Abstract

Venture capital (VC) firms play a crucial role in fostering the growth of startups by providing financial resources, strategic guidance and support in accessing capital markets. However, the impact of VC support on firm performance following an initial public offering (IPO) remains widely debated, particularly in emerging markets characterized by a distinct institutional and structural environment. This study provides evidence on VC support and its effect on firm outcomes after listing. The sample comprises 422 non-financial firms that went public between 2003 and 2019. Post-IPO performance is evaluated over 5 years after listing by employing both accounting-based and market-based metrics. After addressing concerns of selection bias and endogeneity, the study demonstrates that the impact of VC support is two-fold. While VC support is linked to lower operating performance and firm profitability, it is associated with higher market valuation for firms post-listing. This divergence implies that although VC involvement may not consistently translate into superior post-listing operating outcomes, the presence of VCs continues to serve as a credible indicator to investors, aligning with their certification role in influencing investor perceptions. This research presents novel findings, providing significant insights for issuers, managers, regulators and investors.

Introduction

A critical pillar of the entrepreneurial ecosystem across global markets, venture capital (VC) firms enable startups to overcome resource constraints and foster long-term growth. VCs engage in a rigorous screening process to identify and select young firms with promising future business potential (Baum & Silverman, 2004; Chemmanur et al., 2011) and provide them with the required capital. They also provide strategic insights, monitoring and access to valuable networking opportunities while preparing the firms for a successful initial public offering (IPO) (Barry et al., 1990; Hellmann & Puri, 2002; Lerner, 1994). One of the most favoured exit strategies for VCs is through an IPO (Hu et al., 2012). Throughout the years, the occurrence of an IPO has served as an effective context for researchers to delve into how VC support affects the success of the portfolio firms (da Silva Rosa et al., 2003; Dolvin, 2005; Michala, 2019; Pennacchio, 2014). Existing studies have found that VC support improves IPO performance and lowers underpricing by certifying firm quality and alleviating information asymmetry (Megginson & Weiss, 1991). Moreover, involvement of lead VCs after the IPOs has been found to raise acquisition valuations and lower litigation risks, thus highlighting the continued certification role of VCs after IPO (Basnet & Walker, 2024). Conversely, it has also been observed that young VCs initiate the IPO of their portfolio firms at a relatively nascent stage to bolster their reputation, which subsequently exacerbates information asymmetry and results in increased underpricing (Gompers, 1996; Lee & Wahal, 2004).

There exists ample evidence on VC support and immediate IPO outcomes; however, whether such impact persists after the listing of the firm is still contested. The IPO process induces fundamental changes in the firm’s ownership, governance and regulatory requirements, all of which can reshape the dynamics of VC support and their subsequent impact on firm performance. This calls into question the relevance of VC support in determining a firm’s performance after the IPO phase, an aspect that has been underexplored given India’s distinct institutional setting.

This study is motivated by the need to understand how VC involvement shapes a firm’s performance after an IPO in developing markets. VCs typically enter firms as large block holders prior to listing and possess a comprehensive understanding of the firm’s operations, which may position them to impact post-IPO outcomes (Barry et al., 1990; Kaplan & Strömberg, 2004). In an institutional setting such as India, characterized by concentrated family ownership and limited investor protection laws, VCs may have heightened incentives to undertake monitoring activities. Such monitoring helps to protect their invested capital and limit potential agency conflicts between controlling owners and minority shareholders (Jensen et al., 1976). At the same time, under situations of pronounced information asymmetry around IPOs, the presence of VC support may serve as a certification signal to external market participants regarding firm quality and governance, thereby influencing market performance (Megginson & Weiss, 1991). Against this backdrop, this study examines whether VC support is associated with differences in operating performance and market valuation during the post-IPO period in the Indian context.

Existing studies focus on the United States (Jain & Kini, 1995; Lehnertz et al., 2022; Megginson et al., 2019), European countries (Bessler & Seim, 2012; Pommet, 2017; Tykvová, 2018) and China (Guo et al., 2015; Song & Kutsuna, 2023; Tan et al., 2013). These countries are characterized by relatively stronger institutional frameworks and more developed capital markets. The generalizability of these findings to the Indian context remains uncertain, given the substantial differences in investor participation, regulatory depth and market structure. The entrepreneurial ecosystem in India has evolved significantly over time to become one of the largest and most vibrant startup ecosystems globally. This growth is marked by a notable increase in VC funding and IPO volume, highlighting India’s increasing stature in the global entrepreneurial landscape (Gonzalo & Kantis, 2021; Raza & Natarajan, 2022). However, despite this growth, the Indian VC industry is relatively nascent, in contrast to developed economies, with smaller deal sizes, weak syndication patterns and limited exit opportunities (Gupta & Shukla, 2025; Sivaprasad & Dadhaniya, 2020). The Indian capital market also continues to struggle with persistent institutional and structural rigidities, high levels of information asymmetry across firms and market players, weak investor protection laws, non-transparent financial reporting and a substantially large participation of unsophisticated retail investors (Arora & Singh, 2021; Gogineni & Upadhyay, 2023; Nikbakht et al., 2021). India’s institutional framework, dynamic capital market and growing VC ecosystem, therefore, provide a distinct and underexplored setting to evaluate whether VC support translates into improved firm performance after listing.

