Abstract

This study examines how the United States–Iran military escalation of February 28, 2026, was transmitted across 17 global equity markets. Using event study, panel regression with Driscoll–Kraay standard errors, Fama–MacBeth estimation, and generalized autoregressive conditional heteroskedasticity (GARCH) modeling, we document significant negative cumulative abnormal returns of approximately −2.5%. A negative war effect (β = −0.00356, p = .044) is confirmed under panel and cross-market frameworks, transmitted primarily through global risk sentiment. Interaction analysis reveals an oil channel sign reversal during the crisis. Extended-sample GARCH shows significant volatility elevation in 14 of 17 markets, consistent with a persistent shift in volatility conditions.

Keywords

1. Introduction

The impact of geopolitical shocks on equity markets has attracted considerable academic attention, particularly following a series of high-profile conflicts and diplomatic crises since 2020. The escalation of armed hostilities between the United States and Iran on February 28, 2026, represents a recent and economically salient geopolitical shock, coinciding with a sharp rise in the CBOE Volatility Index (VIX) and the Geopolitical Risk (GPR) index of Caldara and Iacoviello (2022). This episode provides a timely opportunity to examine how such shocks propagate across global equity markets, with particular attention to transmission channels and the differential responses of developed and emerging economies.

The financial consequences of geopolitical shocks may materialize through several mechanisms. First, heightened uncertainty elevates the global equity risk premium, depressing valuations even in markets with no direct conflict exposure (Pástor & Veronesi, 2013; Smales, 2021). Second, oil price movements associated with Middle East tensions generate heterogeneous effects across oil-importing and oil-exporting economies, as documented by Kilian and Park (2009). Third, safe-haven flows toward gold and the US dollar redistribute financial conditions across markets (Beirne & Renzhi, 2025; Pandey & Kumari, 2021). Whether these channels operate symmetrically during and outside crisis periods, however, remains an open question.

Despite a growing empirical literature, three gaps persist. First, most existing studies rely on a single empirical method, which limits the ability to simultaneously capture short-run price dynamics and more persistent transmission effects. Second, the stability of transmission channels across regimes, specifically whether the sensitivity of equity returns to oil, gold, and VIX changes during geopolitical crises, has not been formally tested in a panel setting. Finally, the February 2026 United States–Iran escalation has not yet been systematically examined. This article addresses these gaps through a multi-method framework applied to 17 global stock markets.

The empirical strategy combines four approaches. First, an event study documents short-run price reactions and tests for cross-market heterogeneity. Second, panel regression with DKSE identifies persistent transmission channels robust to cross-sectional dependence. Third, Fama and MacBeth’s (1973) two-stage estimation allows for fully heterogeneous slope coefficients across markets, directly addressing concerns about the aggregate panel specification. Finally, generalized autoregressive conditional heteroskedasticity (GARCH) models assess whether the shock is associated with changes in conditional volatility dynamics. The extended sample (to May 20, 2026) provides robust evidence on the persistence of volatility effects.

The main findings are as follows. The event study documents cumulative average abnormal returns (CAAR) of −2.50% over the [−3,+3] window and −2.44% over [−5,+5], both significant at the 5% level. The largest market-level declines are recorded in DFMGI UAE (−12.1%), Bovespa (−8.8%), and BSE SENSEX (−6.5%). Panel regression confirms a negative war effect (β = −0.00356, p = .044), with VIX as the dominant channel (β = −0.032, p < .001). The Fama–MacBeth (FM) estimation yields a virtually identical estimate (−0.003557, p < .001), confirming that the panel result is not an artifact of pooling. Interaction estimates show that the oil channel reverses sign during the war period (total effect: −0.097), and a joint Wald test rejects the stability of transmission channels (χ²(4) = 84.68, p < .001). GARCH analysis finds no significant war effect on S&P500 conditional volatility in the acute window, but extended-sample estimation across all 17 markets reveals significant volatility elevation in 14 cases.

The remainder of the article is organized as follows. Section2 reviews the relevant literature and states the hypotheses. Section3 describes the data and empirical methodology. Section4 presents the results. Section5 discusses the findings and their implications. Section6 concludes.

2. Literature Review and Hypotheses

2.1. Geopolitical Risk and Equity Market Vulnerability

A substantial body of research links geopolitical uncertainty to declines in investment, output, and equity valuations. Caldara and Iacoviello (2022) construct a text-based GPR index and show that elevated geopolitical tensions are systematically associated with lower equity returns and higher risk premia across a large panel of countries. Bloom (2009) provides a broader theoretical foundation, demonstrating that uncertainty shocks reduce investment and output through a real-options mechanism and transmit rapidly through financial markets. Baker et al. (2016) extend this framework to economic policy uncertainty, documenting negative stock price responses to policy ambiguity. Pástor and Veronesi (2013) formalize the theoretical link between political uncertainty and equity risk premium, showing that higher ambiguity about government policy raises discount rates and depresses valuations.

Emerging economies are particularly vulnerable to these dynamics. Their financial systems tend to feature shallower capital markets, greater reliance on external financing, weaker institutional frameworks, and higher sensitivity to global risk sentiment (Bouras et al., 2019; NguyenHuu & Ørsal, 2024). These structural characteristics amplify the pass-through of external shocks to domestic asset prices. Balcilar et al. (2018) document asymmetric responses in BRICS equity markets, with the direction and magnitude of reactions varying with energy-export status. Boubaker et al. (2022) discovered that equity market reactions to the Ukraine conflict depended on trade linkages and commodity exposure, while Zaremba et al. (2022) showed that investor overreaction to geopolitical news may generate mean-reverting patterns over longer horizons.

2.2. Transmission Channels

The empirical literature identifies three main channels through which geopolitical shocks reach equity markets. The risk sentiment channel operates through the VIX as a proxy for global risk aversion. Bekaert et al. (2013) show that uncertainty shocks raise the risk premium globally, affecting markets regardless of their direct exposure to the underlying event. Smales (2021) confirms a negative relationship between GPR and equity returns through this channel. Beirne and Renzhi (2025) extend these findings to capital flow volatility, showing that GPR amplifies cross-border flows, particularly in emerging markets.

