Abstract

Internet Banking is an example of B2C business model, where transactions can be carried out without visiting the bank branch physically. The objective of the empirical study is to identify the dimensions and their impact on the adoption of Internet Banking on the various adopter categories. In order to get an insight of the different adopter segments, two important constructs such as customer perception constituting perceived ease of use and perceived security risk and perception towards demographic variables consisting of age, gender, education, income and occupation of the users are identified from the existing literature. The cluster analysis reveals that the clusters formed are innovators, early majority, late majority and laggards for adopting Internet Banking. Our study substantiates that only income as a variable acts as a roadblock in the adoption of Internet Banking services. The study will help Internet Banking marketing managers to design their strategies so as to encourage adoption and attract more customers.

Keywords

Introduction

In the preceding decade, the financial service sector has witnessed a swift change owing to the augmentation of globalization and liberalization. One of the key forces behind these developments is technology, leading to novel products, offering new services and tapping of market opportunities (Liao and Cheung, 2002). The scenario in the macro environment has not only revolutionized technology but has fostered new dimensions in the financial service sector. In the banking arena, Internet technology has had a colossal change the way financial services are being planned and offered. Alfansi and Sargeant (2000) opine that technology has brought a transformation in the financial services in the context of Internet Banking. This technological change has led to offering of products and services in accordance with the changing preferences of the consumers and their lifestyles, which has resulted in the exchange of information virtually by providing technology-oriented banking services. Internet Banking offered by the financial institutions is providing services which are prompt, convenient, economical and user friendly, which is expected to increase the efficiency of the banking system. This technology facilitates the Internet banks to deliver products and services without visiting the bank branch physically and transact electronically by logging into the banks’ web site. Laforet and Li (2005) while stressing on the advantages of Internet Banking vouch that the benefits offered would outweigh the traditional banking services and will be able to penetrate the market by gaining competitive advantage.

The changes in the macro environment have enhanced the need to comprehend the Internet Banking adopter categories and their attributes in the Indian context that would facilitate the bank marketers to frame their marketing and promotional strategies accordingly. A diagnostic study conducted in terms of adoption will identify who adopts Internet Banking, and why. The banks need to recognize who precisely are adopting the new technology and the justification behind its usage needs to be explored. As per the specified existing and expected future enormity of Internet Banking (Mattila et al., 2003) the banks must comprehend the complete knowledge of the consumer-based electronic revolution. Consecutively, the article facilitates in understanding the dimensions having a direct impact on the adoption behaviour of Internet Banking by the various adopter categories. Further, in order to get an insight into different adopter segments, adopter categories of Internet Banking and their characteristics are profiled. Three important constructs of perceived ease of use, perceived security risk and demographic variables are identified from the existing literature, which are hypothesized to affect the adoption behaviour of customers of Internet Banking. Demographic profile consists of perception towards age, gender, education, income and occupation of the users. Segmenting the different profiles will facilitate the service providers to identify the different homogeneous groups of adopters, understand their attributes, preferences and demographic characteristics so as to present a lucid understanding of the determinants that influence the adoption behaviour of Internet Banking services in India. Further, this exercise will facilitate the bank marketers in identifying and understanding the potential Internet Banking customers so as to target these segments and cater to their requirements.

Adoption is the decision of a prospective customer to be converted into a regular user of the product. Moore and Benbasat (1991) stress that it is not the potential adopters’ perceptions of the innovation itself, but rather their perceptions of using the innovation that are key to whether the innovation will be adopted or not. Results from prior research reveal that the success of Internet Banking is gauged not only by banks but by customers’ acceptance of it. The latter has had a great influence on the adoption of Internet Banking which has been substantiated in the previous studies (Karjaluoto et al., 2002; Mattila et al., 2003; Pikkarainen et al., 2004; Rotchanakitumnuai and Speece, 2003; Sathye, 1999). The preceding studies mentioned have been conducted globally pertaining to diffusion of Internet Banking. However, not many studies have been found in the Indian context, which have steered their investigation in the context of Internet Banking adoption.

It was Rogers (1995) who previously documented that consumers do not adopt innovations simultaneously. In the formative classification, Rogers (1995) suggested that adoption of new products take place over time and that the adoption curve can be segmented into identifiable groups as:

Innovators Early adopters Early majority Late majority Laggards

It can be further interpreted that innovators are risk takers who venture onto new products and adopt them. Early Adopters are futurists and look forward for products that are novel. Early Majority are pragmatists who adopt a ‘wait-and-see’ attitude towards new applications of innovation and need concrete orientation prior to adopting it. Late Majority are the traditionalists who adopt an innovation late in the process of adoption. Once it has been recognized among the Late Majority, it is accepted at last by the Laggards, who are considered to be the last in the process of adoption.

The focus of the empirical study is to identify the dimensions and their impact on the adoption of Internet Banking by profiling various adopter categories of Internet Banking. To achieve the objectives the constructs used in this study have been examined. Further, a conceptual model is presented and relationships among the key dimensions have been discussed.

