Abstract

This research examines the drivers of financial inclusion in the Pradhan Mantri Jan Dhan Yojana (PMJDY) scheme. Also, it investigates the influence of financial inclusion through PMJDY on the socioeconomic status of marginalized people. Primary data were collected from 393 marginalized people of Himachal Pradesh. This study presents new insights by analysing the demand-side perspective of marginalized people using structural equation modelling approach. The study identified outreach, quality of financial services, usage and accessibility as statistically significant determinants in the PMJDY scheme for financial inclusion. Further, results confirm that financial inclusion promoted by PMJDY substantially improves the socioeconomic status of marginalized people. The study links financial inclusion and the socioeconomic wellness of beneficiaries, with income serving as a moderator; this is the research’s unique contribution to reducing financial exclusion. The research findings have implications for policymakers and financial institutions in formulating effective strategies to attain comprehensive financial inclusion, which can contribute to a strong socioeconomic development of marginalized people through PMJDY.

Keywords

Introduction

Background

Financial inclusion as a development goal has gained much attention from policymakers at global/national levels. It has been tremendously popular in India for more than four decades. Financial inclusion is a strong economic instrument for overall and inclusive development as services related to financial inclusion have given a significant contribution for penetration of untapped rural market (Raichoudhury, 2020). Financial inclusion is also a main indicator of social development as it can add towards poverty reduction, minimize the income gap, help in increasing savings, promote more gender equality and direct towards better financial decisions (Gallego-Losada et al., 2023). It develops a financial system and a sound financial system paves the way for connecting people with a diverse range of financial facilities like bank accounts and advances to a significant segment of society (Demirguc-Kunt & Klapper, 2013). Study of Anwar et al. (2020) explores that government assistance builds up the link between the success of the new venture and entrepreneurial finance. In the direction to ensure ‘financial access’, a person must first have an account and its access and use to save money that brings financial inclusion growth (Demirguc-Kunt et al., 2018). Similarly, Asif et al. (2023) discovered that fintech businesses aided financial inclusion in India. However, numerous studies on the financial exclusion of underprivileged populations concluded that despite the efforts of the government and banking institutions, such as making it easier to open an account, lowering banking costs and aiding in promoting the services, financial exclusion concerns remained to exist among disadvantaged populations (Bhagat, 2013; Polloni-Silva et al., 2021; Singh et al., 2022). Like, Roy and Patro (2022) declared that multiple cultural and socioeconomic variables affect financial exclusion of women and reality of gendered financial inclusion is primarily because of these demand side factors. Overall, efforts towards enhancing marginalized people’s financial inclusion can lead to socioeconomic empowerment and economic development (Lal, 2021; Yadav et al., 2023). However, most Indian states continue to have a low or moderate financial inclusion level (Singh et al., 2021). As a result, there needs to be more social and economic change due to inadequate financial inclusion. Niaz (2021) argues that improving access to financial services for the economically disadvantaged is a crucial step towards achieving sustainable development. Even social sustainability is possible with the help of the self-reliance of the rural population (Yadav et al., in press). According to Roy and Patro (2022), socioeconomic factors are also observed to influence the financial exclusion of women. Therefore, adding people in the financial system is very necessary for the economically inclusive growth of the nation.

Financial Inclusion in India

Numerous researches have evaluated the time to time status of financial inclusion in India. Dixit and Ghosh (2013) demonstrates that Indian states with a high financial inclusion index (FII) have higher GDP per capita and literacy rates. In contrast, states with a low FII have lower GDP per capita and literacy rates. According to Ambarkhane et al. (2016), Kerala and Goa were classed as states with upper-medium financial inclusion, while Himachal Pradesh, Andhra Pradesh, Tamil Nadu and Punjab were designated as states with lower-middle financial inclusion. All other states fall into the low-growth category, indicating room for improvement. According to demand-side and supply-side analysis for financial inclusion, India falls under the category of high financial inclusion (Sethi & Sethy, 2019). CRISIL (2018) demonstrated a rise in the country’s total financial inclusion, and India’s CRISIL Inclusix score increased to 58.01 in fiscal 2016 from 50.12 in fiscal 2013. Financial inclusion in India has increased with Pradhan Mantri Jan Dhan Yojana (PMJDY) as Banerjee and Gupta (2019) discovered that bank account accessibility has increased with PMJDY. Sharma et al. (2018) evidenced that PMJDY has successfully made rural banks more accessible to low-income residents. However, Singh et al. (2021) discovered state-by-state comparison of the FII measure and showed that only a slight improvement happened once the PMJDY system was implemented in India. A significant segment of India’s population is unable to avail formal financial system.

Financial Inclusion and Its Determinants

Various researchers have used different determinants to measure financial inclusion. Income, employment opportunities and infrastructure are the most essential factors of financial inclusion (Raichoudhury, 2020). However, Sarma (2008) used three elements of financial inclusion to create the financial inclusion index (IFI), including banking penetration, usage and availability of financial services. Similarly, Chattopadhyay (2011) and Yadav and Sharma (2016) utilized access to banking, banking system and banking penetration as parameters for measuring financial inclusion. A study of Gupte et al. (2012) attempted to create an IFI for India with four dimensions: outreach, transaction convenience, usage and transaction costs. Goel and Sharma (2017) developed FII using three dimensions: penetration of banking, availability of banks and access to insurance. Similarly, Okello Candiya Bongomin et al. (2017) measured financial inclusion based on the four pillars that is access, utilization, quality and welfare as drivers to construct IFI. Nandru and Rentala (2019) quantified five components of financial inclusion. These components include geographic proximity, availability, access, affordability and usage.

Research Gap, Novelty and Objectives of the Study

The lack of financial inclusion in India is the research concern of this study. The Indian government has started PMJDY to guarantee access of vital financial services for all Indian households. This scheme had tremendous success in increasing the bank account ownership of households. After a thorough review of existing research in the financial inclusion domain, it was discovered that most of studies focused on developing an IFI and its influence on economic development. However, the existing literature is silent on the nature and extent of the effect of financial inclusion on the socioeconomic progress of marginalized people with PMJDY from demand side perspective. There is also a lack of studies exploring the determinants that help to achieve financial inclusiveness. The current study targets to fill this research gap and explores the determinants of financial inclusion through PMJDY with a method of multivariate analysis. Thus, the novelty of this research is to investigate the dimensions contributing to financial inclusion concerning with PMJDY and to check how the socioeconomic development of marginalized people is influenced with participation in the PMJDY scheme. This research also seeks to answer the question of whether or not income serves as a moderator between financial inclusion and disadvantaged people’s socioeconomic position. The results of the study contribute to the new body of knowledge.

The remaining article is organized into the seven sections mentioned below. The literature review is discussed second, followed by a proposed research model and hypotheses for the study in the third section. Next, the fourth section is the methodology section, followed by discussion in fifth section on data analysis and results. Conclusion and policy implications are mentioned in the sixth section, and limitations and future research possibilities are discussed in the seventh section.

Literature Review and Theoretical Framework

Financial inclusion has been studied extensively in both national and international contexts. An extensive survey of the literature on financial inclusion is provided in this part, including studies on determinants of financial inclusion and its impact on marginalized groups’ socioeconomic growth.

