Abstract

This article investigates the impact of the chief executive officer’s (CEO’s) power on research and development (R&D) expenditures in Saudi Arabia. Mainly, it studies the influence of CEOs’ power (ownership power, structural power and expert power) on their risk-taking behaviour. Empirically, we used a panel model with data from a sample of 60 Saudi firms listed from 2016 to 2019. We developed five models to examine both the direct and moderating effects of the power indicators on R&D expenditures using OLS regression. Findings demonstrate that Saudi firms promoting insider CEOs with short tenure and no ownership are more innovative. These results have great implications for researchers and investors to understand what kind of power they should consider when selecting leaders to carry out innovation plans and thus ensure long-term firm growth.

Introduction

Competitive and dynamic environment requires firms to maintain a constant flow of innovations (Hamel & Prahalad, 1994). Moreover, the decision to invest in innovation is even more important insofar as it directly affects the survival of many companies (Aghion et al., 2013). Several studies demonstrate that R&D is one of the primary activities leading to firm innovation (Ahuja et al., 2008; Carboni & Medda, 2020). In this context, Curtis et al. (2020) concluded that R&D expenditures positively affect future firm profitability and that this association weakens over time. Nevertheless, the R&D investment remains very risky, insofar as R&D projects require significant resources, which is likely to negatively affect its current performance, and their benefits remain unpredictable (Naaman & Sun, 2022; Sheikh, 2019). De Massis et al. (2018) suggested that the decision to increase R&D activities induces an increase in the risk of bankruptcy. Thus, risk-taking has often been proxied in business research by R&D expenditures (AlHares et al., 2018).

Considering the CEO as the most important person responsible for critical decisions, many studies investigated the association between CEO characteristics and R&D expenditures (Barker & Mueller, 2002, Harymawan et al., 2020; Hsu et al., 2020). Most of these studies are based on the upper echelon theory (UET), initiated by Hambrick and Mason (1984) and updated by Carpenter et al. (2004) and Hambrick (2007). The UET considers that the top management team (TMT) has the power to set the firm’s direction, and consequently strategic decisions and outcomes would be affected by the top managers’ values, ideology, religious beliefs, cognitions, age, gender, experiences and risk preferences. However, the theoretical and conceptual review conducted by Saidu (2019) showed that few studies have explored the concept of CEO power, particularly in third-world countries. Moreover, according to Naaman and Sun (2022), studies investigating the consequences of CEO power led to mixed results. In this study, we tried to partially fill this gap by investigating the impact of CEO power on R&D expenditures in the Saudi context. This study is all the more important as Saudi Arabia has climbed up, according to the Global Innovation Index (GII), from the 66th rank in 2020 to the 51st rank in 2022. 1

In this article, we aim to examine how R&D expenditures vary in relation to the CEO’s power (ownership power, structural power and expert power). Theoretically, this study helps to examine the impact of different CEO power indicators on risk taking as proxied by innovation costs and provides real implications by identifying the role of executives’ strengths in innovative companies in the Saudi context.

The article is structured as follows: first, a literature review is conducted on the relationship between CEO power and R&D expenditure, and hypotheses are then developed. Next, the methodology used is presented, and then the findings and their implications are discussed.

Literature Review and Hypotheses Development

Power is defined by Finkelstein (1992, p. 506) as ‘the capacity of individual actors to exert their will’. According to Adams et al. (2005), the CEO’s power affects the firm’s performance negatively or positively depending on the corporate decisions he takes; these decisions often have extreme consequences. Many studies have found a positive association between CEO power and firm performance and outcomes (Breit et al., 2019; Keltner et al., 2003). Contrary to these results, other studies found a negative association (Bebchuk et al., 2011; Dikolli et al., 2018; Han et al., 2016; Liu & Jiraporn, 2010).