Using a data set of 422 IPOs of non-financial firms listed between 2003 and 2019 on the Bombay Stock Exchange (BSE), the study examines how VC support affects post-IPO firm performance in an emerging country. The performance of firms is tracked over a 5-year post-listing horizon, and the results reveal that the firms supported by VCs exhibit significantly lower operating performance and shareholder profitability after listing, as reflected in return on assets (ROA) and return on equity (ROE), respectively. However, such firms demonstrate a higher market valuation relative to their non-VC-supported counterparts, as noted from the market-to-book (MTB) ratio and Tobin’s Q.

By conducting the research in the Indian context, where it remains relatively underexplored, the study enriches the emerging market literature. Furthermore, it illustrates the trade-offs of VC support, highlighting its differential impact on the firms’ operating efficiency and market valuation. Overall, the study offers insights for managers, VCs, investors, policymakers and regulators seeking to strengthen the capital markets and evaluate the outcomes of VC support.

The subsequent sections are arranged as outlined below: a comprehensive literature review is presented in the second section, subsequently accompanied by the methodology in the third section and the empirical findings outlined in the fourth section, followed by discussion and implications articulated in the fifth section, while the sixth section includes the conclusion.

Literature Review

High-growth companies greatly benefit from VC support, as VCs provide financial investments and also contribute a range of value-added services (Hellmann & Puri, 2002). A significant corpus of the prior literature has largely focused on the role of VC support around the IPO event, especially its effect on IPO pricing and investor returns. However, there is limited and inconclusive evidence on whether VC support translates into improved operating and market performance post-listing of the firms.

This study is grounded in two complementary theoretical perspectives—the agency theory and information asymmetry theory—to examine how VC support is associated with firm outcomes in the post-IPO period. The ownership structure of firms in emerging economies like India is typically characterized by concentrated shareholding and insider control, leading to principal–principal agency conflicts between controlling owners and minority investors. In such a setting, controlling shareholders may be involved in expropriation and rent-seeking behaviour at the cost of the minority shareholders. The agency theory argues that such conflicts can be alleviated by the presence of external investors who can provide monitoring and governance oversight (Jensen et al., 1976; Shleifer & Vishny, 1986). VCs, as informed and concentrated owners, are positioned to engage in monitoring of their portfolio firms with the potential to influence operational efficiency, sales growth and market value (Barry et al., 1990; Guo & Jiang, 2013) and also strategically time the IPOs to maximize returns (Lerner, 1994). VCs are also involved in implementing strategic management decisions, designing and formulating human resource policies and financial contracts, establishing corporate governance mechanisms to safeguard shareholders’ rights, and serving as board members (Chahine, 2007; Hellmann & Puri, 2002; Kaplan & Strömberg, 2004; Lerner, 1994).

The information asymmetry theory suggests that IPO markets are characterized by pronounced information disparities between firm insiders and market participants, and the investors have a hard time effectively evaluating the quality of the firm (Akerlof, 1970; Rock, 1986). The role of credible intermediaries becomes crucial in this context, as they can signal firm quality and significantly mitigate information asymmetry. Megginson and Weiss (1991) and Barry et al. (1990) indicate that VCs serve as a reliable certification mechanism that signals firm value to external investors and mitigates information asymmetry, leading to lower IPO underpricing and boosting market confidence. Several studies have found evidence supporting the certification role of VCs (Belghitar & Dixon, 2012; Chemmanur et al., 2011; Cho & Lee, 2013; Pennacchio, 2014). It is anticipated that these certification impacts would endure beyond listing and be evident in the firm’s market price after the IPO (Deb & Banerjee, 2024; Otchere & Vong, 2016).

Numerous other studies document that VC support results in long-term benefits and advantages post-listing. These include improved operating performance (Guo et al., 2015; Jain & Kini, 1995; Johnson & Sohl, 2012; Matanova et al., 2022; Song & Lee, 2018), developments in innovation (Chahine & Zhang, 2020; Feng et al., 2020), strengthened governance practices (Farag et al., 2014; Krishnan et al., 2011), less information asymmetry (Chemmanur et al., 2021) and decreased risk of default or failure relative to non-VC-supported firms (Michala, 2019). Following an IPO, seasoned VCs continue their investments in the portfolio companies to comply with lock-up agreements and liquidity concerns (Bruton et al., 2010; Levis, 2011), to protect their reputation (Gogineni & Upadhyay, 2023) and to reap the benefits from the growth of the listed firms (Jain & Kini, 1995). Recent empirical research indicates that retained VC ownership is linked with a firm’s financial policies, including delaying dividend initiation, undertaking merger and acquisition transactions, and entry into the corporate bond market (Amini et al., 2022).

