, the study reports a paradox for BG firms: higher CSR investments do not always lead to higher financial returns. This indicates the need for firms to design CSR strategies that not only support the SDGs but also optimize the firm’s economic growth.

The subsequent sections of this document are structured in the following manner. Section 2 of the article provides an overview of the related literature. Section 3 outlines the proposed data and methodology to be employed in the study. The results and analysis are presented in Section 4. The discussion and implications are presented in Section 5. The present study concludes with a conclusion and limitations in Section 6.

Relevant Literature and Theoretical Underpinning

2.1. SCT and SVT Perspective of CSR and Firm Performance

CSR involves various activities, such as philanthropic activities, community advancement, environmental sustainability, ethical corporate conduct and employee well-being (Ikram et al., 2019; Koh et al., 2023; Sarwar et al., 2024; Sung Kim & Oh, 2019). A plethora of literature has investigated the link between CSR and a firm’s financial performance; however, they have produced inconclusive results. According to SCT, CSR activities can cultivate favourable social networks/connections with stakeholders, thus enhancing a firm’s social capital and consequently leading to better performance (Asiaei et al., 2023; Hoi et al., 2018; Liu et al., 2021; Russo & Perrini, 2010; Sen & Cowley, 2013). SCT asserts that social networks, reciprocal interactions and interwoven relationships are valuable assets for businesses (Nahapiet & Ghoshal, 1998; Putnam, 2001) because it helps them develop social capital and gain access to valuable resources, expertise and support from various sources (Graafland & Smid, 2004; Masulis et al., 2023). Using CSR initiatives as their strategic move, firms can establish trust, enhance their reputation and gain legitimacy with stakeholders, thereby strengthening their authorization to conduct business (Bothello et al., 2023; Russo & Perrini, 2010). The CSR policies need to engage stakeholders effectively, and only then can they lead to market expansion, improved buyer–supplier relationships and collaborations and increased community support (Sen & Cowley, 2013). Therefore, several studies have reported a significant, positive and direct relation between CSR and financial performance (Lin et al., 2019; Giannarakis et al., 2017; Oeyono et al., 2011; Orlitzky et al., 2003; Tsoutsoura, 2004).

On the other hand, SVT, introduced by Milton Friedman, emphasize that the main task of a firm is to optimize profits for its shareholders (Friedman, 2007). According to SVT, CSR activities are a misuse of valuable resources that could have been more efficiently allocated to core business operations to increase profit and shareholders’ return (Blomgren, 2011; Brammer et al., 2006; Karim et al., 2023; Selcuk & Kiymaz, 2017; Servaes & Tamayo, 2013). Drawing from the tenets of SVT (Friedman, 2007; Godfrey et al., 2009; Manchiraju & Rajgopal, 2017; Martin et al., 2009; O’Connell & Ward, 2020), it can be construed that firms are allocating funds towards non-essential business operations if they participate in CSR activities because it does not have an immediate positive impact on the shareholder returns (Friedman, 2007). Prior studies have reported a negative impact of CSR on financial outcomes, which is consistent with SVT (Blomgren, 2011; Lin et al., 2015). For instance, Lin et al. (2015) reveal that CSR is an additional expense for firms, which results in lower earnings. Nollet et al. (2016) show a U-shaped relationship between CSR and accounting-based performance metrics. This implies that CSR may have a detrimental impact on short-term financial performance.