Nevertheless, studies investigating the impact of powerful CEOs on R&D expenditures remain rare, and their results are inconclusive (Naaman & Sun, 2022; Zhang et al., 2022). Some of these studies concluded a positive association between CEO power and R&D expenditures (Aibar-Guzmán & Frías-Aceituno, 2021; Naaman & Sun, 2022; Qiao & Fung, 2016; Sariol & Abebe, 2017; Sheikh, 2018; Zhang et al., 2022). According to Zhang et al. (2022), this positive impact is accentuated when the number of independent directors increases and when competition in the market is intense. The authors argued that an important power may encourage CEOs to allocate more important resources to green R&D activities. These findings join those of Sariol and Abebe (2017) and Sheikh (2018), suggesting that CEO power allows him to freely inspect the institutional environment and allocate the necessary resources to implement strategic actions. Sheikh (2018) emphasizes, however, that this positive association is determined by market competition, and consequently, this relationship only exists when the CEO operates in highly competitive markets. Chen (2014) concluded that CEO power has a moderating impact on the association between board and innovation, suggesting that the board is more likely to promote innovation by providing the necessary resources for R&D activities when CEOs are powerful.

These findings are contrary to those of Naaman and Sun (2022), who suggested that more powerful CEOs cause a higher level of agency conflict, leading them to invest less in risky projects such as R&D. The authors explained that the long-term benefits of R&D investment are under valuated by powerful CEOs. Naaman and Sun added that this association becomes more important in firms with a low level of governance. Zhang et al. (2022) confirm this negative association and argue that these results are in line with agency theory (Jensen & Meckling, 1976), suggesting that CEOs are frequently risk-averse since their compensation and career are only dependent on their firm. The agency theory considers that it is important to limit and control the CEO’s power given the existence of a positive association between CEO power and the agency conflict level (Jensen & Meckling, 1976). Moreover, the agency theory argues that CEO power intensifies managerial entrenchment (DeAngelo & Rice, 1983) and consequently inhibits managerial to invest in risky projects with uncertain cash flows (Sheikh, 2018). According to Sheikh (2019), there is a close relationship between CEO power and managerial risk-taking. These suggestions join those of Dikolli et al. (2018), who argued that powerful CEOs have greater incentives to avoid risk and adopt opportunistic behaviour; consequently there is a strong relationship between CEO power and agency conflicts. However, Shui et al. (2022) suggested that the association between CEO power and environmental innovation depends on the existence of board archetypes and the ownership structure.

In the current study, we investigated the impact of CEO power on R&D expenditures in the Saudi context using the power dimensions identified by Finkelstein (1992). According to Finkelstein, there are four dimensions relating to power, including structural, ownership, expertise and prestige aspects. However, we followed Tang et al. (2011) and Sheikh (2018) and retained three power dimensions: structural power, ownership power and expert power. Tang et al. (2011) argued that the fourth dimension related to prestige power should not be included when measuring CEO power since it cannot be considered a proximal measure relative to the other dimensions.

Ownership Power

The second power dimension is related to ownership power. Finkelstein (1992, p. 509) suggested that ‘The strength of a manager’s position in the agent-principal relationship determines ownership power’. Thus, there is a positive association between the top manager’s shareholdings in an organization and his ownership power (Finkelstein, 1992). Moreover, Finkelstein suggested that CEO stock ownership reduces agency problems, mitigates board influence and increases CEO power. When CEOs have a high proportion of the company’s shareholding, they have the power to influence most of the company’s activity (Mio et al., 2016) and dominate most of the board’s decisions (Zhang et al., 2016).

Considering R&D investment as a strategic decision, many studies have investigated the association between stock ownership and R&D expenditures (Chen & Hsu, 2009; Chen & Huang, 2006). Chen and Huang (2006) concluded that employee stock ownership positively affects the R&D expenditures. The authors explained that this result suggests a positive impact of employee stock ownership on mitigating agency problems. However, Chen and Hsu (2009) found a negative association between family ownership and R&D investment. The authors explained this result by the undervaluation of R&D activities by the family-owned firms. According to Kim and Lu (2011), if the external governance is weak, the CEO’s ownership will affect the R&D spending.

