Abstract

In the 1980s, Maruti had no real competition in India, and it did not even have to market its products. There were long waiting lists, and they made more than half of their cars in white, thus saving costs. However, once Hyundai entered the market, things started to change. Hyundai started focusing on quality, customer care and service. It talked about its technology like multi-point fuel injection (MPFI) which emitted lower emission and met Euro norms. It brought in Santro Zip Drive version which was the first small car with a power steering. It advertised Santro as being a five-seater as opposed to Maruti Suzuki’s products, and it brought in fluidic sculpture design with Verna and promoted it. As a result, Maruti Suzuki, which controlled 70 per cent of the Indian market at its peak, came down to 52 per cent in twenty years, whereas Hyundai reached around 22 per cent. It was a long battle in a sector whose dynamics were changing as a result of government policies, such as excise duty cuts, increase in customs duty, lower interest rates and the introduction of goods and service tax (GST) besides the ambitious ‘Make in India’ campaign.

With change in the demographics in the country over the past 10 years the average car buyer’s age today has dropped drastically. With a plethora of opportunities for youngsters today & the general change in attitude to life & access to finance, the automobile industry has found an entirely new bracket of buyers ranging from the age group of approximately 25 to 32.

Introduction

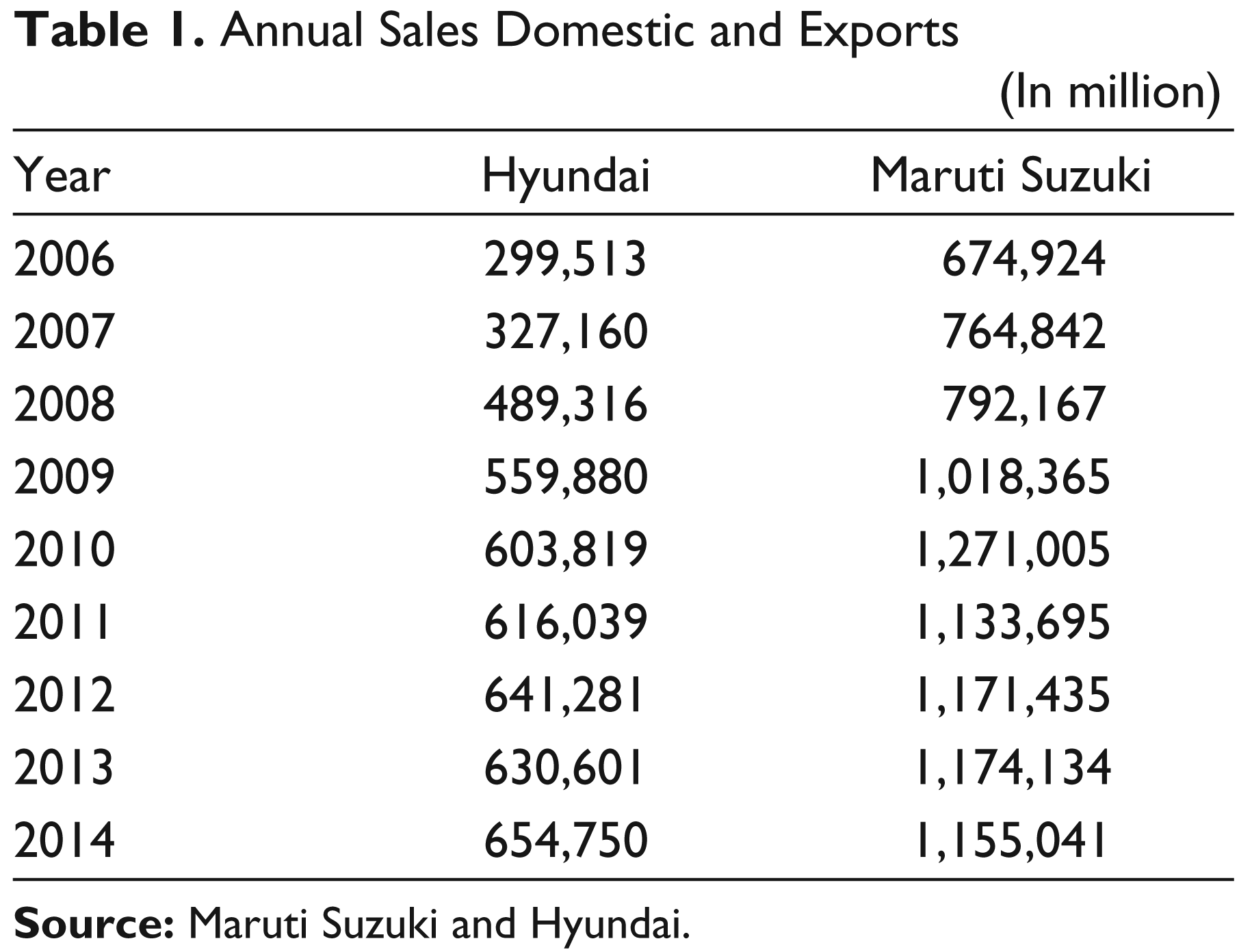

Hyundai finished the year 2014 on a high scale with a market share of 22 per cent, which was the highest it had ever reached. Maruti Suzuki was way ahead, but it had also started fifteen years earlier. Hyundai, however, was much ahead of Honda, the number three which only had 8 per cent market share. In 2014, after Maruti, Hyundai became the only other company that had sold over 400,000 cars in India. Its profit for the Indian unit had doubled in the last five years, and it had been the largest exporter of cars from the country since 2008 (see Table 1).

Annual Sales Domestic and Exports (In million)

