Abstract

This article undertakes a rigorous reassessment of the framework governing resource transfers from the union to subnational governments in India, interrogating its constitutional foundations, distributional adequacy and implications for development finance, with specific reference to the recommendations of the Sixteenth Finance Commission. The central contention is that the progressive hollowing out of the divisible pool, driven primarily by the union’s persistent recourse to non-shareable cesses and surcharges, has eroded the revenue entitlements of state governments that are constitutionally guaranteed. A methodological argument is advanced that prevailing assessments of transfer size, which normalise total transfers relative to gross tax revenue (GTR), systematically misrepresent the union’s actual resource availability; since FC grants as well as non-FC grants alike draw upon the Consolidated Fund of India, they are more appropriately measured as shares of gross revenue receipts. The empirical analysis reveals that the systematic drift of transfer composition towards conditionality-laden non-FC flows has progressively curtailed subnational budgetary discretion. This article further shows that the existing vertical devolution architecture is structurally inadequate for bridging the fiscal gap between the union and states and argues that the FC-16’s institutional modifications, including a conditional bargain on cesses and the termination of revenue-deficit grants, do not resolve the underlying structural deficit. These findings raise substantive questions about whether cooperative federalism can be sustained under the prevailing transfer architecture.

Keywords

Introduction

India’s fiscal federal framework has never been static. Over the seven-plus decades since the Constitution came into force, the financial relationship between the union and state governments has been continuously recast, driven by changing developmental imperatives, evolving political bargains and the successive institutional interventions of finance commissions (FCs). The structural foundation inherited from the Government of India Act 1935 and the Niemeyer Award 1936 concentrated revenue authority at the centre while assigning the larger share of public expenditure responsibility to the states, particularly in domains such as primary health, school education, agriculture, rural infrastructure and civil order. This deliberate asymmetry between revenue and expenditure authority at different governmental tiers is what fiscal federalism literature identifies as vertical fiscal imbalance (VFI), the systematic divergence between the tier that mobilises revenue and the tier that discharges service delivery obligations (Bird & Tarasov, 2004; Boadway & Shah, 2009; Oates, 1972).

The Constitution’s response to VFI operates through a layered set of transfer instruments. Under Article 270, a constitutionally mandated share of union tax proceeds is devolved to states through what is termed the divisible pool. Article 275(1) empowers the FC to recommend grants in aid to states, while Article 282 provides a broad enabling authority for discretionary union transfers, most significantly the centrally sponsored schemes (CSS). The FC, periodically constituted under Article 280, occupies the central position in this architecture by calibrating both the divisible pool share and the grant allocations for each five-year award period. The Sixteenth FC (FC-16), whose award spans 2026–2027 to 2030–2031, has elected to retain the states’ divisible pool share at 41%, the same level recommended by its predecessor. This decision was taken despite near-unanimous state-level advocacy for an increase to at least 50% and amidst extensive documentation of how cess proliferation has progressively reduced the divisible pool relative to gross tax revenue (GTR). Against this background, this article assesses whether the vertical devolution and grants-in-aid framework, as currently configured, is capable of meeting the fiscal needs of India’s subnational governments.

India’s VFI is among the most pronounced in the world, exceeding analogous imbalances observed in Brazil, Canada and Australia (Reserve Bank of India, 2023; Sharma, 2021). The imbalance has been further deepened by the steady accumulation of cesses and surcharges in the union’s revenue portfolio; since these levies fall outside the constitutional definition of the divisible pool, the states’ share of GTR has contracted even where their nominal divisible pool percentage has remained constant. Compounding the vertical dimension, substantial interstate fiscal disparities persist, rooted in differentials of economic structure, demographic profile and inherent tax capacity (Bird & Tarasov, 2004; Kawadia, 2026; Rao & Singh, 2006). These horizontal inequities render the intergovernmental transfer design simultaneously a question of vertical adequacy and horizontal equity.

Normative frameworks in classical fiscal federalism provide a systematic basis for evaluating these institutional arrangements. In Oates’s (1972, 2001) formulation, the efficient allocation of fiscal authority across governmental tiers must account for the scale of externalities, the realisation of economies in tax collection and the degree of heterogeneity in local public good preferences. Building on this framework, Boadway and Shah (2009) construct a comprehensive normative model that links equity and efficiency objectives to the design of intergovernmental transfers, providing a benchmark against which India’s transfer practices may be evaluated. Their taxonomy distinguishing unconditional block grants, which leave expenditure priorities to subnational discretion, from conditional matching grants, which redirect subnational spending towards federally designated objectives, is directly relevant to the Indian experience of expanding CSS conditionality.

Trends in India’s intergovernmental fiscal relations reflect a pronounced centralising tendency. State governments have repeatedly documented the erosion of their programmatic autonomy as the CSS footprint has expanded; the secular decline in unconditional transfers relative to growing conditional grant flows has systematically narrowed states’ capacity to align expenditure patterns with locally determined priorities (Chakraborty & Chakraborty, 2018; Rao, 2005). The implementation of the Goods and Services Tax (GST) has further reduced states’ own-source revenue base, deepening their dependence on union transfers. Collectively, these developments have revived debate over whether the constitutionally envisaged model of cooperative federalism is being systematically undermined by the operation of the transfer system (Kelkar, 2019).

The existing literature contains several important lacunae that this study addresses. A significant share of empirical work on intergovernmental transfers predates the GST transition and therefore cannot assess how the shift to a destination-based consumption tax has reconfigured the union–state fiscal balance (Rao & Singh, 2006; Sharma, 2021). The precise quantitative relationship between divisible pool contraction and vertical imbalance deepening has not been comprehensively examined. As the vertical gap widens, the FC’s capacity to address horizontal disparities is correspondingly constrained; an analytical framework that treats vertical and horizontal dimensions simultaneously is therefore needed (Boadway & Tremblay, 2006; Oates, 2001; Rao, 2002). The effectiveness of conditional grants in meeting their stated objectives remains empirically underdeveloped; notwithstanding successive FCs’ experimentation with performance-linked, sector-specific and outcome-oriented transfers, rigorous evaluation of their effects on expenditure autonomy or subnational development outcomes is scarce (Chakraborty & Chakraborty, 2018; Rao, 2005). The proliferation of non-FC grants outside the formal constitutional transfer architecture has generated further opacity in union–state fiscal relations.