Xie et al. (2024) indicate that VC support in emerging markets fosters innovation investment and alleviates excessive corporate financialization, while Pommet (2017) reports that a longer period of VC engagement before an IPO is linked to greater survival rates of firms post-listing. According to Cumming et al. (2023), IPOs supported by VCs have more robust internal controls and more informative disclosures post-IPO. Similarly, Somaya and You (2024) underscore the role of VC funding availability on IPO timing and valuations, as the authors find that highly scalable firms tend to delay their listing and obtain higher valuations at IPO when the availability of VC financing is abundant. An investigation of Hong Kong Stock Exchange (HKEX) IPOs reveals that VC-supported cornerstone investors mitigate price uncertainty, reduce underpricing and positively impact aftermarket activity (Suen, 2026).

However, increasing evidence indicates that the positive impact of VC support may not be consistent across different market and institutional settings and may diminish under specific conditions. Lehnertz et al. (2022) observe that firms with a VC ‘mega deal’ exhibit favourable performance post-listing for only the first two years, after which the positive effect fades away. Similarly, Basnet et al. (2025) conclude that VC involvement initially improves firm performance, but such returns begin to decline following the exit of the lead VCs.

Another stream of research indicates the structural and strategic limitations associated with VC involvement post-IPO. Since the IPO event induces significant changes in the shareholding pattern of a company, continuous engagement by VCs post-IPO limits their ability to invest funds in new and early-stage ventures with greater growth potential (Gogineni & Upadhyay, 2023). Consequently, the coaching and monitoring roles of VCs after the listing of portfolio firms may be limited, potentially reducing their effect on firm outcomes. Wang et al. (2003), Tan et al. (2013) and Ye et al. (2025) have documented that VC-supported enterprises exhibited inferior operating performance. Song and Kutsuna (2023) find that, although VC-supported companies have a significantly higher market value, they exhibit marginally lower profitability. According to Nain et al. (2025), a large supply of VC funds causes private firms to postpone their IPO, thus allowing lower-quality companies to list sooner, potentially resulting in poorer post-IPO performance. Aldatmaz and Celikyurt (2023) demonstrate the detrimental consequences of VC support on innovation performance. Wu et al. (2025) indicate that greater institutional, geographical and cultural distance between VCs and portfolio firms leads to greater underpricing and lower stock returns post-IPO due to higher information asymmetry and reduced effectiveness of VC certification. Similarly, Li et al. (2024) find that governmental VC support is linked to lower IPO valuations in China, in contrast to the conventional certification hypothesis. Empirical findings indicate that VC-backed companies go public sooner, leading to lower post-IPO returns but an increased chance of obtaining VC refinancing (Basnet et al., 2022). Moreover, cross-country evidence suggests that the post-IPO performance is contingent upon the macroeconomic factors and the legal-institutional environment of the country (Bruton et al., 2010).

While the link between VC support and IPO performance has been researched worldwide, the Indian context remains largely unexplored. Owing to the differences in regulatory frameworks, investor protection laws and the emerging entrepreneurial ecosystem, India’s capital market and VC network differ significantly from those of the developed economies (Arora & Singh, 2023; Gogineni & Upadhyay, 2023). There are notable differences in access to funding across regions and sectors (Gupta & Shukla, 2025; Rajan Annamalai & Deshmukh, 2011). In light of this structural heterogeneity, it is crucial to consider whether conclusions drawn from other countries can be extrapolated to India.

Previous studies conducted in the Indian context on VC support and IPO performance have mostly focused on short-term abnormal returns (Drebinger et al., 2019; Sivaprasad & Dadhaniya, 2020) or governance and market performance (Gogineni & Upadhyay, 2023; Katti & Raithatha, 2020). Deb and Banerjee (2024) provide a longitudinal analysis of VC-supported IPOs, focusing on post-listing stock returns. Although such contributions have brought development in the domestic literature, these contributions do not jointly analyze operating performance and market outcomes during the critical post-listing period, where the certification and monitoring roles of VCs are most significant. This study, therefore, investigates an aspect that has received limited attention in the context of emerging markets like India. In light of the above discussion, the following hypotheses are proposed.

Based on agency theory and the monitoring hypothesis, the study proposes:

H1: VC support significantly impacts the accounting performance of Indian firms after IPO.

Similarly, based on information asymmetry theory and the certification hypothesis, the study proposes:

H2: VC support significantly impacts the market valuation of Indian firms after IPO.

