Abstract

Digital payment is one of the payment methods that is used for exchanging currency digitally without the use of actual cash. Digital payments have revolutionized the way people spend their money. The present study aims to provide an extensive literature review of emerging digital payment technologies. The authors have gathered data from different databases, which include Scopus, Web of Science, EBSCO, and Elsevier using the keywords “Digital Payments”, “Internet Banking”, “Mobile Banking”, “E-payments”, “Electronic Payments”, “Online Payments”, and “Virtual Payments”. The research papers have been selected using certain selection criteria that have been discussed in this article. The present study has been divided into many sections including top contributing countries in the field of digital payments, trends of citation, prominent author’s citations, and prominent research methodologies of research papers. It highlights the worldwide spread of research on digital payments, including notable contributions from India, China, the United States of America, Malaysia, and Indonesia, among other nations. Regarding research methodology, surveys and quantitative approaches are often used, and one common data analysis tool is structural equation modelling. The present study highlighted themes such as adoption, usage, engagements, and infrastructure that dominate in most research. Also, many researchers did not use any research models and theoretical frameworks in their studies, with the unified theory of acceptance and use of technology (UTAUT) and the technology acceptance model (TAM) being the most favoured models and theoretical frameworks when utilized. The present study also provides the factors affecting digital payment adoption. This study provides academic contribution by providing global research trends, methodological preferences, and theoretical frameworks. Future directions and thrust areas in the field of digital payments have also been discussed, which guides academicians in the direction of more thorough studies.

Introduction

The world has been becoming digitally advanced for quite a while. In terms of wireless communication, the internet has drastically changed the way a business conducts its operations in recent years. The recent development is more effective than anything the internet has ever provided since it gives users a framework that can operate anywhere and at any time (Barnes, 2002). Nonetheless, the year 2020, due to the COVID-19 pandemic, put into our point of view the desperate need to adopt digitally advanced technology at the earliest opportunity (Surabhi, 2020).

In the field of payments and settlement, digital payment is one of the payment methods, that is growing and changing the lives of individuals. Digital payment is an exchange that happens through online or digital modes, with no cash transaction included. This indicates that the two players, that is, payer and payee, utilize digital payment to trade cash (Bhatia, n.d.).

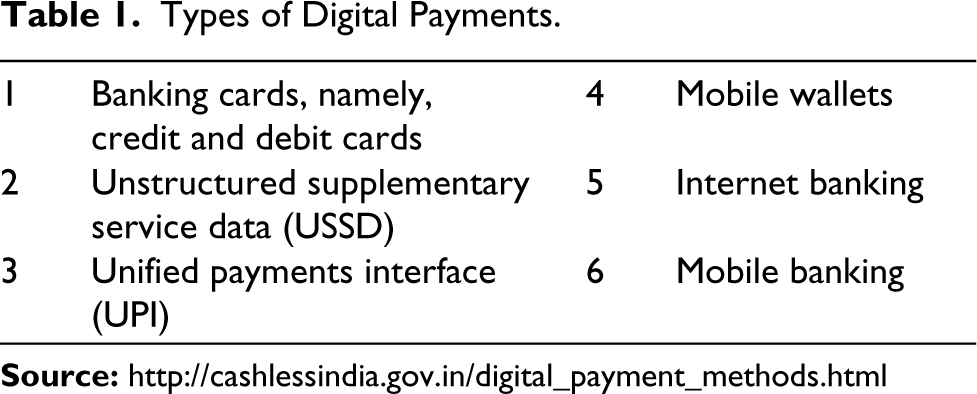

There are many different types of digital payments, as shown in Table 1.

Types of Digital Payments.

Banking Cards, Namely, Credit and Debit Cards

Those payment cards that enable their owner to take out an advance from a financial institution to cover expenses or make purchases are called credit cards. The cardholder has a deadline to repay the borrowed money, normally plus interest, and they can choose to pay it back all at once or in instalments each month. With a debit card, a person can make purchases or take money out of their bank account using this payment method. Whenever a debit card transaction is done, the money is withdrawn from the cardholder’s bank account right away. A debit card does not need to borrow money and does not incur interest, in contrast to a credit card (Scholnick et al., 2006).

Unstructured Supplementary Service Data (USSD)

The Global System for Mobile (GSM) service called Unstructured Supplementary Service Data (USSD) fosters interactive communication between its user and application. The term “USSD digital payment” describes the use of USSD technology to enable money transactions and digital payments without Internet connectivity (Mallik et al., 2020).

Unified Payments Interface (UPI)

The National Payments Corporation of India (NPCI) created the mobile-based payment system known as the Unified Payments Interface (UPI

E-Wallets

A digital wallet, also referred to as an electronic or mobile wallet, is a tool that allows individuals to conveniently store and oversee their financial information, such as credit card numbers, loyalty programmes, and banking details, in a centralized manner. It is a system of transactions that lets customers transact money, make purchases, and carry out other financial operations via mobile devices or the Internet without having to enter their information again (Nizam et al., 2019).

Internet Banking

The term “Internet banking”, sometimes referred to as “online banking” or “e-banking”, describes the electronic banking services that financial institutions offer to their clients online. Customers can use it to conduct a range of banking services and transactions from a distance without going to a physical bank branch. These services usually include paying bills, asking for loans, viewing account statements, transferring money between accounts, and verifying account balances (Furst et al., 2002).

Mobile Banking

Mobile banking is a service provided by bank institutions for conducting financial and non-financial transactions via a mobile device. This concept covers accessing bank accounts using mobile devices and carrying out different tasks like making payments, transferring funds, selling stocks, and checking bank account status and profile (Shaikh & Karjaluoto, 2015).

Although digital payments are becoming more and more popular as an emerging technology, the adoption rate in developing nations remains lower than the desired outcomes (Augsburg & Hedman, 2014). This may be due to the competition that alternative payment methods, with a long history in developed nations, pose to digital payments (Slade et al., 2014). Still, things are very different in emerging markets. Mobile payments are widely accepted in nations like the Philippines and Kenya, where traditional banking institutions are not as widely used (Jesse McWaters, 2015).

Undoubtedly, digital payment has huge potential to bring out financial inclusion in emerging economies, especially for users who do not have basic banking, and improve their lives. Recently there have been many programmes and initiatives launched by the Government of India to improve the public welfare and delivery system, ensuring transparency in financial transactions and reducing tax evasion. The Indian government has been encouraging digital payment very aggressively, beginning with demonetization back in 2016 (Business Standard, 2021). The Digital India initiative has been the primary catalyst behind various financial and economic policies that have encouraged Indians to transition towards online payment methods (Aggarwal et al., 2021). According to the Government of India (n.d.a), the Digital India programme is a prominent programme of the Indian government, and one of its stated objectives is to promote a “Faceless, Paperless, Cashless” approach. Other initiatives include Pradhan Mantri Jan Dhan Yojana (PMJDY) (Government of India, n.d.b). The Government of India started the PMJDY financial inclusion programme to give the unbanked population access to financial services such as savings accounts, remittances, loans, insurance, and pensions. Through the expansion of financial services, the programme has contributed significantly to the rise in the usage of digital payments. There are many more initiatives and programmes UPI application, Aadhaar Enabled Payment System (AEPS), Cashless India, and so on.

Despite many promotional initiatives and programmes, and the advantages of digital payments, there is still a reluctance to adopt digital payments not only in India but also in other nations. Therefore, the basic objective of the current study is to address this issue and provide viable solutions.

