Abstract

The purpose of this article is to identify the dimensions of service quality (SQ) in the banking sector and examine the effect of SQ dimensions on customer satisfaction (CS), and therefore the effect of CS on corporate image (CI) in the selected public sector banks (PSBs) in India. The sample of the study consists of 640 retail customers of PSBs in the National Capital Region (NCR) of India and the data were collected through a structured questionnaire using a 7-point Likert scale based on purposive sampling. Therefore, the authors empirically validate a measurement model using structural equation modelling (SEM) through path analysis. The findings revealed that ‘tangibility’ and ‘assurance’ dimensions were most important predictors of CS among all five dimensions of SQ. In addition, the results also validate that CS is an important antecedent for influencing CI, and therefore CS acts as a linkage between SQ dimensions and CI in the Indian context. Finally, the research article presents the conclusion, implications and limitations and the possible directions for further research.

Introduction

The banking system of any country has a greater place in the service sector, and is treated as an essential institutional and functional vehicle for the transformation of the economy of the country; therefore, the banking sector acts as a barometer of the financial system. After the post-liberalization and globalization period in the Indian banking system, the entry of private and foreign bank players made the Indian banking sector more competitive. Consequently, customers have more choices to select their banks in the modern era of the Indian banking system (Singh & Arora, 2011). Hence, it is necessary for public sector banks (PSBs) to serve their target customers’ needs and demands by offering superior service quality (SQ) and value than their private counterparts.

Customer satisfaction (CS), SQ and corporate image (CI) are the most powerful determinants of a marketer’s success in the present era of stiff competition in the banking and financial services (Amin, Isa & Fontaine, 2013; Bloemer et al., 1998; Ladhari et al., 2011). In the marketing literature, the above phenomenon has consistently achieved enormous attention by various scholars worldwide in the service industry context, and they confirmed the significant relationship among these determinants as an integrated model from the retail banking perspective (Amin et al., 2013; Bloemer et al., 1998; Ladhari et al., 2011). However, CI has been less probed in the financial and banking sector than in other services, such as tourism, hospitality and medical (Baisya, 2013; Dowling, 2004; Ennew & Waite, 2013).

On the other hand, such studies are still limited in the Indian banking context, mostly researchers examined the relationship between SQ and CS using the standard scale of SERVQUAL (Khare, 2011; Krishnamurthy, SivaKumar & Sellamuthu, 2010; Selvakumar, 2015) or the modified scale with factor analysis (Choudhury, 2008; Gupta & Dev, 2012). However, the relationship between CS and CI has rarely been investigated in the Indian context; thus, no particular study has validated ‘CI’ as an outcome of CS in the Indian banking sector so far, particularly in Indian PSBs.

Therefore, the present empirical article strives to fill the research gap in the literature of service marketing by identifying the dimensions of SQ in the banking sector via factor analysis. Next, it examines their relationship with CS. This is followed by determining the effect of CS on CI using the structural equation model (SEM) through path analysis in the retail banking context with special reference to Indian PSBs.

The present article is organized into the following sections. The literature review presents the ‘Theoretical Framework and Hypothesis Development’ with a brief outline of the constructs, that is, CI, CS and SQ, and six hypotheses have been formulated to examine their relationship. This is followed by the ‘Research Methodology’ section. Next, the study presents a discussion about the findings, implications and limitations in the section ‘Conclusion and Implications’ with concluding remarks for future research.

Theoretical Framework and Hypothesis Development

Corporate Image

In marketing domain, CI is commonly found to be the main source of corporate reputation and corporate branding in the service context mostly in medical, hospitality and tourism sectors (Baisya, 2013; Dowling, 2004). In addition, this phenomenon has been much emphasized in the product marketing context in terms of brand image as a strategic factor of differentiation (Aaker, 1991; Keller, 1993; Keller & Lehmann, 2006). However, it has been less investigated from the perspective of banking sector compared to other services, such as tourism and hospitality. Concerning this phenomenon, several scholars emphasized corporate branding and CI; for example, Kennedy (1977) stated that CI mainly consists of two components, namely, functional and emotional. The functional component is associated with tangible dimensions that can be easily identified and measured. On the other hand, the emotional component is related to psychological aspects of customers’ experiences and attitude towards a firm (Amin et al., 2013), which are subjective. In addition, corporate image is associated with customers’ attitude and experience towards the firm’s financial performance, and its ability to differentiation that cultivate corporate brand image. Therefore firm image is evaluated by customers via comparing these attributes with other related organizations (Dowling, 2004).

Particularly in the banking industry, CI can be operationalized based on image attributes, namely, bank outlets, service delivery processes, interest rates and investment returns, which establish the source of corporate positioning (Ennew & Waite, 2013). Therefore, a positive image is one of the important aspects of a firm’s ability to retain its relative market position in the competitive banking sector (Bloemer et al., 1998). Hence, the notion is that CI is always concerned with a firm’s intangible asset which cannot be imitated, and therefore influences the customers’ overall perception towards the organization (Barney, 1991; Porter & Claycomb, 1997).

Customer Satisfaction

In the marketing literature, the phenomenon of CS has constantly drawn enormous attention from the academic scholars and practitioners since the day of inception of marketing. The phenomenon of CS is subjective based on one’s beliefs and experiences resulting from product and/or service performance (Solomon, Russell-Bennett & Previte, 2012). Concerning this subjective phenomenon, Oliver (1997) argued that satisfaction is generally conceived as a pleasurable outcome, a desirable end state of consumption or patronization.