Materials and Methods

Selection of Sample and Overview of Data Source

The study examines a sample of 422 non-financial firms in India that conducted IPOs between 2003 and 2019 and were listed on the BSE. Firm performance is examined over 5 years following the IPO. The IPO year is treated as year t, while post-IPO performance is measured from (t+1) years, corresponding to the first financial year (FY) after listing, and continues up to (t+5) years. Accordingly, for firms that went public in 2019, the IPO year is FY 2019–2020 and post-IPO performance is observed from FY 2020–2021 through FY 2024–2025, ensuring a complete and up-to-date financial assessment. The Prime database was used to collect data on the total IPOs in India, and the Venture Intelligence database was subsequently used to classify IPOs supported by VCs and those that are not. The final sample comprises 102 VC-supported IPOs and 320 non-VC-supported IPOs. Post-IPO performance data relevant to each firm was compiled from the Prowess database maintained by Centre for Monitoring Indian Economy (CMIE).

Variables, Model Specification and Methodology

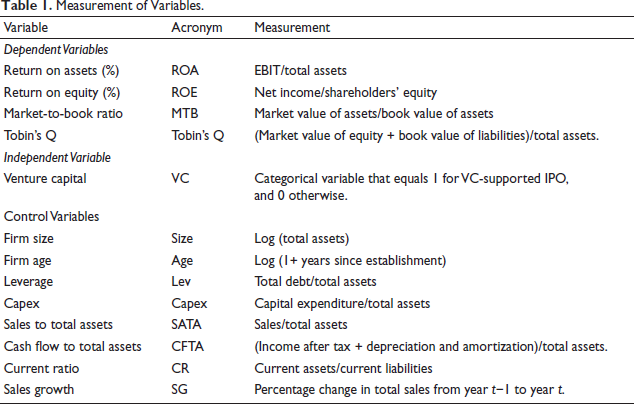

The company’s performance is measured using two dimensions, that is, accounting performance and market performance. For accounting performance, we employ ROA and ROE. While ROA captures operating performance, ROE indicates firm profitability. Similarly, the MTB ratio and Tobin’s Q serve as indicators of market-based performance. VC is the independent variable. Following previous studies, control variables are incorporated to account for factors that could influence performance outcomes. Winsorization of the variables was carried out at the 5% and 95% levels. The industry fixed effects are included to control for sector-specific effects. The definitions and measurements of study variables appear in Table 1.

The econometric model employed is as follows:

where

Measurement of Variables.

Measurement of Variables.

Descriptive Statistics

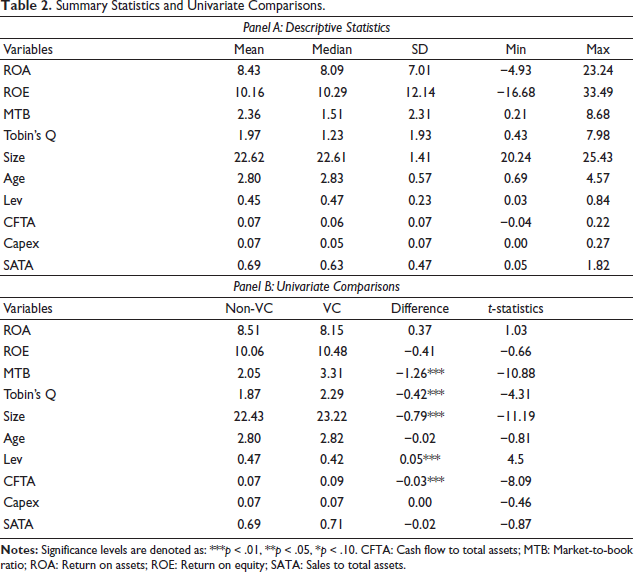

Table 2 presents an overview of the summary statistics and results of the univariate comparisons.

Summary Statistics and Univariate Comparisons.

Summary Statistics and Univariate Comparisons.

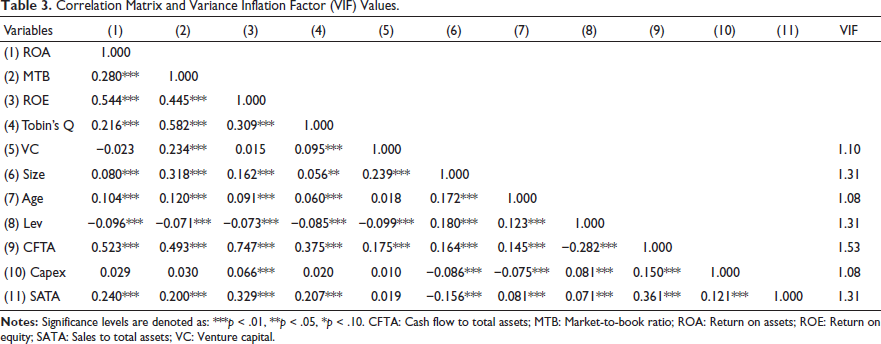

As shown in Panel A, the mean ROA and ROE are 8.43% and 10.16%, respectively, with standard deviations of 7.01% and 12.14%, indicating significant variability in accounting performance. The sample includes firms with negative operating returns (minimum ROA of −4.93%) as well as highly profitable companies (maximum ROA of 23.24%). The average MTB ratio is 2.36, indicating that companies in the sample are valued at more than twice their book value. Similarly, the mean Tobin’s Q value is 1.97, ranging from 0.43 to 7.98. The outcomes of the independent samples t-test comparing VC-supported firms with those of the non-VC-supported ones are documented in Panel B. The univariate analysis indicates that no statistically significant differences are observed in the ROA and ROE of both groups. However, the MTB ratios and Tobin’s Q are significantly higher for firms with VC support, indicating higher market valuation. VC-supported firms are also significantly larger and have lower leverage, indicating greater reliance on equity financing. The average CFTA for VC-supported firms is significantly higher, suggesting that such firms have stronger operational cash performance. Table 3 depicts the variables’ correlation matrix and the variance inflation factors (VIF) values, which are below the cutoff value of 10, indicating no serious issues of multicollinearity.

