Abstract

Business mergers enable firms to produce more efficiently, diversify product lines or expand their operations. Indonesia’s economic growth has triggered the establishment of several multi-business firms over the past 30 years. These firms continue to develop their businesses in both related and unrelated fields. To manage their portfolios, these firms operate under holding companies. Contemporary business strategy development requires firms, including multi-business conglomerates, to be more effective and efficient. This study aims to examine and analyze the impact of holding formation and asset restructuring on state-owned enterprise (SOE) performance and to compare the financial performance of SOEs before and after holding formation. This study offers three novel contributions. First, it is the first empirical examination of SOE mergers in Indonesia. Second, it employs Monte Carlo simulation to project future performance, particularly for mergers that occurred during 2020–2021. This simulation approach was necessary because some sampled firms had not yet reached sufficient post-merger periods, whereas effect formation typically becomes apparent several years after a merger. Third, this study uses both cross-sectional and time-series dummy variable tests to obtain more robust results. The findings indicate that merger synergies fail to materialize when measured using both regression and pairwise comparison methods.

Introduction

In facing business competition, a firm needs to know its conditions because every firm has a different situation. A firm is said to be financially healthy if it can survive in a challenging economy, pay its obligations and finance operating activities to develop its business. Hossain’s (2021) research results revealed that mergers and acquisitions (M&A) could improve firm performance due to synergies obtained, market power, accelerated profitability and risk diversification. These findings exemplify how M&A benefits are not only reflected in the operational and market aspects of an entity, but also in its financial and strategic performance (Rashid & Naeem, 2017; Rufolo et al., 2025; Zhang et al., 2025). From a financial perspective, a holding firm intends to increase the capital structure of the consolidated financial statements to improve credit ratings and create financial independence due to the rising firm’s leveraging capacity, which eventually will increase the firm’s value. In Indonesia, holding entities were first established in 1997 in the fertilizer industry and continue to this day. During this period, the government actively established cross-sectoral holding companies in strategic industries, including energy, mining, banking, infrastructure and logistics. These cross-sectoral holdings were able to strengthen consolidated capital structure and improve leverage capacity, which leads to greater access to funding and investment, which translates to long-term growth.

Prior literature on M&A and asset restructuring has gained prominence and interest from researchers in corporate finance literature due to its strategic importance in generating value and performance improvement. However, empirical findings regarding the impact of M&A on firm performance remain inconclusive. M&A has demonstrated a significant positive effect on financial performance in China, with stable improvement trends following M&A decisions, although results vary across industrial sectors (Zhang et al., 2025). Conversely, M&A has negatively affected profitability and liquidity in post-merger firms in Pakistan (Rashid & Naeem, 2017). This inconsistency indicates that M&A outcomes are highly contextual and influenced by firm characteristics, institutional environments and the restructuring strategies employed.

Nevertheless, existing research has largely relied on historical data and has not considered future projections or short-term post-merger limitations (Chen et al., 2020; Wu, 2024; Wu et al., 2025). A further gap exists in that studies examining the impact of M&A and holding strategies on state-owned enterprises (SOEs) remain scarce in emerging market economies such as Indonesia. Indonesia has undertaken SOE restructuring through the formation of cross-sector holdings with substantial asset values; however, empirical evaluation of post-holding performance remains highly limited, particularly in measuring changes in capital structure, asset efficiency and financial performance.

This study conceptually and empirically extends the M&A literature by positioning holding formation and asset restructuring of Indonesian SOEs as its primary focus. Unlike previous studies that predominantly examined private firms using publicly available data, this study utilizes non-public data, tests the consistency of M&A impacts, and provides significant public policy implications. The present study aims to examine and analyze the impact of holding formation and asset restructuring on SOEs’ performance and to compare the financial performance of SOEs before and after holding. This study further analyzes the consistency and examines in detail the impact of M&A on SOEs (holding) in Indonesia.

