Abstract

The study investigates the moderating role of a firm’s size while assessing the level and direction of the association between female board directors and the firm’s performance in the pharmaceutical sector. The study applies a fixed effects model, suggested by the Hausman test, to control for unobserved firm heterogeneity. Robustness check of the model is ensured with the panel unit root test, followed by the generalized least squares model, which handles panel-specific heteroskedasticity and autocorrelation. The endogeneity concern is addressed using a two-step system generalized method of moments model. The quantile regression is also applied at different distribution levels to capture the relationship on different scales. The findings disclose that female board directors positively enhance the firm’s performance when the firm’s size plays a moderating role, and the relationship significantly reverses the direction of the relationship. The study offers a foundational strategy to regulators and investors to boost board composition and the inclusion of more females on the boards. This study employs a unique empirical approach to examine the relationship between female board directors and the firm’s performance, with a particular focus on the firm’s size as a moderator to achieve the mandated goals of governance bodies.

Keywords

Introduction

With the increasing attention towards the composition of boards in business organizations, the inclusion of females on the boards has become mandatory in the majority of emerging economies (Arora et al., 2026; Mazza et al., 2024). With the diverse dimensions of board diversity, the presence of female board directors (FBD) has emerged as a subject of growing relevance in both academic research and policymaking (Smulowitz et al., 2025). A set of studies on FBD argues that the inclusion of females in decision-making fosters more balanced perspectives, enhances transparency, ethical governance and improves stakeholders’ trust (Mishra, 2025; Nicolò et al., 2022), along with making a favourable contribution to the firm’s performance. However, despite a few studies that have argued in favour of positive contributions of FBD towards the firm’s performance, the performance implications of FBD remain mixed due to unintended effects and their roles, particularly in emerging economies (Al-Shaer et al., 2024; Joecks et al., 2012; Looi et al., 2025).

The involvement of females in corporate boards represents not only a question of fairness but also a means to remove gender inequality and as a strategic consideration with potential implications (Biswas et al., 2021; Fan et al., 2024). Despite regulatory-mandated efforts to enhance FBD, the actual influence of FBD on a firm’s performance remains conditional and context-based according to businesses (Aggarwal et al., 2019). As firms are increasing pressure for accountable governance, whether FBD have the expertise or not for their allotted work, including symbolic appointees, becomes a critical concern (Arora et al., 2026; Jayaraman et al., 2024).

While a few research studies have discussed a positive association between FBD and a firm’s performance, a few studies report statistically insignificant and negative relationships (Mishra, 2025; Tanwer, 2025; Usman et al., 2026). The present endeavour reveals that the relationship between FBD and a firm’s performance may not be uniform in all sectors (Ferrary & Déo, 2023). Instead, it is probably contingent on firm-specific factors like the firm’s size (FSZ). In the perspective of resource dependence theory (Alodat & Hao, 2025; Nguyen & Huynh, 2023) suggests that larger size firms may offer higher supportive systems and greater resources, which can raise the contributions of FBD in decision-making (Alodat et al., 2023; Lin & Xie, 2024). In contrast, agency theory (Ain et al., 2021; Smulowitz et al., 2025) suggests that as firms grow and performance increases, it may create agency conflicts. In smaller firms, the impact of FBD may be constrained due to a limited governance system or weak managerial practices (Farooq & Ahmad, 2023).

The present endeavour focuses on the pharmaceutical sector of an emerging economy, a highly regulated, capital-intensive sector that runs under a strict regulatory environment (Mulinari et al., 2024; Sanad & Musleh Al-Sartawi, 2023). In the current scenario, the Indian pharmaceutical sector, ranking third globally in medicine production, accounts for nearly 20% of the global level supply and over 60% of the world’s total output (Ganguly & Ghosh, 2025; Thatoi et al., 2025). With a market cap of more than $50 billion, the Indian pharmaceutical sector is playing a crucial role in public healthcare and India’s gross domestic product (Ganguly & Ghosh, 2025).

In such a setting, board composition, particularly the presence of FBD, may significantly influence a firm’s performance (Saeed, 2025). However, the existing literature on FBD often ignores FSZ, which may moderate this relationship (Hassan, 2023; Joecks et al., 2024). Therefore, this context allows us to study how FSZ moderates the FBD and firm’s performance link and imparts new insights into the governance literature, particularly in emerging economies. However, the actual impact of FBD on a firm’s performance remains underexplored in the rising economies like India, where the female presence on the boards is still evolving (Alodat et al., 2022).