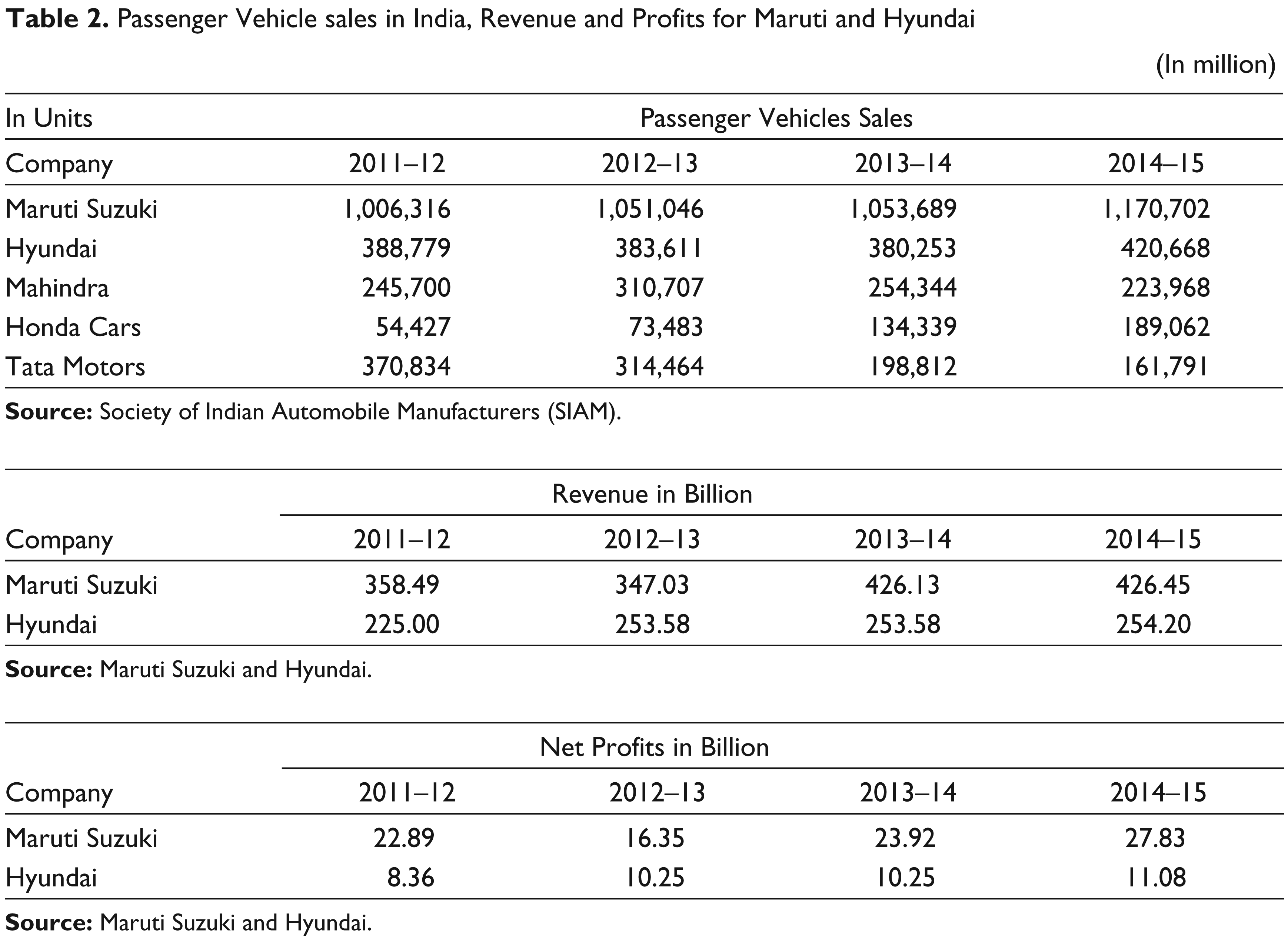

After the delicensing of the car industry in 1993, many companies entered India (from 1995 onwards) like General Motors’ Opel Astra, Honda City, Daewoo Motor’s Cielo, Mitsubishi Lancer and Ford Escort. However, none of them understood the Indian consumer and cracked the India code as well and as fast as Hyundai did (see Table 2). Hyundai benefited from a fierce battle in the 1990s between Japan’s Suzuki Motor Company and the Indian government for control of Maruti. Due to the tussle, Maruti did not launch a new car between 1994 (Esteem) and 1999 (Baleno), and it also delayed the launch of Wagon R till 2000.

Passenger Vehicle sales in India, Revenue and Profits for Maruti and Hyundai (In million)