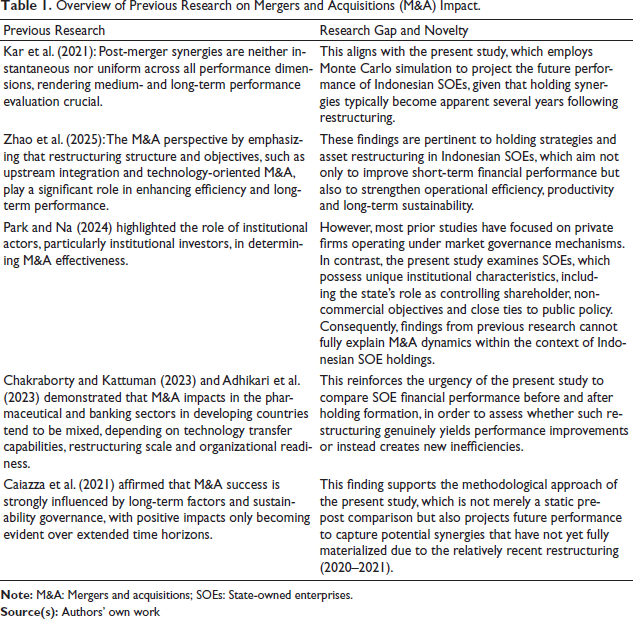

The research gap is evident from the fact that most previous studies focused on private companies operating under market governance mechanisms, so the resulting findings have not fully explained the dynamics of M&A in the context of SOEs. SOEs have unique institutional characteristics, such as the role of the state as a controlling shareholder, the existence of non-commercial objectives and strong linkages with public policy. Moreover, synergies from holding formation generally do not emerge instantly, but rather become visible several years after restructuring. A number of studies have also shown that the impact of M&A tends to be varied and contextual. Chakraborty and Kattuman (2023) and Adhikari et al. (2023) found that M&A outcomes in the pharmaceutical and banking sectors in developing countries depend on technology transfer capabilities, the scale of restructuring, and organizational readiness. Kar et al. (2021) confirmed that post-merger synergies do not occur uniformly across all performance dimensions, so medium- and long-term evaluation is important. Zhao et al. (2025) highlighted that the structure and objectives of restructuring, such as upstream integration and technology-based M&A, play a role in improving long-term efficiency. Meanwhile, Park and Na (2024) emphasized the importance of the role of institutional actors in determining M&A effectiveness, and Caiazza et al. (2021) showed that M&A success is heavily influenced by long-term factors and sustainability governance. These findings indicate that short-term evaluation alone is insufficient to comprehensively capture the impact of restructuring. Based on this gap, this study contributes by using original data without projections through a difference-in-differences (DiD) approach, supplemented by a Monte Carlo simulation to project the future performance of Indonesian SOEs as a robustness test. This is given that the relatively recent holding restructuring means the potential synergies have not yet fully materialized. This approach not only compares financial performance before and after holding formation statically, but also projects future performance to capture synergy effects resulting from gradually developing holding formation.

The novelties of this study are as follows. First, this study employs a Monte Carlo simulation to project the future period. The simulation was used because some sampling firms did not reach a specific post-merger year, while holding effects began to be seen several years after the merger. Second, this study is the first to empirically test the effect of SOE mergers in Indonesia, which possess unique institutional characteristics, a massive and relatively recent restructuring scale and provide significant public policy implications. Third, it utilizes data that is not publicly available because some sampled firms are non-listed entities. This study underscores the importance of post-restructuring financial performance analysis as a basis for evaluating formation success and as a reference for formulating future restructuring policies.

The remainder of this article is organized as follows. Section 2 presents the theoretical background, while Section 3 reviews the literature and develops hypotheses. Section 4 outlines the methodology. Sections 5 and 6 present results and discussion, and Section 7 provides conclusions, implications, suggestions and limitations.

Literature Review

Merger synergy theory posits that M&A can create value (Li & Huang, 2025) when the combined entities are able to realize operational, financial and managerial synergies, so that the combined value exceeds the pre-restructuring value of the firms. This perspective is complemented by market expectation theory, which states that capital market reactions to holding or M&A announcements are reflected in abnormal returns around the event date (Ma et al., 2016; Wu, 2024). This indicates that there are investor expectations regarding the successful realization of synergies and improved performance in the future. In addition, corporate restructuring theory views holding and M&A as strategic mechanisms for improving governance and reallocating resources to more productive uses. However, although restructuring tends to produce positive impacts, asset and cash flow consolidation can also increase debt capacity, potentially amplifying financial risk (Rashid & Naeem, 2017).

The presence of institutional theory deepens the understanding that the formation of SOE holdings in Indonesia is not solely driven by economic efficiency motives, but also by institutional pressures of a regulatory, normative and mimetic nature. The government, as the controlling shareholder, plays a dominant role in determining the direction of restructuring, so that holding formation often aims to enhance the legitimacy of public policy, strengthen coordination across strategic sectors and support the national development agenda. In this context, market expectations of synergies (Ma et al., 2016; Wu, 2024) are not only based on operational efficiency, but also on the belief that government institutional support can strengthen SOE stability and access to funding. In addition, restructuring as a resource-allocation mechanism also reflects the government’s efforts to create a more integrated and productive industrial structure in accordance with prevailing institutional pressures. On the other hand, agency theory provides the perspective that SOE ownership structure creates a more complex principal–agent relationship than private companies, because the government pursues not only profitability objectives but also social and political goals. This condition has the potential to create conflicts of interest among the government as shareholder, SOE management and other stakeholders. Holding formation can serve as a control mechanism to reduce agency problems through governance consolidation, enhanced oversight and strategic alignment among entities. The operational and managerial synergies described in merger synergy theory (Li & Huang, 2025) in the context of SOEs also encompass the reduction of functional duplication and improved coordination among companies within a holding group. However, increased debt capacity resulting from asset and cash flow consolidation (Rashid & Naeem, 2017) can also amplify new agency risks, particularly if investment decision-making is not fully based on economic efficiency. As a result, the effectiveness of SOE holding formation in Indonesia depends not only on the realization of economic synergies, but also on the institutional dynamics and governance mechanisms that influence the relationship among the government, management and the market.

