Abstract

This article examines the effect of economic policy uncertainty (EPU) on the dividend policies of Vietnamese listed firms moderated by the role of government shareholders. A wide range of control variables and different regression methods are used to ensure the reliability of the results. We find that firms distribute more cash to shareholders under increased EPU. Notably, the presence of the government shareholder reduces the effect of EPU on dividends. Further analyses indicate that firms with state ownership cut dividends for increasing capital expenditures rather than other purposes such as cash hoarding, debt reduction, inventory expansion, or dealing with declined profits. This article enhances the understanding about the connection between government ownership, EPU, and dividend policy.

1. Introduction

Dividend policy is 1 of the most important pillars of corporate finance. After the 2007–2008 financial crisis, the global environment has become more uncertain for firms in nearly all countries. In such a situation, firms are required to understand the possible impacts of uncertainty and make appropriate adjustments to their dividend policies. Uncertainty comes from many sources and can be understood in different ways. For instance, uncertainty can be regarded as political crisis (Huang et al., 2015), political uncertainty (Farooq & Ahmed, 2019), financial crisis (Bliss et al., 2015), cash-flow variability (Chay & Sud, 2009), etc. Baker et al. (2016) developed a new measure known as “Economic Policy Uncertainty” (EPU) that effectively reflects the complicated and multi-dimensional nature of uncertainty. However, the EPU has been constructed for 29 countries so far, making it unavailable for investigating its effects in other countries. The research of Ahir et al. (2018) provides an alternative for the EPU by constructing the world uncertainty index for 143 countries. Since then, a considerable number of studies have examined the influences of economic uncertainty on corporate decisions in general and dividend policy in particular. The findings of existing articles indicate that economic uncertainty can either positively or negatively affect firms’ dividend payouts, which can be explained by the 2 main motives. The agency motive argues that when the uncertainty increases, firms distribute more dividends to shareholders to reduce agency problems while the precautionary motive predicts that firms retain more earnings and decrease dividends to deal with the higher uncertainty.

This article investigates the impacts of the EPU on the dividend policies of Vietnamese firms and examines the role of government ownership in determining the connection between uncertainty and firms’ dividend policies. Vietnam is focused by this article due to its unique political-economic characteristics. Particularly, Vietnam is a socialist-oriented market economy where the state has a special role in maintaining the stability and development of the whole country. Through government ownership, the state exerts control over the key sectors of the economy. Due to the presence of government ownership, many listed firms in the stock market can be more resilient to unfavorable shocks during crises or uncertain periods. While Vietnam and China have some similarities in terms of political environment and the special roles of government ownership in vital industries, they also have distinctive features. For instance, China is among the largest economies in the world while Vietnam is a small emerging country. This implies that the responses of Vietnamese firms in revising their dividend policies, moderated by the unique role of state ownership, under the influence of EPU are distinguishable from those of the Chinese counterparts. As no research has examined the case of Vietnam, a gap remains in understanding how Vietnam’s specific institutional characteristics influence firms’ dividend policies in times of EPU.

This article uses the data covering the 2010–2021 period and includes a wide range of control variables. The results show that when policy uncertainty increases, Vietnamese firms increase the dividend-to-asset ratio. Nevertheless, the presence of government ownership reduces the positive effect of uncertainty on dividend payouts. The results are robust among several robustness checks, including alternative measures of dividends, different proxies of government shareholder presence, other types of ownership, macroeconomic condition controls, and alternative estimation methods. Provided the lower dividend of firms with the presence of government shareholders, we seek the explanations that we think may come from state-owned firms’ poorer performance or the other use of cash from dividend cutting. We find that government-owned firms cut dividends under high uncertainty not for reasons such as hoarding more cash, paying off debts, increasing inventories, or poorer performance, but for increasing capital expenditure.

This article contributes to the current literature by enhancing our understanding of the interplay among government ownership, policy uncertainty, and dividend policy. While the current literature predominantly concentrates on the connection in mature markets (Attig et al., 2021; Baker et al., 2021; Tran, 2020), this study provides insights into the nexus in a small developing country. The degree of EPU and its impact on corporate policies in developing countries are believed to be dissimilar to that of developed countries. Emerging markets, also their firms, can be heavily affected by the uncertainty of economic policies all around the world (Amendolagine et al., 2019; Hansen & Rand, 2006; Makki & Somwaru, 2004) and have weaker shock absorbers (Loayza et al., 2007). Moreover, while government ownership has been found as a crucial factor influencing dividend policy (see Ankudinov & Lebedev, 2016; Lei et al., 2015; Sarwar et al., 2020), the significance of government ownership in the connection between policy uncertainty and dividend policy has been insufficiently explored. Recent studies predominantly highlight the effects of state ownership in firms within emerging markets, such as agency problems and potential expropriation under normal circumstances (Bai et al., 2013; Lin et al., 2010; Tian & Estrin, 2008). However, there exists a notable gap in understanding the intervention of the government shareholder under conditions of greater uncertainty where the positive aspects of state ownership may be more likely revealed. For instance, as a stakeholder in a firm, the government shareholder possesses the capacity to guide the company toward tangible initiatives, such as fostering investments that are typically more restrained in times of high uncertainty. This proactive role of the government shareholder can contribute to economic stimulation and employment stabilization. By focusing on the distinguishable dividend policies of state-owned firms in contrast to other firms under uncertain conditions and exploring plausible explanations for these variations, the article highlights the impact of government shareholder presence on corporate decisions in order to mitigate the influence of external uncertainty on real activities in such scenarios. This finding diverges from the evidence in China, where Sarwar et al. (2020) observe that Chinese state-owned enterprises exhibit a higher probability of initiating dividend payouts and a lower likelihood of discontinuing them when faced with heightened EPU, which is attributed to their convenient access to external funds, such as loans from state-owned banks and the support provided by the government during periods of increased uncertainty.

The rest of this article is organized into 4 sections. Section 2 summarizes the relevant studies and proposes the hypotheses. Section 3 describes the methodology and data. Section 4 reports the empirical results and discussion. Section 5 displays the concluding remarks of the article.

2. Literature Review and Hypothesis Development

Firms’ dividend policies are so interesting that numerous studies have examined their diverse aspects in different circumstances (Allen & Michaely, 2003; Baker & Weigand, 2015; Ed-Dafali et al., 2023). The number of published articles about dividend policies has proliferated since 2005, and most of them are conducted in the US and the UK, while many issues relating to emerging markets are unexplored (Pinto et al., 2020). The remaining of this section provides a review of some notable studies and depicts the hypotheses to be tested.

The role of uncertainty in affecting firms’ dividend policies has become increasingly important since the 2007–2008 financial crisis. Many articles focus on event-based uncertainty, especially the 1 connected with political and financial crises, in examining the linkage between uncertainty and firms’ dividend policies. For example, Huang et al. (2015) examined the impacts of political crises (measured by the number of political crises per annum) on the dividend policies of firms in 35 countries during the period 1990–2008. They reported that the rise of political crisis increased the chance of dividend termination and reduced the probability of dividend initiation. Farooq and Ahmed (2019) found that firms in the US paid more dividends during the election years than the non-election years, which indicated the significant impact of political uncertainty on dividend policies. Lei et al. (2015) measured the political uncertainty in China by the change of regional party leaders and documented that the uncertainty negatively affected firms’ dividend payouts. Bliss et al. (2015) observed that US firms, especially those with high leverage and low cash balance, significantly cut dividend payouts during the 2007–2008 financial crisis, which is compatible with the findings of Hauser (2013). Besides the uncertainty associated with political and financial crises, some other studies examined the roles of other events, especially the COVID-19 pandemic, in affecting firms’ dividend payouts. For instance, Krieger et al. (2021) used the sample of US firms from 2015Q1 to 2020Q2 to analyze the impact of COVID-19 on dividend payouts. They showed that the COVID-19 pandemic strongly reduced firms’ dividend payouts in all industries. Accordingly, they commented that while the 2007–2008 financial crisis mainly affected the dividend payouts of financial firms, the COVID-19 pandemic influenced both financial and non-financial firms. Ali (2022) scrutinized 8,889 firms in G-12 countries during the period 2015–2020 and demonstrated that the COVID-19 pandemic caused the drop, as well as, the omission of dividends. Ntantamis and Zhou (2022) inspected the dividend policies of G-7 countries’ firms under the impact of COVID-19. They observed a noticeable reduction in the dividend payouts of the firms in France, Germany, Italy, and the UK. Buchanan et al. (2017) investigated the impacts of the uncertainty from the change of US tax policies on firms’ dividend policies. They reported that the expected rise in tax increased dividend payments and dividend initiation as well.