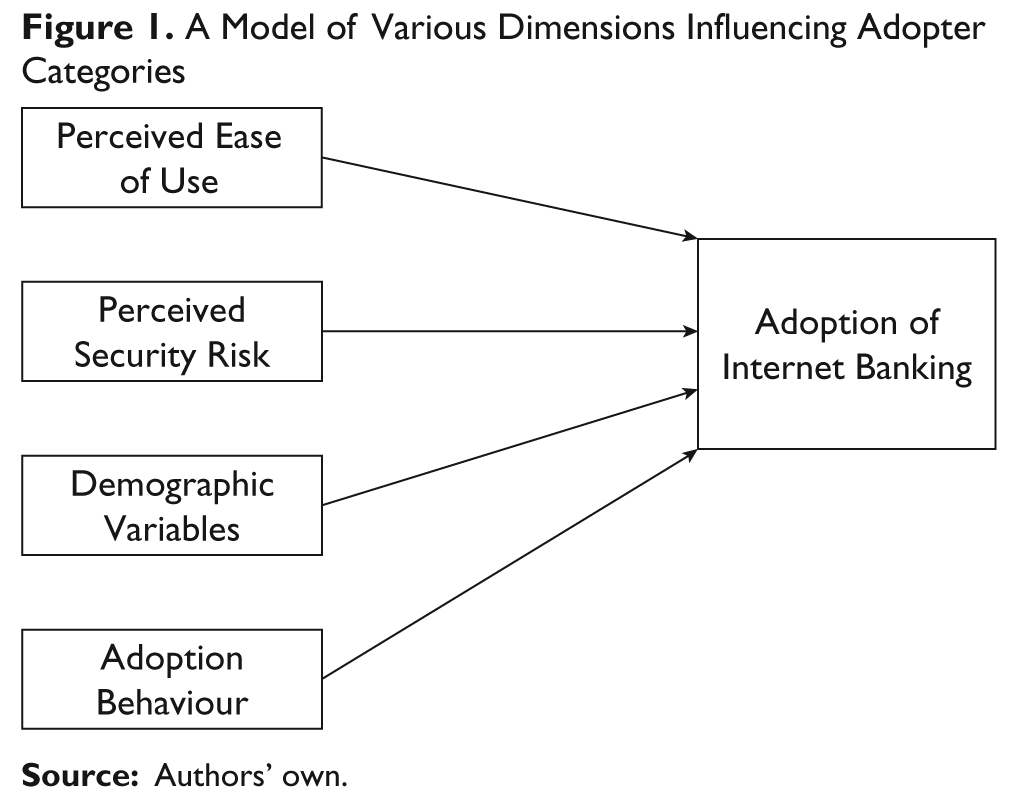

The Conceptual Framework

In developing the conceptual framework (Figure 1), prior literature has been reviewed to define the key constructs of the framework and describe the theoretical grounds and their relationships in the model.

Adoption Behaviour

In the adoption literature, multiple concepts are referred to with a strong emphasis on ‘acceptance’ and ‘rejection’ of a product or a service. The most universal definition of adoption is ‘the acceptance and the continued use of an innovation’ (Robertson, 1971, p. 56). On the other hand, Rogers (1962, p. 17) views adoption as ‘a decision to continue full-scale use of an innovation’. This section explores the behaviour of adopters in the various stages of adoption process. For a new technology-based service, it is likely that only a small subset of consumers adopt it (Lee et al., 2005). The difference between the adopter categories pertaining to their behaviour and their attributes towards adoption of Internet Banking services have been gauged and segmented under distinct grouping. Prior literature has outlined the personal traits and demographics to profile the adoption behaviour of different categories of Internet Banking users. Peters and Venkatesan (1973) regard that personal characteristics and environmental variables have a significant impact in the adoption process. In the diffusion of innovation and adoption of a new product, the innovators have a vital role to play. Prior studies have highlighted the personal characteristics of the consumer innovators in adoption of a product and regard that this segment of consumers have higher levels of income, education and are younger in age (Akinci et al., 2004; Dickerson and Gentry, 1983; Lee et al., 2005; Tornatzky and Klein, 1982; Uhl et al., 1970). Mahajan et al. (1990) compare the adopter categories generated by the classical approach proposed by Rogers (1983). The results indicate that the adopter categories are significantly different from each other in terms of age, education, household income and occupation. Further, the adopters who adopt technology earlier than others tend to use it more often and have greater expertise in its usage.

Customer Perception

Perceived ease of use as defined by Davis (1989, p. 985) is regarded ‘to be the degree to which an individual perceives that using a particular system will involve less effort’. An application perceived to be easier to use than another product or service is more likely to be accepted by users. Internet Banking has been perceived as an innovation relatively easy to comprehend and use (Cheng et al., 2006; Liao et al., 1999; Liao and Cheung, 2002). It is designed to operate and to create a user-friendly interface leading to easy-to-use technology, which will facilitate in adoption by the users (Premkumar et al., 1994; Straub, 1989). Davis (1989) emphasizes that the variable perceived ease of use influences the computer acceptance in individuals. Wang et al. (2003) have focused on perceived ease of use exerting a strong influence on adoption of Internet Banking. Swanson (1987) regards that perceived ease of use is a fundamental construct that plays a vital role in influencing the decision to use an information technology product/service. Eriksson et al. (2004) opine that customers use Internet Banking when they perceive it as easy to use. Thus, it is imperative for Internet banks to offer well-designed and easy to use Internet Banking services if they want to promote customer adoption. Daniel (1999), Moore and Benbasat (1991), Sathye (1999), Taylor and Todd (1995), Yang et al. (2004) and Ndubisi and Sinti (2006) regard that ease of use enhances the use of technology and identify it as one of the vital factors.

