Abstract

Determinants of financial behaviour have increasingly attracted scholarly interest as financial advancement and digitalization have been growing. Whereas good financial decisions have been associated with good financial literacy, new studies have provided insights into the significance of accounting psychological aspects and digital skills to elucidate financial performance. This article evaluates the implications of objective, subjective and digital financial literacy and financial anxiety on financial behaviour as well as satisfaction. Listing 400 digitally engaged people as a sample analysed with the help of structural equation modelling and AMOS 26, a structured questionnaire was carried out using verified reliability and validity assessments. The positive predictors of financial behaviour were digital financial literacy, objective knowledge and subjective knowledge. The financial anxiety conditioned a poor effect on financial capacities and emotional state. Financial literacy partially mediated the association between financial anxiety and financial behaviour in digitally motivated situations. There was a significant gender moderation effect of this relationship, with negative associations between females, but no significant effect of age. Cognitive, emotional and digital integration further develop the behavioural finance theory and promote the financial health of everyone in a changing economic environment.

Keywords

Introduction

The formation of financial ecosystems, financial literacy and financial behaviour knowledge have become more relevant to people who work in sophisticated and technologically oriented financial spheres. The digitization of the financial industry, such as online banking, mobile payment, robotic advisor services and cryptocurrency trading, requires not only the knowledge of work in financial systems but also the level of cognitive and psychological preparations and digital skills to make effective decisions (OECD, 2020). Cognitive, affective and environmental factors have significant impacts on financial behaviour, such as budgeting, saving, borrowing and investing (Xiao & Porto, 2017). OECD defines financial literacy as the combination of financial awareness, knowledge, skills, attitudes and behaviour required to make informed financial decisions and achieve financial well-being (OECD, 2020). Objective financial knowledge refers to the knowledge of the financial terms of interest rates, inflation and diversification, typically determined by quizzes (Lusardi & Mitchell, 2014). Self-perceived financial capacity is subjective financial knowledge and may be used to make decisions without facts (Allgood & Walstad, 2016). The most relevant psychological variable, which is still growing and underdeveloped in this aspect, is financial anxiety (FA), which can be defined as an emotional distress or stress of a person when handling financial issues, resulting in procrastination, avoidance or impulsivity during financial decision-making, which jeopardize financial stability (Archuleta et al., 2013; Shapiro & Burchell, 2012). Digital financial literacy (DFL) or the capacity to use, read and see digital financial products and services is essential when financial products and services become more digital (Grohmann, 2018; OECD, 2022). Several studies have examined these variables in isolation, but there are no holistic empirical models that investigate how FA, objective and subjective financial knowledge, DFL and their interdependencies affect financial behaviour or satisfaction (Yuneline & Rosanti, 2023). This dismantled framework fails to account for the integrated process of financial decision-making, especially in light of the growing use of digital finance platforms that can empower or intimidate users depending on their cognitive and psychological readiness (Lusardi, 2019; Stolper & Walter, 2017). Existing literature has not widely examined whether FA suppresses the beneficial influence of financial knowledge or whether DFL will mediate or moderate this influence, and this is an appropriate gap for research that needs to be addressed through theory-building and policy-making (Farrell et al., 2016). In an attempt to address these gaps, a structural equation modelling (SEM) has been developed for exploring the dynamic interaction between FA, objective and subjective financial knowledge, DFL and their effect on financial behaviour and satisfaction. With reference to the research questions of interest, the overall research questions of this study are as follows:

RQ1: In digital finance, how does objective and subjective financial knowledge influence financial behaviour and satisfaction? RQ2: How does financial anxiety suppress or forecast financial results? RQ3: How does digital financial literacy affect financial anxiety, knowledge and behaviour?

An Examination of Existing Literature

Financial Behaviour and Satisfaction

Financial behaviours such as saving, budgeting, borrowing and investing have inherent connections with the financial well-being and happiness of a person (Dew & Xiao, 2011; Xiao & Porto, 2017). Financial satisfaction would generally be a key measure of influence in behavioural finance studies, and financial satisfaction is a personal judgement of an individual about their financial situation and feeling safe (Brüggen et al., 2017). Being involved in healthy financial behaviour has positive impacts on emotional and psychological well-being and greater financial enjoyment (Serido et al., 2010). Psychological and behavioural constructs such as self-control, planning and trust can influence levels of financial satisfaction (Joo & Grable, 2004). These findings suggest that examining the determinants of financial behaviour can provide useful information about the processes by which financial well-being is achieved in virtual and real environments.

Objective Versus Subjective Financial Knowledge

Subjective financial knowledge (SFK) refers to how confident individuals feel about their understanding of financial concepts such as inflation, interest rates and risk diversification, whereas objective financial knowledge (OFK) is measured through correct answers to factual financial questions (Allgood & Walstad, 2016; Lusardi & Mitchell, 2014). These two are relatively important, but they affect behaviour differently. Rational decision-making is normally associated with objective knowledge; subjective knowledge tends to influence real behaviour based on overconfidence or miscalculation (Lone & Bhat, 2024). As an example, highly subjectively knowledgeable persons can take too many financial risks when they have little actual capacity (Hadar et al., 2013). However, objective knowledge remains a powerful forecast to make good financial decisions (Xiao & Porto, 2017). Therefore, the study hypothesized that:

H1: OFK positively influences FBS. H2: SFK positively influences FBS.

Financial Anxiety and Its Psychological Impact

FA is a kind of psychological distress that is centred on money management, which in most cases is manifested through avoidance, indecisiveness and physical symptoms of stress (Shapiro & Burchell, 2012). It normally occurs due to doubt regarding incomes, debts and unforeseen costs. Research shows that FA negatively affects cognitive functioning, leading to poor financial decisions (Archuleta et al., 2013). It also reduces positive financial behaviours such as saving, budgeting and seeking professional advice (Norvilitis et al., 2006). Moreover, FA is linked with depressive symptoms and lower overall life satisfaction (Prawitz et al., 2017). Overall, it weakens financial performance by increasing avoidance and emotional misjudgement. Accordingly, it is hypothesized that:

H3: FA negatively influences FBS.

Digital Financial Literacy in the Contemporary Context

DFL is the ability and knowledge to utilize digital platforms to conduct financial activities, prepare and secure (OECD, 2022). With growing online and app-based financial services availability, DFL has become a central factor in financial capability among youth and the poor (Grohmann, 2018). Greater DFL is linked to more secure financial behaviour, greater utilization of digital financial services and a lower prevalence of fraudulent transactions (Yuneline & Rosanti, 2023). Digital literacy is, however, technologically and digitally infrastructure-dependent, opening digital divides, which enhance financial exclusion (Van Deursen & Helsper, 2015). As a capability allowing users to utilize financial systems confidently, DFL will achieve far superior financial behaviour and overall satisfaction. Thus, it is hypothesized that:

H4: DFL positively influences FBS.

