Abstract

This case revolves around the acquisition of Bhushan Power and Steel Ltd (BPSL) by JSW Steel Ltd BPSL faced severe financial difficulties, prompting its lenders, including prominent Indian banks, to initiate insolvency proceedings under Section 7 of the Insolvency and Bankruptcy Code in 2019. JSW Steel Ltd entered the competition to acquire BPSL’s assets and secured the bid. However, complications arose as the Enforcement Directorate and BPSL’s promoters raised objections, leading to delays in the insolvency process.

The case spotlights a significant Indian corporate reform represented by the Insolvency and Bankruptcy Code and the establishment of the National Company Law Appellate Tribunal (NCLAT). This reform proved essential as it provided an alternative to distressed companies, which previously had no choice but to cease operations, adversely affecting both employees and lenders. The NCLAT has since introduced a win-win solution for most stakeholders.

Furthermore, the case delves into the crucial characteristics of the steel industry, an indispensable product utilized across various global industries, and how these features significantly impact strategic decision-making. It underscores the strategic value of JSW Steel Ltd’s acquisition of a struggling company. In summary, it offers a comprehensive perspective on the insolvency process, the roles of the NCLAT and Enforcement Directorate, and the value generated through the acquisition.

Keywords

Discussion Questions

What major challenges did JSW Steel Ltd encounter during the acquisition of BPSL?

Can you share your insights into the competitive landscape within the steel industry, and do you have any comments on the Herfindahl Index’s relevance in this context?

Was the decision to pursue expansion the right strategic move for JSW Steel Ltd, and if so, why?

How would BPSL situation differ if the Insolvency and Bankruptcy Code (IBC) had not been implemented or if the NCLAT had not been established?

What were the key benefits that JSW Steel Ltd aimed to achieve through the acquisition of BPSL?

What were the primary factors causing the delays in the acquisition process?

Could you provide an explanation of debt restructuring, financial distress and the distress resolution process as they relate to this case?

Dressed in a suit that mirrored the hue of the cold-rolled steel sheets his company manufactured, Sajjan Jindal, India’s steel magnate, gazed out from his Bandra Kurla office. Jindal Mansion, his older and more opulent office adorned with exquisite artworks from around the world, at Peddar Road in Mumbai, was no longer sufficient for his steel empire. Hands in his pockets, a contemplative expression on his face, he observed the Mumbai skyline, reminiscing about his journey in the steel industry, which had commenced in 1984.

A newlywed and a young engineer, Jindal had relocated from Hisar in Haryana to Mumbai. He was entrusted with the responsibility of managing a small steel plant on the city’s outskirts owned by his father. The company, with a turnover of approximately ₹90 million, was operating at a loss. The plant incurred monthly losses in the millions, and Jindal was financially strapped. He recalled the modest cabin within the plant, where he spent nearly 15 to 18 hours daily, and where he had dared to dream of becoming India’s foremost steel producer. His ambitions were scoffed at by his father, who refused financial assistance.

In 1993, following India’s embrace of liberalization, Jindal approached Mr N. Vaghul, the then-chairman of ICICI Ltd As a nervous young entrepreneur with a vision to reach new heights, he sought to persuade Vaghul to fund a two-million-tonne steel plant in Vijaynagar, Karnataka, a cumulative capacity that Tata Steel (India’s largest private steel company at the time) had taken 90 years to achieve. The memory of his unwavering determination came flooding back. The passion that had fuelled him was unrelenting and all-encompassing.

The establishment of the Vijaynagar plant in Karnataka had been a turning point, and from that moment on, he had never looked back. The journey had been anything but easy, but sheer determination and tireless effort had brought him to his current position. His flagship company, JSW Steel Ltd, had held the position of the second-largest private-sector steel producer in India, but that was about to change. As he pondered this, a confident smile, characteristic of his resolute nature, graced his lips, as he internalized the realization that he was on the cusp of becoming India’s largest steel producer. In the midst of this moment of reflection, he received unexpected news that the Enforcement Directorate (ED) had intervened, potentially thwarting his plans.

In August 2018, JSW Steel Ltd proposed a resolution plan of ₹197 billion to acquire the struggling Bhushan Power and Steel Ltd (BPSL). This plan finally received approval from the National Company Law Appellate Tribunal (NCLAT) in September 2019. However, on 23 November 2019, a significant setback occurred when the ED arrested Mr Sanjay Singhal, the chairman of BPSL, on money laundering charges. They also seized approximately ₹4 billion worth of BPSL’s assets, thus challenging the NCLAT’s approval. Consequently, the NCLAT suspended the acquisition process. At this point, Mr Jindal’s aspiration of becoming the largest steel manufacturer in the country hung in the balance.

