Abstract

The rising proclivity among firms to amass cash and the influx of foreign flows in promoter-dominated Indian Inc. is a trend in development. In this backdrop, this study investigates the governance role of foreign institutional investors (FIIs) in determining the economic value of corporate cash resources in emerging markets. We report that FIIs strengthen the efficiency of cash assets in leading Indian firms. The effects amplify with a rise in ownership levels. Corroborating the global investor hypothesis, the results evidence that ‘foreignness’ of FIIs adds to their superior monitoring abilities, more so for firms facing deep agency costs and higher financial constraints, a peculiar feature of emerging markets. Importantly, these governance benefits persist during periods of high economic uncertainty, indicating that FIIs can act as reliable monitors when domestic institutions are weak. The results remain robust even after controlling for board and ownership variables. Possible concerns of endogeneity are addressed using generalized method of moments.

Introduction

Cash holdings are a significant asset for organizations, influencing shareholders’ wealth (Al-Najjar & Belghitar, 2011; La Rocca & Cambrea, 2019; Opler et al., 1999). Firms maintain cash for financing investments, servicing debt and precautionary motives (Al-dhamari & Ismail, 2014; Campello et al., 2010; Chen et al., 2017; Jensen, 1986). However, hoarding excess cash is associated with the ‘dual problem’ of lower returns and agency issues (Luo & Hachiya, 2005; Reeb, 2007) owing to suboptimal investments (Tong, 2010). Agency theory posits that entrenched managers tend to tunnel cash when governance is weak (Singh et al., 2023), more so because cash assets are under the direct discretion of managers (Myers & Rajan, 1998). To boot, recent trends show proclivity among firms to amass cash, and India is no exception to this (Wellalage et al., 2023; Yung & Nafar, 2014).

Foreign institutional investors (FIIs) play a key role in ameliorating the corporate governance environment (Gillan & Starks, 2003; Pronobis & Schaeuble, 2020) and add economic value to the firm (Banik & Chatterjee, 2020). FIIs are more independent and practical when evaluating return on their investments (Ferreira & Matos, 2008). They monitor managers (Cheng et al., 2010), making it costly to tunnel resources for their self-interests (Bena et al., 2017). FIIs ‘vote with their feet’ and are likely to exit mismanaged firms (Sridharan & Joshi, 2018). Therefore, we examine the moderating role of FIIs on the marginal value of cash in leading Indian firms.

While the literature has paid attention to their individual linkages (e.g., Das et al., 2025; Loncan, 2020), there is a dearth of studies analyzing the amalgamated impact of cash and FIIs on shareholders’ wealth under the unique conditions of uncertainty and financial constraints (Ilyas et al., 2023; Karim & Ilyas, 2020), especially in the context of emerging economies like India. India presents a unique case for several reasons. India’s stature and economic growth have seen unprecedented levels in recent times (Organization for Economic Co-operation and Development [OECD], 2026). Further, Indian firms are dominated by controlling owners who bear considerable influence on corporate decisions (Dharwadkar et al., 2000). The profusion of FIIs is believed to have an impact on the governance environment and decision-making and presents a case study (Dhingra et al., 2016). FIIs are key players in the Indian markets and share a significant relationship with stock market returns, volatility and economic growth (Banerjee & Banerjee, 2012; Jena et al., 2020; Mukherjee & Tiwari, 2022). India’s attractive economy, combined with landmark government initiatives, is the key driver of foreign investments in India (Chauhan & Kumar, 2017; Nikhil et al., 2023).

Reporting positive moderation effects, we argue that cash strengthens business performance in the presence of adequate monitoring by FIIs, corroborating the global investor hypothesis. This is true even during times of uncertainty, financial constraints and acute agency issues. To the best of our knowledge, this is one of the novel studies to report such findings. We contribute to empirical literature by introducing contextual factors that better explain the cash–performance relationship. The study will act as evidence for furthering the flow of ‘foreign’ capital into emerging markets from an economic, governance and financial facet (Khanna & Palepu, 1999). Considering the channels of agency costs, financial constraints and uncertainty, we add to the scant literature that underpins the monitoring role of FIIs in the unique institutional context of emerging markets.

Literature Review

Corporate Governance and Value of Cash Holdings

Strong corporate governance is fundamental in shaping investors’ perceptions about the marginal value of cash held by an entity (Dittmar & Mahrt-Smith, 2007; Kusnadi, 2011; Nam & Nam, 2004). For instance, Kalcheva and Lins (2007) report that cash resources are favourably valued in countries with strong investor-protection and lower agency costs. Similar findings were reported by Pinkowitz et al. (2006), Frésard and Salva (2010) and Jabbouri and Almustafa (2020).

Monitoring Role of Foreign Institutional Investors

With global barriers fading away, financial flows crossed borders, leading to a growth in foreign investments. However, there is heterogeneity in the monitoring role of institutional investors (Ferreira et al., 2017). In contrast to domestic institutional investors (DIIs), FIIs do not have close relations with company insiders and management and, hence, have no compulsions of loyalty towards them (Aggarwal et al., 2011). They are more focused on their investments and associated returns. The global investor hypothesis posits that FIIs possess a comparative advantage due to their proclivity for activism and their capacity to implement advanced monitoring technologies (Kim et al., 2016). Their international experience, governance skills and flexibility in re-allocating funds add to their advantage (Mian & Mian, 2023). Moreover, the governance effectiveness of institutional investors is contingent upon the institutional and legal norms of their domicile jurisdiction (Das et al., 2025). FIIs from countries with superior investor protection enhance corporate governance (Areneke et al., 2022) and reduce earnings management in investee firms in emerging economies (Gu et al., 2022; Lel, 2018). Consequently, cash contributes to the market value of firms when FIIs hold a higher ownership (Karim & Ilyas, 2020; Loncan, 2020). Unlike DIIs, FIIs positively moderate the contribution of ‘excess’ cash to firm valuation (Ilyas et al., 2021, 2023; Ward et al., 2018). In sync with existing literature, the following hypothesis is being framed:

H1: FIIs strengthen the contribution of cash holdings to firm performance.

