Abstract

Drawing on Chinese listed-firm data (2005–2022), this article examines the impact of productivity and state ownership on outward foreign direct investment (OFDI). Productivity robustly facilitates OFDI, whereas state ownership impedes it. The productivity effect is strongest in high-sunk-cost industries, eastern and central regions, and subsidiary-level investment; the ownership barrier persists across high- and low-sunk-cost sectors, the eastern region, and subsidiary ventures. Productivity partly offsets the ownership disadvantage, and firms’ international experience amplifies the productivity effect. Notably, central state-owned enterprises reverse the negative ownership effect. Overall, China’s OFDI is driven predominantly by productivity-induced market-seeking, offering new micro-level evidence on its determinants.

Keywords

1. Introduction

Due to its diverse ownership structure, China’s outward foreign direct investment (OFDI) is a distinct and growing force in international cooperation and global market integration. Yet this diversity obscures the fact that Chinese firms are increasingly productive, making it unclear why China’s OFDI is expanding (Buckley et al., 2007; Dai et al., 2022; Morck et al., 2008; Wang et al., 2012), specifically whether its growth stems from the spontaneous market behavior by the private sector or from non-economic objectives tied to state ownership. This ambiguity has fueled considerable controversy and tighter scrutiny of China’s OFDI (Li & Meyer, 2023; Ufimtseva, 2020). If driven by market forces, China’s OFDI would grow sustainably; however, if state ownership dominates, it may display irregular trends, concentrating rapidly in specific regions, periods, and industries. For example, state-owned enterprises (SOEs) actively acquired undervalued overseas assets after 2008. Such investment growth appears contingent upon macro-policies (Du & Zhang, 2018; Zhao & Lee, 2021) and would likely diminish substantially should policy priorities shift toward domestic or alternative concerns, as evidenced by SOEs’ leading role in Belt and Road investments after 2014.

Figure A1 illustrates annual trends in mean productivity, SOE proportion, and OFDI stock among listed firms over the past two decades. China’s OFDI growth appears to track variations in firm productivity and state ownership, and these two factors exhibit opposing trends as firms go global. As firm productivity has risen, the proportion of SOEs has declined annually, suggesting a gradual weakening of state control over listed firms. This phenomenon warrants attention to the effects of firm productivity and state ownership on China’s OFDI.

The existing literature on China’s OFDI offers two distinct perspectives. One centers on firm productivity and the economic logic of OFDI firms. International business theory considers the productivity of multinational enterprises (MNEs) as an important source of competitive advantage (Buckley & Casson, 1976; Hymer, 1960). Firm heterogeneity theory argues that high-productivity firms can substitute OFDI for exports in serving foreign markets (Feng et al., 2022; Helpman et al., 2004; Tian, 2024). They provide the important theoretical foundations for further studies. High-productivity firms typically possess greater absorptive capacity, enabling them to bear higher sunk costs and risks associated with OFDI, overcome outsider disadvantages, and navigate cultural and institutional challenges. Sanfilippo (2015) conducted the first comparative analysis of MNEs’ productivity between emerging markets represented by BRICS countries and high-income countries and Europe, finding that the productivity levels in the former is lower than in the latter. This indicates that MNEs from emerging markets face a competitive disadvantage in terms of productivity. Shao and Shang (2016), Kong et al. (2021) and Tian (2024) find that firm productivity exerts a positive effect on Chinese firms’ propensity to engage in OFDI. Moreover, ex post learning and investment experience have been identified as potential avenues for enhancing firm productivity (Hejazi et al., 2021; Zhao et al., 2023). Zhou (2021) reports that OFDI firms’ productivity exceeds that of non-OFDI firms pre-investment only in labor-intensive industries, while post-investment productivity gains occur only in capital-intensive industries, suggesting that the impact of productivity may differ depending on firm learning and experience accumulation.

The other focuses on firm ownership and the non-economic motives of China’s OFDI from the institutional perspective. China’s institutional arrangements bias resources and support toward SOEs (Buckley et al., 2007; Morck et al., 2008). These arrangements not only directly facilitate their global expansion through financial subsidies and streamlined administrative reviews but also help them overcome outsider disadvantages (Cull et al., 2015; Li & Luo, 2023; Luo et al., 2010). This may render SOEs insensitive to risks associated with OFDI (Duanmu, 2012). Zhang et al. (2022) find that private firms initiate fewer overseas investment projects than SOEs. Zhao and Lee (2021) report that the Belt and Road Initiative favors central SOEs’ OFDI but not that of private firms or local SOEs. These studies suggest that SOEs are encouraged to pursue OFDI and act as leaders and practitioners in response to national strategies and industrial policies (Nie, 2022; Zhao & Chu, 2021). However, resource dependence theory holds that the dominant position conferred by institutional arrangements alters SOEs’ attitude toward internationalization (Vernon, 1979). SOEs may curtail OFDI motivation due to the dependence on domestic resource endowments or pursue OFDI actively to escape government influence and control. Cui and Jiang (2016) and Huang et al. (2017) report a weakening effect of state ownership on Chinese firms’ internationalization. Rodrigues and Dieleman (2018) and Choudhury and Khanna (2014) find that government-linked enterprises and SOEs in Brazil and India reduce their dependence on the home country through internationalization.

These studies offer pertinent insights into the rationale underpinning China’s OFDI, highlighting productivity and ownership as important perspectives. Chinese firms may be driven either by market-seeking motives as productivity improves or by institutional imperatives as state ownership increases. However, the literature offers little insight into which impact is more dominant. It is of theoretical and practical significance to distinguish the dominant factors at the firm level in order to assess whether China’s OFDI is experiencing sustainable and strong growth. To the best of our knowledge, only Sun et al. (2021) examine both productivity and state ownership in the Chinese context. They find that firm productivity positively correlates with the probability of OFDI in non-Belt and Road countries, yet not in Belt and Road countries; conversely, SOEs’ productivity impedes OFDI in Belt and Road countries while facilitating it elsewhere. The authors posit that government–firm relations may compensate for productivity disadvantages, enabling SOEs to respond to national strategies. This suggests China’s OFDI is not driven by a single factor, motivating our continued exploration of its micro-level determinants.