The Steel Industry in India and the World

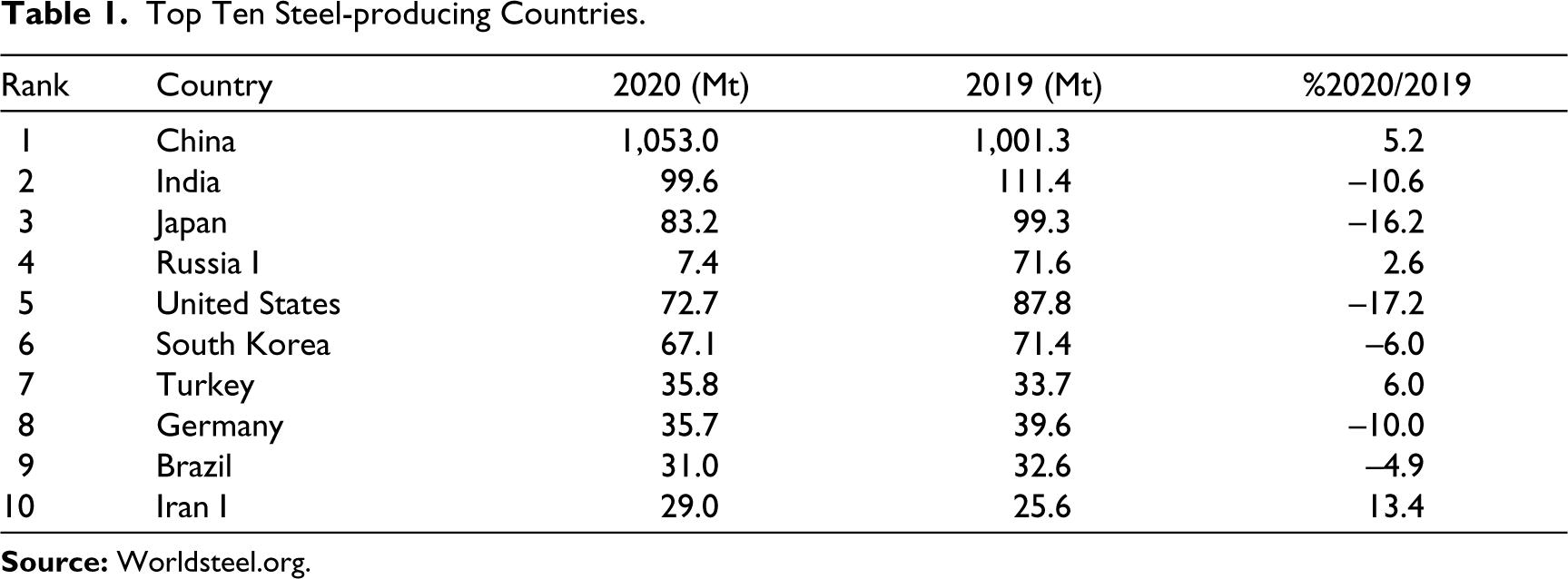

The Indian steel industry held a significant position in the global steel sector, producing approximately 111 million tonnes of steel in 2019. However, there was a notable decline in 2020, falling to about 99.6 million tonnes, marking a drop of over 10 per cent. Exhibit 1 provides insights into the production capacity of the top 10 Indian steel companies.

India occupied the second position in global steel production, trailing only behind China, which accounted for nearly 56.5 per cent of the world’s total steel output (Worldsteel Association, 2021b). Nevertheless, by 2021, India’s share of global steel production had been reduced to approximately 6 per cent. This decline was in contrast to India’s favourable conditions, including abundant high-grade iron ore reserves, cost-effective labour, a readily available supply of affordable coal and supportive government policies, which rendered Indian steel companies competitive on the global stage.

As seen in Table 1, the top ten steel companies globally contributed to a total steel production of approximately 504 million tonnes in 2020, which accounted for roughly 27 per cent of the worldwide steel output. In contrast, the top three iron ore companies were responsible for producing approximately 44 per cent of the world’s total iron ore consumption.

Top Ten Steel-producing Countries.

According to data from the Worldsteel Association in 2021, approximately 52 per cent of the total steel produced worldwide was utilized in the construction and infrastructure industries. The global construction sector was projected to reach a value of $10.5 trillion by 2023, with a consistent compound annual growth rate (CAGR) of around 4.2 per cent. China, India, the USA, Indonesia and the United Kingdom were anticipated to emerge as the top five construction markets globally by 2030 (Construction Placements, 2020).

India’s consumption of finished steel experienced substantial growth, with a CAGR of 5.2 per cent, reaching 100 million tonnes between 2016 and 2020. This figure is projected to surge to 230 million tonnes by 2030–2031 (IBEF, 2021).

Estimations indicated that the world’s population, standing at about 7.7 billion in 2019, would increase by an additional 2 billion people by 2050, with a significant portion expected to reside in urban areas (Worldsteel Association, 2021a).

As of 2021, the USA boasted the world’s largest construction industry, valued at approximately $1.4 trillion, although the largest construction companies were headquartered in China and Europe. The automobile sector ranked as the second-largest consumer of steel worldwide, with around 83 million tonnes of steel used in 2019, producing roughly 91.8 million vehicles (Worldsteel Association, Steel in Automotive, 2021).

Steel: The Material

Steel stood as the most pivotal component in global construction and engineering, finding utility in nearly every facet of human existence. From homes, cars, dams and bridges to utensils, electrical and mechanical appliances, medical equipment and tools, steel’s versatility knew no bounds. The world boasts over 3,500 diverse types of steel, each endowed with unique physical, chemical and environmental properties. Adding to its allure, steel is entirely recyclable, exhibits exceptional durability and requires less energy for production compared to other metals. An exceptional attribute of steel is its unchanging properties, even through multiple recycling cycles, earning it the distinction of being a permanent material in the circular economy, as acclaimed by Wordsteel.org. Wordsteel.org introduced four futuristic ₹for steel: reduce, reuse, remanufacture and recycle (Circular Economy, 2022), forming the basis of its circular economy approach.

Reduce: The steel industry made significant strides in reducing the material, energy and resources required for steel production over the years. The weight of steel in various products had seen a substantial decrease. The last five decades have witnessed the development of advanced ultra-high-strength steel grades, reducing the weight of many steel applications by as much as 40 per cent. Between 1960 and 2020, the energy consumption per tonne of steel production decreased by a remarkable 60 per cent, even as overall steel production escalated by nearly 500 per cent during the same period.

Reuse: Steel had exceptional recyclability for reuse from old structures or machinery, either for the same purposes or in similar applications. By-products of steel production, such as slag, were utilized in the production of cement, fertilizer, road stone and asphalt. Dust, another by-product, could be harnessed for the extraction of zinc and iron. Process gases emitted during steel manufacturing were repurposed for generating heat and electricity. Further, by-products of steel served as raw materials for the production of plastics, paints and more.

Remanufacture: In the context of the circular economy, products that had ceased functioning optimally were refurbished to a condition akin to new, a process referred to as remanufacturing. Steel played a pivotal role in this practice, with various steel products, including construction and agricultural machinery, truck and car engines, electrical motors, domestic appliances and wind turbines, undergoing remanufacturing. This approach capitalized on the durability of steel components, preserving the energy invested in their creation.

Recycle: The exceptional recyclability of steel allowed it to be reused infinitely without compromising its properties, contributing significantly to the conservation of raw materials. Steel’s innate magnetic properties facilitate its separation in recycling processes. This gave rise to the creation of new employment opportunities in industries related to scrap collection, separation and recycling.

