Abstract

In this study, we examine how firms’ reliance on external capital affects their real earnings management (REM) practices. The sample comprises 366,065 firm-year observations from G20 nations over the period from 2003 to 2022. Our results reveal that firms reliant on external capital engage in REM activities. The findings also emphasize that early-stage enterprises, primarily financed with equity capital, indulge in REM activities. In addition, our heterogeneity analyses suggest that businesses in common-law countries utilize REM as a preferred choice for accrual-driven earnings management (AEM). This finding shows that stronger law enforcement in such countries increases the costs of AEM practices. Overall, the results demonstrate that REM practices are conditional on firms’ dependence on external finance, life-cycle stage, and the institutional context in which firms organize their operations. These findings remain consistent across several additional tests, including alternative REM metrics, different financing metrics, and alternative scaling methods. The findings provide significant implications for investors and regulatory institutions, who seek to enhance the quality of reporting practices.

1. Introduction

Enterprises that depend on external capital have a strong motivation to report consistent and favorable earnings (Rajan & Zingales, 2003). These motivations become important when investors rely on reported financial statements to assess a firm’s financial viability (Armstrong et al., 2010; Healy & Palepu, 2001). In situations of volatile performance and limited internal funds, reported earnings serve as an important indicator for obtaining external finance on favorable terms (Chen et al., 2018; Leuz & Wysocki, 2016). Firms often embark on earnings management (EM) practices to influence investors’ perceptions (Frank & Goyal, 2009). Although EM activities through the means of accruals (AEM) have been a common practice (Dechow et al., 1996; Kothari et al., 2005), the implementation of the Sarbanes–Oxley Act intensified the regulatory oversight, increasing its detectability and associated costs (Cohen et al., 2008). Hence, a growing number of firms have embarked on real EM (REM) practices. They involve adjustments to normal operating activities, including revenue timing, production levels, and discretionary spending to meet reporting objectives (Gunny, 2010; Roychowdhury, 2006). In comparison to AEM, REM activities directly impact a firm’s earnings and are also less prone to regulatory scrutiny 1 (Badertscher, 2011; Zang, 2012).

The intensity of REM practices varies across firms’ life-cycle stages (Sun et al., 2014; Zang, 2012). For instance, young firms with their limited retained earnings and uncertain internal cash flows depend on external sources for their growth capital (Dickinson, 2011). Their reliance on external funding provides them with incentives to utilize REM activities to signal stability (Berger & Udell, 1998). REM also helps firms reliant on equity financing to meet their valuation benchmarks (Cohen & Zarowin, 2010; Teoh et al., 1998), whereas firms reliant on debt financing indulge in REM to avoid covenant violations (Nagar & Radhakrishnan, 2017). Further, we contend that the institutional context in which firms organize their operations also affects their earnings management choices. In nations with robust investor protection regimes, such as common-law jurisdictions, AEM causes increased legal and regulatory risk (Ball et al., 2003; La Porta et al., 1998). Hence, firms in such institutional environments may prefer REM as a discreet method to achieve earnings objectives without explicitly violating accounting regulations (Enomoto et al., 2015). Although earlier studies documented this substitution effect (Badertscher, 2011; Cohen & Zarowin, 2010; Zang, 2012), there is limited evidence on how it interacts with firms’ external financing dependence and the stage of their life-cycle across various institutional environments.

We utilize a large panel of 366,065 firm-year data from G20 nations over the period 2003–2022 and investigate whether firms’ reliance on external financing influences their engagement in REM practices. We subsequently analyze how this association varies across firm-specific and institutional characteristics. In particular, we analyze the heterogeneity across the corporate life-cycle stages, concentrating on younger and resource-constrained firms. We conduct sub-sample analysis to assess how varied institutional contexts (common law vs civil law) condition the association between external financing dependence and firms’ REM activities.

In this study, our dependent variable, abnormal REM, captures the extent to which managers alter real operating and investing activities to influence reported earnings (Gunny, 2010). The main independent variable, dependence on external finance, is constructed following Zhang et al. (2020). It is the ratio of capital obtained through debt and equity in relation to retained earnings. Our empirical evidence indicates that external financing dependence has a positive effect on REM practices. We also show that REM practices are more prevalent among equity-financed firms at the early phase of the corporate life cycle. Furthermore, the findings indicate that REM practices are prevalent in common-law nations, aligning with the notion that robust enforcement discourages AEM. We adopt several empirical methods to establish the causal interpretation of our results and to alleviate potential endogeneity concerns. We employ Srivastava’s (2019) model of real earnings management that incorporates lagged firm performance, prior-period REM, and expected future sales to mitigate omitted variable bias. Our empirical design includes firm-fixed effects to account for unobserved firm-specific variations. We also incorporate interactive fixed effects involving country, industry, and year indicators to account for institutional and sectoral variations over time. Additionally, we employ a series of additional tests using alternative financing variables, different scaling approaches, and firm-specific adjustments to account for simultaneity and measurement error. Overall, we contend that these approaches enhance the reliability of our estimates and validate that the observed relation between dependence on external finance and REM is not driven by endogeneity.

The study provides a minimum of three contributions to the prevailing literature. First, we integrate two research streams: influence of external financing dependence on REM (Cheng & Warfield, 2005; Dechow et al., 1996) and life-cycle effects on managerial behavior (Dickinson, 2011; Krishnan et al., 2021). We show that the relation between dependence on external finance and REM is not uniform across firms; rather, it is more prevalent among early-stage firms that face heightened information asymmetry, financial constraints, and dependence on external capital. In a way, we identify the firm life cycle as an important boundary condition in comprehending managers’ incentives to engage in REM. Second, the study extends the financing-based view of EM by distinguishing between debt and equity financing across life-cycle stages. While previous studies establish a general association between external financing and EM (e.g., Zhang et al., 2020), we report that the relationship is predominantly influenced by equity-financed enterprises in the introductory stage of their life cycle. Third, we add to the international EM literature by elucidating the effect of institutional contexts on enterprises’ reporting choices. In particular, we document that the positive association between reliance on external finance and REM is prominent in common-law countries where enhanced investor protection, more active capital markets, and efficient enforcement increase the costs of AEM. These findings complement the previous evidence that institutional quality affects earnings management incentives and the choice between accrual and real EM practices (Enomoto et al., 2015; Leuz et al., 2003).

The subsequent sections of the article will proceed as follows. In Section 2, we present the literature review and develop our empirical hypotheses. Section 3 delineates the sample, variables and empirical method. Section 4 reports the findings and additional analyses. In Section 5, we conclude the study with key findings and implications.