Theoretical Framework

The theoretical framework of this research integrates the financial capability framework (Atkinson et al., 2007) and the theory of planned behaviour (TPB; Ajzen, 1991). The financial capability framework believes that financial results stem as well from knowledge as from mental dispositions such as attitude and confidence, and from outside circumstances like service accessibility. TPB advanced that attitudes, subjective norms and behaviour control predispose intentions towards action, and intentions act as predictors of actual behaviour (Ajzen, 1991). These theoretical frameworks support one another in validating the postulation that objective and subjective finance knowledge, ICT literacy and psychological dispositions such as anxiety interplay and determine financial conduct. Integration of these models allows for an overarching viewpoint through which the behavioural and cognitive mechanisms of financial satisfaction may be investigated.

Identification of Research Gap

Financial behaviour and literacy research is vast; however, empirical research on the interaction effects of FA, OFK, SFK and DFL is scarce. Most of the research is in isolation, studying these variables one by one without considering the interaction between psychological forces and digital abilities (Rani & Siwach, 2023). Also, fewer studies considered the interaction between subjective and objective knowledge or tested whether DFL is a moderator variable that influences the relationship between FA and behavioural outcomes (Lusardi, 2019). The absence of integrated modelling has led to theory and practice gaps regarding the effects of the different dimensions of financial literacy on behaviour patterns and satisfaction in digitally empowered financial situations. The present study fills the gap by considering all four dimensions in a structural equation model and hypothesizes that:

H5: FA negatively influences DFL, which mediates its effect on FBS.

Overarching Model

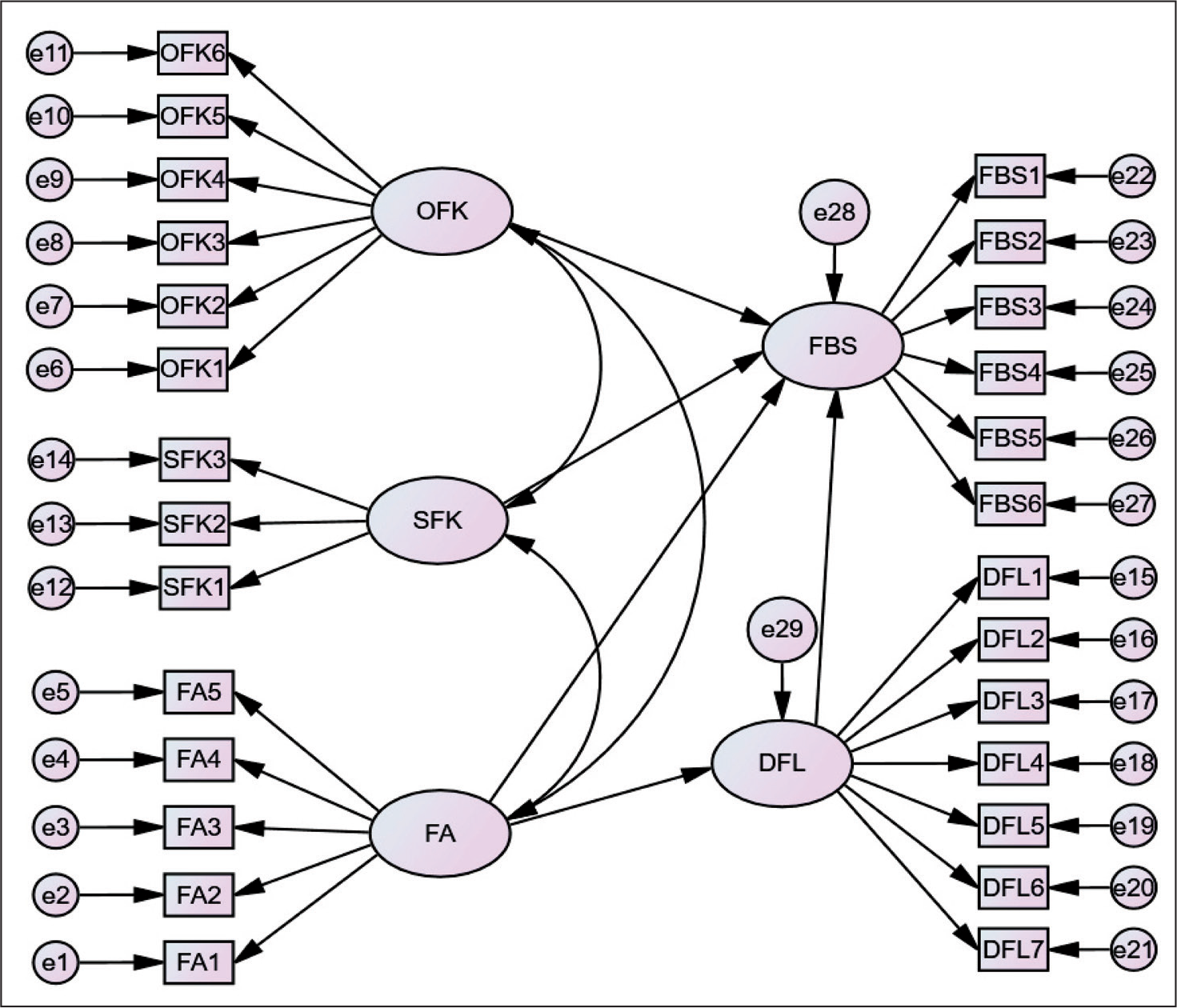

The present study examines FA and objective, subjective and DFL as predictors of financial behaviour and satisfaction using SEM to estimate direct and indirect effects. FA is expected to negatively influence outcomes, whereas literacy dimensions show positive effects, with digital literacy acting as a mediator. Therefore, the proposed model is presented in Figure 1.

Guided by the integrated framework and H1–H5, this study employs structural equation modelling to empirically test the proposed relationships. SEM is appropriate because it estimates both direct and indirect effects among multiple latent constructs while accounting for measurement error. Validated multi-item scales are used to measure each construct to guarantee that theory and empirical testing are in line with each other. The next section describes the sampling, instrument development and data analysis methods.

