Abstract

Controlling for the US stock market, we find that the reaction of the Indice de Precios y Cotizaciones (IPC) (Mexican equity market) to changes in the federal funds target rate is asymmetric and depends on the state of the Mexican economy. Specifically, Mexican equity markets, like US equity markets, suffer more during cyclical downturns when faced with US monetary surprises than during expansions. This result is important since it suggests that exogenous credit events in the US can affect Mexican equity markets and that the magnitude of the effect depends on the state of the Mexican economy; additionally, it shows that the credit channel theory applies across the US–Mexican border. While other studies have confirmed that US monetary surprises can affect the Mexican equity market, none have looked at this aspect as it relates to business cycles.

JEL Classification: E52, F36, F42

Introduction

The Federal Reserve announcement concerning the federal funds target rate is one of the most important news items concerning monetary policy in the world. Numerous studies show that the US stock market is responsive to changes in the US monetary policy (see Bernanke & Kuttner (2005); Ehrmann & Fratzscher 2004; Gürkaynak, Sack & Swanson 2005; Jensen & Johnson 1995; Jensen Mercer & Johnson 1996; Patelis 1997; Rigobon & Sack 2004; and Thorbecke 1997). The US monetary policy also affects foreign exchange rates and foreign interest rates (see Andersen, Bollerslev, Diebold & Vega 2003, 2007; Arora & Cerisola, 2001; Durham 2001; Ehrmann & Fratzscher 2002; Husted & Kitchen 1985; Miniane & Rogers 2007; Robitaille & Roush 2004; Roley 1987; Tandon & Urich 1987; Johnson and Jensen (1993), Ehrmann and Fratzscher 2005, 2009; Ehrmann, Fratzscher and Rigobon 2005 and Wongswan 2006, 2009 examine the impact of Federal Open Market Committee (FOMC) announcements on foreign equity indices. In particular, foreign equity markets respond to the US monetary policy both directly and indirectly; in addition to the influence of the change in US monetary policy, foreign equity indices are also affected by induced changes in the US equity market.

One issue receiving less attention is the importance of business cycles in determining the magnitude of the equity market reaction to monetary policy. Basistha and Kurov (2008) look at US equity market reactions to the surprise component from FOMC announcements. They find that US equity market reactions are more pronounced when the US economy is in a recession. Using the Granger causality statistics, Rodríguez and Rowe (2007) find that US monetary policy can affect Hong Kong gross domestic product (GDP). They suggest that if Hong Kong were in a recession, given that Fed policy is exogenous to Hong Kong GDP, FOMC announcements could be detrimental to the Hong Kong economy. Specifically, they blame the fixed exchange rate of Hong Kong and point to interest rates as the transmission mechanism.

Here, we look at a prominent equity market of Mexico, a country that does not have a fixed exchange rate. We show that unexpected changes in the federal funds target rate affect the Indice de Precios y Cotizaciones (IPC). More importantly, we find that the state of the Mexican economy is significant for the IPC reaction to US monetary policy. In other words, it suggests that the credit channel theory applies across international borders.

Wongswan (2009) and Hausman and Wongswan (2006) find that a surprise increase in the federal funds target rate of 10 basis points provokes a decline in the Mexican equity market of approximately 0.6 per cent. The authors argue that since Mexico is in the same time zone as the US, these effects are negligible. However, Ehrmann and Fratzscher (2009) hold that even though Mexico is in the same hemisphere as the US, US equity markets must be controlled for when looking at the Mexican equity market’s reaction to FOMC announcements. They find that the reaction of the Mexican equity market to surprise changes in the federal funds target rate is statistically insignificant. However, one major and important difference from their study to ours is that we test to see if the state of the economy matters when credit changes occur. Another difference is that we control for effects that the US equity market might have that are independent of US monetary shocks.

Our baseline result used for calibration of our model supports Wongswan (2009) and Hausman and Wongswan (2006). Controlling for the US stock market, we find that the IPC drops by 66.6 basis points when the federal funds target rate is increased unexpectedly by 10 basis points and vice versa. More importantly, we also find that the state of the Mexican economy matters. During periods where Mexico has witnessed at least two consecutive quarters of negative growth in real GDP, the IPC reacts by over 60 basis points to an unexpected one-basis-point change in the federal funds target rate. When the Mexican economy is not in recession, the IPC reaction is significantly weaker. Using recession dates generated from a Markov-switching model, the magnitude is smaller, but is significant both economically and statistically. This result is important in that it suggests that Mexican equity markets react asymmetrically to the exogenous event of a US monetary surprise and that this reaction is greater when the Mexican economy is experiencing negative real growth. Hence, the credit channel theory, at least going from the US to Mexico, applies across the border. The Mexican equity market, like US equity markets, suffers more during cyclical downturns when faced with US monetary surprises. These results add to the literature in that previous work has ignored this aspect when looking at the surprise component of the FOMC announcements and their effect on foreign equity markets.

Transmission Channels and Testable Hypotheses

Transmission of Monetary Policy to Equity Markets

From the finance literature, the discounted cash-flow approach calculates the price of a financial asset as the present value of future cash flows. A surprise increase in the discount rate lowers asset prices. Empirical evidence overwhelmingly supports this assertion. Ehrmann and Fratzscher (2004), Rigobon and Sack (2004) and Bernanke and Kuttner (2005) all conclude that a 10-basis-point surprise in the federal funds target rate would provoke a change in the US equity market in the range of approximately 40–60 basis points; this correlation is negative.

Transmission Channels to Foreign Equity Markets

Just as US equity markets react to US monetary policy, foreign equity markets might as well. The link depends on whether the federal funds target rate affects foreign interest rates, too. If so, then, the same logic as given by the discounted cash flow reasoning would apply to foreign equity markets. A surprise tightening in the federal funds target rate would increase the foreign discount rate through its effect on the global interest rate and, hence, foreign equity prices would fall. Monticini and Vaciago (2005) find that Euro bond rates do react to FOMC surprises, but British rates do not. 1 However, stock market comovements must also be considered. For example, in their study of the Japanese and US equity markets, Lin, Engle and Ito (1994) find that there is significant comovement between these two markets with the causality going in both directions.

Credit Channel Theory

Bernanke and Gertler (1989) show that the state of the economy can play an important role when investigating the effects of changes in monetary policy. Specifically, when an economy is in a recession, changes in credit conditions brought on by monetary surprises have a bigger impact than when the economy is experiencing positive real GDP growth. This happens through two channels. Borrowers that are dependent on external financing suffer when the supply of bank credit is reduced. In addition, firms become less creditworthy due to deterioration in the quality of their balance sheets from the cyclical downturn in the economy. Both of these channels together have a multiplier-type effect on real output. Because of this, the economy becomes more sensitive to macroeconomic changes during economic downturns than during economic booms.