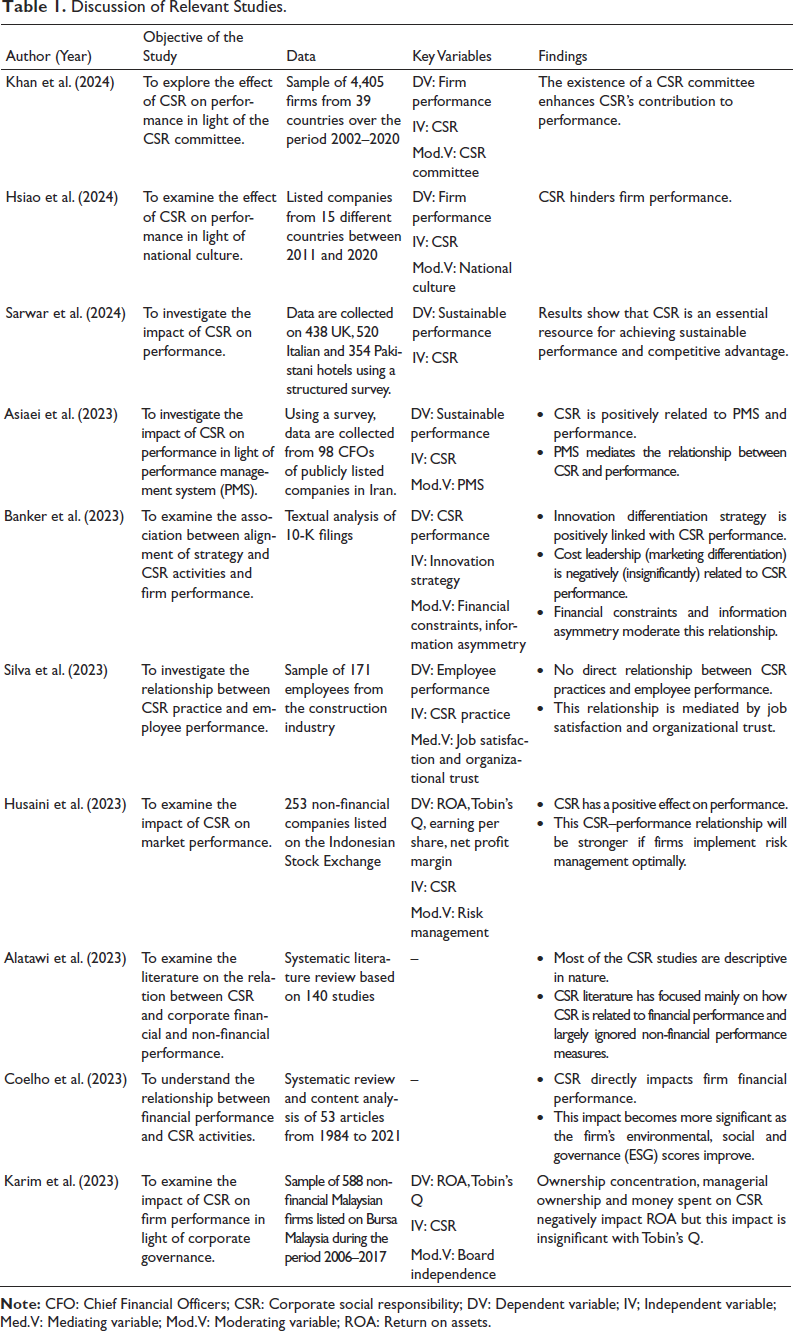

These competing empirical evidence on the CSR–performance relationship (Al-Shammari et al., 2022; Brammer et al., 2006; Ikram et al., 2019; Maury, 2022; McGuire et al., 1988; Oeyono et al., 2011; Orlitzky et al., 2003; Sarwar et al., 2024; Silva et al., 2023; Tsoutsoura, 2004) emphasize the need for a re-examination of this relationship dynamics. It is also important to consider factors such as CSR measurement, performance metrics and contextual variables that may influence the CSR–performance (Feng et al., 2018; Ghoul et al., 2017; Rhou et al., 2016). Table 1 discusses recent and relevant literature on the CSR–performance relationship.

Discussion of Relevant Studies.

Discussion of Relevant Studies.

Note: CFO: Chief Financial Officers; CSR: Corporate social responsibility; DV: Dependent variable; IV; Independent variable; Med.V: Mediating variable; Mod.V: Moderating variable; ROA: Return on assets.

2.2. CSR and Organizational Structure

One of the main characteristics of emerging countries is the inadequacy of basic inputs and resources usually required to strengthen economic growth (Masulis et al., 2023; Siegel & Choudhury, 2012). Institutional infrastructure is either immature or lacking completely, while social services are often severely underfinanced in developing economies, which hampers the hiring and maintenance of a skilled labour force. Due to such inadequacy of basic amenities, there is a huge shortage of subsidiary industries that provide other essential inputs. According to Fisman and Khanna (2004), these challenges are generally so extreme that it is surprising ‘how does anything get done at all?’ (p. 609). A plethora of studies has addressed the critical role of BG in such an economic environment (Bhaumik et al., 2012; Khanna & Rivkin, 2001; Richter & Chakraborty, 2023; Saiyed et al., 2023; Yiu et al., 2007). In developing economies, firms are categorized based on organizational structure, that is, BG-affiliated firms or standalone firms. BGs emerge as a response to underdeveloped institutions or ‘institutional voids’, policy distortion and market inefficiencies (Lee et al., 2023; Granovetter, 2005; Khanna & Palepu, 1997). Rooted in the institutional voids perspective, prior research has identified the positive side of the BG affiliation (Hoskisson et al., 2005; Khanna & Palepu, 2000). Most argue that BGs provide a platform to overcome some imperfections in the product, capital and labour market (Dewenter et al., 2001; Douma et al., 2006). In the context of CSR, prior studies have argued that BG affiliation offers unique opportunities to leverage shared resources, coordinate synergistic efforts, engage stakeholders comprehensively, manage reputation risks and align CSR with BG’s overall strategy. By integrating CSR practices across their subsidiaries and adopting responsible business behaviour, BGs can enhance their social and environmental impact while contributing to sustainable development.

BG firms are inclined to invest more in CSR as they acknowledge the importance of their reputation and brand identity, not solely for individual entities within the BG but for the BG as a whole (Sung Kim & Oh, 2019). BG-affiliated firms are known for showing their commitment to ethical business operations, social well-being and environmental sustainability with the help of CSR activities. It helps build brand reputation, customer loyalty and stakeholder trust (Choi et al., 2018). Also, BG firms show a high level of responsiveness towards the diverse expectations of their stakeholders (e.g., customers, employees, suppliers, local communities and regulatory bodies) (Gopalan et al., 2007). In response to increasing stakeholder concerns on social and environmental challenges, BG firms recognize the significance of meeting these expectations to build positive stakeholder relationships (Saiyed et al., 2023; Sung Kim & Oh, 2019). Therefore, they invest significantly in CSR, which is consistent with the tenets of SCT. Moreover, BG acknowledges the significance of efficient risk management. Due to a huge interdependency among affiliated sister firms and their operations, BGs are exposed to a number of risks (e.g., bad reputation and supply chain disruptions). These risks have the potential to negatively affect the group as a whole. The integration of CSR practices enables affiliated firms to take a proactive approach towards managing potential risks. CSR activities may include practices like ethical sourcing, environmental sustainability and the provision of employee welfare programmes. These practices not only mitigate risks but also minimize the adverse effect on overall BG performance. Moreover, BGs utilize synergistic effects and cost advantages in their CSR activities. For example, by sharing tangible resources, knowledge and expertise among affiliated firms, they can effectively coordinate and pool resources to undertake CSR initiatives on a larger scale. As a result, it would enhance the efficacy of their CSR activities and optimize resource allocation across the group (Gopalan et al., 2007). It is also critical for BGs to follow legal and regulatory needs as they operate in various industries and geographical locations. CSR enables firms to take a proactive approach to meeting regulatory requirements, and thereby, ensure compliance with social and environmental norms. Compliance with such regulations not only facilitates risk management but also establishes the group’s reputation as a responsible business entity. Finally, BG firms prioritize long-term strategies for sustainability. As a result, they align CSR investments with the overarching vision and long-term success of the organization. In other words, BG firms focus on creating sustainable value for both present and future stakeholders by considering the social and environmental impact of their business operations. The emphasis on long-term objectives holds significant relevance for family-owned businesses, as CSR plays a critical role in facilitating succession planning and safeguarding the family’s heritage.

