Abstract

The present study focuses on deciphering how varied psychological and cognitive factors interact in shaping the way Indian retail investors approach socially responsible investments (SRIs), based on social cognitive theory. A well-grounded set of 487 active, registered Indian retail investors were accumulated for the purpose of obtaining meaningful patterns by implementing a hybrid data analysis approach by mixing structural equation modelling and an Artificial Neural Network, using SmartPLS 4 and SPSS 21.0. The results confirm that all the determinants, including financial literacy, environmental beliefs and the extent to which people adhere to social cues, tend to strongly predict the SRI behaviour of a retail investor. Interestingly, ‘social norms’, among all predictors, surfaced as the strongest determinant of SRI behaviour. These insights can be practically implemented in designing sustainable financial literacy programmes, which could further give investors the confidence to include SRI options in their portfolios.

Introduction

The increasing evidence on the impact of global challenges such as poor regulatory compliance, environmental risk management and climate crisis on financial stability has been significantly shifting investors’ perspective towards considering environmental, social and governance (ESG) funds in their portfolios (Rathee & Aggarwal, 2022; Widyawati, 2019). Consequently, ‘socially responsible investment (SRI)’ has emerged as an integral investment strategy while advancing the global commitment towards Sustainable Development Goals (SDGs) (Arefeen & Shimada, 2020; Matharu, 2019; United nations, n.d.).

The financial market plays a key role in supporting SDGs. However, despite the emerging potential of SRI in the financial market, owing to the limitation of information and acceptability related to ESG funds in India, its recognition is still at a nascent stage as compared to other high-income nations (Janz et al., 2025; Jonwall et al., 2022; Weber, 2014). Consequently, a substantial gap in knowledge persists with regard to determining whether factors, such as ‘financial literacy (FL)’, ‘social norm (SN)’ and ‘environmental belief (EB)’, can potentially drive ‘socially responsible investment decisions (SRID)’ among retail investors in India. In the pursuit of filling this gap, the study proposes integration of all these factors together within a comprehensive conceptual framework. Stakeholders can better manage portfolio performance and lower risks arising out of environmental and social challenges. Financial knowledge acts as a significant determinant of investment decisions as lack of it may lead to ‘sub-optimal’ investment decisions by neglecting the ESG issues and their long-term impact on profits and also on society (D’Hondt et al., 2022; Filippini et al., 2024). Therefore, the knowledge and consequences of sustainable investing, as well as the better decision-making, are based on the level of financial intelligence. Furthermore, investor preference for SRI has also been linked to the appreciation of their EB. Vanwalleghem and Mirowska (2020) emphasized the importance of EB as the driving force behind the demand for sustainable practices. SN, on the other hand, represents issues such as societal standards, peer pressure and cultural attitudes towards sustainable investment’s performance, aggregately impacting investment behaviour (Mishra, 2023).

Although investment decisions have been studied thoroughly, most of the work has been done in the context of traditional investment techniques (Akhtar & Das, 2018; Mittal, 2019). The present study contributes to the existing literature by shedding light on the subject of the investors’ behavioural dynamics resulting from SRI imperatives, which has received comparatively less attention than SRI performance evaluation analysis studies (Widyawati, 2020).

Moreover, most of the prior research on SRI behaviour has been grounded on proven theories, such as the ‘theory of planned behaviour (TPB)’, the ‘theory of reason action (TRA)’ and the ‘goal-setting theory’ (Adam & Shauki, 2014; Nair & Ladha, 2014; Raut et al., 2020; Singh et al., 2021; Sultana et al., 2018). This study, however, uniquely applies the ‘Social Cognitive Theory (SCT)’ to comprehend the psychological motivating factors among retail investors leading to their SRI behaviour.

Furthermore, as highlighted by Hassan et al. (2023), most studies have limited their research to ‘investment intention’ as the dependent variable. In this study, we have extended it by assessing ‘investment decision’ as the outcome variable, which has not been thoroughly explored. Besides, the majority of the Indian studies in this context have drawn their sample using convenience sampling from a specific region, hindering the generalizability of the findings across diverse socio-economic settings (Garg et al., 2022; Mathivathnan et al., 2022).

Consequently, the current investigation uses SCT as a basic framework that investigates the pathway to SRI decision-making. Specifically, it questions the complex interactions among FL, EB and SN. Moreover, the research requests responses from Indian retail investors to comprehend the determinants of SRI engagement among retail investors by incorporating a hybrid sampling design using both random and convenience sampling techniques.

Accordingly, the research questions to be addressed in the study are as follows:

RQ1: To what extent is the level of financial literacy of an individual related to the level of involvement in socially responsible investments? RQ2: How do individual environmental beliefs, which include environmental sustainability and concern about climate change issues, influence their choice of SRI options? RQ3: In what way do social norms influence individual investment decisions, especially in the domain of environmentally conscious investing? RQ4: What are the specific nonlinear relationships among FL, EB and SN that contribute to SRID?

The main purpose of the research is to devise a conceptual framework that answers the above research questions. To this end, an empirical analysis of dynamics of all the predictive variables (FL, EB and SN) with respect to individual investor SRI decisions in India is pursued. In addition, the research aims to explain the mediating mechanisms by which environmental convictions and social norms affect investment decisions, thereby highlighting the implications for the promotion of sustainability. Finally, the study attempts to find out the most salient antecedents of socially responsible investment behaviour among Indian retail investors and propose strategies for leveraging the antecedents to facilitate the transition towards a more environmentally conscious economy.

The remaining portion is structured into five sections. The second section entails the arguments on the theoretical background for model conceptualization. The literature review of the study is included in the third section. The fourth section provides a detailed discussion of the research methodology, including data analysis. The findings are discussed in the fifth section, while the sixth section concludes.

Theoretical Framework and Conceptualization of Model

Theoretical Premise

Unlike the classical economic view of how people make investments, behavioural economics explains that investing decisions are driven by many different attributes such as cognitive processes, psychological attitudes and social influences (Kahneman, 2003; Sofi et al., 2023). SCT explains that individuals learn through interactions with their social environment and that the social environment, along with the behaviours of others, directly affects the way we think, behave and interact (Bandura, 1986). SCT has been employed as a theoretical framework for studying a variety of disciplines and topics, including organizational management (Chang & Edwards, 2014; Wood & Bandura, 1989), health-related behaviours (Anderson et al., 2007; Tsai, 2014), purchasing decisions (Lim et al., 2019; Milakovic, 2021; Perera et al., 2019) and a wide array of other multidisciplinary areas. Therefore, due to the versatile applicability of SCT across various contexts, the present study conceptualizes the proposed model rooted in SCT.

