Abstract

This study examines the bidirectional relationship between environmental, social and governance (ESG) performance and firm performance in the global pharmaceutical sector, employing a cross-lagged panel model for 255 firms from 2016 to 2022. Using Bloomberg ESG scores and three performance metrics, namely return on assets (RoA), return on invested capital (RoIC) and Tobin’s Q, we uncover nuanced, non-linear relationships. Results indicate that lagged ESG performance positively influences accounting-based measures (RoA and RoIC), supporting the notion that sustainability investments yield operational efficiencies over time. However, market-based valuation (Tobin’s Q) exhibits a U-shaped relationship, suggesting initial investor scepticism followed by long-term rewards for persistent ESG commitment. On the other hand, financial performance does not consistently drive subsequent ESG improvements, rejecting reverse causality. The inverted U-shaped relationship for RoIC aligns with the environmental Kuznets curve (EKC), revealing diminishing returns to ESG investments beyond a threshold. These findings contribute to stakeholder and signalling theories, demonstrating that ESG integration enhances financial resilience while highlighting market inefficiencies in pricing sustainability. The study advances the ESG–performance literature by providing sector-specific insights, emphasizing the strategic value of ESG in pharmaceuticals, where regulatory and reputational stakes are high. Policymakers and managers can leverage these insights to optimize ESG resource allocation and improve disclosure frameworks.

Introduction

The concept of sustainability, first formally defined by the Brundtland Commission (1987) as meeting present needs without compromising future generations’ ability to meet theirs, has evolved into a critical business imperative. Dyllick and Hockerts (2002) operationalized this concept at the firm level, emphasizing the dual requirement of satisfying stakeholder needs while maintaining future operational capacity. This imperative becomes particularly salient given that modern production and consumption generate substantial toxic waste and depend heavily on non-renewable resources.

Financial research has established the materiality of environmental and social disclosures for market participants (Bernardi & Stark, 2018). The environmental Kuznets curve (EKC) hypothesis suggests an inverted U-shaped relationship between economic development and environmental degradation at the macro level, a pattern that may extend to firm-level dynamics. Supporting this micro-level application, Broadstock et al. (2018) demonstrated that financially constrained firms exhibit poorer environmental performance, implying that enhanced firm performance enables greater environmental stewardship. These findings emphasize the importance of examining the environmental, social and governance (ESG)–performance relationship.

The biopharmaceutical sector presents a compelling case study of these tensions. While single-use disposable systems reduce contamination risks, they generate approximately 30,000 tons of plastic waste annually through landfilling and incineration (Kaylor, 2024). Concurrently, the European ESG investment market is projected to exceed $18 trillion in assets under management by 2030 (Mahtani, 2024), creating strong incentives for firms to improve their ESG profiles, both to mitigate risks and capture sustainability-linked opportunities.

Energy consumption represents another critical challenge, with the pharmaceutical sector producing 193 million metric tons of CO2 in 2022 (Kaylor, 2024). The sector’s energy-intensive processes demand urgent adoption of alternative energy sources and efficiency measures. These environmental impacts carry significant human costs, as climate change increasingly threatens basic necessities (clean air, water, food security and others) and exacerbates health disparities (Williams, 2024).

The pharmaceutical and biotechnology sectors face the dual challenge of implementing environmentally sustainable practices while maintaining rigorous safety standards amid complex regulatory requirements (Kaylor, 2024). This challenge is further compounded by the global proliferation of counterfeit drugs affecting both generic and branded medications (Khan & Khar, 2015). In response, industry leaders are increasingly adopting standardized frameworks, such as the Science Based Targets initiative (SBTi), to establish verifiable climate goals and improve ESG disclosure quality.

This strategic shift reflects a growing recognition that sustainable operations are critical for both industry viability and societal welfare. As stakeholder demands for corporate accountability intensify, the integration of ESG principles into core business strategies has become imperative for building organizational resilience and ensuring long-term competitiveness. Within this context, the pharmaceutical sector’s substantial energy consumption and its social impact on human health emerge as particularly critical dimensions requiring focused examination.