The purpose of this article is to ascertain whether productivity or state ownership constitutes the primary driver of firms’ OFDI decisions. To the best of our knowledge, this paper is among the first English-language studies to empirically examine both firm productivity and state ownership in China’s OFDI. It offers three marginal contributions. First, this article advances an integrative framework by elucidating how firm productivity and state ownership interact to shape OFDI decisions. While existing literature largely treats these factors in isolation—focusing either on productivity-driven market-seeking or on state-led strategic imperatives—this study demonstrates that productivity partially compensates for the ownership disadvantage, that international experience amplifies the productivity effect, and critically, that central SOEs can overturn the negative ownership effect. These findings reveal that China’s OFDI is shaped by configurations of firm-level capabilities and institutional embeddedness rather than singular drivers, offering a more nuanced understanding of how economic and institutional logics coexist, interact, and even substitute for one another. This speaks directly to the ongoing debate regarding whether China’s OFDI is predominantly market-seeking or strategically motivated, providing fresh grounds for dialog between foreign and Chinese scholars.

Second, this article sharpens the empirical precision of recent firm-level OFDI research through a substantially more comprehensive data set and methodological approach. Unlike Sun et al. (2021), whose analysis is constrained by the China Industrial Enterprise Database and limited to basic firm-level controls (age, capital scale, employment) plus district, industry, and year fixed effects, this article exploits listed-firm panel data spanning 2005–2022 across 18 non-financial industries. This enables not merely richer control variables also but rigorous causal identification and granular heterogeneity analysis that prior micro-level studies of China’s OFDI have been unable to achieve.

Third, this article clearly unpacks contextual contingencies and mechanisms. By dissecting heterogeneous effects across sunk-cost intensities, regional contexts (eastern, central, western), and investment modes (subsidiary versus non-subsidiary), the analysis identifies where and when productivity and ownership matter most-findings that challenge the blanket assumption that state ownership uniformly promotes OFDI. The exploration of complementary effects between core factors, refined state ownership typologies, and the moderating role of international experience yields distinctive evidence that not only illuminates the sustainability of China’s OFDI growth trajectory but also furnishes actionable insights for firms optimizing internationalization strategies.

2. Theoretical Analysis

2.1. Firm Productivity and OFDI

Drawing on international business theory and firm heterogeneity theory, firms engaged in OFDI are distinguished by high productivity (Helpman et al., 2004; Hymer, 1960). Derived from technology, capital, and management inputs, productivity enables firms to enter overseas markets and sustain their market position. Its key role in OFDI decisions is reflected in three aspects. First, high-productivity firms possess stronger markup power, which is conducive to competitive advantage. Yue and Li (2023) find that Chinese manufacturing firms’ productivity significantly increases markups. Hwang (2022) notes that the influx of foreign firms reduces average markups, indicating that entrants require sufficient markup space to survive competition. Therefore, productivity can help firms to compete in host countries and gain market position by increasing their markup advantage.

Second, high-productivity firms typically exhibit stronger technological advantages and higher management levels. Zhu et al. (2021) and Bloom et al. (2013), respectively, find that firm productivity is positively correlated with technology input and management efficiency in emerging markets. These intangible assets have a very low transfer costs within MNEs, which are beneficial for improving the multinational business performance after OFDI (Bilicka & Scur, 2024). Moreover, high-productivity firms can pay more attention to environmental, social, and governance (ESG) commitments (Du et al., 2024; Li et al., 2024; Sun & Saat, 2023). Bai et al. (2022) and Zhang and Liu (2022) argue that ESG helps firms with financial constraints in the domestic credit market, which can meet the capital needs of OFDI. ESG can also be helpful to overcome outsider disadvantages under today’s conditions where ESG commitments are widely endorsed by most countries. Therefore, productivity can increase firms’ motivation for OFDI by improving technical and management advantages and ESG levels.

Third, high-productivity firms are inclined to enter overseas markets earlier. Chawla (2019) and Qi et al. (2021) find that the initial time of OFDI is positively related to firm productivity in the emerging markets. Firms that go global earlier would gather more investment experience, including coping with foreign investment scrutiny and adapting to cultural and institutional differences. Such valuable experiences constitute an important information source for OFDI decision-making, especially in the context that the scarcity of international investment experience remains a notable feature since China’s OFDI started late. Firms can quickly collect information and reduce collection costs from past experiences. These experiences are also believed to contribute not only to improving firms’ learning ability but also to enhancing the ability to perceive changes in overseas markets (Gaur et al., 2014; Hejazi et al., 2021; Zhao et al., 2023). Therefore, productivity can encourage firms’ OFDI by involving internationalization earlier.

Based on the above analysis, this article puts forward H1.

H1: Firm productivity is conducive to OFDI.

2.2. State Ownership and OFDI

The role of state ownership in OFDI decisions is manifested in two distinct aspects. On the one side, state ownership can facilitate access to capital and information, reducing the barriers posed by financial constraints and lack of information. First, state ownership plays a positive role in the information provision, loan guarantee, and reputation endorsement, helping firms obtain loans and relieve financial constraints. Cull et al. (2015) find that the firms associated with the government have a lower degree of financial constraints. Bai et al. (2021) report that China’s credit resources were biased toward SOEs. Moreover, state-owned shares represent the most direct link between firms and the government. They can respond to macro-policies and bear the policy burden through internal proposals and voting, which has led to more government subsidies for SOEs (Buckley et al., 2007; Liao et al., 2023; Lin et al., 1998). Thus, the available funds are added and the capital requirements of OFDI are alleviated. Second, state ownership can transfer valuable investment experience, reducing the information asymmetry in OFDI decision-making. With the expansion of China’s OFDI, SOEs were the primary actors in formulating overseas plans, with private firms following suit (Morck et al., 2008; Zhao & Chu, 2021). It implies that state-owned capital gains investment experience at an earlier stage. Their sensitive comprehension of the global market trends and their familiarity with the host country’s system serve as crucial information sources for decision-making when state-owned capital assumes the principal shareholder. Therefore, state ownership can have a positive impact on firms’ OFDI by improving the availability of financing and enriching decision information.