In light of the above discussion, it can be argued that affiliated firms tend to allocate more resources towards CSR initiatives (Cuervo-Cazurra, 2018) as they tend to rely more on relational/social capital for various transactions (Pant et al., 2021). They do this in a way to enhance their public image, address diverse stakeholder interests, reduce risks, comply with regulatory requirements and prioritize long-term sustainable performance (Sung Kim & Oh, 2019). However, this is in contrast to SVT, which emphasizes maximizing shareholder returns (Godfrey et al., 2009; Manchiraju & Rajgopal, 2017; Martin et al., 2009; O’Connell & Ward, 2020), and therefore, CSR investments may be recognized as a misallocation of resources from core business activities (Cuervo-Cazurra, 2018). BGs understand that the unethical behaviour of a single affiliated firm can have a spillover effect, leading to a negative impact on all affiliated firms’ reputations. Hence, BG firms may tend to have a greater inclination towards investing in CSR, which could potentially lead to a decline in their financial performance. Prior studies have argued that the costs associated with CSR initiatives for BG firms may outweigh the financial benefits in the short term. However, these costs are often considered investments in building long-term relationships, brand value and intangible assets that can positively impact the financial performance of the entire BG in the long run.

3.1. Data

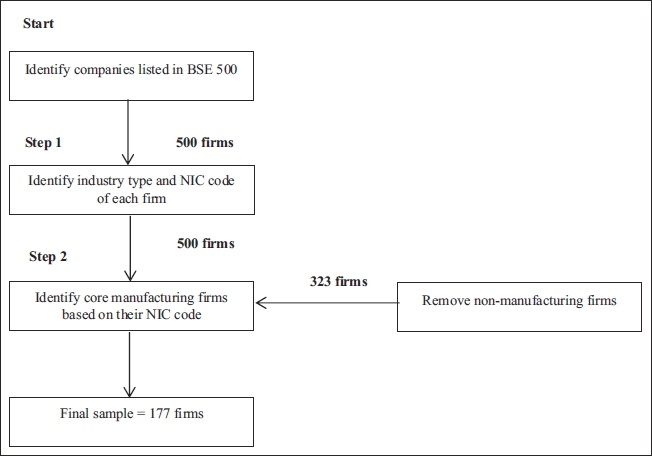

To empirically address our proposed research questions (see Section 1), this study relies on the Prowess database as the primary source of information. Prowess is controlled by the Centre for Monitoring Indian Economy (CMIE). In 1976, renowned economist Dr Narottam Shah established CMIE. It is the most reputable secondary source of information on Indian companies, both public and private. A number of significant research in the fields of corporate finance and strategic management, including Gopalan et al. (2007) and Siegel and Choudhury (2012), have made use of the Prowess database. Starting from 1989, the Prowess data set collects information on over 1,500 financial factors. Additionally, it includes details on board composition, ownership structure and BG affiliation. We collect panel data on the CSR investment intensity and the organizational structure for all firms listed in the BSE 500 during the time frame of 2015–2022. Inspired by Popli et al. (2017), our study classifies companies according to their organizational structure by ascertaining whether they are associated with a BG or not. The detailed data collection process is shown in Figure 1.

Data Collection Process.

Data Collection Process.

3.1.1. Variables

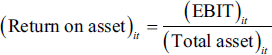

Considering past literature (e.g., Lu & Shang, 2017; Mackelprang et al., 2015), we use return on assets (ROA) as our main dependent variable. ROA is the most reliable accounting measure because it is a true representation of operational efficiency, management effectiveness and profitability (Hull & Rothenberg, 2008). It is calculated as follows:

where EBIT = Earning before interests and taxes.

The key independent variable used in this study is CSR-related investment. Inspired by Coelho et al. (2023), we have used annual CSR expenditure as the proxy for CSR-related investment. In our study, BG affiliation is considered the moderating variable. Inspired by Siegel and Choudhury (2012), the firm’s affiliation to a BG is determined in the following binary representation:

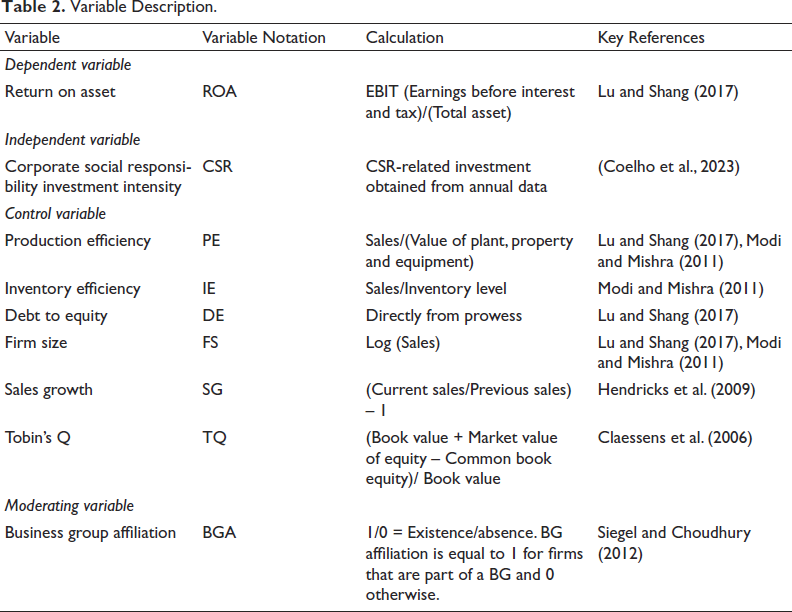

The detailed information on dependent, independent, moderating and control variables used in this study is presented in Table 2.

