Abstract

Using high-frequency stock returns in the Indian banking sector, we find that the beta on jump movements substantially exceeds that on the continuous component, and that the majority of the information content for returns lies with the jump beta. We contribute to the debate on strategies to decrease systemic risk, showing that increased bank capital and reduced leverage reduce both jump and continuous beta with slightly stronger effects for capital on continuous beta and stronger effects for leverage on jump beta. However, changes in these firm characteristics need to be large to create an economically meaningful change in beta.

Keywords

Introduction

The risk of an investment is typically divided into two parts: idiosyncratic risk and systematic risk, which results from exposure to overall market shocks and is often represented as beta in a capital asset pricing model (CAPM) framework. The CAPM typically quantifies the co-movement of returns in an individual asset (or portfolio) with the market. However, the price process is also known to be a combination of continuous and jump components; refer Merton (1976) and plentiful references since. Jumps are the means by which new information may be incorporated into the market, and there is an emerging literature hypothesising that the CAPM beta for the jump and continuous components of the price process may differ. For example, Patton and Verardo (2012) provide a learning argument and empirical evidence for increased beta around the release of earnings information on individual stocks, and Todorov and Bollerslev (2010) provide evidence for 40 US stocks.

This article estimates continuous and jump betas for equities in the Indian banking sector using recent developments in high-frequency financial econometrics by Todorov and Bollerslev (2010). The application to individual stock prices in emerging market equities is novel; there is little literature on the high-frequency behaviour of emerging markets (the exceptions are for market indices in Chinese markets) (Liao, Anderson, & Vahid, 2010; Zhou & Zhu, 2012), and in Eastern European markets in Hanousek and Novotný (2012) and nothing on individual stocks in the financial sector. Yet, the emerging markets are critically important to the future of the world economy, and their financial sectors drive that development. Emerging economies, termed ‘the world economy’s 21 st century sprinters’ by The Economist leapt to producing over half of world output in the first decade of this century. India is one of the major drivers of this growth, with a large aggregate output, a vast young population and underutilised resources. The market for the Indian rupee has grown from 0.1 per cent of global turnover in 1998 to 1 per cent in 2013 (BIS, 2013), and in 2012 was among the top 10 global equity markets by market capitalisation. Indian markets have a number of important advantages over those of other BRIC economies with strong institutional structure, unburdened with the non-performing assets and ageing population structure of China, the Russian exposure to the Chinese slowdown or the high inflation of Brazil.

The Indian banking sector follows the British structure of banking, India is one of the English common law countries (Buchanan, English II & Gordon, 2011), and listed banks are not only under the purview of the Reserve Bank of India but also under the Securities and Exchange Board of India which ensures strong information disclosure to investors. Rathinam and Raja (2010) attribute the phenomenal growth in the Indian financial sector to legal development, improvements in property rights protection and contract enforcement and positive changes in the regulatory environment. The banking sector (commercial banks, regional rural banks, rural and urban co-operative banks) accounted for 63 per cent of India’s financial assets in the 2012–2013 financial year, with the remainder shared between insurance companies (19%), non-banking financial institutions (8%), mutual funds (6%) and provident and pension funds (4%). The 89 commercial banks operating in India in 2012–2013 consisted of 43 foreign banks, 20 local privately owned banks and 26 nationalised banks. The market is distinguished by significant government ownership in a number of banks, exposing 73 per cent of total banking sector assets to some degree of government investment. However, the sector is well-dispersed with a five-bank concentration ratio of 38 per cent in 2012–2013 and only one bank, the State Bank of India, with a significant dominance (17% of 2012–2013). The total deposits of the banking sector were 74.29 trillion Indian rupee representing 73.46 per cent of GDP at the end of the 2012–2013 financial year, employing over 1 million employees across 92 thousand bank branches/offices. 1

We initially confirm the existence of jumps in the 5-minute stock returns for 41 banks listed on the National Stock Exchange of India over 2004 to 2015, providing the motivation for our estimation of separate continuous and jump betas. The estimated jump beta is generally higher than the corresponding continuous beta, supporting the hypothesis that stocks behave differently in response to jumps than continuous market movements. When testing the validity of the disentangled betas against the CAPM standard beta, we find that it is the jump beta rather than the continuous beta which has explanatory power over the variation in stock returns, leading to the conclusion that the predictive power of CAPM beta comes mainly from the jump component.

We relate the variation in betas to firm characteristics and find that financial leverage, capital adequacy and firm size have significant impacts on each of the jump and continuous beta estimates. These relationships are informative for the debate about reducing systemic risk via options to constrain leverage or increase the capital base of the banking sector. We show that financial leverage has a positive effect on beta, indicating that a more heavily leveraged firm is more exposed to market movements, although we demonstrate that the impact of changes in leverage are economically very small. Greater capital adequacy reduces both jump and continuous beta, but again requires relatively large changes to have a substantial economic effect. Thus, our results support the direction of the impact of policies to decrease leverage and increase the capital base on reducing systematic risk, but throw some doubt on the size of the changes needed to obtain an effective impact in reducing risk in the financial sector.

Competing hypotheses on firm size suggest that either larger firms are more stable and able to weather market shocks more easily, or that as they are a substantial part of the market they are more exposed to market shocks. Our results support the hypothesis that larger firms are more exposed with higher beta, but this effect is more evident for continuous movements; the effects for jump beta are statistically significant but smaller. Our estimates also find that price volatility is a contributing factor for higher continuous beta, but not jump beta, and that more profitable firms have lower continuous and jump beta although the relationships are not statistically significant in contrast with the hypothesis that these firms may be taking more risk to achieve these profits.

The rest of the article is organised as follows. Second section reviews the literature related to the decomposition of CAPM and third section elaborates the methodology employed for jump detection and beta estimation. We outline data collection and cleaning process along with choices of calibrated parameter value in fourth section. Fifth section discusses the results of the empirical analysis and sixth section concludes.

The CAPM and Decomposition of Beta

The CAPM (Sharpe, 1964) and Lintner (1965) model the return on an asset (or portfolio of assets) as a linear combination of return on the risk-free asset and a market risk premium multiplied by the associated beta. The CAPM beta itself is estimated as the covariance between the asset return and market return, standardised by the variance of market return. A subsequent large literature of empirical studies shows mixed results on the effectiveness of beta in explaining the variation of stock returns. A number of alternatives have been proposed to improve empirical CAPM including multi-factor models, such as the three factor model of Fama and French (1993), arbitrage pricing theory by Ross (1976), incorporating higher order co-moments (Faff, Ho, & Zhang, 1998; Friend & Westerfield, 1980; Harvey & Siddique, 2000; Kraus & Litzenberger, 1976), CAPM conditional on market conditions (such as Fabozzi & Francis, 1978), and CAPM with time varying beta (such as Bollerslev, Engle, & Wooldridge, 1988; Fraser, Hamelink, Hoesli, & MacGregor, 2000).

This article takes the approach of decomposing the price process into a continuous and jump component consistent with recent evidence (refer to, Aït-Sahalia & Jacod, 2012; Andersen, Bollerslev, & Diebold, 2007; Barndorff-Nielsen & Shephard, 2004b, 2006; Dungey, McKenzie, & Smith, 2009; Huang & Tauchen, 2005), and consequently estimating betas on the two components using the method developed in Todorov and Bollerslev (2010).

The standard one factor CAPM relates the return of individual stocks to the return of the benchmark market portfolio as follows:

where ri is the return of the ith asset, and r0 denotes the return of the market portfolio which represents the systematic risk factor. The βi coefficient quantifies the sensitivity of the asset return to the movement of the market return.