Conceptual Model

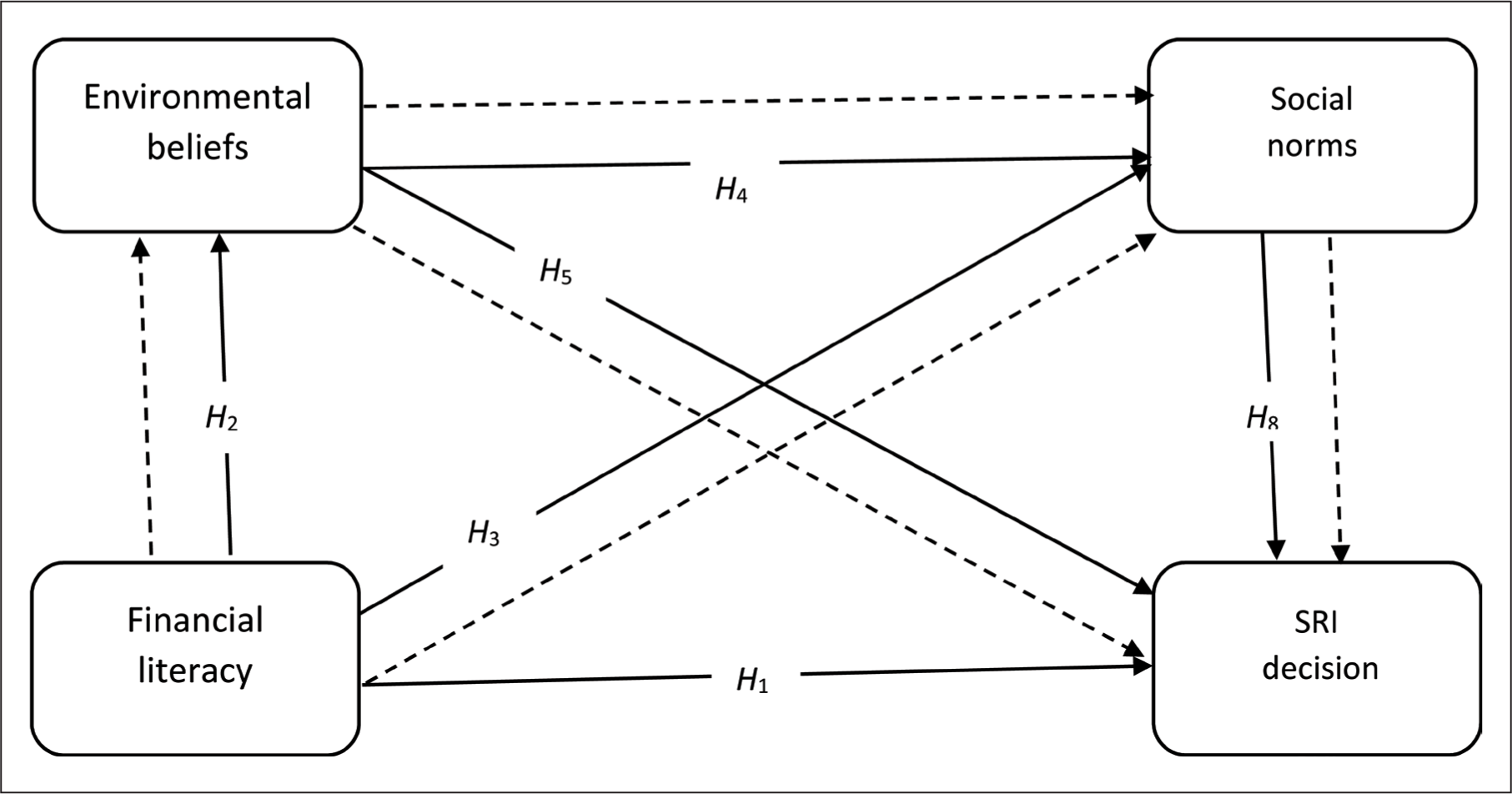

Based on SCT, the current study aims to examine three essential factors in the SRI choice process: (a) financial literacy (FL), as a personal factor affecting an individual’s likelihood to invest responsibly (Dwiastanti, 2015; Pa et al., 2022; Raut, 2020); (b) the EB of an individual investor, as a cognitive factor, influencing an investor’s decision to engage in socially responsible investing (Egan, 1986; Henry & Dietz, 2012); and (c) SN, as an environmental factor and as a factor driving an individual’s willingness to make investment decisions regarding socially responsible investment and SRI decision-making as a behavioural response (Kinzig et al., 2013; Perry et al., 2021) as depicted in Figure 1.

Review of Literature and Hypotheses Formulation

The Relational Dynamics Between FL, EB, SN and SRID

Financial literacy is relevant to having the financial awareness and broader knowledge of financial management of personal finance, and hence enabling the making of informed and ideal financial choices, such as financial budgeting, saving and financial investment choices (Lusardi & Mitchell, 2014; OECD, 2017; Remund, 2010). Empirical studies have shown over and over that people with higher levels of financial literacy have a better understanding of non-financial risk factors and their potential influence on investment decision-making (Hermansson & Jonsson, 2021; Lusardi & Messy, 2023; Molina-García et al., 2023). Access to such knowledge allows for a critical appraisal of investment options in accordance with both non-economic and economic objectives (Jonwall et al., 2022; Lusardi & Mitchell, 2014).

The conceptual definition of FL has moved outside the limits of conventional numerical proficiency and basic financial knowledge to also include sustainability considerations, ethical decision-making and social awareness (Lusardi & Mitchell, 2014; OECD, 2017). Moreover, according to OECD (2017), financial literacy is important and needs to be made sustainable, which is a framework that considers non-economic factors in the decision-making process of financial matters. Notably, poor FL, as reported by Rahmandoust et al. (2011), can be a major hindrance in the path of sustainable development, and also, improving the FL of individuals can greatly mitigate the consequences of economic downturns. FL has been proven to be a crucial antecedent to individual investment choices as well as societal outcomes (Kar & Patro, 2024; OECD, 2017). Furthermore, the comprehensive knowledge of financial concepts creates social norms related to financial decision-making, namely conformity to societal expectations with regard to saving and spending habits, adherence to cultural investment strategies and also the impact of peer behaviour through herd behaviour and social proof (Banerjee & Das, 2023; Hidayanti et al., 2023; Rind et al., 2023). In addition, Katini and Amalanathan (2022) uncovered the fact that financially literate people are more likely to actively support sustainable products and practices, which implies the positive correlation between FL and sustainable progress. With more and more financial knowledge, investors prefer to invest a large portion of their investment portfolio in shareholder-responsible investing (Cucinelli & Soana, 2023; Nilsson, 2008). Supporting this tendency, Kumari and Harikrishnan (2021) further confirmed the potential of FL to improve decision-making and strengthen environmental sustainability.

Furthermore, a number of factors associated with social norms (including peer influence and the compliance of cultural and workplace norms) have a significant impact on financial decisions of investors. These influences take the form of behavioural biases such as herd mentality and social proof, which explains the tendency of individuals to base their financial decisions on the actions of others (Banerjee & Das, 2023; Bapna, 2017; G, 2021). Fernandes et al. (2014) emphasized the potential of FL to enhance social norms through sharing information. Nonetheless, the need remains to understand and validate FL’s effect on social norms in a social context (Lusardi & Mitchell, 2014).

Based on the above discussion, we formulate the following research hypotheses:

H1: FL positively affects SRID. H2: FL positively affects EB. H3: FL positively affects SN.