One intriguing aspect of steel was that, despite being a time-honoured industry, it lacked viable substitutes (Banerjee, 2013). While aluminium came closest, it was three times more expensive than steel. The automotive sector, a major consumer of steel products, had begun substituting steel with aluminium due to its lighter weight, which reduced overall vehicle weight and improved fuel efficiency. However, this transition also came at an increased cost. Meanwhile, the construction industry, the largest consumer of manufactured steel worldwide, had yet to identify a cost-effective, lightweight, recyclable and reusable alternative to steel. Other materials, such as polymers, concrete and engineered wood, could only partially replace steel in various applications.

JSW Steel

JSW Steel Ltd (JSWSL) served as the flagship company of the JSW Group, 1 a prominent conglomerate in India. By 2020, JSW Steel had attained the largest steel portfolio in the country, with exports reaching approximately 100 countries across five continents.

JSW Steel began its humble venture into steel with a single plant in Vasind, near Mumbai in 1982. Subsequently, it acquired Piramal Steel Ltd in Tarapur, Maharashtra, renaming it Jindal Iron and Steel Company Ltd (JISCO) in the same year. Over the next two decades, Jindal Steel underwent a remarkable transformation, marked by numerous acquisitions and ambitious expansion plans.

In 1994, Jindal Vijaynagar Steel was established in Toranagallu, Bellari, Karnataka. It was a huge project sprawling across 10,000 acres of land in the high-grade iron-ore belt of Karnataka, strategically positioned near the ports of Goa 2 and Chennai. 3 In 2005, JISCO and the Jindal Vijaynagar Steel Plant merged into one entity. Another significant addition to its assets was the acquisition of Salem Steel, a specialty steel plant with a capacity of 1 million metric tonnes per annum, located in Salem, Tamil Nadu, in the same year. This plant was known for producing nearly 850 steel grades.

In 2006, JSW Steel acquired mining assets in Mozambique (Kalesh, 2006), followed by a joint venture in 2007 with Geo Steel LLC, a steel producer based in Georgia (JSW Steel and Geo Steel to Set up JV in Georgia, 2007). This partnership led to the construction of a new $42 million bar mill in Rustavi, Georgia, with an annual capacity of 175,000 million metric tonnes per annum of rebar. This expansion enabled JSW Steel to broaden its market presence and cater to demand in countries such as Georgia, Armenia, Azerbaijan and Russia.

One of the company’s most notable acquisitions was ISPAT Industries. JSW Steel acquired a majority stake in ISPAT in 2010 and subsequently merged the company into JSW Steel in 2012. This move solidified JSW Steel’s position as one of the country’s largest steel producers, boasting an annual capacity of approximately 14.3 million metric tonnes per annum (Subramani, 2010).

In 2010, the company expanded its reach to the United States by acquiring mining assets through the purchase of United Coal, a West Virginia–based company (JSW Steel Eyes United Coal Company of US - The Economic Times, 2008). Further international collaborations were formed, including a technical tie-up with JSE Corporation of Japan in 2013 to manufacture high-grade automobile steel (JSW Steel Rallies on Technical Tie-up with Japan’s JFE Steel Corp, 2013).

JSW Steel continued its expansion with the acquisition of Welspun Maxwell Ltd, a plant with a capacity of 900,000 tonnes, situated near the Dolvi plant in 2013 (Sanjai, 2014). The company also secured mining licences for 1,200 acres of magnetite-rich iron ore lands in the Atacama region of Chile the same year (JSW Gets Mining Rights in Chile for $52 Million, 2013).

Over the subsequent years, JSW Steel added to its portfolio with the acquisition of Vardhman Industries Ltd (2019), Monet Ispat and Energy Ltd (2018) and Acero Junction in the USA (2018). In Italy, JSW Steel acquired a steel group comprising three companies: Aferpi, Piombino Logistics and GSI Lucchini (JSW - JSW Steel Acquires Facilities at Piombino, 2021; JSW Steel Completes Acquisition of Vardhman Industries for ₹63.50 Crore | Business Standard News, 2019; Mazumdar, 2018). By 2020, JSW Steel boasted state-of-the-art plants located in Karnataka, Tamil Nadu, Maharashtra, West Bengal, Italy and the USA, with a collective capacity to produce 18 million tonnes of steel per annum.

The following timeline covers the history of the firm ( 1982: Jindal Group sets up a steel plant at Vasind, near Mumbai. 1982: Acquires Piramal Steel Limited (later renamed JISCO). 1994: Sets up Jindal Vijayanagar Steel Ltd (JVSL). 2004: JSW acquires Salem Steel Works. 2005: JISCO and JVSL merge to form JSW Steel Ltd. 2008: JSW Steel enters the rebar JV in Georgia. 2010: Acquires integrated steel plant at Dolvi, Maharashtra. 2013: Ties up with Japan’s JFE in electrical steel JV. 2014: Acquires Welspun Maxsteel in a deal valued at ₹10 billion. 2018: Buys a 100 per cent stake in Italy’s Aferpi for €55 million. 2018: Signs a JV agreement with JFE for Indian auto steel production. 2018: Invests $150 million in the first tranche for a greenfield Texas plant. 2019: NCLT approves JSW’s takeover of bankrupt Bhushan Power. 2019: Announces the sale of a significant stake in Geo Steel. 2020: Emerges as the preferred bidder for three iron ore mines in Odisha. 2020: NCLAT grants JSW immunity in the acquisition of Bhushan Power. 2020: JSW’s purchase of Bhushan Power was challenged in India’s top court. 2020: Agrees to buy the remaining 26.45 per cent stake in JSW Vallabh Tinplate. 2020: Purchases the remaining 31 per cent stake in Italy’s GSI Lucchini. 2021: Completes the purchase of Bhushan Power & Steel Ltd. 2021: JSW Steel Italy acquires a 31 per cent stake in GSI Lucchini. 2021: Sets a CO2 target of 1.95 tonnes per tonne by fiscal year 2030. 2022: Puts Piombino long-product business in Italy up for sale.

The Dolvi plant, situated approximately 100 km from Mumbai, featured an impressive 3.5 million tonnes per annum capacity, equipped with a state-of-the-art modern blast furnace installed in 2016. JSW Steel has always been at the forefront of technology adoption. During the replacement of the old furnace at the Dolvi plant, the company sought guidance and consultation from Nippon Steel, a Japanese steel giant. The result was not only a replacement of the old furnace within a minimal shutdown period of just 90 days but also a remarkable 75 per cent increase in the furnace’s capacity. The second such furnace at Dolvi was inaugurated in 2020.

