Abstract

This study assesses how external stakeholders shape corporate social responsibility (CSR) reporting in a mandatory CSR regime. While previous research demonstrates the role of stakeholders in influencing responsible business conduct, research has offered little evidence on how external stakeholders, such as regulators and other external constituents, influence CSR reporting practice, particularly in a developing country context. We gathered relevant longitudinal data of 132 Indian companies for eight years from 2010 to 2024 (covering 2010, 2012, 2014, 2016, 2018, 2020, 2022 and 2024) to comprehend the CSR reporting trend preceding and following CSR regulation in India. The same data set was used for content analysis and quantitative analysis. Content analysis revealed an increase in CSR reporting in India over the studied years. Relying on a mixed-methods approach, we first analyzed panel data to examine how external stakeholders such as regulators, CSR-promoting institutions and industry characteristics affect CSR reporting. Our findings highlight that external stakeholders exert significant influence on CSR disclosure practices, with a stronger impact coming from environmentally sensitive industries. We complemented this with in-depth interviews with 20 senior CSR managers to interpret how organizational actors interpret the regulator’s CSR expectations and respond to institutional pressures. Our qualitative findings reveal that regulation, cultures and values, and firm reputation drive managers’ perception and action towards CSR reporting in a mandatory CSR setting. By integrating the quantitative and qualitative analyses, our study advances the existing scholarship on how external stakeholders shape CSR reporting behaviour in the context where regulators’ demands increasingly drive corporate accountability.

Keywords

Introduction

Corporate social responsibility (CSR) reporting has long been a vital tool for companies to signal their accounts of social and environmental conduct. While CSR reporting provides detailed information about a company’s impacts (Reid et al., 2024), it also serves as a strategic response to stakeholders’ pressures (Guo et al., 2024) and influences a company’s image (Arena et al., 2018; Garcia & Orsato, 2020), reputation (Sadou et al., 2017) and performance (Salehi et al., 2018). Stakeholder theory suggests that such assessments are shaped by the salience of different stakeholder groups (Mitchell et al., 1997; Saxton et al., 2021), with influence stemming from both internal and external constituents (Clarkson, 1991; Freeman et al., 2010). Recent studies highlight that external stakeholders such as regulators, the community and other key stakeholders play an important role in scrutinizing corporate conduct, especially in environmentally hazardous industries (Bhuiyan et al., 2023; McKinsey & Company, 2023). This study positions external stakeholders at the centre of CSR reporting dynamics in the Indian context.

Extant research suggests that external stakeholders can be as influential as, or even more influential than, internal stakeholders in shaping responsible conduct and public judgment (Moura-Leite et al., 2014). Yet past studies have mostly investigated the impact of internal stakeholders on CSR spending and reporting (Acuti et al., 2024; Moura-Leite et al., 2014), leaving limited evidence on how external constituents influence CSR reporting (Mahmood et al., 2024). Only a handful of studies have examined the impact of specific external stakeholders, such as creditors and media, on CSR and environmental disclosures (Ramadhini et al., 2020), revealing a notable gap.

Such an inquiry is warranted in the institutional context of developing countries, where the formal arrangements are less mature, and the demand for CSR accountability is driven by external actors (Ali et al., 2017). While research on CSR reporting has expanded in countries like China, Malaysia and South Africa (Igwe et al., 2023; Jamil et al., 2021; Parsa et al., 2021), India remains underexplored despite its position as one of the few countries to mandate CSR reporting and practice since 2014 (Panwar et al., 2023). As a corollary, studying how CSR regulation influences reporting practice is especially important given the continuous environmental externalities and violations in sectors such as mining and manufacturing (Kumari et al., 2022) and the strategic manoeuvre of reporting in these industries (Ren et al., 2023).

Regulatory interventions are known to influence corporate behaviour (Pedersen et al., 2013). Evidently, India witnessed a marked rise in CSR reporting since the CSR law was enacted in 2013 (Panwar et al., 2023). Whether this surge in CSR reporting reflects genuine engagement or a compliance-driven behaviour remains unclear. There is also a need to study how CSR managers interpret these regulatory and broader institutional demands in relation to CSR reporting.

Industry characteristics shape the content and emphasis of CSR reporting. Companies in polluting industries often engage in strategic CSR reporting to maintain a positive public image (Ren et al., 2023). Less is known about how industry type, particularly in environmentally sensitive sectors, affects CSR reporting in developing countries. Persistent environmental violations in mining and manufacturing industries raise questions about whether mandating CSR has enhanced CSR activities and reporting in the environmentally sensitive sectors in emerging countries, including India (Basu & Ray, 2020).

Most studies on CSR disclosure in developing countries rely on quantitative research methodologies that uncover broad patterns. However, they provide limited insights into managerial reasoning (Ali et al., 2017). With little qualitative (Mahmood et al., 2024; Pratihari & Uzma, 2020) or mixed-methods research on CSR reporting (Ervits, 2021; Khan et al., 2020), and research in the Indian context primarily focusing on analyzing secondary corporate reports (Chaudhary, 2020; Kumari et al., 2022), there is a need for deeper investigation on the subject.