The oil price channel is especially relevant for Middle East conflicts. Kilian and Park (2009) decompose oil price shocks into supply- and demand-driven components and show that supply disruptions generate significantly negative equity returns, while demand-driven price increases may be associated with positive returns. This decomposition has important implications: a military escalation in the Persian Gulf region is likely to be perceived as a supply-side event, generating a distinct pattern of equity market responses relative to demand-driven oil price movements. Mei et al. (2020) confirm that GPR increases oil futures volatility. Thenmozhi and Maurya (2021) document heterogeneous transmission of oil volatility across equity markets, with effects varying by commodity exposure. The safe-haven channel involves capital reallocation toward gold and the US dollar during episodes of elevated uncertainty. Baur and McDermott (2010) show that gold serves as a safe haven for major equity markets, while Pandey and Kumari (2021) document safe-haven flows during the COVID-19 period.

Whether these transmission channels are stable across regimes is, however, rarely examined directly. Most studies estimate unconditional average effects, implicitly treating the oil–equity and VIX–equity sensitivities as fixed parameters. This assumption is difficult to defend for geopolitical events: a Middle East escalation shifts the interpretation of an oil price increase from a demand signal to a supply disruption, which should alter the sign of the oil–return relationship, not merely its magnitude. The present study tests this directly.

2.3. Event Study Evidence on Geopolitical Shocks

Event study methods, developed by Brown and Warner (1985) and MacKinlay (1997), are the standard tools for identifying discrete event effects on asset prices. Corrado (2011) reviews these methods and confirms that parametric approaches are appropriate for short-window analysis of daily returns. The empirical record on geopolitical shocks is largely consistent: negative CARs are documented across a range of events and samples. Pandey and Kumari (2021) find significant negative CAAR across both developed and emerging markets in response to the COVID-19 pandemic. Boubaker et al. (2022) and Boungou and Yatié (2022) report negative abnormal returns following the Russia–Ukraine conflict, with magnitude varying by energy exposure and geographic proximity. Kumari et al. (2022) extend these findings to border disputes in emerging Asia. A recurring observation in this literature is that emerging equity markets tend to exhibit more gradual price adjustment following shocks, consistent with informational frictions and lower market efficiency (Fama, 1970). A notable gap is that most event studies document the magnitude of abnormal returns without testing whether the underlying transmission channels (oil, VIX, and safe-haven flows) behave differently during the event window than outside it. Without this test, it is unclear whether the aggregate war effect reflects a genuine average or a conflation of opposing channel-level dynamics.

2.4. Volatility Dynamics

Modeling of conditional volatility using ARCH-GARCH frameworks (Bollerslev, 1986; Engle, 1982) consistently finds that equity market volatility is highly persistent, with geopolitical shocks entering primarily through the level of unconditional variance rather than through short-run ARCH effects. Salisu et al. (2022) apply a GARCH-MIDAS approach to emerging markets and show that GPR contributes to higher long-run volatility components. Boubaker et al. (2022) find that price declines following the Ukraine conflict were not accompanied by structural changes in volatility dynamics. The GJR-GARCH model of Glosten et al. (1993) allows for asymmetric volatility responses to positive and negative shocks, a feature that may be relevant for geopolitical events, which tend to generate predominantly adverse return outcomes.

2.5. Research Gaps and Hypotheses

Three gaps in the existing literature motivate this study. First, most papers employ a single method, making it difficult to jointly characterize short-run and persistent effects. Second, the stability of transmission channels across crisis and non-crisis regimes has not been directly tested in the context of geopolitical shocks. Third, the February 2026 United States–Iran escalation has not been examined. These gaps lead to the following hypotheses:

H1: Geopolitical shocks are associated with significant negative CARs, with emerging markets experiencing larger declines than developed markets. H2: Geopolitical shocks exert a significant negative effect on equity returns through macro-financial transmission channels, with global risk sentiment (VIX) as the dominant and most robust pathway. Transmission channel intensities shift materially during the crisis period. H3: Geopolitical shocks do not significantly alter short-run conditional volatility dynamics in the acute phase (which remain persistence-driven); however, extended-sample analysis reveals a broad-based elevation in the unconditional variance level across markets.

3. Data and Methodology

3.1. Data

The analysis uses daily closing prices for 17 global equity market indices, obtained from Yahoo Finance via the quantmod package for R. The main sample spans January 2024 to March 20, 2026, yielding 695 trading days and an unbalanced panel of 11,815 market-day observations (n = 17, T = 695). The sample end point is set at the acute phase of the shock, providing 18 post-event trading days. An extended sample for robustness analysis extends to May 20, 2026 (747 trading days, 70 post-event observations) and is used exclusively for GARCH robustness analysis. Restricting the main sample to the shorter window avoids confounding from subsequent policy developments.

The 17 markets span four regions. North America is represented by the S&P500, NASDAQ, and TSX (all developed markets). Europe is represented by the FTSE100, DAX, CAC40, and AEX (all developed markets). Asia-Pacific is represented by the Nikkei225, Hang Seng (developed markets), KOSPI, TWII, SSE Composite, STI, and BSE SENSEX (emerging markets). Latin America is represented by Bovespa and IPC Mexico (emerging markets), while the Middle East by DFMGI UAE (an emerging/frontier market). Following the MSCI market classification framework, the sample includes nine developed and eight emerging or frontier markets, enabling comparison across development classifications.

The geopolitical event is the United States–Iran military escalation on February 28, 2026, treated as an exogenous shock. The event received extensive international media coverage and coincided with a sharp increase in the GPR index (Caldara & Iacoviello, 2022) and the VIX. A binary WAR dummy equals 1 for all trading days on or after February 28, 2026, and 0 otherwise. Four macro-financial variables capture potential transmission channels: Brent crude oil daily log-returns (Oil), gold price daily log-returns (Gold), CBOE VIX daily log-returns, and US Dollar Index (DXY) daily log-returns. All variables are expressed as daily logarithmic differences. Stationarity is confirmed by augmented Dickey–Fuller tests, which reject the unit-root null at the 1% level for all series.