Against this background, this article makes three principal contributions. First, it analyses the compression of the divisible pool in the context of the FC-16’s 41% retention decision and the political economy that shaped it. Second, it advances a methodological position that since both FC and non-FC grants are charged upon or voted from the Consolidated Fund of India, assessing them relative to GTR alone misrepresents the union’s resource availability, and gross revenue receipts constitute the more defensible denominator. Third, it offers a critical evaluation of the quantum and composition of total central transfers, with particular attention to the tension between tied and untied grant instruments and their implications for state fiscal autonomy. The remainder of this article is structured as follows. The second section surveys the relevant literature; the third section delineates the constitutional framework for central transfers; the fourth section presents the descriptive and empirical analysis; and the fifth section synthesises the findings and draws policy conclusions.

Related Literature

The welfare-theoretic case for intergovernmental fiscal transfers was classically elaborated in Musgrave’s (1959) tripartite functional taxonomy of government, which partitions public finance responsibilities into allocative, stabilisation and redistributive roles. In this framework, allocative functions that cater to localised preferences are most efficiently discharged at the subnational level, while macroeconomic stabilisation and interpersonal redistribution appropriately remain central government responsibilities, given the factor mobility effects that would undermine decentralised stabilisation and the spillovers that complicate subnational redistribution (Oates, 1972). The distributional consequence of this assignment is structural VFI: Central governments, equipped with administratively efficient broad-based tax instruments and capable of capturing inter-jurisdictional spillovers, accumulate revenue authority disproportionate to their expenditure responsibilities, while subnational governments confront expenditure mandates that exceed their revenue mobilisation capacity. Oates (1999) characterises this as the defining tension in fiscal federalism, arguing that expenditure decentralisation unaccompanied by commensurate revenue devolution renders vertical transfers not merely helpful but structurally indispensable.

Boadway and Shah (2009) systematise the normative objectives for transfer system design into four analytically distinct goals: eliminating the vertical gap between central revenue surplus and subnational expenditure need; achieving horizontal equalisation among jurisdictions with heterogeneous fiscal capacity; correcting for inter-jurisdictional spillovers from subnational public expenditures; and guaranteeing minimum service standards in programmes of national priority. Their analytical distinction between unconditional transfers, which protect subnational allocative freedom and are instrumentally better suited to closing vertical imbalances, and conditional matching grants, which may effectively internalise externalities but introduce principal–agent inefficiencies and reduce fiscal autonomy, is particularly relevant to the Indian CSS debate (see also Bird & Smart, 2002; Martinez-Vazquez & Searle, 2007).

The empirical literature on vertical fiscal transfers raises substantive concerns about their incentive effects. Sharma (2012) cautions that transfers structured without regard to fiscal effort may blunt subnational own-revenue mobilisation. Eyraud and Lusinyan (2013) find a robust positive association between the magnitude of VFI and consolidated fiscal deficits, suggesting that transfer-dependent subnational governments tend to exhibit weaker fiscal discipline. Within the political economy tradition, Rodden (2006) identifies the ‘soft budget constraint’ problem: subnational governments expecting central bailouts tend to incur expenditure commitments beyond their resource base, a dynamic with clear resonance in India’s persistent subnational debt pressures. The second-generation theory of fiscal federalism, synthesised by Oates (2005) and Weingast (2009), reorients the analytical lens from the quantity to the architecture of transfers, arguing that incentive-compatible design that preserves subnational fiscal effort is more consequential for subnational performance than the volume of transfers per se.

India-specific scholarship has progressively sharpened the analytical framing. Rao and Singh (2006) demonstrate that in the Indian context, it is the composition rather than the aggregate volume of transfers that most accurately captures the real distribution of fiscal autonomy between the union and states. Rangarajan and Srivastava (2008) trace the historical trajectory of FC recommendations, documenting that while successive commissions progressively raised states’ nominal divisible pool share, the post-transfer effective resource distribution remained relatively stable across periods, a finding that foreshadows the present study’s central argument. The qualitative shift in transfer architecture was sharply accelerated by the FC-14’s 42% devolution recommendation, to which the union responded by cutting its CSS co-financing contribution and simultaneously deepening its reliance on cesses and surcharges, functionally reclaiming much of the fiscal space nominally transferred (Chakraborty, 2016). Chakraborty and Gupta (2025) quantify this reclamation, estimating that the divisible pool contracted from roughly 90% of GTR in 2011–2012 to approximately 75.7% by 2022–2023 and that CSS co-financing obligations effectively absorb around four percentage points of the nominal devolution entitlement, making the true untied transfer considerably smaller than headline figures suggest.

The GST transition introduced a qualitatively new dimension to state fiscal stress. By requiring states to surrender both rate-setting and base-determination authority to the GST Council, the reform eliminated the principal discretionary tax instruments through which states had historically managed revenue shortfalls and pursued locally determined fiscal objectives. Joseph and Kumary (2023) characterise the resulting arrangement as exhibiting coercive federalism tendencies, with states rendered chronically dependent on GST compensation flows and vulnerable to revenue volatility without the autonomous tax adjustment mechanisms needed to respond to fiscal shocks. Srivastava (2025) argues that this context demands that fiscal transfers be embedded within an integrated fiscal sustainability framework, rather than treated as a subordinate residual in fiscal consolidation arithmetic. Studies in international economics and finance further reinforce the view that revenue authority and expenditure responsibility must be aligned at each governmental tier for federal systems to function equitably (Bernardi et al., 2006).

