Abstract

In the evolving landscape of financial markets, technical analysis remains a cornerstone for traders seeking to gain an edge. This article presents a comprehensive analysis of two pivotal technical indicators: the Relative Strength Index (RSI) and Moving Averages (MA). Through meticulous research, we dissect the intricacies of these indicators, evaluating their predictive power and effectiveness in various market conditions. Our study employs a robust methodological framework, incorporating historical data analysis, algorithmic testing, and behavioural finance perspectives to assess the utility of RSI and MA in unlocking trading insights. We reveal how the RSI’s overbought and oversold signals, when combined with MA’s trend-following properties, can be harmonized to refine entry and exit strategies. The article also explores the adaptability of these indicators in the face of market volatility and the potential for enhanced performance through algorithmic integration. Our findings suggest that while RSI and MA are potent tools individually, their combined application can significantly bolster trading strategies. This research not only enriches the existing body of knowledge but also provides practical frameworks for traders aiming to optimize their technical analysis toolkit.

Introduction and Background

Technical analysis plays a crucial role in modern trading strategies, offering traders a means to analyse historical price data and make informed decisions about future price movements. It involves the use of various technical indicators and chart patterns to identify potential trading opportunities. Among the multitude of technical indicators available, two widely used ones are the Relative Strength Index (RSI) and Moving Average (MA) indicators. The RSI is a momentum oscillator that measures the speed and change of price movements. It is primarily used to identify overbought and oversold conditions in the market. According to Wilder (1978), the RSI compares the magnitude of recent gains and losses over a specified time, typically 14 days by default, and generates values ranging from 0 to 100. This indicator is valuable for traders seeking to gauge the strength of a trend and potential reversal points in price action. On the other hand, the MA indicator is a trend-following technical tool that smooths out price data by calculating the average closing price over a specific period. It aids traders in identifying the direction of the prevailing trend and potential support or resistance levels. MAs come in various forms, including simple moving average (SMA), exponential moving average (EMA), and weighted moving average (WMA), each with its unique calculation method and sensitivity to price changes.

In the intricate tapestry of financial markets, traders and investors are perpetually in pursuit of strategies that can provide a competitive advantage. Amidst the myriad of analytical tools available, technical analysis stands out as a beacon for those navigating the tumultuous seas of market speculation. This article delves into the heart of technical analysis, focusing on two of its most revered navigational instruments: the RSI and MA.

The genesis of technical analysis can be traced back to the early seventeenth century, evolving through the ages as traders sought to predict future market movements based on historical price patterns. The RSI is a momentum oscillator that measures the speed and change of price movements (Wilder, 1978). It has become an indispensable tool for identifying overbought or oversold conditions in a market. On the other hand, MAs, which smooth out price data to create a single flowing line, have been the cornerstone of trend-following strategies.

The convergence of these two indicators, RSI and MA, offers a powerful lens through which traders can decipher market sentiments and dynamics. This article aims to unlock the trading insights hidden within the interplay of RSI and MA, providing a comprehensive analysis of their predictive power and effectiveness. By examining their performance across various market conditions and integrating algorithmic approaches, we seek to offer traders not just a theoretical understanding but a practical framework to enhance their trading acumen.

Through this research, we aspire to contribute to the rich tapestry of financial literature, offering fresh perspectives on the use of RSI and MA in modern trading. It is a journey into the very fabric of market psychology, where numbers and charts whisper the secrets of future market directions to those who dare to listen. Hence the primary objective of this study is to evaluate the effectiveness of RSI and MA indicators in enhancing trading strategies through a methodical analysis, incorporating historical data, algorithmic testing, and behavioural finance insights.

Review of Literature

In order to achieve the study’s goal, a brief review of the literature was carried out. It was found that there are few studies on topics such as market volatility, algorithmic integration, RSI, MA, and technical analysis. At the forefront of this quest are technical indicators that serve as the compasses and maps for traders worldwide. The present study aims to investigate two navigational tools, specifically the MA and the RSI.

