Abstract

This article examines the impact of institutional, financial, and economic development on firms’ access to finance in Latin America and Caribbean region. Based on firm- and country-level data from the World Bank databases, we employ an ordered logit model to understand the direct and moderating role of institutional, financial, and economic development in determining firms’ financial obstacles. The results show that older, larger, facing less competition and regulation burden, foreign owned, and affiliated firms report lower obstacles to finance. Second, better macro-fundamentals help to lessen the level of obstacles substantially. Third, the role of institutions in promoting firms’ inclusive finance is quite different to the role of financial development and economic growth.

1. Introduction

Recent literature has emphasized the non-monotonic relationship between finance and growth (Arcand et al., 2015; Chu & Chu, 2020). Empirical research also indicates several explanations for the non-monotonic relationship, including rapid and excessive credit growth (Ghenimi et al., 2017), financial liberalization (Rousseau & Wachtel, 2011), bank and stock market crises (Asteriou & Spanos, 2018; Kaminsky & Reinhart, 1999), credit components (Beck et al., 2012), institutions (Demetriades & Law, 2006; Law et al., 2013), and economic development (Fufa & Kim, 2018). It means that not only the quantity but also the quality and coverage of financial development are important for ensuring the positive role of financial development in economic growth. Thus, access to finance by enterprises (and also households), especially constrained ones, is of increasing concern to policymakers and researchers across the world.

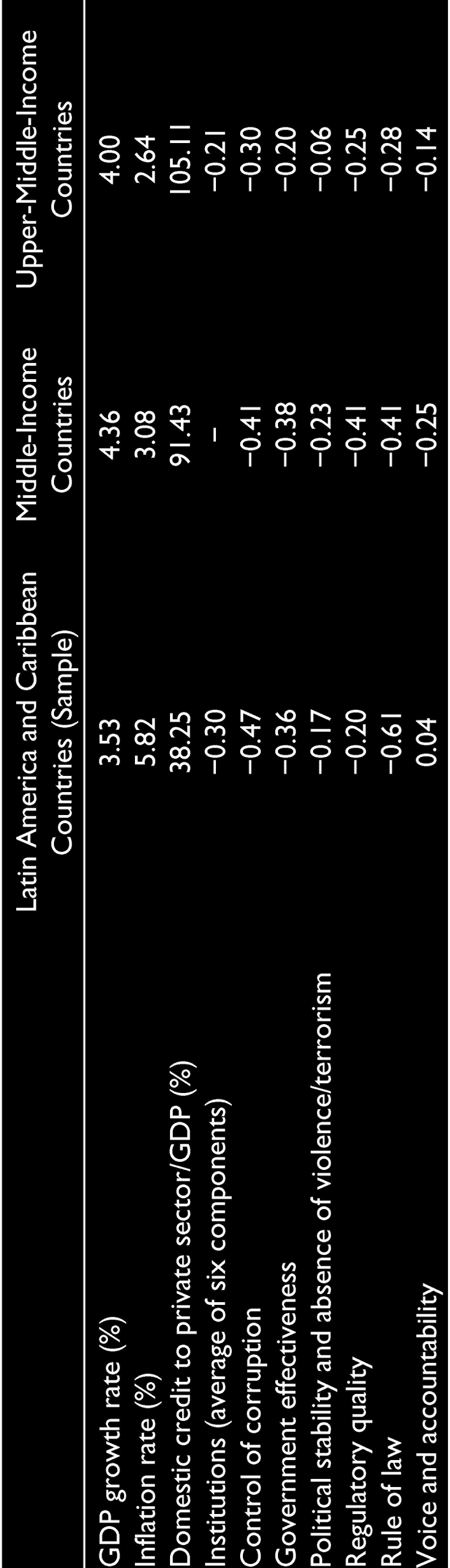

Latin America and Caribbean (LAC) has been known for a region of erratic performance of economic development. The pressing problems of macro-economic instability, in terms of low and volatile gross domestic product (GDP) per capita growth rate, low savings and investment rate, and high inflation rate, have been attributed to the low quality of institutions (Sawyer, 2010). Table 1 reports that, from 2013 to 2017, the average GDP growth rate of the LAC region is much lower than that of middle-income and upper-middle-income country groups, but the inflation rate is much higher. Moreover, the financial sector of this region is relatively underdeveloped in comparison to the two peers. According to de la Torre et al. (2012), the region continues to face some core financial gaps and challenges. Specifically, banks tend to lend less to private sectors, and the liquidity of equity market remains thin when compared with financial markets in comparable region around the world. With regard to institutional quality, LAC countries have lower development level than that of the upper-middle-income country group but still marginally better than the middle-income country group (in a measurement of overall quality). However, the development of each institutional component varies. For example, the regulatory quality, voice, and accountability of LAC countries are better than the peers, but the control of corruption and rule of law are significantly worse.

Macro-economic Indicators of Latin America and Caribbean

Due to underdeveloped macro-framework in the LAC region, firms face severe obstacles in financial access, especially small, young, domestic ones (Presbitero & Rabellotti, 2014). The literature has also concluded that, smaller and younger firms experience more financial obstacles (Makler et al., 2013). In contrast, large and foreign-owned firms face fewer financial constraints (Galindo & Schiantarelli, 2012), while state-owned firms do not enjoy any financial privileges (Leitner & Stehrer, 2013). However, Solari et al. (2014) find that firms’ size, industry, and age are not always significant in explaining Latin American firms’ financial constraints. Because these variables per se might not demote informational asymmetries, the interaction between them and other country-level factors need to be re-examined, especially with the inclusion of institutions. There are two possible reasons for this conjecture. First, the relationship between institutions and financial development has been demonstrated to follow an inverted U shape (Arcand et al., 2015). Second, the role of institutional quality in explaining financial development is more significant in developing countries than in developed countries (Le et al., 2016). Hence, it could be believed that the differences in the institutions might have distinctive effects on firms’ access to finance, depending on firms’ characteristics and economic conditions. Empirically, Audretsch and Elston (2006) and Beck et al. (2008) find that small firms grow faster than large firms, given the change in institutions. Similarly, the inefficient institutions have a stronger negative impact on small firms than larger firms (Carvalho, 2008). Lemma and Negash (2013) find that the origin of the legal system, shareholder rights, rule of law, and creditor rights of a country significantly influence and also influence differently the way firm-specific factors determine capital structure.

We observe that few studies have focused exclusively on the direct impact of institutional, financial, and economic development on LAC firms’ access to finance, and no study, to our best knowledge, has analyzed their moderating roles. First, the effects of institutional improvement on firms’ access to finance may vary across firms’ characteristic groups as the improvement can ease obstacles of some firms but intensify those of other firms. In contrast, the evolution of economic fundamentals and financial sectors could reduce the obstacles for all types of firms. Thus, the policymakers should consider these differences and tailor appropriate policies for different groups of firms. Second, the firms should understand which factors and how they constrain their financing access. It helps them to develop suitable strategies to deal with such obstacles. Given the limited empirical attention devoted to country-level variables in the literature and the possible practical implications, the aim of this article is to investigate whether and how country-level factors affect firms’ accessing to finance in the LAC region.

This study extends the literature in several aspects. First, we examine the effects of institutional, financial, and economic development on the firms’ access to finance rather than traditional measurements such as financial depth, liquidity, and efficiency (Beck et al., 2000). An increasing attention has focused on the role of finance to a firm’s growth (Beck & Demirguc-Kunt, 2006; Fowowe, 2017) and the role of the firm in supporting economic growth. Moreover, since the early 1990s, many LAC countries have undertaken significant efforts in macroeconomic reform and stabilization to generate growth and propensity. These intense efforts include, but are not limited to, institutional, economic, and financial reforms. Although financial inclusion of firms in the region has been broadly at par with its peers (Dabla-Norris et al., 2015), the development has continued to lag other emerging market groups (Heng et al., 2016). Given this context, it is interesting to investigate how institutions, finance, and economic development reduce firms’ financial obstacles. Second, the literature has pointed out that because of the environment of underdeveloped legal frameworks and economic development, and weak financial systems, firms obtain less external financing, which, in turn, results in lower growth (Beck et al., 2008; La Porta et al., 1997, 1998). However, the literature has less to say about how these macro-fundamentals have impacts on firms’ financial access across different characteristics. Therefore, we contribute to the literature by exploring how the relationships among the institutional, financial, economic development, and firm’s characteristics affect financial access in the context of the LAC region.

We address these issues by taking data from the World Bank’s Enterprise Surveys, World Development Indicators, Global Financial Development, and Worldwide Governance Indicators for 12 LAC countries. Combining these databases allow us to use a variety of both firm- and country-level characteristics.

We obtain the following results, which are stable in extensive robust analyses. First, the firm’s characteristics such as size, competition, ownership, corporate structure, regulation burden, and age are significant determinants of LAC firms’ financial access. Second, the well-developed institutions, financial development, and economic growth help to lessen the firm’s financial constraints. Third, while the financial and economic development are conducive to better access to finance for most firms, institutional development levels the playing field between small and large firms, domestic-owned and foreign-owned, and nonaffiliated and affiliated firms. Moreover, it is noteworthy that different components of institutional quality have heterogeneous impacts on financial access across firms’ characteristic groups. These results underline the importance of having tailored suitable policies rather than one-size-fits-all solutions, for the LAC region.

The rest of this article is structured as follows. The second section reviews relevant literature about the determinants of firms’ accessing to finance. The third section describes data and model specifications. The fourth section presents the main result and robustness test. The fifth section concludes with implications for policymakers.

2. Literature Review

The theoretical literature has long recognized that market imperfections constrain firms’ ability to obtain finance. Asymmetric information, which leads to adverse selection and moral hazard problems, is the main culprit that hinders firms from raising fund for investment. Given the lack of credibility and protection, the investors are reluctant to lend or invest any money to firms. In contrast, a well-developed legal and regulatory environment could mitigate this market imperfection by strengthening investor rights (Levine et al., 2000) and facilitating better contract enforcement (Berger & Udell, 2006). Then, the legal rights and enforcement mechanisms ensure the quantity and quality of services provided by the financial system (Beck et al., 2003; La Porta et al., 1997, 1998). Similarly, Demetriades and Andrianova (2004) conclude that the institutions, including financial regulations, the legal system, and related institutions, have a first-order effect on financial development. Baltagi et al. (2007) find that economic institutions are one of the major determinants of the variation in financial development across countries and over time since the 1980s. Empirically, Demirgüç-Kunt and Maksimovic (1998) and Beck et al. (2006) find that differences in both legal and financial systems have influence on the firms’ access to finance. Similarly, Johnson et al. (2002) and Beck et al. (2008) conclude that a country’s legal right and judicial environment significantly affect the financing patterns of firms. With regard to financing choices, in the absence of effective formal institutions, external finance becomes more costly. A recent study by Madestam (2014) reports that weaker legal institutions do increase the popularity of informal finance. On a macro-economic context, Demetriades and Law (2006) conclude that financial development has a larger effect on long-run economic development when the financial system is embedded within a sound institutional framework. Similarly, Law et al. (2014) conclude that the marginal impact of financial development on growth depends on institutional quality.

Financial development is considered to ameliorate, though not necessarily eliminate, the cost of acquiring information, enforcing contracts, and making transactions (Levine, 2003). First, by allocating resources efficiently, monitoring corporate governance, reducing risk, mobilizing savings, and facilitating transactions, financial development encourages savings, borrowings, and investments. As a result, it helps to lessen financial obstacles of firms. Beck et al. (2006) and Leitner and Stehrer (2013) find a negative relationship between financial development, measured by domestic credit to the private sector and firms’ financial obstacles. Moreover, as financial market develops, firms tend to use formal external finance rather than informal or internal funds (Beck et al., 2008; Love, 2003). Second, based on market power and information hypothesis view, the financial development, in terms of banking competition, also leads to lower costs and better access to finance (Marquez, 2002). Leon (2015) shows that bank competition alleviates credit constraints in developing countries.