2. Literature Review and Hypothesis Development

2.1. Relationship Between External Financing Dependence and REM

The reliance on external financing incentivizes managerial discretion and influences the reporting environment. In light of a greater information asymmetry, corporate managers utilize reported earnings to lower uncertainty as well as signal firm quality to external stakeholders (Healy & Palepu, 2001). Agency theory also asserts that when the cost and accessibility of capital are contingent upon the perceived performance, managers have a strong motivation to influence these perceptions (Jensen & Meckling, 1976). Real earnings management practices, operationalized through operating and investment decisions, provide managers with a means to affect the reported performance (Zhang et al., 2020).

In equity markets, reported earnings have a prominent role in valuation, particularly for equity investors who assume the residual risk of firms’ prospects and their performance (Gao et al., 2017). Managers aiming to issue additional equity or maintain current equity valuation often employ REM practices to report favorable operating performance (Rangan, 1998; Teoh et al., 1998). These signaling efforts of managers convey positive private information. In corporate debt markets, managers have an incentive to maintain contractual obligations rather than market valuation. Loan agreements impose stringent covenants and conditions for contractual repayment. The violations of these agreements lead to penalties, renegotiations, and eventual default (DeFond & Jiambalvo, 1994). Therefore, managers may utilize EM practices to preserve perceived financial health and sustain borrowing capacity (Dichev & Skinner, 2002; Guay, 2008; Trueman & Titman, 1988). Although equity- and debt-driven EM efforts have distinct objectives, they both underscore the importance of reporting favorable accounting performance. In both contexts, the heightened regulatory scrutiny incentivizes managers to adjust real operating and investing activities to secure cost-effective financing. This perspective leads to the following hypothesis:

H1a: Firms’ external capital dependence positively influences their real earnings management activities.

However, an alternative perspective suggests that increased dependence on external financing can make it harder to manage earnings. Firms that rely on external funds face intense scrutiny from creditors, investors, and analysts. This oversight can limit their opportunistic behavior (Ball & Shivakumar, 2008; Hope, 2003). Debt contracts impose external discipline. Firms’ regular access to capital markets increases reputational concerns and discourages aggressive earnings reporting (Jensen & Meckling, 1976). Thus, we contend that the effect of external financing dependence on EM is theoretically ambiguous. In a way, it posits a trade-off between the advantages of signaling and the costs of external monitoring. We propose to clarify such a theoretical ambiguity by examining the following empirical hypothesis:

H1b: Firms’ external capital dependence negatively influences their real earnings management activities.

2.2. Influence of Firm Life-cycle Stages

The stages of the life cycle affect firms’ financing needs and access to capital markets. During the introduction phase, businesses generate limited or negative cash flows. Given their limited operational history, financial institutions regard them as high-risk (Byoun, 2008). These younger firms face several constraints in obtaining debt capital, which requires collateral and compliance with stringent covenants. As a result, equity financing becomes the primary source of external capital for early-stage firms (Cohen & Langberg, 2009). As firms mature, their increased cash flows enhance their creditworthiness. It facilitates debt financing and reduces their reliance on equity finance (DeAngelo et al., 2010; Hasan & Rahman, 2017). Faff et al. (2016) and Kieschnick and Moussawi (2018) show that US firms primarily utilize equity capital during the initial stages of their life cycle, and they prefer debt in the later stages, particularly at the mature stage.

Early-stage firms face significant information gaps and investor skepticism. As a result, their external capital raising on favorable terms becomes challenging. From a signaling perspective, managers therefore have a motivation to convey strong operational performance to gain the confidence of market participants (Zhang et al., 2020). As REM involves altering operational and investment activities, they replicate legitimate performance improvements and are less traceable than AEM practices (Gunny, 2010; Roychowdhury, 2006). Therefore, we argue that the incentive to employ REM is more evident when firms rely heavily on equity markets, where valuations prioritize reported earnings (Zhang et al., 2020).

Mature businesses, on the other hand, benefit from consistent earnings, accumulated reputational capital, and established credit profiles. As a result, they access debt finance at a favorable cost (DeAngelo et al., 2010; Lemmon & Zender, 2010). The financial flexibility of firms at the mature stage diminishes their need for aggressive EM to secure external capital. Further, external financial markets’ oversight limits managerial discretion and constrains the mature firms’ scope for engaging in EM practices (Nagar & Radhakrishnan, 2017). In contrast, firms in the decline phase operate in a distinct environment. Their reduced profitability and limited or no growth opportunities constrain their ability to access external capital markets (Kieschnick & Moussawi, 2018). While the signaling theory posits that managers of these firms may employ REM activities to exhibit resilience (Zhang et al., 2020), their effectiveness is limited in the context of decline-stage firms. Investors also undervalue the reported earnings of distressed firms and prioritize validating fundamental factors, including cash flow sustainability, asset quality, and the restructuring potential (Florou & Kosi, 2015; Shleifer & Vishny, 1997). Prior literature also documents that investors penalize EM practices of distressed firms more severely as they view such acts as opportunistic rather than value-enhancing (Cohen & Zarowin, 2010; Enomoto et al., 2015). Therefore, we note that the decline-stage firms derive limited marginal benefits from REM. Moreover, their EM may undermine their credibility and intensify financing constraints relative to firms in early life-cycle stages. In consideration of the above-mentioned reasons, we contend that the incentive to employ REM practices is more evident in the introduction-stage firms. Hence, we propose to evaluate the ensuing hypothesis:

H2a: Firms at the introduction stage that rely on equity capital engage in REM practices.

Nevertheless, we note that an alternative strand of literature suggests that early-stage enterprises face stronger governance and disclosure pressures. In the case of high-growth firms, equity investors, venture capitalists, and underwriters implement stringent due diligence and monitoring mechanisms to protect their interests (Berger & Udell, 1998; Jensen & Meckling, 1976). Further, these high-growth firms depend significantly on their reputation to secure continued access to capital markets, making them less likely to undertake activities that could hurt their credibility (Healy & Palepu, 2001). Thus, the heightened scrutiny and reputational concerns may limit the early-stage firms’ engagement in REM practices. In attention to the above discussion, we propose to test the ensuing competing hypothesis:

H2b: Firms at the introduction stage that rely on equity capital do not engage in REM practices.

2.3. Influence of Institutional Environment

The institutional environment in which firms organize their operations influences the choice of their EM strategies. We note that legal and regulatory frameworks define the standards for acceptable reporting practices, which influence monitoring intensity and establish the consequences for non-compliance (Leuz et al., 2003). These institutional attributes affect how managers balance the advantages of meeting the expectations of external capital providers relative to the risk of detection, adverse reputational effects, and regulatory sanctions from engaging in EM practices.

In common-law countries with well-established capital markets, the costs of AEM practices are substantial (Daske et al., 2008; Shima & Gordon, 2011). Companies operating in these jurisdictions engage in REM practices, which are difficult to differentiate from legitimate business operations (Zang, 2012). The REM allows the managers in these countries to demonstrate strong operational performance while avoiding the increased regulatory risks associated with accrual EM practices. From a signaling perspective (Ball et al., 2003), managers’ preference for REM practices may be viewed as efforts to reassure investors in light of heightened scrutiny in common-law countries. Conversely, in civil-law jurisdictions, where investor protection is less robust, the reduced enforcement intensity lessens the deterrent effect against AEM endeavors. In those institutional environments, the management of discretionary accrual accounts is less expensive and, in certain instances, a preferred alternative (Achleitner et al., 2014).