Perceived security risk is defined by Kim et al. (2008, p. 546) as ‘consumer’s belief about the potential uncertain negative outcomes from the online transaction’. Further, Dowling and Staelin (1994, p. 119) elaborate the concept of perceived security risk as ‘the consumer’s perception of the uncertainty and adverse consequences of buying a product or a service’. Adoption of a service takes place when a customer perceives a product or service to be secure, free from risk and maintains security. Authors like Frambach (1993), Ostlund (1974) and Webster (1969) regard that risk as a dimension influences adoption of a product or a service. It has been substantiated (Bhimani, 1996; Cockburn and Wilson, 1996; Siu and Mou, 2005; Quelch and Klein, 1996) that a pervasive roadblock to the adoption of electronic commerce is the lack of security and privacy over the Internet. This has further led to the perception that transacting virtually is a risky activity. Thus, it is anticipated that individuals who perceive that using Internet Banking involves low risk, would be inclined to adopt it. Bhatnagar et al. (2000) regard that since the transaction is considered to be open in the virtual environment, it may result in the interception by the third party which may further lead to security concerns among the consumers. Liao and Cheung (2002) assert that consumers’ expectation and fulfillment of the security influences the adoption of Internet Banking services. Hoffman et al. (1999) point out that in the virtual environment, the customer’s personal information invades consumer’s privacy which plays a negative role in individuals’ decision to adopt a new technology. Rotchanakitumnuai and Speece (2003) regard that misuse of customers’ information may result in greater perceived security risk. Emphasizing on the impact of Internet security, Miyazaki and Fernandez (2001) assert that it builds consumer confidence. Thus, for a web-based service provider, it is essential to assure its customers that their privacy and safety are protected.

Demographic Variables

Perceptions related to demographic variables consist of age, gender, education, income and occupation of the users. Prior studies have identified that the demographic characteristics are significantly associated with adoption of Internet Banking (Karjaluoto et al., 2002; Kolodinsky et al., 2000; Sathye, 1999). Explorations of demographic correlations pertaining to acceptance of technology have resulted in contradictory viewpoints with respect to adoption. Gender has not been found to have a direct impact on adoption of technology in general (Taylor and Todd, 1995), on the other hand Gefen and Straub (1997) validate that men and women appear to have dissimilar acceptance level of technology, with men more ready to adopt. Prior literature exhibits linkage of age with adoption of technologies, with younger people being more willing to adopt (Karjaluoto et al., 2002; Lee et al., 2002; Trocchia and Janda, 2000; Zeithaml and Gilly, 1987). Further, income and education have a propensity to influence adoption of an innovation (Donnelly, 1970; Labay and Kinnear, 1981; Lee et al., 2002). Im et al. (2003) regard that income, education and age are the most widely accepted identifiers for innovators. Mattila et al. (2003) find that income and education predict whether or not consumers adopt Internet Banking. Authors like Shergill and Li (2005) and Wan et al. (2005) regard that males adopt Internet Banking more easily than females. Prior literature validates that Internet Banking is associated with moderate income level, middle aged and higher level of education of the users. Listing the significant factors influencing the adoption of Internet Banking, Jaruwachirathanakul and Fink (2005) stress that demographic variables of gender, education and income have an impact on adoption, but not age. Jayawardhena and Foley (2000) find that customers who have high income level are more likely to use Internet Banking. Gilly and Zeithaml (1985) validate in their study that age influences the adoption of technology and assert that the older the customer, the higher the negative perception towards technology.

Thus, the above discussed dimensions of customer perception and demographic variables are the factors influencing the adoption behavior of customers of Internet Banking in the study. Although, public and private sector banks are offering Internet Banking services in India, it is still in its nascent stages.