The firms’ access to finance (in term of financial obstacles or financing pattern/capital structure) significantly relates to the economic development of a country (Beck et al., 2006, 2008; Knack & Xu, 2017; Lemma & Negash, 2013). A firm’s financial decision might be affected by the rate at which a country grows because the country’s growth rate determines the growth opportunities, financing needs, and also cost of financing (Beck et al., 2002).

The literature suggests that a variety of firms’ characteristics affect their financial access such as size, age, ownership, corporate structure, export, and regulation. First, smaller and younger firms report higher financing obstacles than large firms (Beck et al., 2006, 2008). Additionally, small and medium firms are believed to be put in an unfavorable light to suppliers of finance because of short time operating, low creditworthiness (Gertler, 1988), poor solvency, low real assets (Guariglia, 2008), and informational opacity (Berger & Udell, 1998). Consequently, the relationship among firms’ size, age, and the probability of being financially constrained is significantly positive (Beck et al., 2006; Du & Girma, 2012). Second, foreign-owned firms might alleviate financial constraint (Beck et al., 2006), thanks to the direct funds from foreign partners and lower bankruptcy risk, which are benefited from the adoption of international quality standards (Mertzanis, 2017). Empirically, foreign-owned firms in the Latin American region face fewer financial constraints than domestic firms do (Harrison & McMillan, 2003). Third, firms that belong to a group have a lower probability of facing financial obstacles, as these firms can take advantage of the group’s internal cash flow (Shin & Park, 1999) and close relationship with banks (Hoshi et al., 1991). Leitner and Stehrer (2013) find that LAC firms, which belong to a larger enterprise, mostly rely on internal financing sources from their mother company. Fourth, according to Melitz (2003), direct exporting is costly; thus, exporters mostly perform as better non-exporters in terms of production efficiency and have stronger financial backup. Moreover, exporting activities enable firms to achieve economies of scale that further aid their financial capabilities. As a result, export-oriented firms may acquire and signal better creditworthiness than non-exporters. Aterido et al. (2013) and Leitner and Stehrer (2013) empirically conclude that exporters find it easier to finance their investments than non-exporters. Fifth, the literature also indicates that regulation burden could retard economic performance as well as firms’ productivity, innovation, and growth. Loayza et al. (2005) conclude that a heavy regulation imposed on the firms (goes in hand with worse governance) has a detrimental impact on economic growth. Amin and Ulku (2019) indicate that corruption and excessive regulation reinforce each other and affect firms’ performance negatively. With regard to financial access, the World Bank (2014) finds that regulatory burden (measured by manager’s time spent to deal with government regulation) significantly affects firms’ access to bank loan. Sixth, a firm’s competition level could have a relationship with its ability to access to finance. For example, a firm operating in a competitive industry may have a greater need for external finance to innovate and win over their rivals. Moreover, given the lower profitability due to high competition, the firms face more restrictions in generating internal fund and face more difficulties in obtaining finance from lenders. Bernini and Montagnoli (2017) find that in a relatively underdeveloped financial system, firms’ competitive pressure affects both supply and demand sides of the credit market. Finally, yet importantly, firms’ sector could lead to the difference in the accessibility of funds (Huang, 2006). For example, it could be easier for service firms located in an urban area to build a relationship with commercial banks than agricultural firms located in rural area. Hence, manufacturing, agricultural, and construction firms face higher barriers to access finance than those in the service industry (Beck et al., 2006).

3. Methodology

3.1 Data and Sample

For this study, we employ firm-level data from the Enterprise Surveys as well as country-level data from the World Development Indicators, Global Financial Development, and Worldwide Governance Indicators conducted by the World Bank. The sample includes 12 countries of the LAC region, which were surveyed in 2016 and 2017. These countries, namely Argentina, Bolivia, Colombia, Dominican Republic, Ecuador, El Salvador, Guatemala, Honduras, Nicaragua, Paraguay, Peru, and Uruguay, are chosen as they belong to a relatively coherent group in the American region, and the survey on each country is conducted within a similar time span.

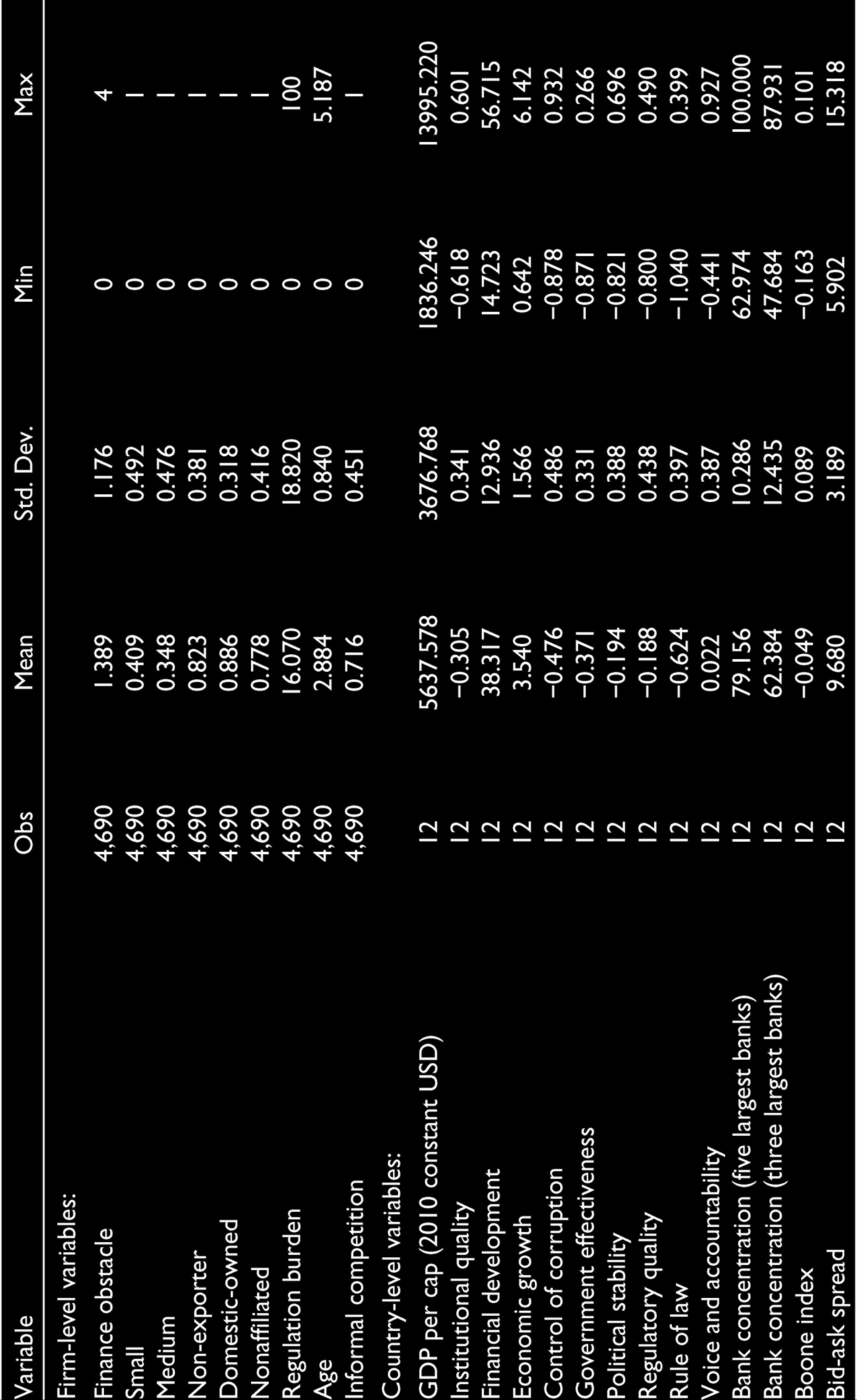

The Enterprise Surveys use standard survey instruments to collect firm-level data on the business environment from business owners and top managers. The surveys cover a broad range of topics, including access to finance, government relations, infrastructure, crime, competition, labor, obstacles to doing business, and performance. The use of this database has several major advantages. First, the data are offered in two formats—standardized and country survey forms. With regard to the former, the country data are matched to a standard set of questions, which allow us to compare and analyze across countries. Second, unlike several databases that focus mainly on listed or large firms, this database allows us to examine the access to finance across a firm’s size and sector. Our sample includes 4,690 firms, of which 41% are small, 35% are medium, and 24% are large firms. Third, because the survey follows the global sampling methodology (which are stratified by the business sector, location, and the firm’s size), the sample is representative at the country level. In our sample, manufacturing, retail, and service firms account for 49%, 19%, and 32% of the sample, respectively.