On the other side, the institutional benefits of state ownership can work in the opposite direction, which could diminish firms’ motivation for OFDI in the long run. According to resource dependence theory, the internationalization of SOEs depends on the comparison of domestic and foreign resources (Vernon, 1979). SOEs may pursue OFDI to escape government influence and control, or conversely, their reliance on domestic resources may diminish their OFDI motivation. Rodrigues and Dieleman (2018) and Choudhury and Khanna (2014) find that government-linked enterprises in Brazil and SOEs in India reduce their dependence on the home country through internationalization. But Cui and Jiang (2016) and Huang et al. (2017) report the weakening effect of state ownership on firm internationalization in China. What reason could account for this discrepancy? In addition to the policy incentives, subsidies, and reputation that SOEs enjoy at home, we cannot ignore the appeal of China as the world’s largest emerging market. Especially in the context of international political instability and the anti-globalization trend, China maintains an active economic policy agenda. In 2020, China demonstrated a heightened focus on the domestic market, fully opened its financial and capital markets, and proposed to build a “dual circulation” development pattern. Thus, China’s SOEs tend to focus on the domestic market and reduce OFDI, which could enhance operational stability. Moreover, they are subject to the rigorous scrutiny and the host countries’ misunderstanding due to state ownership (Drysdale, 2011; Li & Meyer, 2023). This situation further reduces their OFDI motivation.

Based on the above analysis, this article proposes H2a and H2b.

H2a: State ownership encourages a firm’s OFDI.

H2b: State ownership discourages a firm’s OFDI.

3. Method

3.1. Model and Variables

For examining the impacts of firm productivity and state ownership on OFDI, this article sets Equation 1.

Where i and t denote firm and year. The coefficients β1 and β2 are the main parameters in this article. λk and θt represent industry and year fixed effects. εit is the random disturbance term.

lnOFDIit represents the logarithm of OFDI stock by firm i in year t. China Stock Market Accounting Research (CSMAR) OFDI data show the control rights of listed companies over foreign subsidiaries, associated companies, and joint ventures. Accordingly, this article calculates the annual OFDI stock of firms. This measure is theoretically preferable to flow for capturing the structural dimensions of internationalization. First, stock data capture the persistence and cumulative nature of internationalization, embodying firms’ established competitive positions abroad through persistent and irreversible commitments (Wacker, 2016), while the flow data would treat each annual investment as an isolated event (Wang et al., 2012). Second, given the high fixed costs and potential strategic orientation characteristic of China’s OFDI (Du & Zhang, 2018; Zhao & Lee, 2021), it better represents the depth of international embeddedness and the scale of overseas deployment. 1

TFP and SOE denote firm productivity and a state ownership dummy. The OP method (Olley & Pakes, 1996) and LP method (Levinsohn & Petrin, 2003) are widely employed to measure firm-level total factor productivity. Following Xiao and Xue (2019) and Hu et al. (2020), this article uses the LP method to estimate firm productivity (TFP) as the core variable and employs the OP method construct as an alternative measure (TFP_OP) for robustness test.

The top 10 shareholder documents from CSMAR provide top-10 shareholders’ name, nature, and shareholding ratio. This enables the calculation of the proportion of state-owned shares (soe), defined as the combined holdings of state shareholders and state-owned legal persons. A state-ownership dummy (SOE) is determined if soe exceeds 30%. This threshold navigates between zero and 50% thresholds employed elsewhere (Li & Meyer, 2023; Zhang et al., 2022), capturing de facto control often exercised well below the majority stakes. It further aligns with cross-jurisdictional regulatory practices, where 30% typically triggers mandatory takeover obligations (Habersack, 2018). For robustness, alternative thresholds—non-zero (SOE0), 40% (SOE4), and 50% (SOE5)—are used to ascertain the sensitivity of our findings to these definitional variations. Furthermore, firms related to state ownership are divided into two categories. Firms are regarded as central SOEs and the dummy Central is 1, when the shares of state shareholders exceed 30%. Firms are regarded as local SOEs and the dummy Local is 1, as the shares of state legal persons exceed 30%.