A holding firm consists of the parent and the subsidiary firms that are involved in developing corporate strategies. Based on the parenting-fit matrix, a subsidiary firm can be located in the heartland, ballast, alien territory (Javier Forcadell et al., 2020) and value trap businesses. However, those studies have not empirically examined how such configurations affect financial performance in the context of SOE restructuring. The literature on M&A consistently positions corporate restructuring as a strategic mechanism for enhancing firm performance and resilience in response to dynamic business environments. Several studies indicate that M&A and restructuring, including holding formation, play a significant role in driving performance upgrading through asset consolidation, resource reallocation and strategy integration, both in international and domestic expansion contexts (Barbosa, 2020). This indicates that there are still limitations in explaining the restructuring dynamics of entities with special governance characteristics such as SOEs. The impact of M&A on performance is reflected not only in medium-term accounting indicators such as acquirer profitability and liquidity but also in capital market responses influenced by investor expectations and prevailing macroeconomic conditions (Aggarwal & Garg, 2023; Nuta et al., 2025). However, those studies adopted an approach focused on post-merger evaluation within a limited time horizon. They did not consider long-term performance projections when restructuring synergies had not yet fully materialized. During crises or periods of uncertainty, such as the COVID-19 pandemic, the effectiveness of restructuring and M&A becomes increasingly dependent on sectoral characteristics and firm strategies, which moderate the relationship between corporate actions and stock market performance. Furthermore, the strategic management literature affirms that M&A success is largely determined by the alignment of competitive strategies and internal process efficiency (Wang, 2024), including working capital management and post-merger operational governance (Habib, 2023). Recent studies also highlight that integrating business strategy with sustainability practices and environmental, social and governance (ESG) post-M&A can strengthen financial resilience and reduce financial distress risk, thereby expanding the meaning of synergy beyond short-term value creation to encompass long-term stability and sustainability mechanisms (Habib et al., 2024). Those studies remain limited to market-oriented firm contexts and have not specifically examined holding restructuring in large-scale SOEs with distinct institutional characteristics. This study positions itself as a new contribution by examining SOE holding restructuring in Indonesia, which has unique governance characteristics, dual objectives and the government’s role as controlling shareholder. Unlike previous studies, which generally rely on short-term historical evaluations, this study employs Monte Carlo simulation to project future performance in order to capture long-term synergy potential that has not yet been fully visible post-restructuring. This approach extends M&A impact analysis, which previously focused on accounting indicators or market responses (Aggarwal & Garg, 2023; Nuta et al., 2025), by incorporating performance projection dimensions and post-holding dynamics. In addition, this study also provides an empirical contribution by using non-public data from both listed and unlisted SOEs, thereby complementing the restructuring literature previously dominated by private companies and public data (Barbosa, 2020; Habib et al., 2024). Accordingly, this study not only enriches the M&A and restructuring literature but also offers a new perspective on the effectiveness of holding formation in SOEs in improving financial performance and long-term sustainability. Table 1 is presented to address these research gaps.

Overview of Previous Research on Mergers and Acquisitions (M&A) Impact.

Overview of Previous Research on Mergers and Acquisitions (M&A) Impact.

Utoyo et al. (2019) revealed the performance of SOEs before and after holding and used financial indicators as a determining factor for the performance of SOEs. The results of this study indicated that there are performance differences, seen through the increase in the return on assets (ROA). Moreover, there are performance differences in debt to assets, net profit margin and stock returns (Sengar et al., 2021). Nasir and Morina (2018) theorized that there are differences in financial performance before and after M&A, seen through the current ratio and ROA. Mergers take place to lower the costs of the firm relative to the same revenue stream as well as increase margins, reconfigure the firm’s product and service mix and distribution channels in a more effective and efficient way (Bianconi & Tan, 2019; Hossain, 2021; Yang et al., 2019).

According to Gitman and Zutter (2015), the solvency ratio, also known as the debt ratio, measures a firm’s ability to pay off its debts, either using equity or assets in the long term. The debt capacity of SOEs signifies a firm’s ability to take advantage of tax savings to increase the firm’s value. If we look at the Modigliani and Miller relevance propositions, an increase in debt will increase the market value. The collateral hypothesis states that SOEs with relatively large assets can raise funds from external sources. Firms that have debt need to pay interest, and this interest expense can reduce profits. Profit is the basis for calculating tax, so that interest can reduce the tax paid by firms. Sengar et al. (2021) revealed that the solvency ratio, represented by debt to assets, decreases before and after the holding period. Various factors contribute to this decrease, one of which is that the holding firm members are operating less than optimally; thus, they cannot optimize the cost of capital.

