Abstract

The board-level sustainability committee (SC) serves as a pivotal mechanism for enhancing the quality and transparency of environmental, social and governance reporting (ESGR). However, the existing literature offers limited insight into how specific attributes of SC play a role in influencing ESGR quality. This study aims to bridge this gap by empirically examining the relationship between specific SC attributes and ESGR quality among the publicly listed companies in the Association of Southeast Asian Nations (ASEAN)-5. The study’s findings were based on 896 firm-year observations from the non-financial listed firms in ASEAN-5, covering from year 2020 to 2022. Employing a panel-corrected standard errors regression analysis, the results suggest that SC independence acts as a key driver in enhancing the ESGR quality. Conversely, SC gender diversity is found to have a negative effect on ESGR quality. Moreover, we find no statistical evidence that SC size, educational level and expertise have a significant effect on ESGR quality. These findings offer fresh insights into how SC attributes influence ESGR quality, particularly in the ASEAN context. It also provides practical guidance for regulators by emphasizing the need to embed committee independence when formalizing such committees within board governance frameworks.

Keywords

Introduction

Over the years, environmental, social and governance reporting (ESGR) has grown rapidly and become increasingly prominent on a global scale. As of year 2022, nearly 80% of the world’s largest companies are disclosing their sustainability information, a notable growth since its inception in the early 90s (KPMG, 2022). Such widespread adoption of ESGR also aligns with the United Nations Sustainable Development Goals (SDGs) 12, specifically target 12.6, which encourages companies to embrace sustainable practices and incorporate sustainability information into their regular reporting cycles. The growing emphasis on ESGR highlights how companies are responding to stakeholder expectations by embracing transparency and accountability as crucial components of their commitment to sustainable development (Seow, 2025).

However, a survey conducted by PricewaterhouseCoopers in 2023 revealed that 94% of investors believe that corporate reporting includes some degree of greenwashing (PwC, 2023b). Likewise, a survey conducted by Ernst & Young in 2022 found that 76% of investors perceive companies to be highly concerned about the selective disclosure of ESG information, commonly known as ‘cherry-picking’ (EY, 2022). For example, Association of Southeast Asian Nations (ASEAN) companies were found to excel in disclosing fundamental aspects of ESGR but fell short in providing sufficient justification for their disclosure, such as the selection of material factors and the process of identifying stakeholders (Loh & Singh, 2020).

Consequently, investor confidence in ESGR has been undermined, leading to scepticism towards certain ESG aspects reported by the companies (EY, 2022). Ironically, it has been discovered that not all companies possess full confidence in the information they report to stakeholders through their ESGR (EY, 2022; Workiva, 2022). This could be attributed to the companies’ failure in embracing the benefits of ESGR and merely treating it as a compliance burden rather than an opportunity. Thus, they often approach it as a mere box-ticking exercise (CFA Institute, 2019; PwC, 2023a).

Previous research has consistently demonstrated that a robust corporate governance (CG) mechanism can improve the quality of ESGR (Cucari et al., 2018; Nuhu & Alam, 2024). Specifically, the establishment of a dedicated board committee, known as a sustainability committee (SC), has been identified as a crucial sustainability governance mechanism that facilitates the alignment and adaptation of ESGR to the firm’s specific cultural context (Hassanein et al., 2024; Tahat & Hassanein, 2024). Moreover, a specialized SC enhances this role by effectively navigating cultural complexities and thereby strengthening reporting credibility while reducing the risk of greenwashing (Hassanein et al., 2024; Kateb & Youssef, 2025).

Prior studies suggest that firms with SC are more likely to improve ESGR (Alta’any et al., 2026; Gerwing et al., 2022). Nonetheless, existing research mainly measures SC using a binary indicator (Chairina & Tjahjadi, 2023; Elmaghrabi et al., 2025; Kateb & Youssef, 2025), thus providing a limited understanding of how heterogeneous SC attributes influence ESGR quality. To bridge this gap, we extend the literature by unpacking how the heterogeneous attributes of SC (Velte & Stawinoga, 2020) can exert influence on the quality of ESGR through the lens of resource dependency theory (RDT). Unlike previous studies that focus on ESG performance (Abdullah et al., 2024; Elmaghrabi, 2021; Jarboui et al., 2023), we assess ESGR quality through a structured checklist based on the Global Reporting Initiative (GRI) Standard 2016.

Moreover, ASEAN’s status as the fifth-largest economy in the world (The ASEAN Secretariat, 2022) underscores the importance of businesses in the region in driving impactful ESG activities and reporting. However, existing research on SC-ESG has largely concentrated on developed (Abdullah et al., 2024; Elmaghrabi, 2021) or developing countries (Jarboui et al., 2023), with the ASEAN region remaining notably under-researched. The regional focus on ASEAN-5, therefore, adds practical relevance as sustainability governance in these countries remains largely voluntary. The findings are valuable not only for academic advancement but also for informing regional policymakers and investors seeking to strengthen the transparency of ESGR through committee-level governance.

Specifically, our study extends the limited research on the understanding of SC attributes and their impact on ESGR quality. While prior studies have largely focused on the presence of SC, this study extends the analysis by examining the impact of heterogeneous SC attributes in influencing ESGR quality. To our best knowledge, prior research on SC attributes primarily focuses on ESG performance (Elmaghrabi, 2021; Jarboui et al., 2023). Accordingly, our findings contribute to the literature by being among the earliest that assess how heterogeneous SC attributes shape ESGR quality. Furthermore, studies related to SC and ESG-related outcomes have largely been confined to individual country settings. By examining ASEAN-5 as a regional context, our study offers a broader perspective that enriches the understanding of how SC attributes play a role in elevating ESGR quality. Moreover, our findings extend RDT by showing that SC attributes function as heterogeneous governance resources in shaping ESGR quality in ASEAN-5 firms. Overall, our findings suggest that a higher representation of independent directors (IDs) on the SC can lead to improved ESGR quality. The SC gender diversity, however, has a negative impact on ESGR quality.

This article consists of three main sections: Section 2 presents the theoretical background of the study, reviews relevant literature, and develops the hypotheses. Section 3 outlines the research methodology, and Section 4 delivers the empirical results and discussion. The final section discusses the study’s conclusions and implications.

Literature Review

We utilize RDT to examine the relationship between SC attributes and ESGR. RDT posits that a firm’s behaviour and operations are influenced by its reliance on external resources (Alodat et al., 2023). To ensure their continued survival, firms must secure access to and effectively utilize indispensable resources from the external environment. In this context, SC serves as a valuable resource, offering expert guidance to management in meeting stakeholders’ expectations and facilitating the development of sustainability strategies (Al-Shaer & Zaman, 2018). Moreover, the directors’ relevant experience and expertise, particularly sustainability-related, are crucial factors in enabling the firm to secure better external resources (Hillman & Dalziel, 2003).

