Abstract

Purpose:

This research highlights how behavioural, demographic and perceptual aspects affect bottom of the pyramid (BoP) customers’ intentions to use digital banking services in India. To comprehend how constructs such as perceived usefulness, ease of use, behavioural control, trust, risk perception and fees/charges shape attitudes and eventually determine digital banking adoption intention within economically underprivileged banking consumers is the main objective of this study. It acknowledges the critical value that digital financial inclusion has in promoting the use for those who have low incomes.

Methodology:

The research follows an analytical structure that is based on a quantitative research methodology and structural equation modelling. To collect accurate data, standardized questionnaires were given to an accurate representation of 504 BoP customers from different parts of India. A 5-point Likert scale was applied to test 34 items that covered 8 important variables connected to adopting digital banking. The constructs’ resilience was significantly checked by thorough validity and reliability testing, which covers exploratory factor analysis and confirmatory factor analysis. Perceived usefulness (PU), perceived ease of use (PEOU), perceived behavioural control (PBC), perceived risk (PR), perceived trust (PT), fees/charges (FC), attitude towards digital banking (ATDB) and intention to adopt digital banking were all assessed directly and through mediation by the hypothesis testing conducted within the SEM framework.

Findings:

The study’s findings indicated that each of the seven proposed hypotheses is positive and statistically significant. In particular, ATDB are significantly improved by PU (β = 0.183, p < .001), PBC (β = 0.157, p = .004), PEOU (β = 0.198, p < .001), PR (β = 0.162, p = .002), FC (β = 0.122, p < .001) and PT (β = 0.175, p < .001). Among BoP users, this positive attitude significantly predicts their propensity to utilize digital banking (β = 0.543, p < .001). However, although PR usually prevents adoption, the positive effect found indicates that BoP consumers have a positive ATDB when problems are seen as controllable or exceeded by benefits, with adequate transparency and trust. The framework used has an outstanding goodness-of-fit indices (CMINdf = 1.737, RMSEA = 0.038, CFI = 0.961) which highlight the findings’ validity and dependability.

Originality:

This research is focused on India’s BoP customers, who are among the most economically disadvantaged and technologically disadvantaged consumers, in contrast to the majority of earlier studies that focus on modern cities or higher-income consumers. The research improves the knowledge of digital banking adoption among low-income consumers by combining several behavioural, demographic and perceptual aspects into a strong SEM framework and validating extensive scales with good reliability (Cronbach’s α > 0.75 across constructs). Conventional assumptions are further challenged by the positive correlation between PR and attitude, pointing to complex dynamics in the relationship between risk and trust for BoP consumers. This unique addition speeds up the adoption of digital banking in lower-middle income nations by offering a useful scholarly and academic guide.

Keywords

Introduction to the Topic

Digital transactions are crucial for bottom of the pyramid (BoP) customers because they are very accessible and convenient (Sinha et al., 2024). Many research projects have explored how these customers in lower-middle income countries intend to behave when using new technologies. The BoP, which consists of the economically disadvantaged portions of the community, offers a distinct and challenging adoption frontier, whereas urban residents and middle-income groups have easily incorporated online banking into their everyday financial routines (Prahalad, 2012). This group, which makes up a sizeable section of people in India, is frequently distinguished by poor earnings, lack of education and inadequate availability of standard banking facilities.

Since the consumers in large Indian cities are more educated and have the advantage of having more possible wealth, they are particularly prominent and loud in their demands for their entitlements and regulations are primarily designed to meet their needs. Therefore, the ‘forgotten piece’ in India’s banking system is still the BoP segment. Having a bank account for savings and depositing funds into it is frequently equated with being financially empowered. These days, a customer can use an internet rating as a forum for evaluating an item while sharing their satisfaction with it with others. Comments can quickly circulate across the internet and reach a large audience, which could harm the brand of a business (Kim & Kang, 2018). Additionally, it is anticipated that banks will provide freshly developed products and services that are more affordable and time-efficient than those they offered in the past (Rahi & Abd. Ghani, 2019). It is also important to be aware of how challenging it is to keep an eye on a business’s digital image, given the amount of facts available (Rantanen et al., 2019). The development of numerous remote or mobile-based products and services has been facilitated by the improvement of internet platforms in lower-middle income nations like India. Because they are highly convenient and easily accessible, mobile payments are significant for consumers who are at the BoP, according to various surveys (Shukla et al., 2023; Sinha et al., 2024). Many research efforts have looked at how individuals in lower-middle income nations intend to use modern technologies (Neelam & Bhattacharya, 2023). The growing usage of technology is leading to an increase in the proportion of internet-enabled cell phone owners (Neelam & Bhattacharya, 2023). Numerous financial institutions have found that using online banking is a highly lucrative and inexpensive solution (Lee, 2009). Numerous banks have taken advantage of this to cut expenses while simultaneously enhancing their offerings (Xue et al., 2011). Even though electronic banking has many advantages for users, its performance has consistently lagged behind banks’ goals (ProQuest, n.d.). Traditional banking services are always considered less risky than establishing premises that purchase Internet banking services (Cunningham et al., 2005). The banking sector has had a paradigm shift in its services. The adoption of technology is low although digital technology covers a lot of facilities (Ly & Ly, 2022).

The coronavirus disease 2019 (COVID-19) pandemic continues to emphasize and demonstrate the value of digital banking systems (Liu et al., 2019), which offer banking anywhere, at any time. The most populous but frequently disadvantaged economic category in the human race is known as the base of the pyramid.

This group of individual residents frequently deal with insufficient resources, such as restricted availability of power, hygienic water, restrooms and conveyance. This may affect their general health and standard of living. Most of the published research shows that those users have unique wants that are different from middle-of-the-pyramid clients (Sinha et al., 2024).

Literature Review

Numerous elements impact the wide acceptance of digital bank services among purchasers with a low level of income. Acceptance is encouraged by perceived benefits, usability and favourable sentiments around mobile banking, but it is hampered by perceived hazards and discouragements (Purohit & Arora, 2023). The use of internet banking by BoP customers is also influenced by fiscal, natural and cultural factors. Many variables impact the acceptance of electronic banking in India, particularly within underprivileged communities. Smartphone possession, banking practices and socio-economic traits all have a big influence on digital financial participation. Merely 35.2% of the participants reported using electronic banking services, indicating that adoption levels are still poor in spite of its attempts to encourage financial literacy using electronic means (Ali & Ghildiyal, 2023). BoP customers’ adoption and use of m-payments were found to be significantly facilitated by perception, social factors and self-confidence (Shankar, 2024). Fears about vulnerability, confidentiality and safety risks have been determined to be major barriers to BoP customers’ acceptance and utilization of digital banking services (Shankar, 2024). Users’ transition to digital banking may be facilitated by in-branch interaction with consumers, digital branch alteration, user-centric campaigns and redefining the function of branch employees. The need for comprehensive organizational and societal shifts at the institutional level to win over users’ assurance and belief in digital banking is the primary driver of the increased adoption of electronic financial services in India (Kaur, Ali, et al., 2021). Consumers’ belief and faith in online banking are largely influenced by peer pressure, desired performance and perceived security risk when it comes to the acceptance of the Unified Payments Interface among BoP consumers (Joshi, 2024). For the majority of Indian consumers at the BoP, accessibility and peer pressure have a beneficial influence on their desire to adopt online banking applications. There is no significant relationship between the intent to accept digital banking and creativity, trust or compatibility. The association involving digital adoption intention and adaptability is moderated by gender as well (Sodhay et al., 2024). The three primary drivers of digital financial accessibility in India are banking practices, mobile phone control and socio-economic characteristics (Ali & Ghildiyal, 2023). According to Kaur and Batra (2023), Indian women customers are prepared to embrace digital banking and their intent to utilize it is encouraged by perceived utility, usability and behaviour. Digital financial access has significantly replaced social and economic financial services in the Indian banking industry (Sarkar & Thapa, 2021). The COVID-19 pandemic and technological developments have caused this change, which has led to an increase in the use of online banking facilities (Kaur, Kiran, et al., 2021). Transfer of money using the banning services on a hand-held device is one of the many online or smartphone-based services that have evolved as an outcome of the growth of digital networks in lower-middle income countries like India (Kautish et al., 2023). Multiple studies highlight the importance of online transactions for consumers at the BoP because it is relatively easy to use (Glavee-Geo et al., 2019; Neelam & Bhattacharya, 2023; Senyo et al., 2023; Shukla et al., 2023). Users can communicate with the bank via smartphone apps, facilitating a range of banking functions from a distance (Picoto & Pinto, 2021).