The Relational Dynamics Between EB, SN and SRID

An individual’s attitudes and convictions regarding environmental and sustainable issues are summed up in their EB (Dietz et al., 2005). EB come from personal experience, external influences and sustainable financial literacy, which significantly aid in internalizing the sustainability practices (Stern, 2002). Moreover, EB tend to positively nudge SN related to sustainability and the adoption of sustainable behaviours (Dilla et al., 2019; Gifford & Nilsson, 2014; Kollmuss & Agyeman, 2010).

Empirical investigations have consistently shown that people with a heightened environmental consciousness exhibit greater sensitivity to environmental variables and that they proactively consider the relevant information in investment decision-making (Gutsche et al., 2023; Miller et al., 2022). Bolton and Kacperczyk (2019) claim that people with high EB factor in environmental risk variables, such as carbon emissions, climate change and transition risks, in their evaluation of investment alternatives. Likewise, Schoenmaker and Schramade (2023) note that value investors focus on social responsibility in their investment decisions. Follows and Jobber (2000) support that such behaviour is significantly fuelled by a person’s dedication to sustainability.

Therefore, we offer the subsequent research hypotheses:

H4: EB has a favourable effect on SN. H5: EB has a favourable effect on SRID. H6: EB is a mediator in the association between FL and SN. H7: EB is a mediator in the association between FL and SRID.

The Relational Dynamics Between SN and SRID

In the last few decades, academics have supplemented classical economic models with social and psychological determinants in order to account for collective behaviour. SN as a set of unwritten codes determines human conduct (Bicchieri et al., 2023). Previous scholars have identified several mechanisms by which SN affects behaviour. For example, Li et al. (2021) show how different cultural norms influence investment choices, while Nguyen et al. (2020) show how media information and social networks influence investment choices. The tendency of people to follow the social beliefs that have been established changes their investment choices and drives the behaviour of herding (Cialdini & Goldstein, 2004). Bikhchandani and Sharma (2001) in a further attempt to explain herding behaviour attribute it to SN, where such norms require individuals to follow the prevailing market trends, and this is well reflected in market dynamics.

Based on the above arguments, we put forth the following hypotheses:

H8: There is a positive relationship between SN and SRID. H9: SN is a mediator in the association between EB and SRID. H10: SN is a mediator in the association between FL and SRID. H11: EB and SN collectively mediate the relationship between FL and SRID.

Materials and Methods

Data Descriptions

An explanatory research design using primary data was chosen as a means of executing the study. Additionally, the study implemented a combination of both random and convenience sampling strategies as part of a mixed sampling strategy to collect data from retail investors across India as to their perceptions regarding social responsibility issues within investing. This ensured that the study would be able to capture a broad range of demographics, geographical regions and other characteristics of investors across various regions, which include Northeast, North, South, East, West and Central regions, using a structured survey instrument that utilized a ‘5-point’ Likert scale. Data were accumulated between 10 December 2022 and 19 June 2023.

Discrete factors, including FL, EB, SN and SRID, were contained within the database. The dependent variable, SRID, represents how individual retail investors make investment choices in socially responsible funds. The independent variables were FL, EB and SN; however, EB and SN serve as mediators that explain the effects of FL and EB on the SRI decision-making processes of individual retail investors. Multiple regression analysis was performed to measure the total effect of FL, EB and SN on SRID. Artificial neural networks analysis was further integrated into the study to increase the depth and precision of the study’s findings relative to the behavioural dimensions of SRI decisions made by individual retail investors (Sharma et al., 2021).

Measurement Instrument

The questionnaire used in this study was carefully developed after an extensive literature review, elicitation of expertise recommendations and pilot testing (Carpenter, 2018). An explanatory framework was followed in the study in which primary data were collected in order to explore the hypothesized relationships. The measurement items were mostly drawn from existing literature, with selected items modified to fit the contextual nuances of the current study. For instance, items relating to the construct of ‘financial literacy’ were redefined to include ‘sustainable financial literacy’ in the context of investment decisions by retail investors (Appendix A).

The survey instrument included four constructs with a total of 17 items as FL, EB, SN and five items for self-regulated investment decisions. Each construct was rated on a ‘5-point Likert scale’ from ‘1 (strongly disagree)’ to ‘5 (strongly agree)’. Pre-testing, where the items were discussed with five experts who had worked at the field, was carried out per Churchill’s (1979) guidelines, resulting in minor changes in the wording of items. The final instrument was divided into two sections; the first section captured demographic data of the respondents, while the second section contained all the primary measures relating to the primary constructs.

Sampling and Data Collection

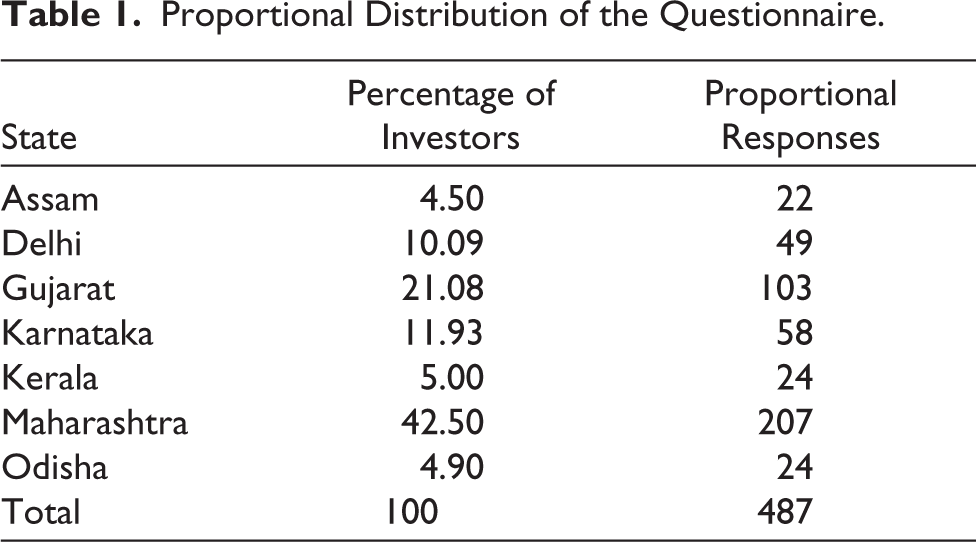

The positivist paradigm was considered the most appropriate to analyse the role of FL, EB and SN in SRID (Lee, 1991). Accordingly, retail investors of India’s capital market were identified as a target population and information was extracted from individual investors in various cities of India using a standardized survey protocol. Data collection was a two-stage sampling procedure. In the first stage, the number of registered investors per state was retrieved from the database of BSE India (n.d.), which is publicly accessible. A simple random sampling approach was applied to select seven states (Assam, Delhi, Gujarat, Karnataka, Kerala, Maharashtra and Odisha). In the second stage, questionnaires were mailed to individual investors within each selected state with the distribution proportional to the number of retail investors within the state as shown in Table 1.

Proportional Distribution of the Questionnaire.