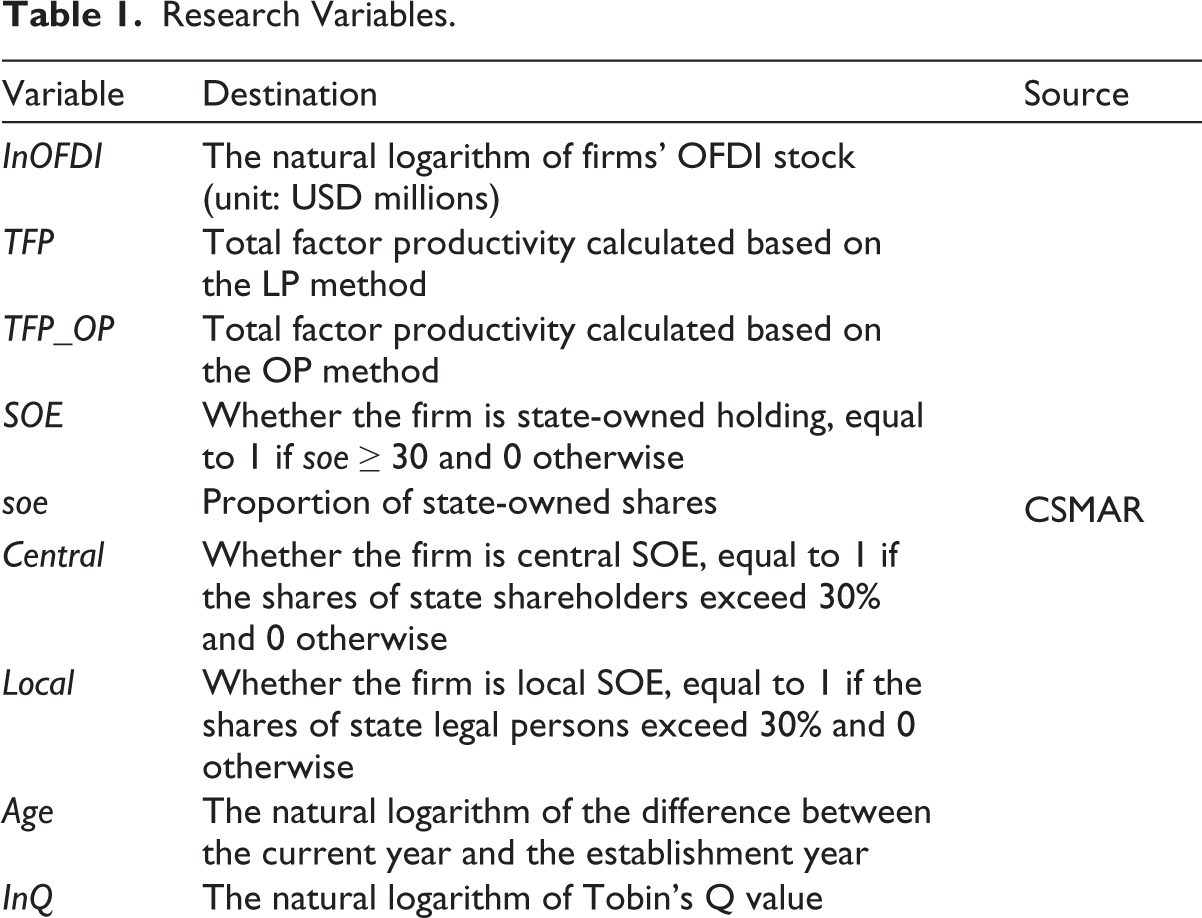

Controls are the control variables. Following prior studies (Cen & Dong, 2022; He et al., 2024), firms’ age, market value, capital intensity, leverage ratio, net profit growth rate, and tax burden level are taken as firm control variables. The initial year of OFDI is added to measure the attention to overseas business and the experience of overseas investment. Considering the potential impact of regional development differences, macroeconomic trends, and public health emergencies, this article includes provincial GDP, provincial level of infrastructure, the real effective exchange rate of the renminbi, the Belt and Road Initiative implementation variable and COVID-19 shock variable. The above variables are presented in Table 1.

Research Variables.

3.2. Data

Taking 2005–2022 as the observation window, this article constructs the research data set from three sources: CSMAR database, CEInet Statistics Database, and IMF International Financial Statistics (IFS). The OFDI stock data of listed firms is obtained from CSMAR OFDI data, which are subsequently merged with the shareholders’ and financial indicators data from CSMAR, regional GDP and infrastructure data from CEInet, and exchange rate data from IFS. The following companies are excluded for the accuracy and stability of the data: (a) ST, *ST, and PT companies; (b) companies in the financial industry; (c) companies whose key variables are missing; and (d) companies whose debt ratio is greater than 1.Finally, we obtain 20,540 valid observations of 2,452 non-financial listed companies from 2005 to 2022. 2 The continuous dependent and control variables are winsorized at 1% and 99% before data analysis.

3.3. Sample Overview

Descriptive statistics and correlation coefficients are reported in Tables A1 and A2. lnOFDI ranges from 0 to 18.69, indicating marked differences in investment scale across China’s OFDI firms. TFP (TFP_OP) spans from 3.10(4.68) to 6.29(10.03), suggesting significant productivity variation, while the standard deviation of SOE is 0.44, showing substantial variation in state-owned share proportions. First_year ranges from 1999 to 2022, implying sustained overseas investment activity over the past two decades. lnOFDI is significantly and positively correlated with TFP (0.198***) and SOE (0.049***), suggesting that productivity and state ownership may both exert a positive influence on OFDI. Conversely, First_year is negatively correlated with lnOFDI (−0.283***), indicating that earlier overseas investment is associated with greater current OFDI. These characteristics underpin our research.