Decomposing the market return into continuous and jump components suggests the following form:

where the market return r0 is decomposed into the continuous market return,

The calculation of jump beta is motivated by the fact that the price process of any asset is a combination of a Brownian semi-martingale plus jumps. Denoting the return of an asset as dptt, where pt is the log-price series, the continuous-time model for the asset return is as follows,

where μt is the drift term, σt represents the spot volatility and Wt is a standard Brownian motion. The third term, ktdqt captures the jumps in the price process, where qt is a counting process with dqt = 1 if there is a jump occurred at time t, and 0 otherwise. kt is the size of the jump at time t. The quadratic variation for the process in Equation (3) is defined as follows,

In practice, we can only observe the asset price at discrete time intervals, say, every ∆

n

interval. Hence, the observed return series becomes

Barndorff–Nielsen and Shephard (BNS) (2004b) introduce an alternative measure, realised bi-power variation, defined as follows,

where µ = 2/π =

As first proposed by BNS (2006), the discrepancy between RV[0,T] and BV[0,T] is utilised to detect the presence of jumps. We apply their adjusted ratio test statistic. The feasible test statistic of jump detection is given by following equation,

where

We reject the null hypothesis of no jumps if the test statistic is significantly negative.

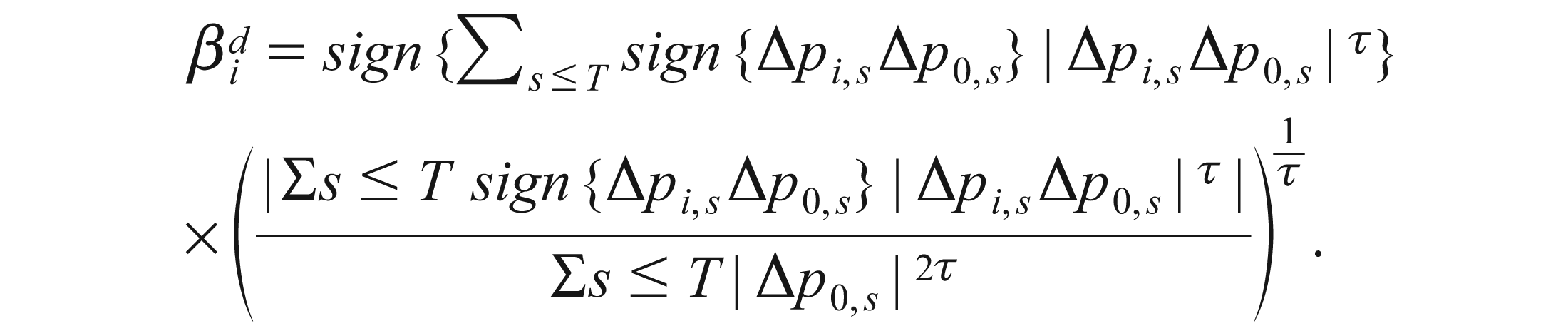

The detection of jumps paves the way to separately estimate continuous and jump beta. Todorov and Bollerslev (2010) derive the non-parametric estimates of both

In reality, observing price data on continuous basis is not possible. Therefore, the estimator of

where

For the discontinuous price movement, Todorov and Bollerslev (2010) show that the jump beta of the ith asset,

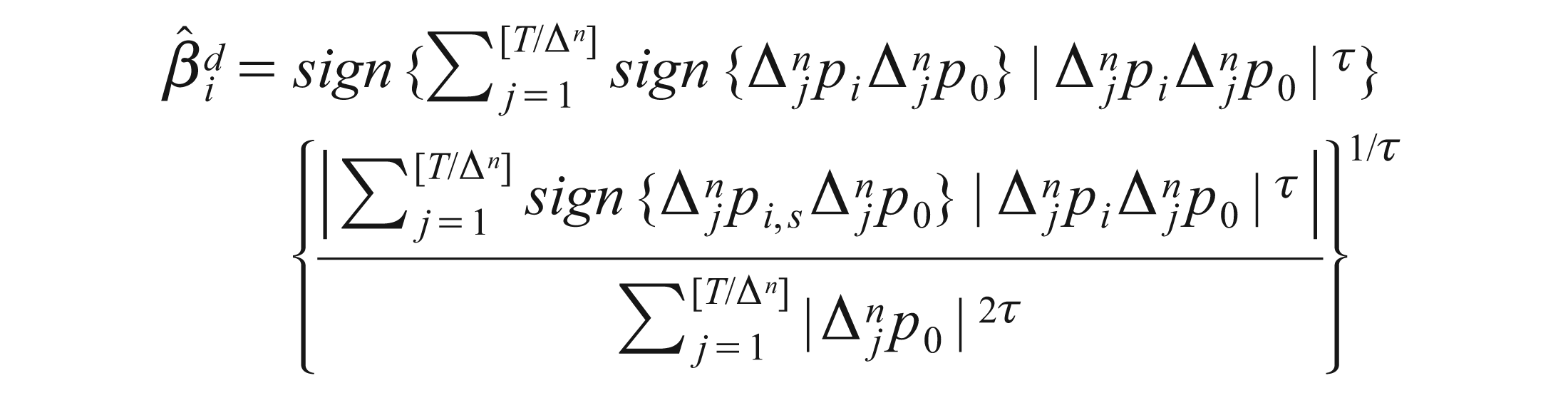

The discrete time estimator

where i = 1, …, N, and the power τ is restricted to be τ ≥ 2, so that the presence of continuous price movements becomes negligible asymptotically, and only the discontinuous movements matter. Todorov and Bollerslev (2010) show that

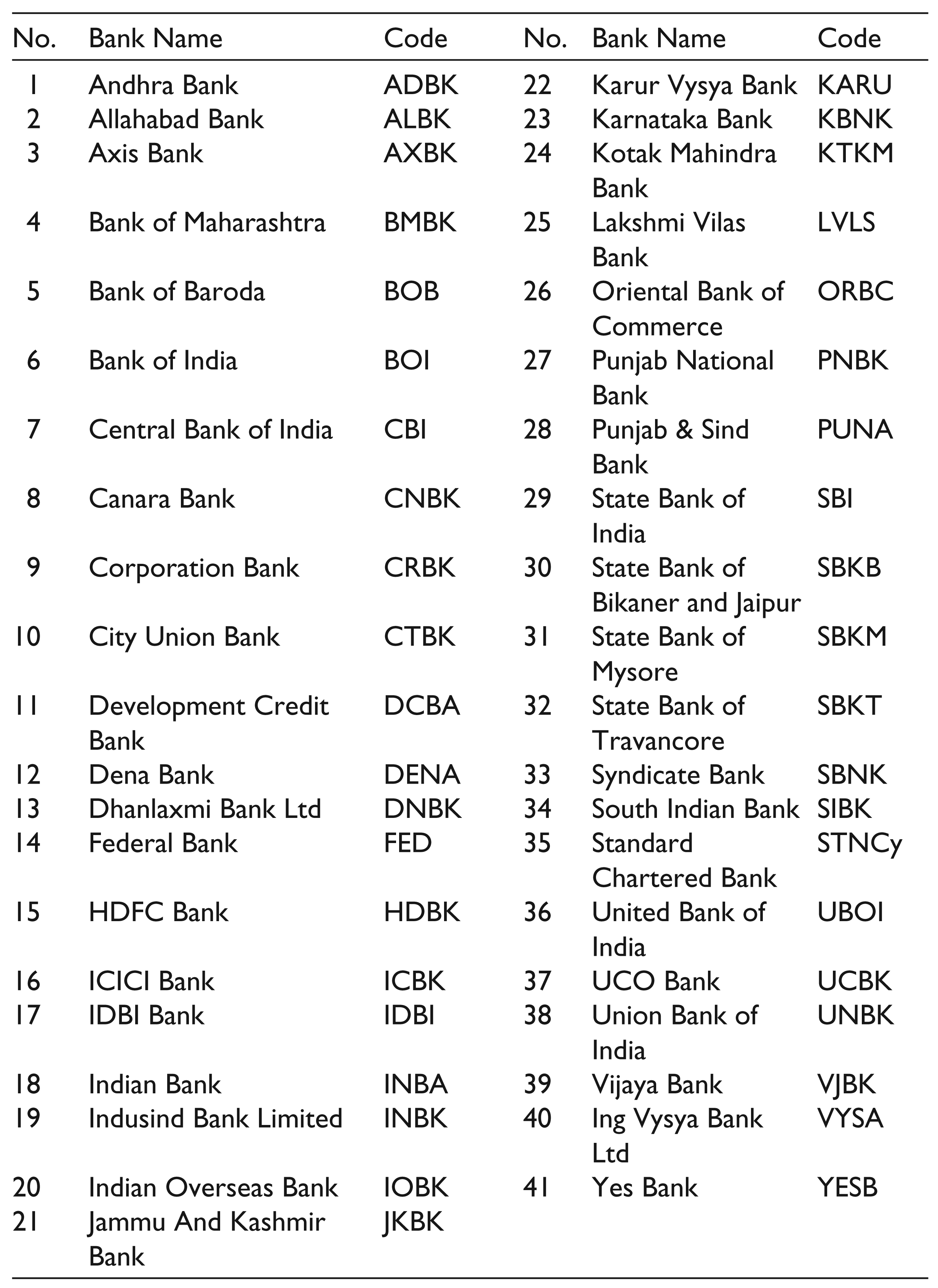

The high-frequency stock price data are extracted from the Thompson Reuters Tick History (TRTH) database provided by SIRCA for the sample period from 1 January 2004 to 31 December 2015. We collate data on 5-minute stock returns for 41 commercial banks listed on the National Stock Exchange (NSE) of India shown in Table 1. The NSE was established in 1990 and soon became an important exchange by providing a fully automated screen-based trading system. It is now the largest stock exchange in India in terms of daily turnover and number of trades, and ranks second in terms of total market turnover, behind the Bombay Stock Exchange, with turnover in July 2013 of USD 0.99 billion.