The preceding discussion emphasizes that the institutional environment interacts with financing requirements to influence the choices of EM practices. In common-law countries, where regulatory oversight is stronger and reliance on capital markets is greater, we argue that businesses reliant on external capital adopt REM as a viable strategy. Accordingly, we propose to empirically evaluate the following hypothesis:

H3: The positive association between external financing and REM is stronger in common-law countries.

3. Methodology

3.1. Data

We consider publicly listed firms from G20 nations over the period 2003–2022 for the empirical investigation. The study period represents the post-reform environment following the United States’ implementation of the Sarbanes–Oxley Act and similar governance reforms in other major economies. This period provides a stable regulatory setting for examining REM across various institutional contexts. We obtain firm-specific financial information from Refinitiv Eikon Datastream (Florou & Kosi, 2015; Leuz et al., 2003). Following prior studies, we eliminate finance and utility companies owing to their distinct regulatory reporting requirements (Gunny, 2010). We also drop observations with missing data for key variables, including those representing REM activities. Our final sample includes 366,065 firm-year observations from 31,570 unique firms across G20 countries. 2 Of the sample countries, China accounts for 21.8% of the total firm-year observations, followed by Japan (13.7%), Canada (10.6%), the United States (8.7%), and Argentina, which accounts for the least (0.17%) total firm-year observations. We utilize a cash flow-based methodology to identify the firm-year records with their respective life-cycle phases (Dickinson, 2011). Further, we classify firm-year observations into 24 major industry groups, consistent with Fama and French’s (1993) industrial classification.

3.2. Variables

3.2.1. Dependent Variable

We compute expected values of REM components 3 separately for each country-industry-year group with at least 15 firm-year records (Beyer et al., 2018; Gunny, 2010). We subsequently calculate the firm-level abnormal REM components as the disparity between reported and expected values. These components include (a) abnormal expenditure on research and development, (b) abnormal expenditure on SG&A activities, (c) abnormal production costs (multiplied by –1), and (d) abnormal asset sales (also multiplied by –1). We aggregate these four components to construct a composite measure of abnormal REM (AB_RM), which is our dependent variable in the ensuing analysis.

3.2.2. Independent Variables

We measure our primary independent variable, firms’ reliance on external financing, as a ratio of external-to-internal capital (EX_FIN). It is computed as the sum of interest-bearing debt and equity capital, scaled by retained earnings (Zhang et al., 2020). To assess the impact of various sources of external financing, we construct a debt financing measure (DEBT_FIN) as a ratio of total debt to retained earnings and an equity financing measure (EQUITY_FIN) as the equity capital scaled by retained earnings.