Last but not least, Prahalad (2012) said that the invention approach was crucial due to social–cultural settings, illiteracy rates, limited accessibility and lack of instruction of BoP users for these types of offerings. This might influence how they perceive danger and make them anxious about using modern technologies, particularly for BoP users who are uneducated or only partially educated.

Theoretical Framework

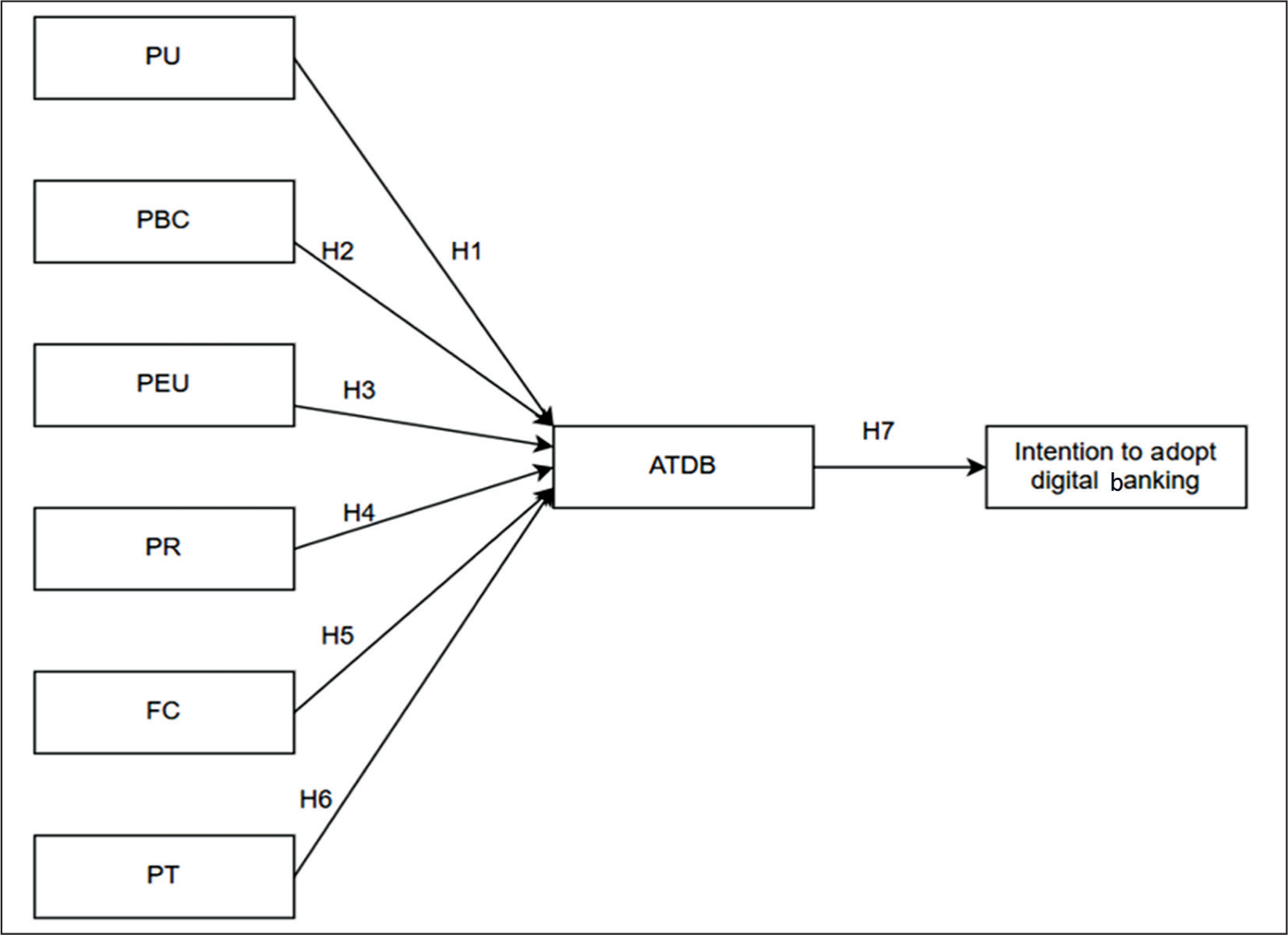

More precisely, the research aids in examining the function of the ‘Theory of Planned Behaviour’ (TPB) and the ‘extended Technology Acceptance Model’ (TAM3) in foretelling the uptake of digital cashless banking. TAM and its extended versions serve as the primary theoretical foundation for this research. These models highlight how users’ attitudes towards technology are influenced by perceived utility and PEOU, influencing their behavioural intention and true acceptance. The theory also includes components from the TPB, acknowledging that intent is greatly affected by attitudes, subjective standards and PBC. Such models incorporate concepts such as PR, PT, FC and demographic characteristics (gender, age and education) that act as a combination of primary influencers and possible mediators in order to reflect the varied nature of user behaviour.

A more complicated awareness of the ways that cognitive assessments (e.g., usefulness and trust), emotional perceptions (e.g., risk) and sociodemographic factors interact to affect the desire to adopt online bank facilities, especially at the base of the pyramid, is made possible by this integrative paradigm. Thus, the model is suitable for examining digital adoption behaviour in various and developing user groups since it serves both descriptive and prognostic roles. Figure 1 represents the research framework and the process followed.

Proposed Model.

Problem Synopsis and Research Motivation

In addition to increasing virtual platforms, the current administration is introducing several new technologies. To effectively introduce digital payments at the BoP is the nation’s guiding principle. Normal activities alongside innovative solutions that clients may choose are constantly linked together on the Web pages of all banks. This includes nationalized, local as well as private banks. Yet, there continue to be a lot of people and long lines at the bank, notably among ‘BoP’ users, local shop owners and traders. This demonstrates that a majority of this group still does not understand internet banking and its features or is not embracing digital technology. The prime goal of the investigation is to study how users are adopting digital banking facilities. To determine whether embracing ‘Internet banking’ is legitimate, the researcher has chosen this theme. Most of the published research shows that those users have unique wants that are different from middle-of-the-pyramid clients (Sinha et al., 2024).

Research Methodology

This step aims to deliver an explanation of the fundamental framework, techniques and steps involved in achieving the intended goals. A serious effort has been taken to organize and conduct the research investigation, which comprises classifying and clarifying the variables impacting the uptake of facilities provided by the bank online, primarily in the Indian context, following the established framework. This chapter describes the critical steps taken to gather data and identify the research objectives. The research conducted is empirical, wherein information has been collected from banking users who belong to the lowest-earning community. For this research, the term ‘respondent’ is applied equally. The information concerns customers of both public and privately owned banks in India. The survey has undergone testing in a pilot survey, and the results are detailed in the subsection that follows.

Research Questions

What prevents BoP banking consumers from switching to digital banking?

What influences BoP banking users to adopt digital banking?

What are the key security concerns of BoP consumers that affect their use of digital banking

Research Objectives

To identify the factors affecting the digital banking behaviour of BoP consumers

To identify the driving forces behind the adoption of digital banking by BoP consumers

To examine the consequences of risk, security and trust on the use of digital banking.