Literature Review

Theoretical Background

Contemporary firms face significant social and political pressures to maintain their social contracts for organizational survival. This has heightened recognition of the role of stakeholder engagement in shaping sustainability narratives. Corporate disclosures often emerge as legitimizing mechanisms in response to environmental factors (Guthrie & Parker, 1989). Legitimacy theory suggests stakeholders intrinsically value social and environmental sustainability, prompting firms to align disclosures with societal expectations. Non-compliance risks organizational legitimacy and financial sustainability.

However, Guthrie and Parker’s (1989) Australian research challenges legitimacy theory’s universal applicability as a primary driver of social reporting. Alternatively, signalling theory posits that higher-performing firms voluntarily disclose sustainable practices beyond mandatory requirements. The incomplete revelation hypothesis supports this view, showing firms present positive earnings reports more readably than negative ones (Bloomfield, 2002), suggesting favourable information spurs voluntary disclosure.

Stakeholder theory addresses the interests of a firm’s diverse internal and external constituencies. Notably, European boards do not universally prioritize shareholder wealth maximization (Denis & McConnell, 2003). The theory connects fundamentally to corporate social responsibility (CSR), defining appropriate corporate conduct while pursuing profitability, stability and growth (Campbell, 2007). Effective stakeholder engagement fosters innovation by identifying emerging trends and unmet needs, while building crisis resilience through stronger community relationships. A holistic approach integrating social, environmental and economic dimensions creates sustainable value benefiting both firms and society.

Stewardship theory asserts that collective long-term interests should prevail over individual objectives, emphasizing trust and collaboration among stakeholders (Hernandez, 2012). The Madoff Ponzi scheme exemplifies the consequences of prioritizing personal gain over collective welfare, demonstrating how such behaviour undermines both stakeholder interests and organizational sustainability. Distinct from agency theory’s shareholder wealth maximization paradigm, stewardship theory incorporates sociological and psychological principles to promote pro-social behaviour that transcends short-term self-interest (Hernandez, 2012). This perspective defines stewardship as the willingness to subordinate personal interests to protect collective long-term benefits, thereby emphasizing sustainability.

Transparency-focused complementary theoretical perspectives, like legitimacy and signalling theories, inform our approach in this study. As discussed above, legitimacy theory emphasizes disclosures as a legitimizing mechanism, and signalling theory suggests firms selectively disclose positive information (Bloomfield, 2002). Both underscore transparency’s importance. We operationalize these concepts using ESG scores as comprehensive metrics of organizational performance across ESG dimensions, consistent with stakeholder theory’s emphasis on addressing diverse stakeholder needs.

The future-oriented nature of sustainability makes stewardship theory particularly relevant for examining the EKC hypothesis. This framework allows us to analyze the dynamic relationship between ESG performance and firm performance over time, revealing how sustainable practices enhance long-term organizational viability. By investigating the financial implications of ESG initiatives, our study elucidates the interconnection between ethical practices and economic success. These insights can inform organizational decision-making that aligns strategic objectives with societal responsibilities, promoting sustainable business ecosystems.

Empirical Studies and Hypotheses

Recent studies challenge the conventional unidirectional focus on ESG–performance relationships by examining reciprocal effects. Hamdi et al. (2022) demonstrated positive bidirectional correlations between ESG initiatives and firm performance in US markets, while Nekhili et al. (2021) revealed conditional investor responses among French firms, showing ESG engagement generally attracts positive sentiment except when employees hold board seats. Their findings further indicate that performance–ESG effects vary across ESG dimensions during periods of policy uncertainty and oil price volatility. These context-dependent relationships (Behl et al., 2022) motivate our bidirectional hypotheses:

H1a–c: Lagged ESG positively affects return on assets (RoA), return on invested capital (RoIC) and Tobin’s Q.

H1d–f: Lagged performance (RoA, RoIC and Tobin’s Q) positively affects ESG.

Region-specific analyses reveal nuanced patterns. US evidence shows that ESG disclosures enhance overall performance, although environmental/CSR components exhibit divergent effects, depressing RoA while boosting Tobin’s Q (Alareeni & Hamdan, 2020). European markets similarly show ESG’s positive association with Tobin’s Q (Dkhili, 2024). A meta-analysis of 2,000 studies confirms predominantly non-negative ESG–financial performance relationships (Friede et al., 2015), though effects are context-dependent. Yoon et al. (2018) found that ESG’s market pricing impact in South Korea weakens significantly in environmentally sensitive industries.