The Vijaynagar Steel plant in Karnataka, conceived in 1993, had evolved into a world-class facility with a production capacity exceeding 12 million metric tonnes per annum by 2021. Nestled in the Bellari–Hosapete iron ore–steel belt and sprawling across an expanse of 10,000 acres, this plant was renowned for its exceptional cost-efficiency. It featured one of India’s largest blast furnaces and boasted an impressively low carbon footprint. An astounding 96 per cent of the coke oven gas used for power generation within the plant was being recycled, further underscoring its commitment to sustainability. Technologically, it was recognized as one of the most advanced steel plants in India.

JSW Steel’s product portfolio encompassed flat steel products, including hot-rolled coils, plates and sheets, cold-rolled coils and sheets, as well as colour-coated products for roofing and sheets. It held the distinction of being the largest producer of colour-coated products in India and also produced aluminium and zinc colour-coated sheets. JSW Steel stood as the largest manufacturer and exporter of galvanized steel in India, pioneering the supply of products with a higher coating of 550 gsm to the solar sector in the country.

Furthermore, JSW Steel secured the distinction of becoming the first licenced galvalume producer in India, employing technology from BIEC International, USA. This technology licence enabled the production of galvalume, a superior-quality alloy-coated product with applications in the construction and automobile industries. Galvalume boasts exceptional corrosion resistance and heat reflectivity, making it a valuable asset in various sectors.

JSW Steel also had a robust production line of long steel products, including TMT bars, wire rods and special alloy steel. Their TMT bars adhered to quality standards prescribed by India, America, Great Britain and Australia. The company marketed its products under various brand names, showcasing a commitment to quality and innovation. These included JSW Everglow for roofing technology, JSW Colouron+ and JSW Pragati for colour-coated roofing sheets, JSW Vishvas+ for colour-coated aluminium–zinc sheets and JSW Galvos for premium galvalume products, among others.

By 2021, JSW had evolved into one of India’s fastest-growing conglomerates, expanding its interests beyond steel to encompass the infrastructure, cement and energy sectors. The JSW Group’s total valuation had reached approximately $13 billion in June 2021 (JSW Group - Amongst India’s Largest Conglomerates, 2022). Starting from its humble beginnings in the Indian steel industry, the group had gradually expanded its operations to South America, Africa and Europe. By 2021, it boasted over 16,000 retail outlets for its diverse product range and was actively exporting steel and other products to over 100 countries across five continents. The company’s key clientele spanned major industries, including construction, infrastructure OEMs, automotive and white-goods OEMs and MSMEs. Notable clients included Volkswagen, Maruti Suzuki, Toyota, Isuzu, the PSA Group, Morris Garages, BHEL, Crompton, Panasonic, Enercon, Bharat Forge, Laxmi Machine Works, Oriental Containers and many others. JSW Steel had strategically established mining assets in Chile, Mozambique and the USA. In 2018, the company’s acquisition of a plant in Piombino, Italy, further expanded its footprint in the European steel markets.

The company’s financial performance showcased consistent growth over several years, with profitability ratios trending upward until 2019 (JSW Steel Ltd Financial Balance Sheet, 2021). The details of the financial performance can be observed in Exhibits 2–4.

In 2020, JSW Steel encountered several challenges, largely exacerbated by the COVID-19 pandemic. Mr Sheshagiri Rao, the company’s representative, highlighted three main obstacles faced by JSW Steel in India, which revolved around liquidity, logistics and labour issues. Given that the steel industry was inherently capital-intensive, JSW Steel had a substantial debt burden. Leading banks and Life Insurance Corporation (LIC) of India were primary lenders to the steel sector, and the flow of credit to the industry had been dwindling. A significant contributing factor to this decline was the insolvencies of major steel giants like Bhushan Steel Ltd, Essar Steel Ltd and BPSL, among others.

JSW Steel had previously relied on borrowing from international markets through the issuance of external commercial borrowings (ECBs), bonds and even credit from customers. Consequently, the company had exposure to currency fluctuations and international interest rate risks. The steel sector, known for its capital-intensive nature, also demanded skilled labour. However, the lack of readily available skilled manpower and the non-return of labour after the COVID-19 pandemic presented considerable challenges for the company (Dutt & Dutt, 2020).

Bhushan Power and Steel Ltd

BPSL, founded by Brij Bhushan Singhal in 1970 and officially incorporated in 1999, was an unlisted company registered with the registrar of companies in Delhi. The company’s reins were later taken over by his elder son, Sanjay Singhal, who assumed the role of the majority owner and chairman after parting ways with the family business in 2011.

BPSL began its journey with a small steel plant in Chandigarh, primarily engaged in the production of door hinges and catering to a limited customer base. Over time, the company expanded its operations to various cities across India. Their product portfolio evolved to encompass railway track fasteners, followed by the manufacturing of Tor steel and iron rods at their Chandigarh facility. They established units in Kolkata, Thelkoloi in Odisha and Derabassi in Punjab.

In the years leading up to 2014, BPSL witnessed remarkable growth. The company diversified into manufacturing flat products, including coated products, galvanized aluminium products, colour-coated products, cold-rolled products, cable tapes and long products such as sponge iron and iron-making products. BPSL ventured into the production and marketing of steel pipes, grooved pipes, carbon steel tubes and hollow steel sections. Their product range also included hard-rolled coils, black pipes, galvanized iron pipes, galvanized plain sheets, galvanized corrugated sheets, direct reduced iron (DRI), billets, cold-rolled coils, precision tubes, tor steel, carbon wire rods and special alloy steel wire rods.

BPSL served a diverse array of industry verticals, including irrigation, agriculture, heating, ventilation and air-conditioning (HVAC), fire extinguishing, construction, including rectangle hollow section (RHS), square hollow section (SHS) and circular hollow section (CHS), gas and oil pipelines, automobiles, cement manufacturing, sugar mills, paper mills, steel companies, bicycle manufacturers, power projects and general engineering companies worldwide (Business Insider, 2019).