Hypothesis Development

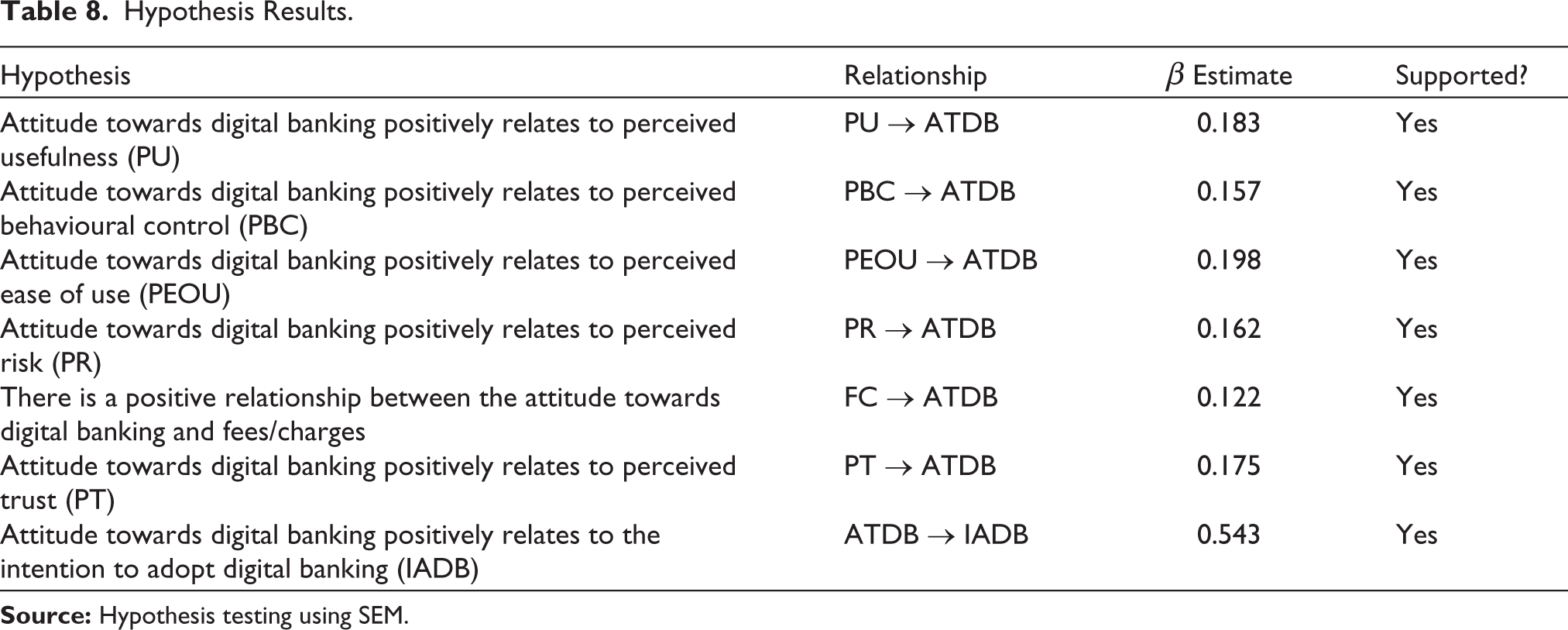

H1: There is a positive relationship between the attitude towards digital banking and perceived usefulness.

H2: There is a positive relationship between the attitude towards digital banking and perceived behavioural control.

H3: There is a positive relationship between the attitude towards digital banking and perceived ease of use.

H4: There is a positive relationship between the attitude towards digital banking and PR.

H5: There is a positive relationship between the attitude towards digital banking and fees/charges.

H6: There is a positive relationship between the attitude towards digital banking and perceived trust.

H7: There is a positive relationship between the attitude towards digital banking and the intention to adopt digital banking.

The suggested framework was designed keeping the research objectives and hypotheses in focus in Figure 1.

Research Design

This is a method that allows the rational blending of many elements. ‘Descriptive, exploratory’, and ‘informal study styles’ are generally regarded as primary categories of survey methods. Because the study’s concern is characterized and hypotheses are further developed, the exploratory design facilitates an accurate proposed approach. However, because the study and hypotheses are well established, the design will not be appropriate for this study. Instead, a descriptive design is more appropriate because this study will use a descriptive design to evaluate relationships among the factors, a key benefit of descriptive design. A survey will be used to gather data for this investigation. Hence, interaction would be the focus of this work. The methodology of this investigation is descriptive, which may be summarized. Throughout the research, the sampling dimension is an important factor. The bigger the number of participants, the greater in-depth the research, according to Luck and Rubin (1987).

Operational Definition of the Predominant Construct

Most BoP consumers often encounter challenges such as limited access to technological advances, an absence of digital literacy and worries regarding confidence and safety in online services; it is imperative to comprehend their behavioural intentions. To promote financial stability and independence, this research project intends to find solutions to boost the use of online banking among this group by analysing the factors impacting their choices for behaviour.

Perceived Usefulness

Perceived usefulness (PU) is the degree to which a person believes that using a particular device would enhance their capacity to do what they do. PU is primarily composed of perceived ease of use (PEOU), network effectiveness and trustworthiness. The likelihood of continuing to use a product is more strongly predicted by happiness. If variables impacting the acceptability of digital banking are ranked, the PU comes in second.

Perceived Ease of Use

The level of confidence that a person believes using a tool will be simple is known as PEOU. It is perceived comfort of use and is used to describe the degree of comfort experienced by consumers when they perform financial transactions and how comfortable they are operating a bank’s digital application (Rana et al., 2025).

Attitude Towards Digital Banking

The idea of attitude plays an important role in understanding the usage and adoption of digital banking services. Attitude refers to an individual’s favourable or unfavourable approach towards engaging in a particular behaviour, specifically the operation of online banking features. It is presently critical that it strongly influences behavioural intention, which increases the likelihood of a user adopting electronic banking services

Perceived Risk

An individual’s personal opinion of perceived risk (PR) is influenced by a variety of factors, including mood, past experiences and environment. It may have a considerable influence on a user’s opinion of using digital banking services. PR is a concept that captures consumers’ worries about possible drawbacks when utilizing mobile banking solutions.

Intention to Adopt Digital Banking

The ‘Intention to Adopt Digital Banking’ (IADB) construct concerning digital banking adoption is the preparedness or desire of a person to use digital banking features. It is actually about figuring out what drives consumers to utilize digital banking features and allowing bankers and other financial organizations to tackle these issues and increase the accessibility and popularity of banking on the go. Getting individuals enthusiastic and at ease with handling their money while on the fly is the primary aim. Research has indicated that numerous considerations are more significant for some individuals.

Perceived Behavioural Control

In behavioural science, the term ‘perceived behavioural control’ (PBC) describes a person’s belief that they have the power to influence other people’s behaviour. PBC in the framework of acceptance of digital banking relates to a person’s belief in their capacity to persuade others to embrace the use of digital banking services. The construct takes into account things like the accessibility of the assets that can affect behaviour. Studies have indicated that PBC significantly influences the use of online banking services.

Fee/Charges

Even if using digital banking has made financial services more accessible, consumers still need to understand the associated fee structure in order to successfully manage their spending. These might include the expenses involved in obtaining the digital banking services and the costs connected with the device used to access these services, such as internet-enabled mobile devices.

Perceived Trust

A person’s perception of trust is a major factor when choosing to adopt digital banking services. It is characterized as users’ anticipation that their requirements will be satisfied during risk-free electronic transactions and that adopting digital financial features is safe and contains protections for privacy. It may also cover things such as how easy it is to operate the gadget and the organization’s reputation. The degree of confidence that people or organizations believe that digital platforms are dependable and secure is known as perceived trust (PT) in the acceptance of digital banking services. It has a high implication on both the likelihood and how the digital services are consumed. Many variables impact the PT construct. PT is among the primary factors associated with the widespread usage of digital banking services, besides PU and ease of use, according to a few studies. According to other research, the factor that has the largest influence on users’ decisions to keep using digital banking services is trust.

Validation of the Instruments

Before making any inferences from survey data, we need to be certain that each instrument’s questions (or items) accurately and consistently reflect the fundamental ideas of the theory. There are various uses for validation:

Verifying accuracy: It attests to the correct measurement of every construct, including perceived utility, trust, risk and simplicity of use. Creating consistency: It confirms that the objects are internally coherent, which means that each of them stands for an identical fundamental idea. Evaluating dimensionality: It determines if the findings fall within the parameters or predicted characteristics specified by theoretical frameworks (e.g., extended TAM).

The questionnaire collected a variety of common demographic data, such as:

Gender Age group Educational qualification Occupation Residential location (urban/semi-urban/rural)

