Abstract

The rising surge of corruption and financial fraud cases seems to be urging the inclusion of forensic accounting in the educational curriculum, particularly in developing countries. This study examines the current state of forensic accounting education in India and explores its effectiveness through the prism of commerce and management students. It reveals an increasing demand for forensic accounting education because of the increasing fraud cases. Students perceive that forensic accounting professionals are pivotal in preventing and reducing fraud incidents and enhancing financial reporting quality. However, there are several challenges that hinder the expansion of forensic accounting education in India, such as limited awareness, insufficient resources, shortage of trained faculties and perceived scarcity of career opportunities. Further, the underrepresentation of the multidisciplinary nature of forensic accounting and the struggle to balance while integrating theory with practice are additional obstacles. Despite these hurdles, there is a strong interest among students in integrating forensic accounting topics into the existing curriculum.

Keywords

Introduction

Background of The Study

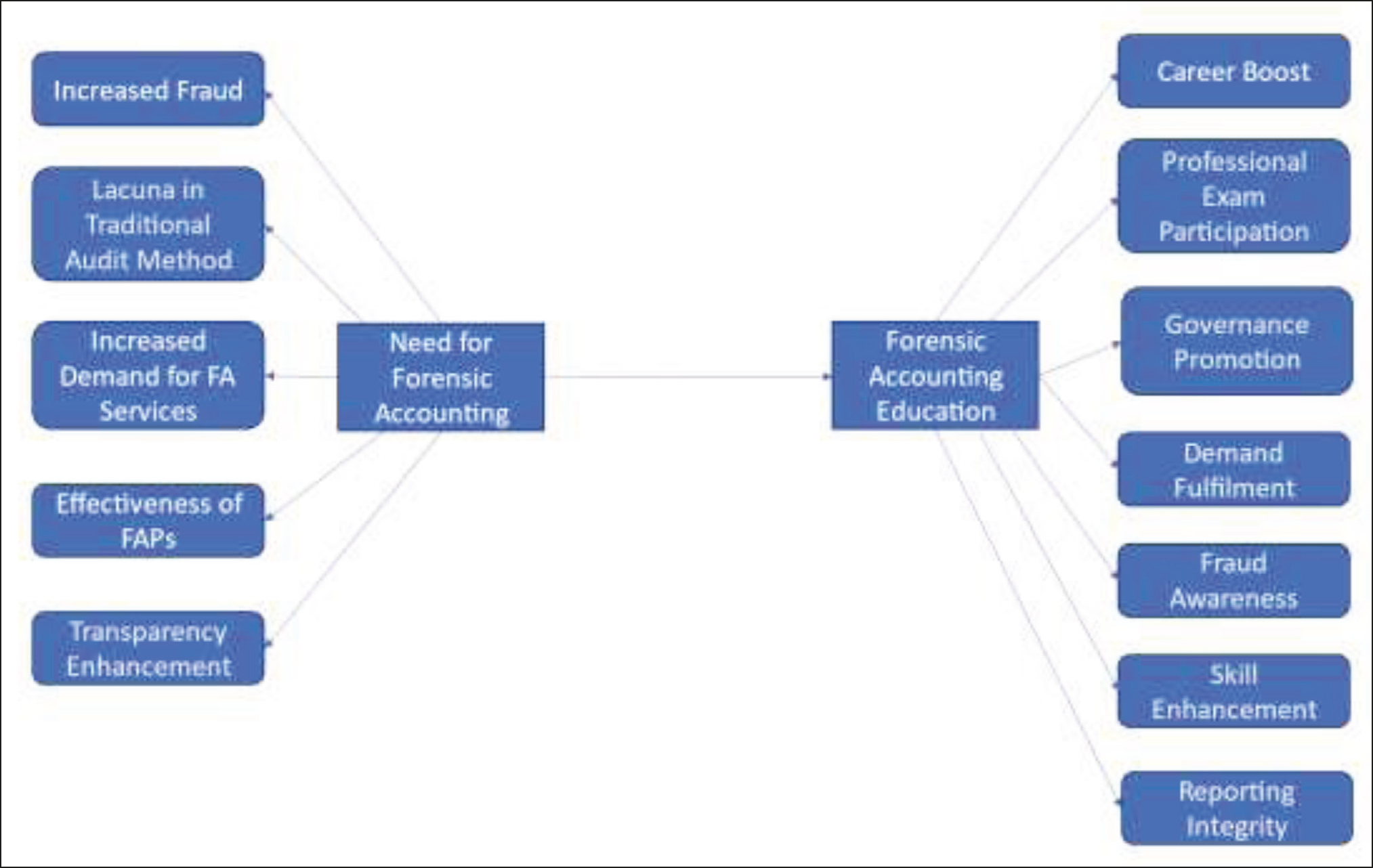

A string of corporate scandals, including Enron, WorldCom, Parmalat and Toshiba, has shaken the confidence of diverse stakeholders. It has raised serious doubts over the integrity and relevance of the accounting and auditing profession, bringing forensic accounting (FA) practice to emergence (Rezaee et al., 2016; Bhavani & Mehta, 2018). In this light, the rudimentary objective of FA is to identify and reduce fraud in organizations. According to Tiwari and Debnath (2017), FA practice involves meticulous data gathering and analysis in contexts such as litigation support, consulting and non-scientific testimony. Globally, there is a growing need for FA, as can be discerned from its ever-evolving volume of literature (Huber & DiGabriele, 2014; Honigsberg, 2020; Ozili, 2020). According to Yang and Lee (2020), FA has significant applications for businesses and their stakeholders. Furthermore, the relevance of FA is not limited to businesses alone. Fraudulent activities also impede a nation’s progress. In this regard, Ehioghiren and Atu (2016) suggest the engagement of forensic accounting professionals (FAPs) to reduce the risks of financial crimes and ensure good governance practices.

The rising demand for FA services necessitates specialized professional education (Brooks & Labelle, 2006). Current views on forensic accounting education (FAE) emphasize the development of rigorous and relevant FA curricula to make the graduates industry-ready (Oleiwi, 2023; Al-Daoud et al., 2023). FA curriculum that not only imparts theoretical knowledge but also hones practical skills and ethical judgement, aligning educational outcomes with professional expectations, is thus vital in the present context (Tarjo et al., 2021; Alsheikh et al., 2022). It is corroborated by a systematic literature review, which indicates a positive correlation between comprehensive FAE and the effectiveness of fraud detection and prevention (Kaur et al., 2023). Numerous studies have explored the availability of such education (Alshurafat et al., 2020; Kramer et al., 2017; Rezaee et al., 2016; Seda & Kramer, 2015; Wang et al., 2016). They attest that adding FA to the curriculum is thus necessary to improve the skills of accountants (Bhasin, 2013).

While research in developed countries, such as the United States (Kramer et al., 2017) and Australia (Alshurafat et al., 2019), has substantiated the significance of FAE and its assimilation into the curriculum, a discernible gap exists between FA practices and education, particularly in emerging economies including India (Al-Balqa et al., 2021; Hidayat & Al-Sadiq, 2014; Ibadov & Huseynzade, 2019; Okoye et al., 2020). Further, prior studies have predominantly revolved around the perceptions of academicians and practitioners, leaving a significant lacuna regarding the educational inclinations of students poised to enter this field (Seda & Kramer, 2015; Kramer et al., 2017). Consequently, this study aims to explore students’ viewpoints concerning the future and potential of FAE in India.