Gitman and Zutter (2015) defined liquidity ratios as measures of a firm’s ability to pay off its short-term debt. Increasing a firm’s liquidity will encourage SOEs to have sufficient internal funds as part of their working capital. However, an overly high liquidity ratio can hurt a firm’s performance because it cannot utilize its current assets for productive activities. These results are in line with Dewiningrat and Mustanda (2018), who underlined an adverse effect of liquidity on capital structure. With a considerable growth opportunity, Indonesia’s SOEs should be supported by cheaper external finance to help them take advantage of the existing investment opportunity set. The establishment of an SOE holding should increase the SOE’s business scale so that the investment opportunity set will be higher. Liquidity allows firms to invest without having to access new costly debt or equity, so liquidity plays a vital role in investment decisions, including mergers. Laiman and Hatane’s (2017) study, which postulated the impact of M&A on firms, supports this hypothesis.

H1: There is an effect of financial indicators on the performance of SOEs before and after holding.

H1a: There is a negative effect of solvency on the performance of SOEs before and after holding.

H1b: There is a negative effect of liquidity on the performance of SOEs before and after holding.

H1c: There is a negative effect of the investment opportunity set on the performance of SOEs before and after holding.

Financial performance reflects business sector results that show the overall financial health of the sector over a specific period (Naz et al., 2016). Ardany and Solikin (2018) and Utoyo et al. (2019) showed that the restructuring of SOEs impacts the financial performance of the holding firm as a whole. The establishment of an SOE holding must improve the performance of the holding and its subsidiaries. The use of external finance raises a manager’s vigilance because it can increase the cost of obtaining these funds. If income is low and costs due to debt are high, firms are in a state of insolvency. The establishment of an SOE holding will affect a firm’s solvency ratio. There is a significant difference in a firm’s debt before and after restructuring (Wulandari, 2020). The debt ratio of the merged firms tends to increase relative to the total wealth of the firms. The increase is due to the lack of synergy from the merger, so firms cannot optimize their debt (Ni’mah & Samryn, 2015). The establishment of the SOE holding will affect firms’ liquidity ratios. Wulandari (2020) and Ni’mah and Samryn (2015) stated that there is a significant difference in firm’s performance before and after restructuring, which is caused by the restructuring firm experiencing a decrease in liquidity because the firm focuses more on organizational adjustments one year before and one year after restructuring. One of the concerns is a firm’s ability to finance its short-term liabilities and adjust its short-term asset management. SOE holding makes firms have a different investment opportunity set. Sundari (2016) stipulated a significant difference in the price-earnings ratio and price-book value of firms conducting M&A. This difference is due to the market reaction that assesses the M&A, and it indicates that the firm cannot increase profits by taking advantage of the investment opportunity set.

H2: There is a performance difference between before and after holding.

H2a: The solvency of SOEs after holding is lower than before holding.

H2b: The liquidity of SOEs after holding is lower than before holding.

H2c: The investment opportunity set of SOEs after holding is lower than before holding.

This study focuses on SOE restructuring in Indonesia through holding and M&A strategies as instruments to examine improvements in operational efficiency, capital structure and inter-entity synergy. This study also employed panel data, incorporating both cross-sectional and time-series data to simultaneously analyze data from different units and periods. The sample in this study consisted of SOEs in the mining, oil and gas, financial services, insurance and pharmaceutical sectors. These sectors are among the most active in implementing restructuring policies through holding and M&A, making them relevant for examining the impact on firm performance. The diverse industry characteristics, ranging from capital-intensive to service-based and highly regulated sectors, enable comprehensive cross-sectoral analysis (PricewaterhouseCoopers [PwC], 2025).

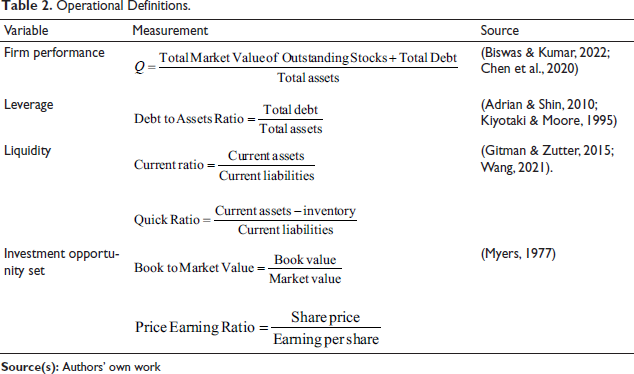

To examine the holding effect, this study uses actual data (without estimation) in holding formation. The initial step involves measuring each variable used in the study (Table 2), followed by selecting the appropriate estimation model, and then measuring using the regression method. Finally, the holding effect results are measured using the DiD method.