The link between the domestic economy and domestic equity markets is well documented for many different economies. Andritzky, Bannister and Tamirisa (2007) show that the bond market in emerging economies reacts to US macroeconomic news. Lustig (2001) highlights how the US economy can affect Mexico.

For stock market reactions to monetary surprises, most work looks at domestic monetary changes and the domestic equity market reaction. Using newspaper announcements and daily stock returns in the US during the early 1990s, Warner and Georges (2001) find little evidence that supports the credit channel theory. Basistha and Kurov (2008), however, find support for the credit channel theory. They look at a longer time period and use a more sophisticated method for measuring monetary surprises and they show that the US stock market responds approximately twofold more to unexpected changes in the federal funds target rate during tight credit conditions than when credit is easier.

Hypotheses

This article tests two hypotheses. The first is that US monetary shocks cause reactions by the Mexican equity market. This hypothesis is strictly to calibrate our findings with previous studies. The second hypothesis is the centre piece of this article and represents our contribution to the literature. While foreign equity market responses to US monetary surprises have been examined in the literature, the importance of cyclical variations for this response has not. We test to see if the Mexican equity market response to US monetary surprises is asymmetric. Greater reactions by Mexican equity markets during Mexican recessions are indicative of an international credit channel effect.

Estimation Framework

Event-based Approach

For this study, the events of interest are FOMC announcements of the target federal funds rate. These announcements are made during meetings of the FOMC, and include those meetings where the decision was for no change in the target. Given that these policy statements are anticipated by the market, all or some of the effect should already be incorporated into the foreign equity prices in the IPC. Complete anticipation by markets would suggest that IPC prices completely adjusted before the FOMC announcement. However, if the markets were surprised, or rather did not anticipate the event with complete accuracy, some reaction in IPC prices would be expected.

For each announcement, we look at the daily movement of IPC prices and the surprise component of the target change. These target-rate announcement events are exogenous since the event window is short and the Fed is unlikely to make policy choices in response to Mexican equity markets. We also control for US equity prices since some of the change in IPC prices could be due to the reaction of US equity prices to US monetary policy announcements rather than the announcements themselves. The FOMC announcement on 17 September 2001, in response to the events that took place on 11 September 2001, was not included in this study (see Bernanke & Kuttner, 2005. All other FOMC announcements from November 1993 through September 2008 are included. 2 The sample includes 131 observations.

Target Rate Surprises

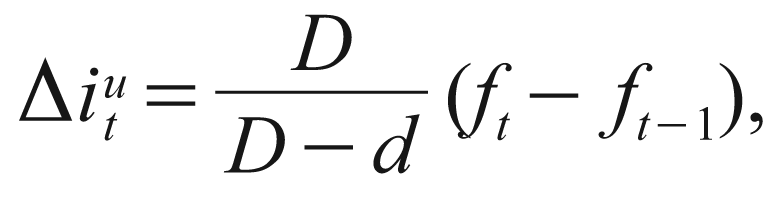

To identify the effect of the FOMC announcements, the unanticipated component of the change in the federal funds target rate is inferred from changes in the current-month fed funds futures rate for the day of the announcement. 3 This technique due to Kuttner (2001) is used extensively in the literature. It is calculated by the following formula:

where

Mexican and US Equity Data

To measure Mexican equity returns, we use the IPC, a capitalisation weighted index of leading stocks traded on the Bolsa Mexicana de Valores. Since the exchange is open for trading between 10:30 and 5:00 pm EST, the relevant data for measuring the effect of monetary policy is the daily close-to-close percentage return from the IPC index on days of FOMC announcements.

Despite the fact that US equity and Mexican equity markets have similar trading hours, it is possible that changes in the IPC are being caused by the US equity market itself, rather than the surprise component of the FOMC announcement. To control for US equity prices, we use the daily close-to-close percentage return of the Standard & Poor’s 500 Index (S&P). To isolate the effect that the S&P has on the IPC that is not related to US monetary policy, we follow Basistha and Kurov (2008) and estimate the following equation from November 1993 through September 2008:

Here,

Business Cycle Data

To test whether cyclical variation matters for IPC reactions to the surprise component of FOMC announcements, we need a proxy for Mexican business cycles. In the US, business cycles are determined by the National Bureau of Economic Research (NBER). A similar measure for Mexico does not exist. The NBER defines a recession as follows:

A recession is a significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in production, employment, real income, and other indicators. A recession begins when the economy reaches a peak of activity and ends when the economy reaches its trough. Between trough and peak, the economy is in an expansion.

5

In order to test whether cyclical variation matters for IPC reactions to the surprise component of FOMC announcements, we use two methods for dating Mexican business cycles. The first is the standard ‘newspaper’ definition of at least two quarters of negative real GDP growth. One of the major criticisms of this method is that since the frequency of the GDP series is quarterly, it gives a very general, if not vague, signal of when a change in the business cycle actually occurred. Since our goal is not necessarily to determine the exact dates for the Mexican business cycle, but rather to determine general periods of cyclical variation, this measure should be marginally sufficient. Using this metric, Mexico has experienced two recessions: one occurs during the first three quarters of 1995 and the other occurs in the third quarter of 2008.