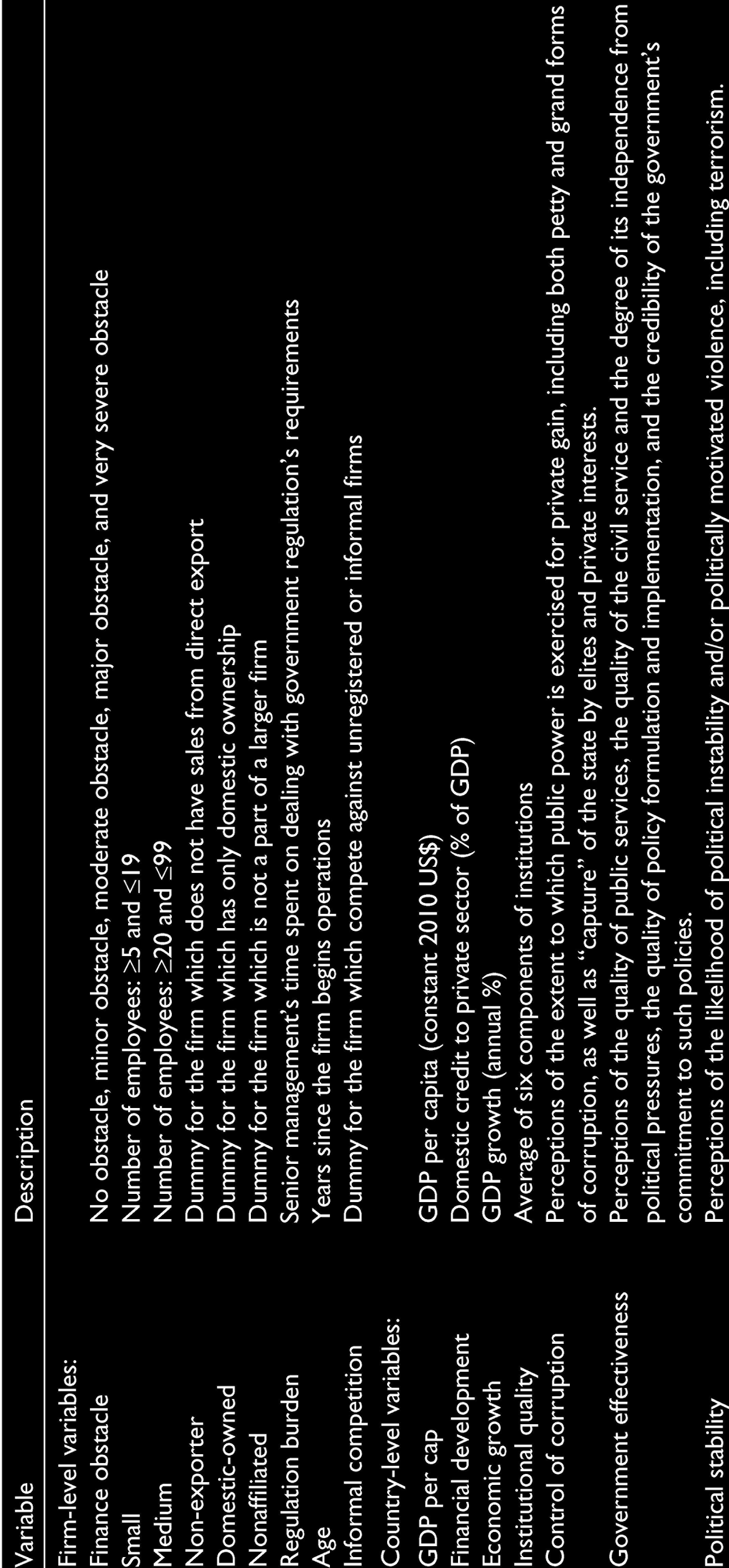

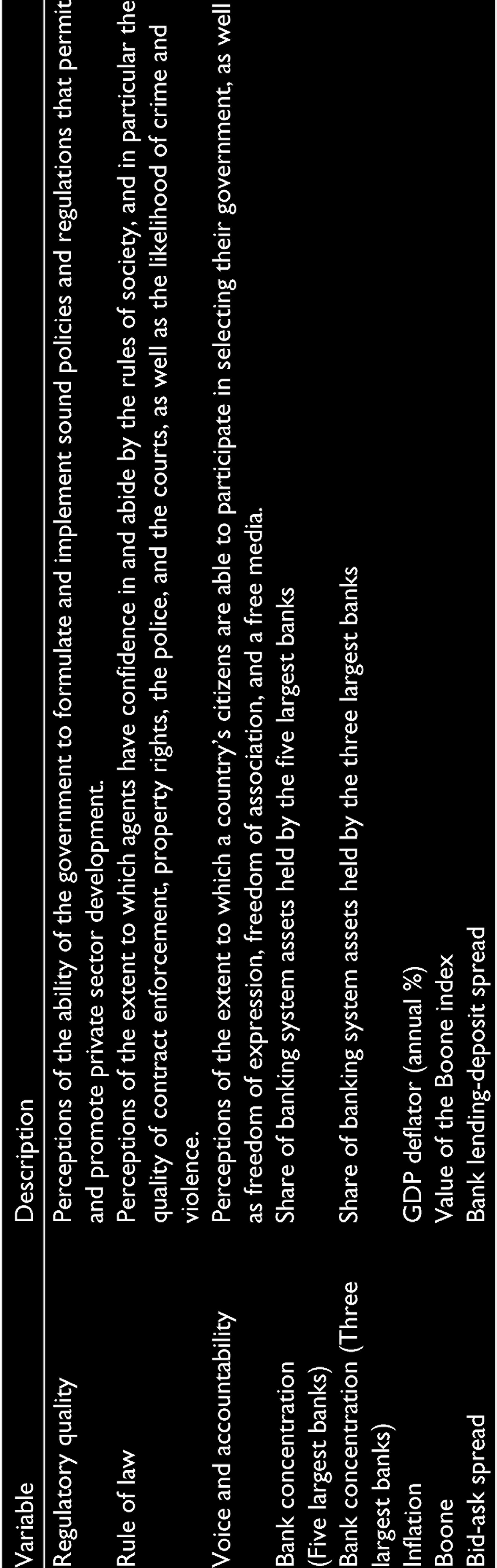

The country-level variables are taken from the World Development Indicators, Global Financial Development, and Worldwide Governance Indicators databases. The World Development Indicator is the World Bank’s premier compilation of cross-country comparable data on development. We take data on GDP per capita, economic growth, and inflation rate from this database. To measure financial development, we take into consideration three aspects: the domestic credit to the private sector to measure the liquidity, the Boone indicator to measure the degree of competition, and the bank lending–deposit rate to measure the efficiency. These variables are taken from the Global Financial Development database, which is an extensive annual dataset of financial system characteristics for over 200 countries. The Worldwide Governance Indicators report individual governance indicators for over 200 countries and territories for six dimensions of governance. The six composite measures are evaluated to be useful as a tool for broad cross-country comparisons. We use all six components and also create an aggregate indicator by taking their average. 1

To measure the level of institutional, financial, and economic development, we use a variety of macro-variables. The GDP per capita is used to control for difference in economic development between countries. The GDP growth rate and inflation rate are included to reflect the current economic condition of the country. The domestic credit to the private sector, which equals claims on the private sector by deposit money banks and other financial institutions, reflects the liquidity of the financial market. The Boone indicator and bank asset concentration are used to measure the competition of the banking sector. The efficiency of the banking sector is measured by the bank lending–deposit rate. We follow Kaufmann et al. (2010) to use six dimensions of institutional quality to measure institutional quality. First, voice and accountability, political stability, and absence of violence belong to “the process by which governments are selected, monitored, and replaced.” Second, government effectiveness and regulatory quality constitute to “the capacity of the government to effectively formulate and implement sound policies.” Lastly, rule of law and control of corruption explain “the respect of citizens and the stage for the institutions that govern economic and social interactions among them.” All country-level variables are averaged over the period from 2013 to 2017. Table 2 presents the description and source of variables. Table 3 reports summary statistics.

Variable Description and Data Sources

Summary Statistics

To measure the access to finance in the LAC region, we use a Likert-scale variable that represents the firms’ assessment of the difficulties they face in obtaining finance. Specifically, we use the survey question To what degree is Access to Finance an obstacle to the current operations of this establishment? The answer is categorized into five following scales: no obstacle, minor obstacle, moderate obstacle, major obstacle, and very severe obstacle. The majority of firms (30.3% and 30.2%) report “no obstacle” and “moderate obstacle,” respectively. Around 22.5% of the respondents respond that they face a minor obstacle in accessing finance, while 12.1% and 4.9% of firms experience major and very severe difficulties in raising funds, respectively.

Financing obstacles vary with a firm’s characteristics. Based on the literature, we use the following set of explanatory variables to control for firm’s heterogeneity. They comprise the firm’s size (small, medium, vs. large), degree of competition (informal competition vs. formal competition), export orientation (non-exporter vs. exporter), foreign ownership (domestic-owned vs. foreign-owned), corporate structure (affiliated vs. nonaffiliated), regulation burden (time spent in dealing with government regulation), and age. We choose these variables as most LAC countries have been characterized by a high proportion of small and medium firms, informal sectors, growing economic integration, and a high regulatory burden.

3.2 Model Specification

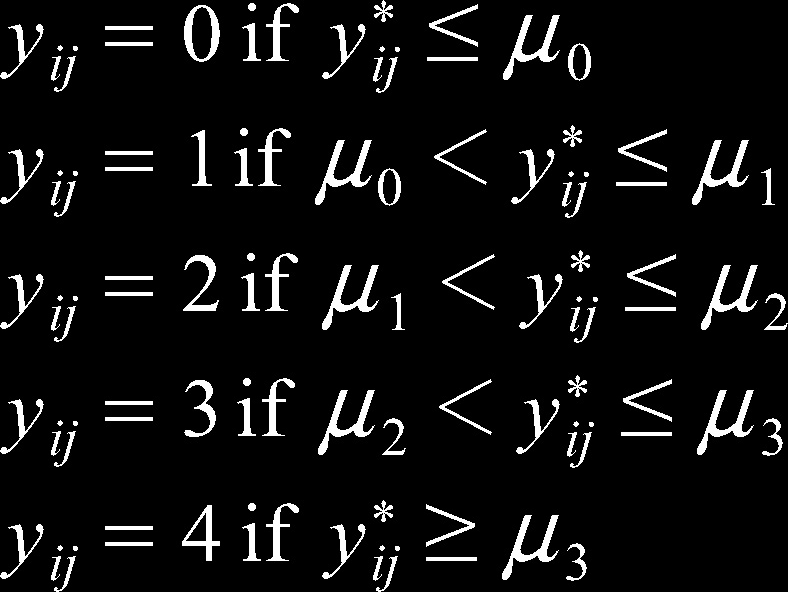

Given the fact that the dependent variable—financing obstacle—is an ordinal variable, we employ an ordered logit approach. The proposed model is of the following form:

where

with no obstacle, minor obstacle, moderate obstacle, major obstacle, and very severe obstacle coded as 0, 1, 2, 3, and 4, respectively. The μ is unknown parameters (usually named as cut-off points) that will be estimated together with β and γ.

The inclusion of macroeconomic variables not only allow for testing the effect of institutional, financial, and economic developments, but it also constitutes a robustness test for the firm-level characteristics. However, the results might be driven by the high correlation between country-level variables if we include all of them in one equation. Thus, to avoid multicollinearity, we add variables measuring each of economic conditions one by one while still controlling one economic development indicator—GDP per capita.

We also explore the variation of the relation among institutional, financial, and economic development with financing obstacles across different firms’ characteristics. We do this by introducing interaction terms of country-level variables with firm-level variables for size (small, medium, vs. large), export orientation (non-exporter vs. exporter), foreign ownership (domestic-owned vs. foreign-owned), corporate structure (affiliated vs. nonaffiliated), degree of competition (informal competition vs. formal competition), regulation burden, and age.