4. Analysis and Results

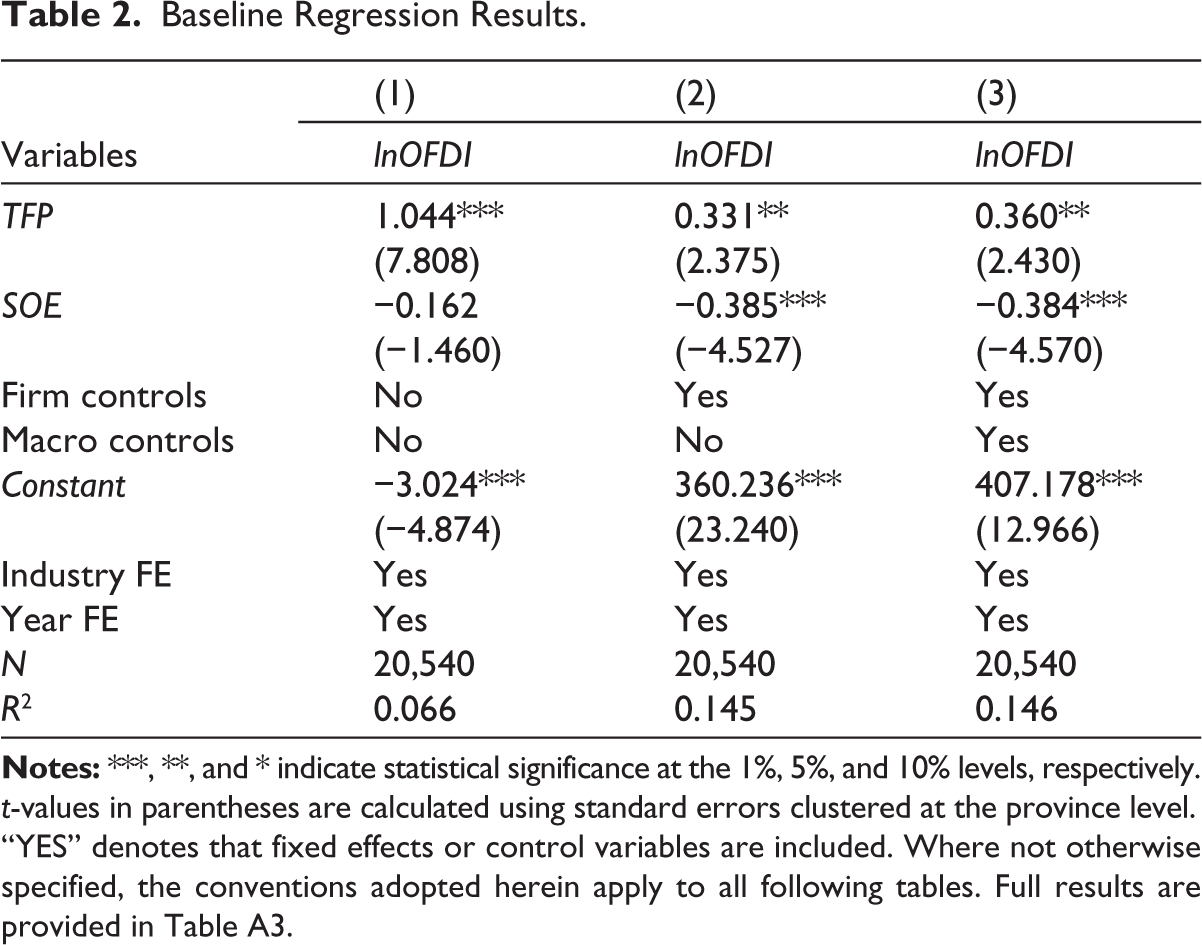

4.1. Baseline Regression Results

The impact of firm productivity and state ownership on China’s OFDI is evaluated using ordinary least squares (OLS), as presented in Table 2. Column 1 examines the relationship between firm productivity, state ownership, and OFDI with industry and year fixed effects. TFP is positive and significant at 1%, while SOE is negative and insignificant. Columns 2 and 3 introduce firm- and macro-level control variables, with the signs of TFP and SOE remaining consistent with Column 1. The coefficient of TFP is positive and significant at 5%, indicating that firm productivity plays an active role in the growth of OFDI scale. All else equal, OFDI scale increases by 15.69% when firm productivity increases by 10% of the mean (4.358). The coefficient of SOE is negative and significant at 1%, indicating that state ownership acts as a barrier. With other variables held constant, SOEs’ OFDI scale is lower than that of non-SOEs.

Baseline Regression Results.

4.2. Robustness Tests

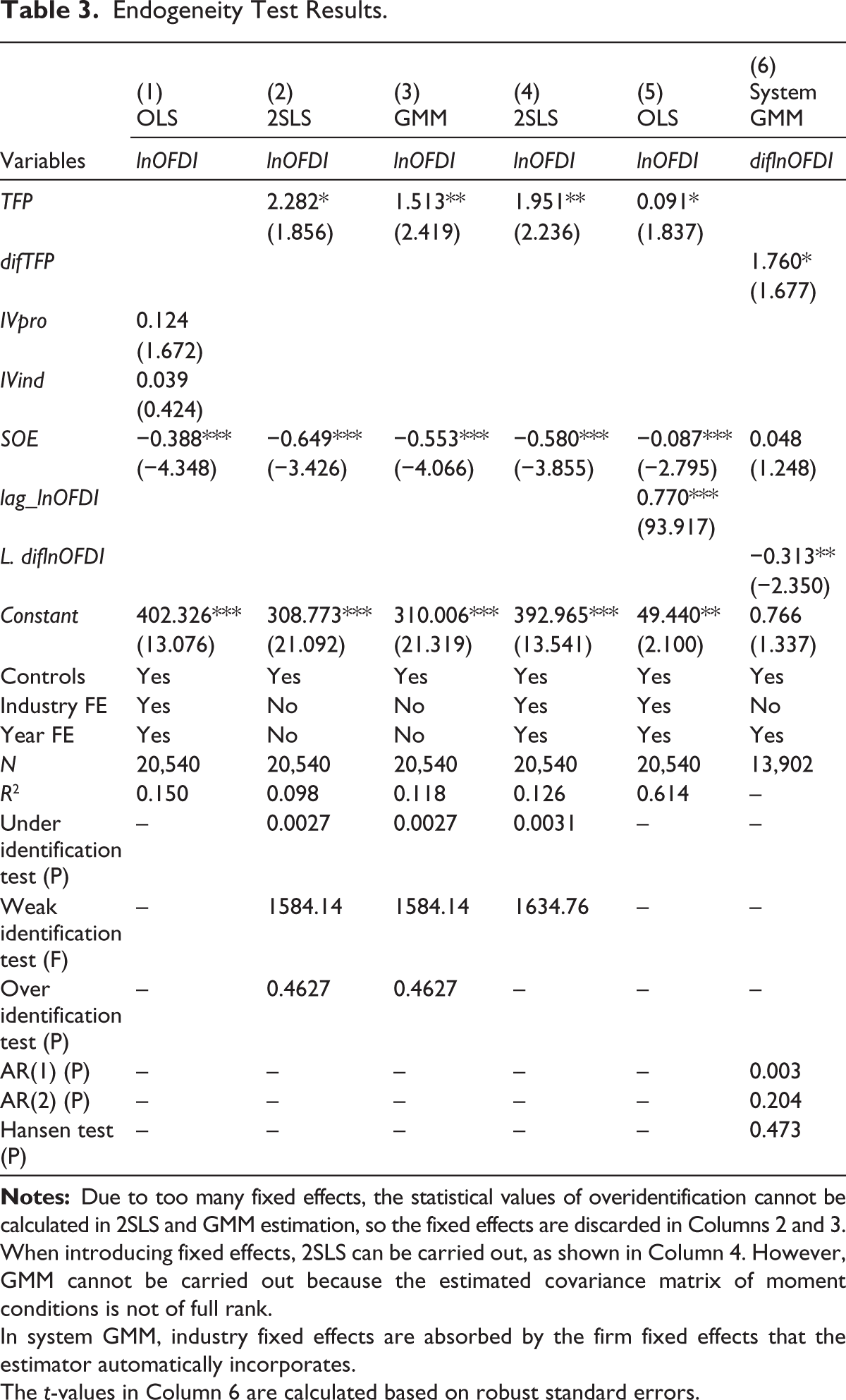

The baseline regressions may suffer from endogeneity and variable selection concerns. First, endogeneity arises from reverse causality. While high productivity drives OFDI, OFDI itself may enhance productivity through access to foreign technologies and resources (Peng et al., 2023), thereby biasing baseline estimates. In this regard, this article employs instrumental variable (IV) strategy and system generalized method of moments (GMM) estimation. First, IVs are constructed in cubes of the difference between the firm productivity and the sample mean of provinces and industries (Lewbel, 1997). These aggregate deviations satisfy the exclusion restriction as no individual firm can influence provincial or industry-wide averages. The cubic specification preserves directional productivity advantages and captures distribution skewness. Columns 1–4 of Table 3 present the test results. The coefficients of IVpro and IVind are statistically insignificant, indicating that the exogeneity requirement is satisfied. The relevant indicators confirm that both instruments pass the underidentification, weak identification, and overidentification tests. The coefficient of TFP remains positive and significant, indicating that the productivity continues to play a meaningful role in firms’ OFDI.