Operational Definitions.

Operational Definitions.

Where:

Tobin’sij = Tobin’s Q as a proxy of the firm’s financial performance

DARij = Debt to asset ratio

CRij = Current ratio

QRij = Quick ratio

BMVij = Book-to-market value

PEij = Price earnings ratio

εij = Error

All SOE samples underwent holding formation, and implementation occurred at different times across sectors, thereby forming a staggered treatment structure (Figure 1). Specifically, the mining sector (4 companies) formed a holding in 2017, the oil and gas sector (2 companies) in 2018, the financial services sector (10 companies) in 2019 and the insurance sector (2 companies) and pharmaceutical sector (2 companies) in 2020. The selection of sectors in this study reflects different industry characteristics and the relevance of each sector to SOE restructuring policy. The mining, oil and gas sectors exhibit capital-intensive characteristics and were among the earlier adopters of holding structures, so changes in financing capacity and investment efficiency can be more clearly observed. The financial services and insurance sectors operate under strict regulation, so holding implementation in these sectors relates to governance adjustments, risk management and financial performance. Meanwhile, the pharmaceutical sector represents an innovation-based strategic industry, where holding formation relates to improved operational synergies and research capacity. These differences in characteristics across sectors, along with their important role in national economic development and the implementation of government restructuring programmes, provide a relevant context for assessing the impact of holding and M&A strategies on firm performance in cross-sector analysis. Furthermore, variation in holding formation timing allows companies in sectors that have not yet undergone holding formation to serve as control groups for sectors that received treatment in previous periods. Therefore, this study estimates the model with two-way fixed effects encompassing firm and year fixed effects to control for both unobserved heterogeneity and common macroeconomic shocks, including those related to the COVID-19 pandemic. This specification is expected to strengthen the identification strategy and allow this study to better isolate the effect of holding formation on SOE performance.

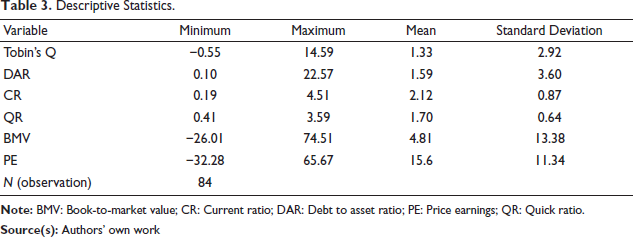

Descriptive Statistics

Table 3 exhibits the descriptive statistics of various variables used in the research model. The empirical reality is that SOEs possess highly diverse investment opportunities and market perceptions despite operating within the same state ownership and control framework. These differences may be influenced by variations in business sectors as represented in this study’s sample, profitability levels or capital structures, as well as non-uniform stages of holding restructuring (Li & Huang, 2025; Zhang et al., 2025).

Descriptive Statistics.

Descriptive Statistics.

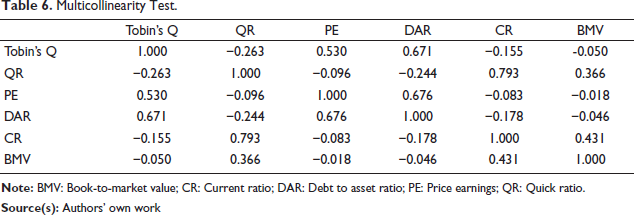

Several additional tests were also conducted in this study to ensure that the data are unbiased (Tables 4–6).

Chi-Square.

Hausman Test.

Multicollinearity Test.

In the chi-square test (Table 4), the p value was <0.05, indicating that the Fixed Effect Model (FEM) was selected, thus requiring the subsequent Hausman test (Table 5).

Based on the Hausman test, the p value was <0.05, confirming that the FEM was selected. The subsequent assumption tests employed were the multicollinearity test and the heteroscedasticity test. Table 6 presents the multicollinearity test results.

Based on the multicollinearity test results, all values were <0.85, thus passing the multicollinearity test. Based on the heteroscedasticity test, all variables had p values >0.05, indicating that the data passed the heteroscedasticity test.

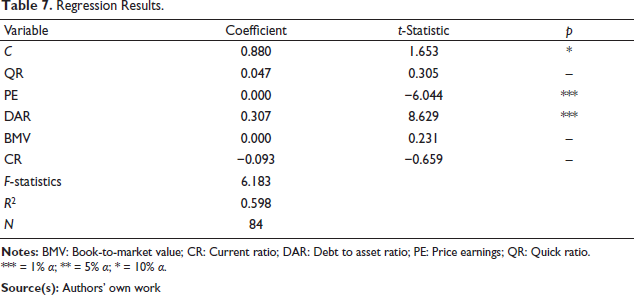

The regression results are shown in Table 7.

Regression Results.