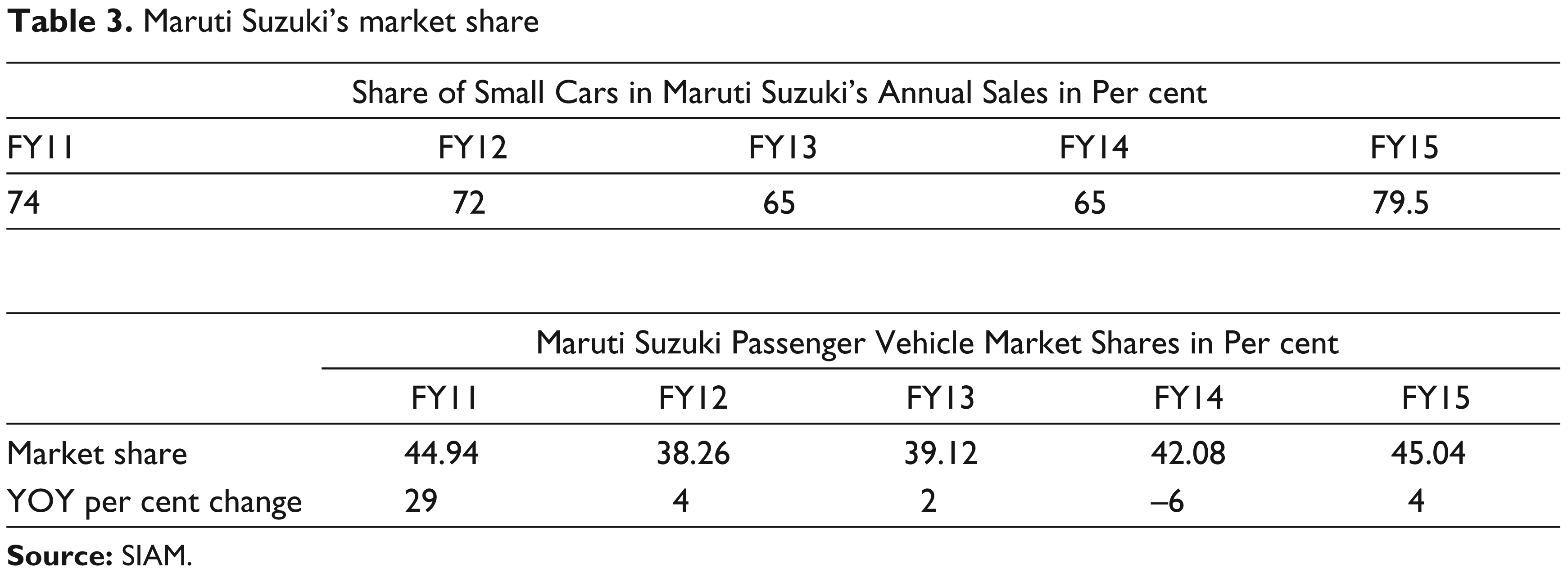

Maruti Suzuki’s market share

Hyundai took advantage of this and emerged as the major, real challenger for the reigning Maruti Suzuki. For Hyundai, the Grand i10 had established itself quickly by selling more than 100,000 models in 2014. The i20 had started to slow down, but it got a boost with the Elite version. The compact sedan Xcent which replaced the Accent sold 51,600 models in 2014. The sale of Verna had slowed down, but Hyundai refreshed it again to boost it up. For Maruti Suzuki, the Swift and DZire that were its sedan variant did tremendously well selling over 400,000 models in 2014. The new Celerio was selling well, and the Wagon R maintained its space (see Table 3). Ciaz by Maruti presented a challenge to Hyundai’s Verna to which Hyundai responded by a refreshed Verna. Hyundai planned to compete with Maruti’s Ertiga which was doing well in the small multi-utility segment, and both were looking to enter the compact and urban sports utility vehicle (Sinha, 2015). The battle was only heating up.

Evolution of Indian Automotive Industry

The growth was relatively slow between the 1950s and 1960s due to nationalization and the license raj, which hampered the Indian private sector. After 1970, with restrictions on the import of vehicles set, the automotive industry started to grow, but the actual acceleration came from the manufacturing and selling of tractors, commercial vehicles and scooters, as cars were still considered as a major luxury item at that time. In the 1970s, price controls were finally lifted, inserting a competitive element into the automobile market.

By the 1980s, the automobile market was dominated by companies such as Hindustan Motors and Premier, which sold superannuated products in fairly limited numbers. During this time, only a handful of competitors began to arrive on the scene.

In 1986, to promote the auto industry, the government organized Delhi Auto Expo to showcase how the Indian automotive industry was absorbing new technologies, promoting indigenous research and development and adapting these technologies to the rugged conditions of India. 2

Liberalization

Eventually, multinational automakers such as Suzuki and Toyota of Japan and Hyundai of South Korea were allowed to invest in the Indian market, furthering the establishment of an automotive industry in India. Maruti Suzuki was the first and the most successful among these new entries, and in part the result of government policies to promote the automotive industry establishment beginning in the early 1980s. As India began to liberalize its automobile market in 1991, some foreign firms also initiated their joint ventures with existing Indian companies. The variety of options available to the consumer began to multiply eventually in the 1990s. By 2000, there were twelve large automotive companies in the Indian market, most of which were offshoots of global companies (Kamboj, n.d.).