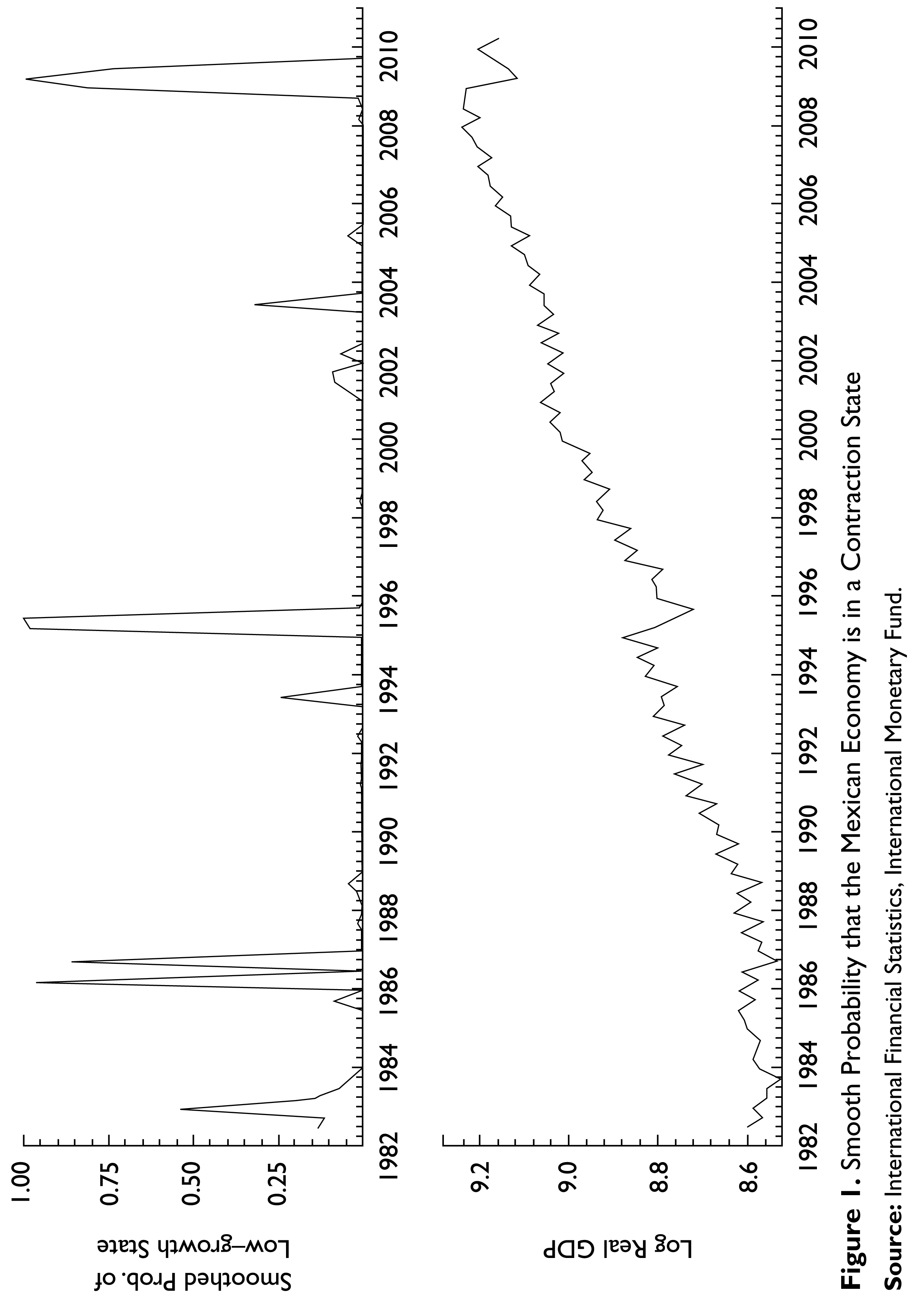

In addition, we estimate an autoregressive model of Mexican GDP growth where parameters depend upon an unobserved state indicator. Hamilton (1989) shows that estimates for the unobserved state of the US economy’s growth are closely related to NBER dating of post-war recessions. A similar approach is used to estimate the unobserved state of the Mexican economy, where smoothed maximum likelihood parameter estimates of a Markov-switching model for Mexican real GDP indicate recession probabilities. We follow Hamilton (1989) and use 0.5 as the threshold for the probability of a low growth state to mark turning points of economic growth, as this threshold relates US data to NBER cycles. In line with Hamilton’s results, the probability-threshold estimates compare favourably to ‘newspaper’ definitions of recessions, finding a shorter recession of the first two quarters of 1995 and between the fourth quarter of 2008 and the second of 2009.

Markov-Switching Model for Mexican Production Data

This section outlines the empirical method to estimate the unobserved state of the Mexican economy. We follow Hamilton (1989) in developing the model, and as is the convention, we use the signal of the probability estimate of a low-growth state to be greater than 0.5 to signal a recession.

Let yt equal the log growth rate of Mexican real GDP. Figure 1 shows the smoothed probabilities of a recession from the model fitting

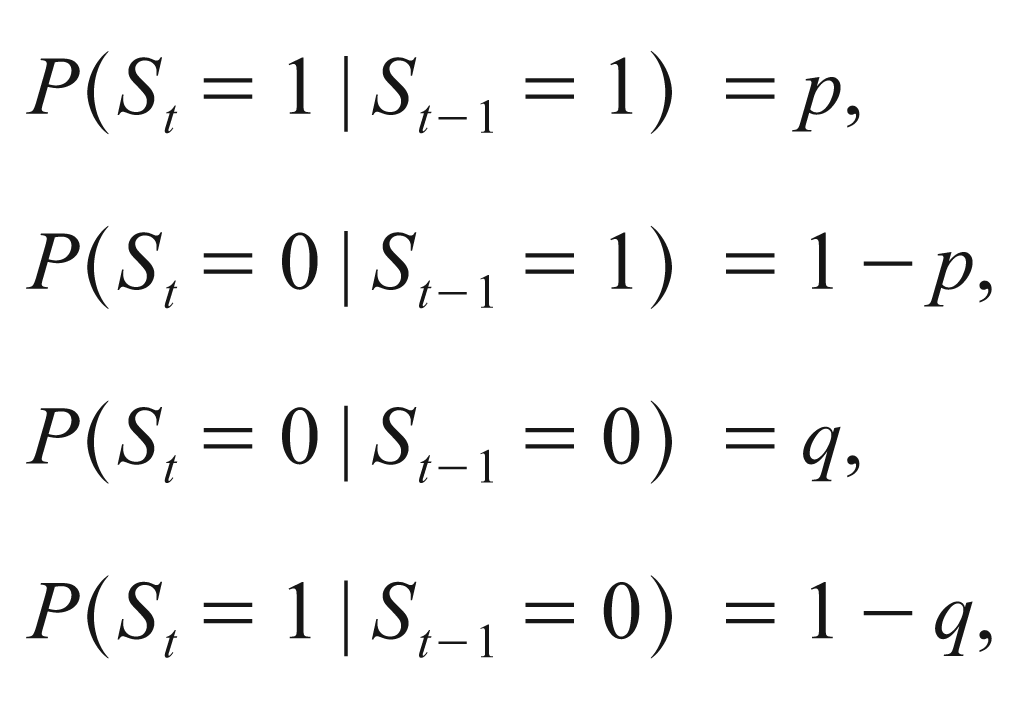

where st = {0,1} serves as a particular realisation of a random variable St, indicating the unobserved state of the economy. The probability of the present quarter being in recession given the economy was in recession in a previous quarter equals p, such that