3.2. Event Study

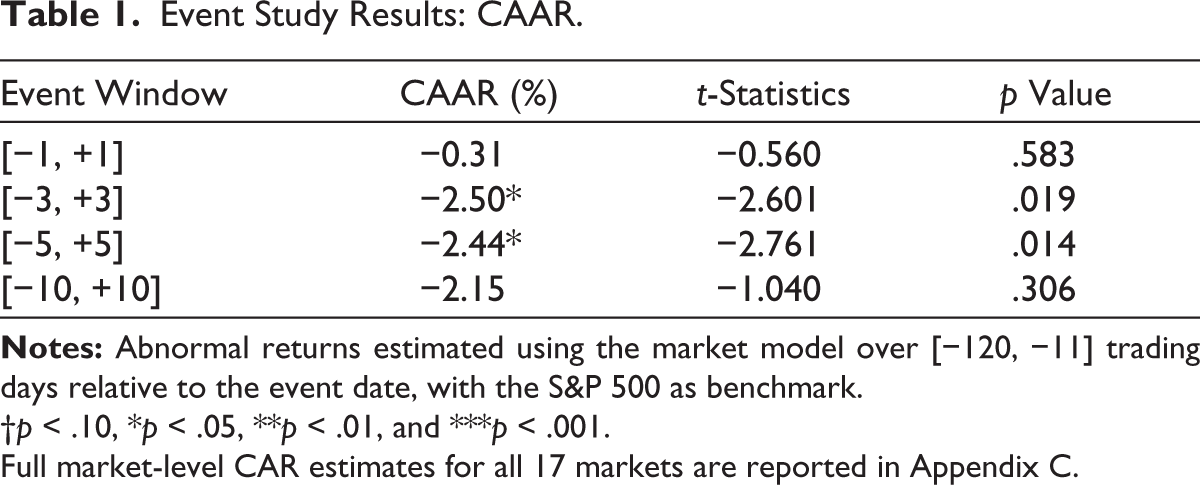

To test H1, we apply the market model event study framework of Fama et al. (1969), Brown and Warner (1985), and MacKinlay (1997). Expected returns are estimated over the window [−120, −11] trading days relative to the event date using the S&P500 as the global benchmark: Rᵢₜ = αᵢ + βᵢRᵀₜ + εᵢₜ. Abnormal returns are computed as ARᵢₜ = Rᵢₜ − (αᵢ + βᵢRᵀₜ) and cumulated over four event windows: [−1,+1], [−3,+3], [−5,+5], and [−10,+10]. Cross-sectional CAAR and t-statistics are computed following the parametric approach of Corrado (2011). Market-level CARs for all 17 markets across the [−1, +1], [−3, +3], and [−5, +5] windows are reported in Appendix C.

3.3. Panel Regression, Fama–MacBeth Estimation, and Transmission Channels

To test H2, we estimate the following panel model:

where μᵢ captures unobserved market-specific fixed effects. A Hausman (1978) specification test and an F-test for individual effects (p = .062) support the fixed-effects (FE) specification; FE absorb meaningful cross-sectional heterogeneity in average returns (range: −0.00044 to +0.00152). VIX is included as a transmission channel rather than a pure control variable; the WAR coefficient, therefore, captures the geopolitical shock effect conditional on contemporaneous movements in global risk sentiment.

Three diagnostic tests motivate the use of Driscoll–Kraay standard errors (DKSEs): the Pesaran (2021) CD test rejects cross-sectional independence (z = 49.26, p < .001); the Breusch–Pagan (BP) test indicates heteroskedasticity (BP = 170.03, p < .001); and the Wooldridge test detects serial correlation (χ² = 2,249.3, p < .001). DKSEs are robust to all three issues simultaneously and remain valid under spatial and temporal dependence (Driscoll & Kraay, 1998). The presence of strong cross-sectional dependence also renders conventional pooled standard errors invalid, as market returns share common factors (Forbes & Rigobon, 2002). The maximum lag is set to five trading days, corresponding to one calendar week.

Since the macro-financial regressors (WAR, Oil, Gold, VIX, and USD) vary over time but not across markets, slope coefficients are identical across pooled OLS, FE, and random-effects (RE) specifications; only standard errors differ. Compared to structural VAR or network-based spillover approaches, the panel-DKSE framework preserves daily frequency identification while jointly accounting for cross-sectional dependence. These properties are particularly important for the short event window studied here. To address directly the concern that a specification with time-varying but cross-sectionally constant regressors reduces to an aggregate time-series model, we complement the panel evidence with Fama and MacBeth’s (1973) two-stage estimation. In Stage 1, Equation 1 is estimated separately for each of the 17 markets by OLS, yielding a market-specific vector (βᵢ₁,…,βᵢ₅). In Stage 2, the cross-sectional mean and standard deviation of each coefficient vector are computed, and significance is assessed using the cross-market standard error. This approach allows fully heterogeneous slopes while producing a formal aggregate estimate directly comparable to the panel result. A short-window robustness check replaces WAR with WAR_short (equal to 1 for the first five post-event trading days, February 28 to March 6, 2026).

To test whether transmission channels shift during the crisis period (H2), we augment the baseline model with interaction terms between WAR and each macro-financial variable: WAR × Oil, WAR × Gold, WAR × VIX, and WAR × USD. The interaction coefficients capture changes in the marginal effect of each channel during the war period relative to the pre-event baseline. A joint Wald test, using the DKSE covariance matrix, assesses whether the interaction terms are collectively significant.

3.4. GARCH Volatility Analysis

To test H3, we estimate a sGARCH(1,1) model for S&P500 returns with the WAR dummy in the variance equation: σₜ² = ω + αεₜ₋₁² + βσₜ₋₁² + γWARₜ. The S&P500 is used as a proxy for the global volatility process, consistent with its role as the primary reference index in international financial markets. We additionally estimate a GJR-GARCH(1,1) to allow for asymmetric volatility responses to positive and negative innovations. Main-sample estimates (18 post-event observations) assess the acute-phase volatility response. Robustness is provided by extended-sample estimation (70 post-event observations) applied individually to all 17 markets using the same specification. This allows the assessment of whether the volatility response is broad-based and whether it differs between developed and emerging markets. Model adequacy is evaluated using ARCH LM tests, the sign bias test, and the Nyblom (1989) parameter stability test. All models are estimated by quasi-maximum likelihood using the rugarch package in R.

