Abstract

Taxes have always been an indispensable part of state revenue. They have existed as old as the existence of civilizations themselves. The question of enforcing compliance has always been an aspiring goal for the exchequer. Compliance is not everything about enforcement for tax collections alone; it carries attempts of modern-day states to build an obedient and self-policing society. While a host of empirical research efforts have solicited tax compliance problem, soliciting its dynamics from taxpayers’ perspective has not been adequately focused upon. The present study postulates a three-dimensional holistic model of taxpayers’ compliance attitude defining tax payee’s relationship (both economic and non-economic dimensions) with the state. The proposed scale would contribute in studying the compliance problem in a comprehensive framework.

Introduction

Empirical research suggests that taxpayers have been found to exhibit varied behavioural tendencies under comparable situations. However, what still remains a mystery is the possible determinants behind such varying behavioural acts. Such varied behavioural tendencies are usually justified across several drives—from an economic perspective 1 to an antithetical psychological or social perspective. The economic models emphasize tax compliance in terms of a cost-benefit decision, that is, as a function of penalties and audit rates vis-à-vis successful tax evasion.2–6 This approach perceives compliance as a barometer of four economic determinants, namely probability of detection (audit), penalty rate (fines), tax rate, and income base with deterrence as the underlying stimuli. However, Andreoni, Erard, and Feinstein 7 observed that levels of tax compliance indeed differ from what they should have been, given the application of standard economic approach only. Research has noticed the inability of this “portfolio approach” in explaining the all-inclusive dynamics of compliance behaviour in practice. 8 While there are certain individuals who tend to behave honestly despite so many opportunities to evade, others tend to indulge in dishonest behaviour despite the provision of a stringent deterrence framework. The standard tax compliance models based on economic perspective fail to account for such contingencies. However, studies such as Cowell, 9 Scotchmer and Slemrod, 10 Falkinger and Walther, 11 and Alm, Sanchez, and De Juan 12 have attempted to broaden the horizon by bringing non-economic factors into the limelight. Instead on simply relying on negative outcomes (deterrence and penalty), positive inducements (like rewards and recognition) were suggested for inducing the level of tax compliance. An alternative branch explaining compliance behaviour as a “behavioural or sociological” element thereafter emerged. This branch asserted human element plays a central role in an individuals’ tax compliance decision process (socio-psychology, political legitimacy, comparative treatment, fiscal exchange, modernization theory, crowding theory, compositional modelling, and equity theory among others).

Historically, implementing universal tax compliance is considered virtually impossible “until there is a tax administrator under every bed”. 13 James 14 suggested that an individual is not only a self-centric independent entity aiming maximization of utilities, but also acts as a social animal in accordance with their attitudes, beliefs, and norms. The standard economic model perceives tax compliance as a problem of portfolio management—a taxpayers rational decision process of how much to disclose and how much to evade in terms of probability of successful evasion vis-à-vis penalties in case of being caught. However, modern research efforts have emphasized upon recognizing tax evasion as a comprehensive function of both economic as well as non-economic determinants. The mystery of tax compliance can therefore be understood comprehensively when research efforts incorporate the entire set of possible determinants affecting the compliance problem. Hence, there is a dire need of having a comprehensive scale for measuring tax compliance dynamics from a tax payee’s perspective.

Background Literature and Rationale

A perusal of literature suggests the presence of varied compliance frameworks touching upon divergent (economic as well as behavioural) perspectives. The two modular perspectives attempt to delve into compliance problem altogether differently. The classical model of tax evasion by Allingham and Sandmo 1 has been the benchmark economic perspective framework. The classical model was guided by the benchmark model of economic crimes given by Becker 2 and basically applied the criminal activity approach to the tax domain. The classical model holds tax compliance behaviour as a function of four important determinants as outlined earlier. Kolm 3 and Srinivasan 4 also approved Allingham and Sandmo’s assertion that taxpayers were rational utility maximisers—although recognizing that the function of tax system is not revenue collection alone, Yitzhaki 5 provided for a major correction in the economic model by asserting the application of penalty on the extent of tax amount being evaded rather than on the practice of incomes so undeclared. Furthermore, Graetz, Reinganum, and Wilde 6 defined the dynamics of economic deterrence model to be a function of a “game”—a dynamic interaction between the taxpayers and the tax authorities.

However, research has noticed the inability of this “portfolio approach” in explaining dynamics of compliance behaviour in practice. The traditional economic framework based on Allingham and Sandmo’s 1 model turned out only as an initial starting push into the research efforts towards tax evasion theoretical framework. Batrancea, Nichita, Batrancea, and Moldovan 15 have held that the uncertainty component in real life scenario can take the form of either financial penalty, criminal prosecution or even a social boycott. Further, as Dean, Keenan, and Kenney 8 held “To abandon taxation studies to arid suppositions concerning how taxpayers might act if they were condemned to being entirely rational, utility-maximizing automations can only serve to postpone the emergence of realistic tax theories and useful policy insights.”

The behavioural branch on the other hand asserted that human element plays a vital role in individuals’ tax compliance decision. A host of theories specifying various models have emerged in this domain with socio-psychology, political legitimacy, comparative treatment, fiscal exchange, modernization theory, crowding theory, compositional modelling, and equity theory among others. These various models approach the problem of compliance from different dimensions. Moreover, research attempts have also recognized the relevance of including the dynamics of shadow economy in the tax compliance framework16,17 thereby incorporating a complex web of structural and governance issues in the domain.