Based on the facts mentioned in prior studies, the present study covers the following objectives. First, to examine the standalone impact of FBD on the firm’s performance. Second, to assess the impact of FSZ on the firm’s performance. Third, it examines whether FSZ moderates the relationship between FBD and a firm’s performance by interacting FSZ with FBD. These clearly defined objectives provide the foundation for hypothesis development and empirical analysis.

Therefore, this study contributes to a more nuanced understanding and addresses a significant gap in governance literature in the field of an innovative, data-driven and sensitive sector of an emerging economy. The present study includes robustness assessments by applying different models to deal with econometric concerns, consisting of heteroskedasticity, endogeneity, autocorrelation and distributional misspecification.

The structure of this present study is as follows: Section 2 outlines the theoretical exploration and scanning of the existing literature. Section 3 includes the research methodology and variable descriptions. Section 4 presents results and analysis. Lastly, Sections 5 and 6 discuss the conclusion, implications and limitations, respectively.

Literature Review

Board Structure and Regulatory Guidelines in India

The Indian pharmaceutical sector is designed with a combination of corporate laws, sector-specific guidelines and evolving mandates regarding female directors on boards (Aggarwal et al., 2019; Patil & Yadav, 2026). The appointment of at least one female on boards of the listed firms is an important step towards promoting gender diversity, female leadership and enhancing transparency and accountability (Eckbo et al., 2022; El-Dyasty & Elamer, 2024; Omenihu et al., 2025). In India, this regulation was first introduced in 2015 by the Securities and Exchange Board of India under Regulation 17(1)(b) of the Listing Obligations and Disclosure Requirements (Bansal, 2024). Next, the Companies Act, 2013, also initiated the same for listed firms by April 2015 (Patil & Yadav, 2026).

A few other bodies, such as the Central Drugs Standard Control Organization, the Drugs and Cosmetics Act, 1940 and 1945, also impact the governance in an indirect way by emphasizing ethical practices and accountability, focusing on legal compliance (Sah et al., 2025). The firms are also required to adopt good manufacturing practices due to the implementation of the Drugs and Cosmetics Rules, which necessitate the effective supervision of boards (Dashawant et al., 2025; Kumar et al., 2025). Including females on the boards, guided by regulatory bodies, displays a strategic decision to understand the value of gender-balanced leadership (Cambrea et al., 2023). The female director’s presence is not just a compliance but also a governance imperative aimed towards enhancing ethical decision-making, stakeholder engagement and social accountability in healthcare (Ardito et al., 2021). From this standpoint, the FBD is seen as a valuable resource of human capital, which needs to be appreciated and utilized strategically (Shin & Moon, 2026).

Role of Female Board Directors and Firm’s Size on Firm’s Performance

Grounded in agency theory and resource dependence theory, the effectiveness of FBD in improving a firm’s performance is debatable (Alodat & Hao, 2025). While a few studies value the FBD to enhance board goals, stakeholder expectations, long-term investment decisions, and to improve a firm’s performance (Shin & Moon, 2026; Usman et al., 2026), and a few others, evidence suggests a complex relationship (Nguyen & Huynh, 2023). Several empirical investigations have reported a negative association of FBD with a firm’s performance and other factors (Brahma et al., 2021; Joecks et al., 2012; Li & Chen, 2018; Pandey et al., 2023; Tanwer, 2025), suggesting that, considering it as a racial minority status, FBD may not always lead to improved performance (Mendiratta & Tasheva, 2025). Furthermore, Mei et al. (2026) found that the relationship may change according to the role of FBD in firms. Also, a few studies revealed that FBD may face structural barriers, limited influence and symbolic representation, which may decrease the decision-making processes and create coordination challenges (Almarayeh, 2023; Arora et al., 2026; Zheng & Wang, 2024).