Review of Literature

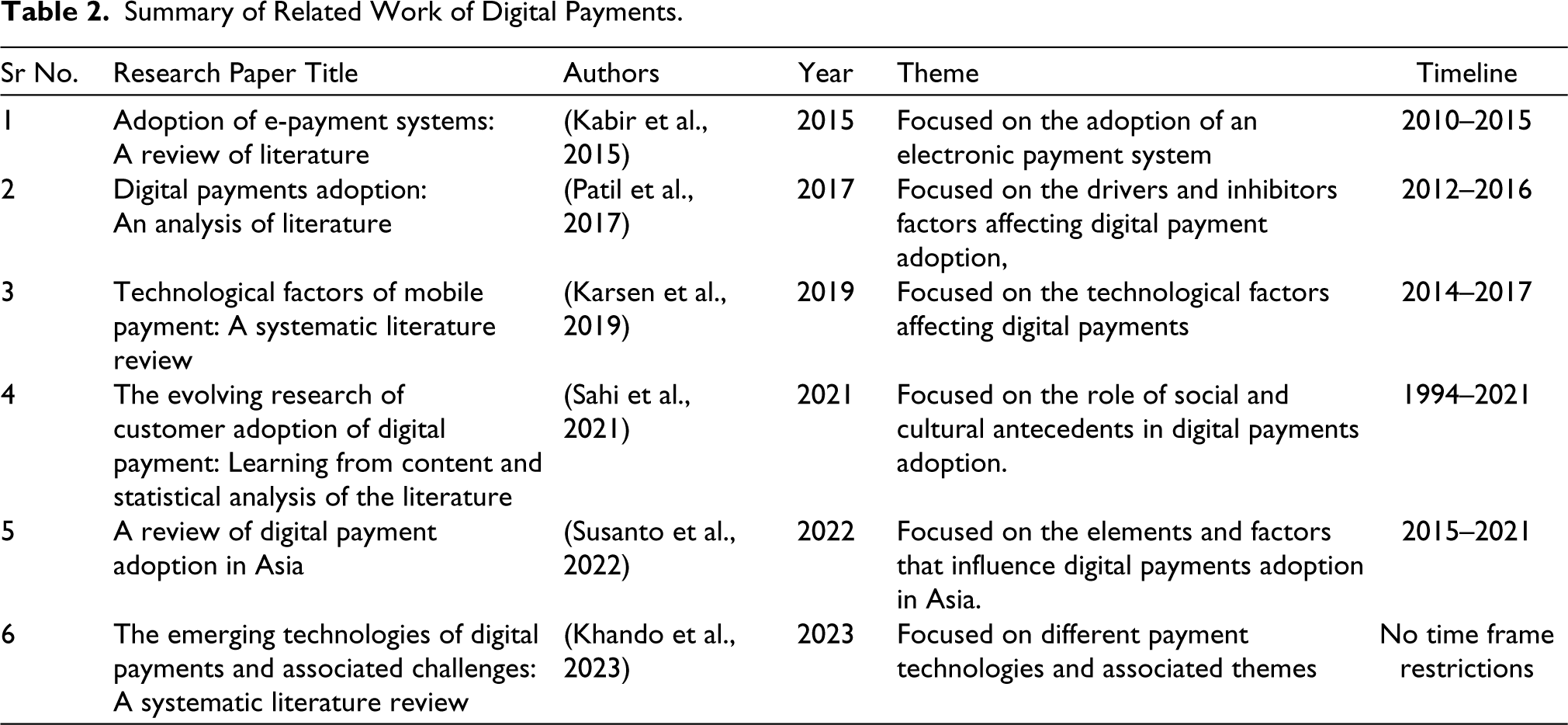

Extensive studies have been conducted in the past concerning digital payments. Table 2 provides summarized highlights of the past studies. In these studies, different approaches were adopted to study the systematic literature review (SLR) on digital payments.

Summary of Related Work of Digital Payments.

Kabir et al. (2015) focused on the e-payments adoption system. Patil et al. (2017) studied the drivers and the inhibitor factors that affect the digital payment system. Technological perspective was considered in the study of Karsen et al. (2019). Sahi et al. (2021) studied the cultural and social variables in the adoption of digital payments. Susanto et al. (2022) studied those factors that impact the adoption of digital payments. Different technologies like bank cards, mobile banking, QR codes, and associated themes were discussed in the study of Khando et al. (2023).

Research Significance

In the previous section, the authors discussed past studies related to digital payments. There are some limitations of the previous studies, such as some of the studies only focused on the limited time frame like Kabir et al. (2015), few studies focused only on the limited geographical area like Susanto et al. (2022) and some studies focused only on specific adoption factors like Sahi et al. (2021) Therefore, the current study is adopted to provide a comprehensive study on digital payments. There are many other reasons to study this field, such as (a) the emergence of new methods of digital payment like E-Rupi that come in the market, and new governmental policies and regulations that come in the market, which need further exploration; (b) digital payments have impacted the economic activity in many countries (Messi et al., 2021; Ravikumar, 2019); and (c) digital payments have had an impact on society and have changed the behaviour of spending, which needs further exploration.

The present study aims to systematically review the available latest literature on online databases from 2018 to 2022. This area of research is evolving day by day, as with new technologies, the dimensions of digital payment change daily and need further exploration. This research will address five questions, which are listed in the next section.

Research Questions

For the present study, the research questions that will assist academics, professionals and policymakers in selecting other studies and making decisions are given as follows:

How regionally diverse is this digital payment research? What are the themes associated with digital payment research? What research methodologies (RMs) are adopted in digital payment research? What are the citation trends in digital payment research? Which models and theoretical concepts or frameworks are used frequently in digital payment research?

Research Methodology

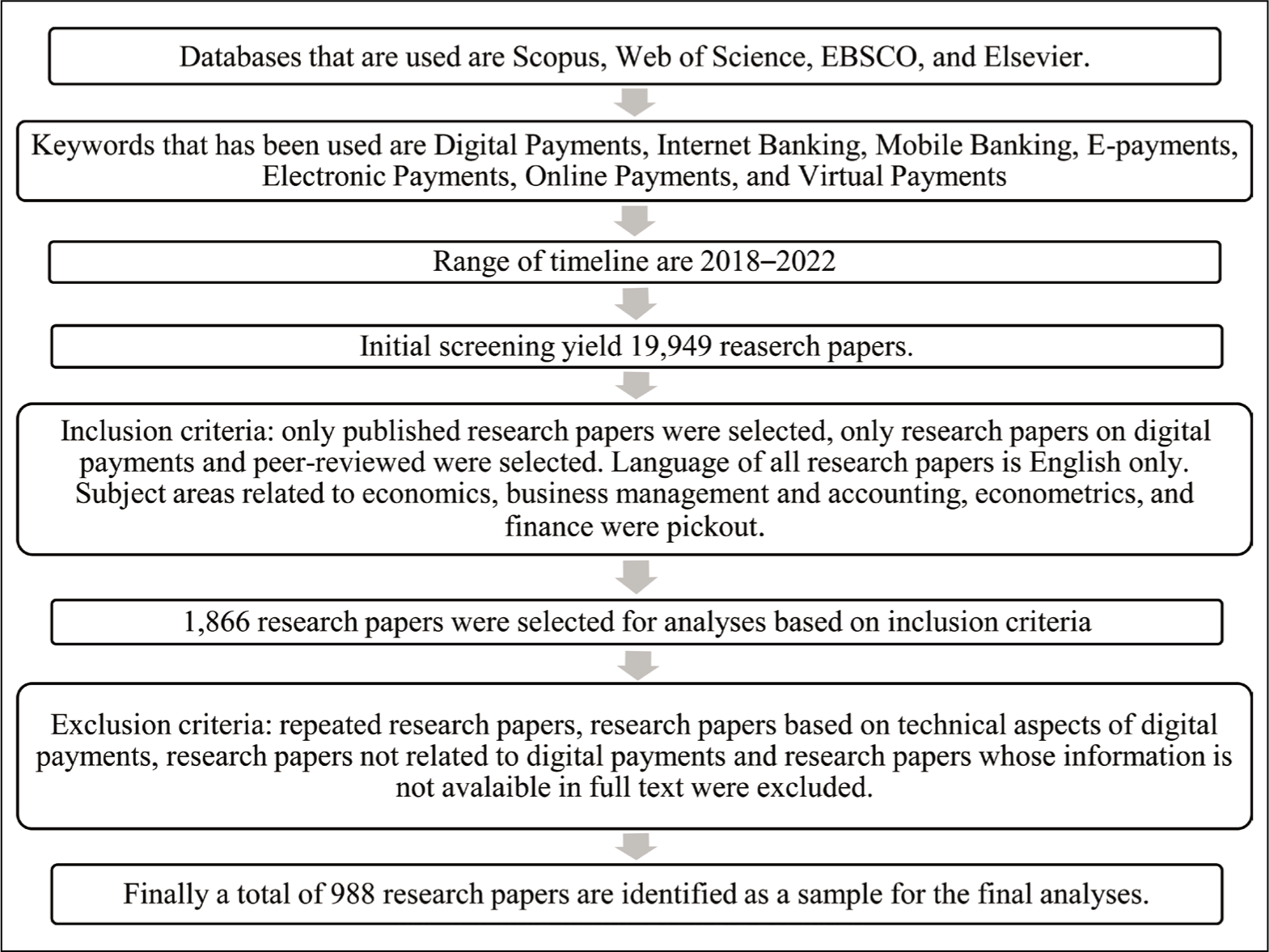

The authors attempt to analyse the available literature on digital payment from the last five years, that is, 2018 to 2022, as the authors aim to provide a comprehensive overview of the current status in the existing body of knowledge. Within the selected timeline, data had been collected from different databases, namely, Scopus, Web of Science, EBSCO, and Elsevier. A combination of different keywords was used for selecting the sample size for data analysis. Those keywords were Digital Payments, Internet Banking, Mobile Banking, E-payments, Electronic Payments, Online Payments, and Virtual Payments. Authors used certain criteria (inclusion and exclusion criteria) to select a sample size of research papers for data analysis, which is mentioned in Figure 1.

Selection Criteria of Research Papers.

Inclusion Criteria

Those research papers that were published based on digital payments and peer-reviewed ones were considered. The language of all research papers was English only. Subject areas related to economics, business management and accounting, econometrics, and finance were considered.

Exclusion Criteria

Those research papers that are repeated ones, based on technical aspects of digital payments, not related to digital payments and whose information was not available in full text were excluded from this study.

Initial searching of keywords from the aforementioned databases yielded 19,949 research papers. After considering the inclusion criteria, a total of 1,866 research papers were selected for further analysis. Finally, after considering the exclusion criteria, a total of 988 research papers were selected for the final analysis.