Socio-politico Domain and Compliance Behaviour

People turn underground not only to avoid the tax payments, but indeed to reduce the regulatory burden in terms of bureaucratic controls and corruption. 18 Timberg 19 examined four major potential welfare costs referred to “loss of revenue for the state”, “negative impacts on social morality”, “increased inflation due to enhanced liquidity” and “underestimation of national incomes and statistics” as being directly related to tax evasion. The economic as well as political conditions are said to define the revenue extraction across modern states.20,21 Society-oriented variables especially macroeconomic conditions and class organization in society were found to have a more prominent role in defining the level of revenue extraction. Non-economic factors like a more corrupt government, quality of institutions or increased irregular payments besides efficiency of government spending and political freedom have been held to play a vital role in determining tax compliance.22–24

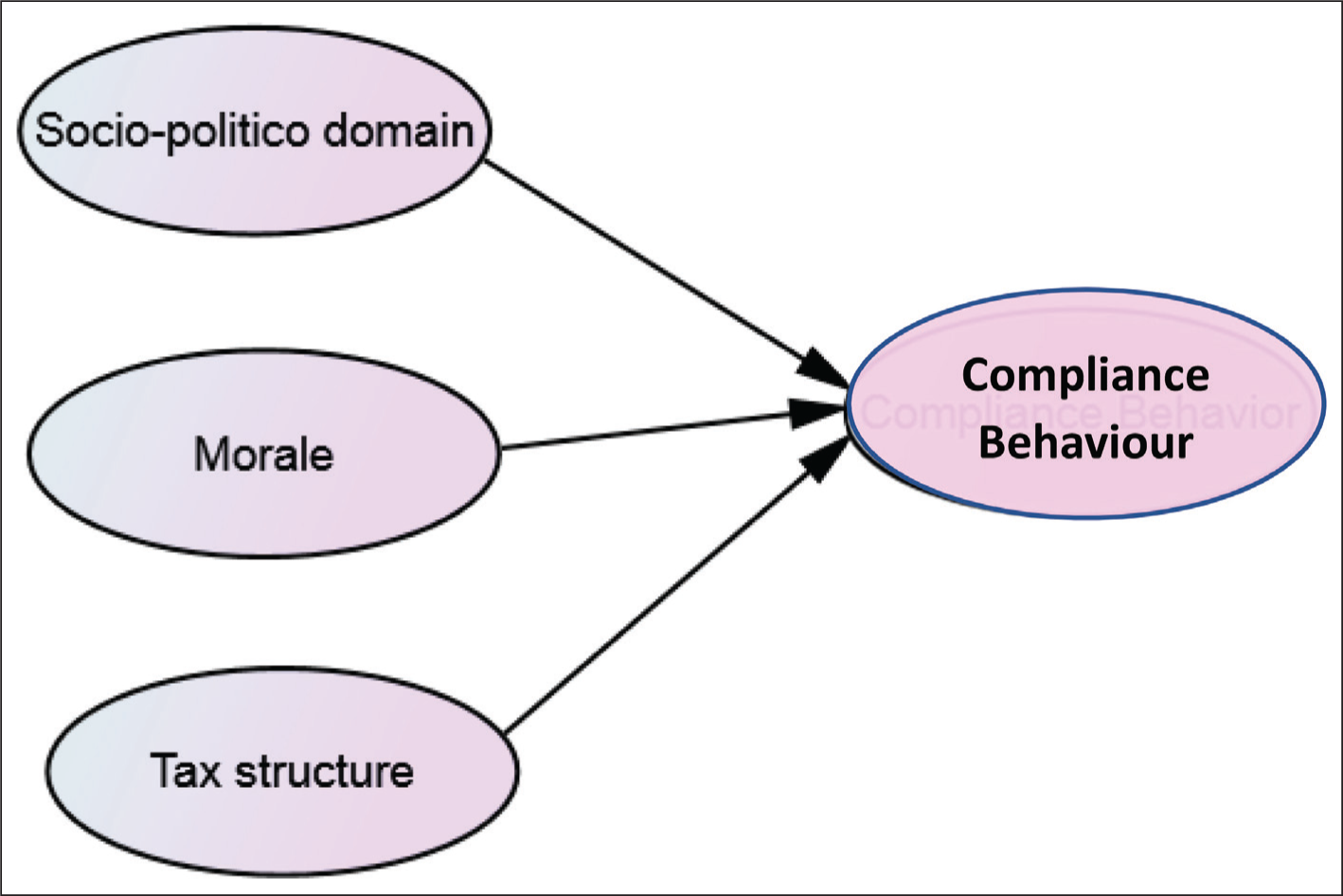

H1: There is a significant relationship between socio-politico domain and compliance behaviour (H1: β1 = 0).