4. Empirical Results

4.1. Descriptive Statistics

Stock market returns average approximately zero over the full sample, with a standard deviation of 0.96%, negative skewness (−0.27), and excess kurtosis of 9.33, consistent with typical daily equity return distributions. VIX returns display the highest variability (standard deviation: 8.0%), reflecting their sensitivity to sudden changes in risk sentiment. The positive correlation between WAR and VIX (0.108) and between WAR and Oil (0.266) confirms that the event was associated with a rise in global risk and energy prices. Variance inflation factors are below 1.21 for all variables, and augmented Dickey–Fuller tests reject non-stationarity at the 1% level throughout. These diagnostics support the validity of the regression framework.

4.2. Event Study Results

Table1 presents the CAAR for four event windows. The absence of a significant response in the [−1,+1] window (−0.31%, p = .583) indicates that markets did not fully incorporate the shock on the day of the event, a pattern consistent with gradual information diffusion in some of the markets in the sample. Significant negative CAARs of −2.50% (p = .019) and −2.44% (p = .014) are recorded in the [−3,+3] and [−5,+5] windows, respectively. These magnitudes are comparable to those reported for the Russia–Ukraine conflict (Boubaker et al., 2022; Boungou & Yatié, 2022). The 10-day CAAR of −2.15% (p = .306) is not statistically significant, which is partly attributable to the limited number of post-event observations available at this horizon.

Event Study Results: CAAR.

†p < .10, *p < .05, **p < .01, and ***p < .001.

Full market-level CAR estimates for all 17 markets are reported in Appendix C.

Market-level CARs over the [−5,+5] window reveal substantial cross-sectional variation, consistent with H1. The largest declines are recorded in markets with direct geographic or energy-sector exposure to the conflict: DFMGI UAE (−12.12%), Bovespa (−8.81%), BSE SENSEX (−6.49%), IPC Mexico (−3.08%), and FTSE100 (−0.66%). Several developed markets record near-zero or modest declines, including NASDAQ (+0.63%), AEX (+0.85%), and Hang Seng (+0.51%). This pattern is consistent with the reallocation of capital from markets with conflict-zone exposure toward relatively insulated developed markets. Twelve of the 17 markets record negative CARs (the S&P 500 is zero by construction, as it serves as the benchmark), confirming the broad direction of impact.

4.3. Panel Regression and Fama–MacBeth Results

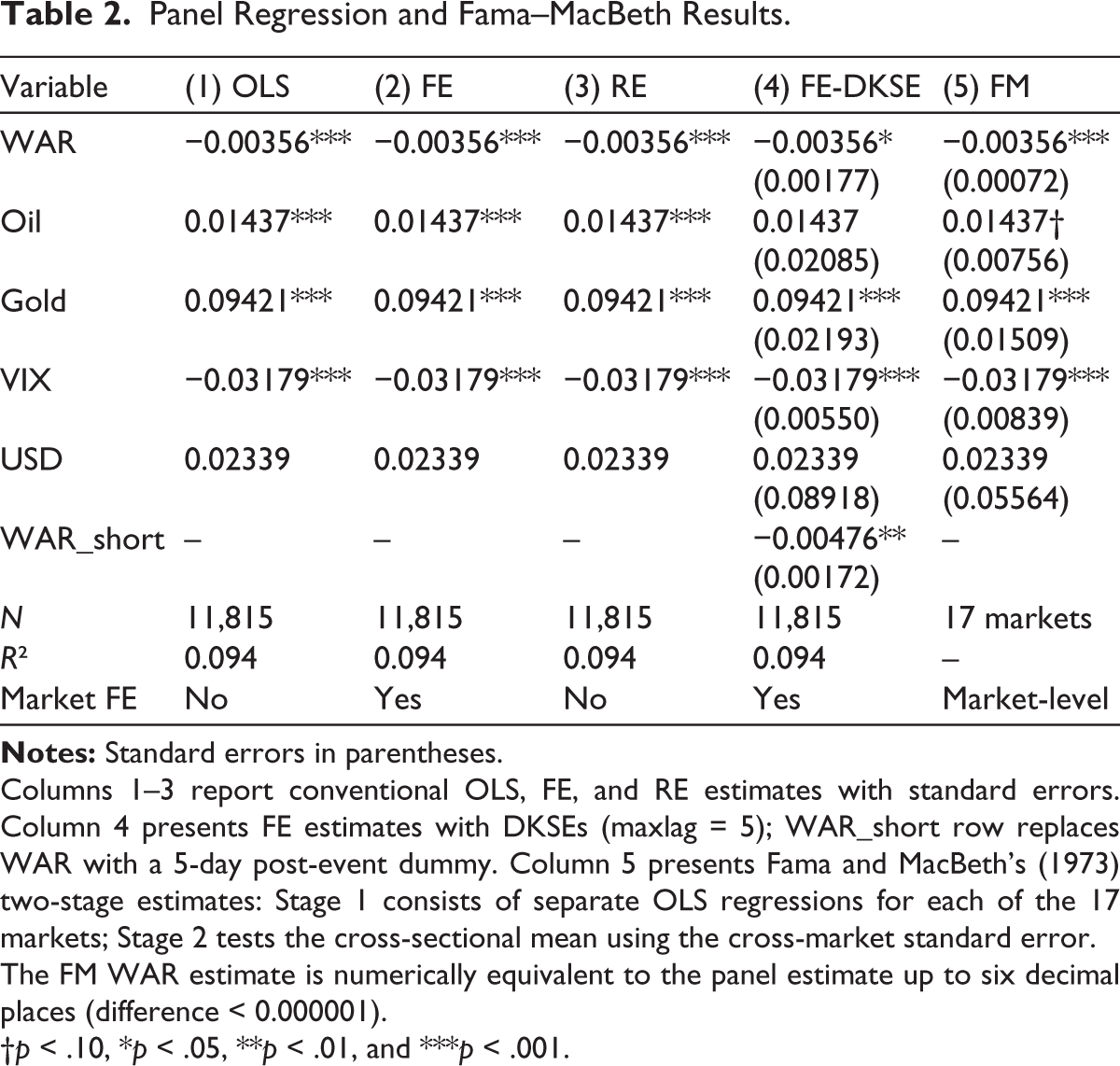

Table2 presents results across five specifications. As noted in Section 3.3, the slope coefficients are numerically identical in Columns 1–3 because the regressors have no cross-sectional variation; however, the standard errors differ. The DKSE specification in Column 4 accounts for the strong cross-sectional dependence identified by the Pesaran CD test (z = 49.26, p < .001) and is the preferred baseline.