In India, incorporating FA into accounting education is a neoteric concern. This study is of paramount importance for three distinct reasons. First, this exploration is particularly timely and relevant given the critical significance of FA in the current milieu of business operations and the embryonic phase of FAE within the Indian academic landscape. It is an arena scarcely examined before, especially from the students’ vantage point. Second, the recent issuance of the Forensic Accounting and Investigation Standards (FAIS) by the Institute of Chartered Accountants of India (ICAI) is another push to standardize the FA practice in India, making FAE imperative. Third, the study’s temporal congruence with India’s New Education Policy (NEP) implementation offers a distinctive framework for investigating the possibility of the FAE’s interdisciplinary approach in fostering a more holistic and practical curriculum. This in turn may aid in strengthening the readiness of future professionals in this field.

By examining the incorporation of FA into the Indian accounting education system from the perspective of commerce and management students, this study adds pioneering evidence to the existing stream of research. It has important implications for the education sector because it outlines the best ways to integrate FAE into current accounting curricula.

Data for the study was garnered from students on the opportunities and challenges within FAE. It includes an assessment of the need for FA, challenges and related benefits of FAE.

This article is structured into the following segments. The immediately preceding section elaborately discusses the extant literature attributed to the domain followed by the methodology section. In the next segment, the results obtained are discussed. Finally, the concluding remarks mark the end of this study.

Research Context

Numerous fiascos, such as Yes Bank (₹20,000 Cr), Punjab National Bank (₹14,000 Cr), DHFL (₹31,000 Cr) and more, have rocked the Indian financial sector, thereby greatly wavering the confidence of the stakeholders (Gangwani, 2020). To reinstate their confidence, the implementation of FAE has become quintessential. Given its exigency, the ICAI has introduced a FA certification programme to equip its members with the requisite FA expertise. Further developments in this regard have also been witnessed from the Institute of Cost and Management Accountants (ICMAI), which has formulated a similar diploma course for its members and final-year students. The Pune-based training and educational organization, IndiaForensic, has also pioneered FA courses, both independently and in collaboration with the National Stock Exchange of India. Nationwide, several universities have also come forward to incorporate FA in their curriculum. Notable among them are Pondicherry University, the Central University of Karnataka and the Central University of Haryana.

Moreover, to combat the ever-escalating magnitude of fraud, the Government of India established a specialized agency, the Serious Fraud Investigation Office, in 2015 to curb such malpractices under the aegis of the Ministry of Corporate Affairs. Additionally, the introduction of FAIS by ICAI to standardize the FA practices in the nation is yet another diligent effort in this direction.

Theoretical Framework

Economic crimes in the current era reiterate time and again the exigency of FA (Chetry et al., 2023, 2024). This need for FA is embedded in the inefficacy of traditional audits to counter advanced fabrications of recent origin (Rezaee et al., 2004). The benefits attributed and efficacy documented by FA further reinstate its demand (Al-Balqa et al., 2021; Ebaid, 2022; Ismail et al., 2018). With the growing demand for FA, the need to hone FAE comes to light (Carpenter et al., 2011; Rezaee et al., 2004). This is plausible as FAE boosts job prospects (Melancon, 2002), encourages professional certification and promotes good corporate governance (Luke, 2013). It fosters social change towards greater transparency (Carpenter et al., 2011). FAE prepares professionals to enhance the credibility of financial reporting (Lee et al., 2015) and meet industry demands (Okoye et al., 2020), thus contributing to a more transparent financial environment. The growing demand for FA in India necessitates the enhancement of FAE. FAE prepares future professionals to instil integrity in financial reporting and governance. It has the potential to help reduce the chances of fraud and increase the credibility of the financial sector.

Furthermore, educational research houses numerous theoretical constructs that propose variegated knowledge dissemination options. These theoretical underpinnings are germane to inform the development of any discipline of knowledge. This study explores the potential relevance of FAE in India through the theory of planned behaviour (TPB). Many studies have used the TPB to understand and predict various human behaviours, such as choosing leisure activities, seeking jobs, applying to graduate school and selecting a career (Ajzen, 2001). This theory provides a broad model for behaviour suitable for studying students’ intentions and choices regarding their majors. The application of TPB in educational research, particularly in the accounting and management domains, is well-established. For instance, Cohen and Hanno (1993) and Allen (2004) utilized TPB to examine students’ perspectives and choices of business majors, while Tan and Laswad (2006) investigated students’ intentions to major in accounting and non-accounting disciplines. The TPB specifically focuses on the psychological antecedents of intention, making it particularly suitable for this study. The TPB, developed by Ajzen (1988), is an extension of the Theory of Reasoned Action (TRA) developed by Fishbein and Ajzen (1975). TPB posits that behavioural intention is determined by three primary constructs: attitude towards the behaviour, subjective norms and perceived behavioural control (Ajzen, 1991; Armitage & Conner, 2001). Attitude reflects an individual’s favourable or unfavourable evaluation of the behaviour; subjective norms represent the perceived social pressure to perform or not perform the behaviour; and perceived behavioural control denotes an individual’s belief in their ability to execute the behaviour.

In the context of this study, the behaviour in question is the pursuit of FAE. By examining the interplay of attitudes, subjective norms and perceived behavioural control, the study aims to provide valuable insights into students’ decision-making processes. The study’s findings shall enable policymakers and regulators to design appropriate curricula for enhancing FAE in the country. Attitudes towards FAE include students’ beliefs on perceived effectiveness, demand, challenges and benefits of FAE. Subjective norms encompass the awareness regarding FAE, perception of corruption, fraud and effectiveness of traditional audit methods. Perceived behavioural control involves students’ satisfaction, an appropriate approach for integration and curriculum design. The findings of the study will help policymakers understand students’ views on the challenges, benefits and potential of FAE in India, using the TPB to design effective curricula.

Literature Review

Forensic Accounting Education

To be effective, FAPs must be equipped with the necessary knowledge, skills and abilities (Brooks & Labelle, 2006). According to the existing literature, FAE has evolved from a limited aspect of professional education for practicing accountants to a standalone course (Crumbley et al., 2015; Kramer et al., 2017; Kranacher et al., 2008; Rezaee & Burton, 1997). There are several universities and international accounting bodies in developed nations such as the United States, Australia and Canada that offer FAE courses (Seda & Kramer, 2015; Alshurafat et al., 2019)

Conceptual Framework.