Sustainability Committee Composition and Environmental, Social and Governance Reporting

Size

Based on RDT, the larger the committee size, the more effective the committee is, as it comprises directors from diverse backgrounds, expertise, experience and knowledge. Thus, it allows SC to obtain a more discerning judgement on ESG challenges, such as ways to improve ESGR quality (Minciullo et al., 2022).

Nevertheless, a larger committee size may not necessarily be beneficial, as it could also create potential problems. For example, it could lead to coordination and communication problems (Kilincarslan et al., 2020; Pasko et al., 2021), as a larger committee size takes more time to reach a consensus. Eventually, this leads to ineffectiveness in decision-making (Al-Hajaya et al., 2025; Pasko et al., 2021). Moreover, there is a tendency for the occurrence of free rider issues (Pasko et al., 2021). In a larger committee size, the existence of the directors in the committee can be merely symbolic rather than operational. A smaller size of the committee, therefore, can overcome the problem as each director is required to exert more effort in completing the tasks and makes them less dependent on the contribution of other directors for decision-making (Eberhardt-Toth, 2017).

To date, there is extensive research that has explored the relationship between board of directors (BOD) size and ESGR (Bhatia & Marwaha, 2022; Kateb & Youssef, 2025; Kumari et al., 2022), with little focus on the impact of SC size and ESGR. Specifically, it was found that literature on SC size tends to focus on corporate social responsibility (CSR)/sustainability performance (Elmaghrabi, 2021; Jarboui et al., 2023; Minciullo et al., 2022) and not on the reporting perspective. The findings in this respect are nevertheless mixed. Jarboui et al. (2023) and López-Arceiz et al. (2022) indicate a positive relationship, in contrast to Eberhardt-Toth (2017), who found a negative relationship, while Abdullah et al. (2024), Minciullo et al. (2022) and Elmaghrabi (2021) documented an insignificant relationship. The variance in these findings could be due to the different measurements used by these studies as a proxy for CSR/sustainability.

Considering these divergent findings, we developed the following non-directional hypothesis:

H1: The level of SC size has a significant impact on ESGR quality.

Independence

The insubstantial relationship of IDs with the firm allows them to discharge their oversight role more effectively, as they are subject to less pressure from management and shareholders compared to internal directors (Kılıç et al., 2021). Being impartial in nature, ID will likely enhance the company’s ESG-related issues, instead of focusing solely on the economic concerns. Thus, it enables the ‘voices’ of the different stakeholder groups are be heard rather than just the shareholders’ (Minciullo et al., 2022). Moreover, RDT postulates that ID will leverage its various upbringings, experiences and network ties to facilitate the adoption of effective ESG practices.

Empirically, the literature on ID and ESGR is focusing more towards the BOD perspective, and little has been done in terms of SC. Yet, there is an inconclusive finding with respect towards the board independence and ESGR (Arayssi et al., 2020; Chairina & Tjahjadi, 2023; Erin et al., 2022; Fahad & Rahman, 2020). The divergence of the findings can be explained by the various measurements that are used to proxy ESGR, such as some studies utilize the content analysis methods, while others depend on the data extracted from third-party databases (Chairina & Tjahjadi, 2023; Erin et al., 2022; Fahad & Rahman, 2020).

In the limited scholarly literature on SC’s independence, Elmaghrabi (2021), Eberhardt-Toth (2017) and Jarboui et al. (2023) findings show that a higher proportion of ID in SC enhances CSR performance, and Li et al. (2023)’s research extends this by showing benefits to environmental performance. Nevertheless, Abdullah et al. (2024) found no association between SC independence and ESG performance.

Moreover, Nicolò et al. (2026) reported a negative association between SC independence and SDG disclosure, suggesting that formal independence does not necessarily lead to effective oversight. Despite their formal independence, IDs may still be influenced by personal connections, social affiliations or other external factors that could affect their judgement and decision-making (Nicolò et al., 2026; Raimo et al., 2022). Thus, these factors may limit their ability to contribute effectively to elevating the transparency in SDG-related disclosures.

To date, there is a dearth of studies exploring the SC’s independence in ESGR, leading to a scarcity of knowledge in this domain of study. Given the mixed findings above, a non-directional hypothesis is proposed:

H2: The level of SC independence has a significant impact on ESGR quality.

Sustainability Committee Diversity and Environmental, Social and Governance Reporting

Educational Level

A director with a higher education level is portrayed as possessing higher knowledge, skills and competency, which can contribute to the firm’s success (Beji et al., 2021) and support the notion of RDT. This is because these directors are believed to be equipped with the bird’s-eye-view ability and to have a greater breadth of insights (Post et al., 2011).

Ratmono et al. (2021) put forward that directors with higher education levels have a greater awareness of the importance of sustainable development principles and the implementation of ESG practices, particularly if they are specialized in the economy and business fields. Whereas Garcia-Blandon et al. (2019) documented that chief executive officers (CEOs) with engineering degrees show higher ESG performance. In contrast, CEOs with MBAs were found to have no association with ESG performance.

At present, the literature on CG bodies’ education levels has yielded mixed results. For instance, Issa et al. (2022) and Ramadhan et al. (2023) demonstrate that directors with higher education levels can positively influence ESGR, partly because these directors can use their cognitive ability to align with the key interests and demands of various stakeholder groups. Nonetheless, other studies show that the directors’ educational level has no effect on CSR disclosure (Khan et al., 2019; Maswadi & Amran, 2023) and ESG performance (Abdullah et al., 2024). This suggests that companies may appoint highly educated directors mainly to satisfy legitimacy pressures that can lead to symbolic rather than substantive involvement in ESG-related matters (Abdullah et al., 2024). Even when educational diversity exists among directors, differences in cognitive background can create conflict and coordination challenges (Abdullah et al., 2024), thereby affecting their effectiveness in enhancing ESG-related outcomes.

Despite growing interest in SC, research examining the relationship between directors’ education levels and ESGR remains limited. Additionally, there is a lack of studies that specifically examine emerging countries such as ASEAN-5, despite the fact that education level (i.e., knowledge) has been specifically highlighted by the CG code in these countries as one of the crucial attributes to be included in appointing directors to the board/committee. Therefore, we propose the following non-directional hypothesis:

H3: The level of SC education has a significant impact on ESGR quality.

Expertise

Sustainability-related expertise directors play a pivotal role in shaping ESGR outcomes (Elmaghrabi, 2021; Erin et al., 2022), as they can offer effective guidance on managing the increased challenges of sustainability-related issues (Homroy & Slechten, 2019).