Recent studies demonstrate nuanced relationships between ESG practices and corporate performance. Kim and Li (2021) identified a positive ESG–profitability correlation, particularly for large firms, with governance factors proving most impactful in weakly governed firms. Institutional investors show preferential weighting towards governance and environmental metrics over social factors, reflecting stronger market responses to shareholder rights and emissions performance (Park & Jang, 2021). Patel et al. (2021) further established that ESG performance improvements reduce long-term implied volatility, influencing investment decisions through enhanced predictability.

Cross-country evidence reveals differential impacts. Mardini (2022) has documented positive ESG effects on both market-based (Tobin’s Q) and accounting-based (RoA) metrics across 35 countries, though social factors exhibit negative financial impacts. Reporting quality significantly moderates these relationships, with integrated reporting outperforming standalone disclosures (Mervelskemper & Streit, 2017). Institutional ownership emerges as another key determinant, amplifying ESG performance particularly in firms with strong ex ante ESG potential (Liu et al., 2019). In a study of 512 Indian companies, it was observed that ESG enhances firm valuation (Yadav, 2025).

Sector-specific analyses yield complementary insights. Shariah-compliant Malaysian firms show positive ESG–performance linkages (Lee & Isa, 2023), while Giakoumelou et al. (2022) demonstrated ESG’s crisis-period insurance value during the 2008 financial downturn. These studies direct us to probe if (a) there is a significant positive association between ESG and accounting-based firm performance (H2a) and (b) there is a significant positive association between ESG and market-based firm performance (H2b).

The EKC framework provides theoretical grounding for these hypotheses. The inverted U-shaped EKC relationship suggests that initial environmental degradation during early development phases gives way to improved environmental quality at higher income levels (Broadstock et al., 2018). This pattern emerges from (a) initial development phases that focus on output maximization over environmental externalities (Kula, 1997); (b) subsequent productivity gains reducing emissions intensity and (c) eventual diminishing returns to scale in pollution reduction.

Early economic models treated environmental resources as free goods, encouraging overconsumption and pollution externalities. The sustainability paradigm shift has driven academic interest in ESG–performance relationships within this EKC framework, typically assuming emissions reductions accompany economic scale.

Recent sectoral analysis of global energy firms reveals a non-linear, inverted U-shaped relationship between sustainability performance and corporate financial outcomes (Kumar et al., 2022). This pattern demonstrates that in the initial phase, improved financial performance correlates with reduced sustainability reporting and in the subsequent phase, beyond a threshold, further financial gains accompany enhanced reporting quality. This finding aligns with the EKC framework, suggesting that firms initially prioritize financial performance at the expense of sustainability disclosures before reaching an inflection point where both objectives become complementary. Building on this evidence, we hypothesize that the relationship between ESG performance and firm performance follows a non-linear (inverted U-shaped) pattern (H3).

Materials and Methods

Our analysis utilizes data for the top 255 pharmaceutical companies by market capitalization (2016–2022) sourced from Bloomberg. We examine the bidirectional ESG–performance relationship using a cross-lagged panel model with three performance measures: RoA, RoIC (accounting-based) and Tobin’s Q (market-based). ESG scores, derived from Bloomberg’s comprehensive evaluation of 800+ disclosure parameters (Behl et al., 2022), serve as our independent variable. In the pharmaceutical industry, Bloomberg assigns equal weight to the environmental (E), social (S) and governance (G) dimensions of ESG assessment. Within the environmental pillar, key indicators include climate risk, resource efficiency and emissions management. The social dimension encompasses factors such as human capital management, health and safety standards and supply chain practices. Under the governance component, Bloomberg evaluates parameters including executive remuneration, board independence, audit quality, shareholder rights, diversity, entrenchment and instances of overboarding.

To test for non-linearity (H3), we estimate eit = α + β1pit + β2pit2 + ɛ, where eit = firm performance metric; pit = ESG score and ∊ = error term.

This specification follows Broadstock et al. (2018) in capturing potential quadratic relationships. We complement this with quadratic fit curve estimation and nested regression analysis for robustness.

Performance metrics are calculated as follows: RoA = net income/total assets; RoIC = Net operating profit after tax (NOPAT)/average invested capital and Tobin’s Q = market value/asset replacement cost

The EKC framework informs our expectation of an inverted U-shaped relationship. Initial development phases show firms prioritizing profits over sustainability, while mature firms demonstrate enhanced productivity, reduced resource misallocation and greater societal impact consideration.