Furthermore, in a traditional or male-dominated sector, the FBD may also encounter resistance and fail to immediately achieve performance benefits (Centinaio, 2024; Gharbi & Othmani, 2023). Although few studies have indicated that the long-term impact of FBD in terms of a firm’s performance does not have consistent and positive outcomes (Simionescu et al., 2021). Also, a few of them confirm that the relationship may be negative under certain conditions (Octavio & Setiawan, 2024). Furthermore, Shin and Moon (2026) confirmed that if FBDs are appointed to satisfy regulatory mandates, the relationship remains statistically insignificant. This relationship is essential to evaluate whether increased FBD serves as a performance-enhancing or symbolic construct (Lefley & Janeček, 2024; Mendiratta & Tasheva, 2025). In this context, the null hypothesis (H1) is framed for the endeavour as: H1: There is a negative relationship between FBD and firm’s performance.

The relationship between FSZ and firm’s performance has been widely examined in the existing literature (Alodat & Hao, 2025; Lefley & Janeček, 2024). The larger size firms often benefit from economies of scale, better presence in the market, and financial resources access, which may contribute to improving the firm’s performance (Biswas et al., 2021). As they expand, firms typically develop more structured management systems and internal controls, which also support the strategic execution (Looi et al., 2025). Prior studies also emphasize that FSZ is positively associated with a firm’s performance, which is essential to sustain in dynamic markets (Li & Chen, 2018). Larger size firms have better and effective risk diversification, which can maintain the returns and help in positively improving the firm’s performance (Jayaraman et al., 2024). In the context, the null hypothesis (H2) is established as: H2: There is a positive relationship between FSZ and a firm’s performance.

Moderating Role of Firm’s Size in the Relationship Between Female Board Directors and Firm’s Performance

The FBD is seen as a critical aspect of a corporate board, as it reflects gender diversity and may improve the firm’s performance (Al-Shaer et al., 2024; Omenihu et al., 2025). The association of FBD and a firm’s performance is not uniform and may be shaped by structural characteristics like FSZ, which may influence the firm’s complexity, resource availability and governance (Al-Shaer et al., 2024). Thus, FSZ can moderate this relationship by improving the effectiveness of female directors to shape a firm’s performance (Guedes et al., 2024).

As per contingency theory, in large firms, the FBD presence may have a more notable impact on the firm’s performance due to greater resource availability and regulated governance structures (Li & Chen, 2018; Park, 2020). In smaller firms, the influence may be constrained due to the limited board influence on decision-making (Aggarwal et al., 2019; Farooq & Ahmad, 2023). Also, when FSZ is larger and FBD is nominal, the absence of gender-based diversity on the board may hinder the governance structure (Joecks et al., 2024). The combination of higher FBD and larger FSZ may increase governance benefits, supervision and accountability in improving the firm’s performance (Alodat et al., 2023; Hussain et al., 2024). So, this interaction represents a contextual moderating role. Thus, the null hypothesis (H3) is established as: H3: FSZ positively moderates the relationship between FBD and firm’s performance.

With the above discussion, the recent investigations on FBD and firm’s performance provide mixed and both situation-specific results with evidence spread between the positive (Mishra, 2025; Usman et al., 2026) and non-significant (Brahma et al., 2021; Pandey et al., 2023) impacts in institutional or industry-specific contexts and according to FBD roles in firms (Mei et al., 2026). Also, very little focus has been paid to the sector dynamics in emerging economies and the conditional role played by firm-level characteristics like FSZ. The endeavour presents an effective strategy that can help in explaining the relationship between FBD and firm’s performance.

The present endeavour offers several key contributions to the existing literature of corporate governance. It adds value by providing new insights into how optimizing the FBD in aligning with FSZ can improve the firm’s performance in a positive way. While prior studies have extensively explored the standalone impact of FBD, the present study introduces an interaction term between FBD and FSZ. Depending on organizational characteristics, the impact of females may be complex or lead to mixed results in the relationship, so further exploration is needed. By examining the pharmaceutical firms, which are marked by innovation and regulatory supervision, the current endeavour offers a more refined understanding of the ways FBD can be strategically leveraged for a firm’s performance.