In India, Section 135 of the Companies Act, 2013, mandates that businesses meeting certain thresholds allocate a pre-defined percentage of their net profit to responsible business conduct and publicly report these activities. This sets India apart from other countries where CSR remains largely a voluntary activity, driven by market, moral or reputational pressures. This also makes India a unique setting to examine how mandatory regimes shape CSR reporting (Bhagawan & Mukhopadhyay, 2025). After the implementation of the Companies Act, 2013, many firms continue discretionary CSR spending above required levels, particularly in manufacturing and services (Kapoor & Narayan, 2022). This suggests that regulation plays a role in reshaping organizational norms and expectations around CSR.

Against this background, the current study advances scholarship on CSR reporting by examining how external stakeholders, including regulatory and CSR-promoting institutions, shape CSR reporting in India’s mandatory regime. Using a mixed-method design, we first examine how external pressures interact with industry characteristics to shape CSR reporting, how managers interpret regulatory expectations and what motivates or constrains such disclosures. This contribution is salient in contexts where civil society remains less pronounced in demanding corporate accountability (Bhatia & Dhawan, 2024) and where CSR reporting inconsistencies and violations persist despite the mandatory requirements (Subramanian & Kumar, 2021).

Literature Review

Past research on CSR reporting draws the moral imperative from institutional theory (IT) (DiMaggio & Powell, 1983), among others. IT suggests that firms’ practices are shaped by both formal and informal institutions (Risi et al., 2023). Institutions are ‘formal or informal rules, regulations, norms and understandings that both constrain and enable behaviour’ (Galleli & Amaral, 2026; Wang et al., 2025). Instead of considering CSR as voluntary, IT places CSR within the broader realm of economic governance, characterized by drivers such as state regulation, industrial unions and societal norms. The neo-IT theory posits that the institutional environment exerts direct and indirect pressures on businesses, thereby influencing their practices, values and actions (DiMaggio & Powell, 1983).

External stakeholders, such as CSR reporting networks, non-governmental organizations (NGOs), standard-setting bodies and special interest groups, serve as CSR-promoting institutions that shape norms and expectations of responsible conduct (Sisaye, 2021). IT theory demonstrates how such actors, beyond market forces, shape CSR reporting practice (Chuang & Huang, 2018) across developed and developing countries (Zhao et al., 2020). Normative pressures from organizations like the United Nations Global Compact (UNGC), Global Reporting Initiative (GRI), International Organization for Standardization (ISO) 26000 and NGOs (Mahmood et al., 2024) encourage firms to adopt CSR initiatives and expand their reporting.

Stakeholder management theorists underscore the critical role of stakeholders in shaping firms’ socially and environmentally responsible behaviour (Hao et al., 2023). Following Freeman’s (1984) argument about the importance of stakeholders in making firms responsible, Clarkson (1991) distinguishes between internal and external stakeholders. While internal stakeholders such as shareholders, employees and the board are concerned about a firm’s financial performance, external stakeholders such as the government, special interest groups and regulatory agencies influence and are influenced by a firm’s actions (Bansal & Horning, 2020; Lüdeke-Freund & Dyllick, 2019). There has been considerable growth in the influence of external stakeholders on a firm’s actions in recent years (Bhuiyan et al., 2023). Some external stakeholders have more power than internal stakeholders to influence firms’ social actions through public opinion, which can negatively affect a firm’s image (Rivera-Franco et al., 2024).

Despite the increasing influence, research on how external stakeholders affect CSR reporting practices remains limited, especially in contexts where these roles might be more pronounced (Sun et al., 2025). The gap highlights the need for deeper inquiry into how businesses navigate these external pressures.

Corporate Social Responsibility Regulation and Corporate Social Responsibility Reporting

CSR reporting in developing countries is influenced by external stakeholders such as regulators and government regulations, which positively impacts the compliance and quality of CSR disclosure (Singh & Mukherjee, 2023; Subramanian & Kumar, 2021; Velte, 2023). Conversely, their absence is a primary reason for CSR non-disclosure, particularly in developing countries such as India (Desai & Rao, 2024; Kapoor & Sharma, 2024). A company’s image and reputation improve when it reports on its CSR activities due to regulations (Arena et al., 2018; Garcia & Orsato, 2020; Khalid et al., 2024). Past studies in developing countries like China (Situ et al., 2018) and Pakistan (Khan et al., 2020) have found increased CSR reporting after the introduction of CSR laws.

In 2013, the Indian government mandated CSR spending and reporting for profitable Indian companies by amending the Companies Act, 1956. Schedule VII of the Companies Act, 2013, even prescribes social activities that should be part of the CSR initiatives of Indian firms (Bhatia & Mahendru, 2020). Before this law, the government had mandated CSR in state-owned enterprises (SOEs) in 2010 on a pilot basis. Past research (Desai & Rao, 2024; Ghosh, 2020; Kapoor & Sharma, 2024) in the Indian context has established that regulation and the fear of non-compliance positively impact CSR reporting. Hence, we propose:

H1: CSR reporting will increase with the imposition of CSR regulation.