Banks listed on the NSE

Banks listed on the NSE

The sampling frequency of 5 minutes is relatively standard in the high-frequency literature. It provides a reasonable compromise between the need to sample at very high frequencies to resemble the continuous price process (Andersen, Bollerslev, Diebold, & Labys, 2001), and possible contamination from micro-structure noise. The literature developing optimal sampling frequency for the analysis of multiple assets, with or without noise, is on-going.

We use the last price recorded in each of the 5-minute interval from 9:15

We apply the calibrated parameter values implemented by Todorov and Bollerslev (2010) and Alexeev, Dungey and Yao (2017). Following those authors, we estimate both daily and monthly betas, so that T = 1 represents one day in the first case and one month in the second. As ∆

n

is the reciprocal of the number of observations during a given period, it equals 1/72 for daily estimation but varies from month to month; for example, ∆

n

equals to 1/1584 in a month with 22 trading days. The threshold values, un are chosen by taking ω = 0.49. We implement

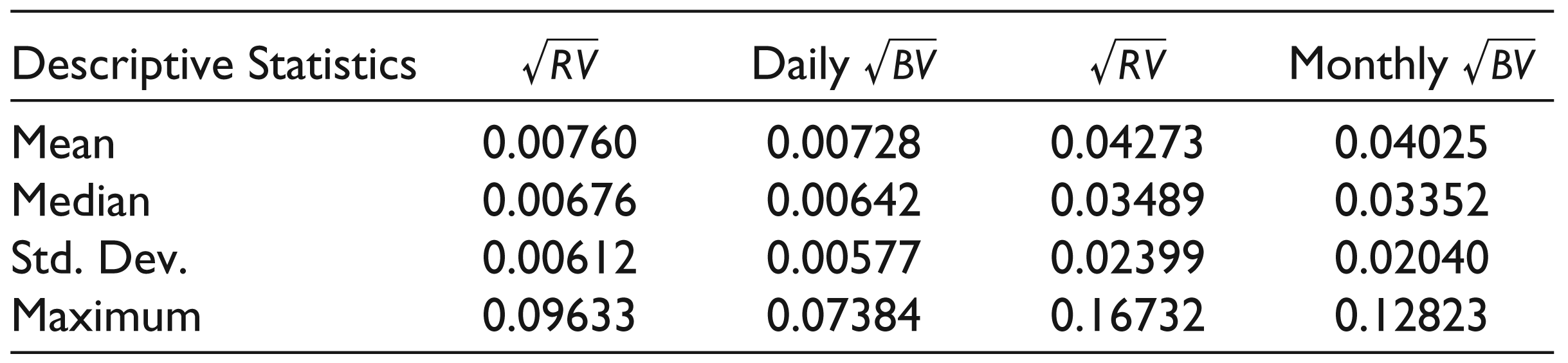

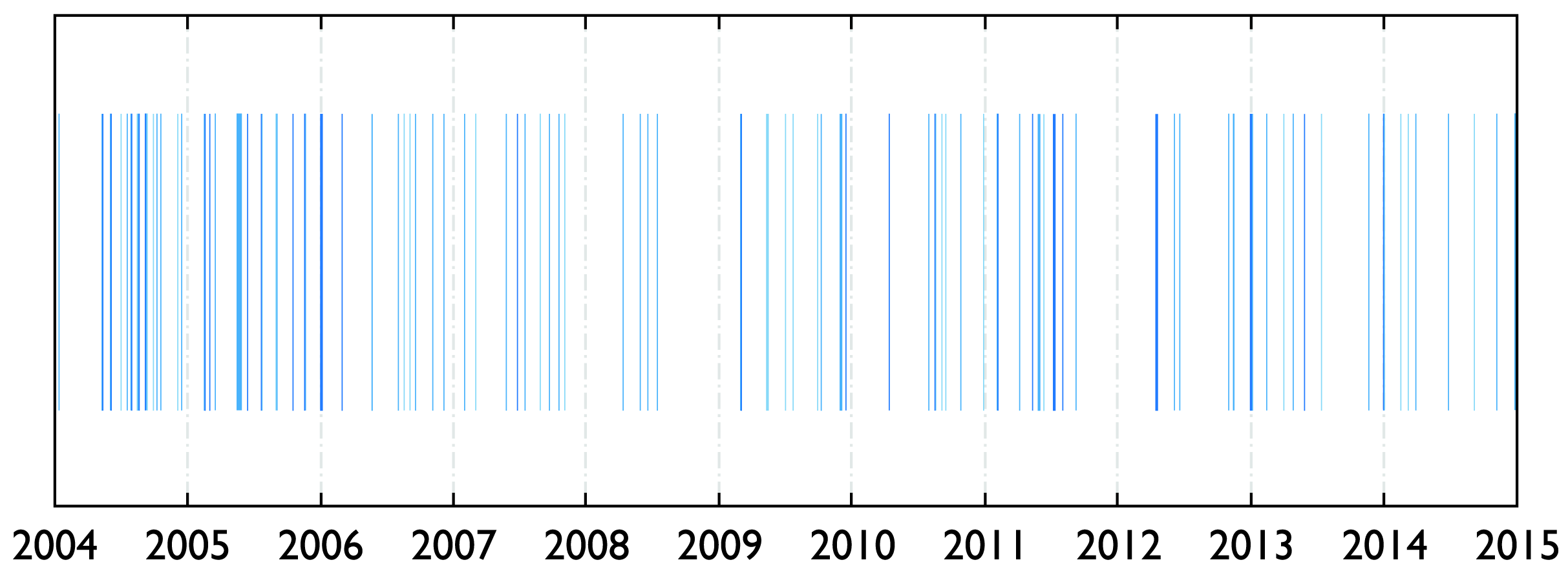

The first step in the empirical analysis is to determine the existence of jumps in the Indian market. Table 2 reports the descriptive statistics of the two daily volatility measures RV and BV of the CNX500 and Figure 1 depicts the occurrence of jump days detected using the BNS test in the market index throughout the sample period of 2004–2015.

Within our sample period from 2004 to 2015, we find 136 jump days out of 2,904 trading days in the market index, that is, in 4.68 per cent of our sampled trading days. This percentage is lower than the percentage reported by Todorov and Bollerslev (2010) for the US market using a test statistic based on the difference between RV and BV (106 out of 1,241 days or 8.54%). However, our percentage is higher than the reported proportion of Alexeev et al. (2017) who apply the same test statistic in (8) to the US market. We cannot verify our results with any literature on Indian market as this is the first study of jump detection for this market. However, the proportion of jump days reported by Zhou and Zhu (2012) for China is similar to our results. Applying the same methodology, they report 2.25 per cent jump days for the SSE A Share Index, and 5.75 per cent jump days for the SSE B Share Index. Of the 144 months in our sample, 87 months have at least one jump day.