Methodology

Framework of Research

According to the theoretical framework and hypotheses, the present study is based on the cross-sectional quantitative design because of the need to describe the relationship existing between FA, OFK, SFK, DFL and financial behaviour and satisfaction (FBS). The proposed model is tested with the help of structural equation modelling, which allows estimating direct and indirect effects at the same time and considering the measurement error (Hair et al., 2019). The cross-sectional design captures relationships at one point in time and compatible with the behavioural finance research conducted in the digital context (Xiao & Porto, 2017). This design is suitable, as the study examines an empirically supported theoretical framework of existing relationships between psychological, cognitive and digital literacy constructs. Given that the short-term and medium-term views of OFK, SFK and DFL are rather consistent, their measurement after one time would give a valid indication of the relationships between all of them (Hair et al., 2019; Kline, 2016). Longitudinal designs also have the disadvantages of attrition and lack of consistency in the measurements (Menard, 2002). Experimental designs may enhance causal inference but require manipulating variables like anxiety or literacy, raising ethical and ecological concerns. Therefore, in this context, cross-sectional SEM is widely used in financial literacy research for robust structural testing (Grohmann, 2018; Xiao & Porto, 2017). The quantitative approach further strengthens hypothesis testing and generalizability (Creswell & Creswell, 2018).

Sample Size and Population

In a bid to ensure comparability, the questionnaire sought respondents aged 18 years and above with access to financial online channels. Stratified random sampling was also enlisted with the aim of providing balance between age, gender and income. Stratified sampling usage has been reported to be useful in ensuring studies conducted via questionnaire usage representativeness and validity (Etikan & Bala, 2017). Sample size determination has been guided by SEM requirements of having at least 10 respondents per observed variable (Kline, 2016). Due to the model complexity, at least 400 respondents have been sought with the aim of ensuring proper statistical power as well as model validation (Hair et al., 2019).

Instrument Development and Validation

Stage 1: Instrument Development

The measurement instrument was developed using established multi-item scales to ensure theoretical alignment and robustness (Jamwal & Kamboj, 2025). FA was assessed with the Financial Anxiety Scale (Archuleta et al., 2013). SFK items were adapted from Allgood and Walstad (2016), while objective knowledge items were drawn from the OECD (2020) Adult Financial Literacy Questionnaire for national comparability. DFL was measured using OECD (2022) items, supplemented with mobile payments and online banking practices. FBS scales were adapted from Brüggen et al. (2017) and Xiao and Porto (2017). This approach reduced construct under-representation (DeVellis, 2017).

Stage 2: Pilot Testing

Prior to full-scale administration, pilot testing of the draft questionnaire was conducted on a purposive sample of 30 respondents that reflected the target population in terms of demographic profile and digital use behaviours. Pilot testing enabled an evaluation of the clarity, relevance of questions, survey length and ease of completion (Presser et al., 2004). Respondents provided structured feedback on ambiguous terms or ordering of items that confused them, and this resulted in minor changes of wording and ordering so as to enhance readability and fluidity. Pilot testing also aided in determining technical issues inherent in the use of the online survey platform so that navigation and response capturing proceed smoothly. This procedure facilitated face validity, that is, the extent to which the instrument appears to measure the intended construct (Boateng et al., 2018).

Stage 3: Validity and Reliability Assessment

After pilot revisions, the refined questionnaire was assessed for content and construct validity. Content validity was ensured through expert evaluation by two behavioural finance academics and one digital banking professional, who reviewed item relevance and cultural appropriateness. Reliability was tested using Cronbach’s α, with all constructs exceeding the 0.70 threshold (Thorndike, 1995). Construct validity was examined through confirmatory factor analysis (CFA). Convergent validity was supported as factor loadings exceeded 0.60 and AVE values were above 0.50 (Hair et al., 2019). Discriminant validity met the Fornell–Larcker criterion, and composite reliability (CR) values exceeded 0.70, confirming measurement robustness.

Stage 4: Final Implementation

The final questionnaire based on the existing scale was subsequently shared within a period of 6 weeks, with the main study sample using online sources of distribution, including social media, professional networking platforms and special mailing lists. Such channels of distribution were considered effective, cost-effective and the right choice, with attention to DFL in a digitally literate population (Evans & Mathur, 2018). Each of the respondents was clearly informed about the purpose of the research, data confidentiality and voluntariness, and provided informed consent to participate. The survey site had filters that ensured that only complete and valid answers were utilized during the analysis.

Bias and Diagnostic Checks

Considering that self-report and cross-sectional design are employed, diagnostic tests have been carried out to avoid statistical bias in the outcomes of SEM. VIF and tolerance values were measured for multicollinearity in SPSS. VIFs were 1.21 to 3.42, which are below the conservative levels of 5.0 (Hair et al., 2019) and 10.0 (Neter et al., 1996), which show that there are no severe collinearity problems. To address common method bias (Podsakoff et al., 2003), procedural remedies such as anonymity and varied scale anchors were applied (MacKenzie & Podsakoff, 2012). Harman’s single-factor test showed 31.6% variance, below the 50% threshold. The common latent factor test in AMOS revealed no substantial path changes (>0.20), confirming robustness.

Data Analysis

Data analysis was done by structural equation modelling within AMOS 26.0. SEM was chosen owing to the fact that it can be used to simultaneously estimate complex relationships among the various latent constructs and also corrects the measurement error, which is a methodological benefit over more traditional regression methods (Hair et al., 2019; Henseler et al., 2015). The structural model was analysed in a two-step process; the measurement model was evaluated initially to define construct validity and reliability, and subsequently to test hypothesized relationships such as mediation and moderation effects. The appropriate fit of the models was evaluated based on several measures (CFI, TLI, RMSEA and χ2/df) based on the standard values of good fit (Hu & Bentler, 1999). This was a strict methodology that made both the measurement and theoretical models powerful, in both statistical and theoretical terms.

Results and Data Analysis

Respondents’ Demographic Data

Table 1 shows that 53% of the 400 respondents were men, consistent with research indicating higher male participation in early fintech adoption (Grohmann et al., 2018). Most (59.5%) people were aged 18–35, which is an indication of high commitment to mobile banking and online transactions by young adults (OECD, 2020). The majority of respondents were graduates or post-graduates (64.5%), which corroborates the fact that higher education is associated with financial literacy (Lusardi & Mitchell, 2014). The income distribution was concentrated in the ₹25,001–₹50,000 range (36.5%), a segment frequently targeted for digital inclusion initiatives (OECD, 2020). It is noteworthy that 82.5% employed digital banking, which proves appropriate to test the hypothesis of DFL and behaviour.

Respondent Demographics.

Analysis of Reliability

Table 2 indicates high internal consistency of all constructs with Cronbach α values greater than 0.70 (Thorndike, 1995). FA (α = 0.872) and DFL (α = 0.881) have high reliability values, which means that they are consistent in measuring psychological and digital aspects. FBS (α = 0.844) and SFK (α = 0.812) are also good, and hence, they should be included in the SEM model. OFK is a little bit less (α = 0.794), but it is in the acceptable range, which indicates coherent measurements. These results confirm the psychometric robustness of the instrument and reliable SEM analysis (Hair et al., 2019).

Analysis of Reliability.