The fiscal consequences of cess proliferation have attracted growing scholarly attention. Ramakumar (2024) and the Reserve Bank of India (2023) comprehensively document the expansion of cesses and surcharges as a share of GTR since 2014–2015, tracing both their absolute magnitude and their compositional displacement of divisible pool revenues. Motkuri and Revathi (2023) highlight the perverse fiscal logic embedded in this pattern: A substantial portion of union education expenditure is now financed from an education cess, simultaneously reducing states’ divisible pool revenue and leaving them without adequate resources to discharge their own constitutional education obligations. Mohan and Ramakumar (2024) respond to this evidence with a concrete recommendation that the FC-16 increase the devolution share to approximately 45.5% of net proceeds. More recently, Kawadia (2026) provides an early quantitative treatment of fiscal devolution and regional equity in India, establishing that devolution design choices have distributional consequences across states that cannot be captured by examining aggregate transfer volumes. Public finance scholarship on the Indian federal system, collected in Srivastava and Shanmugam (2023) and Rao (2017), increasingly converges on the position that the existing transfer architecture has reached its structural limits in addressing VFI under conditions of cess-driven divisible pool compression.

The preceding review identifies a recurrent theme: While individual channels of fiscal stress—divisible pool erosion, declining FC grant share and CSS conditionality—have been examined in isolation, a joint treatment that connects these channels to each other and to the design of the FC-16’s institutional responses has been lacking. This article addresses that gap. It also introduces a specific methodological contribution to the measurement of transfer adequacy: Since both FC and non-FC grants draw on the Consolidated Fund of India rather than on union tax revenue specifically, benchmarking them against GTR misrepresents the union’s true resource position, and gross revenue receipts provide the more analytically defensible denominator. The empirical evaluation of the FC-16’s grand bargain on cesses, while discussed in policy circles, has not been formally assessed for its implications for VFI closure, revenue buoyancy or constitutional feasibility (Varughese et al., 2025).

Constitutional Framework of Central Transfers

Resource sharing between the union and states in India is governed by a constitutionally specified set of instruments that differ both in their legal character and in the degree of subnational fiscal discretion they preserve. The primary and most significant channel is Article 270, which mandates the sharing of the net proceeds of specified union taxes between the two tiers of government, with the FC determining both the divisible pool share and the horizontal allocation formula among states. At the time of the Constitution’s adoption, Article 270 encompassed only income tax. The 80th Constitutional Amendment of 2000, giving effect to the FC-10’s Alternative Scheme of Devolution, expanded the mandatory sharing obligation to cover virtually all central taxes from the FC-11 period onwards. Several categories of revenue are statutorily excluded from the divisible pool: revenues under Articles 268 and 269; surcharges levied under Article 271; purpose-specific cesses; and, following the Hundred and First Constitutional Amendment of 2016 that introduced GST, the integrated GST component under Article 269A (Finance Commission of India, 2025). The constitutional exclusion of cesses and surcharges was originally designed as a safeguard enabling emergency revenue mobilisation unconstrained by mandatory sharing, with the FC-16 report noting that the framers intended cesses as exceptional instruments for contingencies such as war, famine, or pandemic (Finance Commission of India, 2025, para. 7.49). Their subsequent transformation into permanent and institutionally entrenched revenue instruments, with the Health and Education Cess, the Road and Infrastructure Cess and the Agriculture Infrastructure and Development Cess collectively generating revenues of a magnitude comparable to dedicated tax heads, represents a fundamental deviation from this original design intent, with consequences for the divisible pool that the constitutional framers did not anticipate (Ramakumar, 2024).

The second constitutional channel is Article 275(1), which authorises the FC grants in aid to states. A legally consequential feature of these grants is that they are charged upon the Consolidated Fund of India, meaning they are non-votable and automatically appropriated, providing states with a measure of constitutional fiscal predictability that supports medium-term planning. Historically, FC grants have addressed four distinct fiscal needs: revenue-deficit support for states whose post-devolution budgets remain in deficit; grants to local bodies for service delivery; disaster management funds; and purpose-specific grants for tribal welfare and educational improvement. Yet despite their constitutional certainty, the share of FC grants in total transfers has not grown commensurately with states’ expenditure needs. From the FC-11 and FC-12 average of 5.3% of GTR, this share declined to 4.6% during FC-13, recovered partially to 5.4% in FC-14, and stood at 5.5% during FC-15. The FC-16 has introduced a significant further retrenchment by abolishing revenue-deficit grants and eliminating sector- specific transfers, substantially narrowing the unconditional grant base (Finance Commission of India, 2025).

The third channel is the broadest in scope and the most consequential for subnational autonomy. Article 282 permits the union or any state to make grants for any public purpose, without the constraint that the purpose fall within the legislative competence of the relevant legislature. This provision constitutes the constitutional foundation for CSS, through which the union channels resources to states for programme delivery across a wide range of concurrent and even state-list subjects, spanning education, health, agriculture, rural development and urban infrastructure. Unlike Article 275 grants, CSS transfers are voted expenditures subject to annual parliamentary appropriation; they are therefore inherently subject to year-to-year variation and carry extensive scheme-specific conditionalities governing beneficiary criteria, implementation modalities, procurement norms, fund release protocols and expenditure reporting obligations. The institutional asymmetry that flows from this design is analytically central: Article 270 devolution is both unconditional in end-use and mandatory in appropriation; Article 275 grants are formula-determined and constitutionally certain; and Article 282 grants are discretionary, conditional and revocable, making them susceptible to unilateral revision and strategic deployment by the union executive (Boadway & Shah, 2009; Martinez-Vazquez & Searle, 2007). Consequently, the secular migration of transfer composition away from Articles 270 and 275 towards Article 282 constitutes a structural erosion of subnational fiscal autonomy that aggregate transfer figures cannot capture.

Descriptive Analysis

The Contraction of the Divisible Pool

The most structurally significant trend in India’s intergovernmental transfer architecture over the past 15 years has been the progressive contraction of the divisible pool as a proportion of GTR. This contraction is a direct consequence of the union’s deepening fiscal dependence on cesses and surcharges: Since these levies are constitutionally outside the divisible pool, the entire revenue they generate accrues to the union without any sharing obligation towards states. The effect is a systematic reduction in the revenue base from which states receive their constitutionally mandated entitlements, independent of any change in the nominal devolution percentage.