Quality

The term ‘financial services quality’ relates to the extent to which financial goods and services meet customers’ requirements, the variety of choices offered to clients and the level of knowledge and comprehension of financial products by the customers (Alfred & Jansen, 2014). The eight measures of quality dimension are transparency, affordability, fair treatment, convenience, financial education, indebtedness, consumer protection and choice (AFI, 2016). Financial inclusion has been determined to be strongly related to the quality of financial services (Lal, 2018, 2019). Beck et al. (2009) and World Bank (2014) used the quality of banking services as one of the primary factors to quantify financial inclusion. Similarly, several researchers regard ‘quality’ as determining factor of financial inclusion (Demirguc-Kunt et al., 2015; Okello Candiya Bongomin et al., 2017). Thus, the subsequent hypothesis is made in light of the previous debate:

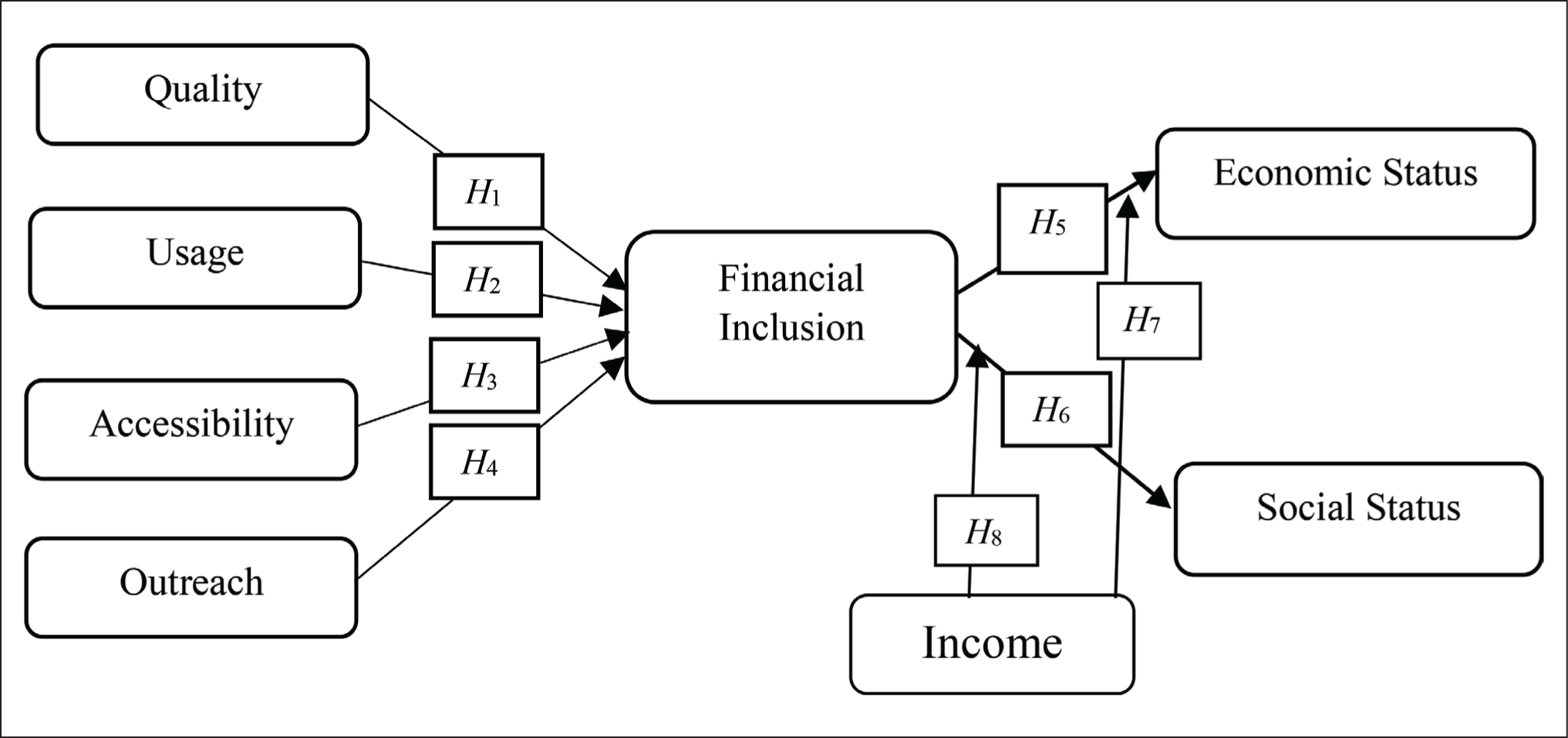

H1: The quality of financial services is an important determinant in promoting financial inclusion

Usage

The term ‘usage’ refers to the continued and extensive application of financial services and products. Additionally, it is concerned with the frequency, duration and consistency of usage throughout time (Alfred & Jansen, 2014). A crucial factor in determining the degree of financial inclusion is the degree to which individuals use financial services (Beck et al., 2007; Ghosh, 2011; Kendall et al., 2010). In order to be considered financially inclusive, a bank account must be well utilized (Sarma, 2008). Beck et al. (2007) proved that expanding branch and ATM network density in proportion to population density results in greater individual use of financial services. Nandru and Rentala (2019) and Nandru et al. (2021) found financial service usage as a major predictor of financial inclusion. According to the available literature, the use of the banking system was included in the development of FII (Chattopadhyay, 2011; Goel & Sharma 2017; Gupte et al., 2012; Ifediora et al. 2022; Mehrotra et al., 2009; Sarma, 2008; Sharma, 2016; Yadav & Sharma, 2016). As a result of this discussion, the below mentioned hypothesis is suggested:

H2: The usage of financial services is an important determinant in promoting financial inclusion.

Accessibility

Accessibility represents the ability to access and utilize existing banking products and services and the lowest possible barrier to opening a bank account in formal institutions (AFI, 2011; Alfred & Jansen, 2014). Financial inclusion is associated with enhanced access to formal banking services, such as lower transaction costs, more convenient branch locations and simplified requirements for opening a bank account (Allen et al., 2016). Further, Nandru and Rentala (2019) and Nandru et al. (2021) investigated that access to financial services had a significant impact on financial inclusion. Accessibility is one of the three basic pillars of financial inclusion (Sarma, 2008). In the same way, other authors also used accessibility as a proxy to evaluate financial inclusion when they made IFI (Chakravarty & Pal, 2013; Goel & Sharma, 2017; Gupte et al., 2012). Thus, taking the preceding discussion into account, the subsequent hypothesis is made:

H3: The accessibility to financial services is an important determinant in promoting financial inclusion.

Outreach

The term ‘outreach’ refers to the ‘number of branches per square kilometre’, ‘the number of ATMs per square kilometre’ and ‘the number of branches per 1,000 residents’ (Demirguc-Kunt et al., 2015). Arora (2010) created an FII for developed and developing nations by including outreach as a dimension of financial inclusion. Similarly, Gupte et al. (2012) and Ifediora et al. (2022) developed an IFI for India using outreach as a financial inclusion predictor. In light of the above debate, the following hypothesis is suggested:

H4: Outreach to financial services is an important determinant in promoting financial inclusion.

Financial Inclusion and Socioeconomic Development

Financial inclusion is one of India’s primary measures for attaining inclusive economic development. Ghalib et al. (2008) claimed that increased availability of banking services would boost economic growth of the country. On the other side, insufficient availability of banking services is one of the most significant hurdles to income generation and social security. Expanding access to financial services for the economically poor is essential to achieve sustainable development (Niaz, 2021). Financial inclusion influenced the economic growth of underprivileged areas in India (Lal, 2021). There is a long-run relationship between economic growth and financial inclusion in the SAARC countries and also bi-directional causality exists among financial inclusion and economic growth (Kuri & Laha, 2011; Singh & Stakic, 2021). Khan et al. (2022) discovered through the study of 54 countries that financial stability has been significantly improved with financially inclusive system and as a result, poverty and income inequality is going down in these countries. Financial inclusion through cooperative banks aids in poverty alleviation (Lal, 2018). According to a recent study conducted by Ifediora et al. (2022), economic growth is found to be positively affected by the dimensions of financial inclusion including composite financial inclusion, penetration and availability. The usage dimension of financial inclusion was found to improve economic growth but not to a statistically significant extent. Additionally, Bhatia and Singh (2019) revealed that financial inclusion initiatives influenced urban women’s socioeconomic and political empowerment. Participation in financial inclusion by women promotes both economic and social well-being around the world (Cabeza-Garcıa et al., 2019). Nandru and Rentala (2019) found that enhancing the financial inclusion status of a deprived population leads to overall socioeconomic development. Moreover, an investigation of Singh et al. (2021) found that the financial inclusion scheme (PMJDY) has increased economic growth. Therefore, financial inclusion is strongly connected with the economic growth of marginalized people through social and economic empowerment (Lal, 2021). Hence, subsequent hypotheses are made in light of the previous debate:

H5: Financial inclusion, as facilitated by the PMJDY scheme, has a significant impact on the economic status of marginalized people. H6: Financial inclusion, as facilitated by the PMJDY scheme, has a significant impact on the social status of marginalized people.