From the RDT perspective, the inclusion of sustainability expertise in SCs will lead to a stricter focus on ESG-related monitoring activities (Velte & Stawinoga, 2020), as they possess valuable experience in ESG practices, thus enabling the ESGR quality to be elevated. Additionally, SC expertise could also minimize the risk of greenwashing behaviour and boilerplate practice in the ESGR (Velte & Stawinoga, 2020).

Empirical studies suggest that directors with sustainability expertise can contribute to lower greenhouse gas emissions (Homroy & Slechten, 2019) and higher environmental (Asad et al., 2025) and ESG performance (Collevecchio et al., 2025). Their extensive experience in sustainability matters equips them to provide valuable guidance that helps the company better understand and respond to ESG challenges. Their presence also contributes to the integration of ESG considerations into organizational decision-making (Collevecchio et al., 2025), which collectively contributes to the improvements in the company’s ESG performance.

Existing research on SC expertise focuses on its impact on CSR and sustainability performance (Elmaghrabi, 2021; Jarboui et al., 2023), CSR and ESGR assurance (Rossi & Tarquinio, 2017). Specifically, Elmaghrabi (2021) revealed that ‘expertise’ is a less important attribute of SC, as it has an insignificant impact on CSR performance, CSR strategy and CSR controversies. However, by using a different measurement in evaluating SC expertise, other scholars show that SC expertise may enhance sustainability performance (Jarboui et al., 2023), improve transparency in environmental reporting (Peters & Romi, 2014), and be better associated with implementing sustainability assurance (Rossi & Tarquinio, 2017).

Nonetheless, limited attention has been devoted to the association between SC expertise and ESGR (Peters & Romi, 2014), leaving the area underexplored. Hence, we propose the following non-directional hypothesis:

H4: The level of SC expertise has a significant impact on ESGR quality.

Gender Diversity

Within the CG studies, scholars generally argue that gender-diverse boards may enhance the sustainability report information disclosures (Benameur et al., 2024; Injeni et al., 2022; Tahat & Hassanein, 2024). This is because women directors possess more communal attributes compared to their male counterparts and thus, they are more concerned towards the entire society’s interest and welfare rather than solely focusing on the investors’ interests (Bhatia & Marwaha, 2022; Helfaya et al., 2023).

From the perspective of RDT, the presence of women directors enriches the board with a heterogeneous set of skills, professional experiences, competencies, knowledge, leadership styles and perspectives (Nicolò et al., 2022). This diversity can similarly benefit the SC, where diverse expertise and viewpoints contribute to more effective oversight and decision-making. These traits enable them to perform closer monitoring, provide more profound insights (Bravo & Reguera-Alvarado, 2019; Qaderi et al., 2022) and eventually elevate ESGR quality. Besides, women are found to be more diligent in scanning for and collecting information associated with environmental and social issues. Hence, they are more prone to accentuate the value of ESGR (Bravo & Reguera-Alvarado, 2019).

Nonetheless, some studies found that the presence of women directors does not necessarily help in enhancing sustainability disclosure (Cucari et al., 2018; Issa et al., 2022; Kumari et al., 2022). Besides gender, the lower level of experience or qualifications may also confine the ability of the women directors to influence ESGR quality (Cucari et al., 2018), thus leading to greater risk aversion and conservatism in their decision-making (AlJanadi, 2026). Furthermore, within the context of tokenism, the presence of women directors may not translate into substantive influence, as their involvement is often limited to symbolic gestures aimed at boosting the board’s legitimacy rather than contributing to the decision-making processes (AlJanadi, 2026).

Currently, there is a lack of studies that focus on the board committee level (Bannò et al., 2023) and ESGR, particularly on SC. For instance, Appuhami and Tashakor (2017) and Bravo and Reguera-Alvarado (2019) found that the presence of women directors on the audit committee can exert influence on the level of ESGR. Similarly, other studies documented that a higher proportion of women directors in SC can improve ESG disclosure (Khemakhem et al., 2023) and SDG disclosure (Nicolò et al., 2026). Additionally, their presence can also lead to a reduction in waste generation and an increase in waste recycling practices (Gull et al., 2024). Conversely, Abdullah et al. (2024), Elmaghrabi (2021) and Eberhardt-Toth (2017) discovered an insignificant linkage between sustainability/CSR committee gender diversity and ESG/CSR performance. Nonetheless, Elmaghrabi’s (2021) findings further reveal that the women chair of the CSR committee plays a critical role in enhancing CSR performance.

Considering the conflicting evidence on board committee gender diversity and ESG outcomes, the following non-directional hypothesis is developed:

H5: The level of SC gender diversity has a significant impact on ESGR quality.

Materials and Methods

Population and Sample Selection

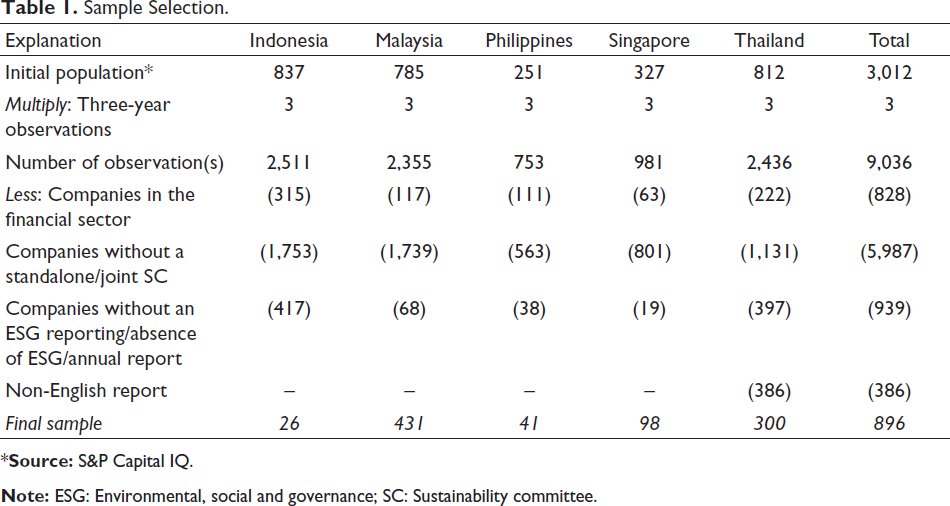

The initial population of this study covered a total of 2,736 non-financial public limited companies (PLCs) from the ASEAN-5 countries as of 31 December 2022, extracted from the S&P Capital IQ database (Table 1). ASEAN-5 was selected because it accounted for 85% of the region’s total gross domestic product (GDP) (The ASEAN Secretariat, 2022). Despite Vietnam playing a significant role in the region’s GDP, it is excluded from this research because most of the annual reports published by Vietnamese companies are not written in English. We focus on the years 2020–2022 to align with the implementation of mandatory ESGR across ASEAN-5, and exclude data from 2023 onwards as it is subject to the GRI Standards 2021, which became effective in January 2023.