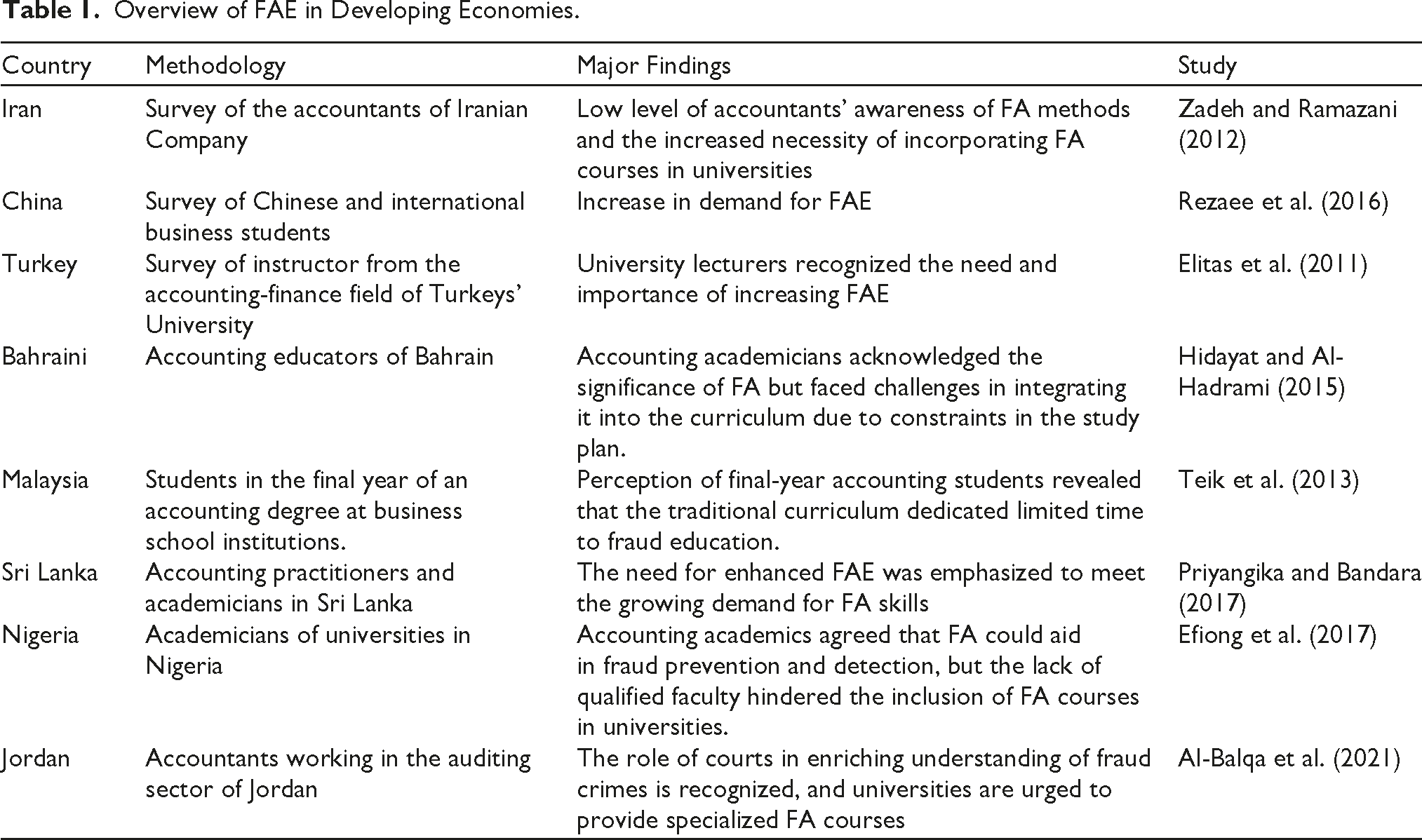

Table 1 presents an overview of FAE in developing countries. In contrast to advanced economies, there exists a widespread disparity in the demand for FAPs and the prevalence of FAE in emerging economies. It quintessentially commands urgent developments in FAE. Factors such as increasing financial fraud and technological advancements further accentuate this demand (Pearson & Singleton, 2008). Empirical evidence argues that traditional accounting education lacks in equipping its students with tactics and expertise to tackle modern-day fraud (Pearson & Singleton, 2008; Rezaee et al., 2016). Asserting the need for inclusion of FA courses in the accounting curriculum, Buckhoff and Schrader (2000) attest that incorporating FA courses can help equip scholars with the expertise to counter fraud and thus be of substantial aid in reinstating the confidence of the diverse stakeholders. Consequently, many universities have started offering FAE as honours, minors and certificate programmes (Kramer et al., 2017). Adding to it, Akyel (2012) states that for FAE to combat fraud effectively, it should include knowledge of financial transactions, investigative techniques, legal testimony and criminology.

Overview of FAE in Developing Economies.

Skill Sets and Technique Required for FA

FA is a sophisticated and advanced extension of traditional accounting and auditing practices and demands a broader skill set. The quality and quantum of fraud detection by an FAP is contingent on his/her skill set (Christensen et al., 2005; DiGabriele, 2008). Being a multidisciplinary area, FA requires a wide array of knowledge, including accounting, law, information technology, criminology, psychology and sociology (Kresse, 2008). Broadly, the skill sets of an FAP can be categorized into core skills and enhanced skills. While core skills are foundational to the profession, enhanced skills are acquired through experience (Ozili, 2015). While core accounting skills are integral to FA, acquired analytical and synthesis skills, critical thinking, investigative flexibility and legal knowledge are also crucial. Nevertheless, any skill can be deemed pertinent contingent upon its ability to detect and combat fraud (Oyerogba, 2021). It is, however, imperative to note that these skills may vary across nations (Prabowo, 2013).

Challenges in FAE

Standardizing the FAE curriculum is difficult owing to its contingent and multidisciplinary nature (Chetry et al., 2023). However, law, accounting, criminology, psychology and sociology are the thrust areas that must be included in the curriculum (Kresse, 2008). Another challenge in FAE, according to Cook and Clements (2009), is inconsistency in the mode and content of instruction. According to Fleming et al. (2008) and Chetry et al. (2024), several factors might hinder the delivery of FAE. These may include a rigid curriculum, lack of textbooks and instructional resources, lack of administration interest and support and lack of faculty engagement. One strategy to mitigate these shortcomings is to include FA themes in courses like auditing and accounting.

Research Methodology

Survey Description

The present study is exploratory in nature. A structured questionnaire was administered to collect data from commerce and management students enroled in Indian universities. The collected data was then analysed and summarized using descriptive statistics, specifically mean and standard deviation. Given the non-normal distribution of the data, a nonparametric test, specifically the Mann–Whitney U test, was employed to compare two related samples. As Tiwari and Debnath (2021) explain, this test assesses differences in population mean ranks between two related samples. Hence, the respondents were purposefully divided into two distinct groups. The first group comprised students pursuing BCom/MCom in other specializations (59.8%). The second group consisted of students enroled in BCom/BBA/MCom/MBA programmes focusing on FA specialization and professional certificate courses (40.2%), such as CA/CS/CMA. The subsequent section of the study delved into the perspectives of commerce and management students concerning integrating FA concepts into their accounting education. This section comprised six categories of questions, which were developed based on studies conducted in various countries (Ebaid, 2022; Hidayat & Al-Sadiq, 2014; Ibadov & Huseynzade, 2019; Rezaee et al., 2004; Rezaee et al., 2016; Seda & Kramer, 2008; Yusof et al., 2007).

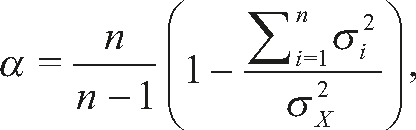

Following the collection of demographic information, students were asked about their awareness of the term ‘FA’ to be responded with either ‘Yes’ or ‘No’. The analysis was conducted based on the affirmative responses. The next set of questions harnessed the students’ perception of the necessity of FA. This set consisted of questions to assess the students’ understanding of the escalating corruption and the efficacy of traditional audit practices in detecting and combatting it. Subsequently, the responses for the prospect of FA as a profession in India were secured by a 5-point Likert scale ranging from 1, which denotes ‘strongly disagree’, to 5, which denotes ‘strongly agree’. The same was adopted until the third series of questions. In the proceeding segment, the respondents were asked to identify the challenges that hindered FAE development in India. It was followed by questions highlighting the benefits of incorporating FA concepts in accounting curricula. Specifically, two questions were asked about the appropriate approach to integrate FAE in India, with options including ‘introducing a separate FA course’, ‘integrating FA topics into existing accounting and auditing courses’ and an open-ended ‘other’ category for additional opinions. The second question explored the appropriate level at which to integrate FA, with options including the ‘undergraduate level’, ‘master’s level’, as part of a ‘diploma course’, or exclusively through a ‘certificate course’. The fifth series of questions delved into students’ preferences concerning FA topics to be included in the curriculum. Students were presented with 17 FA topics derived from relevant literature. They were asked to rate the importance of each topic on a 5-point Likert scale, ranging from ‘totally unimportant’ (1) to ‘totally important’ (5). Two distinct questions were asked of students pursuing MBA/Mcom/BBA/Bcom programmes in FA. The initial question asked participants to rate how satisfied they were with their chosen programmes on a scale from 5, ‘strongly satisfied’, to 1, ‘strongly dissatisfied’. Subsequently, an open-ended question was included to garner students’ perspectives on the challenges and prospects of pursuing these programmes. It is important to note that the questionnaire’s overall reliability coefficient was high (0.972), indicating the robustness of the survey questions in generating reliable results.

where n is the number of variables, σ2i is the score variations on each variable and σ2x is the total variance of the overall score.