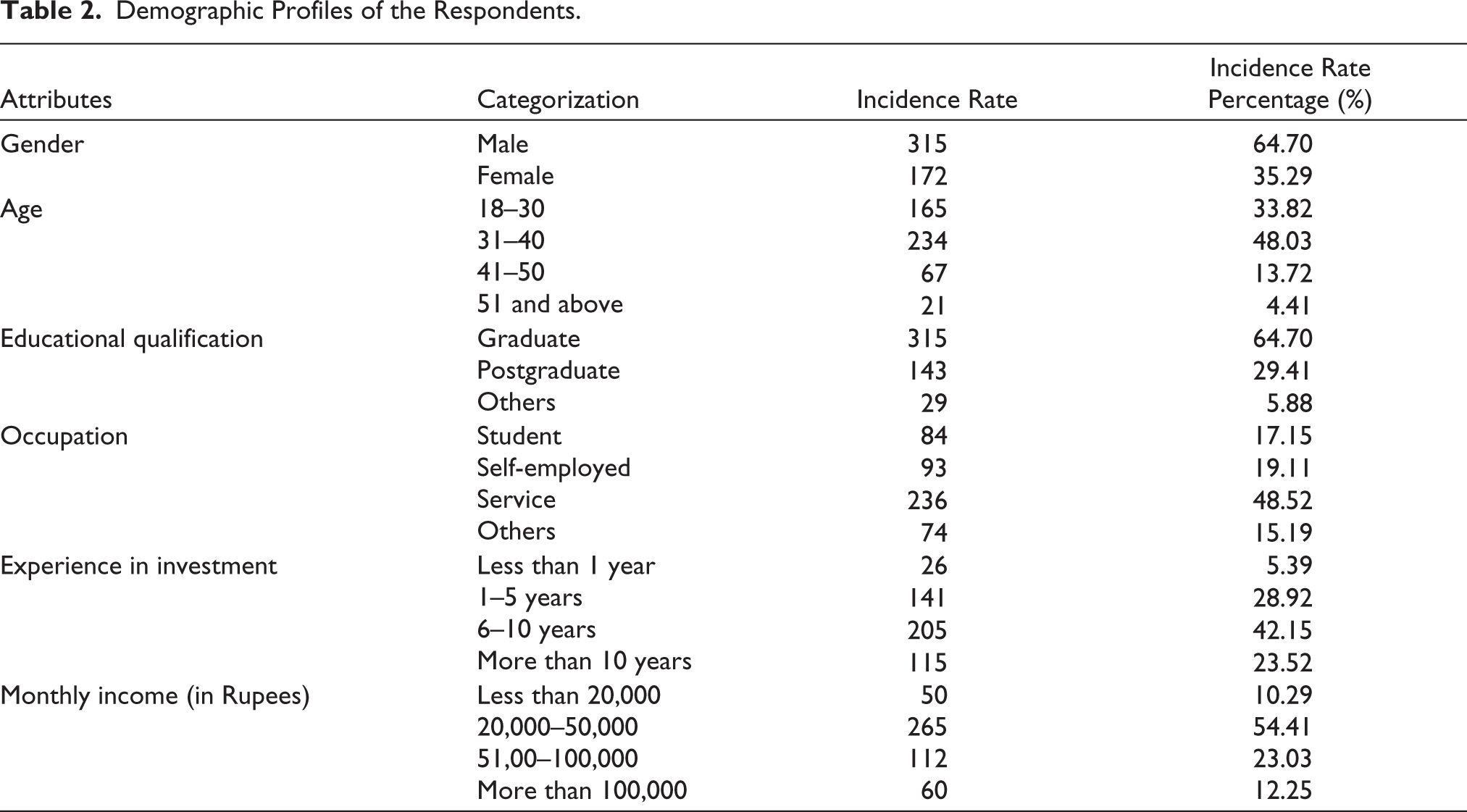

To make the data collection process more streamlined and systematic, the survey instrument was implemented using Google Forms. The questionnaire was distributed directly to the target population, consisting of acquaintances, colleagues and active stock market investors, face-to-face and by using e-mail, WhatsApp in professional groups and LinkedIn. Following Faul et al. (2009), the minimum sample size required was computed using the software ‘G*Power (v3.1.9.4)’. Three predictors and an expected effect size of 0.05 indicate that the minimum sample size needed to achieve a statistical power of 0.80 is 159. Accordingly, a total of 550 questionnaires were distributed with 506 completed responses; 19 data were excluded as outlier data; therefore, the final sample was 487 respondents. Table 2 shows the demographic profiles of these participants, which illustrates a diverse pool of respondents. The sample was mostly male (64.70%), aged 31–40 years. A majority of respondents were working in the services industry (48.52%) or were self-employed (19.11%) and held postgraduate qualifications (29.41%). It is noticeable that 23.52% (115 people) had over 10 years of investment experience, while 42.15% (205 people) reported 6–10 years of investment experience.

Demographic Profiles of the Respondents.

Results and Discussion

We have employed a two-staged analysis approach to execute the study. In the first stage, we utilized PLS-SEM with SmartPLS v4.0.8.7 software for structural and measurement analyses (Ringle et al., 2022). PLS-SEM offers the advantage of testing intricate models, including mediation and moderation effects, within a unified framework. Unlike covariance-based SEM, PLS-SEM does not impose any assumptions regarding data normality (Becker et al., 2018; Sarstedt et al., 2019) in a single model, making it more flexible. ‘PLS-SEM’ was deemed appropriate for our study due to its capacity to construct comprehensive models. Following Hair et al. (2019)’s directions, we first evaluated the measurement model and then analysed the structural model. Next, we utilized the artificial neural network (ANN) technique using the SPSS 21.0 software for complex predictive analysis.

Common Method Bias

The likelihood of the existence of common method bias (CMB) remains because of the complication of utilizing one instrument in the data collection of both dependent and independent variables using the same population of participants. To eliminate this possibility, we used two different techniques, namely the procedural technique, in which we randomized all the items of the instrument and conducted two statistical procedures to explore whether there is ‘CMB’ or not. At first, the ‘Harman one-factor’ test result indicated the maximum variance explained by all items to be 42.578%, which is below the critical value of 50%, thus practically eliminating any significant presence of ‘CMB’ (Fuller et al., 2016; Podsakoff et al., 2012). Subsequently, the multicollinearity test was conducted, and the findings confirmed that the latent constructs in the present study had VIF between 1.36 and 1.79, and they were less than 5.0, indicating that the study is not subject to CMB.

Measurement Model Analysis

The findings indicate that all of the constructs’ outer loadings were statistically significant and surpassed the predetermined 0.70 criterion. ‘Cronbach’s α’ and ‘composite reliability (CR)’ were assessed for validating the internal consistency. An adequate level of internal consistency was demonstrated with values above 0.07 for both measures. Furthermore, as per Hair et al. (2017, p. 165), all constructs exhibited average variance extracted (AVE) values significantly transcended the limit of 0.50, corroborating robust convergent validity in compliance with the standards, as indicated in Table 3

The discriminant validity in the study is confirmed by using the ‘heterotrait-monotrait (HTMT) correlation ratio’ in addition to Fornell-Larcker’s (1981) criterion, as shown in Tables 4 and 5, respectively. The HTMT values below 0.85 established the discriminant validity of each construct.

Measurement of Convergent Validity.

Heterotrait–Monotrait (HTMT) Ratio.

Fornell-Larcker Values.