Volatility Measures for Indian Market during the Sample Period 2004–2015

Volatility Measures for Indian Market during the Sample Period 2004–2015

The number of jump days in the CNX500 index decreases gradually from 2004 (22 days) to 2008 (4 days), then increases in 2009 (13 days), and remains stable afterwards; refer Figure 1 for a depiction. During the global financial crisis (GFC), there is no evidence of a notable increase in the number of jump days. In fact, during 2008, when the GFC was at its nadir, the Indian market experiences a lower number of jumps than the adjacent years. This result may indicate the resilience of Indian market against global shocks, although Bianconi, Yoshino and de Sousa (2013) and Mensi, Hammoudeh, Reboredo and Nguyen (2014) show that the USA and global crisis spread through the BRIC countries including India. However, a number of studies show similar reductions in the number of jumps detected during the crisis period compared with the prior tranquil period; Barada and Yasuda (2012) and Chowdhury (2014) for the Japanese market, Novotný, Hanousek and Kocenda (2013) for six mature and three emerging stock market indices, Black, Chen, Gustap and Williams (2012) and Alexeev et al. (2017) for the US stock market. An alternative explanation, supported by these studies, is that during the crisis period the threshold of jump identification increases with the overall market volatility and some price discontinuities that may be classified as jumps during the tranquil period may be classified as continuous movements during the crisis period.

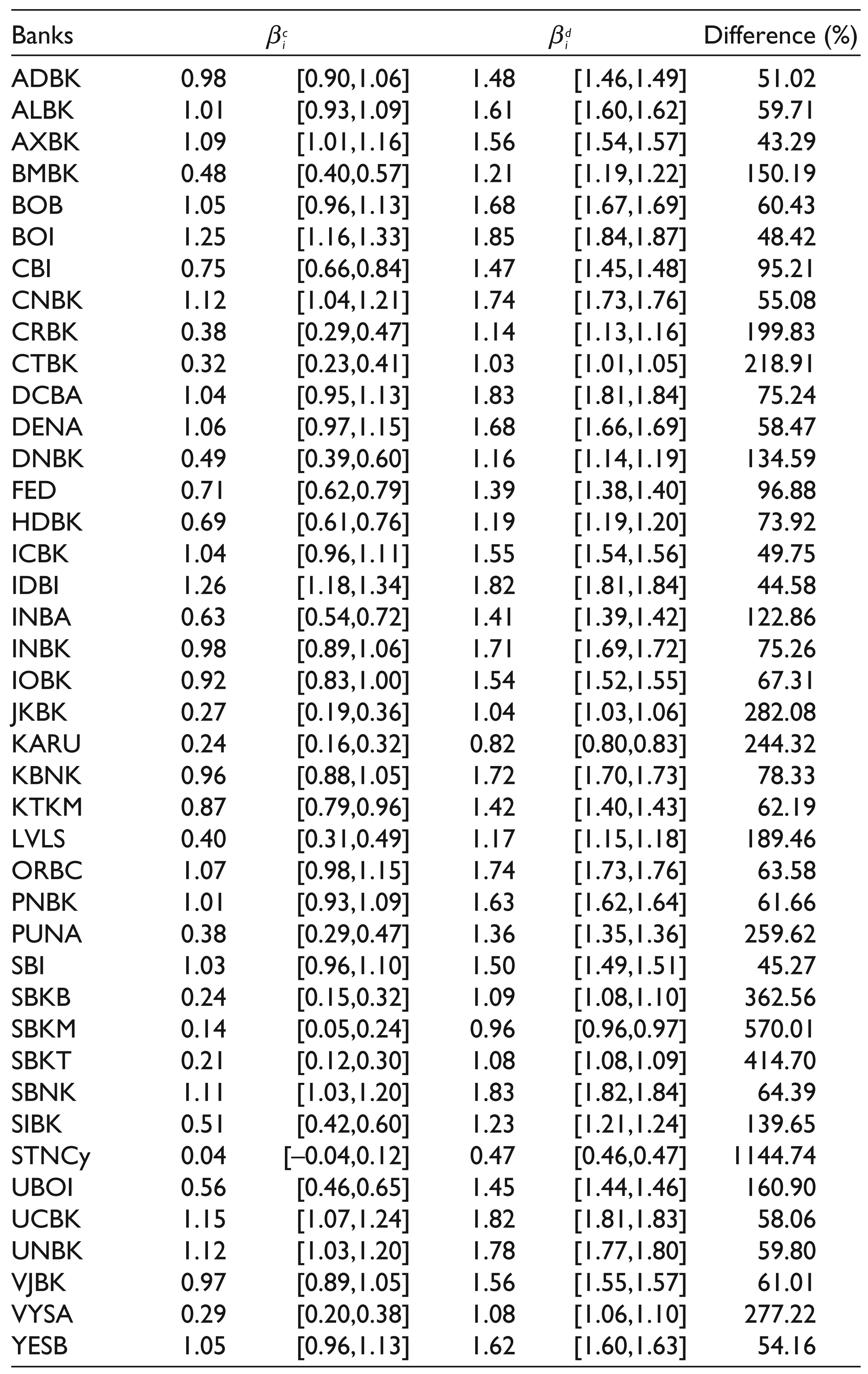

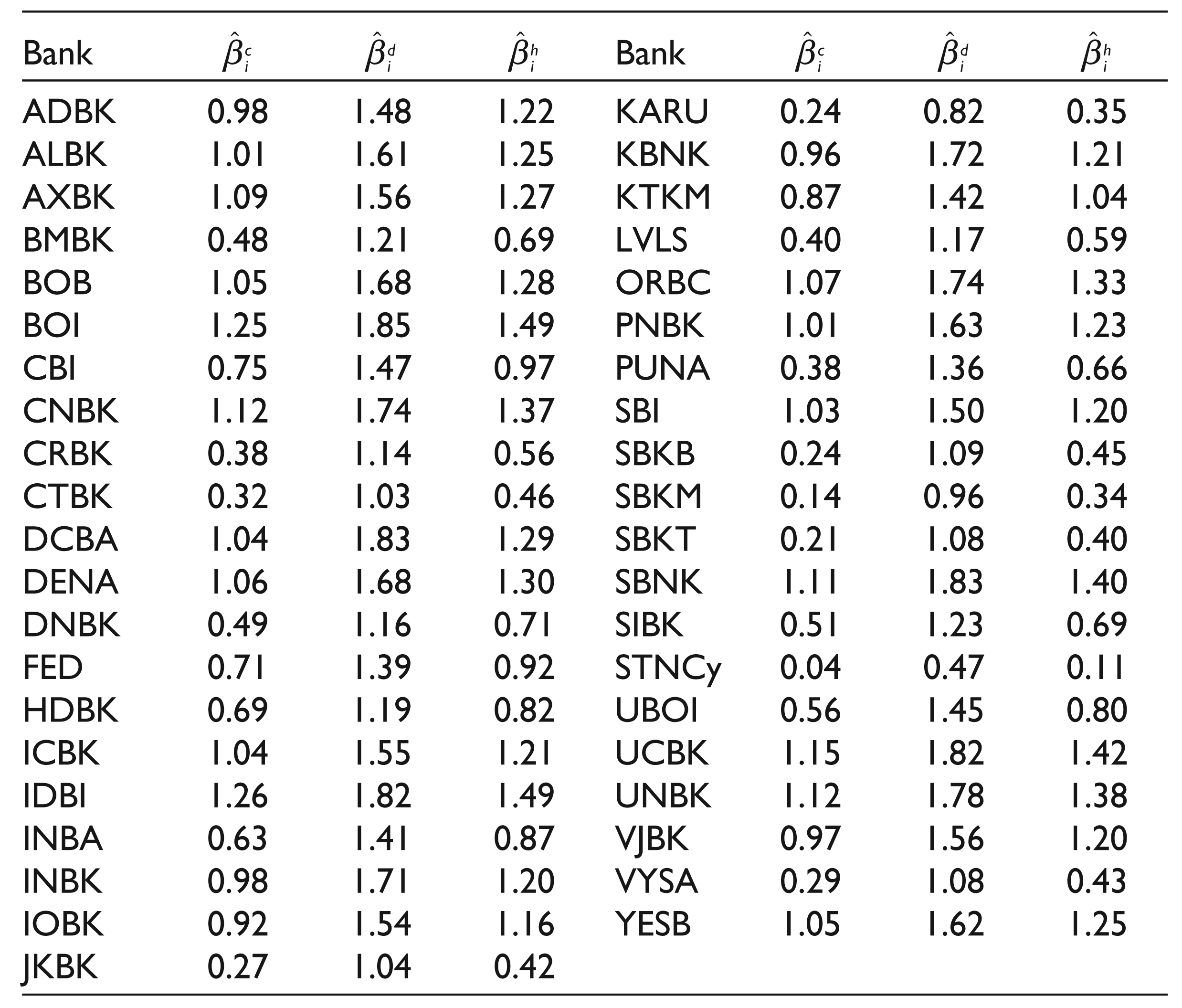

Table 3 shows that for each of the banks the monthly average-estimated jump beta,

Of the 41 banks in our sample, 38 have an average jump beta larger than one. This indicates that the returns of banking stocks move more than the return of the market itself when the market experiences jumps. The DCBA is the bank with highest average jump beta (1.92) followed by IDBI (1.74). The bank with lowest average jump beta is STNCy (0.63), consistent with its very low continuous beta, followed by KARU (0.81).