Materials and Methods

Sample Description

The study focuses on the Indian pharmaceutical sector, which is a key contributor to the global healthcare sector, and is recognized as one of the largest producers of generic drugs worldwide (Dashawant et al., 2025; Kumar et al., 2025). This sector provides a distinctive context to examine the FBD and firm’s performance relationship. The present study examines a 15-year period of firm-level data spanning from the financial year 2009–2010 to 2023–2024, a period marked by evolving regulations, increasing emphasis on corporate governance and transparency. The study focuses on 73 pharmaceutical firms out of a total of 152 listed firms on the Bombay Stock Exchange. These firms are scrutinized and selected on the basis of the data availability of comprehensive, reliable financial and governance disclosures; firms with insufficient or incomplete data were excluded.

The data related to board size (BSZ) and FBD were retrieved directly from the corporate governance section of the official annual reports, where board composition is clearly presented in a structured and standardized form in terms of the regulations. The annual reports are available at the firms’ official website and the Bombay Stock Exchange website (Singh & Sharma, 2023). The BSZ is considered the total number of directors sitting on the board of the firm (Adem & Dsouza, 2024). The FBD is identified with the prefix of Mr/Ms, which is mentioned in the board of directors list (Arora & Singh, 2020). The data extraction process is based on direct transcription without any subjective interpretation. The handpicked figures were duly compared with the original reports to maintain the credibility of data set, while data related to financial variables were collected from the Prowess database of CMIE Ltd, which is also an authentic and trusted source for firm-level financial data, including private and publicly listed firms, as previously studies have also mentioned (Pant et al., 2023; Pant & Sharma, 2025). Examining this sample extends existing governance research beyond emerging economies.

Variables Description

Dependent Variables

Independent Variables

Control Variables

Variables Definition.

Variables Definition.

Equation (1) is employed to examine how firm-level variables influence a firm’s performance in the pharmaceutical sector.

The firms’ related unobserved heterogeneity showcases a significant challenge in research. To address these types of issues, the Hausman test is conducted for the present study, which preferred to choose the fixed effects (FE) model over the random effects model, suggesting that time-invariant unobservable characteristics may be correlated with the regressors and also indicates that explanatory variables may be correlated with unobserved firm-level characteristics (Ab Aziz et al., 2024; Liu, 2024). For the baseline, the ordinary least squares (OLS) model is included to review the basic changes in the variable results. To check the reliability of results and to address the expected violations, the generalized least squares (GLS) method is applied with both panel-specific heteroskedasticity and autocorrelation (Daëron & Vermeesch, 2024). This model is relevant to the longitudinal nature of the data for performance measurement and firm-specific shocks. The GLS model enhances the robustness of the estimates.

The endogeneity is also a critical concern when assessing the relationship. To address this concern, a two-step system generalized method of moments (GMM) approach is applied to ensure a reliable conclusion (Assfaw & Sharma, 2024; Farzana et al., 2024). While panel estimations handle time-invariant heterogeneity, the quantile panel approach extends this analysis by applying the model to different distributions to disclose the inconsistency and heterogeneous effects at various levels (Shawtari et al., 2016). This approach enhances understanding of variables that may have different impacts at different distribution levels (Abed et al., 2025; EmadEldeen et al., 2025).

Results and Discussions

Descriptive Analysis

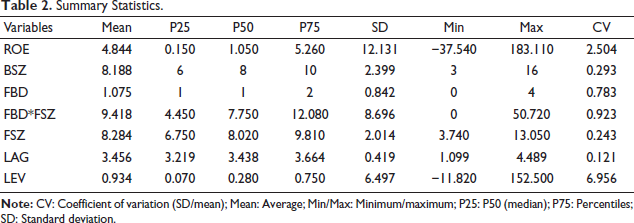

The descriptive statistics of the variables incorporated in this study (refer to Table 2). ROE with a mean of 4.844 and a wide range from a minimum of −37.540 to a maximum of 183.110, highlighting substantial differences in the firm’s profitability. The BSZ registers a mean of 8.188, and it ranges from 3 to 16, indicating significant variation in BSZ across the firms. The FBD is having a mean of 1.075, with numbers ranging from 0 to 4, indicating varying levels of FBD across the firms. The interaction of FBD and FSZ reflects a mean of 9.418, ranging from 0 to 50.720, indicating substantial variability in how FBD and FSZ jointly influence a firm’s performance. FSZ explicates a mean of 8.284 and varies from 3.740 to 13.050, capturing firms of diverse scales. The LAG reflects a mean of 3.456, with a minimum of 1.099 and a maximum of 4.489, reflecting the presence of both young and well-established firms. Similarly, LEV shows a mean of 0.934 but exhibits an extremely high coefficient of variation, suggesting the inclusion of highly leveraged or financially distressed firms. The descriptive statistics provide a solid base for the subsequent empirical analysis.