Our regression analysis strategically incorporates both linear and squared ESG terms to amplify the detection of non-linear effects, particularly for high ESG performers. This approach provides comprehensive insights into how varying ESG levels differentially affect performance outcomes.

Results and Discussion

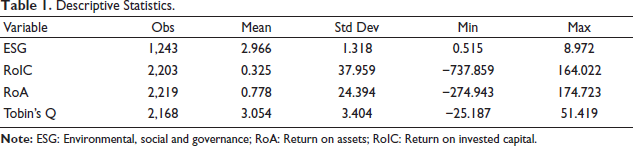

Table 1 reports the summary statistics for the primary variables. The ESG scores display considerable variation, reflecting pronounced heterogeneity in firms’ sustainability practices. The dispersion is even more evident in the financial performance indicators, that is, RoIC (mean = 0.325), RoA (mean = 0.778) and Tobin’s Q (mean = 3.054). This wide variability in performance measures encompasses both highly efficient firms and those facing profitability challenges, thereby offering a robust empirical setting to investigate the dynamics of the ESG–performance relationship.

Descriptive Statistics.

Descriptive Statistics.

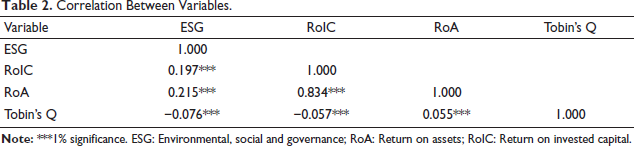

Table 2 reports correlation coefficients between ESG scores and performance measures. We find a positive correlation between ESG and RoIC, suggesting that sustainability-focused firms achieve superior capital returns potentially through enhanced investment attractiveness, stronger stakeholder relationships and improved regulatory compliance. We also observe a positive relationship between ESG and RoA, indicating ESG leaders demonstrate greater asset productivity, likely due to operational efficiencies from sustainable practices and consumer preference for responsible businesses. However, we observe a negative association between ESG and Tobin’s Q, revealing market scepticism about ESG firms’ growth potential, possibly due to perceived trade-offs between sustainability and profitability and longer time horizons for ESG benefits to materialize.

Correlation Between Variables.

The observed negative correlation between ESG performance and Tobin’s Q, in contrast to the positive accounting-based results, can be interpreted through the lens of signalling theory and market efficiency dynamics. In the short run, markets may undervalue firms with strong ESG commitments due to information asymmetry and reporting lags in recognizing the financial implications of sustainability initiatives. Investors may perceive ESG investments as cost-intensive activities that dilute near-term profitability, particularly when the benefits, such as risk mitigation, innovation capacity or reputational capital, materialize over longer horizons (Gregory et al., 2014; Krüger, 2015). This short-term bias, often described as investor myopia, leads to underpricing of ESG-oriented firms until verifiable performance outcomes emerge (Flammer, 2015).

Moreover, the absence of standardized disclosure frameworks and the evolving nature of ESG metrics exacerbate interpretive uncertainty, constraining markets’ ability to accurately price sustainability-related information (Dyck & Zingales, 2002; Fatemi et al., 2018). Within the pharmaceutical industry, where ESG initiatives frequently involve long-term R&D investments, supply-chain overhauls and compliance adaptation, the delayed visibility of financial returns may further reinforce initial valuation discounts. Over time, as firms establish credible disclosure records and demonstrate the materiality of ESG-driven efficiency gains, markets tend to revise their expectations, consistent with signalling theory’s premise that credible, observable actions gradually reduce information asymmetry (Connelly et al., 2010).

These findings present a nuanced picture. While ESG correlates with stronger accounting performance, market valuations appear to discount sustainability efforts. This divergence suggests that investors may undervalue the long-term competitive advantages of ESG integration, focusing instead on short-term financial metrics.

