Abstract

This study’s main objective is to assess the relative importance of fiscal and monetary policies on the Asia-Pacific Economies. We have empirically investigated both the original St. Louis equation and its expanded version to study the comparative relevance of one over the other. Our empirical results indicate that both monetary and fiscal policies are essential in promoting economic growth. In both models, monetary policy is more effective than fiscal policy. In the expanded St. Louis model, exports, exchange rate and inflation variables substantially impact gross domestic product than the conventional monetary and fiscal measures.

Introduction

The monetary and fiscal policies are twin policy frameworks that are available to the government worldwide to promote socio-economic growth and stability in society. The monetary policy leverages money supply as a facilitator of credit creation, price stability and economic development, whereas the fiscal policy utilizes different forms of government expenditure programmes and taxation policies to influence aggregate demand and economic growth. Each of the policy frameworks has multiple instruments and objectives. The transmission mechanism of these policy instruments in producing desired results differs significantly. There has been unanimity among academia on the vital importance of both the policy frameworks in promoting socio-economic growth, but there is a big question mark around the relative potency of one versus the other. The aim of this study is to empirically test out the relative importance of monetary policy over fiscal policy in the Asia-Pacific context.

Fiscal and Monetary Policies Settings in Asia Region

The effectiveness of fiscal and monetary policies is widely debated in the macroeconomic literature. While Keynesian school focuses on the multiplier effect of fiscal policies in government spending and tax cuts, the monetarist completely disagrees with the Keynesian view that the role of government in the economy is minimal. The monetarist places greater importance on money and monetary policy over its fiscal counterpart in influencing economic growth.

The Asia-Pacific is a large and diverse region. Social, economic and cultural differences are stark. Irrespective of their differences, one thing that is common is that they are swift in implementing prudential macroeconomic policies to come out of the past crisis. During the period of study, the region has passed through the severe impact of the global financial crisis. Exactly 10 years prior to this, in 1997–1998, the region had gone through a severe meltdown as well. The region is going through a pandemic exactly after a decade of the global financial meltdown. Post-crisis fiscal stimulus packages have been instantaneous, and recovery has been faster than the rest of the world. This seems to give an indication that fiscal stimuli work well in the region through empirical pieces of evidence that suggest otherwise (Tang et al., 2010). Government fiscal stimulus programmes encourage businesses to restart production activities and help to generate employment and income for the consumer. Tax rebates and concessions increase disposable income and promote higher consumption.

Post-crisis fiscal stimulus size and structure have been big and bold in the region. The Republic of China announced a fiscal rescue package of 13% of gross domestic product (GDP). These were invested in infrastructure, education and health sectors. India’s investment close to around 3.5% of the GDP in high priority infrastructure and social sectors programmes can directly place income in peoples’ hands. Indonesia and the Republic of Korea invest 1.5% of GDP each (Hur et al., 2010). These measures were supplemented by various tax cuts and direct cash transfer benefits to bring back the economy on track. Over the analysis period, government expenditure as a per cent of GDP is hovering around 14.5%. There is a wide variation within the region in terms of government spending to GDP ratio. While countries like Bangladesh, Cambodia, Pakistan, the Philippines and Pakistan share is at 7%, the average for the rest of the countries is at 13% (Asia Development Bank, 2020). This is an indication that government plays a significant role in vitalizing various sectors of the economy to promote socio-economic stability.

The role of monetary policy in facilitating growth and stability is no less in the region. Despite the different monetary policy frameworks adopted by different countries in the region, one thing that is common is a strong focus on inflation management. Over the period of analysis, the regional inflation average of around 4.3% gives an indication that the region has enjoyed a moderate level of inflation post-Asian financial crisis (Asia Development Bank, 2020).

The monetary transmission mechanism is complex, unlike fiscal policy measures. When monetary authority implements a monetary measure, it works in two stages. In stage one, commercial banks first absorb signals from the central bank and in stage two, the banking system passes signals to the real sector of the economy. Rangarajan (2020) calls this as the ‘inner leg’ and ‘outer leg’ of the monetary transmission mechanism. Post-Asian financial crisis sustained accommodative monetary policy has kept the interest rate at an extremely low level. The real interest rate for half of the countries is near zero or negative (Asia Development Bank, 2020).

A significant part of Asia’s economic upliftment is attributed to its high level of trade integration with the rest of the world (Brooks, 1998). Asian financial crisis, in particular, showed the region the importance of exchange rate management policies to promote a better growth path. The external asset and liability ratios rose for all Asian countries between 1990 and 2009 (Morgan, 2013). In this study, we aim to look at the impact of key monetary and fiscal instrument on economic growth.