Variable Description.

3.2. Methodology

We conduct multiple regression analyses examining: (a) the impact of CSR investment on firm performance, (b) the CSR investment intensity among BG and standalone firms, and (c) the moderating effect of BG affiliation on the CSR investment intensity–firm performance relationship. All regression models include industry and year effects, with robust standard errors accounting for heteroscedasticity (Amin et al., 2015). Based on the Hausman test, we find the random effect estimator more suitable for our model (Baltagi, 2008; Baltagi et al., 2003; Torres-Reyna, 2007). Accordingly, we employ a random effect panel data regression methodology for all models. Table 2 provides detailed information on variables used in the following regression model.

3.2.1. CSR Investment Intensity and Firm Performance

To examine the relation between CSR investment intensity and firm performance (proxied by ROA), we use Equation (1) as a baseline model to test our first research question, where subscripts refer to firm i at time t.

where ROA: Return on assets; PE: Production efficiency; IE: Inventory efficiency; DE: Debt-to-equity ratio; FS: Firm size; SG: Sales growth; TQ: Tobin’s Q; ID: Industry dummy; YD: Year dummy; E: Error.

3.2.2. CSR Investment Intensity

Past research asserts that BG firms tend to rely more on social and relational capital with their stakeholders. Therefore, it can be construed that BG-affiliated firms will have significantly higher CSR investment intensity due to their excessive focus on reputation and brand image. To analyze this hypothesis, we estimate the t-test using Equation (2).

3.2.3. Moderating Role of BG Affiliation

As discussed, BG firms tend to have a very high CSR investment intensity relative to their counterparts and therefore, create a possibility that they might have lower bottom-line performance. Therefore, we argue that BG affiliation will negatively moderate the relationship between CSR investment intensity and firm performance. To test this hypothesis, we estimate Equation (3):

where ROA: Return on assets; BGA: Business group affiliation; PE: Production efficiency; IE: Inventory efficiency; DE: Debt-to-equity ratio; FS: Firm size; SG: Sales growth; TQ: Tobin’s Q; ID: Industry dummy; YD: Year dummy; E: Error.

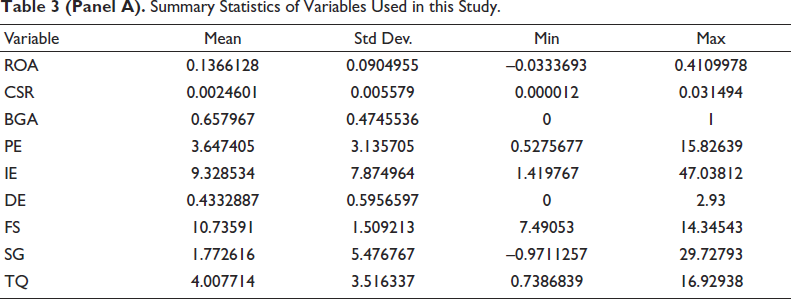

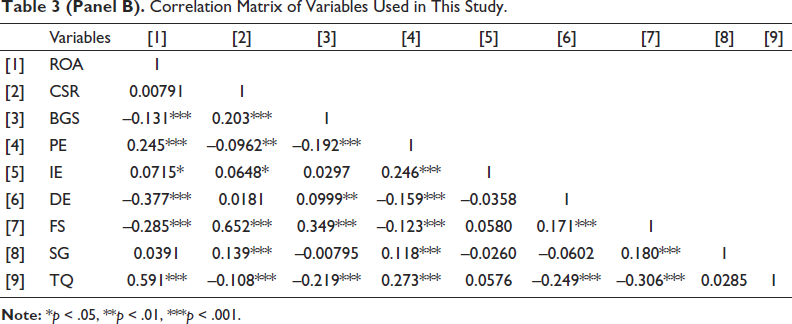

3.3. Correlation Matrix and Summary Statistics

The correlation matrix and summary statistics are presented in Table 3 (Panel A and Panel B). It has been done to get a preliminary indication of the CSR–performance relationship. For instance, the correlation matrix reports that there is an insignificant relation between CSR and ROA. However, we note that the univariate analysis may be misleading as it overlooks potential confounding effects.

Summary Statistics of Variables Used in this Study.

Correlation Matrix of Variables Used in This Study.