Summary Statistics.

Summary Statistics.

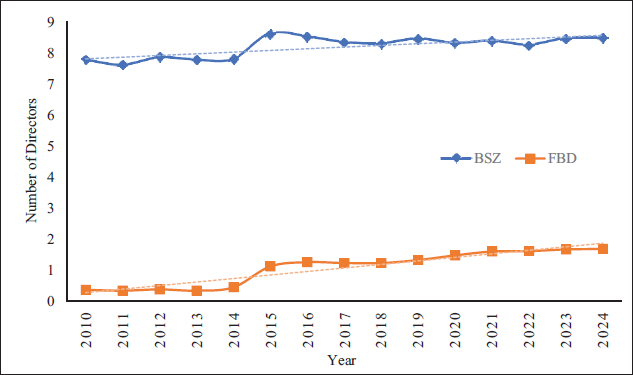

The results (refer to Figure 1) show a notable rise in FBD, as it was minimal prior to 2014, indicating limited gender diversity. However, a noticeable increase occurred from 2015 onward, potentially due to the government mandate requirement of at least one female on the board (Patil & Yadav, 2026; Zheng & Wang, 2024). The gradual increase in FBD also shows significant changes in BSZ, which indicates an intentional strategic shift towards inclusive governance rather than structural expansion (Biswas et al., 2021; Joecks et al., 2024). The stable BSZ reflects that including females does not coincide with an expansion in the board numbers, but instead reflects an intentional shift towards gender diversity.

Year-wise Board Size (BSZ) and Female Board Directors (FBD) Analysis.

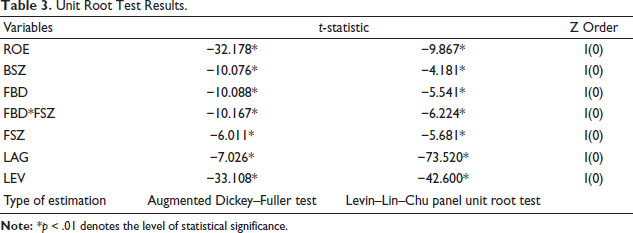

The present study employed the augmented Dickey–Fuller test and the Levin–Lin–Chu panel unit root test to examine the stationarity of selected variables (refer to Table 3). Both tests are widely accepted in accounts for potential deterministic trends and enhancing the reliability of the stationarity assessment (Wiredu et al., 2025; Zhao & Fan, 2025). The results indicate that all the included variables are stationary at the significance level (p < .01), and confirm that all the variables meet the stationarity condition required for reliable analysis and ensure robustness of the econometric modelling.

Unit Root Test Results.

Unit Root Test Results.

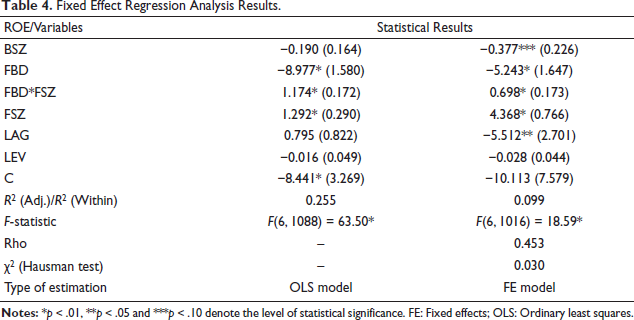

The present endeavour applied two estimation approaches, that is, OLS and FE models (refer to Table 4). The OLS model serves as a baseline, while the FE model is preferred, as suggested by the Hausman test result (Ab Aziz et al., 2024). In the OLS model, key variables such as FBD, the interaction of FBD and FSZ and FSZ are statistically significant and consistent, and more or less similar results are registered by the FE model. In both models, the FBD and firm’s performance relationship is statistically significant and negative, and it turns to a positive sign when FSZ plays a moderating role in this relationship. It supports the contingency theory and hypothesis, indicating that the FSZ moderates the FBD and firm’s performance relationship, and also supports another hypothesis that the direct relationship between FBD and firm’s performance is negative.