The institutional environment of emerging markets possesses distinct characteristics (Young et al., 2008). Amateur bond markets and an evolving regulatory framework, together with concentrated ownership structures driven by family and state, lead to heightened agency costs as well as information asymmetries, having a direct bearing on corporate decisions (Manos et al., 2007; Stein, 2003). Agency issues lead to subpar investments, eroding shareholders’ wealth (Jiang et al., 2011). Prior research indicates that FIIs are more effective in monitoring environments that are susceptible to information asymmetries and agency problems (Das et al., 2025; Lel, 2018). They improve voluntary disclosures (Tsang et al., 2019) and inhibit earnings management in emerging markets (Mian et al., 2023). FIIs are, hence, deeply interlinked to agency costs through various channels. In the sub-sample analysis, we investigate the moderation effects of FIIs in low and high agency firms, based on median values of agency costs (captured using asset utilization ratio and operating expenses to sales).

H2: FIIs strengthen the contribution of cash holdings to firm performance, more so for firms facing higher agency costs.

FIIs decrease the cost of new capital (Chari & Henry, 2004). Simultaneously, they enhance access to funds (Stulz, 1999). With the presence of FIIs as shareholders, firms experience better corporate governance and more transparency, thereby reducing information asymmetries (Huang & Zhu, 2015). This helps cut down on premiums charged by potential investors on new funds supplied. The need for firms to hoard cash falls, leading to optimal investment choices. FIIs, therefore, alleviate financial constraints by improving access to new financing (Laeven, 2003). Smaller firms, being more constrained, benefit immensely from the monitoring of FIIs (Loncan, 2020). Using size-age index (Hadlock & Pierce, 2010) and cash flows, the study re-examines the moderating role of FIIs for constrained versus unconstrained firms.

H3: FIIs strengthen the contribution of cash holdings to firm performance, more so for financially constrained firms.

Economic Policy Uncertainty (EPU) severely impacts cash holdings and foreign flows (Cui et al., 2022; He et al., 2021; Simran & Sharma, 2024). High EPU fuels the tendency of firms to amass cash (Das et al., 2025; Didin-Sonmez et al., 2024; Duong et al., 2020), exacerbating the need for monitoring. Withal, FIIs outperform leading indices during high uncertainty (Jain & Saha, 2023). EPU is also a key determinant of the value of cash (Tran, 2021). Therefore, it becomes essential to test the monitoring role of FIIs under environments of uncertainty.

H4: FIIs strengthen the contribution of cash holdings to business performance, more so when EPU is high.

Materials and Methods

Sample Description

We begin by considering a full set of Indian companies listed on NIFTY 500 over the period 2013–2022. Based on the Global Industry Classification Standard (GICS®), financial firms and firms with missing data are excluded from our sample. The final sample consists of a panel of 2,253 firm-year observations based on 280 unique firms. The firm-level data has been obtained from Bloomberg®. Data for foreign institutional holdings has been extracted from Prowessdx, Centre for Monitoring Indian Economy (CMIE), while the macroeconomic variable is gathered from the World Bank database.

Measurement of Variables

The key variable is ‘FII’, representing the proportion of foreign institutional ownership in the firm in percentage 1 (Ilyas et al., 2021; Karim & Ilyas, 2020; Loncan, 2020). Firm performance (Tobin’s Q and net operating profitability) is the main dependent variable. Short-term investment decision is represented by the sum of cash and cash equivalents scaled by the book value of assets. The complete list of variables is provided in Appendix A, Table A1.

Empirical Model

The estimation technique involves a combination of static and dynamic regression models. The static model is described in Equation (1) that represents firm performance (Tobin’s Q and profitability) as a function of CASH, FII and an interaction term, CASH*FII, along with firm and country-level control variables. Fixed-effect (FE) linear regression is employed along with industry and year-fixed effects (Dittmar et al., 2003; Kalcheva & Lins, 2007; Popli et al., 2020; Sah, 2020). Standard errors are robust to heteroskedasticity. The system’s generalized method of moments (GMM) model underpins the importance of dynamism in panel data and incorporates the lagged value of the dependent variable in the regression equation (Equation 2). Standard tests like AR (2), Hansen J and F-statistic are reported to gauge the fitness of the model. Robust standard errors reported are adjusted as per Windmeijer (2005) to have more accurate inferences.

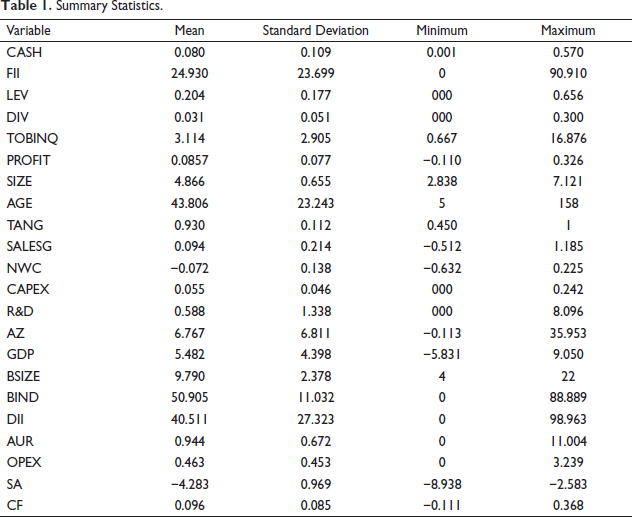

Summary Statistics

The summary statistics for key variables regarding Indian sample firms over the period 2013–2022 are shown in Table 1.