Structural Model Analysis

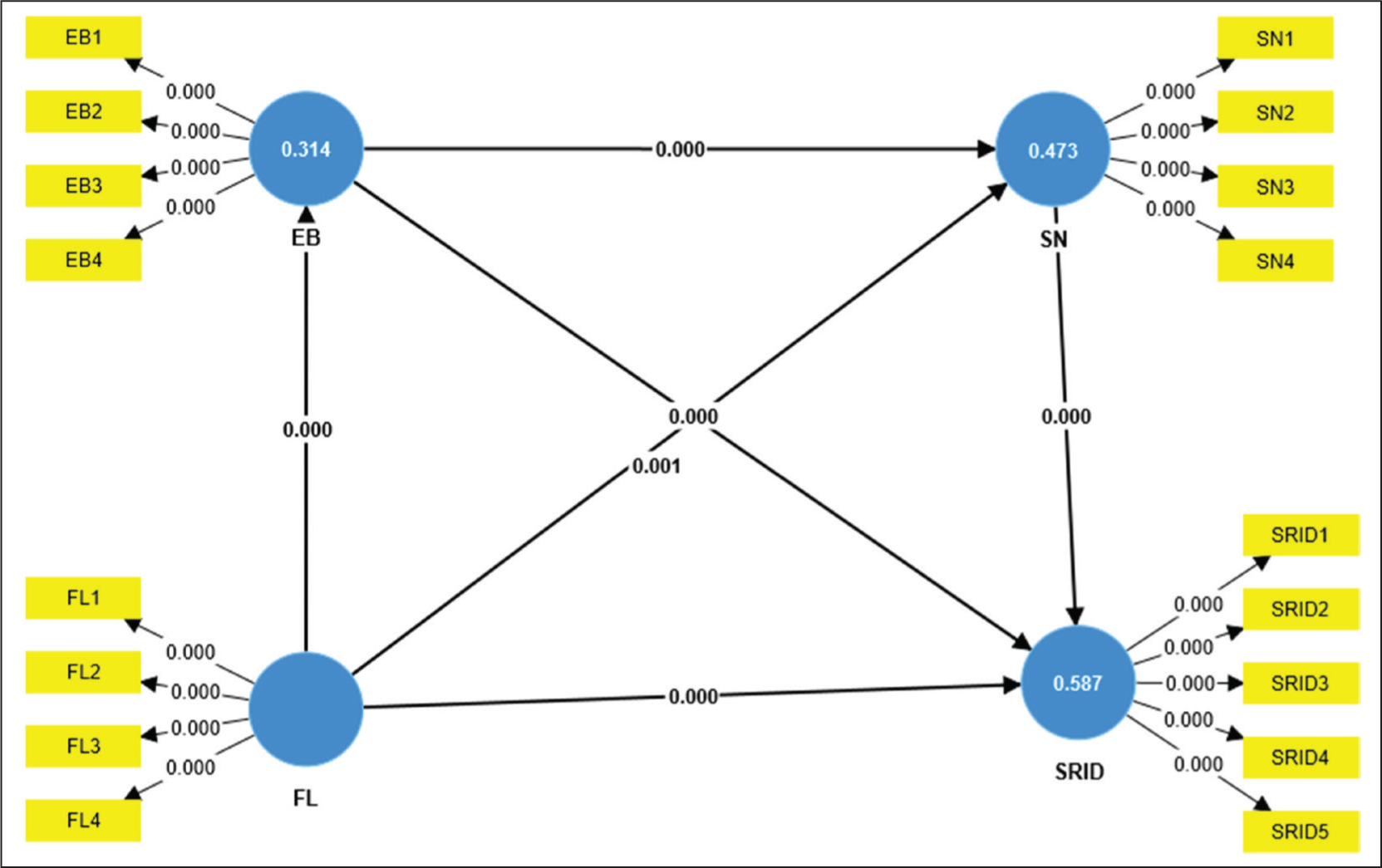

The standardized root mean square residual (SRMR) value was referred to as the model evaluation criterion to establish the appropriateness of the structural model. Ideally, one would like the estimated SRMR value more than the saturated SRMR value, since the latter value is a perfect fit and impossible to achieve in real life. In contrast, the estimated SRMR considers the model fit while taking into account the complexity of the model, which helps to analyse the model fit to how well the model reproduces correlations between variables. In the present study, a good fit was obtained with an estimated SRMR value of 0.075 (Henseler et al., 2016), which indicates that the hypothesized relationships in the model are statistically sound and that the model is an adequate representation of the underlying data structure (see Table 8).