and p + q = 1. The transition matrix for the Markov chain is therefore given by

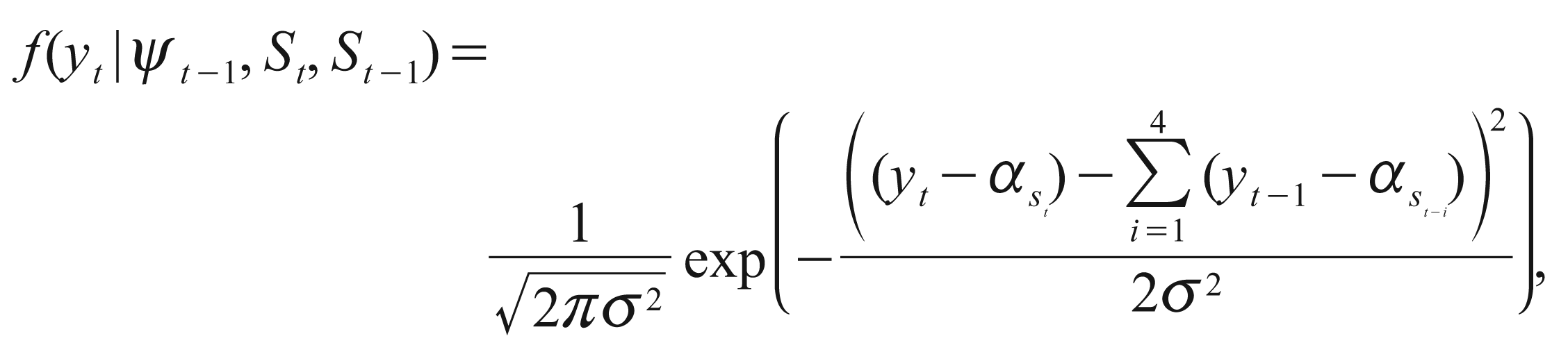

Maximum likelihood parameter estimates and probabilities of latent state variables are produced using the filtering algorithm of Hamilton (1989), with the smoothing algorithm of Kim (1994) and Kim and Nelson (1999). Given all information known at time t, Ψt–1, the density of yt equals

and the log likelihood function equals

where only the previous state of the economy matters given the first-order Markov properties.

The filter is initialised at the steady-state probabilities

where

in the steady state,

and

Letting

In each period t, the joint density of yt, St, St–1, St–2, St–3, St–4 given all past information Ψt–1 equals

Summing over all values of St and St–1 produces the marginal density f(yt | Ψt–1) as a weighted average of the four conditional densities with weights P(St = j, St–1 = i | Ψt–1), for i = {0,1}:

The log likelihood equals the sum of equation (17) over all t. For each time t, the weighting terms

where P(St = j | Sy–1 = i) is given by transition probabilities

After observing yt at the end of time t, probabilities are updated as

where

The filter is initialised at t = 1 using the steady-state probabilities and ϕ from the linear AR(4) model given the results of the model selection Schwartz criterion over all models with less than 6 lags. A lag length of four is selected by the Schwartz criterion searching over all models with less than six lags. Given the fact that higher-order autoregressive processes are computationally prohibitive in the regime-switching framework, and the sample includes only 117 quarterly observations, this determination is parsimonious and consistent with the empirical model selection criteria. Without loss of generality, we let initial values of P(St = 1 | St–1 = 1) > P(St = 0 | St–1 = 1). Estimates of p, q and σ are constrained non-negative, with likelihood maximised with the Optmum package under the Broyden–Fletcher–Goldfarb–Shanno (BFGS) algorithm of GAUSS 10.