Literature Review

Monetary policy mostly consists of macroeconomic policies that are governed by the central bank of the country. It includes focus on the management of money supply and managing the interest rate. Some of the instruments that are used to manage the monetary policy are open market operations, discount rate and reserve requirement, and the primary goal is to maintain price stability. Fiscal policy is the policy adopted by the central government of the country to stabilize the economy. Some of the instruments that are used by the central bank are efficient collection and allocations of taxes and government expenditures. Both policies are effective in inflation management and efficient economic performance. These two are the most used macroeconomic policy instruments, and economists often debate about the supremacy of the two. There are various theories that had been supporting the importance of one over another for a long time. Keynesians economists argue that fiscal policies such as an increase in government spending and a decrease in taxation will increase the demand, and that will have a positive impact on the economy. At the same time, Keynesians sustained that monetary policy would necessarily but not strongly help stabilize an economy over the short-run period. The other economists, mainly monetarists, maintained that fiscal policies are not necessary. They maintained the superiority of monetary policies.

‘St. Louis Equation’, as published by Andersen and Jordan (1968), has been a subject of great debate. They used quarter-to-quarter data to estimate a reduced form equation referred to in the literature as the St. Louis model, found monetary actions in the USA more important than fiscal actions. Later, the equation was subject to many counter studies that focused on many challenges with data definitions, reduced form equations and time period of study. There had been many researchers like Arestis and Sawyer (2004) and Senbet (2011) who validated the same finding for the USA. Moayedi (2013) found that in Iran’s case, monetary policy is much less effective than fiscal policy in stimulating permanent economic growth and the findings were converse to what scholars found when examining Western countries. Tadesse and Melaku (2019) analysed the impact of monetary and fiscal policies on economic growth in Ethiopia. They found an empirically significant relationship between growth and monetary and fiscal policies. Both monetary and fiscal policies have a positive impact on economic growth in Ethiopia. Another interesting finding was that fiscal policy was found to be more effective in inducing real GDP. Ahmed and Johannes (1984) point to the existence of bias in the model and find that it does not accurately describe the impact of monetary and fiscal policies. According to Batten and Thornton (1986), the three major critiques are the omission of relevant exogenous variables, simultaneous equation bias and failure to identify appropriate measures of monetary and fiscal policies. Other critiques include heteroskedasticity problem, endogeneity problem and the use of the Almon lag procedure. There are three more interesting variations of the equation that focused on trade, economic sectors and tourism factors as an extension to the model and equation. Batten and Hafer (1983) criticized the A–J equation for not capturing international trade; hence they included export. Nwaogwugwu and Evans (2016) using vector autoregression techniques analysed the impact on five sectors of the economy such as agriculture, building, services, industry and wholesale. It was found that the monetary actions have a direct and measurable significant impact on three sectors such as agriculture, services and wholesale. At the same time, the impact magnitude was different for all three sectors. Vanegas (2018) tested for the first time the link among economic growth, tourism development, monetary policy and fiscal policy, and visited the monetary versus the fiscal policy debate in the case of Nicaragua.

Some studies on Asian countries that have been done for Bangladesh, India, South Korea, Malaysia, Pakistan and Thailand and others carry mixed results on the relative effectiveness of fiscal and monetary policy actions. Some of the studies found that the effect of monetary actions on economic activity was stronger than fiscal actions. However, the opposite was established by other studies. Chowdhury (1986a, 1986b), Hussain (1992) and Fatima and Iqbal (2003) found that the effect of monetary actions on economic activity was weaker than those of fiscal actions.

Objective

As one can see above, the empirical evidence around the comparative supremacy of monetary policy vs fiscal policy is far from a settled debate in the field of macroeconomics. Empirical work in the Asia-Pacific context is relatively limited. As a part of this piece of research, we have taken all the major 16 countries in the region and 14 years (2005–2018) data to evaluate the debate after a gap of nearly 50+ years. One of the major criticisms of the St. Louis model was its oversimplified representation of monetary and fiscal measures. The model assumed narrow money (M1) as a proxy for monetary policy and government expenditure (expenses–revenue) as representation for fiscal policy by ignoring many other factors like exchange rate, interest rate and inflation and trade openness stimulant of growth and development. To cater to these concerns, we have tried to test both the original version and expanded equation specification by including various exogenous variables like trade competitiveness, inflation, exchange rate and interest rate variable in the model.