Average Continuous and Jump Betas for Listed Indian Banks

Average Continuous and Jump Betas for Listed Indian Banks

The jump betas of all banks are on average 159 per cent higher than their continuous betas, and the columns of average confidence intervals of continuous and jump betas in Table 3 show that there is no overlap between the confidence intervals of

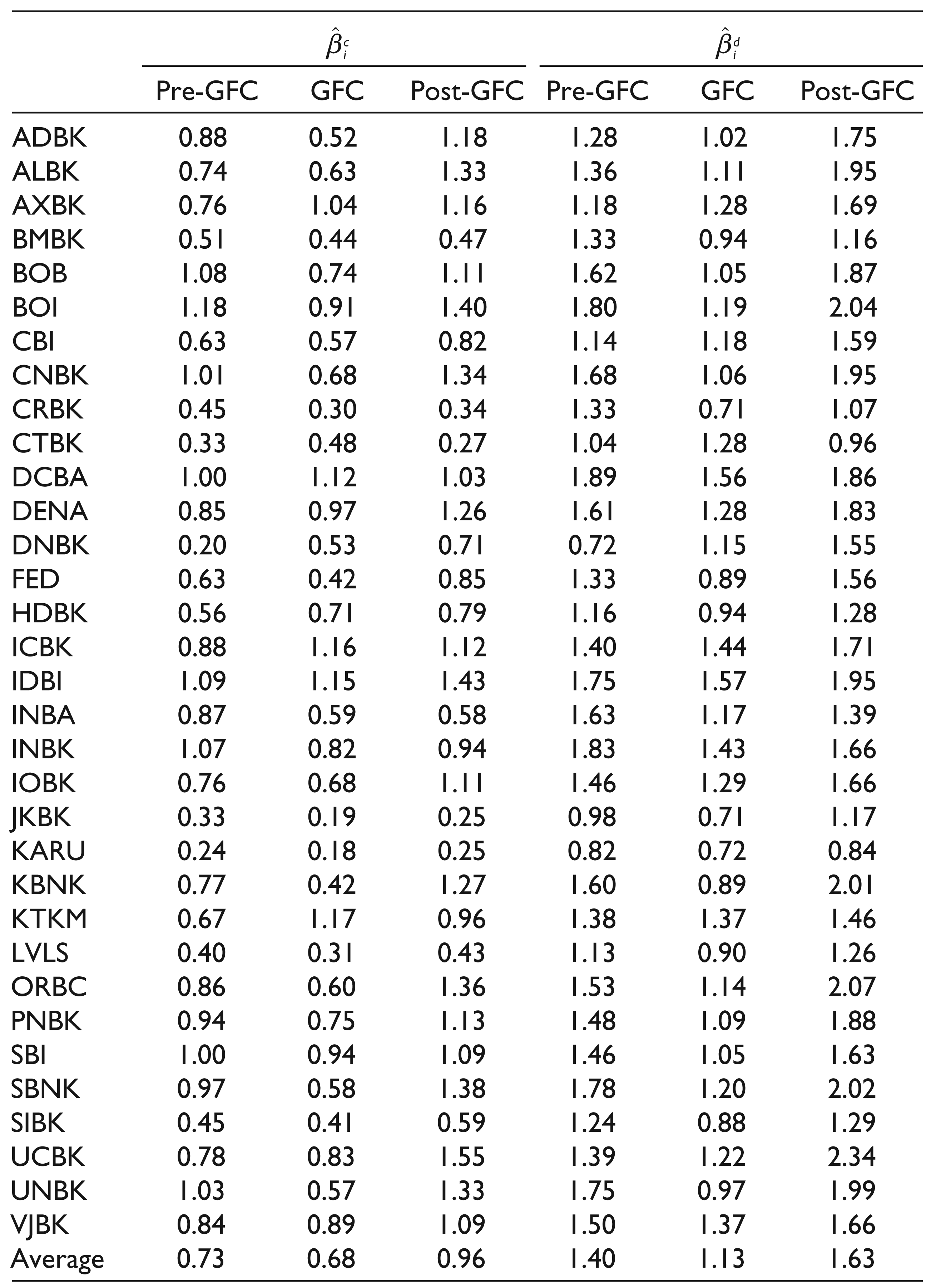

Average Continuous and Jump Betas during the Pre-GFC, GFC and Post-GFC Periods for Listed Indian Banks. The Banks which were not Listed on NSE for the Full Sample Period are excluded here.