Notably, Bhushan Power and Steel’s profit surged from ₹7.11 billion to ₹18.14 billion in 2014, and their earnings per share (EPS) saw an increase from ₹19 to ₹33 over four years. As of 31 March 2020, BPSL reported a turnover of ₹86.35 billion, with approximately 5,800 employees working across their various factories (Dinesh, 2020a).

However, between 2007 and 2014, the directors of Bhushan Power and Steel embarked on significant borrowing from Indian banks and financial institutions, particularly from Indian public sector banks like the State Bank of India, Punjab National Bank, Canara Bank and Union Bank. Unfortunately, the borrowed funds were not always directed towards business growth, and the company started defaulting on interest payments on these loans. This financial turmoil was exacerbated by the global steel industry’s challenges following the 2008 financial crisis.

The demand for steel from China significantly declined after the 2008 Olympics. As global steel demand waned, the price of Indian steel took a nosedive. Steel, known for its cyclical nature, was typically financed through debt during prosperous times. However, when demand plummeted, debt became an overwhelming burden for companies. To manage this, some companies, including BPSL, resorted to borrowing fresh funds to repay existing loans. By 2012, the entire Indian steel industry was grappling with overdue interest payments. Nevertheless, substantial debt was not uncommon in the steel sector, with many major firms carrying significant debt loads. Additionally, the iron ore supply had been posing challenges due to government restrictions on mines in Karnataka and Goa since 2011 (Vyas & Babar, 2014).

Indian banks had been liberally lending to the steel sector since 2003, fuelled by the anticipation of a thriving Indian automobile sector. During this period, project financing gained momentum in India. Public sector banks in India frequently lent to high-risk projects (Chari et al., 2019; Varma, 2015). Promoters continued to expand their businesses with borrowed funds. The years 2009–2010 were marked by optimism in the Indian steel industry, and banks were eager to provide loans to companies like BPSL, which boasted impressive order books. Concerns about project viability and profitability were often overlooked, under the assumption that the steel industry would eventually thrive alongside the expected automobile sector boom. As the entire Indian steel industry grappled with financial strain, it was evident that companies resorted to borrowing from one bank to repay another. Indian public sector banks faced a dilemma: either acknowledge losses by curtailing lending or persist in lending, hoping for a sector turnaround (Sethi, 2017).

Banks in India portrayed themselves as victims in the larger non-performing asset (NPA) crisis that began in the mid-2000s. However, it could not be denied that banks shared responsibility for the NPA debacle, as they failed to adequately monitor projects and conduct thorough due diligence (Tayal, 2022). Indian banks adopted the practice of ‘evergreening’ loans, where old loans were rolled over into new ones, initially reporting low defaults but leading to a full-blown crisis in the long term.

In 2014, a consortium led by the State Bank of India once again sanctioned new loans to BPSL. Unfortunately, steel prices did not rise, and the company’s interest costs surged. Between 2014 and 2016, BPSL’s total debt increased by 30 per cent. The primary issue with the company was the urgent need for deleveraging. However, they achieved this by transferring debt to group companies and then converting it into equity for BPSL (Sethi, 2017). By 2018, the company had accumulated a debt of approximately ₹350 billion, and it was in a desperate situation that demanded drastic measures.

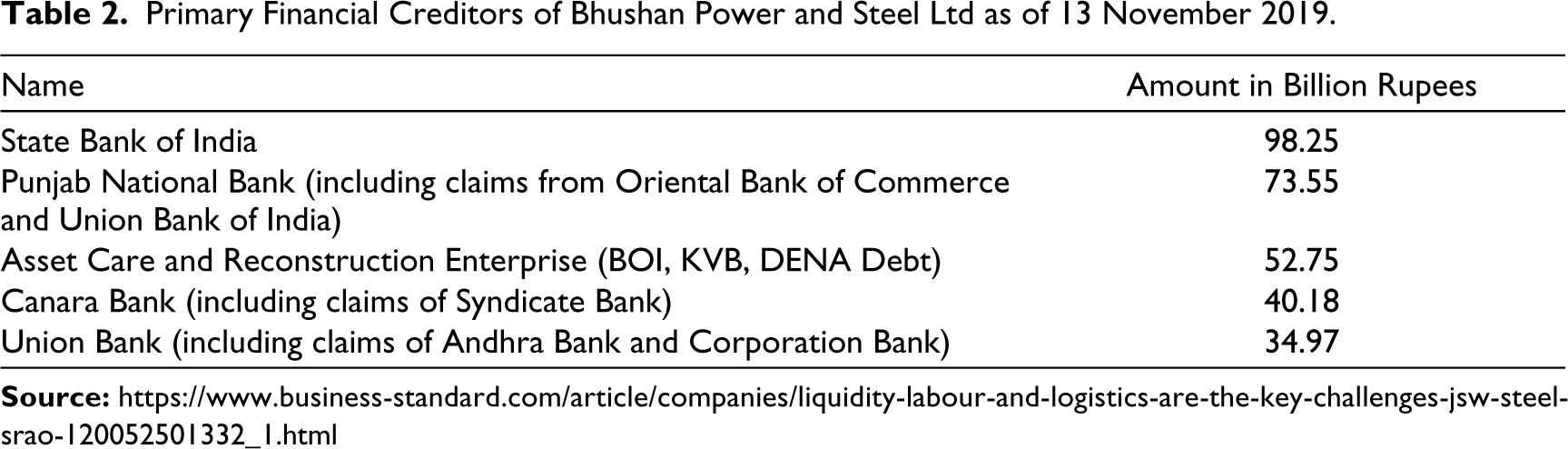

The Punjab National Bank was the first financial institution to assert its dues and initiate insolvency proceedings against the company in July 2019. Subsequently, other banks, including Bank of India, State Bank of India and Bank of Baroda, followed suit with similar claims. By the close of 2019, it was confirmed that the company had acquired loans amounting to approximately ₹472.04 billion from thirty-three different financial institutions. The company had failed to meet obligations totalling over ₹478.80 billion and was taken to the insolvency tribunal in July 2017. The annual turnover, as of the end of March 2020, stood at ₹86.35 billion, a decrease from the previous year’s ₹91.12 billion. For the fiscal year ending in March 2018, the turnover was ₹77.91 billion (Parmar, 2021). Table 2 depicts the list of banks and financial institutions that had lent money to BPSL.