According to Kotler and Armstrong (2012), satisfaction or dissatisfaction is the post-purchase assessment of products or services done by customers while matching their expectations. Similarly, in services, Woodside, Frey and Daly (1989) and Zeithaml et al. (2011) stated that satisfaction or dissatisfaction is an evaluation of a product or service offering to meet a customer’s needs or expectations. In other words, it is a trade-off between performances and expectations done by customers in relation to market offerings, and therefore customers will be satisfied if the performance matches with their expectations, and vice versa (Kotler et al., 2009). Moreover, exceeding performance results in customers being more delighted; consequently, a highly satisfied/delighted customer base plays an important role in customer retention and loyalty which are treated as a firm’s strategic factors in the competitive banking industry across the globe (Berry, Seiders & Grewal, 2002; Caruana & Malta, 2002; Ennew & Waite, 2013) as well as in the Indian banking context (Choudhury, 2008; Khare, 2011; Selvakumar, 2015; Sureshchandar, Rajendran & Anantharaman, 2002).

The Relationship between Customer Satisfaction and Corporate Image

The relationship between the two phenomena, CI and CS, has remained a highly discussed matter in the marketing literature. Many scholars have confirmed empirically that there is a significant relationship between CS and CI in the service industry including the banking sector (Amin et al., 2013; Dick & Basu, 1994; Hu, Kandampully & Juwaheer, 2009; Ladhari et al., 2011), and thus have argued that a satisfied customer base fosters favourable and positive CI, which in turn can also affect customers’ repeated patronage or loyalty and word of mouth. Therefore, CI is highly considered as one of the important sources of competitive advantage in service marketing (Bloemer et al., 1998; Davies, Chun, Da Silva & Roper, 2003). Similarly, in Indian banking, Vyas and Raitani (2014) recognized that bank reputation/image is one of the key factors for the switching behaviour of customers in India.

Therefore, the notion is that CS is an important predictor of CI in the banking sector; however, such a relationship was hardly found in the Indian banking context, and thus no particular study is available so far emphasizing on PSBs in India. Hence, the above statements lead to the development of the following hypothesis.

H1: Customer satisfaction has a significant impact on CI in the banking sector.

Service Quality

Service quality is unanimously recognized as an important factor of a firm’s competitiveness (Parasuraman, Zeithaml & Berry, 1985, 1988). Generally, it refers to the degree of excellence of service performance (Zeithaml et al., 2011) which is consistently treated as a strategic weapon that leads to a satisfied customer base in the service industry (Karatepe, Yavas & Babakus, 2005; Ladhari, 2008), and therefore enables firms to gain a competitive advantage by offering superior SQ (Cronin & Taylor, 1992; Ghobadian et al., 1994; Ladhari et al., 2011).

Berry, Zeithaml and Parasuraman (1988) argue that customers evaluate SQ by comparing what they want or expect with what they actually get or perceive after getting it (service offerings). Similarly, Parasuraman et al. (1985, 1988) suggested that SQ can be measured by the comparison of customers’ expectations with their perceptions towards actual service performance based on five dimensions of SQ, namely, tangibility, reliability, assurance, responsiveness and empathy; thus, they proposed the gap model of SERVQUAL. On the other hand, Cronin and Taylor (1992) proposed the performance-based SERVPERF model as a criticism of the gap model of SERVQUAL due to ambiguity in its operationalization, when to measure it, either before or after getting the service (Caruana & Malta, 2002; Cronin & Taylor, 1992, 1994; George & Kumar, 2014). However, SERVQUAL approach is the most popular, and generalizes the measures to evaluate SQ across the world including the Indian banking sector.

Therefore, the irrespective of gaining popularity of SERVQUAL, such standard scale is questionable due to its operationalization and effectiveness in different cultural context.

Hence the researchers applied only performance based service quality model in the present study, and thus indentified the following five dimensions of service quality (SQ) as tangibility, reliability, assurance, responsiveness and empathy for assessing the banking service quality in Indian context with emphasize on public sector banks.

The Relationship between Service Quality Dimensions and Customer Satisfaction

In service marketing literature, several authors emphasized the relationship between SQ and CS and they found that the higher the SQ, the higher is the CS in the banking service sector (Caruana & Malta, 2002; Jamal & Naser, 2002; Lee & Moghavvemi, 2015; Shanka, 2012; Siddiqi, 2011; Sureshchandar et al., 2002). Regarding the relationship between the two popular phenomena, Parasuraman et al. (1988) argued that SQ and satisfaction are two different concepts but are closely related to each other in the service context. Further, Oliver (1993) recognized that SQ is an antecedent to CS and that it is an important tool to measure CS.

In recent years, several researchers in major Asian countries including India have emphasized the relationship between these two popular constructs in their local banking contexts and they found that SQ is a strong predictor of CS (Choudhury, 2014; Karim & Chowdhury, 2014; Krishnamurthy et al., 2010; Lenka, Suar & Mohapatra, 2009; Selvakumar, 2015; Siddiqi, 2011). Hence, the SQ dimensions, namely, tangibility, reliability, assurance, responsiveness and empathy, are the key predictors of CS in PSBs. The next section presents the hypotheses development.