Sample

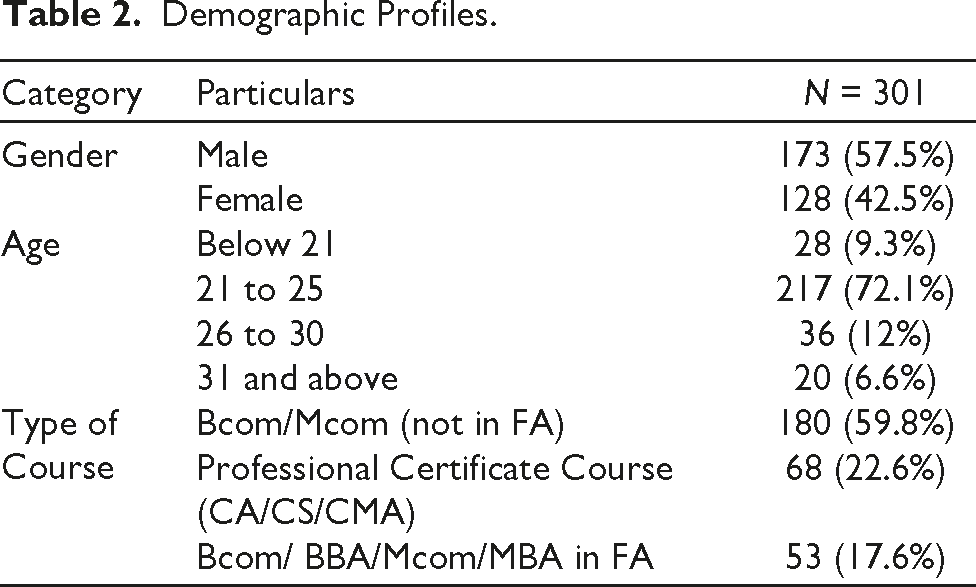

This cross-sectional survey provides preliminary exploratory evidence on how commerce and management students in India perceive the prospects of FAE. Given the novelty of the integration of FA in accounting education in India, this study aims to explore students’ perceptions regarding its integration. The sample size was not predetermined when the questionnaire was distributed. The study employed the purposive sampling method, in which participants were chosen based on predetermined criteria relevant to a specific research question. The study’s target population was the students in Bcom/Mcom in other specializations, Professional Certificate Course (CA/CS/CMA) or Bcom/ BBA/Mcom/MBA in FA specialization. Bcom/BBA/Mcom/MBA students are from seven central universities, four state universities, two private universities, two institutes of national importance and two centrally funded business schools for management and ICAI, ICMAI and Institute of Company Secretaries of India (ICSI). The questionnaire was emailed to some of the representatives of the universities with a request to share the same with the students. The faculty members were requested to share the questionnaire with the students, especially in institutions of national importance, namely Rashtriya Raksha University and National Forensic Sciences University. A total of 361 students participated in the study. Of these, 301 responded ‘Yes’ to the question on the awareness of the term ‘FA’. Therefore, the total sample size of the study was 301. The demographic profiles of the respondents are presented in Table 2. The table shows a higher representation of males (57.5%) in the sample than females (42.5%). Most respondents (72.1%) are between the ages of 21 and 25. Around 18% of the respondents are pursuing ‘Bcom/BBA/Mcom/MBA in FA’, while 22.6% of respondents are pursuing ‘Professional Certificate Course (CA/CS/CMA)’. Most of the respondents (59.8%) are pursuing ‘Bcom/ Mcom/(not in FA)’.

Demographic Profiles.

Analysis and Findings

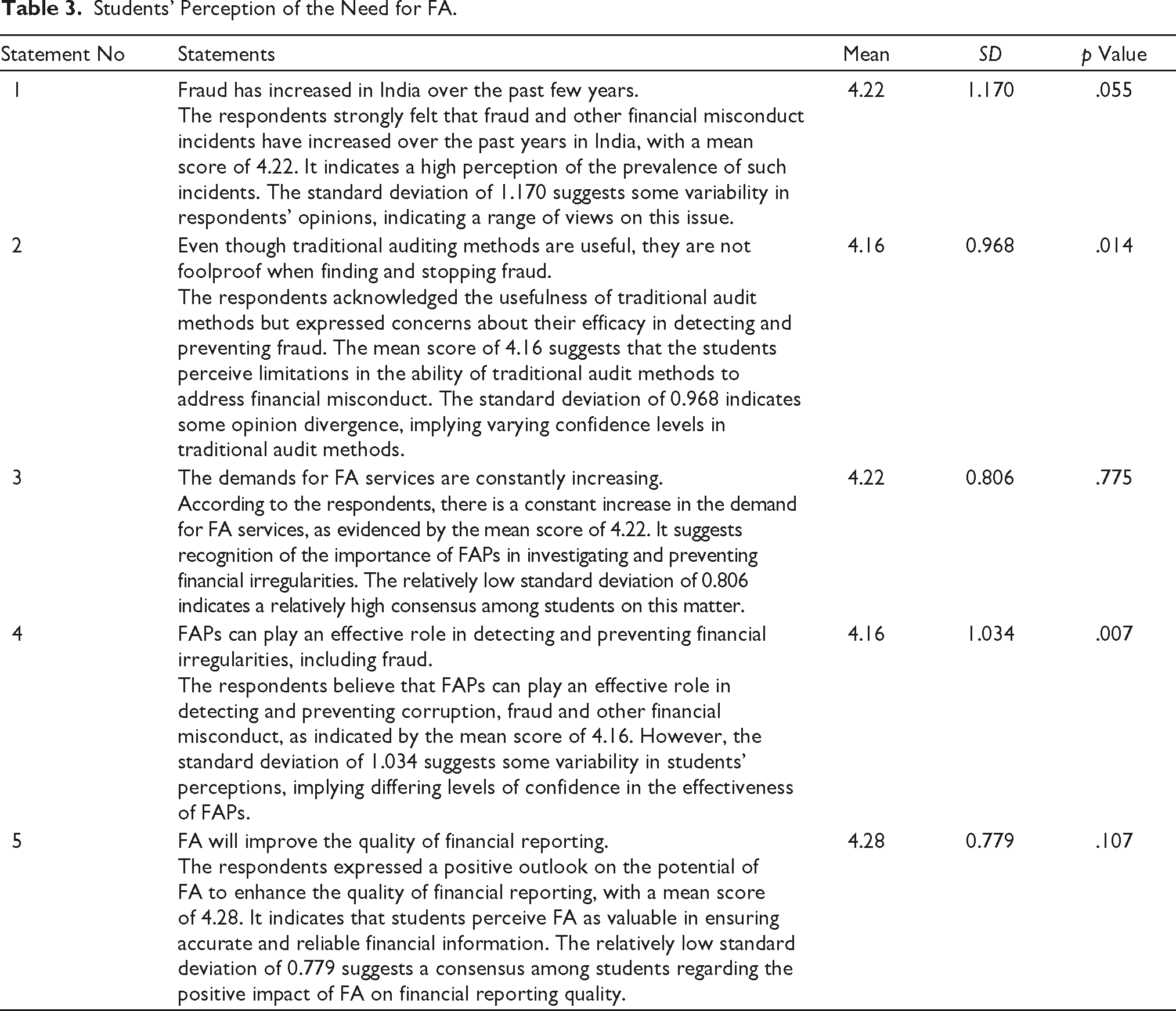

Students’ Opinions on the Necessity of FA

Table 3 depicts the Mann–Whitney U test result conducted to examine if there was any significant difference between the two groups relating to the opinion on the importance of FA. Based on the p values, it is observed that there are statistically significant differences (p < .05) in the responses between the two groups for statement 2 (z = –2.448, p = .014) and statement 4 (z = –2.691, p = .007). These findings suggest that students with FA specialization have differing perspectives compared to students without FA specialization on the effectiveness of traditional auditing methods and the role of FAPs in detecting and preventing financial irregularities. The significant difference in statement 2 suggests that students with FA specialization might be more aware of the limitations and vulnerabilities associated with traditional audit techniques when detecting and preventing fraud. Further, in statement 4, the difference could arise from the fact that students with FA exposure are likely to have a deeper understanding of the specialized skills and techniques that FAPs possess. It is plausible that they may be aware of how FAPs can capitalize on their expertise to detect any embezzlement.