4. Results

4.1 Main Results

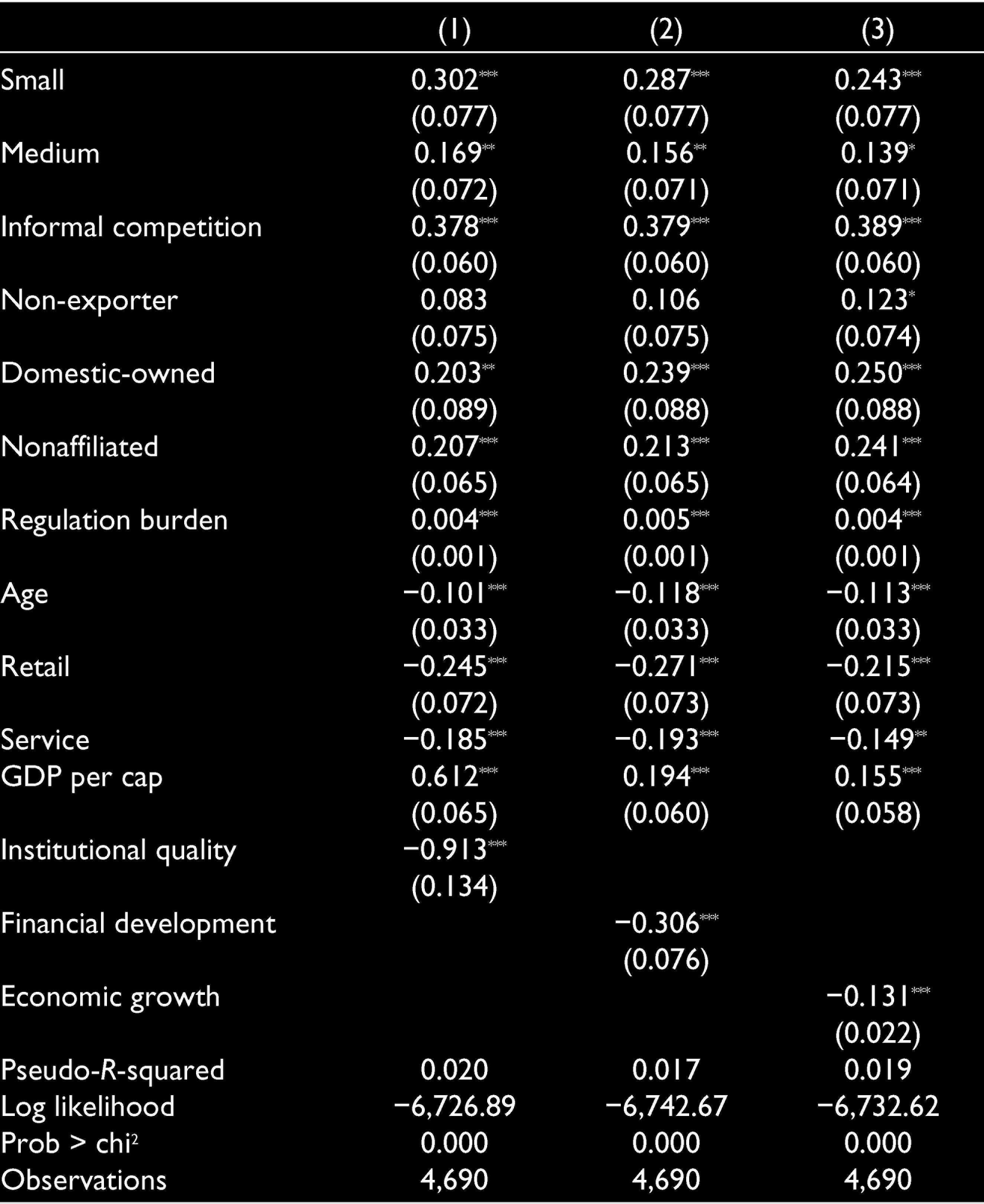

Table 4 presents the estimation of determinants of both firm-level and country-level characteristics on firms’ financing obstacles. With regard to firm characteristics, we find that size, competition, ownership, corporate structure, regulation burden, and age are significant determinants of LAC firms’ financing obstacles. Large-sized firms facing less competition, foreign owned, affiliated, facing less government regulation, and older firms report significantly fewer obstacles to finance. Manufacturing firms face more difficulties in obtaining funds than firms in retail and service sectors. Export orientation is not significantly relevant for financing obstacles. With regard to country characteristics, the results show that better institutions, finance development, and economic growth help overcome obstacles in raising capital. Specifically, higher level of institutional quality has a negative impact on the financing difficulties, while strong credit provision for private sectors significantly reduces the trouble in financing. Firms in faster growing economies face fewer financial constraints.