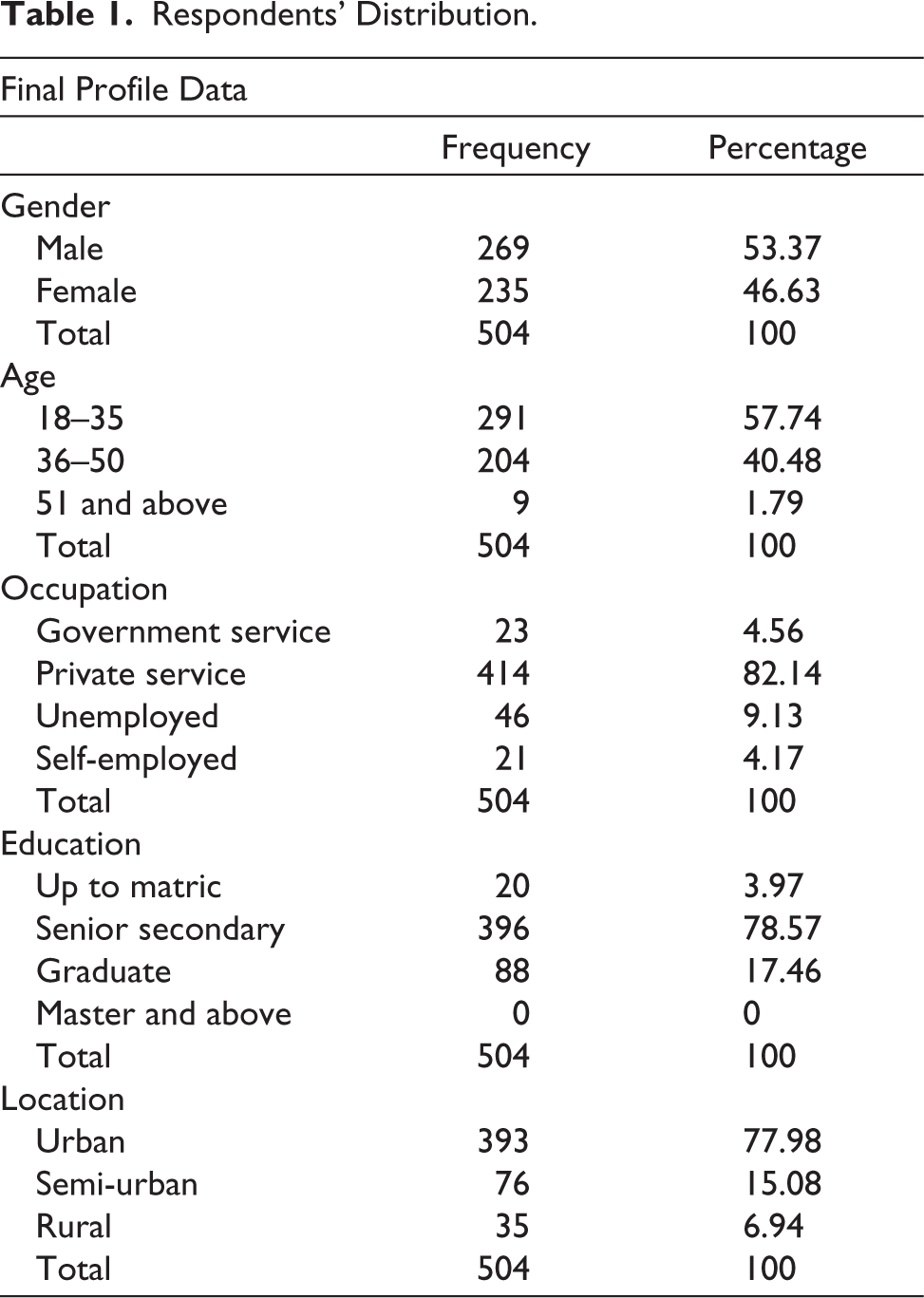

A cumulative of 504 replies were obtained from the below poverty line consumers using banking services. The data are shown in Table 1. A total of 53.37% of the respondents were males, and 46.63% of them were females. The largest participation was from the age group 18–35 years.

Respondents’ Distribution.

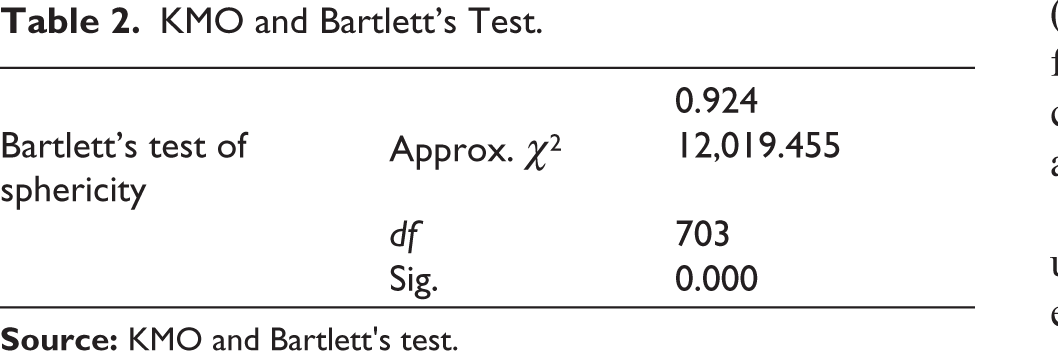

KMO and Bartlett’s Test

The findings of the sample adequacy ‘Kaiser– Meyer–Olkin’ (KMO) test are reported in Table 2. The reading of KMO was 0.924, which is above 0.6; the result supports that the sample was sufficient for the research. ‘Bartlett’s Test of Sphericity’ p value was below .05, supporting the idea that the sample was sufficient for the study.

KMO and Bartlett’s Test.

Analysis

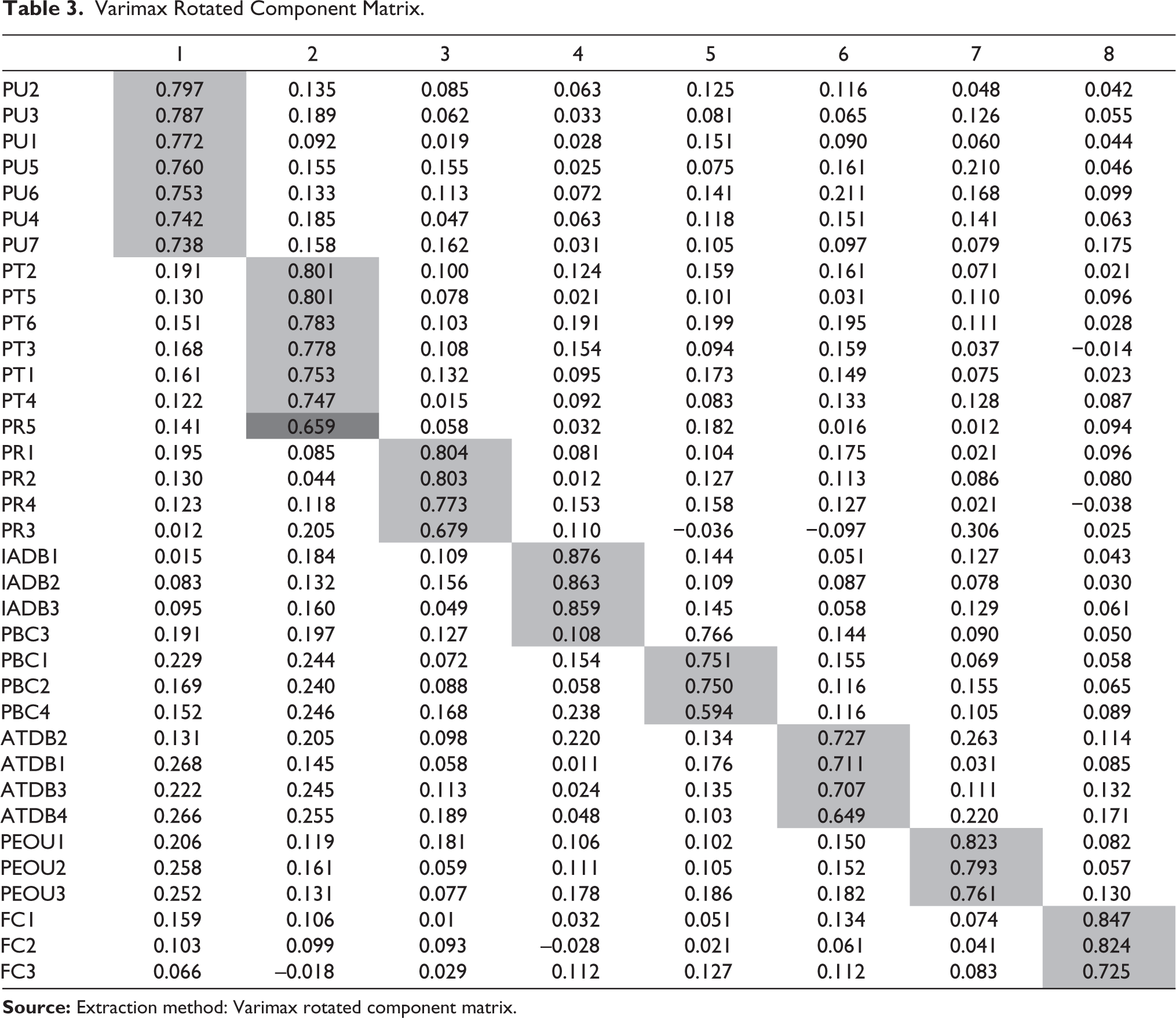

A factor load of more than 0.50 is highly important for the research (Hair et al., 2010). Therefore, any component in this investigation that did not load upon one factor at 0.5 or below was eliminated. Additionally, Lederer et al. (2000) and Vijayasarathy (2004) proposed repeating the factor analysis till each component loaded at 0.5 or above on a single factor. The scale’s dependability shows that it has no chance of accidental mistakes in the research. Cronbach’s coefficient α was adopted in the current research to evaluate the internal consistency. The validity and reliability of the components taken into consideration for the investigation on a Likert-type scale are often assessed by Cronbach’s α test. The stated constructs and the demographic profile were statistically analysed by the author using SPSS Version 29.0.2.0(20). A number of 0.7 or higher indicate that the scale’s sections measure the same item. The minimum cut-off value to measure internal consistency is 0.60. The Cronbach’s α was studied for the cumulative magnitude of digital banking adoption. An eigenvalue higher than the criterion of 1 was implied to decide the number of variables.