Correlation Matrix Analysis

Table 3 presents substantive correlations between all the major constructs, which substantiate the hypothesized correlations. FA is also associated with other variables, namely FBS (r = −0.462, p < .01), in agreement with the findings that financial stress leads to less-rational decision-making and well-being (Shapiro & Burchell, 2012). DFL has a positive correlation with OFK and SFK (r = 0.512 and r = 0.491, p < .01), which indicates the relationship between cognitive and digital skills (OECD, 2022). Both these types of knowledge are associated with FBS in a positive way (Lusardi & Mitchell, 2014; Xiao & Porto, 2017). Furthermore, DFL is the most associated with FBS (r = 0.528, p < .01; Grohmann, 2018).

Correlation Analysis Matrix.

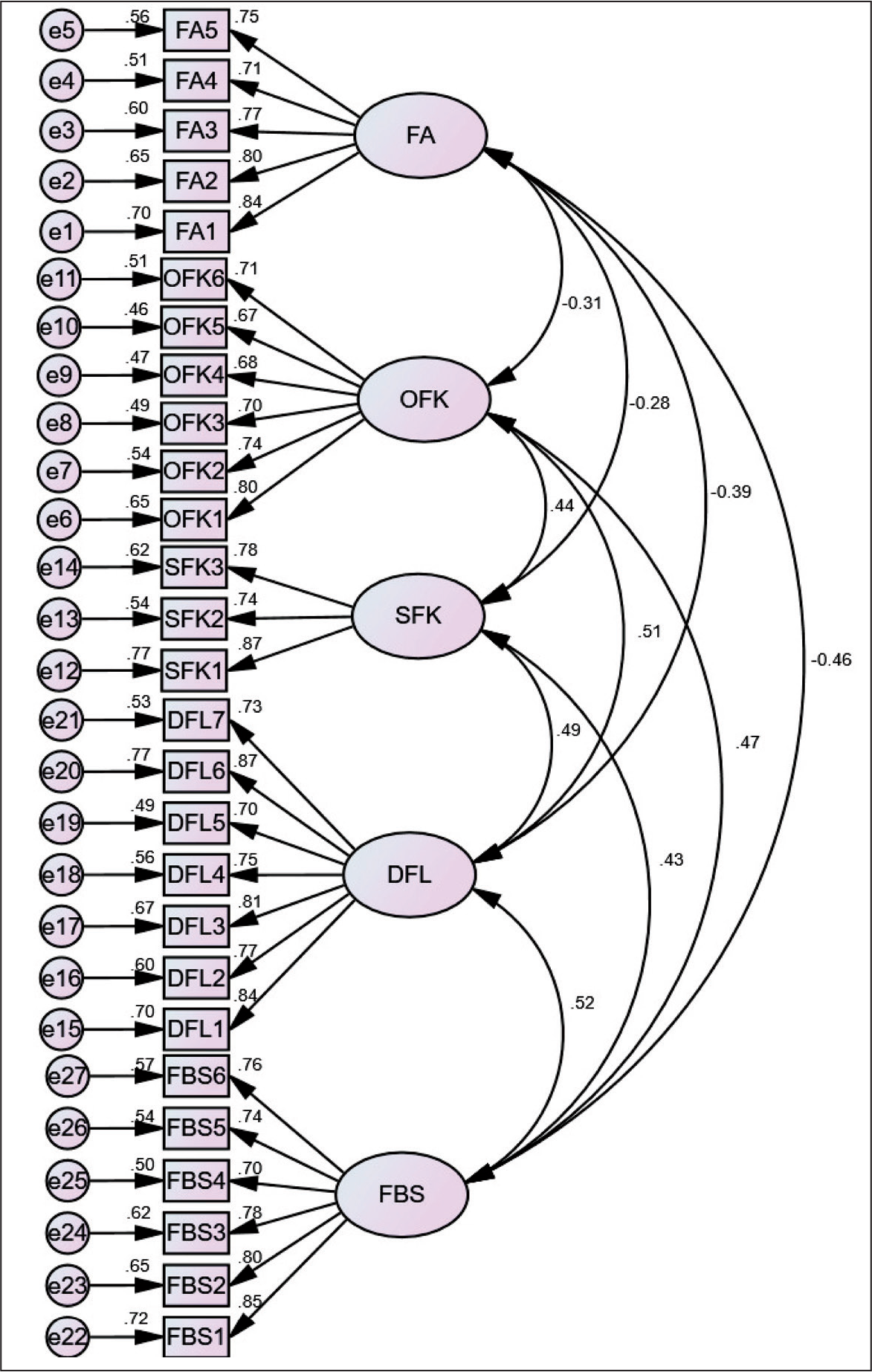

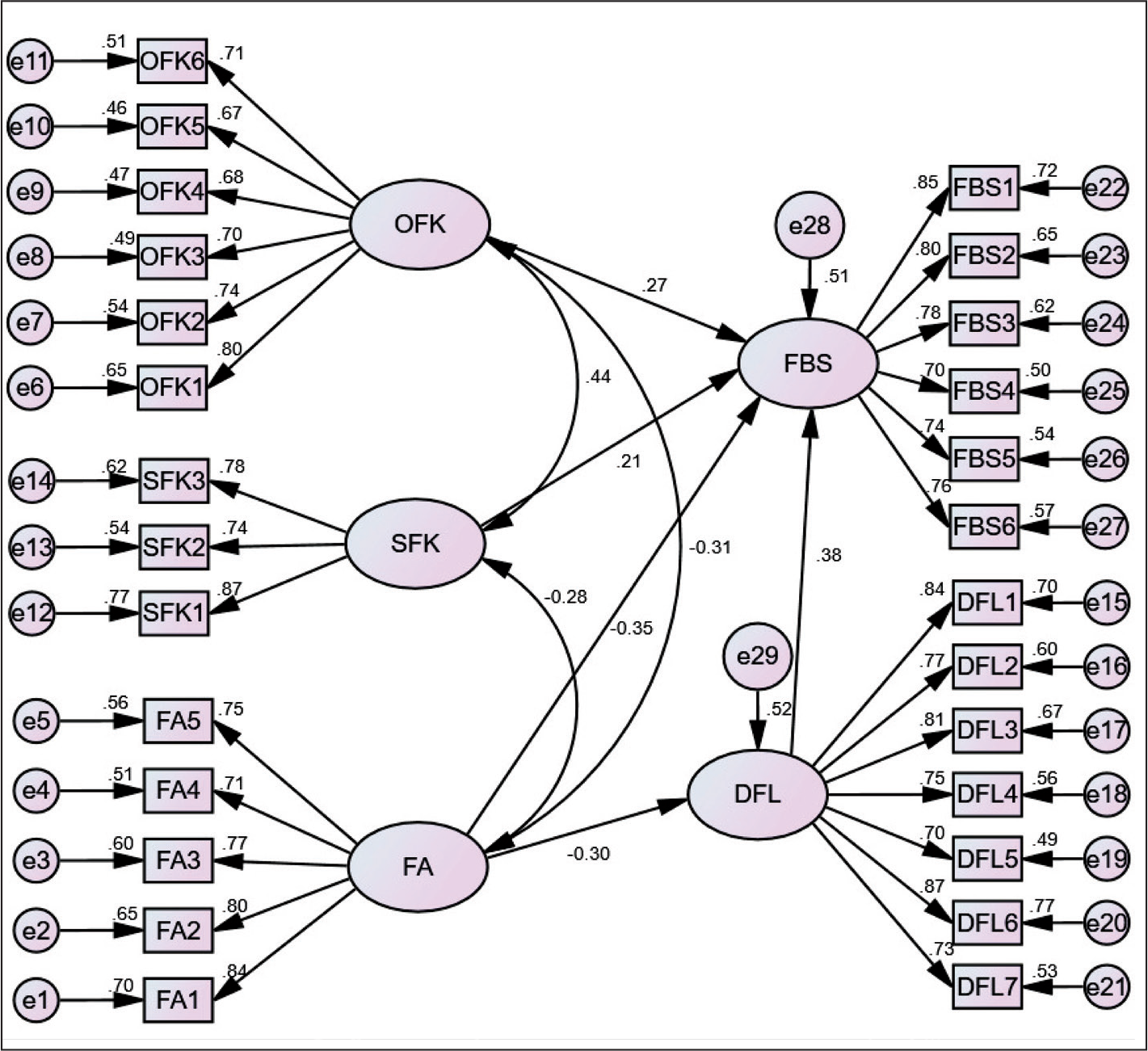

Figure 2 presents the CFA model assessing five latent constructs: FA, OFK, SFK, DFL and FBS. Most standardized loadings exceed 0.70 (e.g., FA1 = 0.84, OFK1 = 0.81, SFK1 = 0.88, DFL1 = 0.84, FBS1 = 0.85), confirming strong reliability and convergent validity (Hair et al., 2019). A few items (e.g., OFK5 = 0.68; OFK6 = 0.72) remain acceptable for social science research (Byrne, 2016). Inter-construct correlations are below 0.60 (e.g., FA–OFK = –0.31; DFL–FBS = 0.52), supporting discriminant validity (Fornell & Larcker, 1981). Overall, the measurement model demonstrates a good fit for SEM analysis.

CFA Measurement Model.