4.1. CSR Investment Intensity and Firm Performance

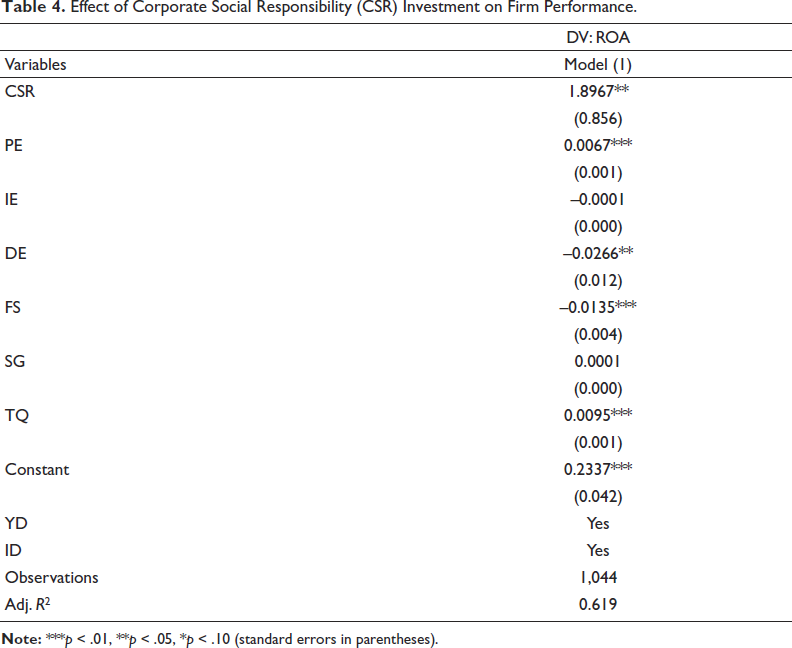

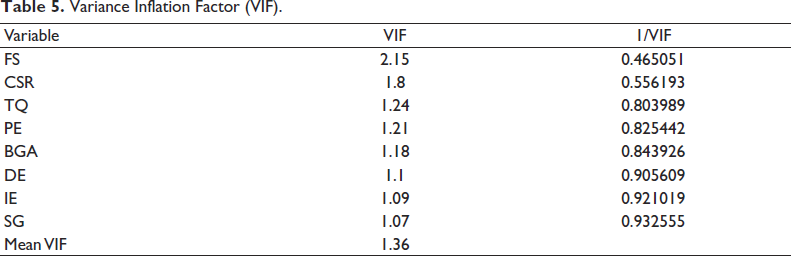

Equation (1) estimates the association between CSR investment and the performance of a firm, as measured by its ROA. The outcomes of this analysis are displayed in Table 4. As shown in Model (1), the coefficient on CSR is positive and statistically significant (β = 1.8967, p < .05). It indicates that a one standard deviation increase in CSR investment increases the ROA by two basis points. This result is consistent with prior literature that supports the bright side of CSR investment and indicates that CSR investment facilitates social capital between a firm and its stakeholders, which consequently results in better performance (Asiaei et al., 2023; Husaini et al., 2023; Ikram et al., 2019; Sen & Cowley, 2013; Soundararajan & Brown, 2016). This study has conducted an assessment of multicollinearity by computing variance inflation factors (VIFs). The results of this analysis, which are presented in Table 5, indicate that VIF values ranged from 1.07 to 2.15, suggesting that multicollinearity is not a significant concern (Popli et al., 2017). In summary, the findings provide evidence in favour of the positive performance effect of CSR investment and, thereby, are consistent with the tenets of SCT.

Effect of Corporate Social Responsibility (CSR) Investment on Firm Performance.

Effect of Corporate Social Responsibility (CSR) Investment on Firm Performance.

Variance Inflation Factor (VIF).

4.2. CSR Investment Based on Organizational Structure

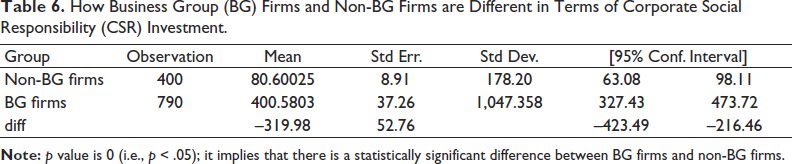

According to Pant et al. (2021), organizational structure can be categorized in terms of BG firms and non-BG firms (or standalone/independent firms). Prior studies argue that BG firms heavily rely on social or relational capital (Saiyed et al., 2023; Pant et al., 2022). In light of this, we believe that BG firms are likely to invest or engage more in CSR compared to their counterparts as they strategically create a good image and brand reputation through social capital. Accordingly, we have done t-tests (based on Equation (2)) and the results are presented in Table 6. It shows that BG firms and independent firms differ in terms of CSR investment intensity. The magnitude presented in Table 6 is higher for BG firms. Consistent with SCT, it implies that BG firms invest more in CSR compared to independent firms.

How Business Group (BG) Firms and Non-BG Firms are Different in Terms of Corporate Social Responsibility (CSR) Investment.