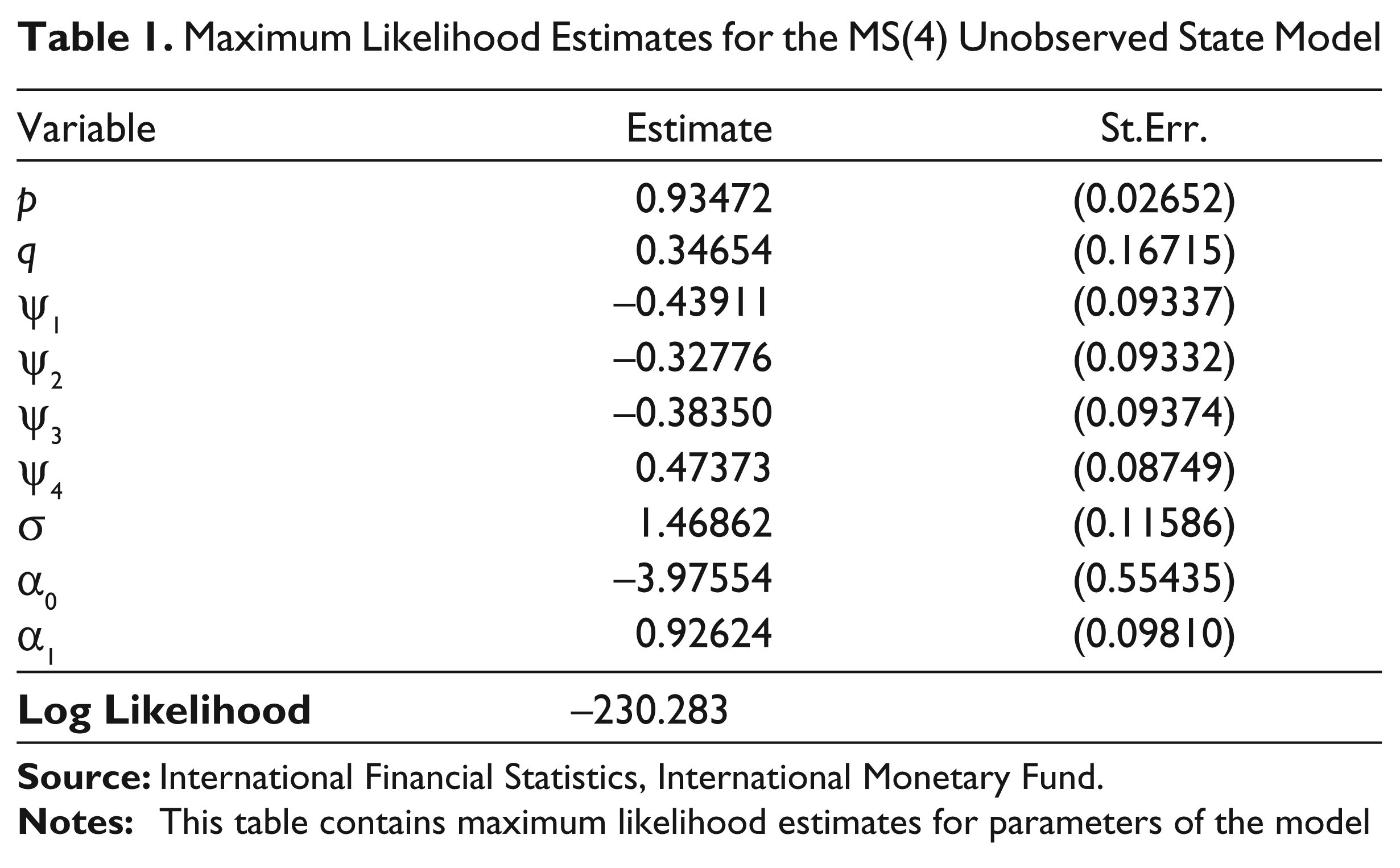

Table 1 shows the estimates from the Markov-switching model of seasonally adjusted Mexican real GDP between 1981:Q1 and 2010:Q1. The top frame shows smoothed estimates of the probability that the Mexican economy is in a low-growth state. The bottom frame shows log change of seasonally adjusted Mexican GDP. Based on Hamilton’s 0.5 threshold rule, recessionary quarters relevant to the present study include 1995:Q1 and Q2, and 2008:Q4-2009:Q2.

Maximum Likelihood Estimates for the MS(4) Unobserved State Model

where st = {0,1} serves as a particular realization of a random variable St, indicating the unobserved state of the economy. The probability of the present quarter being in recession given the economy was in recession in a previous quarter equals p, such that

The dependent variable yt equals the log change of seasonally-adjusted Mexican GDP in 2005 dollars for 1981:Q1 to 2010:Q1. The first five observations are lost to the difference and AR terms.

Empirical Results

Benchmark Results

For the benchmark result, cyclical variations in the Mexican economy are ignored. Equation (25) is estimated:

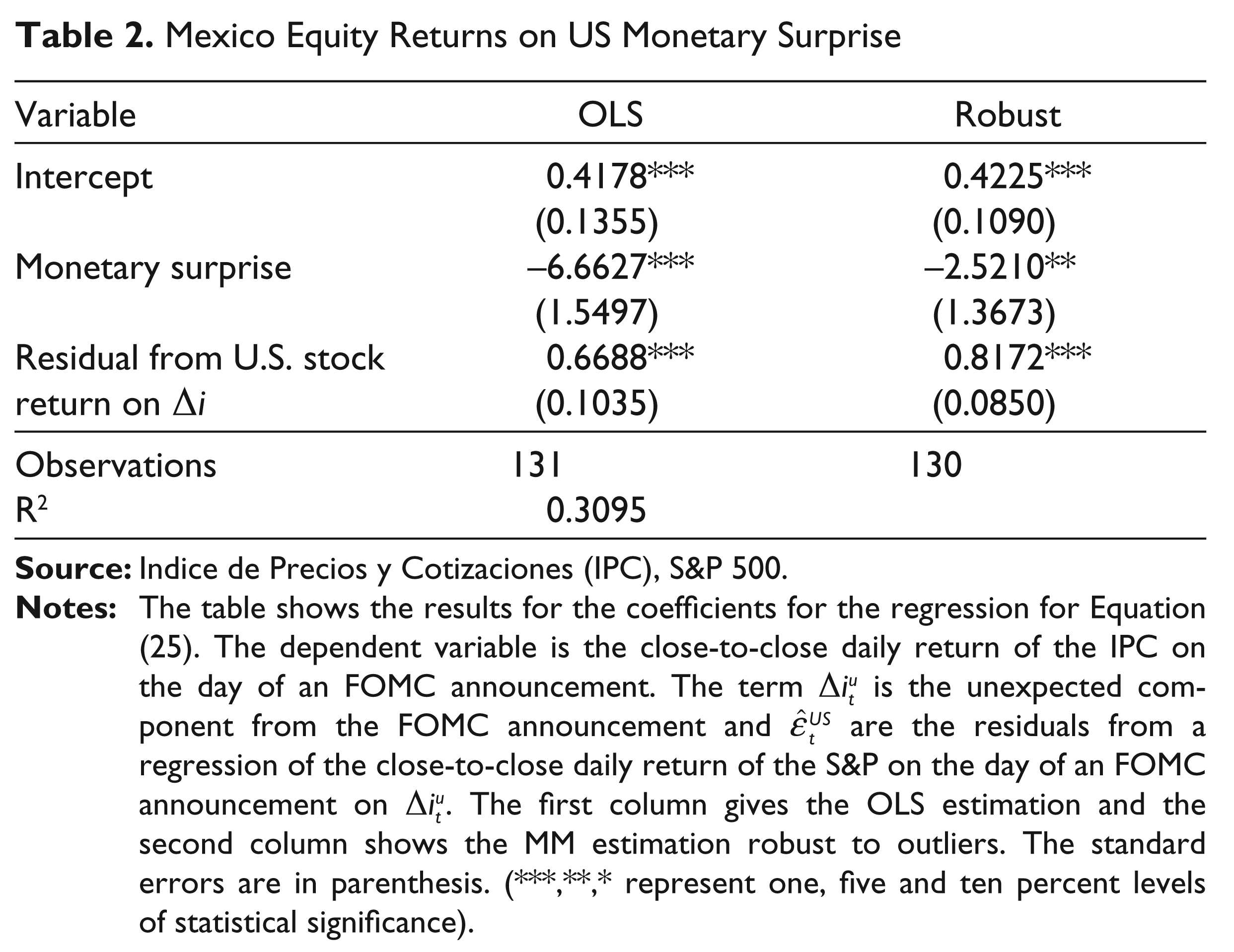

Mexico Equity Returns on US Monetary Surprise

Here, the new term relative to equation (2) is

Table 2 shows the results from both estimations of (25). For the OLS estimation,

Business Cycle Indicator Using Real GDP

Next, we allow for business cycles as measured by real Mexican GDP. We estimate equation (23) below:

The new term relative to (25) is the cyclical variation variable

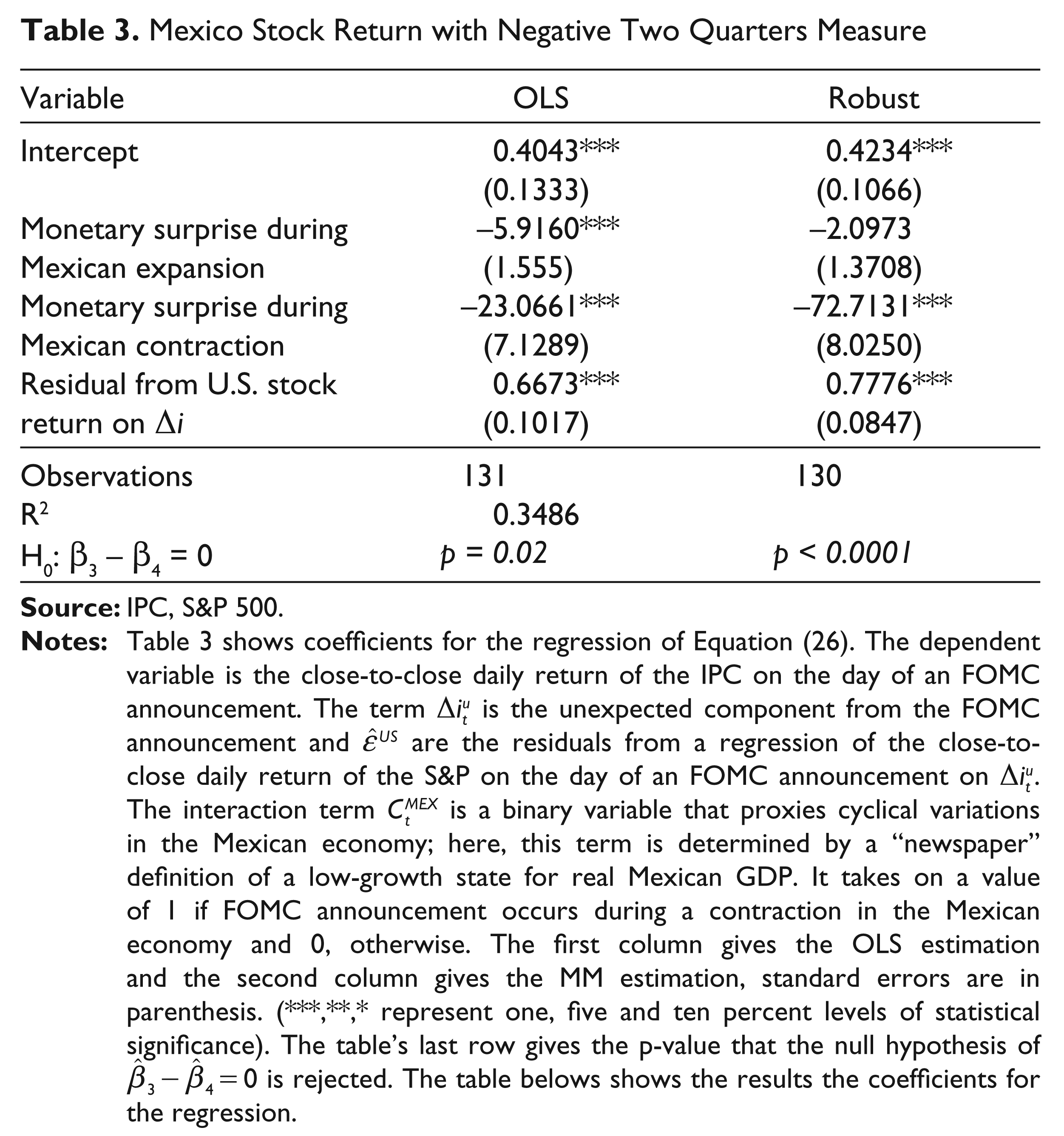

Mexico Stock Return with Negative Two Quarters Measure

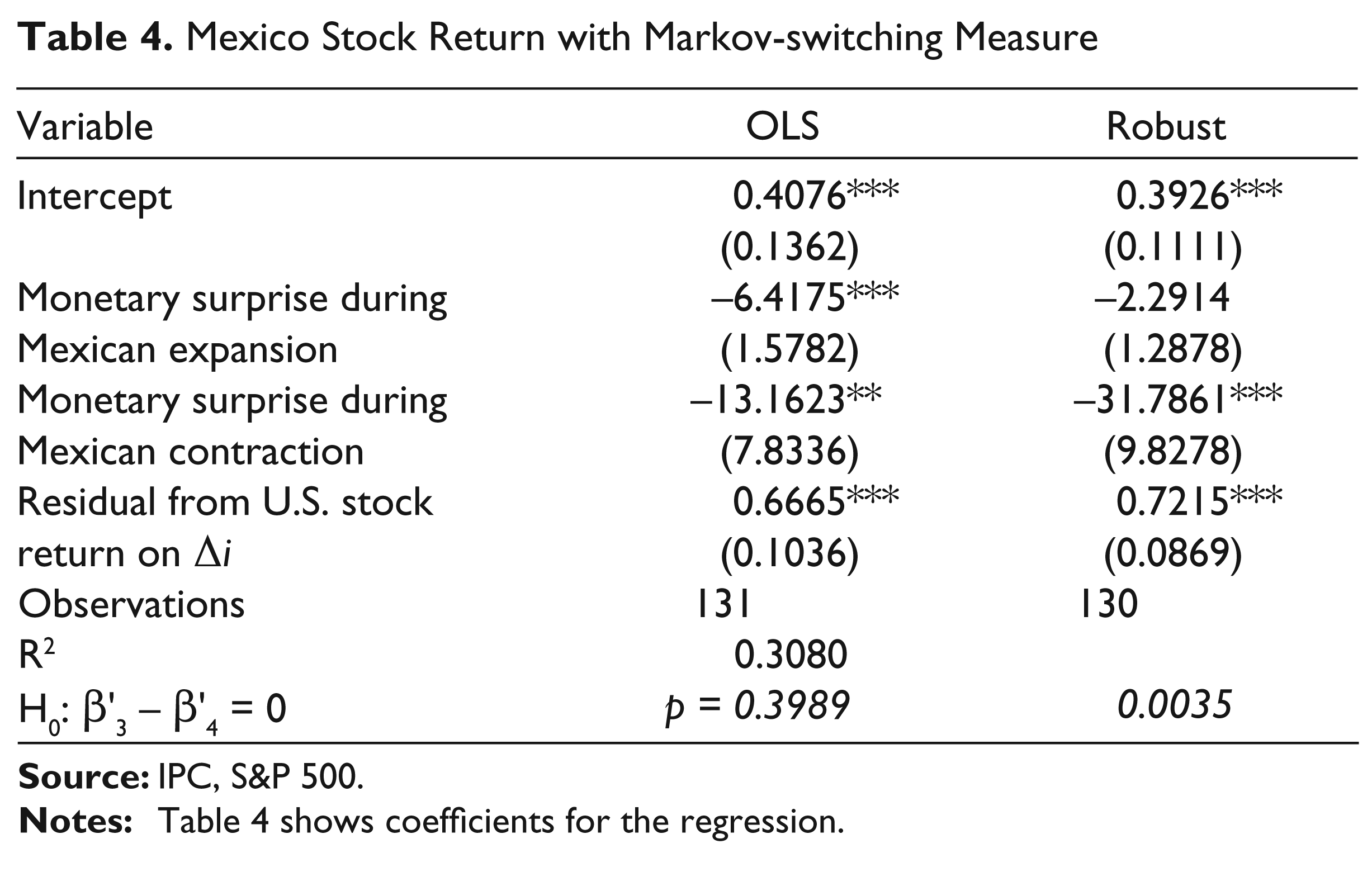

Mexico Stock Return with Markov-switching Measure

The dependent variable is the close-to-close daily return of the IPC on the day of an FOMC announcement. The term

Table 4 reports OLS and MM estimations where Mexican business cycles are dated using the Markov-switching model. US monetary shocks have a significant and economic effect on the IPC. However, in the MM estimation, the FOMC effect on the IPC is economically more significant when the Mexican economy is in a low-growth state. This is confirmed by the results of the Wald test.