In the present study, authors have selected, organized, analysed, and reviewed the existing research data from reputed electronic databases. Then they constructed a review framework comprising geographical distribution, key RM, themes, and citation trends for this study.

The final data contains information such as the author’s name, title of research paper, journal name, year of publication, and citation of each research paper. Other important data collected includes the institution’s geographical location, publisher, and themes of each research paper.

Data Analysis

For research question 1 (RQ1), to study how geographically diverse digital payment research across various countries is, the authors selected and analysed the citations and documents published by the top 21 countries that have citation scores of 200 or more using the VOSviewer software. For research question 2 (RQ2), to study the themes associated with research papers, the authors identified the factors responsible for respondent’s behaviour towards digital payments. Research themes, that is, digital payments usage, digital payments adoption, digital payments engagements, and digital payments infrastructure were derived from the original article of Kapoor et al. (2024), research paper’s titles, and research paper’s objectives that we have selected for this research

For research question 3 (RQ3), McCusker and Gunaydin’s (2015) study served as the benchmark for categorizing the various kinds of research, such as qualitative research, quantitative research, and mixed-methods research (Wilkinson & Birmingham, 2003). The study served as the benchmark for categorizing the various research instruments/tools such as questionnaires, interviews, content analysis, focus groups observation, and so on. Online blog searching, online platform surveys, data mining techniques, critical incident techniques, and netnography were also added based on the data thus analysed. Data analysis techniques/methods were based on the data we collected and analysed.

For research question 4 (RQ4), the authors used VOSviewer software to study the citation trends and frequent citation work in digital payment research using descriptive statistics. For research question 5 (RQ5), to study the frequent models and theoretical concepts or framework, the author used descriptive statistics by coding models that were used in sample size.

Findings of the Study

This section is divided into five sub-sections and each research question that is mentioned in the previous section has been thoroughly discussed.

RQ1: How Regionally Diverse is This Digital Payment Research?

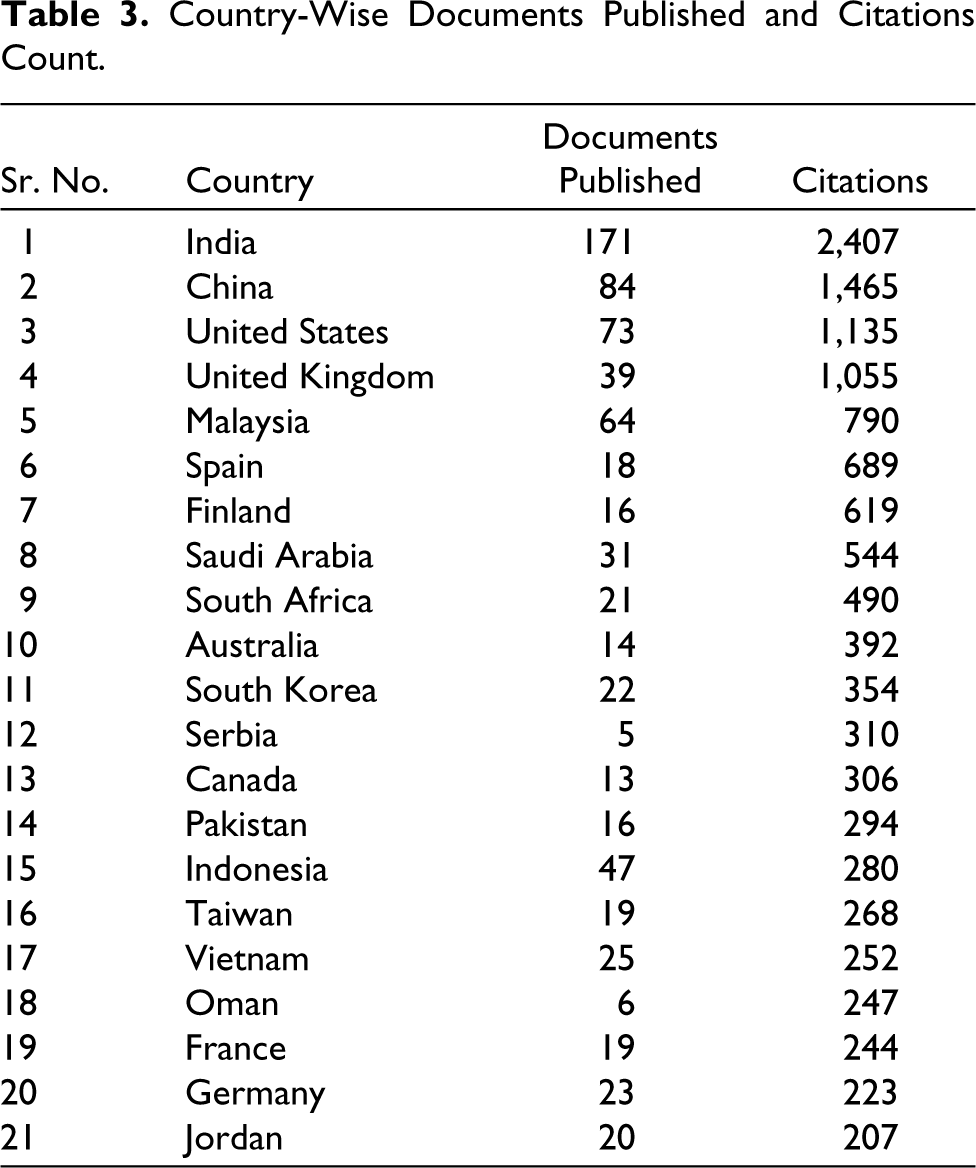

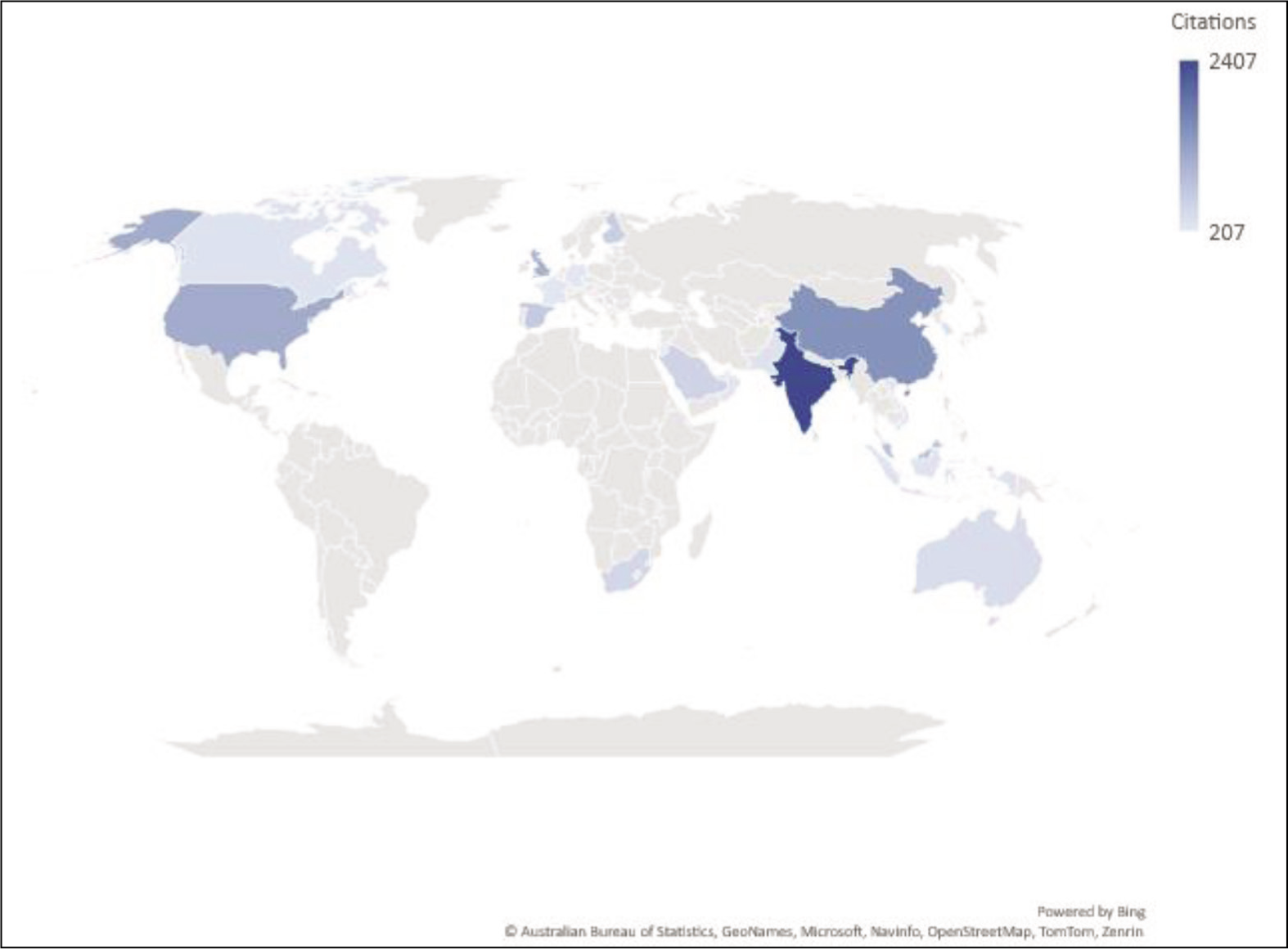

This section discusses the geographical distribution of research papers across the globe. Table 3 represents the top 21 country-wise documents publication count and citations count for countries that have citation scores of 200 or more, and Figure 2 represents the top 21 country-wise citations counts across the globe in different continents that have citation scores of 200 or more. India is at the top position with 171 publications and 2,407 citations, followed by China with 84 publications and 1,465 citations. Brazil and Australia are in the lowest position with 14 publications each. In the case of citation count, Iran and Brazil come at the lowest in the list with 188 and 144 citations respectively. Other countries’ documents publication count and citation count are depicted in Table 3: the United States, United Kingdom, Malaysia, Spain, Finland, Saudi Arabia, South Africa, South Korea, Pakistan, Indonesia, Taiwan, Vietnam, France, Germany, Bangladesh, Jordan, Iran, and Brazil also comes in the top 21 list of countries of highest citations.