Corporate Social Responsibility Promoting Institutions and Corporate Social Responsibility Reporting

In the last two decades, external stakeholders, such as UNGC, GRI and ISO 14000, have been found to prescribe guidelines to firms about responsible business practices (Khan et al., 2021; Weber, 2014). These normative CSR-promoting institutions encourage regular communication of firms’ governance and social initiatives with their stakeholders (Gidage et al., 2024). For example, UNGC’s principle-based framework for CSR encourages firms to adopt it and report on its implementation to stakeholders.

Past studies (Orzes et al., 2018; Schembera, 2018) suggest that a firm’s membership with UNGC is highly correlated with CSR disclosure, albeit the relationship differs across countries. Studies in the context of Pakistan and China suggest that greater engagement of companies with CSR-promoting institutions and NGOs improves CSR reporting (Ali & Frynas, 2018; Khan et al., 2020; Zhang et al., 2020). In emerging countries, such as India, where civil society was historically less active in demanding CSR and firms did not undertake social initiatives unless pressure groups demanded it (Mishra, 2019), studying the roles of external stakeholders, such as CSR-promoting institutions and NGOs, in impacting CSR reporting assumes greater importance. However, there is limited research on how these external constituents influence CSR reporting (Mahmood et al., 2024). In the Indian context, a few content analyses and case-based studies examine the influence of global institutions such as GRI, UNGC and ISO 14001 on CSR and environmental disclosures (Banerjee & Rao, 2021; Kapoor & Singh, 2022; Mahmood et al., 2024). However, there is scant in-depth research linking normative CSR-promoting institutions and CSR disclosure in the Indian context. Hence, we propose:

H2: CSR reporting will increase with the existence of CSR-promoting institutions.

Industry Characteristics and Corporate Social Responsibility Reporting

Industry characteristics influence the nature and scope of CSR reporting. Companies operating in environmentally sensitive industries report more on their social and environmental performance (Bhatia & Makkar, 2020; Pizzi et al., 2024). Firms in environmentally sensitive sectors such as energy, mining and agriculture report more on CSR than firms in low environmental sensitivity sectors like banking (Rudyanto & Pirzada, 2020). Stakeholders scrutinize polluting industries more for their higher environmental visibility (Sodhi & Tang, 2018). Polluting firms strive to reverse their negative image and gain society’s acceptance through higher CSR reporting (Arena et al., 2018; Garcia & Orsato, 2020).

In India, there has been a sharp increase in the number of environmentally sensitive firms in the last decade, which has adversely impacted the social and environmental conditions in the country (Basu & Ray, 2020; Orazalin & Mahmood, 2018). Hence, CSR spending and reporting in Indian companies have often been linked to their environmental impacts (Bhatia & Makkar, 2020; Singh & Banerjee, 2024). Some of the CSR activities prescribed by Schedule VII of the Companies Act, 2013, focus on ecological balance, environmental sustainability and conservation of natural resources. The Securities and Exchange Board of India, which regulates listed companies in India, has introduced new disclosure requirements in 2023 that mandate the top 150 listed companies to offer ‘reasonable assurance’ on their environmental, social and governance impact (Singal, 2023). In this context, we expect environmentally sensitive Indian firms to engage in higher CSR reporting. Hence, we propose:

H3: CSR reporting will be more prevalent in environmentally sensitive industries.

Past studies also establish that a firm’s size and financial performance impact the intensity and quality of CSR reporting. India-specific studies show that larger firms provide more quantifiable and governance-linked CSR disclosures compared to smaller firms (Narayan & Pillai, 2022; Subramanian & Kumar, 2021). Higher financial performance of a firm is also associated with better CSR reporting (Desai & Rao, 2024; Narayan & Pillai, 2022). Both firm size and financial health enhance a firm’s ability to comply with and benefit from mandatory CSR disclosures, if there are governance mechanisms in place to facilitate implementation (Singh & Banerjee, 2024).

This study considers firm size and financial performance as control variables to delineate the influence of independent variables, CSR regulation, CSR-promoting institutions and environmentally sensitive industry, on CSR reporting, the dependent variable.

The following model has been employed to test the hypotheses:

We adopted a mixed-methods approach (Gibson, 2017) for data analysis. The quantitative part of the study examined how external stakeholders, such as CSR regulation, CSR-promoting institutions and environmentally sensitive industries, influence CSR reporting. The qualitative analysis included interviews with managers to gain deeper insights into their perceptions of mandatory CSR laws and to complement the findings of the quantitative analysis, aiding data triangulation (Gibson, 2017; Pedersen et al., 2013).