Financial Inclusion and Social Economic Development: Income as Moderator

As per the literature, financial inclusion is important for both community development and economic progress (De Koker, & Jentzsch, 2013; Sarma & Pais, 2011). It has significantly improved the economic and social conditions of tribal communities (Nandru & Rentala, 2019). Literature also suggests that greater financial accessibility is reported by those who with a higher socioeconomic status in comparison with those having a lower socioeconomic status (Della Peruta, 2018; Sha’ban et al., 2020). According to Cabeza-Garcia et al. (2019), economic growth is found to be more affected by financial inclusion of women when it is considered in terms of credit cards and access to bank accounts. Similarly, literature provides evidence that financial inclusion in terms of savings and credit facilities bring low-income households out of poverty (Swamy, 2014). In addition, Dupas and Robinson (2009) emphasized on the importance of savings accounts as people with access to savings accounts are found to be interested in increasing their consumption, productivity and also invest more in preventive health care. Demirguc-Kunt et al. (2018) found that the individuals in economies with a higher income have greater access to formal financial services than those in economies with a lower income. Literature discovered a positive relationship between income and formal account ownership (Abdu et al., 2021; Allen et al., 2016; Demirguc-Kunt & Klapper, 2013). Hence, income is a crucial factor in determining financial inclusion (Raichoudhury, 2020). Despite the accelerated economic growth of the preceding decades, income inequality persists in developing countries, including India. Nevertheless, a greater availability of banking services promotes financial inclusion, particularly among lower-income individuals (Park & Mercado, 2018). Hence, integration of low-income individuals into the formal financial system, increases their financial wealth and social economic standing. Following hypotheses are proposed to check income role as moderator in case of financial inclusion through PMJDY:

H7: Income is moderating the relationship between financial inclusion and economic status of marginalized people. H8: Income is moderating the relationship between financial inclusion and social status of marginalized people.

The postulated model was developed using the evidence gleaned from the literature review. Figure 1 Depicts research model based on four elements of financial inclusion: accessibility, usage, quality and outreach. Additionally, the model examines the link between financial inclusion via the PMJDY program and socioeconomic development.

Proposed Research Model.

Research Methodology

Generation of Measurement Scale

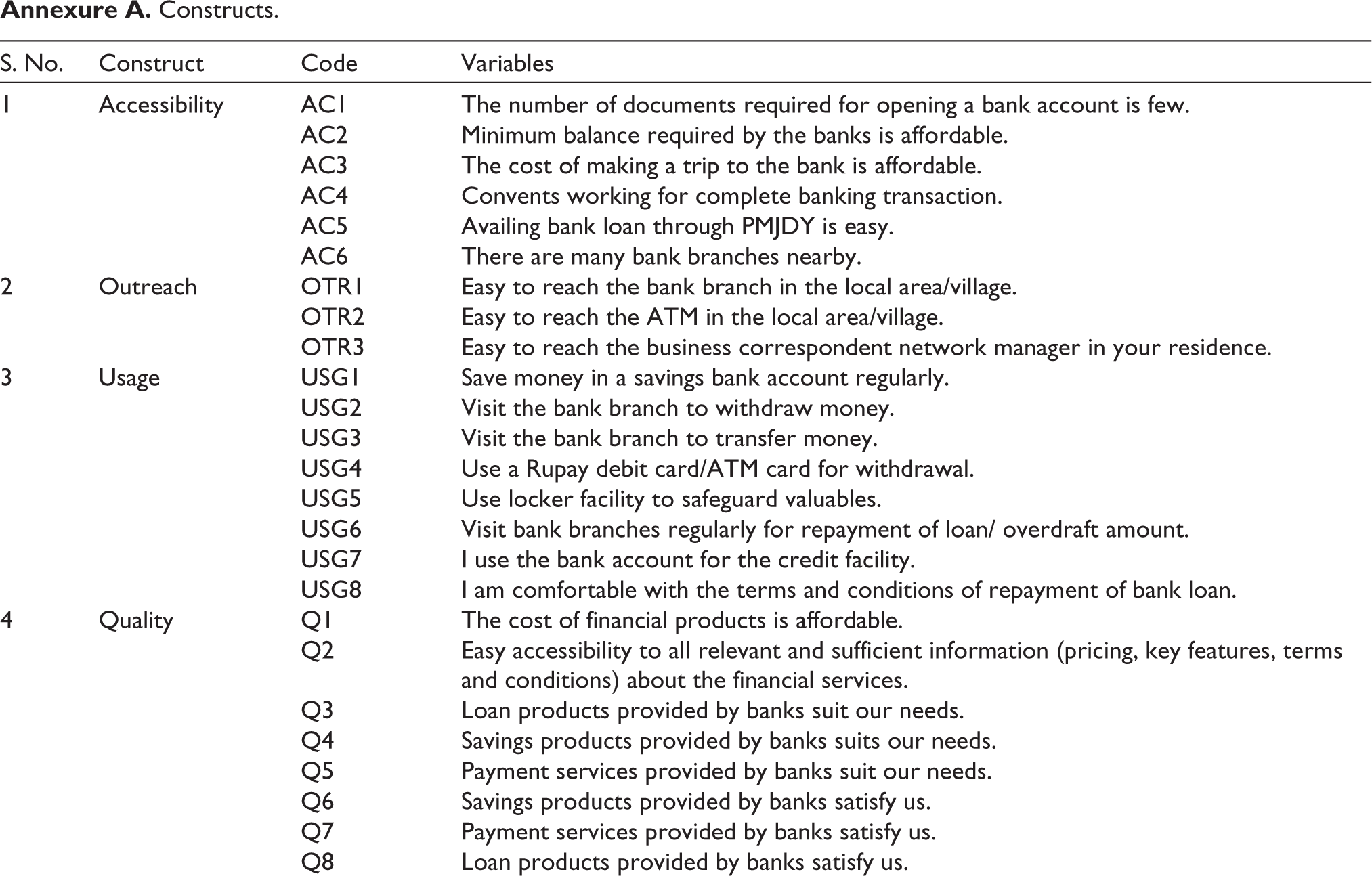

The scale statements used to assess respondents’ perceptions were designed following a literature review. Apart from demographic information such as gender, marital status, age, education, occupation and income; the questionnaire included 44 statements about accessibility, outreach, usage, quality, financial inclusion and socioeconomic status (Annexure A). Outreach was operationalized using three items adopted from Sharma et al. (2016) and Nandru and Rentala (2019). Accessibility was measured using six items obtained from Nandru and Rentala (2019) and Bongomin et al. (2018). The measures of usage comprise eight items taken from Nandru et al. (2021) and Nandru and Rentala (2019). Eight measurement scale items about quality were adapted from AFI (2016), Amidzic et al. (2014), and Bongomin et al. (2018). Economic status was assessed using six items derived from Swamy (2014) and Nandru and Rentala (2019). Eight items obtained from Lal (2021) and Nandru and Rentala (2019) were applied to operationalize social status. Five items of financial inclusion are derived from Rastogi and Ragabiruntha (2018) and Nandru et al. (2021). These measurement items were revised to fit in the context of PMJDY and for a broader understanding of marginalized people using financial services through this scheme to maintain content validity. To collect the data, a five-point scale from strongly disagree (1) to strongly agree (5) was used. After pilot testing and further revisions, the questionnaire was administered.