The event-induced approaches to uncertainty used by most of the existing research fail to capture the uncertainty during non-event periods (Attig et al., 2021). Moreover, a single measure of uncertainty in the event-induced approaches cannot completely reflect different aspects of uncertainty. Therefore, to overcome this limitation, recent studies utilize the EPU developed by Baker et al. (2016) to effectively capture the multi-dimensional uncertainty. The connection between the EPU and dividend policy can be explained by 2 major mechanisms. The first 1 relates to agency problem (Jensen & Meckling, 1976), which can escalate when firms reduce investment and hold more cash during periods of high EPU. And investors also prefer more dividends in times of high uncertainty (Bilel & Mondher, 2021). In response, firms pay more dividends to deal with the heightened agency problem (Attig et al., 2021). Thus, the agency-problem channel predicts that the EPU positively affects dividend payment. The second mechanism relates to the precautionary motive of firms’ dividend policies. As EPU can lead to heightened risks in firms’ operations, declined revenue, and increased income volatility, firms can choose to lower dividends to allow firms to conserve more cash to deal with the risks as well as decrease their reliance on external funding (Krieger et al., 2021; Lie, 2005). Also, by reducing dividends, firms can finance their operations or investments internally, avoiding raising capital under unfavorable conditions (Lie, 2005). Besides the 2 main mechanisms, the impact of EPU on dividend payment can also be explained by the signaling theory (Bhattacharya, 1979; John & Williams, 1985). Specifically, raising dividends is regarded as a signal for firms’ optimistic profitability in the future (Kanojia & Bhatia, 2023; Miller & Rock, 1985). Thus, in times of high EPU, firms, especially the high-performing ones, increase dividend payments to show their capabilities, as well as, commitments for future growth, which goes in line with the demand of shareholders (Baker et al., 2021).

Attig et al. (2021) examined the relationship between the EPU and the dividend policies of 23,042 firms in 19 countries (Australia, Brazil, Canada, Chile, China, France, Germany, India, Ireland, Italy, Japan, the Netherlands, Russia, Singapore, South Korea, Spain, Sweden, the UK, and the US). They showed that firms raise dividend payouts when the EPU increases to reduce the agency problem. Tran (2020) investigated the bank-holding firms in the US and documented that more dividends are paid during high EPU periods. Baker et al. (2021) also reported that the EPU positively influenced the dividend payouts of US firms.

Meanwhile, Sarwar et al. (2020), together with Sarwar and Hassan (2021), observed the negative impact of the EPU on the dividend payment of Chinese firms. Namely, when the EPU increases, the probability of dividend initiation (termination) is lower (higher). This outcome can be attributed to the rise of managers’ perceived risks and costs of external capital. Alternatively, firms cut dividends for a precautionary motive.

To the authors’ knowledge, the connection between EPU and firms’ dividend policies is a new research topic of recent studies that have emphasized only a limited number of countries, especially the US and China. And the lack of empirical evidence for emerging markets is noticeable. For instance, to the authors’ knowledge, no research on the link between EPU and firms’ dividend policies is available for Vietnam—an emerging country with an interesting political-economic environment. Thus, this article tries to provide new empirical evidence for the case of Vietnamese firms. As the EPU can positively affect firms’ dividend payouts (due to the agency-reduction motive) or has a negative impact (due to the precautionary motive), we construct the first hypothesis to be tested in this article as follows:

H1: Vietnamese firms raise dividend payouts when economic policy uncertainty increases. H1b: Vietnamese firms cut dividend payouts when economic policy uncertainty increases.

Ownership structure is an essential determinant of firm dividend policy (Jacob & Lukose, 2018; Kumar, 2006). And the linkage between the EPU and dividend payouts can be moderated by the ownership structure, especially state ownership. Sarwar et al. (2020) documented that state ownership is an important factor influencing Chinese firms’ dividend payouts. Specifically, while the non-state-owned firms cut dividends under the impact of the high EPU, the state-owned ones increased the dividend payouts. They explained that the state-owned firms play a vital role in the Chinese economy and thus can receive support from the government and gain more access to external funds. To the authors’ knowledge, Sarwar et al. (2020) is the only research that investigates the moderating effect of ownership structure in the connection between the EPU and dividend policies. However, the work of Sarwar et al. (2020) can be compared with some studies that scrutinized the moderating role of ownership structure in the linkage between event-based uncertainty and firms’ dividend payouts. For example, Lei et al. (2015) found that state ownership reduces Chinese firm’s dividends during high political uncertainty, which is different from the results of Sarwar et al. (2020). Besides, Ankudinov and Lebedev (2016) found that state ownership diminishes the dividend payouts of Russian firms during the financial crisis. Thus, based on the existing literature, it can be concluded that the moderating effect of state ownership in the relationship between the EPU and firms’ dividend policies can be positive (Sarwar et al., 2020) or negative. Therefore, in this article, we propose the second hypothesis as follows:

H2a: Vietnamese firms owned by the state increase dividend payouts when economic policy uncertainty increases. H2b: Vietnamese firms owned by the state decrease dividend payouts when economic policy uncertainty increases.

3. Data and Models

3.1. Sample Selection

We utilize the sample period from 2010 to 2021. The data from 2009 and backwards are not included in the model to eliminate the impact of the global financial crisis 2007–2009. The sample is selected based on the following criteria: non-financial firms, at least 3 yearly observations in a row, and non-missing dividend data. Financial data, stock return data, analyst data, and ownership structure (state-owned, institutional, foreign, and block) are collected from Datastream. We also collect manually who provides auditing services for firms. We winsorize all variables at 5% 2 tails, except the dummy variables. The EPU is the world uncertainty index, obtained from

3.2. Model

To examine the effects of the EPU on dividends, we use this regression model:

To investigate the effect of state ownership on the DIV-EPU relationship, we add state ownership (GOV) and its interaction term with EPU in the model (1) to obtain:

In these models, the dependent variable, DIV, is cash dividend scaled by one-lag total assets. In the robustness check, we use 2 alternative dividend measures, namely dividend change and dividend scaled by accumulative retained earnings. We do not use dividends to earnings since some firms have negative earnings in a certain year. The main independent variable in Equation (1) is EPU. X is a vector of control variables, including firm characteristics and outside corporate governance. These control variables are selected based on the literature of dividend policy, such as Tobin’s Q (Bliss et al., 2015; Huang et al., 2015; Kahle & Stulz, 2021; Sarwar & Hassan, 2021; Sarwar et al., 2020); cash flows (Attig et al., 2021; Bliss et al., 2015; Holder et al., 1998; Kahle & Stulz, 2021); Retained earnings (Attig et al., 2021; Hauser, 2013; Sarwar & Hassan, 2021); Leverage (Ali et al., 2022; Attig et al., 2021; Baker et al., 2021; Farooq & Ahmed, 2019; Huang et al., 2015); Capital expenditure (Baker et al., 2021; Farooq & Ahmed, 2019; Kahle & Stulz, 2021); Loss (Bliss et al., 2015; Kahle & Stulz, 2021; Tran, 2020); Profitability (Attig et al., 2021; Baker et al., 2021; Huang et al., 2015; Sarwar et al., 2020; Setiawan et al., 2016); Log of assets (Attig et al., 2021; Huang et al., 2015; Kahle & Stulz, 2021; Mehdi et al., 2017; Tran, 2020); Asset growth (Huang et al., 2015; Sarwar & Hassan, 2021; Tran, 2020); Stock return volatility (Baker et al., 2021; Holder et al., 1998; Huang et al., 2015; Sarwar et al., 2020); Cash-flow volatility (Bliss et al., 2015; Chay & Sud, 2009); and Analyst coverage (Farooq & Ahmed, 2019; Huang et al., 2015). We also control for ROA volatility and stock return. ϑi is time-invariant unobservable variable, and ε it is an error term.