Rodríguez-González et al. (2011) addressed the pursuit of accurate stock price prediction that has led to the investigation of many approaches, with a particular emphasis on the RSI within the context of technical analysis. CAST’s innovation, which employs artificial intelligence and feedforward neural networks, offers a significant advancement in the refinement of RSI calculation, known as iRSI. This improvement promises more accuracy in anticipating market movements, as demonstrated by its successful application to the Spanish IBEX 35 index and its constituent companies. However, Pramudya and Pramudya (2020), explored the conceptual clarification on technical analysis; indicators such as moving average convergence and divergence (MACD), Bollinger Bands (BB), and RSI have been intensively researched. According to research, although the MACD provides a comprehensive perspective of market momentum, it may be slower to predict timely buy and sell points than the BB and RSI. Bollinger Bands have been acknowledged for their ability to efficiently capture sell signals, especially in tumultuous markets. However, studies show that RSI alone may not always precisely reflect market circumstances, necessitating the usage of a variety of indicators to improve precision in trading decisions. Besides this, Alalaya and Alawad (2018) opined that technical analysis integrates historical data with trade volume and price changes in stock market forecasting by utilizing many techniques such as the MACD, RSI, and EMA. These indicators produce predictions that are more accurate, thanks to computer methods such as support vector machines and neural networks. Combining conventional methods with algorithmic strategies improves forecasting accuracy, which is essential for making wise investment choices in volatile markets. The problems of parameter setting were overlooked in past studies (Kuo & Chou, 2021), and this work presented a novel method of using MAs in trading methods. It pioneers a dynamic and intelligent framework by utilizing EMAs and WMAs and a global best-guided quantum-inspired tabu search algorithm with a two-phase sliding window for strategy optimization. The findings of the experiment suggest that it performs better than conventional techniques and can be profitable in developed as well as emerging stock markets. Along with understanding about parameter settings, the stoke market analysis is crucial for investment. Hence, Hari and Dewi (2018), emphasized how crucial stock market analysis tools are for assisting investors in making well-informed decisions about which stocks to purchase and sell, including the MA and the RSI. Scholars underscore the importance of investors comprehending the relationship between elevated profits and elevated risks, a crucial facet that is frequently disregarded by the industry. The unpredictability of stock price volatility highlights the necessity for cautious interpretation and decision-making, even when these techniques provide insightful information. Also, Lutey (2022), mentioned that technical indicators have been shown to be more successful in trend-following tactics than the conventional buy and hold method in recent research on the subject. Bollinger Bands and the RSI have both underperformed MA indicators, which have demonstrated the highest returns. According to research, BB and RSI produce positive returns as well, although they are not as reliable as MA in different portfolio deciles based on size and volatility. Furthermore, BB and RSI indicators’ resilience is preserved under various parameter and entry configurations, confirming their usefulness in financial market analysis. Khand et al. (2019) explored technical analysis in developing markets—more especially, the stock market in Pakistan. The effectiveness of technical trading principles, such as the EMA, MACD, RSI, and momentum, in this particular context has been the subject of limited prior research. The predictive and profitable qualities of these rules—especially in times of financial crisis—are empirically supported by this research. Even after taking transaction costs into consideration, the results highlight the importance of these technical indicators in generating higher profits. This emphasized that the indicators of technical analysis, such as the RSI, BB, and MA, are frequently used to forecast changes in stock prices. Previous research has disputed these measures’ usefulness in different market environments. The present study adds to the existing body of literature by investigating the accuracy of the LQ45 index in the Indonesian stock market from February to July 2021. The