Panel Regression and Fama–MacBeth Results.

Columns 1–3 report conventional OLS, FE, and RE estimates with standard errors. Column 4 presents FE estimates with DKSEs (maxlag = 5); WAR_short row replaces WAR with a 5-day post-event dummy. Column 5 presents Fama and MacBeth’s (1973) two-stage estimates: Stage 1 consists of separate OLS regressions for each of the 17 markets; Stage 2 tests the cross-sectional mean using the cross-market standard error.

The FM WAR estimate is numerically equivalent to the panel estimate up to six decimal places (difference < 0.000001).

†p < .10, *p < .05, **p < .01, and ***p < .001.

The WAR coefficient is −0.00356 and significant at the 5% level under DKSE (p = .044), corresponding to a daily return decline of approximately 0.36% after controlling for macro-financial channels. The WAR_short coefficient is larger in absolute value (−0.00476, p = .006), indicating a stronger immediate effect that attenuates over the post-event window, consistent with the mean-reverting pattern in the event study. The Fama–MacBeth estimate in Column 5 is −0.003557 (p < .001), virtually identical to the panel result while exhibiting stronger statistical significance. The FM standard error (0.00072) reflects the cross-market dispersion of individual coefficients, all of which point in the same negative direction (16 of 17). Among developed markets, the mean FM coefficient is −0.003456 (p < .001); among emerging markets, it is −0.003671 (p = .035). The consistency across both panel and FM frameworks confirms that the pooling assumption does not introduce bias.

VIX is the dominant and most robust channel (β = −0.032, p < .001 under DKSE and FM). This pattern accords with theoretical predictions that geopolitical uncertainty transmits to equity markets primarily through the risk premium (Bekaert et al., 2013; Pástor & Veronesi, 2013). Oil returns become insignificant under DKSE (p = .491), which we interpret as evidence of compositional heterogeneity: positive oil-return effects in exporting economies offset negative effects in importing economies, yielding an insignificant aggregate coefficient. Gold retains a positive and significant association (β = +0.094, p < .001), reflecting the terms-of-trade improvement in gold-producing economies when gold prices rise (Baur & McDermott, 2010).

4.4. Transmission Channel Interaction Analysis

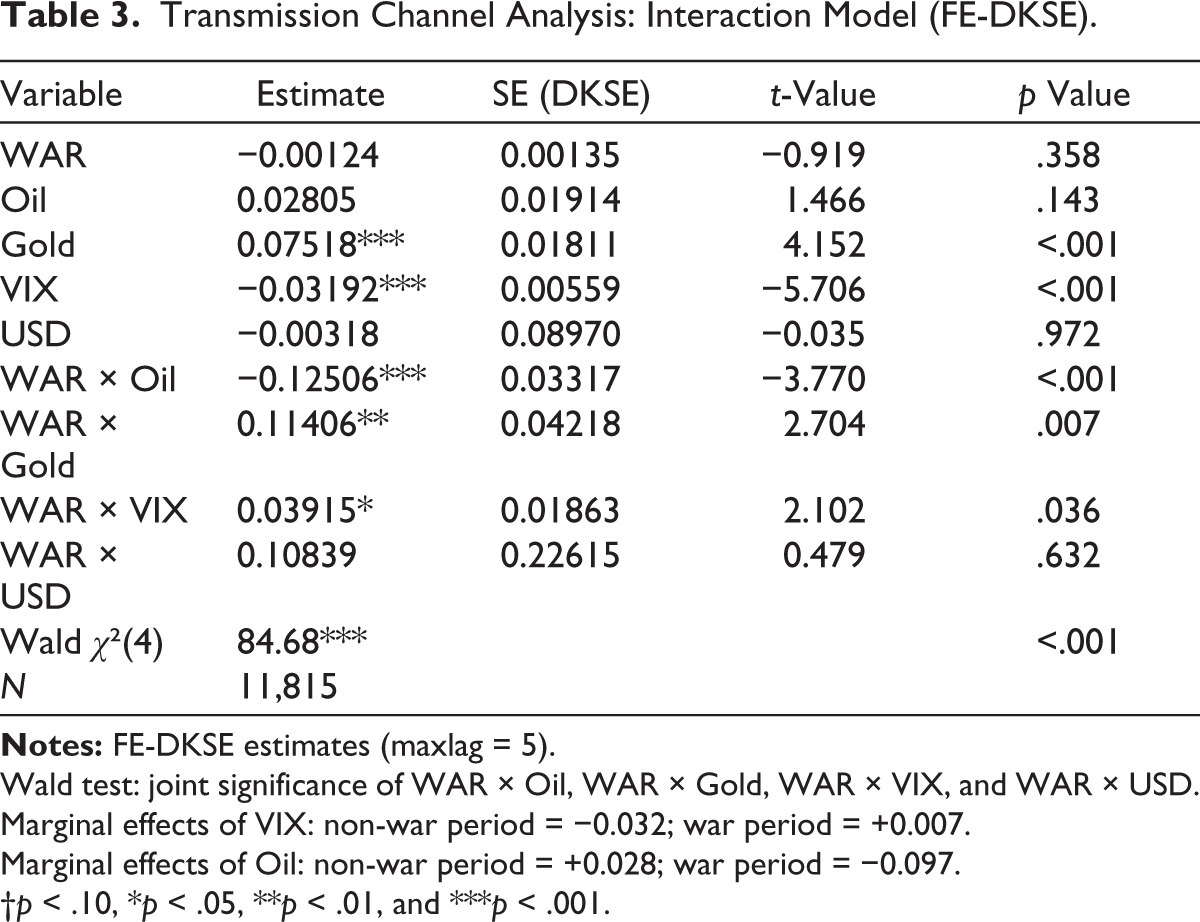

Table3 presents the interaction model results. The joint Wald test strongly rejects the null hypothesis of stable transmission channels (χ²(4) = 84.68, p < .001), confirming that the relationship between macro-financial variables and equity returns changes significantly during the war period.

Transmission Channel Analysis: Interaction Model (FE-DKSE).