In the current study, we propose the following hypothesis:

Structural Power

The first power dimension identified by Finkelstein (1992) is the structural power based on the formal organizational position. Finkelstein suggested that CEOs have high structural power, allowing them to control the behaviour of their subordinates and consequently manage uncertainty. The author created a structural power scale using three variables: percentage with higher titles, compensation and number of titles. Other variables were also used to measure the structural power, such as CEO duality (Adams et al., 2005; Qiao & Fung, 2016) or CEO insider (Cheikh & Zarai, 2008; Sariol & Abebe, 2017; Wu et al., 2011; Zhang et al., 2022). In the current study, the structural power is proxied by CEO insider. Kesner and Sebora (1994, p. 335) defined outsiders as ‘the individuals who were not employed by the organization, while insiders are current or previous employees’. According to Sariol and Abebe (2017), the CEO’s power enhances the explorative innovation activity. However, the authors concluded that the CEO outsider status has a moderating role in the association between CEO power and exploitative innovation activity. They suggested that the CEO’s power enhances exploitative innovation activity when the CEO is an outsider. Sariol and Abebe (2017, p. 43) explained that ‘outsider CEOs are wary of “rocking the boat” too much by introducing extensive strategic change, thereby damaging the performance and standing of the firm. In this instance, they perhaps resort to stabilizing the competitive position and performance of the firm before venturing to more aggressive ventures’.

In the current study, we advance the following hypothesis:

Expert Power

The third power dimension is related to expertise, defined by Finkelstein (1992, p. 513) as ‘the ability to deal with environmental dependencies’. According to Shui et al. (2022, p. 793), ‘CEO expert power refers to a CEO’s executive expertise in general management. Therefore, it has normally been operationalized as CEO tenure in many studies’. Wu et al. (2011) suggested that expert power is the result of knowledge or cognitive work experience acquired over time. When the CEO acquires experience in areas critical to the firm’s success, he accumulates considerable expert power, enabling him to deal with environmental requirements and critical contingencies (Hambrick, 1981). In addition, their decision-making regarding the venture’s innovative orientations as well as the way in which they manage external pressures are directly affected by their professional backgrounds (Hambrick, 2007). While demonstrating great caution, having relevant expertise increases an individual’s confidence in making risky decisions about pursuing innovations (Finkelstein, 1992). Shui et al. (2022) argued that, regarding environmental innovation, the CEO’s expert power can derive from either environmental management or from R&D expertise. According to Zucker et al. (1998), CEOs with expert power are better able to set the technological direction of the company given the importance of discretion and control of the resources granted to them. These findings join those of Turner and Makhija (2012), suggesting that expert CEOs have a better holistic understanding of difficult problems, and consequently a more reasonable approach to risky innovation given their tacit knowledge to appreciate the risks and opportunities. According to Park and Tzabbar (2016), R&D expertise can provide power to CEOs; this power enables them to attenuate the positive or negative association between venture capitalist funding and innovation novelty, respectively, in the early or late stage of the venture.

In accordance with Tang et al. (2011), Zhang et al. (2022) and Shui et al. (2022), the CEO tenure is used in the current study to explore the association between expert power and R&D expenditures. Thus, the following hypothesis is proposed:

Moderating Effect of Power Indicators

UET theory discusses the concept of power proposed by Carpenter et al. (2004) and Finkelstein (1992) and has presented power as a moderator variable. CEO power is defined as a person’s ability to exercise their will, and powerful CEOs feel empowered to make important and risky decisions. Four dimensions of power were identified. While several studies have tested the impact of CEO power, few have examined the moderating effect of all aspects of power separately or together. Carpenter et al. (2004) mentioned the tendency of CEOs to express a ‘bundle’ of power’s dimensions and suggested that it is important to consider the moderating role of different dimensions rather than reflect them separately. Thus, we aim to test the following hypothesis:

Research Design

The study considers the effect of CEO’s power, particularly, ownership power, structural power and expert power, on the company’s R&D expenditure. The study data were collected from the annual reports of a sample of Saudi listed firms on Tadawul. The sample of the study comprises 60 firms. The study contains 4 years (from 2016 to 2019) panel data as a total of 240 observations.