study’s conclusions point to no discernible difference between expected and actual stock price changes, with RSI turning out to be the most accurate of the three indicators (Daniswara et al., 2022). The importance of technical indicators such as the MACD and RSI on stock performance has been demonstrated by recent studies. Both RSI and MACD alone have a favourable and considerable impact on stock performance, according to research done on finance companies listed on the Indonesian Stock Exchange (IDX). Furthermore, these variables have an even greater impact on stock performance when they are controlled by the debt-to-equity ratio (DER). For more reliable investing strategies, these findings highlight the need of combining technical analysis with financial leverage measurements (Wijaya et al., 2021. It was investigated that the importance of technical analysis for short-term stock price prediction has been emphasized in recent research, especially in high-frequency trading. Research contrasting the effectiveness of technical indicators—such as the MACD and the RSI—shows how differently they affect trading tactics. Studies show that the MACD encourages frequent trades, raising transaction costs, while the RSI produces fewer, longer term indications. The best way to combine trading frequency and transaction costs and increase profits in erratic markets is to integrate both the RSI and MACD signals (Panigrahi & Pandey, n.d.). Hasan et al. (2024) in their recent studies on the IDX’s manufacturing sector assess the efficacy of technical analysis methods with particular attention to the MA, MACD, and RSI indicators. Compared to the MA (58% accuracy, 101% return) and the MACD (55% accuracy, 161% return), the RSI showed better signal accuracy (92%) and return on investment (ROI) (238%). The results highlight the RSI’s consistent capacity to provide positive returns, indicating that it should be the main factor considered when making investments. The study emphasizes the necessity of thorough market analysis and the evaluation of extra indicators in order to develop well-informed investing plans. The study revealed that the use of data analytics, mathematical computations, quick execution capabilities, and automated algorithmic trading has emerged as a critical tool for reducing human biases and improving stock trading decision-making. An innovative method in trading methods is to combine sentiment analysis from financial news with several technical indicators, such as the EMA and RSI. While single indicators have been the subject of previous research, this combined approach using Python’s vector module showed a greater success rate, 88% for the S&P 500 index. An 84% accurate bidirectional encoder representations from transformers for natural language processing (BERT NLP) model was used in sentiment analysis, and real-time testing through the Alpaca API produced a 6.26% ROI over a six-month period (Mehra & Shetty, 2024). The stock market forecasting, technical analysis—MAs in particular—is frequently employed to pinpoint trends and important price points. Despite their effectiveness, MAs are lagging indicators, typically indicating changes only after notable fluctuations in price. Recent work attempts to apply machine learning methods to improve these indicators’ effectiveness. This strategy addresses the inherent delays in existing methods by adding regression models to MAs in an effort to improve trend reversal prediction and decrease signal latency (Dinesh et al., 2021). The effectiveness of active trading techniques versus more passive tactics has been the subject of renewed debate in recent studies because of behavioural finance and fresh evidence that challenges the efficient market hypothesis. Moving average regulations were shown to be significantly more profitable in emerging markets, according to a study that examined data from 1989 to 2003 in 15 emerging and 3 developed markets. Longer MAs in these markets also continued to be profitable for MA rules, suggesting persistent patterns. This implies a notable distinction in the return patterns of developing and developed markets, which could have consequences for the efficacy of trading strategies (Fifield et al., 2008). The MA-based trading rules through particle swarm optimization. By optimizing long/short durations for the golden cross strategy, the article aims to maximize trading profits. Real-world indices from diverse stock markets validate the effectiveness of this approach over a three-year period. The proposed method offers a valuable contribution to technical analysis strategies for investors (Kwok et al., 2009).