4.3. Moderating Role of BG Affiliation

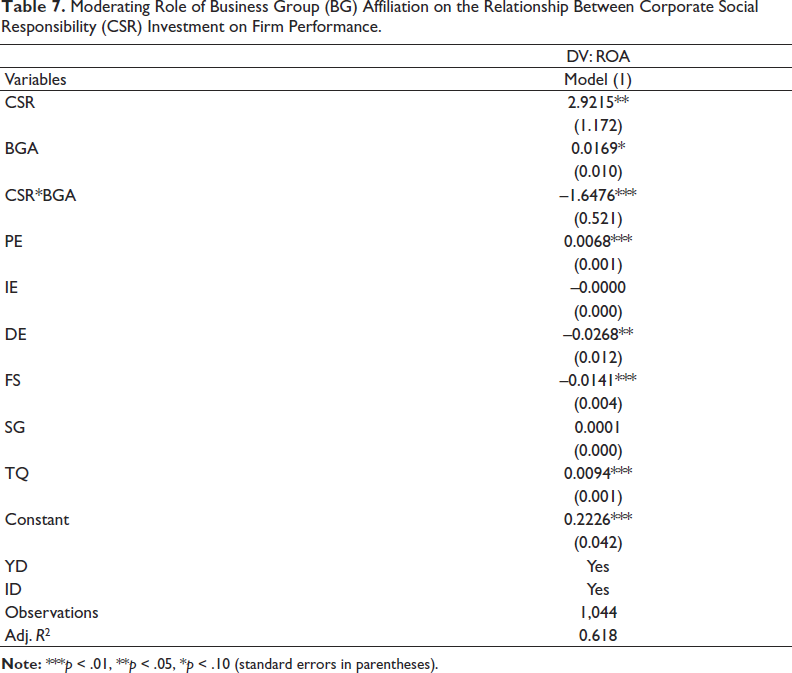

Our empirical results reveal that BG firms tend to invest significantly more than standalone firms to enable social and relational capital as shown in Table 7. Therefore, in this section, we examine the performance of BG firms based on their CSR investment strategy. Table 7 presents the results of model 1 that show the role of the interaction term (CSR × BGA) on ROA. The coefficient on CSR × BGA is negative and statistically significant (β = –1.6476, p < .01). The findings indicate that the BG firms’ CSR investment intensity is significantly higher compared to independent firms, and therefore, they experience lower financial performance (Purkayastha & Gupta, 2023). It can be construed that the huge reliance on social capital pulls down the financial performance of BG firms (Richter & Chakraborty, 2023; Pant et al., 2022). Building on SVT, this result argues that BG affiliation will negatively moderate the relationship between CSR investment intensity and firm performance, such that the positive effect of CSR on firm performance will diminish.

Moderating Role of Business Group (BG) Affiliation on the Relationship Between Corporate Social Responsibility (CSR) Investment on Firm Performance.

4.4. Additional Tests

4.4.1. Alternate Direct Measures of Performance

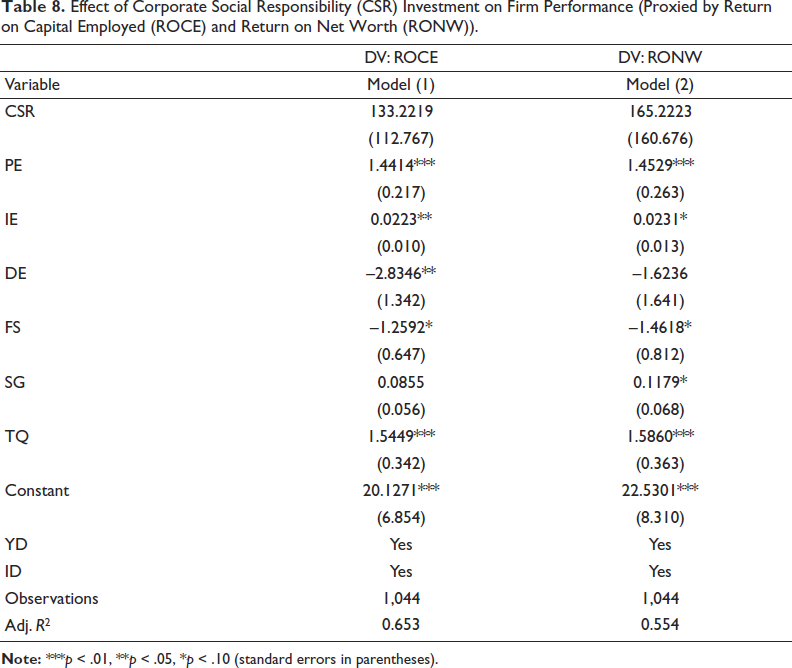

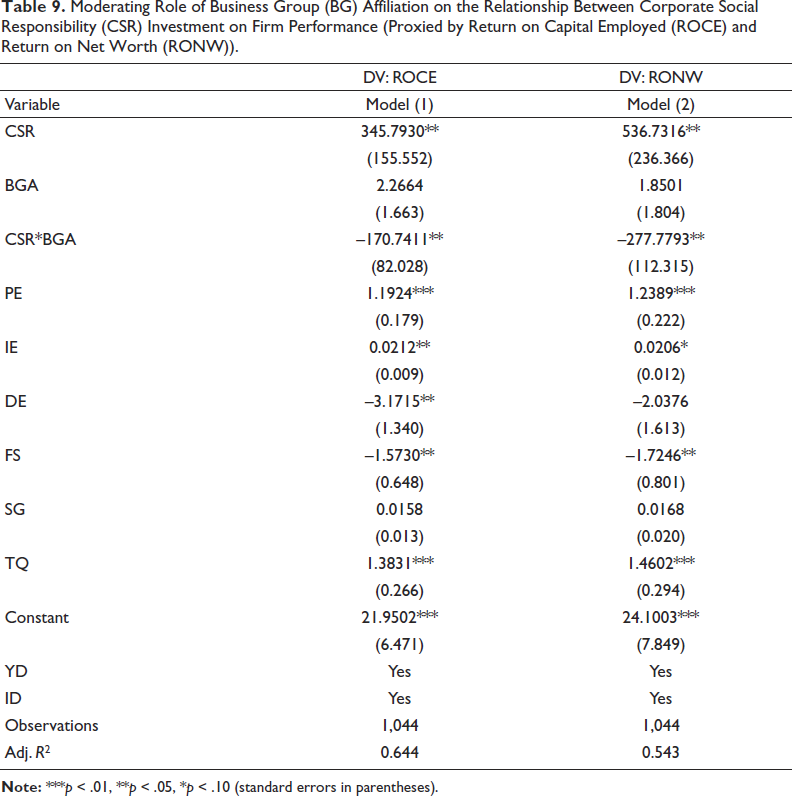

We carry out additional tests with direct measures of firm performance, namely return on capital employed (ROCE) and return on net worth (RONW). The results are qualitatively similar and ensure that our main findings are robust as shown in Tables 8 and 9.