Primary Financial Creditors of Bhushan Power and Steel Ltd as of 13 November 2019.

Sanjay Singhal found himself under arrest in a money laundering case where it was alleged that funds initially intended for expansion were diverted to around 200 shell companies and then funnelled back into the company as equity. This strategy allowed them to borrow larger amounts from banks (Business Standard, 2019; Dinesh, 2020b).

Insolvency Procedure and the Role of NCLT

The insolvency procedure against BPSL was initiated by the Punjab National Bank in 2019. The petition was filed under Section 7 of the Insolvency and Bankruptcy Code (IBC) of 2016. The NCLAT granted approval to the banks to commence insolvency proceedings against the company to recover the defaulted loans. Mr. Mahendar Kumar Khandelwal was appointed as the interim resolution professional (IRP) and directed the company’s management, officials and promoters to cooperate with him in the proceedings.

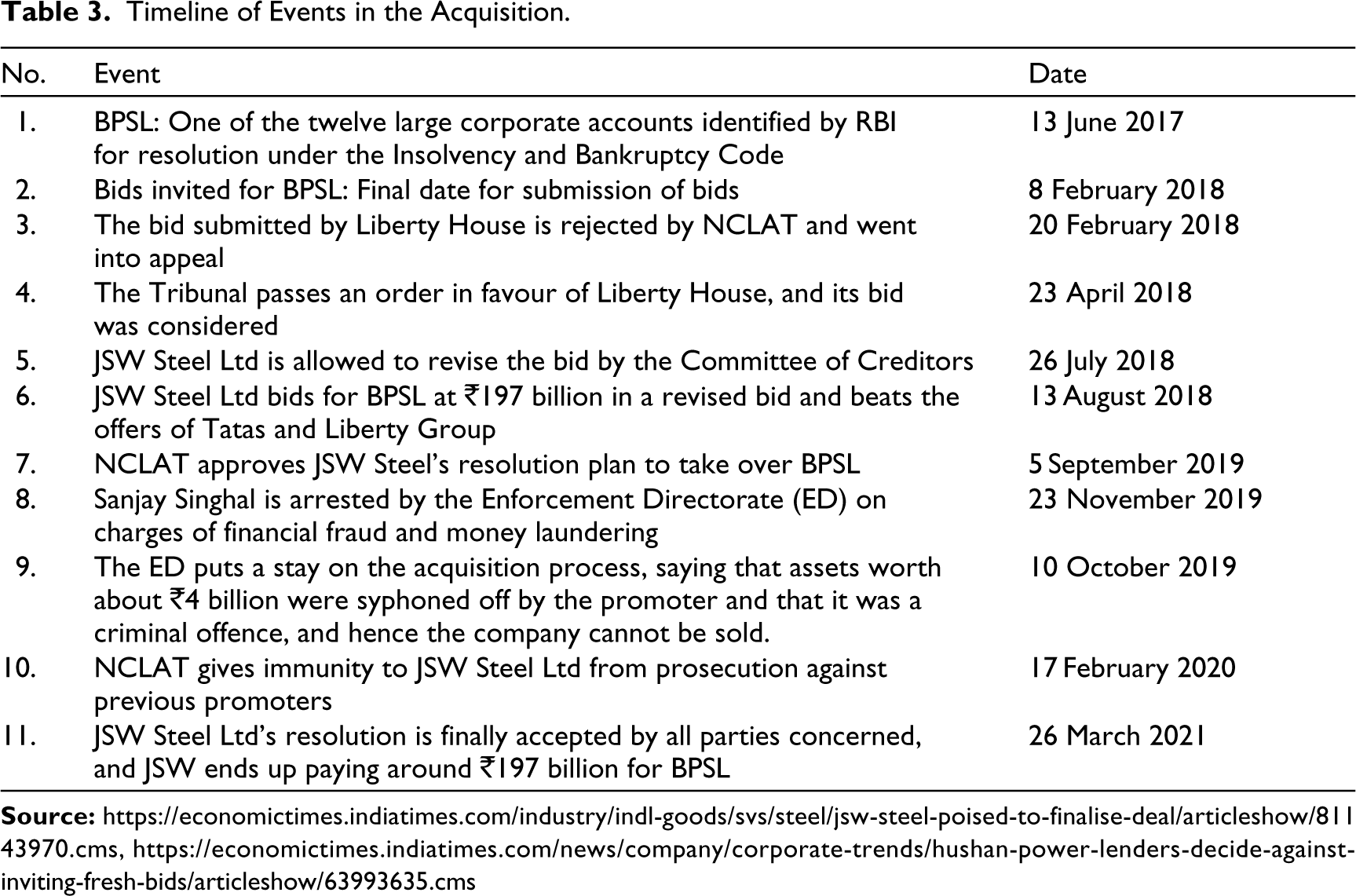

Bids were solicited from interested parties for the sale of BPSL’s assets. Three main contenders emerged for the company: Tata Steel Ltd, JSWSL. and Liberty House. The NCLAT approved JSWSL.’s resolution plan, but it encountered opposition from the ED, an arm of the Finance Ministry. Table 3 shows the timeline of the events until the acquisition. The role of NCLAT in the Indian business environment can be found in Exhibit 8, and the procedure for insolvency and bankruptcy can be found in Exhibit 9.

Timeline of Events in the Acquisition.

The Uncertainty Brought in by the Enforcement Directorate

The ED’s 4 money-laundering case was initiated following an examination of the first information report (FIR) filed by the Central Bureau of Investigation (CBI) against the company, Singhal and others on charges of corruption. The CBI’s FIR 5 had contended that BPSL, through its directors and staff, deceitfully diverted about ₹23.48 billion from the loan accounts of Punjab National Bank (Delhi and Chandigarh), Oriental Bank of Commerce (Kolkata), IDBI Bank (Kolkata) and UCO Bank (Kolkata) into the accounts of various companies or shell companies without any apparent purpose, thus misusing the funds.