Previous studies have provided more details on the advantages and disadvantages as well as the accuracy of technical analysis indicators. However, there are discrepancies in the study results that point to unequal accuracy results when using technical indicators such as the MA and RSI. This study examines the accuracy of the two technical analysis methodologies utilizing a novel test between the indicator’s price prediction signal and the actual price in order to close this gap in the literature.

Methodology and Approach

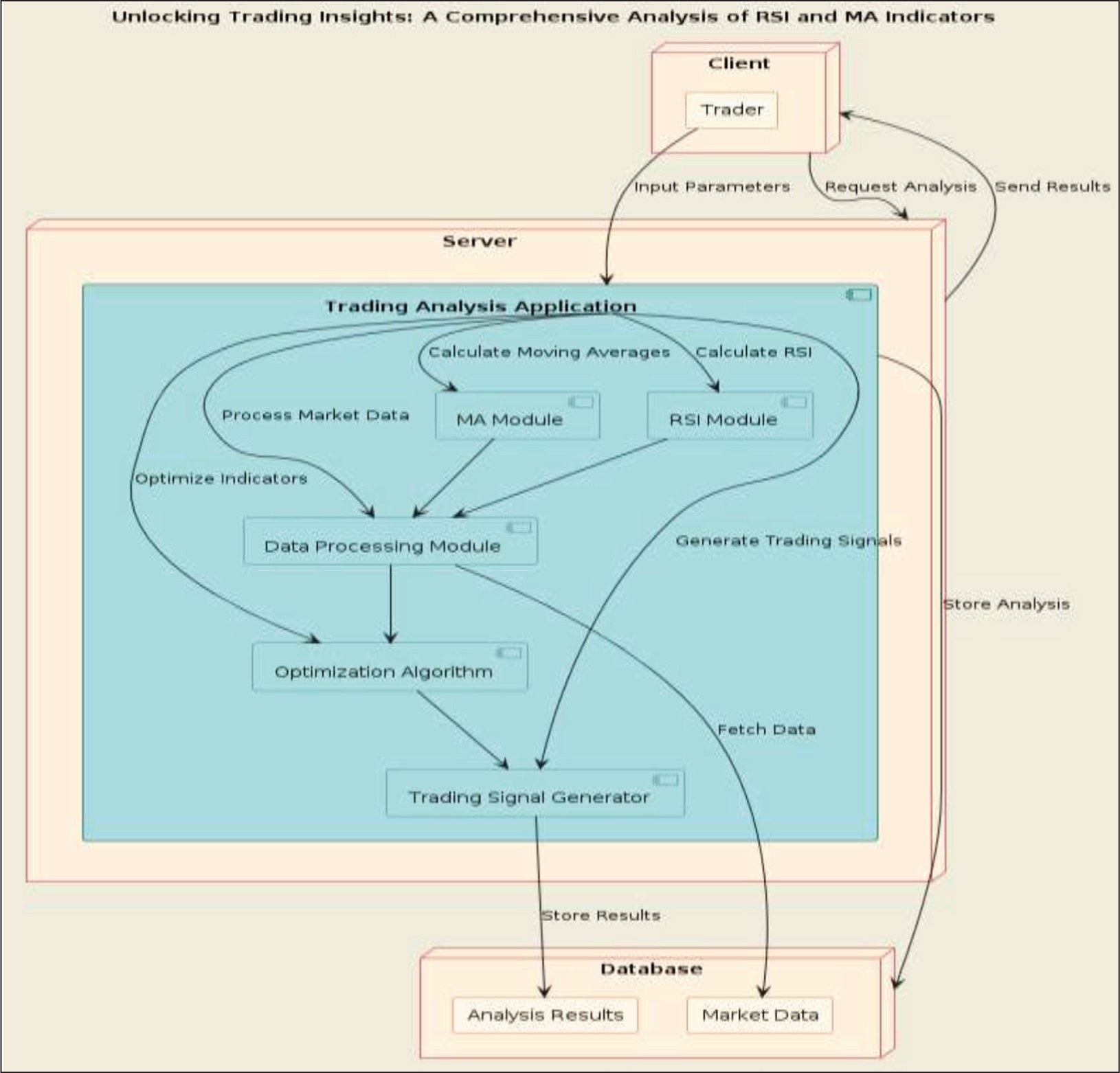

Using technical indicators on past stock prices, such as the RSI and MA, is part of the unique strategy that is suggested in Figure 1. Several stocks from different countries’ market sectors are used to backtest this technique. An NLP model is created that uses the BERT language model to categorize daily news sentiments and ultimately provide investors with a signal on whether to purchase or sell shares in order to increase the strategy’s dependability.

Approach for developing a model.

The deployment diagram represents the architecture of a trading analysis system designed to unlock insights using the RSI and MA indicators. The diagram consists of three primary nodes: client, server, and database, each interacting with specific components to perform the analysis.

Client Node

Trader: The trader represents the end user who interacts with the trading analysis application. The trader inputs parameters such as stock symbols, time frames, and other preferences to initiate the analysis.

Server Node

Trading analysis application: This core component is hosted on the server and contains several submodules.

RSI module: It is responsible for calculating the RSI based on the input parameters and market data.

MA module: It calculates MAs, another key indicator used in technical analysis.

Data-processing module: It processes the raw market data, making it suitable for further analysis by the RSI and MA modules.

Optimization algorithm: It utilizes techniques like particle swarm optimization to fine-tune the parameters for the RSI and MA indicators to maximize trading profits.

Trading signal generator: It generates buy/sell signals based on the optimized indicators and analysis results.

Database Node

Market data: It stores historical and real-time market data necessary for performing the analysis.

Analysis results: It stores the results of the analysis, including optimized parameters and generated trading signals.

Interaction Flow

The trader initiates a request for analysis by providing input parameters to the trading analysis application. The application retrieves market data from the database through the data-processing module, which processes the data to make it suitable for analysis. The RSI module calculates the RSI based on the processed market data, while the MA module calculates the MAs. The data-processing module ensures that the calculated data are in a format suitable for optimization. The optimization algorithm then optimizes the parameters for the RSI and MA indicators to identify the best trading strategies. The trading signal generator uses the optimized indicators to generate trading signals (buy/sell recommendations). The generated signals and analysis results are stored in the analysis results database. The trading analysis application sends the final results back to the trader, completing the request.

Technical Indicators

Technical indicators are statistical computations used to analyse past stock data in order to identify patterns and trends in price. Positive entry and exit points may be indicated by these trends and patterns. In addition to confirming trading signals and pointing out overbought and oversold situations, indicators can help traders make well-informed selections before purchasing or disposing of shares.