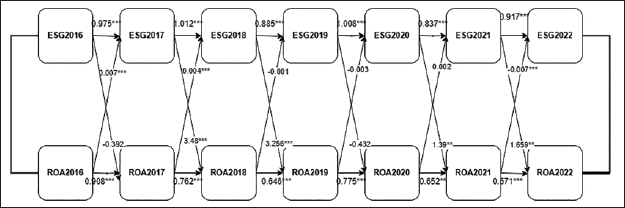

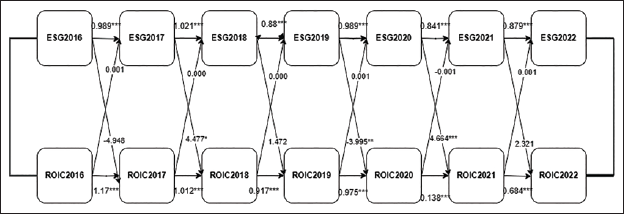

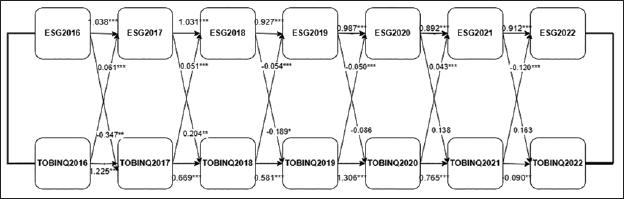

Our cross-lagged analysis reveals important asymmetries in the dynamic relationships between ESG performance and firm financial outcomes (see Figures 1 and 2). The results demonstrate that lagged ESG values exert a significant positive influence on current RoA and RoIC, thereby supporting H1a and H1b. This relationship holds consistently across our sample period, with the notable exceptions of 2017 and 2020, years marked by unique market conditions that may have temporarily disrupted the typical ESG–performance linkage. In contrast, we find no evidence of consistent reverse causality, as lagged values of RoA and RoIC show either insignificant or economically negligible effects on subsequent ESG performance, leading us to reject H1d and H1e.

The relationship between ESG and Tobin’s Q proves particularly complex, with our analysis yielding inconclusive results, characterized by a mixture of positive and negative coefficients of varying statistical significance across different time periods. Consequently, we are unable to establish reliable support for either H1c or H1f regarding bidirectional effects between ESG and market-based valuation metrics (see Figure 3). These findings regarding accounting-based performance measures align with the foundational work of McGuire et al. (1988) and Waddock and Graves (1997), while our null results for Tobin’s Q corroborate more recent evidence presented by Behl et al. (2022).

Cross-lagged Model of Environmental, Social and Governance (ESG) Score and Tobin’s Q.

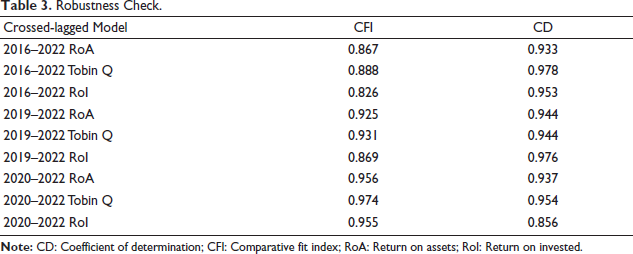

We conducted additional robustness tests using the comparative fit index (CFI) and the coefficient of determination (CD) to evaluate model adequacy (see Table 3). The cross-lagged regressions estimated for the 2016–2022 period yielded consistently significant coefficients of determination across all performance indicators, affirming the explanatory strength of the models. However, CFI values ranged between 0.82 and 0.88, marginally below the conventional threshold of 0.90, indicating an acceptable but suboptimal model fit. Restricting the sample to 2019–2022 improved the fit considerably, with CFI values of 0.925 for RoA, 0.931 for Tobin’s Q and 0.869 for RoIC. Further narrowing the analysis to the 2020–2022 window produced strong fit indices across all performance measures (CFI = 0.956 for RoA, 0.974 for Tobin’s Q and 0.955 for RoIC), confirming the model’s robustness. The results remained substantively unchanged, with ESG showing significant positive effects on RoA and RoIC, while its relationship with Tobin’s Q remained inconclusive. CFI was employed as the primary fit index due to its established reliability in evaluating measurement models (Goretzko et al., 2024).

Robustness Check.

The evolution of ESG reporting practices across jurisdictions provides additional context for these findings. While ESG disclosures have gained significant momentum globally, regulatory adoption remains uneven. Reporting continues to be voluntary in the United States, whereas in China, only 13.2% of firms disclosed ESG information as of 2021 (Shen et al., 2023). In India, mandatory ESG reporting requirements were introduced beginning in the 2022–2023 fiscal year. The limited disclosure coverage prior to 2018 likely contributed to marginal CFI values during the earlier sample period. Restricting the analysis to the recent three- and four-year windows, when ESG reporting became more institutionalized, yielded improved model fit and results consistent with the baseline estimations.