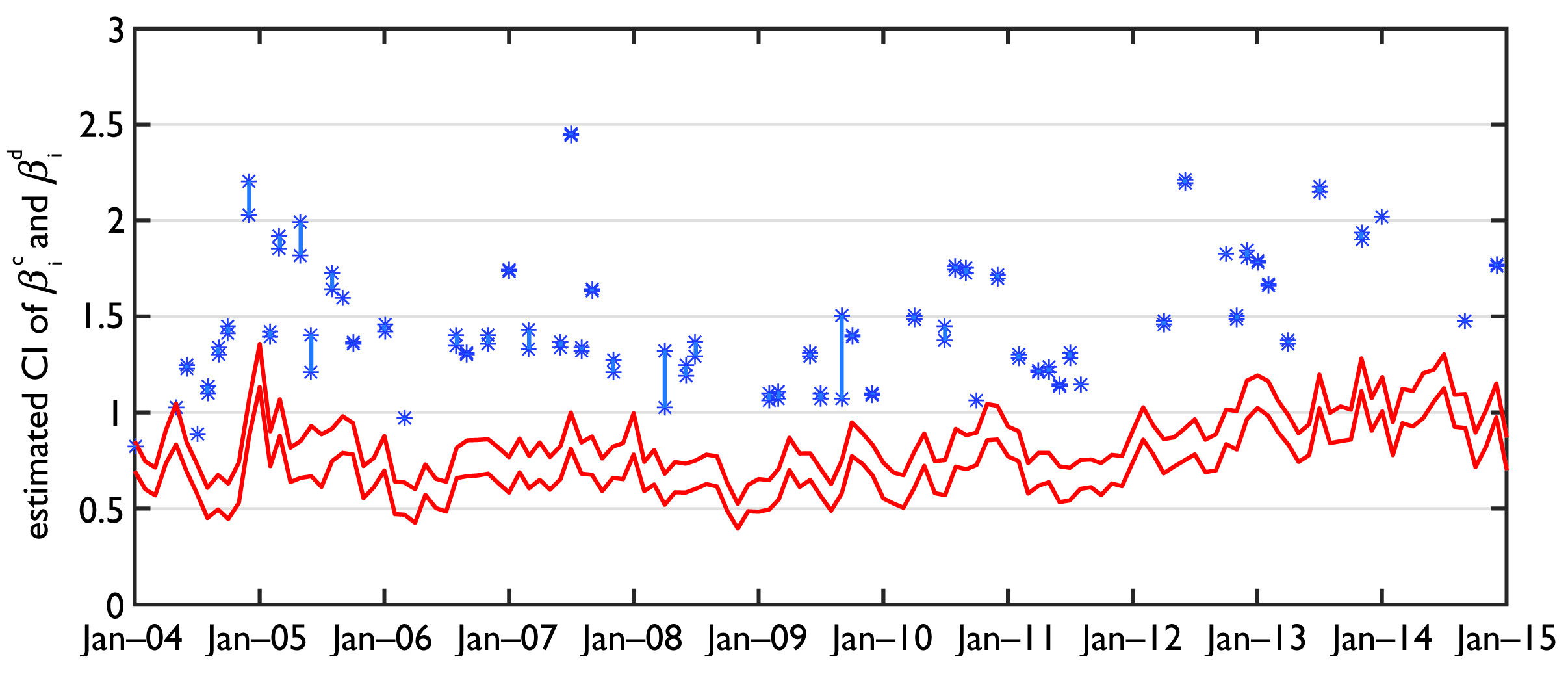

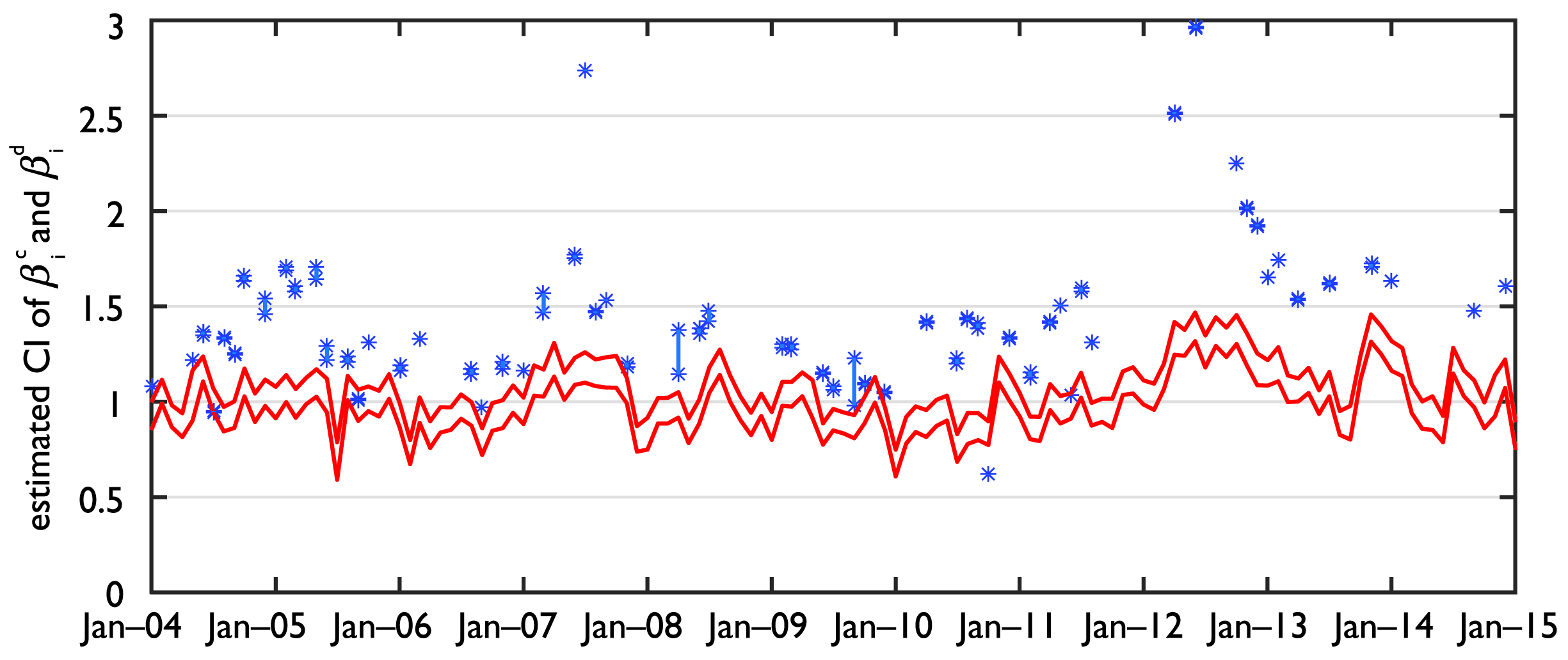

We may expect that changes in the beta estimates caused by the GFC since 2008. Hence, we divide our full sample into three sub-periods: pre-GFC (January, 2004 to August 2008), GFC (September, 2008 to March, 2010) and post-GFC (April, 2010 to December, 2015), and calculate the average beta estimates for the three sub-sample periods. Results for each bank are shown in Table 4. The range of the beta estimates varies considerably for each individual bank. For example, the continuous beta for KARU during the GFC is as low as 0.19, while for DCBA and IDBI, the continuous beta estimates are consistently above unity in any sub-sample periods.

For most banks, the average continuous and average jump betas of banking stocks decrease during the GFC from the pre-GFC period. However, these betas increase after the GFC and rise above the pre-GFC level. This pattern of changes is more prevailing for jump beta than continuous beta. However, it contradicts what we would expect from the financial contagion literature that co-movements among assets during crisis would become stronger. On the other hand, this phenomenon could be explained as a distinctive feature of an emerging market compared to well-developed financial markets. As the banking sector was hit particularly hard by the crisis, investors of these stocks may refrain from trading. Consequently, these stocks may become detached from the market resulting in lower betas.

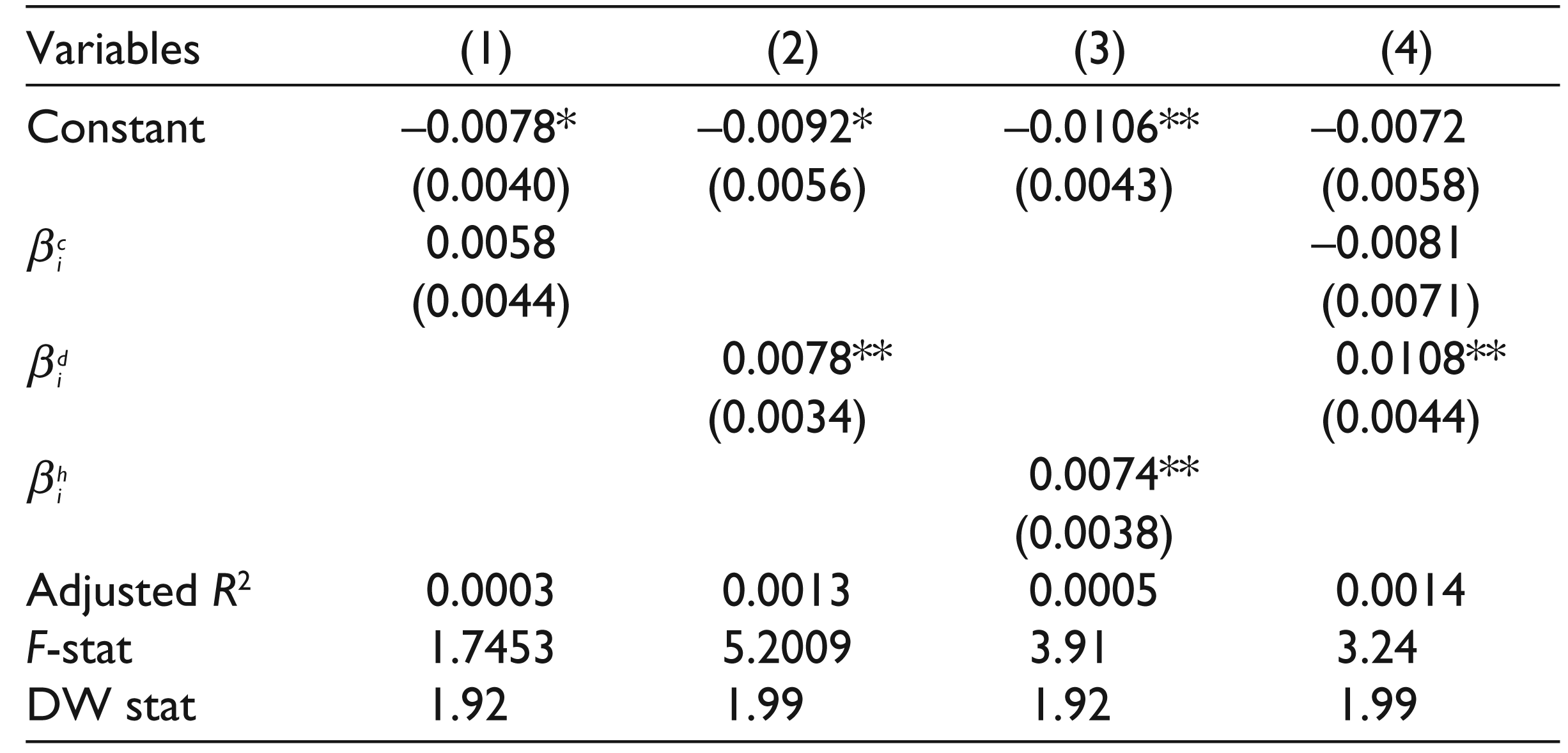

The estimates of beta are now considered with respect to their explanatory power for observed stock returns (refer, e.g., Black, Jensen, & Scholes, 1972; Fama & MacBeth, 1973). The usual approach regresses the standard CAPM beta on stock returns, using a pooled OLS approach, as follows