To address potential causality bias and strengthen the identification strategy, this study employs a DiD approach with a staggered treatment design. The dependent variable used is Tobin’s Q, while the treatment variable is measured using a holding formation dummy that equals one after the company joins a sectoral holding and zero in the period prior. The variation in holding formation timing across sectors—specifically mining in 2017, oil and gas in 2018, financial services in 2019 and insurance and pharmaceuticals in 2020—allows companies that have not yet undergone holding formation in a given period to function as a temporary control group. The model is estimated using a two-way fixed effects panel encompassing firm fixed effects and year fixed effects to control for unobserved heterogeneity and common macroeconomic shocks.

The estimation results show that the coefficient of the holding variable is negative at −0.027 with a p value of 0.979 (Table 8), indicating that holding formation has no significant effect on ROA. This finding suggests that following holding formation, no meaningful financial performance change was observed in the SOEs studied. In other words, the synergies expected from holding formation had not yet materialized during the study period. The constant coefficient of 1.701, significant at the 5% level, represents the average Tobin’s Q of the firms when the treatment variable equals zero, after controlling for firm and time fixed effects. Overall, these results indicate that restructuring through holding formation has not been able to significantly improve SOE profitability, even though DiD approach controlled for differences in firm characteristics and external factors that changed over time.

Difference-in-Differences (DiD).

For the robustness test, Monte Carlo simulation was conducted with the following steps: The samples taken were audited financial statements from 2014 to 2020, adjusted by dividing the period into t − 3 to t + 3, with 2021–2023 included accordingly. The division of periods from t − 3 to t + 3 was employed to comprehensively capture firm performance dynamics before and after holding strategy implementation, while minimizing short-term bias (Ma et al., 2016). The 2021–2023 period was included as t + 1 to t + 3 to accommodate the early post-restructuring phase. The data used are ex-post facto data, namely the financial statements of each firm before and after holding, corresponding to each holding period. The financial statements were then analyzed using financial ratio indicators as measurement tools to assess the impact of the holding strategy on SOE performance. The study period encompassed three years before holding (t − 1, t − 2 and t − 3) and three years after holding (t + 1, t + 2 and t + 3), while t0 represents the year of the main event, namely the year of holding formation or M&A. News and information from mass media were used to determine the holding period. SOE holding period in each sector (Appendix 1, available as Supplementary file).

The limitations of financial data, especially for the period after 2020, cause an imbalance in the time-series model, which brings difficulty when comparing the before-and-after holding data. Most of the data was private or non-public firm data; thus, comprehensive data collection is required. In addition, several firms and industries just carried out holding after 2020, so the data was not balanced. This study employed a Monte Carlo simulation approach using Risk 8 Industrial software from Palisade to supplement the lack of data due to the incoming observation period and firms’ incomplete data. A Monte Carlo simulation with minimum and maximum value constraints was used, and the data distribution was limited within a standard distribution curve. The data results were within the range of shared data. They can be accounted for because the simulation was carried out with the intervention of random variables in predicting the probability of different results. The basic concept of Monte Carlo simulation uses an unexpected approach to explain the research model using a deterministic principle. For the 2022–2023 financial data, the authors used the Monte Carlo projection method. The projection of each variable follows the empirical rule with a total simulation of 10,000 times. In this practical rule, three times the standard deviation (SD) aims to produce normally distributed data. The Monte Carlo experiment using random values with each indicator’s minimum and maximum values was based on actual data. The source of data used was secondary data obtained from the financial statements of SOEs for the period t − 3 to t + 3 according to the period division and from the firm’s official websites, Indonesia Stock Exchange, and various literature and journals.

After estimating using the Monte Carlo approach, the results are then measured using a regression model (Appendix 2) with test sequences of cross-sectional bias and time-series bias. Moreover, Models 3–5 add a dummy variable for conditions before and after holding. The next step is the Research Model Pairwise (Appendix 3), which is used to demonstrate the direct impact of holding strategy implementation on firm financial performance through paired comparison analysis before and after holding. The pairwise test results function as validation and a complement to the panel regression analysis, thereby strengthening research inference power and consistency while providing practical implications for policymakers and SOE management in evaluating the impact of holding on capital structure, liquidity and firm value.

A robustness test was conducted by incorporating variables beyond market performance, namely financial performance, to examine the impact of successful SOE holding (Appendix 4, available as Supplementary file). The results of the study show that the formation of a holding company increases the company’s performance and value as well as market perception and even financing capacity, but its impact on the liquidity of company members is limited. These findings indicate that holding formation enhances market perception and firm financing capacity. This suggests that investors and creditors possess relatively high levels of confidence and optimism towards firms within the holding structure. Meanwhile, the impact on liquidity varies across individual firms, as QR and CR do not consistently increase. Thus, although holding strengthens firm attractiveness, liquidity evaluation cannot be disregarded and must remain a firm priority. The test results indicate that the direction and significance of the effects remain consistent (Appendix 5–6, available as Supplementary file).