Method

Sample Design and Data Collection

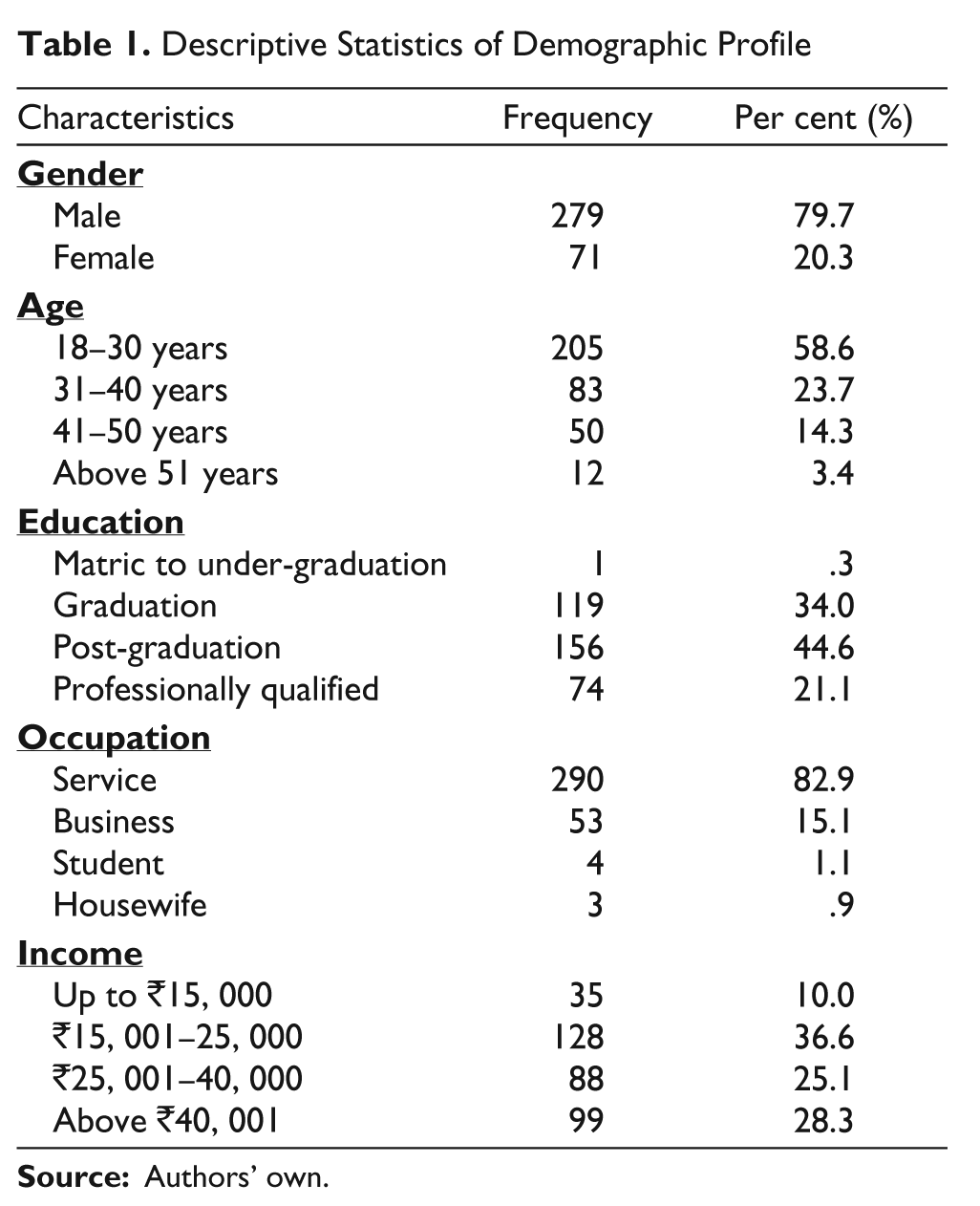

A survey was conducted using a convenient sample of 350 active users of Internet Banking. The survey was conducted in the three cities of the state of Punjab and Chandigarh in India. For sampling purposes, the population consisted of Internet Banking users of the four cities of Amritsar, Chandigarh, Jalandhar and Ludhiana and 80–95 respondents were selected from each city. The sample represented a cross-section of Internet Banking users in terms of gender, age, education, occupation and income. Maximum users (58.6 per cent) belonged to age group of 18–30 years, 23.7 per cent were from 31–40 years age group, 14.3 per cent belonged to 41–50 years age group and 3.4 per cent constituted respondents above 51 years of age. Internet Banking users were mostly post-graduates (44.6 per cent), graduates were 34 per cent, professionally qualified were 21.1 per cent and under graduation constituted only 0.3 per cent of the total sample. Of the respondents, 82.9 per cent were engaged in service as occupation, followed by business 15.1 per cent, students accounted for 1.1 per cent and housewives also constituted 0.9 per cent of the sample. Amongst the users 10 per cent had income levels of up to ₹15,000, 36.6 per cent belonged to the income category between ₹15,001–25,000, 25.1 per cent constituted income level of ₹25,001–40,000, followed with 28.3 per cent of income level above ₹40,001. Of the Internet Banking users, 72 per cent belonged to private sector banks, whereas 28 per cent were from the public sector. Of the respondents, 79.7 per cent were male and females constituted only 20.3 per cent of the Internet Banking users. The frequency distribution of the demographic profile of the respondents is depicted in Table 1.

Descriptive Statistics of Demographic Profile

Zonal offices of almost all the banks located in the region were approached and finally officials of nine banks provided the complete lists of their customers using Internet Banking. Out of the nine banks, whose customers were finally tapped, five were private sector banks, namely Citibank, ICICI Bank Ltd., HDFC Bank Ltd., Standard Chartered Bank and Axis Bank. Customers of four public sector banks namely State Bank of India, Punjab National Bank, Bank of India and Canara Bank were also approached. The list of customers provided by the banks was exhaustively covered, the customers were contacted telephonically and were asked, if they were active users of Internet Banking. If they replied in the affirmative, they were requested to participate in the not-for-profit survey on Internet Banking. If they agreed, an appointment was fixed with them at a convenient place and time and the questionnaire was personally got filled from each of the respondents. The total numbers of questionnaires filled were 370, out of which incomplete and biased responses were extracted and only 350 final responses were retained.

Cluster Analysis

Cluster analysis is applied in the present study on dimensions of perceived ease of use; perceived security risk; perception towards demographic variables of age, gender, education, income and occupation which have been extracted from the literature reviewed. These dimensions are examined as interdependent variables, as cluster analysis makes no distinction between dependent and independent variables. Rather, interdependent relationships between the whole set of variables are examined. The primary objective of cluster analysis is to classify objects into relatively homogeneous groups based on the set of variables considered (Malhotra, 2007). Cluster analysis has been performed on the data, using hierarchical and non-hierarchical clustering methods and subsequently comparing their results. In the first stage, hierarchical clustering is used to determine the number of clusters. The non-hierarchical is applied in the second stage to authenticate the results (Keen et al., 2004). Further cross tabulation is conducted to gauge the number of customers using Internet Banking in each cluster along with their demographic details.

Thus, the study on active users of Internet Banking has been conducted to identify the adopter categories using cluster analysis. The homogeneous clusters are hypothesized to have similar characteristics and preferences for adoption of Internet Banking services.

Measurement Scales Used

The framework of the questionnaire was structured and non-disguised, with closed-ended questions measuring respondents’ agreement/disagreement on a five-point Likert scale of (1) strongly disagree to (5) strongly agree. In constructing the survey items specific to this study, a pool of existing items from the previously studied literature was reviewed. Appropriate measures for each construct were selected from the literature and adapted. The survey instrument included a set of 20 items designed to measure the factors influencing the adoption of Internet Banking by various adopter categories. The dimensionality of perceived ease of use was evaluated using the framework given by researchers like Davis (1989), Venkatesh and Davis (2000) who have used statements like ‘I am willing to try Internet Banking services’, ‘Internet Banking is costly to access’, ‘The usage of Internet Banking is confusing’, There is lack of appropriate information on the web site of Internet Bank’, ‘I find Internet Banking easy to use’, ‘It will be easy for me to become skillful at using Internet Banking’, and ‘My interaction with Internet Banking is clear and understandable’. The items as given by Grewal et al. (2003), ‘If I transact through Internet Banking, I believe it will be a secure transaction’, ‘I believe that transactions conducted through Internet Banking are secure’, ‘Perceived security risk is the main factor behind non adoption of Internet Banking’, ‘I believe that security for Internet Banking transactions, present a low level of risk’, ‘I am not satisfied with the security and privacy of Internet Banking’, has been entitled as perceived security risk. Demographic variables were assessed with the help of the scale developed by Hernandez and Mazzon (2007); Jaruwachirathnakul and Fink (2005) and Wan et al. (2005) who have used statements like ‘Income might be a hindrance to adoption of Internet Banking’, ‘Better understanding of Internet Banking is related to education’, ‘I find the services compatible with my occupation’, ‘I feel that only computer literate can operate Internet Banking services’, and ‘Age might be a hindrance in its adoption’. Measures for adoption behaviour were adapted from Mahajan et al. (1990) who have used statements ‘I will be the first one to adopt Internet Banking’, ‘I have prior experience and knowledge of computer interactivity’ and ‘I am interested in its novel value’. A detailed listing of the items of constructs along with their source is provided in the Appendix.