Summary Statistics.

Summary Statistics.

The average Tobin’s Q is 3.114, while net profitability is 8.57%. The mean value of DIV is 0.031. The average CASH is 0.08, meaning Indian firms carry around 8% of their total assets in cash and liquid assets (Mittal & Singh, 2024). The average FII stands at around 25% in our sample. This is clearly higher than around the 8% reported by Shruti and Thenmozhi (2024) and Bena et al. (2017), thus indicating a rise in foreign flows in Indian Inc. The financing structure of leading firms in India is dominated heavily by equity investors as leverage constitutes meagre 20.40% of the total assets. The Indian economy exemplifies sustained growth in its GDP over the period 2013–2022, with an average rate of 5.48% per annum.

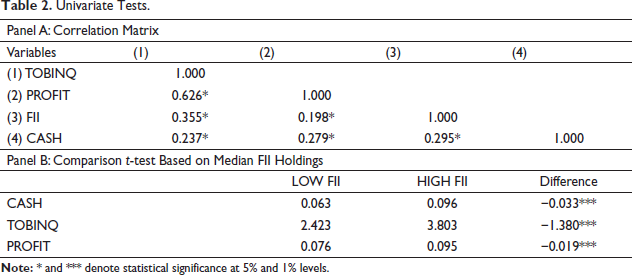

Pearson’s correlation coefficients in Panel A of Table 2 clearly suggest that CASH and FII are positively correlated with TOBINQ and PROFIT. All coefficients are well within the generally accepted limit of 0.80. As a further check, we analyzed variance inflation factors (VIF) (Appendix A, Table A2). All VIF scores are well below 10, which is the touchstone for detecting multicollinearity (Gupta et al., 2019). Hence, there are no concerns of multicollinearity in the study.

Univariate Tests.

Univariate Tests.

Panel B compares the mean values of CASH, TOBINQ and PROFIT of sample firms based on the median level of FII ownership. It documents that firms with high FII are associated with higher cash assets and better performance, surmising the governance role of FIIs.

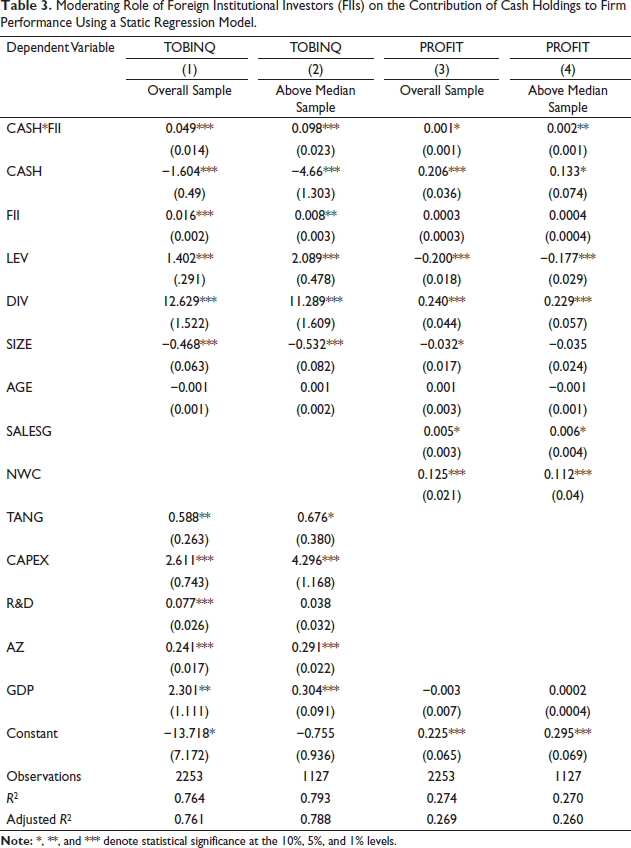

Table 3 discusses the impact of FIIs on the contribution of cash holdings to firm performance in Indian sample firms.

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Using a Static Regression Model.

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Using a Static Regression Model.

Table 3 evinces that the cash holdings have a significantly negative (positive) standalone impact on market value (profitability) of Indian firms, in sync with agency (precautionary motive) considerations (Bates et al., 2009; Jensen, 1986; Yun et al., 2020). The presence of FIIs has a positive and significant impact on Tobin’s Q (Seth & Mahenthiran, 2022). Good governance is directly related to enhanced operating and market performance of Indian firms (Narula et al., 2023). The coefficient of interest, the interaction terms (CASH*FII), are significantly positive. Putting things into perspective, although the standalone impact of cash on firm value is negative, in the presence of FIIs, this effect turns positive (column 1). While FIIs augment the positive impact of CASH on firm profitability (column 3). This implies that FIIs bring in good governance in the firm in letter and spirit, inculcating confidence in investors about the functioning of the firm. The investors believe that FIIs would act as a ‘monitoring device’ on managers and, hence, the cash resources would be optimally utilized and not tunnelled. This positively drives the performance of investee firms (Ilyas et al., 2021; Loncan, 2020).

As a further check, we investigate whether the strength of moderation changes with the change in institutional holdings. Columns 2 and 4 exhibit the moderating role of FIIs when the holdings are high (FII > median level of 17%). The coefficient of the interaction term gets doubled, indicating that the moderation effect amplifies at higher ownership levels. Overall, we validate the applicability of the global investor hypothesis (Kim et al., 2016).