Methodology and Data

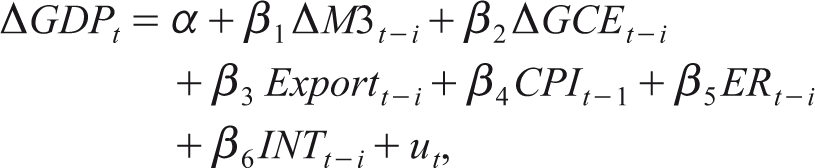

To estimate the impact of fiscal and monetary actions on national growth, Andersen and Jordan (1968) proposed a simple equation that regresses quarter-on-quarter change in gross national product on quarter-on-quarter changes in the money stock and various alternative measures of fiscal actions covering government expenditure (E), government revenue receipts (R) and budget surplus/deficit (R − E). This is otherwise known as the famous St. Louis equation. This model was simple, easy and intuitive and subjected to many criticisms as to its findings contrary to conventional knowledge of that time. One of the major criticisms came from Blinder and Solow (1974) and Modigliani and Ando (1976), which highlighted the potential specification bias as other regressors were excluded from the model.

We have not seen much work done in this space in the Asia-Pacific region hence an attempt is made to test out the original equation and consider the major criticism by including more monetary and fiscal variables into the original model specifications. All the used fiscal and monetary measures are in the level form and are non-stationary in nature. Firstly, these series are converted into logarithmic form before taking their first differences as applied by Matthews and Ormerod (1978).

The original model is estimated as:

where, the endogenous variable is real GDP, exogenous variables are money (M3) and government consumption expenditure (GCE). The delta indicates the first difference.

Following criticism from Blinder and Solow (1974) and Modigliani and Ando (1976), Batten and Hafer (1983) introduced export variable into the model. Trade openness has substantially contributed to the region’s economic growth. Keeping this in mind we have included export and exchange rate as proxies for fiscal and monetary actions as well. Post-Asian financial crisis, price management has been a key activity for the central banks hence both inflation and interest rates are used in the model as well.

where trade openness is presented by export (Export), trade competitiveness proxied by exchange rate (ER), two monetary variables price and interest rate (INT) are used in the model.