Country-Wise Documents Published and Citations Count.

Further, Figure 2 represents how geographically the studies related to digital payments diversify across the different continents. A total of five continents have contributed to the studies related to digital payments. In Asia, a total of 11 countries contributed to the study related to digital payments, namely, India, China, Malaysia, Saudi Arabia, South Korea, Pakistan, Indonesia, Taiwan, Vietnam, Oman, and Jordan. In Europe, a total of six countries contributed to the study related to digital payments, namely, the United Kingdom, Spain, Finland, Serbia, France and Germany. In North America, two countries contributed, namely, the United States of America and Canada. Lastly, Australia contributed from the Australian continent. Therefore, five out of the seven continents contribute to the studies related to digital payments, which is roughly 71% of the total continents, which signifies how vastly the studies related to digital payments are diversified.

Countries-Wise Citation Count of Research Papers.

RQ2: What Are the Themes Associated with Digital Payment Research?

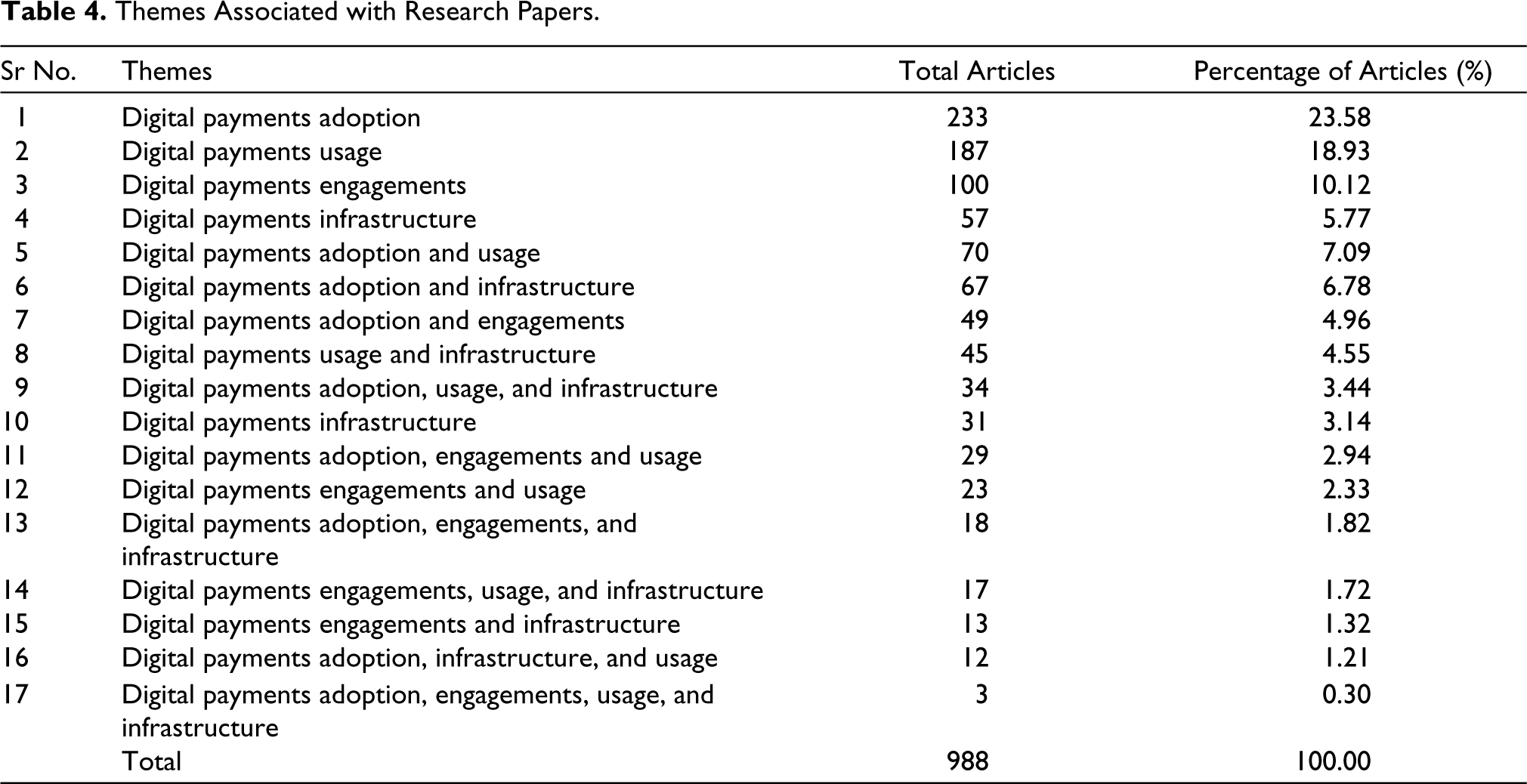

This section discusses the themes associated with digital payment studies. From Table 4, it was found that 23.58% of the studies in the sample size were related to the theme of adoption of digital payment followed by digital payments usage (18.93%), digital payments engagements (10.12%), and digital payments infrastructure (5.77%). Next, 7.09% of studies of the sample size were based on themes of digital payments adoption and usage, followed by digital payments adoption and infrastructure (6.78%), and digital payments adoption and engagements (4.96%).

Themes Associated with Research Papers.

A 4.55% sample size of research papers focused on the theme of digital usage and Infrastructure, followed by adoption, usage, and infrastructure (3.44%). 3.14% studies of the sample size are solely based on the theme of digital payments infrastructure. Next, 2.94% studies of sample size are based on the theme of digital payments adoption, engagements and usage, followed by the theme of digital payments engagements and usage (2.33%), digital payments adoption, engagements, and infrastructure (1.82%), digital payments engagements, usage, and infrastructure (1.72%), and digital payments engagements and infrastructure (1.32%). Finally, the theme based upon adoption of digital payments, infrastructure, and usage comprises 1.21% of the sample size followed by digital payments adoption, engagements, usage and infrastructure at 0.30%. Hence, about 50% of the research papers were associated with the theme of digital payment adoption, digital payment usage, and digital payment engagements, and the majority of the researchers and academicians focused on the adoption, usage and engagement aspects of digital payments.

RQ3: What Research Methodologies Are Adopted in Digital Payment Research?

This section discusses the RMs used in the sample size by various academicians and researchers in their studies related to digital payments. This section is divided into further three subsections,: Research Methods, Research Tools, and Research Analysis Techniques/methods.

Research Methods

In the present study, to describe what research methods are adopted by the various academicians and research scholars in their studies, the authors divided them into three types of research methods, namely, those who used adopted quantitative approach only, those who adopted the qualitative approach only and those adopted both qualitative and quantitative methods. From Table 5, it was evident that a total of 587 research papers comprising 59.41% of the sample size were quantitative in nature. 254 research papers were based on qualitative studies, which is 25.71% of the total research papers. Finally, 147 (14.88%) research papers were based on both quantitative and qualitative (mixed methods) studies. Hence, the majority of academicians and research scholars use quantitative methods in their studies followed by qualitative methods.

Research Methods Used in Digital Payments.