Students’ Perception of the Need for FA.

Challenges in Developing FAE in India

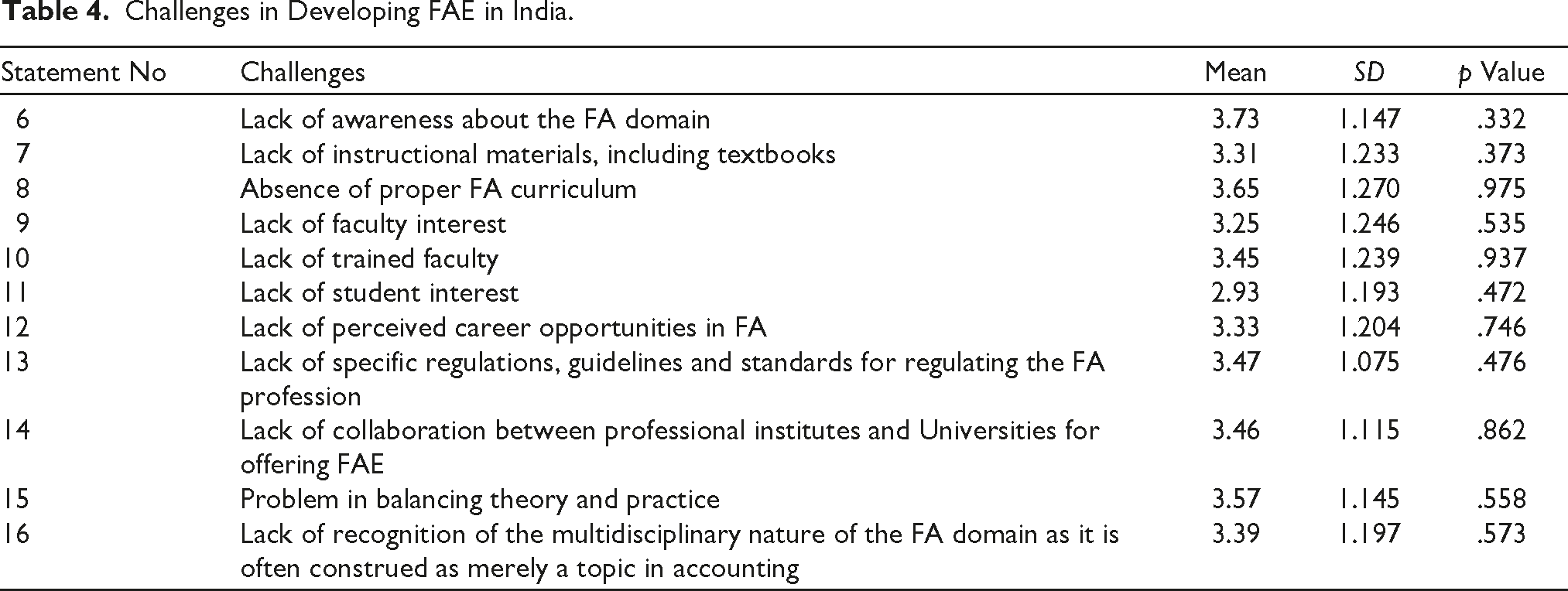

The second set of questions aimed to elicit students’ perspectives regarding the difficulties of advancing FAE in India. The respondents were asked to rate their opinion on 11 challenges identified from the FA literature on a 5-point Likert scale. The findings are presented in Table 4.

Challenges in Developing FAE in India.

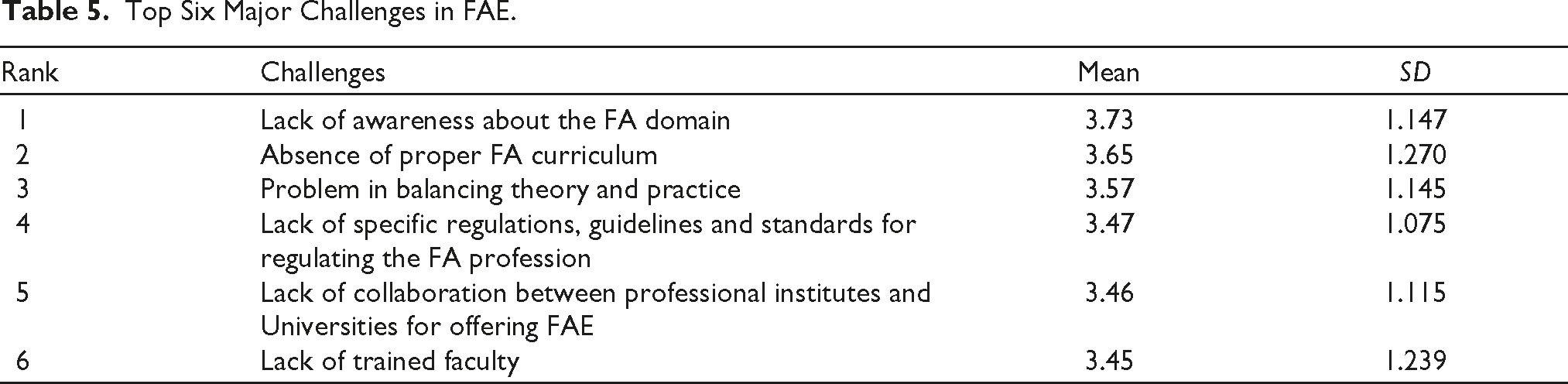

The results in Table 4 indicate that students recognize the significance of each of the stated obstacles to the development of FAE in India. According to Table 4, the six most significant student-perceived statements (Table 5) are as follows:

Top Six Major Challenges in FAE.

The respondents acknowledged a lack of awareness about the FA domain as a significant challenge in FAE. It shows that stakeholders’ awareness and comprehension of FA’s significance and scope are limited. Second, the respondents pointed to the lack of a proper FA curriculum as another barrier. It demonstrates that structured educational programmes designed especially for FA are considered lacking. Respondents mentioned the balance between theory and practice in FAE as the third major challenge in FAE. It implies that there exists a perceived gap between theoretical understanding and practical skills. Fourth, the absence of precise rules, standards and procedures for governing the FA profession was also mentioned as a challenge by the respondents. It shows that one challenge in creating FAE is the absence of a clear regulatory framework. Fifth, the lack of professional institutes and universities working together to provide FAE is again seen as a major barrier. The lack of collaboration and coordination between these institutions impedes the development of comprehensive FA programmes. In addition, the sixth significant barrier was the absence of trained faculties. These findings imply that the FA knowledge of the faculties imparting the same needs further enhancement.

Further, considering the p values, there are no statistically significant differences (p > .05) in the perceptions of challenges between the two groups for any of the statements. It suggests that both students with an FA specialization and those without it hold similar opinions regarding the challenges faced in FAE. These findings may imply that certain challenges are universally recognized within FAE, regardless of students’ exposure to FA concepts. It could also reflect the broader consensus within the academic community regarding the obstacles faced in developing and delivering effective FAE.