Fixed Effect Regression Analysis Results.

Fixed Effect Regression Analysis Results.

The FSZ reflects a strong, positive and statistically significant relationship with a firm’s performance in both models. It supports the hypothesis, indicating a positive FSZ and firm’s performance relationship. The results suggest that larger size firms perform financially better, due to advantages like better access to financial resources and stronger market positioning. In the FE model, BSZ is significant and negatively associated with a firm’s performance, suggesting that larger BSZ may curtail effectiveness and a firm’s performance.

The LAG shows mixed results across the models. In the OLS model, LAG has a positive but statistically insignificant relationship with a firm’s performance, while in the FE model, it turns out to be negative, suggesting that older firms may experience declining firm’s performance over time. The LEV registers the absence of a statistically significant relationship with the firm’s performance and indicates that capital structure does not directly influence the firm’s performance. The R2 of the FE model reflects a modest explanatory power, and the F-statistic confirms the model’s overall significance. Moreover, in both models, results establish that the FBD and firm’s performance relationship shifts from negative to positive when FSZ plays a moderating role.

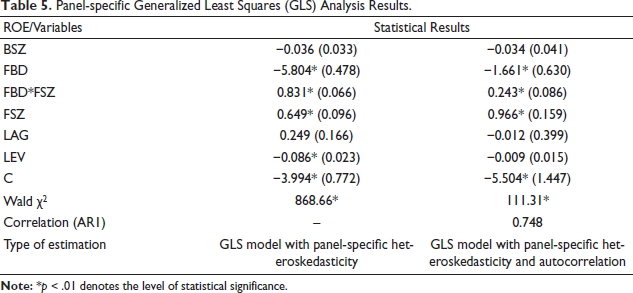

To validate the robustness of estimates, the study applied the GLS model (refer to Table 5). The GLS model results are consistent with the FE model and indicate the reliability. In particular, the significance of FBD, FSZ, and the level and direction of the interaction of FBD and FSZ are maintained. The GLS regression results present two models: first, controlling for panel-specific heteroskedasticity, and the second adjusting for both heteroskedasticity and autocorrelation (Daëron & Vermeesch, 2024). In both models, the results indicate that the FBD and firm’s performance relationship turns from negative to positive when FSZ playing a moderating role, which supports the perspective of contingency theory.

Panel-specific Generalized Least Squares (GLS) Analysis Results.

Panel-specific Generalized Least Squares (GLS) Analysis Results.

The FSZ reflects a strong, positive and statistically significant relationship with a firm’s performance in both models, confirming that larger size firms tend to be more profitable. In contrast, the LAG is statistically insignificant, implying that LAG does not significantly influence the firm’s performance. The LEV is negatively significant in the first model, reflecting that the higher LEV is associated with lower firm’s performance due to financial risk, which reduces firm’s performance, and BSZ is negative and statistically insignificant, indicating that BSZ has little effect on firm’s performance, because a larger BSZ may face coordination difficulties. The Wald χ2 confirms the model’s statistical significance. Thus, the GLS model accounting for heteroskedasticity and autocorrelation confirms the reliability of the results.

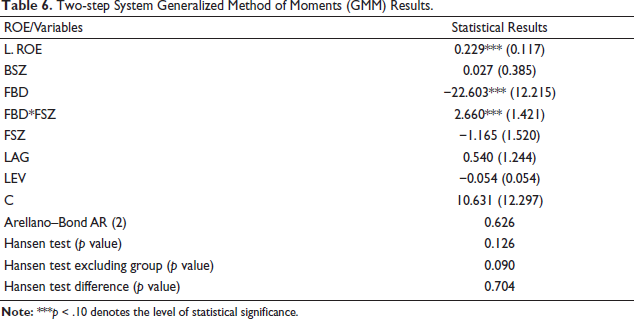

The two-step System GMM model ensures consistent estimates by using internal instruments derived from lagged variables (Assfaw & Sharma, 2024; Farzana et al., 2024). The lagged ROE is positive and statistically significant, reflecting persistence in the firm’s performance over time, which is suitable to address potential endogeneity concerns (refer to Table 6). The FBD and firm’s performance relationship changes from negative to positive when FSZ plays the role as a moderator, which favours the contingency theory. The results suggest that FBD alone is associated with a decrease in a firm’s performance. However, the interaction of FBD and FSZ implies the adverse effect of FBD on the firm’s performance. The result also indicates that higher FSZ does not mean that it improves performance; however, it plays a critical role in enhancing performance when acting as a moderator. Other variables do not reflect any statistically significant relationship with the firm’s performance.