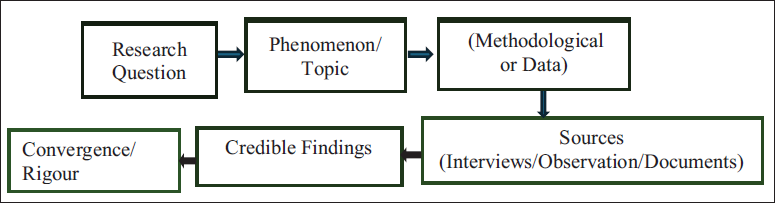

Guba and Lincoln (1994) recommend that data for research questions be obtained from multiple sources, such as interviews, observation and documents, to ensure credible findings. Convergence of findings from different sources can also help establish rigour in research (Figure 1). Accordingly, we deployed quantitative analysis, qualitative analysis and content analysis in the study.

Method of Triangulation (Guba & Lincoln, 1994).

Method of Triangulation (Guba & Lincoln, 1994).

We studied the relationship between the variables with the help of a random-effects model using R software. CSR regulation, CSR-promoting institutions and environmentally sensitive industries were considered independent variables while CSR reporting was the outcome variable. Firm size and financial performance were the control variables. We collected the required data regarding the variables from the firms’ annual reports and CSR reports. As CSR reporting is mandatory only for large profitable companies in India, we analyzed the annual reports of the top 500 companies listed on the Indian National Stock Exchange (NSE).

We gathered longitudinal data of companies over eight years from 2010 to 2024 (covering 2010, 2012, 2014, 2016, 2018, 2020, 2022 and 2024) to comprehend the CSR reporting trend preceding and following CSR regulation in India, similar to past studies (Arena et al., 2018; Whelan & Muthuri, 2017). We took the year 2010 as the base year, as in this year, the Indian government had introduced the CSR guidelines for all profitable SOEs. Because CSR reporting was not mandated for all other companies till 2014, we could gather the requisite data from only 132 companies to conduct the before-and-after analysis.

Measures for Variables

Corporate Social Responsibility Reporting

We developed an index for CSR reporting with the help of content analysis of the annual reports and CSR reports of the selected firms. Content analysis is a prevalent technique for studying firms’ annual reports across disciplines, including management (Duriau et al., 2007). It uses varied units of analysis such as words, sentences, pages or indices and categorizes textual documents into thematic components to derive valuable insights (Krippendorff, 2018).

With the help of content analysis, we developed a comprehensive checklist of 44 items for the CSR index after reviewing global CSR reporting standards, various conceptual frameworks and past research (Bhatia & Chander, 2014; Khan et al., 2020) to gauge the CSR reporting practices of the chosen companies. This checklist was structured into five sub-themes: Community involvement (12 items), labour practices (8 items), environment and energy (12 items), product and customer responsibility (9 items) and other CSR activities (3 items) (Appendix A, Table A1). The index served as a checklist to quantify the presence or absence of CSR-related information in the annual reports. It was treated as a binary variable, assigning a score of ‘1’ for the presence of an item and ‘0’ for its absence. Rigorous manual reviews and word checks of annual reports were conducted to ensure comprehensive coverage of items. CSR scores were aggregated for each company by dividing the number of reported items by the total number of items in the index.

It is critical to ensure reliability and validity in content analyses. Stability, reproducibility and accuracy serve as fundamental tests to assess data reliability. Due to the absence of CSR coding standards, researchers often rely on stability and reproducibility rather than accuracy testing (Vourvachis & Woodward, 2015). Because of COVID-19 restrictions during the study period, two coders, along with the authors, virtually reviewed and discussed the content analysis results to ensure reliability. Validity helps in bringing objectivity to data collection. Potter and Levine-Donnerstein (1999) propose a two-step process for testing the validity of content analysis: developing a coding scheme aligned with established theories and checking coder decisions against standards. Five themes emerged after reviewing extant literature on CSR reporting (Bhatia & Chander, 2014; Khan et al., 2021).

Corporate Social Responsibility Regulation

The Companies Act, 2013 mandates CSR spending and reporting in India for companies with a net worth of ₹5,000 million or more, or a turnover of ₹10,000 million or more, or a net profit of ₹50 million or more. We assigned a score of 1 to firms that qualified for such regulations; otherwise, 0.

Corporate Social Responsibility-promoting Institutions

We treated membership in UNGC as the proxy variable for CSR-promoting institutions. A company was assigned a score of 1 if it is a member of UNGC; otherwise, it got 0.

Environmental Sensitivity

Industries such as extraction or mining, cement, tobacco, petroleum and chemicals have been considered environmentally sensitive in past studies (Rudyanto & Pirzada, 2020). A company operating in any of these categories got a value of 1, else 0.

Control Variables

Firm Size

The logarithm of total assets was taken as a proxy for firm size.

Financial Performance

We considered return on assets (ROA) as a measure of financial performance, consistent with previous studies (Mishra & Mohanty, 2014). ROA was calculated as the ratio of net profit after tax (NPAT) to total assets (TA).