Sample Selection.

Sample Selection.

We exclude finance-related companies due to their industry-specific attributes and distinct accounting implications. Furthermore, we include only PLCs that have established a standalone and/or joint SC at the board level. PLCs that did not establish the committee were eliminated. Additionally, companies with an absence of annual reports and/or non-English reports were also excluded from the analysis. Consequently, the final sample consisted of an unbalanced panel of 896 firm-year observations.

Dependent Variable

The content analysis method has been among the popular techniques that are utilized by scholars in ascertaining the quality of ESGR (Argento et al., 2019; Gerwing et al., 2022; Kumar et al., 2022), which is based on GRI, the standard that is widely used internationally (KPMG, 2022). Following previous studies, we define ESGR quality by developing a checklist based on the GRI Standards 2016 (Al-Amosh et al., 2023; Injeni et al., 2022). Since our study period falls within 2020 and 2022, it allows us to evaluate ESGR using the GRI Standard 2016, which was made effective from 1 January 2018 to 31 December 2022. A checklist encompassing 94 ESG items is developed based on the GRI Standards 2016, where 32 items are environmental-related disclosures (GRI 301-1 to GRI 308-2), 40 items are social-related disclosures (GRI 401-1 to GRI 419-2), and 22 items are governance-related disclosures (GRI 102-18 to GRI 102-39).

The 0–3 scoring system, adapted from Wiseman (1982) and Ghuslan et al. (2021), was selected for its ability to capture varying levels of disclosure depth, which aligns with the GRI-based indicators employed in this study. A score of 3 denotes disclosure of specific quantitative and/or qualitative items and/or containing monetary information; a score of 2 for companies that made specific quantitative or qualitative information; a score of 1 for companies that made specific ESG-related general disclosure; while 0 score is for companies that do not provide any specific ESG information. Finally, we computed the ESGR quality by dividing the total disclosure score by the maximum total disclosure score and expressed it in percentages (Kumar et al., 2022). The formula used is as follows:

where:

QUALI = ESGR quality; n = total disclosure score; N = maximum total disclosure score.

For consistency purposes, only one coder is involved in conducting the entire content analysis to ensure the consistency of the coding process. We have taken three approaches to ensure the coding’s reliability. First, the intra-coder reliability was ensured by developing a checklist based on the GRI Standards 2016. Second, an additional coder was invited to independently re-code a randomly selected 10% of the sample using the same 0–3 scoring system (Mackey & Gass, 2005; Neuendorf, 2002). Any inconsistencies between coders were identified and resolved through discussion, thereby ensuring consistent interpretation of the scoring system and enhancing the objectivity of the content analysis. Third, we utilize the Cronbach’s alpha test to ensure that the items coded are valid and reliable. The result shows that it is above the threshold of 0.7 and leads us to conclude that the coded items were highly consistent (Bland & Altman, 1997) and fit for further analysis.

Independent Variables

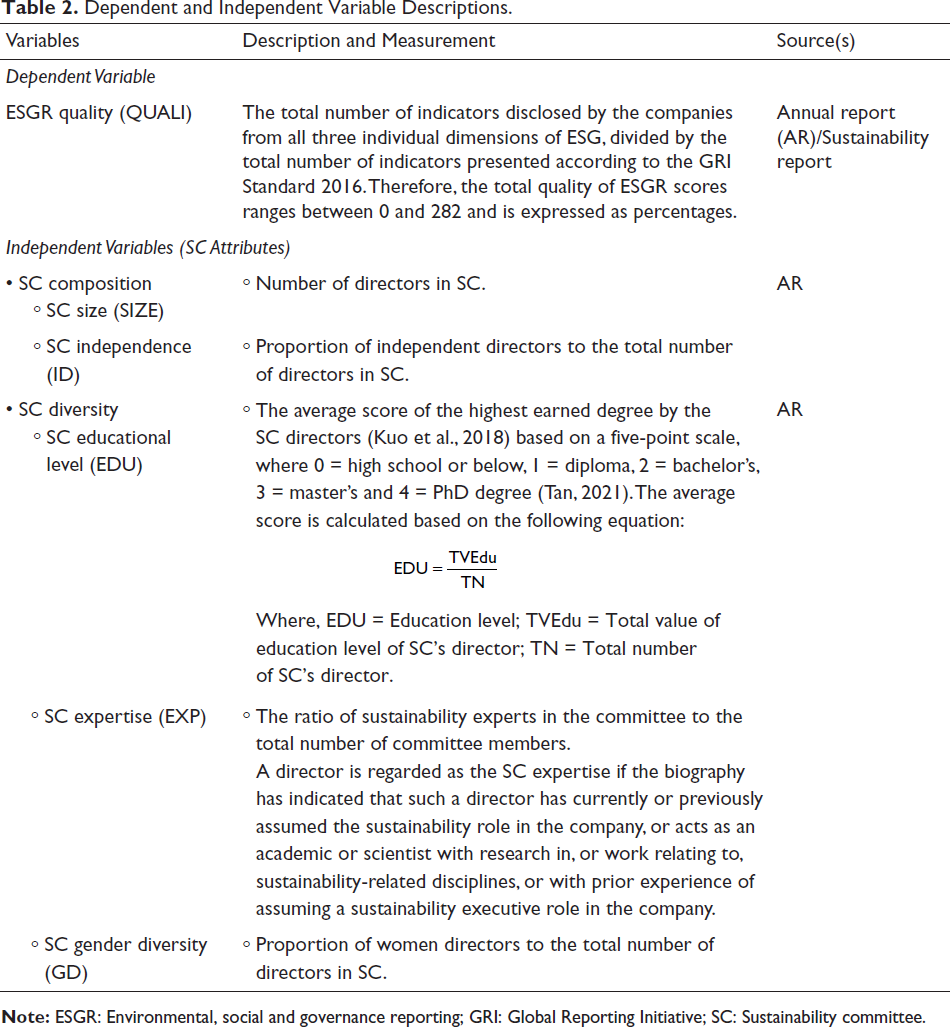

To capture the SC effectiveness on ESGR, this study has categorized the six SC attributes recommended by Velte and Stawinoga (2020) into two groups, namely the SC’s composition and SC diversity. The SC’s composition includes size and independence (Elmaghrabi, 2021; Jarboui et al., 2023) while the SC’s diversity encompasses the educational level (Tan, 2021), expertise (Jarboui et al., 2023; Li et al., 2023) and gender diversity (Eberhardt-Toth, 2017; Elmaghrabi, 2021). Table 2 presents the detailed measurement of each independent variable.