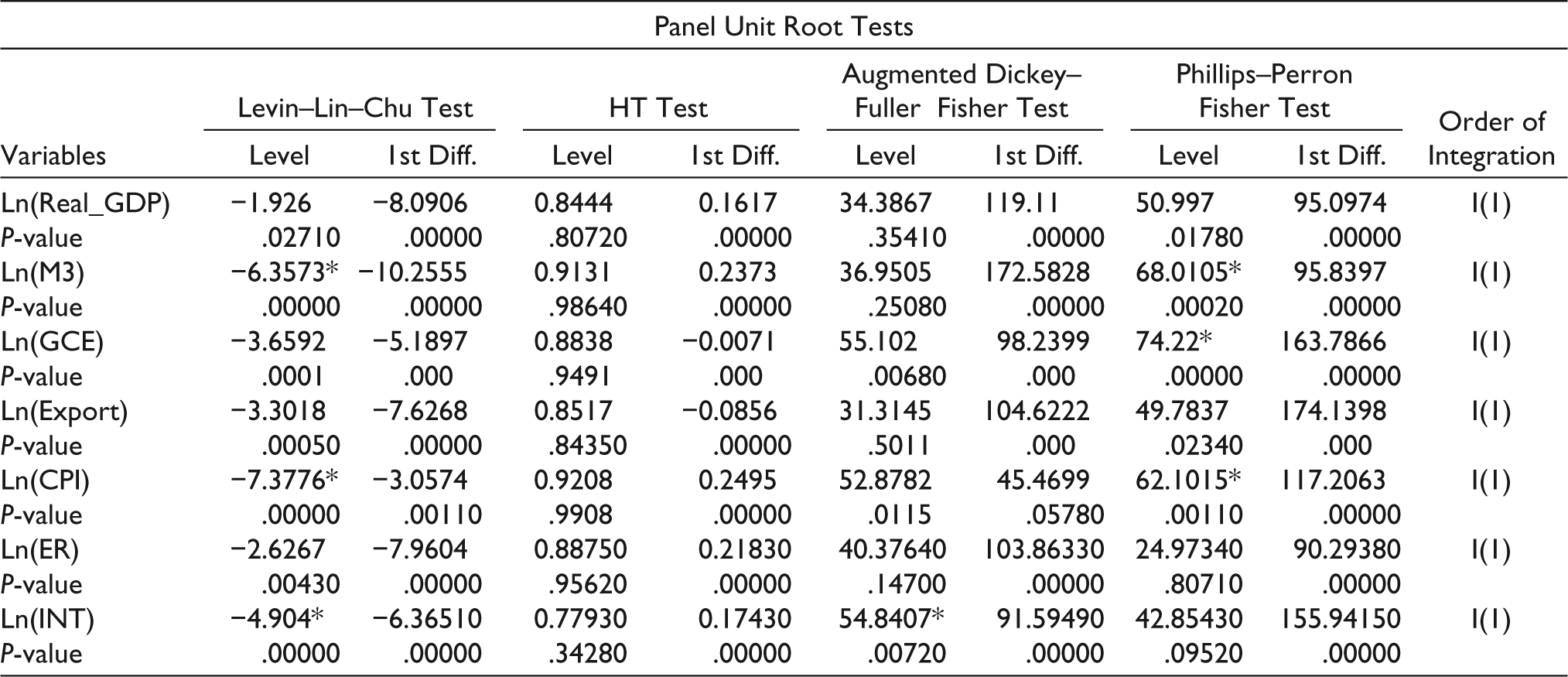

The study uses data from 2005 through 2018 across 16 countries in the Asia-Pacific region. Since unit root feature of some of these variables can create problems in drawing statistical inference, we must test the time-series properties of used data series. Also, the stationarity of time series model is a key characteristic that has been studied through a panel series of stationarity tests like Levin–Lin–Chu (LLC) test (Levin et al., 2002), Harris–Tzavalis (HT) test (Harris & Tzavalis, 1999) and Augmented Dickey–Fuller (ADF)/Phillips–Perron (PP) Fisher-type test (Choi, 2001). We have used panel regression to estimate the model.