Research Tools

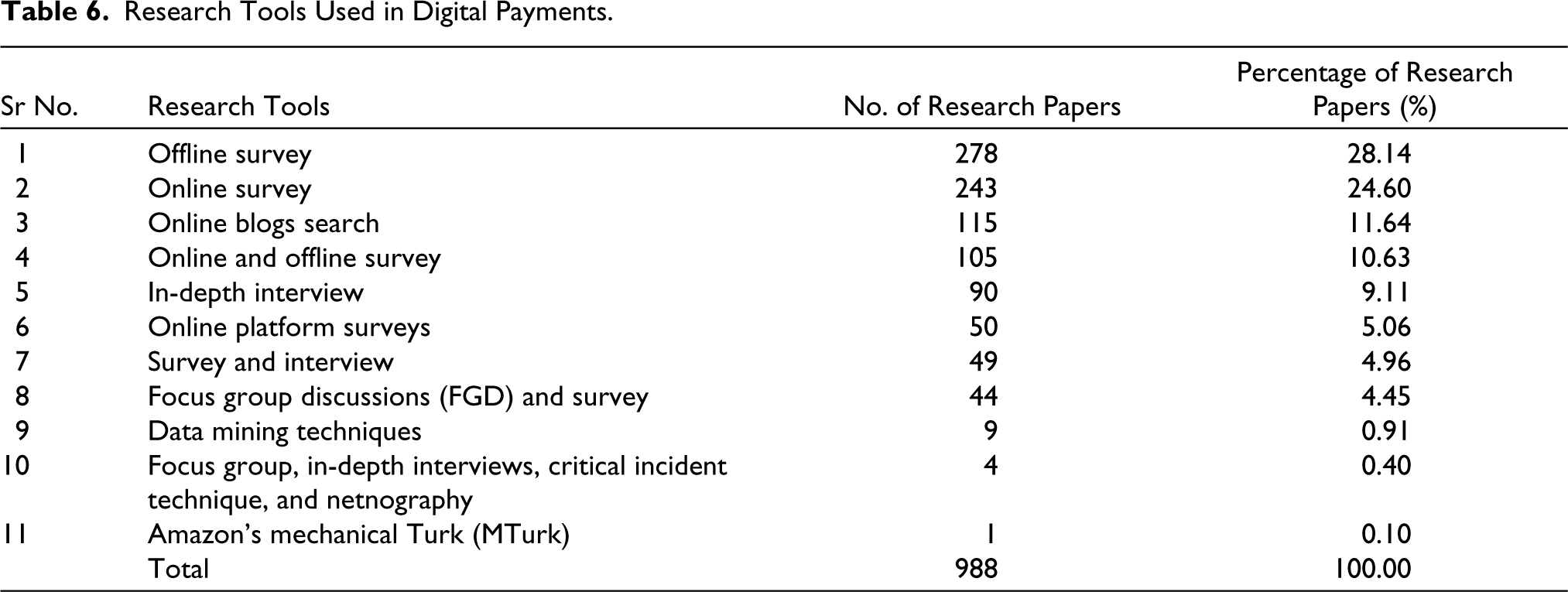

There are many research tools that are used by various academicians and research scholars in their studies, which are described in Table 6. From Table 6, it was evident that the offline survey as a research instrument contributed to 28.14% of the overall studies followed by the online survey (24.60%). Also, online blog search (like Google, Bing, and so on) contributes 11.64% as a research instrument of the sample size. Online and offline surveys are at 10.63%, in-depth interviews at 9.11% and online platform surveys at 5.06%.

Research Tools Used in Digital Payments.

The combination of surveys and interviews contributes 4.96% of the overall sample size, and focus group discussions (FGD) and survey is 4.45%. Further data mining techniques contribute 0.91% followed by focus groups, critical incident technique, in-depth interviews and netnography (0.40%). Lastly, Amazon’s Mechanical Turk (MTurk) as a research instrument contributes only 0.10% of the overall sample size of 988. Hence, more than 50% of the academicians and research scholar had used online and offline survey in their studies as research tools. Moreover, online and offline surveys are used by 10.63% of the ample size.

Data Analysis Techniques/Methods

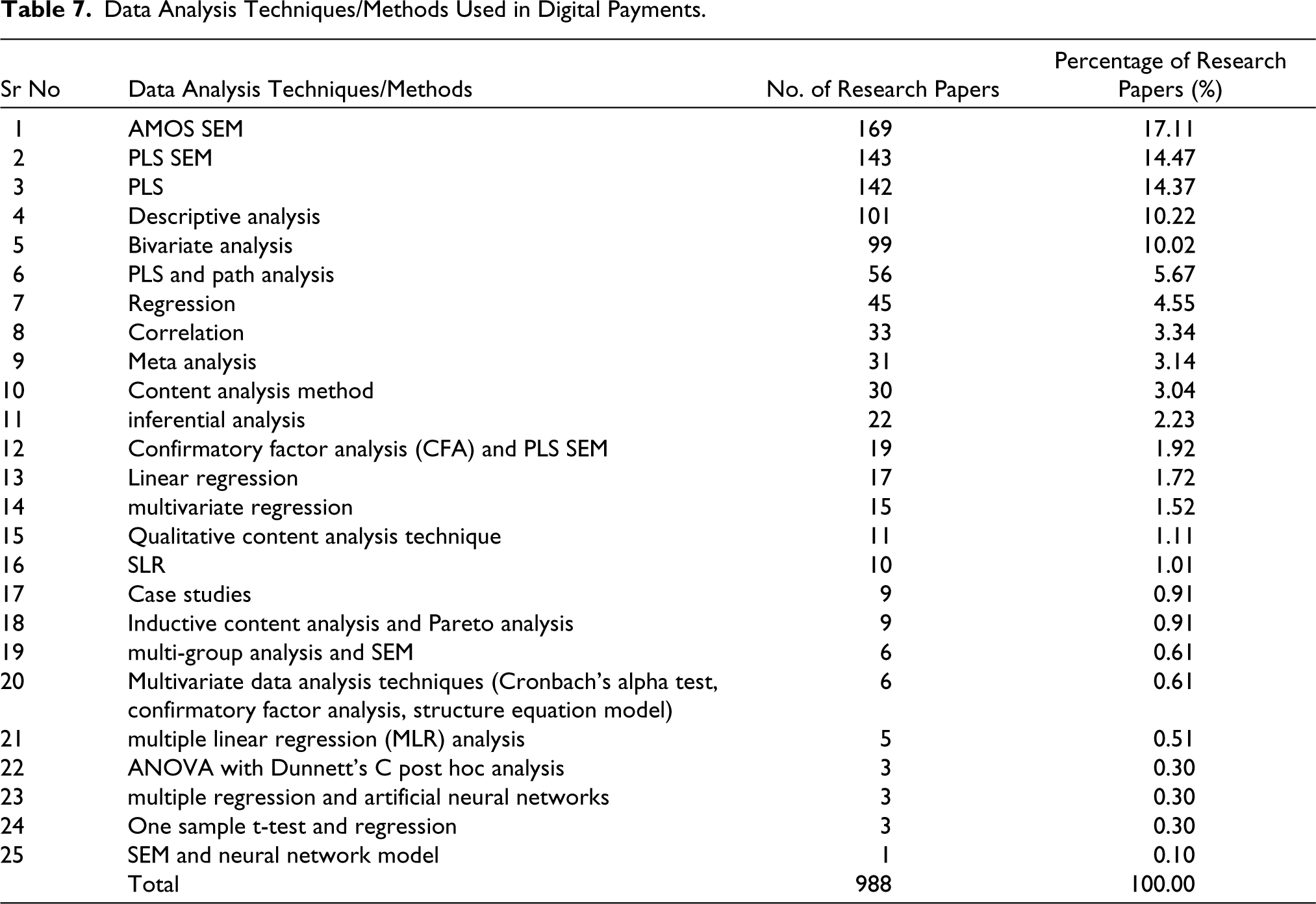

This section discusses the various data analysis techniques or methods used in the sample size by the various academicians and scholars in their studies. Table 7 depicts the data analysis technique or methods used in the sample size of the research papers. From Table 7, it was evident that AMOS structural equation model (SEM) with 169 articles in sample size contribution as a data analysis technique is the highest followed by PLS-SEM (14.47%). Further, partial least square (PLS) contribution is 14.37%, descriptive analysis contribution is 10.22%, and Bivariate analysis as 10.02%.

Data Analysis Techniques/Methods Used in Digital Payments.

A combination of PLS and path analysis contributes 5.67%. Regression, correlation, and meta-analysis as 4.55%, 3.44%, and 3.14%, respectively. Content analysis and inferential analysis contribute 3.04% and 2.33%, respectively, followed by a combination of confirmatory factor analysis (CFA) and PLS-SEM as 1.92%. Linear regression, multivariate regression, and qualitative content analysis techniques contribute 1.72%, 1.52%, and 1.22%, respectively. SLR, case studies, a combination of inductive content analysis and Pareto analysis with 10, 9 and 9 articles, contribute 1.01%, 0.91%, 0.91%, respectively. A combination of multi-group analysis and SEM contributes 0.61% in the sample size.

Multivariate data analysis techniques (Cronbach’s alpha test, CFA and SEM] were contributed by six articles with 0.6%. Multiple linear regression (MLR) analysis and ANOVA with Dunnett’s C post hoc analysis contribute 0.5% and 0.30%, respectively. The combination of multiple regression and artificial neural networks contributes least among the sample size, with 0.30% followed by the combination of One sample t-test and regression with 0.30%. Lastly, the combination of SEM and neural network model contributes the least with 0.10%. Hence, the majority of the researchers and research scholars have referred more sophisticated data analysis techniques or methods (Wilkinson & Birmingham, 2003) in their studies like PLS, SEM, and so on rather than traditional methods like descriptive analysis, correlation, and so on.

RQ4: What Are the Citation Trends in Digital Payment Research?