Summary of the CFA Model

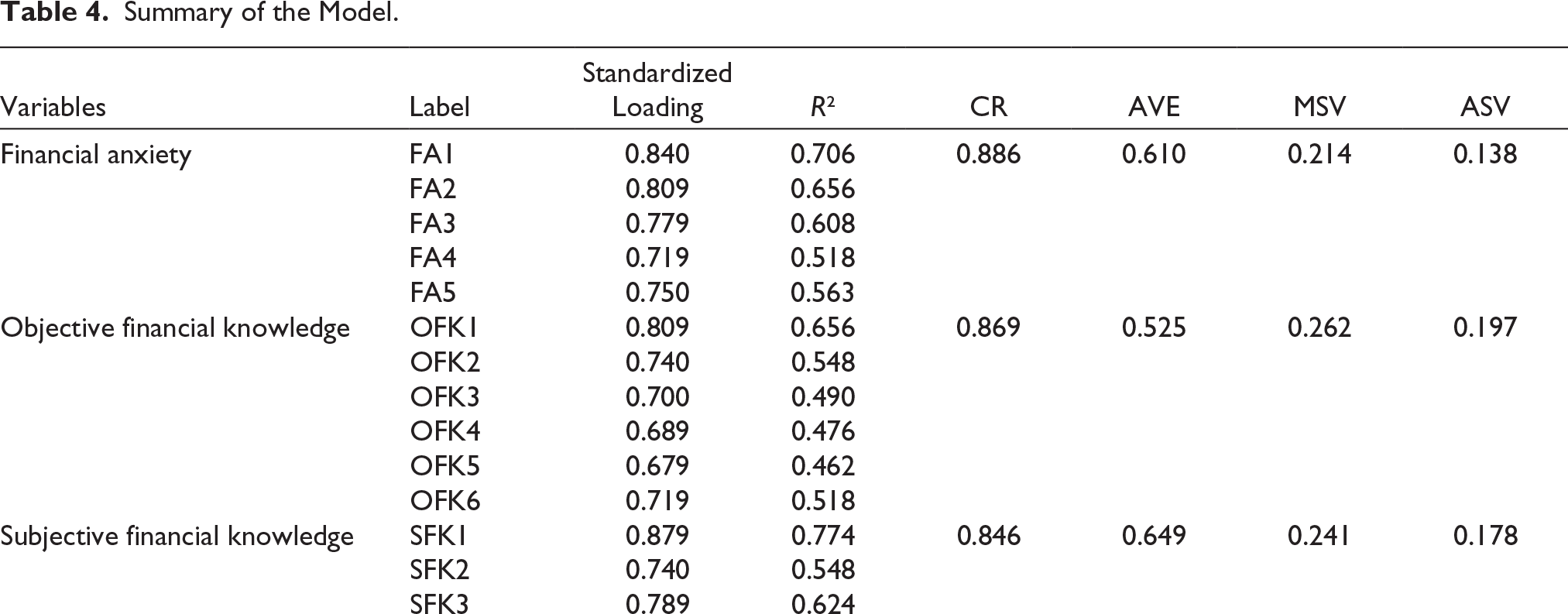

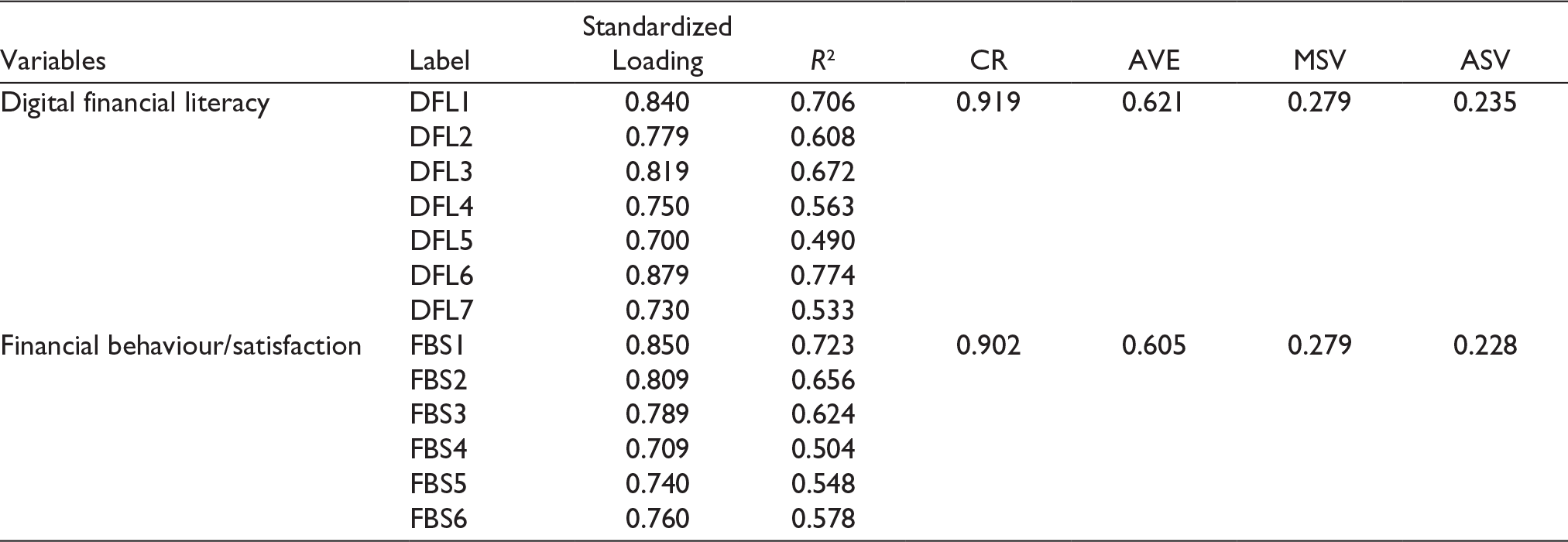

As indicated in Table 4, all the constructs exhibit high psychometric properties applicable in SEM. The standardized loadings are over 0.70, which proves that the contributions of items are substantial (Hair et al., 2019). R2 between 0.518 and 0.774 indicates the reliability of the indicators. Internal consistency standards are satisfied by a CR value of more than 0.84 (Fornell & Larcker, 1981). Convergent validity is established because all AVE scores are greater than 0.50, with SFK recording the highest value of 0.649 (Bagozzi & Yi, 1988). Discriminant validity is also supported by ASV and MSV values (Henseler et al., 2015). In general, the measurement model is valid and suitable in structural analysis.

Summary of the Model.

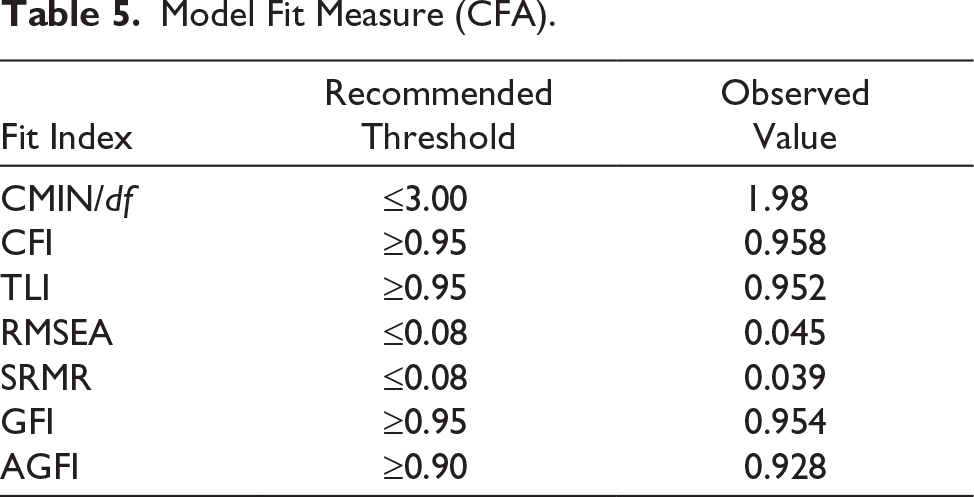

Model Fit Measure

Table 5 reveals that the CFA model has a good fit across all the indices, which proves measurement reliability. The ratio of χ2/df is 1.98, which is less than 3.00, and it shows that the model fits well (Kline, 2016). CFI (0.958) and TLI (0.952) are above 0.95, and they exhibit an excellent incremental fit (Hu & Bentler, 1999). RMSEA (0.045) and SRMR (0.039) are lower than 0.08, which indicates the low residual error and good parsimony (Hair et al., 2019). Also, both GPI (0.954) and AGFI (0.928) exceed advisable values, indicating the suitability of the model as a whole (Byrne, 2016). These results validate that there is a consistent model of measurement that can be used to analyse the structural equation modelling.

Model Fit Measure (CFA).

Figure 3 shows the SEM predictions of FBS based on FA, OFK, SFK and DFL (Hair et al., 2019). The positive impacts of DFL (β = 0.38) and SFK (β = 0.21) are followed by the positive impact of OFK (β = 0.27), and the negative impact of FA (β = −0.35) is in support of the fact that FA decreases financial performance (Shapiro & Burchell, 2012). Exogenous variables also show positive correlation, as the correlation between OFK and SFK (r = 0.44) and SFK and FA (r = −0.28) is statistically significant. Moreover, reliability was ensured by strong factor loadings, and the model explains 51% variance in FBS, which shows that it has a significant explanatory power (Farrell et al., 2016).

Structural Equation Modelling (SEM).