Variable Measurement

The main objective of this study is to explain the direct relationship between three CEO power indicators and the firms’ R&D expenditures. The dependent variable ‘R&D expenditures’ is measured by R&D amount per sales (Baysinger et al., 1991).

The explanatory variables are CEO power indicators especially CEO ownership power, CEO structural power and CEO expert power.

CEO ownership power is operationalized as part of direct and indirect stock the CEO holds in the firm (Hamidlal & Harymawan, 2021; Han et al., 2016). The direct property is the portion of capital held by the executive, and the indirect property is the stock held by the executive in corporations that have important ownership in the firm he manages.

The CEO’s expert power is proxied, similarly to Han et al. (2016) and Hamidlal and Harymawan (2021), by the CEO’s tenure, which indicates the number of years since the CEO’s appointment by the firm. The authors specified that the longer the executive’s tenure, the more knowledge he has and the more the CEO shows a high level of skills and proficiency that can impact the choices he make (Hamza et al., 2020).

Following Wu et al. (2011), the CEO’s structured power is proxied by the CEO origin before his appointment. CEO has structural power when he is an insider. The variable is a dummy; it takes 1 if the CEO is selected within the company (Zhang & Rajagopalan, 2010) and 0 if he is an outsider.

Control Variables

The CEO’s characteristics may logically vary with firm features, and accordingly we should control for firm specificity by using some of its attributes. Numerous variables have been, previously, used in the firm R&D study to control for firm-specific impact on the model results (Hamza et al., 2020). In our study, we use firm financial performance indexed by ROE ratio, and firm size measured by the number of employees.

Model

The study performed OLS regression to examine the hypotheses developed earlier in the literature review. The endogenous variable is firm innovativeness, operationalized by R&D expenditure. Explanatory variables are CEO ownership power, structural power and expert power. The basic theoretical model is as follows:

where:

α = intercept; Own_Power = CEO ownership power; Struct_Power = CEO structural power; Expert_Power = CEO expertize power; ROE = return on equity; F_size = firm size; Ɛ = error term.

The moderating effect of different power variables on the firm’s R&D spending is tested on the following sub-models:

Results

Descriptive Statistics

Table 1 provides a summary of the descriptive statistics of all the study variables. Statistics show that R&D expenditures represent 2% of total assets for Saudi firms. Furthermore, 60% of Saudi firms’ chief executives are insider and, consequently hold structural power. Results confirm that the general practice in Saudi companies is to select internal managers and not recruit outsiders (Hamza et al., 2020). Statistics show, also, that only 14% of CEOs hold a percentage of the company’s ownership. Thus, Saudi firms’ executives have weak ownership power. Concerning CEO expertise power, the mean of the tenure is 5.595833 and the standard deviation is 5.019542, which confirms that the average CEO’s expertise is approximatively 5 years.

Descriptive Statistics.

Correlation Matrix

Pearson correlation between the study variables is shown in Table 2. The correlations between R&D expenditure and the CEO’s ownership power and expertise power are negative. However, the correlations between R&D expenditure and CEO structural power and firm performance and firm size are positive. Accordingly, we can conclude from observing the correlation matrix that Pearson correlations between all independent variables are less than 0.5, which validates their presence in the same model.

Pearson’s Correlation Matrix.