Results

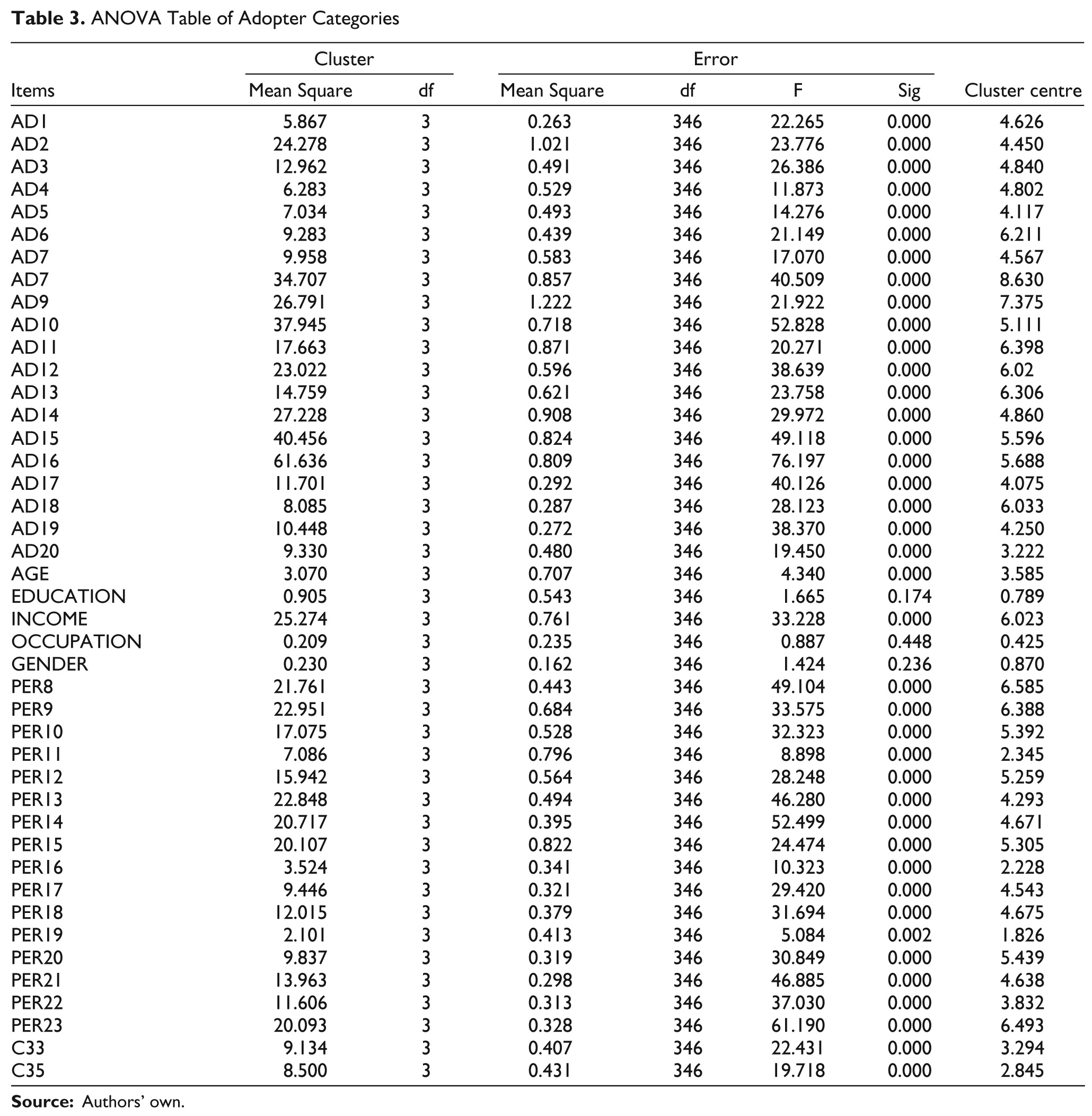

In order to identify homogeneous clusters, a four-cluster solution has been accomplished. After determining the four-cluster group, the analysis reveals that the clusters formed are innovators, early majority, late majority and laggards for adopting Internet Banking, which is depicted in Tables 2 and 3.

Non-hierarchical Cluster Analysis

ANOVA Table of Adopter Categories

The following clusters are revealed after performing cluster analysis and cross tabulation gives insights (Table 4) regarding the number of respondents and their demographic characteristics in each cluster group.