The Relationship between Tangibility and Customer Satisfaction

The tangibility dimension of SQ can be outlined by tangible facets of servicescape in the banking sector, such as model equipment, physical facilities, well-dressed employees and visually appealing materials (Parasuraman et al., 1985; Sureshchandar et al., 2002). Therefore, it can be confirmed that there is a positive impact of tangibility on CS in the banking sector (Ananth, Ramesh & Prabaharan, 2011; Olorunniwo & Hsu, 2006; Sanjuq, 2014); such results are found in the Indian context as well (Choudhury, 2008; Krishnamurthy et al., 2010; Selvakumar, 2015). Based on the above arguments, the study proposes the following hypothesis.

H2: Tangibility has a significant impact on CS in the banking sector.

The Relationship between Reliability and Customer Satisfaction

In the service sector, the reliability dimension of SQ positively affects CS (Parasuraman et al., 1985, 1988) and this dimension can be considered to be the extent to which customers can be dependent on a firm’s promised service with accuracy (Ennew & Waite, 2013). Concerning the above relationship in the banking sector, various scholars confirmed that reliability has a significant impact on CS in the banking context, including India (Krishnamurthy et al., 2010; Lee & Moghavvemi, 2015; Shanka, 2012). Therefore, the above propositions lead to the following hypothesis.

H3: Reliability has a significant impact on CS in the banking sector.

The Relationship between Assurance and Customer Satisfaction

In general, assurance dimension of SQ refers to the employees’ knowledge, competence, courtesy and ability to inspire confidence in customers (Parasuraman et al., 1985). In financial and banking context, it is also related to the degree to which a customer feels secure in relation to banking transactions (Ennew & Waite, 2013) and it has been recognized that it has a positive and direct relationship with CS in the banking domain (Selvakumar, 2015; Shanka, 2012). Therefore, the study develops the following hypothesis.

H4: Reliability has a significant impact on CS in the banking sector.

The Relationship between Responsiveness and Customer Satisfaction

The responsiveness dimension of SQ refers to a firm’s willingness to help customers and its ability to provide prompt service (Kotler et al., 2009), and thus it is related to the timeliness of services (Parasuraman et al., 1985). It has been confirmed that responsiveness has a direct relationship with CS in the banking context worldwide (El Saghier & Nathan, 2013; Johnston, 1997; Krishnamurthy et al., 2010; Selvakumar, 2015) and therefore the research develops the following hypothesis in the Indian context.

H5: Responsiveness has a significant impact on CS in the banking sector.

The Relationship between Empathy and Customer Satisfaction

In service marketing, empathy dimension of SQ is primarily concerned with factors such as good communication, understanding of customer needs and friendly behaviour (Ennew & Waite, 2013), which are directly related to the provision of care and customized attention to customers (Parasuraman et al., 1985). Similarly, in the banking sector empathy dimension plays a vital role in satisfying customers in the retail banking industry (Krishnamurthy et al., 2010; Selvakumar, 2015; Shanka, 2012). Therefore, based on the above arguments, this research proposes the following hypothesis.

H6: Empathy has a significant impact on CS in the banking sector.

Methodology

Research Design

This research is based on a conclusive research where several hypotheses are used to prove the relationship between the variables. In this study, the dependent variable is CI which relies on the various SQ dimensions in banks, such as tangibility, assurance, reliability, responsiveness and empathy. Customer satisfaction plays a mediating role between CI and the various SQ dimensions in banks. The results were obtained through a structured questionnaire.