Endogeneity Test Results.

When introducing fixed effects, 2SLS can be carried out, as shown in Column 4. However, GMM cannot be carried out because the estimated covariance matrix of moment conditions is not of full rank.

In system GMM, industry fixed effects are absorbed by the firm fixed effects that the estimator automatically incorporates.

The t-values in Column 6 are calculated based on robust standard errors.

Second, system GMM addresses OFDI persistence and endogeneity from unobserved heterogeneity. Column 5 of Table 3 shows that the lagged dependent variable, lag_lnOFDI, is positive and highly significant, confirming the dynamic persistence of stock investment. Unit root tests indicate that both lnOFDI and TFP are non-stationary; their direct application in system GMM generates complex serial correlation and invalidates inference. We therefore apply first-differencing to lnOFDI and TFP to obtain diflnOFDI and difTFP, respectively. Diagnostic statistics are satisfactory: AR(1) p < .01, AR(2) p > .1 and Hansen p > .1, confirming instrument validity. Column 6 of Table 3 shows that dif TFP is positive and significant at 10%, indicating that productivity promotes OFDI even after accounting for serial correlation in investment stock.

While neither approach achieves perfect identification—province- and industry-level policy interventions may correlate with the instruments, and system GMM remains sensitive to instrument proliferation and lag structure misspecification—the convergence of results across both methods, together with satisfactory diagnostic statistics, suggests that residual endogeneity risks lie within acceptable bounds.

Second, this article re-estimates the impacts of core variables using alternative proxies and excluding the special samples, including: (a) replacing independent variables with TFP_OP and soe, one period lagged terms (lag_TFP and lag_SOE), three definitional variables of SOEs (SOE0, SOE4, SOE5); (b) replacing controls with Age2, ROA, First_lnOFDI, and REER; (c) adding the province fixed effect, (d) excluding the financial-crisis years (2005–2010) and the COVID-affected years (2020–2022). Tables A4 and A5 report these results in turn. The signs and significance of independent variables are similar to those presented in Table 2. The above results prove that the baseline results are robust. H1 and H2b are supported.

4.3. Heterogeneity Checks

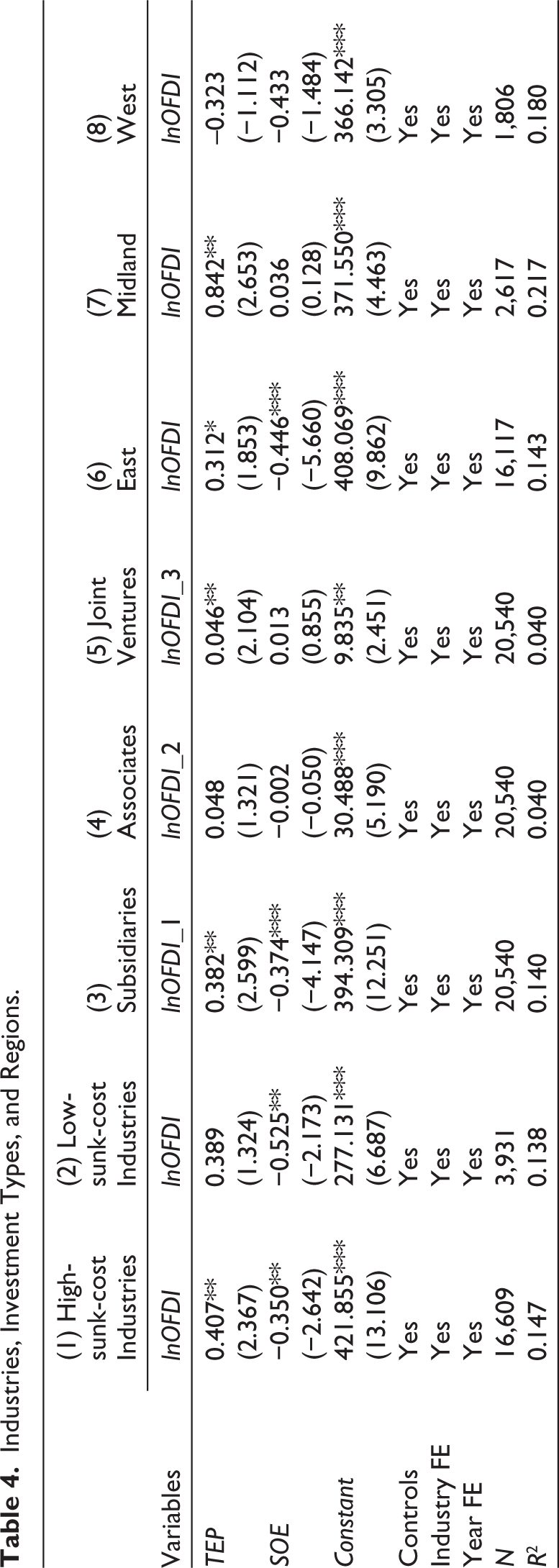

First, industry-level sunk costs shape OFDI risk and complexity (Cushman, 1985), conditioning firms’ propensity to internationalize. This article distinguishes firms’ industries into high-sunk-cost and low-sunk-cost groups. As reported in Columns 1 and 2 of Table 4, while state ownership deters OFDI irrespective of sunk-cost intensity, productivity exerts a markedly stronger effect among high-sunk-cost firms. For such firms, substantial irreversible commitments in plant, machinery, and specialist labor strategically oblige decisive productivity advantages prior to expansion, as erroneous entry carries prohibitive exit costs. Financially, capital market imperfections restrict high-sunk-cost firms to internal financing for these substantial outlays; consequently, only the most productive among them can generate sufficient retained earnings to fund international ventures without resorting to costly external capital (Dai et al., 2022). Conversely, low-sunk-cost sectors entail modest, reversible investments; trial entry is inexpensive, rendering productivity a less-stringent prerequisite.