where

where dpi indicates stock returns, and

We first estimate monthly standard single factor CAPM beta to compare the results with the disentangled betas. The average values of the estimated standard CAPM betas

Average Monthly Continuous, Jump and Standard CAPM Betas for Indian Banks

The results imply that the predictive power of CAPM beta is derived mainly from its jump component rather than the continuous component. The regression results for Equations (14) and (15) are reported in Table 6. We find positive and significant coefficients of only jump and CAPM betas but not for continuous beta in univariate regressions shown in models (1), (2) and (3). When we regress the stock returns on continuous and jump betas together as shown in model (4), jump beta remains significant, the continuous beta again do not have a significant coefficient. 4

Impact of Continuous and Jump Beta on Stock Returns

b All models are estimated using pooled OLS regression with the dependent variable monthly stock returns. The number of banks included cross section is 41. The number of periods is 144 in regression 1 and 3 and 87 in regression 2 and 4.

There is substantial heterogeneity in the estimated continuous and discontinuous betas across the banks although they belong to the same industry. Patton and Verardo (2012) suggest that the variations in beta are associated with firm-specific news and stock fundamentals. We hypothesise that firm characteristics may contribute to the variations in the bank betas. The size of the banks, their profitability, leverage, capital stock against risky assets and ownership may contribute to the estimated differences.

The Basel regulatory framework advocates higher capital stock as a buffer against risky assets for banks implying that banks with higher capital adequacy ratios (CAR) should have lower chance of failure and hence be more resilient to risks arising from the market. Our first hypothesis is that CAR is negatively related to the systematic risk of banking firms.

Leverage, on the other hand, has been argued to increase systematic risk through correlation with business cycle conditions. Buiter and Rahbeir (2012) argue that leveraging is positively related to long-lived and costly systemic risk. Thus, our second hypothesis is that leverage is positively related to the systematic risk of banks.

Larger banks may be able to withstand market downturns via their ability to diversify and increase market power, and hence the third hypothesis is that larger firms have a lower beta. Profitable firms may exhibit stable price behaviour, stemming from the confidence that investors bestow on these stocks, making profitable firms less volatile than the market as a whole, leading to hypothesis four that higher profitability is negatively related to beta. Finally, we test whether similarly private versus government ownership reduces or increases the systematic risk of a bank, as investors may have different degrees of confidence on these two ownership modes.

Incorporating these firm characteristic factors, we estimate the following regression model:

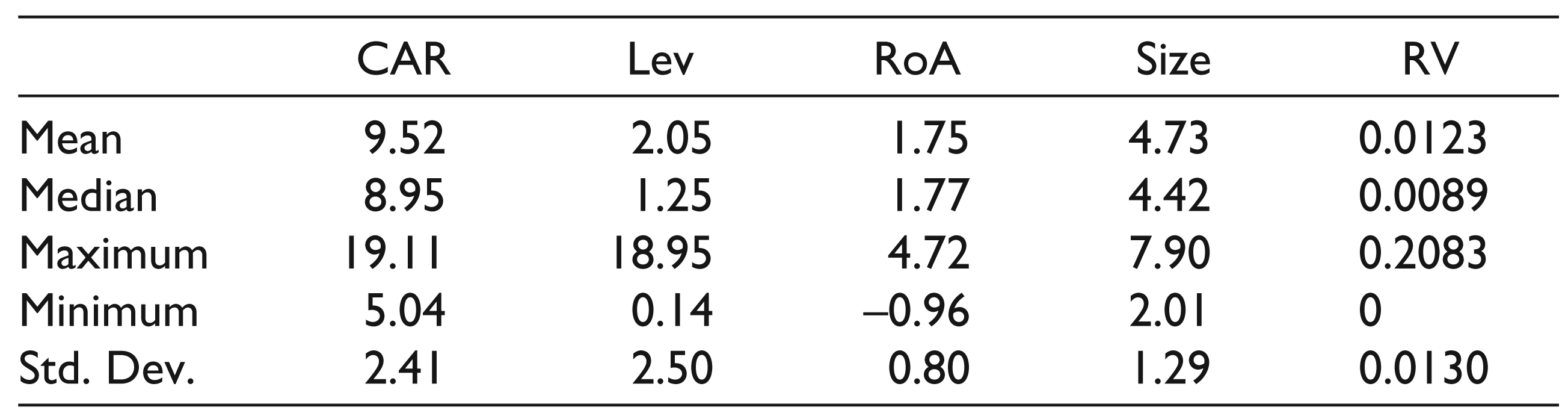

for both jump and continuous betas separately, where Xi,t are the firm characteristic variables of ith bank at time t. We collect data on the firm characteristics for 23 Indian banks from Datastream and regress the jump beta or continuous beta on firm size, profitability, leverage, ownership and CAR separately. Firm size is represented by market capitalisation in log form. Leverage is computed as the ratio of total debt to market capitalisation. Profitability is measured in percentage of the return on assets (RoA), computed as earnings before interest tax and depreciation and amortisation (EBITDA) divided by market value of assets. We use a dummy variable for nationalised versus private ownership of the banks and CAR is directly extracted from Datastream. The summary statistics for the firm characteristics are reported in Table 7.