3.2.3. Control Variables

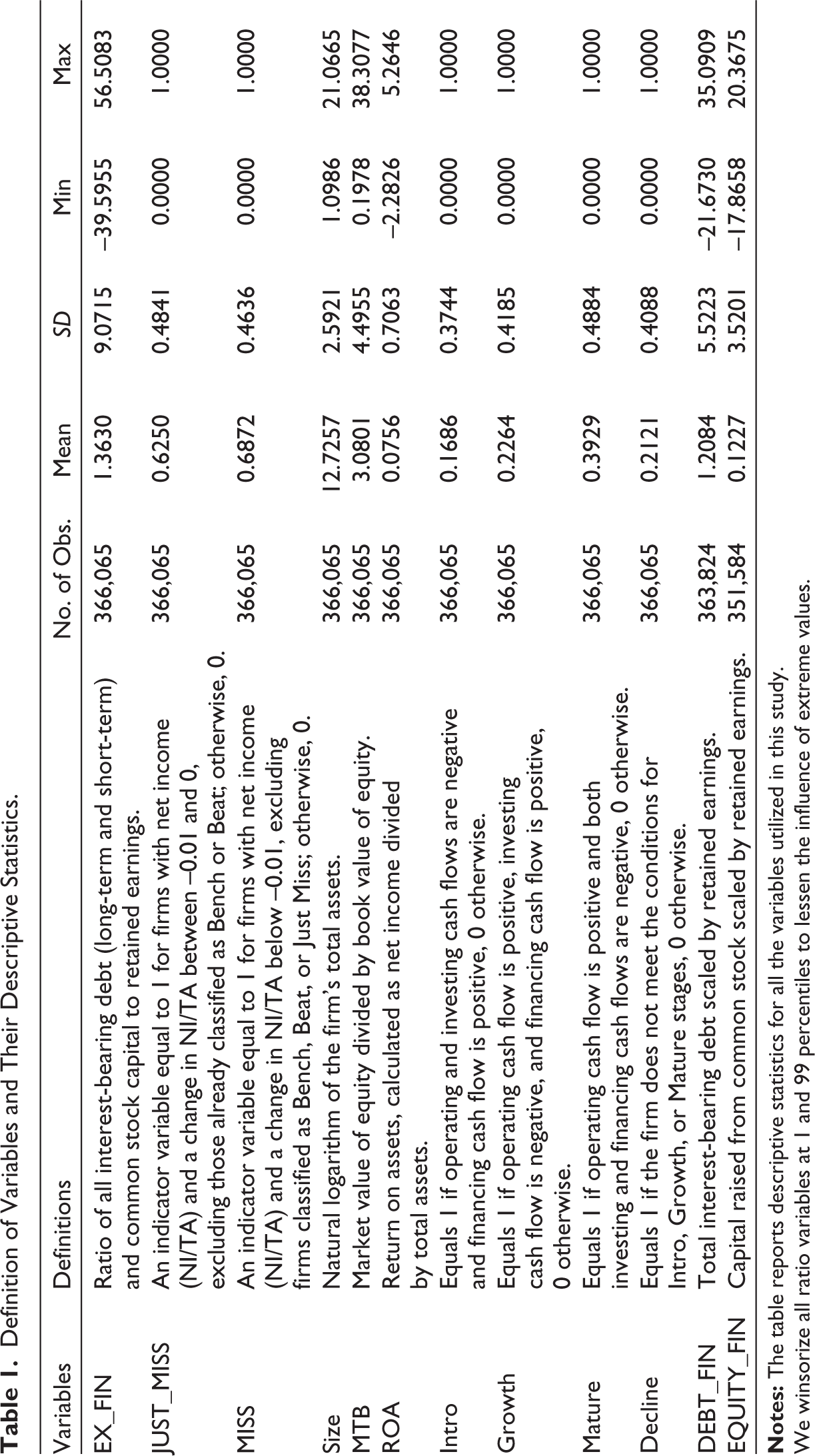

In a multivariate analysis, we account for various firm-specific attributes that may affect the extent of REM. They include Size, the ratio of market value to book value of equity (MTB), and return on assets (ROA; Gunny, 2010). We measure Size as the natural log of total assets. Larger companies face increased scrutiny from analysts, which diminishes their ability to adopt aggressive reporting practices. Hence, we contend that Size has a negative impact on abnormal REM (Cheng & Warfield, 2005). MTB reflects firms’ growth opportunities. Firms with greater prospects have an incentive to engage in REM, as it allows them to sustain favorable earnings that align with market expectations and secure affordable external financing (Zang, 2012). ROA serves as a measure of profitability. Firms with lower profitability tend to indulge in REM to meet earnings thresholds and reassure external stakeholders (Cohen & Zarowin, 2010; Roychowdhury, 2006). Further, we note that firms that fall short of meeting their performance thresholds embark on more EM activities to avoid adverse market reactions (Burgstahler & Dichev, 1997; Siriviriyakul, 2014). We consider the previous year’s profit and zero profit as the earnings benchmarks (Gunny, 2010) and control for these firms’ tendencies by constructing two binary variables. They include JUST MISS and MISS, which identify firm-year observations that report earnings slightly below the benchmark and substantially below the benchmark, respectively. We provide the description of these variables in Table 1.

Definition of Variables and Their Descriptive Statistics.

We winsorize all ratio variables at 1 and 99 percentiles to lessen the influence of extreme values.

3.3. Estimation Procedure

We assess whether firms that rely on external finance embark on REM by estimating the following econometric model (Beyer et al., 2018; Gunny, 2010):

The dependent variable, AB_RMit, measures the aggregate REM of the ith firm in year t. The negative value of the coefficient β1 indicates engagement in REM activities. We include firm-fixed effects (γi) and country-industry-year interactive fixed effects (θcjt) to account for time-invariant firm-specific unobserved heterogeneity and the temporal variation arising from the industry-specific events over the study period across the sample countries, respectively.

4. Results and Discussion

4.1. Univariate Analyses

Table 1 shows the univariate statistics for all the variables used in the analysis. We winsorize the ratio variables at 1 and 99 percentiles to mitigate the impact of outliers. The external financing variable (EX_FIN) has an average value of 1.36 and a standard deviation (SD) of 9.07, indicating considerable variability in sample firms’ reliance on external capital. We note that the minimum value of EX_FIN is negative and is due to negative cumulative retained earnings reported by a few of our sample firms for a very small number of years during the study period. Further, we report that the mean value of DEBT_FIN (1.21) is higher than that of EQUITY_FIN (0.122), suggesting a greater dependence on debt capital. The reported values of firm size (mean = 12.72, SD = 2.59) and MTB (mean = 3.08, SD = 4.49) highlight substantial heterogeneity in operating scale and growth opportunities across the sample firms.

We present pairwise Pearson correlation coefficients among the variables in Table A1. The reported findings suggest that sample firms’ real earnings management activities (AB_RM) negatively correlate with their dependence on external financing (EX_FIN), regardless of their source (DEBT_FIN and EQUITY_FIN), suggesting that firms relying on external finance engage in REM activities. Further, we note that AB_RM positively correlates with firm profitability (ROA) and negatively correlates with Size. Nevertheless, the average variance inflation factor values remain close to unity, which is significantly lower than the conventional threshold. It confirms that multicollinearity does not pose a concern in our multivariate analysis (O’Brien, 2007; Saleh et al., 2020).