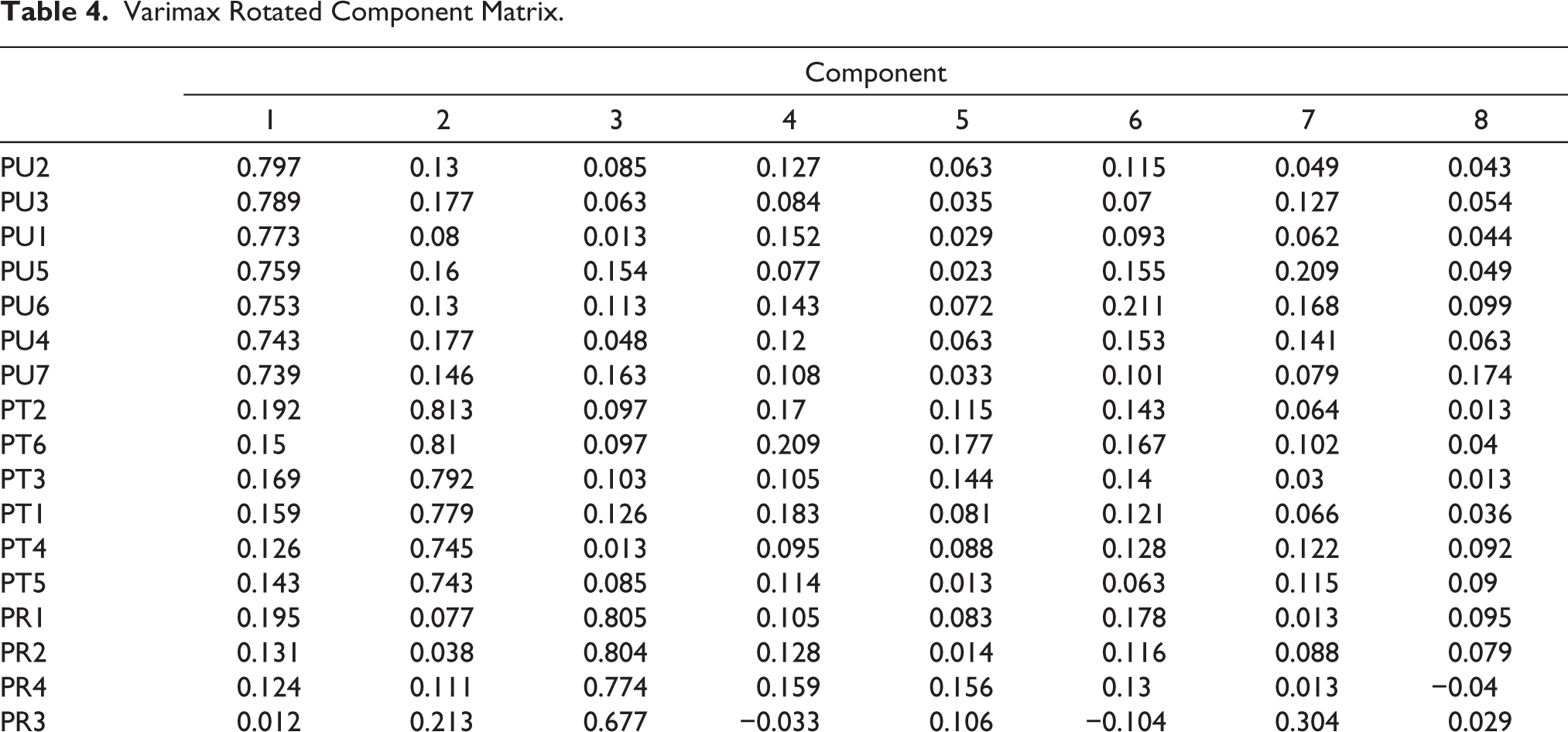

The eight factors accounted for 71.461% of the variance, and all the data points were loaded on the appropriate components as per the expectations, except item PR5 (I feel I need to be more careful while using digital banking services). This was expected to load in Factor 3 (PR), but it was cross-loaded with Factor 2 (PT). As a result, it was decided to take this item off the scale and repeat the factor analysis once again to gather nine components. Table 3 displays the outcome of the main component factor analysis using Varimax rotation to extract eight elements.

Varimax Rotated Component Matrix.

As the results demonstrate, in the output in Table 4, all the items are loaded as expected and the value of each item was more than 0.50. Finally, 34 items were considered significant for the study. Eight components account for 72.138% of the overall variance, making it greater than 50%, and every factor’s eigenvalue is greater than 1. A model of data was discovered using the factor analysis of the rating system that contained the 34 items that were identified (Table 4).

Varimax Rotated Component Matrix.

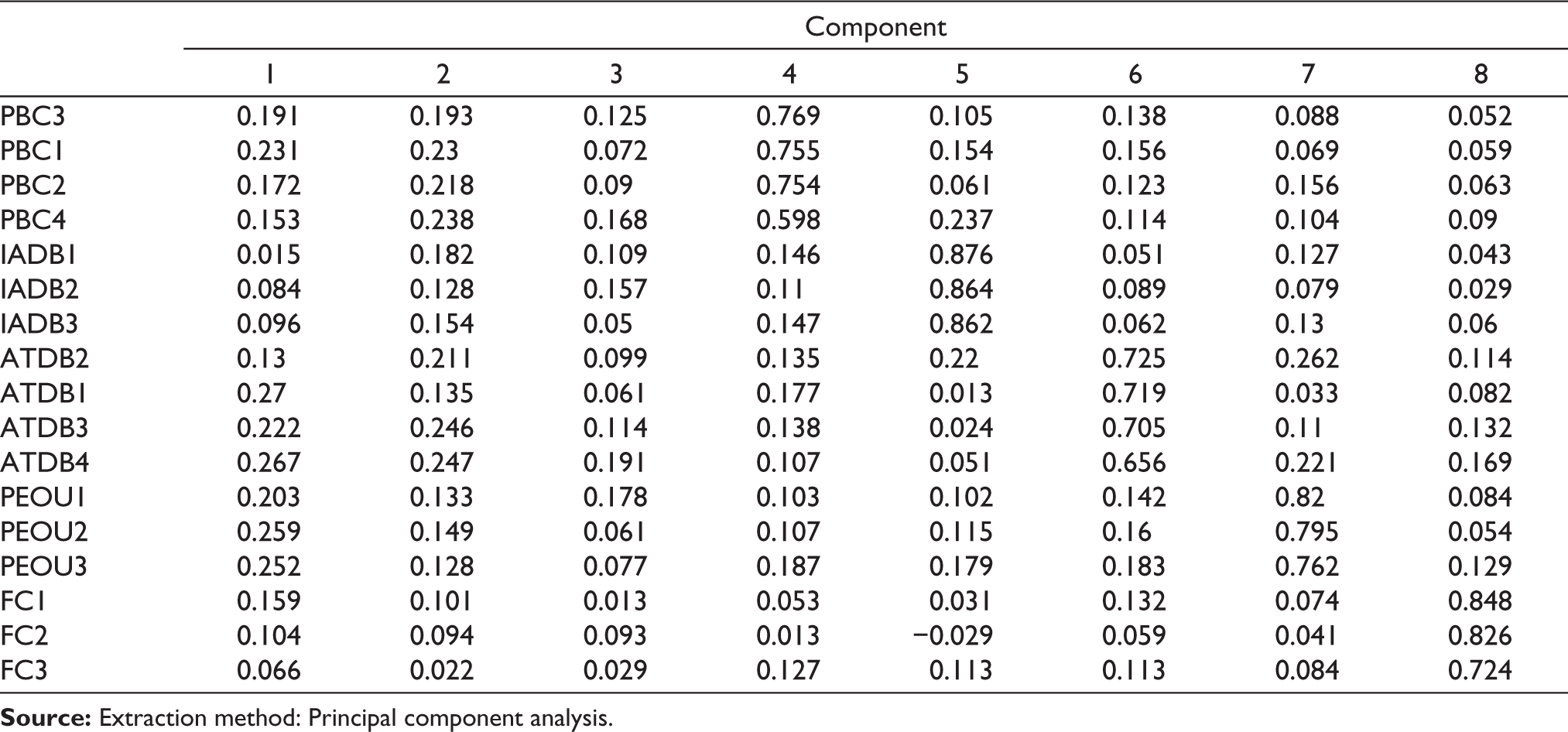

In Table 5, Cronbach’s α (reliability) scores for each factor exceeded the recommended cut-off point of 0.7, as suggested by Jr et al. (2019) and Nunnally (1978).