In the robustness check, we include more control variables for other types of ownership (i.e., state-owned, institutional, foreign, and block) because they are corporate governance mechanisms that can affect firm payouts. We also include 2 macroeconomic factors (i.e., the change in log of CPI and the change in log of GDP) because the impacts of the EPU on dividends may eventually originate from macroeconomic conditions that have not been included in the model. We also allow for dividend adjustment by including the lag of the dependent variable. The definitions of all variables are presented in the Appendix section (Table A1).

4. Results and Discussions

4.1 Summary Statistics

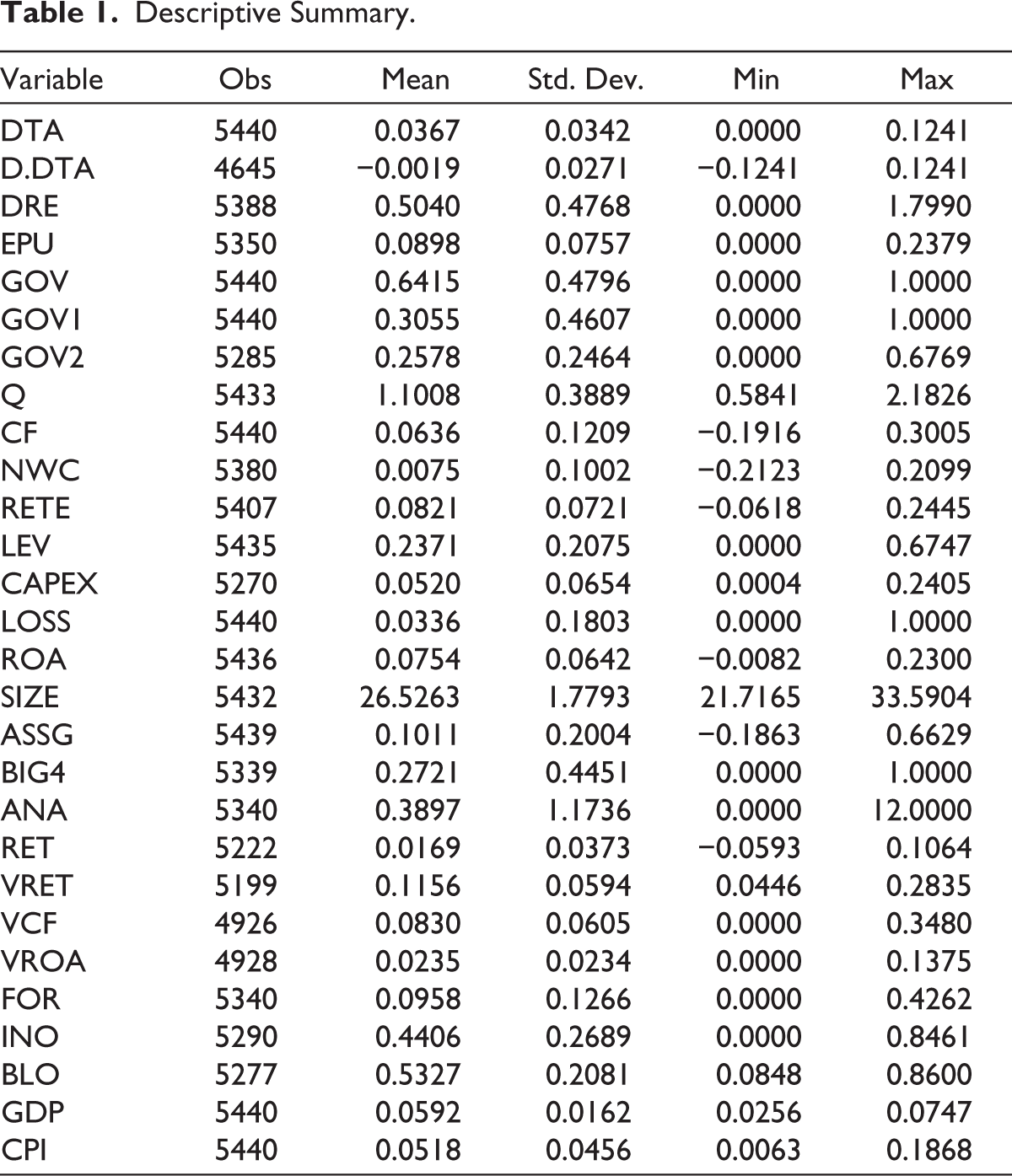

The summary statistics of the variables are shown in Table 1. On average, the dividend of a Vietnamese firm is equivalent to 3.7% of total assets or 50% of retained earnings. Over the research period, dividend on total assets decreases by −0.19%. The mean of EPU is approximately 9%. Government ownership is 25% of shares, 60% of the firms in the sample have the government as a shareholder, and 30% of the firms have government as the control shareholder (holding over 50% of firm shares).

Descriptive Summary.