Regression

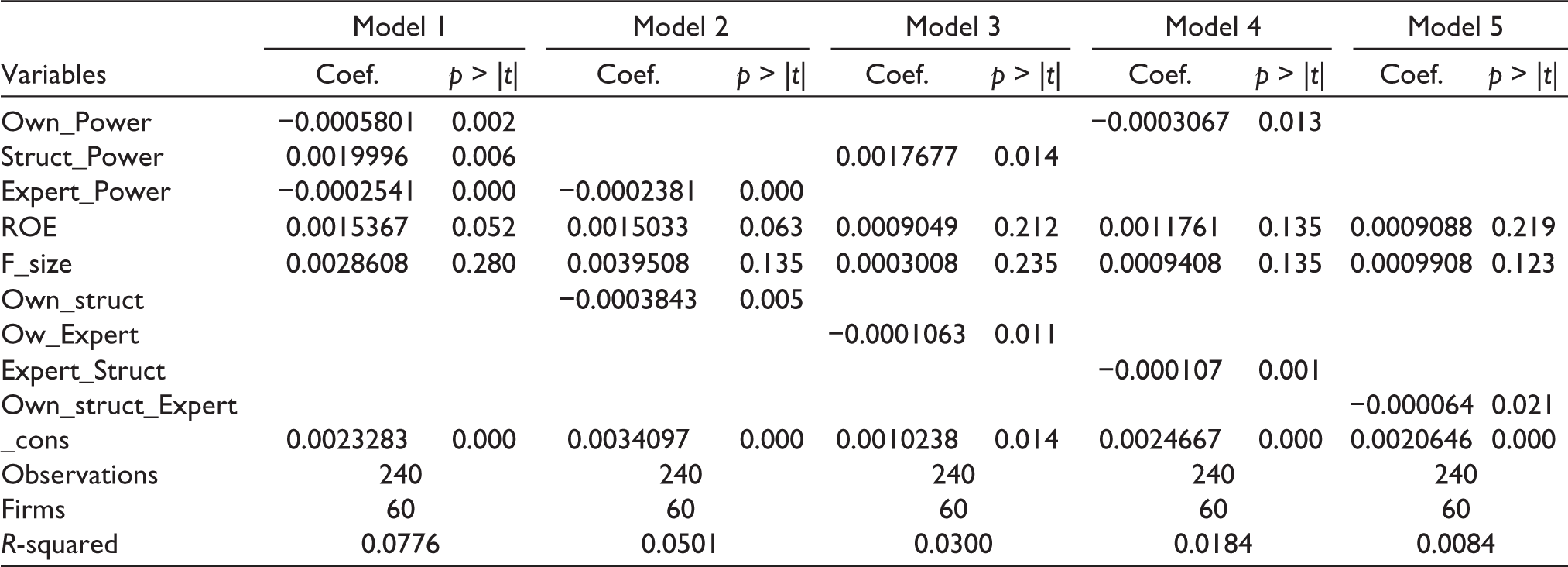

This study examines the effect of the CEO’s power indicators (ownership, structural and expertise power) on the firm’s R&D expenditures. Testing the hypothesis that have been developed above is processed using OLS regression of the five theoretical models. The basic model aims to test the direct relationship between the executive’s ownership power, structural power, expertise power, the firm’s financial performance and size, and R&D expenditures. The second and third models are developed to test the moderating effect of the ownership power, consecutively, in the relationship between the structural power and expertise power and the firm’s innovation. The fourth model is used to test the moderating effect of structural power in the relationship between expertise power and R&D expenditures. The fifth model is used to test the effect of the CEOs’ power score on R&D expenditure.

Discussion

Table 3 shows the regression results for the main model and the four sub-models testing the moderating effect of the CEO power indicators. Concerning the relationship between ownership power and R&D expenditures, the results in models 1 and 4 display a negative and significant association between the two variables. This contradicts the majority of previous studies, such as Han et al. (2016), who found that the greater the CEO holds shares, the greater he has power. Thus, authors concluded that CEOs who have ownership power decide strategic choices, lead developments efficiently and perform well to create long-term wealth (Ulrich, 1998). This positive relationship is argued by the conclusions of the agency theory. When the CEO holds shares in the firm, his interests will be aligned with those of other shareholders. Consequently, the CEO with great ownership power will make decisions that will maximize the shareholders wealth, such as innovation investment. However, the negative relationship we found between ownership power and R&D expenditures is in line with previous studies suggesting an inverted-U-shaped relation between the CEO’s ownership and the firm innovation argued by the owner’s risk-taking behaviour (Wright et al., 1996).