Hyundai Story in India

Hyundai Motor India Limited (HMIL) was formed on 6 May 1996, which was a wholly owned subsidiary of the Hyundai Motor Company of South Korea. At that time, the Hyundai brand was practically obscure in India, and there were just five noteworthy vehicle manufacturers in India, and they were Maruti, Hindustan, Premier, Tata and Mahindra. 3

HMIL’s first launch was the Hyundai Santro which was on 23 September 1998, and it did spectacularly well. Buoyed by the early success, HMIL launched Hyundai Accent in 1999. Both Santro and Accent secured top positions in JD Power Asia Pacific 2001 Initial Quality Study (IQS) and Automotive Performance Execution and Layout (APEAL) studies and HMIL started exporting both in large quantities. Soon HMIL turned into the second biggest auto producer and the biggest vehicles exporter in India in a few months. 4 In 2000, the sales of Santro crossed 100,000, and soon HMIL launched a different version of Santro called Santro Zip Drive and the next year, a new-look Santro. In 2001, HMIL also entered the luxury car segment by launching luxury sedan Sonata.

For HMIL, the success continued as it rolled out the 200,000th car in thirty-two months and the 350,000th car in fifty months. Accent was ranked number one in APEAL for the second time in a row, and Santro topped both IQS and APEAL for the third time in a row. It soon launched different versions of Santro (Automatic transmission and Santro Xing), Sonata (2.7 V6) and Accent (CRDi, VIVA) besides a premium SUV, Terracan. 5 By that time, it had also won a lot of awards.

By 2004, Santro became the largest single selling brand in India across segments with 12,061 units and HMIL also exported 1 00,000 vehicles and became the largest exporter in the industry. It did not stop there and continued launching new cars over the next year (Getz, Elantra, SUV—Tucson). It came up with different versions of the existing cars (Accent Viva CRDi, Getz-GLE, Sonata Embera and Santro Xing with eRLX technology). 6

In 2007, HMIL came up with another trump—the i10 which received tremendous reception and was awarded by many as the ‘Car of the Year 2008’. On the back of its success, HMIL launched the premium hatchback i20 the following year. The i20 also won many awards and both i10 and i20 achieved tremendous sales.