Hypothesis Testing and Structural Model Results

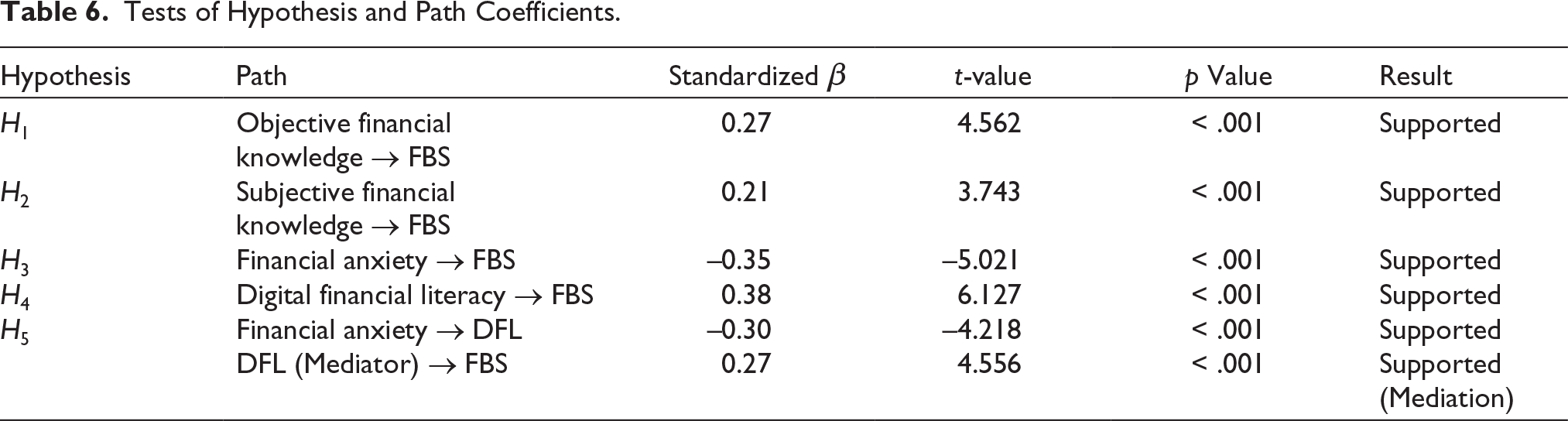

All tested hypotheses (H1–H5) were statistically significant at p < .001, as shown in Table 6 and Figure 3. In support of H1, OFK positively influenced financial behaviour and satisfaction (β = 0.27, t = 4.562, p < .001), consistent with Lusardi and Mitchell (2014). Regarding H2, SFK had a significant positive effect (β = 0.21, t = 3.743, p < .001), supporting Allgood and Walstad (2016). Similarly, H3 was confirmed, as FA negatively affected FBS (β = –0.35, t = –5.021, p < .001), in line with Shapiro and Burchell (2012). H4 was supported, with DFL emerging as the strongest predictor (β = 0.38, t = 6.127, p < .001), reinforcing OECD (2022). Furthermore, H5 was validated, as FA negatively influenced DFL (β = –0.30, t = –4.218, p < .001), while DFL positively predicted FBS (β = 0.27, t = 4.556, p < .001), confirming partial mediation (Farrell et al., 2016).

Tests of Hypothesis and Path Coefficients.

Indirect Mediation Effects Analysis

Table 7 shows a significant negative indirect effect of FA on FBS through DFL (β = –0.081, t = 3.762, p < .001), confirming partial mediation. Higher anxiety reduces DFL, which in turn lowers FBS. However, strong digital skills help offset anxiety’s impact. This supports Grohmann et al. (2018) on digital capability and inclusion, and Lusardi (2019) on its compensatory role. The findings emphasize integrated financial education in digital economies (OECD, 2022).

Mediation Analysis.

Multi-group Moderation Analysis: Gender and Age

Table 8 indicates that gender significantly moderates the relationship between FA and FBS, with a stronger negative effect among females (β = –0.42) than males (β = –0.29) (Δχ² = 4.87, p = .027). This aligns with prior evidence that women report higher FA and greater behavioural consequences (Archuleta et al., 2013; Farrell et al., 2016; Lusardi & Mitchell, 2014; OECD, 2020). However, age did not significantly moderate this relationship (Δχ² = 2.12, p = 0.145), suggesting anxiety’s negative impact is consistent across age groups (Prawitz et al., 2017; Shapiro & Burchell, 2012).

Moderation Effects Analysis.

Discriminant Validity Matrix

As indicated in Table 9, the AVE values for all the constructs, FA (0.781), OFK (0.725), SFK (0.806), DFL (0.788) and FBS (0.778), exceed their corresponding correlations with other constructs. This indicates that all the constructs have greater variation with their measurement indicators than any other, which satisfies discriminant validity requirements (Fornell & Larcker, 1981). The low-to-moderate correlations among the constructs also indicate that the latent variables are empirically unique, which enables more accurate estimation of structural paths in the model. These findings validate the conceptual separation between psychological, cognitive and digital dimensions of financial literacy, supporting their use in integrated behavioural models as recommended in recent financial capability literature (Hair et al., 2019; Henseler et al., 2015).

Discriminant Validity.

Discussion

The study illuminates the multidimensional interconnectivities between FA, OFK, SFK, DFL and FBS through direct and indirect structural equation modelling channels. To begin with, previous studies attributed objective literacy to better decision-making and risk management, and this idea is confirmed by the fact that FBS is promoted by OFK (Lusardi & Mitchell, 2014). The influence of SFK is justified because of the influence of confidence and perceived competence in a financial situation and confirms the fact that financial self-perception has the power to influence actual behaviour outside objective literacy (Allgood & Walstad, 2016). FA negatively affects financial behaviour, which confirms earlier studies on the incapacitating psychological tension, diminishing planning behaviour and increasing financial avoidance (Prawitz et al., 2017; Shapiro & Burchell, 2012). But it is interesting to note that DFL was the strongest indicator of healthy FBS, confirming its growing importance in digital economies where mobile banking, fintech platforms and e-wallets constitute the financial environment (Grohmann et al., 2018; OECD, 2022). Also, the mediation study established that DFL has some buffer capacity against financial anxieties, and therefore, digital competence may have buffer capacity against psychological constraints (Farrell et al., 2016). The strong moderation by gender confirms the literature on the fact that women can be more financially anxious than men because of the socio-economic differences, variations in financial socialization and the differing access to resources (Lusardi & Mitchell, 2014; OECD, 2020). Studies also show that women often report lower financial confidence and higher susceptibility to stress-induced financial avoidance (Archuleta et al., 2013; Farrell et al., 2016), which may explain the stronger negative FA → FBS path observed for females in this study. These findings indicate that gender-sensitive financial counselling and education programmes may be very useful in overcoming FA and cultivating healthier financial behaviours (Hung et al., 2012). The non-significance of an age-based moderation effect implies that the negative effect of FA on financial behaviour does not cut across generations. Similar to Shapiro and Burchell (2012) and Prawitz et al. (2017), this result implies that interventions designed to alleviate FA ought to involve all ages and still acknowledge the greater vulnerability of women in this aspect. Previous models failed to incorporate the complex interplay between emotional and cognitive influences and digital proficiency in order to inform financial behaviour. Contributions of the study include empirically validating psychological, cognitive and digital dimensions into behavioural finance research and providing policymakers and educators with tangible findings towards the establishment of overall financial well-being in digital economies (Xiao & Porto, 2017).

Practical Implications and Theoretical Contribution

The present study also has significant policy relevance for policymakers, financial educators, mental health experts and digital service providers interested in enhancing financial well-being in the context of a rapidly digitizing economy. The stronger direct effect of DFL on financial behaviour also puts emphasis on massive-scale, inclusive and interactive literacy programmes. Traditional delivery models like face-to-face workshops or static Web-based modules might be inferior in the current setting, where ease of access, interactivity and customization determine engagement. Accordingly, app-based learning delivery systems, gamified teaching instruments and mobile-optimized curricula hold great promise as delivery channels that will resonate with both young age groups and digitally literate yet financially apprehensive adults (Grohmann et al., 2018; OECD, 2022). It is important to note that such interventions should involve the use of behavioural nudges such as personalized prompts, micro-educational resources and goal-tracking features to ensure that acquired knowledge is translated into long-term behavioural changes.