Tax Morale and Compliance Behaviour

It is not viable to understand an individual’s tax compliance decision completely without incorporating the “ethical” dimension into the discussion. An individual is not only a self-centred entity attempting at utility maximization, but also does interact with others in a social setup. 14 Chung and Trivedi 25 assert that tax evasion or its compliance is a moral decision made by individuals. The impact of tax morale over tax compliance has been upheld across the cross-cultural settings.23, 26–29 Compliance is enhanced when payment of taxes is being viewed as a fair Fiscal Exchange exercise by the taxpayers. 30 While Sa, Martins, and Gomes 31 found a significant role of individuals financial satisfaction, trust in others in society, and religiosity level in shaping tax morale, Kondelaji, Sameti, Amiri, and Moayedfar 32 found conditional cooperation and economic situation (income level and financial satisfaction) to be significantly influencing an individuals’ tax morale. Furthermore, social capital variables (confidence in government and national pride) and demographic factors (age and education) are suggested to positively increase the credibility of institutional framework as a policy toll to improve tax morale.

H2: There is a significant relationship between morale and compliance behaviour (H2: β2 = 0).

Tax Structure and Compliance Behaviour

“The manner in which taxes are administered and collected, and the uses to which they are put, define the symbolic relationship between the state and its citizens”. 33 The interaction level between the taxpayers–tax administrators is a very crucial element in better two-way relationship management. The Direct Taxes Enquiry Committee Report 34 emphasized upon improved public relations between the taxpayers and tax department to improve compliance. The presence of complexity in the tax structure is associated with more underreporting and non-compliance.35–37 Das-Gupta 38 suggested a six-pronged approach to resolve the issue of high compliance costs in India by: “Tax structure simplification, institutional reform, procedural reform, automation, monitoring and client feedback, tax policy process and drastic tax reform for reducing compliance costs simultaneously improving compliance”. Muhrtala and Ogundeji 39 emphasized the need to educate taxpayers in ensuring tax compliance and maintenance of records, the change in orientation among tax authorities by making them taxpayer centric and provision of high-quality taxpayer services as a fundamental in building a tax compliance orientation among citizens.

H3: There is a significant relationship between the tax structure and compliance behaviour (H3: β3 = 0).

Although a perusal of literature holds the level of efforts put by abundant studies in examining the issue of tax evasion and compliance in a holistic manner, states have usually resorted to tackle the menace through a combination of coercive cum educative measures, but in isolation. Christians 40 proposed a “theory of sovereignty” that advocated only a conditional autonomy for the states (in tax matters) in a global economically interdependent world. It indicated the trade-off that governments had to make between being autonomous (politico-social-economically) and nurturing of economic relations with other states. The study mentioned such trade-off as “OECD harmful competition” work—where one country’s fiscal choices impact others significantly. This view is said to reflect the existence of “social contract among states” wherein tax policy matters are viewed as a function of multifaceted and dynamic “transnational grid of power and principle”. However, the study primarily deals with states as principal entities in this contractual relationship while leaving out the role of individual citizens in such a transaction significantly. The states, according to this theory, are expected to recognize the status and concerns of other states while framing their tax policy designs.

Uslaner, 41 on the other hand, advocated creation of trust among people coupled with a strong legal system to deal with the problem of tax evasion. The study examined relationship of tax evasion to two versions of trust—general trust (trust among citizens) and trust in the government (legal system). It noted that “Confidence in government, not faith in fellow citizens, matters for tax compliance”. Furthermore, studies42–44 have also held that people are likely to be more honest in paying their taxes when they trust government and the legal systems, that is, trust in democratic institutions. Ali, Fjeldstad, and Sjursen 45 observed the determinants of tax compliance behaviour among individuals to be a function of one of the five different theories: “economic deterrence, fiscal exchange, social influences, comparative treatment, and political accountability” which invariably affect the decision concerning payment or evasion of taxes by the individuals.

However, what is found to be missing empirically is that what defines the relationship between state and its subjects contemporarily and how the state’s morality coupled with individual morality and tax law concerns comprehensively define tax compliance conduct. The purpose of the present study is to mark an attempt to bridge the aforementioned fissures in the existing understanding and gain new insights into the dimensionality structure (Figure 1) of compliance problem.

Methodology

The study deploys a four-step procedure of scale development outlined by Mann and Ghuman. 46 The process started with developing an initial pool of relevant items based on empirical literature. The item(s) development procedure used both inductive and deductive approach for item generation. The process started inductively with a classification of dynamics of tax compliance. Thereafter, the question of designing a questionnaire to accurately access compliance attitude was addressed. For this, unstructured interviews with the tax officials, tax professional service providers (chartered accountants, tax return preparers), and individual taxpayers were conducted. A total of 60 unstructured interviews were being conducted spreading across tax officials (12), tax professional service providers (16) and individual taxpayers (32). The inputs from unstructured interviews coupled with a review of existing empirical literature led development of 88 itemized pool of statements. These statements covered three broad dimensions across which tax compliance attitude has been examined (socio-politico domain, morale, and tax structure).

The initial pool of 88 items was then put to content analysis and validity. Content validity has been established by two methods—one by deriving items after an extensive review of subject literature and second, thorough discussions and cross examination of items by five academic experts in the field. Based on the inputs received, a total of 13 items were deleted and certain others were reworded and reframed to bring uniformity to the domain under study. The items were scaled using a Likert scale. The revised sets of items were pre-tested which led to further removal of six items that were found to be non-uniform, overlapping, and contradictory. Hence, a total of 69 items were being used for the final survey of taxpayers’ attitude towards tax compliance.