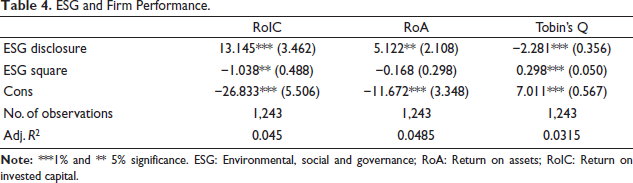

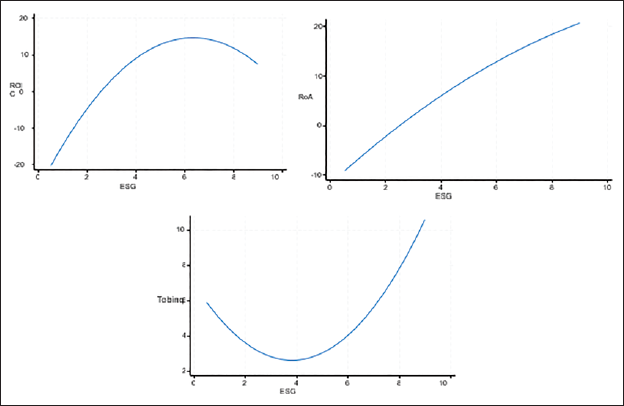

The examination of non-linear relationships through our quadratic specification yields several important insights. For accounting-based performance measures, we document distinct patterns: RoA maintains a consistently positive linear association with ESG scores, whereas RoIC follows a statistically significant inverted U-shaped trajectory (see Table 4).

ESG and Firm Performance.

This curvilinear pattern for RoIC suggests that initial improvements in ESG performance generate substantial efficiency gains in capital deployment, but that these benefits eventually face diminishing returns as firms reach higher levels of ESG commitment, potentially due to increasing marginal costs of additional sustainability investments.

Market valuations, as captured by Tobin’s Q, reveal an equally interesting but fundamentally different U-shaped relationship. This pattern indicates that equity markets initially discount firms’ ESG investments, possibly due to concerns about short-term profit sacrifices, but eventually reward sustained ESG commitment as the long-term competitive advantages become more apparent and quantifiable.

The mechanisms underlying these relationships warrant careful consideration. The linear positive association between ESG and RoA likely reflects direct operational improvements stemming from more sustainable business practices, including enhanced resource optimization, reduced waste streams and more efficient production processes (see Table 5). These operational efficiencies translate directly into improved profitability relative to the firm’s asset base. The inverted U-shape for RoIC suggests that while early-stage ESG improvements generate meaningful efficiency gains in capital allocation, the financial returns from additional ESG investments eventually decline as firms exhaust the most cost-effective sustainability opportunities. The U-shaped market valuation pattern for Tobin’s Q reveals important insights into investor psychology and market efficiency. Initial ESG investments appear to trigger investor scepticism about their financial merits, leading to valuation discounts. However, as firms demonstrate the durability and profitability of their sustainability transformations, the market appears to reappraise these firms more favourably, ultimately rewarding those that persist with substantial ESG commitments (see Figure 4).

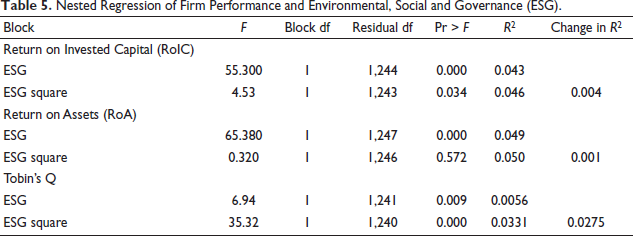

Nested Regression of Firm Performance and Environmental, Social and Governance (ESG).

These findings contribute significantly to several strands of existing literature. The non-linear relationships we identify for RoIC and Tobin’s Q provide empirical support for the theoretical frameworks developed by Lahouel et al. (2022) and Sun et al. (2019), while our linear results for RoA align with the earlier work of Barnett and Salomon (2012), Brammer and Millington (2008) and Chen et al. (2018). The differential patterns across performance metrics highlight the importance of considering both accounting- and market-based measures when assessing the financial impact of corporate sustainability initiatives. Additionally, the temporal asymmetries we document suggest that the financial benefits of ESG performance may require time to materialize fully and may follow different adoption curves across various dimensions of firm performance.