The relationship between structural power and R&D expenditures is positive and significant, as shown in both models 1 and 3 results. Results confirm many previous studies such as Balsmeier and Buchwald’s (2014) and support the idea that internal leaders possess more important firm-specific knowledge than external leaders and are therefore more empowered to decide innovation activities. Furthermore, findings are in line with Balsmeier and Buchwald (2014), who found that firms where the executive is an external have fewer patent filings than others with an internal CEO. The authors propose that the promotion of insider CEOs permits an important focus on innovation plans compared with firms recruiting external executives. Accordingly, Cummings and Knott (2018) find that external CEOs spend less on R&D than internal CEOs. Authors argue that external CEOs may lack the technical skills necessary in leading the firm’s R&D. However, the authors notify that while they do not advise boards to shun outside CEOs, they do recommend considering technical expertise and its impact on innovation when hiring an executive.

Findings in Table 3 show a negative and significant relationship between expertise power and R&D expenditures in both models 1 and 2. Contrary to some previous studies (Li et al., 2016), which demonstrated that CEOs who have led the firm for a long period have more knowledge in the firm’s industry, our study’s results confirm some other studies, such He et al. (2021) and Li and Patel (2019), who found that executives with short tenure build their expertise from numerous firms and diverse industries, and, thus they are more capable and skilled to make strategic decisions that benefit the firm.

Regression Results.

Concerning the moderating effect of the power indicators in models 3, 4 and 5 results show a negative and significant moderating effect of the three powers indicators on R&D expenditures. Findings are consistent with the results found by Bebchuk et al. (2011) and confirm that CEO power, in general, is negatively related to the company value. Similarly, Wei (2019) shows that CEO power is, in different contexts, positively and negatively correlated with firm wealth. However, our findings are contrary to some other previous researches that studied the interactive effect of the executives’ powe,r such as Dowell et al. (2011), who found that the CEO’s power is positively correlated with firm value. Additionally, Sheikh (2018) concluded that the more powerful a CEO is, the greater the value of the firm he manages. Han et al. (2016) examine, also, the impact of CEO power on firm performance. The authors showed that CEO power is positively related to organizational performance. They argued that the results show that CEOs are empowered to reduce conflict and resolve issues, so they can make decisions faster and more effectively.

Robustness Check

We aim in this part to run additional tests of the robustness of the study’s results by changing control variables proxies.

In Table 4, you find the regression results of the robustness test of the basic model employed using alternative proxies for control variables. For firm financial performance, we use ROA instead of ROE, while for firm size, we substitute the log of the number of employees for the log of total assets.

Robustness Check.

Findings show the non-variability of the relation between R&D expenditures and CEO power indicators due to change of the measures of control variables.

Conclusion

This study expands the research on CEO power and focuses on the association between CEO power and R&D expenditures by providing many academic and practical contributions. First, from a theoretical viewpoint, it contributes to the studies belonging to the upper echelon theory by providing an analysis of the effect of each power indicator on the manager’s risk-taking and strategic choices (innovation). The study also contributes to the agency theory literature by providing empirical evidence related to the consequences of having a powerful CEO. Empirically, the study offers evidence concerning the association between a CEO trait (CEO power) and strategic decisions (to invest in R&D).

Second, from a practical viewpoint, the results extend the financial accounting literature investigating the determinants of R&D expenditures and explaining the underinvestment in R&D activities. Additionally, the study helps Saudi investors concentrate on their firms’ long-term wealth by selecting CEOs who are more willing to invest in innovative activities.

However, these findings have some limitations. First, other indicators related to the power dimensions should be used. Second, innovation should also be measured through its outputs, such as patents. This is all the more important since, in 2022, Saudi Arabia is ranked 37th according to the Global Innovation Index (GII) (using the innovation inputs) and 65th according to the GII (using the innovation outputs). 2

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.