As for control variables, leverage (LEV) has a positive (negative) impact on Tobin’s Q (profitability). Firms carrying leverage transmit positive signals to investors about the health of the company, displaying the ability to service and repay debt holders (Ibhagui & Olokoyo, 2018). Withal, debt deteriorates operating efficiency, owing to high agency costs (Mathur et al., 2021). The information content hypothesis drives firm performance in dividend (DIV) paying firms (Miller & Rock, 1985; Rees, 1997). When markets are imperfect with high information asymmetries, more so in emerging markets, dividend commitments signal key information to stakeholders and reduce agency issues (Dionne & Ouederni, 2011; Ham et al., 2019; Le & Phan, 2017). Year-on-year growth in revenues (SALESG) is directly associated with enhanced profits, as higher turnover translates into greater profits (Tripathi et al., 2024). Working capital (NWC) ensures a smooth operating cycle and improves business performance (Banjade & Diltz, 2022). Contrary to common belief, smaller firms (SIZE) command better market values as they possess higher growth potential (Ullah et al., 2021). Capital expenditure (CAPEX), R&D (Mak & Kusnadi, 2004) and asset tangibility (TANG) favour Tobin’s Q (Ramzan & Lau, 2022). Altman Z-score captures the possibility of a firm going into bankruptcy, where higher (lower) values indicate less (more) risk. Quite relevantly, firms with lower bankruptcy risks have better values. Regarding macroeconomic variables, it can be argued that firm performance is directly linked to the economic cycle (Natto & Mokoaleli, 2025).