The mediation results that reveal that FA is a crucial psychological correlation between DFL and behaviour also show that knowledge acquisition itself is not sufficient to ensure that the optimum financial choices are made. FA can impair information processing and justification-avoidant behaviour and lead to suboptimal decision-making even among already financially literate individuals (Farrell et al., 2016; Shapiro & Burchell, 2012). Therefore, finance education must possess dual purposes of enhancing information-driven competencies as well as reducing affective barriers. Practical interventions may include the introduction of stress-management skills, financial counselling and peer support group hotlines into literacy programmes so that individuals are able to cope with the informational and emotional aspects of financial choice. Mental health professionals can greatly contribute to this integration and will be able to provide evidence-based solutions to the reduction of anxiety that will take into account additional traditional training in the financial field.

The critical design implications of the moderation results, that is, the gender gap concerning the FA–behaviour relationship, are for the inclusive financial capability programmes. The greater negative relative to women can also be attributed to the fact that women are supposed to receive low financial confidence, more anxiety and be more responsive to financial stressors compared to men (Archuleta et al., 2013; Lusardi & Mitchell, 2014). Interventions in finance thus ought to take a gender-sensitive approach and deliver gender-specific confidence-building workshops, mentorship opportunities and context-specific illustrations that mirror women’s experiences. Policy settings also might encourage financial institutions towards the production of gender-sensitive products and services like flexible savings products or women-specific investment clubs that build capability while managing anxiety.

From a theoretical perspective, the research adds to behavioural finance through the building and empirical examination of an integrated framework that combines cognitive (DFL), emotional (FA) and demographic (gender, age) drivers of financial behaviour. In doing so, it overcomes shortcomings of conventional models such as the financial capability model and TPB that tend to isolate knowledge and attitudes (Xiao & Porto, 2017). In revealing that DFL acts both directly and indirectly through emotional channels and that these relationships vary between demographic groups, the research extends the theoretical discussion of financial capability to incorporate both affective and demographic moderators. Placing these mechanisms into the context of accelerating digitalization, it also provides a fresh point of view of financial resilience with technological predisposition at the centre, as well as traditional financial capabilities. The practicality of theoretical behavioural finance, as is corroborated by real-world changes, renders the theoretical behavioural finance more relevant to policy and practise.

Overall, the results indicate the significance of a contextual approach to the process of financial capability building, which is holistic. To policymakers, it is simple; the interventions would need to be inclusive, technologically advanced and psychologically enlightened. On the part of educators, the results support the significance of content customization, in terms of both knowledge and emotional conditions. To researchers, the research provides a model that can be modified and expanded to other socio-economic, cultural and technological settings, leading to future cross-cultural and experimental confirmations.

Research Limitations and Future Avenues

Despite the fact that this study offers valuable information about the relationship between financial literacy, financial distress and financial behaviour in the digital world, some gaps should be mentioned to serve as points of reference in further studies. First, the survey design of a single point in time places restrictions on the ability to determine causality since it represents relationships in one moment rather than following the changes in behaviours over time (Creswell & Creswell, 2018). Second, the use of self-report measures puts certain biases at risk, including social desirability and memory-based biases, which might predominantly influence constructs such as subjective knowledge and financial conduct (Podsakoff et al., 2003). Future research might use objective measures such as behavioural tracking data on financial transaction records or app usage data to increase the validity of measurement. Third, the sampling frame of only digitally competent adults might exclude certain groups of people from low incomes, rural areas and older citizens with low exposure to digital financial instruments. This under-representation might restrict the findings’ generalizability into other wider socio-economic and demographic segments (OECD, 2020). Stratified sampling or quota sampling, among other more heterogeneous socio-economic and geographic groups, might close the gap. Lastly, though gender and age moderation effects have been investigated here, other possible moderators such as financial self-efficacy and trust in finance and also conformity to norms in cultures have been omitted. Inclusion of these variables in future models might allow more nuanced perspectives of differences in behaviours within cultural and institutional settings (Farrell et al., 2016; Xiao & Porto, 2017).

In addition to these avenues, future studies might use experimental methods to establish causal inference and determine the effectiveness of interventions designed specifically for favourable behavioural outcomes among different segments of the population (Carpena et al., 2019). Randomized controlled trials might be used to ascertain whether customized DFL programmes developed with gender-sensitive and anxiety-reduction enhancements significantly enhance behavioural outcomes for different segments of the population. Laboratory experiments might also vary exposure to financial stress and assess related decision-making and thus hold constant the psychological mechanisms of the FA–behaviour relationship (Shapiro & Burchell, 2012). Longitudinal panel studies might also record the dynamic development of financial literacy, anxiety and behaviour and help identify pivotal life phases or economic incidents where intervention might have the greatest effect. This would not only expand theoretical knowledge but also generate evidence-based advice on how to design scalable and inclusive financial capability initiatives in swiftly digitizing economies.

Conclusion

The current research examines the impacts of FA, objective and SFK, and DFL on the digital FBS of individuals. With the help of SEM, the study confirms that actual knowledge and perceived self-efficacy have positive impacts on financial conduct, while FA has a negative impact on the outcome of conduct and thus prevents them. Surprisingly, DFL was also discovered to exist in direct prediction and mediation roles, considering its ability to neutralize psychological distress. Additionally, the moderation analysis revealed that gender significantly shapes the strength of the FA–behaviour link, with women experiencing a stronger negative effect, underscoring the need for gender-sensitive financial capability programmes and policy interventions. These contributions strengthen the behavioural finance theories by adding digital competence as an essential element in financial capability and thus bridging a gigantic gap in cognitive- and attitudinal-based theories (Lusardi & Mitchell, 2014; Xiao & Porto, 2017). The study also provides empirical support for the inclusion of emotional variables, including anxiety, in financial literacy models, as earlier argued that financial well-being should be addressed holistically (Shapiro & Burchell, 2012). The implications of the findings are most applicable to the field of digital financial inclusion, particularly in lower-middle income economies, where mobile platforms are the most common in financial transactions (OECD, 2022). The fact that the analytical system includes the demographic, emotional and cognitive determinants gives the study a multidimensional idea of financial behaviour in the digital age, which provides a strong foundation for theoretical refinement, along with the particular practical interventions. Through its emphasis on the complex relationships between knowledge, feelings and digital literacy, the current study provides a solid basis for the subsequent work, education policy and study in enhancing financial resilience in the technologically dynamic societies. Further longitudinal and experimental studies in the future would help to support these associations and determine intervention strategies that have the most causal effects on various population groups.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.