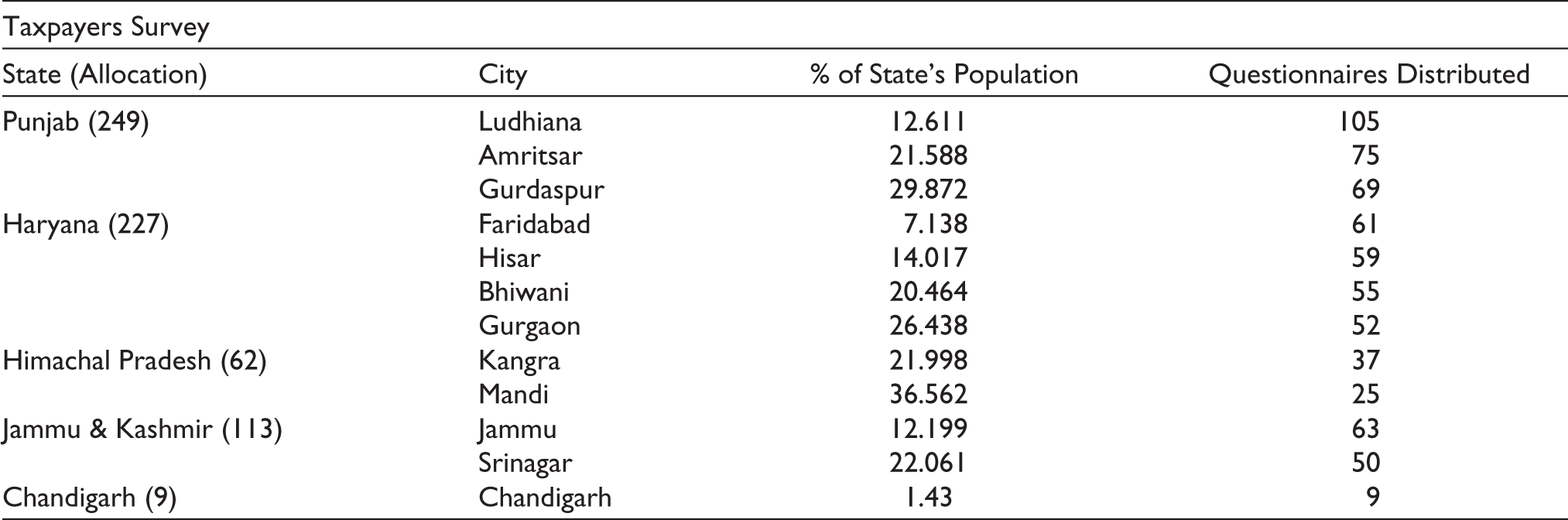

The survey was administered across the major cities of north-west region of India (as classified by C.B.D.T) comprising the states of Haryana, Punjab, Himachal Pradesh along with Union Territory of Jammu & Kashmir.

The sampled cities (Table 1) have been selected in line with the spread of population in the states according to official census statistics, 2011, with a rider that the cumulative spread across these cities constitutes at least 25% of the states’ population. Based on the above rule, 12 cities were selected—Punjab (Gurdaspur, Ludhiana, Amritsar), Haryana (Faridabad, Hisar, Bhiwani, Gurugram), Himachal Pradesh (Kangra, Mandi), Jammu & Kashmir (Jammu, Srinagar). A total of 406 responses duly filled and completed in all respects were obtained. Within this composition, a total of 237 responses were obtained from business category respondents with 178 responses from professional respondents. Majority of the survey respondents (73%) were male, with the rest 27% being the female taxpayers. Most of the survey respondents were found to be within the age bracket of 30–60 years of age (57%) followed by 61–80 years (24%), 18–29 years (9%), and rest constituting > 80 years of age (10%). On the income front, similarly, a majority of the survey respondents were in the income level of ₹5,00, 001–₹10,00,000 per annum (54%), followed by ₹2,50,001–₹5,00,000 (25%), ₹10,00,000 and above (18%), < ₹2,50,000 per annum (3%).

Distribution of Sample Survey.