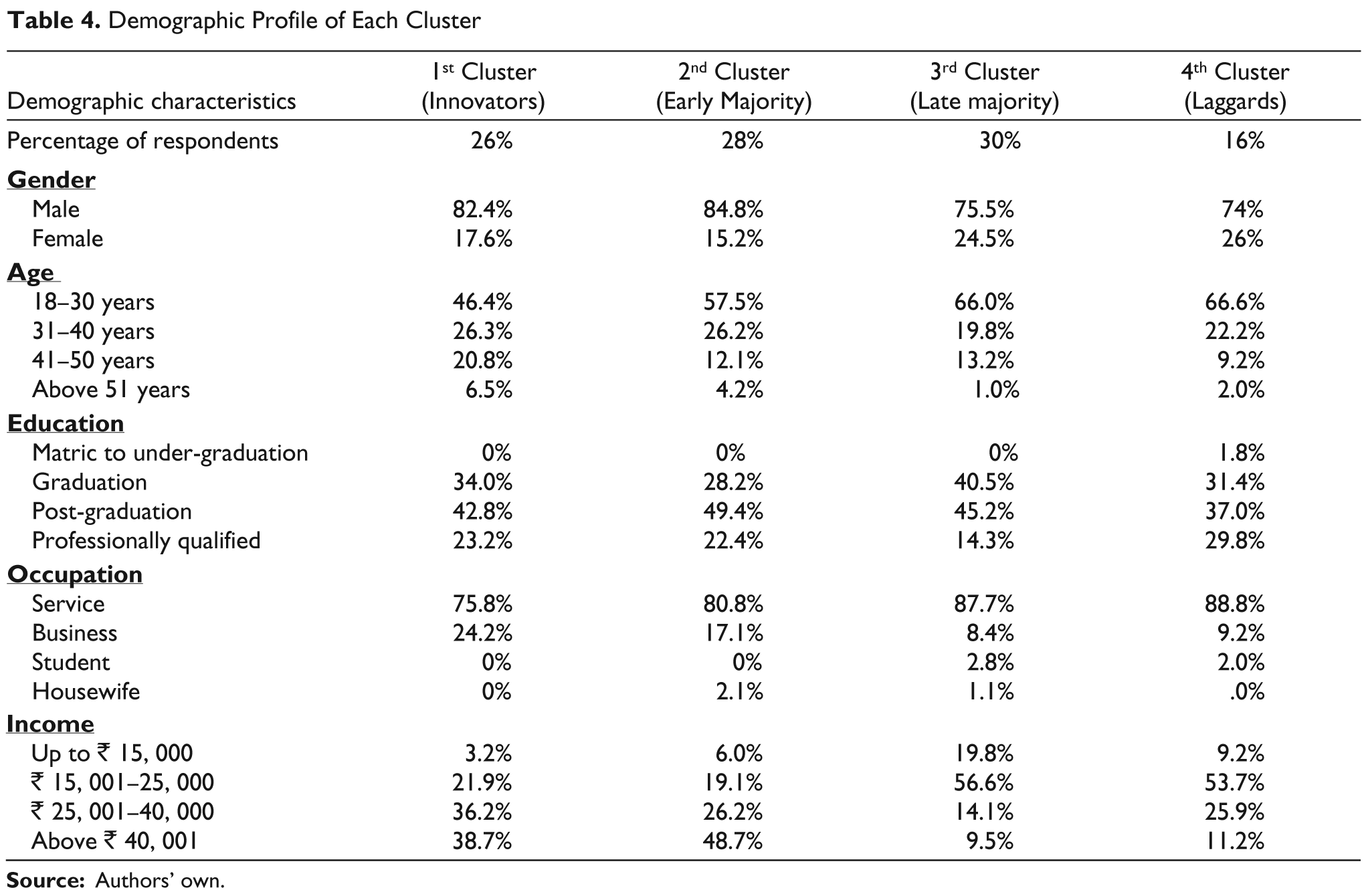

Demographic Profile of Each Cluster

The results in Tables 2 and 3 provide an evidence that the clusters are distinct pertaining to the usage of Internet Banking services, their understanding, information, security issues, willingness to adopt the services and the impact of various demographic variables of age, gender, education, income and occupation on the adoption of Internet Banking in India.

Cluster 1––The first cluster which has been named innovators consists of 26 per cent of the total respondents, who are strongly willing to try and adopt Internet Banking services first. Their perception is that the services offered by Internet Banking are novel, easy to use and understandable. This cluster does not consider age to be a roadblock whereas income is perceived as a hindrance in the adoption of Internet Banking. Innovators regard that understanding of Internet Banking is not related to education whereas they strongly agree that they have prior experience of computer interactivity and perceive that web pages are confusing due to improper information of the web site. This cluster further disagrees that Internet Banking lacks personal contact or is costly to access. Innovators highly perceive that usage of Internet Banking is pleasant and easy to use. Further, innovators are ready to adopt Internet Banking services as they neither perceive security risk nor regard it as a hindrance in its adoption. The results reveal that on the whole innovators are influenced by the demographic characteristics of age, gender, education, occupation and income, in the adoption of Internet Banking services. Thus, innovators score high on the facilitators of perceived ease of use and score low on the inhibitors of perceived ease of use. Similarly, they score high on the perception towards security of transactions and low on the deterrents to security in the perceived security risk construct.

Cluster 2––The second cluster represents early majority, constitute 28 per cent of the total respondents, who are not willing to adopt Internet Banking services instantly. This segment agrees that they give importance to seeking information and perceive that education helps in better understanding of Internet Banking services. Early majority regard that age and income, moderately act as a hindrance in adoption of Internet Banking. They have prior experience and knowledge of computer interactivity and perceive that due to clarity of information on the web site, web pages and their usage is not confusing. Further, early majority highly perceive that perceived security risk is not a factor behind non-adoption of Internet Banking. This cluster, in addition disagree that only computer literate can operate Internet Banking services and find it easy to become skillful at using Internet Banking services. Early majority agree that interaction with Internet Banking does not require a lot of mental effort and therefore highly perceive Internet Banking as easy to use.