Dependent and Independent Variable Descriptions.

Dependent and Independent Variable Descriptions.

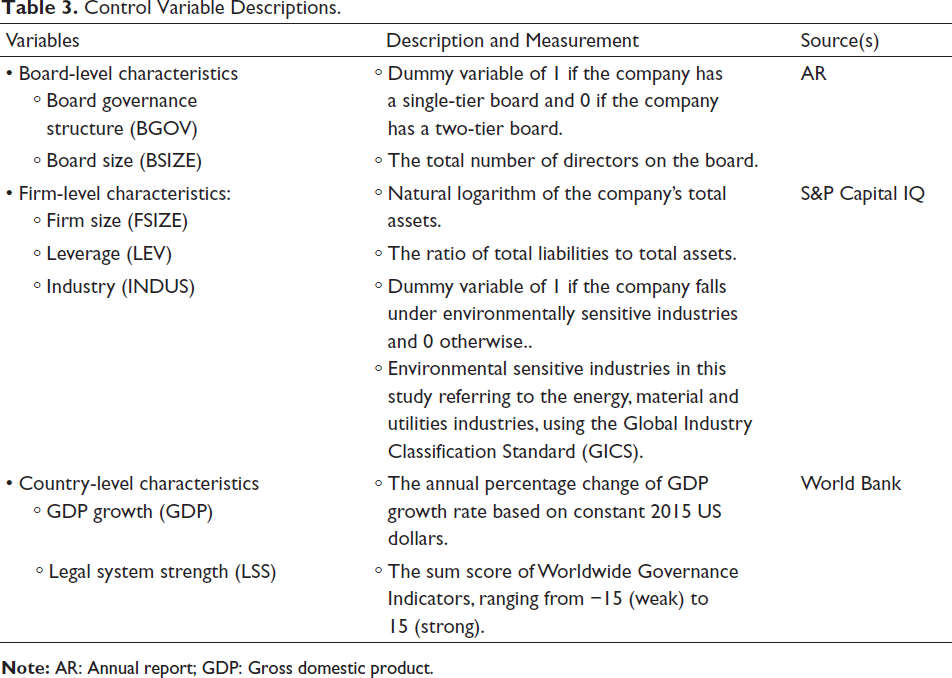

We control for three sets of variables to avoid model misspecification, namely the board-level characteristics (Jarboui et al., 2023; Pucheta-Martínez et al., 2019), the firm-level characteristics (Chaklader & Gulati, 2015; Fahad & Rahman, 2020; Jarboui et al., 2023) and the country-level characteristics (Barakat et al., 2015; Bose et al., 2024). These variables are included as prior studies have demonstrated their influence on ESGR. The measurement of each of the control variables is presented in Table 3.

Control Variable Descriptions.

Control Variable Descriptions.

We utilized the panel-corrected standard errors (PCSE) estimator as our baseline regression model, as the diagnostic test indicated that our model suffers from issues of heteroskedasticity, autocorrelation and cross-sectional dependence. Hence, PCSE is a preferred estimator in this study for two reasons: (a) it is more efficient, as it can generate robust estimates in dealing with the above issues (Beck & Katz, 1995; Hoechle, 2007), and (b) it is more suitable for studies that leverage on the short panel data, where the number of firms is greater than its time dimension (Hoechle, 2007). Additionally, firm and year fixed effects are incorporated into the research model to control for unobserved firm-specific heterogeneity and common time-specific influences, thereby reducing potential omitted variable bias in estimating the relationships among the variables.

Indeed, other panel data estimators that could be used are pooled ordinary least squares (POLS), fixed effects, random effects or generalized method of moments (GMM). However, POLS, fixed effects and random effects are not ideal regression models in our study because they fail to take into consideration the cross-sectional dependence issue (Hoechle, 2007). With the short time dimension of our data, we could not utilize GMM. Thus, PCSE is noted to be the most efficient estimator that we could use to examine the hypotheses. Accordingly, our baseline model is represented as follows:

Results and Discussions

Descriptive Analysis

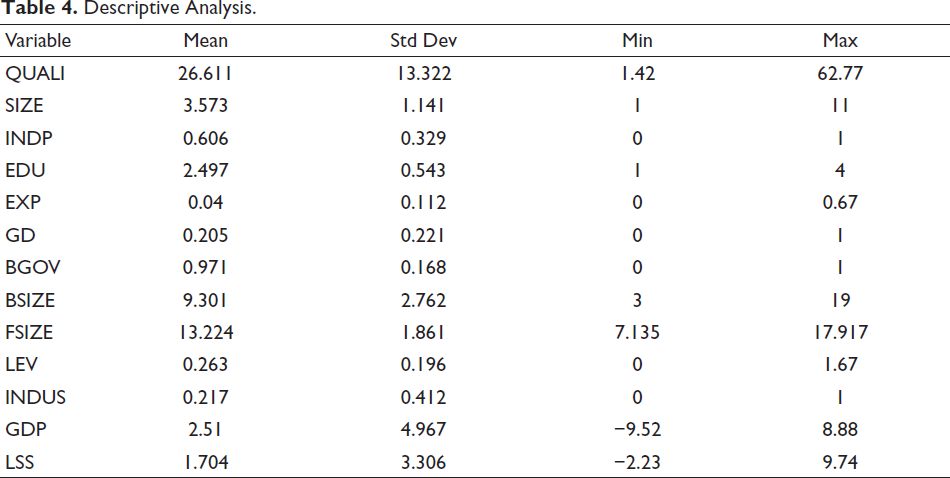

Table 4 lists the descriptive statistics for all the variables. The average value for ESGR quality is 26.61, and the standard deviation is 13.32, which indicates that the overall ESGR quality is not high among the ASEAN-5 companies. We note that some companies report the information comprehensively, while some merely report it in the simplest manner, thus contributing to the variance of the scores.

Descriptive Analysis.

Descriptive Analysis.

In terms of SC composition, it was found that, on average, SC consists of four directors, with a minimum of one and a maximum of 11 directors sitting on the committee (excluding the management-level personnel who sit on the committee). We acknowledge that it is uncommon for a company to have only a single director who sits on the board committee. However, considering that some companies are in their early stages of establishing the committee, and with limited resources in the company, hence, it is justifiable that they take a gradual approach, prioritizing key objectives and building capacity over time. SC independence has a mean of 0.61, implying that there is at least 61% ID in the SC.