The ED claimed that BPSL had also made real-time gross settlement (RTGS) payments to various entities for purported ‘fictitious purchases’ of capital goods. These entities, in turn, had transferred cash to BPSL, which was ultimately identified as having been used to fabricate an artificial long-term capital gain tax by inflating the prices of low-value stocks through synchronized trading, according to the ED.

An additional sum of ₹33.30 billion, invested as equity (comprising share capital and premium) by promoter companies, was also determined to be channelled out of the funds obtained as various loans, then diverted from BPSL’s accounts and portrayed as advances to various shell companies through different entry operators. It was further alleged that the proceeds generated were laundered by incorporating them into the books of accounts as equity to manipulate the debt–equity ratio for the purpose of financial window dressing (Business Standard, 2019).

Sanjay Singhal, along with certain other company officials and even bank officials involved in the transactions, was taken into custody on 20 November 2019 (Das, 2019).

The ED and the NCLAT found themselves in a dispute regarding the attachment of properties belonging to BPSL in relation to alleged money-laundering activities. While the NCLAT requested that the ED revoke the attached properties, the ED declined, citing the Prevention of Money Laundering Act 6 (PMLA), specifically Section 41, 7 which stated that the probe agency could not revoke any action taken under the PMLA unless the Supreme Court intervened. The ED even took the matter to the Supreme Court to challenge the NCLAT’s request. The ED argued that insolvency proceedings were governed by civil law and could not be overridden by criminal law proceedings (Choudhary, 2019). 8 Furthermore, they referred to a Delhi court order that affirmed the precedence of the anti-money laundering law over the IBC proceedings. The ED also contended that JSWSL could not take protection under Section 32A of the bankruptcy code, as it was not applicable retroactively to JSWSL’s bid, and JSWSL was considered a related party to BPSL due to their joint venture partnership for a coal block in 2008.

Sanjay Singhal, the chairman of BPSL, also raised objections to JSWSL’s resolution plan in the Supreme Court. JSWSL sought assurance from the banks that they would return the funds in the event of an adverse judgement in the case. This series of disputes and legal challenges led to the freezing of JSWSL’s resolution plan for BPSL.

All’s Well That Ends Well

On 26 March 2021, JSW Steel’s resolution plan was finally accepted for the acquisition of BPSL, marking the end of a prolonged corporate insolvency resolution (CIR) process that had spanned over three years since 2017. JSW Steel agreed to pay ₹193.5 billion for the acquisition of BPSL, funding the transaction through a combination of debt and equity.

To facilitate the acquisition, a special-purpose vehicle named Makler was established. JSW Steel secured ₹86.14 billion from one of its subsidiaries, Piombino Steel Ltd, using a mix of equity, optionally convertible instruments and debt. Out of this amount, ₹85.50 billion was invested in Makler, the bidding company. The remaining ₹108 billion was financed through loans from institutions such as the State Bank of India, Bank of Baroda, Deutsche Bank and Standard Chartered Bank.

Following the implementation of the resolution plan, JSW Shipping & Logistics Ltd converted its debt into equity, increasing its stake in Piombino Steel Ltd to 51 per cent. Consequently, JSW Steel’s stake in Piombino Steel Ltd was reduced to 49 per cent. JSW Steel also held optionally convertible debentures in Piombino Steel Ltd, which could be converted to equity at a later date, making Piombino Steel Ltd (and BPSL) a subsidiary of JSW Steel. Until that conversion, BPSL would be classified as an associate company of JSW Steel, and its profit or loss would be added to JSW Steel’s consolidated profit after tax (PAT).

The resolution plan entailed paying ₹193.5 billion to the creditors of BPSL, following which Makler would be merged into Piombino Steel Ltd, resulting in Piombino Steel Ltd holding 100 per cent of BPSL. This resolution would allow the lenders to recover approximately 41.03 per cent of their claims, amounting to ₹471.58 billion. The State Bank of India was the largest beneficiary, with an admitted claim of ₹98.26 billion, followed by Punjab National Bank with ₹43.99 billion. An asset reconstruction firm had claims of ₹52.75 billion, while Canara and Allahabad Bank had claims of ₹22.44 billion and ₹21.30 billion, respectively. The deal also provided for a 47.69 per cent recovery on operational creditors’ claims, which amounted to around ₹3.50 billion against their total claims of ₹7.34 billion.

Synergies from the Deal

The acquisition of BPSL by JSW Steel has had a significant impact on the company’s growth and expansion plans. JSW Steel aims to achieve a production capacity of 45 million tonnes by 2030, and the acquisition of BPSL played a pivotal role in achieving this goal.

With the addition of BPSL’s 2.8 million tonnes plant in Jharsuguda, Odisha, JSW Steel’s capacity increased from 19 million tonnes (18 million tonnes from JSW and 1 million tonne from the earlier acquisition of Monet Ispat and Energy) to 21.8 million tonnes. This made JSW Steel the largest steelmaker in India, surpassing even Tata Steel Ltd The acquisition also strategically positioned JSW Steel in the eastern part of India, where major iron ore mines are located.

BPSL’s facilities brought significant advantages to JSW Steel, including backward integration capabilities such as beneficiation, sintering, coke ovens and pelletization plants. Additionally, they offered downstream facilities, including a cold rolling mill, galvanizing and colour-coating lines, and a pipe and tube mill, all of which could be synergized with JSW Steel’s existing capacity (Rebello & Dilipkumar, 2021).

The acquisition also included downstream units located in Chandigarh and Kolkata. JSW Steel planned to revamp BPSL’s production capacity from its existing 2.8 million tonnes to 3.5 million tonnes per annum. There was also a 5 million tonnes capacity expansion planned at the Dolvi plant by 2022, which would further increase production to 26.5 million tonnes of steel (Mirchandani & Malik, 2020). JSW Steel aimed to revamp BPSL in the coming months post-acquisition, potentially increasing production capacity by 7 to 8 million metric tonnes.

JSW Steel’s captive iron ore mines and the nearby steel plant of JSW Ispat Special Products Ltd in Chhattisgarh synergized well with BPSL’s integrated steel plant in Jharsuguda, Odisha. The acquisition offered benefits in terms of backward integration through facilities such as beneficiation, sintering, coke ovens and pelletization plants. It also facilitated forward integration with the addition of a cold rolling mill, galvanizing and colour-coating lines, and a pipe and tube mill. BPSL had a strong portfolio of value-added products, and its presence in eastern India provided JSW Steel with a more extensive market reach.