Effect of Corporate Social Responsibility (CSR) Investment on Firm Performance (Proxied by Return on Capital Employed (ROCE) and Return on Net Worth (RONW)).

Moderating Role of Business Group (BG) Affiliation on the Relationship Between Corporate Social Responsibility (CSR) Investment on Firm Performance (Proxied by Return on Capital Employed (ROCE) and Return on Net Worth (RONW)).

4.4.2. Addressal of Endogeneity Concerns

The issue of potential endogeneity may arise due to the omitted variables bias, autocorrelation and heteroscedasticity in sample selection (Guide Jr & Ketokivi, 2015). The issue of endogeneity may be addressed through the utilization of panel data sets and generalized method of moments (GMM) and the 2SLS method using instrument variables. However, according to Roodman (2009), GMM and 2SLS methods often suffer from instrument proliferation and weak identification issues in small to moderate sample sizes. Therefore, the present study has employed panel data sets as a means to tackle the potential issue of endogeneity, as noted by Ketokivi and McIntosh (2017). Furthermore, our empirical approach involves the collection and construction of control variables that have been identified in the literature as having an impact on financial performance. Put differently, we aim to include variables in our regression analysis that, if left out, may give rise to endogeneity issues. In a recent study, Shang et al. (2017) utilize the control variable technique in lieu of the instrument variable approach. It is acknowledged that, despite the extensive range of controls employed in this investigation, achieving complete elimination of endogeneity is improbable, thereby constituting a constraint of this research. Furthermore, inspired by Baltagi (2008) and Torres-Reyna (2007), all our panel ordinary least squares (OLS) models incorporate industry and year effects and robust standard errors to mitigate issues of heteroscedasticity and autocorrelation.

In panel data regression analysis, lagged independent variables were also employed to obtain unbiased estimates. Incorporating a lagged independent variable in the models is a sensible approach because the current ROA level can heavily rely on past CSR engagement, sales growth and debt-to-equity ratio. Failing to include a lagged independent variable in such instances would result in omitted variable bias. Consequently, all regression models were re-run with lagged control variables to validate the robustness of the primary findings. It was observed that the results remained qualitatively consistent with the main findings. While the detailed results are not reported here, they are available upon request.

In conclusion, while it is difficult to completely eliminate the possibility of endogeneity, our study incorporates several approaches to mitigate the potential endogeneity.

This study investigates the association between CSR investment intensity and firm performance, taking into account the organizational structure and SCT. The analysis utilizes a firm-level panel data set from 2015 to 2022. Drawing from the operations management literature (Masulis et al., 2023; Pathak et al., 2014; Saiyed et al., 2023), we employ a firm’s association with a BG as a means of approximating its organizational framework. First, we investigate the relation between CSR investment and ROA. The findings of our study indicate that the allocation of capital resources towards CSR initiatives has a significant positive effect on ROA (Asiaei et al., 2023; Husaini et al., 2023; Ikram et al., 2019; Sen & Cowley, 2013; Soundararajan & Brown, 2016). Drawing from the SCT, it can be construed that a firm’s active involvement in CSR initiatives can facilitate social capital between the firm and its stakeholders, ultimately resulting in improved firm performance (Sung Kim & Oh, 2019). This is consistent with the findings of Sarwar et al. (2024). Using 438 UK, 520 Italian and 354 Pakistani hotels, they reveal that CSR is critical for sustainable performance and competitive advantage. With the help of 253 non-financial companies listed on the Indonesian Stock Exchange, Husaini et al. (2023) report a positive CSR–performance relationship. They also report that the CSR–performance link can be strengthened if firms implement risk management optimally. According to Asiaei et al. (2023), CSR positively impacts organizational performance, and the performance management system (PMS) mediates the CSR–performance relationship in publicly listed firms in Iran. Pant et al. (2022) assert that there exists a significant interdependence among BG firms with respect to technology, internal capital markets, brand image, reputation and capital. Therefore, it can be observed that BGs tend to allocate greater resources towards CSR initiatives owing to their recognition of the significance of their reputation and brand image (Saiyed et al., 2023). This is not limited to individual firms within the BG but extends to the BG as a collective entity (Sung Kim & Oh, 2019). The results of this research support our assertions and indicate that firms operating in a BG set-up exhibit a CSR investment that is roughly five times greater than that of independent firms. Subsequently, it has been revealed that business organizations with a high level of investment in CSR exhibit lower performance outcomes. In other words, BG affiliation moderates the relationship between CSR investment and firm performance, such that the positive effect of CSR investment diminishes. One possible explanation for this phenomenon is the significant decrease in EBIT resulting from overallocation of resources towards CSR initiatives. This result is in line with the findings of Coelho et al. (2023) and Banker et al. (2023), which used samples from emerging and developed nations. They highlight that CSR–performance relationship dynamics can be influenced by moderating factors (e.g., organizational structure, ESG, financial constraints and information asymmetry). Their findings suggest that the CSR–performance relationship becomes more significant as the firm’s environmental, social and governance (ESG) scores improve. The present research aligns with the theoretical framework of SCT, which posits that excessive dependence on social or relational capital can have a detrimental impact on the operational efficacy of a firm (Pant et al., 2022).