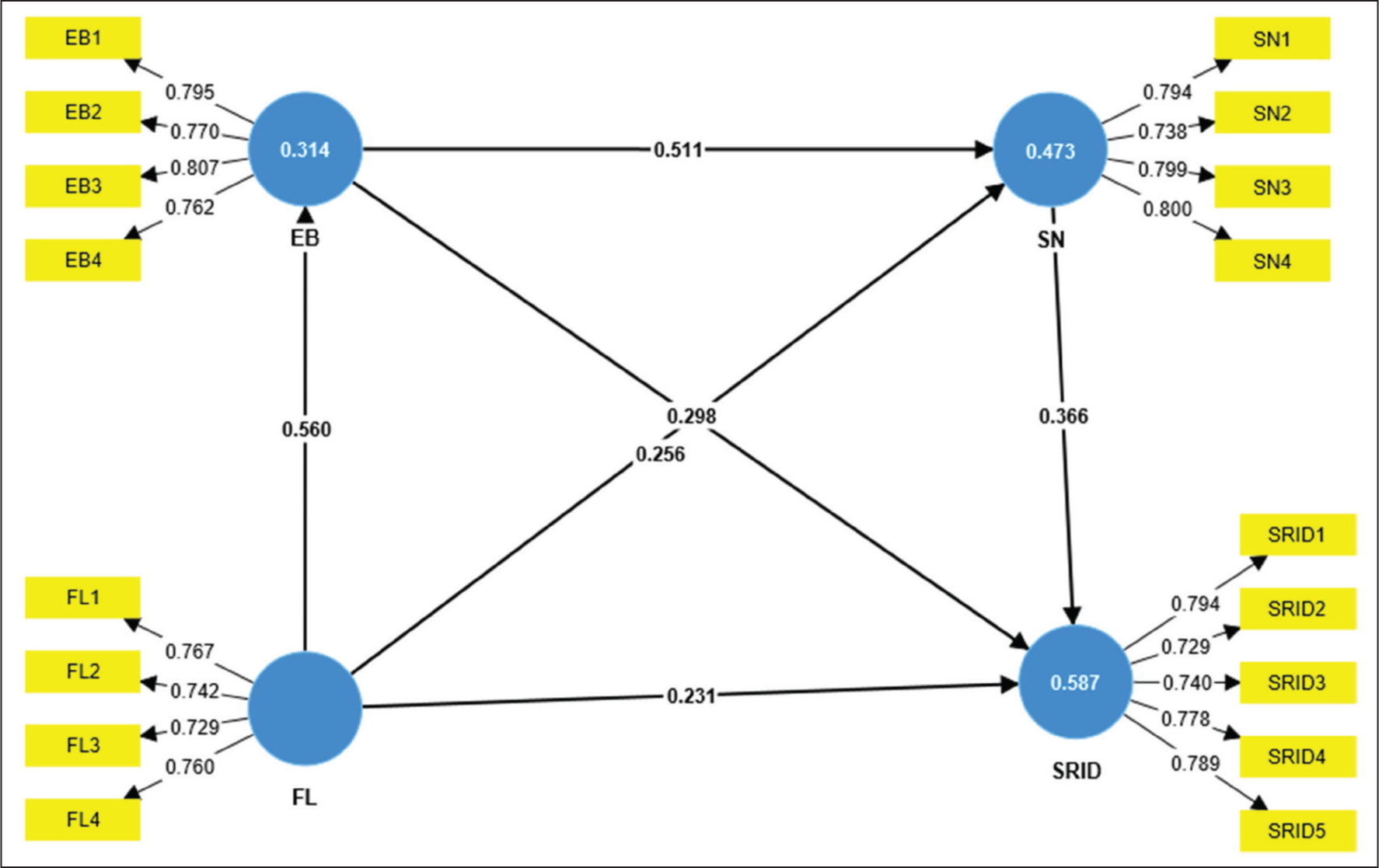

To assess the predictive value of the structural model, the following step was to use R2 and Q2 values, which are suggested by the study by Yao et al. (2023). Chin (1998) suggested different ranges for the R2 values that are used to classify the degree of fit: weak (0.02–0.13), moderate (0.14–0.26) and substantial (above 0.26). In the current investigation, all endogenous variables showed R2 values between 0.314 and 0.587, which indicates a significant level of fit in the model, as shown in Figure 2. This validates the model to explain a significant percentage of variance in the endogenous constructs. Likewise, all exogenous constructs showed the results of Q2 ranging from 0.278 to 0.344, which indicated the significant contribution of individual exogenous constructs in predicting the hypothesized relationships (Hair et al., 2017). Correspondingly, values above 0.00, 0.25 and 0.50 classify the model’s predictive accuracy as ‘small’, ‘medium’ and ‘large’, respectively.

Measurement Model.

Consequently, these results suggest that the variables included in our model are effective in explaining the variations which are observed in the endogenous constructs and are therefore valuable in providing insights into the factors, which can influence socially responsible investment decisions.

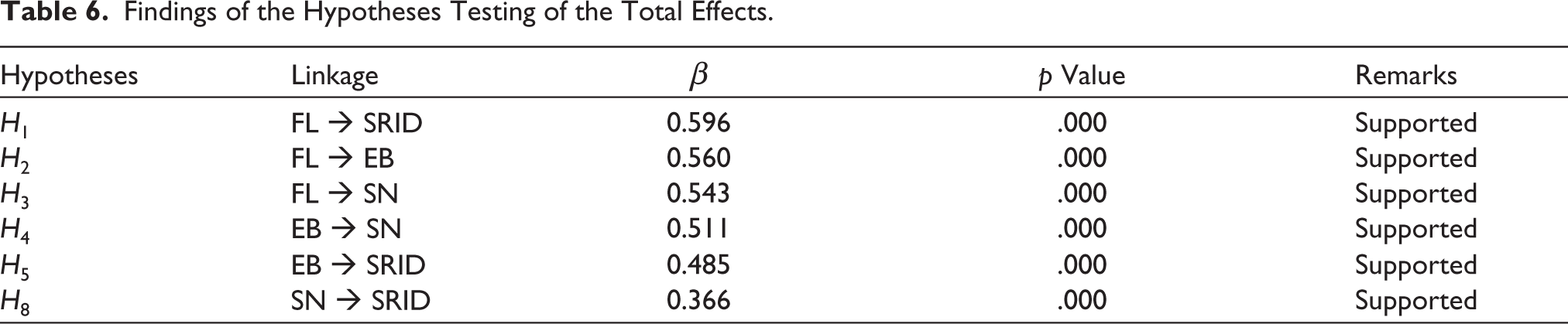

Furthermore, the bootstrapping technique was performed, using 5,000 subsamples in order to test the path coefficient values rigorously. The results related to the hypothesized correlations are described in Table 6 and Figure 3.

Findings of the Hypotheses Testing of the Total Effects.

Structural Model.

It was postulated in H1, H2 and H3, respectively, that FL has a significant impact on SRID, EB) and SN. We found that financial literacy has a significant influence on socially responsible investments engagement (β = 0.596, p < .001), supporting RQ1. It was postulated in H1, H2 and H3 that FL has a significant impact on SRID, EB and SN, respectively. We found that financial literacy significantly influences engagement in socially responsible investments (β = 0.596, p ≤ .000), supporting RQ1. This implies that individuals with better knowledge about sustainable finance have a higher propensity to engage in SRI. The findings indicate that FL significantly influences SRID, EB and SN (β = 0.596, 0.560 and 0.543, with p ≤ .000, respectively), leading to the acceptance of H1, H2 and H3. Similarly, in support of H4 and H5, it was found that EB has a substantial and positive impact on both SN and SRID with p ≤ .000 and β = 0.511 and β = 0.485, respectively. Consequently, H4 and H5 were verified and accepted. Further, SN proved to have a substantial effect on SRID with β = 0.366 and p ≤ .000. Therefore, H8 was also accepted.

The Mediating Effect of Environmental Beliefs and Social Norms

In this study, we introduced two crucial factors, namely EB and SN, as mediating variables. The stated hypotheses for this study were that EB and SN will mediate the relationship between FL and SRID. In order to examine the mediation of EB and SN, we utilized the bootstrapping resampling approach suggested by Preacher and Hayes (2008). We also tested for the significance of interaction terms to see how they impacted the dependent variable. As indicated in Table 7, we found that EB has a statistically significant mediation effect between FL and SN, as well as FL and SRID, which supports H6 and H7. Furthermore, we found a statistically significant mediating effect of EB and SN, suggesting that individual beliefs and social influences should be considered when analysing the interaction between FL and SRI decision-making. These findings indicate that environmental awareness and social norms play key roles in influencing people’s attitudes and behaviours towards sustainable investing.

Findings of the Hypotheses Testing of the Specific Indirect Effects.

Artificial Neural Network Diagram.

Similarly, SN turned out to have a substantial effect on the dynamics between EB and SRID (β = 0.187, p = .000) as well as FL and SRID (β = 0.094, p = .005). Our results provide an answer to RQ2 by demonstrating positive and significant correlations between EB and both SN and socially responsible investment (β = 0.511 and β = 0.485, p < .001). These results suggest that people strongly convinced about the environment are more likely to favour socially responsible investment options, suggesting the importance of environmental consciousness in SRI decision-making.

Regarding RQ3, our analysis shows that SN significantly impacts investment choices (β = 0.366, p = .000), especially for the group of people who are interested in environmentally conscious investments. As a result, H9 and H10 were accepted. Furthermore, the effect of environmental beliefs and social norms combined has a significant impact on the effect of FL on SRID (β = 0.105, p = .005). As such, the predicted hypothesis (H11) was also accepted.

These findings highlight the role of individual beliefs, social influences and financial literacy in shaping socially responsible investment decisions and underscore the importance of taking a comprehensive approach that takes into account both individual and social factors in promoting sustainable investment behaviour.