Discussion

Firms must be careful in developing a merger strategy by integrating sources after the merger. The use of external finance is directed at the level of firm performance. The amount of external finance will increase the cost of obtaining these funds. If the proportion of external finance used in running the firm is substantial and income is relatively low, the firm’s expenses will increase, so that the firm will not record good performance. A firm financed by high long-term debt will contribute to its business risk, putting it in a state of insolvency. Current assets are an essential source of finance for a firm. Higher existing assets reflect a firm’s growth rate and ability to generate significant internal finance. In addition, a firm with a small liquidity value signifies that the firm is a risky firm and vice versa. From a micro perspective, capital market imperfections contribute to financial frictions, as a consequence of which firms face a cost premium on external finance. In these circumstances, the suggested solution is to use internal funds such as cash or other current assets rather than external funds. In addition, liquidity allows firms to invest without having to access new costly debt or equity, so liquidity plays a vital role in investment decisions, including mergers. On the other hand, high liquidity provokes managers to accommodate their self-interest by making investments or mergers that can harm the firm. In Indonesia, capital-intensive SOEs in the mining and oil and gas sectors tend to have greater external financing needs to support long-term projects and infrastructure investments (Li & Huang, 2025). However, high dependence on debt also increases exposure to global commodity price fluctuations and exchange rate risk, which can ultimately amplify insolvency risk. Meanwhile, in the highly regulated financial services and insurance sectors, liquidity is an important indicator for maintaining financial system stability, so merger decisions are more cautious and take capital adequacy into account. In contrast, in the innovation-based pharmaceutical sector, the use of internal funds to support research and development becomes more relevant due to high investment outcome uncertainty (Wu, 2024). Therefore, cross-sector characteristics in Indonesia indicate that the relationship between liquidity, external financing and merger decisions is not uniform, but is strongly influenced by the capital intensity, regulation and innovation orientation of each sector (Rashid & Naeem, 2017; Wang, 2002; Yang et al., 2019).

Holding can increase investment opportunities set on the performance of SOEs. However, in contrast to BMV, PE shows a negative and non-significant impact, meaning that there is a negative effect of the investment opportunity set on the performance of SOEs, but not significant. If a firm intends to gain a competitive advantage, it needs to invest more in research and development (R&D) and continue drug development. In addition, the firm that has performed a merger can enter the stock market to realize economies of scale, resulting in good firm value. Based on the results of regression testing, the price-earnings ratio is inversely proportional to firm performance. These results are because the sampling firms are in a cycle of the increasing stage before the merger (Zhang et al., 2018), so that the performance before the merger increases and after the merger decreases. These findings are supported by several studies linking market reactions integrated with macroeconomic factors. Market reactions can also be influenced by macroeconomic shocks and policy changes simultaneously (Duca et al., 2024; Fernanda et al., 2023). Such conditions create high uncertainty, whereby the impact may either amplify or dampen market responses to holding or M&A events. Future research may consider macroeconomic factors to understand how the market absorbs information related to holding (Ochirova & Miriakov, 2025). The negative and non-significant result on PE may reflect market expectations that have not yet fully materialized following holding formation, particularly in the financial services and insurance sectors affected by regulatory policy and industry reforms. Moreover, in the pharmaceutical sector, R&D investment requires a long time before yielding visible financial performance, so improvements in PE are not directly reflected in short-term performance. In the mining, oil and gas sectors, commodity price fluctuations and government policy interventions can also affect market perceptions, weakening the relationship between PE and performance. The institutional characteristics and economic dynamics of Indonesia reinforce the likelihood that the investment opportunity set reflected through market indicators does not yet fully capture the fundamental performance of SOEs following restructuring (Zhang et al., 2018).