Wald test: joint significance of WAR × Oil, WAR × Gold, WAR × VIX, and WAR × USD.

Marginal effects of VIX: non-war period = −0.032; war period = +0.007.

Marginal effects of Oil: non-war period = +0.028; war period = −0.097.

†p < .10, *p < .05, **p < .01, and ***p < .001.

Two-channel shifts carry material economic significance. First, the WAR × Oil coefficient is −0.125 (p < .001), implying that the total effect of oil returns on equity returns during the war period is +0.028−0.125 = −0.097. This reversal from mildly positive to strongly negative is consistent with the supply-shock interpretation of Kilian and Park (2009): a Middle East military escalation is likely perceived as a supply disruption, in which higher oil prices signal increased production costs and a deteriorating macroeconomic outlook, rather than stronger demand. The result underscores that the aggregate oil coefficient, which is statistically insignificant in the baseline, obscures a large and economically meaningful crisis-period effect. Second, the WAR × VIX coefficient is +0.039 (p = .036), implying that the negative sensitivity of equity returns to VIX movements attenuates during the war period (total effect: −0.032 + 0.039 = +0.007). This attenuation may reflect partial anticipatory pricing of GPR before the observed spike in measured uncertainty, implying that the contemporaneous comovement between VIX movements and equity returns becomes weaker during the event window.

4.5. GARCH Volatility Results

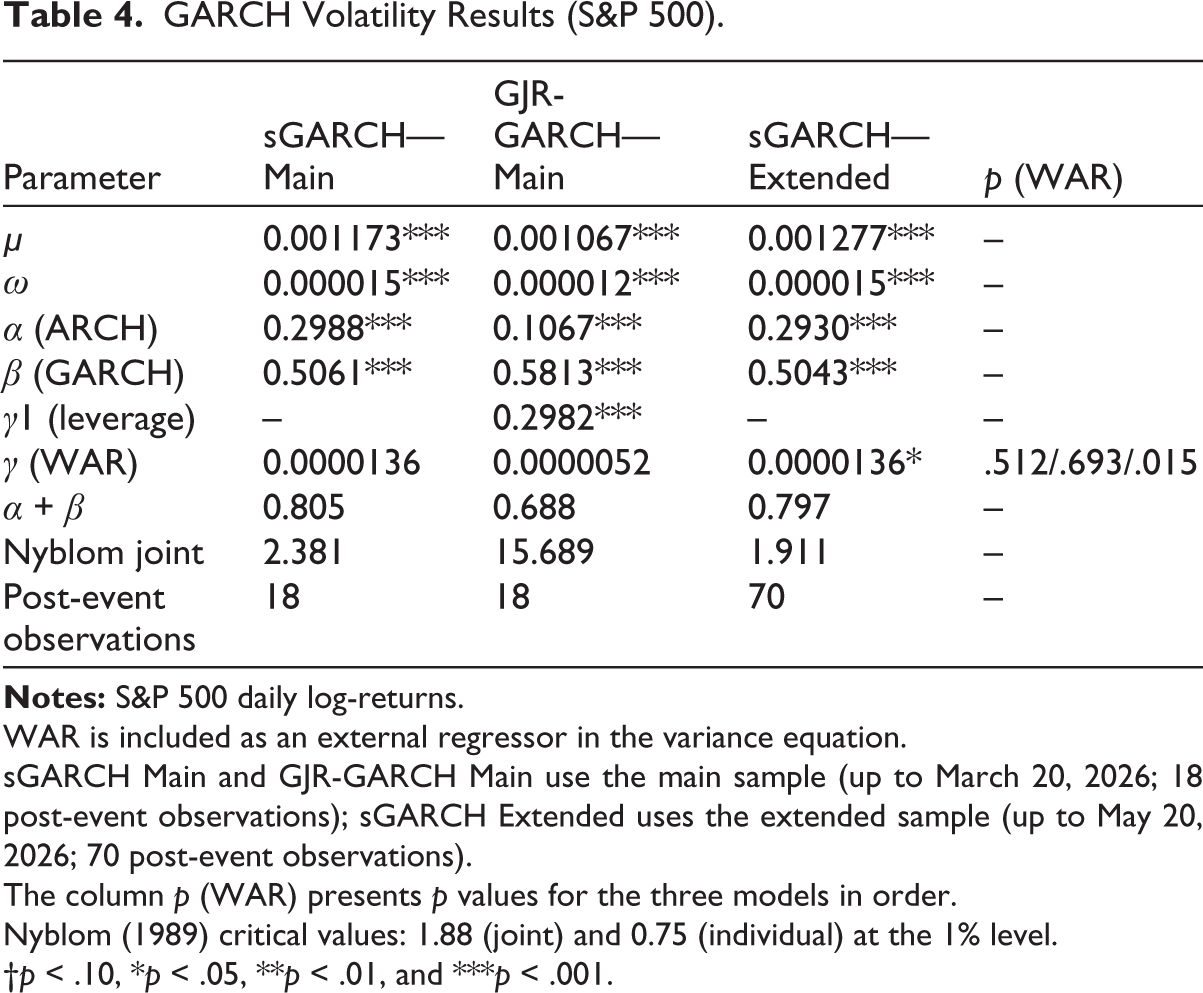

Table4 presents GARCH estimation results for the S&P500. In the main sample sGARCH(1,1), the ARCH and GARCH parameters are α = 0.299 and β = 0.506, respectively, yielding a persistence sum α + β = 0.805. The WAR coefficient in the variance equation is positive but statistically insignificant (γ = 0.000014, p = .512). These results are consistent with H3: in the acute-phase window, conditional volatility dynamics are dominated by inherent persistence rather than the geopolitical shock itself. ARCH LM tests confirm no remaining ARCH effects (all p > .12), and the sign bias test is not significant (p = .377), indicating adequate model specification.

GARCH Volatility Results (S&P500).

WAR is included as an external regressor in the variance equation.

sGARCH Main and GJR-GARCH Main use the main sample (up to March 20, 2026; 18 post-event observations); sGARCH Extended uses the extended sample (up to May 20, 2026; 70 post-event observations).

The column p (WAR) presents p values for the three models in order.

Nyblom (1989) critical values: 1.88 (joint) and 0.75 (individual) at the 1% level.