4.2 Main Results

4.2.1 The Effects of the EPU on Corporate Dividends

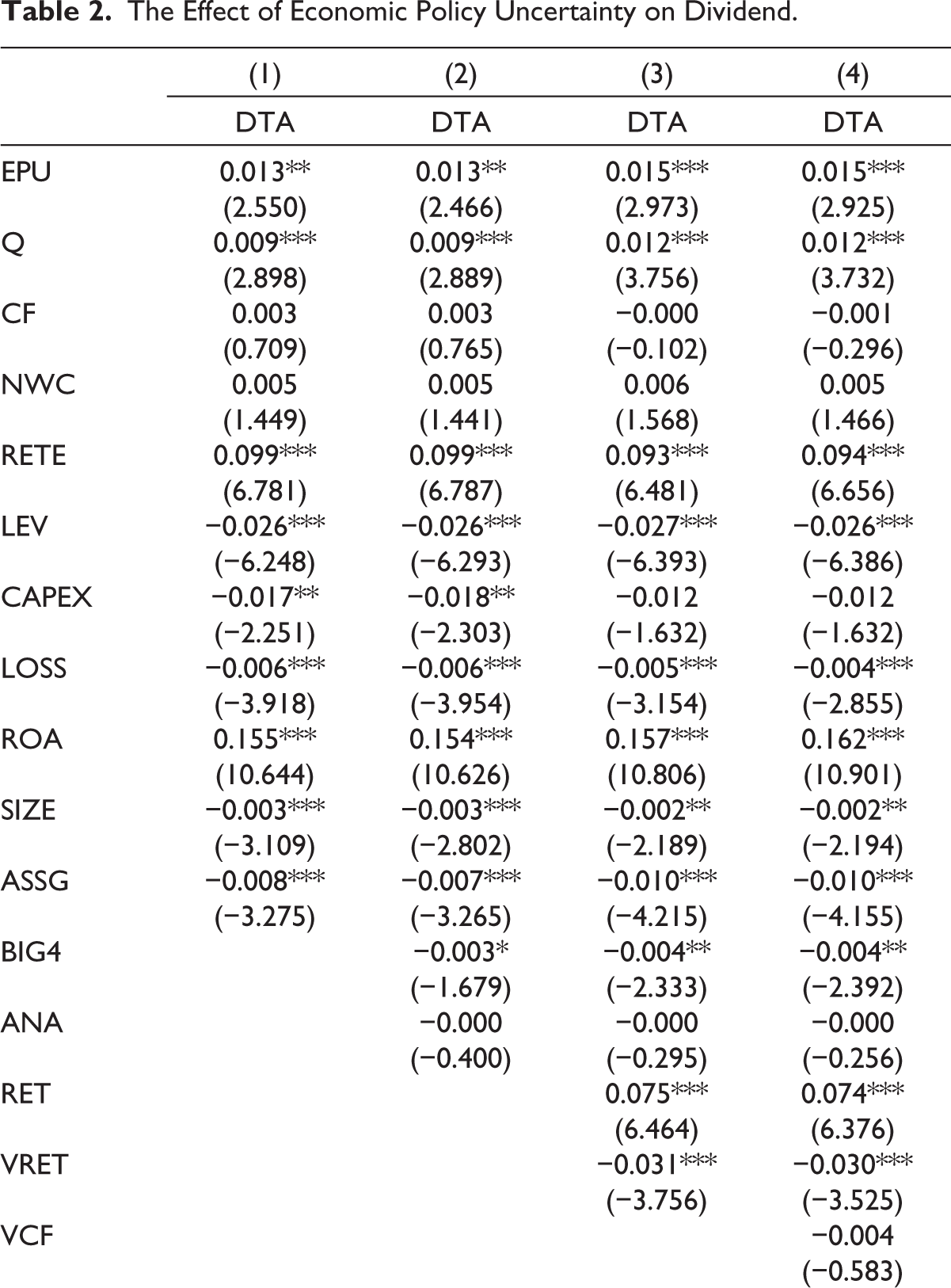

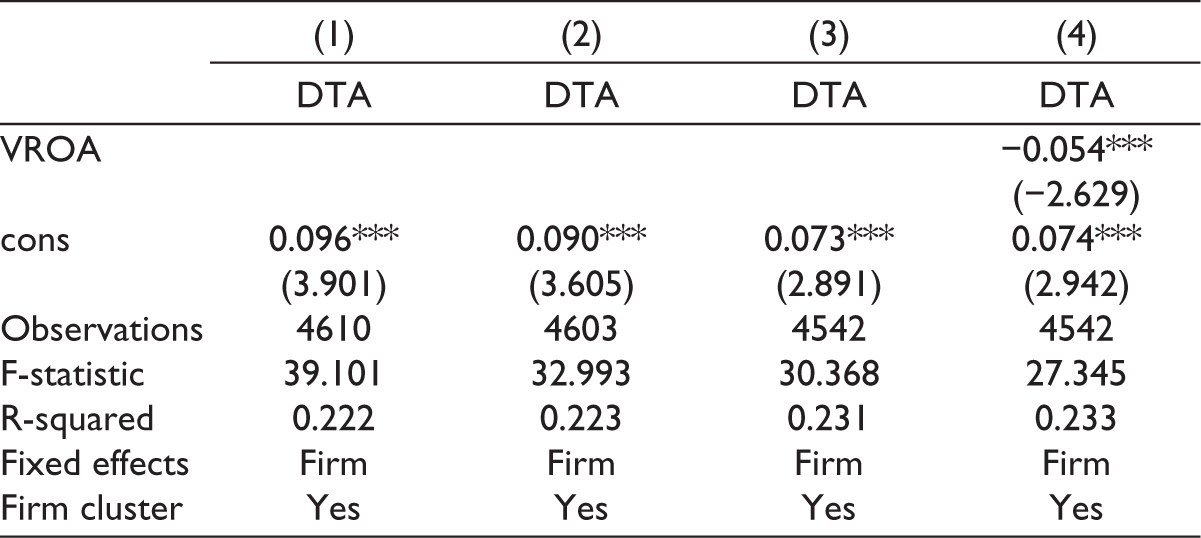

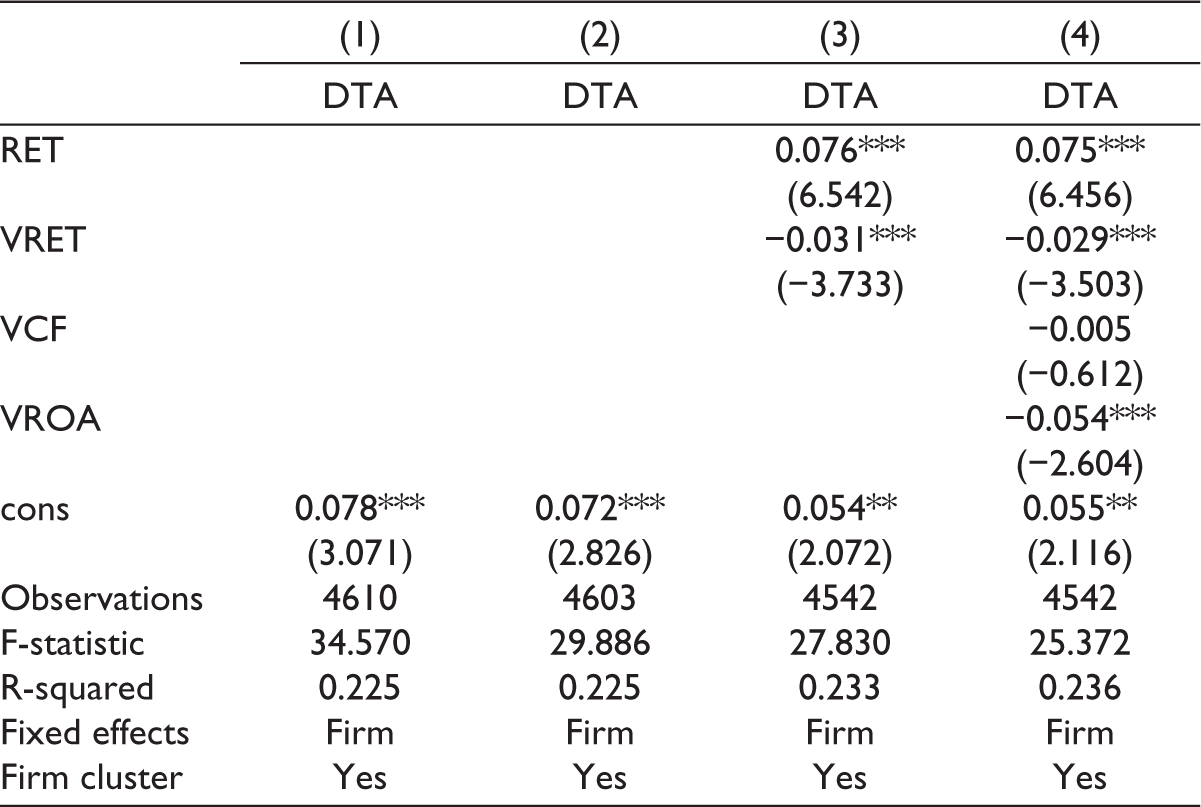

We start our analysis by conducting the empirical test for the first hypothesis regarding the effects of the EPU on firm dividend payouts. The results of the test are presented in Table 2. From Column (1) to Column (4), we gradually add more control variables. Specifically, in Column (1), we control for baseline firm-specific variables; in Column (2), we control for 2 additional variables, Big4 and Analyst, which represent external monitoring; in Column (3), we add 2 variables of the firms’ stock market conditions, stock returns and stock volatility; and finally, the internal uncertainty which is represented by the volatility of cash flows and the volatility of profitability are also controlled in Column (4). In all 4 regressions, standard errors are clustered by firm.

The Effect of Economic Policy Uncertainty on Dividend.

As reported in Table 2, the coefficients of EPU are positive and significant at or below the 5% level, and the coefficients’ magnitude is stable among the 4 specifications, indicating that the effects of the EPU on Vietnamese firms’ dividend policies are strong and consistent. To be more specific, we use the result in Column (4) to quantify the EPU’s impacts on dividend. One standard deviation increase in EPU is associated with a 0.033 standard deviation increase in DTA. This result suggests that higher EPU is positively associated with higher corporate dividend. With this positive impact of the EPU on dividends, our finding is consistent with the hypothesis H1a which states that firms increase dividend payouts when they confront a higher level of uncertainty in economic policy. This supports the rationale of the agency-problem argument and goes in line with Attig et al. (2021) and Baker et al. (2021). It is possible that Vietnamese firms are perceived to have lower transparency and potential misuse of cash especially in the heightened time of uncertainty. Investors may worry about that misuse and demand the firms to pay higher dividends, and managers may not ignore shareholders’ wants to improve the firms’ image or reduce investors’ concerns.