In 2010, HMIL became the first car organization in India to accomplish the export of one million cars in a little more than ten years. It also launched the successful Santa Fe SUV in 2010, New Fluidic Verna in 2011 and Neo Fluidic Elantra in 2012. 7

As of 2015, HMIL exported cars to more than 120 nations in Asia, America, Latin America, EU, Africa, Middle East and Australia. It had also been the biggest Indian exporters of cars for eight years in a row (Saad, 2013).

Changing Dimensions and Perspective of Indian Government on Indian Automobile Sector

The battle of the two automobile giants in the Indian automobile sector was also being influenced by the policies of the government. The Union Budget 2015 was a mixed one in terms of reviving the automobile sector. The following were some of the policy initiatives along with ‘Make in India’ campaign that showed the changing dimension and perspective of the Indian government on Indian automobile sector which would impact HMIL.

Excise Duty Cut

In the February 2014 interim budget, the previous United Progressive Alliance (UPA) government slashed the excise duty for SUVs to 24 per cent from 30 per cent; for mid-sized cars, the government slashed the excise duty to 20 per cent from 24 per cent and to 24 per cent for large cars from 27 per cent earlier. The government hoped to boost the sector, which was struggling due to the economic downturn. In June 2014, the new government led by Prime Minister Narendra Modi extended the excise duty concessions till December 2014. In the interim budget, however, it was withdrawn from January 2015 and the excise duty hike affected demand because of a 4–6 per cent price increase across passenger vehicle categories.

Customs Duty

Fully imported cars attracted a customs duty in excess of 125 per cent. In the budget, the customs duty on commercial vehicles was increased from 10 to 40 per cent. This move by the government was made mainly for benefiting domestic CV majors, such as Tata Motors and Ashok Leyland etc., forcing others to consider opening manufacturing units in India.

Lower Interest Rates

Over 80 per cent of the vehicles purchased in India were purchased with financing from banks and other institutes, according to a business world report. The focus of the government was on reducing the bank rates which in turn would reduce the vehicle loan costs, thereby, encouraging the customers to purchase two-wheelers and four-wheelers. Consequently, this led to improved demand for the sector and higher sales for both the companies as well.

Introduction of GST

As per the demand of the auto industry, the government said that the GST would come into effect from April 2016. The introduction of the proposed GST would help the auto manufactures to boost their sales (Yogi, 2014).

Besides this, appropriate implementation of the recommendations of the seventh pay commission on salaries of the employees of the state and central government employees would result in an increase in automobile sales in double digits, especially the compact hatchback and mini segment. After implementation, almost 20 per cent of state government and 25 per cent of central government employees would become eligible car buyers with a salary of B40,000 annually (Ghosh, 2015).

Maruti would benefit the most from this as it had many offerings in the entry level segment like Swift, Wagon R, Alto and Celerio. Hyundai could register more sales with its i10 and Eon.

‘Make in India’ Campaign

The policy initiative of the Indian government ‘Make in India’ was for the Indian manufacturing industry that contributed nearly 22 per cent to the country’s gross domestic product. It was expected to benefit the automobile sector.

The primary focus of the ‘Make in India’ campaign was on the infrastructure which was a major driver of growth for the auto industry. This campaign was expected to give a major boost to public policy making and planning that was, in turn, likely to boost demand in the automobile sector which would benefit both Maruti Suzuki and Hyundai.

The second focus of the ‘Make in India’ campaign was on reforms. There were many strikes due to outdated labour laws, and it was the flash point for automotive companies and the labour force. Maruti Suzuki was particularly affected by it as seen in 2011 when workers went on a two-week strike. Introducing a new bankruptcy law, labour law, announcing a roadmap to lower corporate taxes and other such actions were clearly directed towards making India more competitive in business and effective in taking care of such issues.

The third focus of the ‘Make in India’ campaign was the ease of conducting business. This would certainly go a long way in assisting automotive companies especially the component suppliers looking to set up their research and development (R&D) centre or offshoring centres in India. Apart from boosting the innovation quotient of Indian suppliers, this would help in promoting R&D investment in the sector (Verma, 2015) and both Hyundai and Suzuki were keen to set up an R&D base in India.

The policies of the government and the campaign presented a scope for faster growth, and if Hyundai capitalized on this opportunity better, it could reduce the gap with Maruti Suzuki.