For SC diversity, the results show that the average education level of the SC directors was 2.5, which suggests that most of the directors in this committee possess at least a bachelor’s degree. However, there is a lack of sustainability-related expertise and women directors in the committee, which is evident by the average value of 0.04 and 0.21, respectively. Considering their current minimal presence, it would suggest that such members have a greater influence on heightening ESGR quality if any of these attributes were identified as significant elements towards ESGR quality.

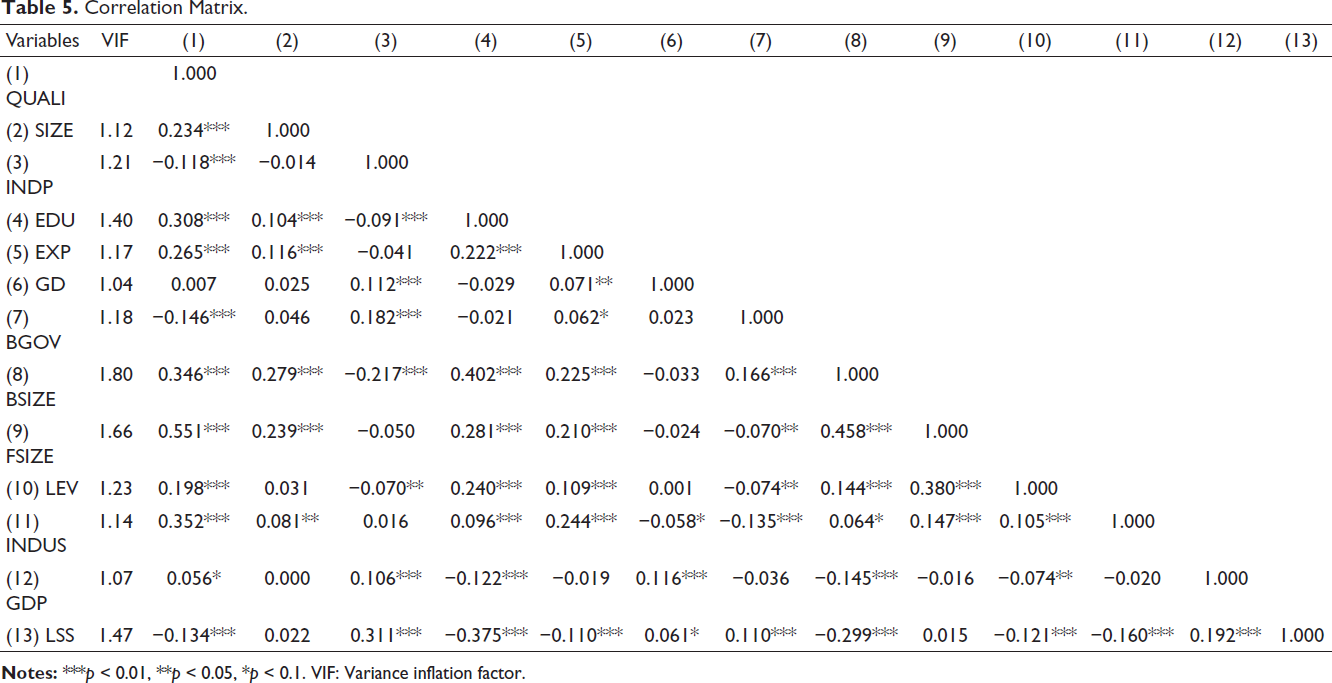

Table 5 illustrates the Pearson correlation matrix among the research variables. The highest correlation coefficient is recorded between firm size and ESGR quality. However, it does not pose any problem of multicollinearity, as it does not exceed the threshold of 0.80 (Gujarati, 2004). Additionally, the variance inflation factor (VIF) values among the variables ranged between 1.04 and 1.80, which are less than the threshold of 10 (Gujarati, 2004). Thus, we conclude that multicollinearity is not an issue in this study.

Correlation Matrix.

Correlation Matrix.