Sample Design

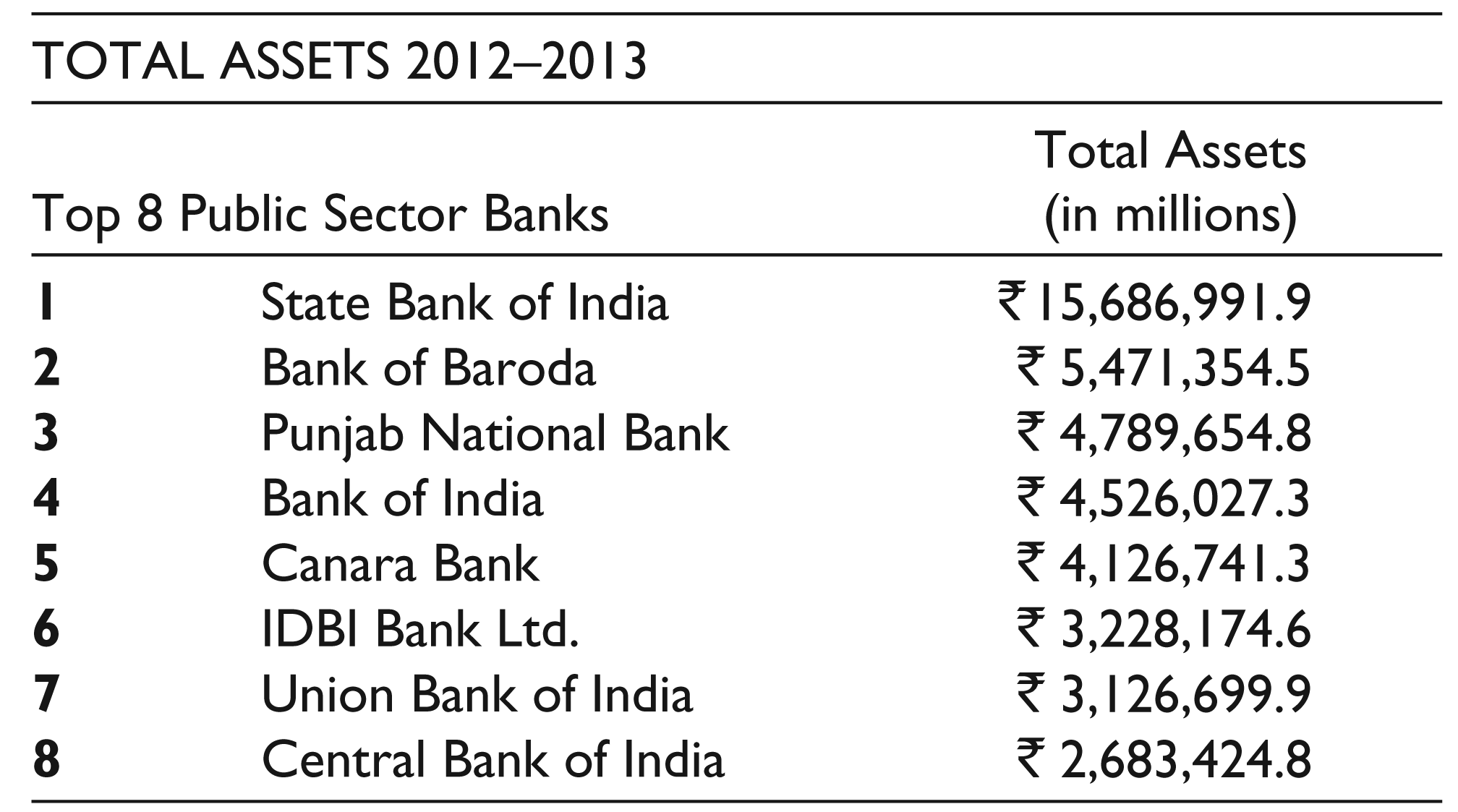

The data were collected from May 2015 to January 2016 in the National Capital Region (NCR), a major metropolitan area in North India, by using a purposive sampling technique. For the study, data were obtained from retail customers of eight major PSBs which are shown in Table 1. The sample includes 640 customers. More than 1,000 questionnaires were distributed to customers out of which only 64 per cent questionnaires were found to be suitable for the study. Respondents were selected from the customers who visited the sampled banks at different times.

Name of Selected Public Sector Bank on the basis of Total Assets

Measures

The language for collecting data was Indian English as it is also the official language of India. The constructed questionnaire consists of two sections. The first section covers various demographic profiles of the respondents: age, gender, educational qualification and their occupation. The second section covers the level of agreement and disagreement on various SQ dimensions (tangibility, reliability, empathy, responsiveness and assurance), CS and CI. Customers of the selected PSBs reported their perceptions on a 7-point Likert scale that ranged from 1 = ‘strongly disagree’ to 7 = ‘strongly agree’.

All the variables were derived from previous studies. ‘Tangibility’ was adopted from Keisidou, Sarigiannidis, Maditinos and Thalassinos (2013), Ladhari et al. (2011), Culiberg and Rojsek (2010) and Agarwal (2012). Items for ‘reliability’ were taken from Agarwal (2012), Culiberg and Rojsek (2010) and Sanjuq (2014), while for ‘responsiveness’ items were taken from Siddiqi (2011), Ladhari et al. (2011), Culiberg and Rojsek (2010) and Sanjuq (2014). Items for ‘empathy’ were adopted from Sanjuq (2014), Loke, Taiwo, Salim, Downe and PETRONAS (2011) and Agarwal (2012). Items for ‘assurance’ were adopted from Culiberg and Rojsek (2010) and Agarwal (2012). In addition, items for ‘image’ were adopted from Keisidou et al. (2013), Bloemer et al. (1998) and Ladhari et al. (2011), while items for ‘CS’ were adopted from Yee, Yeung and Cheng (2010) and Vera and Trujillo (2013).

Descriptive Statistics

Among the respondents, 52 per cent were from the youth population of India aged 20–35, while 22 per cent were in the age group 36–55; 67 per cent respondents were males, whereas remaining 33 per cent respondents were females. In terms of education, 39 per cent were graduates, while 28 per cent were postgraduates. This shows that majority of the respondents (67 per cent) were well educated. In terms of occupation of the respondents, majority of the respondents belonged to business class (45.6 per cent) and service class (33.3 per cent), while a very small proportion of respondents belonged to professional and other occupations in the study. The profile of respondents indicates they are young, educated and decently employed and understand the value of their responses.