Industries, Investment Types, and Regions.

Second, unlike associates or joint ventures, wholly owned subsidiaries afford firms maximum control yet impose the greatest managerial, strategic, and resource burdens. Using CSMAR disclosure, this article disaggregates OFDI into subsidiaries (lnOFDI_1), associates (lnOFDI_2), and joint ventures (lnOFDI_3). As revealed in Columns 3–5 of Table 4, both productivity and state ownership exert their strongest influence on subsidiary investment. Establishing a subsidiary demands irreversible commitments, complex risk-bearing, and superior capabilities; hence, only high-productivity firms possess the requisite technological, managerial, and ESG advantages. Conversely, state shareholders, exhibit positive coefficients for associates and joint ventures, indicating a preference for shared-risk vehicles.

Third, China’s staggered regional development—east first, then central, followed by west and northeast—has yielded marked disparities in resources, market openness, and state-capital density. This article divides firms’ provincial locations into the east, middle, and west regions. As shown in Columns 6-8 of Table 4, productivity significantly promotes OFDI among eastern and central firms, while state ownership deters it only in the east. These patterns mirror the sequencing of reform: early-mover eastern provinces enjoy greater policy autonomy, deeper markets, and denser agglomerations of both productive firms and SOEs. Consequently, productivity advantages and state-imposed constraints are most salient where marketization is most advanced.

4.4. Further Discussion

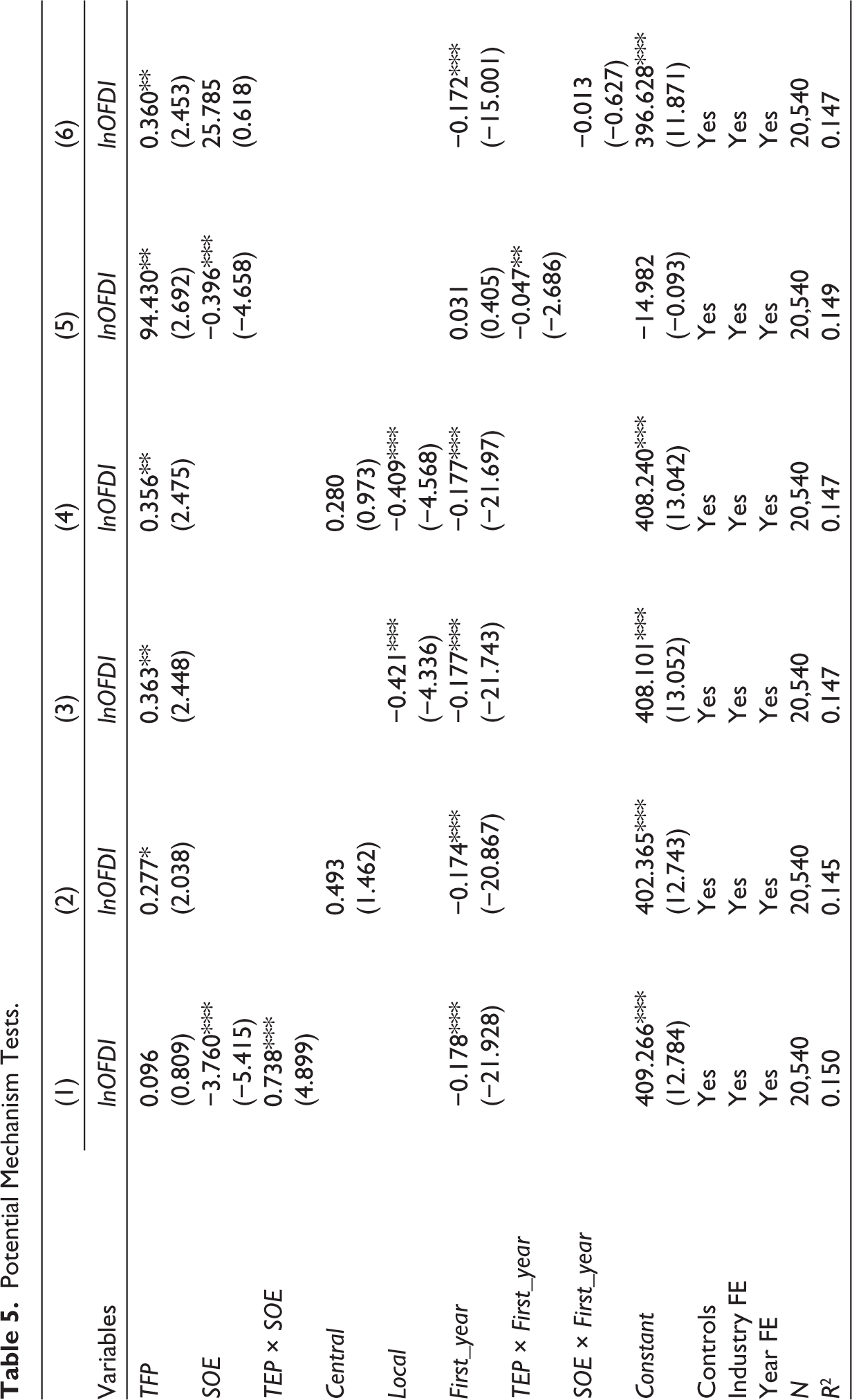

This article further discusses the potential mechanisms. First, the possible complementary relationship between the two core determinants is examined. Column 1 of Table 5 shows that the interaction TEP × SOE is positive and highly significant, confirming that higher productivity can mitigate the negative effect of state ownership in a compensatory manner. Specifically, more efficient SOEs possess stronger operational competencies and resource orchestration skills, which enable them to better address host-country regulatory scrutiny and to cultivate strategic momentum for sustained internationalization. These productive advantages thus serve as a countervailing force against the dependence on domestic resources and markets typically associated with state ownership. Yet SOE remains strongly negative. Evaluated at the mean of TFP (4.358), a 10% productivity increase merely raises the marginal effect of SOE from −3.76 to −3.44, leaving a sizeable net impediment to OFDI. This limited compensatory effect suggests that while productivity enhances SOEs’ capacity to manage external legitimacy challenges and cultivate strategic commitment to internationalization, such firms nevertheless continue to rely upon domestic resource advantages and exhibit a marked preference for home-market opportunities over overseas expansion.