Sampling Procedure

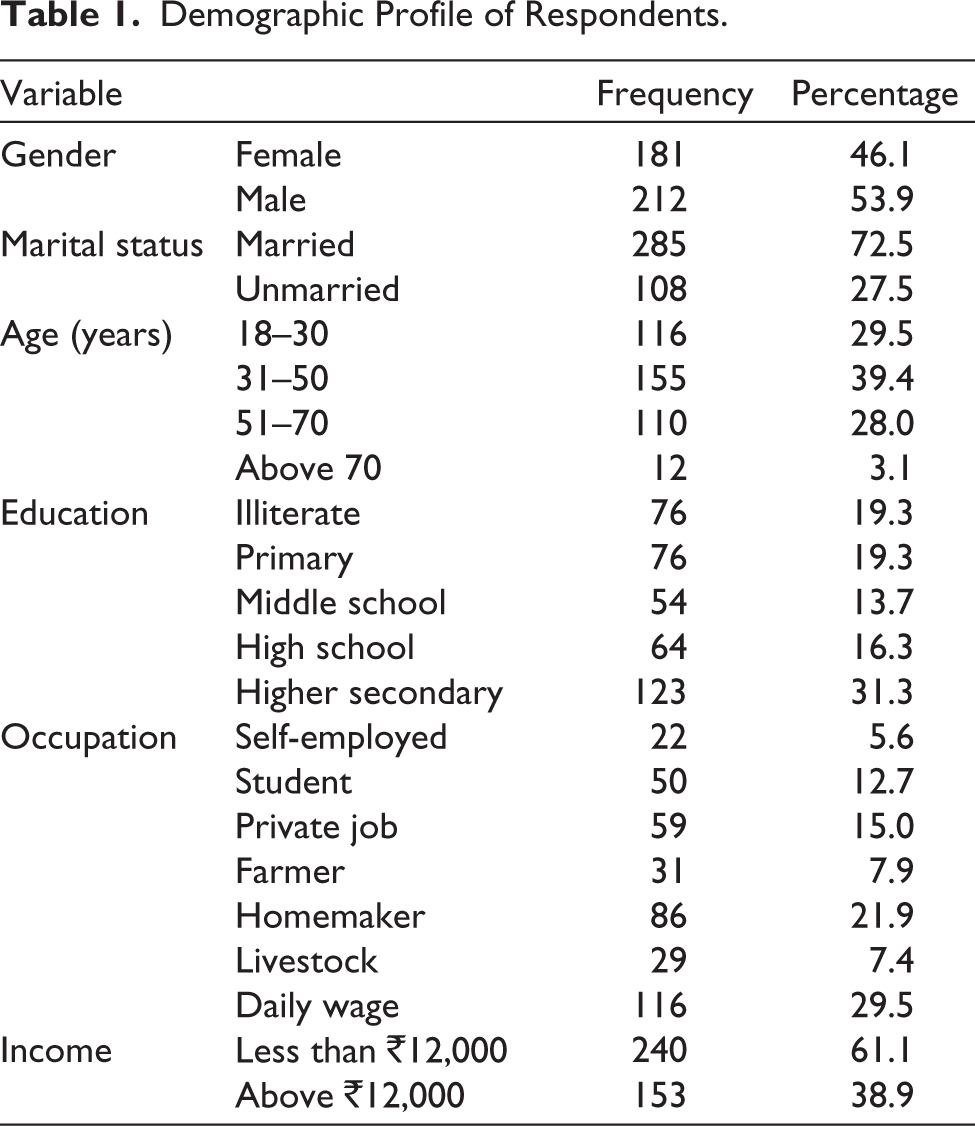

The sample design is based on empirical research that has already been done. The sampling unit is made up of marginalized individuals who have a PMJDY bank account. The sample area was chosen using a multi-stage sampling procedure. In the first stage, five districts were chosen, namely, Kangra, Shimla, Mandi, Solan and Una, based on their largest marginalized populations in Himachal Pradesh, an Indian state, as per the 2011 Census. Two blocks from each selected district were randomly picked in the second stage. The third stage involved the random selection of two villages from each block. The final stage involved contacting beneficiaries of the PMJDY scheme in chosen areas using the snowball sampling approach. The data was gathered via structured interviews with respondents in the study areas. A total of 450 marginalized people were contacted for the study. Following the initial screening of the interview schedule, it was discovered that 40 interviews schedule had missing data, and 17 respondents did not have any bank accounts. Thus, the final sample of 393 respondents having PMJDY bank accounts was utilized for the final data analysis. In addition, the sample is divided into low-income and high-income groups to investigate how income moderates the connection link among financial inclusion and socioeconomic status. People with income below ₹12,000 are considered as low-income, whereas people with income above ₹12,000 are considered as high-income (Singh et al., 2021).

Sample Profile

All respondents, regardless of gender, have nearly identical profiles. The majority of respondents are married. In case of education, the respondents majorly studied up to a higher secondary level (31.3 %), followed by those who were illiterate (19.3 %) and educated up to the primary level (19.3 %). Daily wage employees dominate the occupation, followed by homemakers and persons with private jobs. In all, 39.4 % of respondents are between the age of 31 and 50, followed by 29.5 % of respondents between 18 and 30. In terms of income, majority of respondents earn less than ₹12,000 per month (Table 1).

Demographic Profile of Respondents.

Data Analysis Tools

The study used the value of skewness and kurtosis to assess the normality of data. After those various methods of data analysis, that is exploratory factor analysis (EFA), confirmatory factor analysis (CFA) and structural equation modelling (SEM) are used to investigate the primary data. Multigroup modelling technique is used to measure the moderating effect. Purification of scale items and assessment of reliability and validity is accomplished using EFA and CFA on the data. In addition, SEM was applied to examine the hypotheses of the current study. SPSS 25.0 and AMOS 25.0 are used for data analysis.

Analysis and Results

For the relevance of the proposed tool, it is prerequisite that data should be normally distributed. Data can be considered as a normally distributed if the value of skewness lies between −3 and +3 and kurtosis value lies between −10 and +10 (Kline, 2013). Results of the skewness and kurtosis for all items are found in the above-mentioned range. Subsequently, it had been presumed that data accomplished the assumption of normality.