Exploratory Factor Analysis

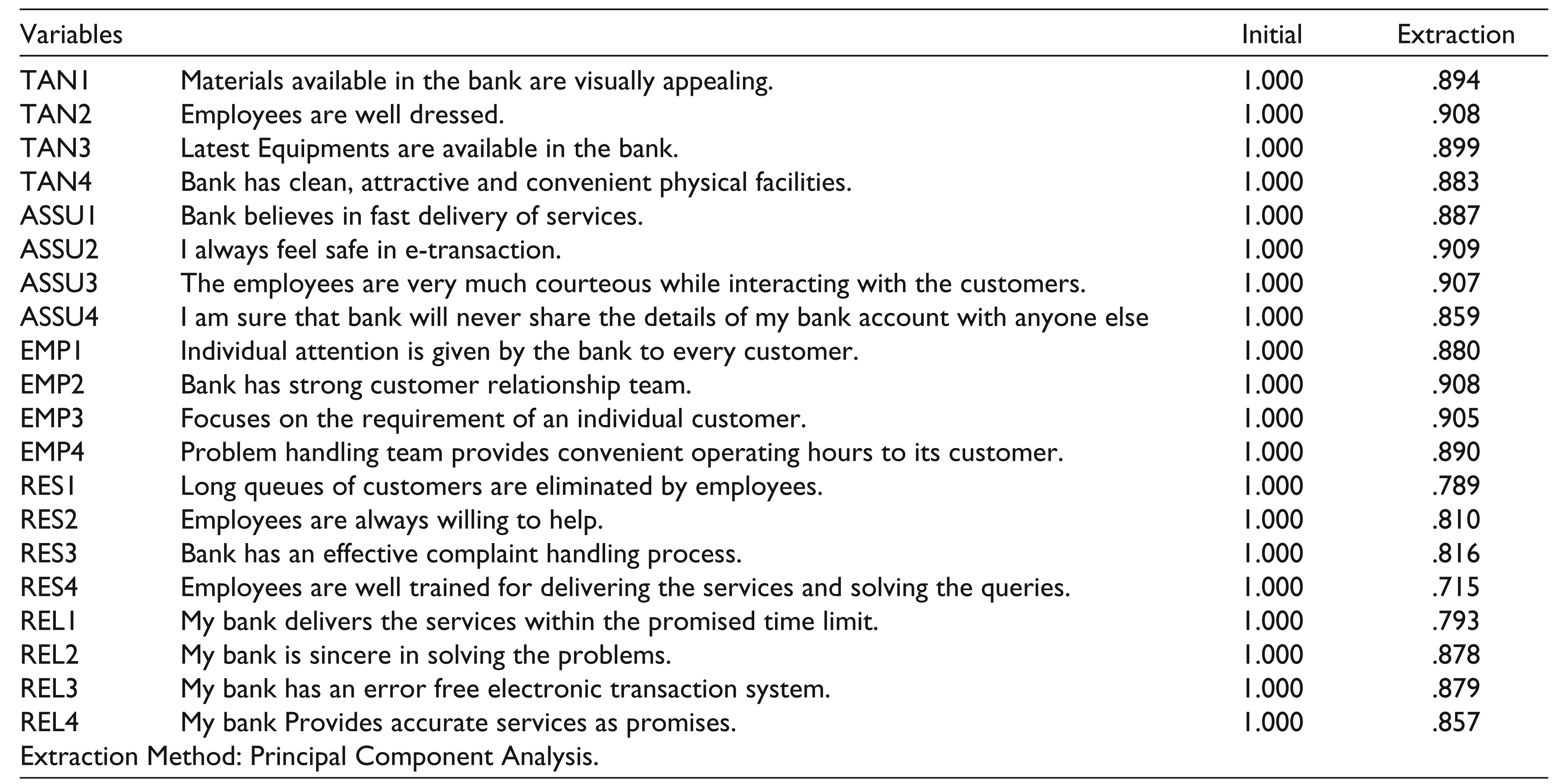

The validity of the constructs was evaluated through exploratory factor analysis (EFA) which was done using Statistical Package for Social Sciences (SPSS) on the 20 items to identify the underlying factors following the guidelines of Anderson and Gerbing (1988). The value for Kaiser–Meyer–Olkin (KMO) measure of sampling adequacy was 0.883, justifying the applicability of factor analysis on the sample. Bartlett’s test of sphericity value of 13,165.233 was also found significant (p = 0.001). Table 2 shows the final output of the factor analysis using principal components with varimax rotation. Factors with eigenvalue greater than 1 and factor loading greater than 0.50 have been retained for further analysis (Hair et al., 2015). All the five constructs were accepted, and totally 20 factors explained 86.332 per cent of the variance after varimax rotation.

Communalities

Reliability and Validity

In order to test the constructs’ reliability and convergent and discriminant validity of measures in the measurement model, confirmatory factor analysis model was estimated using AMOS through maximum likelihood procedure. The result indicates that the model fit was found acceptable up to the recommended level (Hair et al., 2015; Malhotra & Dash, 2011), that is, chi-square/df = 1.80, goodness-of-fit index (GFI) = 0.945, adjusted goodness-of-fit index (AGFI) = 0.930, incremental fit index (IFI) = 0.987, normed fit index (NFI) = 0.971, comparative fit index (CFI) = 0.987 and root mean square error of approximation (RMSEA) = 0.035.