Correlation Matrix and Variance Inflation Factor (VIF) Values.

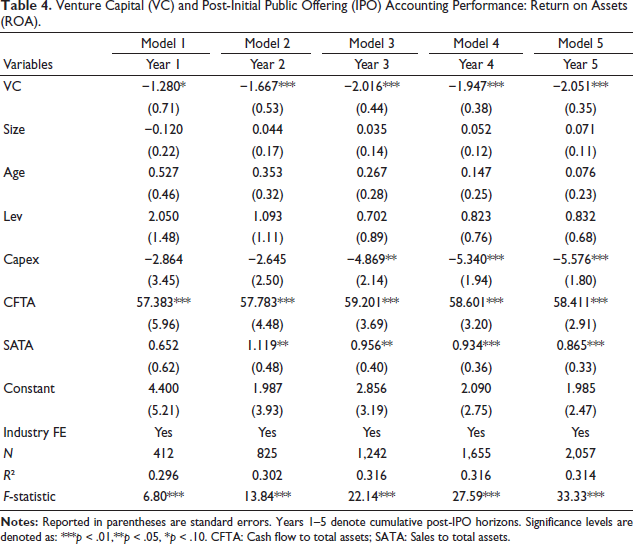

The regression estimates using ROA and ROE as the outcome variables are presented in Tables 4 and 5.

Venture Capital (VC) and Post-Initial Public Offering (IPO) Accounting Performance: Return on Assets (ROA).

Venture Capital (VC) and Post-Initial Public Offering (IPO) Accounting Performance: Return on Assets (ROA).

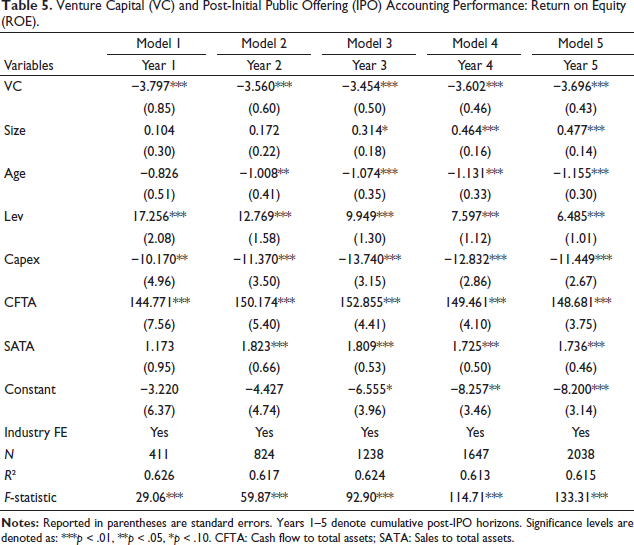

Venture Capital (VC) and Post-Initial Public Offering (IPO) Accounting Performance: Return on Equity (ROE).

The estimates reflect the average association between VC support and accounting performance of IPO firms across a cumulative post-IPO horizon extending from (t+1) through (t+5) years. Across Models 1–5 in Table 4, the coefficient of VC support for ROA of firms is consistently negative and statistically significant. A comparable trajectory is noted for ROE, implying that the VC support is associated with persistently negative outcomes across the 5-year post-listing period. Model 5 in both tables indicates that VC support is associated with a reduction of 2.05 percentage points in ROA and 3.70 percentage points in ROE. These results reveal that the VC-supported companies record lower ROA and ROE in the post-IPO period, and having VC support does not systematically translate into higher operating performance or profitability after going public. These results corroborate existing studies documenting the inferior operating performance of VC-supported IPOs (Chen & Liang, 2016; Deb & Banerjee, 2024; Song & Kutsuna, 2023; Ye et al., 2025).