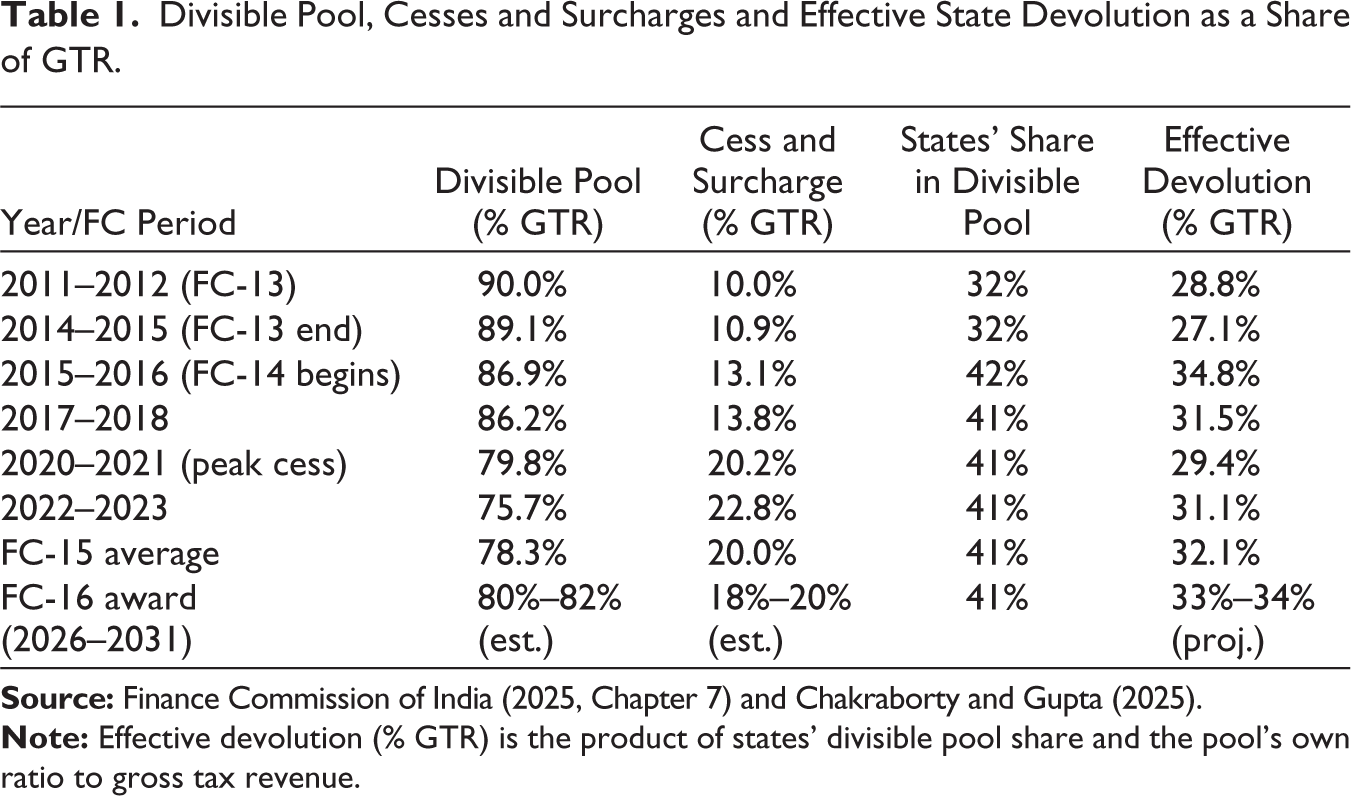

Table 1 documents this erosion empirically across successive FC periods. The divisible pool, which represented approximately 90% of GTR in 2011–2012, had declined to roughly 75.7% by 2022–2023. The FC-15 average stood at 78.3%, while cess and surcharge revenues, which accounted for approximately 5.16% of GTR in 2009–2010, had escalated to 14.07% by 2024–2025—a near-threefold increase in 15 years. The implications for effective devolution are arithmetically straightforward but politically underappreciated: Even when an FC nominally increases the states’ divisible pool share, as occurred when the devolution rate rose from 32% under FC-13 to 42% under FC-14, the effective transfer as a share of GTR need not improve proportionately if the pool itself is shrinking. Table 1 makes this arithmetic transparent (Chakraborty & Gupta, 2025; Finance Commission of India, 2025).

Divisible Pool, Cesses and Surcharges and Effective State Devolution as a Share of GTR.

The Changing Composition of Central Transfers

Beyond tax devolution, the union channels resources to states through a diverse array of grant instruments. Non-FC transfers encompass national disaster response and mitigation fund assistance, support for externally aided projects, special- purpose and capital grants and the large-volume CSS and central sector scheme transfers. CSS functions primarily as matching grants that require state co-financing, while central sector schemes are non-matching, entirely union-financed instruments (Government of India, 2024; Rao & Singh, 2006). The decisive institutional distinction, however, is not organisational but legal: FC grants under Article 275 are unconditional and constitutionally certain, allowing states the discretion to deploy resources in accordance with locally identified fiscal priorities; non-FC grants under Article 282 are tied to scheme-specific parameters and therefore systematically limit subnational programmatic autonomy (Darshini & Gayithri, 2024). As Chakraborty and Bhadra (2025) emphasise, it is this legal asymmetry in grant character, rather than the aggregate transfer magnitude, that is the operative determinant of subnational fiscal autonomy.