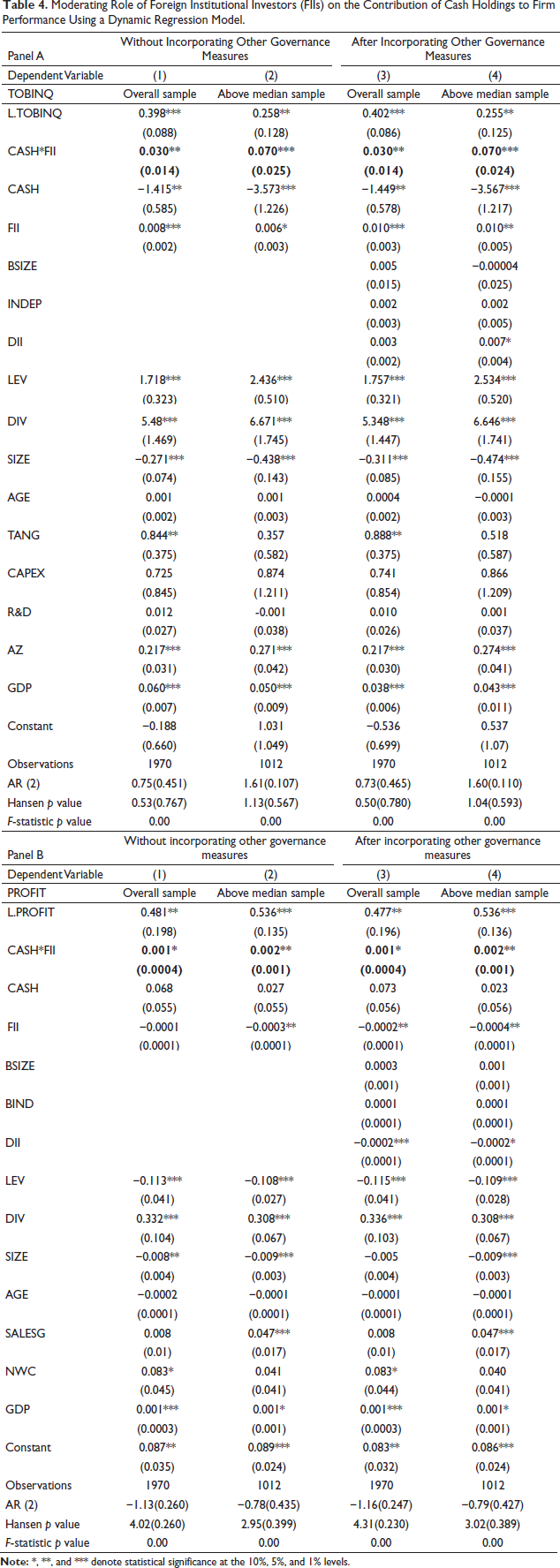

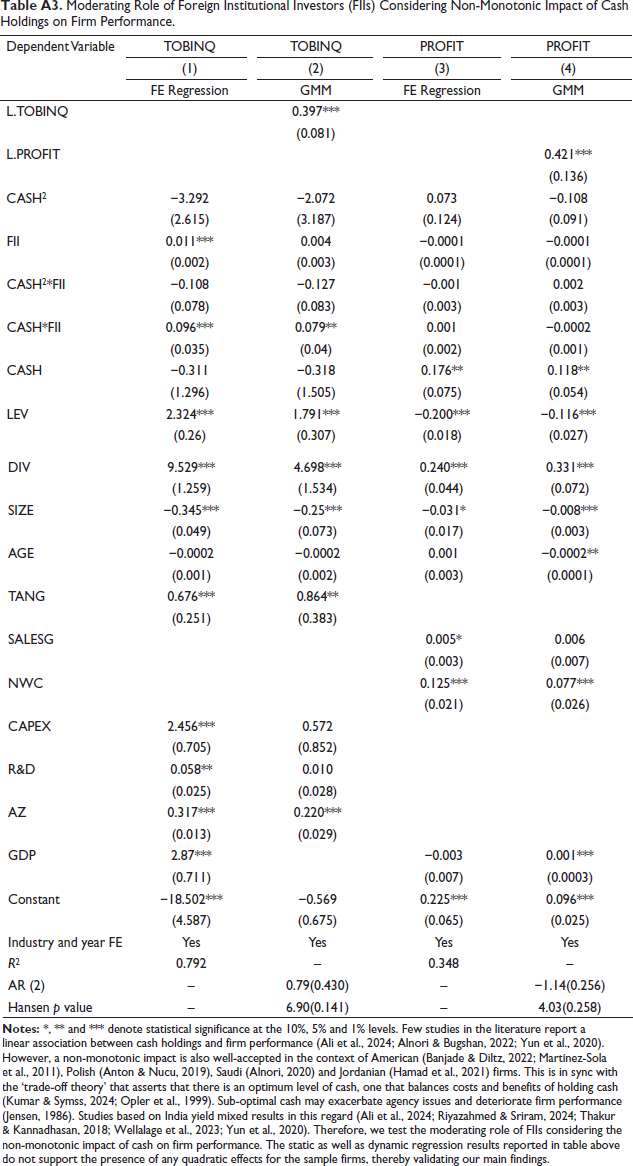

It is reported that FIIs are attracted to firms that have favourable firm performance or are larger in size (Venkatesh et al., 2021) or operate in a better macroeconomic environment (He et al., 2021). This can cause issues of reverse causality and/or simultaneity. However, literature has largely overlooked this aspect (Ilyas et al., 2021; Loncan, 2020; Sah, 2020). We validate our key findings of FE regression by using a more advanced and robust econometric technique, two-step system GMM as proposed by Arellano and Bond (1991) and Blundell and Bond (2000), that controls for the plausible concerns of endogeneity in the panel data. In both Panel A and Panel B (Table 4), the interaction term is highly significant, 2 validating our earlier results. We also test the quadratic effects of CASH on firm performance employing both static and dynamic regression models. The results reported in Table A3 in the Appendix, however, refute presence of any non-monotonic effects.

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Using a Dynamic Regression Model.

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Using a Dynamic Regression Model.

Other governance mechanisms also impact corporate decision-making, for example, board attributes attenuate investment inefficiencies (Yadav & Yadav, 2024). Moreover, corporate governance mechanisms function as a ‘cluster’, where one mechanism is linked to another (Singh & Singla, 2022). For instance, CEO duality is associated with improved independence of the board in Indian firms, especially when the ownership is predominantly held by family and insiders (Bansal & Thenmozhi, 2021). Likewise, institutional ownership acts as an effective channel that enhances the efficiency of the board in mitigating agency conflicts (Kapoor & Goel, 2025). In view of the same, we re-estimate the GMM results by incorporating necessary corporate governance measures, including board size, independent directors and proportion of ownership held by local institutions. In both panels, columns (3) and (4) report that the interaction coefficients remain unchanged, both quantitatively and qualitatively. Board measures (BSIZE and INDEP) do not have any significant impact, while DIIs have a positive (negative) association with market (accounting) performance.

Agency Costs

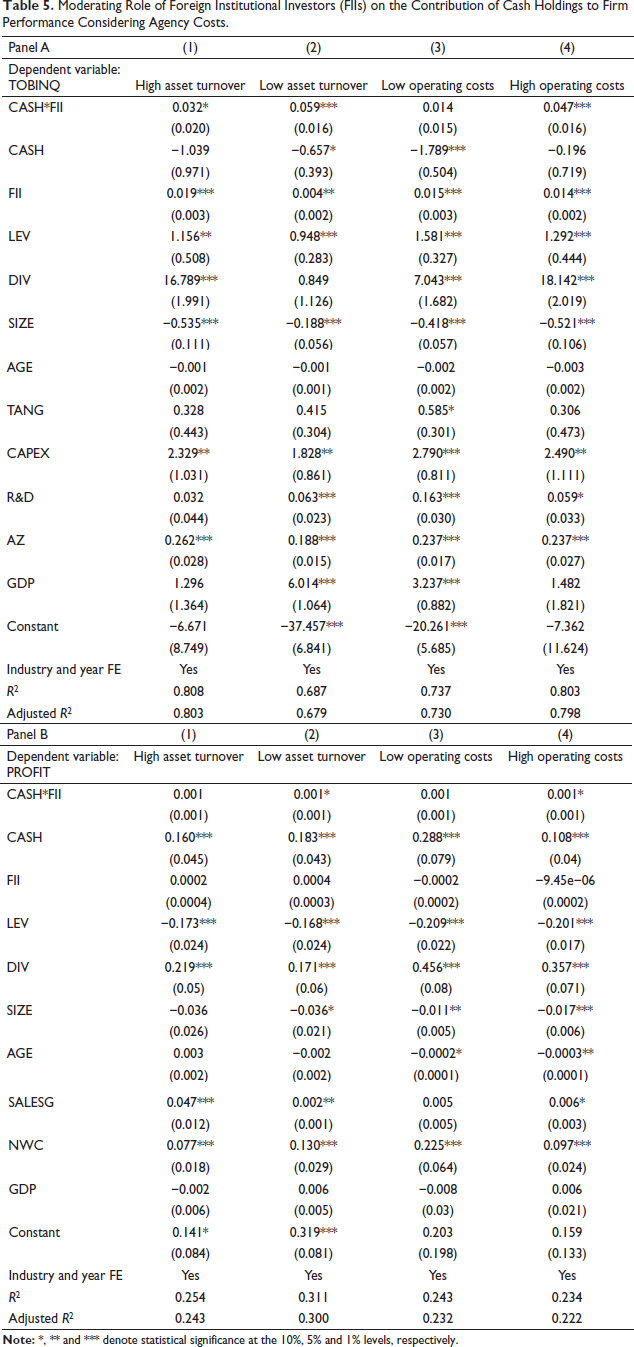

The confounding relationship between foreign ownership, cash holding and firm performance is pinned deeply to the agency theory of Jensen (1986). Agency theory argues that the incongruency of interests between managers (agents) and shareholders (principals) leads to wastage of cash resources in negative net present value avenues, giving birth to agency costs. For capturing agency costs, the study employs two key measures, including asset utilization ratio and operating expenses to sales (Purkayastha et al., 2022).