†p < .10, *p < .05, **p < .01, and ***p < .001.

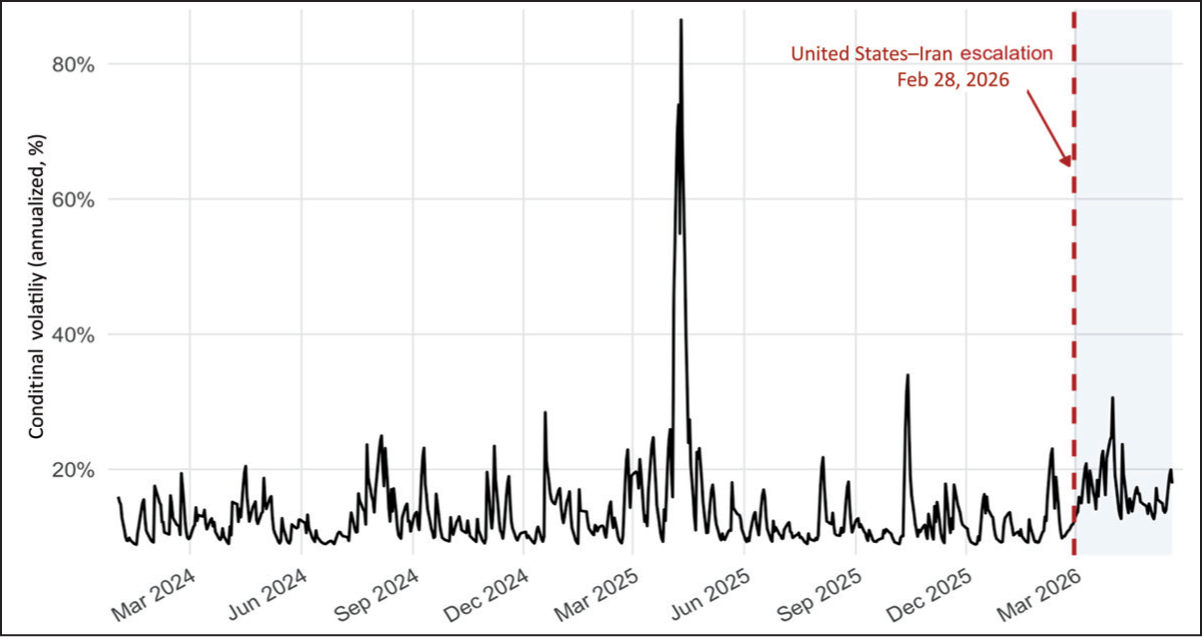

The GJR-GARCH(1,1) confirms significant asymmetric volatility dynamics: the leverage parameter γ1 = 0.298 (p < .001) indicates that negative return innovations generate disproportionately larger volatility increases, a feature directly relevant to adverse geopolitical shocks. The Nyblom (1989) stability test reports a joint statistic of 2.381, exceeding the 1% critical value of 1.88, driven primarily by the variance constant ω (individual statistics: 0.944 > 0.75). This instability is consistent with a shift in the unconditional variance level following the shock, rather than instability in the ARCH or GARCH dynamics themselves. Extending the estimation sample to May 20, 2026 (70 post-event observations), the Nyblom joint statistic falls to 1.911, still above the 1% critical value but closer to the boundary, consistent with transient instability driven by the acute shock. Split-sample analysis confirms that the S&P500 unconditional variance is approximately 1.32 times higher in the post-event period. A Chow test applied to S&P 500 squared returns at the event date yields F = 0.096 (p = .908), confirming no discrete structural break in variance at the event date. The Nyblom instability is therefore more consistent with a gradual shift in the unconditional variance level than with an abrupt regime change, supporting the use of the WAR dummy approach rather than a full regime-switching specification. In the extended-sample model, the WAR coefficient in the variance equation is statistically significant (γ = 0.0000136, p = .015), confirming a detectable volatility effect when sufficient post-event observations are available. Figure 1 plots the estimated conditional volatility over the full extended sample.

The vertical dashed line marks the United States–Iran escalation (February 28, 2026); the shaded area denotes the post-event window.

The April–May 2025 spike reflects a separate macroeconomic episode unrelated to the geopolitical event.

Individual GARCH estimation across all 17 markets using the extended sample yields significant WAR coefficients in 14 of 17 markets (developed markets: 7 of 9; emerging markets: 7 of 8), with detailed results reported in Appendix B. The breadth of this finding indicates that the volatility effect is not confined to the US market or to the markets with direct conflict exposure but reflects a systemic shift in global volatility conditions following the geopolitical shock.

5. Discussion

5.1. Geopolitical Shocks as Return Compressors, Not Volatility Regime Changers

Taken together, the four methods point to a consistent picture. Geopolitical shocks of the type studied here operate primarily through equity valuation compression rather than through fundamental changes in conditional volatility dynamics. The negative abnormal returns, the persistent war effect in the panel and FM specifications, and the stronger immediate effect in the short window all point in this direction. The acute-phase GARCH evidence is consistent with prior findings for other geopolitical episodes (Boubaker et al., 2022; Salisu et al., 2022): volatility remains persistence-driven, and the shock does not appear to generate a distinct short-run volatility regime in the immediate aftermath. Over the extended sample, however, a detectable increase in unconditional variance emerges, suggesting that the shock does affect the equilibrium level of volatility even if it does not alter the short-run dynamics.

This two-phase pattern has implications for how the financial consequences of GPR should be characterized. The standard narrative that GPR primarily elevates uncertainty and, therefore, volatility is at best incomplete for the type of discrete, bounded conflict examined in this study. The primary near-term cost appears to be a compression of equity valuations, with mean-reversion beginning within 2–3 weeks. From a development finance perspective, even a temporary compression in emerging market valuations can increase the cost of equity capital during the period of adjustment, with potential downstream effects on investment and long-run growth convergence (Pástor & Veronesi, 2013). The disaggregated FM estimates reveal that both developed (mean β = −0.003456, p < .001) and emerging markets (mean β = −0.003671, p = .035) exhibit significant negative war effects, with emerging markets recording a marginally larger average response. At the market level, the range of CAR[−5, +5] from −12.1% (DFMGI UAE) to +0.85% (AEX) indicates that geographic and energy-sector proximity to the conflict zone, rather than development classification per se, is the primary cross-sectional determinant of impact. This finding cautions against treating development status as a sufficient proxy for geopolitical shock exposure in risk management applications.