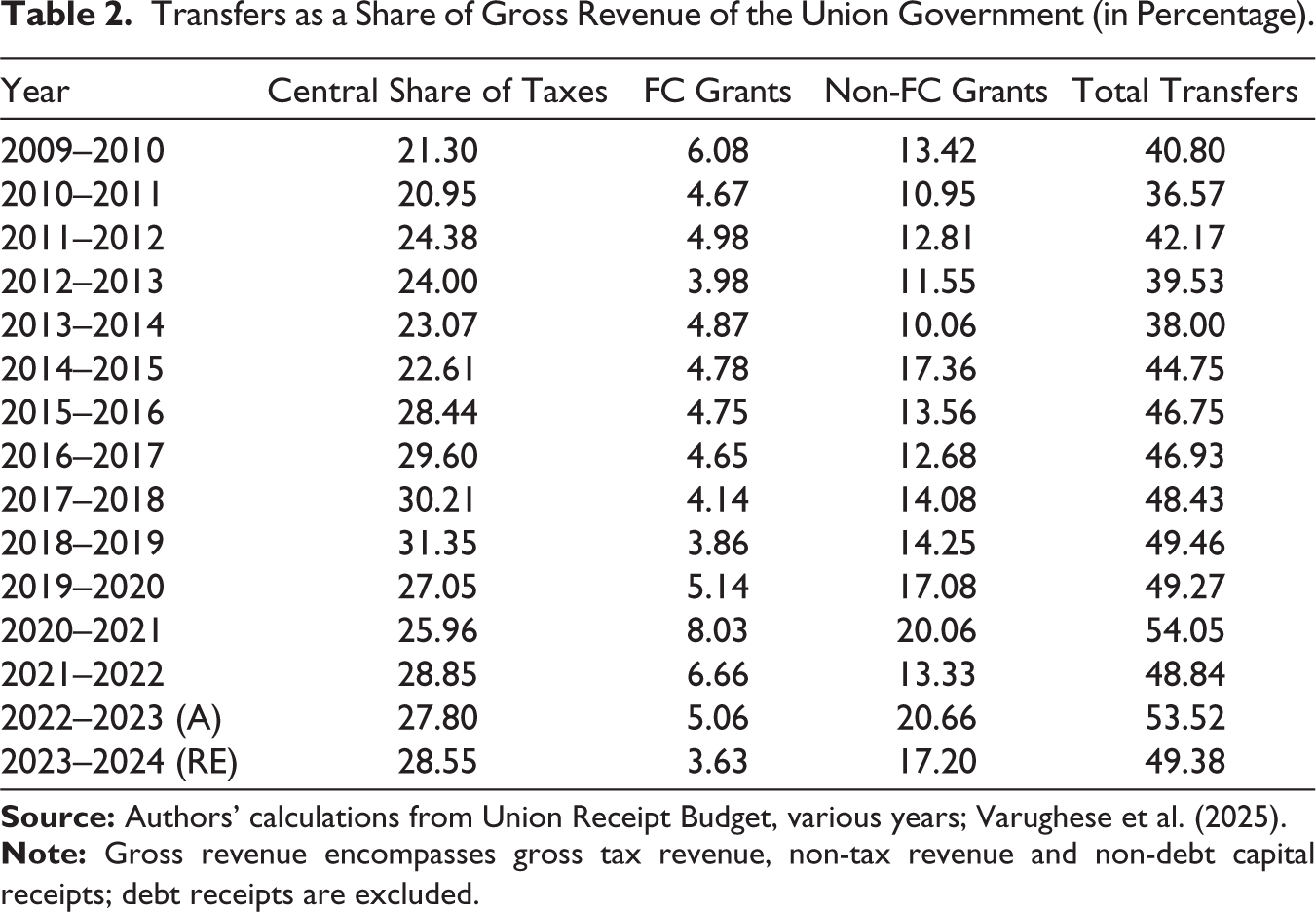

A methodological innovation offered in this article distinguishes it from existing assessments of transfer adequacy. The standard practice in both academic and official assessments of intergovernmental transfers, including the FC-16’s own analysis, is to normalise total transfers relative to GTR. While this is an appropriate denominator for tax devolution since the divisible pool is itself defined as a function of GTR, it is not the appropriate base for assessing grant transfers. Both Article 275 grants and Article 282 grants are charged upon or voted from the Consolidated Fund of India, which draws on a resource pool considerably broader than union tax revenue alone. The union’s consolidated receipts encompass non-tax revenues from dividends and profit transfers from public sector undertakings, surplus remittances from the Reserve Bank of India, interest on government loans, regulatory fees and charges and non-debt capital receipts from asset monetisation, disinvestment and spectrum assignment. None of these revenue streams carries a constitutional sharing obligation. Using GTR as the denominator for evaluating grant transfers, therefore, employs a reference base that progressively understates the union’s actual fiscal capacity. Gross revenue receipts, the sum of GTR, non-tax revenue, and non-debt capital receipts, provide a more analytically defensible denominator, enabling a more accurate characterisation of the union’s effective transfer burden (Rangarajan & Srivastava, 2008; Srivastava, 2025).