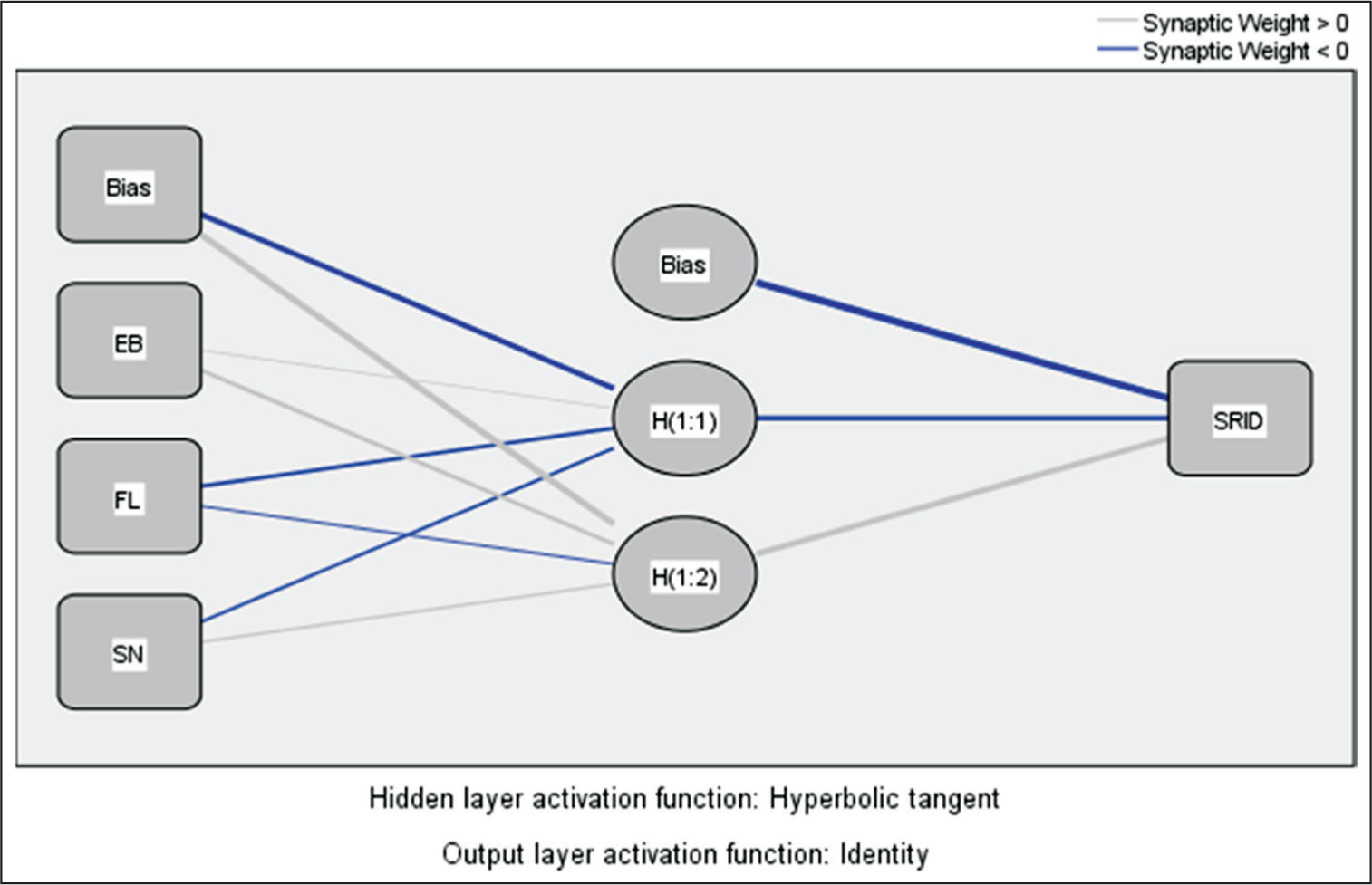

ANN Results

In this work, the second stage of analysis was applied based on the ANN approach to identify and investigate the possible non-linear correlations that may exist in the variables of interest. The ANN model was built on the exogenous variables discovered by SEM, which had a significant impact on the endogenous variable. As a result, all three independent variables, that is, FL, EB and SN, were taken into account, as illustrated in Figure 4. We performed the ANN analysis using the software package of the statistical programme (SPSS, version 21.0). ANN models have proven to show strength in terms of robustness, responsiveness and accuracy in contrast to traditional statistical approaches (Sim et al., 2014). Nevertheless, as emphasized by Chan and Chung (2012) and Leong et al. (2013), it is imperative to acknowledge that the ‘black box’ nature of ANN methodology makes it unsuitable for hypothesis testing and establishing causal relationships. Accordingly, Cabanillas et al. (2018) postulate to complement ‘linear’ and ‘compensatory’ SEM models with ‘non-linear’ and ‘non-compensatory’ ANN approaches for an overall analysis.

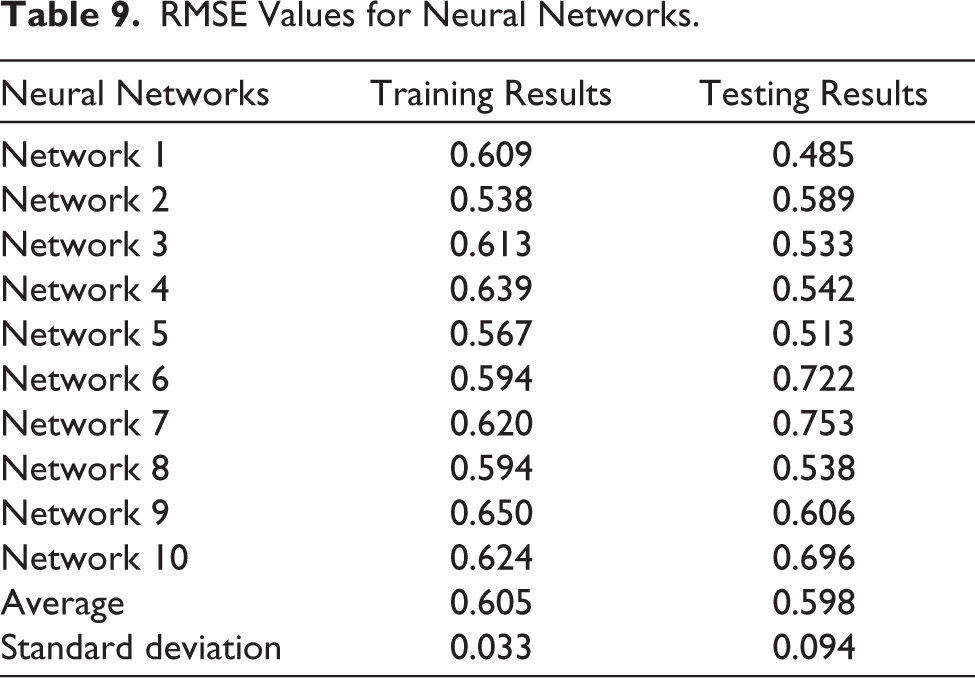

In line with the approach proposed by Lee et al. (2020), we used a deep ANN with one hidden layer per output neuron node. The sigmoid function was to initiate the output and hidden neurons. For the training as well as testing of data sets, our study resulted in ‘mean RMSE’ values of 0.605 and 0.598, respectively, as shown in Table 9.