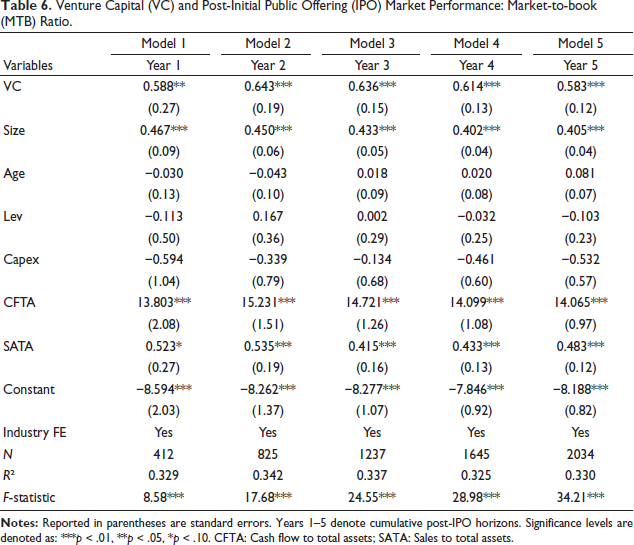

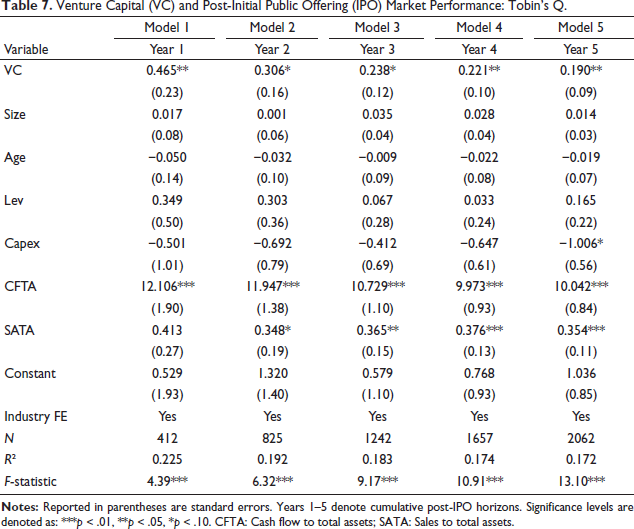

The outcomes of the regression analysis for market-based performance measures, measured using the MTB ratio and Tobin’s Q over cumulative post-listing horizons extending from (t+1) to (t+5) years, are displayed in Tables 6 and 7 across Models 1–5.

Venture Capital (VC) and Post-Initial Public Offering (IPO) Market Performance: Market-to-book (MTB) Ratio.

Venture Capital (VC) and Post-Initial Public Offering (IPO) Market Performance: Tobin’s Q.

The VC coefficient depicts a statistically significant positive relationship with the MTB ratio across all model specifications. In both tables, Model 5, which captures cumulative post-IPO performance over the 5-year horizon, indicates that VC support is associated with a higher market valuation, as the MTB ratio increases by 0.58 points and the Tobin’s Q increases by 0.19 points. Taken together, these results indicate that VC support is associated with positive market-based performance after listing. This is in line with existing theoretical arguments that VC support serves as a certification signal of the firm’s growth potential and scalability. The positive relation between VC support and market performance aligns with previous research results (Guo et al., 2015; Song & Kutsuna, 2023).

Collectively, these results suggest that despite the lower operating performance and profitability, the VC-supported firms are perceived more favourably by the investors. This pattern reflects the dual role of VCs. Since VCs usually fund startups during early stages, the earnings are typically low, which may result in weaker operating performance and profitability post-listing. At the same time, VCs tend to choose firms with strong future growth potential, thereby shaping investor expectations and leading to higher market valuations. Moreover, in the post-listing phase, the VCs may prioritize maximizing market value to improve their exit outcomes. These results are pertinent to the Indian context, where, in the recent past, VC investors have preferred to invest in businesses that are highly scalable, technology-driven, and have a long-term growth orientation, rather than instant profitability. These results underscore the contrasting effect of VC support in India and contribute to understanding its role in shaping firm outcomes in emerging markets.