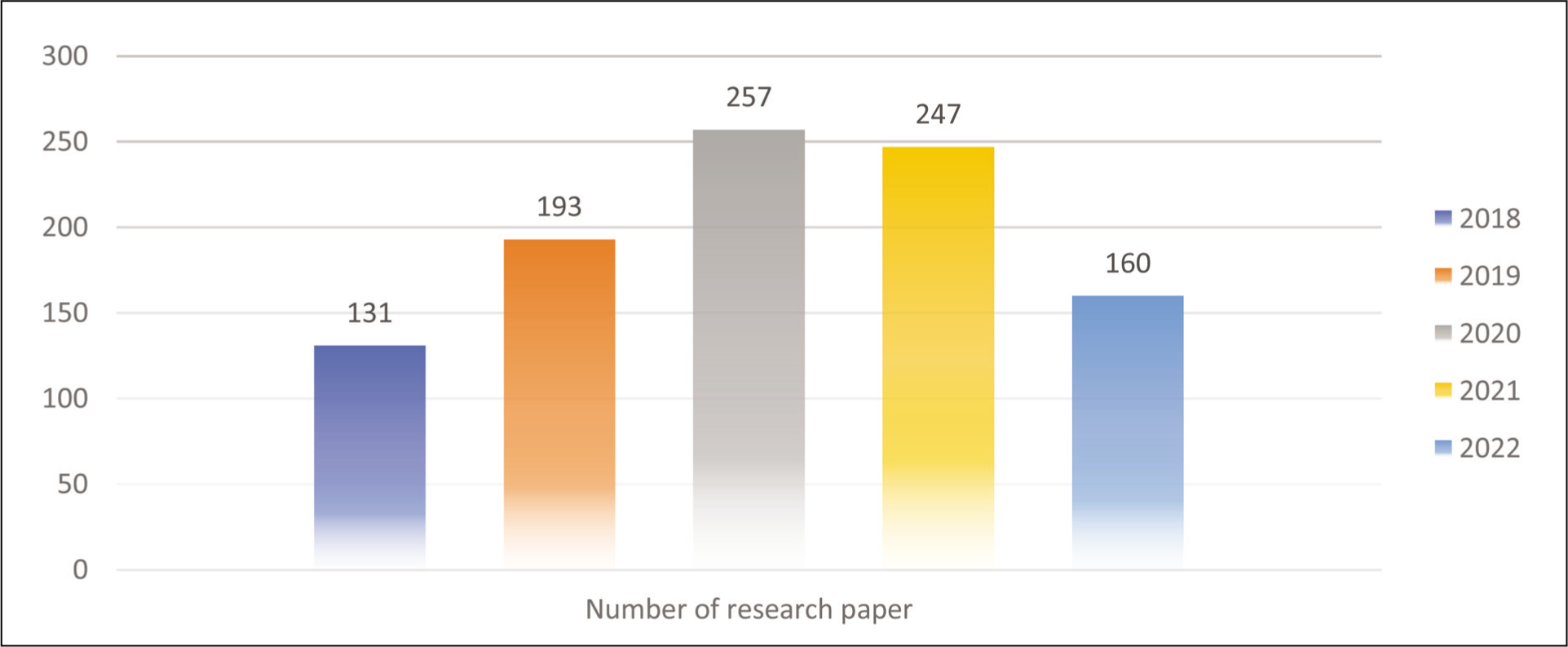

This section discusses the citation trends in the realm of digital payment studies. Figure 3 depicts the number of research papers published in each year from 2018 to 2022 in the research area of digital payments after consideration of inclusion and exclusion criteria. Maximum research papers were published in 2020 with a count of 257, followed by 247 in 2021. A total of 194 research papers were published in 2019. The least number of research papers were published in 2022 and 2018 with a count of 160 and 131, respectively. Hence, the research paper’s publication trend increases at a decreasing rate from 2018 to 2019 and from 2019 to 2020 at the rate of 47% and 33%, respectively. After 2020, the growth rate started decreasing till 2022, as shown in Figure 3.

Year-Wise Publications of Research Papers.

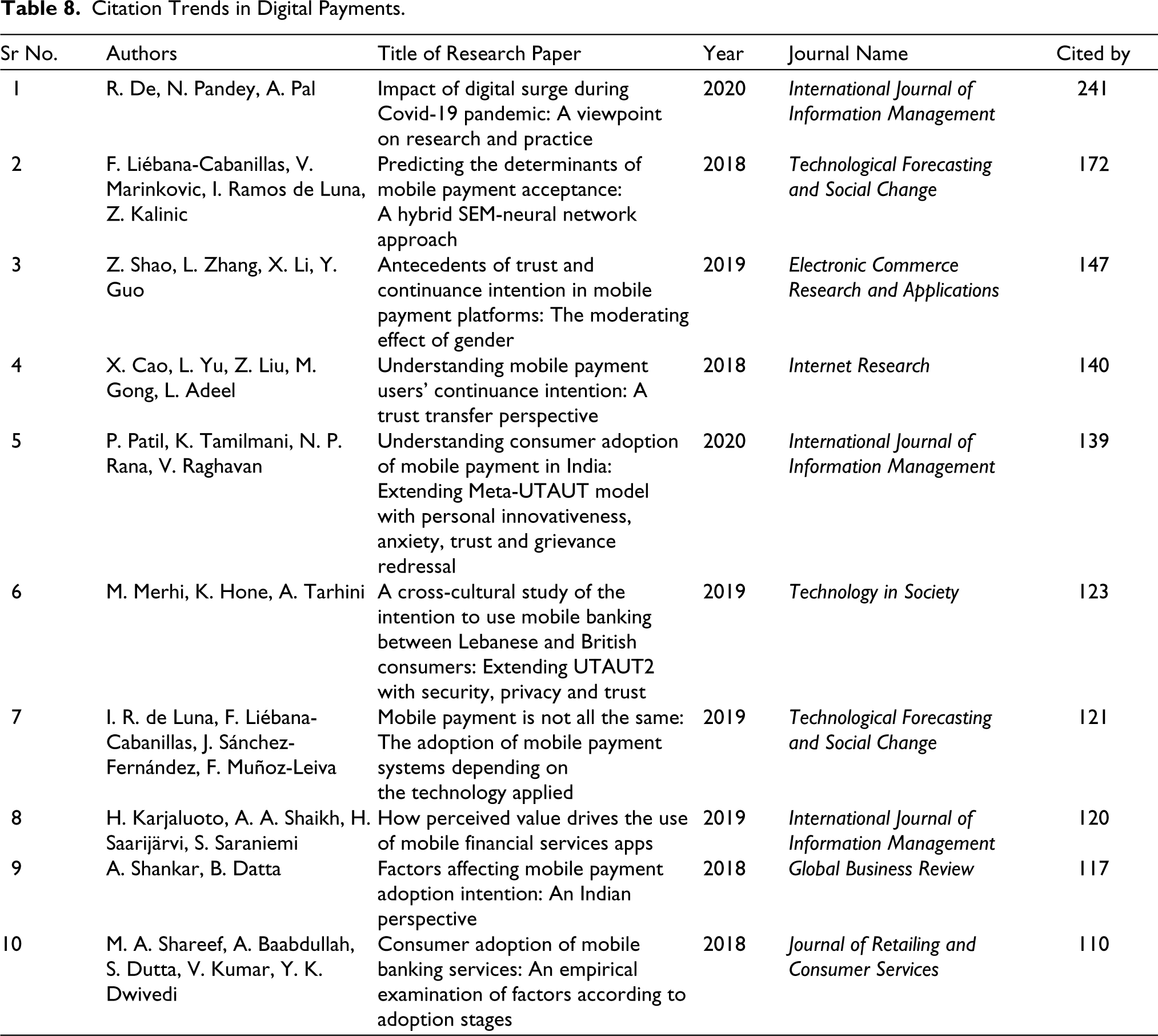

Further, Table 8 depicts the top 10 research papers with the highest citations. “Impact of digital surge during COVID-19 pandemic: A viewpoint on research and practice (2020)” by R. De, N. Pandey, and A. Pal. is one of the top cited research papers. This article explains the effects of the COVID-19 pandemic on digital surge and the consequences for research and practice that arise from it. In the context of the growing usage of the digital technology both during and after the COVID-19 pandemic, the researcher addresses many scenarios and research gaps. Topics such as online fraud, growing digitization, workplace surveillance, gig and remote labour, internet access and the digital divide, internet governance, digital currency, surveillance, and privacy are all covered. The research paper offers implications for practice and emphasises the need for research in these areas.

Citation Trends in Digital Payments.

The second research paper in the list is “Predicting the determinants of mobile payment acceptance: A hybrid SEM-neural network approach (2018)” by F. Liébana-Cabanillas, V. Marinkovic, I. Ramos de Luna, and Z. Kalinic with 172 citations. This research presents a hybrid model of SEM-neural network approach to predict mobile payment adoption variables. With an emphasis on near field communicator (NFC)-based mobile payments, the study examines the variables impacting the uptake of mobile payment systems. The study employs a multi-analytical methodology that integrates artificial neural network (ANN) analysis with SEM to capture complicated nonlinear correlations as well as linear relationships between predictors and dependent variables. According to the study, the tendency to accept mobile payment is significantly influenced by perceived security, perceived utility, individual mobility, compatibility, subjective norms (SN), and perceived usefulness (PU). The theoretical framework, research model, methodology, and research consequences are also covered in this article.