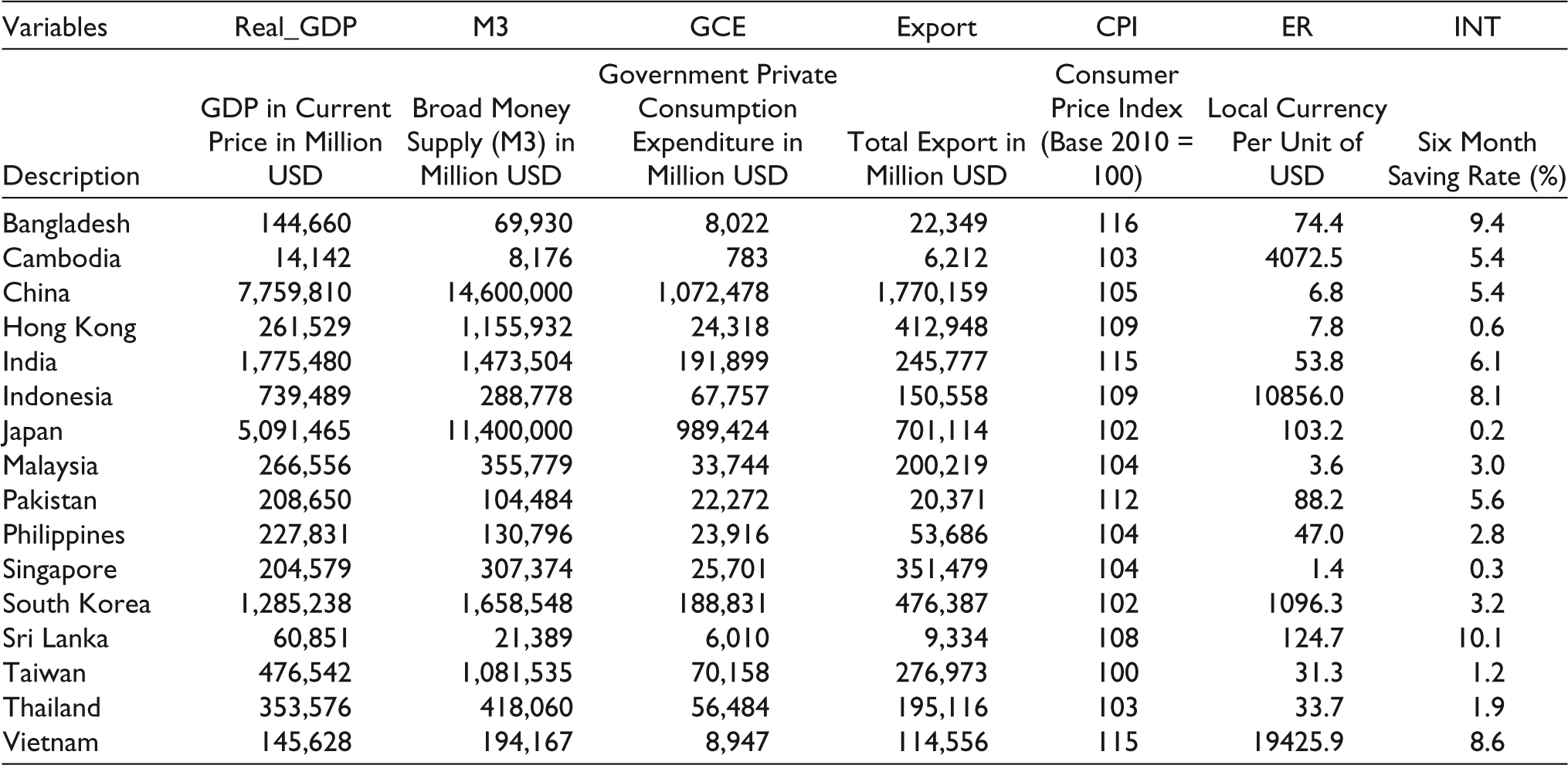

The study covers 16 countries covering Bangladesh, Cambodia, India, Indonesia, Malaysia, Pakistan, Philippines, Sri Lanka, Thailand and Vietnam. We have used annual data from 2005 to 2018, collected from the Asian Development Bank database. Original data appear in local currencies, and we have used the annual exchange rate to convert the data series into US dollars. Real GDP is computed by deflating nominal GDP to the consumer price index (CPI). The exchange rate is expressed in terms of local currencies per unit of the US dollar.

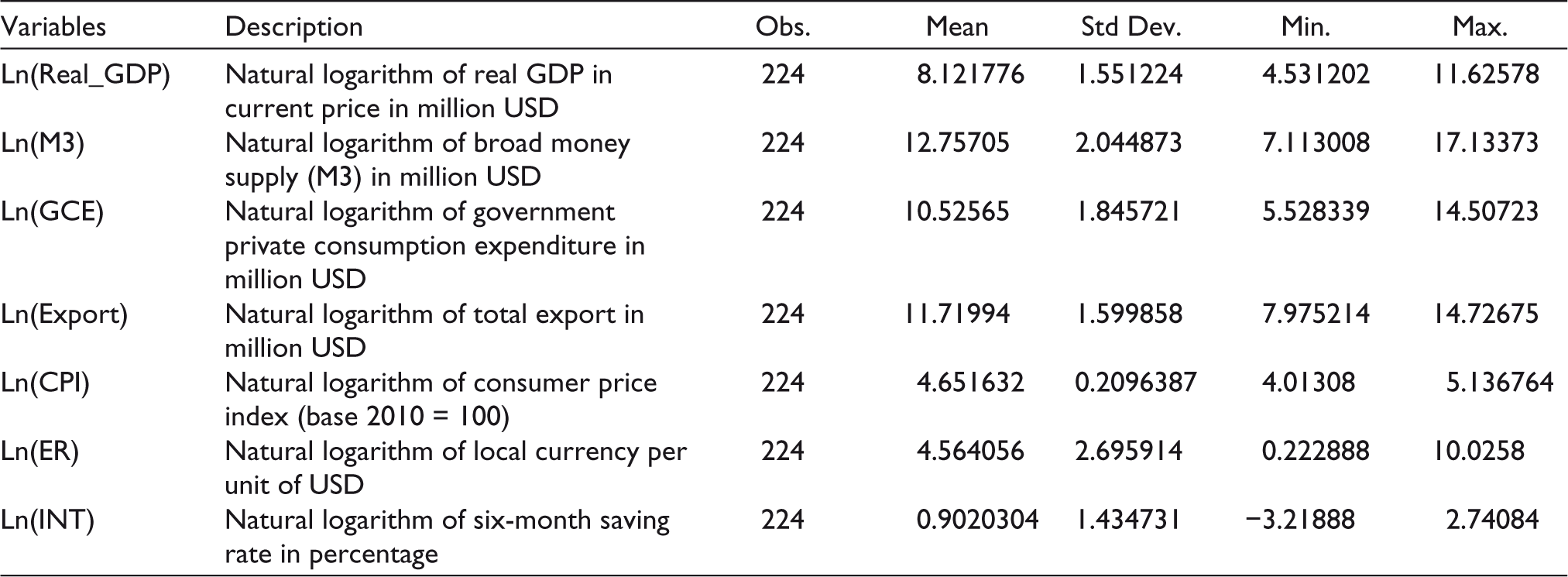

A summary of the key variables is presented in Table 1.