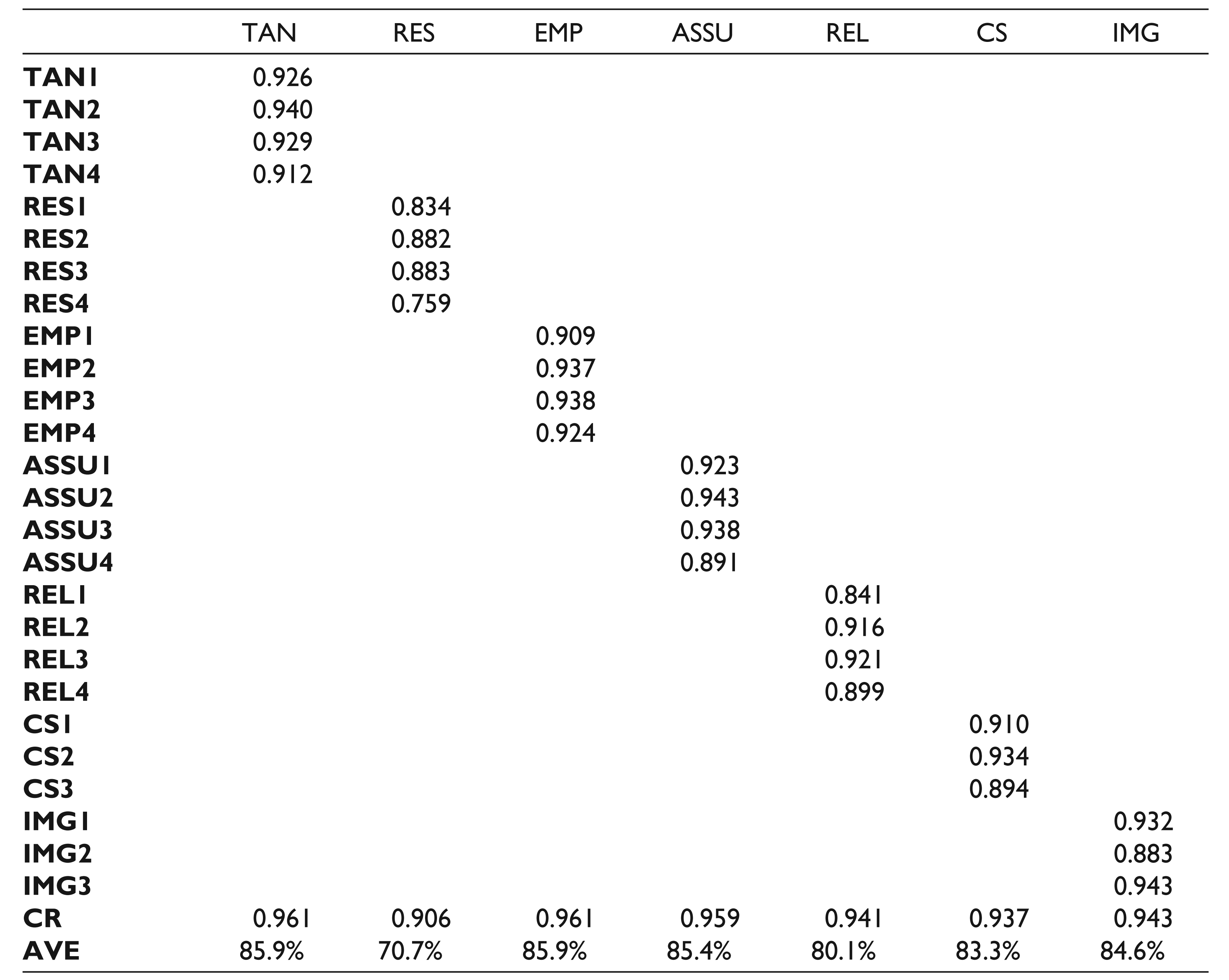

Table 3 displays standardized loadings (standardized regression weight), composite reliability and average variance extracted (AVE) for PSBs. The standardized loading ranged from 0.759 to 0.943 which is greater than the standard value of 0.70. The construct reliability and AVE are shown at the bottom of Table 3. The AVE estimates range from 70.7 per cent for responsiveness to 85.9 per cent for tangibility and empathy. All the values exceed the 50 per cent rule of thumb (Hair et al., 2015). Construct reliability ranged from 0.961 to 0.906, again exceeding the standard value of 0.70, suggesting adequate reliability (Hair et al., 2015; Malhotra & Dash, 2011).