Determinants of Firms’ Financing Obstacles

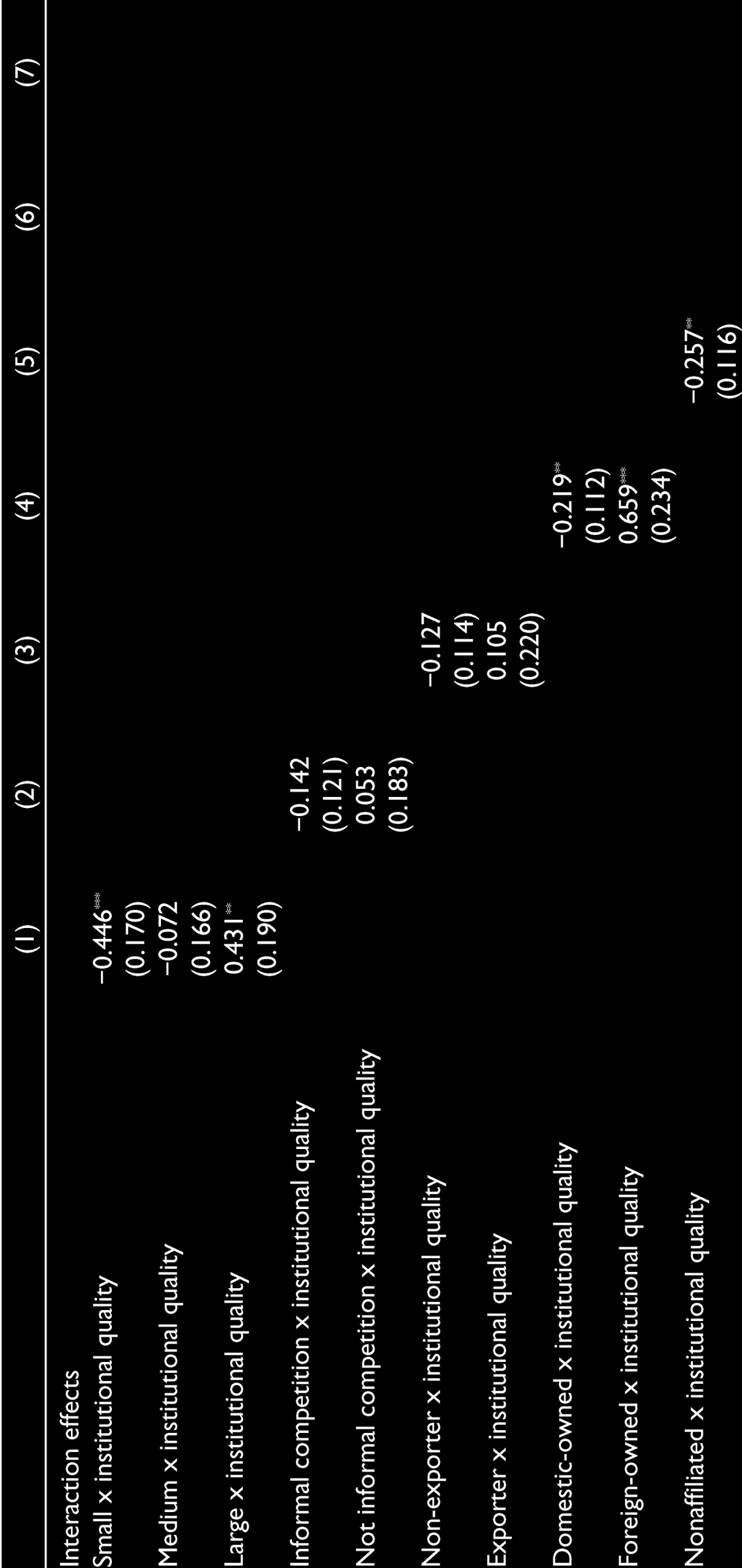

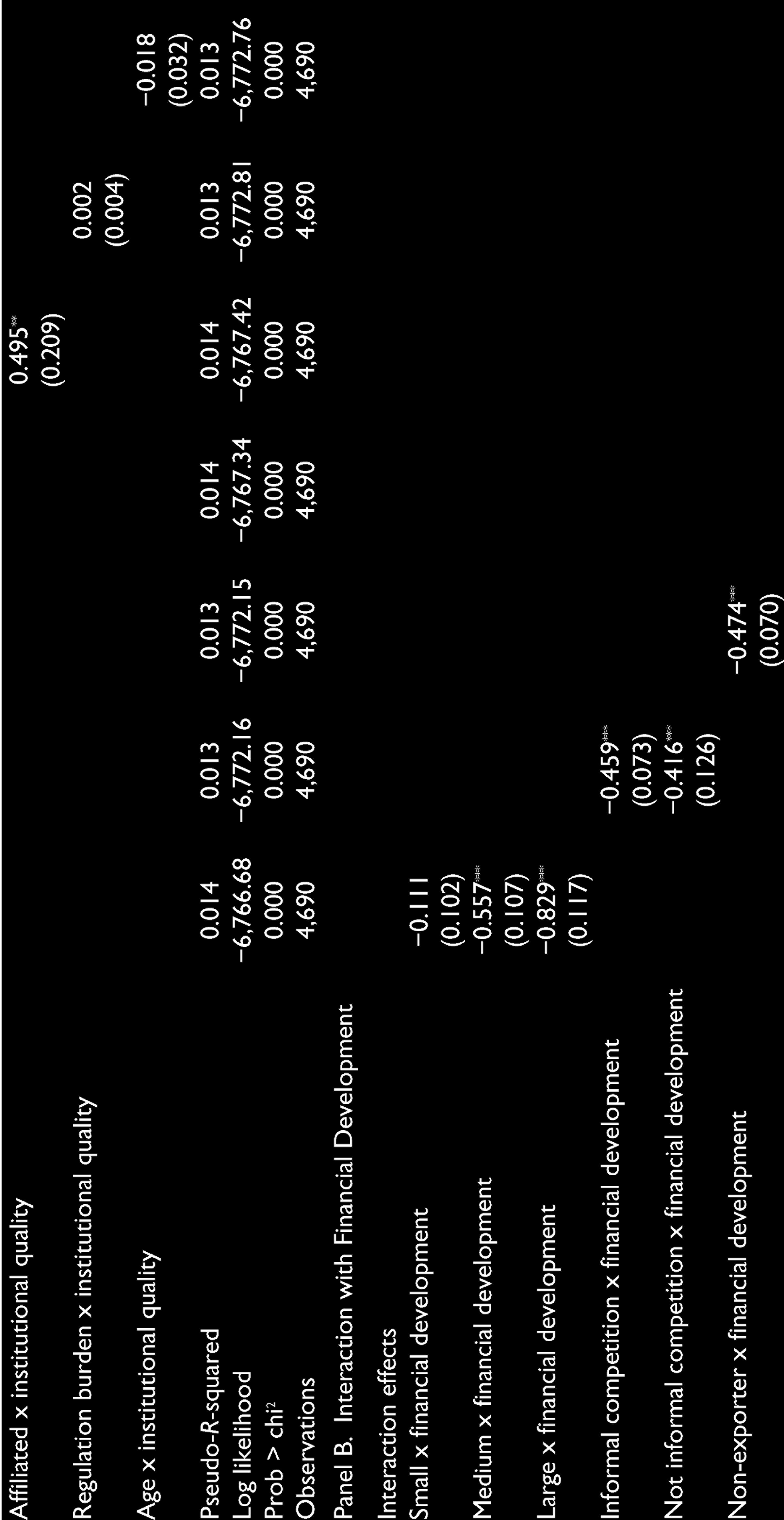

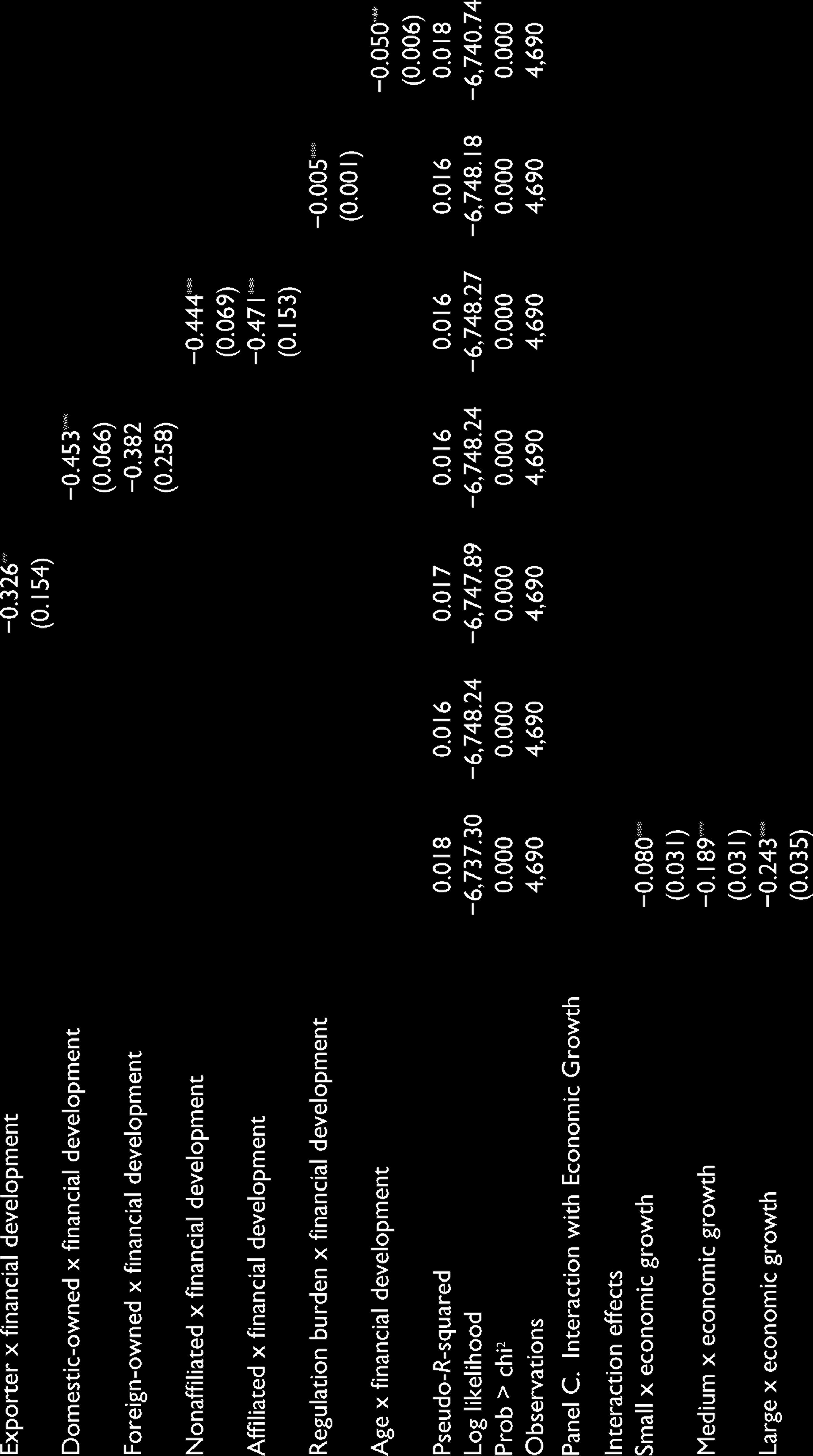

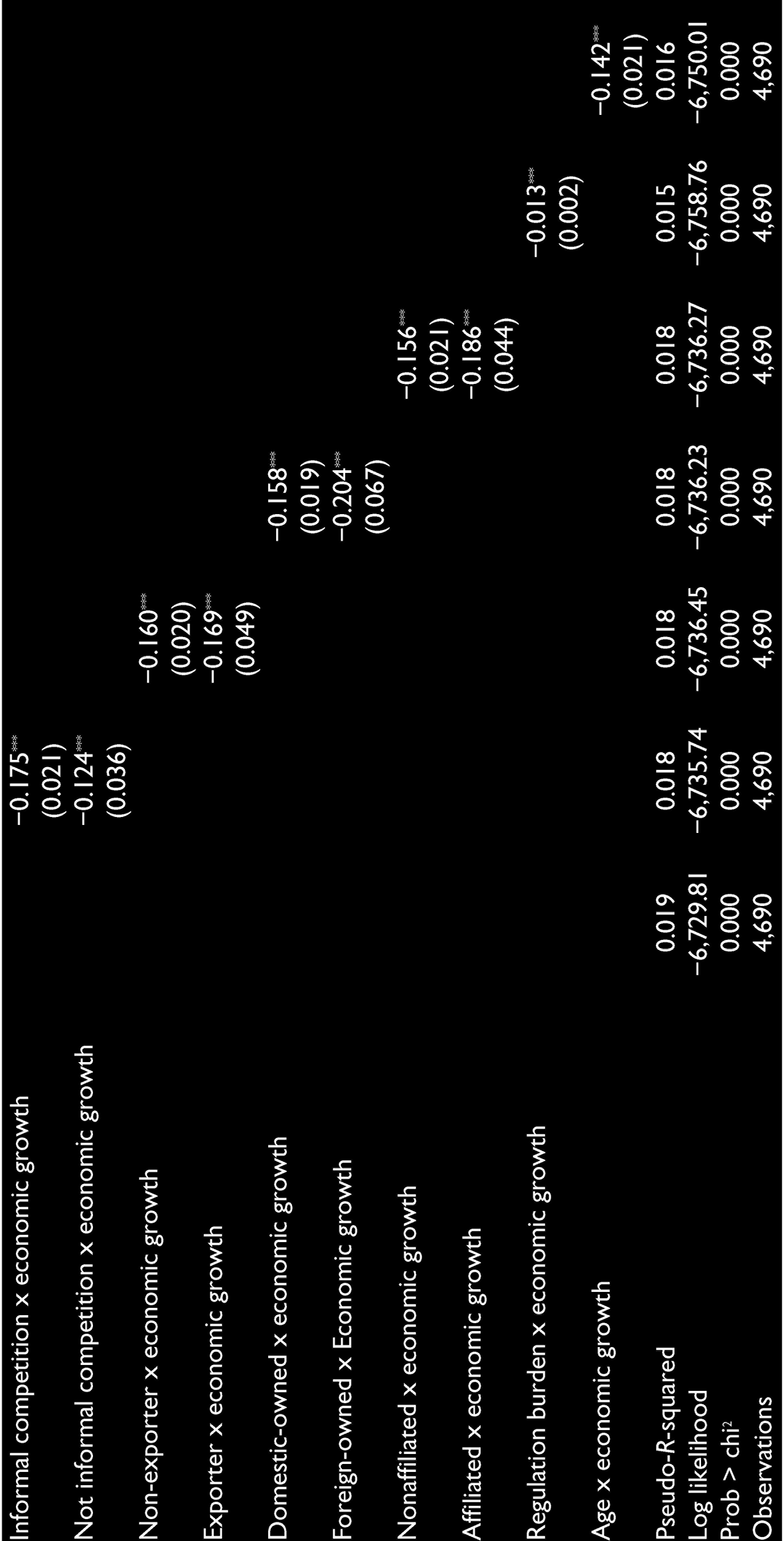

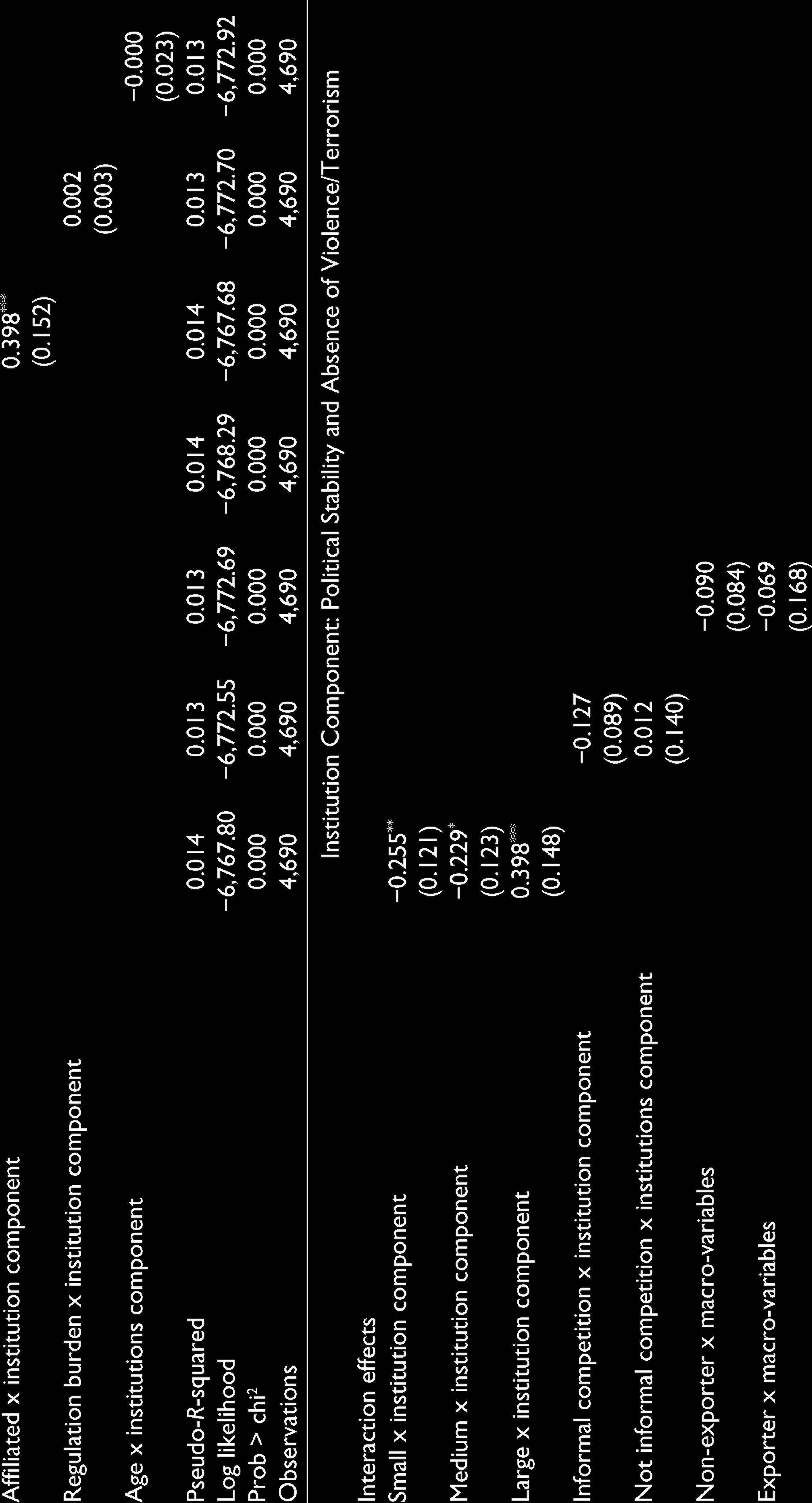

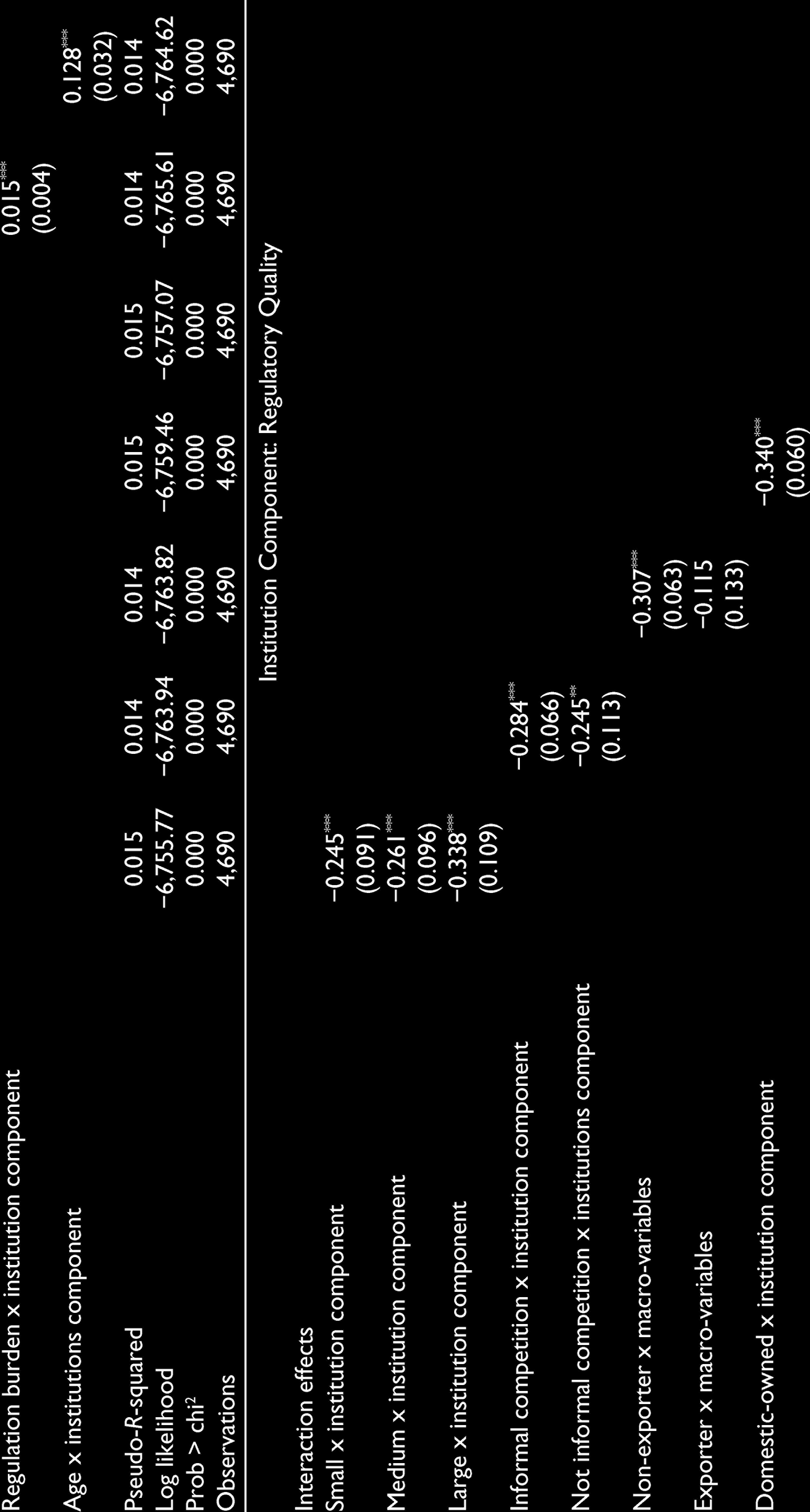

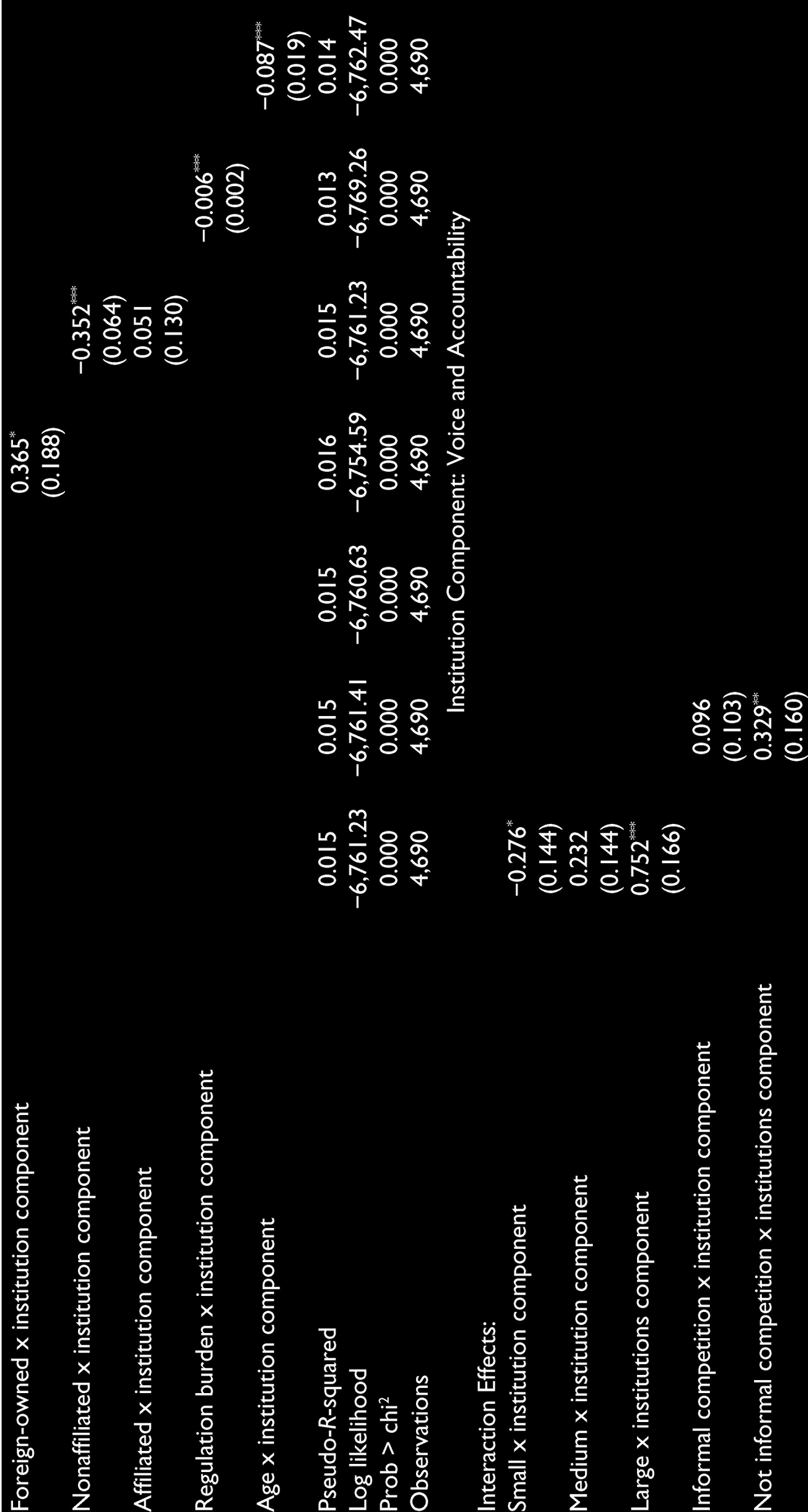

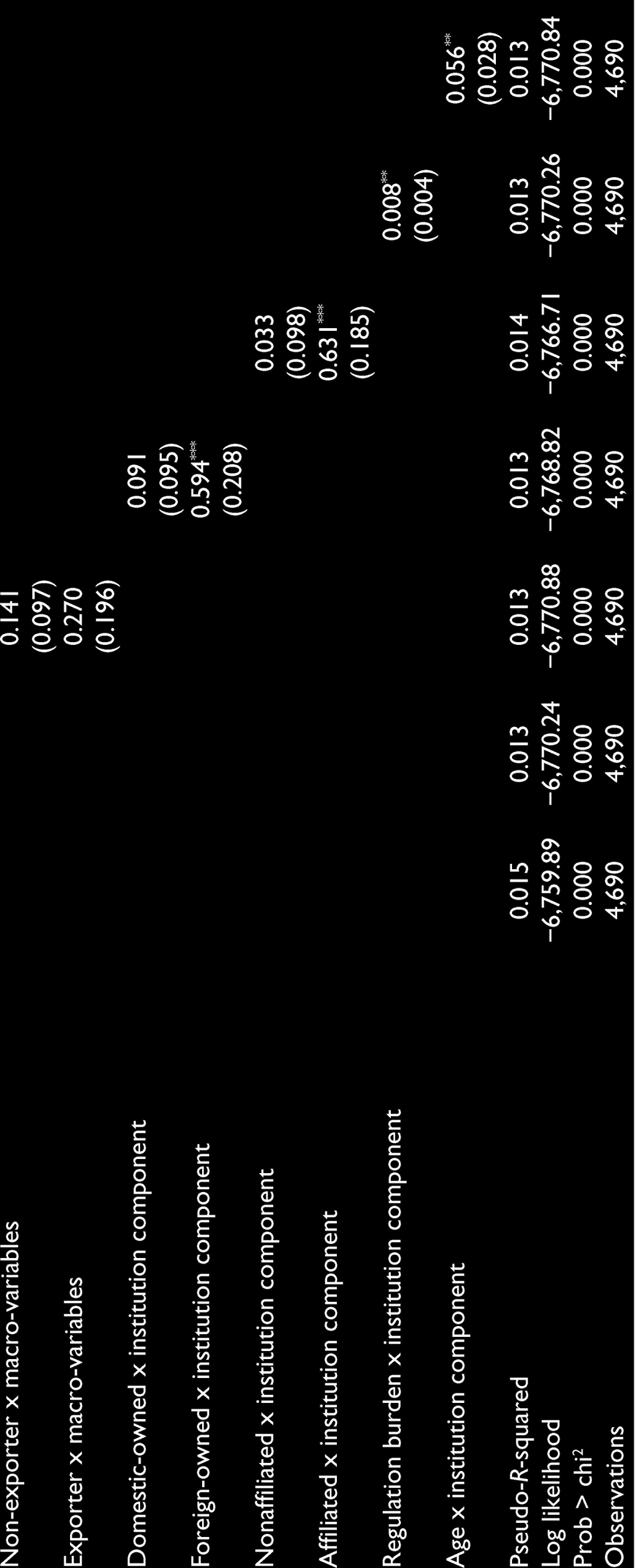

Table 5 explores the variation of the relation among institutional (Panel A) development, financial development (Panel B), and economic growth (Panel C) with financial obstacle across different firms’ characteristics. We introduce interaction terms of macroeconomic variables with firm-level variables and report the result of interaction terms only to save space (full regression results are available upon request). First, Panel A indicates that good institutions reduce the financial constraints for small firms but increase the financial constraints for large firms. Similarly, we find evidence that better institutional quality helps lessen financial obstacles for domestic-owned and nonaffiliated firms, while it makes foreign-owned and affiliated firms face higher financial obstacles. We do not find evidence of different effect of institutional quality on medium firms. Second, Panel B reports that financial development is conducive to better access to finance for all, except for small and foreign-owned firms. Third, Panel C shows that a higher GDP growth rate has a positive impact on financial access for firms across all characteristics. It is noteworthy that among the three macroeconomic variables, only better institutional quality levels the playing field between small and large firms, domestic-owned and foreign-owned, and nonaffiliated and affiliated firms. In other words, the role of institutions in promoting inclusive finance is quite different to the role of financial development and economic growth.