When governance is weak, entrenched managers make poor investment decisions that deteriorate asset turnover, leading to a loss in revenues. Thence, asset utilization or turnover ratio (AUR), calculated as total sales to total assets, is an important indicator of agency costs in a firm (Ang et al., 2000; Mendiratta et al., 2023). Low AUR indicates managers’ laxity in efficiently deploying firms’ assets and thus, higher agency costs (Florackis & Ozkan, 2007). The proxy has been used in previous studies (Jelinek & Stuerke, 2009; Singh & Davidson, 2003; Tayeh et al., 2023). We rank firms based on the median value of AUR (0.835), where values below and equal to the median represent high agency costs and values above the median represent lower agency costs.

Likewise, operating expenses represent the discretionary expenditures incurred to produce revenues. Agency issues are closely correlated with the operating expenses-to-sales ratio (OPEX) (Chaudhary, 2021). An elevated value signifies a substantial degree of agency expenses (Ang et al., 2000; Hoang et al., 2019; Sdiq & Abdullah, 2022). Firms with high OPEX signify greater discretionary spending and thus, higher agency issues. The sample is divided based on the median value, which stands at 0.616, and the results are reported in Table 5.

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Considering Agency Costs.

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Considering Agency Costs.

FIIs significantly benefit from the contribution of cash to business performance in firms with high agency issues. While the impact is negligible in firms with low agency costs. The monitoring role of FIIs has real benefits for firms facing high agency concerns. Firms operating in emerging markets like India, with weak external shareholder protection and dynamic regulatory environments, are often associated with high information asymmetries and agency costs (Bahlous-Boldi, 2021; Tripathi et al., 2024) as managers possess a more complex array of information than other stakeholders (Dahiya et al., 2023). Indian firms with closely held ownership exacerbate these issues (Chaudhary, 2021). However, FIIs can function as a strong governance mechanism to improve investment efficiencies and attenuate agency concerns in such firms (Kim et al., 2016; Mian & Mian, 2023).

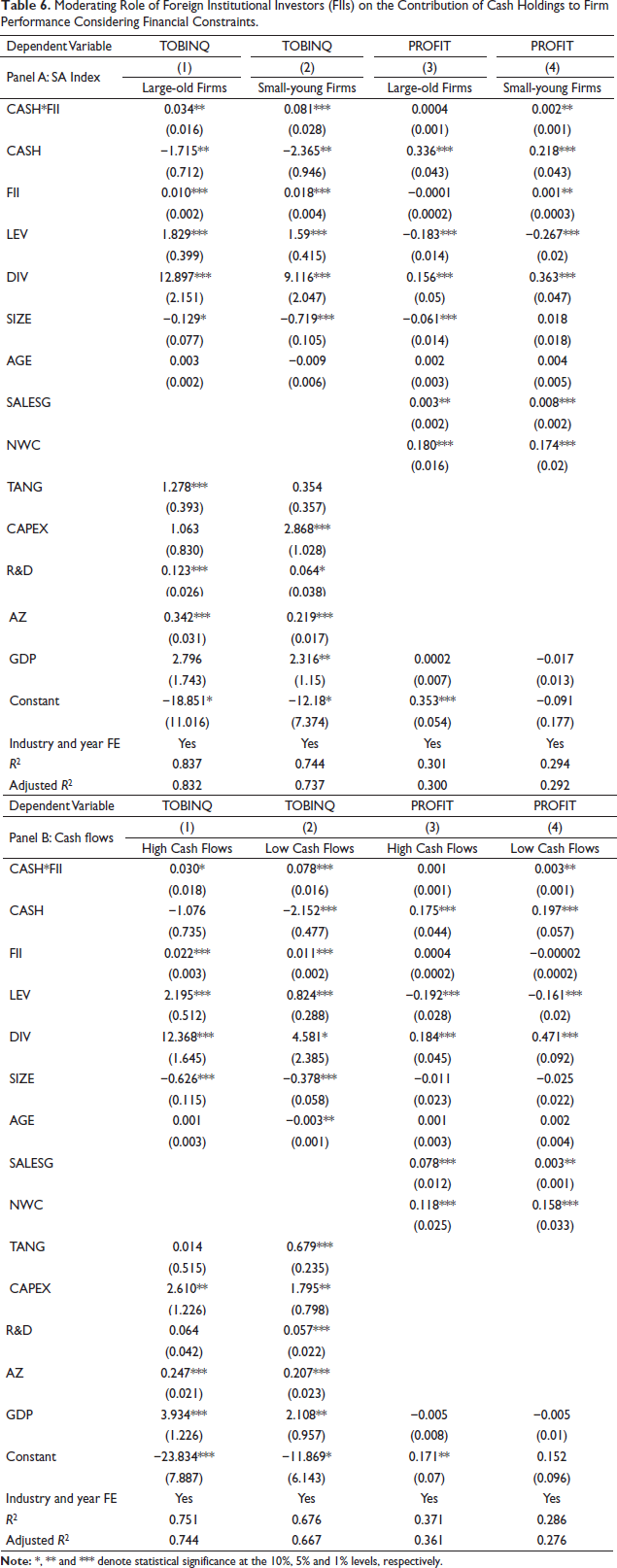

One of the key reasons why firms carry cash is to grab viable investment opportunities, especially when external funding dries up (Ferrando et al., 2016; Marchica & Mura, 2010). Unlike developed economies, emerging markets are saddled with financial constraints as the markets are underdeveloped, and the institutional environment is still embryonic (Khurana et al., 2006). The study, therefore, examines how financial constraints shape the influence of FIIs in cash management and utilization in this regard. We deploy two key measures:

Size-age index (SA): Firm size and age are key determinants of financial constraint, where relatively smaller and younger firms are prone to higher constraints than their peers (Chang et al., 2018; Kurt, 2017). Building on the work of Kaplan and Zingales (1997), Hadlock and Pierce (2010) curated the popular ‘size-age index’, and the same has been deployed in this regard. Lower (higher) values are associated with more (less) financial constraints. The firms are divided based on the median value of SA (−4.053), where firms with above the median value represent low financial constraints. Cash flows (CF): Fazzari et al.’s (1988) seminal study argues that cash flow indicates a company’s financial constraint since capital market imperfections make internal finance cheaper than external finance. Cash flow refers to the funds generated from a company’s core business operations within a specific accounting period. Firms with internally generated funds, being unconstrained, can support their investments easily.

FIIs have highly positive and significant moderation effects for financially constrained firms across both panels (Table 6), while the impact is comparatively weaker for unconstrained firms. This has notable lessons for firms operating in emerging and transitioning economies, facing a paucity of funds. These firms can attract foreign institutions to enhance investment efficiencies and, consequently, firm performance.

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Considering Financial Constraints.

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Considering Financial Constraints.

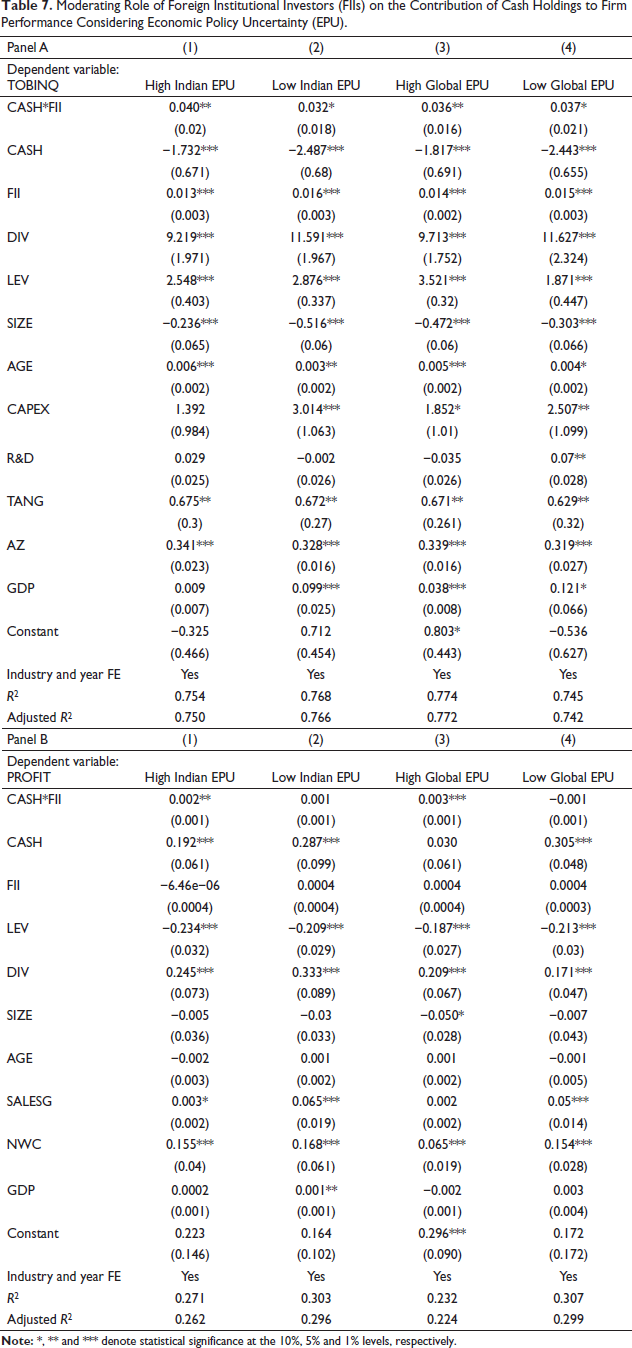

Employing Baker et al. (2016) and Davis (2016) Economic Policy Uncertainty (EPU) index, we divide the sample into high and low EPU based on median values of Indian and global EPUs. The findings in Table 7 (Panels A and B) depict that the monitoring role of FIIs is significant even under uncertainty. Investors appreciate the value of cash in well-governed firms during crisis periods (Chang et al., 2016). We find compelling evidence that FIIs are not ‘fair-weather friends’ and are superior monitors during uncertainty (Venkatesh et al., 2021).

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Considering Economic Policy Uncertainty (EPU).

Moderating Role of Foreign Institutional Investors (FIIs) on the Contribution of Cash Holdings to Firm Performance Considering Economic Policy Uncertainty (EPU).

Making a headway from the conventional corporate governance mechanisms like board, audit, and so on, we focus our attention on the governance role of FIIs in the context of an important emerging economy, India. Corporate governance is an important dimension of modern firms, and literature is continuously growing in a quest to unravel innovative governance mechanisms that can monitor entrenched managers. FIIs have been increasingly recognized as an effective monitoring mechanism in this context. Their practical and independent approach, as well as ‘foreignness’ plays a key role. Building upon the direct relationships explored in past studies, we link investment decisions (cash holdings), governance (FIIs) and shareholders’ wealth in a comprehensive set of hypotheses considering EPU, agency costs and financial constraints. In a rare effort, both market (Tobin’s Q) and accounting (profitability) performance have been examined. The results evince that FIIs strengthen the contribution of cash holdings to firm performance in leading Indian enterprises; besides, the benefits accruing increase with the rise in ownership. Put differently, it can be said that investors appreciate the value of cash held in the presence of good governance. The results remain robust even after controlling for board and other ownership factors. Further, the benefits of FII monitoring are far greater for firms facing high agency costs, financial constraints and uncertainty, a peculiar feature of modern entities.