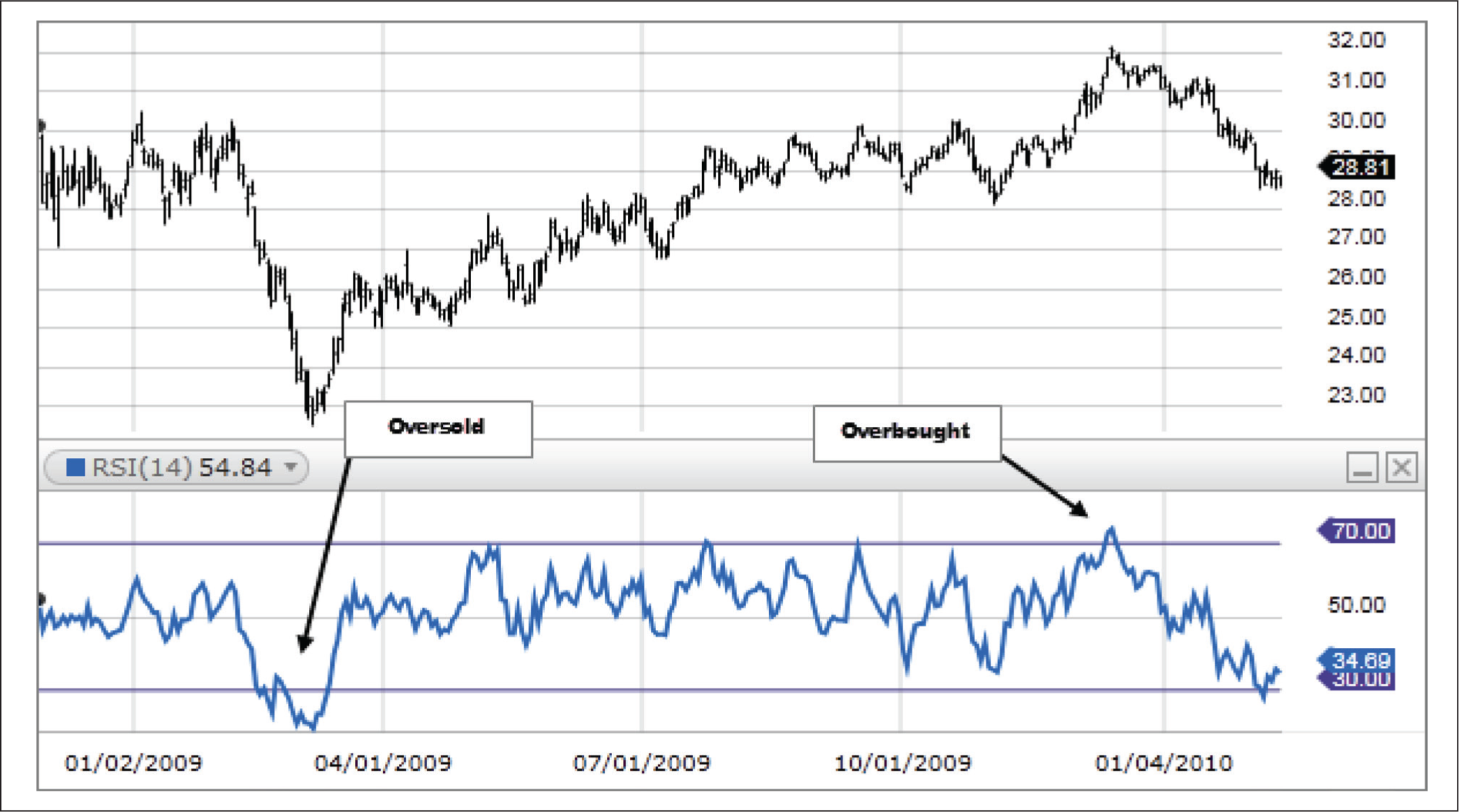

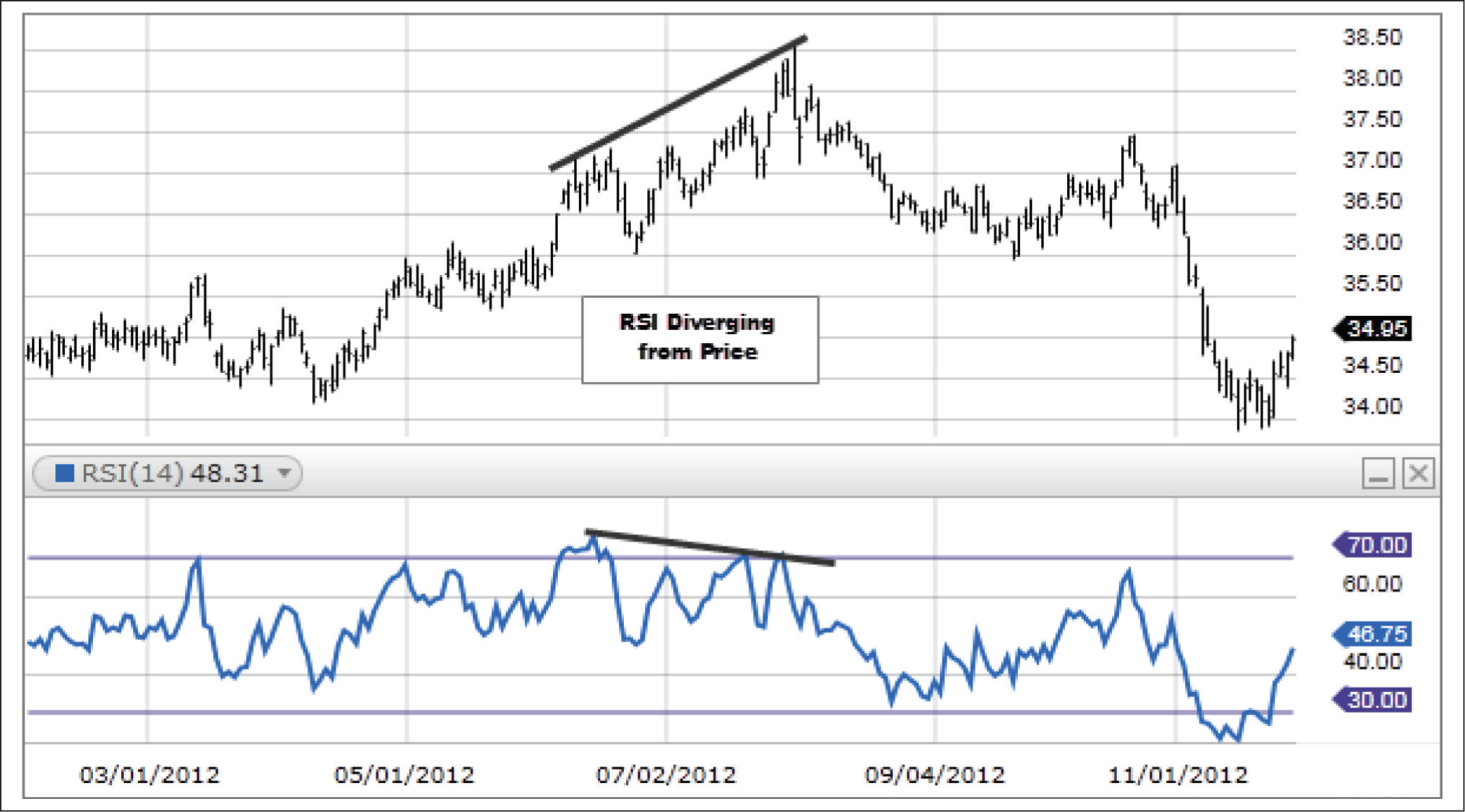

Relative Strength Index

As shown in Figures 2 and 3, the RSI is a momentum oscillator that gauges the rate and direction of price changes. The range of the RSI oscillates is 0–100. In the past, the RSI was deemed oversold when it fell below 30 and overbought when it rose above 70. Searching for divergences and failure swings can produce signals. Additionally, RSI can be utilized to determine the overall trend (Wilder, 1978).

The RSI is a versatile and widely used technical indicator that can provide valuable insights into market conditions. It identifies overbought and oversold conditions using the traditional levels of 70 and 30, respectively, but these thresholds can be adjusted to better suit the characteristics of specific securities. The RSI can also reveal chart patterns such as double tops, double bottoms, and trend lines that may not be apparent on price charts. In bullish markets, the RSI typically ranges between 40 and 90, with the 40–50 zone acting as support. Conversely, in bearish markets, it usually ranges between 10 and 60, with the 50–60 zone acting as resistance. Importantly, divergences between RSI and underlying price movements can signal potential reversals, providing early warning signs to traders. Specific patterns such as top swing failures and bottom swing failures further enhance the RSI’s utility in predicting market trends and reversals. Overall, the RSI is a powerful tool for traders, offering a blend of flexibility and depth in its application across different market conditions and securities.

Though it is a pretty simple formula, the RSI might be hard to understand without a number of examples. To learn more about the calculations, consult Wilder’s book (Wilder, 1978). The fundamental calculation is as follows: RSI = 100 – [100 / (1 + (Average of Upward Price Change / Average of Downward Price Change))}].