4.2.2 The Effects of the EPU on Dividends Conditional on State Ownership

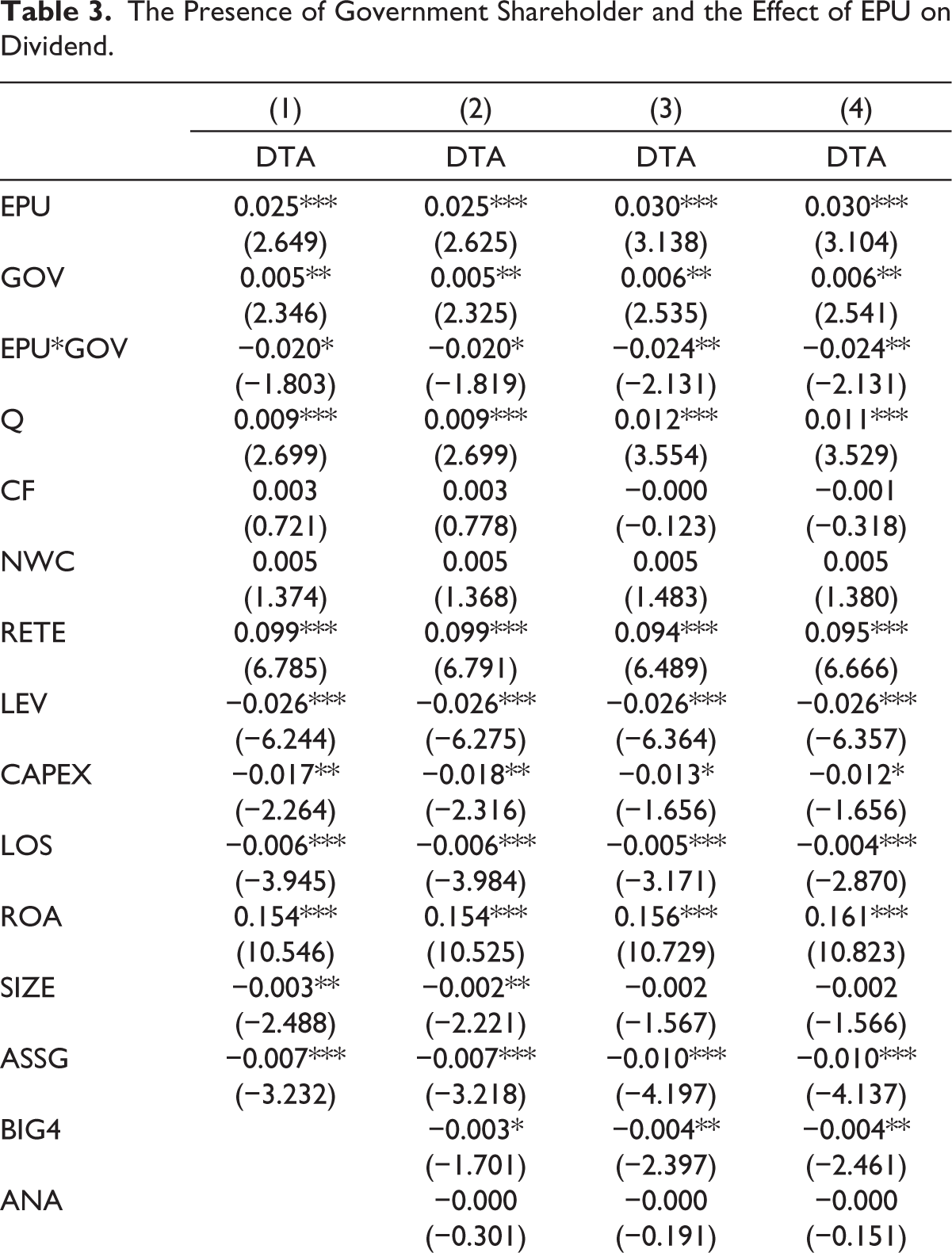

The empirical test for the second hypothesis is presented in Table 3. In Columns (1) to (4), we control for the variables similar to those used to test the hypothesis 1. The variable of interest in this test is the interaction term between EPU and GOV (i.e., EPU*GOV). The results show that the coefficients of this variable are negative at the 10% or 5% significant level. Taking the result in the last 2 columns for quantifying the economic significance, 1 standard deviation increase in EPU is associated with 0.013 standard deviation decrease in DTA of stat-owned firms compared to non-state-owned firms. We also note that the stand-alone state ownership is still positively related to dividends.

The Presence of Government Shareholder and the Effect of EPU on Dividend.

4.2.3 Robustness Checks

4.2.3.1 Alternative Dividend Measures

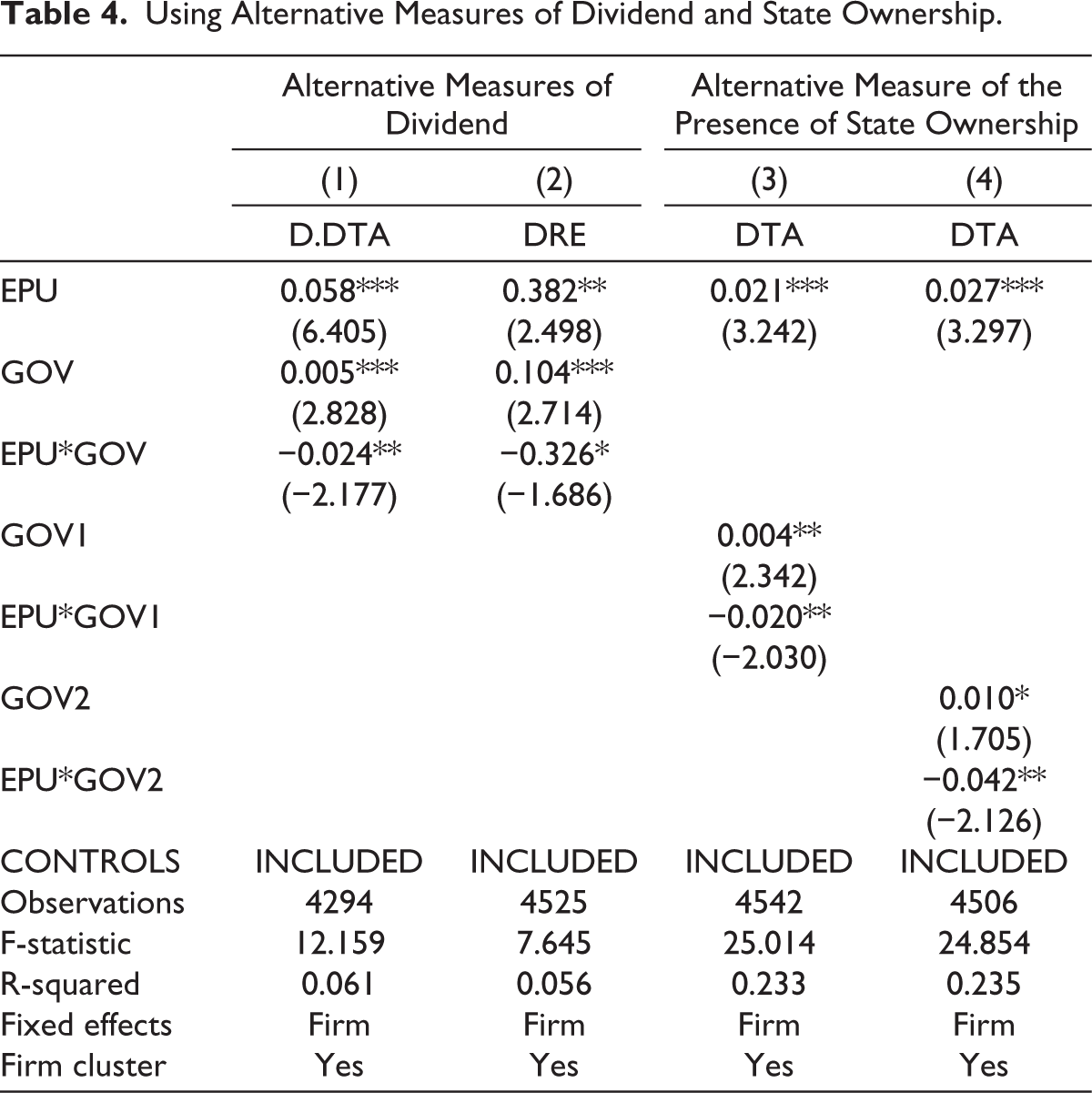

The first robustness check is to test whether the main results presented in Sections 4.2.1 and 4.2.2 still hold with alternative dividend measures, including DRE (dividends over retained earnings) and DDIV (the change of the ratio of dividends over total assets). We control for all variables used in the above regressions, and standard errors are clustered by firm. The result for D.DTA is presented in Column (1), and the result for DRE is in Column (2) of Table 4. As the table shows, the coefficients of EPU are positive and significant. D.DTA (DRE) increases following an increase in the EPU, consistent with hypothesis H1a. In addition, the coefficients on interaction term, EPU*GOV, are negative and significant in both columns, consistent with hypothesis H2a. It is not useful to compare the magnitude of the coefficients on EPU variables and the interaction variables in Table 4 with those in Tables 2 and 3 due to the different measures of the dependent variable.