Exploratory Factor Analysis

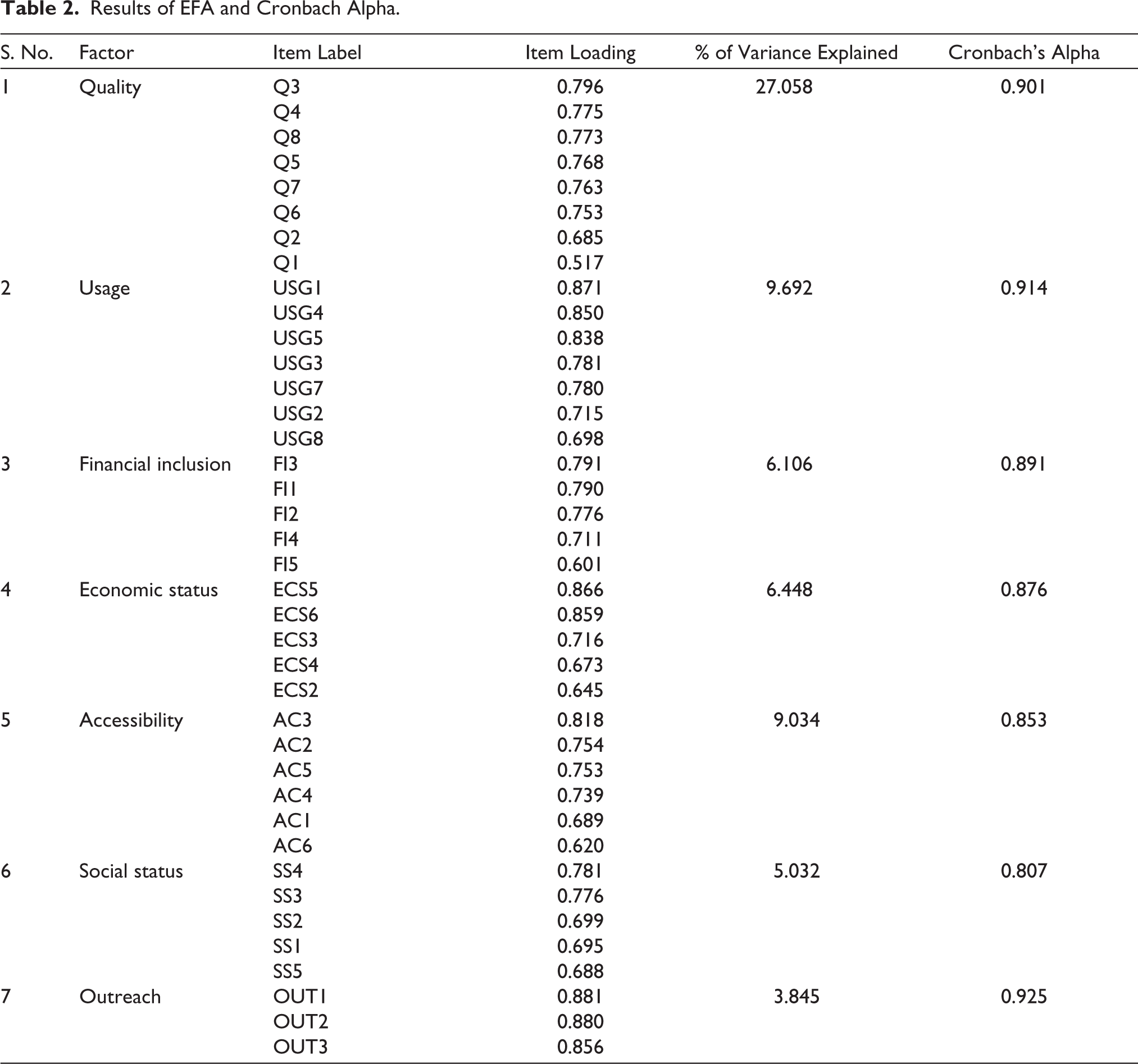

Seven factors were identified based on EFA using the principal component method with varimax rotation. These identified constructs are outreach, accessibility, usage, quality, financial inclusion, economic status and social status. All extracted factors have eigenvalues greater than 1 (Malhotra & Dash, 2020). The data shown in Table 2 demonstrated that the loading of items of each construct is highly substantial as the items loaded with a value of more than 0.50 (Hair et al., 2013). Due to lower loading values, certain questions were omitted from the list, including USG6, ECS1, SS6, SS7 and SS8. Thus, the original 44 questions were reduced to a more practical 39 questions with more than 0.50 loading. As per the results, Kaiser Meyer–Olkin (0.868) measure indicates the adequacy of sample size, and Bartlett’s sphericity test suggests a high degree of significant correlation between the statements given in the research (10,487.434, significant p value at the 1% level). All Cronbach’s alpha values reported in Table 2 for estimated factors in this study are more than 0.80 and are considered reliable (Kline, 2013).

Results of EFA and Cronbach Alpha.

Measurement Model

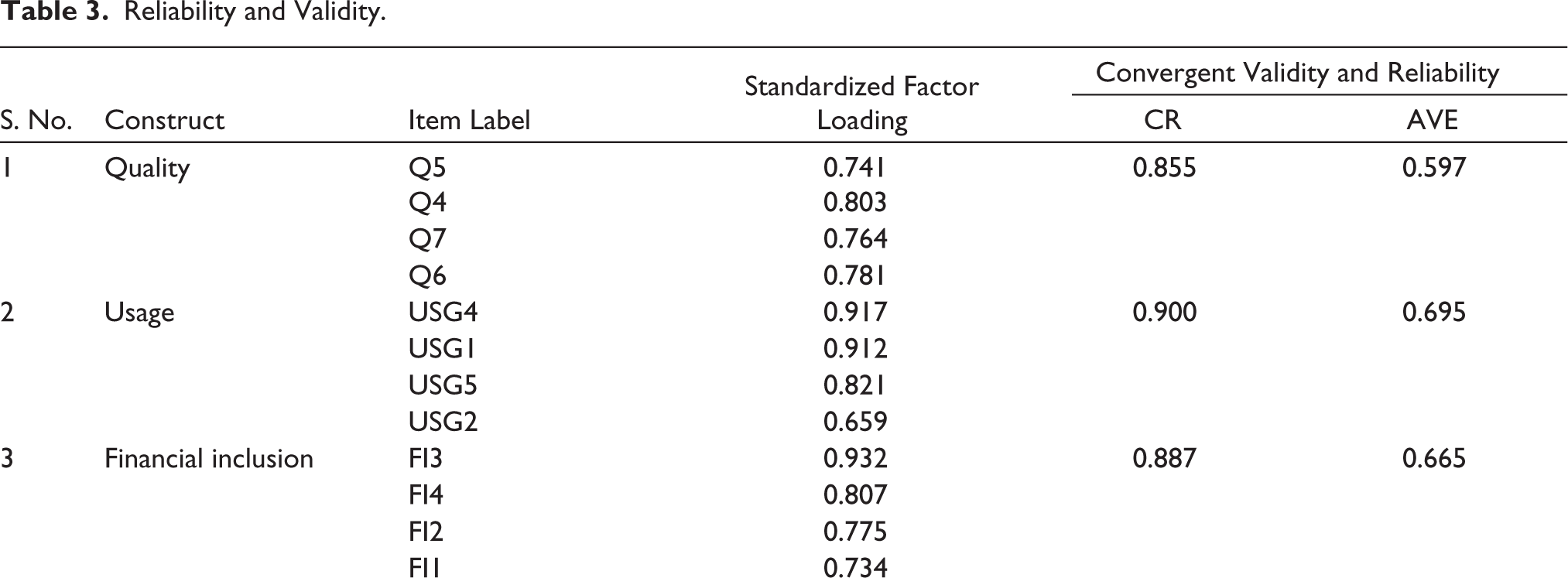

Following the identification of seven factors by EFA, the underlying factors were confirmed through CFA. The CFA analysis aims to ascertain the extent to which latent constructs generate evident variables. By following the recommendation of Hair et al. (2013), USG3, USG7, USG8, Q1, Q2, Q3, Q8, AC3, AC6 and FI5 are deleted from the latent constructs because of loadings less than the threshold of 0.60. It was done to improve the constructs’ validity. The results of the measurement model with regard to goodness of fit statistics (Table 5) reported that χ2/df ratio is 2.556, which is below the cut-off value level of 5, indicating a strong model fit (Byrne, 2010). According to the model, the RMSEA value is 0.063, the GFI value is 0.870 and the AGFI value is 0.840, all of which meet the threshold value (Hair et al., 2013). Additionally, incremental fit indices indicated that TLI is 0.908, CFI is 0.920 and IFI is 0.920. These values of more than 0.900 indicate that the suggested model is well-fitted (Hair et al., 2013).