The Mean Statistics of the Main Variables Used in the Model

Drawing inference from non-stationary variable at times can be spurious. In this analysis we have taken first difference of natural logarithm of the variables. Table 2 provides the list of variables used in the study, their description and basic statistics.

Descriptive Statistics of the Main Variables Used in the Model

Results

As mentioned earlier, before running the panel regression model, it is essential to test the stationarity property of all the fiscal and monetary policy variables used in the study. We have used a variety of stationarity tests covering LLC test (Levin et al., 2002), HT test (Harris & Tzavalis, 1999) and ADF/PP Fisher-type test (Choi, 2001).

As shown in Table 3, all the series are non-stationary by level. We have performed the unit root test using six-unit root test methods and rejected the null hypothesis by confirming that they are integrated at Order 1.

Panel Unit Root Test Performance Across Different Unit Test Methods for Key Macro Indicators Used in the Study

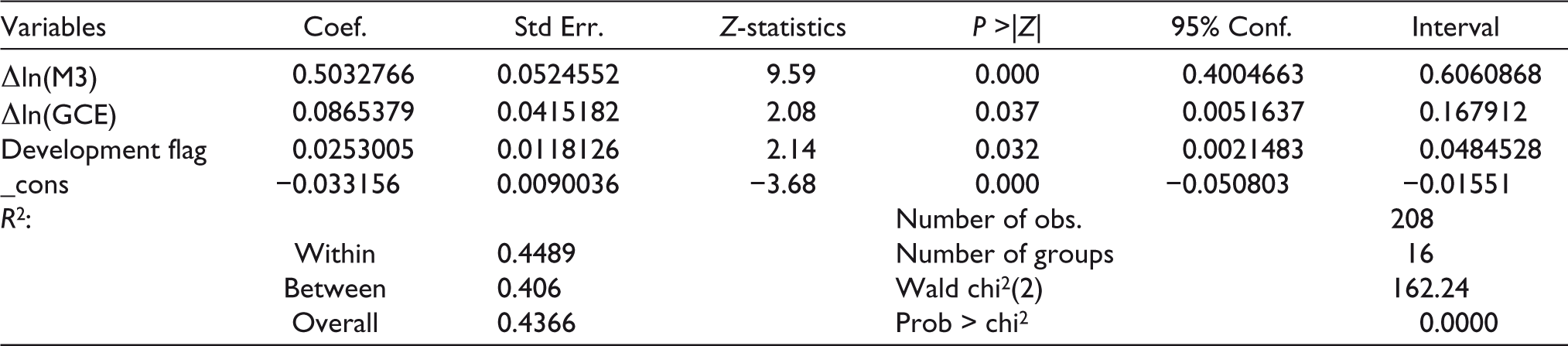

After checking the stationarity test, we have regressed (Equation 1) broad money (M3) and GCE over real economic growth. Since there is a wide socio-economic difference across countries in the region, we have introduced a dummy to indicate the country’s development status and its impact on the overall relationship. While China, Japan, Hong Kong, Singapore, Taiwan and South Korea are considered developed, the remaining ones are regarded as developing countries.

Results in Table 4 show that both the monetary and fiscal variables are positively contributing to economic growth. Both the variables are statistically significant at 1% and 5%, respectively. The elasticity of money supply (M3) to real GDP is at 0.50, whereas for GCE is at 0.09, indicating the importance of money supply over fiscal measures in driving national income growth, which is in line with Andersen and Jordan (1968). The low overall Model R2 indicates that it is important to include both lags and other exogenous variables to improve the overall fitment of the model. The development status of the country is statistically significant as well.