Students’ Perception of the Benefits of FA Integration

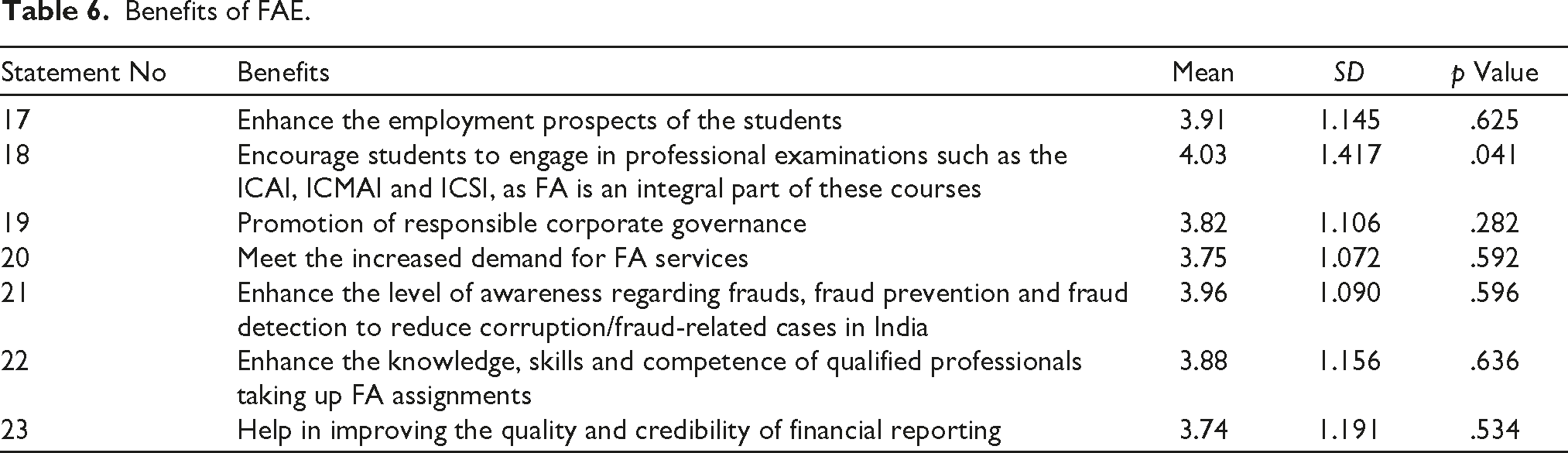

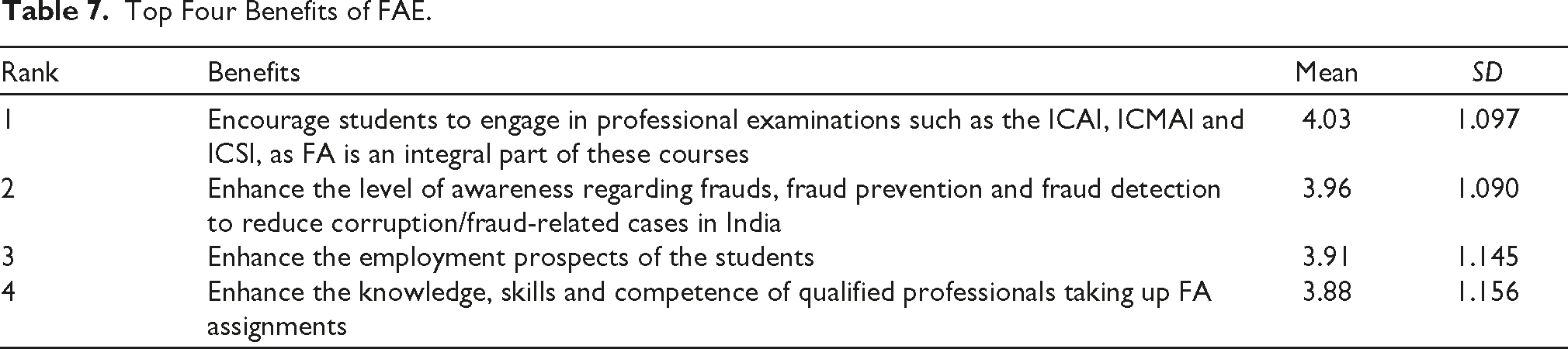

Table 6 shows that students observed the significance of each benefit statement. The four most important benefits from the students’ perspective are as follows:

Benefits of FAE.

Table 7 demonstrates that respondents agreed that FA is a crucial component of professional exams conducted by institutions such as the ICSI, ICAI and ICMAI. Students can improve their career opportunities by pursuing these professional certificates with the help of FAE. Additionally, FAE was viewed as a vehicle to spread knowledge about fraud and ways to avoid and detect it. By giving the understanding of FA, education can assist in reducing corruption and fraud-related instances in India. Respondents also agreed that improving students’ career chances may be accomplished by obtaining FA knowledge and expertise. Due to the frequency of fraud and the need for specialized knowledge when examining financial anomalies, FAPs are in great demand.

Top Four Benefits of FAE.

Additionally, FAE strengthened the skills of professionals accepting FA responsibilities. It equips them with the necessary knowledge and skills to effectively investigate financial irregularities and provide reliable FA services. Further, considering the p values, there are statistically significant differences (p < .05) in the perceptions of benefits between the two groups for the statement relating to encouraging students to engage in professional examinations (p = .041). It suggests that students with FA specialization have a more positive view than students without it, particularly regarding the zeal to engage in professional examinations such as those conducted by ICAI, ICMAI and ICSI, where FA is considered an integral part of the courses. For the remaining statements, the p values are higher than .05, indicating no statistically significant differences in the perceptions of benefits between the two groups. It implies that both groups hold similar opinions on the other benefits listed. These findings are attuned with those of Ebaid (2020).

Students’ Perception on Introducing FA

The fourth set of survey questions was intended to elicit students’ feedback on the preferred method for incorporating FA into the accounting curriculum. Students were given two options: (a) introducing a distinct FA course covering all FA topics and (b) incorporating FA topics into existing accounting and auditing courses. Table 8 presents the descriptive statistics of students’ responses to this question. According to the data presented in Table 8, the majority of the respondents (52.2%) agreed with integrating FA topics into existing accounting and auditing courses as the most effective method for teaching FA.

Appropriate Approach for Integration.

On the other hand, 43.9% of respondents supported introducing FA as a separate course. This approach emphasizes the unique nature of FA and the need for dedicated coursework focused specifically on this domain. It recognizes the importance of providing specialized education to students pursuing FA as a career path. However, a small proportion of respondents (4.0%) suggested two distinct alternative approaches beyond those specified in the questionnaire. The first suggestion is to offer FA as a specialized area exclusively provided by professional bodies such as the ICAI and the Association of Certified Fraud Examiners. This approach emphasizes the importance of recognized professional organizations delivering specialized education in FA. The second suggestion advocates integrating FA topics into current undergraduate accounting courses while introducing a separate specialized course in a master’s programme or as a specialized degree. This approach seeks to balance incorporating relevant FA content into existing educational programmes and recognizing the need for dedicated and more in-depth study at the postgraduate level. Students can gain foundational knowledge and awareness of the subject by integrating FA topics at the undergraduate level. Additionally, offering a distinct master’s-level course allows for a more comprehensive and advanced education in FA.