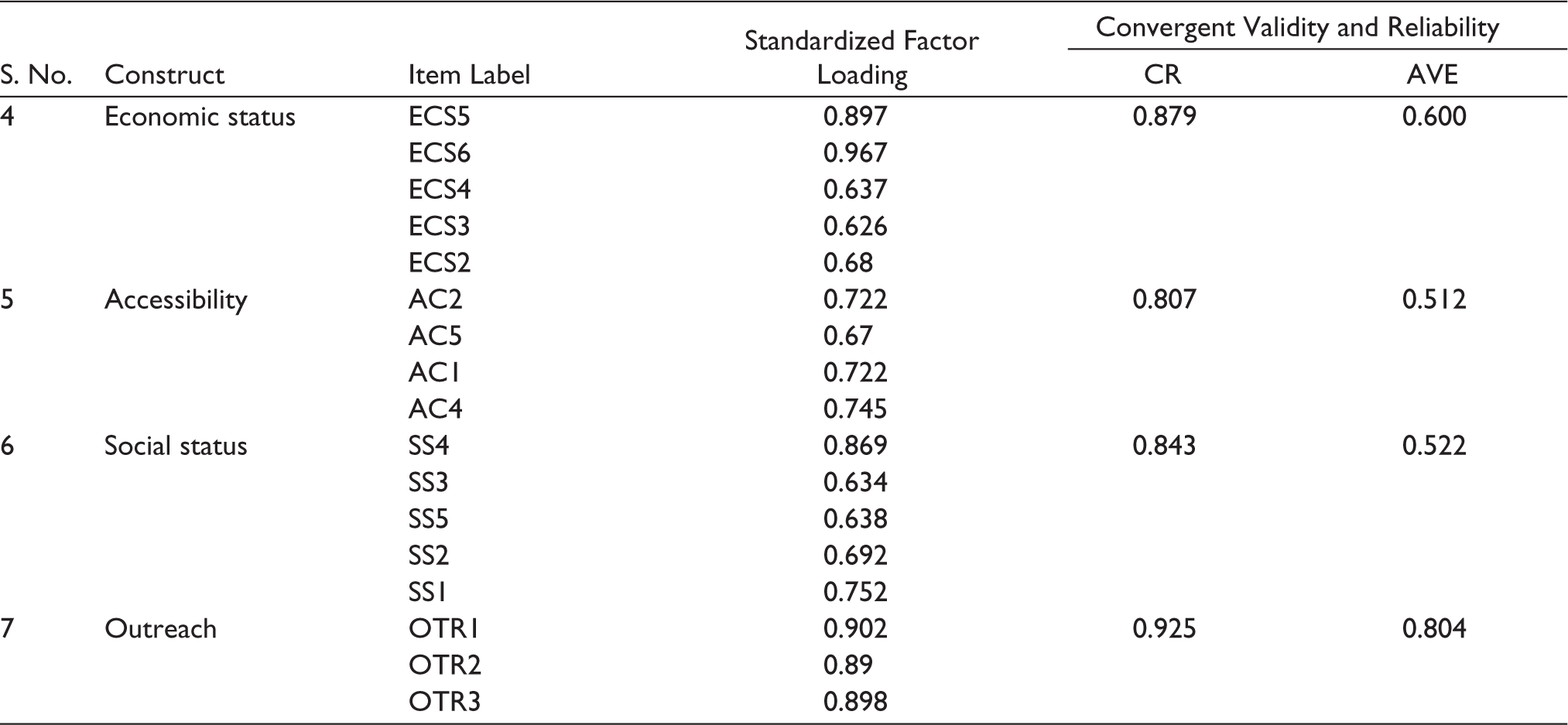

After analysing the model fit criteria, assessing the measuring instrument’s reliability and validity is necessary. Table 3 describes the validity of the measurement model. Two assumptions must be considered while determining convergent validity. First, composite reliability (CR) of constructs must exceed 0.7. Second, the value of AVE (average variance extracted) should be more than 0.05 (Hair et al., 2013). As shown in Table 3, CR values of all constructs in this current research are more than 0.7, indicating that the constructs are reliable.

Reliability and Validity.

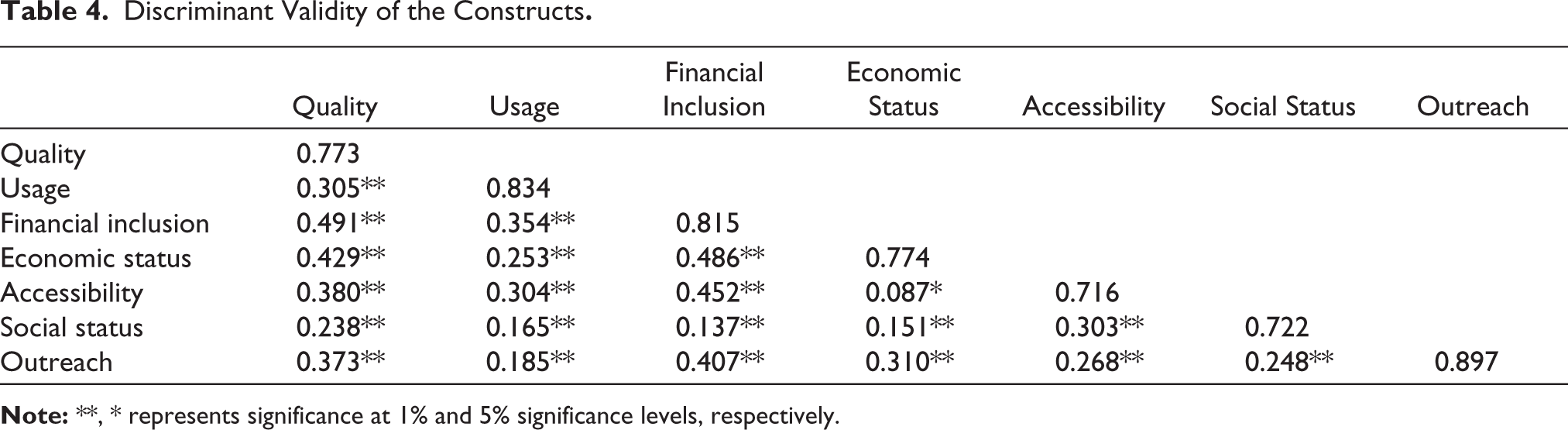

Additionally, AVE values of all constructs are found to be greater than 0.50. Thus, the data set satisfied the convergent validity assumption of the model. The values for discriminant validity are summarised in Table 4. The bold numbers on the diagonal indicate the square root of AVE (SRAVE), whereas the numbers off-diagonal reflect correlations between the constructs. According to the analysis, the correlations between the two constructs are smaller than the SRAVE values, which shows a high degree of discriminant validity (Fornell & Larcker, 1981) in case of all latent constructs.

Discriminant Validity of the Constructs.

SEM Analysis and Testing of Hypotheses

Hypothesized association of constructs is analysed using SEM because this technique determines the robustness of hypothesized connections between several latent components (Hair et al., 2013). SEM is applied based on 29 measurement items under seven extracted constructs in this current research. The structural model is evaluated using a set of fit indices. The assessment of the statistical feasibility of the structural model demonstrates that χ2/df ratio is 2.725, which is below the cut-off value level of 5 (Table 5). All other model fit indices (GFI = 0.861, AGFI = 0.832, RMSEA = 0.066, FII = 0.909, TLI = 0.898 and CFI = 0.909) are within the suggested range (Byrne, 2010; Hair et al., 2013).

The Goodness of Fit Statistics for CFA and SEM.