4.2. Multivariate Analyses

4.2.1. Impact of External Financing on REM

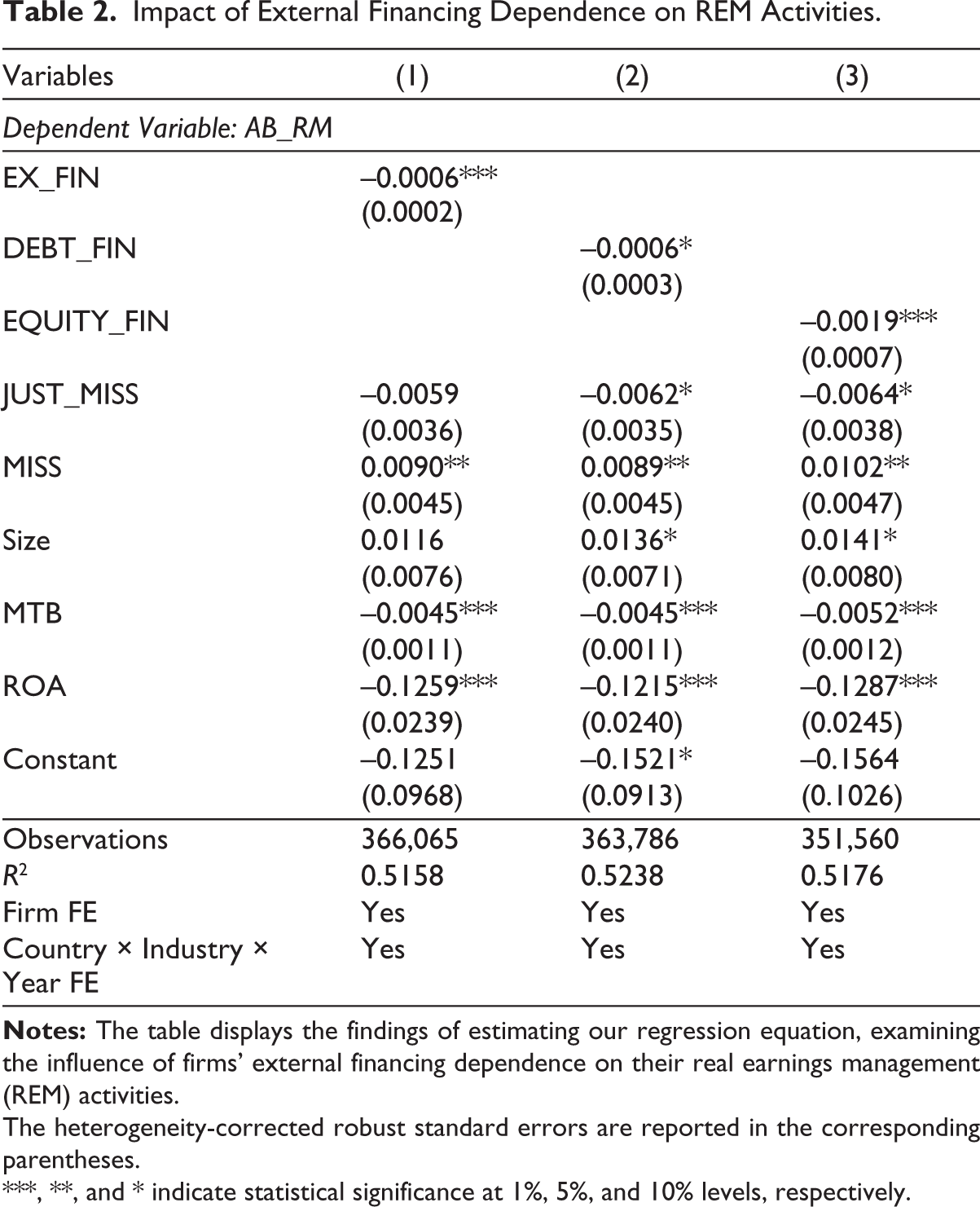

Table 2 shows the findings of our regression equation, which assesses how reliance on external financing affects REM practices. In Column (1), we use EX_FIN, the ratio of external to internal capital, as our measure of external financing dependence. Its coefficient is negatively significant, implying that firms relying on external capital engage in REM to influence reporting earnings. Beyond statistical relevance, the magnitude of the coefficient indicates that reliance on external capital has economically meaningful effects on firms’ REM practices. In Columns (2) and (3), we consider reliance on debt and equity financing. The reported findings suggest that firms relying on external financing, irrespective of the source, engage in REM activities, though our results are highly significant in the case of firms that rely on a greater amount of equity capital. The stronger effect associated with the reliance on equity financing aligns with the prominent role of reported earnings in equity securities’ valuation (Gao et al., 2017; Rangan, 1998; Teoh et al., 1998). In debt markets, by contrast, managerial incentives are oriented toward meeting contractual obligations rather than influencing market perceptions, as covenant violations carry direct penalties including renegotiation and default (DeFond & Jiambalvo, 1994). The relatively weaker effect of debt financing dependence on REM thus reflects a fundamentally different incentive structure compared to equity financing. These findings confirm H1a. Our regression model controls for sample firms’ compulsions to meet their earnings benchmarks (JUST_MISS, MISS), size, profitability, and growth potential. These variables capture firm-level characteristics that potentially influence REM (e.g., Gunny, 2010; Zang, 2012). Their inclusion in the econometric model accounts for the impact of firm scale, performance, and investment opportunities on the association between external capital dependence and firms’ REM activities.

Impact of External Financing Dependence on REM Activities.

The heterogeneity-corrected robust standard errors are reported in the corresponding parentheses.

***, **, and * indicate statistical significance at 1%, 5%, and 10% levels, respectively.

4.2.2. Role of Corporate Life-cycle Stages

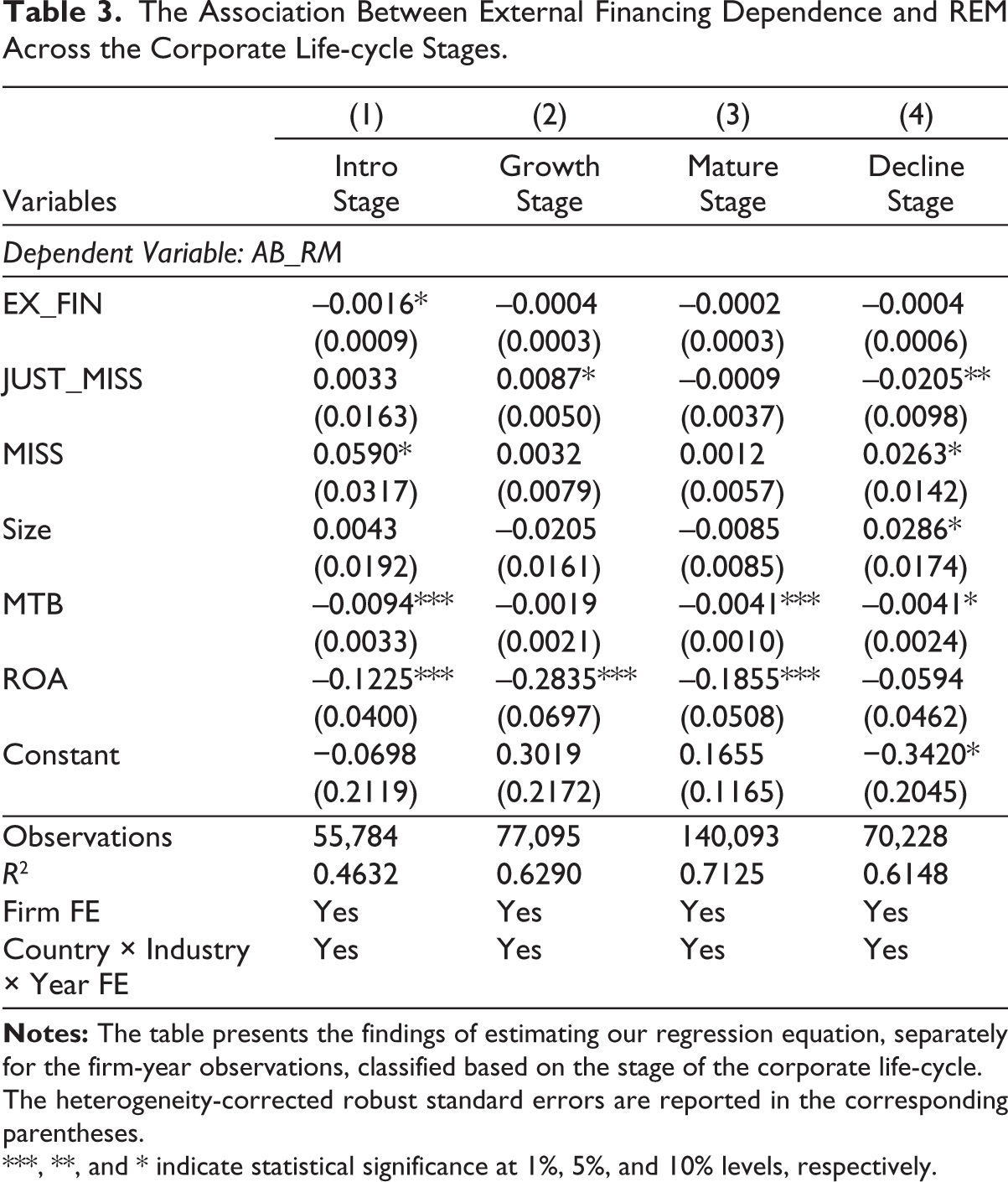

Table 3 reports the findings from estimating our baseline regression equation separately for firm-year observations, classified by their life-cycle stages. For enterprises in the introduction stage, the coefficient estimate on EX_FIN is negative, implying that the dependence on external capital is associated with higher REM at this phase. We also note that, in the case of growth-, mature-, and decline-stage firm-year observations, the coefficients on EX_FIN are not statistically significant. They suggest that the external financing and REM relationship is not prominent among firm-year observations at those stages. Our results, in a way, underscore the financial constraints of introduction-stage firms and support H2a. They operate with little or no internal cash flows, limited debt capacity, and significant information asymmetry (Cohen & Langberg, 2009). As a result, early-stage firms have an incentive to utilize REM as a mechanism to influence perceptions of external resources. However, in enterprises at later stages in their life cycle, the availability of internal funds, established reputations, and enhanced monitoring mechanisms appear to mitigate the need for REM (Lemmon & Zender, 2010).