Two-step System Generalized Method of Moments (GMM) Results.

Two-step System Generalized Method of Moments (GMM) Results.

The Hansen test reflects that the instruments are valid, as a p value > .05 reflects validity. Similarly, the Arellano–Bond AR (2) test reflects that there is no second-order serial correlation in the residuals. A p value > .05 supports this assumption and suggests that the instruments used are completely valid and robust. Also, the difference in the Hansen tests for the instrument confirms instrument reliability.

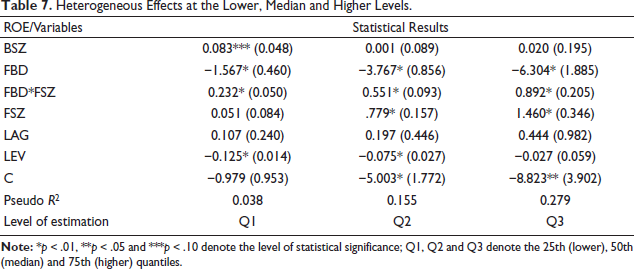

In addition, the quantile panel regression approach is estimated with the motive to check at which level the relationship of FBD and the firm’s performance is changing. Also, this approach more effectively controls for time-invariant firm-specific effects, a feature that makes it stronger to analyze the inconsistency at any level (Abed et al., 2025; EmadEldeen et al., 2025; Shawtari et al., 2016), which aligns more closely with the study’s primary objectives. Overall, the results reflect that the relationship between FBD and the firm’s performance is consistently negative at each level (refer to Table 7). Also, the moderating role of FSZ in this relationship consistently reflects the positive relationship at each level as expected, which showcases the robustness and reliability of the previous models.

Heterogeneous Effects at the Lower, Median and Higher Levels.

Heterogeneous Effects at the Lower, Median and Higher Levels.

In a broader manner, at the lower level, BSZ registers a positive and statistically significant impact on a firm’s performance, indicating that a larger BSZ may contribute positively to low-performing firms. It suggests that the benefits of a larger BSZ are more relevant in low-performing firms. The FBD confirms a negative and statistically significant effect on a firm’s performance across all levels, and FBD as a standalone is linked with lower firm performance. The relationship becomes negative to positive across levels when FSZ contributes as a moderator. The result indicates that the negative impact of FBD is mitigated in larger size firms, where greater resources and more inclusive governance structures enhance the effectiveness. The FSZ is positive and significant at the median and higher levels, which suggests that larger size firms perform better.

The LAG is positive but statistically insignificant across all levels, indicating that LAG does not have a meaningful effect on a firm’s performance at any level. The LEV registers statistically significant but negative effects in terms of a firm’s performance at the lower and median level, showing that higher LEV harms lower and median-performing firms. Overall, the quantile model across different distribution levels reveals that FSZ is a consistent and strong positive determinant of a firm’s performance.

The present study addresses an empirical analysis of FBD with various methods, as a minimum of female directors on the board is mandated by the government authorities (Aggarwal et al., 2019; Patil & Yadav, 2026; Zheng & Wang, 2024). The study contributes to the understanding of female roles in governance and a firm’s performance. While existing studies have produced mixed results, such as Brahma et al. (2021) found a statistically significant and positive relationship between gender diversity and a firm’s performance, based on critical mass theory, and some have also shown a positive impact (Nguyen & Huynh, 2023; Usman et al., 2026). In contrast, Marquez-Cardenas et al. (2022) found that females do not impact a firm’s performance due to the underrepresentation of women on boards, limiting their potential contributions, and few other studies found a negative or no relationship (Joecks et al., 2012; Mishra, 2025; Tanwer, 2025).