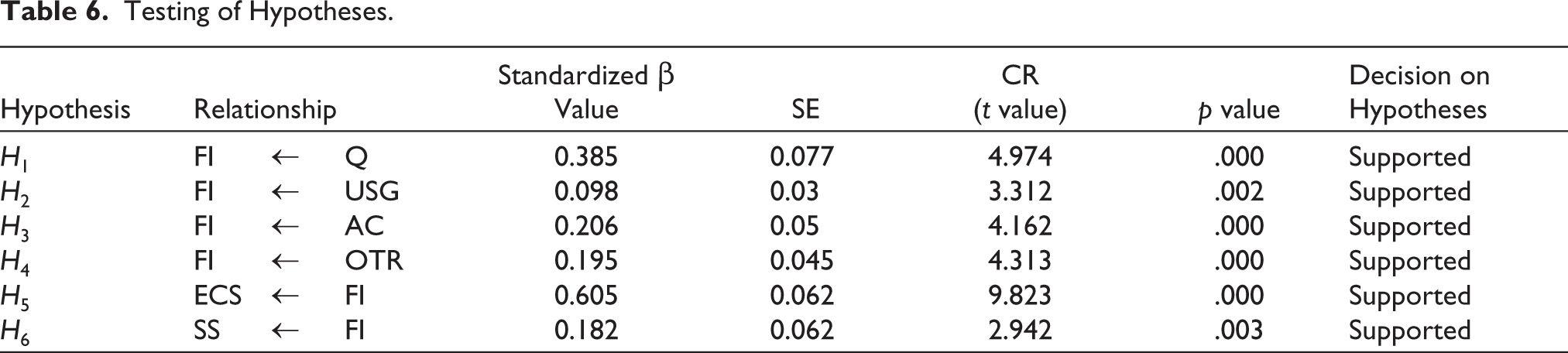

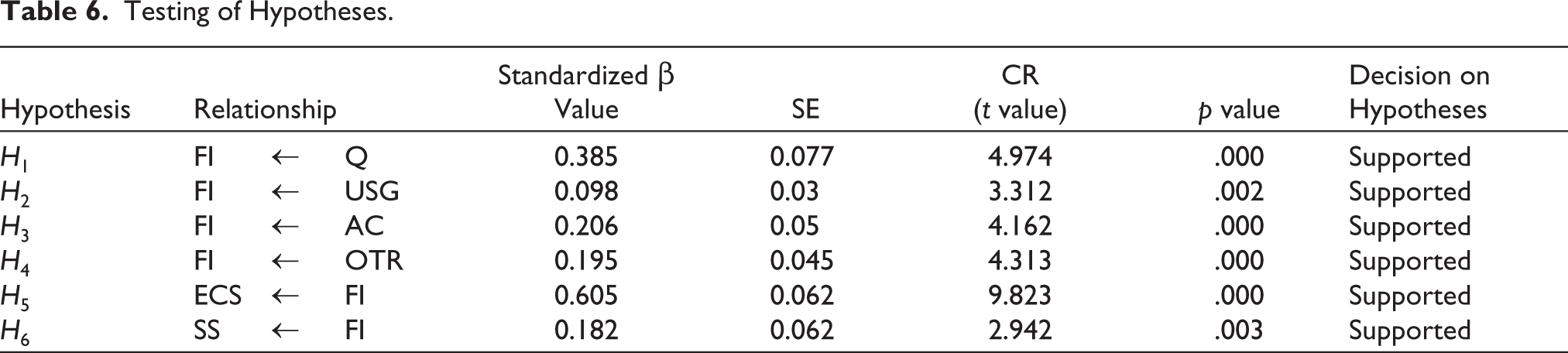

The result statistics of the multivariate analysis technique ‘SEM’ are presented in Table 6. The hypothetical associations are evaluated using regression beta (β) values and critical ratios. In order to prove the causal correlations between constructs are statistically significant at 1 %, the critical ratio (t values) must exceed 1.96 and the p value should be less than 0.01 (Hair et al., 2013). The quality of financial services and regular usage of bank accounts are found to be a statistically significant factors in promoting financial inclusion for the PMJDY scheme (H1: β = 0.385, t value = 4.974, p < .01; H2: β = 0.098, t value = 3.312, p < .01). Similarly, the hypothesis that access to financial services, and outreach to financial services are important determinant in promoting financial inclusion concerning PMJDY scheme are also found statistically significant(H3: β = 0.206, t value = 4.162, p < .01; H4: β = 0.195, t value = 4.313, p < .01). Further, it was also found that the impact of financial inclusion, as facilitated by the PMJDY scheme which makes financial inclusion easier, has a positive effect on the economic status and social status of marginalized people (H5: β = 0.605, t value = 9.823, p < .001; H6: β = 0.182, t value = 2.942, p < .01). In a nutshell, the findings of the study verified that all of the hypotheses (H1–H6) are statistically proved.

Testing of Hypotheses.

To examine the moderating effect of income, group analysis is undertaken with the sample divided into two income groups. The results from Table 7 reveal that financial inclusion (β = 0.909, p = .000) strongly predicts economic status among the high-income group and significantly associated with economic status (β = 0.459, p = .000) among low-income group. To test the hypothesis, z score statistics is estimated and compared across groups. The findings explored higher effect of financial inclusion on economic status in the high-income group in comparison to low-income group (z = 3.244 > 1.96). Thus, this supports the Hypothesis 7 that income moderates the association between financial inclusion and economic status. Further, it can also be seen from the Table 7 that financial inclusion (β = 0.274, p = .000) strongly predicts social status among the high-income group. However, financial inclusion has insignificant impact on social status among low-income groups. On the basis of z score statistics, the findings indicated that income is not moderating between financial inclusion and social status of marginalized people (z = 1.309 < 1.96).

Testing Moderation Effect of Income.

Discussion

The suggested study model is analysed to determine hypothetical relationships of the extracted factors of financial inclusion (outreach, accessibility, quality and usage) on financial inclusion concerning the PMJDY scheme that authors observed scantly in the literature. A structural model combining determinants of financial inclusion concerning PMJDY and socioeconomic status of marginalized people is the unique contribution of this present research. According to the findings of SEM, financial services quality under the PMJDY scheme is the most crucial and significant determinant in terms of financial inclusion that ensures people’s access to formal financial services. Many earlier researchers have found similar outcomes (Lal, 2018, 2019; Okello Candiya Bongomin et al., 2017). The current analysis of the study demonstrates that quality of banking services and products offered by banks under the PMJDY plan assists marginalized groups in entering the formal banking system and contributes to the government’s goal of universal financial inclusion in India. Further, frequent use of variety of banking financial services under PMJDY scheme strongly participate in financial inclusion of marginalized people who have opened bank accounts under PMJDY scheme. Consequently, indicating that usage by marginalized people should be increased to boost financial inclusion. The outcome is analogous to the results of other earlier research analysing financial inclusion (Beck et al., 2007; Ghosh, 2011; Kendall et al., 2010; Nandru et al., 2021; Nandru & Rentala, 2019). Although, usage of banking services is found to be a least impacting factor in this study. Further, accessibility to financial services under PMJDY scheme is also found as a critical predictor of financial inclusion. It demonstrates that facilitating access to financial services under the PMJDY scheme aids marginalized persons in connecting them with the financial system. This result is in line with numerous preceding researches for predicting financial inclusion (Chakravarty & Pal, 2013; Goel & Sharma, 2017; Gupte et al., 2012; Nandru et al., 2021; Nandru & Rentala, 2019; Noelia & David, 2015). Moreover, the findings suggest that outreach to financial services under the PMJDY scheme is a crucial determinant of financial inclusion for marginalized people under the PMJDY scheme. Hence, marginalized people of the country can be better connected with the national financial system by enhancing the outreach of financial services under PMJDY scheme. Past studies have also demonstrated that a lack of physical outreach is problematic for financial inclusion (Gupte et al., 2012).

As, PMJDY scheme was started with the aim to expanding national financial inclusion for promoting the socioeconomic condition of marginalized people in the country, hence the effect of PMJDY scheme on the socioeconomic status of marginalized people was also analysed in this study. Lal (2021) found that the economic prosperity of marginalized populations significantly influences financial inclusion. The current study suggests that the economic status of marginalized people is significantly impacted by PMJDY scheme for financial inclusion. Hence, outreach, usage, quality and access to financial services under the PMJDY scheme will effectively improve the economic status of marginalized people. This improvement in economic status through financial inclusion helps to reduce poverty (Lal, 2018). Various other studies also support the results (Bhatia & Singh, 2019; Maity, 2016; Nandru & Rentala, 2019; Swamy, 2014; Varghese & Viswanathan, 2018; Yadav et al., 2021). The research established that financial inclusion through PMJDY also significantly influenced the social status of marginalized people. This finding is supported by various previous studies on financial inclusion (Beck et al., 2009; Demirguc-Kunt & Klapper, 2013; Maity, 2016; Nandru & Rentala, 2019; Swamy, 2014). Hence, focus on various services under the PMJDY scheme will effectively improve the social status of marginalized people.