The Association Between External Financing Dependence and REM Across the Corporate Life-cycle Stages.

The heterogeneity-corrected robust standard errors are reported in the corresponding parentheses.

***, **, and * indicate statistical significance at 1%, 5%, and 10% levels, respectively.

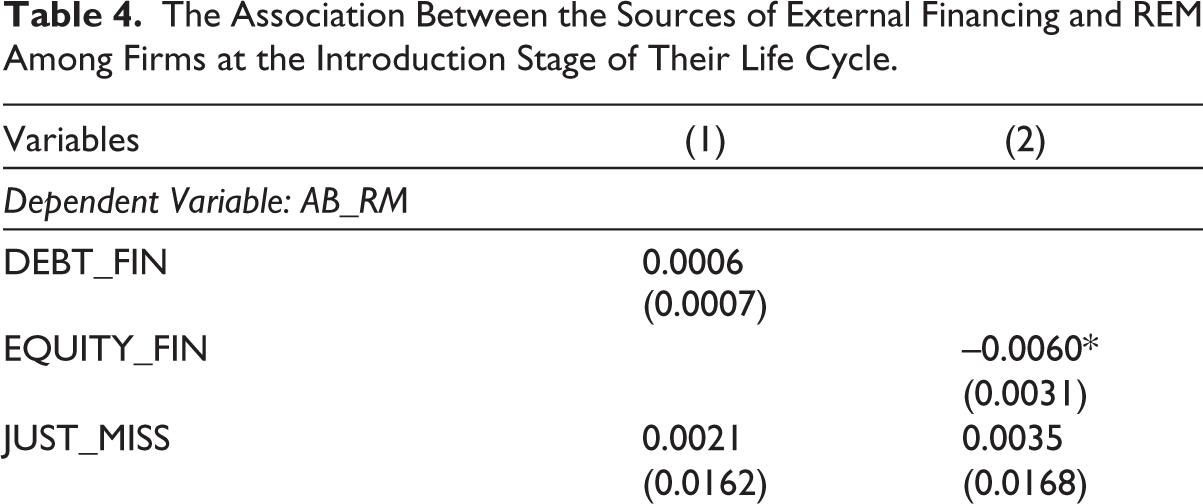

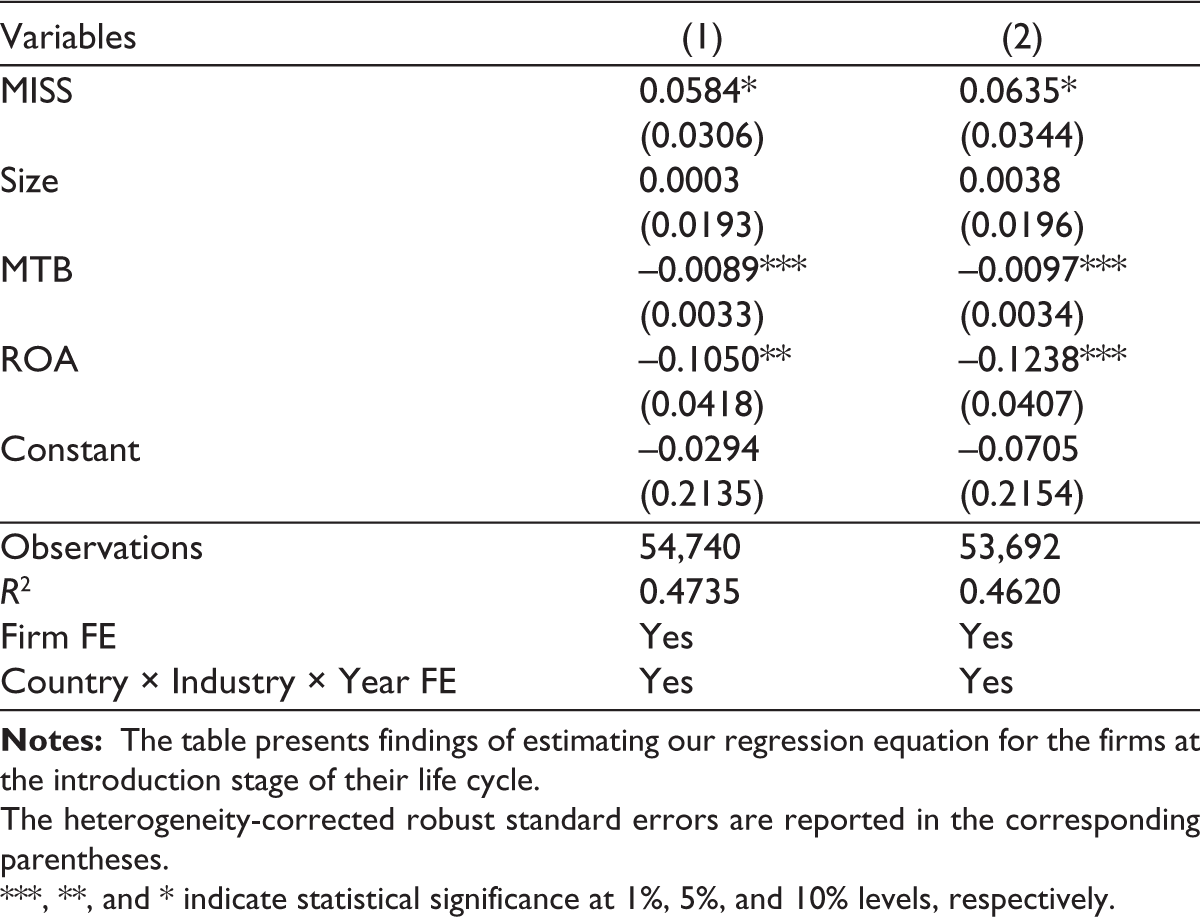

Further, we assess the relationship between the choice of external financing and the firms’ REM activities among early-stage firms. The reported estimates in Table 4 show that firms’ reliance on equity capital at their introduction stage incentivizes them to utilize REM practices. On the contrary, firms dependent on debt financing do not utilize REM to showcase their performance. These results support our contention that younger firms, with non-existent internal cash flows and limited reputational capital (Dickinson, 2011; Miller & Friesen, 1984), have a motivation to report sustained performance.

The Association Between the Sources of External Financing and REM Among Firms at the Introduction Stage of Their Life Cycle.

The heterogeneity-corrected robust standard errors are reported in the corresponding parentheses.