Statistical Results

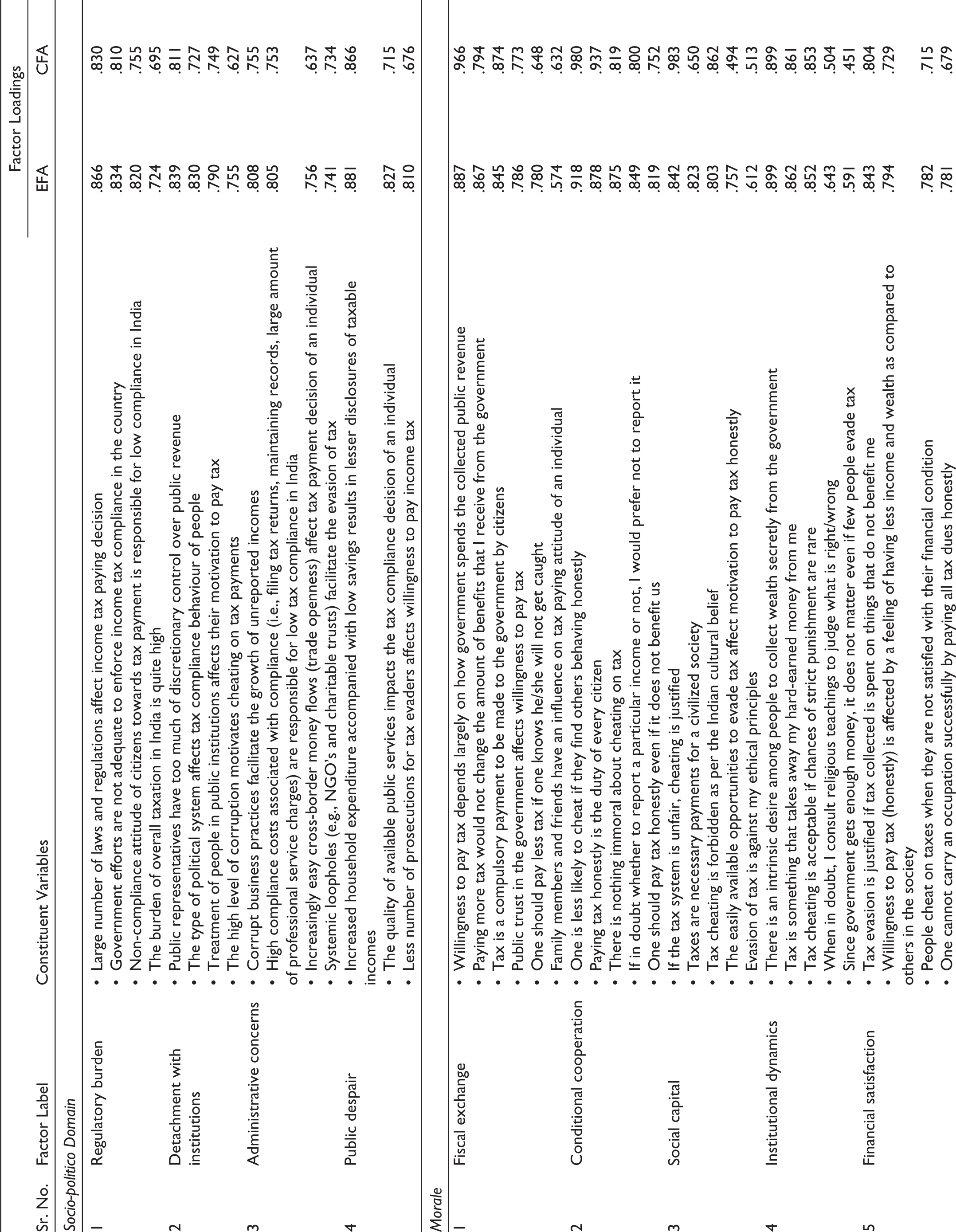

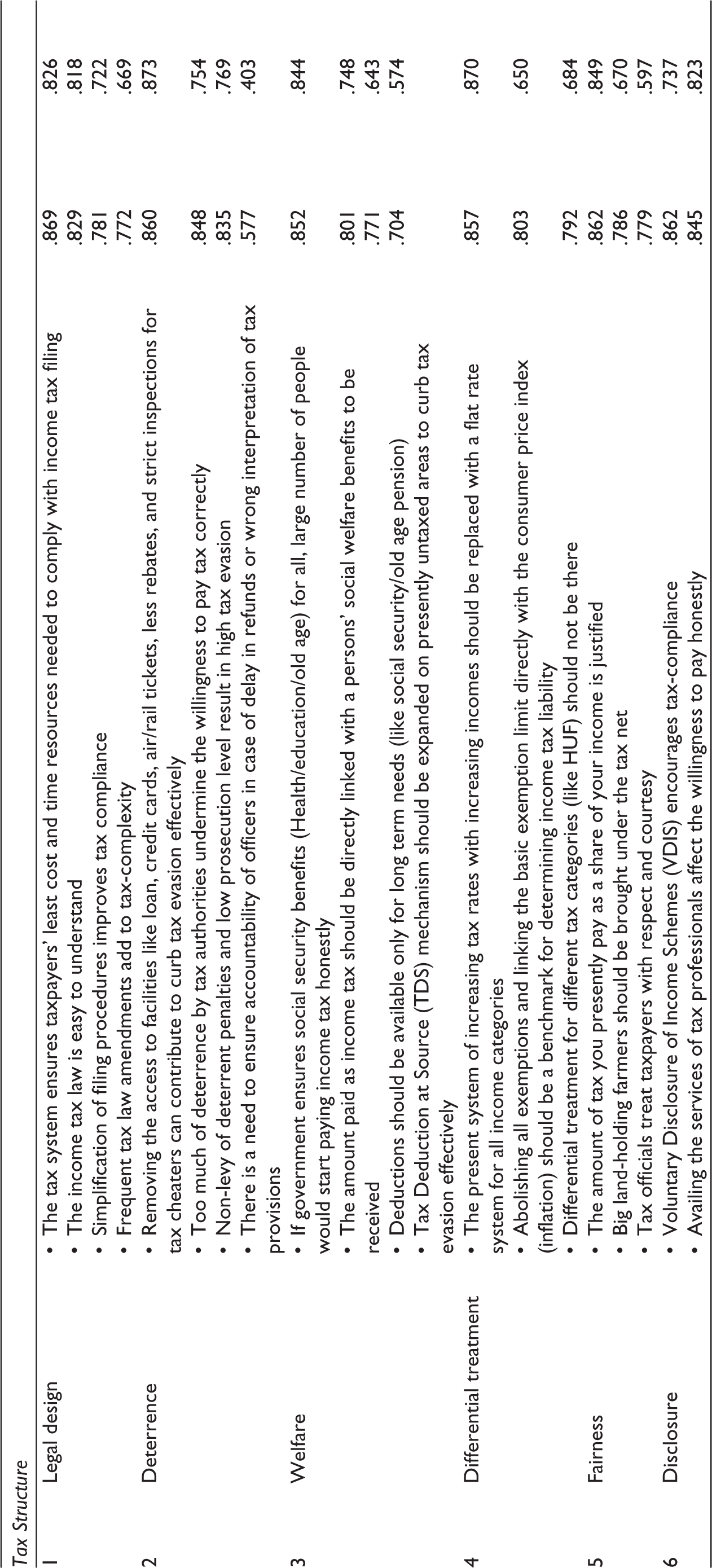

The exploratory factor solution was performed across the three-dimensional structure. The initial factor solution across 18 items (socio-politico domain) generated 4 factors explaining 64.34% of the variation. A closer look at the factor results indicated one item to be having low communality (less than 0.3) and another item to be having low factor loading (less than acceptable value of 0.4) while one item was found cross loading significantly over the two factors. Subsequently, these three items were dropped and a four-factor solution with 15 statements explaining 67.98% variation was obtained (Bartlett’s test of sphericity-Chi square: 2482.563(0.000), KMO: .795). For the dimension representing tax morale, the exploratory factor solution for 28 scale items constituting 6 factors with 72.47% of variance explained was obtained. An attentive inspection revealed two items to be cross loaded and one item with low factor loading than acceptable limits. Subsequently, these items were removed and revised factor solution with 25 items having five factors explaining 69.39% of total variation has been obtained.