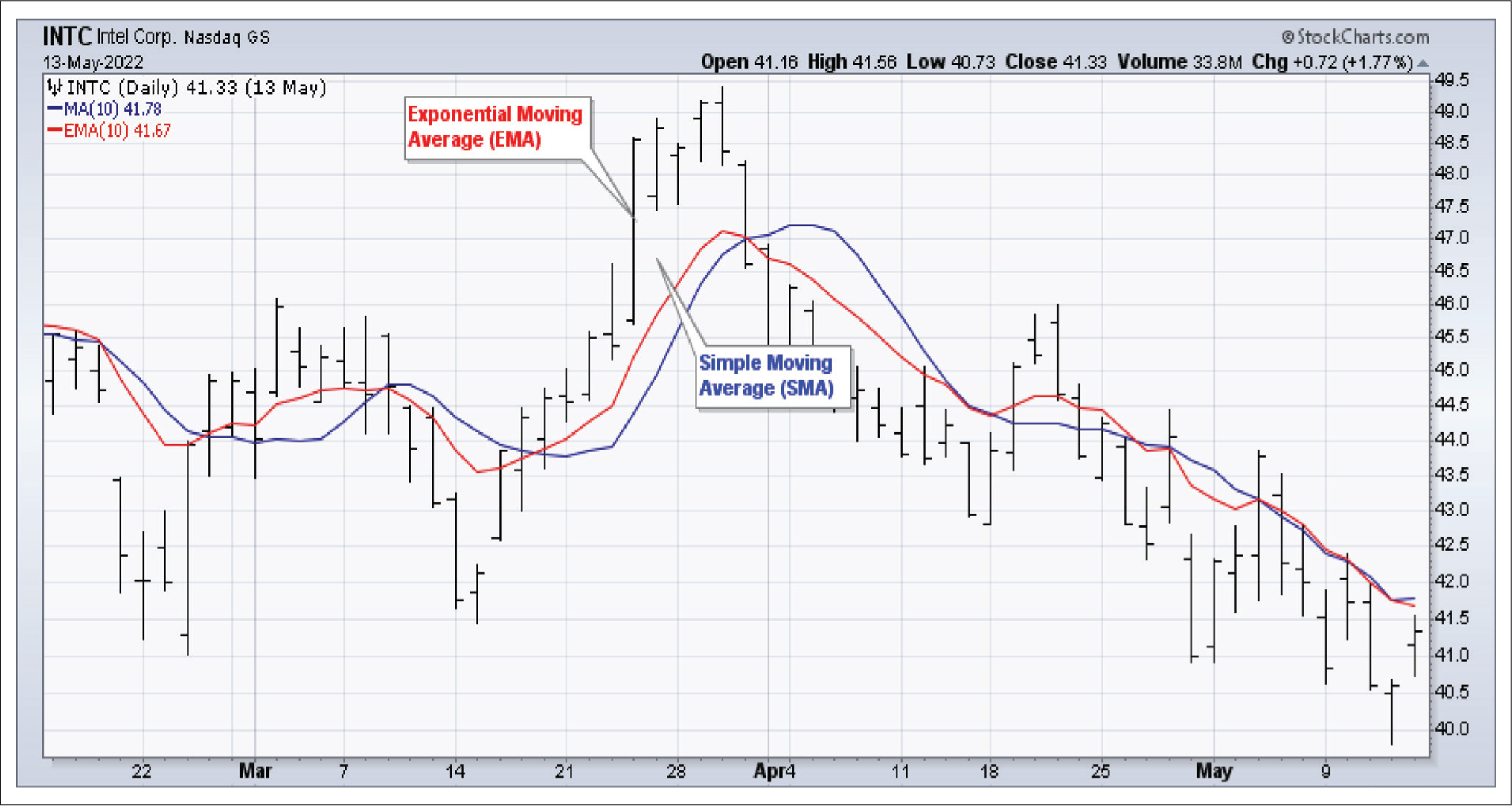

Moving Average Indicator

An average of data points over a given time period, usually price, is called an MA. What makes it “moving?” This is so because information from the preceding X periods is used to calculate each data point. Moving averages smooth the price data to create a trend-following indicator by averaging previous data. No MA can forecast the direction of prices. Rather, it delineates the present course. An MA, however, is based on historical values; thus, it usually lags. Nevertheless, MAs are used by investors to reduce noise and smooth out price movement.

Moving averages can be used to establish possible levels of support and resistance or to determine the direction of a trend. Additionally, they serve as the foundation for a variety of other technical overlays and indicators, including the BB, the McClellan oscillator, and MACD. The EMA and the SMA are the two most widely used MAs. While EMAs give more weight to current prices, SMAs average values across the given timeframe.

Results and Discussion

Figure 4 was used as a thorough investigation that included historical data, algorithmic testing, and behavioural finance insights was used to determine how well the MA and RSI indicators enhance trading methods. The study’s findings are essential to comprehending the usefulness of these technical indicators in relation to trader psychology and market dynamics. The results of the thorough analysis of the MA and RSI indicators in trading methods are shown in this section. To ascertain whether these technical indicators are useful for improving trading decisions, the analysis combines the examination of historical data, algorithmic testing, and behavioural finance insights.

Historically Data Analysis

To ensure the validity of our conclusions, we conducted a decade-long analysis of historical data under a range of market conditions. We assessed the individual and combined performance of the RSI and MA indicators in a variety of asset classes, such as FX, commodities, and equities.

RSI performance: The indicator of overbought and oversold conditions, RSI, produced a mixed bag of findings. RSI frequently generated purchase signals too soon in erratic markets, which resulted in losses. On the other hand, the RSI’s signals were more trustworthy in trending markets, particularly when thresholds were changed (e.g., 30 for oversold and 70 for overbought). By making this adjustment, the win rate was raised by about 10% above the typical criteria (30/70).