Hyundai Versus Maruti Suzuki

The biggest competition in the Indian auto industry had been between Maruti Suzuki and Hyundai. This competition had been there for quite a while, and both firms had been forceful in their methodologies towards the business.

In the 1980s, Maruti had no real competition in India, and it did not even have to market its products. There were long waiting lists, and they made more than half of their cars in white, thus saving costs. Once Hyundai entered, it started focusing on quality, customer care and service. It talked about its technology like MPFI which emitted lesser emission and met Euro norms as against to Maruti’s carburettors. The Supreme Court forced Maruti to accept the Euro norms and Maruti incurred costs as well as some loss of reputation. Hyundai continued setting the agenda when they talked about Santro’s Zip Drive version which was the first small car with a power steering. Hyundai also advertised that Maruti’s Alto and Wagon R were four-seaters as they only had two rear seat belts whereas the Santro had three in the back making it a five-seater. Hyundai again proved that it was more aggressive as in March 2011 as it obtained an innovative design philosophy with Verna calling it fluidic sculpture and promoted it. Maruti, on the other hand, had a new design philosophy in 2005 from the Swift, and henceforth, its cars were curvier, muscular and sporty, but it did not promote these changes. Hyundai followed Maruti everywhere. Maruti tied up with the State Bank of India (SBI) to offer unique packages to its buyers and soon Hyundai also had its tie-ups. Maruti began focusing on the rural markets in 2009 and Hyundai too started it in 2011 (Sinha, 2015).

Hyundai’s Market Share

At its peak, Maruti Suzuki controlled 70 per cent of the Indian market. Almost twenty years after that, Maruti had a car market share of nearly 52 per cent, whereas Hyundai had 22.32 per cent and Honda Cars had 8.4 per cent (see Table 4). Maruti focused on price and compact size, whereas Hyundai went after the value.

There were various similarities between Hyundai and Maruti Suzuki. First, both were the backups of the organizations situated in Southeast Asia, which was one reason for why they had a stunning comprehension of the economic situations. Furthermore, both organizations produced high incomes from their individual models in the hatchback section. Finally, Maruti Suzuki and Hyundai had colossal brand values in the nation and were trusted by the shoppers. 8 Mainly, both of the heavyweight auto creators were set against one another for matchless quality in the small auto segments that collected a tremendous lump of volumes in the 2 million Indian auto markets.

Eon, the small auto offering from South Korean carmaker, was reckoning some solid rivalry from Alto 800, Maruti’s offering, that got more than 40,000 bookings in the first month of dispatch and immediately after that the media battles started (Chauhan, 2012). Hyundai Motor started its marketing campaign ‘Trendsetter V/s Follower’ claiming that their small car Eon was much superior to the newly launched Alto 800 from its arch-rival Maruti Suzuki. While Maruti had yet to react, Hyundai was quick to advance the benefits of its cars.

Hyundai, however, also suffered a setback when the Competition Commission of India (CCI) penalized Hyundai for B4.2 billion as it was found guilty of unfair trade practices. It was found that it was involved in anti-competitive practices, for instance, not making the genuine spare parts available in the market freely. 9