Student’s Perception of the Appropriate Level of FAE

Table 9 reveals that most respondents (54.5%) preferred offering FAE courses at the undergraduate level. It indicates a significant interest in introducing FA topics and concepts to students early in their academic careers. It allows for a larger audience and assures students of a foundational understanding of FA principles. Around 28% of participants said that a master’s degree in FAE ought to be offered. It represents the belief that significant expertise and specialization are required to completely comprehend and implement FA techniques and methodologies. Students seeking in-depth knowledge in this discipline could be accommodated by offering a specialized master’s programme in FA. However, FAE should be offered as a certificate course according to 13.3% of respondents. In addition, offering FAE as a diploma programme was proposed by only 4% of respondents. It shows the necessity for intensive, short-term programmes that impart specialized knowledge and skills relevant to the FA. According to the findings, there is interest in implementing FAE at various educational levels. It is, however, important to note that the optimal combination of educational levels may vary depending on the specific educational institution, student demand, available resources and industry requirements. Further research and consultation with relevant stakeholders are necessary to design comprehensive and effective FAE programmes in India.

Appropriate Level to Introduce FAE.

Students’ Perspective on FA Topics

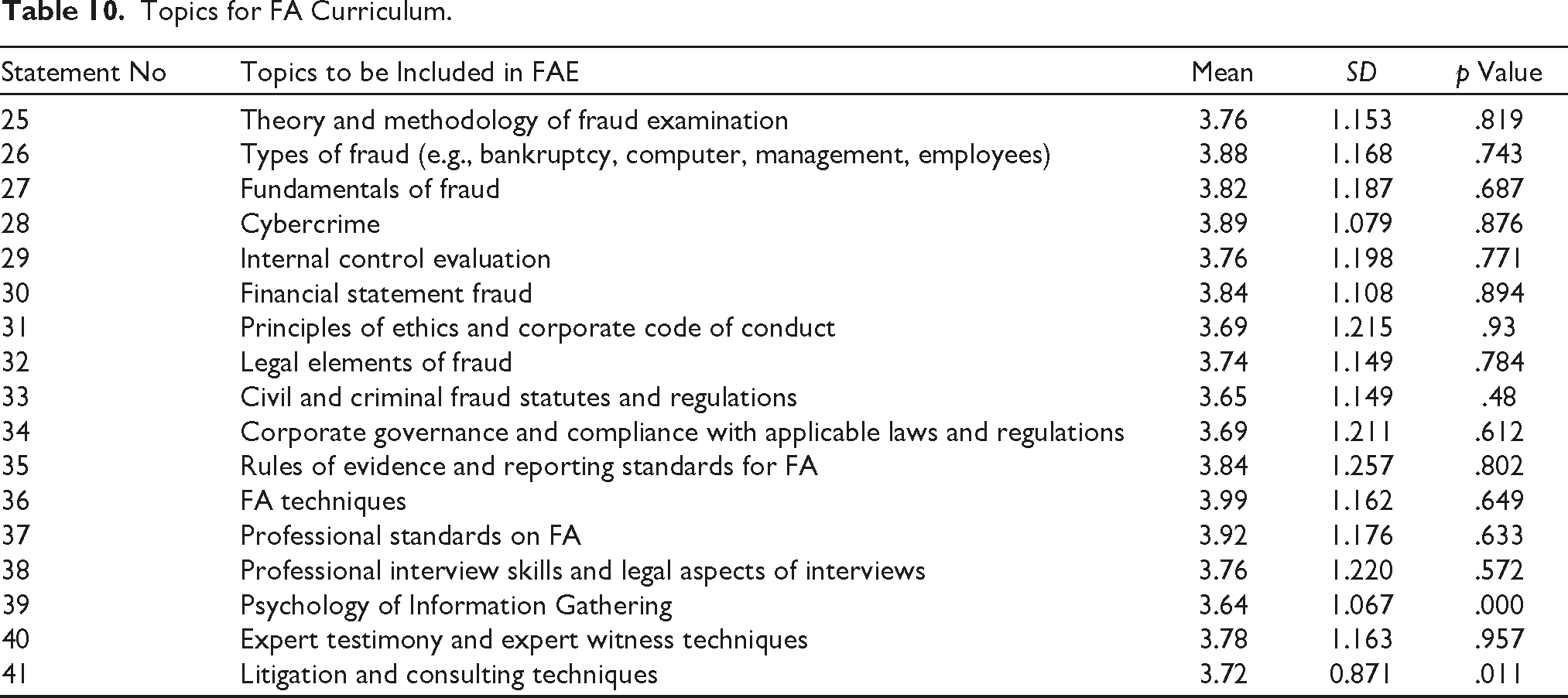

The final series of questions aimed to collect students’ opinions on the FA topics to be included in the FA curriculum. Students were given 17 FA topics and requested to rank their relative significance. The responses of students to these questions are summarized descriptively in Table 10.

Topics for FA Curriculum.

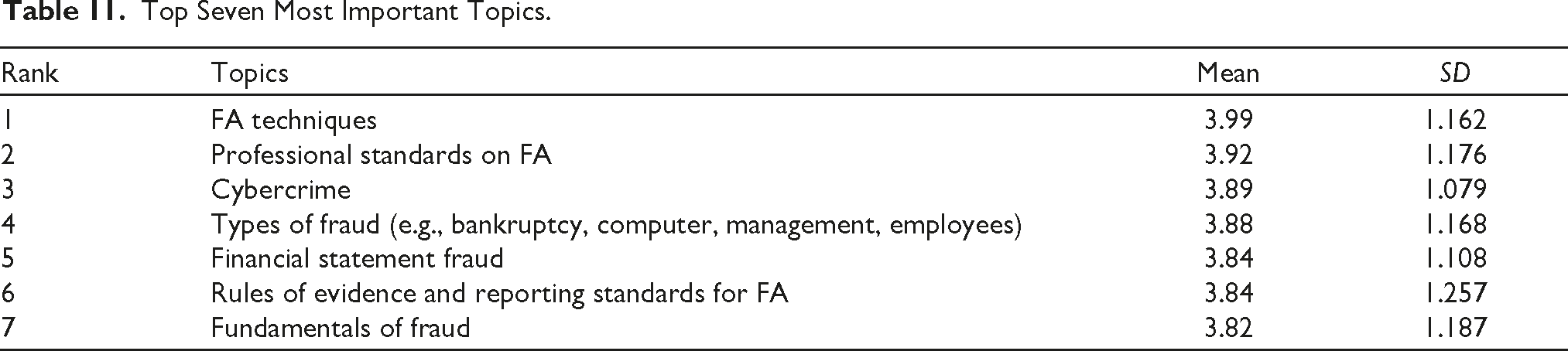

Table 11 presents the seven most significant topics for FAE from the perspective of students.

Top Seven Most Important Topics.

It is important to note that all the topics listed in the survey received mean scores above 3, indicating their perceived importance in FAE. The ranking of topics can guide curriculum development for FAE programmes and ensure that key areas of knowledge and skills are adequately covered to prepare competent FAPs. These seven highest-ranked topics reflect the respondents’ emphasis on practical aspects of FA, including techniques, fraud detection and investigation. The result of the Mann–Whitney U test shows that the two groups have significant differences on the topics of ‘Psychology of information gathering (z = –6.018, p < .01)’ and ‘litigation and consulting techniques (z = –2.557, p < .05)’. Students with FA specialization recognize the significance of psychological aspects in gathering information as an important skill for effective FA. This difference could stem from their exposure to the intricacies of conducting thorough investigations and understanding human behaviour in the context of fraud. Further, students with FA specialization might value the understanding of litigation and consulting techniques as crucial skills for FAPs, who often serve as expert witnesses in legal proceedings. This difference could arise from their awareness of the role FAPs play in legal cases.