Determinants of Firms’ Financing Obstacles: Interaction Effects of Macro-Variables and Firm-Level Characteristics

Panel A. Interaction with Institutional Quality

4.2 Robustness

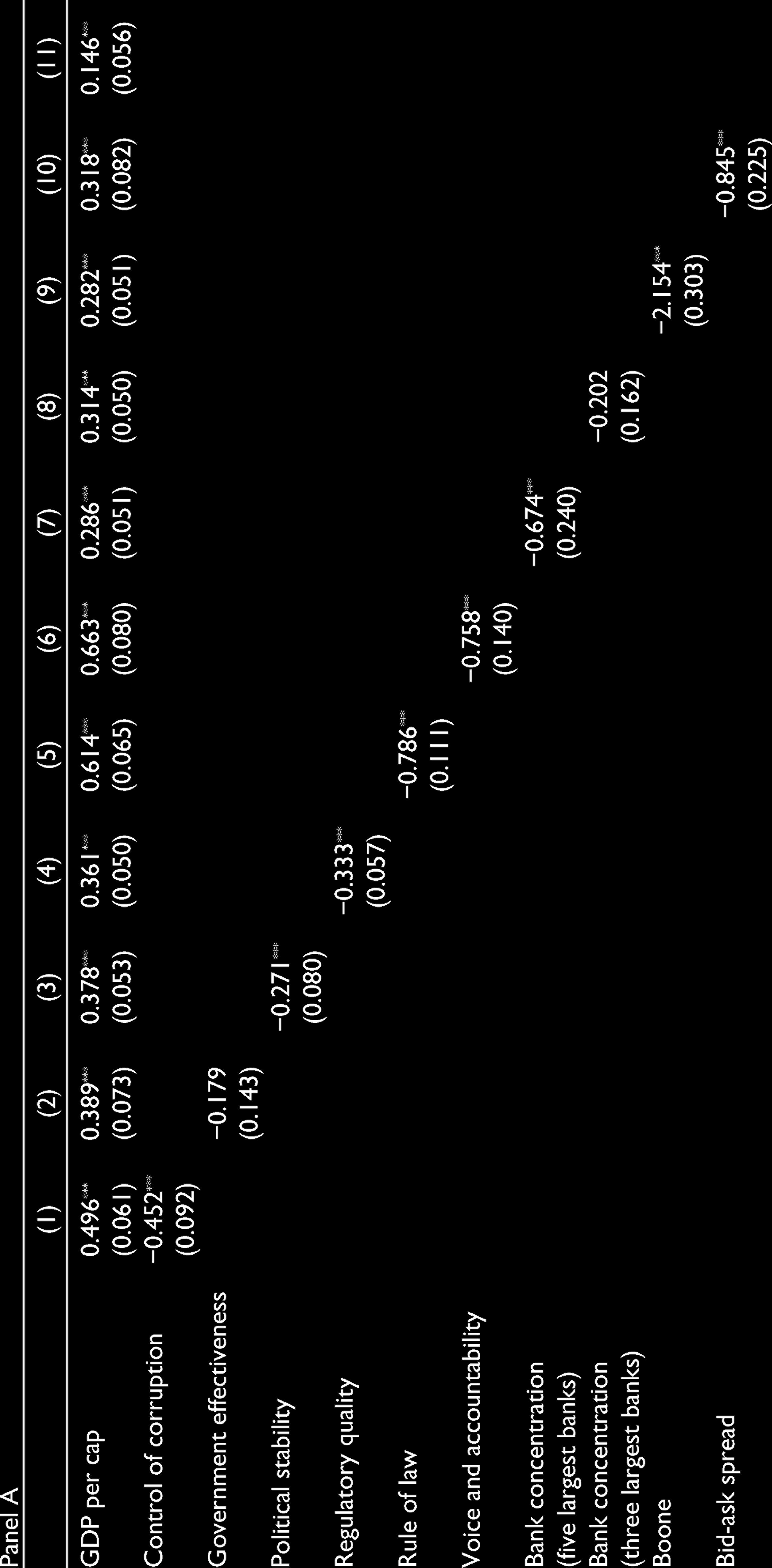

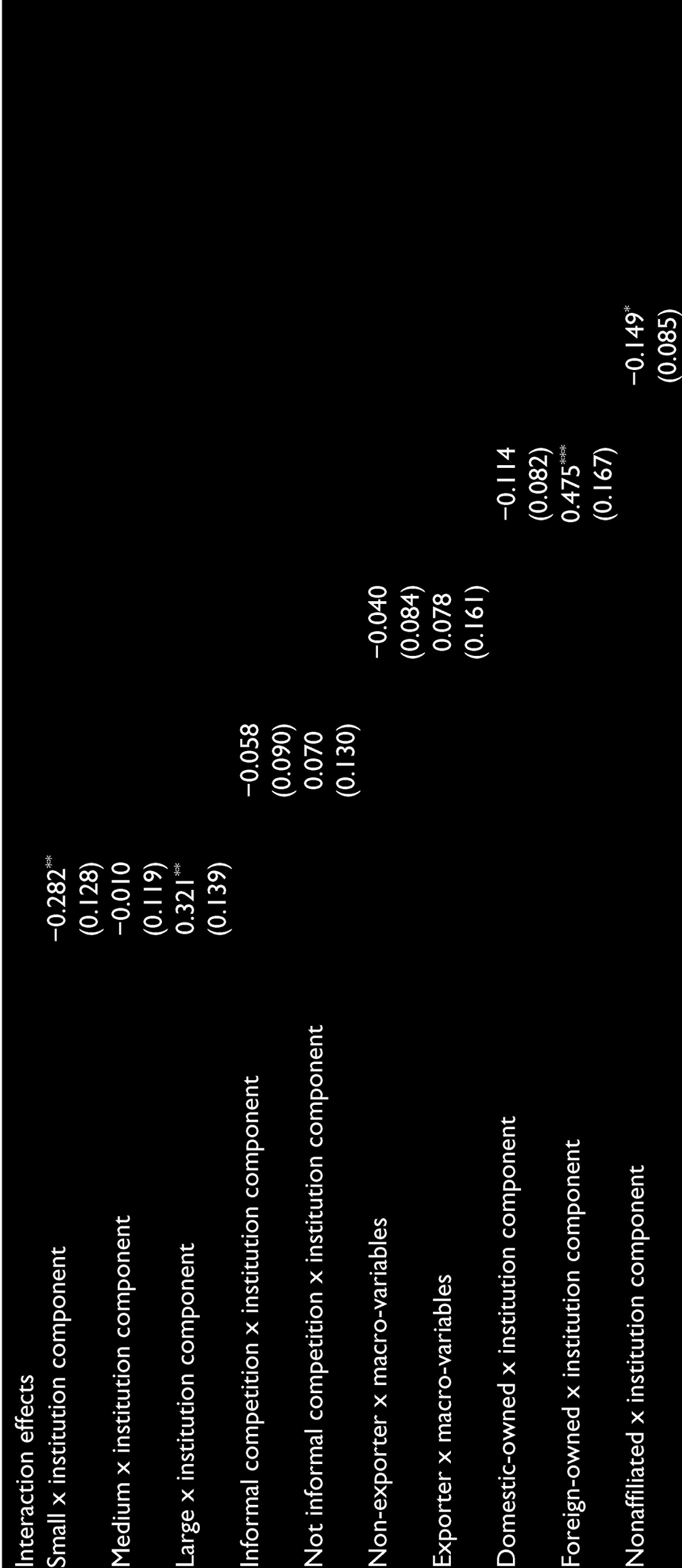

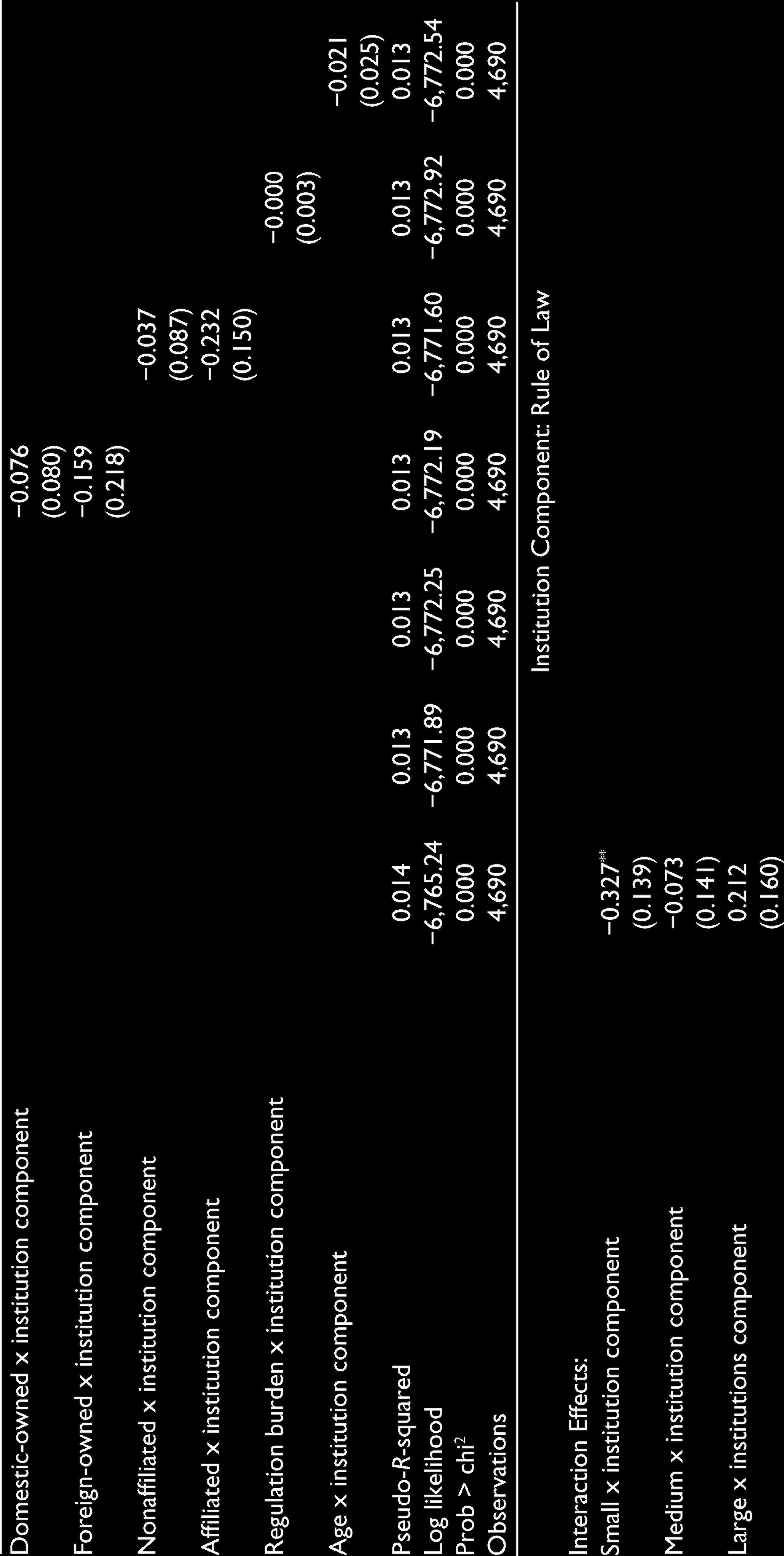

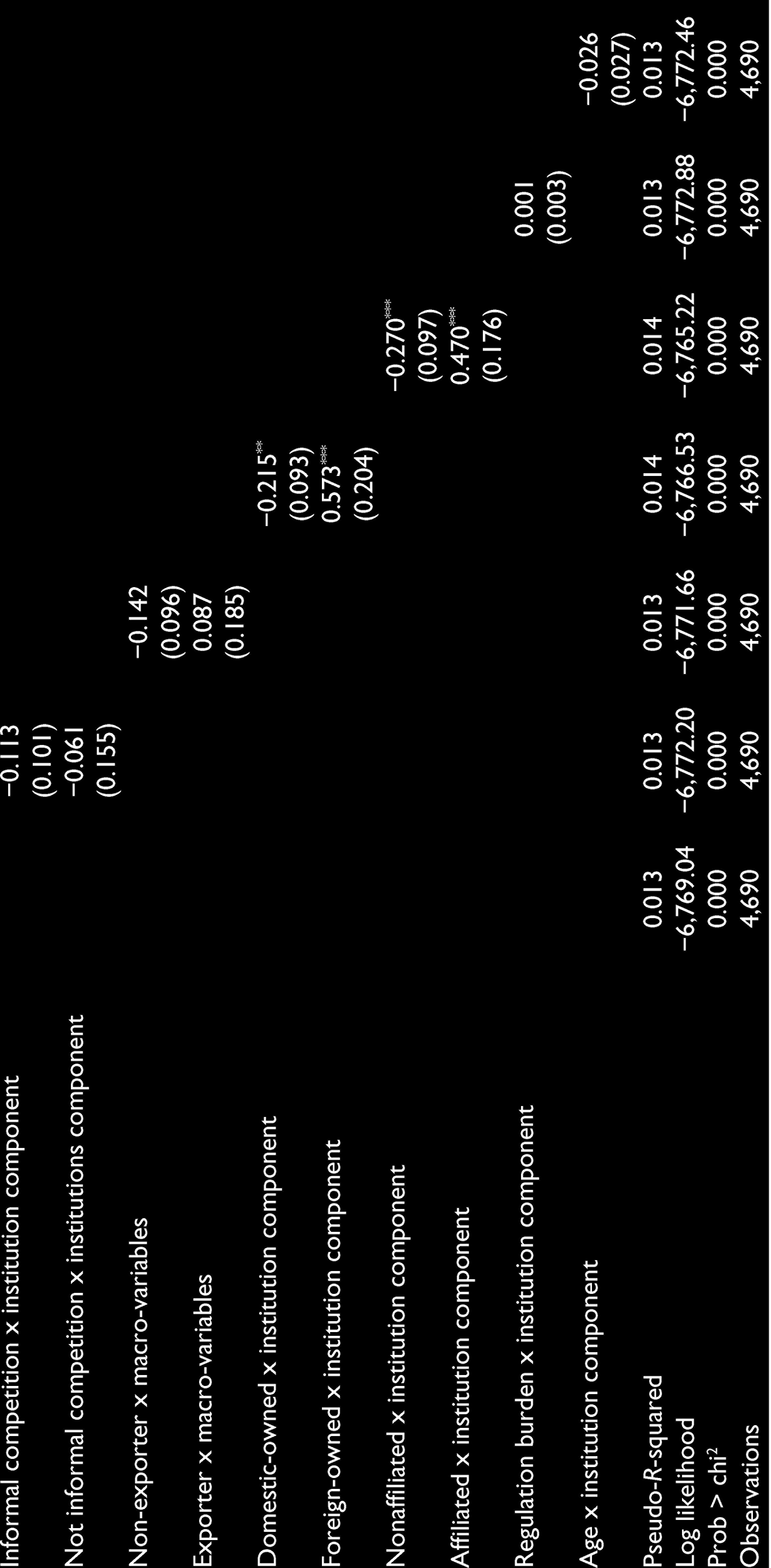

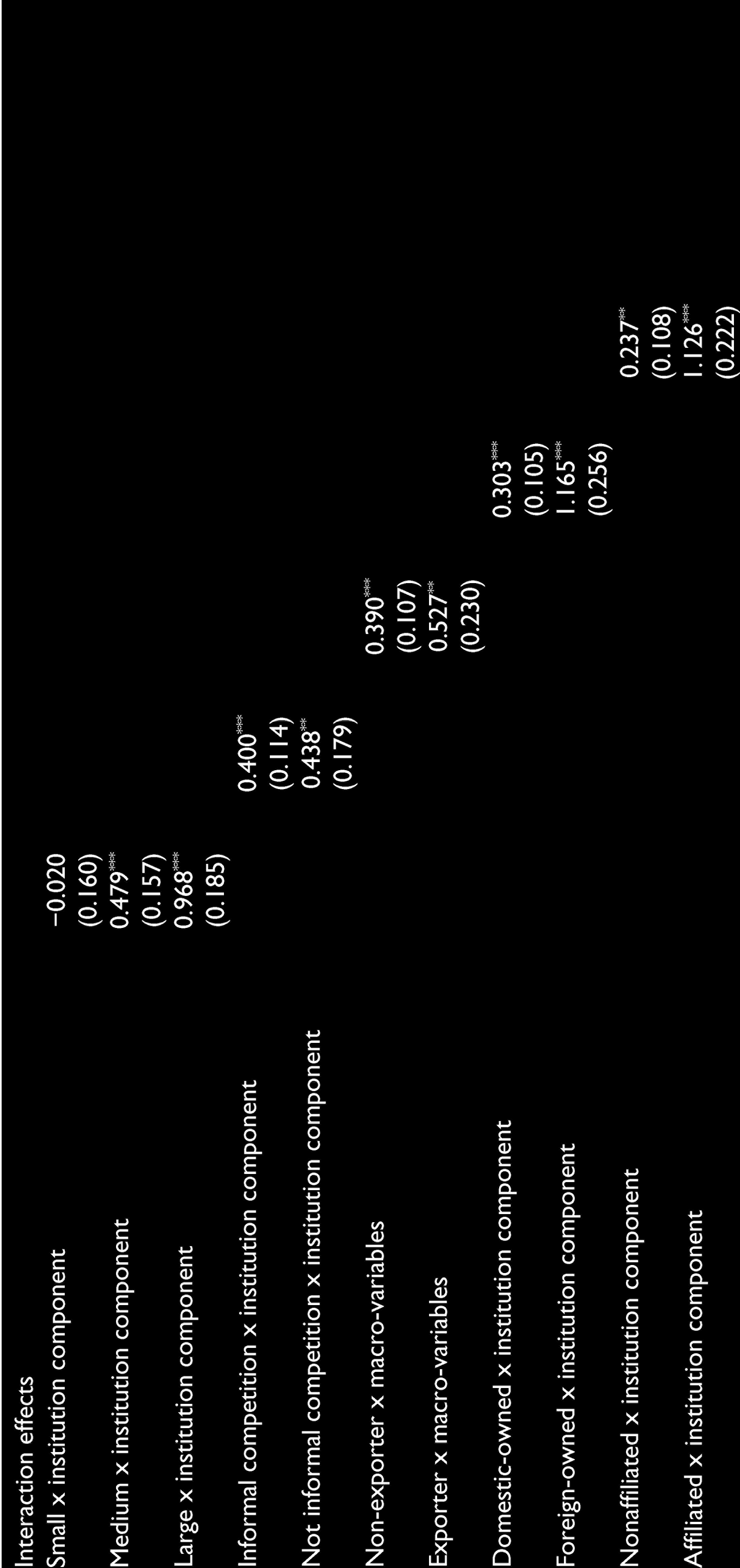

We examine whether the results are robust to several modifications, including different proxies for country-level variables, sample, and an alternative measure of dependent variable. First, we replace institutional quality by each of its components, private credit by bank competition and efficiency, and GDP growth rate by inflation rate and see how these different proxies affect our results. Panel A of Table 6 indicates that five components of institutional quality, bank concentration (five largest banks), Boone index, bid-ask spread, and inflation are significant determinants of financial obstacles. Panel B of Table 6 presents several notable findings, and we report the result of interaction terms only to save space (full regression results are available upon request). With regard to institutions, better institutions (a) reduce obstacles for financially constrained firms (small and medium; domestic-owned; and nonaffiliated) but simultaneously increase difficulties for financially favored firms (in cases of control of corruption and rule of law), (b) increase obstacles for firms across all characteristics (in the case of government effectiveness), (c) lessen obstacles for firms across most characteristics (in the case of regulatory quality), (d) does not affect obstacles for firms across most characteristics, except for the firm’s size (in the case of political stability and absence of violence/terrorism) and (e) increase obstacles for financially favored firms across most characteristics (in the case of voice and accountability). In contrast, firms across all characteristics receive benefits from higher level of bank competition, lower level of bid-ask spread, and lower level of inflation rate in dealing with financial obstacles (not reported here to save space). These findings confirm the main results of the different impacts of institutions, financial, and economic development.

Determinants of Firms’ Financing Obstacles: Robustness

Panel A

Panel B

Second, because the survey data were conducted over a period of 2 years—2016 and 2017—the time factor might affect our results regarding some of the other external economic variables. To deal with this potential problem, we remove countries for which the survey data were conducted in the year 2016 (El Salvador, Honduras, Nicaragua, and Dominican Republic). Except for several changes in the significance level of firm-level characteristics, the results, especially those of country-level variables, remain statistically unchanged (full regression results are available upon request).

Third, we construct another measure of financing constraints by organizing firms into two groups: firms that need credit and those that do not need credit. For firms that need credit, we identify those that applied for any lines of credit or loans, but the outcome was rejection. For firms that do not apply for any lines of credit or loans, we choose firms’ reason that it is because of complex application procedure, unfavorable interest rate, high collateral requirement, insufficient loan size and maturity, and being self-perceived that the loan will not be approved, other than the reason that the firms have enough capital. Based on these classifications, we create a dummy variable, which equals 1 if a firm is credit-constrained, and 0 otherwise. We then apply a logit model, instead of ordered logit model, and the dependent variable is a dummy variable. The result reveals that this modification yields similar conclusion to our baseline one (full regression results are available upon request).