Intra-industry mergers can improve firm performance, while cross-industry mergers will hurt performance. Studies that support the results are, as both postulated, that the restructuring of SOEs impacts the financial performance of SOE holding firm members. Restructuring can also stimulate firms’ business activities that eventually increase the firm’s overall performance. Mergers involve a complex and dynamic process encompassing trade-offs between the potential benefits of synergies and the potential costs of conflict in terms of personal, integration and organizational culture. Cultural differences may also decrease the firm’s value. As a result, cultural costs (language and law) and procedural (rules/regulations) will take place (Hassan & Giouvris, 2020) because they must adapt and carry out consolidation after the merger. When costs increase due to the use of high external funds, the firm’s performance due to mergers decreases. When short-term debt increases more than current assets, the liquidity ratio decreases. As the liquidity of SOEs decreases after holding, this hypothesis is accepted. Studies that support the results are, as both inferred, a decline in liquidity of firms undergoing restructuring due to the firms’ current focus on restructuring. The contrasting difference in PE remains in line with BMV, where an increasing mean of market value causes the decline in BMV. In this circumstance, the SOE holding firm members are considered overvalued. The investment opportunity set variable, namely BMV, decreases while PE increases. BMV reflects a substantial value compared to its market value. The decrease in BMV indicates that the SOE holding firm members are considered overvalued. Furthermore, the decrease in BMV accompanied by an increase in PE indicates that the market assigns a higher valuation compared to the current fundamental value. From the perspective of market expectation theory, this condition reflects investor optimism towards future SOE performance. SOE holding formation in Indonesia is largely conducted on an intra-sector basis, such as in mining, financial services and pharmaceuticals, so the potential for operational synergies is relatively greater than in cross-sector mergers. Nevertheless, the consolidation process in SOEs often faces bureaucratic challenges, differences in management systems and cross-entity regulatory adjustments, which can increase integration costs in the short term (Zhu et al., 2024). In the financial services and insurance sectors, for example, harmonization of risk and compliance policies takes time, so liquidity may temporarily decline. In the mining, oil and gas sectors, asset and project integration requires large investments that increase working capital needs (Zhu et al., 2024). Meanwhile, in the pharmaceutical sector, R&D synergies only become apparent in the long term, so the market tends to assign higher valuations even though fundamental performance has not yet improved. This explains why BMV declines, and PE increases, reflecting market optimism towards the prospects of Indonesian SOEs even as the restructuring process is ongoing and short-term performance has not yet fully improved (Ardany & Solikin, 2018; Cui et al., 2021; Ni’mah & Samryn, 2015; Utoyo et al., 2019; Wulandari, 2020; Zhang et al., 2018).

Conclusion

This present study aims to examine and analyze the impact of holding strategy and asset restructuring on the SOEs’ performance and compare the financial performance of the SOEs before and after the merger. The results of this study show that the merger synergy fails when measured using both regression and pairwise. If external financing dominates while firm income remains low, expenses tend to rise, leading to weaker performance. High levels of current assets may also trigger agency problems, as excess liquidity can be used for managerial perquisites. From a microeconomic perspective, capital market imperfections create financial frictions, causing firms to face higher costs of external financing. Therefore, the use of internal funds such as cash or other current assets is considered more efficient under such conditions. However, the empirical findings do not strongly confirm that increased external financing directly reduces firm performance. Instead, the impact of financing structure appears conditional, particularly in environments characterized by commodity price volatility and exchange rate risk. Moreover, the relationship between liquidity, external financing, and SOE performance in Indonesia should be interpreted cautiously due to limited statistical significance and sectoral differences. Changes in BMV and PE primarily reflect market expectations of restructuring benefits rather than definitive evidence of merger synergy outcomes.

This study advances the field of knowledge by presenting systematic empirical evidence regarding the impact of holding formation and M&A on financial performance and market-based firm value in SOEs in Indonesia, a context that remains relatively underexplored in the restructuring and corporate finance literature. By focusing on SOEs, this study also enriches the governance and public sector finance literature, while providing contextual insights into how state-led restructuring strategies influence firm value and financial behavior in emerging economies. Additionally, if firms want to gain a competitive advantage, they need to invest more in the sector that suits their needs. There are other motives than the financial profit used as the basis for mergers making the merger’s results not optimal financially. In these circumstances, the Ministry of SOEs can impose a policy in the holding scheme. The holding must continue to align with the right competencies to have good synergy and increase firm value. Future research should extend the observation period, incorporate non-financial performance indicators and apply more advanced methods, while policymakers need to ensure that SOE restructuring is supported by strong governance and sustainable financing frameworks and evaluated using both financial and market-based measures.

Footnotes

Acknowledgements

The authors would like to express their sincere gratitude to all parties who have supported the completion of this research. Special appreciation is extended to the affiliated institution for providing the necessary resources and academic support. The authors also acknowledge colleagues and reviewers for their valuable insights and constructive feedback throughout the research process.

Authors’ Contribution

The first author contributed to conceptualization, data collection and manuscript drafting. The second author contributed to research design, data analysis and supervision. The third author contributed to data processing, literature review and interpretation of results. The fourth author contributed to manuscript editing, review and final approval of the version to be published.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: The authors gratefully acknowledge Universitas Airlangga for funding this research under the Faculty Excellence Research Scheme 2021 and extend their sincere appreciation to all participants for their valuable contributions to the data collection process.

Informed Consent

This study does not involve human or animal participants. All data used in this research were obtained from secondary sources and publicly available data sets. Therefore, ethical approval and informed consent were not required. The authors declare that artificial intelligence (AI) was used solely for English-language proofreading and improving sentence structure. All research ideas, theoretical frameworks, methodology, data collection, analysis and interpretation are the original work of the authors. Any AI-assisted text was carefully reviewed and verified prior to inclusion, and no ideas, data or references were generated from AI. The authors take full responsibility for the content and integrity of this manuscript.

Supplementary Material

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.