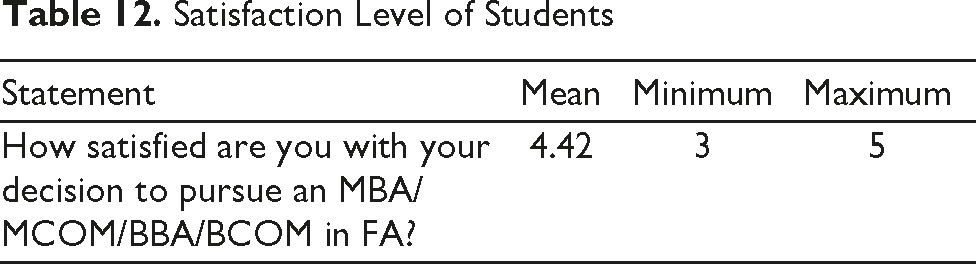

Students’ Perception of Satisfaction in Pursuing MBA/MCOM/BBA/BCOM in FA

Two additional questions were asked of students pursuing MBA/MCOM/BBA/BCOM in FA. Table 12 indicates that students who pursue MBA/MCOM/BBA/BCOM in FA are quite satisfied with their decision. The mean score of 4.42 indicates a positive sentiment and that most students are content with their choice. Factors contributing to this high satisfaction level include the relevance and value of the programme, career prospects in the field of FA, networking opportunities and overall personal and professional growth experienced during the programme. Further, they were asked to share the problems or prospects of pursuing MBA/MCOM/BBA/BCOM in FA. The comments provided by students are summarized and presented below.

Satisfaction Level of Students

Problems

Lack of quality teachers: There is a shortfall of teachers with practical knowledge in the FA field, making it challenging for students to gain practical exposure. The absence of practical exposure hinders applying theoretical concepts in real-world scenarios. One student stated,

The major problem is quality teachers. As at present most of the teachers at universities or colleges lack practical knowledge considering this field is new. Hence, practical knowledge is tough to gain.

Requirement for analysis and expensive software: FA often involves extensive data analysis, which may require expensive software. It poses a challenge for students who do not have access to such resources.

Challenging curriculum: Designing a comprehensive curriculum for FA presents a significant challenge due to the diverse backgrounds of students entering the programme. Students with a commerce or management background typically have a solid grasp of fundamental accounting concepts, such as debits and credits. However, they may encounter difficulties when it comes to understanding programming languages like Python. On the other hand, students with science backgrounds may find concepts relating to programming more approachable but struggle to understand accounting principles. The disparity of prior basic knowledge and skills makes it challenging to develop a curriculum that successfully meets the requirements of different students from different domains.

Prospects

Career prospect: Despite the challenges in FAE, pursuing MBA/MCOM/BBA/BCOM in FA provides numerous career opportunities, as this field is gaining recognition. It provides career options such as corporate investigator, fraud examiner, risk management, consultant and so on.

Competitive salary: With the rising demand for FA professionals, this profession offers competitive salaries to the participants.

Competitive advantage: The MBA/MCOM/BBA/BCOM programme in FA can act as an investigative eye-opener by providing invaluable knowledge in the field of fraudulent activities, which will give a competitive advantage to students.

Discussion

FAE Challenges and Benefits

The objective of the present study was to evaluate the incorporation of FA into accounting education, with a particular focus on the perspectives of students in Indian universities. According to the findings, students in India recognize the significance of FA as a profession. The findings corroborate with previous empirical results in the same direction (Hidayat & Al-Hadrami, 2015; Rezaee et al., 2004; Rezaee et al., 2016; Seda & Kramer, 2008). The areas identified as roadblocks by the respondents include lack of awareness, specific regulations, absence of an appropriate curriculum, lack of collaboration between professional institutes and universities, dearth of qualified faculty and an imbalance between theory and practice. These areas mirror the findings of Seda and Kramer (2008) and Rezaee et al. (2004). To address the challenges in FAE, universities and colleges should consider inviting guest lecturers with practical experience in FA. It can help to bridge the gap between theoretical understanding and real-world implementation.

Additionally, efforts should be made to enhance the practical elements of the curriculum and better align them with industry demands. The study also demonstrates that Indian students are keen to acquire knowledge in FA to advance their education and pursue professions in this industry after graduation. These findings are in line with the research by Ebaid (2020).

Integration and Inclusion of FAE

Despite the increasing demand for FA services due to the rise in corruption and fraud cases, the study indicates a clear deficiency in the coverage of FA topics within the accounting curriculum of Indian universities. This observation aligns with similar studies conducted in other developing countries, such as Rezaee et al. (2004), Kranacher et al. (2008), Teik et al. (2013) and Hidayat and Al-Hadrami (2015). Regarding the integration of FA topics into the accounting curriculum, while some studies suggest introducing a separate course (Priyangika & Bandara, 2017; Sofianti et al., 2014), the current study indicates that students in Indian universities prefer integrating these topics into existing accounting and auditing courses. This preference is consistent with findings from other studies, such as Rezaee et al. (2004), Corkern et al. (2013) and Hidayat and Al-Sadiq (2014).

Curriculum for FAE

The study discovered that students in India show interest in various FA topics concerning the unique content of the course. However, their focus is on methods for detecting fraud, including professional standards on fraud, cybercrime, types of fraud, financial statement fraud, rules of evidence and reporting standards for FA, fundamentals of fraud, expert testimony and expert witness techniques. The study’s findings differ significantly from those conducted in developed countries like the United States. The developed countries include a more diverse content of FA in their FA course (Alshurafat et al., 2019; Jones & Zucker, 2018; Rezaee et al., 2018).

Leveraging on TPB

The findings gathered from leveraging the TPB revealed a positive inclination of students’ perception towards FAE. The findings exhibited that students hold strong positive attitudes towards FAE, recognizing the increasing demand for FA services (mean = 4.22) and its role in improving financial reporting quality (mean = 4.28). Subjective norms are evident as students perceive a rise in financial fraud in India (mean = 4.22) and acknowledge the limitations of traditional audit methods (mean = 4.16). The challenges affecting perceived behavioural control include the lack of awareness about FA (mean = 3.73) and inadequate curriculum (mean = 3.65). Despite these obstacles, students perceive significant benefits associated with FAE, such as enhanced employment prospects (mean = 3.91) and encouragement for professional certifications (mean = 4.03). These insights suggest that addressing these challenges through targeted curriculum development and awareness programmes can better align FAE with students’ needs and societal demands.

Conclusion

The study found that commerce and accounting students are becoming increasingly aware of the importance of FAE in Indian universities. Shortcomings of traditional auditing procedures in detecting and preventing such fraudulent activities and the rise in corruption and fraud have led to students’ strong perception of the need for FAE. Further, students consider that FAPs can effectively aid in identifying and preventing fraud and corruption and thereby improve the accuracy of financial reporting. However, there are several challenges to the growth of FAE in India. These challenges include the lack of awareness about the FA domain, insufficient instructional materials clubbed with the absence of a proper curriculum, lack of trained faculty and the absence of specific regulations and guidelines for regulating the FA profession.

Additionally, the problem of balancing theory and practice and the lack of collaboration between professional institutes and universities for offering FAE further hinders its integration into the development of FAE in India. The study concluded that students perceive FAE as beneficial for those who want to engage in professional examinations such as those conducted by the ICAI, ICMAI and ICSI. It is also attested that FAE can enhance awareness levels regarding fraud, increase the students’ employment prospects and enhance the knowledge, skills and competence of qualified professionals taking up FA assignments. Further, most students opted for integrating FA topics into current accounting and auditing courses at the undergraduate level. The study provides recommendations for policymakers and educators on enhancing FAE by addressing the key beliefs identified through the TPB framework. Based on the evidence, integrating FA into the accounting curriculum of universities in India is strongly recommended.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: ICSSR Doctoral Fellowship administered through the Institute of Public Enterprise (IPE; File No. RFD/Inst/22-23/IPE/GEN/24).