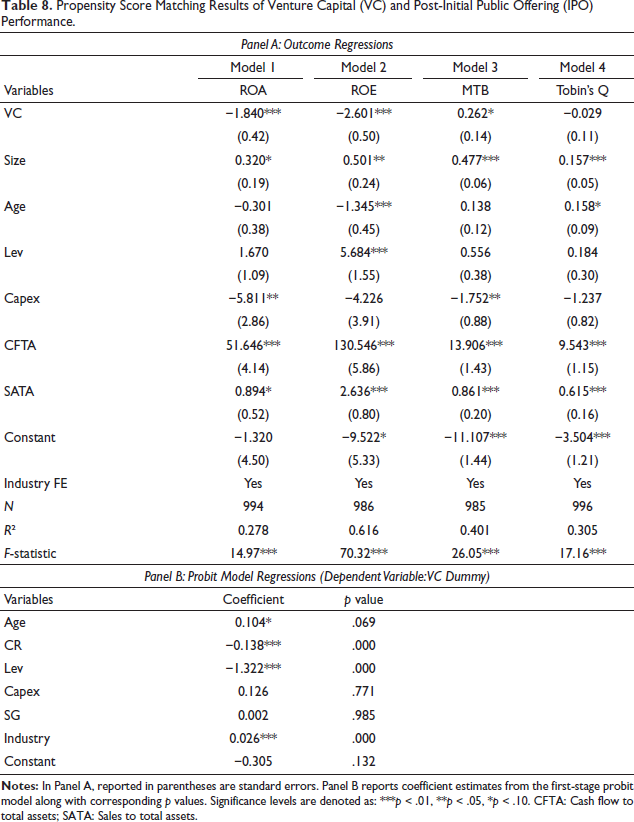

The propensity score matching (PSM) technique, as first outlined by Rosenbaum and Rubin (1983), is applied to account for endogeneity in VC funding decisions. A probit model is employed to estimate the likelihood of obtaining VC funding. VC-supported firms are subsequently matched with non-VC-supported firms exhibiting similar propensity scores. After the matching procedure, the baseline regressions are re-estimated, with the corresponding results reported in Panels A and B of Table 8, respectively.

Propensity Score Matching Results of Venture Capital (VC) and Post-Initial Public Offering (IPO) Performance.

Propensity Score Matching Results of Venture Capital (VC) and Post-Initial Public Offering (IPO) Performance.

Here, the regression equations capture the average impact of VC support on the accounting and market performance over the cumulative 5-year post-listing period. The results indicate that VC support is linked to lower ROA and ROE and a higher MTB ratio. These estimates are in line with the preliminary findings, where VC-supported firms have lower accounting performance but a higher market value post-listing. The VC coefficient is negative for Tobin’s Q; however, the impact is insignificant.

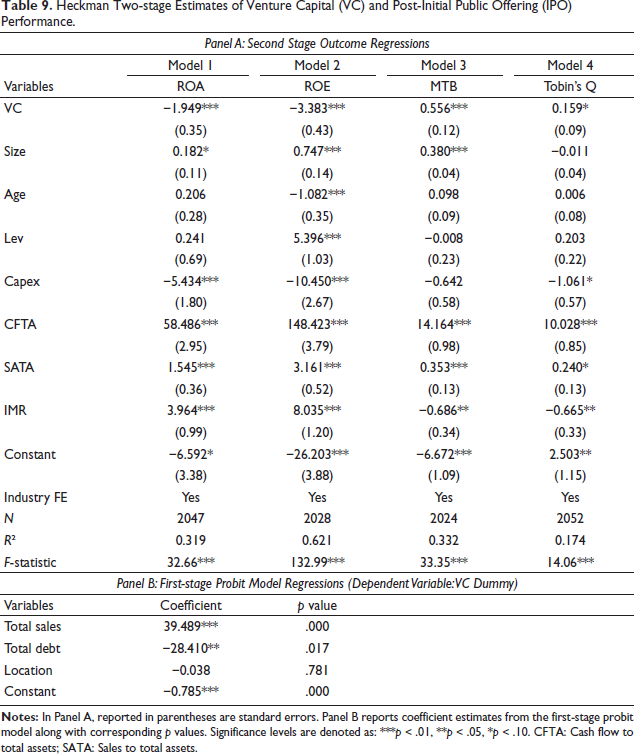

To address selection bias resulting from the non-random allocation of VC funds, the Heckman selection model (Heckman, 1979) is employed using a two-step estimation procedure. The analysis begins with estimating a probit model using total sales, total debt and location to model the likelihood of receiving funding from VCs. From the first stage, the Inverse Mills Ratio (IMR) derived is subsequently used in the second-stage regression to correct for biases in performance estimation. The outcomes are presented in Table 9, where Panel A reports the regression estimates while Panel B displays the Probit regressions.

Heckman Two-stage Estimates of Venture Capital (VC) and Post-Initial Public Offering (IPO) Performance.

Heckman Two-stage Estimates of Venture Capital (VC) and Post-Initial Public Offering (IPO) Performance.

The significant IMR indicates the presence of potential selection bias. The evidence indicates that the effect of VC support on operating performance (ROA) and profitability to shareholders (ROE) is negative and significant, while for market-based performance measures, the MTB ratio and Tobin’s Q, the estimated coefficient for VC support is positive and significant. These results corroborate the study’s preliminary findings, indicating that the conclusions remain robust after accounting for selection bias.