This study builds on prior literature as it selected the pharmaceutical sector to examine, as the sector is critical to healthcare. By employing different types of relevant econometric models, the study aimed to investigate the FBD and firm’s performance relationship, while considering the moderating role of FSZ. The empirical findings are consistent and provide interesting evidence that FBD does not register a statistically significant and positive relationship with a firm’s performance across the models, which implies that the standalone impacts of FBD do not lead to better firm’s performance and do not showcase a positive relationship, which supports the null hypothesis of a negative relationship between FBD and firm’s performance.

Further, the analysis also registers that the FSZ can be considered a major moderating factor in this relationship. Using the interaction term of FBD and FSZ, the study found that the negative effect of FBD is neutralized and eventually showcases a reverse effect in the larger size firms, which exhibited a statistically significant and positive association with the firm’s performance across the models, reflecting a contingent nature of the relationship. It supports the null hypothesis that larger size firms are better placed to take advantage of the benefits of organizational resources and also supports another null hypothesis that the size of the firm plays a moderating role in the FBD and firm’s performance relationship, which reflects that FSZ not only showcases positive impacts on the firm’s performance but also enhances gender diversity. The findings align well with the objectives of the study and confirm that the firm’s performance connotations of FBD are not consistent across sectors. The findings highlight the significance of contextual variables like FSZ in determining the validity and role of gender-diverse boards and reflect a more subtle picture of FBD and a firm’s performance relationship. The findings also carry important implications for future research and policies and offer directions for further examination of these relationships across different contexts.

Theoretical Implications

The study advances governance research by examining this relationship. The negative relationship between FBD and firm’s performance supports agency theory (Ain et al., 2021; Smulowitz et al., 2025), which suggests a reduced need for agency costs due to coordination issues and the requirement for broader oversight. Meanwhile, the positive relationship between FBD and firm’s performance, with the moderating role of FSZ, supports contingency theory (Donaldson, 2001; Li & Chen, 2018; Park, 2020), which suggests that larger size firms seek diverse board and strategic advice to bring in varied expertise. The study provides more contextual understanding of the board by adding different variables that influence the firm’s performance. The findings of the present study challenge the assumption of a direct positive relationship between FBD and a firm’s performance, as this study reflects a significant positive relationship that is shaped by FSZ. The study contributes to refining governance models by emphasizing the conditional nature of FBD. This study also confirms the year-wise FBD mandate effect, presents sector-relevant insights and extends the theoretical framework related to gender diversity.

Managerial Implications

The present study offers useful insights for policymakers, corporate leaders, advisors and investors by focusing on this conditional relationship. Smaller firms should rationally increase gender diversity on the board, reduce coordination challenges and dilute individual accountability. The study showcases the need for board policies to consider FSZ and avoid one-size-fits-all policies for emerging economies like India. The present endeavour recommends that, on the board composition strategies, firms should consider the FSZ, as it works as a moderator to improve the relationship and the firm’s performance. The study becomes more practical as governance authorities mandate the inclusion of females on the board (Aggarwal et al., 2019; Patil & Yadav, 2026; Zheng & Wang, 2024). Firms’ executives are encouraged to start performance-aligned, innovation and data-driven board systems to achieve the goals. The results are highly useful for critical sectors like healthcare, pharmaceutical and high-production manufacturing firms. With these results, strategy managers and specialists can design the governance structure by focusing on a gender diverse board in terms of improving the firm’s performance.

Future Scope and Limitations

Like any empirical study, this study is not without its limitations. While the results of this study offer key insights, but also limited by the sample size and are sector-specific in nature, which cannot be generalized to other sectors directly. The data set for the study is restricted to publicly listed firms. This study focuses on the quantitative models; future studies may involve other firms’ performance variables and may include additional board-related characteristics, such as board independence or ownership structure. Expanding the data set across different manufacturing sectors may reveal institutional influences on the role of females. Comparative studies with different sectors may be conducted, or conducted in different regulatory environments. The present research endeavour adds a strong foundation for further exploration of female roles on the board.

Footnotes

Acknowledgements

The authors are thankful to Dr Rohit Kumar Singh and Ms Neha Chandra for providing insightful input, and also to the anonymous reviewers for their insightful suggestions in improving the manuscript.

Authors Contribution

Inder Kumar: Conceptualization, methodology, data curation, software, formal analysis, writing—original draft, writing—review and editing.

Supran Kumar Sharma: Conceptualization, supervision, investigation, validation, visualization, data curation, writing—review and editing.

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author upon reasonable request.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.