Cluster 3––The third cluster comprises late majority, which consists of 30 per cent of the total respondents who are willing to try Internet Banking services, after others have availed it. Late majority has an attitude of seeking information before accepting any banking services. They moderately perceive that better understanding of Internet Banking is not related to education and do not have any prior experience and knowledge of computer interactivity. Late majority are not influenced by the demographic variables of age, income, occupation and gender. Further, they highly perceive that it is not easy to become skillful as the steps involved in performing transactions need to be remembered. Late majority perceive that security risk is the major factor behind non-adoption of Internet Banking services. According to this cluster they disagree that only computer literate can operate Internet Banking services. As Internet Banking requires a lot of mental effort, consequently late majority do not perceive Internet Banking easy to use. They regard that web pages and their usage is confusing since there is lack of appropriate information on the web site of Internet bank. They further agree that Internet Banking is costly to access.

Cluster 4––The cluster comprises consumers who are laggards and constitute only 16 per cent of the total respondents and regard that they have an attitude of seeking information before accepting any banking services. Laggards highly consider that better understanding of Internet Banking is related to education, while alternatively regard that age and income might moderately influence the adoption of Internet Banking. Laggards perceive Internet Banking to be costly to access. They consider that there is lack of appropriate information on the web site. This cluster strongly feels that only computer literate can operate Internet Banking services, as they need to have prior experience and knowledge of computer interactivity. Laggards are not satisfied with the security offered by Internet Banks and highly perceive that perceived security risk is the main factor behind non-adoption of Internet Banking. They perceive that it is not easy for them to become skillful in using Internet Banking as not only a lot of mental effort is required but it is also confusing and per se is not easy to use. Predictably this cluster scores low on the facilitators and high on inhibitors of perceived security risk. Similarly, they score low on the perception towards security of transactions and high on the deterrents to security in the perceived security risk construct.

Demographic Results of the Clusters

A large variation has been observed while scanning the demographic outcome in the four clusters. The analysis reveal that although males constitute a major percentage of uses in all the four clusters, nevertheless the comparison with female adopters of Internet Banking reveal some interesting results. The analysis disclose that majority of male adopters are innovators (82.4 per cent) and early majority (84.8 per cent), whereas females adopt Internet Banking services as late majority (24.5 per cent) and laggards (26 per cent). The results in Table 4 reflect a contrasting trend amongst the gender in their adoption behaviour.

Age as a demographic variable illustrates that the proportion of Internet Banking users in the age category of 18–30 years increase steadily across different clusters, (innovators [46.4 per cent], early adopters [57.5 per cent], late majority [66.0 per cent] and eventually laggards [66.6 per cent]). On the other hand, adoption of Internet Banking in the age category 31–40 years reveal a downward trend with this category constituting 26.3 per cent in the cluster named innovators, 26.2 per cent in the cluster constituting early majority and their percentage in the late majority cluster decreasing to 19.8 per cent, and laggards being 22.2 per cent in this age group. The results also reveal that the proportion of respondents in the 41–50 years age group in the cluster innovators is 20.8 per cent and this proportion decreases to 9.2 per cent in case of laggards. Hence, it can be inferred that age is not a hindrance in the adoption of Internet Banking.

Further, the result of the demographic variable of education shows that post-graduates are the early adopters (49.4 per cent) to adopt Internet Banking and simultaneously constitute the major percentage of adopters across the clusters.

While assessing occupation as a demographic variable, it has been substantiated that although a major segment of adopters of Internet Banking belong to service as an occupation in all the four clusters, there has been a substantial increase in the proportion of service class in the four categories (innovators [75.8 per cent], early majority [80.8 per cent], late majority [87.7 per cent] and laggards [88.8 per cent]), meaning thereby that service class is relatively late to adopt Internet Banking. On the other hand, the proportion of businessmen is more in the cluster named innovators (24.2 per cent) and their proportion declines to 9.2 per cent in the category laggards, meaning thereby that the businessmen are more eager to adopt Internet Banking.

As regard income, the demographic profile depicts an interesting trend. The proportion of the income group ₹15,001–25,000 increases from 21.9 per cent in case of innovators to as high as 56.6 per cent in case of late majority and to 53.7 per cent in case of laggards. The proportion of the income category above ₹40,001 in the four clusters shows a decreasing trend (innovators [38.7 per cent], early majority [48.7 per cent], late majority [9.5 per cent] and laggards [11.2 per cent]). Thus, it can be inferred that income level is a driver of adoption of Internet Banking with the high income falling in the innovators and early adopter categories, and low income falling in late majority and laggards categories.

Thus, the results of the study coincide with the objective of the study that reveals how the various dimensions influence the different adopter categories and reveal the characteristics of various adopter categories of Internet Banking services.

Discussion and Managerial Implications

Overview of the Study

This article has attempted to describe the Internet Banking phenomenon primarily by analyzing the profile, attributes and preferences of the adopter categories of innovators; early adopters; late majority and laggards. The analysis provides evidence that there are significant differences found among the clusters with respect to perceived ease of use, perceived security risk and demographic characteristics consisting of age, gender, education, income and occupation.

Our study has provided evidence that the greater perceived ease of use of Internet Banking services would make the system easy to interact with, resulting in its adoption by various adopter categories.

Security concern is the biggest factor for non-adoption of Internet Banking. Quick response to security issues by the service provider can help in restoring the confidence in the Internet Banking services, which facilitates further adoption of its services. The findings of the study suggest that in order to attract more users to Internet Banking, security risk needs to be reduced as it has an impact on its adoption.