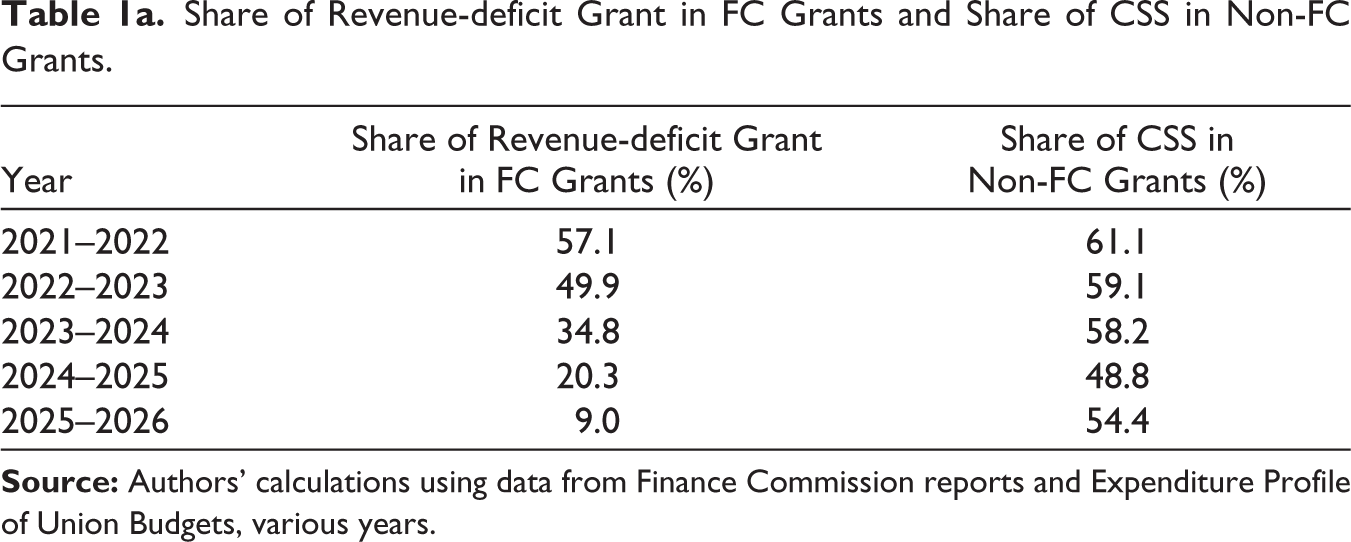

Table 2 presents total central transfers disaggregated by stream as shares of gross revenue receipts for the period 2009–2010 to 2023–2024. Several analytically important patterns emerge. Tax devolution as a share of gross revenue has fluctuated between 21% and 31%, reflecting both divisible pool variation and year-to-year non-tax revenue volatility. FC grants as a proportion of gross revenue contracted from 6.08% in 2009–2010 to 3.63% by 2023–2024, an absolute decline pointing to the progressive inadequacy of the constitutional grant base. Non-FC grants, by contrast, expanded from 13.42% to 17.20% over the same period, reflecting the growing weight of CSS in the transfer mix, with direct implications for subnational discretion. Appendix Table 1a documents that CSS accounted for approximately 57% of non-FC grants during 2021–2022 to 2024–2025, while revenue-deficit grants comprised 34% of FC grants during the FC-15 period. The escalating share of conditional non-FC flows in total transfers represents the most concrete institutional expression of the centralising tendency within India’s fiscal federal system (Varughese et al., 2025).

Transfers as a Share of Gross Revenue of the Union Government (in Percentage).

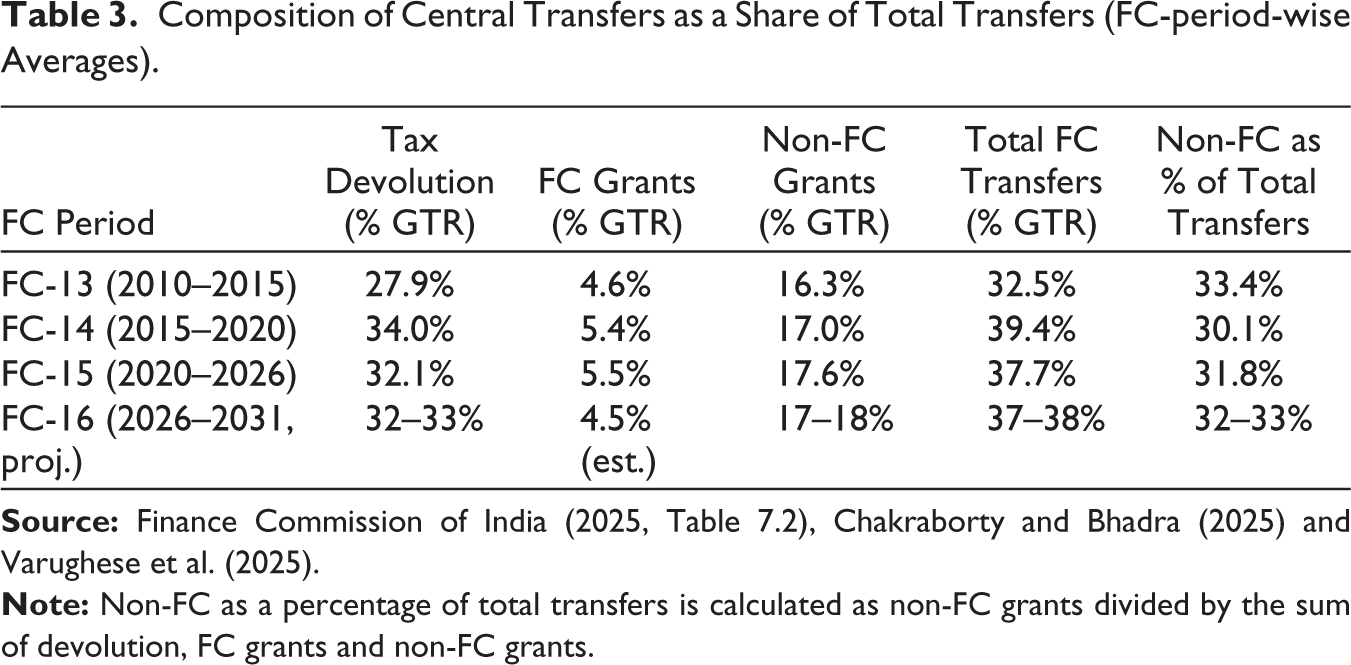

The FC-16’s report presents the aggregate transfer figure of over 49% of gross revenue receipts, demonstrating that further increases in vertical devolution are unwarranted (Sixteenth Finance Commission, 2026). This claim deserves careful scrutiny. The aggregate figure conflates transfer streams that are fundamentally dissimilar in their legal character, conditionality and implications for subnational fiscal autonomy. Table 3 decomposes the aggregate to present FC transfers—comprising tax devolution and FC grants—separately from non-FC CSS transfers across successive commission periods.

Composition of Central Transfers as a Share of Total Transfers (FC-period-wise Averages).

For the FC-15 period, gross revenue receipts averaged approximately ₹30–33 lakh crore annually. Total transfers, encompassing tax devolution of approximately ₹9.5 lakh crore, FC grants of ₹1.7 lakh crore and CSS flows of approximately ₹5 lakh crore, yield an aggregate of ₹16–17 lakh crore, producing the 49% figure. The crucial analytical point is that the three components are not equivalent in fiscal quality. Article 270 devolution is mandatory and unrestricted in end use. Article 275 FC grants are formula-determined and constitutionally appropriated. Article 282 CSS transfers are voted, conditional, co-financing-intensive and subject to unilateral union revision. Treating these streams as equivalent misrepresents the effective degree of fiscal autonomy available to states. The appropriate focus is on the share of unconditional, discretionary resources, not the headline total (Boadway & Shah, 2009; Rao & Singh, 2006; Varughese et al., 2025).

Table 3 reveals a troubling structural regularity: while FC transfers, encompassing devolution and FC grants, have oscillated between 32 and 39% of GTR, the predominantly conditionality-laden non-FC component has consistently constituted 30–33% of total transfer flows across commission periods. Given that Article 282 grants are voted expenditures that impose detailed programmatic requirements, their sustained weight means that a substantial portion of the headline 49% cited by the FC-16 represents resources over which recipient states exercise minimal meaningful allocative discretion.