The third research paper in the list is “Antecedents of trust and continuance intention in mobile payment platforms: The moderating effect of gender” by Z. Shao, L. Zhang, X. Li, and Y. Guo. This study examines the factors that affects trust and intention variables to remain engaged with a mobile payment platform, with a particular emphasis on the moderating role of gender. The study focuses on the processes used by third-party mobile payment platforms to establish trust, and it compares the mechanisms used by male and female consumers to establish trust. The study further examines how mobility, security, reputation, and customization affect trust as well as how gender influences the process of forming trust.

The fourth research paper is “Understanding mobile payment users’ continuance intention: A trust transfer perspective” by X. Cao, L. Yu, Z. Liu, M. Gong, and L. Adeel. This article explains the trust transfer process mechanism from online to mobile payments and how it affects users’ satisfaction and desire for continued engagement with mobile payments. Through information gathered from 219 customers of a well-known Chinese payment company, the study model is empirically evaluated. The finding shows that user satisfaction is positively impacted by trust in digital payment, and that user satisfaction in turn influences the intention of users to continue using mobile payment. The study also takes into account how users’ trust, contentment, and intention to continue using a service are affected by demographic variables like age, gender, education, and usage history.

The fifth research paper is “Understanding consumer adoption of mobile payment in India: Extending Meta-UTAUT model with personal innovativeness, anxiety, trust,, grievance redressal” by P. Patil, K. Tamilmani, N. P. Rana, and V. Raghavan. To better understand how Indian consumers are adopting mobile payments, this article extends the Meta-UTAUT model to include grievance redressal, trust, anxiety, and personal innovativeness. The study’s primary goal is to ascertain the key variables that affect Indian consumers’ adoption of mobile payments, such as social influence (SI), performance expectancy (PE), intention to use, attitude, facilitating conditions, and grievance resolution. In addition, the study examines usage patterns and offers insights into the variables affecting Indian customers’ perceptions and actions concerning mobile payment systems. The study enhances the information regarding the adoption of mobile payments and offers useful advice for mobile payment service providers.

The sixth research paper is “A cross-cultural study of the intention to use mobile banking between Lebanese and British consumers: Extending UTAUT2 with security, privacy, and trust”. This article discusses a cross-cultural investigation that focuses on potential barriers to and enablers of mobile banking service adoption in England and Lebanon. Three new constructs—privacy, trust, and security—are added to the Unified Theory of Acceptance and Use of Technology (UTAUT2) in this study. SEM, based on AMOS 23.0, was used to analyse the data. The findings concludes that both Lebanese and English consumers’ behavioural intention towards the use of digital payment services was affected by habit, trust, perceived security, and perceived privacy.

The seventh research paper is “Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied” by I. R. de Luna, F. Liébana-Cabanillas, J. Sánchez-Fernández NS F. Muñoz-Leiva. This article discusses the acceptability and adoption of mobile payment systems, emphasising on the variables that affect consumers’ willingness to adopt various technologies like NFC, SMS, and QR codes. The significance of attitude, ease of use, SN, PU, and perceived security in influencing customer behaviour towards digital payment systems is also covered in the article. The results concluded that the interactions among these variables differ based on the particular payment system under consideration. The study, which was carried out in Spain, offers suggestions to organizations and regulators as well as insights into the factors that influence the adoption of mobile payments.

The eighth research article is “How perceived value drives the use of mobile financial services apps” by H. Karjaluoto, A. A. Shaikh, H. Saarijärvi., and S. Saraniemi. This study dicusses the relation between the use of mobile financial services apps and perceived value. It focuses at the factors that influence customers’ overall interactions with banks, including perceived risk (PR), self-congruence, personal innovativeness, and novelty in new products. According to the findings, perceived value is mostly influenced by self-congruence and novelty of the new product. Investing in the creation of mobile financial services apps can enhance customer satisfaction and boost bank revenue.

The ninth article is “Factors affecting mobile payment adoption intention: An Indian perspective” by A. Shankar, and B. Datta. This research paper utilizes a conceptual framework based on the technology acceptance model (TAM) model enhanced with four characteristics to examine factors impacting the adoption of mobile payments in India. 381 potential mobile payment consumers provided information through offline and online surveys, which were subsequently analysed using SEM analysis. The results concluded that intentions to use mobile payments are positively influenced by perceived utility, trust, and self-efficacy. However, adoption intention is not considerably impacted by SN or personal innovativeness.

The tenth article is “Consumer adoption of mobile banking services: An empirical examination of factors according to adoption stages” by M. A. Shareef, A. Baabdullah, S. Dutta, V. Kumar, and Y. K. Dwivedi. This article describes the quantitative analysis of the behavioural intents of consumers to usage of mobile banking systems during three different service stages: transaction, interaction, and static. The study offers significant theoretical contributions to the domain of consumer mobile banking services adoption by examining the elements that impact consumers’ behavioural intentions at each stage.

The most highly cited research papers offer in-depth analyses of the adoption of digital payments. They extend well-known models such as UTAUT and Meta-UTAUT by looking at elements like trust, security, and continuance intention. These studies also investigate cultural differences and the impact of the COVID-19 pandemic on digital innovations. The diversity of the digital payment landscape is highlighted by the topics explored, which include workplace surveillance, online fraud, and the digital divide. These studies greatly advance our knowledge of the factors influencing and impeding the broad use of digital payment systems by their thorough analysis and empirical data.

RQ5: Which Models and Theoretical Concepts or Frameworks Are Used Frequently in Digital Payment Research?

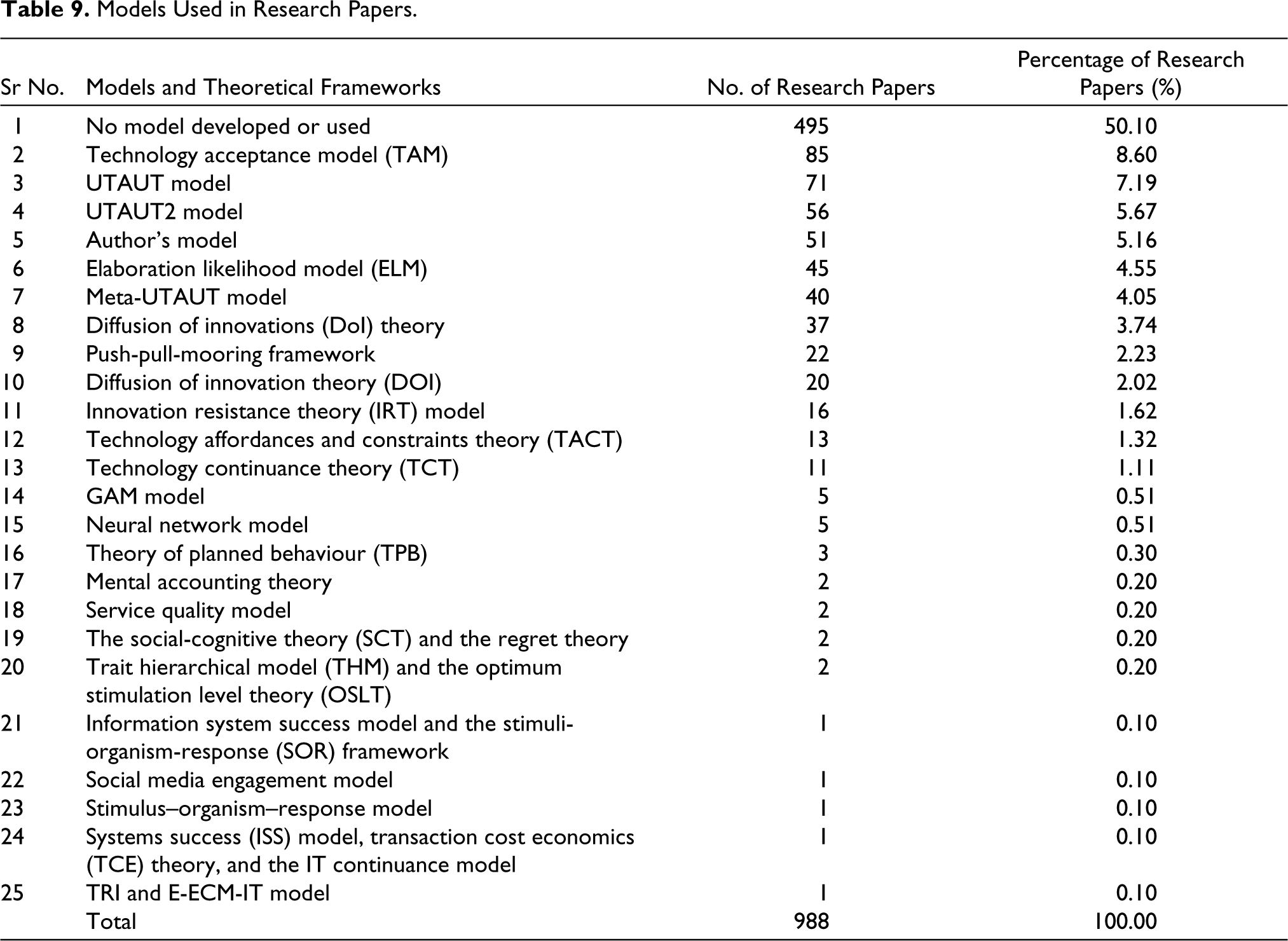

This section discusses the various models and theoretical concepts or frameworks used in the sample size by various academicians and research scholars in their studies. Table 9 depicts the various models and theoretical frameworks used in the sample size. In more than 50% of the sample size, the researchers did not use any model or theoretical framework in their studies. 5.67% of the authors have developed their own model and theoretical framework The remaining researchers extended existing theories or tested and validated them within their various sampling universes, frames, and units of study in their studies.