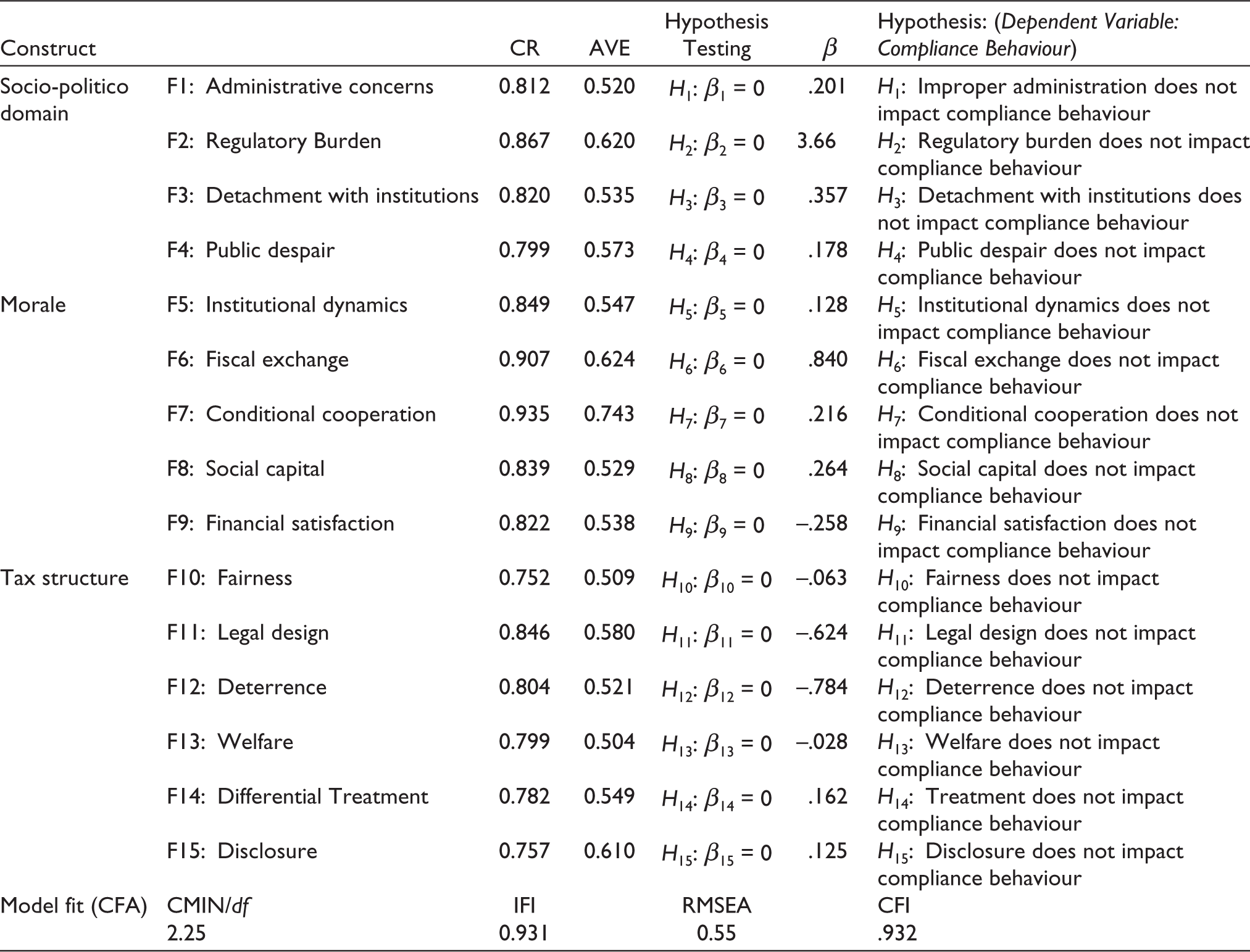

The application of exploratory factor analysis revealed a 15-factorial structure (Table 2) of tax compliance attitude. The socio-politico domain (CMIN/df = 2.04; CFI = .964; RMSEA = 0.50) with four constructs, namely “regulatory burden”, “detachment with institutions”, “administrative concerns”, “public despair”; morale dimension (CMIN/df = 2.33; CFI = .951; RMSEA = 0.57) with five factors, namely “fiscal exchange”, “conditional cooperation”, “social capital”, “institutional determinants”, and “deterrence”; and tax structure dimension (CMIN/df = 2.25; CFI = .932; RMSEA = 0.55) with six-factor structure, namely “legal design”, “deterrence”, “welfare”, “differential treatment”, “fairness”, and “disclosure” has been obtained. The three-dimensional exploratory structure has been further tested for reliability and validity of the scale. Separate factor models were run for the three-dimensional structure. The application of CFA and ordinal regression validated the empirical model (Table 3).

Factor Structure and Constituent Variables.

Psychometric Properties of Scale.

There are numerous measures with exploratory or confirmatory approaches to confirm the reliability and validity in field research. The reliability of the measures has been examined using Cronbach alpha’s, composite reliability (CR), and measure of average variance