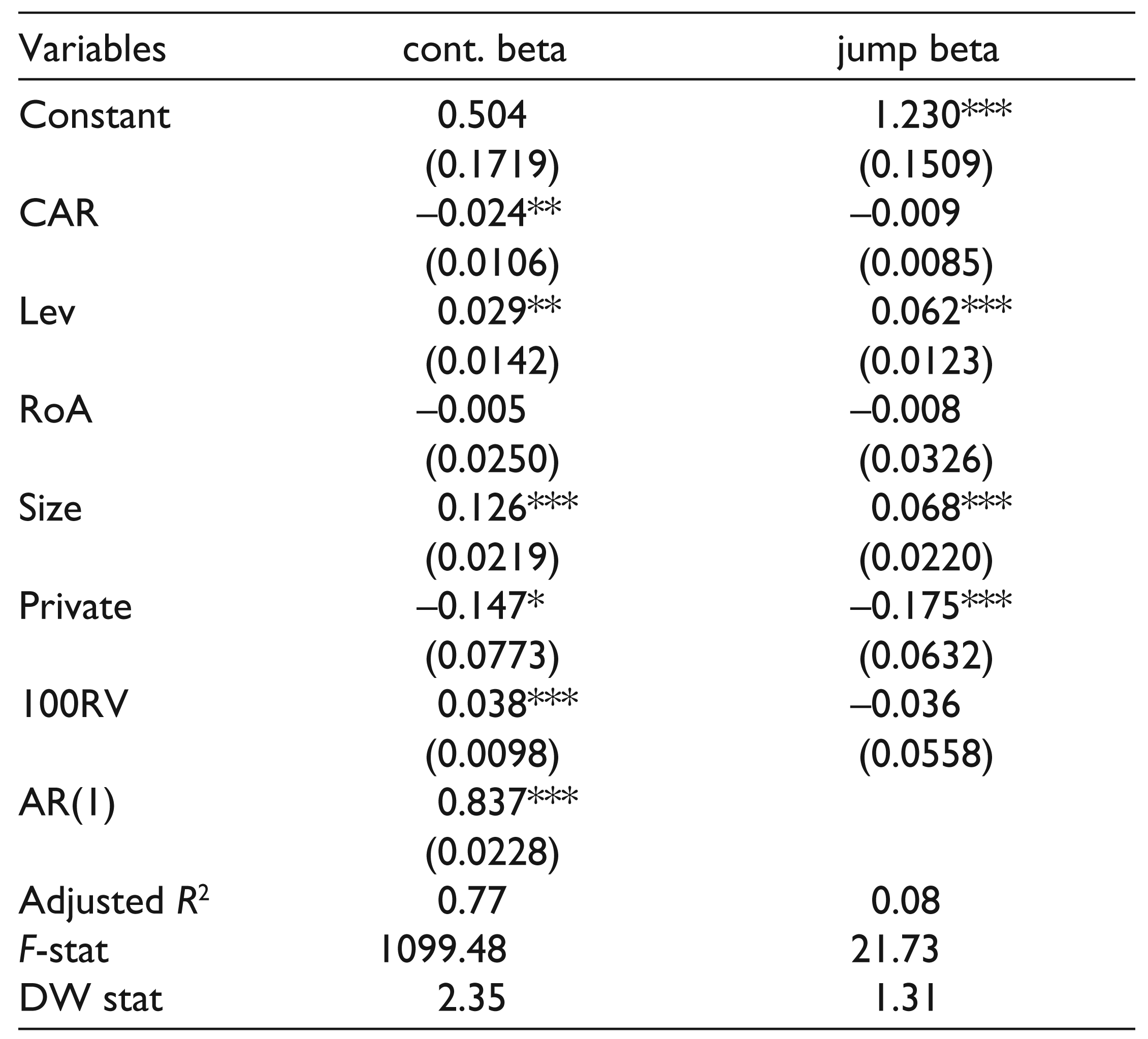

Table 8 reports the regression results on the relationship between betas and firm characteristics. The first column reports the results for continuous beta and the second column reports the results for jump beta. In the continuous beta specification, we additionally include an AR(1) term to tackle the autocorrelation in the error term. The table reports White-adjusted standard errors.

Summary Statistics of Firm Characteristics

Relationship Between Firm Characteristics and the Betas

b Both models are estimated using pooled OLS regression. The number of banks is 23, and the number of periods is 144 for models of

The results in Table 8 show that relationship between continuous beta and leverage is positive and significant, at the 1 per cent significance level, while the relationship of continuous beta with CAR is negative and significant at the 5 per cent level. A decrease of one unit in the leverage ratio is estimated to lead to a decrease of 0.03 in the continuous beta, assessed at the mean value of leverage, this is equivalent to a decrease in the leverage ratio for Indian banks from 2.05 to 1.85 resulting in a decrease in continuous beta of 0.006. It is immediately apparent that a large change in leverage would be required to alter beta to an economically meaningful extent. Similarly, although the relationship between continuous beta and CAR is statistically significant, and negative; the change required in CAR to obtain an economically meaningful reduction in beta is relatively large; an increase in CAR from its mean value of 9.52 to 10.52 results in a small 0.02 decrease in continuous beta.

Size and volatility have significant effects on continuous beta. The positive coefficient of market capitalisation indicates that banks of larger size show higher sensitivities towards continuous market movements. The negative coefficient of profitability (RoA) indicates that less profitable banks have higher continuous systemic risk though the coefficient is not statistically significant. The volatility measure, RV, is a significant and positive factor for the continuous beta, indicating that higher price volatility results in higher continuous risk for these banks. Private versus government ownership (Private) has significant and negative relationship with continuous beta at 10 per cent significance level, implying that government-owned banks are more sensitive than public sector banks towards continuous market movements.

Among the explanatory variables, leverage and size and ownership have significant effects on jump beta, whereas CAR, RoA and volatility, however, do not. The signs are the same as those for the continuous beta estimates; thus, decreased leverage and size and government ownership increase jump beta. The effects of CAR are smaller than in the continuous case and statistically insignificant, thus increasing bank capital has even lower impact here on reducing the reaction to market discontinuities than in the continuous case. The leverage effect is only slightly higher than in the continuous case. Though the coefficient on size almost halves for jump betas compared with continuous betas, in both cases larger firms have lower betas than their comparator firms supporting the hypothesis that larger firms are less able to diversify away from the market. The insignificant coefficient of RoA in both case of betas fails to support the hypothesis that profits provide a buffer from unexpected market movements.

Our investigation quantifies the importance of the well-recognised decomposition of financial price movements into continuous and jump components. We test whether separating the beta estimates for these two components is warranted and unambiguously reject the hypothesis that the jump beta and continuous beta are the same using data for the Indian banking sector. The evidence strongly suggests that jump beta is higher than continuous beta, and that it has more explanatory power over returns, consistent with the view that discontinuities in financial prices are indicative of new information entering the market as in Patton and Verardo (2012) and the evidence for US markets in Todorov and Bollerslev (2010) and Alexeev et al. (2017).

We estimate the continuous and jump betas for an emerging market, and moreover, the banking sector of that market which bears a high responsibility for effectively funding future growth in India. Investigating the banking market specifically ties our results firmly to propositions for reducing systematic risk in that sector, with a view to reducing systemic risk in the economy as a whole. We find that recent proposals to reduce systemic risk via increasing capital requirements or reducing leverage in the banking sector would have the desired effect of reducing the systematic risk in the sector for both continuous and jump betas, but either the changes in capital or leverage required to produce economically meaningful results are very large or there is a substantial non-linearity in the relationship between these variables and systematic risk which is not captured by either this or other existing frameworks.

New tools allow the separate estimation of the beta on the continuous and jump component of the underlying price process, which characterises financial market data. The small existing literature for the USA in Todorov and Bollerslev (2010) and Alexeev et al. (2017) estimate higher jump beta than continuous beta. This article confirms a similar finding for Indian banking stocks. The focus on the Indian banking sector links the results to an important emerging economy with a high reliance on the banking sector for funding future growth, and contemporary issues concerning regulatory proposals for reducing systemic risk in international banking sectors.

Using 5-minute stock price data for 41 listed Indian banks for 2004–2015, we establish evidence of jumps in the Indian equity markets, consistent with existing evidence for developed markets and as yet a small range of equities in emerging market. The results show that the proportion of days containing a jump, at 4.68 per cent of trading days, is not dissimilar to the evidence for developed economies and that the proportion of jumps did not increase during the GFC, also consistent with the small existing literature concerning jump behaviour during crisis periods.

The estimates of separate continuous and jump betas for the Indian banks show that on average jump beta exceeds continuous beta by 159 per cent, and the confidence band on these estimate rarely overlap for any of the individual stocks. We conclude that the reaction of individual stocks to discontinuities in the market indicator price is substantially higher than the reaction to continuous movements. This is consistent with the documented strong association of jumps with news events, particularly unanticipated news, and the learning model posited in Patton and Verardo (2012), which anticipates temporarily increased beta for stocks around the time of earnings announcements. Our study differs from theirs in that we condition the differing beta estimates on the existence of jumps, rather than on the existence of a news announcement (there is clearly overlap between these groups but it is by no means complete).

The estimated continuous and jump betas are related positively to firm size and leverage, and negatively to capital adequacy and profitability. Smaller profitable firms, with lower leverage and strong capital will have lower betas. However, the effect of size on beta is twice as large for continuous beta than jump beta, whereas the effect of profitability is twice as strong for jump beta than continuous beta. These findings have bearing on the debate concerning future regulatory practice for the banking sector in reducing systemic risk. Our results show that proposals to increase bank capital and decrease leverage will act to reduce the systematic risk in the Indian banking sector, with capital slightly more effective against continuous risk and leverage slightly more effective against jump risk, but the extent of the reduction in betas that can be produced in this manner are economically quite small. If the linear specification proposed in this article is correct, the required reduction in leverage or increase in capital to produce an economically meaningful impact on jump or continuous beta is beyond the scope of current policy discussions. The behaviour of beta in response to leverage and capital would need to be highly non-linear to prompt the required regulatory response—the existence of such non-linearities is a scope for further research.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.