5.2. Heterogeneous Transmission and the Limits of Aggregate Estimates

The interaction analysis provides evidence that the transmission channel structure is not constant across regimes. The oil channel, which is statistically insignificant in the aggregate baseline, reverses to a large negative effect during the war period. This reversal illustrates a fundamental issue with aggregate estimation: when the oil price shock simultaneously represents a terms-of-trade gain for exporting economies and a supply cost shock for importing economies, cross-market aggregation masks opposing oil-return sensitivities. Standard aggregate panel estimates, therefore, understate the true impact of oil price movements on individual importing economies during geopolitical crises. This understatement may be economically meaningful. Portfolio risk models that rely on unconditional estimates of the oil-equity sensitivity will similarly underestimate the correlation between energy price risk and equity market downturns in crisis episodes.

The attenuation of the VIX channel during the war period complements this picture. If markets partially price in GPR before the spike in measured uncertainty, the observed sensitivity of returns to contemporaneous VIX movements will be lower during the event window than during normal periods. This has implications for event-driven investment strategies: the equity market’s direct response to subsequent VIX movements following a major geopolitical event may be less than what a model estimated on normal-period data would predict.

5.3. Policy Implications

Several implications follow for policymakers and regulators in emerging market economies. The primacy of the VIX channel suggests that monitoring global risk sentiment in real time is more informative for early warning purposes than tracking the specific geopolitical event itself. Central banks and financial stability authorities in emerging economies may find VIX-linked triggers for liquidity provision and foreign exchange intervention to be more effective than event-specific response protocols. The typical accumulation window of 3–5 trading days suggests that the policy response window is short and that the marginal value of pre-positioned facilities is high.

The energy-structure dependence of the oil channel has direct implications for fiscal and monetary policy design. Oil-importing emerging economies face a compounding of equity market pressure (from the direct war effect and VIX) with an adverse terms-of-trade movement during supply-driven oil shocks. Strategic petroleum reserves, energy subsidy contingency funds, and diversification of supply arrangements are all instruments that could reduce the macroeconomic amplification of this channel. The broad-based volatility elevation documented across 14 of 17 markets in the extended sample indicates that even economies with limited direct exposure face elevated volatility regimes for several weeks following a major geopolitical event, which has implications for risk model calibration, collateral requirements, and margin calls in domestic financial systems.

5.4. Implications for Portfolio Management

The cross-sectional dispersion of market-level CARs (from −12.1% in DFMGI UAE to +0.85% in the AEX) is large relative to both the sample standard deviation of daily returns and the cross-sectional dispersion observed in normal periods. This dispersion reflects the heterogeneity of conflict exposure, energy endowment, and market depth across the sample. Simple emerging market index exposure or region-based GPR scores will miss this heterogeneity. Portfolio strategies that distinguish between energy-importing and energy-exporting emerging markets and that separate markets with direct conflict-zone exposure from those geographically insulated are better positioned to manage geopolitical tail risk. The partial mean-reversion observed in the extended sample also suggests that a portion of the initial return compression may be recovered, although the timing and completeness of this reversal will vary with the subsequent evolution of the geopolitical situation.

6. Conclusion

This study examines the financial market consequences of the US–Iran military escalation of February 28, 2026, using a multi-method framework that combines event study analysis, panel regression with DKSE, FM two-stage estimation, interaction-augmented transmission channel analysis, and GARCH volatility modeling. The analysis is conducted on daily data from 17 global stock markets over January 2024 to March 2026, with robustness analysis extending the volatility sample to May 2026.

The analysis yields four principal findings. Equity markets respond negatively to the shock, with CAAR of approximately −2.5% over 3- and 5-day windows. The cross-sectional pattern, with the largest declines in DFMGI UAE, Bovespa, and BSE SENSEX, reflects geographic and energy-sector proximity to the conflict rather than development classification. Panel regression and FM estimation converge on a negative war effect (β = −0.00356, p = .044), with global risk sentiment (VIX) as the dominant transmission channel; the near-identical FM estimate (p < .001) under fully heterogeneous slopes rules out pooling bias as an explanation. Transmission channel intensities are not stable across regimes: the interaction model documents a reversal of the oil channel from mildly positive to −0.097 during the war period, consistent with a supply-shock re-evaluation, while VIX sensitivity attenuates as markets partially price in uncertainty in advance of the measured spike. Finally, conditional volatility in the acute phase remains persistence-driven rather than shock-driven, yet extended-sample GARCH across all 17 markets reveals significant volatility elevation in 14 cases and an unconditional variance roughly 1.32 times the pre-event level, suggesting a lasting imprint on volatility conditions even as returns normalize.

These findings contribute to the literature in three respects. Relative to prior event studies on geopolitical shocks, which document return effects without testing whether transmission channels are stable across regimes, this article introduces two methodological advances: interaction-augmented panel estimation that formally identifies regime-dependent transmission, and FM cross-market validation that confirms the panel result under fully heterogeneous slopes. These advances convert a descriptive event study into a mechanism-oriented transmission analysis. Empirically, this study provides early systematic evidence on the 2026 US–Iran escalation, showing that its equity market impact is comparable in magnitude to prior episodes. For applied finance, the results caution against using aggregate transmission channel estimates for crisis-period risk assessment, since the oil-equity sensitivity in particular changes sign during supply-side geopolitical shocks.

Several extensions are worth pursuing. The analysis is necessarily limited by the short post-event window available at the time of writing. Longer time-series evidence would allow more precise estimation of the persistence of return and volatility effects, as well as formal testing of mean-reversion dynamics. Multi-event comparison studies, covering a wider range of geopolitical episodes, would improve the generalizability of the transmission channel findings. Sector-level disaggregation within markets would shed light on which industries drive the aggregate responses documented here. Formal regime-switching GARCH models could provide a more rigorous treatment of the volatility-level shift identified in the extended sample, although reliable estimation would require a longer post-event horizon.

Supplemental Material

Supplemental material for this article is available online.

Footnotes

Data Availability Statement

All data used in this study are publicly available from Yahoo Finance and can be fully replicated using the R code described in the article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.