Managerial Implications

In a nutshell, the influx of FIIs in Indian Inc. brings in good news for investors and stakeholders looking to maximize returns, and governments as it advances economic development through efficient utilization of assets. The policymakers should incentivize FII inflows to take advantage of their fine monitoring and attenuate concerns of agency issues, financing and policy uncertainty. Future studies can extend this analysis to other emerging markets to have more generalized findings, and explore interactive effects considering promoter ownership, CEO attributes, and so on, which would enrich understanding of governance mechanisms beyond traditional measures, especially during mounting policy uncertainties.

Footnotes

Acknowledgements

The authors would like to thank the anonymous referees and the editor of GBR for their constructive comments that helped to improve the article substantially. The authors are grateful to have the love, support and motivation of our family members throughout the journey of this article, without which this would not have been possible.

Authors’ Contribution

Aastha Mittal: Conceptualization, formal analysis, data curation, methodology, writing—original draft, writing—review and editing. Shveta Singh: Supervision, validation, writing—review and editing.

Data Availability

The authors do not have permission to share the data.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work is supported by the Senior Research Fellowship from the University Grants Commission (UGC), India, as a part of the PhD programme, received by Aastha Mittal. However, UGC was not involved in study design; in the collection, analysis and interpretation of data; in the writing of the article; and in the decision to submit the same for publication.

Notes

Appendix A

| Dependent Variable | TOBINQ | TOBINQ | PROFIT | PROFIT |

| (1) | (2) | (3) | (4) | |

| FE Regression | GMM | FE Regression | GMM | |

| L.TOBINQ | 0.397*** | |||

| (0.081) | ||||

| L.PROFIT | 0.421*** | |||

| (0.136) | ||||

| CASH 2 | −3.292 | −2.072 | 0.073 | −0.108 |

| (2.615) | (3.187) | (0.124) | (0.091) | |

| FII | 0.011*** | 0.004 | −0.0001 | −0.0001 |

| (0.002) | (0.003) | (0.0001) | (0.0001) | |

| CASH 2 *FII | −0.108 | −0.127 | −0.001 | 0.002 |

| (0.078) | (0.083) | (0.003) | (0.003) | |

| CASH*FII | 0.096*** | 0.079** | 0.001 | −0.0002 |

| (0.035) | (0.04) | (0.002) | (0.001) | |

| CASH | −0.311 | −0.318 | 0.176** | 0.118** |

| (1.296) | (1.505) | (0.075) | (0.054) | |

| LEV | 2.324*** | 1.791*** | −0.200*** | −0.116*** |

| (0.26) | (0.307) | (0.018) | (0.027) | |

| DIV | 9.529*** | 4.698*** | 0.240*** | 0.331*** |

| (1.259) | (1.534) | (0.044) | (0.072) | |

| SIZE | −0.345*** | −0.25*** | −0.031* | −0.008*** |

| (0.049) | (0.073) | (0.017) | (0.003) | |

| AGE | −0.0002 | −0.0002 | 0.001 | −0.0002** |

| (0.001) | (0.002) | (0.003) | (0.0001) | |

| TANG | 0.676*** | 0.864** | ||

| (0.251) | (0.383) | |||

| SALESG | 0.005* | 0.006 | ||

| (0.003) | (0.007) | |||

| NWC | 0.125*** | 0.077*** | ||

| (0.021) | (0.026) | |||

| CAPEX | 2.456*** | 0.572 | ||

| (0.705) | (0.852) | |||

| R&D | 0.058** | 0.010 | ||

| (0.025) | (0.028) | |||

| AZ | 0.317*** | 0.220*** | ||

| (0.013) | (0.029) | |||

| GDP | 2.87*** | −0.003 | 0.001*** | |

| (0.711) | (0.007) | (0.0003) | ||

| Constant | −18.502*** | −0.569 | 0.225*** | 0.096*** |

| (4.587) | (0.675) | (0.065) | (0.025) | |

| Industry and year FE | Yes | Yes | Yes | Yes |

| R 2 | 0.792 | – | 0.348 | – |

| AR (2) | – | 0.79(0.430) | – | −1.14(0.256) |

| Hansen p value | – | 6.90(0.141) | – | 4.03(0.258) |

Notes: *, ** and *** denote statistical significance at the 10%, 5% and 1% levels. Few studies in the literature report a linear association between cash holdings and firm performance (Ali et al., 2024; Alnori & Bugshan, 2022; Yun et al., 2020). However, a non-monotonic impact is also well-accepted in the context of American (Banjade & Diltz, 2022; Martínez-Sola et al., 2011), Polish (Anton & Nucu, 2019), Saudi (Alnori, 2020) and Jordanian (Hamad et al., 2021) firms. This is in sync with the ‘trade-off theory’ that asserts that there is an optimum level of cash, one that balances costs and benefits of holding cash (Kumar & Symss, 2024; Opler et al., 1999). Sub-optimal cash may exacerbate agency issues and deteriorate firm performance (Jensen, 1986). Studies based on India yield mixed results in this regard (Ali et al., 2024; Riyazahmed & Sriram, 2024; Thakur & Kannadhasan, 2018; Wellalage et al., 2023; Yun et al., 2020). Therefore, we test the moderating role of FIIs considering the non-monotonic impact of cash on firm performance. The static as well as dynamic regression results reported in table above do not support the presence of any quadratic effects for the sample firms, thereby validating our main findings.