Qualitative Data Analysis

In-depth Interviews

We conducted online in-depth interviews with the top management from selected companies, leveraging researchers’ connections and employing the snowballing technique (Atkinson & Flint, 2001). The snowballing method involved seeking recommendations from interviewees to identify potential respondents, particularly senior managers from other organizations possessing knowledge and experience in CSR reporting. The initial few senior managers were contacted through researchers’ own contacts. With the help of the snowballing method, data of 62 executives were created. These executives were invited via formal emails to participate, of which 20 agreed, representing 20 companies from the initial 132 selected for data analysis (Appendix B, Table B1). Interviewees did not consent to revealing the name of their organizations. Semi-structured interviews were conducted, probing various aspects related to the study’s defined objectives. As interviews were conducted just after COVID-19, when online interviews were preferred, executives did not consent to physical interviews. So, interviews were conducted online via Zoom and Google. Each interview lasted approximately 60–90 min. We followed the guidelines by Farooq and De Villiers (2019) for conducting interviews. 1

Although English was predominantly used during interviews, Hindi (India’s official language) was occasionally used to get more clarity on managers’ observations. Only three interviewees consented to record their interviews. To facilitate open and detailed conversations, detailed notes were taken during and immediately after each interview for the rest of the interviewees instead of recording. The interview transcripts were shared with the respondents for validation while ensuring the confidentiality of information. Unique ‘B’ numbers were allotted to each interviewee to distinguish between respondents. Qualitative content analysis was employed to examine and interpret the conversation content. After completing the interviews, the researchers followed up with each other. They observed that the discussions had converged around a few central themes, thus indicating that theoretical saturation had been attained after 20 interviews (Guest et al., 2020).

Results

The findings of both the quantitative and qualitative studies are reported as follows.

Quantitative Analysis

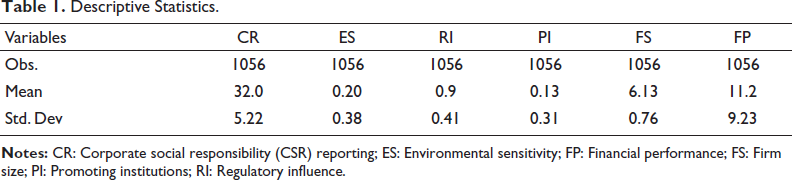

Table 1 presents the descriptive statistics of the six variables used in the analysis.

To test the proposed hypotheses, we adopted a random effects model after carrying out a series of tests for panel model selection. A significant F value at (p < 0.01) established that there was no individual-specific effect, thereby favouring a random effects model over the pooled ordinary least squares (OLS) method. Results of the Hausman specification test established that individual effects were not correlated with the regressor, leading to the choice of the random-effects model over the fixed-effects model. Because key variables in the study were dummy variables that had limited variation over time, the fixed effects model was considered inappropriate for the time-varying test of independent variables (Cameron & Trivedi, 2009).

Before testing the proposed model given in Equation (1), we pre-tested the suitability of the data for multivariate regression analysis. To test if the data fulfilled the OLS assumptions, serial correlation among the studied variables was conducted to find out the value-inflating factor (VIF) value. The mean VIF for all variables was 1.23, much below the accepted threshold value of 10. Further, as the error term was not constant, it indicated a problem of heteroscedasticity, which was resolved by employing a robust regression technique that identified outliers and minimized their impact.

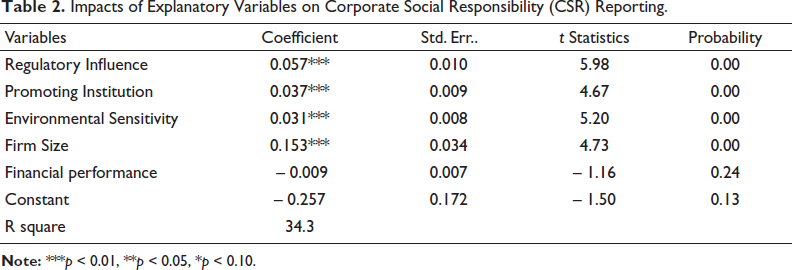

Table 2 presents the results of panel regression examining the relationship between the outcome and explanatory variables. Results show that the F test is statistically significant (F = 99.94, p < 0.05), indicating model robustness. R2 value of 34.3 indicated that the explanatory variables explained almost 34% variation in the dependent variable.

Results established a positive and statistically significant impact of regulatory influence on CSR reporting (β = 0.057, p < 0.01). This proved H1 and established that strong regulations improve CSR reporting in India, like in other developing countries such as China and Pakistan (Khan et al., 2020; Situ et al., 2018). The influence of CSR-promoting institutions on CSR reporting was found to be positive and statistically significant (β = 0.037, p < 0.01), supporting H2. Results were in line with previous studies conducted in India (Kapoor & Singh, 2022) and other countries with similar institutional contexts (Ali & Frynas, 2018). Further, results showed that environmentally sensitive industries had a positive and statistically significant impact on CSR reporting (β = 0.031, p < 0.01), like findings of (Bhatia & Makkar, 2020; Pizzi et al., 2024), thereby supporting H3.