Reliability Test (All Factors).

Confirmatory Factor Analysis: Adoption of Digital Banking Evaluating Model

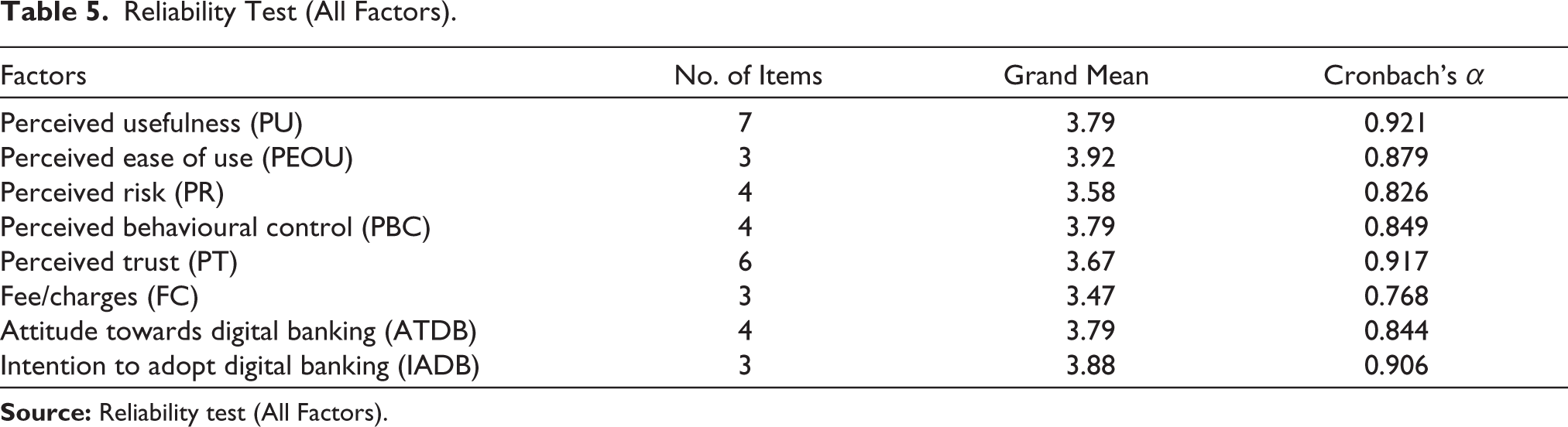

To understand the proposed framework, a confirmatory factor analysis (CFA) was employed. The overall goodness of fit of the model was assessed using eight standard model fit metrics. Goodness-of-fit index (GFI), the ratio of χ2 to the degree of freedom (df) (CMIN/df), adjusted goodness of fit (AGFI), comparative fit index (CFI), normative fit index (NFI) and root mean square error of approximation (RMSEA), Tucker–Lewis’s index (TLI) and incremental fit index (IFI) (Byrne, 2010; Hair et al., 2010). The outcomes of these tests are shown in Figure 2, which provides an overview of these outcomes.

Summary of Model Fit Indices.

The brief in Figure 2 displays the fit indices, which were utilized to understand the goodness of fit for a model. The explanation is shown below:

CMIN/df (χ2 degree of freedom): The model score is 1.737, which is lower than the recommended benchmark value of <3, suggesting the model is a good fit. Values lower than 3 reflect a reasonable match, suggesting that the model does not depart far from reality and successfully balances complexity. The result 1.737 indicates a solid model fit with minimal disagreement compared to the degrees of freedom. RMSEA (root mean square error of approximation): The model value is 0.038, which is lower than the suggested value of 0.08, recommending a good fit with minimum error. The figures less than 0.05 imply a great match, while values between 0.05 and 0.08 represent fair approximations. RMSEA assesses the extent to which a model with uncertain, but ideally designed estimations of parameters fit the sample covariance matrix while accounting for the complexity of the model. It compensates for the inaccuracy of the estimate per degree of freedom. An RMSEA of 0.038 indicates an excellent match with low approximation error. GFI (goodness-of-fit index): The model value is 0.901, which just exceeds the suggested value of 0.90, indicating a good fit. GFI calculates the fraction of variance explained by the calculated group correlation. The comprehensive index of fit ranges from 0 to 1. Measurements surpassing 0.90 are judged good. A score of 0.901 is considerably greater than this threshold, demonstrating that the model matches the data seen in the layout successfully. AGFI (adjusted goodness of fit): The model score is 0.880, which is higher than the recommended >0.80, suggesting a good model fit. AGFI penalizes complicated models to support simplicity by adjusting the GFI for degrees of freedom. A score of 0.80 or above is regarded as appropriate. Even a score of 0.880 indicates that the framework fits effectively. CFI (comparative fit index): The model value is 0.961, surpassing the recommended >0.90, indicating a strong model fit. CFI involves numerous samples and evaluates the intended model’s fit to a baseline model, usually one that assumes no correlations between parameters. It has a range of 0 to 1. An adequate match is indicated by a score higher than 0.90, while a good fit is suggested by a score over 0.95. In comparison to a null model, 0.961 indicates a very high satisfactory model fit. NFI (normative fit index): The model value is 0.912, which is above the recommended value of >0.90, supporting a good fit. NFI measures fit progress by comparing the desired model’s χ2 score to that of a null model. A value >0.90 indicates an excellent fit, and a value of 0.912 indicates that the suggested model fits the information greater than a model that assumes no connections. TLI (Tucker–Lewis index): The model value is 0.956, which exceeds the suggested value of >0.90, showing a strong model fit. The non-normed fit index, sometimes referred to as TLI, evaluates the fit of a model to a null model while accounting for the complexity of the model, preferring models with less complexity where fit is comparable. A good fit is suggested by values >0.90. A score of 0.956 demonstrates a great match between explaining ability and simplicity. IFI (incremental fit index): The model score is 0.961, higher than the >0.90 benchmark, indicating a good-fitting framework. Taking the number of samples and degrees of freedom into consideration, IFI calculates the proportional enhancement of the fit of the suggested framework over a null model. A score of 0.90 or higher is desired. The framework matches significantly better than a baseline model, as indicated by the value 0.961.

Overall, all fit indices met their recommended values, suggesting that the framework supports an excellent fit.