Marketing Strategies of Hyundai Motors India

Product Portfolio

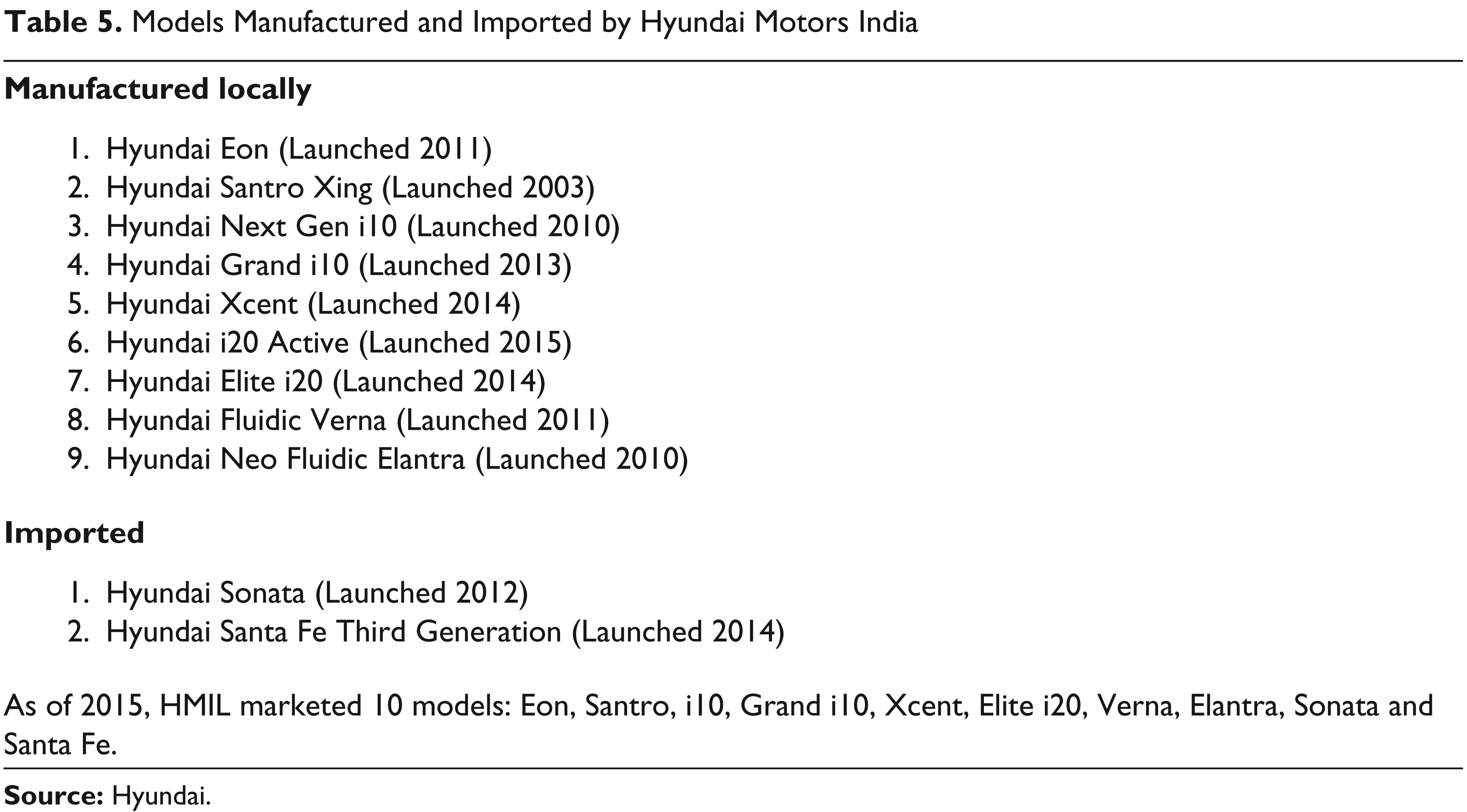

To make its product portfolio strong, HMIL planned to bring models in divisions where it was not present. ‘The company will roll out one completely new product in every segment we are not present in the next two years apart from refurbishing and face-lifting existing products,’ said Rakesh Srivastava, senior vice president and division head, marketing and sales division. 10 Hyundai was not present in the multi-purpose vehicle division and had been offering the Santa Fe SUV as a totally assembled unit. For the hatchback fragment, they had Santro, Eon, i10, i10 Grand and Elite i20. In the sedan division, it had Elantra, Xcent, Verna and Sonata (see Table 5).

Models Manufactured and Imported by Hyundai Motors India

Publicity and Social Media

Hyundai paid particular attention to social media. They focused on correspondence, engagement, and building long-term relationships with its customers and fans in innovative ways and keeping with its brand values. Hyundai first started their social presence through facebook and spread to all mainstream social spaces. This helped Hyundai with its customer relationship management (CRM) especially the ‘relationship’ part of the CRM.

Target Customer Segment

Over the years, India’s demographics had changed, and the average age of the car buyer had come down radically. With plenty of chances for the young people coupled with the change in attitudes towards life as well as access to funds, the purchasers were in the range of twenty-five to thirty-two years. 11 Hyundai identified this range and reached out to them on social media.

Focus on Domestic Market

To become the leader in the compact car segment, Hyundai started focusing more on the domestic market instead of exports. Exports generated scale and benchmarked the quality of its products, but the demand from the domestic market increased, and the company stopped exports to many European markets. They came up with a new tagline, ‘new thinking new possibilities’, and their strategy included more comfortable and easy to drive localized products.

New Design and Technologies

With an intention to increase sales, Hyundai bet on its new idea of ‘Fluidic Design’. The objective was to make its cars more advanced, sporty and sophisticated by taking ideas from its worldwide brands. Hence, Elite i20 was based on the fluidic idea designing it in such a way that it was pleasing to the eye (Narasimhan, 2014).