***, **, and * indicate statistical significance at 1%, 5%, and 10% levels, respectively.

4.2.3. Role of Institutional Environment

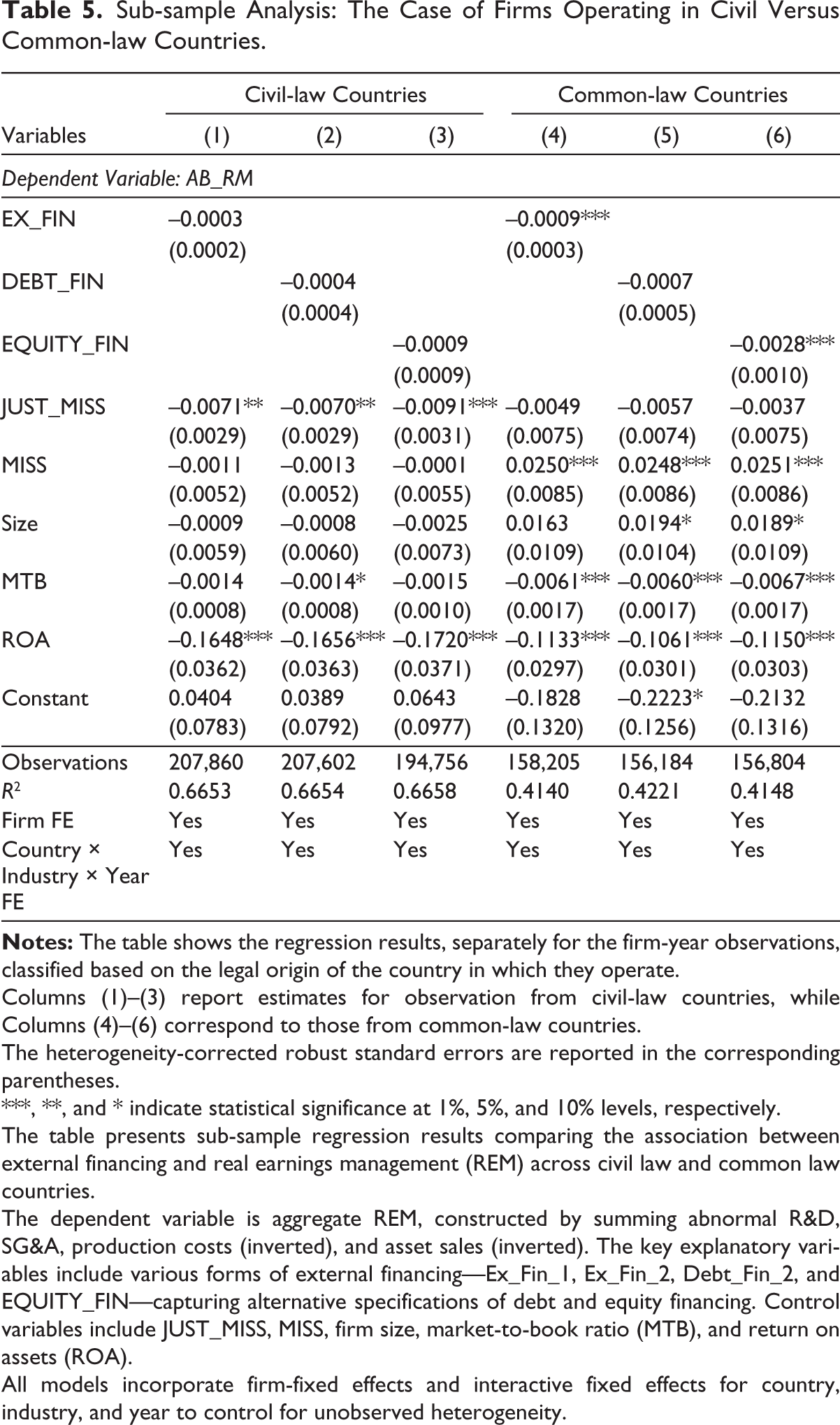

We split the sample firm-year observations into those operating in civil- and common-law countries based on their legal origin and then estimate the baseline regression equation separately for these sub-samples. The findings reported in Table 5 suggest the important cross-country differences in EM practices. In the case of common-law countries (Column (4)), the firms reliant on external capital adjust real activities to influence their reported earnings. We also find that equity-reliant firms in these countries engage more aggressively in REM practices (Column (6)). These findings underscore the pressure firms experience to maintain higher market valuation in investor-driven capital (equity) markets (Cohen & Zarowin, 2010). In contrast, businesses operating in civil-law countries show no significant relationship between external financing and REM. We argue that weaker investor protection and lower enforcement intensity in these jurisdictions reduce the managers’ incentive to undertake REM (Achleitner et al., 2014). Overall, the findings validate H3 that the institutional environment conditions the form and intensity of EM. In particular, in common-law countries, firms that are reliant on external finance undertake REM practices. Our findings complement previous research that underlines the significance of institutional setting in influencing firms’ choice between REM and AEM practices (Enomoto et al., 2015).

Sub-sample Analysis: The Case of Firms Operating in Civil Versus Common-law Countries.

Columns (1)–(3) report estimates for observation from civil-law countries, while Columns (4)–(6) correspond to those from common-law countries.

The heterogeneity-corrected robust standard errors are reported in the corresponding parentheses.

***, **, and * indicate statistical significance at 1%, 5%, and 10% levels, respectively.

The table presents sub-sample regression results comparing the association between external financing and real earnings management (REM) across civil law and common law countries.

The dependent variable is aggregate REM, constructed by summing abnormal R&D, SG&A, production costs (inverted), and asset sales (inverted). The key explanatory variables include various forms of external financing—Ex_Fin_1, Ex_Fin_2, Debt_Fin_2, and EQUITY_FIN—capturing alternative specifications of debt and equity financing. Control variables include JUST_MISS, MISS, firm size, market-to-book ratio (MTB), and return on assets (ROA).

All models incorporate firm-fixed effects and interactive fixed effects for country, industry, and year to control for unobserved heterogeneity.