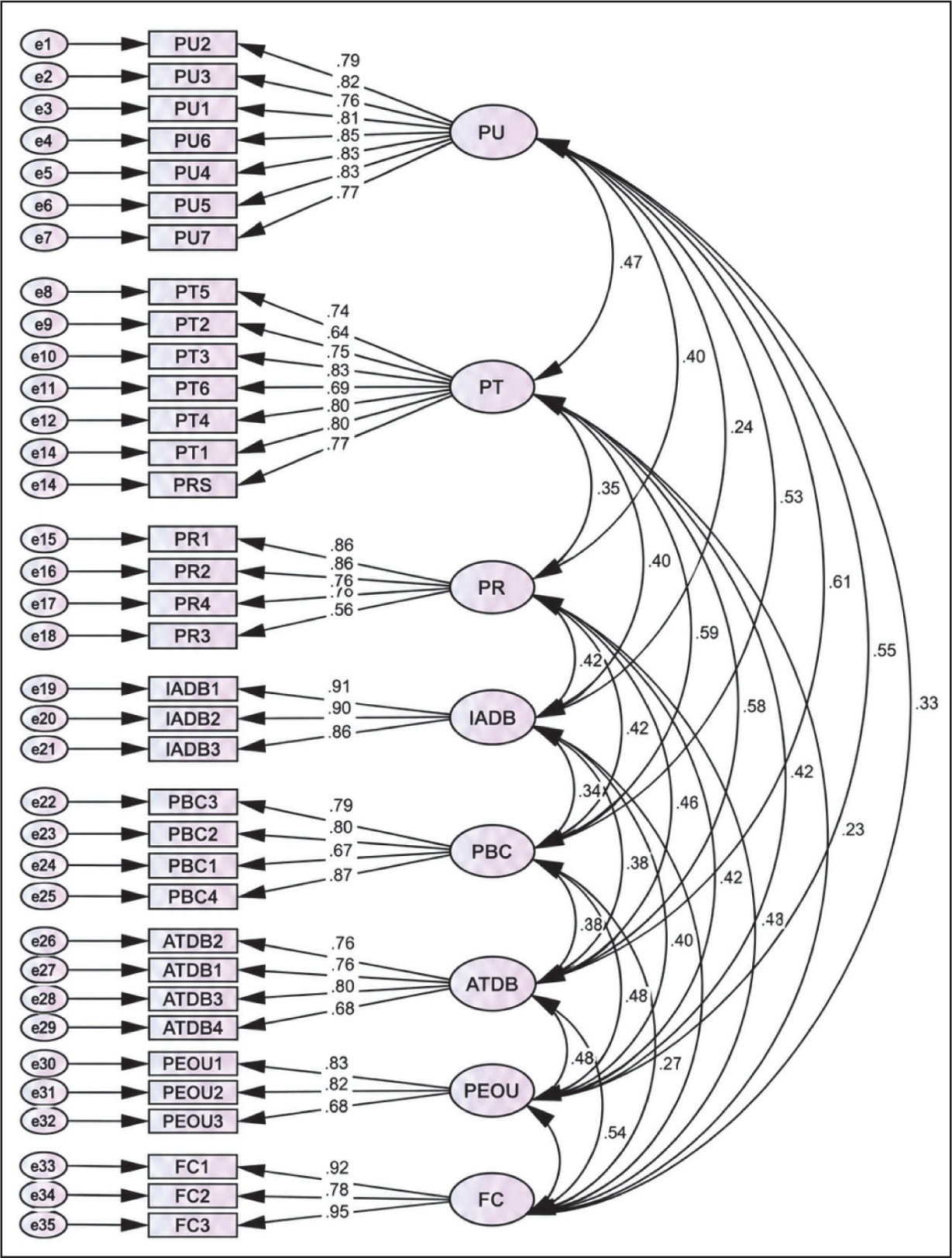

Figure 3 represents the measurement model of IADB.

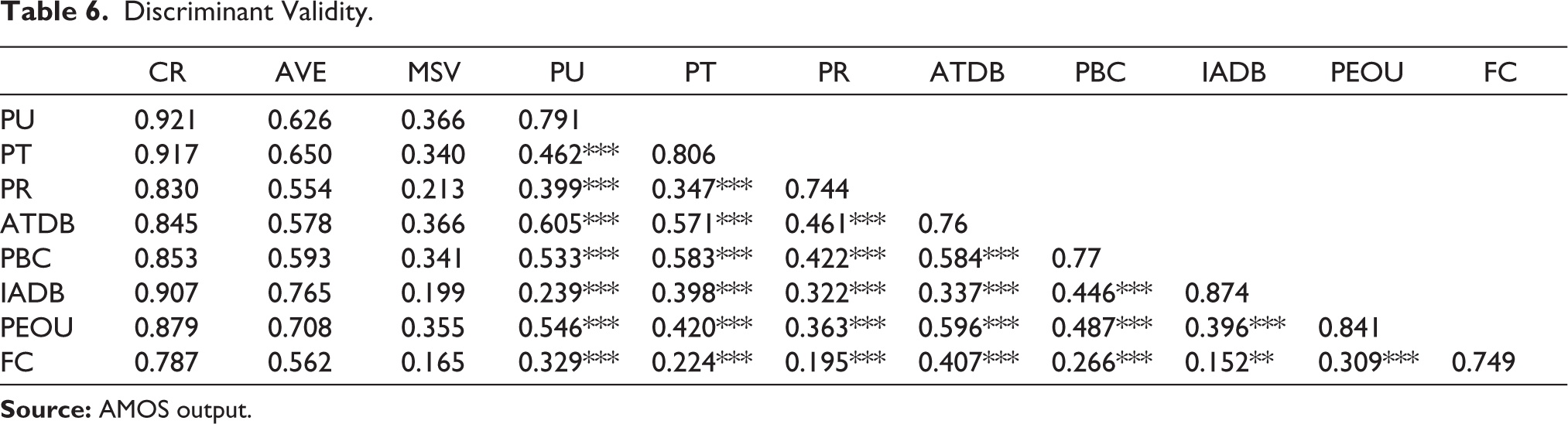

The measurement model’s consistency was examined by utilizing composite reliability (CR). All of the Cronbach’s α’s and CRs were greater than the indicated benchmark of 0.7, suggesting that the scales exhibited strong consistency and reliability. By examining the factor loading that was derived by each scale item in Varimax exploratory factor analysis (EFA), convergent validity was also examined (Hair et al., 2010). Additionally, all of the scale items that were left in place had standardized regression weights greater than 0.50, which satisfies the suggested values (Hair et al., 2010). It also highlights the convergent validity of the scales examined in this research. Additionally, we looked for discriminant validity (Table 6) by analysing the intercorrelation scores and the squared root of the AVE for the latent construct. The square root of the AVE was more than the corresponding coefficients with the factors. In addition, the score of AVE of each construct was higher than MSV, suggesting higher discriminant validity (Fornell & Larcker, 1981). In sum, the study revealed that the scale used in the study carries sufficient validity and reliability and that the model is fit for hypothesis testing.

Discriminant Validity.

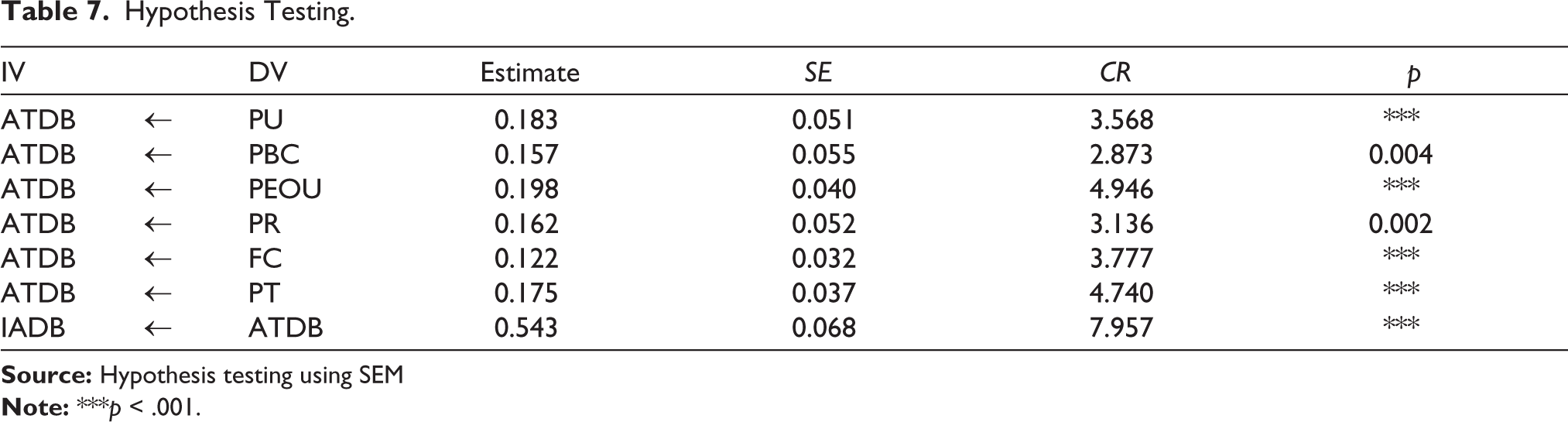

Hypothesis Testing

The next phase was to evaluate the architectural connection to verify the hypotheses after the measurement model had been evaluated and constructed.