extracted (AVE). All the values of coefficient alpha are well above the recommended threshold value. Moreover, all the CR statistics have been above the prescribed limit (0.7) and AVE (>0.5) reaffirming the reliability of the scale. Setting the factor extraction criteria (eigen value >1) and factor loading (>0.5) ensures convergence among correlated items and the underlying construct.

Hypothesis Testing

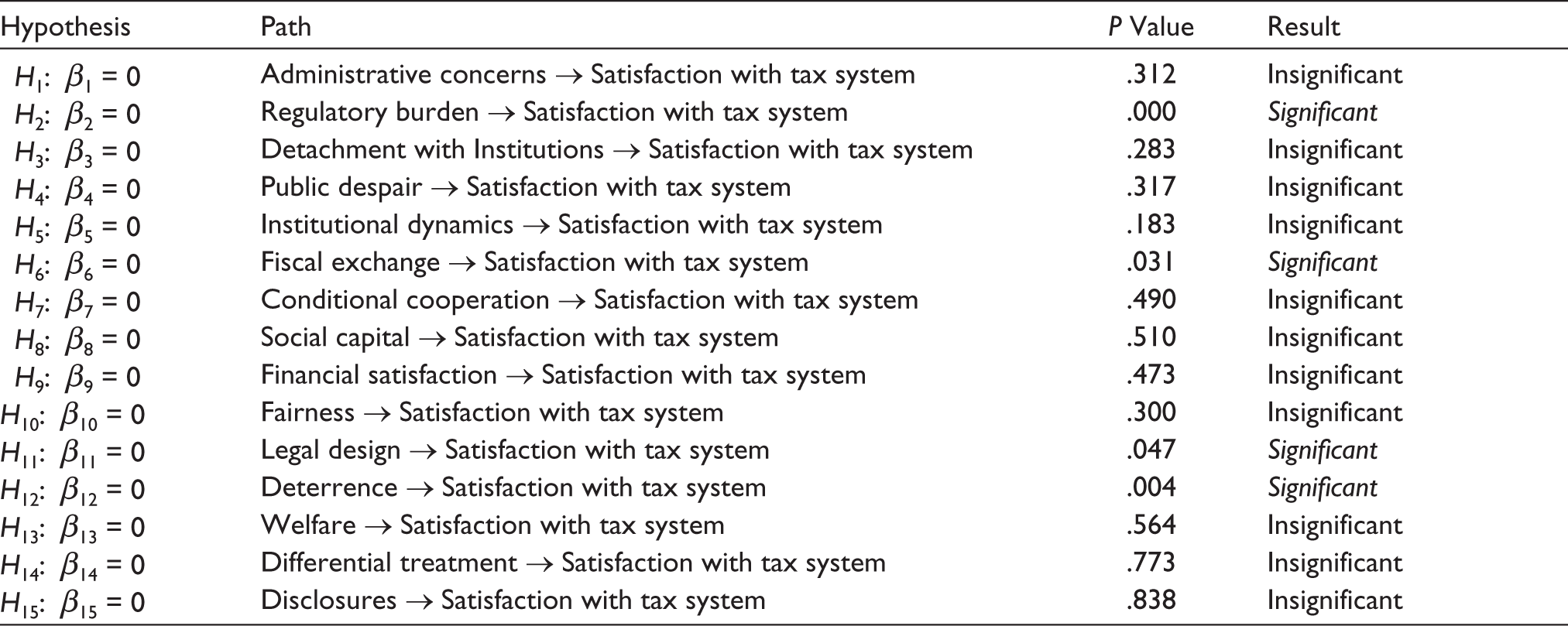

A perusal of literature review prescribes us to believe that there is a variation in taxpayers’ level of satisfaction with the income tax system. Hence, variations across the taxpayers’ satisfaction in reference to these dimensions across the sampled respondents have also been tested. The 15-factoral structure framework of tax compliance attitude (Column 6: Table 3) was testified to examine how well it affects the taxpayers’ satisfaction with the income tax system. The ordinal logistic regression technique has been used to explore the same. The survey respondents were asked a question concerning their level of satisfaction with the present income tax system over a five-point scale response formulating an ordinal outcome to the said question. The constructs comprising tax compliance attitude together explained 48.8% variation in the taxpayers level of satisfaction with the Indian income tax system (Nagelkarke R2: Table 4).