5. Conclusions

Although the finance literature has clearly established the important role of firm-level characteristics in firms’ access to finance, it is conjectured that country-level characteristics, such as institutions, financial development, and economic growth could be the other key determinants. Moreover, given the erratic economic performance and underdeveloped institutional and financial fundamentals in the LAC region, better understanding of the financial obstacles of firms in this region, and especially the role of macroeconomic environment, has an important implication for both government and firms’ managers. We employ the World Bank’s Enterprise Surveys, World Development Indicators, Global Financial Development, and Worldwide Governance Indicators database for 4,690 firms in 12 LAC countries to investigate the determinants of financial obstacles. Specifically, we examine both the direct and moderating impact of institutional quality, financial development, and economic growth on firms’ access to finance.

The results show that larger firms facing less competition, foreign-owned firms, affiliated firms, firms facing less government regulation, and older firms report lower obstacles to finance. Better institutional, financial, and economic environment lessens the level of obstacles firms face when they obtain finance. With regard to moderation effect, the role of institutions in promoting inclusive finance is quite different to the role of financial development and economic growth. While the former helps reduce obstacles for small, domestically owned, and nonaffiliated firms, it increases obstacles for large, foreign-owned, and affiliated firms. In contrast, the improvement in financial and economic fundamentals lessens firms’ difficulty in obtaining finance. These results are robust to extensive robustness tests.

Our findings are not only noteworthy but also have significant policy implication. First, the findings highlight the characteristics of a financially constrained firm that are consistent with the existing literature. Therefore, firms’ managers should focus on their weaknesses as well as take advantage of the government’s policies to increase their access to finance. Given the high uncertainty in economic conditions, the firms should restructure their operation, for example, attracting foreign investors, improving the interconnections between firms, and reinvesting profit to increase size. Second, the government should focus on improving quality of institutions, financial markets, and economic conditions because they ameliorate firms’ that find it difficult to raise capital. Moreover, reducing the regulatory burden and ensuring a fair competitive business environment significantly lessen the financial obstacle for firms. Third, it points out the importance of having tailored and suitable policies from the governments rather than one-size-fits-all solutions, for improving the financial inclusion in the LAC region. For example, an improvement in control of corruption and rule of law should help level the playing field between small and large firms, domestic-owned and foreign-owned, and nonaffiliated and affiliated firms. In contrast, difficulties in accessing finance are found to be reduced for firms across all characteristics if regulatory quality is improved.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.