The control variable, firm size, influenced CSR reporting positively and significantly (β = 0.15, p < 0.01), like the findings of Narayan and Pillai (2022). However, financial performance had a negative and insignificant impact on CSR reporting (β = −0.008, p > 0.05), refuting past research findings (Desai & Rao, 2024; Narayan & Pillai, 2022).

Results of Qualitative Analysis

Content Analysis

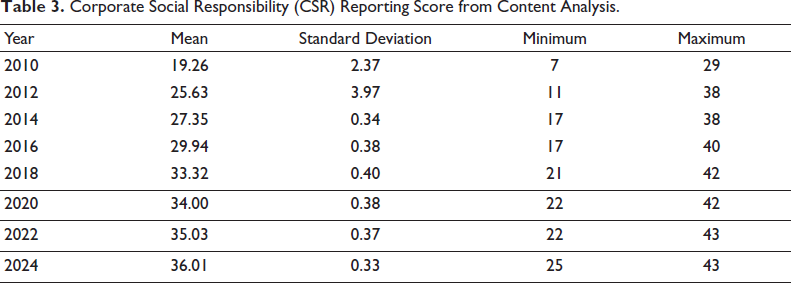

Results of the content analysis of CSR reporting are presented in Table 3. Results showed an upward trend in CSR reporting in India. The average CSR reporting score in 2010 was 19.26, which increased to 36.01 in 2024. Between 2010 and 2014, the increase in CSR reporting can be attributed to the introduction of guidelines on CSR spending and reporting in 2010. After mandatory norms were introduced for all profitable listed companies in 2014, there was a considerable increase in CSR reporting in 2016 and thereafter. However, as the number of firms coming under the ambit of law dwindled, there were some cases of non-compliance, and the growth was less in 2024 (Table 3). However, the overall increase in CSR reporting between 2010 and 2024 established an initial impression of the positive impact of regulations on CSR reporting in India.

We also used the Wilcoxon signed-rank test to compare the CSR reporting data across the studied period. The results in Table 4 show that out of 132 companies, CSR reporting increased in 87 companies, decreased in two companies and remained constant in the rest. A significant Z score at a 1% level implied that changes in CSR reporting were significant during the study years.

Descriptive Statistics.

Descriptive Statistics.

Impacts of Explanatory Variables on Corporate Social Responsibility (CSR) Reporting.

Corporate Social Responsibility (CSR) Reporting Score from Content Analysis.

Wilcoxon Signed-Rank Test Results.

Online in-depth interviews were conducted with 20 senior CSR managers to understand their perception of mandatory CSR reporting. Respondents’ observations during the interviews indicated that the increased CSR reporting in Indian companies was due to various other factors in addition to the hypothesized ones in the study. Three major themes emerged from the interviews as follows:

Law of the land/regulation: Like the findings of the quantitative study, regulatory compliance emerged as one of the key factors influencing CSR reporting. The following are the managers’ observations on CSR reporting: ‘[…] It is mandatory and we need to fulfil the criteria set by the Companies Act, 2013. […], now we have to invest in CSR activities like we pay tax’ (B10). ‘[…] You cannot avoid CSR as it has been made equal to corporate tax. It is now compulsory for the companies’ (B4). ‘[…] After the 2013 regulations, we are doing CSR activities regularly and keeping track of those activities by communicating about them’ (B7). ‘[…] As the Companies Act, 2013 made CSR mandatory, we approach it more systematically. However, balancing compliance requirements with meaningful social impact remains a challenge’ (B13). As Schedule VII of the Companies Act, 2013 requires Indian companies to spend their CSR budget on broadly 17 listed social activities, companies specifically target those activities. According to three interviewees: ‘[…] We have taken different projects which have been mandated in Schedule VII: Education and Swachh Bharat (Clean India Mission, a pet project of the Indian Prime Minister) has been our focus for CSR spending’ (B6 and B11). ‘[…] Our company spends on all the activities listed by the Indian government to comply with the regulations set by the Companies Act, 2013 [….]’ (B8). ‘[…] We align our CSR spending strictly with Schedule VII activities to ensure full compliance with the Companies Act, 2013’ (B15). The above responses highlight that, though CSR spending has increased, it is considered another type of corporate tax by many firms. Also, it is debatable whether governments should prescribe what CSR activities firms should undertake. Culture, value and tradition: CSR in India has been practised for a long period by invoking religion, culture and tradition (Ghosh, 2014). In the nineteenth century and the early part of the twentieth century, traditional business families in India used to spend a part of their profit on various social causes related to education, health and religion, which is practised even now. As mentioned by the respondents: ‘[…] CSR is not a mere event for us, but our traditional relationship with society. […] Our traditional CSR values aim to create a meaningful and lasting impact on the lives of people’ (B8). ‘[…] It is our ethical responsibility to help destitute people. Our culture and tradition have been a source of inspiration for decades to help needy people. […] We practiced it even before it was made mandatory’ (B3). Some managers also consider CSR as a means to fulfil their values. For example, one interviewee commented: ‘[…] Apart from following different norms, it satisfies me as a human being’ (B1) These quotes highlight how giving back to society is still considered an important aspect of business. Indeed, culture and history are informal institutions (Khan et al., 2021) that shape CSR reporting and practices. Company reputation: Creating a good reputation has been an important motivation for firms to report on CSR (Sadou et al., 2017). A firm’s communication about CSR demonstrates its commitment to society. As opined by interviewees: ‘[…] India has now a big middle class, and they are conscious of the responsibilities of companies towards consumers. […] It creates a reputational crisis when they feel that the company doesn’t treat them well’ (B9). ‘[…] Common people have a positive perception of the company when it spends on education and health. We communicate the CSR practices in our reports as activities in silence don’t work’ (B12). ‘[…] Companies invest in different social activities to build a common cause to make people realize that the company cares for society. This realization creates a company’s goodwill’ (B3). ‘[…] Transparent CSR reporting strengthens stakeholder trust and enhances our brand image, especially among socially aware consumers’ (B16). A few managers had contradictory views as follows: ‘[…] Before government guidelines, CSR was used as a tool to strengthen the relationship with society and create a positive perception about the company […]. It is no longer a strategic tool’ (B4). ‘[…] CSR used to differentiate us in the market, but after the regulations, every company is doing it in a similar way’ (B20). ‘[…] The mandatory nature of CSR has reduced managerial flexibility to design initiatives based purely on strategic priorities’ (B19). These observations point to the fact that, though CSR is supposed to be a strategic tool to enhance a firm’s image, when all firms spend and report on CSR, it no longer acts as a differentiator. Respondents also mentioned a few challenges, such as a lack of awareness and experience among implementing managers, local infrastructure, the seriousness of the top management and institutional support, that negatively impacted CSR reporting.