MA performance: SMA and EMA indicators showed a tendency to lag behind trends, frequently confirming them later. Even though there were more false signals, employing shorter timeframes—such as 10- and 20-day periods—helped in identifying early trend reversals. When combining lengthier MAs (50 days and 200 days) for trend confirmation, false positives were decreased, but entry and exit points were delayed, which could have an impact on profit margins.

Combining RSI and MA: There was potential in the way that the two indicators worked together. For example, confirming signals from a 50- and 200-day MA crossing method with a 14-day RSI led to higher accuracy but fewer transactions. This combination raised the average return per transaction by 7% and decreased the frequency of false positives by about 15%.

Algorithmic Testing

Backtesting different methods using the RSI and MA indicators on past price data was a component of algorithmic testing. To replicate trades, we used a strong backtesting framework that took slippage, market impact, and transaction costs into account.

RSI-based strategies: High risk-reward ratios were observed in pure RSI strategies, especially those that used extreme threshold values (e.g., 20/80). The profitability per transaction grew as the number of trades reduced, indicating that algorithmic trading systems that aim to take advantage of overbought and oversold scenarios can benefit more from extreme thresholds.

MA-based methods: A lot of testing was done on MA crossover methods, particularly those that included SMA and EMA. Strong trending periods were especially beneficial for the golden cross (50-day MA crossing above 200-day MA) and death cross (50-day MA crossing below 200-day MA) strategies. They did not perform as well in sideways markets, though, which emphasizes how crucial the market context is when implementing MA methods.

Combined strategies: Performance metrics were greatly enhanced by combining RSI and MA into a single algorithmic technique. An example of an algorithm that performed better than standalone methods was one that started a trade when the RSI indicated overbought/oversold circumstances, as confirmed by a corresponding MA crossover. This algorithm decreased drawdowns and increased the Sharpe ratio by an average of 0.25.

Insights into Behavioural Finance

The reasons behind the superior performance of some RSI and MA techniques were better understood thanks to behavioural finance concepts. Human psychological traits that affect market dynamics and technical indicator efficacy include herd mentality, loss aversion, and overconfidence.

Loss aversion: During market sell-offs, traders overreacted due to their inclination to avoid losses. The RSI’s capacity to spot oversold circumstances profited from these overreactions, enabling methods to join positions at advantageous prices when panic selling occurred. Herding behaviour: Herd behaviour was beneficial for MA indicators, especially longer term ones. Self-fulfilling prophecies were created when more traders and investors identified and responded to MA crosses, which led to price moves that validated the indicators’ indications.

Overconfidence: In optimistic markets, overconfidence frequently resulted in persistent purchasing, which raised prices. In such cases, the overbought signals produced by the RSI were less trustworthy. However, the lagging characteristic of the MA moderated premature selling signals, so combining the RSI with MA provided a counterbalance.

Practical Implications

The results highlight how crucial context and combination are when using the RSI and MA indicators. While pure RSI or MA methods have their uses, their efficacy is highly dependent on the state of the market. Their profitability and dependability can be increased by combining various indicators, modifying thresholds, and adding behavioural finance knowledge.

Contextual adaptation: Depending on the state of the market, traders should modify the parameters of the RSI and MA. Performance can be optimized, for instance, by employing longer MA periods in trending markets and more sensitive RSI criteria during volatile times.

Combining indicators: An even more thorough understanding of market circumstances is provided by combining the RSI and MA indicators. Trade accuracy is improved and erroneous signals are decreased when RSI is used to filter MA signals or vice versa.

Behavioural considerations: Interpreting indicator signals can be made easier by being aware of behavioural biases. Traders can make better decisions by identifying overreaction, herding, and overconfidence trends.

Conclusion

In this study, we have conducted a thorough evaluation of the RSI and MA as technical indicators within trading strategies. Through a combination of historical data analysis, algorithmic testing, and insights from behavioural finance, we have demonstrated that the RSI and MA, while powerful on their own, exhibit enhanced effectiveness when used together. Our research highlights that the RSI’s ability to identify overbought and oversold conditions, paired with MA’s trend-following capabilities, provides a synergistic approach that refines entry and exit points in trading. This combination mitigates the limitations observed when each indicator is used independently, particularly in volatile market environments. Algorithmic testing confirms that integrating RSI and MA reduces false signals and increases the profitability of trades. Moreover, incorporating behavioural finance perspectives has revealed that understanding trader psychology can further enhance the application of these indicators. Traders can better navigate the market dynamics by recognizing patterns of overreaction, herding, and overconfidence.

Overall, this article contributes valuable insights into the effective use of the RSI and MA, offering a practical framework for traders to optimize their strategies and achieve better trading outcomes.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.