Do US Business Cycles Matter?

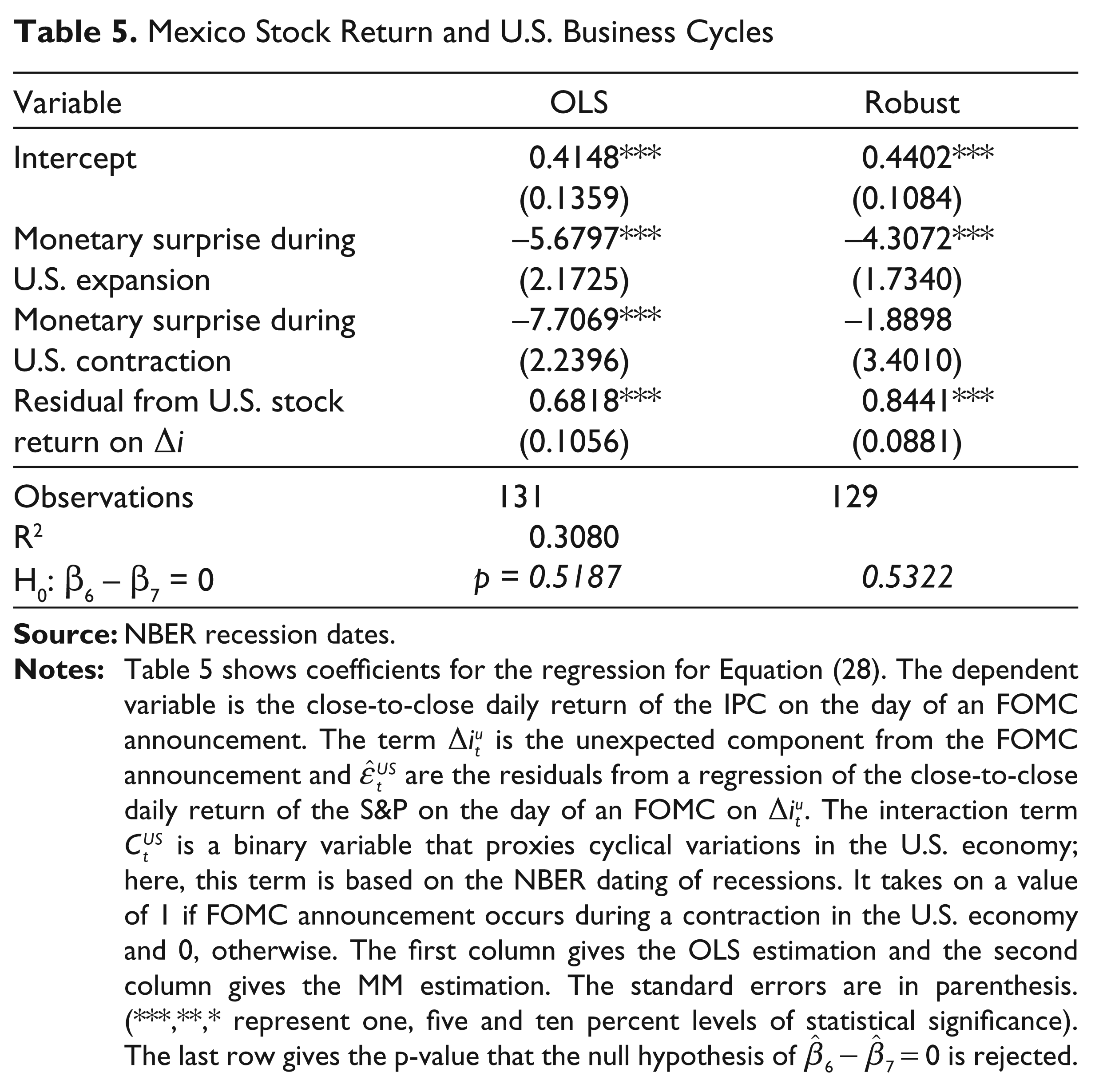

It might be that the IPC is reacting to US business cycles and not cyclical variations in the Mexican economy. Using NBER recession dates, we estimate equation (28), 6

where the cyclical variable

From Table 5, in the OLS estimation, the US business cycle monetary shocks have a statistically significant and economic effect on the IPC. In the robust regression, only the shocks during an NBER expansion are statistically significant. However, in neither estimation is β6 – β7 statistically different from zero. The IPC clearly does not react differently to the FOMC announcements when the US economy is in an NBER recession.