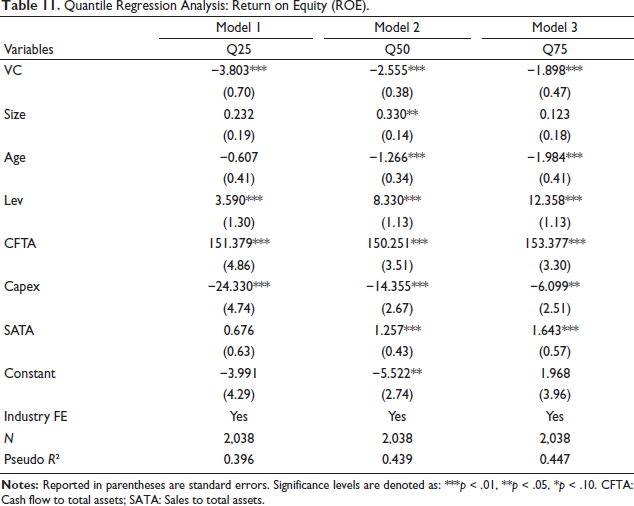

The summary statistics presented in Table 2 (Panel A) indicate that the dependent variables ROA and ROE have significant dispersion, suggesting considerable variations in accounting performance. To address this distributional heterogeneity, the quantile regression approach is adopted to examine whether VC support systematically influences accounting-based performance measures. The quantile regressions are estimated at the 25th, 50th and 75th percentiles, reflecting the impact of VC support across lower-, middle- and higher-performing firms. As illustrated in Tables 10 and 11, VC support has a statistically significant adverse effect on ROA and ROE across all estimated quantiles, indicating that the results are robust throughout the performance distribution and are not driven by outliers.

Quantile Regression Analysis: Return on Assets (ROA).

Quantile Regression Analysis: Return on Assets (ROA).

Quantile Regression Analysis: Return on Equity (ROE).

This study advances existing research by presenting novel empirical insights into the post-IPO outcomes of VC-supported firms in India. Prior studies on Indian IPOs focus on explaining underpricing and short- or long-run post-listing stock returns of IPOs with and without VC support (Deb & Banerjee, 2024; Drebinger et al., 2019; Katti & Phani, 2018; Sivaprasad & Dadhaniya, 2020). Conversely, this study explicitly examines firm performance during the post-IPO period by jointly analyzing operating and market-based measures across cumulative horizons over 5 years. Unlike evidence from developed markets and from China, where VC support is generally associated with superior operating and market performance, growth and stock returns (Bessler & Seim, 2012; Guo et al., 2015; Guo & Jiang, 2013; Jain & Kini, 1995; Kelly & Kim, 2018; Lehnertz et al., 2022; Otchere & Vong, 2016), this study reveals a double-edged impact of VC support. Specifically, VC-supported firms exhibit lower operating performance but command higher market valuations after listing. These results draw attention to the relevance of institutional context and suggest that findings from other economies cannot be readily generalized to the Indian setting. By addressing selection bias and endogeneity concerns using multiple empirical approaches, this study offers a robust understanding of the impact of VC support on post-IPO outcomes in India.

This evidence highlights the necessity for the capital market regulator, the Securities and Exchange Board of India, to prioritize the quality and interpretability of the post-listing disclosures and governance reporting by IPO firms. Additionally, there needs to be concerted effort to enhance investor education and awareness regarding the role of VC support and its implications for firm outcomes. For VCs, the findings suggest that they need to evolve beyond their traditional role as fund providers and certifiers into long-term strategic partners. The findings further indicate that issuing firms and managers should focus on post-IPO performance management, as sustaining the valuation premium might be challenging without corresponding improvements in operating performance. Retail investors should exercise caution when assessing VC-supported firms, as the observed valuation premium may stem from perceived certification effects, thus highlighting the necessity for thorough evaluation of firm-specific financial performance.

Conclusion

Empirical assessment of the trajectories of firms following an IPO indicates that the effect of VC is double-edged. By employing a sample of 422 IPOs in India and using multiple methodologies to deal with endogeneity in VC funding and sample selection bias, the results indicate that VC-supported firms exhibit lower operating performance and profitability, suggesting that the performance-enhancing benefits commonly attributed to VC involvement may not uniformly materialize in the post-listing period. However, the findings demonstrate a higher market valuation for firms supported by VCs, consistent with the certification effect associated with the presence of VC support in the primary market. Although VC support can unlock access to external finance and positively influence market valuation, it can also come at the cost of trade-offs in operating efficiency. Building on prior evidence on VC and IPO performance, including Megginson and Weiss (1991) and Barry et al. (1990), which highlight the certification role of VCs, as well as more recent studies such as Basnet and Walker (2024) and Basnet et al. (2025), this study documents a divergence in the impact of VC support on firms’ operating performance and market valuation in an emerging market context such as India. From a policy perspective, the results highlight the importance of strengthening institutional governance and disclosure standards to ensure that VC support contributes to sustained post-listing firm performance. However, the study has certain limitations, particularly with respect to the availability of data. Future research could consider industry-specific dynamics, stages of VC investment and syndication strategies. A cross-country analysis of emerging economies may help to generalize the findings of this study. Moreover, future studies could explore the channels by which VCs engage in monitoring firm activities and governance, including operational involvement and board participation.

Footnotes

Acknowledgement

The authors acknowledge the Indian Institute of Technology, Kharagpur, for the infrastructural support provided to complete this research work.

Authors’ Contributions

All authors have equal contributions in research structuring, data analysis, paper writing and editing.

Availability of Data and Material

It is available and not uploaded in the text.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Informed Consent

The authors declare that they do not have any informed consent.

Research Involving Human Participants and/or Animals

The authors declare that they do not have any issues with this research involving human participants and/or animals.