Using Alternative Measures of Dividend and State Ownership.

4.2.3.2 Alternative Measure of the Presence of State Ownership

In the main results, we define state-owned firms as those with the government as a shareholder. In this robustness check, we assign a firm with state ownership if the government holds over 50% of the shares outstanding. This definition is stricter because it requires a larger holding of government. In addition, we also use the actual proportion of government holdings, meaning that the state ownership is a continuous variable. Column (3) and (4) of Table 4 present the results using the dummy and continuous variable of state ownership, respectively. The results still support our hypotheses that EPU affects dividend negatively, and government ownership reduces the impact of the EPU on dividends, indicating that higher government holding lowers the positive impact of the EPU.

4.2.3.3 Controlling for Other Ownership, Macroeconomic Factors, and Allowing Dividend Adjustment

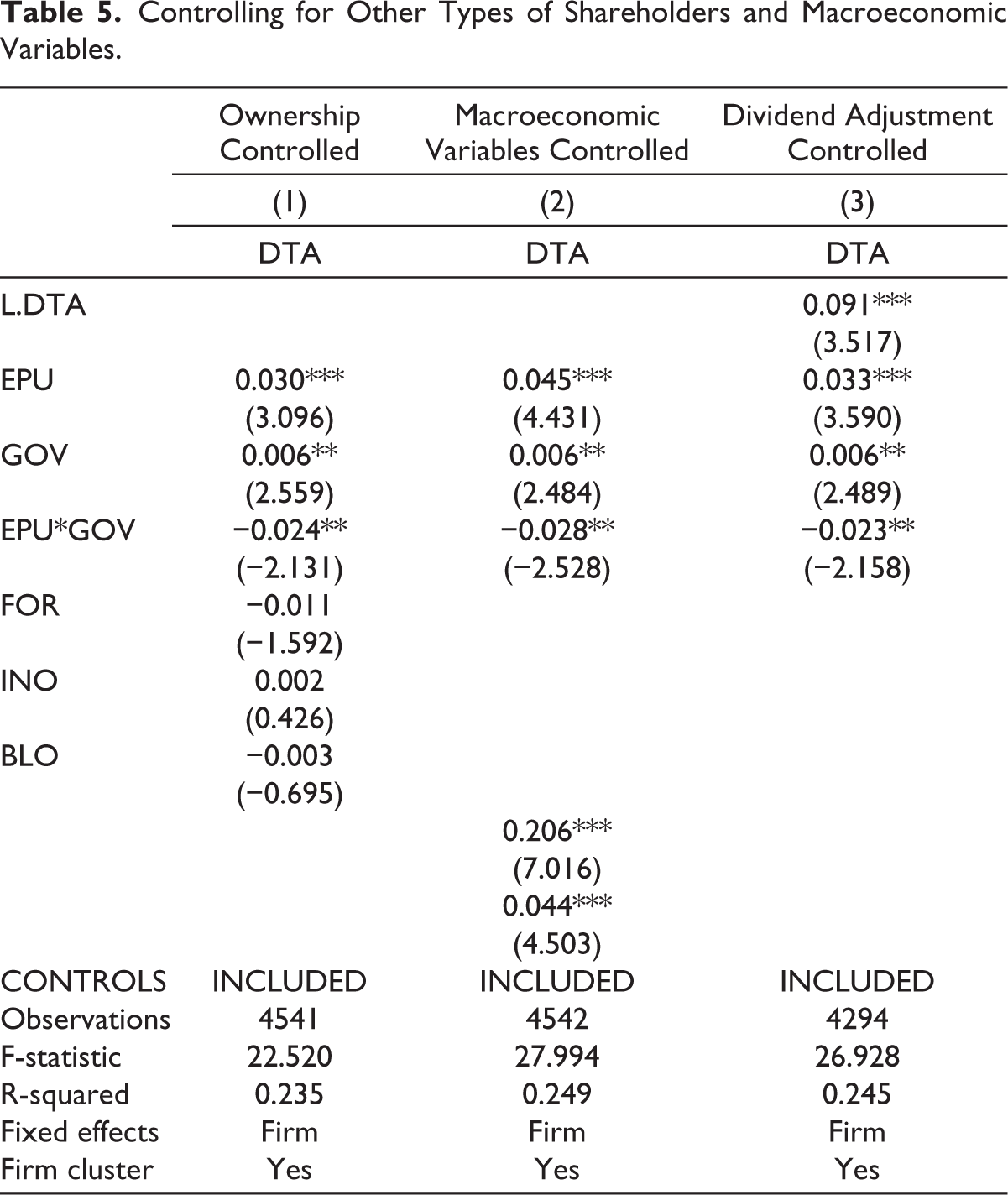

The results when controlling for other types of ownership (foreign owned, institutional owned, and block holdings) are presented in Column 1 of Table 5. As can be seen, adding these types of ownership does not change the main results. The coefficients of the EPU and the interaction term (EPU*GOV) are similar in terms of coefficient magnitude and significant levels to those in Column (4) of Table 3. Thus, these results confirm our findings and indicate that our results are robust.

In our main regressions, we do not control for time-fixed effects because the EPU is the same for all firm-year observations at a particular year, and controlling for years will eliminate the independent variable of interest. However, the lack of time-fixed effects might raise a question that the effect of the EPU on firms’ dividends is actually the impact of important macroeconomic conditions that have not included in the regressions. To alleviate this concern, we re-estimate our regressions controlling for macroeconomic conditions, represented by 2 key variables—GDP growth rate (in real term) and inflation rate. The result in Column 2 of Table 5 shows that the effect of the EPU and EPU with the presence of state ownership on dividends remains stable, with positive and significant coefficients of the EPU and a negative and significant coefficient of the interaction term between the EPU and GOV, except for the larger coefficients compared to main results. This implies that the effects are stronger after controlling for macroeconomic conditions.

Controlling for Other Types of Shareholders and Macroeconomic Variables.

The current literature stated that firms tend to adjust their dividend slowly, thus we incorporate this in our analysis by including a lagged dividend as an independent variable. The result is shown in Column 3 of Table 5, in which the effects of the EPU on dividends and the role of government shareholder are similar to our main results.