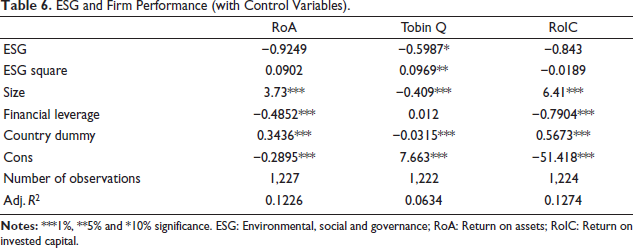

To ensure the robustness of our baseline findings, we augment our regression model with a comprehensive set of control variables. These include firm size, proxied by the natural logarithm of total assets, financial leverage and country-fixed effects to account for unobserved heterogeneity across national jurisdictions. The results of these augmented models are presented in Table 6.

ESG and Firm Performance (with Control Variables).

The analysis reveals a nuanced picture of the ESG–performance relationship, contingent upon the performance metric employed. Upon the inclusion of the control variables, the previously observed association between ESG performance and RoA becomes statistically insignificant. This finding suggests that the purported operational efficiencies and profitability gains from ESG may be partially explained by underlying firm characteristics, such as size and financial stability. It is consistent with the view that ESG-related expenditures (e.g., cleaner technologies, higher labour standards) may act as a short-term cost, offsetting immediate accounting profits or that their benefits are realized over a longer horizon than captured by annual RoA. In contrast, the positive and statistically significant association between ESG performance and Tobin’s Q remains robust. The persistence of this relationship, even after controlling for firm-level factors and country-fixed effects, indicates that the market valuation of the firm incorporates ESG performance beyond what is reflected in current-period earnings.

The divergence between the accounting- and market-based results is theoretically suggestive. It aligns with the premise that capital markets, while largely efficient, may exhibit a learning curve in pricing complex, intangible assets. ESG strengths represent a form of intangible capital, including reputational human capital, innovation capacity and stakeholder trust, whose cash flows are long-term and potentially uncertain.

Our findings imply that while these ESG-derived intangibles may not immediately translate into superior short-term accounting returns, the market anticipates their future value relevance. The significant coefficient on Tobin’s Q indicates that, upon assimilating ESG information, investors do indeed value corporate commitment to ESG principles, embedding a valuation premium into the firm’s stock price. This premium reflects the market’s assessment of reduced long-term risk, for example, regulatory- and reputation-related, and the potential for sustained competitive advantages that are not fully captured in contemporaneous income statements. The robustness of the Tobin’s Q relationship therefore indicates that ESG is valued by the market as a strategic, long-term investment. This distinction is critical for both corporate managers allocating resources and for scholars modelling the financial impact of CSR.

This study provides a comprehensive examination of the bidirectional relationship between ESG factors and firm performance, yielding several important insights with both theoretical and practical implications. Our empirical analysis demonstrates that accounting-based performance measures, specifically RoIC and RoA, exhibit statistically significant positive relationships with lagged ESG values. This temporal pattern suggests that investments in ESG initiatives require time to manifest their full financial benefits, as the operational efficiencies and stakeholder benefits associated with strong ESG performance gradually translate into improved financial outcomes.

The differential impact of ESG factors across performance metrics presents particularly noteworthy findings. While accounting measures show consistent positive associations, our analysis reveals that Tobin’s Q, as a market-based valuation metric, displays no statistically significant relationship with ESG performance in linear specifications. This divergence between accounting and market measures suggests potential inefficiencies in how financial markets process and price ESG-related information, at least in the short term. Market participants may either underestimate the future cash flow implications of ESG investments or require more time to fully appreciate their strategic value. This finding contributes to the ongoing debate about market efficiency with respect to non-financial information and has important implications for investors employing ESG criteria in their valuation models.