Estimated Results for Equation 1

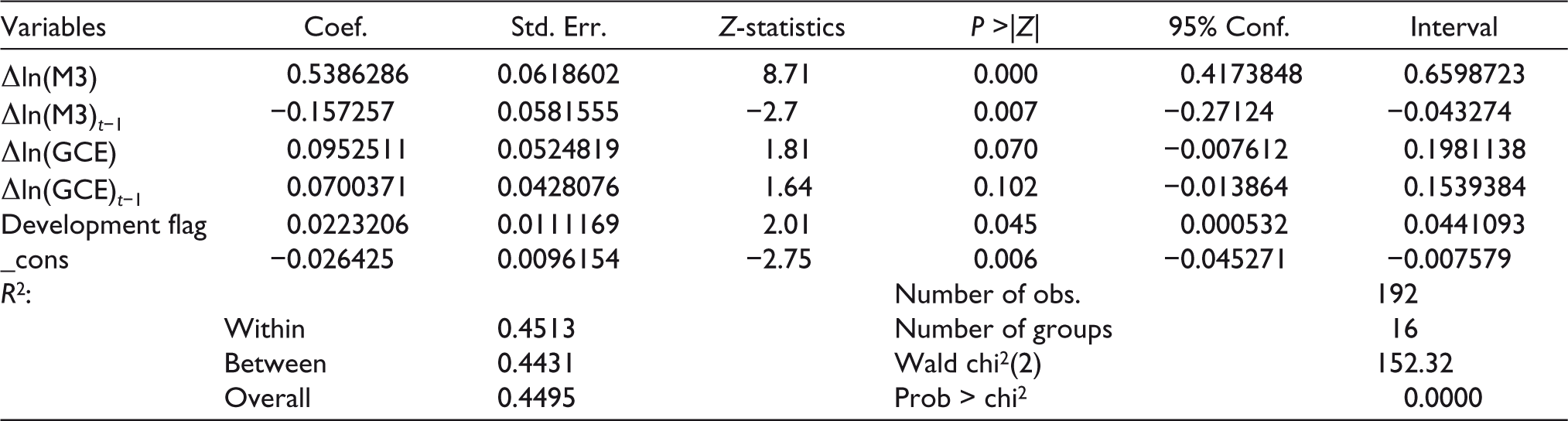

We have re-estimated Equation 1 by introducing current and one-year lag variables and presented the results in Table 5. The introduction of lag variables neither alters the overall model results nor significantly impacts the magnitude and direction of the current monetary and fiscal attributes. Though significant at the 5% level, the money supply lag variable carry a negative sign, whereas the fiscal policy proxy is statically insignificant.