Sarel and Marmorstein (2003) assert that innovators and early adopters are more eager to buy, and are willing to try an innovation that the majority will adopt later. Innovators are the first in the adopter category and are generally educated with higher levels of income, are younger and are willing to adopt new technologies. Innovators have no inhibition pertaining to perceived security risk and as a result use new technology. When they perceive technology to be easy to use and without much hindrance, they adopt it readily. Robertson and Kennedy (1968) and Im et al. (2003) support the contention that innovators are young in age, are more qualified and come in the higher income group. It is due to these characteristics that innovators tend to be risk takers and venturesome. The innovators seek to secure products which are ‘new, first, original, futuristic, distinctively different’ (Uhl et al., 1970). The findings signify that the innovators are keen to accept Internet Banking services in the Indian context. The innovators identify that the services offered are new, simple to apply and can be easily comprehended.

Dickerson and Gentry (1983) investigate the profile of the early adopter, which is middle aged, higher income, more educated, opinion leader and information seeker. Early adopters are significantly different from laggards. They are inquisitive about gathering more information regarding Internet Banking and consider it to be easy to use without much effort.

Late majority grow faster, have high market potentials and have high repeat rates. Authors such as Oumlil and Williams (2000) and Shankar et al. (1998) regard that mature customers generally come under late majority. Mattila et al. (2003) regard that late majority have a negative attitude towards technology and have a negative attitude towards it. The findings reveal that this cluster is prepared to avail Internet Banking services once others have used it. They regard Internet Banking as not easy to use due to its confusing and difficult-to-memorize steps of operation.

Laggards are regarded as the last group of persons to adopt a product, service or idea. Authors like Uhl et al. (1970) and Gilly and Zeithaml (1985) in their studies state that laggards have fewer finances available and do not take the risk until the products have been proved by others to be acceptable. Further, the findings reveal that elderly consumers resist changing with respect to adoption of new technology, but try to gather more information. Thus, laggards are repelled by products which are ‘too new, unproven and risky’ and avoid the risk of trying new products and tend to repeat purchases (Uhl et al., 1970). Our study confirms that this segment of customers accept Internet Banking services later than the others. Their perception towards Internet Banking is not a positive one and is not willing to trust the services being offered.

This study is a pioneering effort in investigating the significant influence of perceived ease of use, perceived security risk and demographic characteristics on the different adopter categories for Internet Banking in India.

Managerial Implications and Conclusion

The analysis will enhance the knowledge of consumer’s perceptions and opinions about Internet Banking services for the service providers. The research results have several implications that may be considered by Internet banks and their managers.

Prior research findings support the contention that perceived ease of use is an important variable affecting the adoption (Daniel, 1999; Sathye, 1999; Yang et al., 2004). To further increase the overall adoption by the users, it becomes important for the marketers to develop a simple and easy to use Internet Banking system, so that the potential users would feel comfortable, once they believe that transactions through Internet Banking are easy and free of effort.

The use of personal information and transacting through a virtual environment is a matter of concern in Internet Banking. Security is of concern in terms of unauthorized use, abuse of accounts and keeping customers’ personal details private. In order to overcome the problems related to security, Internet banks can address the security issue by educating the customers through advertising the security of their secret code, so as to promote the message of reliability among users. The service providers can ensure the customers of its foolproof system by informing them of its security features through its well-designed web site. The service providers need to address another concerns pertaining to providing up to date, accurate and reliable information so that the queries of the users are resolved. It is high time that the service providers take appropriate steps to educate and inform the potential customers and the users of Internet Banking of its utility and value added services. Such an exercise will facilitate the marketing managers to encourage the prospective users to adopt Internet Banking by endorsing its utility. This would inculcate the feeling of security and will further on lead to the adoption of Internet Banking services.

The demographic characteristics of age and income play a vital role in influencing the adoption behaviour of Internet Banking services. Consequently, appropriate strategies need to be designed by the marketing managers for the demographic characteristics and accordingly market may be segmented.

The marketing managers can furthermore blueprint their marketing tactics by transmitting information through promotional campaign that depict Internet Banking as being easily accessed without much mental effort to focus on late adopters and laggards. The marketers need to concentrate on them as they resist change. Further, the new technology provided by Internet Banking needs to communicate the benefits through advertisement, print media, Internet, etc., in such a manner that it generates a momentum in the adoption process.

As Internet Banking is gradually gaining commercial momentum, it can be harnessed as an opportunity by the bank marketers to gain competitive advantage. Arming themselves with complete understanding of the potential users, their needs, demographics and perceptions will assist the marketing managers to have a thorough understanding of the target customers to offer the services, so as to encourage adoption in India. This will not only generate profitable gains for the marketers of Internet Banking but simultaneously create a niche for them in the tough competitive arena.

Appendix: Construct along with Corresponding Items and the Source

Perceived Ease of Use

(Davis, 1989; Venkatesh and Davis, 2000)

I am willing to try Internet Banking services.

Internet Banking is costly to access.

The usage of Internet Banking is confusing.

There is lack of appropriate information on the web site of the Internet bank.

I find Internet Banking easy to use.

It will be easy for me to become skillful at using Internet Banking.

My interaction with Internet Banking is clear and understandable.

Perceived Scurity Risk

If I transact through Internet Banking, I believe it will be a secure transaction.

I believe that transactions conducted through Internet Banking are secure.

Perceived security risk is the main factor behind non-adoption of Internet Banking.

I believe that security for Internet Banking transactions present a low level of risk.

I am not satisfied with the security and privacy of Internet Banking.

Demographic Variables

(Hernandez and Mazzon, 2007; Jaruwachirathanakul and Fink, 2005; Wan et al., 2005)

Income might be a hindrance to adoption of Internet Banking.

Better understanding of Internet Banking is related to education.

I find the services compatible with my occupation.

I feel that only computer literate can operate Internet Banking services.

Age might be a hindrance in its adoption.

Adoption behaviour

I will be the first one to adopt Internet Banking.

I have prior experience and knowledge of computer interactivity.

I am interested in its novel value.