Our curvilinear analysis yields additional layers of understanding about the ESG–performance relationship. The inverted U-shaped pattern observed for RoIC provides empirical support for the existence of an optimal level of ESG investment, consistent with the KC hypothesis. Initial improvements in ESG performance generate substantial efficiency gains and stakeholder benefits that enhance capital productivity, but beyond a certain threshold, the marginal costs of additional ESG investments appear to outweigh their financial benefits. This finding has direct implications for corporate managers seeking to optimize their ESG budgets and allocate resources most effectively across different sustainability initiatives.

Conversely, the U-shaped relationship between ESG performance and Tobin’s Q reveals important insights about market learning and adaptation processes. The initial negative slope suggests that markets may initially penalize firms for ESG investments, potentially viewing them as distracting from core profit-making activities or representing unnecessary costs. However, the subsequent positive slope indicates that as firms demonstrate sustained commitment and capability in implementing ESG initiatives, markets eventually recognize and reward these efforts. This pattern implies that the market’s valuation of ESG activities evolves over time as investors accumulate more evidence about their financial relevance and as reporting standards improve.

These findings align with and extend several strands of existing literature. The positive associations with accounting measures corroborate the results of Lahouel et al. (2022) and Sun et al. (2019), while the linear relationship with RoA specifically supports the conclusions of Barnett and Salomon (2012), Brammer and Millington (2008) and Chen et al. (2018). The theoretical implications are particularly significant for stakeholder theory, as our results demonstrate that addressing diverse stakeholder interests through ESG initiatives can indeed create tangible financial value. The findings also support signalling theory by showing how ESG disclosures and performance serve as credible indicators of management quality and long-term orientation.

The literature has traditionally focused more on energy or financial sectors. So our study addresses an important gap in the literature with its focus on the pharmaceutical industry. Our results suggest that ESG factors may play an even more crucial role in pharmaceuticals, where reputation, regulatory compliance and social license to operate are particularly salient. The positive association with accounting performance metrics indicates that pharmaceutical firms can derive substantial financial benefits from ESG investments, particularly in areas like environmental compliance, ethical marketing practices and transparent governance structures.

The policy implications of these findings are substantial. Regulators and standard-setters may need to consider mechanisms to accelerate market recognition of ESG value, potentially through improved disclosure requirements or investor education. For corporate managers, the results suggest that ESG investments should be viewed as strategic rather than purely compliance-driven, with careful attention to both the timing and scale of such investments to maximize their financial returns.

Several promising avenues emerge for future research. Cross-country comparative studies could illuminate how different institutional environments and regulatory regimes moderate the ESG–performance relationship. Longitudinal analyses tracking firms over extended periods could provide deeper insights into how the financial returns on ESG investments evolve over time. Additionally, more granular examination of how specific ESG components, for example, environmental versus social versus governance, contribute differentially to financial performance could help firms prioritize their sustainability initiatives.

While this study makes significant contributions to the literature, certain limitations should be acknowledged. The single-industry focus, while providing depth, may limit the generalizability of findings to other sectors with different operational characteristics and stakeholder dynamics. The study also relies on available ESG metrics that may not fully capture all relevant dimensions of corporate sustainability performance. While focusing on the top 255 pharmaceutical firms enhances the study’s analytical precision and ensures data comparability, it also introduces an important boundary condition. By design, the sample excludes smaller and unlisted firms that may exhibit different ESG–performance dynamics due to resource constraints, varying disclosure incentives and divergent stakeholder pressures. Consequently, the findings are most generalizable to large, publicly traded pharmaceutical firms with established ESG reporting practices. Future research could extend this analysis to small and medium-sized enterprises (SMEs) or emerging-market firms to explore whether firm size, ownership structure and disclosure maturity moderate the ESG–performance relationship. Future research could address these limitations while building on the important findings presented here.

Footnotes

Acknowledgements

The authors gratefully thank Dr Anselm Schneide, Associate Professor in Organization Theory, Stockholm University, for reviewing an earlier version of the draft.

Authors’ Contributions

Jayasree Mangalagiri: Conceived the research idea, designed the study, collected and analysed data and contributed to manuscript drafting.

Malla Praveen Bhasa: Reviewed and integrated relevant literature, built theoretical arguments, provided critical revisions and refined the narrative structure. Extensively contributed to manuscript writing and revised it across all its versions for clarity and accuracy.

V. Parvathi: Designed the study, collected and analysed data and contributed to manuscript drafting.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported under the minor research grants category awarded by the Indian Council of Social Sciences Research, Ministry of Education, Government of India.