Further, the result indicates that financial inclusion with PMJDY has a higher impact on economic status for higher-income marginalized people than for low-income marginalized people. It is because people with higher income have greater access to formal banking services than those with lower income (Demirguc-Kunt et al., 2018). Additionally, the study found that income does not play a moderating role between financial inclusion and the social status of marginalized people. It can be said that financial inclusion equally contributes to enhance the social status of people despite their income. Gallego-Losada et al. (2023) asserted that financial inclusion is a crucial measure of social development, as it has the potential to contribute to poverty reduction, narrow the income disparity and facilitate increased savings. Thus, regardless of income, financial inclusion contributes equally to the improvement of people’s social status in all PMJDY beneficiaries. This is because of the access to number of services like loans, savings accounts and insurance which can assist individuals and families in enhancing their economic well-being and stability. Additionally, access to these services can contribute to increased confidence and empowerment among individuals, thereby enhancing their social standing for all income group marginalized people. In a nutshell, the current study proved that determinants of financial inclusion through PMJDY are responsible for the socioeconomic development of marginalized people in India. Therefore, efforts should be continued by policymakers to improve financial inclusion through PMJDY.

Conclusion and Policy Implication

The research concentrates on PMJDY plan for exploring the determinants of financial inclusion and its influence on the marginalized people’s socioeconomic status in Himachal Pradesh, India. The study confirms that outreach, accessibility, usage and quality of banking services under PMJDY are greatly helpful to determine financial inclusion and hence, recognized as drivers of financial inclusion in India. Further, financial inclusion promoted by PMJDY scheme has a causal relationship with the socioeconomic status of marginalized people and helps marginalized people to improve their socioeconomic status. The study’s findings highlight important policy implications for improving socioeconomic status of India’s marginalized population. One of the significant implications of the study is that policymakers must prioritize quality, accessibility, outreach and usage of financial services under PMJDY to accomplish the goal of socioeconomic progress with financial inclusion in India. Quality of services is found as the most potential factor to favourably impact the purpose of financial inclusion. There is need to facilitate safe and secure banking services to improve the quality of banking operations. Policymakers should provide proper guidance towards financial literacy. Further, Indian government must do efforts to increase additional beneficiaries in the formal banking system. This will enhance the accessibility of banking services which is found as an essential determinant of financial inclusion in the current study. Bank infrastructural facilities, such as bank branches, ATMs and post offices, are also required to be enhanced for more outreach of formal banking. However, merely opening a bank account and infrastructural facility under PMJDY will not achieve the desired aim. This is intended to increase the utilization of financial services also. However, this study revealed that utilization of banking services has the most negligible influence on PMJDY scheme generated financial inclusion compared to other identified factors. This leads to the conclusion that people who opened bank accounts under the PMJDY scheme have minimal usage of banking services, which is a severe concern for government. Hence policymakers should be more concerned about increasing the usability of financial services. It can be improved by promoting digital payments like UPI and debit card transactions. It is important to note that financial inclusion reduces income inequality, as poverty has been significantly reduced because of this key factor in various countries (Omar & Inaba, 2020). The current study also concluded that financial inclusion has a higher impact on economic status for higher-income marginalized people than for low-income marginalized people. However, regardless of income, financial inclusion contributes equally to the improvement of people’s social status of all PMJDY beneficiaries. This suggests that financial inclusion policies with regard to PMJDY should be tailored to meet the specific requirements of various income categories. In addition, it emphasises the significance of confronting systemic inequalities that prevent low-income marginalized individuals from receiving the full benefits of financial inclusion initiatives.

Limitations and Future Research Directions

This current research is conducted from the perspective of beneficiaries under the PMJDY scheme only. however, future research may be undertaken from the viewpoint of the banks that are the service providers. The present study did not consider all determinants that may affect financial inclusion. Hence, further studies may be conducted to explore additional drivers of financial inclusion, including income, online banking, financial literacy and affordability. Finally, further studies can be extended to measure the effectiveness of PMJDY scheme on financial well-being, economic empowerment and social empowerment of individuals of other geographical locations in India. This result will assist in identifying the requirements of financial inclusion initiatives and utilizing financial resources optimally for better financial inclusion throughout the country.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

Constructs.

| S. No. | Construct | Code | Variables |

| 1 | Accessibility | AC1 | The number of documents required for opening a bank account is few. |

| AC2 | Minimum balance required by the banks is affordable. | ||

| AC3 | The cost of making a trip to the bank is affordable. | ||

| AC4 | Convents working for complete banking transaction. | ||

| AC5 | Availing bank loan through PMJDY is easy. | ||

| AC6 | There are many bank branches nearby. | ||

| 2 | Outreach | OTR1 | Easy to reach the bank branch in the local area/village. |

| OTR2 | Easy to reach the ATM in the local area/village. | ||

| OTR3 | Easy to reach the business correspondent network manager in your residence. | ||

| 3 | Usage | USG1 | Save money in a savings bank account regularly. |

| USG2 | Visit the bank branch to withdraw money. | ||

| USG3 | Visit the bank branch to transfer money. | ||

| USG4 | Use a Rupay debit card/ATM card for withdrawal. | ||

| USG5 | Use locker facility to safeguard valuables. | ||

| USG6 | Visit bank branches regularly for repayment of loan/ overdraft amount. | ||

| USG7 | I use the bank account for the credit facility. | ||

| USG8 | I am comfortable with the terms and conditions of repayment of bank loan. | ||

| 4 | Quality |

Q1 | The cost of financial products is affordable. |

| Q2 | Easy accessibility to all relevant and sufficient information (pricing, key features, terms and conditions) about the financial services. | ||

| Q3 | Loan products provided by banks suit our needs. | ||

| Q4 | Savings products provided by banks suits our needs. | ||

| Q5 | Payment services provided by banks suit our needs. | ||

| Q6 | Savings products provided by banks satisfy us. | ||

| Q7 | Payment services provided by banks satisfy us. | ||

| Q8 | Loan products provided by banks satisfy us. | ||

| 5 | Financial inclusion | FI1 | I access the banking services under PMJDY. |

| FI2 | I get credit from the bank for my financial needs. | ||

| FI3 | I can avail credit for improving my business if I have a bank account. | ||

| FI4 | I can access the financial benefits of government schemes, insurance, pensions, and so on. | ||

| FI5 | My financial needs are fulfilled by the PMJDY scheme. | ||

| 6 | Economic status |

ECS1 | Reduces the borrowing from money lenders. |

| ECS2 | Increase in the savings habit, so we can use money in an emergency. | ||

| ECS3 | Creation of own assets. | ||

| ECS4 | Monthly consumption expenditure has increased. | ||

| ECS5 | Increase in various income sources. | ||

| ECS6 | Improvement in standard of living. | ||

| 7 | Social status | SS1 | Able to take the decision regarding the children’s education. |

| SS2 | Easy to make decisions regarding health care and the purchase of daily necessities. | ||

| SS3 | Improvement in the social image. | ||

| SS4 | Actively participate in community festivals. | ||

| SS5 | After availing of banking services, public relations are improved. | ||

| SS6 | Actively participate in the campaign for candidates. | ||

| SS7 | Decision-making regarding electing the candidates in the local elections. | ||

| SS8 | Aware of the various government schemes such as SBLP and MGNREGAs. |