Discussion

To answer the question of why businesses adopt CSR reporting, extant research has turned to IT to explain its antecedents. But few have tackled the question of how external stakeholders shape such practices in emerging economies, especially those under a CSR mandate. Our study offers a clear account of how external stakeholders shape CSR reporting within the Indian context by using a mixed-methods research design that brings together qualitative interviews and a quantitative analysis. The integration of findings from quantitative, qualitative and content analyses contributes to data triangulation (Gibson, 2017; Guba & Lincoln, 1994; Mak & Huang, 2024; Pedersen et al., 2013), enriching the depth of the study’s outcomes.

Our study reveals a significant impact of external stakeholders on CSR reporting. First, CSR regulation has increased CSR reporting in India. Prior studies have indicated that the absence of CSR regulations or their inadequate implementation often results in the non-disclosure of CSR information in developing countries (Gerged et al., 2025; Khan & Lockhart, 2022). Institutional weaknesses in these countries have been the primary reason behind such underreporting. In developing nations like India, where voluntary CSR initiatives are limited, government institutions play a pivotal role in promoting CSR reporting (Basu & Ray, 2020). Our study substantiates the findings from limited exploratory studies highlighting the significant influence of CSR law in promoting CSR reporting and practices in similar emerging country contexts (Maqbool & Zamir, 2019; Mishra, 2019). Thus, we contribute to the existing literature by showing how regulation not only enhances reporting quantity but also how businesses disclose their social and environmental priorities, reinforcing arguments about institutional pressure.

Second, our study finds that CSR-promoting institutions positively influence CSR reporting. This substantiates prior research findings that underscore the pivotal role of external stakeholders such as CSR forums, multi-lateral agencies and networks in promoting CSR reporting in developing countries, including India, that have limited formal regulation and public pressure on firms to be socially responsible (Ali & Frynas, 2018; Mishra, 2019; Zhang et al., 2020). Advocacy of diverse CSR standards by these institutions plays a crucial role in pressuring firms to adopt such practices. Global standards such as the GRI guidelines and UNGC emphasize collaborative governance and transparent communication with stakeholders, further reinforcing CSR reporting by firms (Gidage et al., 2024). In so doing, our findings offer a more integrated view by navigating how businesses make sense of overlapping normative and regulatory expectations and use global CSR reporting guidelines strategically to enhance legitimacy.

Third, firms in polluting industries report more extensively and positively about CSR, substantiating earlier research findings (Bhatia & Makkar, 2020; Kumari et al., 2022). Heightened scrutiny by stakeholders (Sodhi & Tang, 2018) drives these firms to report extensively on CSR to enhance their image and reputation (Arena et al., 2018; Garcia & Orsato, 2020; Sadou et al., 2017). Therefore, CSR reporting works both as a strategic and defensive signalling function in environmentally hazardous industries, a theme that gained traction across CSR research.