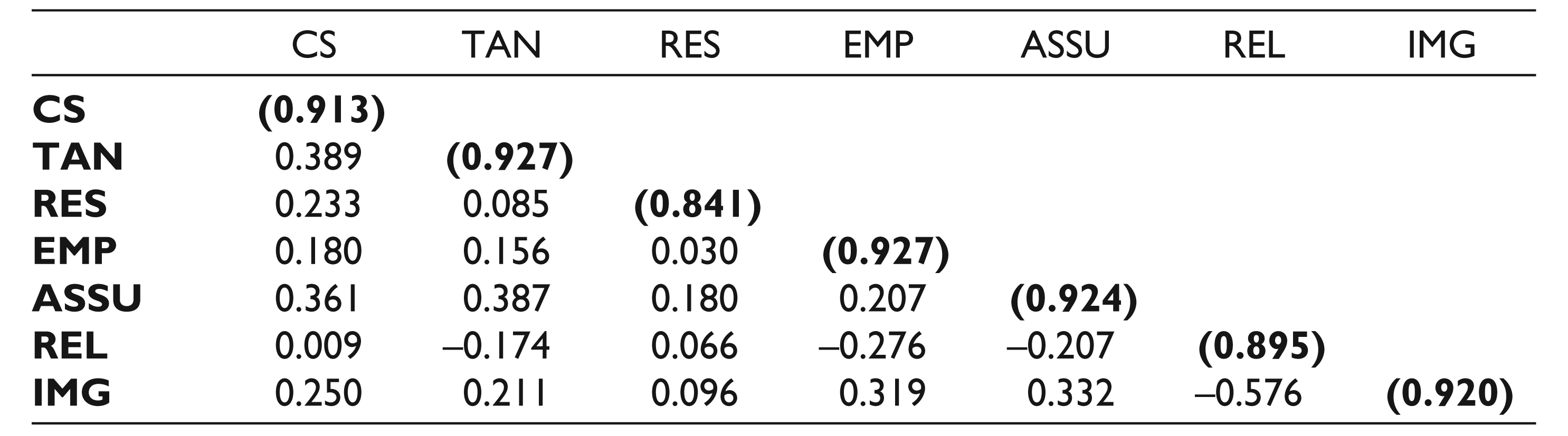

All the AVE estimates for each construct shown in Table 3 are greater than the corresponding inter-construct squared correlation estimates in Table 4. Therefore, this test indicates that there are no problems in the constructs’ reliability and convergent and discriminant validity in the measurement model of the PSBs (Hair et al., 2015).

Factor Loadings, Composite Reliability, Average Variance Extracted for Public Sector Banks

Comparison of Squared Correlation and Variable Extracted

Analysis of Structural Model

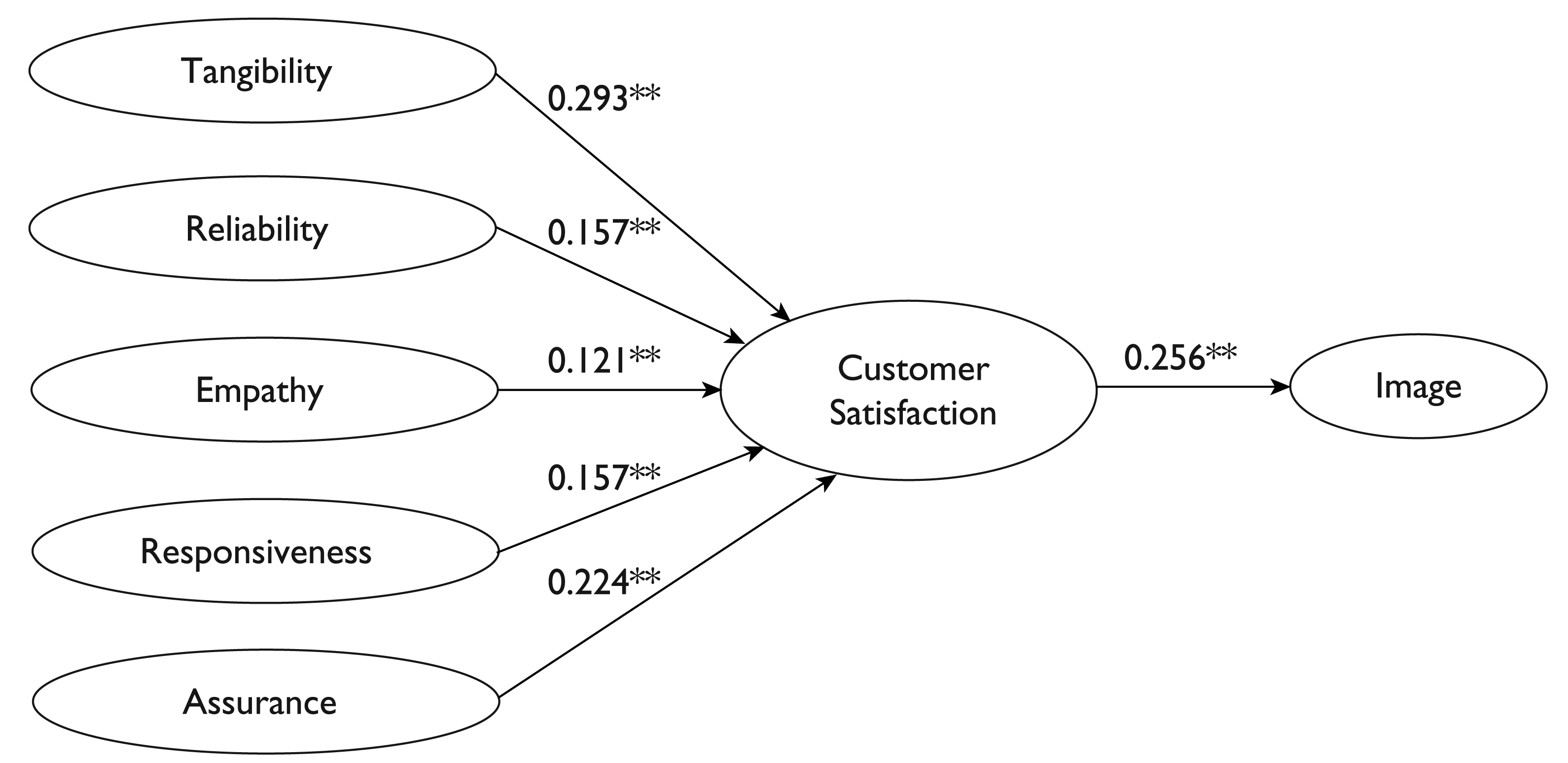

After analyzing the measurement model, the structural model can now be assessed and estimated by path diagram shown in Figure 1. The model fit was found to have adequate data (chi-square/df = 2.74, GFI = 0.923, AGFI = 0.904, IFI = 0.971, NFI = 0.956, CFI = 0.971 and RMSEA = 0.05). Overall, the model fit shows little changes from the measurement model fit because of the change in chi-square value and the difference of two degrees of freedom (Hair et al., 2015).