4.2.3.4 Alternative Estimation Methods

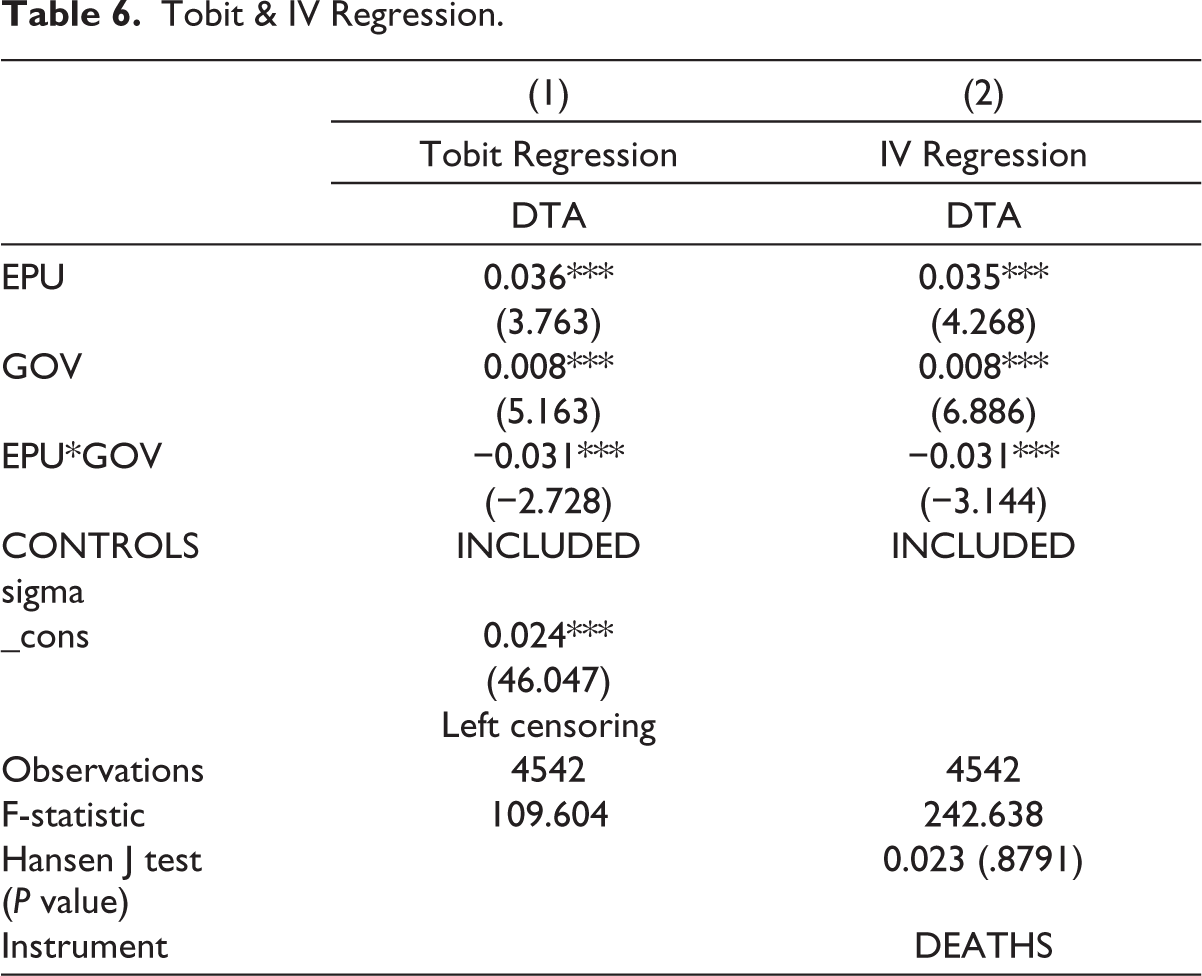

In this section, we conduct 2 alternative estimation methods, Tobit regression and instrumental regression. Employing Tobit as a robustness check follows the previous literature (Al-Najjar & Hussainey, 2009; Setiawan et al., 2016). For IV regression, we propose the number of deaths from disasters an instrument for the EPU (Tran et al., 2024). The rationale is that natural disasters cause death losses for a country, and the more death losses, the more likely the government adjusts its economic policy to help recover from the adverse effects, making the number of deaths from disasters relevant to the EPU. In addition, there is no clear direct impact of the number of deaths from disasters on dividend policies, making this instrument satisfying exogenous criteria.

The outcomes of Tobit and IV regression are reported in Table 6. Both show that the effects of the EPU and EPU*GOV are consistent with the main results in terms of sign and significance level.

Tobit & IV Regression.

4.3 The Possible Explanations for Lower Dividends in Firms with the Government Shareholder Presence When Confronted High EPU

Our results support the hypothesis that state-owned firms exhibit a tendency to distribute lower dividends compared to their non-state-owned counterparts as the EPU increases. This prompts the question about the purpose behind the dividend reduction and the allocation of the resources freed up by such cuts.

To seek the answer, we focus on the key items on the balance sheet and firm profitability. In particular, we test the following predictions. First, lower dividends may be for saving money for hedging purposes under uncertainty. Second, lower dividends may be for increasing inventory because of the concern that uncertainty may affect the inputs’ prices, thereby harming the firm profitability. Third, firms may cut dividends under uncertainty to finance capital expenditure to seize opportunities that can be created by uncertainty but are costly to finance externally. For firms with state ownership, the increase in capital expenditure under uncertainty may be because of another reason: state-owned firms are often driven by strategic objectives beyond solely maximizing shareholder value. These objectives may include promoting social welfare, economic development, employment stability, or supporting specific industries. During economic uncertainty, governments may prioritize retaining earnings in state-owned firms to support their strategic goals rather than distributing dividends. Fourthly, the source of dividend cuts may be used to pay off existing debt to reduce interest burden under uncertainty. Finally, the reduced dividends of firms owned by government may be due to decreased profitability during the highly uncertain period.