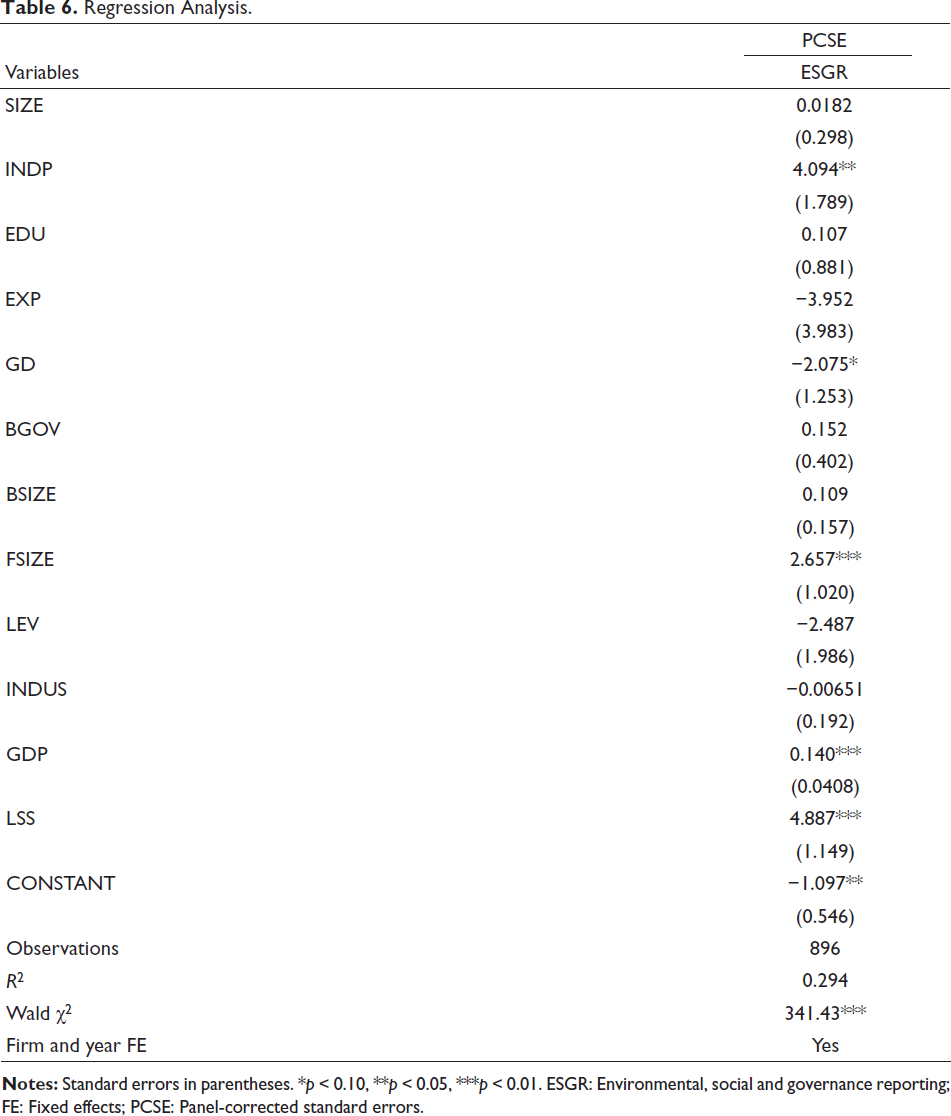

Table 6 reports the regression results. The R2 value of the PCSE regression suggests that the explanatory variables can predict and explain the dependent variable by 29.4%. The Wald chi-square of 341.43 (p < 0.01) implies that the regression model is fit and reliable for prediction, as the explanatory variable substantially contributes to the predictive power of the model.

Regression Analysis.

Regression Analysis.

Our results demonstrate a non-significant association between SC size and ESGR, implying that H1 is not supported. This finding is consistent with Abdullah et al. (2024), Minciullo et al. (2022) and Elmaghrabi (2021), who document insignificant effects of SC size on ESG performance. Nevertheless, our finding differs from Jarboui et al. (2023) and López-Arceiz et al. (2022), who identify SC size as a key factor in enhancing ESG performance. The lack of support may be due to the low proportion of sustainability expertise on the SC (Table 4), which may constrain their ability to meaningfully influence sustainability reporting despite their larger size.

SC independence is found to be positively associated with ESGR at the 5% level. Consequently, H2 is supported. This finding reinforces the theoretical premises of RDT, which posits that ID brings diverse expertise, critical oversight and external perspectives that enhance the firm’s responsiveness to stakeholder expectations (Pfeffer & Salancik, 1978), rather than treating ESGR merely as a ‘box-ticking’ practice. Unlike prior insignificant findings (Abdullah et al., 2024), our study highlights SC independence as a key driver of advocating greater ESGR quality, particularly in ASEAN-5, where regulatory pressures on ESGR are intensifying. This finding is also aligned with prior evidence (Elmaghrabi, 2021; Jarboui et al., 2023), indicating that greater ID enhances monitoring effectiveness, as ID is more likely to support stakeholder-aligned disclosures and thereby improve ESGR quality.

Unexpectedly, our findings do not show any significant association between SC educational level and ESGR among ASEAN-5 firms. Thus, H3 is not supported. This finding is aligned with Khan et al. (2019) and Maswadi and Amran (2023) but contrasting with Issa et al. (2022) and Ramadhan et al. (2023). This may be attributable to the fact that although a higher education level is expected to enhance directors’ cognitive ability and improve alignment with stakeholder expectations, its effectiveness may be constrained when educational credentials function partly as legitimacy signals rather than substantive expertise. Additionally, educational diversity may introduce cognitive heterogeneity that generates coordination challenges and weakens collective decision-making. Thus, our findings highlight the need to transcend credentialism and ensure that educated committee members are empowered to exert influence on ESG policy and reporting, especially in ASEAN-5, where ESG frameworks are still evolving.

Sustainability expert directors are considered a crucial resource for the company, as they can provide useful advice to the firm in better tackling sustainability-related issues (Homroy & Slechten, 2019). Consistent with Elmaghrabi (2021) but different from Jarboui et al. (2023) and Rossi and Tarquinio (2017), our results show that there is an insignificant relationship between SC expertise and ESGR. Hence, H4 is not supported. Nevertheless, the negative coefficient implies that the larger proportion of sustainability expertise does not necessarily lead to greater quality of ESGR. This unexpected finding may be attributed to the severe paucity of directors with sustainability expertise serving on the SC among the ASEAN-5 firms (Table 4); therefore, it restrains the effective role of this expertise in influencing ESGR. Additionally, their influence on ESGR may be limited, as the board holds the ultimate decision in ascertaining the quantity of information that ought to be disclosed in the report.

Finally, our result demonstrates that the greater proportion of SC gender diversity diminishes ESGR quality at a 10% significant level, which contrasts with prior studies that report either a positive (Khemakhem et al., 2023; Nicolò et al., 2026) or non-significant association (Abdullah et al., 2024; Eberhardt-Toth, 2017; Elmaghrabi, 2021). Thus, H5 is supported. The reasons for this finding are twofold. First, women directors possess attributes beyond gender, such as specific experience and expertise, that may affect ESGR quality (Cucari et al., 2018). Second, the findings may reflect tokenism, whereby a higher proportion of women directors exerts limited influence because their appointments are primarily symbolic, rather than empowering them to apply their expertise to enhance ESGR quality (AlJanadi, 2026; Cucari et al., 2018).