The CSS co-financing mechanism imposes an additional, calculable burden on state budgets that further erodes the effective value of devolution. For general-category states, the standard centre–state CSS sharing ratio stands at 60:40, with special-category north-eastern and hill states accessing more favourable 90:10 terms. Chakraborty and Gupta (2025) estimate that states’ own CSS contributions consume approximately four percentage points of the nominal 41–42% devolution entitlement, implying that effective untied devolution approximates 37% of the divisible pool, equivalent to roughly 29% of GTR at the FC-15 average divisible pool ratio of 78.3%. The autonomy cost extends well beyond the matching contribution itself to encompass conditionalities on beneficiary selection, procurement procedures, inter-scheme resource prioritisation and fund release compliance. The Union Budget 2025–2026’s decision to reduce CSS allocations by ₹91,000 crore, following the identification of ₹1.6 lakh crore in unspent state CSS balances is simultaneously an indicator of the implementation constraints generated by CSS conditionalities and an illustration of states’ institutional exposure to unilateral reductions in voted transfer flows.

The imperative of adequate resource transfers rests on substantive constitutional and developmental grounds that transcend distributional politics. While the union’s obligation to discharge its own constitutional mandates in national defence, macroeconomic stabilisation and large infrastructure provision legitimately constrains the quantum available for intergovernmental transfer, this constraint must be balanced against the equally important imperative of equipping states to meet their constitutional obligations in education, public health and social welfare (Bird & Smart, 2002; Oates, 1972). Data from the FC-15 document that states bore 62.4% of consolidated revenue expenditure while commanding only 37.3% of available fiscal resources—a structural asymmetry that renders adequate resource transfer a constitutional and developmental necessity rather than a concession to subnational interest (Government of India, 2021). Rao (2017) demonstrates that the progressive compression of the divisible pool through non-shareable cess levies has further eroded states’ discretionary fiscal space, with adverse consequences for developmental capacity. Robust intergovernmental transfers are, in this perspective, not antithetical to union fiscal responsibility but constitutive of it: inadequately resourced states produce human capital deficits and aggregate demand shortfalls whose costs ultimately constrain national growth trajectories (Rangarajan & Srivastava, 2011; Srivastava & Shanmugam, 2023).

Vertical Fiscal Imbalance and the Adequacy of Central Transfers

A rigorous assessment of structural VFI requires comparing states’ expenditure obligations with their own-source revenue capacity, both before and after factoring in central transfers. The FC-15 found that states’ own-source revenues covered only 38% of aggregate revenue receipts, while states’ expenditures accounted for approximately 61% of consolidated revenue spending (Finance Commission of India, 2020). In the post-GST period, states’ own tax revenue as a share of gross domestic product stabilised at approximately 6.3–6.4% for 2022–2024, only marginally above the pre-GST average of 6.1–6.2%. This minimal improvement provides no meaningful relief from the underlying structural imbalance, particularly in light of the intensified CSS co-financing demands simultaneously drawing on states’ own resources (Joseph & Kumary, 2023; Srivastava, 2025).