Marketing Strategy of Maruti Suzuki India

Product Portfolio

Maruti Suzuki had come up with Kizashi Premium Sedan and Grand Vitara SUV in an effort to enter the premium segment, but it did not work out. The company then planned to gradually go up the segments by initially focusing on small SUVs and mid-size Sedans. Ciaz, which was a mid-sized Sedan, was doing well, while YRA, which was a hatchback bigger than Swift, was also going to be launched in 2015. Maruti Suzuki was also looking to launch greater SUVs and MPVs keeping in mind the end goal to have a full portfolio over all segments.

New Technologies

Keeping in mind that the young and first-time buyers were increasing, Maruti Suzuki also focused on new innovative technologies. It started with the automated manual transmission in Alto K10 and Celerio. Maruti Suzuki also planned to present smaller 800 cc fuel-efficient diesel motors, systems with a start-stop mechanism, petrol engines which would be turbocharged and new elements like entertainment systems for the car which would be touchscreen (Bhattacharya, 2015).

Research and Development

In addition to new technologies, Maruti Suzuki was also making significant investments in research and production capacity. It already had the capacity to produce around 1.4 million cars annually at its two plants in Haryana, yet it also started building a huge factory in Gujarat to add 1.5 million more to its capacity (Bhattacharya, 2015).

Distribution Network

Maruti Suzuki’s biggest plus was its distribution network. It had around 1,500 dealers spread across most of the districts in the country (Bhattacharya, 2015). Its touch points were almost double than its nearest rival, and it could reach almost every potential customer in the country.

Challenges for Hyundai Motors India

Hyundai had a lot of catching up to the leader Maruti Suzuki. Hyundai sold around 30,000–36,000 units per month, whereas Maruti Suzuki sold 85,000–90,000 units per month (Narasimhan, 2014). Maruti also planned to bring out four new models which could increase the gap along with Ciaz and the mid-range Sedan.

Considering the future demand, the production capacity of Hyundai seemed inadequate. In 2014, it had a production capacity of 0.63 million units in a year which could be increased to 0.68 million units. Hence, it needed to have a second plant to increase production capacity.

Compared to Maruti Suzuki, Hyundai had less number of service centres and workshops in India. Therefore, it had to work substantially hard in its customer service segment.

In terms of the different variants and model type, Maruti held an upper hand, the greatest example of which was the recent addition of a significant utility vehicle to its portfolio—Ertiga. However, when it came to Hyundai, it mainly focused on passenger cars and not on other vehicle types like Maruti.

Another aspect where Hyundai lagged behind Maruti Suzuki was its dealership network. Hyundai had 400 dealerships and around 270 rural deals outlets and 1,000 service centres over India in 2014. In comparison, Maruti had around 1,400 business outlets, of which almost half were situated in rural areas (Narasimhan, 2014).

Road Ahead for Hyundai Motors India

Hyundai, with an aggressive strategy, was countering all of Maruti Suzuki’s moves. In response to Maruti Suzuki’s offering of Swift, Hyundai launched the global hatchback Grand i10 and as a response to Alto K10, it launched Eon and the cutting edge i20.

The small car segment had sales of 1.41 million autos in financial year 2013 (FY13) and it comprised 52 per cent of the general passenger vehicle market in India. In that, Hyundai had around 22 per cent share. However, it anticipated it to grow further with new models. Hyundai also planned 8–10 launches in the next three to four years in India like a SUB-4 meter Sedan, a multi-purpose vehicle to tackle Maruti’s Ertiga, a compact SUV and its flagship saloon Genesis (Thakkar, 2013).

For Hyundai, rural markets were the key to growth. Even when the demand from the urban markets had slowed down, the rural market sales were growing. The share of Hyundai’s rural sale increased from 12 per cent in 2011 to 20 per cent by August 2014. Hyundai had increased its rural sales outlets to 320 over the last few years (Sasi & Singh, 2014). They provided service and repairs besides offering models like Santro and Eon. It planned to increase its rural sales to around 30 per cent of its total sales in few years.

As of 2015, Maruti Suzuki was ahead of Hyundai in terms of market share. It remained to be seen whether Hyundai’s strategies would be fruitful, and if the company could capitalize on the opportunity presented by the government policies and campaign to eventually overtake Maruti Suzuki.