Potential Mechanism Tests.

Second, this article disaggregates state ownership by ultimate controller. Columns 2-4 of Table 5 show that Central is positive but insignificant, whereas Local is negative and significant at 1%. This divergence reflects fundamental differences in governance structures and institutional resources. Central SOEs operate under a principal–agent framework wherein national sectors serve as direct principals, endowing them with strategic mandates that decouple internationalization from productivity considerations (Nie, 2022; Zhao & Lee, 2021). Entrusted with securing energy supplies, acquiring advanced technology, and projecting geopolitical influence, they enjoy privileged access to policy support, diplomatic backing, and preferential financing. This attenuates the negative association between state ownership and OFDI. By contrast, local SOEs are embedded in a decentralized governance architecture, wherein local governments and state-owned legal persons exercise control. These multiple principals generate fragmented oversight and competing objectives oriented toward regional industrial development and employment maintenance (Luo et al., 2017). Lacking the strategic mandates and diplomatic resources available to their central counterparts, local SOEs confront weaker institutional incentives for overseas expansion. The resulting governance inefficiencies and principal–agent conflicts manifest in a statistically significant negative effect upon their OFDI propensity.

Third, it is worth caring whether the international investment experience positively moderates the impacts of productivity and state ownership. Column 5 of Table 5 presents that TEP × First_year is negative and significant at 5%, implying that the productivity effect on OFDI strengthens as firms accumulate earlier international experience. This dynamic pattern indicates that productivity and experiential learning function as complementary assets in the internationalization process: firms with prior overseas operations are better positioned to leverage their efficiency advantages when expanding further, suggesting a path-dependent reinforcement of the productivity–OFDI relationship. Column (6) shows no such effect for SOE × First_year, suggesting that state ownership continues to impede OFDI regardless of experiential learning, underscoring its enduring constraint on internationalization. This asymmetry implies that the negative effect of state ownership may be structural—stemming from entrenched reliance upon domestic institutional support, preferential access to home-market resources, and deeply embedded operational routines oriented toward local rather than international markets—and thus cannot be readily ameliorated through accumulated internationalization knowledge. Such findings lend further support to our argument that productivity-driven market-seeking motives and ownership-based non-economic motives warrant integrated theoretical examination, as these determinants operate through distinct channels.

5. Conclusions

This article examines whether productivity or state ownership drives Chinese firms’ OFDI. Drawing on matched data for 2,452 non-financial listed OFDI firms from 2005 to 2022, we find that productivity and state ownership exert opposing effects: firm productivity positively influences OFDI, while state ownership discourages it. These baseline findings prove robust to extensive testing, with effects varying across industries, investment types, and regional locations. Further analysis reveals a complementary relationship between these factors: productivity partially offsets state ownership’s negative effect, suggesting that resource dependence constrains SOEs’ internationalization. Notably, central SOEs exhibit a positive OFDI effect, as they shoulder greater non-economic obligations and respond more readily to national strategy than local SOEs. Additionally, international investment experience moderates the productivity impact, with earlier overseas entrants benefiting more strongly from productivity gains.

These findings yield several implications. First, no single factor can adequately assess the sustainability of China’s OFDI. Overemphasis on state ownership obscures Chinese firms’ rising productivity, as they accumulate knowledge and improve technology—enhancing efficiency and narrowing the gap with high-income-country counterparts. Conversely, state ownership has not positively influenced China’s OFDI as anticipated (Buckley etal., 2007; Morck et al., 2008), but has reduced firms’ willingness to invest abroad over the past two decades. Given rising productivity and a declining SOE proportion, China’s OFDI should achieve sustainable growth driven by firms’ natural demand for international markets.

Second, balancing state ownership against internationalization is imperative. State-owned capital typically prioritizes domestic markets and may obstruct expansion; firms should weigh long-term strategic consequences before accepting such injections. Non-SOE managers should pursue OFDI alongside domestic productivity reforms and technological investment to signal credible commercial intent to host-country regulators. Central SOEs may leverage institutional advantages to facilitate OFDI, while local SOEs should build productivity to offset resource dependence; both should prioritize productivity upgrading before large-scale expansion, particularly in regulated sectors with acute political scrutiny. For all firms, early international experience is critical, enhancing the ability to anticipate market shifts and navigate host-country regulations. More importantly, continued internationalization can catalyze further efficiency gains through learning-by-doing and technology sourcing.

Third, policymakers should focus on the long-term benefits of productivity-enhancing reforms and foster a stable investment environment for sustainable OFDI. While ownership restructuring offers a quicker yet politically contested route, productivity-enhancing reforms strengthen international competitive advantages and yield commercially viable investment resilient to regulatory scrutiny. Meanwhile, host-country scrutiny has increasingly prioritized political over economic considerations, impeding China’s OFDI and raising asset security concerns. Policymakers should negotiate investment scrutiny and protection with partner governments, codifying these through substantive bilateral investment treaties. This dual approach—domestic productivity upgrading coupled with international institutional safeguards—ensures OFDI is both competitively grounded and politically secure.

Several avenues merit future research. First, unlisted private enterprises—often more agile and less politically visible—represent a promising avenue for extension. Future studies might exploit survey or administrative data to examine whether the productivity–OFDI nexus differs systematically between listed and unlisted firms, and whether technology-intensive unlisted firms exhibit distinct locational or entry-mode preferences. Second, the bidirectional dynamics between OFDI and productivity upgrading warrant investigation through dynamic panel estimation models or natural experiments arising from policy shocks, thereby clarifying whether internationalization serves as a conduit for sustained competitive advantage. Third, host-country institutional variables—such as investment screening intensity or bilateral investment treaty provisions—should be integrated to examine how host-country political economy factors moderate the relationship between Chinese firm-level reforms and OFDI success.

Supplemental Material

Supplemental material for this article is available online.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.