Estimated Results for Equation 6

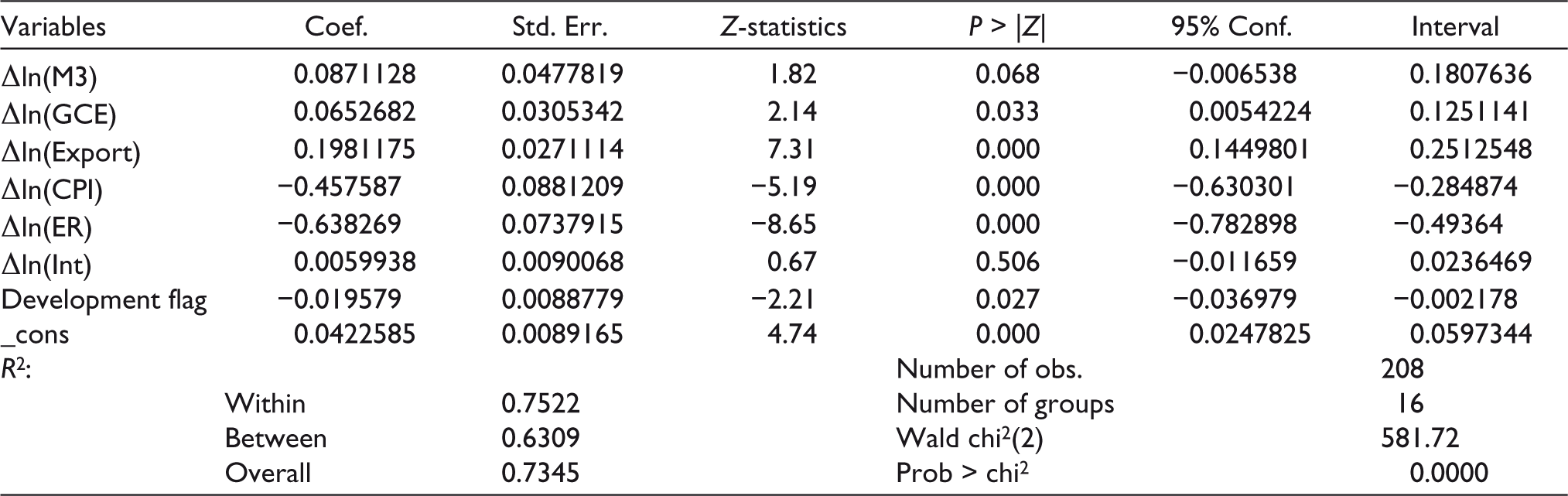

As mentioned earlier, one of the most significant criticisms of the St. Louis equation was the exclusion of other exogenous variables. The Asia-Pacific follows an export-led growth model. Keeping the importance of the trade openness, we have included export (Export), the exchange rate (ER), inflation (CPI) and interest rate (INT) as other exogenous alongside money supply (M3) and GCE. The introduction of other exogenous variables produced exciting results, which are provided in Table 6.

Estimated Results for Equation 2

The rest of the variables covering broad money, government expenditure, export, inflation and exchange rate are significant and directionally appropriate from the expanded form of the equation, except interest rate. The key difference between the output from the more straightforward St. Louis equation and its extended version is, money supply and government spend continue to play a critical role in determining economic growth, though their relative importance lags export, exchange rate and inflation. The elasticity of broad money and government expenditure is 0.09% and 0.07%, respectively.

Trade openness proxied by export as a percentage to GDP turned out to be an important explanatory variable for economic growth. With an elasticity of 0.20, this is positive and significant, re-enforcing the importance of the export led growth model in the Asia-Pacific region. This finding is consistent with Zarra-Nezhad et al. (2014), Keho (2017), Evans and Kelikume (2018) and Trejos and Barboza (2015).

From past three decades, emerging Asia has been soaring in consumption and growth. Moderate inflation induces production activities, whereas low inflation key to sustain consumption. In the current model, we observe a strong and negative relationship between inflation and economic growth. The results suggest that central bank focus on reducing inflation will further spur economic growth in the region. Current findings are supported by observations from Mallik and Chowdhury (2001), Azam Khan and Khan (2018), Thanh (2014) and Khan and Senhadji (2001).

A stable and favourable exchange rate regime is key to trade engagement. Not surprisingly, the study observes a strong and negative relationship between the two which means currency depreciation has a detrimental effect on economic growth by adversely affecting international competitiveness. Ha and Hoang (2020) and Schnabl (2009) support the theory of a stable exchange rate regime, and less exchange rate volatility promotes growth.

When we look at the nominal interest rate and Real GDP relationship, the coefficient is positive but statically insignificant. Post financial meltdown, there has been a sustained reduction in the interest rate in the Asia-Pacific region and the world in general. In fact, for several markets, the real interest rate is close to zero or negative in the region. Bosworth (2014) looked into G7 and 22 Organisation for Economic Co-operation and Development countries and found only a weak relationship between interest rates and economic growth indicators. These results are in line with what we are observing for the Asia-Pacific region.

Conclusion and Policy Implications

The Asia-Pacific region is emerging as the most vibrant economic engine propelling the world economy. The successive financial crisis, regular natural disasters and current pandemic have never been deterrents for growth. Asian governments are continuously adopting conducive fiscal and monetary policies and proactive socioeconomic reform measures to stay competitive. Over the past decade, there has been an intense focus on digitization and innovations to generate new source of revenue.

For the governments to be more effective in policymaking, it is important to know what policy measure works in favour of economic growth. Keeping this in mind, we have revisited the St. Louis model to evaluate the comparative effectiveness of monetary and fiscal policies in influencing economic growth. We have used data from 2005 to 2018 across 16 countries in the Asia-Pacific region to conduct this analysis. Given the nature of multi-country and time series observation, we have flowed a simple panel modelling approach for the analysis. We have tested the original and expanded model specifications to test the impact of all possible fiscal and policy measures on economic growth.

Interesting to observe that both monetary and fiscal policy instruments play a significant role in promoting growth. The simpler specification monetary policy has the upper hand over its fiscal counterpart in impacting economic growth. The results from the expanded form of the model covering other exogenous variables do not change the results. In addition, trade openness, ER and inflation play a critical role in promoting growth. Interest rate seems not to work as a strong monetary policy instrument in influencing demand and growth. Trade openness, ER and inflation seem to play a more significant role than money supply and government expenditure programmes.

To sum up, for the region to continue to lead in the growth front, the governments need to use fiscal and monetary policy measures judiciously. It is not one vs the other, but the policymakers should recognize the importance of every policy instrument and appropriately manage and leverage the same for optimal macroeconomic stability and growth.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.