Overall, JSW Steel is expected to benefit from higher margins on value-added products, cost savings related to iron ore procurement and an expanded market presence due to the acquisition of BPSL (JSW Steel Ltd: long-term rating upgraded to [ICRA]AA (stable); short-term rating reaffirmed at [ICRA]A1+, 2021).

The acquisition of BPSL by JSW Steel marked a strategic move that leveraged the robust state of the steel industry. The post-tax return on capital employed (ROCE) was anticipated to reach about 13 per cent, reflecting a favourable return on the capital investment. As can be observed from Exhibits 5 and 6, JSW Steel’s consolidated net profit for 2020–2021 substantially increased, reaching ₹78.73 billion, with higher steel prices and growing demand for value-added products driving the improved profitability (John, 2021). Operational revenue also rose to ₹798.39 billion. The estimated EV/EBITDA ratio, a measure of valuation, for 2022 was about 6.4 times. Projections indicated BPSL’s assets, at an increased capacity of around 3 million metric tonnes annually, would generate an EBITDA of ₹30 billion to ₹32 billion and a PAT of about ₹14 billion to ₹15.8 billion in 2022 and 2023. The consolidated EPS was expected to rise by approximately 3 per cent post-acquisition. JSW Steel successfully deleveraged its balance sheet, with a net debt-to-EBITDA ratio targeted at 2.75× times; the net movement of debt can be seen in Exhibit 7 (JSW Steel, 2021). The company planned to merge BPSL to further enhance market share, capacity and tax synergies.

The acquisition of BPSL by JSW Steel represented a strategic decision aimed at driving growth while preserving thousands of jobs. This move was significant in contrast to previous instances where companies like Kingfisher Airlines faced financial difficulties and had to cease operations. The managerial and operational expertise of JSW Steel was expected to revitalize the struggling BPSL, rescuing a valuable greenfield asset in the steel sector. This acquisition would facilitate the transfer of organizational knowledge and capital, ensuring a more sustainable future.

Sajjan Jindal’s letter to BPSL employees emphasized the importance of this acquisition within the context of India’s post-pandemic infrastructure development. JSW Steel’s entry into the eastern region marked a pivotal moment in expanding its footprint (Singh, 2021). Jindal expressed the company’s commitment to inclusive growth and creating a conducive environment for nurturing talent and providing livelihood opportunities (Ascent Conclave, 2017).

Additionally, it was vital to acknowledge that BPSL was a substantial steel player producing quality products and available at an attractive valuation, a key factor that sparked interest from Tata Steel as well. By addressing BPSL’s mismanagement of funds and clearing its debt, the acquisition alleviated significant issues. With JSW Steel agreeing to pay ₹193.3 billion to BPSL’s financial creditors, the burden of interest was substantially lightened (John, 2021).

Moreover, this acquisition seamlessly aligned with JSW Steel’s ambitious expansion and growth plans. It allowed the company to scale up its production capacity to approximately 22 million metric tonnes per annum and work towards its goal of reaching 38 million metric tonnes of steel production by 2024.

In the context of India’s new bankruptcy code, this acquisition held unique significance by preventing a prominent Indian steel company from closure, ensuring the industry’s capacity for growth and establishing JSW Steel as the nation’s largest steel producer. Ultimately, this acquisition exemplified the notion that ‘life is still always better than death’, as it breathed new life into a struggling company, preserved jobs and harnessed valuable assets for the benefit of all stakeholders.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Appendix

It is a quasi-judicial body incorporated for dealing with corporate disputes in India that are of civil nature arising under the Companies Act, 2013. It works like a normal court of law in India and is obliged to fairly and without any biases determine the facts of each case and decide matters in accordance with principles of justice. It offers decisions in the form of orders. These orders help in resolving situations or wrongdoing by companies.

NCLAT was constituted under Section 410 of the Companies Act, 2013, for hearing appeals against the orders of NCLAT, with effect from 1 June 2016.

NCLAT is also the Appellate Tribunal for hearing appeals against the orders passed by NCLAT(s) under Section 61 of the Insolvency and Bankruptcy Code, 2016 (IBC), with effect from 1 December 2016. NCLAT is also the Appellate Tribunal for hearing appeals against the orders passed by the Insolvency and Bankruptcy Board of India under Section 202 and Section 211 of IBC.

NCLAT is also the Appellate Tribunal to hear and dispose of appeals against any direction issued or decision made or order passed by the Competition Commission of India (CCI) – as per the amendment brought to Section 410 of the Companies Act, 2013, by Section 172 of the Finance Act, 2017, with effect from 26 May 2017.

The IBC 2016 is the bankruptcy law of India which seeks to consolidate the existing framework by creating a single law for insolvency and bankruptcy. The IBC 2015 was introduced in the Lok Sabha in December 2015. It was passed by the Lok Sabha on 5 May 2016 and by the Rajya Sabha on 11 May 2016. The Code received the assent of the president of India on 28 May 2016. Certain provisions of the Act have come into force from 5 August and 19 August 2016. The bankruptcy code is a one-stop solution for resolving insolvencies, which previously was a long process that did not offer an economically viable arrangement. The code aims to protect the interests of small investors and make the process of doing business less cumbersome.

The Insolvency and Bankruptcy Code (Amendment) Act, 2019, has increased the mandatory upper time limit of 330 days including time spent in legal process to complete the resolution process.

A plea for insolvency is submitted to the adjudicating authority (NCLAT in the case of corporate debtors) by financial or operation creditors or the corporate debtor itself. The maximum time allowed to either accept or reject the plea is 14 days. If the plea is accepted, the tribunal has to appoint an Interim Resolution Professional (IRP) to draft a resolution plan within 180 days (extendable by 90 days), following which the CIR process is initiated by the court. For the said period, the board of directors of the company stands suspended, and the promoters do not have a say in the management of the company. The IRP, if required, can seek the support of the company’s management for day-to-day operations. If the CIR process fails in reviving the company, the liquidation process is initiated.