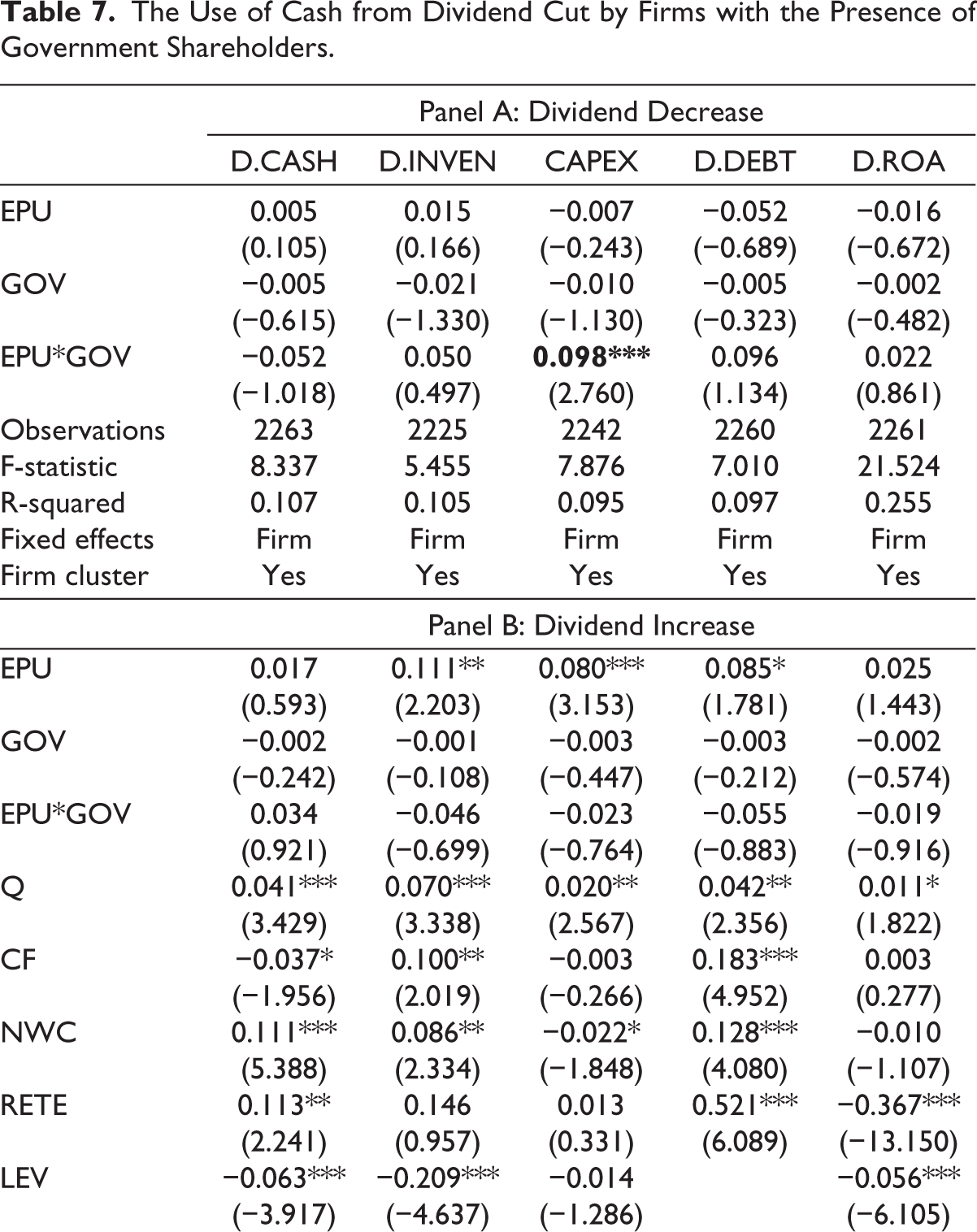

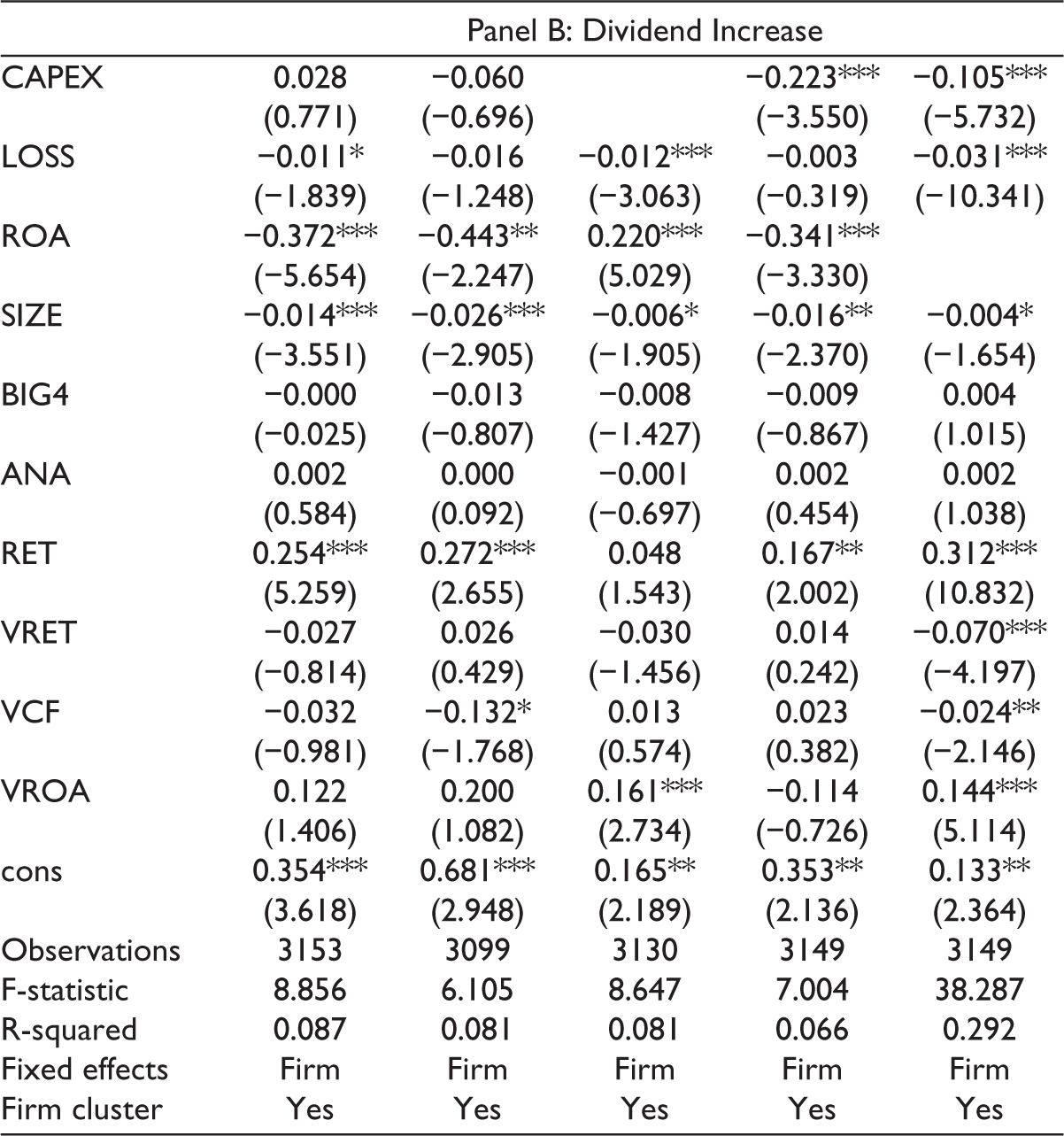

We test these predictions by running regressions of change in cash (D.CASH), change in inventory (D.INVEN), Capital expenditures (CAPEX), change in debt (D.DEBT), and change in profitability (ROA) on the interaction term of EPU*GOV and controlled variables. In Table 7, Panel A shows estimates for firm-year observations that have a dividend decrease, and Panel B shows estimates for firm-year observations that have a dividend increase. The results show that the only case where EPU*GOV has an impact is CAPEX of decreasing dividend firms. The coefficient is 0.098 and statistically significant at the 1% level. At the same time, no evidence is found for the predictions that dividend cuts by state-owned firms under uncertainty are for increasing cash reserves, increasing inventory, or paying off debt. The results in the last columns of Panel A and B show that profitability is not the driver of dividend cut of these firms when they confront uncertainty.

The Use of Cash from Dividend Cut by Firms with the Presence of Government Shareholders.

5. Remarked Conclusion

This research examines the relationship between EPU and the dividend policies of companies listed in Vietnam’s stock markets. Additionally, it explores the impact of government shareholders on this connection. The study’s findings reveal that when the EPU rises, Vietnamese firms distribute greater dividends to their shareholders. However, a distinctive pattern emerges when examining firms with and without government shareholders. For the former, the positive correlation between the uncertainty and dividends is mitigated, suggesting a unique influence of state ownership on dividend policies under conditions of uncertainty. To gain a deeper understanding of this phenomenon, the study scrutinizes the factors contributing to the divergence in dividend policies among state-owned firms and non-state-owned firms. The article documents that the divergence is primarily attributed to an escalation in the firm’s investment activities, while there is no conclusive evidence to suggest that these state-owned enterprises engage in cash hoarding, debt reduction, inventory expansion, or experience a decline in profitability.

The results of this article can give some implications for policy-makers and shareholders. First, the reduction of dividends in firms with government ownership during high uncertainty periods may affect the interest of non-government shareholders in such firms because cutting dividends by state-owned firms to increase capital expenditures under uncertainty can lead to overinvest. Second, the government and the management of the firms should pay attention to the effectiveness of the investment they make during high uncertainty periods, which can strongly impact not only the firms themselves but also the whole economy because state ownership, even though in listed companies on the stock markets, plays a special role in maintaining the stability of Vietnam’s economy. In addition, understanding how Vietnamese firms adjust their dividend strategies in the context of EPU will help policy-makers and investors in other developing countries have further insight into the determinants of corporate dividend decisions and the possible consequences of firm dividend adjustments facing uncertainty in economic policy.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by [University of Economics Ho Chi Minh City (UEH)], and [Ho Chi Minh City University of Law].

Appendix

Variable Definitions.

| Variable | Name | Source of Data |

| EPU | Economic policy uncertainty |

|

| Q | Tobin’s Q | Datastream |

| CF | Cash flows | |

| NWC | Net working capital | |

| RETE | Retained earnings | |

| LEV | Leverage | |

| CAPEX | Capital Expenditures | |

| LOSS | Negative net income after taxes | |

| ROA | Return on total assets | |

| SIZE | Natural logarithm of market capitalization | |

| ASSG | Assets’ growth | |

| BIG4 | Audited by 1 of the 4 biggest auditing companies | |

| ANA | Analyst coverage | |

| RET | Average monthly stock return | |

| VRET | Volatility of monthly stock return | |

| VCF | Volatility of cash flow (3-year rolling) | |

| VROA | Volatility of ROA (3-year rolling) | |

| GDPG | Economic growth rate (real term) | |

| CPIG | Inflation rate | |

| GOV | Presence of government as a shareholder (Dummy variable) | |

| GOV1 | Government holdings more than 50% (Dummy variable) | |

| GOV2 | State ownership (%) | |

| INO | Institutional ownership (%) | |

| BLO | Blockholdings (%) |