Fourth, firm size significantly influences the extent of social and environmental disclosures, similar to previous research findings (Narayan & Pillai, 2022; Subramanian & Kumar, 2021). Larger companies, having more resources, disseminate more CSR-related information than smaller firms (Zhou et al., 2024). However, we do not find a company’s financial performance impacting CSR reporting in India. This could be because, as per the Companies Act of 2013, all listed profitable companies must comply with CSR reporting. Hence, a causal relationship between profitability and CSR reporting was ruled out.

Qualitative data analysis, comprising content analysis and in-depth interviews of managers, brings interesting insights about mandatory CSR reporting. Content analysis reveals a consistent uptick in CSR reporting after the introduction of CSR norms in India. Qualitative interviews establish that CSR reporting is driven by several societal factors such as culture, tradition and ethos, besides concern for reputation. Further, government regulation emerged as a common factor in both the qualitative and quantitative analyses, thereby integrating the findings of both types of research and facilitating data triangulation (Guba & Lincoln, 1994; Mak & Huang, 2024). This underlined the strong influence of formal institutions on CSR reporting (Desai & Rao, 2024; Kapoor & Sharma, 2024; Panwar et al., 2023). In the in-depth interviews, some managers expressed dissatisfaction by terming the CSR law as an additional tax. This can indicate a form of coercive CSR, which is found to have adverse effects in past studies (Jiang et al., 2022). Alternatively, a few studies also establish that coercive CSR (Pedersen et al., 2013; Ren et al., 2023) can enhance CSR reporting at the firm level and initiate mimetic action at the industry level. Thus, our mixed-method study finds a mix of these contrarian findings. Though CSR spending and reporting have increased because of the CSR law, some Indian managers hold a negative perception due to its mandatory nature. Here, our study synthesizes contrasting perspectives by demonstrating how mandatory CSR creates a dual dynamic—strengthening of reporting practices while generating managerial ambivalence.

Conclusions

The study contributes to understanding CSR reporting at the theoretical, policy and practice levels. Our overarching argument aligns with the theoretical perspective that external stakeholders shape CSR reporting practice in meaningful ways. Institutional pressure in the form of regulations not only ensures compliance but also initiates mimetic actions among firms within the same industry (Ren et al., 2023), fostering a collective contribution towards societal well-being. Such actions are important in developing countries, which are characterized by substantial income inequality, and corporations have historically been hesitant to contribute to societal welfare. Furthermore, CSR strategies of firms being influenced by societal factors such as culture, values, traditions and ethos both historically and currently, point to the inherent inclination of Indian managers towards responsible business behaviour. In so doing, our study extends IT by demonstrating how normative and regulative pressures act in a mandatory CSR setting and how businesses adopt strategies that balance compliance with efforts to maintain legitimacy.

Fear of punitive measures influencing CSR reporting raises questions about the commitment of managers to social and environmental goals. Further research is needed to unpack whether mandatory CSR disclosures reflect symbolic compliance or genuine responsibility. While there is scepticism around mandatory CSR reporting, the law has increased CSR contributions and widened corporate involvement in social and environmental causes (Ghosh, 2020).

This study holds implications for policymakers and managers worldwide, including in similar emerging country contexts. Managers can use mandatory reporting not only as a compliance tool, but to articulate strategic CSR priorities, strengthen stakeholder trust and benchmark against industry peers. Regulators can refine CSR-related policies by encouraging quality disclosure, sectoral-specific guidelines and assurance mechanisms. Finally, civil society organizations can use CSR disclosures to enhance monitoring, encourage accountability and work together with businesses on social and environmental causes.

Limitations and Future Research Directions

This study has several limitations that offer pathways for future research. First, the use of a predetermined checklist to evaluate CSR reporting limits the depth and scope of disclosures that can be captured. An inductive content analysis or open-ended coding strategy would allow future researchers to account for emerging categories and provide a holistic view of reporting practices. The study combines mandatory and non-mandatory reporting regimes, which can obscure how distinct forms of regulation shape reporting. Future research could examine these regimes separately to identify their differentiated influence. Additionally, the small sample in the qualitative study can be expanded to include several other stakeholders, such as middle managers, compliance officers, regulators and members of civil society, to facilitate a more layered understanding of how organizations interpret CSR obligations.

The quantitative data analysis explained only a modest share of variance in CSR reporting, suggesting that this might be due to the absence of organizational and contextual factors in the model. Future research could incorporate factors such as ownership structure, governance processes and leadership orientation to enrich the explanatory power of the model. Lastly, the use of secondary data from annual reports introduces potential reporting bias as businesses may strategically present their social and environmental activities. Therefore, complementary data sources, including standalone sustainability reports, websites, social media reporting, regulatory filings and independent audits, would strengthen the validity of future analyses.

Footnotes

Authors’ Contributions

All four authors have contributed to the writing of this work. They have not taken the help of any non-author or artificial intelligence for writing any part of the work.

Data Availability

The data can be made available on request.

Declaration of Conflict of Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Informed Consent

Informed consent for information published in this article was not obtained because the interviews were conducted online.