SRMR Values.

RMSE Values for Neural Networks.

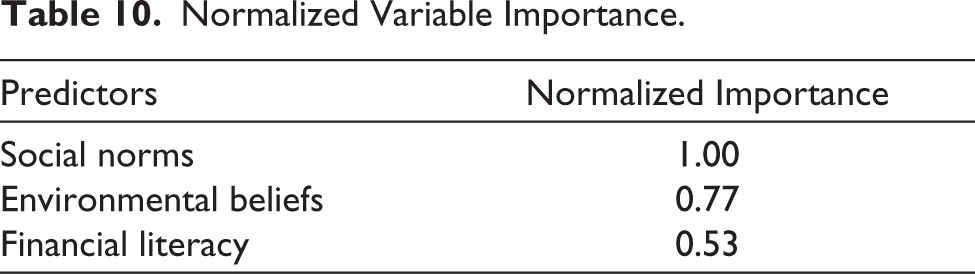

This result tells us about the good predictive power of the ANN model as mentioned in previous studies (Lau et al., 2021; Leong et al., 2020; Liebana-Cabanillas et al., 2017). Subsequently, as shown in Table 10, a ‘sensitivity analysis’ was conducted to group the exogenous factors with respect to their relative significance normalized to the internal construct. The most important predictor for SRID was social norms with normalized importance of 100%, then environmental beliefs with 77% and financial literacy with 53%. Thus, in line with RQ4, the ANN analysis gives insights into the possible non-linear relationships of the variables under study and contributes to a more comprehensive understanding of sustainable investing behaviour by pointing out SN to be the most significant predictor of SRID.

Normalized Variable Importance.

Conclusion

The study empirically validates the effectiveness of SCT in the context of SRI decision-making. The present study empirically tests the interrelationships among FL, EB, SN and SRID, thereby advancing SCT and contributing to the theoretical understanding of these relationships.

Discussion on Main Findings

These outcomes indicate the presence of a substantial relationship between FL and EB, FL and SN, and FL and SRID, as identified in extant studies conducted by Jain et al. (2022), Kumari and Harikrishnan (2021), Raut (2020), Hastings et al. (2013) and Cucinelli and Soana (2023). Moreover, the results clearly identify the direct effects of EB on SN, and the direct effects of SN on SRID, as identified by Stern (2002), Gifford and Nilsson (2014), Derwall et al. (2011), Gutsche et al. (2019) and Nguyen et al. (2020). Therefore, it is concluded that investors who are financially informed are able to evaluate their options for responsible investing and thus contribute to responsible investing through the process of norm diffusion. The mediating characteristics of EB and SN together represent the role that personal values and convictions play in guiding investment decision-making as they relate to long-term goals and are reflective of an increasing global trend where investors prioritize environmental and social concerns in addition to economic returns (Dmuchowski et al., 2023; Tripathi & Kaur, 2020). SN emerged as the primary psychological motivator in determining SRI decision-making in this study. These findings were supported by previous research identifying a positive relationship between normative influence and SRI decision-making (Cialdini & Goldstein, 2004; Gutsche et al., 2019; Hong & Kacperczyk, 2009). Overall, these findings provide clarity on the complex dynamics involved in SRI decision-making and serve as a basis for establishing a structured framework for a wide variety of stakeholders to guide the economy towards more sustainable and environmentally conscious financial practices.

Theoretical Implications

The empirical findings of the present study provide some important theoretical implications. First, the study goes beyond the usual applications of SCT by explicitly using SCT in a model of sustainable investment decision-making. This extension implies there may be greater applicability of SCT to the larger social science domain. Second, the research combines concepts drawn from the different disciplines of behavioural finance and sustainable investing, and it thus examines the psychological biases that govern investment decisions and the alignment of those decisions with ESG values. This integration forms part of a general knowledge of investment decisions related to SRI. Finally, the results challenge the classic economic assumption of individuals as rational ‘Homo Economicus’ by foregrounding the influence of cognitive biases, such as SN, on investment behaviour. Consequently, the study highlights the need for accounting for various types of behavioural and cognitive biases, such as attribution and anchoring, in the testing and extension of existing models of sustainable investment behaviour for retail investors.

Practical Implications

The study provides useful insights that can be aimed at to further sustainable goals and SRI in various stakeholder groups. For example, scholars and policymakers should focus on the design of targeted educational programmes and initiatives which are centred on ‘sustainable finance’, which includes concepts such as green financial instruments, long-term investment planning, climate risk management, ESG scoring and measuring sustainability. Moreover, policymakers should standardize and incentivize the integration of SRI in financial regulation and practice in order to encourage financial institutions to offer SRI options and disclose ESG information on a periodic basis. Additional support for sustainable investments could be done in the form of tax incentives and subsidies to research initiatives related to sustainable technologies and enterprises. Furthermore, the ascendancy of ethical behaviour as a driver of sustainable investment decisions implies that financial advisors and portfolio managers should incorporate ESG factors in their strategies in order to attract a broader investor base by providing investment products that are aligned with diverse ESG themes and risk profiles. The significant influence of SN in investment decision-making could also be capitalized upon by policymakers and organizations through creating campaigns that benefit from the power of peers, public figures and social networks to promote sustainable investing as an activity that is socially acceptable. Overall, these are some of the practical implications that call for a collaborative effort between the stakeholders, in recognition of the fact that sustainable investments can have positive implications in the long run while fostering the move away from short-term profit-seeking behaviours and adopt investment strategies that are consistent with the ultimate goal of sustainable development.

Limitations of the Study

Although the study provides valuable information, it has its limitations. First, although the research is based on a wide range of data with individual investors across various socio-economic backgrounds, the sample may not be entirely representative of the broader population of investors. Additionally, the use of non-probabilistic sampling techniques may affect the generalizability of the findings to the wider population. Future research could involve the use of stochastic sampling methods to obtain more representative data from the target population. Second, in spite of the thoroughness of the approach, the theoretical scope of the study is limited to such a selective choice of variables, as to leave some chances for incorporating other potentially influencing factors while changing the investment decisions. Unmeasured variables, including risk perceptions, past investment behaviour and personal values, may be confounding variables; they can be the cause of the relationships noted in the present study. Lastly, the conclusions of the study are based on data obtained up to a point in time. Ongoing developments in sustainable investment practices, FL initiatives and SN may change investment behaviours in the future. Future researchers should further explore ways of measuring the true effect of SRI on environmental and social outcomes to determine whether investments described as ‘socially responsible’ are really helping to achieve sustainability objectives or whether a standardized measurement of impact is needed.

Supplementary Material

Supplementary material for this article is available online.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflict of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Generative AI in Scientific Writing

The authors analysed the results using SMART PLS-4 software. They meticulously reviewed the material, made necessary edits and assumed full accountability for the published content. AI assistance was used for language enhancement purposes only.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.