Results

As shown in Figure 1, the dimensions of SQ, that is, tangibility (β = 0.293), assurance (β = 0.224), reliability (β = 0.157), responsiveness (β = 0.157) and empathy (β = 0.121), positively and significantly affect CS. Customer satisfaction mediates the influence of service dimensions on image and shows a standardized regression weight of β = 0.256, which is found to be significant and shows that CS significantly influences CI.

Conclusion and Implications

The present article identified the dimensions of SQ in the Indian retail banking context using factor analysis, and examined the impact of the dimensions of SQ on CS, followed by the effect of CS on CI with an emphasis on Indian PSBs. The five dimensions of SQ, that is, tangibility, reliability, assurance, responsiveness and empathy, were recognized as predictors of CS in this study. Results confirmed that all the five dimensions of SQ have a signi-ficant relationship with CS in the Indian banking context. Hence, the above findings were strongly supported by the previous studies of Siddiqi (2011) and Selvakumar (2015). Furthermore, CS was found to significantly influence the CI; this result was previously found in the foreign banking context (Amin et al., 2013; Ladhari et al., 2011). Hence, the present article attempted successfully to fulfil the research gap in the literature of service marketing, especially in the Indian banking context. The notion is that higher CS leads to higher reputation and improved image in the banking sector; therefore, a favourable image directly influences the bank customers to revisit and spread positive word of mouth, and is considered one of the key strategic marketing factors which acts as a source of differentiator in the standardized nature of the Indian banking sector. Moreover, the study also revealed that positive bank image can be enhanced indirectly by offering superior quality of services by banks via higher CS. Therefore, PSBs should focus more on corporate brand-building activities through modern bank outlets, financial performance, etc. accompanied by more modern media vehicles than their major private peers, such as ICICI, HDFC and so on, in order to retain customer base and/or minimize the switching behaviour of the bank population.

In addition, ‘tangibility’ and ‘assurance’ dimensions were found to be most important predictors of CS among all five dimensions of SQ in PSBs. It is clear that PSBs have emphasized more on banks’ tangible facilities, such as modern looks, equipment and modern infrastructure, with the aim of building positive bank image in the minds of target customers as a differentiator factor in the modern era of competitive retail banking in India. Therefore, such findings are supported by previous studies of scholars such as Olorunniwo and Hsu (2006), Choudhury (2008) and Sanjuq (2014).

‘Assurance’ is the second most important aspect of SQ which influences CS and this dimension deals with the human aspects of SQ, that is, knowledge and courtesy of employees and their ability to communicate trust and confidence (Parasuraman et al., 1985). In addition, Donthu and Yoo (1998) recognized that individualist customers would expect service providers to show respect and care towards them, and thus individualist customers are more focused on assurance aspect which leads to belief in and respect for the service provider. Similar views were also found in this study, as most of the Indian population consists of youths and they possess their own independent thoughts or actions. The notion is that PSBs are more focused on the assurance aspect of SQ, and thus they are more proficient to create trust and confidence among the youth segment rather other stakeholders in the Indian banking industry. Hence, such findings are supported by Donthu and Yoo (1998), Shanka (2012) and Selvakumar (2015).

On the other hand, reliability is the ability of giving consistent performance by a service provider to the customers. It also relates to the technical aspect of SQ; for example, now banks have an error-free electronic transaction systems such as ATMs and e-banking. It helps in creating a safe image of the banks in the minds of the customers, such as banks are sincere in solving problems and keep their promise of providing accurate service. The study found a positive impact of reliability on CS and supported the opinions of scholars such as Krishnamurthy et al. (2010) and Shanka (2012).

Responsiveness is the willingness or readiness of employees to help customers. It is the most important factor in people-based industries including tourism, hospitality and banking (Lee, Lee & Yoo, 2000). The study found a positive impact of responsiveness on CS and supported the opinion of Johnston (1997) and Krishnamurthy et al. (2010).

Finally, the dimension empathy also showed a positive effect on CS and thus supported the literature of Krishnamurthy et al. (2010) and Shanka (2012).

However, some limitations were noticed. The study is based on Indian PSBs in the NCR and did not examine the private sector banks, and therefore the research findings cannot be generalized in other banking sectors, such as private and foreign banks in India. Despite such limitations, this research model can be applied to other parts of the nation in the retail banking context. Thus, future research should focus on private sector banks and foreign banks in India using the present model in order to confirm the validity of the research findings in the overall Indian context. Last but not least, the present findings revealed that improvement in SQ dimensions will increase CI through CS in the Indian banking sector, and thus such a research model should be validated to other mass service sectors, such as tourism and hospitality, medical and communication, in the Indian context.