Mexico Stock Return and U.S. Business Cycles

US Returns as Independent Variable

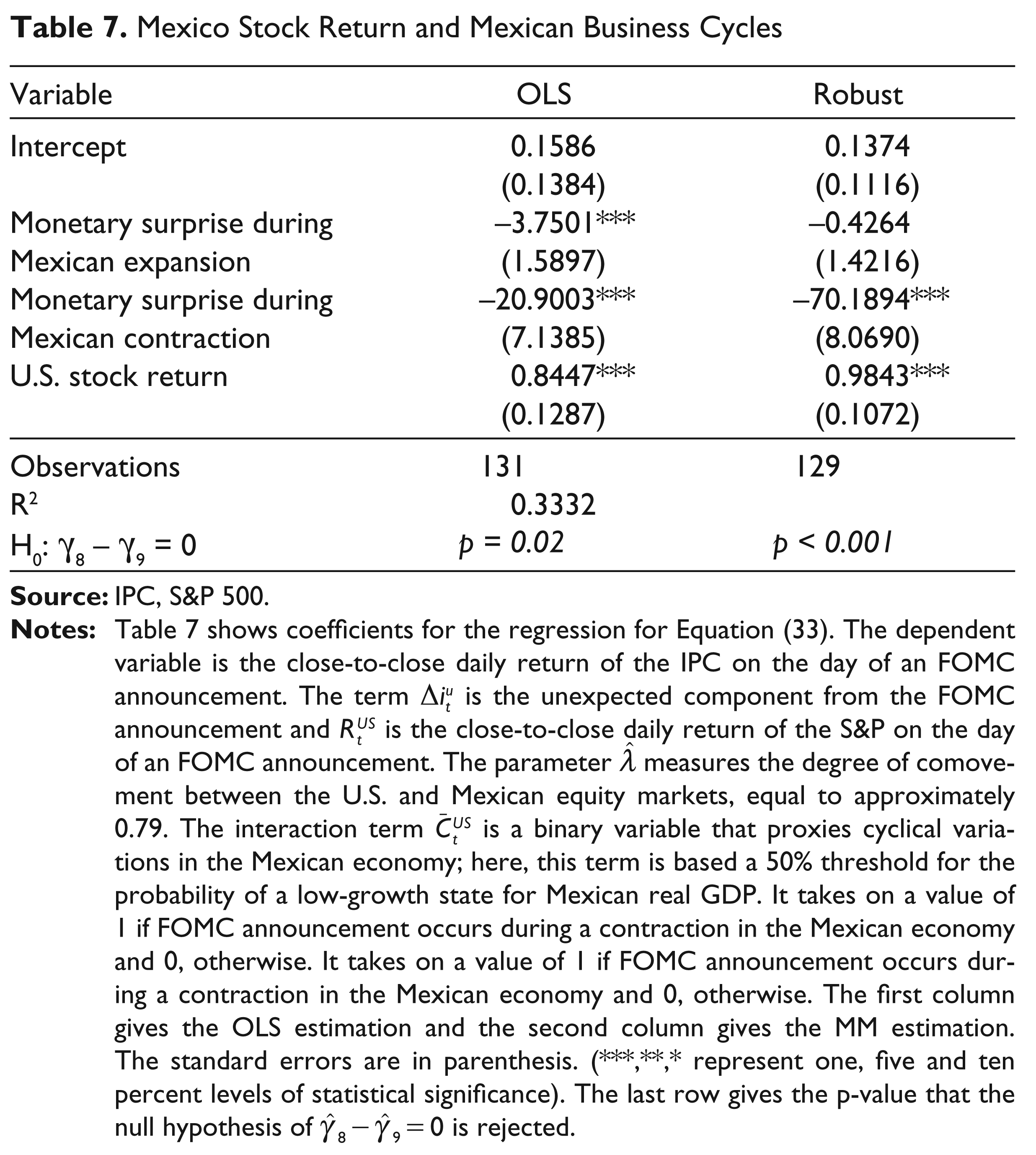

It is quite possible that what is driving the innovations in Mexican equity markets are the US business cycles rather than the Mexican ones. Here we address this issue and show that this is not the case. 7 Hausman and Wongswan (2006) estimate equation (29) and (30):

where

where the daily returns from the IPC are regressed on the daily returns from the S&P over the entire time period of this study (November 1993 through December 2008). The value of

For both the OLS and MM estimation, the IPC responds in a statistically and economically significant manner when the Mexican economy is in a downturn. Furthermore, the coefficient γ5 is statistically insignificant in both estimations. Additionally, both γ5 – γ6 and γ8 – γ9 are statistically different from zero at the 1 per cent level.

Discussion of Results

From Table 2, we see that US monetary surprises had an economically and statistically significant effect on Mexican equities. A one-basis-point increase in the federal funds target rate provoked nearly a seven-basis-point decline in the IPC. Accounting for outliers the magnitude drops to approximately three basis points, but the direction of the effect remains the same and the result is still statistically significant. Since we are using an event study methodology, these reactions from the IPC to US monetary surprises can be viewed as exogenous with the only assumption being that the Federal Reserve does not worry about IPC reactions when it implements monetary policy. This seems to be a relatively safe assumption since the Federal Reserve’s dual mandate concerns fluctuations in US unemployment and US inflation. Clearly, between the US and Mexico the transmission channels of US monetary policy to foreign equity markets exists.

Mexico Stock Return and Mexican Business Cycles

Continuing further, we investigate the credit channel theory as it applies to international borders. We find that surprise increases in the federal funds target rate have a negative effect on the IPC whether Mexico is in a recession or not. However, the size of this effect is larger if Mexico is suffering a recession. This result is robust to different measures of Mexican business cycles. If Mexico is not in a recession, the effect is not as robust. Given that the IPC reaction is greater to US monetary surprises, both statistically and economically, during economic downturns in Mexico than in economic expansions shows that the credit channel theory applies across international borders in the case of Mexico and the US. These results are shown in Table 3 and Table 4.

Mexico Stock Return and Mexican Business Cycles

In Table 5, we eliminate the possibility of US business cycles causing the innovations in the IPC. From this table, it is evident that there is no non-zero difference in the reaction of the IPC to US monetary surprises when Mexico is in different stages of the business cycle. In Table 6 and Table 7, we control for the possible comovements of the IPC and the S&P. Our results do not change. US monetary surprises are transmitted across the border to Mexico causing changes in the IPC and these surprises are greater in both magnitude and statistical significance when Mexico is experiencing a recession.

Concluding Remarks

We document the reaction of the IPC to US monetary shocks. Controlling for the comovement of the IPC with the S&P, we find that the IPC is responsive to the surprise component of US monetary policy. We also examine whether the IPC’s response depends on cyclical variations in the Mexican economy. Given that there are no official business cycle dates, we use two proxies. We find that for the popular recession measure of two or more consecutive contractions in real GDP the IPC reaction is asymmetric. That is, when the Mexican economy is experiencing negative real GDP growth, the Mexican equity market reaction to surprises in the FOMC announcements is greater than when the Mexican economy is not contracting. We also use a Markov-switching model to generate Mexican business cycle dates. Our original finding is robust to this measure.

These findings contribute to the literature by supporting the hypothesis that the credit channel applies across international borders and is certainly present in the case of the Mexican–US border. Credit-constrained firms in Mexico suffer the effects of US monetary surprises when the Mexican economy is in a recession more than when the Mexican economy is growing. The state of the Mexican economy is important.

Footnotes

Acknowledgements

We would like to thank Arabinda Basistha, Alex Kurov and Santiago Pinto for their advice. Additionally, we would like to thank two anonymous referees. Also, we are grateful to the assistance provided to us by our respective institutions, the Harley Langdale, Jr. College of Business at Valdosta State University and Franklin and Marshall College.