Hence about 50% of the researchers did not use and develop any model and 50% used various models to describe their research studies. (TAM is considered the most frequently and widely used framework with 8.60%, followed by the UTAUT model and UTAUT2 model with 7.19% and 5.67%, respectively. Other models that are used are delineated in Table 9.

Models Used in Research Papers.

Factors Affecting the Digital Payments Adoption

This section discusses the factors that describe the digital payments adoption concept across the nations. This section is divided into two sub-sections. The first section describes those factors that enhance the adoption of digital payment, called as “drivers”. The second section describes those factors that hinder the adoption of digital payment, referred to as “inhibitors”.

Drivers Factors

From the review of research papers in the sample size, PE (Chandrasekhar & Nandagopal, 2016; Koenig-Lewis et al., 2015) from the UTAUT model and PU (Chandrasekhar & Nandagopal, 2016; Gao & Waechter, 2017; Koenig-Lewis et al., 2015) from the TAM model are the most significant driver factors that explain the adoption concept of digital payment (Augsburg & Hedman, 2014). SI (Liébana-Cabanillas et al., 2014), and perceived enjoyment (PE) (Liébana-Cabanillas et al., 2014) are also the driver factors that enhance the adoption of digital payments. Other studies (Berrado et al., 2013; Kim et al., 2016; Liébana-Cabanillas et al., 2014; Pliskin et al., 2012) state that perceived ease of use (PEOU) is also one of the “driver factors” for digital payment adoption. Interesting lifestyle (Keramati et al., 2010) is also one of the factors that comes in the category of driver factors. Apart from the aforementioned factors such as external influences like SN (Oliveira et al., 2016) and SI (Staykova & Damsgaard, 2016) also affect the adoption of digital payments positively. Trust factors (Gao & Waechter, 2017) like perceived information quality, perceived system quality and perceived service quality also impact digital payments positively. Perceived benefits (PB) (Lee et al., 2015) and emotional trust (ET) (Gong et al., 2016) also enhance the adoption of digital payments.

Inhibitors Factors

PR (Koenig-Lewis et al., 2015; Pham & Ho, 2015; Pliskin et al., 2012; Slade et al., 2014) is the most significant factor that acts as an inhibitor for the adoption of digital payments. Perceived uncertainty (PU) (Augsburg & Hedman, 2014) also affects the adoption of digital payments negatively. Apart from the aforementioned factors, informational privacy (IP) (Keramati et al., 2010) network externalities (Keramati et al., 2010), and security concerns (Keramati et al., 2010) also act as inhibitors to digital payments adoption process.

Discussions

The Emergence of China and India in the Realm of Digital Payment Studies

In this study, we examined the geographical distribution of the research papers along with the citations, research papers’ authors and journals, RM, and themes associated with research papers from 2018 to 2022 by considering the selection criteria. It was found that India is at the top in terms of most publications of research papers, that is, 171 with 2,407 citations, followed by China with 84 publications and 1,465 citations, as shown in Figure 2. It is evident from this research that these two developing countries are showing acceptance in the field of digital payments. There were other countries like the United States of America (73 publications), Malaysia (64 publications), Indonesia (47 publications) and the United Kingdom (39 publications) with 1,135, 790, 280, and 1,055 citations, respectively. Pakistan and Bangladesh with 16 and 15 publications respectively also come in the top 20 list of countries with higher publications with 294 and 194 citations respectively. These two countries are also in the developing stage and it is quite encouraging for them as they are doing research in the field of digital payments. Countries like Saudi Arabia, Germany, Taiwan, and South Africa are also in the top 20 list, which indicates that research on the area of digital payments is spreading all over the world and is becoming a good area of interest for scholars and academicians.

Excessive Dependence on Quantitative Methods

Research Methods

This study revealed that the widely used method in most of the studies is the quantitative method (59.49%) followed by the qualitative method (25.71%). The mixed method, that is, the combination of both quantitative and qualitative methods, is adopted by 14.88% of the sample size taken for this study. This study supports the study of Sahi et al.’s (2021) finding regarding the research methods adopted in the study.

Research Instruments

In this study, the research has found that the most preferred research instrument for conducting research is a survey. An offline survey is adopted by 28.14% followed by an online survey (24.60%). Both these instruments were adopted by more than 50% of the sample size. Other methods include in-depth interviews, online platforms surveys, FGD)and surveys, data mining techniques, and so on that are also adopted by many authors. This indicates that many authors are also adopting many innovative research instruments to study the behaviour of respondents as suggested by Kabir et al. (2015).

Data Analysis Tool

SEM is one of the most frequently used data analysis tools used by researchers in their study of our sample size. AMOS SEM is used by 17.11% of the sample followed by PLS-SEM with 14.47%. PLS is used by 14.37% of the researchers. SEM estimates two things: first, the measurement model, and second, the structural model (Ullman, 2006). The relationship between the latent variable and the observed variable is explained by the measurement model and the flow of relationships, to identify the strength between them and to analyse the data done by the structural model.

Themes of the Research

Themes based on adoption (23.58%) and usage (18.93%) are the top two themes on which the researcher has focused in the last five years from 2018 to 2022. The next two themes are engagements (10.12%) and infrastructures (5.77%). These four themes constitute more than 50% of the overall research done between 2018 to 2022. The other half of the research papers were focused on the combinations of these themes. Digital payment engagements and infrastructure theme research papers are relatively low in percentage and further research is needed in this field. Also, it was found that most research papers were focused on the adoption side of consumers, thus, future research also needs the seller’s or marketer’s perspectives.

Model and Theoretical Framework

The authors have found that nearly 50% did not use any theoretical models or frameworks to explain their studies. About 5% of researchers have developed their own model. The TAM and UTAUT are the most preferred models in our sample size. The reason behind this could be the study of attributes related to the adoption and inhibitors of digital payments. Other models are also used, but they are only around 23% of the sample size.

Academic Contribution of the Study

This article aims to provide a new comprehensive systematic literature in the realm of digital payments. In essence, the research enhances scholarly discussions on digital payments by offering insights into prevailing research methodological preferences, global research trends and theoretical frameworks. It delineates areas of gaps and challenges within the domain, presenting a strategic direction for forthcoming research endeavours that encourage more thorough and in-depth studies. The study provides he possibilities for future developments in the field and contributes to the scholarly understanding of digital payment dynamics through its analysis and recommendations.

Conclusion

The COVID-19 scenario and the advancement in digital technologies have encouraged many consumers to use digital payment as a new way to spend their money, which is easy to use and hassle-free as compared to cash. The offers given by marketers also encourage the consumer to use more digital payments, and hence it is essential to explore this field of research. In this study, we have analysed the geographical distribution of various research papers published, research methods, techniques, and tools, themes associated with research papers and citation trends from 2018 to 2022 by considering the selection criteria. Further, in this study, factors affecting the adoption of digital payments were also explored. This research will enhance the existing literature and fill the unexplored and unanswered gaps, and will give new dimensions in future research. This study has provided a direction to future academicians strategic direction in which they should focus their studies.

While this review offers a condensed overview of mobile payment adoption studies, it is essential to consider its insights within the context of the following limitations. Only a subset of the research papers has been used to find out the factors that affect the adoption of the digital payments; remaining studies can be used to find out if there are any other inhibitors and driver factors that need to be explored. The other limitation of the current study is that this study only includes the adoption perspective of the consumers, and it does not include the stakeholder adoption and organizational adoption. Future studies should include the other perspective of adoption of digital payments.

Future Direction and Thrust Areas of Digital Payments

After reviewing and analysing research papers, we have identified several gaps that have been addressed in this section. First, due to the COVID pandemic, there is a huge impact on consumer buying behaviour, and lots of further exploration is required to get new insight from the consumer. Second, there are so many studies that are dependent on quantitative data, and future research should be focused on both qualitative and quantitative data that can give better results and provide a broader perspective of the consumers. Third, there are so many researches who are focused on the consumer perspective, but there are hardly any studies that are focused on the marketer or seller perspective. There is a need for research in this direction also. Fourth, many studies have focused on one or two digital payment instruments, but a coalition of two or more digital payment instruments is missing in many studies. Fifth, there are so many studies on the theme of digital payment adoption and usage, but to create more sophisticated solutions for the problems, future research should also focus on the dimension of infrastructure and engagement perspective of digital payments. Sixth, studies should also focus on the role of government bodies in the area of digital payments. Seventh, comparative studies are required in future research for a better understanding of the needs of the consumer.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.