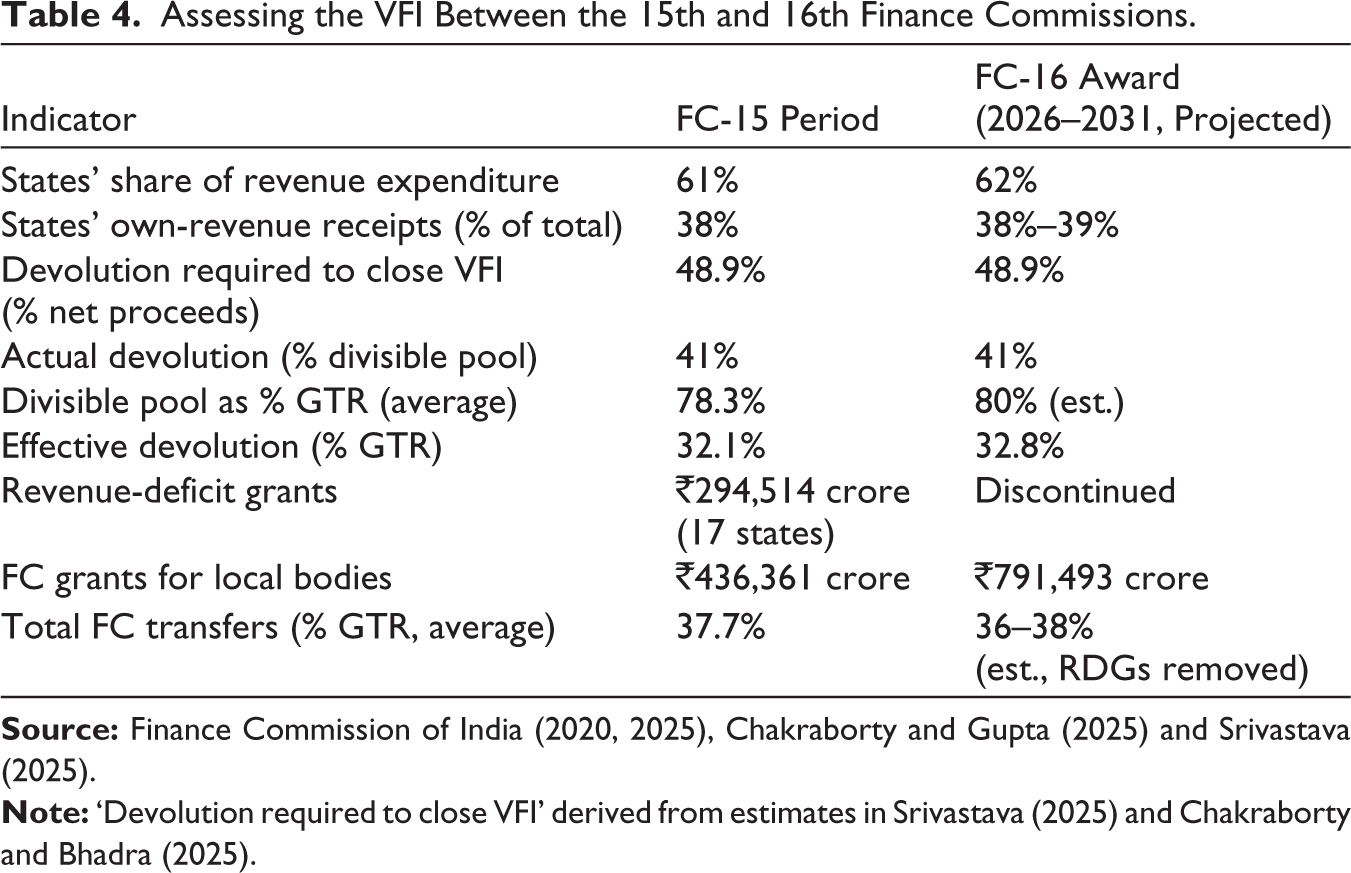

Table 4 exposes the central fiscal arithmetic inadequacy in the FC-16 framework. Even under the optimistic scenario in which the divisible pool recovers towards 80% of GTR as cess revenues stabilise, effective devolution would reach only approximately 32.8% of GTR, falling short by approximately 16 percentage points of the 48.9% of net proceeds estimated as necessary for structural VFI closure (Rangarajan & Srivastava, 2008; Srivastava, 2025). The FC-16’s abolition of revenue-deficit grants withdraws ₹294,514 crore in additional support that the FC-15 extended to 17 revenue-deficit states, partially offset by a substantial increase in local body grants from ₹436,361 crore to ₹791,493 crore. Whether this reallocation improves or worsens the net fiscal position of affected states depends critically on the conditionality and accountability structures attached to local body grants relative to the unconditional nature of revenue-deficit support. The net fiscal adequacy outcome remains, at best, empirically indeterminate.

Assessing the VFI Between the 15th and 16th Finance Commissions.

Conclusion

This article has examined the adequacy of the intergovernmental resource transfer framework under the FC-16’s recommendations, organised around three interconnected lines of inquiry: the structural erosion of the divisible pool, the methodological limitations of gross-tax-revenue-based assessments of transfer adequacy and the autonomy costs imposed by the growing weight of CSS conditionality in total transfer flows.

The central empirical finding is that the FC-16’s retention of vertical devolution at 41% of the divisible pool, while defensible within the constitutional framework and intelligible in light of the distributive politics of formula revision, delivers an effective untied transfer to states that falls materially below the level required to close the structural VFI. At the FC-15 average divisible pool ratio of 78.3% of GTR, the 41% devolution rate yields an effective transfer of approximately 32% of GTR in actual devolution flows. This is approximately 17 percentage points below the estimated 48.9% of net proceeds required for structural VFI closure. The fiscal consequences for states’ ability to discharge their constitutional expenditure mandates are real and cumulative, with implications for the quality and equity of public service delivery across the federation (Rangarajan & Srivastava, 2008; Srivastava, 2025; Rao, 2017).

The methodological contribution developed in the fourth section establishes that the FC-16’s claim that over 49% of gross revenue receipts is transferred to states, while numerically accurate, is analytically insufficient as an indicator of transfer adequacy. The 49% figure aggregates streams of fundamentally different fiscal quality: mandatory and unconditional devolution under Article 270, constitutionally certain FC grants under Article 275, and conditional CSS transfers under Article 282 that carry co-financing requirements, implementation constraints and unilateral revocability. As the co-financing analysis demonstrates, these conditionalities reduce the effective untied transfer by approximately four percentage points of nominal devolution, further compressing subnational fiscal space in ways that aggregate transfer comparisons cannot capture (Chakraborty & Gupta, 2025; Varughese et al., 2025).

The FC-16’s institutional innovations deserve sober assessment. The proposed ‘grand bargain’ on cesses—through which the union would incorporate cess revenues into regular taxes against states accepting a reduced percentage of a correspondingly enlarged divisible pool—is conceptually meritorious in that it would restore the constitutional integrity of divisible pool calculation. However, the proposal is cast in aspirational rather than binding terms within the FC-16 framework; its operationalisation would require either statutory legislative reform or a credible executive commitment that neither is presently demonstrated (Ramakumar, 2024). The High-Powered Committee tasked with CSS rationalisation represents a potentially significant institutional mechanism for reducing conditionality burdens, but its effectiveness is contingent on sustained political will that past reform efforts have struggled to sustain. The discontinuation of revenue-deficit grants, while arguably consistent with fiscal incentive arguments, removes a critical unconditional VFI-bridging instrument without providing a comparably flexible substitute for states that continue to face structural expenditure–revenue gaps. The abolition of sector-specific grants further narrows the conduits through which constitutionally mandated transfer support reaches states with distinctive developmental needs and fiscal vulnerabilities.

Three policy priorities follow directly from the analysis. First, the structural incentive for cess proliferation must be addressed through constitutional or statutory means: either by mandating the inclusion of cess revenues above a defined threshold into the divisible pool or by imposing a binding statutory ceiling on cess and surcharge revenues as a share of GTR. Second, the CSS co-financing architecture requires fundamental restructuring, moving away from parametric conditional transfers towards flexible sectoral block grants that permit states to direct central resources towards locally identified priorities within state-list subjects. Third, the vertical devolution share should be progressively raised towards an intermediate target of 45–46% of the divisible pool, consistent with the structural fiscal arithmetic presented in this article and with the VFI closure requirements estimated in the academic literature, pending a more comprehensive constitutional review. These are not marginal technical recalibrations; they go to the foundational question of whether India’s fiscal federalism can sustain the cooperative and equitable character that the constitution’s architects intended and that inclusive national development requires (Boadway & Shah, 2009; Oates, 2001; Varughese et al., 2025).

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix

Share of Revenue-deficit Grant in FC Grants and Share of CSS in Non-FC Grants.

| Year | Share of Revenue-deficit Grant in FC Grants (%) | Share of CSS in Non-FC Grants (%) |

| 2021–2022 | 57.1 | 61.1 |

| 2022–2023 | 49.9 | 59.1 |

| 2023–2024 | 34.8 | 58.2 |

| 2024–2025 | 20.3 | 48.8 |

| 2025–2026 | 9.0 | 54.4 |