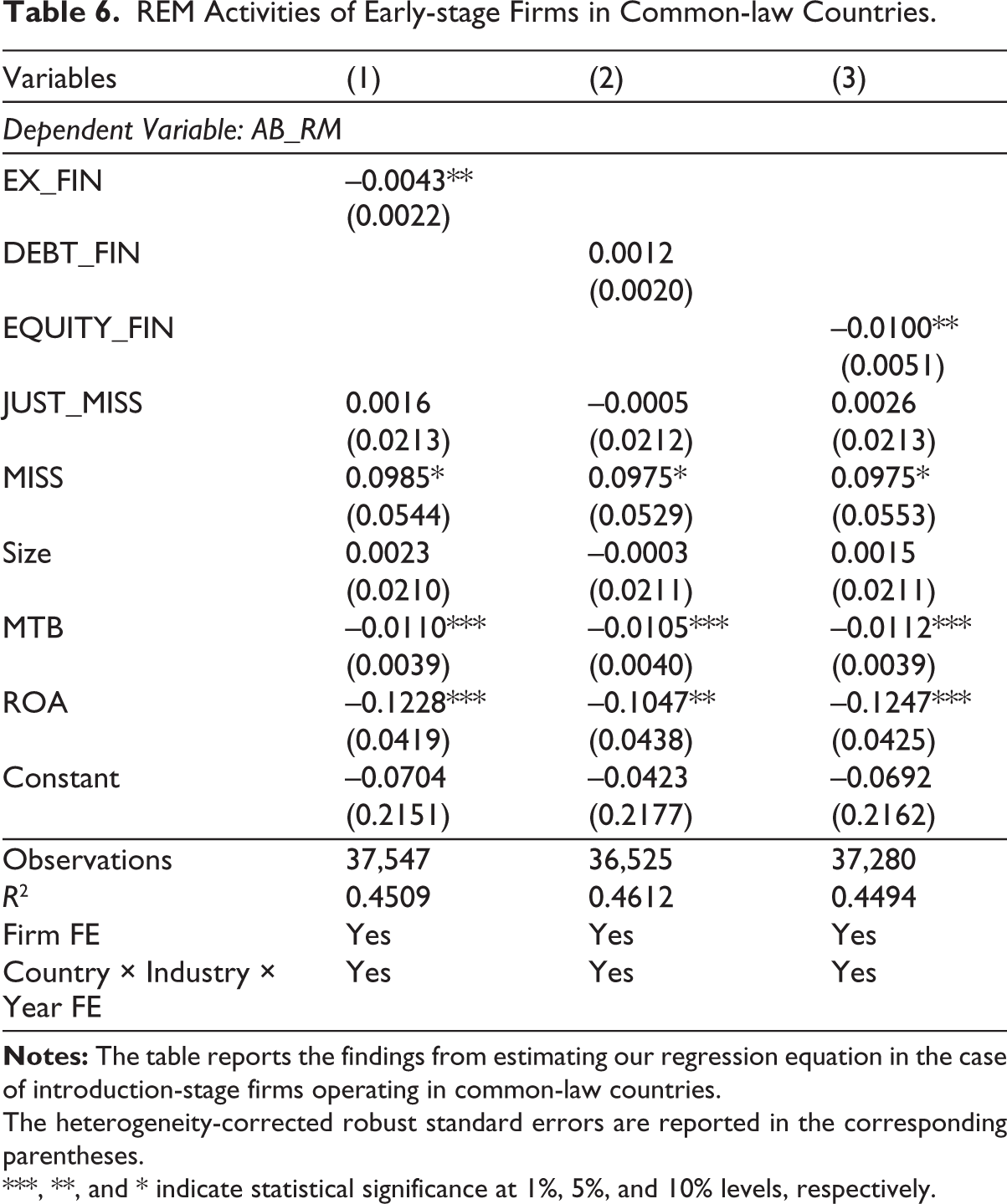

Further, our empirical context allows us to investigate the REM practices of the introduction-stage firms in common-law countries. We estimate the baseline empirical equation for these firm-year records and report the findings in Table 6. In Column (1), the coefficient on EX_FIN is negative (–0.0043) and is significant. It indicates that younger firms dependent on external capital adjust their real activities to influence their reported earnings. The finding also validates our contention that early-stage enterprises have a greater motivation to strategize their operations to obtain external capital on favorable terms. The findings in Columns (2) and (3) reveal that reliance on equity capital is significantly associated with REM, while dependence on debt capital exhibits no such effect. These results reflect the expectations of equity market participants in common-law countries, where capital markets place significant importance on earnings (Cohen & Zarowin, 2010; Teoh et al., 1998). Overall, the results show that firms’ financing structure, life-cycle stage, and institutional setting influence their REM activities.

REM Activities of Early-stage Firms in Common-law Countries.

The heterogeneity-corrected robust standard errors are reported in the corresponding parentheses.

***, **, and * indicate statistical significance at 1%, 5%, and 10% levels, respectively.

4.3. Additional Tests

We conduct a series of additional tests to assess the validity of our findings. First, we employ Srivastava’s (2019) dynamic model that accounts for lagged firm performance, previous-period REM (for dynamic persistence), and expected future sales. This specification mitigates the potential bias arising from the omitted variables. Second, we consider the alternative measures of external financing dependence that include preferred equity and another one that excludes short-term external financing. These alternative measures account for the broader financing structures while excluding transitory funding effects. Third, to address scaling-related concerns, we re-examine the baseline model by considering the financing dependence variable scaled by lagged retained earnings. In an alternative specification, we scale it by the value of total assets. Fourth, we use the country-industry-averaged-adjusted external financing measure to isolate firm-specific deviations. In all the above additional tests, our findings 4 remain consistent with our baseline results discussed in the preceding subsections. In summary, these additional tests show that the direction, magnitude, and significance of external financing and REM relationship are robust to omitted variable bias, scaling choices, and alternative measurement approaches.

5. Conclusion

This study analyses 366,065 firm-year observations from G20 economies over the study period 2003–2022 and assesses whether the reliance on external financing influences firms’ REM practices. We also examine the heterogeneity in firms’ REM practices across their life-cycle stages and institutional contexts. We report at least three important findings. First, firms reliant on external capital indulge in REM activities, particularly those financed through equity capital. Second, incentives to undertake REM are more pronounced among early-stage firms, which face greater capital requirements and limited internal funds. Third, institutional context has a significant impact on firms’ choice of EM practices. In common-law countries, stronger legal enforcement mechanisms elevate the costs of engaging in AEM practices, thereby increasing firms’ reliance on REM, particularly among those with greater dependence on external capital. In contrast, enterprises in civil-law jurisdictions, characterized by weaker investor protection regimes, exhibit no association between external capital reliance and REM practices. Our additional tests involving alternative measures of financial dependence, scaling methods, and model specifications validate our findings.

The findings of the present study provide valuable insights for various stakeholders. For investors, the results suggest a need for increased scrutiny of the earnings of early-stage equity-dependent firms, due to their potential engagement in REM. For policymakers, results suggest that the stronger enforcement against AEM may encourage businesses to indulge in REM, underscoring the need for increased oversight of operating decisions. Our study also cautions managers about the risks associated with prioritizing the operating adjustments that undermine their credibility.

Supplemental Material

Supplemental material for this article is available online.

Footnotes

Acknowledgements

The authors thank the anonymous reviewers, the editor, and the participants of the Research Symposium on Finance and Economics 2025 for their constructive feedback on an earlier version of this article. The authors take the sole responsibility for any remaining errors or omissions.

Data Availability Statement

The data are available in the sources mentioned in the article. The codes pertaining to data preparation and analysis are available on request.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.