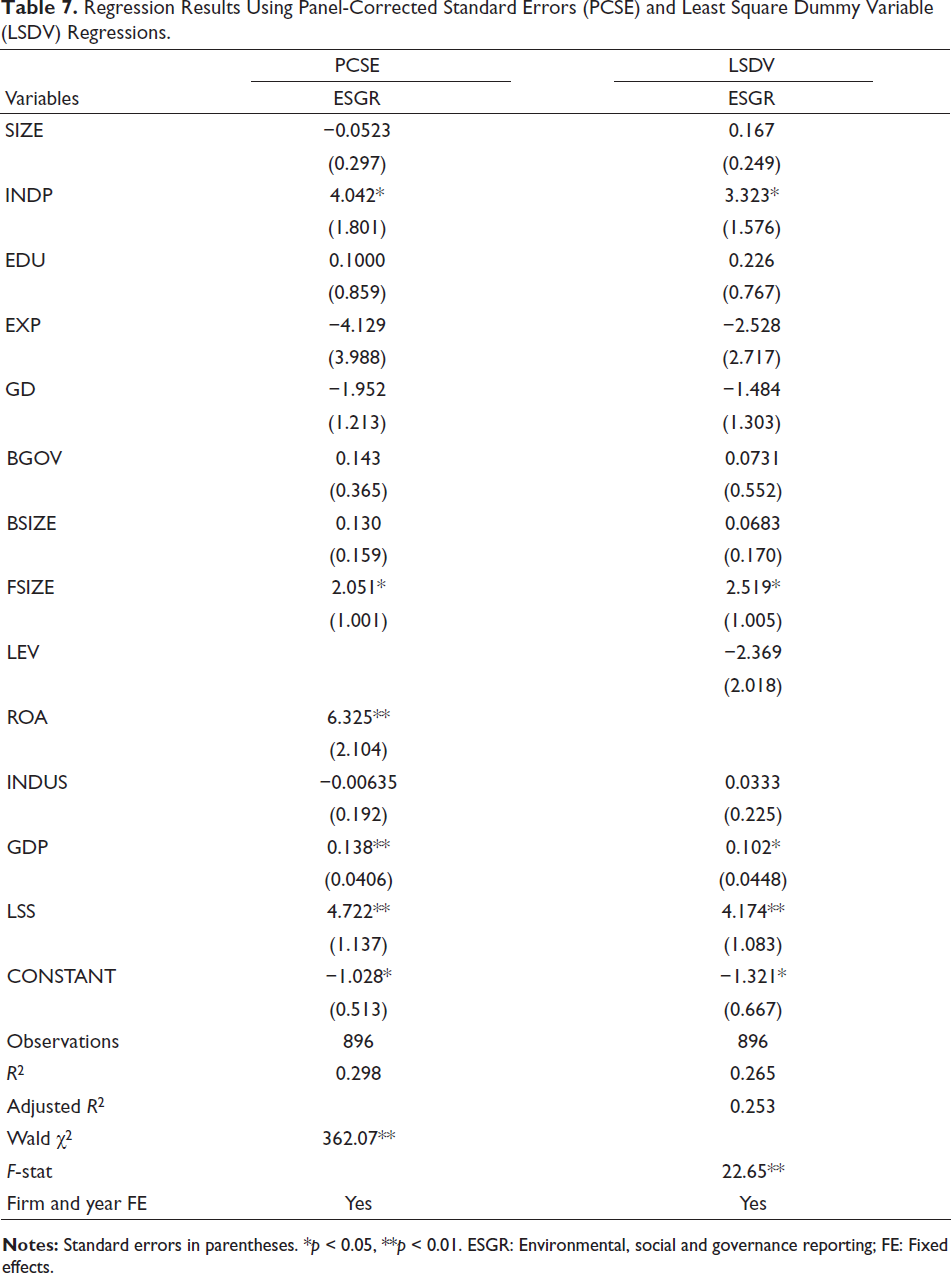

Sensitivity Test

To further validate the relationship between SC attributes and ESGR, we replace the financial indicator—leverage, with return on assets (ROA), as a sensitivity test. As reported in Table 7, the result shows a consistency with our baseline regression (Table 6), except for SC gender diversity.

Regression Results Using Panel-Corrected Standard Errors (PCSE) and Least Square Dummy Variable (LSDV) Regressions.

Regression Results Using Panel-Corrected Standard Errors (PCSE) and Least Square Dummy Variable (LSDV) Regressions.

The Hausman specification test suggests that the fixed effect regression (least square dummy variable (LSDV)) is more appropriate, given that the results are statistically significant at the 1% level. To enhance robustness, we introduce firm-specific and time-specific dummy variables to capture these unobserved effects.

The LSDV model yielded consistent results with our main findings, except for SC gender diversity (Table 7). The significance of SC gender diversity in the PCSE model but not in the LSDV model indicates that its effect on ESGR might be sensitive to the handling of the error structure. Specifically, the PCSE model adjusts for heteroskedasticity and cross-sectional dependence in the error terms, while the LSDV model does not inherently account for this problem. Thus, the lack of adjustment for error dependencies in the LSDV model could result in less reliable estimates, which can cause a reduction in the significance of the results.

Conclusion

Although previous literature has documented that the presence of SC can augment ESGR quality (Alta’any et al., 2026; Gerwing et al., 2022), limited evidence exists regarding which specific SC attributes contribute to this improvement. Building on this, our study specifically examines the impact of SC attributes on ESGR quality, particularly in the ASEAN-5. Our analysis focused on an unbalanced panel data set that consists of a sample of 896 firm-year observations over the year of 2020–2022. Our results reveal that having a greater proportion of ID on the SC is more influential on ESGR quality than the committee size, educational level and expertise. This implies that ID can effectively plays its role in pressuring management to intensify the ESGR to meet stakeholders’ expectations. Consequently, this may help to minimize the risks of companies from exercising the ‘cherry-picking’ and ‘box-ticking’ practices. Conversely, a greater proportion of women directors in SC could deteriorate ESGR quality, partly due to the lack of relevant experience and expertise on these directors, as well as tokenism that limits their influence on elevating ESGR quality.

Our findings have both theoretical and practical implications. Theoretically, our study contributes to the literature through its empirical investigation of the effects of the heterogeneous SC attributes on ESGR quality in ASEAN-5. Unlike prior studies that mainly focus on the presence of SC and ESGR, this study examines how heterogeneous SC attributes influence ESGR quality. By adopting an ASEAN perspective rather than a single-country setting, our study offers a broader perspective that enriches the understanding of how SC attributes play a role in elevating ESGR quality. Moreover, our findings also contribute to RDT and offering fresh insights by highlighting the heterogeneous effects of SC attributes on ESGR quality.

Practically, our findings suggest that ASEAN-5 policymakers and regulators should consider the necessity of making SC mandatory for PLCs in their jurisdictions, with greater emphasis placed on appointing IDs to strengthen ESG oversight. Investors may also enhance their due diligence by assessing the SC independence as a governance signal of a firm’s commitment to ESG and a means to mitigate the risk of greenwashing. Furthermore, our results imply that simply increasing the number of women directors may not enhance ESGR quality, and firms should therefore prioritize appointing women directors with relevant sustainability-related expertise and ensuring their effective empowerment in ESGR decision-making.

There are several limitations in this study that can be further explored by future research. First, our study accounted for only numerous SC attributes to ESGR, while other potentially correlated attributes were not included. Second, a 3-year study period may be limited in capturing the impact of SC on ESGR. Future studies may consider a longer observation period to reaffirm the findings. Finally, our findings may not be generalizable to financial sector firms, as they are excluded from the analysis due to different rules and regulations. Future research may therefore consider comparative analyses of SC’s impact on ESGR across financial and non-financial sectors in the ASEAN-5 context.

Footnotes

Acknowledgements

The authors are grateful to the anonymous reviewers of the journal for their useful suggestions to improve the quality of the article.

Authors Contribution

Kah Yong Chow: Conceptualization, methodology, data collection, statistical analysis, data interpretation and practical insights, writing.

Mohd Zulkhairi Mustapha: Conceptualization, data interpretation and practical insights, and reviewing the original draft.

Ervina Alfan: Conceptualization, data interpretation and practical insights, and reviewing the original draft.

Data Availability

The data that support the findings of this study are available from the corresponding author upon reasonable request.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

This article does not contain any studies with human or animal participants.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.