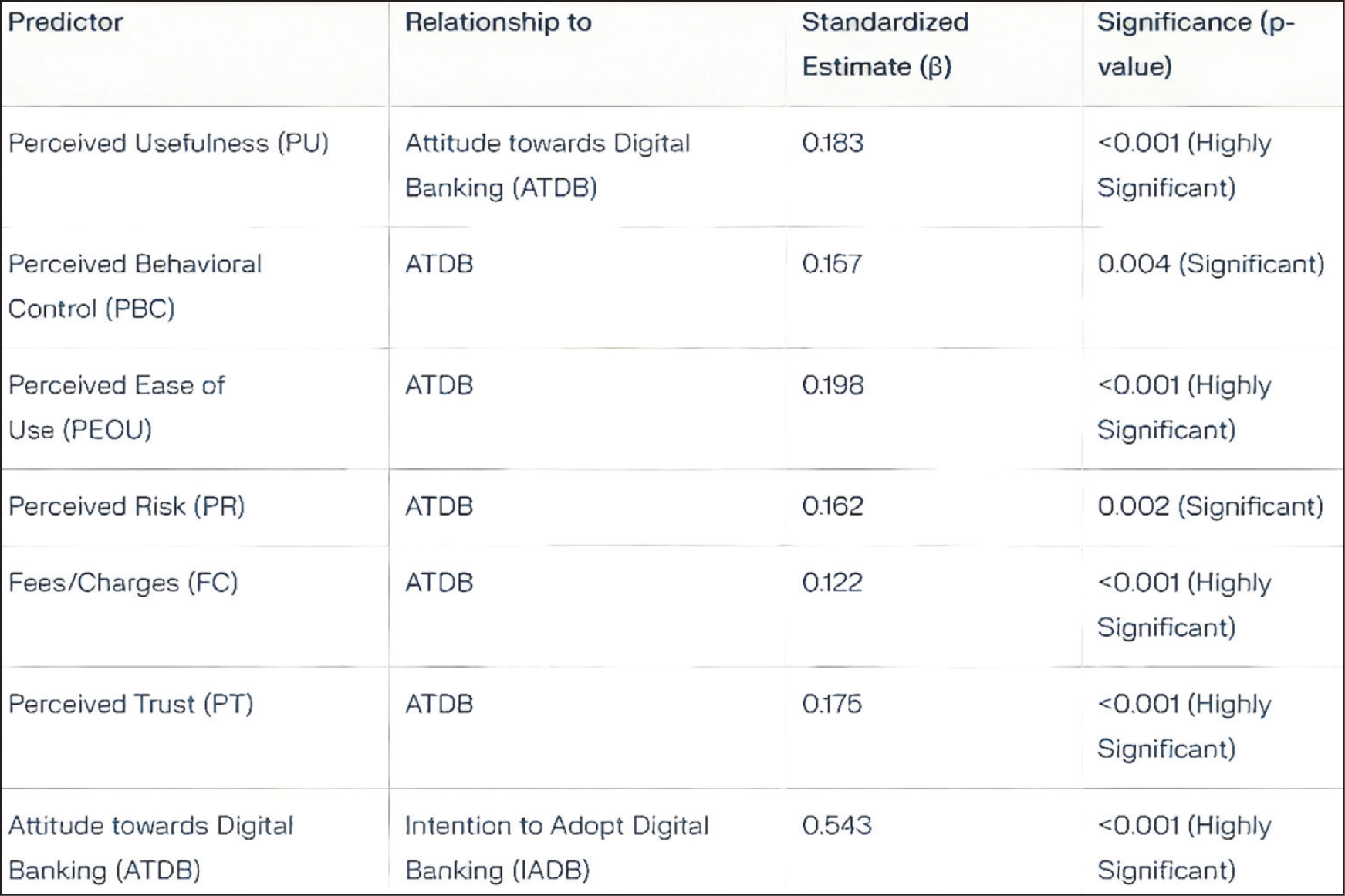

The result shows (Table 7) that PU had a favourable relationship with attitude towards digital banking at value (β = 0.183; t = 3.568, p < .001) and PBC had a favourable and critical relationship with attitude towards digital banking at value (β = 0.157; t = 2.873, p = .004). Similarly, PEOU (β = 0.198; t = 4.946, p < .001), PR (β = 0.162; t = 3.136, p = .002), FC (β = 0.122; t = 3.777, p < .001) and PT (β = 0.175; t = 4.740, p < .001) had significantly positive relation with ATDB. Figure 4 displays the AMOS Output.

Hypothesis Testing.

ATDB and behavioural intention to use digital banking had a pertinent and strong relation (β = 0.543; t = 7.957, p < .001).

Findings revealed that the many contributing variables to the ATDB facilities were the intention to accept electronic banking, followed by PEOU, PT and FC.

Discussion

EFA and CFA confirmed that eight viable components had strong reliability (Cronbach’s α > 0.75 for all): PU, PEOU, PR, PT, PBC, FC, ATDB and intention to use and adopt the same.

Construct validity was confirmed by the good model fit that CFA produced (CMIN/df = 1.737, RMSEA = 0.038, CFI = 0.961). Every association that was hypothesized turned out to be statistically significant. ATDB was the best predictor of IADB (β = 0.543, p < .001). The analyses are visible in Table 8 and Figure 5.

Hypothesis Results.

Hypothesis Results and Significant p Values.

BoP customers are driven by the usable advantages that digital banking services offer to their everyday accounting issues, as seen by the significant advantages of perceived utility on attitude. This is congruent with TAM, which emphasizes PU as the primary factor influencing positive attitudes and adoption intention

Conclusion

This study significantly expands our understanding of how demographic variables and behavioural consequences interact. The study has discovered major links and patterns that both support and challenge prior theoretical presumptions by employing powerful statistical methodologies and thorough hypothesis testing.

The findings show that while educational achievement may not have as big of an influence as previously believed, age and gender continue to have a major effect on how people perceive or react in the circumstances under consideration. The regression model illustrates the presence of additional factors that need to be looked at, given its modest prediction ability.

Theoretically, this study recommends a revision of traditional models and encourages the inclusion of demographic factors as essential components of behavioural models. In terms of application, the results offer a foundation for more specialized strategies in marketing, policy development, community engagement and human resource management. From a social standpoint, the study highlights the importance of equity and inclusion in institutional and public processes. This research demonstrates itself as a significant actual research that adds to scholarly discourses and offers practical information for practitioners and decision-makers by acknowledging its limitations and suggesting future research options. This helps bridge the knowledge gap between research and application, theory and practice and information and decision-making.

The results show that PU and ATDB at cost were positively and significantly correlated, viewed as behavioural control. The following were significantly and favourably correlated with ATDB: PEOU, PR, FC and PT. There was a favourable relationship between the behavioural intention to utilize digital banking and the attitude towards it. Similarly, behavioural purpose and PT were positively correlated. Lastly, there was a favourable relationship between behavioural intention and the desire to use digital banking. The alternative hypotheses, H1 through H7, were thus approved. The results showed that PEOU is the most important variable influencing the intention to utilize bank service digitally, followed by PU, PR and PT.

PU, usability, behavioural control, threat, costs and trustworthiness are all integrated to provide a comprehensive knowledge about the way BoP customers’ views regarding electronic banking develop.

These beliefs have a significant impact on behavioural intentions to use digital banking, highlighting the significance of attitudes in the adaptation process.

The findings validate the suitability of combining contextual factors specific to BoP with TAM and TPB theoretical approaches to explain the uptake of digital banking among low-literacy and economically disadvantaged populations.

Businesses, lawmakers and proponents of financial wellness must aggressively develop user-friendly, secure, affordable and accessible digital banking services to overcome penetration barriers in the BoP category. Initiatives that boost public awareness and confidence must support such offers.

Adoption strategies are also adapted to this vulnerable group by recognizing the intricate relationship between apparent costs and implied risk.

Attitude is a key influencing factor for digital banking adoption intentions, since each independent variable has a significant impact. This reinforces the critical role of attitude as an emotional bridge between perceptions and eventual behaviour. The attitude-to-intention path’s β value of 0.543 is much higher than that of the predictor-to-attitude pathways, indicating that nurturing positive attitudes boosts acceptance desire.

Attitude determinants have β values ranging from 0.122 to 0.198, indicating that each element contributes significantly and works together. This shows that a diversified strategy is required to address the increasing adoption of digital banking.

Ideal model fit and reliability: Statistical analysis confirms the model’s fit and reliability.

This extensive and demonstrated understanding provides the possibility to increase economic mobility through technical innovations that address the lived experiences and views of BoP users.

Limitations and Future Scope

Despite its methodological complexity and interesting conclusions, the study is not perfect. There are numerous limitations to the current study on the adoption of digital banking among Indian BoP customers. The study’s cross-sectional approach limits its ability to follow variations in behaviour over time, and its geographical focus may not sufficiently represent the diversity of events occurring across the country. Possible differences arise from depending entirely on information supplied by participants, and the study’s breadth may have overlooked essential variables such as social consequences and social customs. Furthermore, if not checked periodically, the rapid evolution of digital financial systems may render certain findings outdated.

Long-term checks may give information on behavioural characteristics throughout time, allowing for further research. If socio-economic inclusion rose, the conclusions would be more generally relevant. Other aspects, such as cultural effect and technical expertise, may help to provide a more complete understanding of adoption procedures. Evaluation of the effects of curricular activities and research into cutting-edge technologies such as biometric authentication may help to guide approaches to encouraging digital banking within BoP communities. Analysing administrative and legislative frameworks can also help to improve India’s financial accessibility.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflict of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.