Alternatively, this article has also utilized alternate direct measures of firm performance, namely ROCE and RONW, and the results remain consistent with both measures. In addition, the findings of this study remain consistent with lagged regression models. These additional tests reveal that the proposed models are robust.

Conclusion

Building on SCT, this research investigates the performance impact of CSR investment for a large sample of Indian manufacturing firms, considering their organizational structure. The study specifically examines the performance effect of CSR investment intensity, considering organizational structure (particularly the BG affiliation). The research has utilized secondary panel data on Indian manufacturing firms from the Prowess database to address the above-mentioned research questions. The findings challenge the prevailing notion of CSR investment, indicating that its effects on performance are inconsistent across firms and conditional upon organizational structure. The results suggest that CSR investment positively impacts overall performance, addressing RQ1. Moreover, firms with a BG structure exhibit a negative moderating effect on the CSR investment–firm performance relationship, addressing RQ2. The findings of this research offer various theoretical and managerial implications, which are presented below.

6.1. Theoretical Implications

The findings of this study reveal that there is a positive correlation between CSR investment intensity and firm performance. It strengthens the argument that CSR initiatives promote social capital, trust, legitimacy and collaborative networks with stakeholders, thereby enabling firms to acquire valuable resources and support. This finding offers support to the tenets of SCT. Moreover, the study’s findings highlight the significant role of a firm’s organizational structure in shaping its CSR investment intensity. Specifically, BG firms exhibit a significantly higher level of CSR investment compared to standalone firms. This is consistent with previous research suggesting that BG firms in developing economies prioritize social recognition and community engagement (Sung Kim & Oh, 2019). The higher CSR investment intensity among BG firms may be a strategic decision to mitigate potential negative spillover effects from misconduct by any affiliated firm within the group (Choi et al., 2018). In addition, the study finds that the organizational structure (e.g., BG affiliation) moderates the relationship between CSR investment intensity and firm performance. While CSR investment has a positive impact on performance for both BG firms and standalone firms, the magnitude of this effect is significantly lower for BG firms. This finding suggests that the potential benefits of CSR investments, such as enhanced social capital and stakeholder relationships, may be partially offset by the higher investment intensity among BG firms, leading to a relatively lower financial performance compared to standalone firms.

6.2. Managerial Implications

The positive relationship between CSR investment intensity and firm performance highlights the importance of strategic CSR investments for enhancing organizational performance. Managers should recognize the potential of CSR initiatives to promote trust, reputation and collaborative networks with stakeholders, which can consequently translate into improved financial outcomes. However, it is critical to establish a balance between CSR investments and core business operations to ensure optimal resource allocation and long-term profitability. Moreover, managers should consider their firm’s organizational structure when formulating CSR strategies. BG firms, which tend to have higher CSR investment intensities, may need to carefully evaluate the potential trade-offs between the benefits of CSR (e.g., enhanced social capital) and the associated costs. These firms could explore opportunities to optimize their CSR investments and leverage group-level synergies to maximize the returns on their CSR efforts. In addition, the positive impact of CSR investments on firm performance highlights the importance of effective stakeholder engagement and communication. Managers should proactively engage with their stakeholders, communicate the firm’s CSR initiatives and show their commitment to social and environmental responsibilities. It should be noted that by creating transparent and collaborative relationships with stakeholders, firms can enhance their social capital and reputation and, therefore, improve financial performance. While the study has focused on Indian manufacturing firms, managers should consider the contextual factors specific to their industry, geographic location and cultural environment when formulating CSR strategies. The relative importance of CSR dimensions (e.g., environmental, social, governance) and stakeholder expectations may vary across contexts; therefore, a tailored approach is required for CSR investments and stakeholder engagement.

6.3. Limitations and Future Research Directions

While making significant contributions to the body of literature, this study has certain limitations that present opportunities for future research. First, it focuses solely on the manufacturing sector; future studies could explore other industries like services or mining to assess the generalizability of findings. Second, the timeframe of this study (2015–2022) does not account for potential macroeconomic shocks (e.g., the COVID-19 pandemic), which may have significantly altered CSR policies. Future research should consider such macroeconomic shocks to better understand their impact on the CSR–performance relationship. Third, it is observed that our R2 value varies in the range of 54.3%–64.4%. This implies that a significant amount of within-firm heterogeneity remains unexplained (Markarian & Parbonetti, 2007). Therefore, in future research, scholars can utilize large and longitudinal data across different sectors to reduce heterogeneity within the firm. Fourth, out of 208 manufacturing firms listed on the BSE 500, we have consistent CSR data on 170 firms. In other words, in the present study, the estimated effect of CSR is based on 170 firms. Therefore, there can be a possibility of potential sample selection bias. Put differently, if we had data for all 208 firms, would the estimates change systematically? Future studies can address such sample selection bias issues using Heckman’s sample selection model. Finally, this study utilizes financial performance metrics to evaluate CSR impact; future research could investigate supply chain metrics such as buyer–supplier relationship value, flexibility and quality. Despite these limitations, the study makes valuable contributions to the CSR literature and sets the groundwork for future research into the dynamic inter-relationship between CSR, organizational structure and firm performance.

Footnotes

Acknowledgement

The authors acknowledge the support of the Institute of Management Technology Hyderabad in providing all the necessary facilities in terms of software and databases in a way to execute this research.

Authors’ Contribution

Conceptualization: Pushpesh Pant

Data collection: Pushpesh Pant and Tulika Sharma

Software: Pushpesh Pant and Tulika Sharma

Writing: Original draft preparation: Pushpesh Pant and Tulika Sharma

Writing: Review and editing: Pushpesh Pant

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.