Hypothesis Testing and Results.

The results found 4 of the 15 constructs to be significantly influencing the taxpayers’ satisfaction with the Indian income tax system. For analysing the impact of four significant explanatory variables—regulatory burden, deterrence, fiscal exchange with state, and legal design—the exponential of the estimate values of the explanatory variables has been inferred. Overall, the model found no gender or income differences across the taxpayers’ level of satisfaction with the Indian income tax system.

Discussion and Conclusion

Tax compliance is a multi-dimensional phenomenon. “The reasons underlying taxpayers’ behaviour are not yet completely understood by researchers and by politicians”. 31 However, research has noticed that taxpayers tend to demonstrate differential attitude towards tax compliance even under similar situations. The present research attempted to plug reasons behind these variations by examining the underlying structure of tax compliance. Furthermore, it was examined that how well the present instrument explains the taxpayers’ satisfaction with the Indian income tax system. The attitude towards tax payment could be defined as a composite enabling framework of economic as well as non-economic determinants. As Bird et al. 48 held that in a state, policy ideas (fairness, equity, efficiency), social interests (regional, poor, capital, labour), and key political and economic institutions (democracy, budget, macro-economic policy, and market structure), all interact together in formulation and implementation of tax policy framework.

The scale so developed has been administered to the sampled taxpayers’ population for examining the antecedents behind tax compliance attitude. The survey findings have presented interesting outcomes. Among the socio-politico domain, regulatory burden has emerged as the most important dimension followed by detachment with institutions, administrative concerns, and public despair as the successive dimensions. The anticipated burden of regulations has been felt to be an important factor deriving taxpayers socio-politico concerns. Literature has also held that the quality of governance indeed impacts the motivation of and fiscal exchange between state and its subjects. 49 The increased burden of taxation coupled with intensity of regulations and quality of public service delivery have been empirically held to be the driving forces behind the growth of shadow economy and tax evasion. 50 Furthermore, tax compliance is bolstered when individuals view payment of tax as a fair fiscal exchange exercise with the state ceteris paribus. 51 Among the tax morale construct, fiscal exchange (with the state) has emerged as the top most important dimensional construct followed by conditional cooperation, social capital, institutional determinants, and financial satisfaction as the principal constructs. The literature has also held that personal ethics (intrinsic motivation) indeed significantly affect tax compliance attitude.52,53 The study findings indicate fiscal exchange with the state marked by conditional cooperation principally defines the taxpayers’ intrinsic motivation to pay tax. Among the tax structure dimension, legal design followed by deterrence, welfare, differential treatment, fairness, and disclosures has emerged as the principal constructs specifying taxpayers compliance behaviour.

The statistical findings take us to put forth some recommendations that could be observed by practitioners or those at the helm of affairs to pursue the attempts towards soliciting enhanced tax compliance in India. First, as observed, reducing the overall level of regulatory burden on the taxpayers stands to be the important barometer in re-awakening the flavour for taxpaying honestly. Next, improvements in the quality and improved accessibility of public service delivery can be a motivator in encouraging people to comply voluntarily and completely. Maintenance of a credible deterrence against habitual tax offenders and further reforming the tax structure to minimize complexity and encouraging of honest tax behaviour by imbibing tax education in curriculum can well boost up the desire of paying tax dues honestly. Finally, efforts are desired to enhance the authority and respect for the democratic institutions.

Implications for Practice

The present work has developed a comprehensive scale that examines the tax compliance attitude from a multi-dimensional perspective. The scale reflects the multitude facets of taxpayers’ decision-making affecting compliance behaviour. Besides the standard economic framework, non-economic factors (tax morale and sociopolitical environment) have been incorporated to provide for a composite structure of tax compliance behaviour.

The scale intends to make exclusive contribution to the body of literature in at least two different means. First, the tax morale dimension which has been treated as the black box and has been explored as a multi-dimensional phenomenon. Second, an attempt has been made to include the elements of sociopolitical environment having a bearing on tax compliance attitude of individuals. Past research efforts have attempted to identify the causal drivers of shadow economy on why people participate in underground economy. While there has been an over emphasis on economic determinants, other aspects especially the non-economic dimensions like tax morale and dynamics of shadow economy participation/intention had been under-represented. The present study thus makes an attempt to delve into the unexplored domain of tax compliance attitude through a comprehensive framework of a three-dimensional structure touching upon these aspects of compliance determinants. The generalizability of the scale across the other taxpayers’ categories needs to be validated in terms of future initiatives to solve the puzzle of tax compliance in complete.

Limitations and Future Research

The study is conducted in relation to taxpayers who have been found to be “highly conscious” in responding to the said questionnaire. The nature of present study being the primary one can be another constraint as the perception of the respondents towards the tax system platform may change in terms of longitudinal studies. Since the results pertain to sampled respondents conducted in a dedicated sample region only, results cannot be generalized for all the spheres and shall be kept restricted to the said sampled units only. Future studies may explore to validate the proposed model in varied contexts which can further strengthen the relationship dynamics among the underlying constructs.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed the receipt of the following financial support for the research that forms basis of this article: This work was supported by the University Grants Commission JRF fellowship [UGC Ref No; 1644/NET-DEC., 2012].